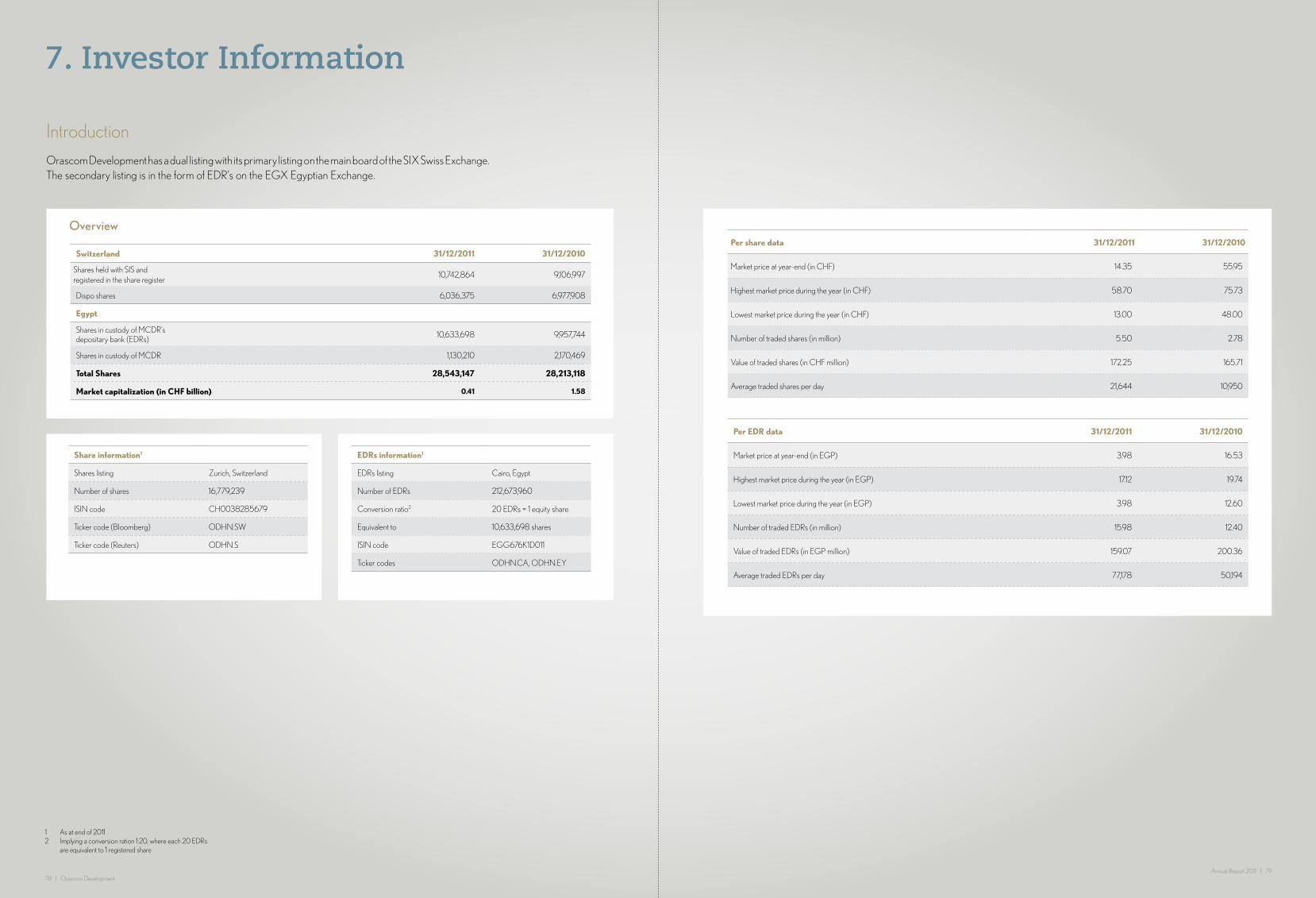

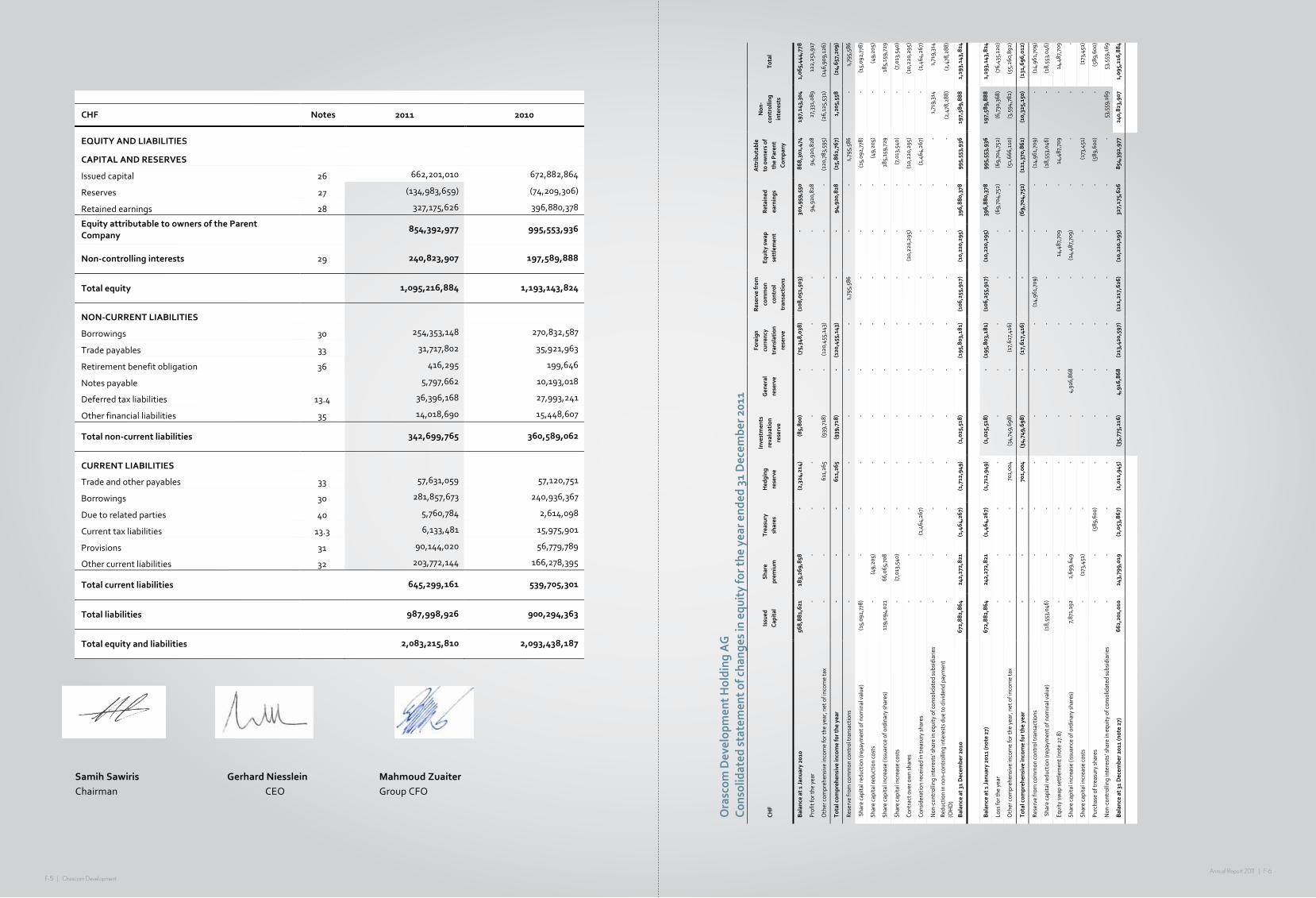

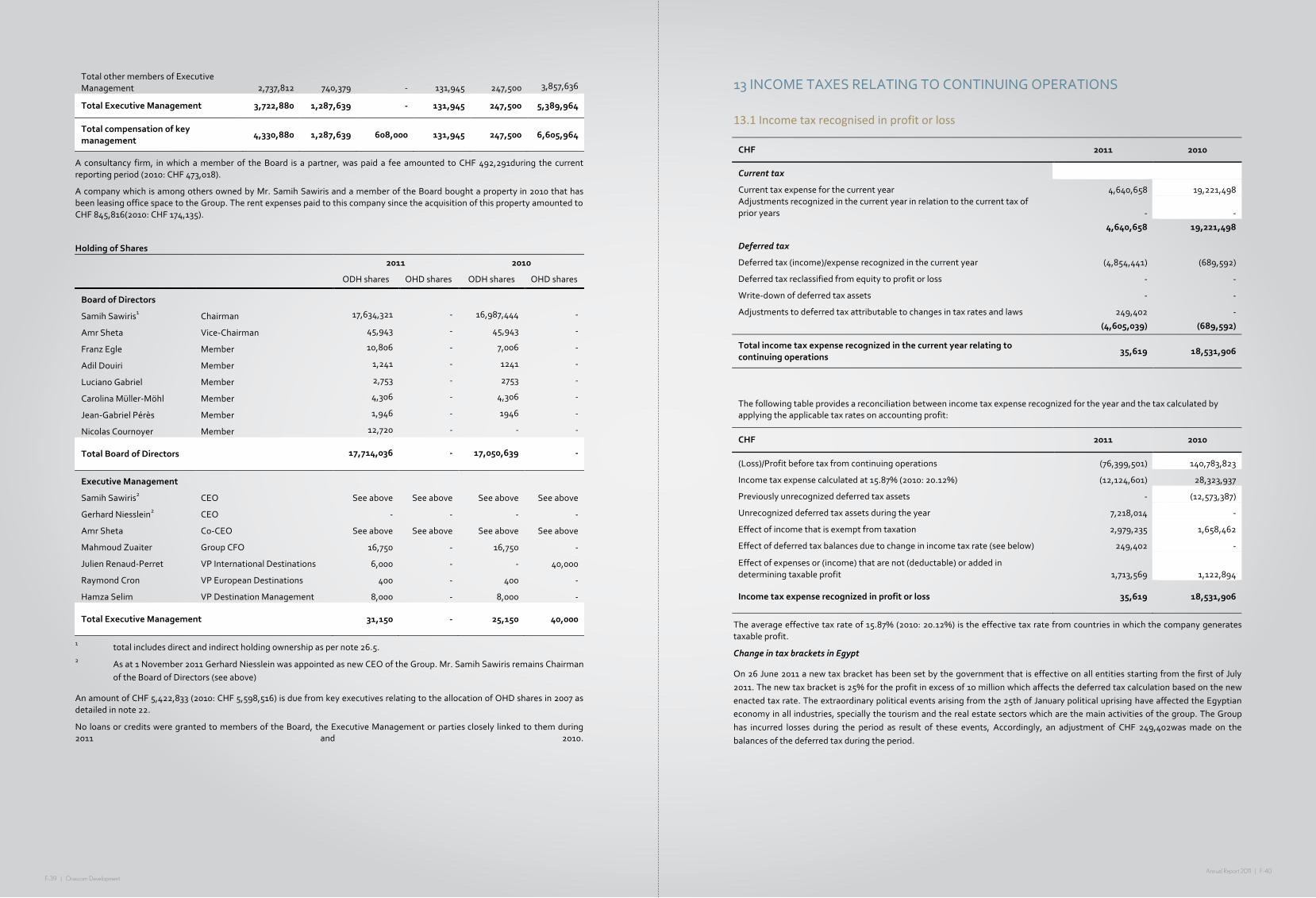

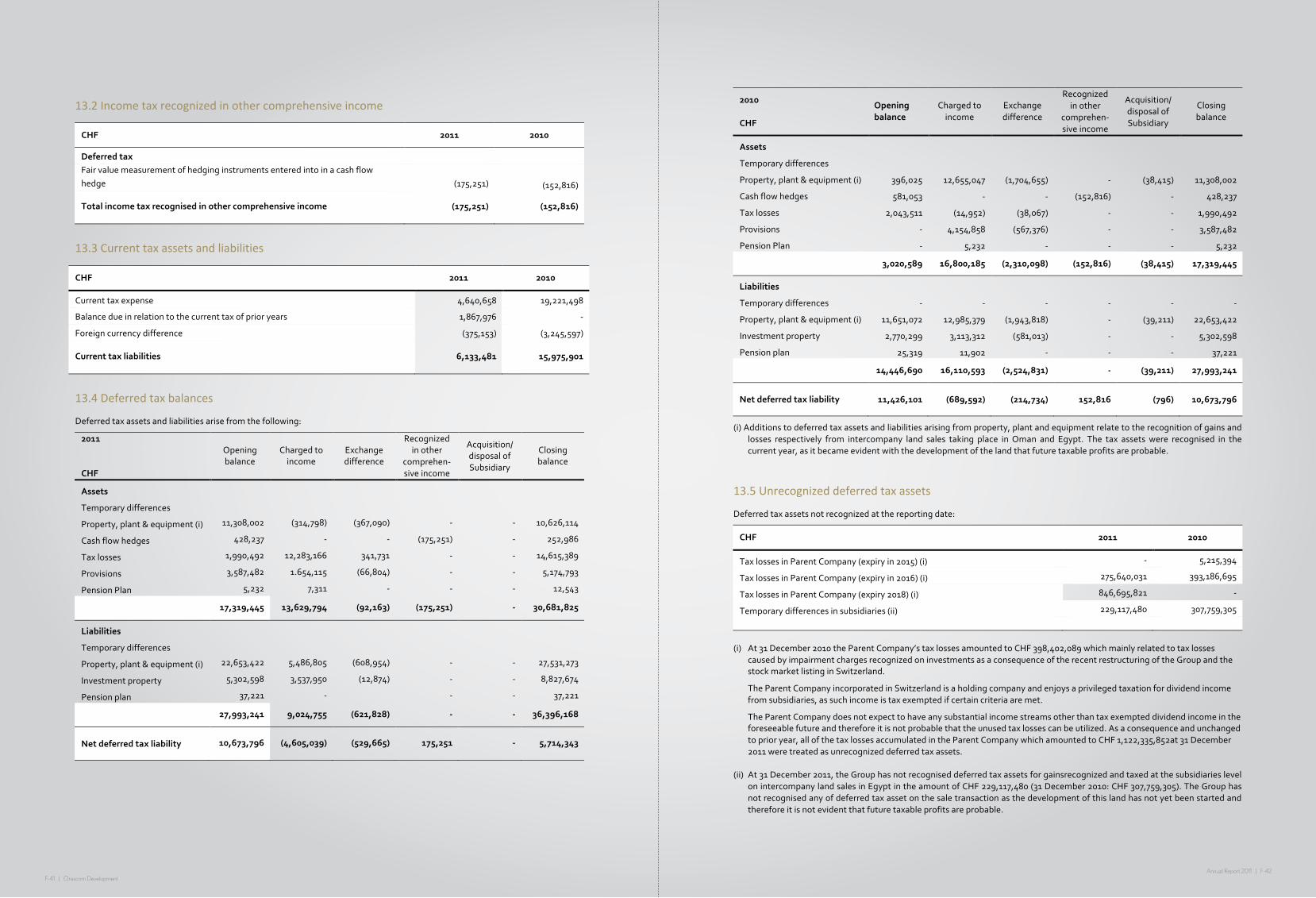

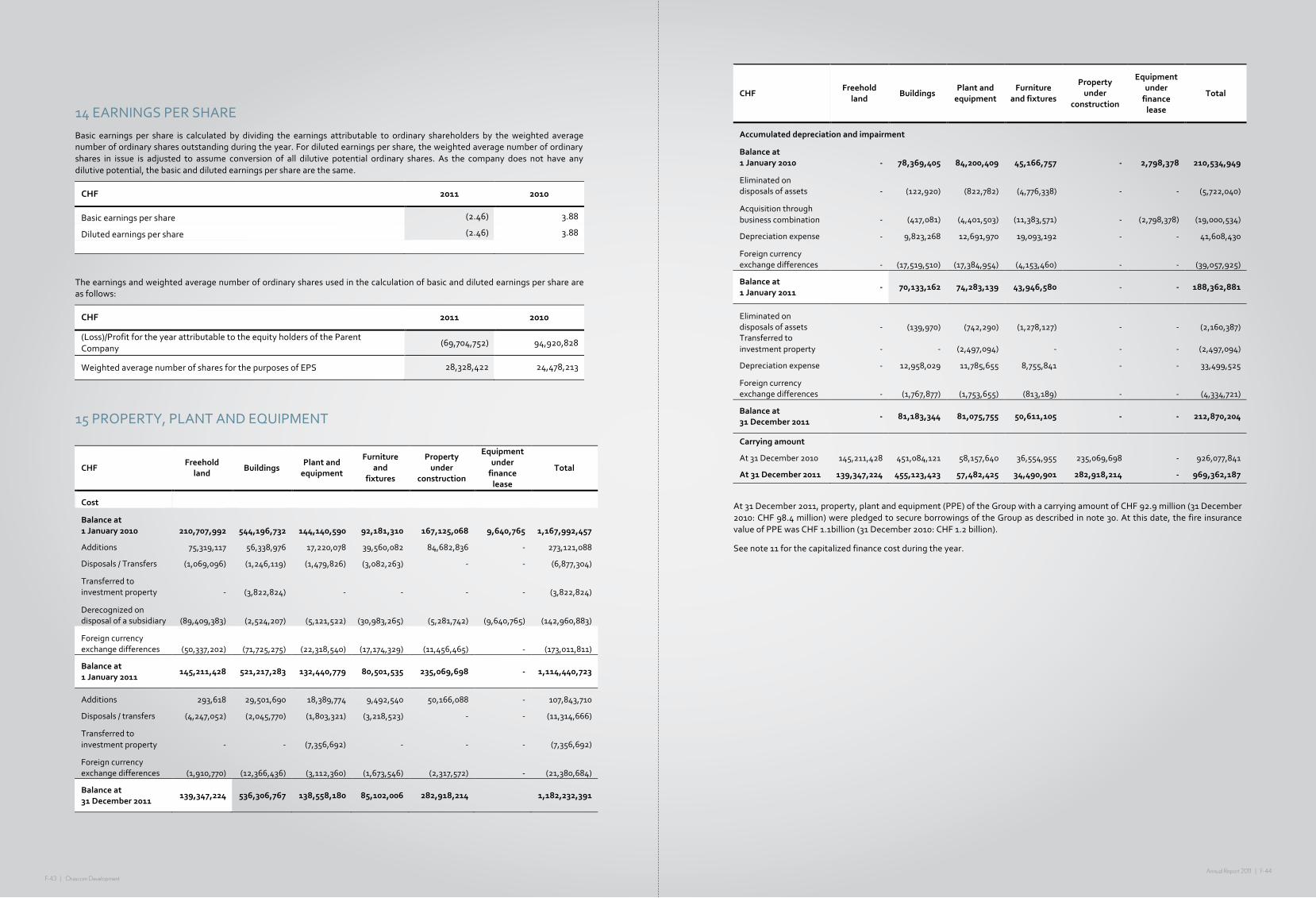

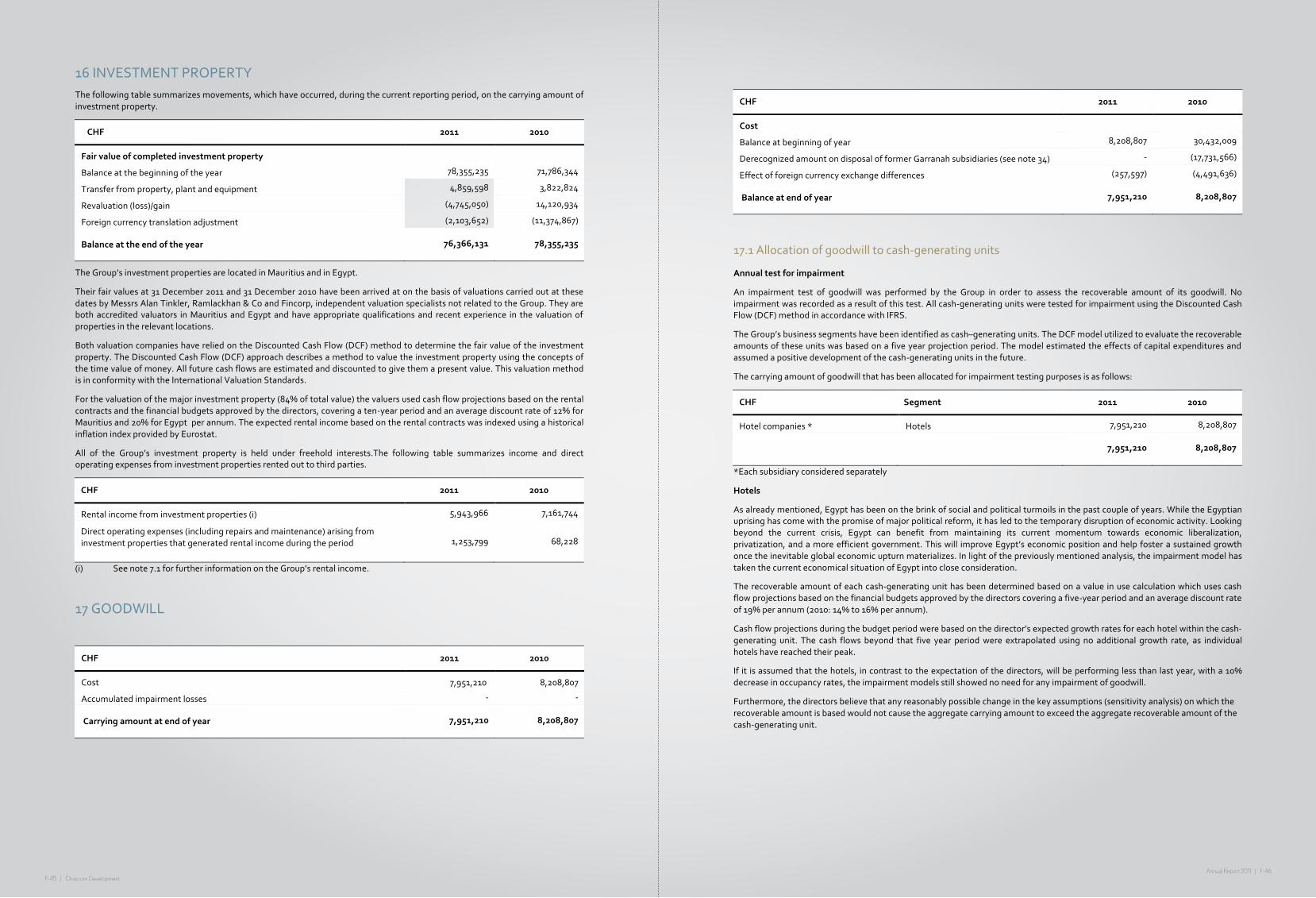

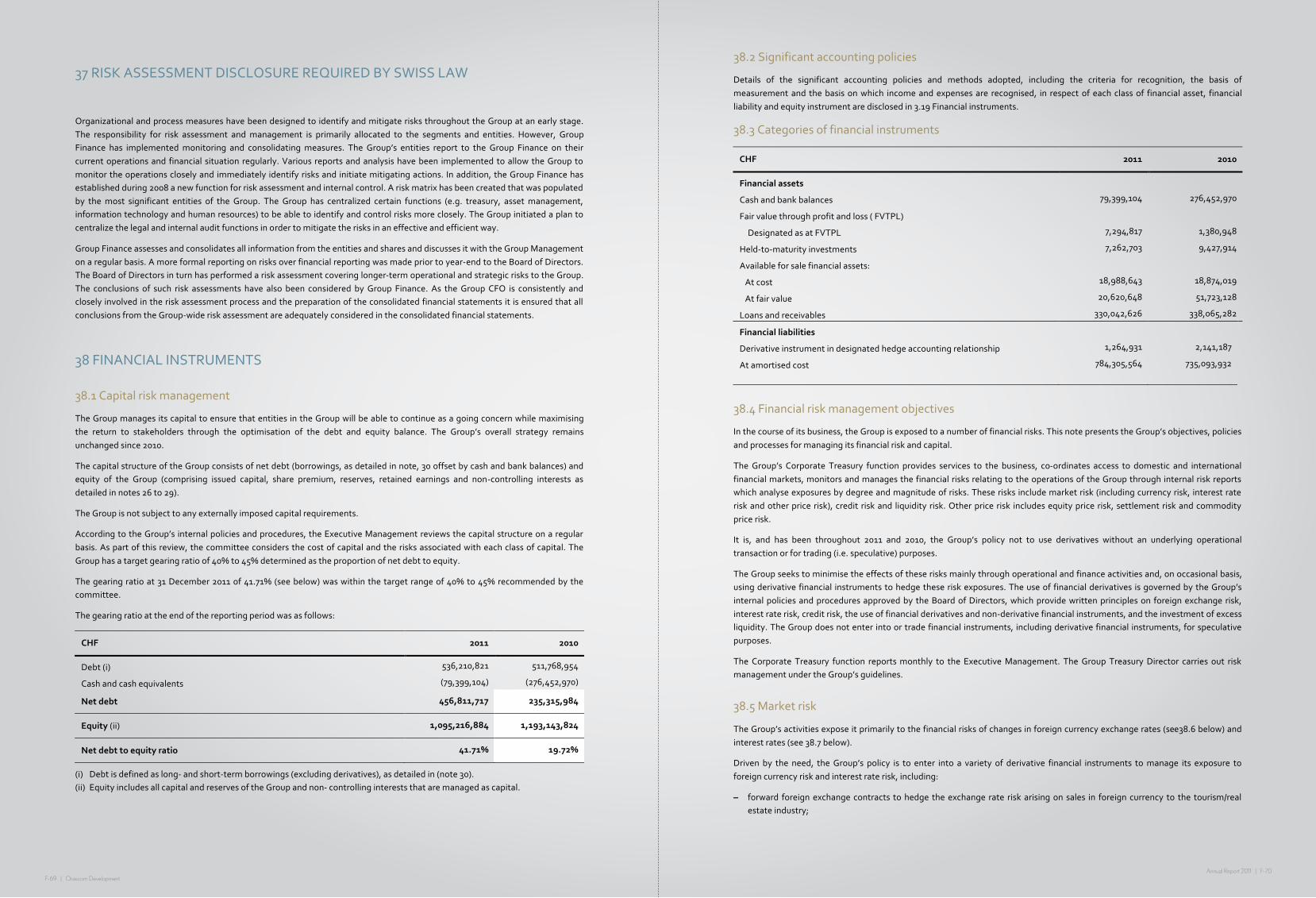

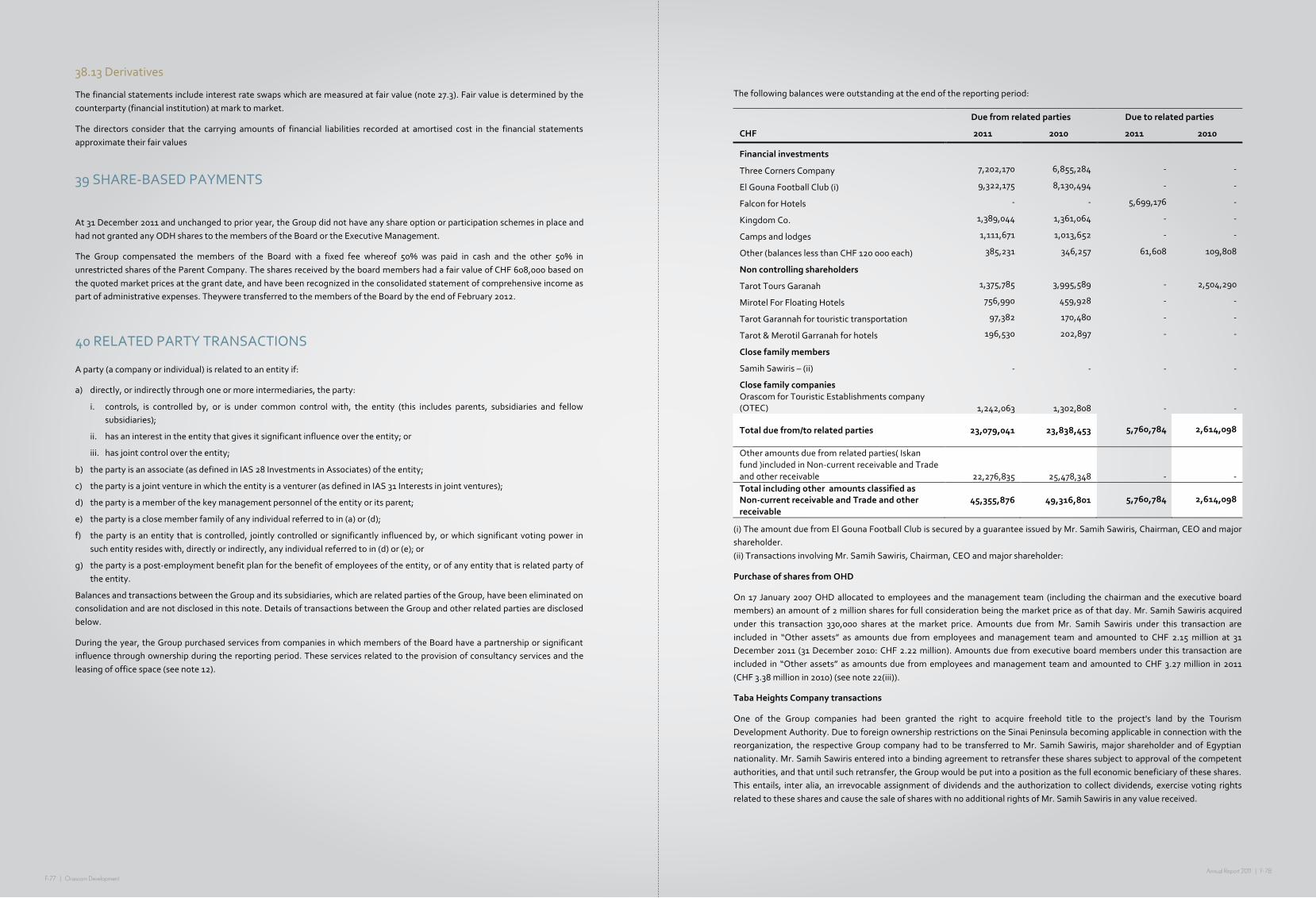

annual report 2011 - orascomdh.com consolidated statement of comprehensive income f-3 8.2...

TRANSCRIPT

ANNUAL REPORT

2011

Value Creation

Contents1. Facts & Figures 2

2. Board & Management Statements 6 2.1 Message from the Chairman 6 2.2 Interview with the CEO 8 2.3 CFO statement 10 2.4 Focus for 2012 12

3. Business Segments 14 3.1 Hotels 14 3.2 Real Estate and Construction 16 3.3 Town Management 18 3.4 Other Segments 19

4. Countries 20 4.1 Egypt 22 4.2 UAE 32 4.3 Jordan 34 4.4 Oman 36 4.5 Switzerland 42 4.6 Morocco 44 4.7 Montenegro 46 4.8 United Kingdom 48 4.9 Romania 49

5. Sustainability 50 5.1 Social sustainability 52 5.2 Environmental sustainability 54 5.3 Economic sustainability 55 5.4 Examples of sustainability in our towns 56 5.5 Interview with the Head of Group Design & Destination Planning 60

6. Corporate Governance 62 6.1 Group Structure and Significant Shareholders 62 6.2 Capital structure 64 6.3 Board of Directors 66 6.4 Executive Management 72 6.5 Compensation, shareholdings and loans 75 6.6 Shareholders’ participation 76 6.7 Changes of control and defense measures 76 6.8 External auditors 77 6.9 Information policy 77

7. Investor Information 78

8. Consolidated Financial Statements 2011 Orascom Development Holding AG F-2 8.1 Consolidated statement of comprehensive income F-3 8.2 Consolidated statement of financial position F-4 8.3 Consolidated statement of changes in equity F-6 8.4 Consolidated statement of cash flows F-7 8.5 Notes to the consolidated financial statements F-9

9. Financial Statements 2011 Orascom Development Holding AG 9.1 Income statement F-85 9.2 Statutory balance sheet F-86 9.3 Statement of changes in equity F-87 9.4 Cash flow statement F-87 9.5 Notes to the financial statements F-88

10. Glossary of Terms 176

2 | Orascom DevelopmentAnnual Report 2011 | 3

2011 Highlights

Revenues by Business Segment

Net Profit (after non-controlling interest)

CHF Million 106 95 -70

EPS (basic & diluted)

CHF 4.59 3.88 -2.46

Shareholder’s Equity(after non-controlling interest)

CHF Million 868 996 854 CHF Million 0.46 0.48 0.41

Total Assets

CHF Million 1,886 2,093 2,083

Property, Plant and Equipment (PP&E)

CHF Million 957 926 969

Net Debt/ PP&E

CHF Million 0.32 0.25 0.47

Net Asset Value/ Share2

CHF Million 37.40 35.29 29.93

Capital Expenditure

CHF Million 188 273 92

Net Debt

CHF Million 310 235 457

1. Facts & Figures

183

240

39

25

65

33

2009

Total Revenues

Chf 586 Million

193

229

1017

28

38

2010

Total Revenues

Chf 516 Million

136

67

2

2

18

31

2011

Total Revenues

Chf 256 Million

Hotels

Real estate and construction

Land sales

Town management

Tours operations

Other operations

EBITDA

CHF Million 215 178 -40

EBITDA (Adjusted)1

CHF Million 215 178 43CHF Million 586 516 256

09 10 11

09 10 11 09 10 11

09 10 1109 10 11

Total Revenues

Note:1 EBITDA Adjusted for extraordinary items.

Note:1 Equity ratio is calculated by dividing shareholders equity (after non-controlling interest) by total assets2 NAV/Share is calculated by dividing equity (after non-controlling interest) by total number of shares outstanding

Equity Ratio1

09 10 11 09 10 11

09 10 11

09 10 11

09 10 11

09 10 11

09 10 11

09 10 11

4 | Orascom DevelopmentAnnual Report 2011 | 5

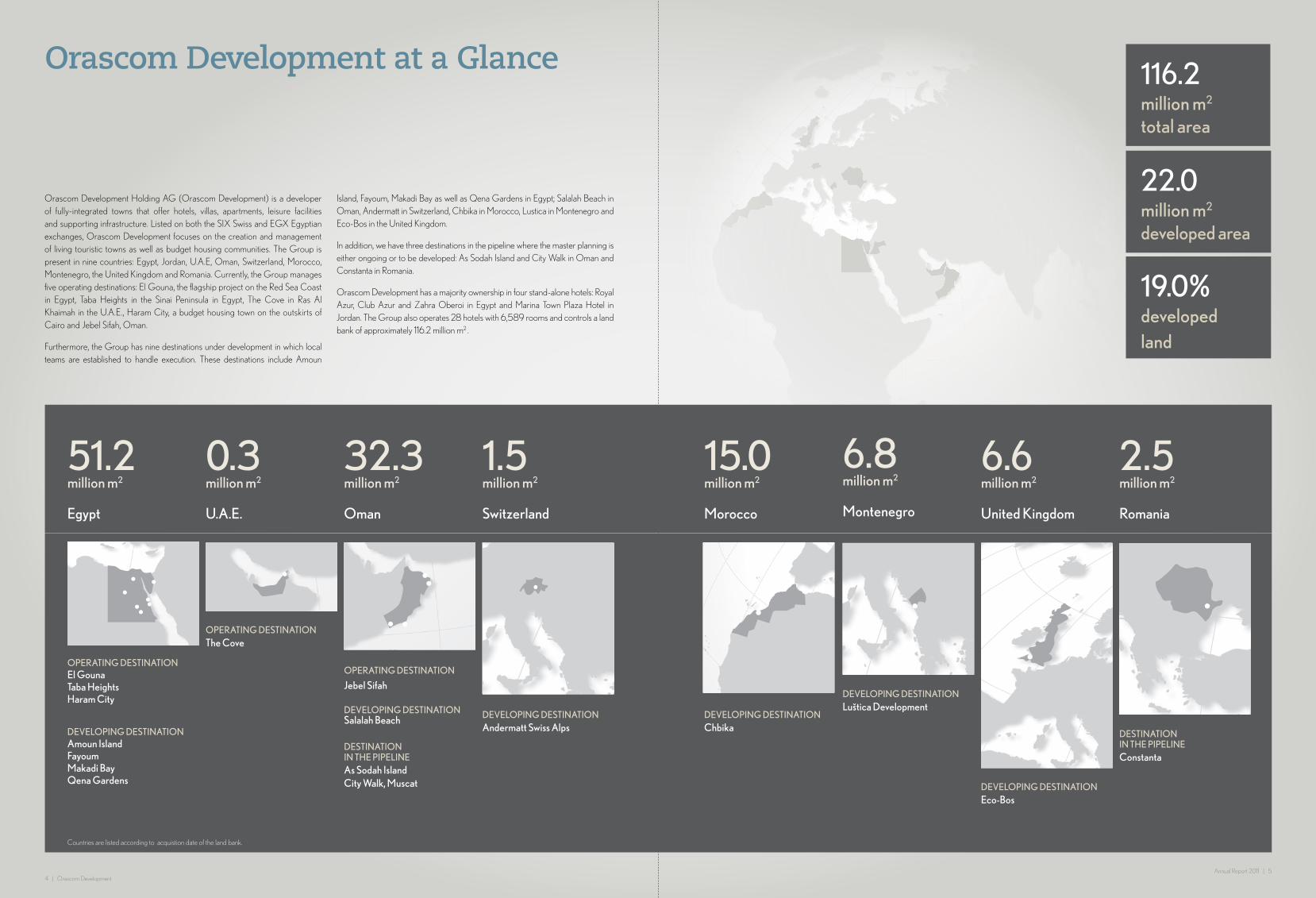

116.2 million m2

total area

22.0million m2

developed area

19.0%developedland

Orascom Development Holding AG (Orascom Development) is a developer of fully-integrated towns that offer hotels, villas, apartments, leisure facilities and supporting infrastructure. Listed on both the SIX Swiss and EGX Egyptian exchanges, Orascom Development focuses on the creation and management of living touristic towns as well as budget housing communities. The Group is present in nine countries: Egypt, Jordan, U.A.E, Oman, Switzerland, Morocco, Montenegro, the United Kingdom and Romania. Currently, the Group manages five operating destinations: El Gouna, the flagship project on the Red Sea Coast in Egypt, Taba Heights in the Sinai Peninsula in Egypt, The Cove in Ras Al Khaimah in the U.A.E., Haram City, a budget housing town on the outskirts of Cairo and Jebel Sifah, Oman.

Furthermore, the Group has nine destinations under development in which local teams are established to handle execution. These destinations include Amoun

Island, Fayoum, Makadi Bay as well as Qena Gardens in Egypt; Salalah Beach in Oman, Andermatt in Switzerland, Chbika in Morocco, Lustica in Montenegro and Eco-Bos in the United Kingdom.

In addition, we have three destinations in the pipeline where the master planning is either ongoing or to be developed: As Sodah Island and City Walk in Oman and Constanta in Romania.

Orascom Development has a majority ownership in four stand-alone hotels: Royal Azur, Club Azur and Zahra Oberoi in Egypt and Marina Town Plaza Hotel in Jordan. The Group also operates 28 hotels with 6,589 rooms and controls a land bank of approximately 116.2 million m2 .

Orascom Development at a Glance

2.5million m2

Romania

DESTINATION IN THE PIPELINEConstanta

6.8million m2

Montenegro

DEVELOPING DESTINATIONLuštica Development

6.6million m2

United Kingdom

DEVELOPING DESTINATIONEco-Bos

15.0million m2

Morocco

DEVELOPING DESTINATIONChbika

1.5million m2

Switzerland

DEVELOPING DESTINATIONAndermatt Swiss Alps

32.3million m2

Oman

OPERATING DESTINATION

Jebel Sifah

DEVELOPING DESTINATION Salalah Beach DESTINATION IN THE PIPELINEAs Sodah IslandCity Walk, Muscat

0.3million m2

U.A.E.

OPERATING DESTINATIONThe Cove

51.2million m2

Egypt

OPERATING DESTINATIONEl Gouna Taba Heights Haram City

DEVELOPING DESTINATIONAmoun IslandFayoumMakadi BayQena Gardens

Countries are listed according to acquistion date of the land bank.

6 | Orascom DevelopmentAnnual Report 2011 | 7

2.1 Message from the Chairman

In order to reflect the broader presence of the Group and to separate the activities of the Executive Management and the Board of Directors, I decided to hand-over my duties as CEO of Orascom Development to Dr. Gerhard Niesslein as of the 1st of November. Dr. Niesslein is a well experienced, broadly networked real estate expert who has served as a leader of various companies in Canada and Germany and previously acted as the CEO of IVG Immobilien AG, Bonn, a listed German real estate company. In his new position, he will lead the day-to-day business of the Group and its subsidiaries. I will keep my position as Chairman of the Board of Directors and focus on developing the long-term strategic goals of the Group.

Finally, I would like to thank Amr Sheta, Vice Chairman and Co-CEO, on his substantial contribution to the growth of the Group, without his active role, the Group could never have developed so vigorously.

OutlookThe beginning of 2012 turned out to be challenging and I expect it to continue being so for the rest of the year. Nevertheless, I strongly believe in the company’s performance and I am confident that we will be able to weather the storm and emerge stronger. I remain committed to the company through my capacity as the Chairman of the Board and worked to secure CHF 125 million in credit agreements earlier this year that will enable us, together with the existing cash reserves and credit lines, to finance all of our activities for the current year. Furthermore, I am also willing to secure additional funding to cover the 2013 investment program if required.

The Group has a unique business model with a proven track record, which I believe can be applied in other parts of the world. In light of the current circumstances, we have adapted the business model to create the best long-term value possible for our shareholders and

increase performance by identifying credible equity investors willing to partner with the Group on potential investments.

Faced with challenges ahead and influenced by the need to change while adapting to new realities, we have to better manage our costs, become more efficient in what we do and become more effective in how we do it. If we are to remain leaders, we need to implement changes swiftly and effectively.

On behalf of the Board of Directors and Executive Management, we would like to thank all our employees for their commitment and the huge efforts they put forward during this time of uncertainty. We also like to thank our clients and business partners for their confidence in our business model. Lastly, we wish to thank you, our shareholders, for the trust you have always placed in the Group, and we are prepared to deliver on that trust.

Dear Shareholders,

2011 has been a truly challenging year for Egypt, the Middle East and the world as a whole. We have witnessed a number of unexpected changes on the political and economic fronts, all of which have had a profound impact on global business. The events in the MENA Region (Middle East and North Africa), which started early in the year, significantly impacted our operations. In Egypt and Oman, tourism demand dropped which affected economic growth. Nevertheless, our hotels managed to pick up the pace with higher room occupancies towards year end. In our real estate market, construction work in Egypt came to a near halt for almost 50 days during the first half of the year resulting in comparatively lower revenues and profits. Beyond the region, high volatility in international currency markets, a deepening of the European debt crisis and slower global economic growth in the second half of the year created additional challenges for the Group.

Despite these harsh market conditions, we managed to achieve several milestones in our destinations. At our Swiss destination Andermatt, considerable construction and investment progress was achieved. We completed the shell of the Chedi hotel in November, one-third of the initial construction of the car-free village Podium and finalized the earthworks for the 18-hole golf course. Even with a robust Swiss Franc and a debate surrounding the development of the ski area, we were able to reach reasonable levels of sales and reservation contracts in Andermatt. We also launched our first hotel in Jebel Sifah; Oman, the Sifawy boutique hotel with 55 rooms and suites in September and are planning to launch the pre-sales of “Lustica Bay,” our new destination in Montenegro, by the second quarter of 2012. These developments continue to support our financial positioning and diversification strategy in the coming years.

Samih Sawiris

Chairman

2. Board & Management Statements

8 | Orascom DevelopmentAnnual Report 2011 | 9

Why did you join Orascom Development Holding AG? For me, Orascom Development is a unique organization with a proven business model, an experienced management team and a land bank of about 116.2 million m2 that is still largely undeveloped. But, the destination portfolio today already consists of five fully-fledged towns and further destinations under development in nine countries. The Group also operates a total of 6,589 hotel rooms.

What is your current role at Orascom ?As CEO, I will lead the day-to-day business of the Group and its subsidiaries.

What are your first impressions about Egypt?Egypt is a fascinating country with a rich history and a long tradition. I have met a lot of enthusiastic and interesting people here and I am optimistic that also the business environment will return to growth once the current situation subsides.

Which areas are you planning to focus on over the next 6-18 months?Our main focus is to become more efficient and effective in what we do and to increase transparency. We are currently reviewing our process landscape, strengthening our Group-wide business practices and more clearly aligning roles and procedures. Another area would be securing further funding requirements for our destinations.

Can you give some examples of what exactly you are planning to do?Yes, of course. In light of the current circumstances, we intend to focus more on the monetization of our land bank, to identify equity partners to convert our equivalent of land into a hotel ownership or joint venture and to more closely work with sub-developers.

We are in the process of setting-up a matrix structure for the Group, with clear profit and support centers. We also simplified processes for staff members with more role specialization and defined responsibilities.

Given the recent changes on the global economical and political side, we decided to assess not only our existing operations, but also our developments from a legal and a financial point of view. This should enable us to come up with several solutions under various scenarios for each destination. Additionally, we successfully prolonged the maturity of our debt facilities.

What is your outlook for budget housing?We believe that the Group is well-positioned to explore new opportunities in the budget housing segment as the political environment in the MENA-region improves. We have an experienced team that has the expertise to build budget housing that can combine business profitability with a consideration of the economic welfare and development of societies.

Any new expansion plans or joint ventures in the pipeline?Today, we have about 94 million m2 of undeveloped land. This should be enough residual land to keep the Group growing organically for at least a decade. Therefore, we do not intend to add any new major developments in the near future.

2.2 Interview with the CEO

Gerhard Niesslein

Chief Executive Officer

10 | Orascom DevelopmentAnnual Report 2011 | 11

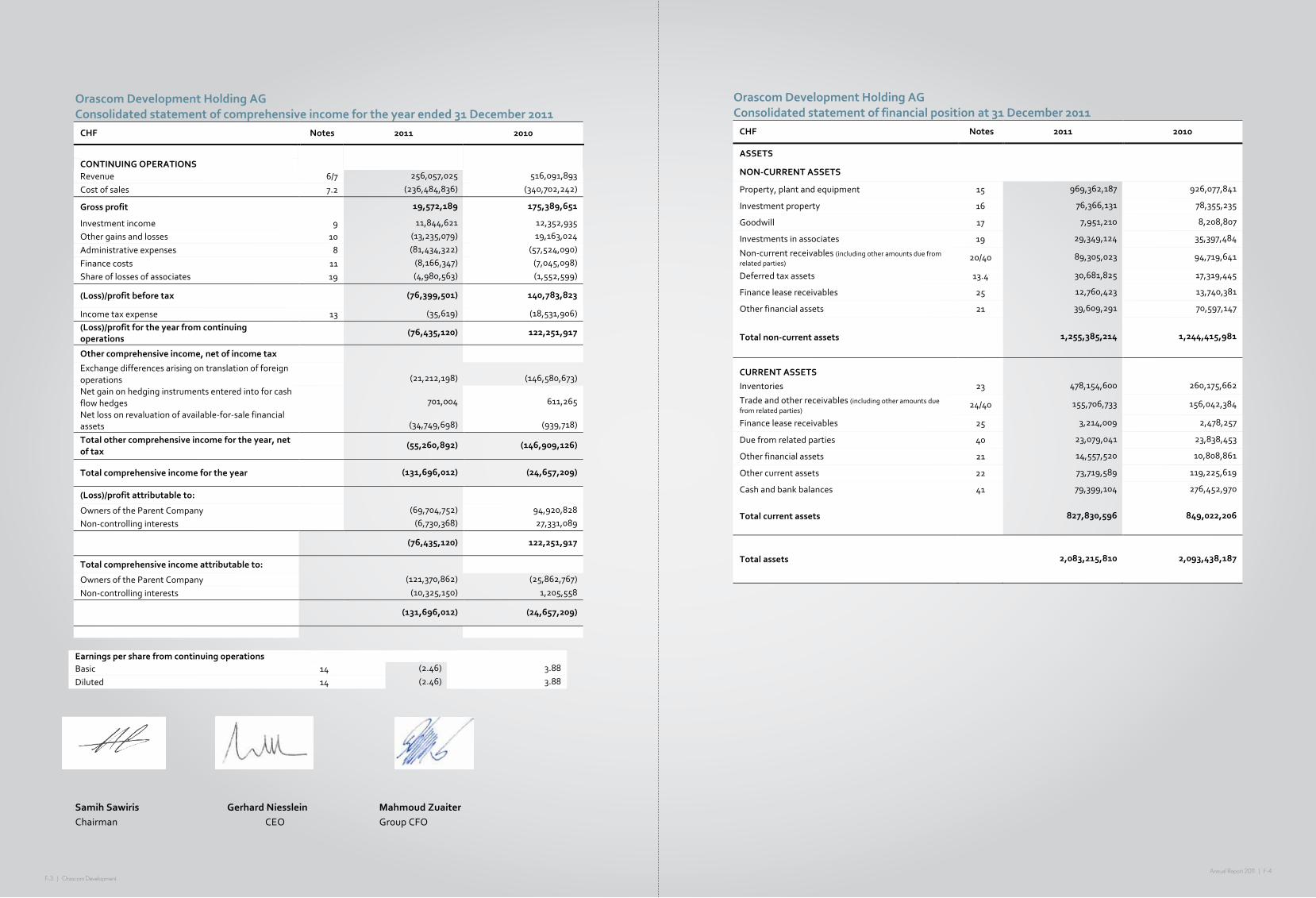

Balance sheet

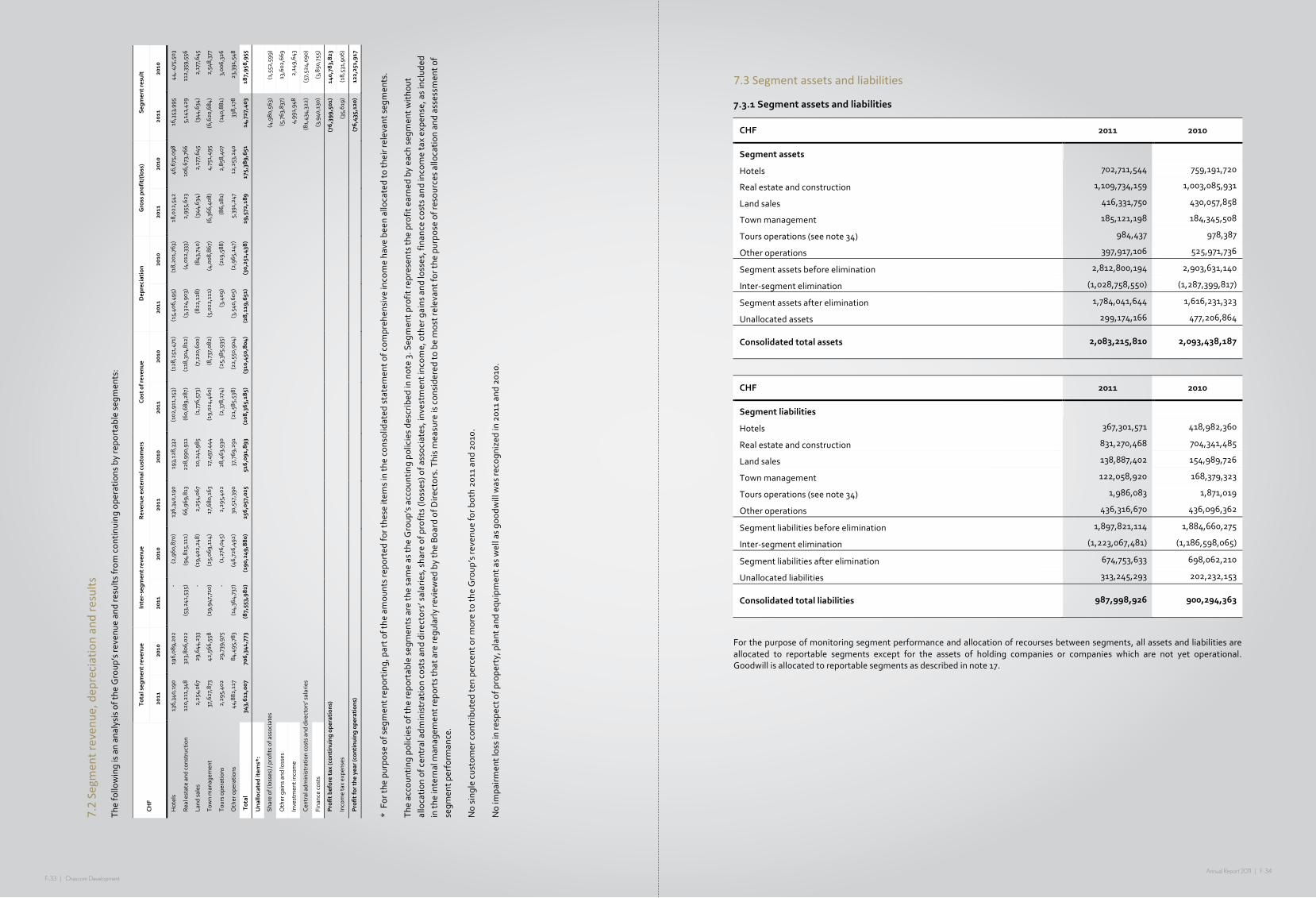

Total assets on the balance sheet remained broadly unchanged at CHF 2,083.2 million compared to CHF 2,093.4 million in 2010. Cash and cash equivalents decreased from CHF 276.5 million to CHF 79.4 million in 2011 in connection with the construction work of real estate units (construction work in progress) that are either contracted or sold or that are ready to be sold. As a result, the inventory balance increased from CHF 260.2 million in 2010 to CHF 478.2 million by the end of 2011. Of the total inventory CHF 346.3 million relates to construction work in progress.

On the liability and equity side, the drop of shareholders`equity (after non-controlling interests) of CHF 141.2 million resulted from three main components: the losses from the continued operations of CHF 69.7 million (net loss), exchange rate differences of CHF 17.6 million and revaluation of assets available for sale of CHF 34.7 million.

Financing

As of 31 December 2011, the net debt position of Orascom Development stood at CHF 456.8 million, almost doubled when compared to 2010 (CHF 235.3 million). While in 2010, the Group successfully concluded rights issue with the proceeds of CHF 185.2 million, that reduced the net debt position considerably, in 2011 the increase of it indebtedness mainly stems from higher real estate inventory (plus CHF 218.0 millon). The high inventory will generate a part of our future cash inflow, once the real estate units are sold.

The Group is working on several financing facilities to fund expansions of hotels in Oman, Switzerland and Egypt. During 2011, Orascom Development succeeded to prolong its debt repayments. Additionally, we are currently working on restructuring our debt to further optimize the cash positions of the Group.

In order to serve the long-term vision of the company, we will increasingly focus in our daily business on the functions of reporting, budgeting and controlling. Furthermore, we intend to improve our finance-related IT tools.

The political changes in the MENA-region, the slowdown of the world economy and the strengthening of the Swiss Franc all affected the performance of the Group during 2011; in particular as 70% of the financial statements are contributed from the Egyptian entities.

Consolidated revenues accordingly declined by 50% to CHF 256.1 million from CHF 516.1 million in 2010. Next to the impact from the political and economical events, the strengthening of the Swiss Franc resulted in a 13.8% decrease in revenues.

The operating results of the Group (EBITDA) stood at a loss of CHF 40.1 million as several extraordinary items, derived from the above mentioned events, occurred. These items in total amounted to CHF 82.8 million and include provisions (CHF 57.1 million), revaluations of investment properties (CHF 8.7 million), legal fees (CHF 5.0 million) as well as currency revaluations from the appreciation of the Swiss Franc (CHF 12.0 million). It is worth noting that more than 90% of these items are non-cash items. When adjusting for these extraordinary items, Group EBITDA was CHF 42.7 million, corresponding to an EBITDA-margin of 16.7% (2010: 34.5%).

Reported net loss (after non-controlling interests) amounted to CHF 69.7 million (2010: profit of CHF 94.9 million).

Mahmoud Zuaiter

Group Chief Financial Officer

Note:1 Group net debt divided by P,P&E

2.3 CFO Statement

MCHF

50

-40.1

57.1

42.7

8.7

5.012.0

-50

-40

-30

-20

-10

40

30

20

10

0

EBITDAReported

Provisions Investmentproperties

Currencyrevaluations

Legal Fees EBITDAAdjusted*

12 | Orascom DevelopmentAnnual Report 2011 | 13

2.4 Focus for 2012

What has changed in your development approach?Orascom Development`s land bank remains the main value driver. Today, we have 94 millon m2 available for development.

In 2012, Orascom is at a crossroad from a strategic standpoint. Over the last years, our land bank has significantly increased due to our new destinations in Morocco, Montenegro, the UK and Romania, which together added some 30 million m2.

As a consequence of this increase, we had to assess first of all the option of shifting towards a more “Capital Light Strategy”; which basically means a higher share of sub-developers in our destinations. Secondly, we are in the process of internally analyzing various options to better monetize our land bank.

What type of investment opportunities could you offer?Orascom as a destination and a community developer provides all activities and components associated with those life centres. Our destinations, which have a strong tourism profile include hotels, leisure infrastructures, residential real estate and necessary amenities to support our residents day to day life (such as schools, shops, restaurants and/or hospitals). All of these could create investment opportunities for third-parties.

What type of investors do you want to attract?First and foremost investors who are interested to invest in undeveloped locations that are also supportive of sustainable solutions respectful of the environment. Second, the capital needs to be mid to long term as we are in the ground up business which takes time to plan, build and mature. Third, investors that like to invest in residential real estate itself, hotels, land or real estate

associated with infrastructure. Finally, capital that can actively participate in our effort by contributing its ideas and past experiences with a strong penchant for low density construction.

What do investors get at this stage?Beyond deploying capital, they get access to scarce land resources and they can benefit from the know-how, brand and experience of Orascom. For example, if an investor is interested to fund or co-fund a hotel, we can provide them with access to our portfolio of international hotel management companies. Co-investors as well also particpiate in the appreciation of the land value, next to an attractive return, once the project is successfully developed. A further benefit is that the investor usually can be provided with an existing high-end infrastructure such as a marina, golf course or a hospital.

Where are your Destinations that are attractive for investors?We are actively developing in five countries: Switzerland and Montenegro in Europe as well as Oman, Egypt and Morocco.

Julien Renaudperret

Chief Development Officer

Our proven business model is based on the acquistions of untapped land and the development and management of fully integrated towns. At the heart of our operations, and thus a key long term value driver of our business model, is our land bank which we acquired in several jurisdictions.

While we in essence remain committed to our business model the global environment has materially changed during the last couple of years. Among the most popular events, we faced the headwinds derived from the global financial crisis since 2008, the deepening of the debt crisis in Europe, the strengthening of the Swiss Franc and the unexpected changes on the political fronts in the MENA-region during 2010-2012. We still feel the effects of these events, having witnessed a reduced demand for real estate and tourism among our destinations which has lead to lower profit and cash generation.

Therefore, we created different initiatives to tackle the current challenges derived from the changed environment. The overall goal of these initiatives is to become more efficient and effective and to increase internal and external transparency.

The key initiative is the comprehensive reengineering of the whole Group. In the framework of this reengineering, we establish a more common understanding of the business we are in. We reviewed our process landscape and optimized the related business, management and support processes. We focus on the group wide standardization of all our processes, organizational structures and

tools. In addition we aligned the roles, objectives and responsibilities across the Group and improved our management principles. The implementation of the results of all these efforts in the daily business is a key factor of success for the reengineering. Hence the respective training of our staff as well as a process based management system which is accessible via our Intranet are important elements of the initiative.

Corporate Initiatives

Raymond Cron

SVP European Destinations & Responsible for Corporate Development

14 | Orascom DevelopmentAnnual Report 2011 | 15

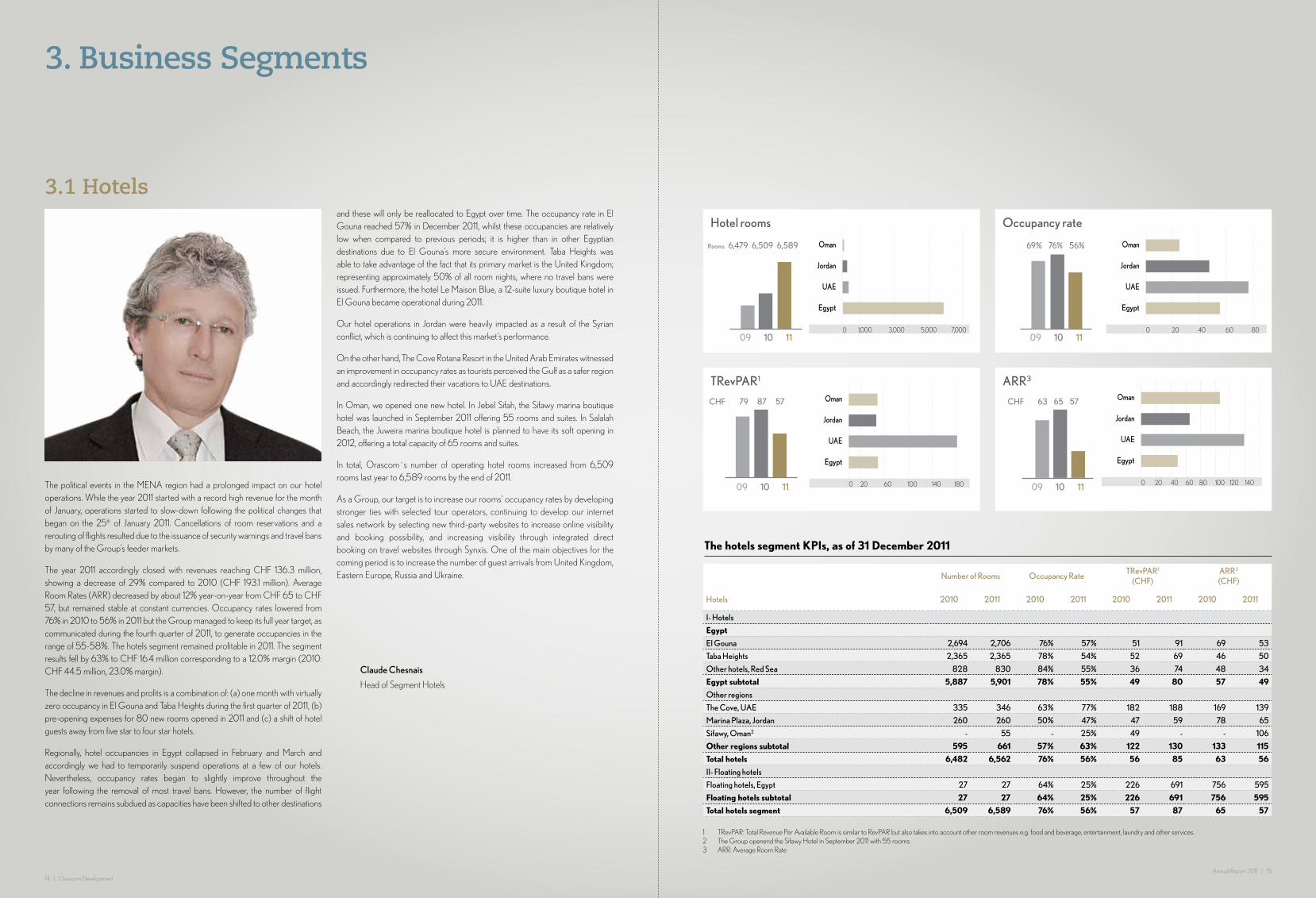

The political events in the MENA region had a prolonged impact on our hotel operations. While the year 2011 started with a record high revenue for the month of January, operations started to slow-down following the political changes that began on the 25th of January 2011. Cancellations of room reservations and a rerouting of flights resulted due to the issuance of security warnings and travel bans by many of the Group’s feeder markets.

The year 2011 accordingly closed with revenues reaching CHF 136.3 million, showing a decrease of 29% compared to 2010 (CHF 193.1 million). Average Room Rates (ARR) decreased by about 12% year-on-year from CHF 65 to CHF 57, but remained stable at constant currencies. Occupancy rates lowered from 76% in 2010 to 56% in 2011 but the Group managed to keep its full year target, as communicated during the fourth quarter of 2011, to generate occupancies in the range of 55-58%. The hotels segment remained profitable in 2011. The segment results fell by 63% to CHF 16.4 million corresponding to a 12.0% margin (2010: CHF 44.5 million, 23.0% margin).

The decline in revenues and profits is a combination of: (a) one month with virtually zero occupancy in El Gouna and Taba Heights during the first quarter of 2011, (b) pre-opening expenses for 80 new rooms opened in 2011 and (c) a shift of hotel guests away from five star to four star hotels.

Regionally, hotel occupancies in Egypt collapsed in February and March and accordingly we had to temporarily suspend operations at a few of our hotels. Nevertheless, occupancy rates began to slightly improve throughout the year following the removal of most travel bans. However, the number of flight connections remains subdued as capacities have been shifted to other destinations

and these will only be reallocated to Egypt over time. The occupancy rate in El Gouna reached 57% in December 2011, whilst these occupancies are relatively low when compared to previous periods; it is higher than in other Egyptian destinations due to El Gouna’s more secure environment. Taba Heights was able to take advantage of the fact that its primary market is the United Kingdom; representing approximately 50% of all room nights, where no travel bans were issued. Furthermore, the hotel Le Maison Blue, a 12-suite luxury boutique hotel in El Gouna became operational during 2011.

Our hotel operations in Jordan were heavily impacted as a result of the Syrian conflict, which is continuing to affect this market’s performance.

On the other hand, The Cove Rotana Resort in the United Arab Emirates witnessed an improvement in occupancy rates as tourists perceived the Gulf as a safer region and accordingly redirected their vacations to UAE destinations.

In Oman, we opened one new hotel. In Jebel Sifah, the Sifawy marina boutique hotel was launched in September 2011 offering 55 rooms and suites. In Salalah Beach, the Juweira marina boutique hotel is planned to have its soft opening in 2012, offering a total capacity of 65 rooms and suites.

In total, Orascom`s number of operating hotel rooms increased from 6,509 rooms last year to 6,589 rooms by the end of 2011.

As a Group, our target is to increase our rooms’ occupancy rates by developing stronger ties with selected tour operators, continuing to develop our internet sales network by selecting new third-party websites to increase online visibility and booking possibility, and increasing visibility through integrated direct booking on travel websites through Synxis. One of the main objectives for the coming period is to increase the number of guest arrivals from United Kingdom, Eastern Europe, Russia and Ukraine.

3. Business Segments

3.1 Hotels

TRevPAR1 ARR3

CHF 79 87 57

Hotel rooms Occupancy rate

69% 76% 56%

CHF 63 65 57

Rooms 6,479 6,509 6,589

Egypt

UAE

Oman

Jordan

0 20 40 60 80

Egypt

UAE

Oman

Jordan

0 20 60 100 140 180

Egypt

UAE

Oman

Jordan

0 20 40 60 80 100 120 140

Egypt

UAE

Oman

Jordan

0 1,000 3,000 5,000 7,000

Claude Chesnais

Head of Segment Hotels

The hotels segment KPIs, as of 31 December 2011

Number of Rooms Occupancy RateTRevPAR1

(CHF)ARR3

(CHF)

Hotels 2010 2011 2010 2011 2010 2011 2010 2011

I- Hotels

Egypt

El Gouna 2,694 2,706 76% 57% 51 91 69 53

Taba Heights 2,365 2,365 78% 54% 52 69 46 50

Other hotels, Red Sea 828 830 84% 55% 36 74 48 34

Egypt subtotal 5,887 5,901 78% 55% 49 80 57 49

Other regions

The Cove, UAE 335 346 63% 77% 182 188 169 139

Marina Plaza, Jordan 260 260 50% 47% 47 59 78 65

Sifawy, Oman2 - 55 - 25% 49 - - 106

Other regions subtotal 595 661 57% 63% 122 130 133 115

Total hotels 6,482 6,562 76% 56% 56 85 63 56

II- Floating hotels

Floating hotels, Egypt 27 27 64% 25% 226 691 756 595

Floating hotels subtotal 27 27 64% 25% 226 691 756 595

Total hotels segment 6,509 6,589 76% 56% 57 87 65 57

1 TRevPAR: Total Revenue Per Available Room is similar to RevPAR but also takes into account other room revenues e.g. food and beverage, entertainment, laundry and other services.2 The Group openend the Sifawy Hotel in September 2011 with 55 rooms.3 ARR: Average Room Rate

09 10 11

09 10 11

09 10 11

09 10 11

16 | Orascom DevelopmentAnnual Report 2011 | 17

REAL ESTATE – OPERATING REVIEW

The effects of the MENA-region on business operations were inevitable and took their toll on the real estate segment’s business performance during 2011. For our real estate and construction segment in total, which next to the tourism real estate includes our Budget Housing activities, the year 2011 accordingly closed with revenues reaching CHF 67.0 million, showing a decrease of 71% compared to last year (CHF 229.0 million). The main reason for the reduction in revenues was that construction works came to a near halt for about 50 days during the first half of the year in Egypt and Oman. Hence lower revenues were achieved, as the company can only realize real estate revenues when the actual construction work is carried out. The segments result fell 95% from CHF 112.4 million (49.1% margin) to CHF 5.1 million (7.7% margin).

Sales activities 2011 In terms of actual sales numbers from 2011, the Group achieved a sales level of CHF 131.4 million (CHF 115.0 million residential real estate and CHF 16.5 million Budget Housing), which compares to CHF 272.8 million sales during 2010 (CHF 177.5 million residential real estate, CHF 95.4 million Budget Housing).

On a more positive side, contracted units of our Andermatt Swiss Alps project in Switzerland (ASA) increased by 13% year-on-year from CHF 62.7 million in 2010 to CHF 70.9 million in 2011. The split of real estate buyers by nationality in 2011, when measured by revenue was: 53% Switzerland, 20% Middle East, 5% each from Germany and the UK and the remaining 17% from other European buyers.

Real Estate sales in Egypt were severely affected as a result of security concerns, a more hesitant attitude from foreign and local investments, a 55-day halt in the stock market, and a complete halt in construction for almost two months approximately 25% of annual working days lost. In total, Orascom sold about CHF 42.8 million worth of real estate including CHF 16.5 million from budget housing versus CHF 183.1 million last year (including CHF 95.4 million from budget housing).

A delay in construction in Oman as a result of the material shortage resulted in almost 50% sales decrease over the year reaching a level of CHF 13.3 million (2010: CHF 24.1 million). It is also worth mentioning that foreign exchange rate fluctuations had a significant negative impact on the Group’s sales in the country.

During the first quarter of 2011, Orascom Development launched the first phase of real estate sales in Chbika, Morocco. In 2011, the company sold 31 units with a value of CHF 4.5 million. Furthermore, we commenced the construction of the town marina during the previous year.

Deferred income (deferred revenue) in 2011 increased compared to last yearIn compliance with IFRS (International Financial Reporting Standards) requirements, Orascom Development treats deferred income from the sale of real estate as a balance sheet position under other current liabilities (net of receivables). Deferred income relates to sold and contracted real estate units that are either under construction or where construction will be carried out in the following years. The corresponding revenues from deferred income will be recognized in the profit and loss statement in 2012 and the years after. By the end of 2011, the balance of deferred income amounted to CHF 262.2 million and is reconciled as follows: (1) 2011 opening balance amounted to CHF 227.9 million, (2) plus the total value of contracted units in 2011 of CHF 131.4 million, (3) less the value of real estate revenues recognized in 2011 and other items, where total revenues amounted to CHF 67.0 million; of which CHF 53.2 million were recognized from the deferred income balance, CHF 8.0 million from extra works, and CHF 5.7 million recognized from third party construction contracts, (4) less the value of cancelled real estate units which amounted to CHF 39.2 million, where Switzerland accounted for CHF 28.1 million and the balance from cancelled units in Oman and Egypt. Due to the net present value calculation of the closing balance of deferred income for 2011, a balance of CHF 4.9 million was transferred to discount account receivable and notes receivable.

Inventory As a Group, our primary focus in 2011 was to continue sale’s efforts and increase cash collection. The main catalyst for this initiative was pushing the sale of built inventory across all destinations and in El Gouna specifically. Accordingly, we instituted cash programs for our clients, offering discounts for paying their outstanding balances before their due date. We also fixed the CHF rate for the Andermatt Swiss project making it all the more attractive for our customers and investors especially in Europe.

Abdallah El Nockrashy

Head of Segment Real Estate

3.2 Real Estate & Construction

Total value of contracted units Total number of contracted units

CHF Millions 218 273 132

Average selling price CHF/m2

(residential)

CHF 3,024 4,432 5,255

Average selling price CHF/m2

(budget housing)

CHF 305 349 352

Average selling price CHF/m2

(total)

3,456 3,557 898Contracted units

Egypt

Moroco

Switzerland

Oman

4,000 8,000 12,000 16,000 20,000

Egypt

Moroco

Switzerland

Oman

0 10 20 30 40 50 60 70

Egypt

Moroco

Switzerland

Oman

0 200 400 600 800

The Real Estate KPIs, as of 31 December 2011

Average selling price CHF/m2 Total value of contracted units (CHF millions)

Number of contracted units

Hotels 2010 2011 2010 2011 2010 2011

I- EGyPT

El Gouna 3,428 2,762 83.5 24.8 211 47

Fayoum 1,070 1,042 4.3 1.5 34 12

Haram City 348 312 31.6 12.5 1,499 649

Makadi 584 591 63.7 3.9 1,752 96

Egypt subtotal 746 683 183.1 42.8 3,496 804

II- U.A.E.

The Cove 2,518 - 2.9 - 5 -

III-Oman

Jebel Sifah 2,928 2,516 12.9 7.4 17 15

Salalah Beach 2,545 2,294 11.2 5.9 26 20

Oman Subtotal 2,724 2,400 24.1 13.3 43 35

IV- Switzerland

Andermatt Swiss Alps 16,373 17,276 62.7 70.9 13 28

V- Morocco1

Chbika - 1,431 - 4.5 - 31

Total real estate 1,071 1,848 272.8 131.4 3,557 898

Total real estate(Excluding budget housing)

4,432 5,255 177.5 115.0 297 152

1 Real Estate sales in Morocco started in 2011

09 10 11 09 10 11

09 10 1109 10 11

18 | Orascom DevelopmentAnnual Report 2011 | 19

Within Town Management, we are responsible not only for providing and maintaining top-quality hotels and residences, but for the day-to-day maintenance and upkeep of the town’s power grid, desalination plants and sewage plants. We are also in charge for the town’s security and other services. As a rule, the town facilities and infrastructure such as hospitals and water desalination facilities, are owned and operated by one of our majority-owned subsidiaries. The term Town Management refers to all revenues generated from municipal facilities. It primarily includes revenues from utilities (such as electricity, irrigation, and telephone lines), as well as community services (such as: airport, museum, sporting club, and bakeries), urban services (such as: garbage collection, security, and fire brigade), and commercial services (such as: fish and fowl farm).

Developments and performance in 2011

We were able to increase the segment revenues in comparison to 2010 by 1% to CHF 17.7 million. However, the segment result decreased to CHF 6.6 million losses versus a CHF 2.5 million profit last year. The main reasons for the decrease of the segment result were as following. First of all, a new destination usually needs two to four years until it becomes operationally break-even. During 2011, the segment Town Management for the first time included the destinations Jebel Sifah and Salalah Beach which hardly provided any revenues, but a substantial amount of costs. In addition in our destination The Cove, U.A.E we paid a low single digit million amount for an increased use of electricity.

We were challenged with the maintenance costs needed to retain the quality of offerings within our destinations as opposed by limited cash collections. A new Electricity grid with 100% power from the Government was introduced in El Gouna, Egypt. Accordingly we disconnected the diesel generators that were previously used and installed the new electricity grid through which we should receive cleaner electricity. The prior connection had a cost of CHF 10 million designed for 100 MV amperes of which 50 are already connected and therefore,

with the newly introduced grid, we expect to reduce the associated running costs during future financial periods. Another milestone was realized during 2011 by signing an agreement with the renowned Troon Golf; the leader in upscale golf course management, development and marketing, to manage two of our golf courses in El Gouna and Taba Heights in Egypt.

Our most recent project was a joint cooperation with the German Technical University Berlin, which is setting up a satellite campus as an external research department. In January 2012, we officially launched our TU Berlin Campus in El Gouna, which should be ready for use as of April 2012 with master courses commencing in October 2012.

During 2012, we intend to focus on improving the service quality to our clients whether it’s a hotel guest, real estate buyer or a member of staff.

Hamza Selim

SVP Destinations Management

3.3 Town Management

Total revenues

2011: CHF 17.7 million

2010: CHF 17.5 million

Segment result

2011: CHF 6.6 million losses

2010: CHF 2.5 million

3.4 Other Segments

Occasionally, the Group sells land where there is no additional development commitments. Revenues from such sales are included in our land sales segment. Land sales segment accounted for only 1% from our total revenues during 2011 (2010: 1.9%).

Total Revenues

2011: CHF 2.3 million2010: CHF 10.2 million

Segment Result

2011:CHF 0.3 million losses2010: CHF 2.2 million

Land Sales

Type of service (CHF Millions) 2010 2011 % Change

Mortgage (real estate financing) 6.7 6.3 (5%)

Sport (golf) 6.7 3.3 (50%)

Rentals 17.1 13.1 (23%)

Hospital services 4.8 3.6 (25%)

Educational services 2.3 2.2 (1%)

Marina 2.2 1.8 (21%)

Limousine 1.6 1.2 (29%)

Laundry services 2.7 1.8 (34%)

Leasing 3.8 4.8 26%

Others 36.7 6.9 (81%)

Total segment revenues 84.5 44.9 (47%)

Intersegment revenues (eliminations) (46.7) (14.4) (69%)

Total revenue from external customers 37.8 30.5 (19%)

Total Revenue

2011: CHF 30.5 million2010: CHF 37.8 million

Segment Result

2011: CHF 0.3 million2010: CHF 23.4 million

The segment result in 2011 was CHF 0.3 million compared to CHF 23.4 million in 2010. The positive contribution in 2010 from the revaluation of the investment properties in Mauritius and the units rented in El Gouna (total CHF 14.1 million) did not take place in 2011. The value of the project in Mauritius in 2011 remained the same as in 2010, while the properties in El Gouna (rented restaurants, shops and apartments) reduced by CHF 4.7 million. As of the end of 2011, the total value of all investment properties owned by Orascom Development was CHF 76.4 million, compared to CHF 78.4 million in 2010.

Other Operations

Tours Operations

Total Revenues

2011: CHF 2.3 million2010: CHF 28.5 million

Segment Result

2011: CHF 0.1 million losses2010: CHF 3.0 million

Until June 30, 2010, the Group held a controlling stake in the Garranah tours operations companies. Following the sale of companies in June 2010, we no longer hold a controlling stake in these entities. As a result, starting July 1, 2010, our consolidated financial statements no longer show revenues generated by the tours operations business of the Garranah tours operations companies as part of our tours operations segment. Rather, the corresponding net income is recognized as income from investment in associates. Our tours operations segment accounted for 0.9% of our total revenues in the financial period ending 31 December 2011 (2010: 5.5%).

20 | Orascom DevelopmentAnnual Report 2011 | 21

4. Countries

Destinations Portfolio

Notes:1 Year in which the master plan is deemed final by the Group (E= estimates).

Orascom Development’s strategy is based on the creation of value in its land bank for the medium to long term. To that end, we accumulate large tracts of land with enough space to develop self-sufficient communities and towns. To date the Group has secured, subject to certain conditions, land banks of approximately 116 million m2 in several jurisdictions. Orascom Development holds its undeveloped land banks primarily by way of contractual rights or usufructs with the option to acquire legal titles. On these land banks, we develop fully-integrated towns, generally retaining or obtaining ownership in hotels, commercial real estate, facilities and staff housing towns while selling the residential units. The revenues generated in our towns primarily originate from the sale of residential units (villas and apartments), hotel operations, the rental of commercial properties, and the management of infrastructure and other facilities.

Orascom Development retains reputable and well-established third party hotel operators including Accor’s Sofitel, Cheval Blanc, Chedi, ClubMed, Four Seasons, Hyatt Regency, InterContinental, Marriott, Mövenpick, Radisson Blu, Rotana, Starwood’s Sheraton, and Steigenberger as well as local chains in Egypt such as The Three Corners (TTC), Azur, and Optima to manage hotels in developed destinations and retain management of only niche hotels. We have established a separate legal entity for each self-managed hotel and while we might invite other reputable partners to participate in those hotel ownership companies, we generally retain a controlling stake.

As a rule, any given town’s facilities and infrastructure (including hospitals and water desalination facilities) are owned and operated by majority-owned subsidiaries of the Group or rented out (such as schools).

Destinations

The Group has developed five fully-integrated destinations which are currently operational: the tourist destinations of El Gouna (Red Sea coast, Egypt), Taba Heights (Sinai Peninsula, Egypt) and The Cove (Ras Al Khaimah, UAE) as well as the budget housing community of Haram City (Greater Cairo area, Egypt). Each of these destinations has the complete infrastructure of a self-sufficient town. Recently, Jebel Sifah commenced operations adding a new operating destination.

In addition, nine destinations including tourist towns and budget housing communities are currently in various stages of development and planning in Egypt, Oman, Morocco, Switzerland, Montenegro, and the United Kingdom, and also three destinations in the pipeline in Oman and Romania. Furthermore, we have participations in other hotels in development in Jordan and Egypt.

The following table provides an overview of our portfolio of destinations, in operation and under development, and in the pipeline as of December 31, 2011.

Destination NameDestination Status/ Type

Development start1 (year)

Total area (million m2)

Developed (million m2)

Undeveloped (million m2)

Developed (%)

EGyPT

El Gouna Operating 1990 36.8 14.7 22.1 40%

Taba Heights Operating 1996 4.3 2.8 1.5 65%

Amoun Island Developing 2007 0.02 - 0.02 0%

Fayoum Developing 2007/08 1.3 0.5 0.8 38%

Makadi Developing 2009 3.8 0.4 3.3 11%

Haram City Operating 2007 4.2 1.9 2.3 45%

Qena Gardens Developing 2011 0.8 0.1 0.7 8%

Royal Azur Other Hotel

Club Azur Other Hotel

Oberoi Zahra Other Hotel

UNITED ARAB EMIRATES

The Cove Operating 2005 0.3 0.28 0.01 94%

JORDAN

Tala Bay Other Hotel 2002

OMAN

Jebel Sifah Operating 2007 6.2 0.6 5.6 10%

Salalah Beach Developing 2007 25.1 0.7 24.4 3%

As Sodah In the pipeline 2009 1.0 0.02 1.0 2%

City Walk In the pipeline 2011 0.05 0.0 0.05 0%

SWITZERLAND

Andermatt Developing 2008 1.5 0.0 1.5 0%

MOROCCO

Chbika Developing 2010 15.0 0.0 15.0 0%

MONTENEGRO

Lustica Developing 2012E 6.8 0.0 6.8 0%

UNITED KINGDOM

Eco-Bos Developing 2013E 6.6 0.0 6.6 0%

ROMANIA

Constanta In the pipeline 2011 2.5 0.0 2.5 0%

Total 116.2 22.0 94.2 19%

Introduction

22 | Orascom DevelopmentAnnual Report 2011 | 23

El Gouna, Egypt

El Gouna’s first phase in 1990 consisted of 15 houses sold exclusively to Egyptian nationals. Real estate value has increased substantially, from an average selling price of approximately CHF 1,071/m2 in the financial year 2000 up to CHF 2,762/m2 by the end of 2011. Buyers come from all over the world, with foreign nationals representing approximately 56 percent of homeowners.

El Gouna has eighteen1 operating hotels with a total capacity of 2,897 rooms. Of these, seventeen hotels are controlled by the Group with a total capacity of 2,731 rooms. Hotels accommodate holiday guests from all over the world, primarily from Europe. The following chart highlights the nationalities of hotel guests for all 12 months ending 31 December 2011.

The primary requirements of a modern town are fresh water, electricity, communications, and roads. The Group has invested in all these forms of infrastructure to make El Gouna more attractive to residents and visitors. All the infrastructure is owned and operated by the Group. This currently includes a water desalination facility, sewage plants with a capacity to treat approximately 15,000 m3/day from El Gouna and Hurghada, an electrical power generator to provide part of the town’s electrical needs in the event of a supply failure, and approximately 5,000 telephone lines and Wi-Fi network coverage for all hotels.

36.8million m2

total land area

14.7m2

developed area

2,897rooms

22,000 - 24,000permanent residents

18operatinghotels

419outlets

The town started as a small collection of villas sold only to Egyptian citizens.

1990 2011

Today, El Gouna is the premier tourism destination on the Red Sea coast.

Operating Destination

Our flagship development is a self-sufficient town built on 10 km of Red Sea coastline. The destination has a total land area of 36.8 million m2 of which only 14.7 million m2 has been developed, providing a large land bank for future development. El Gouna is home to a population of 22,000 – 24,000 permanent residents and visitors from all over the world. The town offers international-standard facilities including a landing strip, a hospital and nursing institute, 18-hole championship golf course, three marinas, four schools, child daycare facilities, a library linked to the Bibliotheca Alexandrina, a branch of the American University in Cairo, and TU Berlin University that should be operational in October 2012, 419 outlets including restaurants, bars, shops, various services, and a vibrant town center. The Group has a 100 percent stake in El Gouna.

29%

16%

10%9%

8%

6%

4%

3%

3%

14%

Nationality of hotel guests during 2011

Egypt

Germany

Belgium

United Kingdom

Netherlands

France

Switzerland

Sweden

Russia

1 As at 31 December 2011, El Gouna’s 18 hotels offered a total capacity of 2,897 operating rooms, of which 17 hotels are controlled by the Group, offering a total capacity of 2,731 rooms. This excludes “El Khan”, 25 rooms, one star hotel, which is 100% owned by the Group and is leased to third party.

24 | Orascom DevelopmentAnnual Report 2011 | 25

2011

Natural beauty and access to regional tourism destinations sets Taba Heights apart.

The Group’s second integrated development on the shores of the Sinai Peninsula.

1996

The town is home to approximately 4,000 permanent residents including facility staff and offers a range of facilities such as a medical center, child daycare services, school, and a vibrant town center. Furthermore, the destination features 102 outlets including restaurants, cafés, bars, and retail, 16 hotel swimming pools, an 18-hole championship golf course, various spas and Egypt’s first Salt Cave. The marina’s 40,000 m2 basin has a berthing capacity of 50 yachts and is host to the Red Sea’s largest water activity center.

The Egyptian Government continues to prohibit the sale of real estate in the Taba area to non-Egyptian nationals, thus Taba Heights is managed exclusively as a holiday

destination. There are six operating hotels with a current capacity of 2,365 rooms. To accommodate holiday guests from all over the world.

Taba Heights has the necessary infrastructure of a modern town, all owned and operated by Orascom Development. It includes a water desalination facility and two town sewage treatment plants. The town is self-sufficient in terms of power supply with an installed capacity of 16 MVA of electrical power generation. Communication infrastructure includes approximately 1,000 telephone lines and a Wi-Fi network covering the whole development including hotels.

Taba Heights, Egypt

4.3 million m2

total land area

2.8million m2

developed area

2,365rooms

4,000Permanentresidents

6operatinghotel

102outlets

Taba Heights is the Group’s second fully self-sufficient resort town, developed after the successful model of El Gouna. The destination comprises a total land area of approximately 4.3 million m2 with around 2.8 million m2 already developed. The destination is situated along the Red Sea coast on the northern end of the Gulf of Aqaba, approximately 200 km north of Sharm El Sheikh and around 20 km south of the Israeli town of Eilat. Taba International Airport is only 25 km away from Taba Heights. The Group has a 99 percent stake in Taba Heights.

27%

18%

12%10%

7%

5%

4%

4%

2%

14%

United Kingdom

France

Israel

Egypt

Belgium

Russia

Poland

Ukraine

Jordon

Operating Destination

Nationality of hotel guests during 2011

26 | Orascom DevelopmentAnnual Report 2011 | 27

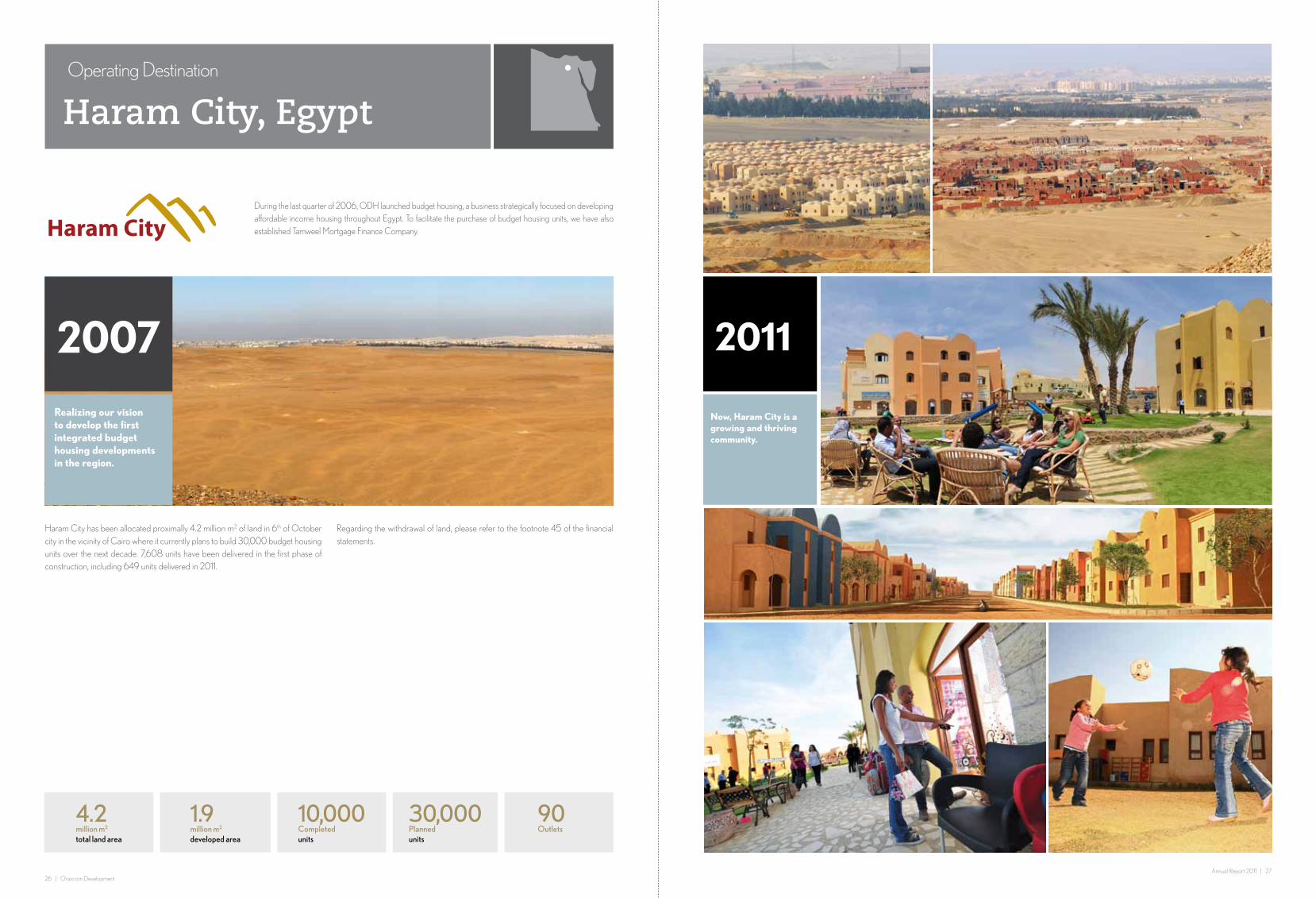

Haram City has been allocated proximally 4.2 million m2 of land in 6th of October city in the vicinity of Cairo where it currently plans to build 30,000 budget housing units over the next decade. 7,608 units have been delivered in the first phase of construction, including 649 units delivered in 2011.

Regarding the withdrawal of land, please refer to the footnote 45 of the financial statements.

Haram City, Egypt

4.2million m2

total land area

1.9million m2

developed area

30,000Plannedunits

10,000Completedunits

90Outlets

Haram City

Realizing our vision to develop the first integrated budget housing developments in the region.

2007

During the last quarter of 2006, ODH launched budget housing, a business strategically focused on developing affordable income housing throughout Egypt. To facilitate the purchase of budget housing units, we have also established Tamweel Mortgage Finance Company.

Operating Destination

2011

Now, Haram City is a growing and thriving community.

28 | Orascom DevelopmentAnnual Report 2011 | 29

38luxurious suites planned

22,000 m2

total land area

Group LVMHhotel partner

62Guest rooms planned

301Residential rooms planned

1.3 m2

total land area

0.6m2

Developed land area

In 1998 Orascom Development was awarded land acquisition rights by the Government of Egypt for a residential real estate destination in El Fayoum Oasis. El Fayoum is located approximately 100 km southwest of Cairo. Total land parcels secured cover approximately 1.3 million m2. The Al Roboua project in Fayoum offers 36 standalone villas in traditional Nubian style with all supporting amenities, covering a total area of 0.07 million m2.

During the third quarter of 2008, the Group launched Byoum, a second real estate project in El Fayoum Oasis. The destination is planned to offer 138 apartments, 127 villas with full access to an attached marina and 4-star 62-room hotel. Site development commenced during the third quarter of 2008 and residential components and the hotel are expected to be operational by mid-2012.

Regarding the withdrawal of land, please refer to the footnote 45 of the financial statements.

Fayoum, Egypt

Qena Gardens, Egypt

In 2010, OHC was allocated 0.8 million m2 of land in the Qena governorate. The destination is planned to offer an additional 8,000 basic affordable housing units. The destination will be developed as a fully-integrated town complete with school, clinics, shopping areas, and entertainment venues. In 2011, there have been 366 completed units with a contractual delivery date in 2012.

Amoun Island, Egypt

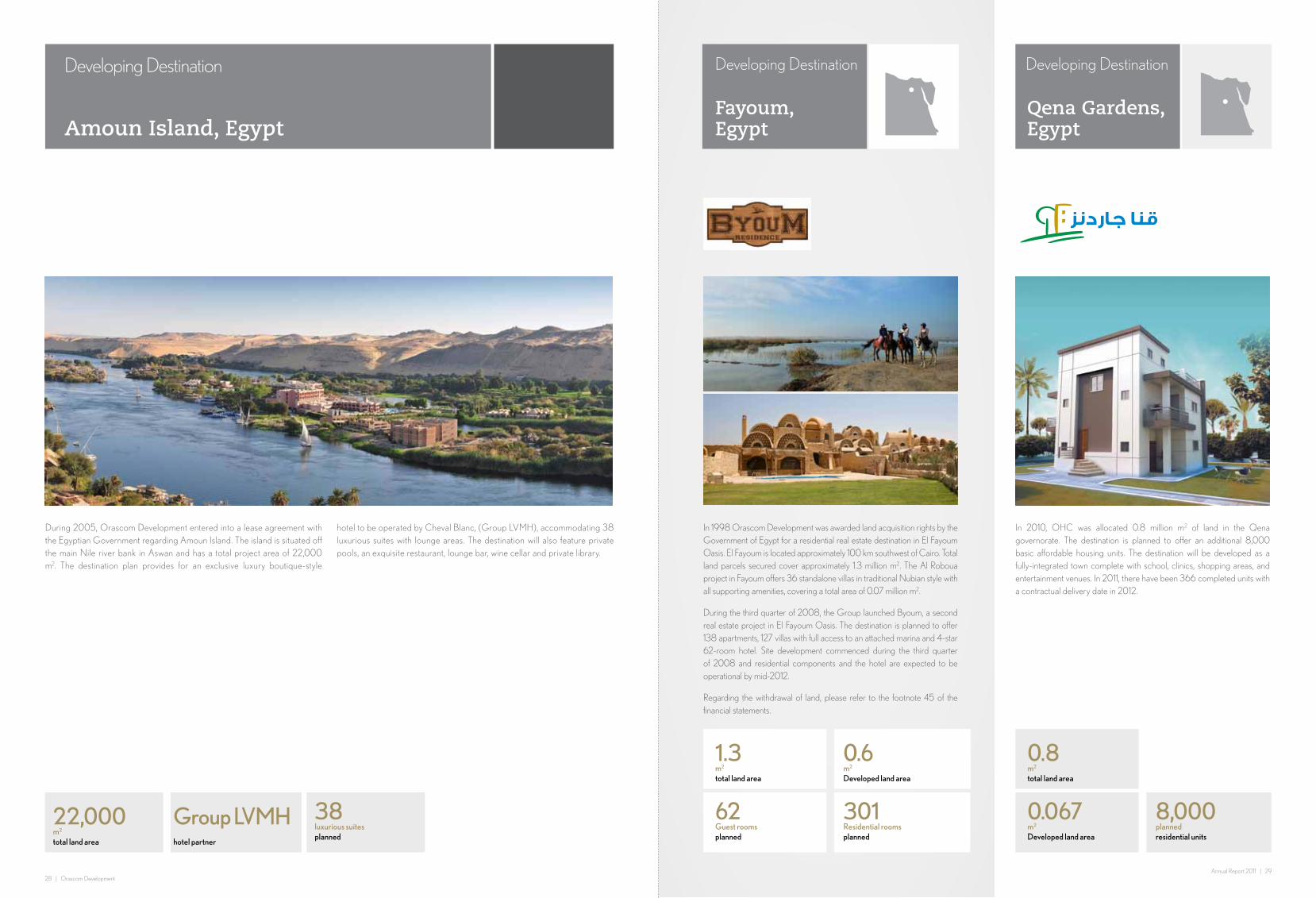

Developing Destination Developing Destination Developing Destination

During 2005, Orascom Development entered into a lease agreement with the Egyptian Government regarding Amoun Island. The island is situated off the main Nile river bank in Aswan and has a total project area of 22,000 m2. The destination plan provides for an exclusive luxury boutique-style

hotel to be operated by Cheval Blanc, (Group LVMH), accommodating 38 luxurious suites with lounge areas. The destination will also feature private pools, an exquisite restaurant, lounge bar, wine cellar and private library.

0.067m2

Developed land area

8,000planned residential units

0.8 m2

total land area

30 | Orascom DevelopmentAnnual Report 2011 | 31

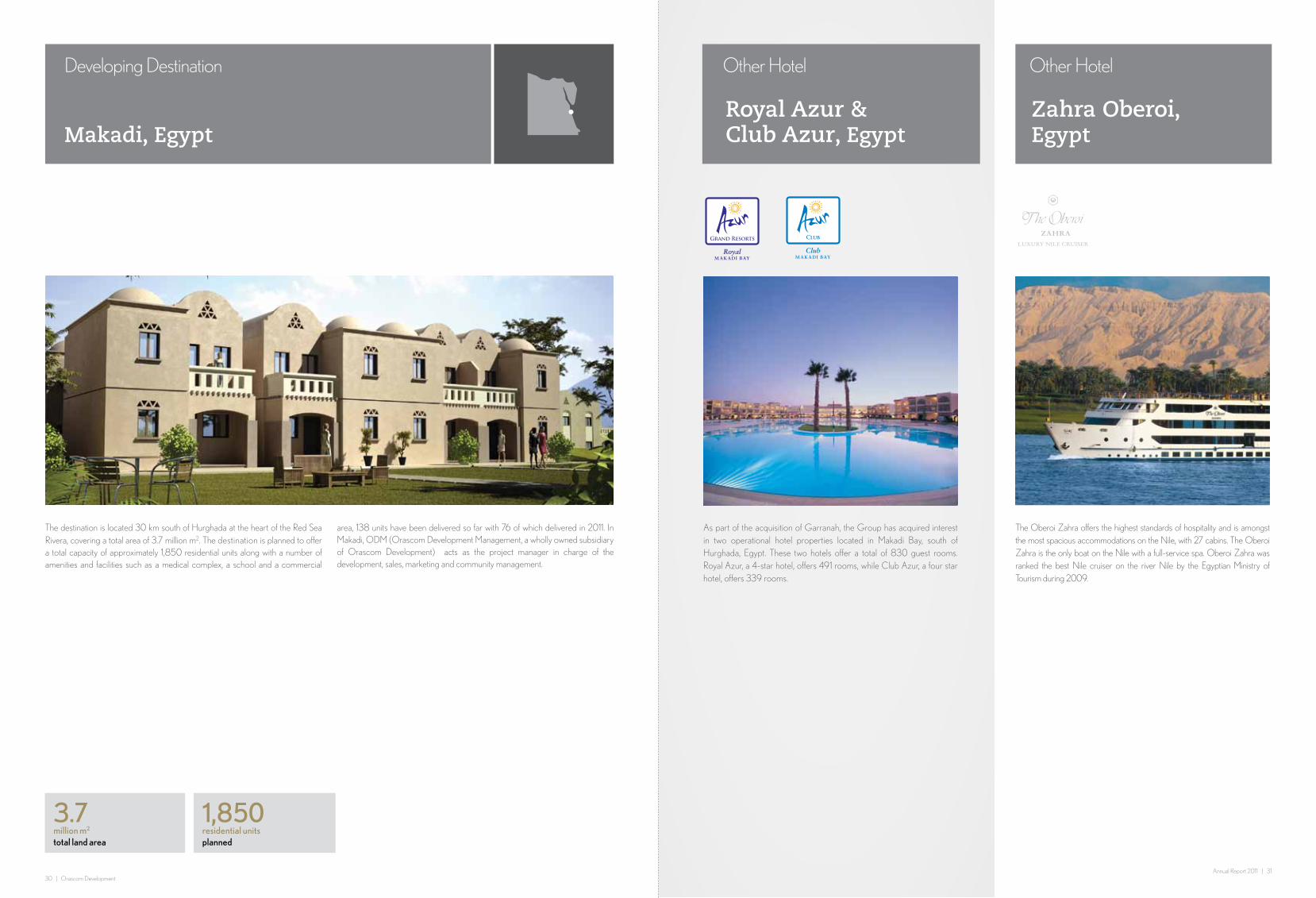

As part of the acquisition of Garranah, the Group has acquired interest in two operational hotel properties located in Makadi Bay, south of Hurghada, Egypt. These two hotels offer a total of 830 guest rooms. Royal Azur, a 4-star hotel, offers 491 rooms, while Club Azur, a four star hotel, offers 339 rooms.

Royal Azur & Club Azur, Egypt

Zahra Oberoi, Egypt

The Oberoi Zahra offers the highest standards of hospitality and is amongst the most spacious accommodations on the Nile, with 27 cabins. The Oberoi Zahra is the only boat on the Nile with a full-service spa. Oberoi Zahra was ranked the best Nile cruiser on the river Nile by the Egyptian Ministry of Tourism during 2009.

Makadi, Egypt

The destination is located 30 km south of Hurghada at the heart of the Red Sea Rivera, covering a total area of 3.7 million m2. The destination is planned to offer a total capacity of approximately 1,850 residential units along with a number of amenities and facilities such as a medical complex, a school and a commercial

area, 138 units have been delivered so far with 76 of which delivered in 2011. In Makadi, ODM (Orascom Development Management, a wholly owned subsidiary of Orascom Development) acts as the project manager in charge of the development, sales, marketing and community management.

RoyalM A K A DI BAY

Grand Resorts

ClubM A K A DI BAY

Club

3.7million m2

total land area

1,850residential unitsplanned

Developing Destination Other Hotel Other Hotel

32 | Orascom DevelopmentAnnual Report 2011 | 33

62%18%

3%

2%2%

13%

In the U.A.E., the Cove represents the Group’s first development in the Gulf.

2005

Our operational destination of The Cove is located close to Ras Al Khaimah International Airport and approximately 100 km north of Dubai. The development comprises a total area of around 300,000 m2, of which approximately 282,000 m2 have been developed. The destination is fully complete, offering 190 residential units with easy access to leisure and town facilities,

including shopping malls, international schools and hospitals within Ras Al Khaimah.

The 5-star Rotana Resort & Spa soft opening took place in early 2009 with 346 rooms. The second phase was completed during the fourth quarter of 2009 with the delivery of 78 residential apartments.

The Cove, U.A.E.Operating Destination

2011

Homes, businesses, and a resort mark the successful application of the Group’s business model.

0.3million m2

total land area

268totalresidential units

0.28million m2

developed area

United Arab Emirates

Germany

Russia

Switzerland

Austria

Others

Nationality of hotel guests during 2011

34 | Orascom DevelopmentAnnual Report 2011 | 35

Tala Bay was the Group’s first regional roll-out of its model outside of Egypt.

Tala Bay is situated on the Gulf of Aqaba in the northern Red Sea, which is Jordan’s only sea gateway. The destination is built on a man-made lagoon and is one of the largest tourism

destinations in the country, covering a land area of approximately 2.7 million m2. The project is located on the outskirts of Aqaba, approximately 10 km from the Aqaba International Airport.

The destination’s masterplan includes residential villas and apartments, a marina, championship golf

course, and commercial facilities. Tala Bay is planned to include four hotels with a total capacity of 1,300 rooms. One of these hotels, the Marina Town Plaza, is wholly owned by the Group and commenced operations in April 2008 with 260 rooms.

Tala Bay, Jordan

Other Hotels

260Rooms

Laying the foundation for the Group’s first experience in the region outside Egypt.

2002 2011

Tala Bay becomes the exciting, exquisite gateway to the Northern Red Sea.

36 | Orascom DevelopmentAnnual Report 2011 | 37

2011

Premier dining, first-class hotels and a stunning marina allow Jebel Sifah to redefine luxury in Oman.

Breathtaking scenery creates the backdrop for hotels, residences, and a fully-integrated community.

2007

Situated some 30 km from downtown Muscat, Jebel Sifah appeals to affluent residents of the country’s capital with its combination of hotels, restaurants, golf course, marina, and retail facilities. The destination comprises a total land area of approximately 6.2 million m2. The initial plan includes five hotels with a total of 804 rooms, of which one hotel will be integrated with a golf course, approximately 950 residential units, a marina, and marina town along with other town features. In the long term, we expect to add to the hotel capacity to reach a target of 800 rooms. World-renowned hotel operators will manage the town’s hotels, such as Rezidor’s Hotel Missoni (250 rooms) and Four Seasons (200 rooms).

During 2011, we launched the Sifawy Boutique hotel offering 55 hotel rooms; we also completed the construction of 18 apartment blocks and we developed out of which 92 apartments and 12 villas. The development of the marina was also completed with a berthing capacity to hold 84 boats in water and 120 on land. The destination is now operating with several restaurants, shops, pharmacies and mini markets are now open serving our clientele’s needs.

Jebel Sifah, OmanOperating Destination

6.2million m2

total land area

0.6million m2

developed area

950residential unitsplanned

800plannedhotel rooms

38 | Orascom DevelopmentAnnual Report 2011 | 39

Set amongst a collection of man-made lagoons with hotels and homes.

Situated in the southern part of Oman approximately 1,000 km from Muscat and 15 km from the Salalah Airport, the destination comprises a total land area of 25.1 million m2. The destination is planned to include five hotels with capacity of approximately 1,300 rooms total, three of which will be under the management of international the hotel operators Mövenpick (391 rooms), Rotana (399 rooms), and ClubMed (398 rooms). Scheduled real estate includes 1,150 units as well as other town features.

In 2011, the construction of the Juweira boutique hotel offering 65 rooms was completed and is planned to have its soft opening during May 2012. The marina apartment blocks construction is nearing completion and is expected to be finished in 2012. As of December 2011, we have developed 9 villas and 43 apartments. We also started the construction of the marina completing 10 berths out of its planned capacity of holding 174 boats in water and 120 on land. The marina is expected to be operational in 2012. Moreover, the Rotana Hotel; is currently under construction were about 40% of the construction work is completed.

Salalah Beach, OmanDeveloping Destination

25.1million m2

total land area

0.7million m2

developed area

1,150residential unitsplanned

1,300plannedhotel rooms

2007

The natural setting for Salalah is one of the region’s most beautiful locations.

2011

40 | Orascom DevelopmentAnnual Report 2011 | 41

As Sodah is an island with a surface of around 11 million m2, of which a total 1 million m2 will be developed to offer a niche luxury boutique hotel. Located off the southern coast of Oman opposite Salalah Beach, As Sodah Island will comprise a

luxury hotel with 32 rooms consisting of 20 guest-one bedroom pavilions, 10 two-bedroom villas and two five-bedroom villas. Each exclusive property has its own swimming pool and access to a private beach. The hotel project will also include a main lodge and

a spa building. During 2009, the Group signed a management agreement with Cheval Blanc (Group LVMH) to operate this luxurious property.

The Group is planning to develop a downtown Leisure City complex with a total built up area of 153,000 m2,

a tower with 19,400 m2 of office space, and a mall with a built-up area of 42,000 m2. Furthermore, the project

plan includes a 5 star hotel with a capacity of 270 rooms scheduled to be managed by Grand Hyatt.

As Sodah Island, Oman City Walk, Muscat, OmanDestination in the Pipeline Destination in the Pipeline

42 | Orascom DevelopmentAnnual Report 2011 | 43

Located in the heart of the Swiss Alps, Andermatt is the Group›s first destination in Europe.

2008

In Andermatt, a Swiss mountain village, the Group plans to develop a comprehensive and self-sustainable Alpine resort village as a year-round destination. Andermatt is situated at about 1,440 meters above sea level and lies approximately 120 km south of Zurich and 180 km north of Milan. The total land bank of the project amounts to approximately 1.5 million m2.

The destination is planned to offer 490 apartments and 20-30 private villas. In addition, six hotels classified as 4 and 5-star properties with a capacity of 844 rooms are planned. World-renowned operators will manage the village’s hotels, such as General Hotel Management Ltd (The Chedi Andermatt) and The Carlson Rezidor Hotel Group (Radisson Blu Andermatt). Aside from the existing 13 ski lifts, the destination will feature various leisure facilities including a professional 18-hole golf course, sports center with all-season leisure pool, and a commercial space.

We plan to use a carbon-free energy supply system for the entire resort by using renewable energy sources. In addition, the planned underground parking lot in the podium will offer a capacity for a maximum of 1,970 cars, reducing air pollution and noise in the town. Subject to certain construction obligations, the Group has been granted an exemption from the Lex Koller legislation, which restricts the acquisition of real estate by non-Swiss residents. Pursuant to this exemption, non-Swiss residents will be able to acquire and transfer residential property without authorization until the end of 2030.

Site development started in the fourth quarter of 2008 with the site-specific master plan approvals. Construction began with the launch of the first phase in September 2009. In this phase, the Chedi Andermatt hotel, basic and flood protection infrastructure, the podium, villas and the 18-hole championship golf course started construction. Considerable progress was also achieved in 2011, both in terms of construction

and investment, with sales and reservation contracts totaling CHF 102 million. (sales: CHF 71 million, reservation: CHF 31 million).

2012 will be another important year for the development of the Andermatt Swiss Alps tourist resort with work across its various construction sites continuing. We will see construction begin on the first apartment building on the 46,000 m2 Podium site as well as the first chalet, both of which will be completed by the end of 2013. At the luxury hotel The Chedi Andermatt, finishing touches will be made to both interior renderings as well as the external façade ahead of its official opening in December 2013. At the 18-hole on-site golf course, landscaping work and construction of the Golf Clubhouse will also take place. The course will be finished in the second half of 2012 and transferred to the operator, Andermatt Swiss Alps, where it will be used for test rounds in 2013 before officially opening to the public in 2014. The projected expenditures for 2012 is CHF 115 million.

Andermatt, SwitzerlandDeveloping Destination

1.5million m2

Project area

490units in 42 buildingsApartments

64- and 5-starHotels

20-30totalVillas

18-hole championshipGolf Course

35,000m2

Commercial space

2011

With its Alpine beauty and modern amenities, Andermatt continues to grow into an luxurious mountain retreat.

44 | Orascom DevelopmentAnnual Report 2011 | 45

In 2007, Orascom Development entered into an agreement with the Government of Morocco to develop Chbika as an integrated self-sufficient tourist destination in the south of Morocco. Located approximately 400 km south of Agadir directly in front of the Canary Island of Fuerteventura on the Atlantic Ocean, the destination’s total land bank amounts to 15 million m2.

Among the planned components are eight hotels with a capacity of 2,500 guest rooms, 1,166 apartments, 685 villas, golf courses, a marina, and city center facilities. The inauguration of the first phase took place in June 2009, marking the start of construction and the Group’s mobilization in Morocco. This phase will encompass 5 hotels, a marina, an 18-hole golf course and approximately 1,100 real estate units. In

2011, we finally received all related land acquisition permits, completed the set up of the construction site; with the Marina basin (back-fill of cover dams) nearly completed and Marina quay walls reached 50% completion. We also commenced the construction of the first mansion walls. The first phase is expected to be operational during the fourth quarter of 2013.

Chbika, MoroccoDeveloping Destination

15.0million m2

total land area

2,500Hotel rooms planned

1,851Residential units planned

A new project is born on the picturesque shores of Morocco.

Activity in Chbika is centered around a vibrant marina town.

20112010

46 | Orascom DevelopmentAnnual Report 2011 | 47

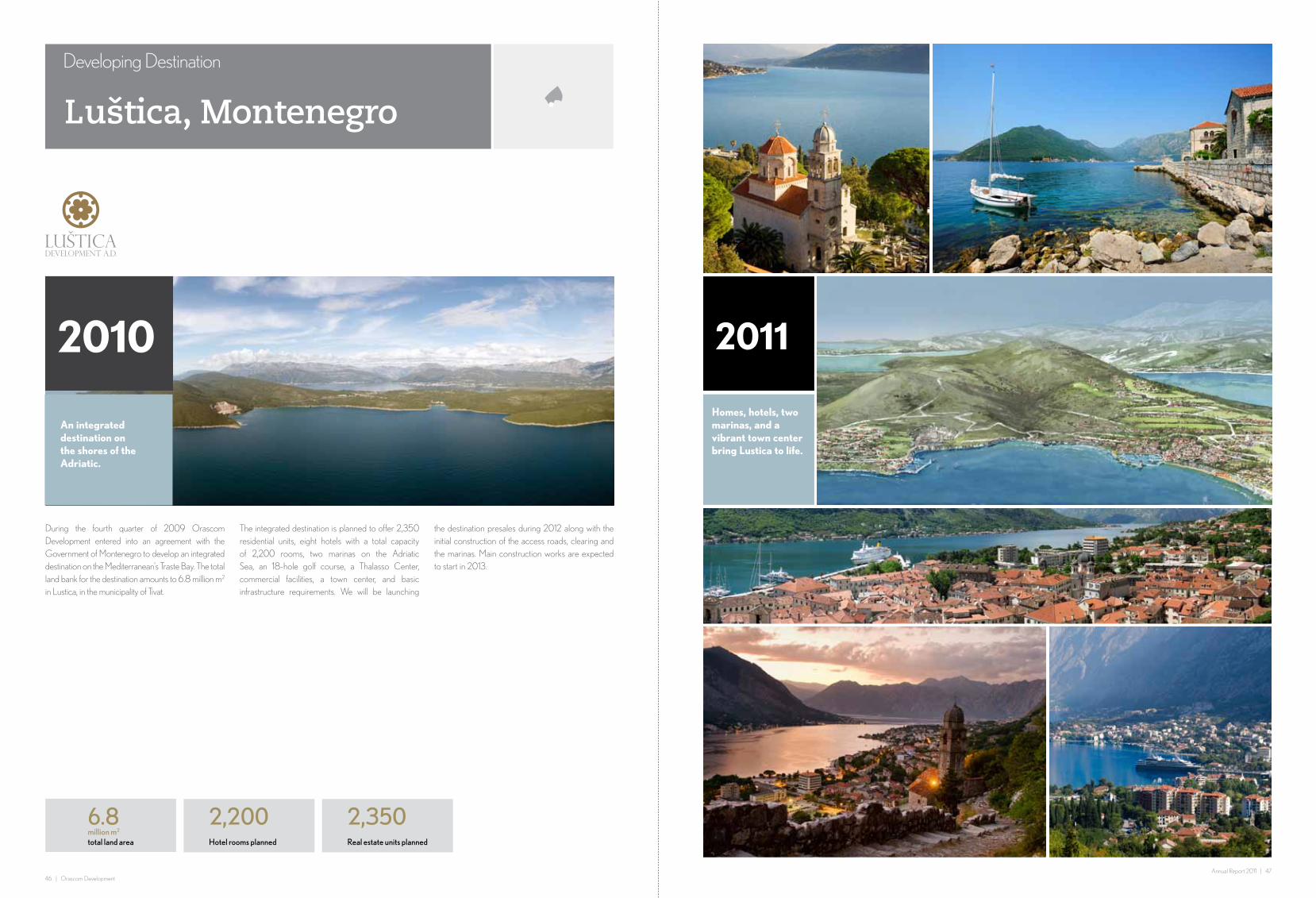

Luštica, Montenegro

During the fourth quarter of 2009 Orascom Development entered into an agreement with the Government of Montenegro to develop an integrated destination on the Mediterranean’s Traste Bay. The total land bank for the destination amounts to 6.8 million m2 in Lustica, in the municipality of Tivat.

The integrated destination is planned to offer 2,350 residential units, eight hotels with a total capacity of 2,200 rooms, two marinas on the Adriatic Sea, an 18-hole golf course, a Thalasso Center, commercial facilities, a town center, and basic infrastructure requirements. We will be launching

the destination presales during 2012 along with the initial construction of the access roads, clearing and the marinas. Main construction works are expected to start in 2013.

6.8million m2

total land area

2,200Hotel rooms planned

2,350Real estate units planned

Developing Destination

An integrated destination on the shores of the Adriatic.

2010

Homes, hotels, two marinas, and a vibrant town center bring Lustica to life.

2011

48 | Orascom Development

Eco-Bos, UK

Developing Destination

During the fourth quarter of 2009, the Group entered into an agreement with Imerys, a multinational industrial minerals company, to develop an integrated Eco Town in Cornwall, United Kingdom. The new joint venture was formally established in May 2010. The total land bank for the project amounts to 6.6 million m2, divided over six plots1. The Cornwall project scheme was developed in response to the United Kingdom Government’s Eco-town competition designed to promote low carbon, sustainable communities across

the country. The project was one of only four to receive ‘Eco-town’ accreditation from the United Kingdom Government and was the sole private led scheme to be awarded such an accolade in the United Kingdom. The project is envisaged to offer a mixed portfolio of real estate units with a total of 5,000 units, including affordable housing and upscale residential units as well as leisure and recreational facilities to include a 5-star hotel and a marina with approximately 125 berths in addition to 251,000 m2 of commercial developments

aimed at job creation in the region. The master planning and design process has been initiated. A detailed planning application for approximately 100 homes was submitted in February 2011 on the first phase of one of the six sites (Baal) contemporaneous with the submission of a wider outline application for the overall site of Baal and the adjacent site of West Carclaze.

6.6million m2

total land area

5,000Eco-homes planned

Orascom signed a joint venture with Imerys for the UK’s newest Eco-Town

2010

The initial Memorandum of Understanding was signed during September 2009 for 6.8 million m2 but between then and final agreements 0.2 million m2 was reserved due to mineral rights. Accordingly, the final agreement signed in May 2010 stated 6.6 million m2.

In 2009 the Group started land acquisition in Constanta, Romania. This destination will be our first budget housing project outside of Egypt.

2.5million m2

total land area

Constanta, Romania

Destination in the Pipeline

2010

50 | Orascom DevelopmentAnnual Report 2011 | 51

5. Sustainability

“Protecting the environment, respecting the social habits of the countries we operate in and safeguarding the sustainability of our developments is deeply rooted in our corporate culture.” Gerhard Niesslein, CEO

Sustainability at Orascom Development

Orascom Development is dedicated to sustainability. As a major town developer with projects in several countries around the globe, the Group recognizes the significant impact on the areas where it operates. These projects are designed to work over the long-term, growing over time and slowly becoming prosperous communities. Therefore, as part of overall strategic planning as well as daily decision-making, the Group implements a range of sustainable practices in all fields to ensure that projects are protected for the future and conserve the pristine natural environment in which the Group operates.

In all Group projects and developments actions are taken based on the assessment of three main areas of sustainability:

• Social

• Environmental

• Economic

The following explanations show how the principles of sustainability are implemented in our daily business.

EnviromentalProtection

SocialConsiderations

EconomicAspects

Sustainable Communities

Social

EconomicEnvironmental

EquitableBearable

Via

ble

52 | Orascom DevelopmentAnnual Report 2011 | 53

5.1 Social Sustainability

Social visionThe Group’s social vision is to integrate local communities, customers and employees, engaging them in the numerous activities and development opportunities available and creating lively communities in which welfare, intercultural understanding and a quality lifestyle become standard. The Group therefore focuses on a holistic development approach. Projects do not simply include homes, but also are completed with the infrastructure to serve the basic needs of the residents as well as the surrounding community. After the construction process is finished, the Group continues to be involved by conducting routine maintenance of town services, implementing certification schemes that provide checklists to ensure that the level of quality provided is never compromised.

Beyond basic services, developments also provide homeowners with a wide array of premium quality services and amenities including international schools, hospitals, and research centres to state of the art marinas and hotels.

The aim of these efforts is to ultimately develop sustainable communities. This requires that everyone, from corporate employees to the local population, gets involved in our projects as responsible contributing members. Through creating jobs, engaging in social causes, educational initiatives, cultural activities and social welfare, the Group ensures that every sector in the community benefits.

Unified code of conductThe Group has a unified code of conduct that all employees must adhere to, part of a handbook prepared according to international standards. The Group is also guided by the principles of sustainability in the selection, development, training and management of employees.

Employee TurnoverThe turnover rate was reduced in 2011 as a result of the outcome of exit interview surveys, loyalty programs, and improving staff recognition.

Work OpportunitiesThe group offers attractive career opportunities to locals in each destination, aimed at improving the standard of living and reduce unemployment.

New Talent Management ProgramThe newly-established Talent Management Program is a systematic planning tool for the development and placement of nominated employees to fill future vacant managerial positions in the company. This program, which already includes eighty-five employees, prepares them for the development process and promotion through talent management training plans, competency development and job rotation methods. The Human Resources department then uses the program to fill key vacant positions with highly-qualified, competent and motivated employees.

Behind the management of our talent are the educational institutions offered across the project portfolio. The quality of universities, schools and other training facilities selected for towns are nothing short of the best in their field, to ensure the ideal lifestyle residents desire. The Group then works to employ graduates of those institutions in various positions in the company.

Training and Education The education department is especially devoted to human development with a focus on the young generations, the key factor in building for the future. Therefore, the department’s main vision is to implement internationally recognised educational standards by integrating different partners in joint projects with local institutions in different educational fields.

End Human Trafficking Now initiativeDeveloped in partnership with the United Nations Global Initiative to Fight Human Trafficking, the Group acts as a main media sponsor for the End Human Trafficking Now Initiative to encourage world leaders and businesses to fight against human trafficking through abiding by ethical business standards.

Learning about Egypt`s heritageSpearheaded by the Egyptian Museum, the Children’s Museum was created in partnership with Lego to develop a place for children to learn more about Egypt’s Pharaonic history by interacting with pieces of history. Replicated monuments are available for children to explore and an added play area lets children build on their own.

Sponsorship of cultural centre in EgyptThe Group also supports many cultural and educational projects, including the Egyptian Center for Culture and Art. Sponsored by El Gouna, the center encourages the diversity of Egypt’s cultural scene, promotes intercultural understanding and presents Egyptian oral and traditional arts.

2008

2009

2011

2010

0% 5% 10% 15%

8.9%

8%

8%

6.5%

Technical University Berlin in El Gouna The Technical University of Berlin (TU Berlin) has recently setup a satellite campus and external research department in El Gouna. Three Masters programs are currently under development, all targeted to the sustainable development of modern urban communities: Energy Engineering, Urban Development and Water Engineering. The first group of students is expected to start courses in September 2012.

American University of Cairo in El Gouna Together with the American University in Cairo, the Group has created a campus in El Gouna for students of the university. This campus serves as an on-site research centre where students can pursue their topics in different academic fields. The branch also offers a number of continuing education and language courses for residents and guests.

Elementary SchoolsAs part of providing comprehensive education, El Gouna is home to an elementary school that offers two programs, national and international. The international program, which currently has 210 students, teaches a British curriculum and is delivered by British-trained instructors. The program is accredited by the Council of International Schools (CIS) and the British Schools of the Middle East (BSME), and is also inspected by the British system to conform with British Schools Overseas standards.

The national section is a higher English language school which delivers the Egyptian National Curriculum in English. Class sizes range from 30 children in some of the primary classes to 15 in the secondary classes.

All children learn Arabic and also have the opportunity to choose a second foreign language, currently French or German, from Primary Level 3. The school has produced students at the top of their level from the Red Sea Governate in the past five years.