annual report 2011 u-bank ltd. · annual report 2011 \ ... – government bonds and makam in the...

TRANSCRIPT

ANNUAL REPORT 2011 U-BANK LTD.

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

2

Annual Report 2011 I Contents

Report of the Board of Directors to the General Meeting of Shareholders 5

Management Review of the Bank’s Financial Position and its Operating Results 133

Certifications of the General Manager and the Chief Accountant 153

Report of the Board of Directors and Management on Internal Control over Financial Reporting and the Report of the Auditors to the Shareholders of UBank Ltd. on Internal Control over Financial Reporting

157

Financial Statements as at December 31, 2011 163

This is a translation from the Hebrew and has been prepared for convenience only. In case of any discrepancy, the Hebrew will prevail.

UBANK LTD. AND CONSOLIDATED COMPANIES

3

Annual Report 2011 I Contents

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

4

Description of the General Development of Bank’s Business History of the Bank 6Profit and Profitability 6Developments in Balance Sheet items 8Holdings Structure Chart 11Principal Investee companies 12Information about the Parent Company 12Description of the Bank’s Operating Segments 12Dividend Distribution 13The Banks' Rating by a Rating Agency 13Human Capital 13Restrictions and Supervision of the Bank’s Activities 15Material Agreements 16Legal Proceedings 17 General Environment and Influence of External Factors on the Bank’s Activity Economic Developments in 2011 18Updates to Legislation relating to the Banking System in 2011 22 Description of the Bank’s Business by Operating Segments 43Fixed Assets and Facilities 56Taxation 56 Additional Information Risk Management Policy 57Accounting Policy on Critical Matters and Critical Accounting Estimates 108Community Activities and Donations 113Disclosure concerning the Bank's Internal Auditor 114Procedure for Approval of the Financial Statements 116Report on Directors with Accounting and Financial Expertise 117Activity of the Board of Directors and Changes in Board Membership 118Members of the Bank's Board of Directors 119Members of the Bank's Management 121Evaluation of Controls and Procedures concerning Disclosure in the Financial Statements 123Details of the Amounts and Benefits paid to Recipients of the Highest Salaries in the Bank 124Remuneration of the Auditors’ 129

UBANK LTD. AND CONSOLIDATED COMPANIES

5

Annual Report 2011 Report of the Board of Directors to the General Meeting of Shareholders

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

6

At the meeting of the Board of Directors held on February 26, 2012 the Board of Directors of UBank Ltd. resolved to approve and publish the audited consolidated financial statements of the Bank and its consolidated companies for the year ended on December 31, 2011. The financial statements were prepared in accordance with the directives and guidelines of the Supervisor of Banks. Description of the General Development of the Bank’s Business History of the Bank The Bank was incorporated in Israel in 1934 under the name “Bank Eretz Israel le’Toelet Ha’ashrai Ltd.” In 1965, the Bank was acquired by Baron Rothschild, who named it “Israel General Bank Ltd.” In 1978, the Bank’s shares were issued to the public on the Tel Aviv Stock Exchange. In 1996, the Bank was acquired by the Investec World Banking Group, and in 1999, the Bank’s name was changed to “Investec Bank (Israel) Ltd.” On December 22, 2004, ownership of the Bank was transferred to “The First International Bank of Israel Ltd” (hereinafter: “FIBI”). Upon acquisition of the Bank by FIBI, and following the acceptance in full of a purchase offer made to the public, the Bank became a private company owned 100% by FIBI. Following the change in ownership, the Bank’s name was changed to “UBank Ltd.” in March 2005, operating as a separate and independent bank, specializing in the personal banking and capital market segments. Profit and Profitability Net profit in 2011 amounted to NIS 40.9 million, compared with NIS 49.0 million in 2010, a decrease of 16.5%. Net operating profit in 2011 amounted to NIS 39.4 million, compared with NIS 49.0 million in 2010, a decrease of 19.6%. In 2011, a profit from extraordinary activities after tax was reported of NIS 1.5 million – see detailed information in Note 25 to the financial statements. Net profit in the fourth quarter of 2011 amounted to NIS 6.8 million, compared with NIS 11.0 million in the corresponding quarter last year, a decrease of 38.2%. The decrease derives mainly from a decline in operating and other income, mainly because of a decline in income from activities in various area of the capital market, which was partly offset by a rise in profit from financing activities resulting mainly from an increase in income due to the effect of fair value adjustments of derivative financial instruments. Operating profit before taxes amounted to NIS 62.8 million in 2011, compared with NIS 79.6 million in 2010, a decrease of 21.1%. The decrease derives mainly from a decrease of 3.1% in operating and other income (NIS 4.2 million), and an increase of 7.4% in operating and other expenses (NIS 12.8 million). which was partially offset by an increase of 2.2% in profit from financing activities (NIS 2.4 million) See details of the effect of the above in the analysis of income and expenses below.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

7

Provision for taxes on operating profit amounted in 2011 to NIS 23.3 million representing 37.1% of the profit before tax, compared with a provision of NIS 29.3 million, representing 36.8% of the profit before tax in 2010. The net return on equity amounted to 9.8% compared with 9.7% in 2010. The net return on equity from ordinary operations amounted to about 9.4% compared with 9.7% in 2010. The return on equity from ordinary activities before taxes amounted to about 15.0%, compared with about 15.7% in 2010. Net profit per NIS 1 par value of ordinary shares amounted in 2011 to NIS 13.1, compared with NIS 15.7 in 2010. Net operating profit per NIS 1 par value of ordinary shares amounted in 2011 to NIS 12.6, compared with NIS 15.7 in 2010. Income and Expenses (NIS million) 2011 2010 Change % Profit from financing activities 110.4 108.0 2.2 Operating and other income 132.0 136.2 (3.1) Operating and other expenses 184.6 171.8 7.4 Of which: other expenses 82.6 79.1 4.4 Of which: salary expenses 75.7 70.5 7.4 Profit from financing activities before income in respect of credit losses amounted to NIS 110.4 million in 2011, compared with NIS 108.0 million in 2010, an increase of 2.2%. The increase derives mainly from a rise in financing income in light of the increase in total credit to the public and in the financing margin on deposits of the public, as well as a rise in income from the effect of fair value adjustments of derivative financial instruments. The increase was partially offset by a decrease in profits from activity in the Bank’s trading portfolio, and a decrease in the current yield on bonds in the portfolio of Israeli securities available for sale, resulting mainly from a decline in the total portfolio and from a decrease in the realization of profits, net. In 2011, a provision was made for impairment of bonds of a nature other than temporary of NIS 0.5 million. In 2010, there was no impairment of bonds of a nature other than temporary. Income in respect of credit losses in 2011 amounted to income in the amount of NIS 5.0 million, compared with income in the amount of NIS 7.2 million in 2010. The income in both years derives from a decrease in the individual provision for credit losses, due mainly to the collection of debts for which a provision was made previously. As of 1.1.2011, the Bank applies the new directive on the measurement and disclosure of impaired debts. Regarding implementation of the directive, see Notes 1 and 4 to the financial statements. Operating and other income amounted to NIS 132.0 million in 2011, compared with NIS 136.2 million in 2010, a decrease of 3.1%. The decrease derives mainly from a decline in income from activity in various

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

8

areas of capital market, and from a decrease in profits of the severance pay fund of the Bank, which were partially offset by an increase in commissions from foreign currency dealing room activity. In addition, a provision was included for impairment of a nature other than temporary in shares in the available for sale portfolio in 2011 of NIS 2.7 million (2010 – NIS 0.8 million). Operating and other expenses in 2011 amounted to NIS 184.6 million, compared with NIS 171.8 million in 2010, an increase of 7.4%. Salaries and related expenses in 2011 amounted to NIS 75.7 million compared with NIS 70.5 million in 2010, an increase of 7.4%, deriving mainly from the updating of salaries of the Bank’s employees and losses by the severance pay fund in the current period compared with profits in the corresponding period last year. The increase was offset by a decrease in the provision for bonuses, due to the decline in profitability from 2010 to 2011. Maintenance expenses and depreciation of buildings and equipment, and amortization of intangible assets in 2011 amounted to NIS 26.3 million, compared with NIS 22.2 million during the corresponding period last year, an increase of 18.5%. The increase derives mainly from the updating of the lease agreement for the premises of the Bank in Tel-Aviv, the opening of new branches, and from a rise in expenses for amortizing intangible assets. Other expenses amounted to NIS 82.6 million in 2011, compared with NIS 79.1 million in 2010, an increase of 4.4%. The increase derives, among other things, from a rise in computer expenses and marketing and advertising that was partially offset by a decline in expenses for professional services. The percentage of cover of operating expenses by operating income was 71.5% in 2011, compared with 79.3% in 2010. The Bank’s share in the results of companies included on equity basis amounted to a loss of NIS 0.1 million in 2011, compared with a loss of NIS 1.3 million in 2010. Developments in Balance Sheet Items Total assets at December 31, 2011 amounted to NIS 7,506.0 million, compared with NIS 7,629.0 million at December 31, 2010, a decrease of 1.6%. Cash and deposits with banks at December 31, 2011 amounted to NIS 2,023.5 million, compared with NIS 2,154.0 million at December 31, 2010, a decrease of 6.1%. Investments in securities at December 31, 2011 amounted to NIS 2,433.9 million, compared with NIS 2,750.8 million at December 31, 2010, a decrease of 11.5%. Investments in securities consists of:

– Government bonds and Makam in the amount of NIS 2,093.5 million; – Bonds of foreign banks (“Eurobonds“) in the amount of NIS 48.7 million, spread over about 6

issuers; – Bonds of Israeli financial institutions in the amount of NIS 127.1 million; – Bonds of companies owned by the Israeli government in the amount of NIS 32.3 million; – Other corporate bonds in Israel and abroad in the amount of NIS 99.4 million, spread over about

26 issuers.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

9

Below is information regarding the duration and rate of the decrease of fair value of available for sale securities, below their adjusted cost, which were recognized direchy in equity and not charged in profit and loss, as at 31.12.11 (in NIS million):

Rate of decrease Duration of decrease Up to 6

months 6-9 months

9-12 months

Over 12 months

Total

Up to 14.6% (3.6) (5.7) (1.2) (4.0) (14.5) 35% * - - - (1.4) (1.4) (3.6) (5.7) (1.2) (5.4) (15.9)

* The bank examined the need to make a provision for other-than-temporary impairment in the bond

in accordance with the accounting policy on critical matters and critical accounting estimates, the Bank Management is of the opinion that there is no need to make a provision. In addition, the decrease in fair value of the available for sale bond declined, approaching the date of approval of the financial statements to 16% and in 20.2.2012, 20% of the bond was redeemed.

Below is information regarding duration and rate of decrease in the fair value of bonds available for sale, below their adjusted cost, which were recognized directly in equity and not charged to profit and loss, as at 31.12.10 (in NIS millions):

Rate of decrease Duration of decrease Up to 6

months 6-9

months 9-12

months Over 12 months

Total

Up to 20% (1.5) (3.5) - (1.7) (6.7) 20.4% - - - (1.7) (1.7) (1.5) (3.5) - (3.4) (8.4)

The decrease in fair value of bonds as at 31.12.2011 includes: A decrease in fair value of NIS 8.4 million of government bonds and government bonds traded abroad. The overall rate of decrease in value of government bonds is up to 20%. An amount of NIS 2.2 million out of the decrease is for a period of up to 6 months, an amount of NIS 5.4 million is for a period of between 6-9 months, and the remainder is for a period of over 12 months. A decrease of NIS 0.7 million in the fair value of bonds of banks including foreign banks, rated A (see also the report on credit exposures to foreign financial institutions). The overall rate of decrease in value of bonds of banks is up to 20%. An amount of NIS 0.1 million is for a period of 6-9 months and the remainder is for a period of over 12 months. A decrease in fair value of NIS 6.8 million of corporate bonds. An amount of NIS 5.4 million out of the decrease in fair value is up to 20%, and the balance is decrease of 35%. An amount of NIS 1.4 million out of the decrease is for a period of up to 6 months, NIS 0.2 million is for a period of 6-9 months, NIS 1.2 million is for a period of 9-12 months, and the remainder is for a period of over 12 months. The negative capital reserve of the Bank increased from NIS 8.4 million at 31.12.10 to NIS 15.9 million at 31.12.11. The data are without the effect of a positive capital reserve and the effect of tax. The total capital reserve as at 31.12.11 is negative in the amount of NIS 8.5 million, including the effects mentioned above (see Note 3 – Securities and the report on changes in shareholders’ equity).

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

10

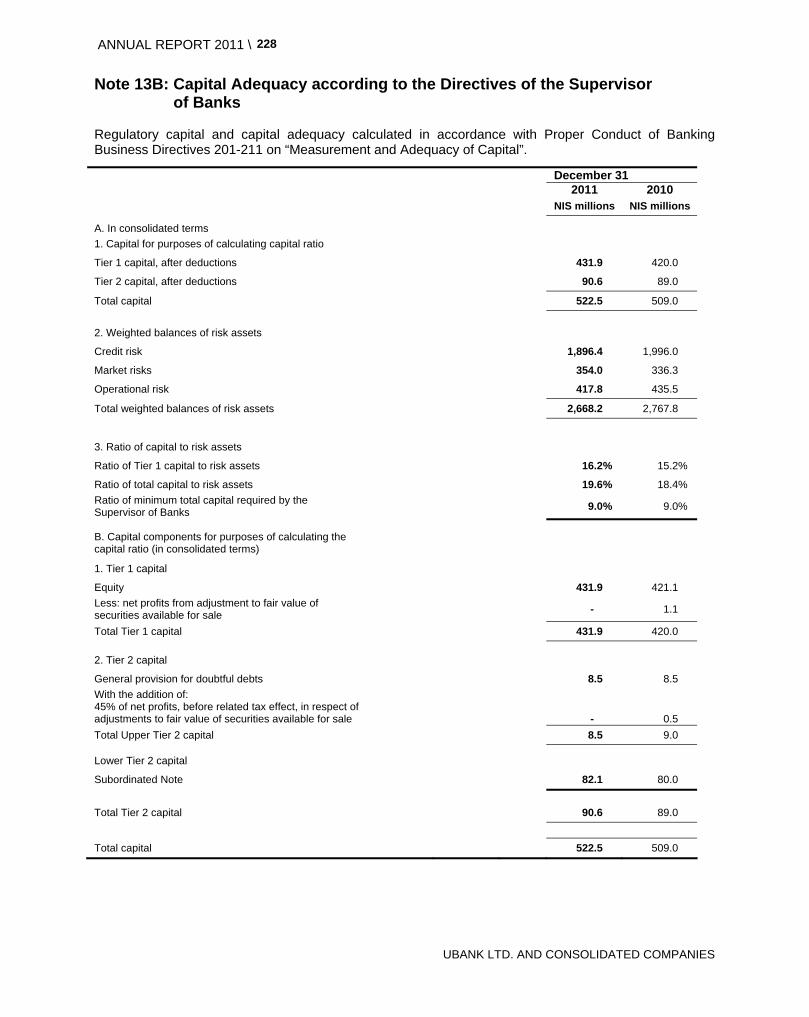

In an examination of the need to make a provision for impairment, in accordance with the accounting policy on critical matters and critical accounting estimates, a provision for impairment of a nature other than temporary was recorded in the Bank’s books in the amount of NIS 3.2 million (regarding the impairment, see Note 3 – Securities). The examination for impairment was made in accordance with that set out in detail in the section on Accounting Policy on Critical Matters in the Directors’ Report and in accordance with the circular of the Supervisor of Banks from 1.3.09. See the section dealing with Impairment of Assets in the Accounting Policy on Critical Matters. Credit to the public, net, amounted to NIS 1,773.3 million at the end of 2011, compared with NIS 1,751.4 million at the end of 2010, an increase of 1.3%. The average balance of credit to the public in 2011 was NIS 1,874.2 million, compared with an average balance of NIS 1,933.7 million in 2010, a decrease of 3.0%. Deposits of the public amounted to NIS 5,715.1 million at the end of 2011 compared with NIS 6,008.1 million on December 31, 2010, a decrease of 4.9%. The average balance of deposits of the public in 2011 was NIS 5,958.1 million, compared with an average balance of NIS 6,599.8 million in 2010, a decrease of 9.7%. Deposits from banks amounted to NIS 34.9 million at the end of 2011, compared with NIS 65.6 million at the end of 2010, a decrease of 46.8%. The changes in this item derive mainly from daily interbank activity. The capital of the Bank at December 31, 2011 amounted to NIS 431.9 million, compared with NIS 421.1 million at the end of 2010. The increase compared with the end of 2010 derives mainly from the net profit for 2011 in the amount of NIS 40.9 million, which was partially offset by the implementation of the new directive on Measurement and Disclosure of Impaired Debts, which led to a decrease in capital in the amount of NIS 20.5 million, and by a decrease in the capital reserve in respect of securities available for sale in the amount of NIS 9.6 million. The ratio of capital to total balance sheet at the end of 2011 amounted to 5.7%, compared with 5.5% at the end of 2010. The total capital ratio at December 31, 2011, calculated in accordance with the provisional directive - “Working Framework for Capital Measurement and Adequacy” (Basel II), reached 19.6% compared with 18.4% at the end of 2010. The ratio of Tier 1 capital to risk assets reached 16.2% compared with 15.2% at the end of 2010. On December 22, 2010, the Board of Directors of the Bank decided on capital targets up until the completion of the SREP process by the Bank of Israel. According to this decision, the minimal overall capital ratio determined will be 15%, and the minimal Tier 1 capital ratio will be 10%.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

11

Holdings Structure Chart *

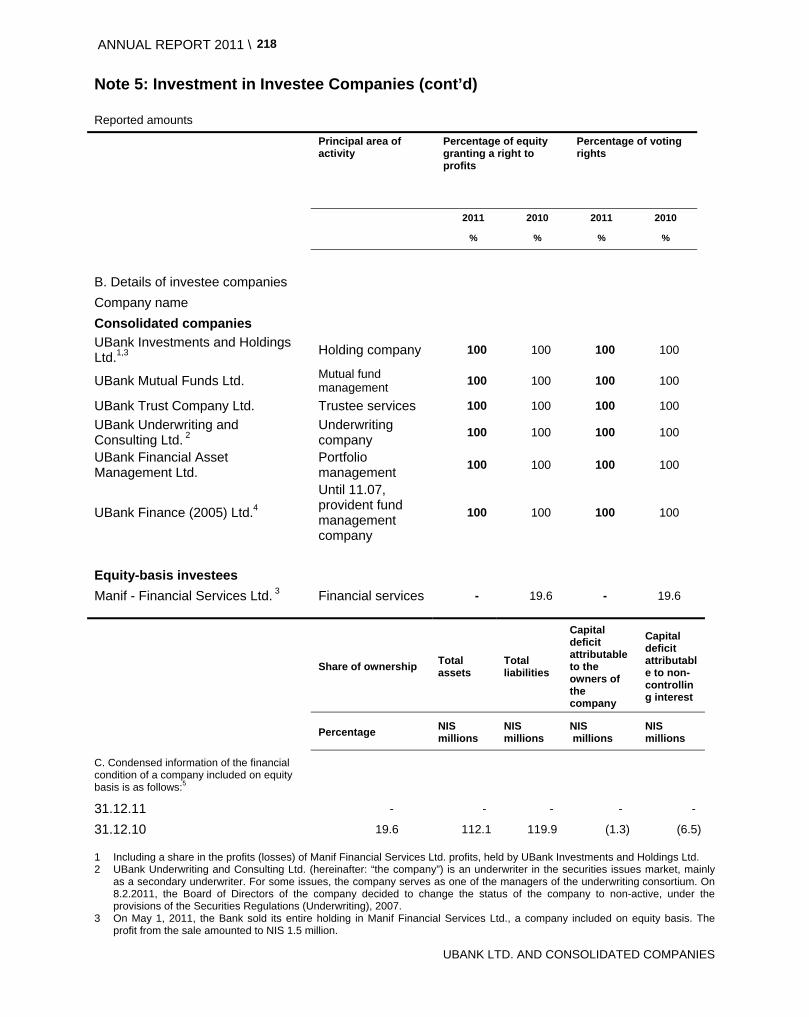

* Principal companies ** On May 1, 2011, the Bank sold all of its holdings in Manif Financial Services Ltd, a company

included on equity basis.

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

12

Principal Investee Companies A. "UBank Financial Assets Management Ltd." (hereinafter: “the Company”) is engaged in providing

investment portfolio management services for private and institutional customers. Total assets under management of the company as at December 31, 2011, is about NIS 0.5 billion. The company ended 2011 with a profit of NIS 0.3 million, compared with a profit of NIS 1.0 million in 2010.

B. "UBank Mutual Funds Ltd." (hereinafter: “the Company”) is engaged in the management of a range of mutual funds. The company ended 2011 with a net profit of NIS 0.2 million, compared with a profit NIS 0.7 million in 2010. Total assets under management of the company as at December 31, 2011, is about NIS 0.5 billion.

C. "UBank Trust Company Ltd." (hereinafter: “the Company”) is engaged mainly in providing trust

services for mutual funds, and in addition, as a trustee for series of bonds of special purpose companies (SPC), as well as private trusteeships in a variety of areas. At December 31, 2011, the company served as trustee for mutual funds with assets totaling about NIS 46.1 billion. The net profit of the company for 2011 amounted to NIS 18.6 million, compared with NIS 18.9 million in 2010.

D. "UBank Underwriting & Consulting Ltd." (hereinafter: “the Company”) dealt with underwriting

issues and financial counseling. The company’s profit amounted to NIS 0.1 million in 2011, compared with a loss of NIS 0.1 million in 2010. On 8.2.2011, the board of directors of the company decided to change the status of the company to inactive, under the provisions of the Securities Regulations (Underwriting), 2007.

E. "UBank Investments and Holdings Ltd." (hereinafter: “the company”) is engaged mainly in renting out premises, equipment and furniture for the Bank and related companies. The loss of the company for 2011 amounted to NIS 0.3 million (of which an operating loss in the amount of NIS 1.8 million and a profit of NIS 1.5 million from extraordinary activities of a company included on equity basis - Manif Financial Services Ltd), compared with a profit of NIS 0.3 million in 2010.

Information about the Parent Company The FIBI Group is one of the five largest banking groups in Israel. The Group operates in a wide range of financial activities: commercial banking, private banking, mortgages, activity in the various layers of the capital market, international financial activity, leasing financing, factoring, credit cards and various financial services. In addition to UBank, the FIBI Group owns three commercial banks in Israel - Otsar Hahayal Bank, Poaley Agudat Israel Bank and Massad Bank Ltd. - and 2 subsidiaries abroad, FIBI Bank (UK) plc in London and FIBI Bank (Switzerland) in Zurich. The Group has 176 branches and units in Israel, of which 80 branches and units of the parent company. Description of the Bank’s Operating Segments The following is a short description of the operating segments of the Bank: Private Banking Segment - includes all the Bank’s private customers and their businesses. These are both private customers belonging to the Personal Banking Division and also private customers in the Capital Market Division, whose principal activities are in securities. In addition, the segment includes the activity of the financial asset management company of the Bank, the mutual fund management company of the Bank, and the customers of the Bank’s trust company, in the area of private and public trust services.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

13

Corporate Banking Segment - includes all the institutional customers whose principal activity is in the financial area, such as groups engaged in the areas of insurance, pensions and provident funds, mutual funds, portfolio management companies, etc. These customers are allocated to the Capital Market Division. In addition, the segment includes customers of the trust company of the Bank in the area of trust services for mutual funds. Financial Segment - this segment incorporates the activities of the dealing rooms, the liquidity unit, and the Assets and Liabilities Management Department of the Bank. For detailed information, including financial analysis, see the chapter dealing with the description of the business of the Bank by operating segment. Dividend Distribution In 2011, no dividend was distributed. In December 2010, a dividend in the amount of NIS 100 million was declared and distributed. In March 2010, a dividend in the amount of NIS 75 million was declared and distributed. In 2009, no dividend was distributed. For further information, see Note 13A to the financial statements. The Bank's Rating by a Rating Agency The Midroog agency rated the Bank’s deposits as Aa3, and the short-term deposits with a rating of P-1. Human Capital Description of the organizational structure and the number of staff employed Six managers are directly subordinate to the Bank's General Manager, as follows: The Manager of the Personal Banking Division, to whom the Bank’s branches are subordinate. The average number of employees in the Personal Banking Division in 2011 amounted to 98 (in 2010 – 96 employees). The Manager of the Capital Market Division, to whom are subordinate the Israeli Securities and Foreign Securities Trading Departments, the Israeli Securities and Foreign Securities Back Office, and the banking team that provides services to the customers of the Division. The manager of the Capital Markets Division is also responsible for the following subsidiary companies: UBank Financial Assets Management Ltd., UBank Mutual Funds Ltd., and UBank Trust Company Ltd. The average number of employees in the Capital Market Division in 2011 amounted to 67 (in 2010 – 68 employees). The Manager of the Financial Division to whom the following departments are subordinate: Assets and Liabilities Management, the Liquidity Unit and the Dealing Room. The average number of employees in the Financial Division in 2011 amounted to 15 (in 2010 - 15 employees).

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

14

The Manager of the Headquarters Division, to whom the following departments are subordinate: Human Resources and Administration, Risk Management, Regulation and Processes, the Legal Department, Planning and Marketing, and the Computerization Liaison Officer. The average number of employees in the Headquarters Division amounted in 2011 to 41 (in 2010 - 40 employees). On January 12, 2011, the appointment of the Manager of the Headquarters Division as Chief Risk Officer of the Bank was approved. As a result, on January 13, 2011, the Credit Department, headed by the manager responsible for credit in the Bank, was transferred and reports directly to the general manager of the Bank. The Risk Management function remains subordinate to the Chief Risk Officer in the Headquarters Division. The average number of employees in the Credit Department amounted in 2011 to 13 (in 2010 - 12 employees). The Manageress of the Chief Accountant’s Division, to whom the following departments are subordinate: Accounting, International and Reconciliations and Bookkeeping and Payments. The average number of employees in the Chief Accountant’s Division in 2011 amounted to 20 (in 2010 - 20 employees). In addition, internal audit services rely for the most part on the Group Internal Audit function. For further information, see the chapter dealing with disclosure with regard to the Internal Auditor of the Bank. Below are data on the number of employees in the Bank and its subsidiaries at the end of the year and the monthly average during the year:

The Bank Subsidiaries Total

Permanent

Staff Other Staff*

Total Permanent Staff

Other Staff*

Total Permanent Staff

Other Staff*

Total

As at year end:

31.12.11 224 9 233 30 - 30 254 9 263 31.12.10 227 8 235 29 - 29 256 8 264

Monthly average:

2011 224 11 235 30 - 30 254 11 265

2010 224 4 228 27 - 27 251 4 255

* Includes hourly staff, staff from manpower agencies and outsourcing. Changes in Manpower 18% of the employees of the Bank commenced working for the Bank during 2011. Manpower turnover allows the Bank an influx of new professional personnel that suits its type of operations and the manpower requirements of the Bank. Employment Contracts All UBank employees are employed under personal employment contracts. These agreements afford the Bank maximum flexibility of employment, while providing a swift response to the needs and conditions of the market and the Banks’ business activity. For information on employees’ rights on retirement - see details in Note 12.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

15

Training Raising the level of professionalism in the Bank is a result of quality and focused recruitment, as well as of a personal and organizational training program that matches the needs of the Bank, and defined in the annual work program. The training program in the Bank includes professional teaching and training in different fields of routine banking activity and the subjects of management and the development of managers. The training program is derived from various changing factors, among which are the business policy of the Bank, developments expected in the market in general, and in the banking sector in particular, regulatory changes, and others. For training purposes, the Bank uses the training function developed by the First International Bank, with courses, seminars, supplementary learning, and training. The training program provides, as a motivating factor for employees, a solution for the development of personal skills and allows for the personal development of employees in different subjects. At the same time, the Bank encourages personal and professional development by means of, among others, participating in the funding of academic studies suitable for the Bank’s needs, and by assisting with vacation days during examinations. Remuneration programs for employees In accordance with the directives of the Supervisor of Banks from April 2009, the Board of Directors of the Bank discusses remuneration policy and the methodology for its implementation, with the aim of finding a balance between the desire to encourage motivation, creating identification among the managers with the long-term interests of the Bank, retaining and rewarding managers and their desire for achievement, together with the need to prevent exaggerated risk-taking. The policy relates to all Bank employees and is a part of Group policy that was put together with the participation of the parent company, in accordance with the directive of the Supervisor of Banks. In addition, the Bank strives to retain key employees and holders of key positions within the organization. Code of Ethics The Bank has a Code of Ethics that promotes ethics and social responsibility and incorporates appropriate norms of behavior among the Bank’s employees and its managers. The writing of the Code of Ethics was carried out with the participation of the Banks’ employees. Ethics functions have been created and activities are carried out for assimilation of the Code of Ethics by every employee on an ongoing basis. Restrictions and Supervision of the Bank’s Activities Proper Conduct of Banking Business Directive 313 - “Restrictions on the Indebtedness of a Borrower and a Group of Borrowers”, includes restrictions according to which the Bank is allowed to extend credit to a “single borrower”, to a “group of borrowers” and to the “six largest borrowers”. On 8.5.11, the Bank of Israel published an amendment to this Proper Conduct of Banking Business Directive, in which the restrictions set out in the directive were changed as of 31.12.11. The changes comprise a number of elements: 1. Limits on a single borrower and group of borrowers - the limit of 30% of the Bank’s equity was

changed to 25% of the Bank’s equity, or NIS 250 million, whichever the higher. The limit on the indebtedness of the six largest borrowers (135% of the Bank’s equity) was replaced with the limit that the indebtedness of all customers with indebtedness of over 10% of the

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

16

Bank’s equity, shall not exceed 135%. This percentage will decrease gradually by 31.12.12 to 120% of the Bank’s equity.

2. The inclusion of indebtedness of banks as customer indebtedness for single borrower purposes. 3. Changes occurred in the definition of indebtedness, for example futures transactions that were

included in the past at the nominal value multiplied by 10%, are multiplied by the add on rate in accordance with the Capital Adequacy Directives of Basel II multiplied by 3.

4. Eligible deductions – based partially on Basel II principles, both in recognition as eligible collateral and in changes in coefficients.

The abovementioned changes result in changes in the examination for compliance with limits such as exposures to sectors of the economy and others. The changes obliged the Bank to make changes in its deployment, including among others a significant reduction in credit facilities of large customers and a reduction in exposures to banks.

In Proper Conduct of Banking Business Directive 337 - “Activity in the Maof Market” there is a restriction, in accordance with which the total amount of the liabilities of a banking corporation vis-à-vis the Maof Clearing System (after eligible deductions) shall not exceed 30% of the Bank’s equity. In light of the large volume of activity of customers of the Capital Market Division in the Maof market, the Bank checks the said restriction on a routine basis. In Proper Conduct of Banking Business Directive 315 - “Supplementary Provision for Doubtful Debts”, it is stipulated that a provision is to be made in respect of concentration of credit by sector. The Bank is exposed to such concentration in the financial services sector. This concentration is in accordance with the business policy of the Bank, in which the capital market customers segment is one of the principal operating segments. The Bank is meticulous in implementing the restriction. In 2010 and 2011, there were no exceptions to the concentration limit in the sectors. In addition, on the subject of the capital market reform, see details in the chapter dealing with operating segments with reference to the activity of UBank Mutual Funds Ltd. Other than the aforementioned, there are no other restrictions and supervision that are unique or apply to the Bank in the relevant years or which are expected to have a significant effect on the activities of the Bank in the future. Material Agreements a. Computer services agreement As part of FIBI Group strategy, computer services, including operational and programming services, are provided by means of a subsidiary company - Mataf. The services are provided directly by the staff of Mataf. As part of this strategy, the employees of the computer unit of the Bank became employees of Mataf in 2005. As a result, all of the Bank’s computer services, including operations and programming services, are provided to the Bank by the Mataf Company. Mataf is engaged in developing advanced technology systems and maintaining the business applications of the Group and of the Bank, while striving to approve the effectiveness, quality, and efficiency of the Group’s computer services. Within the company operates the Methods and Process Analysis Department, which is responsible for drawing up and distributing working procedures and circulars. In accordance with the principles of the undertaking between the Bank and Mataf, until the end of 2009, Mataf bore the costs of the process of unifying applications between the banks, and the Bank paid Mataf

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

17

for ongoing computer services, and bore its share in the development of regulatory and Group applications as agreed, with the addition of an agreed increase. Commencing in 2010, a model was formulated to determine current payments for computer services based on the relative share of the Bank in all computer activities carried out in the FIBI Group.

b. See additional relevant information in the following Notes to the Financial Statements: – With regard to agreements relating to the change of control in the Bank - see Note 17(E). – With regard to the Bank’s liabilities to the Maof Clearing System - see Notes 16(C)(2) and

16(C)(3). – With regard to the Bank’s liabilities to the Stock Exchange Clearing System - see Note 16(C)(4). – With regard to the collateral agreement with Euroclear - see Note 16(C)(5). – With regard to indemnification of office holders - see Note 16(C)(8). – With regard to commitments between the Bank and the FIBI Group - see Note 16(C)(10). – With regard to pledges - see Note 16(D). – With regard to rental of buildings - see Note 16(C)(12).

Legal Proceedings

Set out below are details of claims against the Bank and its consolidated companies, in material amounts exceeding 1% of the Bank’s equity. In the view of Management, based on legal opinions, appropriate provisions have been made in the financial statements, if necessary, to cover any damage resulting from the said actions. In the Bank’s view, based on the opinion of its legal advisers (and in the view of Bank Management, based on the opinion of their legal advisers), the probability of additional risk exposure occurring to the Bank is very low, in all of the five actions specified below:

1. On July 25, 2002 an action was brought in the Tel Aviv District Court against a company which shares were traded on the Tel Aviv Stock Exchange (hereinafter: ”the company”), the Trust Company, Poalim Capital Markets and Investments Ltd., directors of the company, its controlling shareholders, the parent company of the company, and the accountants who audited the company’s accounts. The amount of damage claimed by the plaintiff is about NIS 32,000. Together with the action, a petition was filed in Court to recognize it as a class action on behalf of all the holders of the debentures issued by the company, in an estimated amount of some NIS 40.8 million. In March 2011, the Court dismissed the claim against the Trust Company and against the auditors of the company (the petition against the remaining defendants was approved). The plaintiff submitted an appeal against the dismissal decisions. In the opinion of the Trust Company and its legal advisors, the Trust Company has valid claims, both against the suit being admissible to be judged as a class action, and also on the matter of the lawsuit against the Trust Company.

2. On July 27, 2003 two customers brought a claim in the Tel Aviv District Court for the award of a declaratory judgment to the effect that neither of the customers owes money to the Bank and that the pledge of shares of a company listed on the Stock Exchange that serves as collateral for both customers’ debts, which the Bank is seeking to realize, is invalid. The value of the dispute according to the statement of claim amounts to about NIS 28.6 million. The claim is in the pre-trial stage.

3. On December 22, 2005 a claim was brought in the Tel Aviv District Court against UBank Trust Co. Ltd. (hereinafter: “the company”) which was corrected on September 15, 2009 to an amount of some NIS 34.6 million (as estimated at 31.12.11) by three plaintiffs, which are companies related to each other. The plaintiffs held debentures for which the company served as trustee. Because of financial difficulties, the issuer of the debentures did not discharge its debts to the debenture holders. The company has submitted an amended defense plea. In the opinion of the company and its legal advisors, the company has a good defense against the lawsuit.

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

18

4. In October 2006, judgment was given by the Jerusalem District Court, according to which the counterclaim, submitted by a customer of the Bank, for a declaratory judgment that his losses in the amount of about NIS 11.1 million resulted from the Bank’s errors and negligence, was dismissed. The customer filed an appeal against the verdict in the Supreme Court. On 19.7.2011, the Supreme Court dismissed the appeal. 5. On March 18, 2009, a claim was filed in the Tel Aviv District Court in Tel- Aviv against the Bank by a customer in the sum of NIS 8.5 million. It was claimed that the Bank was negligent in honoring checks amounting to NIS 5.0 million. The checks were forged by an employee of the customer, the Bank has submitted a defense plea and a third party declaration against the employee. Economic Developments in 2011 The Global Environment During the second half of 2011, the debt crisis in Europe worsened significantly, and led to a slowdown in real activity and a sharp increase of risk in global financial markets. The slowdown in Europe spread to other developed countries and to emerging countries (mainly India, China and Brazil) - which responded by undertaking an expansionary monetary policy (mainly reductions in interest rates). In the US, data for business activity improved, although the rate of growth there remained relatively low with a high burden of debt. Europe: In the second half of the year, GDP in the euro zone declined by about 0.3%, compared with a moderate positive growth of about 2% in the first half of the year. Growth forecasts were revised downwards under the concern of deepening recession. Towards the end of the second half of the year, the markets calmed down somewhat in light of the steps taken to enhance fiscal discipline in the euro zone and monetary measures to increase liquidity. At the beginning of 2012, ratings were lowered again for several European countries: France, Italy, Spain, Portugal, Greece, Austria, Malta, Slovakia and Slovenia - this downgrading may hinder the ability of these countries to raise debt, which may lead to further deterioration of the crisis. US: In the second half of the year there was a recovery in real activity in the US, which was reflected in an increase in the rate of growth compared to the first half, and a decline in the rate of unemployment. Nevertheless, despite these positive signs, it should be noted that growth relied heavily on public sector demand, and was supported also by the monetary measures of the Fed which mainly provided relief to the credit market. Emerging markets: Unlike most developed countries, emerging markets reported attractive growth figures until the fourth quarter of the year, with China leading the economies with growth rates of about 10%. However, in the fourth quarter, the global slowdown spread to the emerging markets and growth projections for them were revised downward.

Economic developments in Israel Economic growth Despite moderation in the rate of growth in 2011, especially in the second half, the condition of the Israeli economy in 2011 was relatively good – the level of real activity was high and most indicators pointed to a situation approaching full employment. The Israeli economy grew in 2011 at a rate of approximately 4.8%. All the components of the economy enjoyed relative expansion: exports increased by 4.5%, private consumption increased by 4.0%, investments in fixed assets grew by 14.8%, and public consumption by about 4.5%. It is important to note, as already mentioned, that the rate of growth continued to decline during the year from about 4.9% in the first quarter to an estimated level of 3% in the fourth quarter.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

19

Bank of Israel forecasts of growth for 2012 were cut during the year to a forecast of 2.8% (similar to the OECD forecast).

The unemployment level The level of unemployment rate dropped to a historic low and most of the indicators that support the assessment that the labor market is close to full employment. The growth of the economy in 2011 led to a rapid increase in the demand for workers. In the first nine months of 2011, employment grew by 3.3% (an increase of nearly a hundred thousand new employees). The unemployment rate fell from 6.5% at the end of 2011 to 5.5% in the second quarter, and to an estimate of some 5.4% in November. Although the Israeli economy is approaching a state of full employment, real wages in the economy rose from January-October by only about 0.3%.

State Budget The budget deficit reached some 3.3%, slightly higher than the target of 3% set in the budget for 2011. In the second half there was a decrease in revenues from taxes as a result of the slowdown in activity. In 2011, the Ministry of Finance conducted an expansionary fiscal policy. Although total revenues from taxes increased by 8.1% (not far from the target of 9.2%), but most of the growth occurred by the middle of the year. Beginning in July the increase in taxes came almost to a halt, mainly due to reduced taxes on consumption from a reduction in imports of consumer goods in general, and cars in particular. Tax rebates for the whole of 2011 were lower by NIS 2.5 billion compared with 2010 (about 0.3% of GDP). Funding the deficit of NIS 23 billion was made by privatization revenues of NIS 7.1 billion (mainly from the sale of land) and the net raising of funds in the domestic market of NIS 12 billion. In addition, the Treasury took advantage of surplus funding from previous years totaling NIS 3.8 billion. Government debt continued to decline from 76.6% of GDP in 2010 to an estimated 75% in 2011. The risk of an increase in the deficit in 2012 stems mainly from the possibility of a worsening of the slowdown in the real activity in the local economy leading to more moderate growth in tax revenues than forecast and/or the possibilities of increased defense spending against the backdrop of deterioration of the geo-political situation and the increasing expenses associated with the social protest. Inflation, monetary policy and the exchange rate The inflation rate in the Israel economy was affected by the slowdown that developed during 2011. By the second quarter, there was an acceleration in the rate of inflation from about 2.7% in December 2010 to about 4.2% in June 2011. After that, there was a consistent moderation every month to a level of 2.2% in December 2011. The core inflation rate dropped in the last months from about 3.6% in the first quarter to about 1.9% in December. The rate of increase in housing prices slowed in the second half of the year: the Housing Survey (which measures actual purchase prices according to purchase tax) indicated a cumulative decline of 1.5% in the three latest surveys of 2011. The change in the trend of housing prices stems from the raising of interest rates by the Bank of Israel, a sharp increase in construction starts, Bank of Israel restrictions on the percentage of mortgages at variable interest rates to one third of the total mortgage, and excess taxation on purchasing a second apartment. In view of the slowdown in economic growth in the second half, due to Europe slipping into recession and concerns of a more severe financial crisis and deepening of the global slowdown, the Bank of Israel, in the third quarter of the year, discontinued the trend of interest rate hikes that begin in mid-2009. From December 2010 to June 2011, the Bank of Israel raised the interest rate by 1.25%, to the level of 3.25%. The more the global environment continued to deteriorate, the more monetary policy changed to a reduction in interest rates, which led to two reductions in the last quarter of the year and a further reduction in late January 2012. The Bank of Israel interest rate at the end of January 2012 is 2.5%.

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

20

After appreciation of some 5% in the effective exchange rate in the first half of the year, the trend reversed in the second half and a depreciation was recorded of about 4.7% against the dollar and about 4.2% against the euro. This moderate depreciation of the shekel supported the improvement in the competitiveness of the trading sector, (after erosion in 2010) without the development of inflationary pressure. The exchange rate was influenced by three main factors that gave less support to the appreciation of the shekel compared with previous years: The current account surplus disappeared in 2011; a deterioration in geo-political conditions in the area; and, in contrast, net real investments in 2011 were positive and supported the shekel. Foreign currency purchases by the Bank of Israel were halted in August 2011 after acquiring about $ 5.5 billion by July 2011. This policy was terminated as soon as conditions were created for the depreciation of the shekel. Financial markets Israel's financial markets were affected by the development of the crisis in Europe, as well as local factors, of which the main ones are a high level of political uncertainty in the Middle East. The decline in stock indices in Israel was more moderate than in Europe, but more intense than in most other countries. The stock market After a sharp rise in world capital markets in 2009-2010, 2011 was a year of declines in stock markets in Israel and overseas (except in the US, where the S&P index remains stable). The Israeli capital market (the TA-100 index) decreased by 20% in 2011. The MSCI index of emerging markets decreased by 20.4% compared with a decrease of only 7.6% in the MSCI index of developed countries. Local events in Israel did not support the stock market. Fear of the effects of the vote in the UN in September caused investors to reduce risks. The social protest also hit the stock markets because of the damage expected to the profitability of food companies, the media and marketing chains. The last quarter of the year was characterized by increases in share prices in Israel. The sentiment that the leaders of Europe are moving towards a process of fiscal integration and increasing involvement of the European Central Bank in providing liquidity eased the credit crunch. In addition, better than expected economic data in the US contributed to the positive atmosphere of the markets. The corporate bond market Like the stock market, the corporate bond market is sensitive to a slowdown in economic activity. The same trends that impacted the stock market in 2011 affected corporate bonds. The bond market fell by 1.8% in 2011, in particular the lower rated bonds. The Tel-Bond 20 index rose by 0.7% in 2011 compared with a 1.6% decline the Tel-Bond 40 index, with a widening of margins observed between corporate bonds and government bonds (index-linked) which rose by some 4.3% during the same period. A sharp rise in yields on bonds of a number of companies may make it harder for debt recycling in 2012. The Government bond market In 2011, the bond market responded to two major developments: the trend of the monetary policy of the Bank of Israel and the trend in stock markets (and its impact on foreign bond yields). In the first half of the year, the Bank of Israel surprised the market with rapid interest rate hikes from 2% in late 2010 to a level of 3.25% (by June). Concerns about a continued rapid rise impacted the bond market in the first months of the year. In the third quarter, changing the direction to that of reducing interest rates had a favorable effect on the bond market, and the bond market reacted with price rises in the second half of the year. The Israeli bond market was supported by long-term yields in the US, which declined mainly due to the flight from the stock market.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

21

Updates in Legislation and Rulings affecting the Banking System in 2011 Legislation

Joint Investment Trust Law (Amendment No. 14), 2010

This amendment became effective upon the rules coming into force on the conducting of the required tender, which were published on 28.6.11 and came into force on 28.12.11, which is the effective date of coming into force of this amendment. On 16.2.2010, an amendment was published to the law in the Official Gazette (Reshumot), which was mainly a change to section 69 of the Joint Investment Trust Law. The following are the main points: an obligation to conduct a tender was imposed on the fund manager concerning brokerage commissions with "a trading company" (member of the stock exchange); the board of directors of a fund manager is to establish a procedure for conducting a tender, which is to be approved by the trustee; entering into an engagement with a member of a foreign stock exchange can be done without a tender (under the terms of the law); the engagement of a fund manager in a brokerage agreement with a stock exchange member that controls the fund manager or fund trustee can be done without a tender subject to the following conditions: 1. Compliance by the stock exchange member with the threshold conditions set out in the tender. 2. The commission for each transaction type does not exceed the commission paid to the winner of

a tender for making a similar transaction. 3. The engagement was approved by the audit committee and board of directors of the fund

manager. A fund manager will not make payments out of the fund's assets to stock exchange members related to the fund manager or the trustee during the period of 12 months beginning on the date set out by the fund manager in the prospectus, for executing transactions in the fund for more than 20% of total commissions (of any kind) paid out of the fund's assets during that fiscal year. The Bank and UBank Trust Company Ltd. (a subsidiary company) completed preparations for the implementation of the legislation mentioned above. As a result of implementing the directive, the Bank anticipates a decrease in its income that will not significantly affect the Bank's ongoing operations. Regulations for conducting a tender for engagement with a trading company and conditions for engagement with a related company or an affiliated company with an affinity (hereinafter: “the rules") The rules were published on 28.06.11 and came into force on 28.12.11. Following Amendment No. 14 of the Joint Investment Trust Law, rules were published for public comment according to which it is proposed to oblige the fund manager to carry out a tender for engagement in an agreement to receive brokerage services. It is proposed to exempt companies related to the fund manager from participation in the tender, but to limit the scope of brokerage transactions which can be paid for out of the fund's assets to related companies, so that the fund manager will be required to outsource most of the brokerage activity for which the consideration is paid out of the fund's assets to assets that are not related to him. These proceeds will be limited to 20%. A trading company related to a trustee shall be entitled to participate in the tender and in the event of its winning, it can receive proceeds up to 20% of the commissions that the fund pays per year, or alternatively to end the term of office of the trustee and serve as a trading company without restriction.

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

22

Improvement of Efficiency of Enforcement Procedures in the Securities Authority (Amendments to Legislation) Law, 2011 On 27.1.11, the law was published in the Official Gazette (Reshumot), and came into force on 27.2.11, apart from certain matters within the framework of the law, which will come into force later, as set out in detail in the law. The aim of the law is to enforce more efficiently the provisions of the Securities Law, 1968, the Regulation of Investment Counseling, Investment Marketing and Investment Portfolio Management Law, 1995, and the Joint Trust Investments Law, 1994; to shorten the period of time between the violation and the imposition of punishment; and to adapt the punishment to the severity of the violation. In this context, a new scale of violations was determined, and punishment was made more severe for certain violations. It should be pointed out that the law stipulates a duty of supervision on the chief executive officer of the corporation, under which the chief executive officer of the corporation has to supervise compliance and to take all steps that are reasonable under the circumstances of the matter, as detailed in the relevant paragraph, to avoid violations by the corporation or by any of its employees. The law stipulates that if a violation was committed (except for certain violations), it is presumed that the chief executive officer violated his said duty of supervision, and he will be subject to enforcement measures as if he were the violator, unless the chief executive officer acted to prevent the violation and /or its recurrence, including by deciding on appropriate procedures. The law allows for three parallel tracks of enforcement, at the discretion of the Chairman of the Israel Securities Authority: (1) the imposition of a monetary sanction by the Authority; (2) an administrative enforcement process by means of an administrative enforcement committee; (3) criminal proceedings;

The law also authorizes the Chairman of the Securities Authority to enter into an arrangement with the violator not to start proceedings or to discontinue proceedings, instead of carrying out criminal or administrative proceedings. Entering into an arrangement as mentioned above will be published in a similar manner to the aforementioned in reference to a demand for payment.

On 7.4.11, as part of the implementation of this law, five of the six members of the administrative enforcement committee were appointed. The amendment came into force on 27.2.11, but due to the fact that its coming into force is contingent on the making of regulations (including with regard to discounts in the rates of fines prescribed by law, etc.), it will come into force gradually. The Bank is carrying out a project for preparing an internal compliance plan for the Bank and for the subsidiary companies, with the assistance of external consultants. List of circumstances for examining a defect in the reliability of entities supervised by the Authority – Binding version The list was published on 4.12.11, as the result of the publication of the Improvement of Efficiency of Enforcement Procedures in the Securities Authority (Amendments to Legislation) Law, 2010 (hereinafter: "Administrative Enforcement Law"). Thelist came into effect 30 days after publication. Any change in the list will not apply to a pending proceeding. The main purpose of the law is to establish the administrative enforcement procedure, and at the same time, further amendments were made aimed at improving protection for the public investing in securities, unit holders of mutual funds, and clients of permit holders. Under the Administrative Enforcement Law, the competence of the Securities Authority was clarified with regard to the non-granting of a permit because of the discovery of a defect in reliability, as well as its withdrawing a permit already issued, due to the disclosure of such a defect as mentioned above. The Authority was authorized to cancel permits due to a defect in reliability, including a defect in reliability of related entities, as detailed below, but it is stipulated that such withdrawals would be done on the basis of a list of circumstances which attest to a defect in reliability, in light of which alone the Authority will review such a decision. To this end, the Authority was required to determine and publish a list of circumstances the existence of which is prima facie evidence of a possible defect in reliability.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

23

Publication of this list will help in creating clarity of how the Authority will use its discretion in these cases. Examination of reliability is with regard to a fund manager, a fund trustee, license holders and those having permits to control a fund manager. In the event of existence of one or more of the circumstances, the role of the individual whose reliability is assessed is to be taken into account for purposes of selecting the entity and various considerations such as the length of time between actions and the date of the examination, the manner of conduct of the supervised entity during the period elapsed, and the degree of impact expected from the action and the reaction of the Authority on the capital market capital, public confidence in it in general, and those entities managing public funds in particular. The existence of such circumstances will not necessarily determine that there was a defect in reliability, and will certainly not automatically lead to a decision that there was a defect that justifies the withdrawing of the permit. Below is the list of circumstances that may constitute a defect in reliability, subject to examination by the Authority: 1. Conviction for an offense, an indictment or criminal investigation in connection with the

commission of an offense; 2. Determination that a disciplinary offense was made, the filing of disciplinary claims, or the

commencement of proceedings for investigation the committing of an offense, as mentioned above;

3. Imposition of administrative enforcement measures, including imposition of monetary sanctions, issuing a demand for payment of monetary sanctions or an administrative claim, or commencing an administrative enquiry in connection with the committing of a violation;

4. Engagement in administrative arrangements of an alternative nature to an indictment or the conducting of administrative proceedings, such as payment of a fine, an agreed order, or engagement in an agreement for a conditional discontinuation of proceedings, due to the performance of an offense or violation;

5. Withdrawal of a permit due to a defect in reliability – cancelation of a license, refusal to grant or denial of a permit to practice any profession or in any other area because of a defect in reliability, whether the permit was granted by law or by a trade union;

6. Findings in civil legal proceedings of an infringement that was prescribed in a procedure in which the supervised entity was given the opportunity to present its position - whether as a party to the proceeding or in any other way (such as giving testimony or an affidavit in court);

7. Audit findings and customer complaints – findings of an audit by the Authority, another supervised entity, an independent auditor, internal auditor, the findings of an internal compliance system or mounting complaints by customers - pertaining to significant issues and provided that they are based on facts;

8. Dismissal following the discovery of findings indicating allegedly improper behavior, when they have a connection with activities supervised by the Authority and provided that they are based on facts;

9. Liquidation due to insolvency, declaration of bankruptcy or failure to meet material financial obligations related to the supervised practice.

Criteria for recognition of an internal compliance program in the area of securities Following publication of the Improvement of Efficiency of Enforcement Procedures in the Securities Authority (Amendments to Legislation) Law, 2011, the Israel Securities Authority (hereinafter: "the Authority "), published on 15.8.11 the criteria it formulated for recognition of an internal compliance program in the area of securities – which is a voluntary mechanism adopted by the corporation to ensure compliance by the corporation and the individuals in it with securities laws. In addition, the Authority issued the reliefs an internal compliance program can give individuals and corporations, and the criteria

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

24

by which the effectiveness of an internal compliance program is examined for purposes of deciding on granting relief. Among the criteria determined by the Authority for recognition of an enforcement program as effective: responsibility of the board of directors and management for the formulation, adoption and implementation of the enforcement program; adapting the program to the corporation and its special circumstances after reviewing its business activities and mapping risks involved in them in the area of securities law; adoption of procedures and methods of treatment that will provide a response to the risks that have been mapped, applying the program at all levels of the corporation, appointing an officer in charge of enforcement, proper assimilation of the program at all levels, ongoing monitoring and reporting on the maintenance of the program, proper treatment of failures and violations and learning lessons from them (the burden of claim and proof for the existence and effectiveness of the enforcement program is on the person claiming it). Effective internal compliance means the practical application of internal compliance procedures and not just an enforcement program "on paper". Effective internal compliance that meets the criteria issued by the Authority can serve as a basis for proving that the CEO (who has supervisory responsibility for enforcement) has fulfilled his obligations under the law. The Companies Law (Amendment No. 16), 2011 The Companies Act (Amendment No. 16), 2011, was promulgated on 15.3.11. The purpose of the amendment is to streamline corporate governance prevailing in Israel in accordance with the principles practiced worldwide. Among other things, special emphasis was placed on the principles of independence of the board of directors in general and the external director in particular, strengthening the standing of institutional entities and minority shareholders of public companies in appointing external directors, in order to weaken the power of the controlling shareholder of the company to influence management and to direct its activities in light of his personal goals. In addition, the majority required was amended for approval of transactions in which a controlling owner has a personal interest, the majority required was amended for the appointment an external director, the extension of the maximum term of office of an external director and the determination of provisions regarding the independence of the external director, emphasis was placed on the duty of a director to exercise independent discretion, setting of provisions regarding the possibilities of prohibiting the dual appointment the Chairman of the Board of Directors and CEO of a public company, provisions regarding the Audit Committee – its composition, its methods of decision-making and expanding its roles and responsibilities; granting powers to the Securities Authority to impose financial sanctions on an individual or corporation in the event of breach of certain provisions of the Companies Act, and laying down best practices for corporate governance. The effective date for most of the sections of the Law is 60 days after its publication, and for some of them (mainly relating to the audit committee) within six months of publication, and for others with the coming into force of the Improvement of Efficiency of Enforcement Procedures in the Securities Authority (Amendments to Legislation) Law, 2011. In addition, see also the Amendment to Proper Conduct of Banking Business Directive No. 301. Reform in the area of banking commissions A number of private members’ bills are tabled in the Knesset concerning restrictions on the level of commissions, baskets of commissions, prohibiting the charging of types of populations with certain commissions, prohibiting the charging of certain types of commissions and so on. In addition, there are private member’s bills tabled in the Knesset seeking to oblige banking corporations to pay interest on credit balances in the current accounts of their customers. The Bank is monitoring developments in the legislative process of those proposals, which are still in the preliminary stages of legislation.

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

25

Securities Law (Amendment No. 44) (Postponement of Repayment of an Obligation of a Public Company to a Controlling Shareholder), 2010 The law was published in the Official Gazette (Reshumot) on 12.1.11. The law stipulates that, if a public company that issued debt certificates became insolvent or announced that it is unable to repay the debt certificates, repayment of the obligations to the controlling owners of the company holding debt certificates is to be postponed until repayment in full of the obligations to other holders of debt certificates. Postponement of repayment will also be with regard to the holder of a debt certificate that is controlled by the controlling shareholder by means of a corporation. Antitrust Law (Amendment No. 12), 2010 The law was promulgated on 25.7.11. According to the amendment, a section is added on concentration group to the Antitrust Law and the Commissioner’s authority to declare that a limited group constitutes a concentration group was amended. In addition, the Commissioner was authorized to issue a concentration group directives intended to prevent harm to competition between members of the group or the sector in which they operate. With regard to concentration groups in the banking sector, a special arrangement was made that will impose an obligation on the Commissioner to inform the Governor of the Bank of Israel and the Supervisor of Banks of his intention to declare a concentration group or of his intention to issue directives to a concentration group, and if the Governor or the Supervisor was of the opinion that the giving of the directive would jeopardize the stability of the banking corporation or the stability of the banking system, the Commissioner would refrain from giving the directive. Orders regarding Financial Sanctions (Reduction of Amounts of Monetary Sanction) by virtue of various legislation empowering the Governor to impose financial sanctions The orders were published on 28.6.11. In the orders were set out instances, circumstances and considerations because of which it will be possible to reduce the moneytary sanction prescribed in various laws (Bank of Israel Law, Payment Systems Law, Banking Law (Licensing), Banking Law (Service to the Customer), the Banking Ordinance), according to maximal reduction rates as prescribed in the orders. For example, a reduction of up to 50% of the amount of the sanction if the violation is a first violation, a reduction of up to 15%, if the violator has ended the violation on his own initiative and reported it to the Supervisor or if the violator has taken steps to prevent recurrence of the violation and reduce the damage. Banking Law (Service to the Customer) (Amendment No. 15), 2011 The amendment came into force on 1.11.11. The amendment stipulates that on issuance of checks to an individual customer (not a corporation) the checks will be crossed and a restriction to their negotiability printed on them, unless the customer asked for checks to be issued to him without crossing and without the restriction, as stated. Property Taxation Law (Appreciation and Acquisition) Amendment No. 70, 2011 The amendment came into force on 31.3.11. The amendment imposes on a purchaser of land an obligation to make a payment to land betterment tax to pay in accordance with that stipulated in the law on account of the tax for which the seller is liable ("down payment"), after the purchaser has paid the seller 40% of the proceeds for the rights to the land. The down payment shall be deemed paid to the seller by the purchaser on account of the consideration determined between them, even if provided otherwise by law and/or the contract of sale. The amendment applies to the sale of rights to land that was carried out after 31.3.11. The obligation to deliver the down payment does not apply in two cases: when

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

26

the right to the land is a "qualifying apartment" for which exemption was requested, and when the consideration for the right to the land is not monetary. Banking Law (Licensing) (Amendment No. 18), 2011 The amendment was published in the Statute Book on 15.8.11. It is determined that the clearing of transactions executed by means of debit cards, will only be by a person who has obtained a license for this from the Governor of the Bank of Israel, and that the clearers will be under the supervision of the Supervisor of Banks. In addition, the Supervisor has been granted authority in consultation with the Antitrust Commissioner to oblige a clearer with a wide scope of operations (as defined in the Law), to clear transactions of debit cards issued by a certain issuer as well as allow additional clearers to clear transactions made by means of debit cards issued. Securities Regulations (Dates for Filing Notice of an Interested Party or a Senior Office Holder) (Amendment), 2011 The regulations came into force on 2.10.11. On 13.7.11, the amendment to the law was published in the Official Gazette (Reshumot) that replaces the original section 4, and instead added a new section 4 of which the essence is: a person holding securities of a corporation by means of members of an institutional reporting group under his management/control, shall once a month give the corporation written notice specifying the percentage of the holding in securities of the corporation, including that held by members of the reporting group under his management/control. In addition, if section 33(d) of the Regulations of Periodic and Immediate Reports takes place, regarding the cumulative change in the holdings of a bank or insurance reporting group in the corporation, the institutional group holding securities as aforesaid, is to submit written notice when the change in holdings amounted to 1% of the issued capital of the corporation or 5 % of the total nominal value of the series issued, no later than two business days from the date of the cumulative change, as stated. Corporate Governance Law for Fund Managers and Portfolio Managers (Legislative Amendments), 2011 The law amends the Regulation of Investment Advice, Investment Marketing and Investment Portfolio Management Law, and the Joint Investment Trust Law. Most of the changes deal with the obligations applicable to the board of directors; for example the composition of the board of directors, the appointment of the chairman of the board of directors shall be as customary in a public company, and the chairman cannot be a relative of the CEO, the powers of the chairman of the board of directors, the functions of the board of directors, arrangements for managing meetings of the board of directors, the powers of the Minister of Finance to determine the qualification of directors, the determination that the number of directors that may serve as directors of another financial entity shall not exceed one third, and the prohibition of a director serving in more than two financial institutions at the same time. In addition, the number of directors who are employees of the company shall not exceed one third. Other changes relate to the approval of an Internal control function and approval of an internal compliance program, the addition of adding procedures such as a risk management procedure, proper management of the board of directors, emergency deployment and and ensuring business continuity, and a procedure for engaging with a trading company, the appointment of an audit committee (its duties, composition, arrangements of meetings, etc.), and appointment of an internal auditor. In the Regulation of Investment Advice, Investment Marketing and Investment Portfolio Management Law, the abovementioned amendments were incorporated in a new section, which refers to a “large

DIRECTORS' REPORT 2011 /

UBANK LTD. AND CONSOLIDATED COMPANIES

27

portfolio management company", defined as a group with a license that has over 50 clients and total assets in excess of NIS 5 billion, or a group with a license that has over 1,000 customers on which the above amendments apply. The amendment to the Joint Investment Trust Law includes, in addition to the principles set out above, the prohibition of discrimination between those with different units in various funds managed by the fund manager, and seeks to ensure the independence of the fund trustee from the fund manager, clarifications of the duties of supervision imposed on the trustee and increased mechanisms for control, monitoring and audit of the fund manager and of large portfolio management companies. Regulation of Investment Advice, Investment Marketing and Investment Portfolio Management Law (Reports), 2011 The regulations were published on 29.11.11 and tabled in the Finance Committee. The regulations set out the dates for the quarterly report and the manner it is submitted to the customer, the manner it is presented to the customer, and the method of calculation of the yield in the report. In addition, the regulations stipulate the date and manner of submitting the annual report to the public, and the details to be included in the report. The regulations mandate the filing of an immediate report to the Authority if certain events occur as specified in the regulations, the submission of quarterly and annual report to the Authority, dates for reports and the manner of their submission, and include an appendix with the text of the reports mentioned in the regulations. Regulations of Sale (Apartments) (Assurance of Investments of Persons Acquiring Apartments) (Reduction of the Monetary Sanction to a Banking Corporation), 2011 The regulations were published in the Official Gazette (Reshumot) on 13.11.11. The regulations allow the Supervisor of Banks to a reduce financial sanction imposed on a bank when the circumstances specified in the regulations exist, by the percentage in the regulations specified for the same circumstance, and on the existence of a number of circumstances – by the cumulative amount of percentages specified for them in the regulations, provided that the cumulative reduction will not exceed 85%. Amendment to the Order for Prohibition of Money Laundering (Obligations for Identification, Reporting, and Recordkeeping of Banking Corporations for the Prevention of Money Laundering and the Financing of Terror) (Amendment), 2011 The amendment was approved by the Knesset Constitution, Law and Justice Committee on 6.11.11. Instructions were added for the opening of an account in a closed system, whose aim is to make it easy for customers to deposit funds or execute transactions in mutual funds in a banking corporation which does not handle their daily banking activities. The following provisions shall not apply to the abovementioned accounts: identification in person, instructions for verifying details and document requirements, and the requirement for a declaration of beneficiaries. Prohibition on investment in corporations maintaining business links with Iran On 8.04.08, the Prohibition on Investment in Corporations maintaining Business Links with Iran Law, 2008, was approved. The law prohibits investing, including through the holding of securities or by way of granting certain loans, in a corporation that maintains a material business relationship with Iran as defined in the law. It is also stipulated that a prohibited investment in a corporation, which was declared by law as a corporation as aforesaid, and not selling earlier holdings, are crimes. On 15.6.11, the

ANNUAL REPORT 2011 \

UBANK LTD. AND CONSOLIDATED COMPANIES

28