annual report 2012 - homepage – apc technology group...

TRANSCRIPT

Annual Report 2012

Advanced Power Components plc (APC) is one of the UK’s leading distributors of specialist

electronic components and a provider of technologies developed to reduce energy

consumption or generate electricity more sustainably.

Since incorporation in 1982, APC has developed long-standing relationships with manufacturers of specialistelectronic components and with customers who put significant value on our deep understanding of thechallenges of their individual markets, technical expertise and attention to detail. Markets include defence,aerospace, space, transportation, medical and industrial sectors. Products are wide ranging in theircomplexity and in their application and are sold through a number of semi-autonomous teams. Each teamfocuses on specific technologies or markets but are true to the Company’s central business strategy ofadding value in the supply chain.

Through Minimise Energy, the Group promotes a range of technologies developed to reduce energyconsumption and associated carbon emissions associated with traditional offerings. These products areeither sold individually, through subsidiaries Minimise Limited* and QV Controls Limited or may be combinedto provide an integrated, multi technology solution to the challenge of improving the energy efficiency of anentire organisation.

Sales teams:

• APC-Contech – Custom Keyboards and Data Input Devices

• APC-Displays+ – Displays and Embedded Systems

• APC-Hero – Sensors, Optoelectronics, Semiconductors

• APC-HiRel – Electronic Components for High Reliability Applications

• APC-Locator – Obsolescence and Allocation Specialists

• APC-Novacom – Microwave and RF Components

• APC-Time – Timing Systems, Time and Frequency Generators

Subsidiaries:

• Minimise Energy Limited* – integrated, multi technology energy efficiency solutions includingfinancing options

• Minimise Limited* – LED lighting, imop™, air-conditioning optimisation technologies

• QV Controls Limited – Energy efficient energy monitoring and control systems

ADVANCED POWER COMPONENTS PLC

* Minimise Energy Limited and Minimise Limited became subsidiaries after the year end.

In a challenging trading environment Advanced Power Components plc continued to focus on developingits core electronic components business and entering the growing market for energy saving products:

• Revenue reduced by 5.4% from £14.4 million to £13.6 million.

• Profit before tax reduced from £402,000 to £29,000.

• Cash inflow from operating activities £0.2 million in FY2012 compared to £0.9 million inflow inFY2011.

• Net debt reduced from £1.2 million to £1.0 million.

• Increased shareholding in Minimise Limited during the year to 36.2% and post year end to 51.0%.

HIGHLIGHTS

1

Page

Directors, Officers, Secretary and Advisers 2

Chairman’s statement 4

Business review 5

Director’s report 9

Corporate governance 12

Report of the Remuneration Committee 13

Statement of director’s responsibilities 15

Independent auditor’s report to the members of Advanced Power Components plc 16

Consolidated statement of income 18

Consolidated statement of financial position 19

Company statement of financial position 20

Consolidated and Company statement of changes in equity 21

Consolidated and Company statement of cash flows 23

Notes to the financial statements 24

Notice of Annual General Meeting 47

CONTENT

Will David, MA, FCA (Non-executive Chairman)

Will has more than 20 years’ experience working in corporate advisory and broking roles for small and mid-cap companies. During his professional career he has worked on over 20 flotations for clients across arange of sectors. His experience also includes acquisitions and disposals, public takeovers and secondaryfundraisings and provision of advice on corporate governance matters. Will is non-executive director ofCello plc and Chairman of its Audit Committee. He has also worked at Investec Henderson Crosthwaite,PricewaterhouseCoopers, Hoare Govett & Co and The London Stock Exchange.

Mark Robinson (Chief Executive Officer)

Mark joined the Group in 1985 as a sales engineer and was appointed to the Board in 1992. In June 2001,Mark was appointed Managing Director and then Chief Executive Officer in September 2004. He has beenresponsible for the expansion into new business areas for the Group and has overseen the efforts toenhance operating efficiencies and increase market penetration in recent years.

Phil Lancaster (Operations Director)

Phil joined the Group in 1995 as a product manager and in June 2000 was appointed General Manager ofAPC’s distribution business. He was responsible for developing APC as a dominant technically based salespresence in the UK’s military and aerospace markets. Phil was appointed to the Board in September 2003and then to Operations Director in April 2006. He has been responsible for improving operating efficienciesand for the successful integration of the Company’s acquisitions.

Rob Smith, MSc, FCMA, CGMA (Finance Director)

Rob joined the Group in January 2010 and was appointed as a Director in March 2010. He was previouslyFinance Director and Acting CEO at AIM listed Densitron Technologies plc a manufacturer and distributorof electronic displays. Rob has also served as Finance Director at AIM listed Curidium Medica plc, wherehe successfully led the sale of the business to Avacta Group plc in 2009, and Eco City Vehicles plc, wherehe led the business through the listing process in 2007. Rob’s earlier career was spent principally in theelectronic components industry working for GEC, Centronic and International Rectifier.

John (Ian) Davidson (Non-executive Director)

Ian has 40 years experience in the electronic components industry. He has led start-up and turnaroundsituations as well as running a number of substantial distribution businesses for Diploma PLC, LexElectronics and most recently the Addtron group of companies. During his career he has worked with themost technically advanced products, been involved with companies such as Intel, NEC and Motorola andrecognises the importance of differentiation and focus for business success.

Secretary and Registered Office

Rob Smith, MSc, FCMA, CGMA47 Riverside, Medway City Estate, Rochester, Kent, ME2 4DP

Company Registration Number

01635609

Nominated Advisers

Strand Hanson Limited26 Mount Row, London, W1K 3SQ

2

DIRECTORS, OFFICERS, SECRETARY AND ADVISERS

Stockbroker

Northland Capital Partners60 Gresham Street, London, EC2V 7BB

Auditor

Baker Tilly UK Audit LLPThird Floor, One London Square, Cross Lanes, Guildford GU1 1UN

Solicitors

Ashurst LLPBroadwalk House, 5 Appold Street, London, EC2A 2HA

Principal Bankers

Bank of Scotland plc(part of Lloyds Banking Group plc)33 Old Broad Street, London, BX2 1LB

Registrars

Capita RegistrarsThe Registry, 34 Beckenham Road, Beckenham, Kent, BR3 4TU

Financial Public Relations

Redleaf Polhill11-33 St John Street, London, EC1M 4AA

3

DIRECTORS, OFFICERS, SECRETARY AND ADVISERS(continued)

The year ended 31 August 2012 was a challenging one for UK industry. However, whilst the difficultiesexperienced in the wider economy curtailed the growth in profitability achieved by the Group over theprevious two years, I am pleased to report that early action taken to mitigate the effect of the downturn onprofitability and cash flow enabled the Group to continue its strategic investment in the clean-tech sectorwhilst still reporting a small profit before tax for the year.

Revenues in the year were £13,644,000 compared with £14,419,000 in the prior year. Net profit before taxfor the year was £29,000 compared with £402,000 in 2011. Cash inflow from operating activities was£220,000 during the year compared with an inflow in 2011 of £887,000.

Despite the pronounced weakness in our traditional market in the first half of the financial year, order intakein the electronic component distribution business saw a degree of recovery in the second half resulting inan order book of £4,032,000 on 31 August 2012 compared with £4,493,000 as at 31 August 2011. Ourdistribution activities still made a positive contribution in terms of profit and positive cash flow to the Groupwhich supported the launch of the QV Controls Limited (“QV”) business and allowed the Group to increaseits investment in Minimise Limited (“Minimise”) both during the last financial year and immediately thereafter.

It was especially gratifying to report the first major contract win for Minimise so soon after taking effectivecontrol of the business and I can report that LED lighting installations under this contract were completedto schedule. The success of Minimise in winning orders post year-end reinforces our belief that theclean-tech sector is now starting to mature into a significant business opportunity. This bodes well for thefuture prospects of Minimise and of QV which continues to develop opportunities for monitoring andcontrol solutions designed to reduce energy consumption.

Considering the scale of changes going on within the Group the Board has made the decision to make anumber of alterations to the management structure and board composition.

The Group is being reorganised to create two separate business units. In order to give each business aclear identity, a resolution is being put to the shareholders at the annual general meeting to change thename of the parent company to APC Technology Group plc and to hive down the existing electroniccomponent distribution business into a new subsidiary company to be named Advanced PowerComponents Limited. At the same time our investments in the clean-tech sector will be consolidated undera holding subsidiary called Minimise Energy Limited which will take ownership of the Company’s shareholdings in Minimise Limited and QV Controls Limited.

As we make changes to the structure of the Group, it will be necessary to reshape the composition of theboard of directors. I am, therefore, pleased to confirm that Ms Tessa Laws has agreed to serve as a non-executive director and a resolution to appoint her at the annual general meeting is set out in the attachednotice of meeting. A brief biography for Ms Laws is included in the Report of the Directors.

Whilst the difficult climate meant that the year ended 31 August 2012 was not as profitable as anticipated,it was a year of significant progress in redefining the business. The considerable changes made will positionthe Group to take advantage of the emerging opportunities in the clean-tech sector and a recovery in theelectronic component distribution sector, which is expected to coincide with a wider economic recovery.None of this change would have been possible without the hard work of the staff and the support of ouradvisors and business partners to whom the Board of Directors is grateful.

Will David, MA, FCA

Chairman

28 November 2012

4

CHAIRMAN’S STATEMENT

Financial results

Group revenue for the financial year was £13,644,000 compared with £14,419,000 in 2011, resulting in anet profit before tax of £29,000 compared with a profit before tax of £402,000 last year. Basic and dilutedearnings per share for 2012 were nil, compared with 1.2p per share in 2011.

Sales to customers whose primary markets are in the Euro zone were depressed and generally the Groupsaw a soft market conditions in the commercial and industrial sectors. Defence and aerospace marketswere relatively resilient and the Group has seen success in winning “slots” on a number of key projects inthis sector.

Despite the reduction in sales and profit in 2012 the Group to continued its investment in technical andsales staff and in the continuing development in clean technology products. The need to balance short-term cost reduction so that the Group attained a breakeven financial performance whilst continuing toinvest in activities where the Board sees long term sustainable profit growth was carefully weighed.

In the year, the Group increased its investment in Minimise Limited by acquiring additional shares in thatcompany resulting in a holding of 36.2% at 31 August 2012, as such the investment is treated as anassociated company in the year ended 31 August 2012’s accounts. Post year-end further shareacquisitions have been made that increased the Group’s interest in Minimise Limited to 51.0% and thisentity will be classed as a subsidiary from September 2012.

Changes to the Board

There were no changes to the board during the year.

Operations

The Group continues to focus on winning long run design in business on product lines where we areexclusive distributors. The Group’s order book reduced to £4,032,000 as at 31 August 2012 (31 August2011: £4,493,000) and reflects the difficult trading conditions encountered in the commercial and industrialmarkets particularly in the first half of the Financial Year.

The Group has consolidated improvements made to its inventory management processes in recent yearsand achieved a further reduction of inventory levels throughout the year.

Funding and cash flow

Cash flow from operating activities showed a positive flow of £220,000 building on the inflow of £887,000in 2011. The lower inflow occurred mainly due to reduced profit for the year.

The Group’s overall cash position showed an outflow of £33,000 in the year, compared with an outflow of£118,000 in 2011. Tighter cash management has allowed the Group to keep lower levels of cash on handand therefore reduce its day to day borrowings.

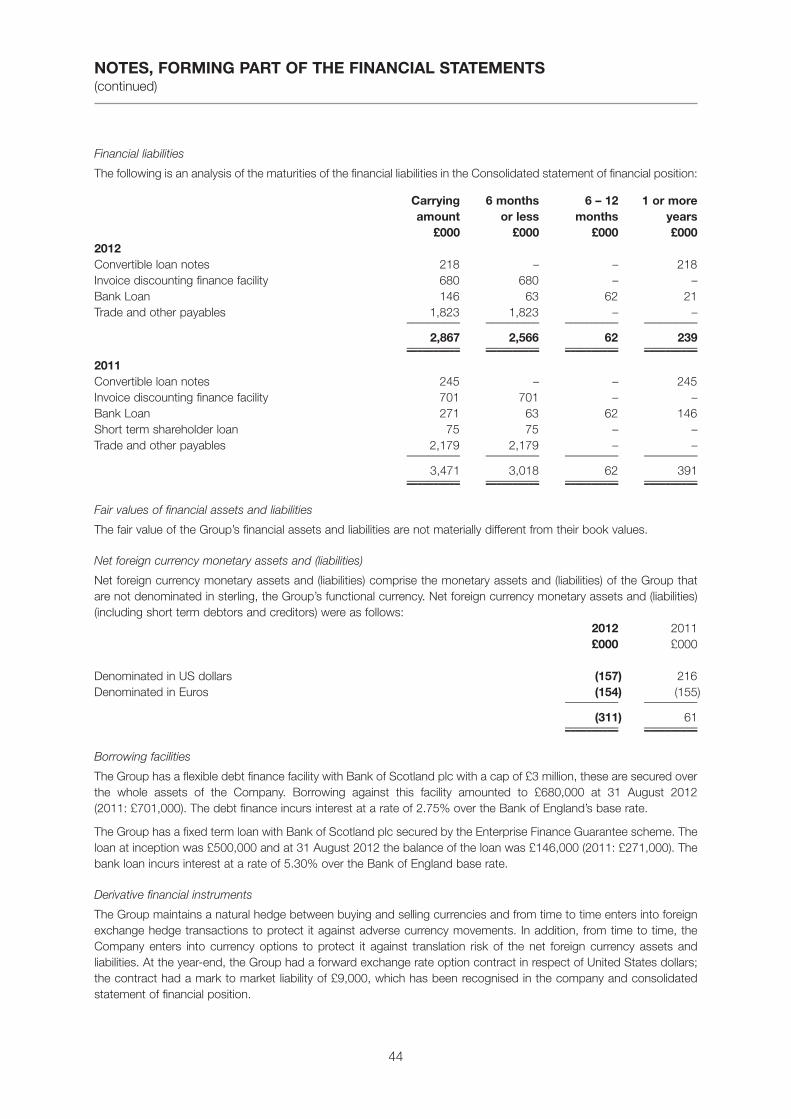

The Group’s Net Debt reduced by £208,000 in the year to £1,035,000 at 31 August 2012. The Group hasan invoice discounting facility with The Bank of Scotland of up to £3 million, as at the 31 August 2012£680,000 (31 August 2011: £701,000) had been drawn down out of a potential availability of £1,409,000(31 August 2011: £1,677,000).

The Group ended the year with a positive cash balance of £16,000 (2011: £49,000).

5

BUSINESS REVIEW

Key performance indicators

The directors set budgets for the year which are reviewed against the management accounts on a monthlybasis. In addition to these results the directors review a number of key performance indicators to assessthe performance of the Group and assist in decision making. The principal indicators monitored are:

Gross margin to sales ratio

The Board recognises the importance of growing the Group’s turnover but believe that this should only bedone at acceptable margins. To that end, targets are set and monitored. The margin achieved in 2012 was29.5% (2011: 30.0%) against a target of 28.6%. Whilst the margin achieved was slightly lower than theprior year the directors were pleased that the result saw an improvement compared with target despite theincreased pressure on pricing in the market.

Overheads to sales ratio

The Board recognises the importance of controlling administrative expenses in line with the overall level ofbusiness. As a technical sales company sufficient resources are required to provide the differentiationessential to enable the business to offer added value to our customers and to ensure that the business isdeveloped to deliver profit both in the current period and future years. Because of the below target sales,the Overheads to Sales Ratio in 2012 increase to 28.6% (2011: 26.3%) compared with target of 26.7%.The Board considers that the overhead expenditure of the Group was well controlled in the current yearand that additional investment in overheads, described elsewhere in the Business Review, is bothaffordable and essential to build future growth.

Profit before tax ratio

The Board recognise that delivering a profit before tax (PBT) is fundamental to the health of the businessand monitors the PBT as a percentage of sales to ensure that an acceptable return is made. In 2012 thedirectors set a target of 3.0% and achieved an actual PBT to Sales Ratio of 0.2% (2011: 2.8%). The needto maintain an adequate level of resources was considered essential for the long term health of thebusiness and whereas the directors were disappointed by the low return during the year it considered thatthe shareholders best interests, in the long run, have been safeguarded during a difficult trading period.

In addition to measures of the profitability of the business the Board measure working capital efficiency toensure that the funds invested in the business are effectively managed to ensure that the business hassufficient liquidity to meet its near term obligations. The Key Performance Indicators used to monitorworking capital performance are:

Inventory turns

The Group maintains inventory so that it can meet customer demand for scarce and long lead-time itemsand to fulfil customer orders where deliveries are scheduled over a number of months or years. During2012 the inventory turned over 15.0 times (2011: 12.9 times) compared with a target of 13.6 times. TheBoard is pleased with the progress made to effectively manage inventory over a sustained period.

Trade receivables days

In line with other companies in the sector the Group extends credit facilities to customers that have asufficiently good credit rating. As at 31 August 2012 the receivables days calculated on a count back basiswas 63 days (2011: 53 days). The lengthening in receivables days resulted from granting extendedpayment terms to three key customers. The Board considers the change in receivables days justified giventhe current market dynamics and continues to monitor this ratio carefully in light of the increase.

6

BUSINESS REVIEW(continued)

Trade payables days

The Group receives credit from a number of suppliers and recognises the importance of paying its suppliersin a timely manner. As at 31 August 2012 the payables days calculated on a count back basis was 44 days(2011: 41 days). The Board considers the change in payables acceptable.

Capital expenditure

There was no significant capital expenditure during the financial year.

Risks and uncertainties

The directors recognise that risk is inherent in any business and seeks to manage risk in a controlledmanner. The key business risks are set out as follows:

Economic

The Group is subject to many of the same general economic risks faced by other businesses and especiallyso during periods of economic downturn such has existed since the middle of 2008. The Group seeks tomitigate this risk by concentrating on defence, aerospace, transportation, medical and industrial sectorswhich have historically been less susceptible to short term economic fluctuations. The Group has alsoentered the market for clean technology products where there is increasing demand driven by higherenergy costs and legislative pressure to reduce global carbon dioxide emissions.

Commercial

The Group operates in a competitive marketplace and faces competition from a number of othercompanies. The risk is managed by giving primary focus on products where the Group is the sole UKdistributor and where the specific designs are registered with the products manufacturer so that the Groupis sole sourced for that particular application.

Supply chain

The Group represents and distributes a range of products from a number of different suppliers and asignificant proportion of the Group’s business is long-term and repeat business. To be able to delivercontinuous supply to customers the Group is dependent on continuity of supply over the long term. Tomanage this risk the Group has established close working relationships with its key suppliers anddiversified the range of products offered to the market.

Financing

The Group’s funding requirements are met through a mixture of long-term loans, convertible loan notes andshort-term invoice discounting facilities. The board meets regularly with all its funders to ensure a goodworking relationship.

Financial

The Group has a specific exposure to credit risk, interest rate and exchange rate fluctuations. The Grouphas established a number of policies to mitigate the risks presented, further details of which are presentedin note 20 to the financial statements.

In addition to regular board meetings, the Group holds frequent Executive and Management Meetings atwhich business risks are reviewed. Any areas that are causing concern are discussed and actions areidentified and taken to address specific concerns.

7

BUSINESS REVIEW(continued)

The risks outlined above are not an exhaustive list of risks faced by the Group and are not intended to bepresented in any order of priority.

Current Trading

Current trading remains relatively steady despite the renewed economic uncertainty and the backlog forthe first half of the year continues to recover. The Group is continuing its focus on long-term “design in”and will progressively develop its core business using this model. The contract win for LED lighting byMinimise is being shipped through the first quarter and quoting activity remains high for LED basedproducts and other clean tech offerings.

Outlook

The economic outlook for the UK has marginally improved compared with the first half of 2012 and thedirectors believe APC’s core business will benefit from the better trading conditions. Sales of the Group’sclean tech products are being stimulated by demand from our customers to reduce their energyconsumption and carbon footprint, this provides an opportunity for the Group to outperform the generaleconomy.

M. R. Robinson

Chief Executive Officer

8

BUSINESS REVIEW(continued)

The directors have pleasure in presenting their report and the audited financial statements of AdvancedPower Components plc (“the Company”) and its subsidiary undertakings (together “the Group”) for the yearended 31 August 2012.

Principal activities

The principal activity of the Group and Company in the year under review was the supply and distributionof specialist electronic components.

Results for the year and dividend

The Group’s loss on ordinary activities after taxation was £32,000 (2011: £295,000 profit) and is dealt withas shown in the consolidated statement of income on page 18.

No interim dividend was paid and it is proposed that no final dividend will be paid this year (2011: £nil).

Review of the business and future outlook

A review of the Group’s activities during the year and future outlook is set out in the Chairman’s Statementand the Business Review on pages 4 to 8.

Events after the reporting period

On 6 September 2012 the Group increased its shareholding in Minimise Limited, a company involved inthe distribution and marketing of clean technology products including the imop™, to 51.0%. To finance theacquisition of the increased stake the Company issued 489,272 ordinary shares at 7.5p per share anddrew down £100,000 cash from a convertible loan note facility agreed with Mr R. Robinson a significantshareholder in the Company. The assets and liabilities of Minimise Limited at the date that the Groupincreased its shareholding to 51.0% were substantially the same as set out in note 12. The cumulativegoodwill in relation to this acquisition will total £474,000. The goodwill represents the value of the futureincome stream attributable to the assets.

On 29 October 2012 the Group announced the acquisition of CeroUK Limited a recently establishedbusiness promoting the integration of sustainable technologies in business models suitable for third partyfinancing. CeroUK Limited’s business will be traded under the Minimise brand and will be transferred toMinimise Energy Limited a holding company that APC is establishing to consolidate its investments in its“green tech” portfolio. Consideration for CeroUK Limited was in the form of an issue of 310,000 shares inAPC at 7.5p per share and £23,250 in cash. CeroUK Limited held no assets or liabilities at the acquisitiondate.

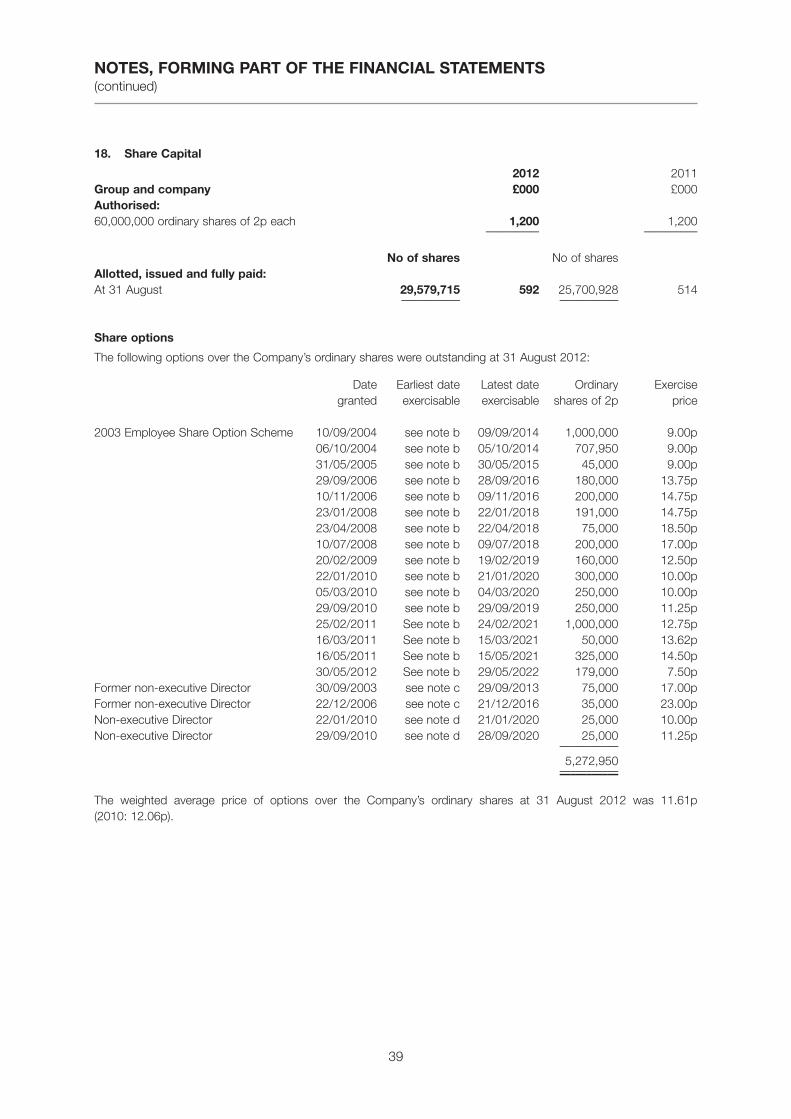

Share capital

Details of the Company’s share capital are set out in note 18 to the financial statements. The followingshares were issued during the year:

Date Reason for issue Shares issued

8 August 2012 Consideration for shares in Minimise Limited 1,212,1218 August 2012 Conversion of loan 1,333,3339 August 2012 Conversion of loan 1,333,333

9

REPORT OF THE DIRECTORS

Substantial Interests

As at 23 November 2012, the last practical date before publication of the Financial Statements, the Grouphas been notified of the following interests of three per cent or more in its issued capital:

PercentageNumber of issued

of shares capital

Roger Robinson and related family trusts 7,493,821 24.7%John Mitchell and related family trusts 4,535,500 14.9%David Elbourne and associated partnership 2,545,454 8.4%Hargreave Hale & Co 1,650,000 5.4%John Edward Evans 1,090,950 3.6%

Directors

The names of the directors who have served since September 2011.

W. DavidM. RobinsonP. LancasterR. Smith J. Davidson

Mr P. Lancaster retires by rotation and, being eligible, offers himself for re-election. Mr Lancaster’sbiography is set out in the Directors, Secretary and Advisers section on page 2 of this report. Mr Lancasterhas a letter of appointment, as described in the Report of the Remuneration Committee on pages 13 and14. A resolution to reappoint Mr Lancaster will be proposed at the forthcoming Annual General Meeting(Resolution 2).

Ms T. Laws has agreed to serve as a non-executive director and a resolution to appoint her will beproposed at the forthcoming Annual General Meeting (Resolution 3). Tessa Laws qualified as a solicitorin 1997 and after 15 years with Rosenblatt Solicitors set up her own practice in 2010 focusingpredominantly on corporate and commercial law, mergers and acquisitions and investment. Tessa alsoruns a consultancy, which seeks to advise and raise funds for companies within the world of renewableenergy and media. A graduate of the London School of Economics and Cranfield School of Management,Tessa was one of the first people to launch frozen yoghurt in this country in 1988 before starting her legaltraining in 1993. Tessa is a trustee of the Food Education Foundation and of Working Chance, a founderof the New Energy Awards and she holds two non-executive positions on the boards of small companieswithin the “clean technology” arena.

Directors’ interests

Details of share options held by the directors over the ordinary shares of the Group are set out in the Reportof the Remuneration Committee.

Share option plan

In June 2003 the Board approved a new share option scheme, the 2003 Employee Share Option Scheme,which superseded the previous share option plan established in 1996. Details of the scheme are set out innote 18 to the financial statements.

Employment policies

The directors recognise the important role played by the Group’s employees in its past success and futuredevelopment and are committed to providing an environment which will attract, motivate and reward highquality employees.

10

REPORT OF THE DIRECTORS(continued)

Financial participation in the Group’s growth and success is encouraged by means of the share optionscheme, as set out in the Report of the Remuneration Committee on pages 13 and 14.

It is the policy of the directors to encourage the employment and training of disabled people whereverappropriate and to evaluate all employees on the basis of merit.

Policy and practice on payment of creditors

Whilst the Group does not have a formal payment code, the Group agrees payment terms with its supplierswhen it enters into binding purchase contracts. It is the Group’s policy to adhere to the payment termsagreed with its suppliers whenever it is satisfied that the supplier has provided the goods or services inaccordance with the agreed terms and conditions. The ratio between the amounts invoiced to the Groupby its suppliers during the year ended 31 August 2012 and the amounts owed to its trade creditors at theyear-end was 27 days (2011: 39 days).

Going concern

On the basis of current financial projections and available funds and agreed facilities, the directors aresatisfied that the Group has adequate resources to continue in operation for the foreseeable future andtherefore consider it appropriate to prepare the financial statements on the going concern basis. SeeNote 1 to the financial statements.

Research and development

Development costs were £5,000 (2011: £24,000). These costs have been treated as an intangible asset inthe consolidated accounts and will be amortised over 4 years.

Donations

During the period £780 (2011 – £1,287) was donated to charities. There were no political donations.

Auditor

Baker Tilly UK Audit LLP were appointed as auditor to the Group at the Company’s Annual GeneralMeeting on 20 January 2012 and have indicated their willingness to continue as auditor.

The directors who were in office at the date of approval of the financial statements have confirmed that asfar as they are aware there is no relevant audit information of which the Group’s auditor is unaware. Thedirectors have taken all the steps that ought to have been taken as directors in order to make themselvesaware of any relevant audit information and to establish that the Group’s auditor are aware of thatinformation.

Annual General Meeting

The Annual General Meeting of the Company will be held on Friday 25 January 2013 at 12 noon at theoffices of Northland Capital Partners, 60 Gresham Street, London EC2V 7BB. The text of all of theproposed Resolutions is set out in the Notice of Annual General Meeting on page 47.

By Order of the Board

R. S. Smith

Secretary

28 November 2012

11

REPORT OF THE DIRECTORS(continued)

Since November 2002 the Company’s shares have been listed on the Alternative Investment Market (AIM).As an AIM listed company, the Company is not required to follow the provisions of the UK CorporateGovernance Code published by the Financial Reporting Council. Nevertheless, the Board is committed tohigh standards of corporate governance throughout the Group. The Board is accountable to theCompany’s shareholders for good governance and this statement describes which principles of corporategovernance that have been applied by the Company.

The Board of Directors

The activities of the Group are ultimately controlled by the Board of Directors. All directors are subject toretirement and re-election by rotation.

During the year under review the Board consisted of three executive directors and two non-executivedirectors, one of whom, Will David, served as non-executive Chairman. The non-executive directorsrepresent a strong and independent element and their views carry considerable weight in the Board’sdecision-making process.

The Group has a formal policy setting out the matters that require approval of the Board. This covers themajor areas of decision-making in all aspects of the Group’s affairs.

Committees of the Board

The Audit Committee meets at least twice a year and considers the appointment of the external auditorsas well as discussing with them the findings of the audit and any reports to the management or thosecharged with governance arising from it. The Committee is also responsible for monitoring compliance withaccounting and legal requirements and for reviewing the interim and annual reports before publication. TheAudit Committee consists of Will David and Ian Davidson with meetings attended by Finance Director RobSmith and other executive directors when appropriate.

The Remuneration Committee operates under the chairmanship of Will David and is responsible for settingthe remuneration of directors and senior management, as well as reviewing the remuneration policythroughout the Group. The Report of the Remuneration Committee is set out on pages 13 and 14.

Owing to the small size of the Group’s Board, it is not considered necessary to have a formal NominationCommittee for the purpose of making recommendations regarding senior Board appointments. All of themembers of the Board are involved in the decision-making process for Board and other seniormanagement appointments.

Internal control

The directors are responsible for establishing and maintaining the Group’s system of internal control. Thissystem of internal control is designed to safeguard the Group’s assets and to ensure that properaccounting records are maintained and that financial information produced by the Group is reliable. Thereare inherent limitations in any system of internal control and such a system can provide only reasonable,but not absolute, assurance against material misstatement or loss. The directors, through the AuditCommittee, have reviewed the effectiveness of the Group’s system of internal control.

12

CORPORATE GOVERNANCE

The Remuneration Committee operates under the chairmanship of Will David. It was formed in order toreview the remuneration of executive directors and senior management, together with remuneration policyfor the Group as a whole, and to make recommendations to the Board.

Remuneration policy

Remuneration

In order to safeguard the interests of the Group, the Committee aims to provide executive directors andemployees of the Group with a remuneration package set to attract, retain and motivate directors andemployees of the appropriate calibre. Bonus schemes are determined for each financial year, based on theGroup's financial performance, targets for which are approved by the Remuneration Committee.

Share options

The Advanced Power Components plc Company Share Option Plan was established on 7 October 1996for the benefit of all employees of the Group employed at that date as well as certain of the directors. On17 June 2003 the Board approved the establishment of a new plan, the 2003 Employee Share OptionScheme, which superseded the 1996 plan.

The 2003 Employee Share Option Scheme requires that certain performance conditions must be satisfiedbefore options may be exercised. The performance conditions are based on achievement of budgetedprofit before taxation.

Details of the share options granted to directors and outstanding as at 31 August 2012 are listed below:

Latest OrdinaryDate date shares Exercise

granted exercisable of 2p Price

M. Robinson 10/09/2004 09/09/2014 500,000 9.0p06/10/2004 05/10/2014 232,050 9.0p

P. Lancaster 10/09/2004 09/09/2014 500,000 9.0p06/10/2004 05/10/2014 117,000 9.0p

R. Smith 05/03/2010 04/03/2020 250,000 10.0p16/05/2011 15/05/2021 250,000 14.5p

J. Davidson 22/01/2010 21/01/2020 25,000 10.0p

W. David 29/09/2010 28/09/2020 25,000 11.25p

In each case these options are exercisable in various proportions dependent upon the performance of theGroup. The earliest date on which each proportion can be exercised is the date on which the results forthe relevant financial year are announced.

Service contracts

Each of the executive directors that served in the year had a service agreement that may be terminated byeither party upon giving between six months and one year's written notice to expire at any time.Non-executive directors have letters of appointment which are terminable at the will of either party.

13

REPORT OF THE REMUNERATION COMMITTEE

Pensions

The Group makes contributions to defined contribution pension schemes for the benefit of the executivedirectors. The Group maintains health care insurance for the benefit of the executive directors and certainemployees and their dependents.

Directors’ emoluments

Employers Salary Benefits national Total emoluments Pension and fees Bonus in kind insurance (excluding pensions) contributions 2012 2011 2012 2011 £000 £000 £000 £000 £000 £000 £000 £000

W. David 24 – – 2 26 26 – –M. Robinson 107 10 16 17 150 155 3 3 P. Lancaster 84 5 13 13 115 116 4 4 R. Smith 84 5 8 13 110 107 4 4 J. Davidson 39 – – – 39 39 – – –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

338 20 37 45 440 443 11 11 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

Benefits in kind shown in the table above comprise the provision of a motor car and private healthinsurance.

14

REPORT OF THE REMUNERATION COMMITTEE(continued)

The directors are responsible for preparing the annual report and the group and parent company financialstatements, in accordance with applicable law and regulations.

Company law requires the directors to prepare financial statements for each financial year. The directorsare required by the AIM rules of the London Stock Exchange to prepare group financial statements inaccordance with the International Financial Reporting Standards (“IFRS”) as adopted by the EuropeanUnion (“EU”) and have elected under company law to prepare the company financial statements inaccordance with IFRS as adopted by the EU.

Under company law the directors must not approve the financial statements unless they are satisfied thatthey give a true and fair view of the state of affairs of the group and parent company and of the profit orloss of the group for that period.

In preparing these financial statements, the directors are required to:

• Select suitable accounting policies and then apply them consistently;

• Make judgements and accounting estimates that are reasonable and prudent;

• State whether applicable IFRSs as adopted by the EU have been followed, subject to any materialdepartures disclosed and explained in the financial statements;

• Prepare the financial statements on the going concern basis for the Company and Group unless it isinappropriate to presume that the company will continue in business.

The directors are responsible for keeping adequate accounting records that are sufficient to show andexplain the Company’s transactions and disclose with reasonable accuracy at any time the financialposition of the Company and enable them to ensure that its financial statements comply with theCompanies Act 2006. They are also responsible for safeguarding the assets of the Company and theGroup and hence for taking reasonable steps for the prevention and detection of fraud and otherirregularities.

The directors are responsible for the maintenance and integrity of the Company’s website. Legislation inthe UK governing the preparation and dissemination of financial statements may differ from legislation inother jurisdictions.

15

STATEMENT OF DIRECTORS’ RESPONSIBILITIES

We have audited the group and parent company financial statements (“the financial statements”) on pages18 to 46 The financial reporting framework that has been applied in their preparation is applicable law andInternational Financial Reporting Standards (IFRSs) as adopted by the European Union and, as regards theparent company financial statements, as applied in accordance with the provisions of the Companies Act2006.

This report is made solely to the company’s members, as a body, in accordance with Chapter 3 of Part 16of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company’smembers those matters we are required to state to them in an auditor’s report and for no other purpose.To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than thecompany and the company’s members as a body, for our audit work, for this report, or for the opinions wehave formed.

Respective responsibilities of directors and auditor:

As more fully explained in the Directors’ Responsibilities Statement set out on page 15, the directors areresponsible for the preparation of the financial statements and for being satisfied that they give a true andfair view. Our responsibility is to audit and express an opinion on the financial statements in accordancewith applicable law and International Standards on Auditing (UK and Ireland). Those standards require usto comply with the Auditing Practices Board’s (APB’s) Ethical Standards for Auditors.

Scope of the audit of the financial statements

A description of the scope of an audit of financial statements is provided on the APB’s website atwww.frc.org.uk/apb/scope/private.cfm.

Opinion on financial statements

In our opinion:

• the financial statements give a true and fair view of the state of the group’s and the parent’s affairs asat 31 August 2012 and of the group’s loss for the year then ended;

• the group financial statements have been properly prepared in accordance with IFRSs as adopted bythe European Union;

• the parent financial statements have been properly prepared in accordance with IFRSs as adoptedby the European Union and as applied in accordance with the Companies Act 2006; and

• the financial statements have been prepared in accordance with the requirements of the CompaniesAct 2006.

Opinion on other matter prescribed by the Companies Act 2006

In our opinion the information given in the Directors’ Report for the financial year for which the financialstatements are prepared is consistent with the financial statements.

16

INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF ADVANCED POWER COMPONENTS PLC

Matters on which we are required to report by exception

We have nothing to report in respect of the following matters where the Companies Act 2006 requires usto report to you if, in our opinion:

• adequate accounting records have not been kept by the parent company, or returns adequate for ouraudit have not been received from branches not visited by us; or

• the parent company financial statements are not in agreement with the accounting records andreturns; or

• certain disclosures of directors’ remuneration specified by law are not made; or

• we have not received all the information and explanations we require for our audit.

Colin Roberts, FCA (Senior Statutory Auditor)For and on behalf of Baker Tilly UK Audit LLP

Statutory Auditor Chartered AccountantsThird FloorOne London SquareCross LanesGuildford GU1 1UN

Date: 28 November 2012

17

INDEPENDENT AUDITORS’ REPORT TO THE MEMBERS OF ADVANCED POWER COMPONENTS PLC(continued)

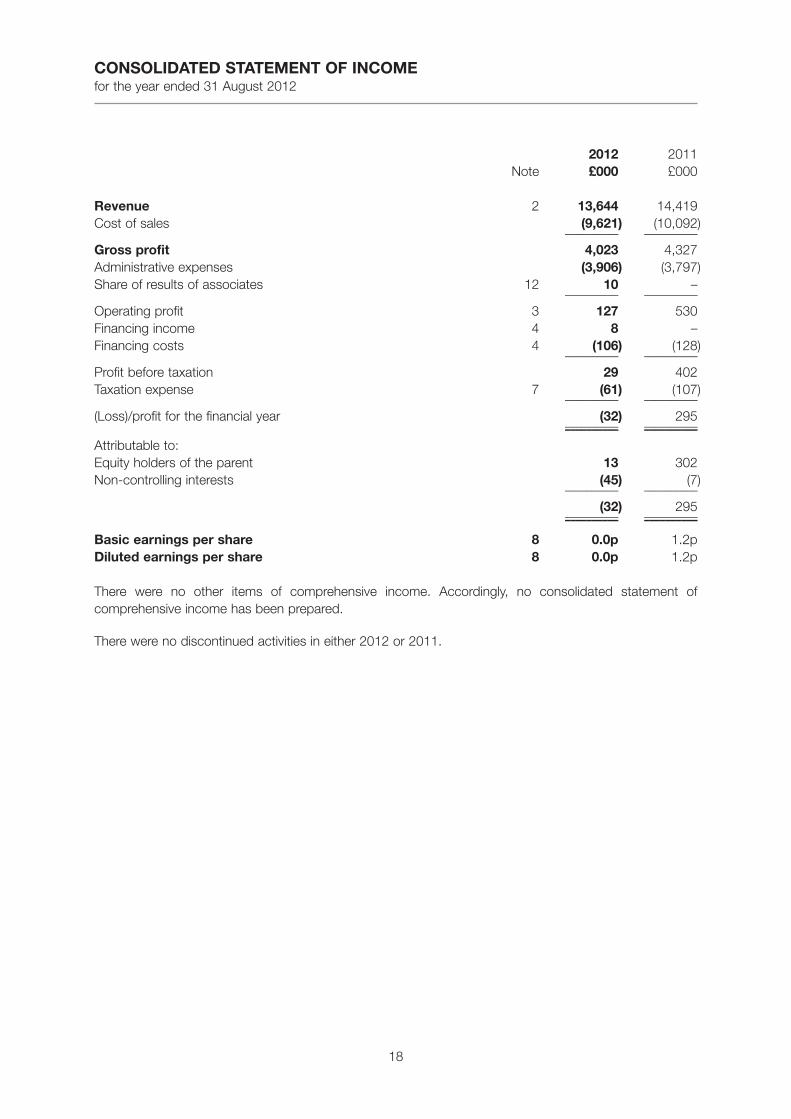

2012 2011Note £000 £000

Revenue 2 13,644 14,419Cost of sales (9,621) (10,092)

–––––––––– ––––––––––

Gross profit 4,023 4,327Administrative expenses (3,906) (3,797)Share of results of associates 12 10 –

–––––––––– ––––––––––

Operating profit 3 127 530Financing income 4 8 –Financing costs 4 (106) (128)

–––––––––– ––––––––––

Profit before taxation 29 402Taxation expense 7 (61) (107)

–––––––––– ––––––––––

(Loss)/profit for the financial year (32) 295–––––––––– –––––––––––––––––––– ––––––––––

Attributable to:Equity holders of the parent 13 302Non-controlling interests (45) (7)

–––––––––– ––––––––––

(32) 295–––––––––– –––––––––––––––––––– ––––––––––

Basic earnings per share 8 0.0p 1.2pDiluted earnings per share 8 0.0p 1.2p

There were no other items of comprehensive income. Accordingly, no consolidated statement ofcomprehensive income has been prepared.

There were no discontinued activities in either 2012 or 2011.

18

CONSOLIDATED STATEMENT OF INCOMEfor the year ended 31 August 2012

2012 2011Note £000 £000

Non-current assets

Intangible assets 9 2,671 2,673Property, plant and equipment 10 144 202Investment in associates 12 306 –Financial assets 12 207 358

–––––––––– ––––––––––

3,328 3,233–––––––––– ––––––––––

Current assets

Inventories 14 625 761Trade and other receivables 15 2,300 2,547Cash and cash equivalents 21 16 49

–––––––––– ––––––––––

2,941 3,357–––––––––– ––––––––––

Total assets 6,269 6,590–––––––––– ––––––––––

Current liabilities

Trade and other payables 16 (1,774) (2,130)Borrowings 16 (805) (901)Current tax liability 16 (55) (49)

–––––––––– ––––––––––

(2,634) (3,080)–––––––––– ––––––––––

Total assets less current liabilities 3,635 3,510–––––––––– ––––––––––

Non-current liabilities

Borrowings 17 (239) (391)Deferred tax liability 13 (9) (3)

–––––––––– ––––––––––

Net assets 3,387 3,116–––––––––– –––––––––––––––––––– ––––––––––

Equity attributable to equity holders of the company

Called-up share capital 18 592 514Share premium account 790 577Share option reserve 261 254Other reserves 9 11Retained earnings 1,787 1,767

–––––––––– ––––––––––

Equity attributable to shareholders of Advanced Power Components 3,439 3,123Non-controlling interests (52) (7)

–––––––––– ––––––––––

Total equity 3,387 3,116–––––––––– –––––––––––––––––––– ––––––––––

The financial statements on pages 18 to 46 were approved and authorised for issue by the Board ofDirectors on 28 November 2012 and were signed on its behalf by:

M. R. Robinson R. S. Smith

Director Director

ADVANCED POWER COMPONENTS plc

Registered No: 01635609

19

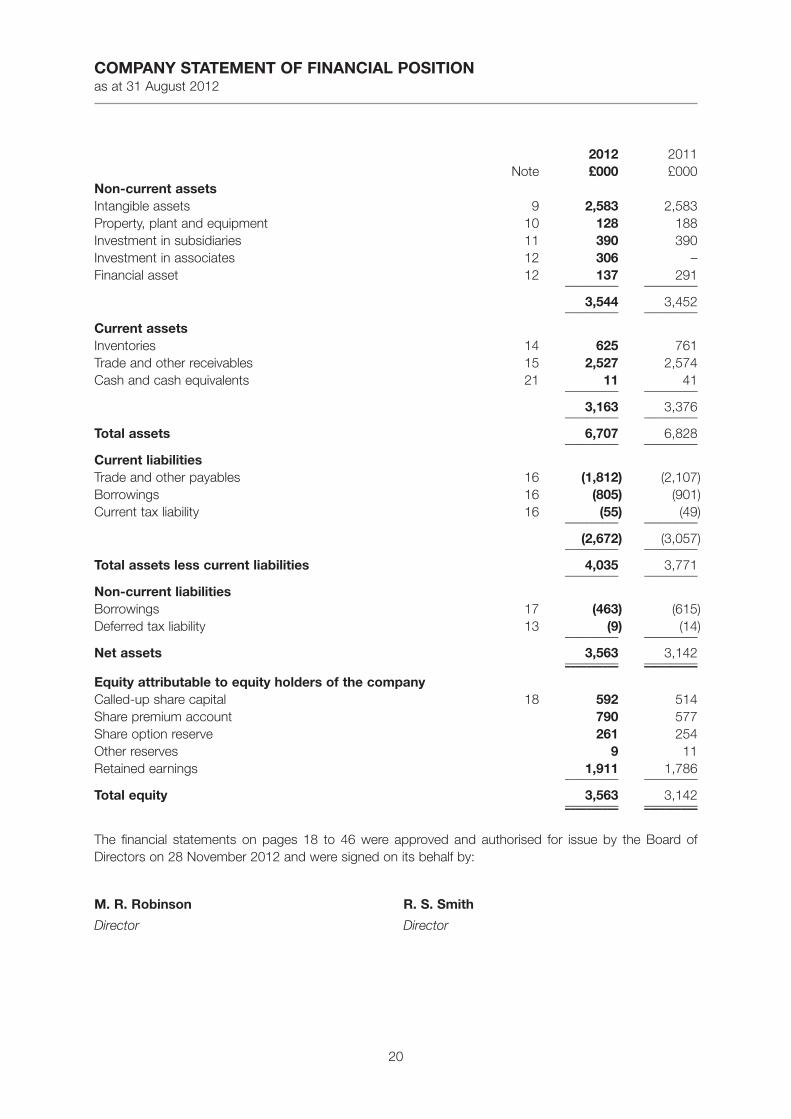

CONSOLIDATED STATEMENT OF FINANCIAL POSITIONas at 31 August 2012

2012 2011Note £000 £000

Non-current assets

Intangible assets 9 2,583 2,583Property, plant and equipment 10 128 188Investment in subsidiaries 11 390 390Investment in associates 12 306 –Financial asset 12 137 291

–––––––––– ––––––––––

3,544 3,452–––––––––– ––––––––––

Current assets

Inventories 14 625 761Trade and other receivables 15 2,527 2,574Cash and cash equivalents 21 11 41

–––––––––– ––––––––––

3,163 3,376–––––––––– ––––––––––

Total assets 6,707 6,828–––––––––– ––––––––––

Current liabilities

Trade and other payables 16 (1,812) (2,107)Borrowings 16 (805) (901)Current tax liability 16 (55) (49)

–––––––––– ––––––––––

(2,672) (3,057)–––––––––– ––––––––––

Total assets less current liabilities 4,035 3,771–––––––––– ––––––––––

Non-current liabilities

Borrowings 17 (463) (615)Deferred tax liability 13 (9) (14)

–––––––––– ––––––––––

Net assets 3,563 3,142–––––––––– –––––––––––––––––––– ––––––––––

Equity attributable to equity holders of the company

Called-up share capital 18 592 514Share premium account 790 577Share option reserve 261 254Other reserves 9 11Retained earnings 1,911 1,786

–––––––––– ––––––––––

Total equity 3,563 3,142–––––––––– –––––––––––––––––––– ––––––––––

The financial statements on pages 18 to 46 were approved and authorised for issue by the Board ofDirectors on 28 November 2012 and were signed on its behalf by:

M. R. Robinson R. S. Smith

Director Director

20

COMPANY STATEMENT OF FINANCIAL POSITIONas at 31 August 2012

Attributable to the equity owners of the parent Non- controlling Share Share interests Share premium option Other Retained Retained capital account reserve reserves earnings Total earnings Total £000 £000 £000 £000 £000 £000 £000 £000Group

At 31 August 2010 503 519 219 13 1,465 2,719 – 2,719 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

Profit for the year – – – – 302 302 (7) 295 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

Total comprehensive income – – – – 302 302 (7) 295 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

Transactions with owners

Issue of new shares 11 58 – – – 69 – 69Convertible loan notes – – – (2) – (2) – (2)Share option charge – – 35 – – 35 – 35 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

11 58 35 (2) – 102 – 102 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

At 31 August 2011 514 577 254 11 1,767 3,123 (7) 3,116 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

Profit for the year – – – – 13 13 (45) (32) –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

Total comprehensive income – – – – 13 13 (45) (32) –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

Transactions with owners Issue of new shares 78 213 – – – 291 – 291Convertible loan notes – – – (2) 7 5 – 5Share option charge – – 7 – – 7 – 7 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

78 213 7 (2) 7 303 – 303 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

At 31 August 2012 592 790 261 9 1,787 3,439 (52) 3,387 –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– –––––––– ––––––––

21

CONSOLIDATED STATEMENT OF CHANGES IN EQUITYfor the year ended 31 August 2012

Share Share premium Share option Other Retained capital account reserve reserves earnings Total £000 £000 £000 £000 £000 £000Company

At 31 August 2010 503 519 219 13 1,469 2,723 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Profit for the year – – – – 317 317 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Total comprehensive income – – – – 317 317 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Transactions with owners

Issue of new shares 11 58 – – – 69Convertible loan notes – – – (2) – (2)Share option charge – – 35 – – 35 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

11 58 35 (2) – 102 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

At 31 August 2011 514 577 254 11 1,786 3,142 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Profit for the year – – – – 118 118 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Total comprehensive income – – – – 118 118 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Transactions with owners

Issue of new shares 78 213 – – – 291Convertible loan notes – – – (2) 7 5Share option charge – – 7 – – 7 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

78 213 7 (2) 7 303 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

At 31 August 2012 592 790 261 9 1,911 3,563 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Share capital and premium

When shares are issued, the nominal value of the shares is credited to the share capital reserve. Anypremium paid above the nominal value is taken to the share premium reserve. Advanced PowerComponents plc shares have a nominal value of 2p per share.

Share option reserve

The share option valuation reserve arises as the expense of issuing share-based payments is recognisedover time. The reserve will fall as share options vest and are exercised, and the impact of the subsequentdilution of earnings per share crystallises, but the reserve may equally rise or see any reduction offset, asnew potentially dilutive share options are issued.

Other reserves

The reserve arises as a result of assessing the equity component of the Convertible Loan Notes issuedduring 2009.

Retained earnings

The retained earnings reserve records the accumulated profits and losses of the Group since inception ofthe business. Where subsidiary undertakings are acquired, only profits arising from the date of acquisitionare included.

22

COMPANY STATEMENT OF CHANGES IN EQUITY(continued)

Group Group Company Company2012 2011 2012 2011

Note £000 £000 £000 £000Reconciliation of cash flows from

operating activities

Profit before taxation for the financial year 29 402 169 435Share of results of associate (10) – (10) –Loss on disposal of property, plant and equipment 23 – 23 –Finance costs 106 128 105 128Finance income (8) – (5) –Taxation (49) – (49) –Amortisation of intangible assets 7 – – –Depreciation of property, plant and equipment 65 78 59 78Decrease in inventories 136 292 136 292Decrease/(increase) in trade and other receivables 247 (237) 47 (264)(Decrease)/increase in trade and other payables (333) 189 (273) 166Share-based payments 7 35 7 35 –––––––––– –––––––––– –––––––––– ––––––––––

Net cash from operating activities 220 887 209 870 –––––––––– –––––––––– –––––––––– ––––––––––

Cash flows from investing activities

Acquisition of property, plant and equipment (29) (63) (21) (54)Acquisition of subsidiary undertakings, net of cash acquired – – – (69)Acquisition of assets through business combinations – (45) – –Acquisition of shares in associate (67) (119) (67) (119)Inception of loans – (132) – (132)Eligible development costs capitalised (5) (24) – – –––––––––– –––––––––– –––––––––– ––––––––––

Net cash used in investing activities (101) (383) (88) (374) –––––––––– –––––––––– –––––––––– ––––––––––

Cash flows used in financing activities

Finance costs (106) (126) (105) (126)Proceed from issue of convertible loan notes 100 – 100 –Repayments of bank short-term invoice discounting facility (21) (371) (21) (371)Repayment of bank loan facility (125) (125) (125) (125) –––––––––– –––––––––– –––––––––– ––––––––––

Net cash used in financing activities (152) (622) (151) (622) –––––––––– –––––––––– –––––––––– ––––––––––

(Decrease) in net cash 21 (33) (118) (30) (126) –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Cash and cash equivalents as at 1 September 21 49 167 41 167(Decrease) in net cash (33) (118) (30) (126) –––––––––– –––––––––– –––––––––– ––––––––––

Cash and cash equivalents as at

31 August 21 16 49 11 41 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

23

CONSOLIDATED AND COMPANY STATEMENT OF CASH FLOWSfor the year ended 31 August 2012

1. Accounting policies

The principal accounting policies applied in the preparation of these financial statements are set out below. Thesepolicies have been applied consistently to all the years presented, unless otherwise stated.

General

Advanced Power Components plc is a public limited company (“the Company”) incorporated in the United Kingdomunder the Companies Act 2006 (registration number 01635609).

The Company is domiciled in the United Kingdom and its registered address is 47 Riverside, Medway City Estate,Rochester, Kent ME2 4DP. The Company’s Ordinary Shares are traded on the Alternative Investment Market (“AIM”) ofthe London Stock Exchange. The Group’s principal activity is the distribution of specialist electronic components.

Basis of preparation

Statement of compliance

These financial statements have been prepared in accordance with IFRS and IFRIC interpretations as adopted by theEuropean Union, and with those parts of the Companies Acts applicable to companies reporting under IFRS.

A separate statement of income for the parent company has not been presented as permitted by section 408(3) of theCompanies Act 2006. The parent Company earned a profit after tax of £118,000 (2011: £317,000).

Functional and presentational currency

These consolidated financial statements are presented in UK Sterling, which is the Company’s functional currency. Allfinancial information presented in UK Sterling has been rounded to the nearest thousand unless otherwise stated.

Going concern

The financial statements are prepared under the going concern basis. The directors believe this to be appropriatebased on historic performance and because:

• The directors have produced forecasts to the 31 December 2013 that identify that the Group has sufficientworking capital and unutilised banking facilities available so that it can meet its financial liabilities as they fall due.The forecast is compared to actual financial performance on a monthly basis and corrective action is taken ifrequired.

• As at 31 August 2012 the Group had total financial facilities of £3 million of which £680,000 (31 August 2011:£701,000) had been drawn down out of a potential availability of £1,409,000 (31 August 2011: £1,677,000).

• In September 2012, the Bank of Scotland plc entered into an agreement with Minimise Limited to provide up to£1.5 million in invoice discounting facilities, further extending the borrowing facilities available to the Group.

Use of estimates and judgements

The preparation of financial statements in conformity with IFRS requires management to make judgements, estimatesand assumptions that affect the application of policies and reported amounts in the financial statements. The areasinvolving a higher degree of judgement or complexity, or areas where assumptions or estimates are significant to thefinancial statements, are disclosed below.

Exercise of Significant judgements

The following new standards have become effective from 1 June 2011 and hence, where relevant, have been reflectedin the financial statements:

• IAS 24 Related Party Disclosures (revised 2009);

• Amendment to IFRIC 14 “Prepayments of a minimum funding requirement”;

• IAS 1 “Presentation of financial statements” – presentation of statement of changes in equity;

• IFRS 7 “Financial instruments: disclosures” – amendments to disclosures;

24

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS

• IFRIC 13 “Customer loyalty programmes” – fair value of award credit; and

• IAS 34 “Interim Financial Reporting – Significant events and transactions”.

There are a number of standards and interpretations issued by the IASB that are effective for financial statements afterthis reporting period. The following have not been adopted by Group.

• Disclosures – Transfers of financial assets (amendments to IFRS 7) (effective for periods beginning on or after1 July 2011)

• Presentation of Items of Other Comprehensive Income – Amendments to IAS 1 (effective for periods beginningon or after 1 July 2011)

• The introduction of IFRS 9 Financial Instruments means that the measurement of certain financial assets maychange dependent on the entity’s business model and the nature of the contractual cash flows. In addition, inadvance of the reporting period end, certain designations and de-designations may need to be made. Financialassets with embedded derivatives will also require re-measurement.

• The introduction of IFRS 10 means that:

o A reassessment of “control” will need to be considered using the new definition as entities may need to betreated differently in consolidated financial statements.

o Consideration of potential voting rights may alter who has control irrespective of whether they are currentlyexercisable.

The application of these standards and interpretations is not anticipated to have a material effect on the Group’sfinancial statements

Revenue

Revenue represents invoiced sales of goods, net of discounts, returns and rebates, to external customers at invoicedamounts less value added tax. Revenue is recognised when the goods are despatched to the customer. Commissionincome is recognised when payment has been received from the principal.

Basis of consolidation

The consolidated statement of comprehensive income and statement of financial position include the accounts of theCompany and all its subsidiaries made up to 31 August 2012. The results of subsidiaries acquired are included in theconsolidated statement of comprehensive income from the date control passes. Intra-group revenues and profits areeliminated fully on consolidation.

The consolidated financial statements incorporate the results of business combinations using the purchase method.In the statement of financial position, the acquiree’s identifiable assets, liabilities and contingent liabilities are initiallyrecognised at their fair values at the acquisition date. The results of acquired operations are included in theconsolidated statement of comprehensive income from the date on which control is obtained. They are deconsolidatedfrom the date control ceases.

Goodwill

Goodwill represents the excess of the cost of a business combination over, in the case of business combinationscompleted prior to 1 January 2010, the Group’s interest in the fair value of identifiable assets, liabilities and contingentliabilities acquired and, in the case of business combinations completed on or after 1 January 2010, the totalacquisition date fair value of the identifiable assets, liabilities and contingent liabilities acquired.

For business combinations completed prior to 1 January 2010, cost comprises the fair value of assets given, liabilitiesassumed and equity instruments issued, plus any direct costs of acquisition. Changes in the estimated value ofcontingent consideration arising on business combinations completed by this date are treated as an adjustment to costand, in consequence, result in a change in the carrying value of goodwill.

For business combinations completed on or after 1 January 2010, cost comprised the fair value of assets given,liabilities assumed and equity instruments issued, plus the amount of any non-controlling interests in the acquiree plus,

25

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS(continued)

if the business combination is achieved in stages, the fair value of the existing equity interest in the acquiree. Contingentconsideration is included in cost at its acquisition date fair value and, in the case of contingent consideration classifiedas a financial liability, re-measured subsequently through profit or loss. For business combinations completed on orafter 1 January 2010, direct costs of acquisition are recognised immediately as an expense.

Goodwill is capitalised as an intangible asset with any impairment in carrying value being charged to the consolidatedstatement of comprehensive income. Where the fair value of identifiable assets, liabilities and contingent liabilitiesexceed the fair value of consideration paid, the excess is credited in full to the consolidated statement ofcomprehensive income on the acquisition date.

Goodwill is reviewed for impairment at least every six months. The recoverable amount is estimated at each statementof financial position date. An impairment loss is recognised when the carrying amount of an asset or its cash generatingunit exceeds its recoverable amount. Any impairment is recognised immediately in the statement of comprehensiveincome and is not subsequently reversed.

Research and development

In accordance with IAS38 Intangible Assets, expenditure incurred on research and development, is distinguished asrelating to a research phase or to a development phase. All research phase expenditure is charged to the statementof income. Development expenditure is capitalised as an internally generated intangible assets only if it meets strictcriteria, relating in particular to technical feasibility and generation of future economic benefits. Expenditure that cannotbe classified into these two categories is treated as being incurred in the research phase.

Expenditure capitalised is amortised over its useful economic life, up to a maximum of 15 years from entry into serviceof the product.

Research and development

Depreciation is provided at the following annual rates in order to write off each asset over its estimated useful life:

Short leaseholds – Over the remaining period of the leasePlant and machinery – 25% on reducing balanceFixtures, fittings, tools and equipment – Parent company – 25% on reducing balance

Subsidiary company – straight line between 3 and 5 yearsExhibition and demonstration equipment – Straight line between 2 and 3 years

Property, plant and equipment are measured at historical cost less accumulated depreciation.

Impairment reviews of fixed assets are undertaken if there are indications that the asset’s recoverable amount may beless than the carrying values.

Investments

Investments in subsidiary undertakings held as non-current assets are stated at cost less any provision for impairment.Investment in assets available for sale are carried at fair value, any movement in fair value is recognised in the statementof comprehensive income.

Inventories

Inventories are valued at the lower of cost and net realisable value after making due allowance for obsolete and slowmoving items, on a first in first out basis.

Taxation

The taxation expense represents the sum of the tax currently payable and deferred tax. Tax currently payable is basedon taxable profits or losses for the period and is calculated using enacted tax rates.

Deferred taxation is provided on temporary differences between the carrying amounts of assets and liabilities forfinancial reporting purposes and the amounts used for taxation purposes. The Group has chosen not to adopt a policy

26

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS(continued)

of discounting the deferred tax provision. Deferred tax assets are recognised only to the extent that the directorsconsider it more likely than not that there will be suitable profits from which the future reversal of the temporarydifferences can be deducted.

Foreign currencies

Assets and liabilities in foreign currencies are translated into sterling at the rate of exchange ruling at the statement offinancial position date. Transactions in foreign currencies are translated into sterling at the rate of exchange ruling atthe date of the transactions. Resulting exchange differences are taken into account in arriving at the operating result.

Operating leases

Rentals paid under operating leases are charged to the statement of comprehensive income on a straight-line basisover the lease term.

Pension

The Group operates a stakeholder defined contribution scheme for directors and staff and also contributes to personalpension schemes of other directors and staff. The assets of the scheme are held separately from those of the Groupin an independently administered fund. Contributions are charged to the statement of comprehensive income whenthey fall due for payment or when the employee provides the services giving rise to the pension contribution.

Financial instruments

The Group classifies financial instruments, or their component parts, on initial recognition as a financial asset, a financialliability or an equity instrument in accordance with the substance of the contractual arrangement.

Financial assets are recognised when the Group has rights or other access to economic benefits. Such assets consistof cash, a contractual right to receive cash or other financial assets, or a contractual right to exchange financialinstruments with another entity on potentially favourable terms. Financial liabilities are recognised when there is anobligation and that obligation is a contractual liability to deliver cash or another financial asset or exchange financialinstruments with another entity on potentially unfavourable terms. When these criteria no longer apply, a financial assetor liability is no longer recognised.

Financial assets and liabilities are recognised at fair value, which in the case of trade receivables and trade payables issimilar to cost, and are detailed in note 21.

Where the fair value of an asset’s carrying amount falls below the asset’s carrying value, any difference is, in the caseof non-current assets, provided for if it is regarded that the impairment is permanent. In the case of current assets,provision is only made to the extent that it is considered as resulting in a lower net realisable value.

Investments in Associate

Investments in associated holdings held in non-current assets are recorded under equity accounting in line with IAS28.This has been applied by stating the investment at cost plus profits attributable to the equity holders of the parent, lessany provision for impairment.

Non-Controlling Interests

Non-Controlling interests, as at the year end, have been calculated based on the non-controlling interest’sproportionate share of net assets of the subsidiary of Advanced Power Components PLC.

Invoice discounting

The Company has an agreement with the Bank of Scotland plc whereby its trade receivables are invoice discounted,with recourse after 120 days. On the basis that the benefits and risks attaching to the debts remain with the Company,the gross debts are included as an asset within trade receivables and the proceeds received are included within bankloans and overdrafts as a liability.

27

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS(continued)

Share options

The Group issues equity-settled share-based payments to certain employees in the form of share options over sharesin the parent company. Equity-settled share-based payments are measured at fair value at the date of the grant,calculated using an independent valuation model, taking into account the terms and conditions upon which the optionswere granted. Non-market vesting conditions are taken into account by adjusting the number of equity instrumentsexpected to vest at each statement of financial position date. The fair value is expensed on a straight line basis overthe vesting period, based on the Group’s estimate of shares that will eventually vest, with the corresponding credit toequity.

2. Revenue and segmental information

The majority of the Group’s activity arises in the United Kingdom from the Group’s principal activity. The directorsmanage and monitor all operations of the business on a unified basis and consider that all of the Group’s operationsare in similar markets and face similar risks. Consequently, the directors consider the Group has one business and oneoperating segment.

An analysis of revenue by geographical destination is given below:

Group Group 2012 2011 £000 £000

UK 12,168 12,495North America 247 333Far East, Europe and other 1,229 1,591 –––––––––– ––––––––––

13,644 14,419 –––––––––– –––––––––– –––––––––– ––––––––––

3. Operating profit

The operating profit is stated after charging:

2012 2011 £000 £000

Operating leases – short leaseholds 120 112 Operating leases – plant and machinery 100 91 Depreciation – owned assets 65 78 Loss/(Gain) on foreign exchange 16 (9)Auditors’ remuneration1 – audit of parent company and consolidated accounts 30 30 Auditors’ remuneration1 – audit of subsidiary company 5 1 Auditors’ remuneration1 – taxation advice 3 –Directors’ emoluments including employers National Insurance 451 454Loss on disposal of fixed assets 23 –Amortisation of developments costs 7 – –––––––––– ––––––––––

1 Auditors remuneration in 2012 refers to Baker Tilly UK Audit LLP; 2011 refers to Reeves & Co LLP.

28

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS(continued)

4. Net financing

2012 2011 £000 £000Financing income

Other Interest receivable 8 – –––––––––– –––––––––– –––––––––– ––––––––––

Financing costs

Bank interest payable 42 53 Convertible loan note interest payable 20 23 Other interest payable 6 6 Other finance costs 38 46 –––––––––– ––––––––––

106 128 –––––––––– –––––––––– –––––––––– ––––––––––

5. Employee information

2012 2011 £000 £000

Wages and salaries 2,132 2,091 Social security costs 260 236 Private health costs 34 37 Other pension costs 45 41 Share option charge 7 35 –––––––––– ––––––––––

Staff costs (including directors’ emoluments) 2,478 2,440 –––––––––– –––––––––– –––––––––– ––––––––––

The average monthly number employees comprised:

2012 2011 Number Number

Sales and distribution 32 29 Operations and administration 28 29 –––––––––– ––––––––––

60 58 –––––––––– –––––––––– –––––––––– ––––––––––

6. Directors’ emoluments

Directors’ emoluments are included in the staff costs in note 5. The directors are considered to be the only keymanagement personnel.

Details of directors’ emoluments are included in the Report of the Remuneration Committee on pages 13 and 14. Totaldirectors’ emoluments, excluding employers national insurance contributions, were £395,000 (2011: £399,000), totalpension contributions £11,000 (2011: £11,000) and the highest paid director received emoluments of £133,000(2011: £138,000) and pension contributions of £3,000 (2011: £3,000).

29

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS(continued)

7. Taxation

2012 2011 £000 £000(a) Analysis of charge in period

Current tax:

UK corporation tax on profits for the current year 55 49 Adjustments in respect of prior years – – –––––––––– ––––––––––

Total current tax (note 7b) 55 49Deferred tax (note 13) 6 58 –––––––––– ––––––––––

Tax charge on profit on ordinary activities 61 107 –––––––––– –––––––––– –––––––––– ––––––––––

(b) Factors affecting the tax charge in the period

The tax charge for the period is different to the standard rate of corporation tax in the UK. The rate of corporation taxfor this purpose has been taken as 24% for 2012 (2011: 26%).

The differences are explained below:

2012 2011 £000 £000

Profit on ordinary activities before tax 29 402 –––––––––– ––––––––––

Rate of corporation tax 24% 26%Tax on profit based on standard rate 7 104 Effects of:Research and development allowance (1) (7)Accelerated capital allowances 1 1 Expenses not deductible for tax purposes 15 26 Marginal relief (4) (1)Losses carried forward 45 –Effects of associates (2) –Adjustments relating to change in tax rate – (16) –––––––––– ––––––––––

Total tax charge for the period (note 7a) 61 107 –––––––––– –––––––––– –––––––––– ––––––––––

There are at present no other factors which will influence the Group’s taxation in future years.

8. Earnings per share

The calculation of basic earnings per share is based on the profit after taxation attributable to equity holders of theparent company for the period and the weighted average number of shares in issue during the period.

Diluted earnings per share is calculated by adjusting the weighted average number of shares outstanding by the dilutiveeffect of ordinary shares that the Company may potentially issue relating to its convertible loan notes and its shareoption scheme. The profit for the year is adjusted to add back the tax interest cost on the liability component of theconvertible loan notes. Where the effect of the above adjustments is anti-dilutive they are excluded from the calculationof diluted earnings per share.

30

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS(continued)

The profit for the year and the weighted average number of shares used in the calculation are set out below:

2012 2011 £000 £000

Earnings – profit attributable to equity holders of the parent 13 302 ––––––––––– –––––––––––

Weighted average number of shares 25,941,692 25,627,092 Diluted number of shares 26,861,487 26,131,274 Earnings per share 0.0p 1.2p Diluted earnings per share 0.0p 1.2p

9. Intangible assets

The Group’s intangible assets consist of development costs and goodwill.

The goodwill balance at the beginning of 2012 arose partly on the acquisition of Silver Birch Marketing Limited and Go!Technology Limited in 2003, partly on the acquisition of Hero Electronics Limited in 2006, partly through the acquisitionof Novacom Microwaves Limited and Contech Electronics Limited in 2008 and partly through the acquisition of thebusiness assets and trade of Quo Vadis Limited in 2011. The Company’s goodwill arises on the transfer to theCompany of the net assets of wholly owned subsidiaries and represents the excess of the consideration for the transferover fair value of the assets transferred.

The Directors have undertaken an impairment review of the carrying value of the Group’s goodwill based on the currentand anticipated performance of the businesses concerned. In preparing these projections the Group’s marginal pre taxinterest rate 8% (2011: 8%) has been used as the discount rate. A future growth rate of 5% (2011: 5%) has beenassumed and the calculations are based on future operating cash flows derived using management’s latest 10 yearforecasts. The outcome of the impairment review was subjected to a sensitivity analysis based on the Internal Rate ofReturn of the businesses concerned. The board considers 10 years as an appropriate forecast period given the longterm nature of the businesses invested in.

Development costs represent acquired development expenditure on assets where it is probable that the futureeconomic benefits that are attributable to the asset will flow to the entity; and the cost of the asset can be measuredreliably. Development costs capitalised in the year relate to lighting controls developed for QV Controls Limited andbased on products previously sold by Quo Vadis Limited. Development cost are amortised in administrative expensesover their estimated useful economic lives currently expected to be 4 years.

31

NOTES, FORMING PART OF THE FINANCIAL STATEMENTS(continued)

9. Intangible assets (continued)

The movement in intangible assets during the year arose as follows:

Group Development costs Goodwill Total £000 £000 £000Cost

Balance at 1 September 2010 – 2,580 2,580 Additions through business combinations – 69 69 Eligible development costs capitalised 24 – 24 –––––––––– –––––––––– ––––––––––

Balance at 31 August 2011 24 2,649 2,673 –––––––––– –––––––––– ––––––––––

Balance at 1 September 2011 24 2,649 2,673 Eligible development costs capitalised 5 – 5 –––––––––– –––––––––– ––––––––––

Balance at 31 August 2012 29 2,649 2,678 –––––––––– –––––––––– ––––––––––

Amortisation

Balance at 1 September 2010 – – – –––––––––– –––––––––– ––––––––––

Balance at 31 August 2011 – – – –––––––––– –––––––––– ––––––––––

Balance at 1 September 2011 – – –Charged in year 7 – 7 –––––––––– –––––––––– ––––––––––

Balance at 31 August 2012 7 – 7 –––––––––– –––––––––– ––––––––––

Net book value

as at 31 August 2011 24 2,649 2,673 –––––––––– –––––––––– ––––––––––

as at 31 August 2012 22 2,649 2,671 –––––––––– –––––––––– –––––––––– –––––––––– –––––––––– ––––––––––

Company Goodwill Total £000 £000Cost

Balance at 1 September 2010 2,583 2,583 Additions through business combinations – – –––––––––– ––––––––––

Balance at 31 August 2011 2,583 2,583 –––––––––– ––––––––––

Balance at 1 September 2011 2,583 2,583 –––––––––– ––––––––––

Balance at 31 August 2012 2,583 2,583 –––––––––– ––––––––––

Amortisation

Balance at 1 September 2010 – – –––––––––– ––––––––––

Balance at 31 August 2011 – – –––––––––– ––––––––––