annual report 2016 - marine produce australia report 2016.pdfcompanies for over 30 years. he is the...

TRANSCRIPT

annual report 2016

contents

chairman’s address 3

shareholder listing 4

annual financial report 5

corporate directory 55

chairman’s address Dear Shareholder,

It is with a great sense of accomplishment that we end FY16 and report on what has been another

productive and successful year. We posted a profit of $3.5m for the period – a 50% improvement on our

maiden profit in FY15; and finally, over 4.5 years on from the State Government announcement of the

development of aquaculture zones, we have now secured the majority share of the Kimberley zone and are

fully licenced to produce 15,000 tonnes finfish per annum at our Cone Bay farm.

In line with our projected expansion plans, much of the focus this year has been on increasing the fish

biomass at the farm – almost doubling the value of our stock over last year; and on expanding the farm

infrastructure capacity to support the increased biomass. We have built an additional 12 80m cages this

year, bringing our total to 34 cages - currently holding almost 2,000 tonnes of our iconic Cone Bay Barra.

We have also added a new 10-cage anchoring system at the farm to accommodate the increased cage

numbers, and now have 3 cage systems on our lease.

You will see that our harvest volume was kept relatively low for FY16, and that we only harvested a little

over 600 tonnes. This was a measured approach to ensuring that future increased harvest volumes did not

come at the expense of fish size, and that we can continue to harvest fish over 4kg. We now have a

significant harvestable biomass at the farm and expect to double our annual harvest tonnage this year.

We have invested significantly this year in improved feeding and cage cleaning equipment – and shortly will

be installing our first automated feed barge at the farm. This feed system has been purpose built and will be

used to feed 10-12 cages from a single anchored barge. We have made this investment in automated

equipment sooner than originally planned, and expect it will significantly improve the efficiency and

effectiveness of our feeding.

In November we will be welcoming two new senior members to our Perth team. Hank Poeschl joins us as

General Manager, and will oversee all farming operations and expansion plans. Hank comes with over 25

years of sea cage farming experience from countries across the world. We are also gaining a new Chief

Financial Officer, Helen Chow, who has near 20 years senior financial management experience. We are

greatly looking forward to having both Hank and Helen as integral members of our group.

I would like to make special mention of the continued hard work of all our staff; in particular our Managing

Director Dr Desiree Allen whose persistence, hard work and focus deserve our great thanks. She is joined

in her efforts by the dedicated MPA team both at Cone Bay and in the Perth office – and I extend our

gratitude to each and every one.

This is going to be another very busy but exciting year for MPA and we look forward to reporting sustained

improvements and ongoing expansion plans as the year continues.

Yours faithfully,

Miles Kennedy

3

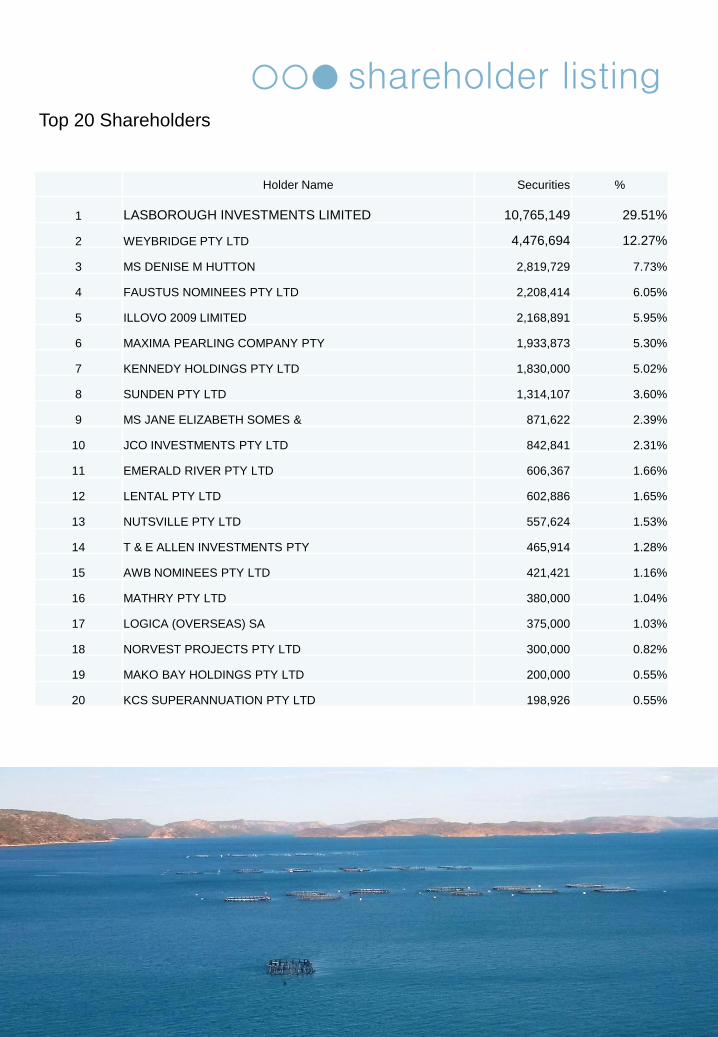

shareholder listing

6

Top 20 Shareholders

Holder Name Securities %

1 LASBOROUGH INVESTMENTS LIMITED 10,765,149 29.51%

2 WEYBRIDGE PTY LTD 4,476,694 12.27%

3 MS DENISE M HUTTON 2,819,729 7.73%

4 FAUSTUS NOMINEES PTY LTD 2,208,414 6.05%

5 ILLOVO 2009 LIMITED 2,168,891 5.95%

6 MAXIMA PEARLING COMPANY PTY 1,933,873 5.30%

7 KENNEDY HOLDINGS PTY LTD 1,830,000 5.02%

8 SUNDEN PTY LTD 1,314,107 3.60%

9 MS JANE ELIZABETH SOMES & 871,622 2.39%

10 JCO INVESTMENTS PTY LTD 842,841 2.31%

11 EMERALD RIVER PTY LTD 606,367 1.66%

12 LENTAL PTY LTD 602,886 1.65%

13 NUTSVILLE PTY LTD 557,624 1.53%

14 T & E ALLEN INVESTMENTS PTY 465,914 1.28%

15 AWB NOMINEES PTY LTD 421,421 1.16%

16 MATHRY PTY LTD 380,000 1.04%

17 LOGICA (OVERSEAS) SA 375,000 1.03%

18 NORVEST PROJECTS PTY LTD 300,000 0.82%

19 MAKO BAY HOLDINGS PTY LTD 200,000 0.55%

20 KCS SUPERANNUATION PTY LTD 198,926 0.55%

Annual Financial Report

Year Ended 30 June 2016

marine produce australia limited

34 Bagot Road Subiaco WA 6008

telephone +61 8 9381 4483 fax +61 8 9381 5817

email [email protected] web marineproduce.com

abn 70 091 805 480

DIRECTORS’ REPORT 1

LEAD AUDITOR’S INDEPENDENCE DECLARATION 10

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

11

CONSOLIDATED STATEMENT OF FINANCIAL POSITION 12

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY 13

CONSOLIDATED STATEMENT OF CASH FLOWS 14

NOTES TO THE FINANCIAL STATEMENTS 15

DIRECTORS’ DECLARATION 45

AUDITOR’S INDEPENDENT AUDIT REPORT 46

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

1 | Page

The directors present their report together with the consolidated financial report of Marine Produce Australia Limited (the Company or MPA), and its subsidiaries (the Group), for the financial year ended 30 June 2016 and the auditor’s report thereon.

1 DIRECTORS

The directors of the Company at any time during or since the end of the financial year are:

Mr Miles Kennedy Chairman Appointed 11 June 2008

Mr Kennedy has held directorships of Australian listed resource companies for over 30 years. He is the non-executive Chairman of Lucapa Diamond Company Limited and was previously the executive Chairman of Sandfire Resources NL, Kimberley Diamond Company NL and RNI NL. Mr Kennedy practised as a Barrister and Solicitor of the Supreme Court of Western Australia and the High Court of Australia and as an Attorney of the Supreme Court of South Africa.

Dr Desiree Allen Managing Director Appointed 5 December 2012

Dr Allen joined MPA in 2011 with a strong background in both genetics (animal breeding) and environmental toxicology. She has a Bachelor of Science from Murdoch University (Australia), a Masters in Environmental Biology from the University of North Carolina (USA), and a PhD in Genetics from Indiana University (USA). Prior to joining MPA she was a Research Fellow at the University of Edinburgh (UK).

Mr Damien Kelly Non-Executive Director Appointed 18 August 2014

Mr Kelly is director of Western Tiger Corporate Advisers, a Perth-based corporate advisory and financial services firm. He has broad corporate and commercial experience spanning over 17 years, providing professional services to ASX and AIM listed companies predominately in the mining and energy sector. Mr Kelly has a MBA, Bachelor of Commerce, a Graduate Diploma in Applied Finance and Investment, full CPA qualifications and is a former officer in the Australian armed services, having graduated from the Royal Military College, Duntroon. He is also a fellow of the Financial Services Institute of Australia (FINSIA) and a member of CPA Australia.

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

2 | Page

2 COMPANY SECRETARY

Mr Mark Clements Company Secretary Appointed 16 February 2015

Mr Clements gained a Bachelor of Commerce degree from the University of Western Australia. He is a Fellow of the Institute of Chartered Accountants and a member of both the Australian Institute of Company Directors and the Institute of Chartered Secretaries in Australia. Mr Clements currently holds the position of Company Secretary of a number of publicly listed companies and has experience in corporate finance, accounting and administration, capital raising and ASX Compliance and regulatory requirements.

3 DIRECTORS’ MEETINGS

The number of directors’ meetings and number of meetings attended by each of the directors of the Company during the financial year are:

Board Meetings Director Attended Held while a

director

Mr M Kennedy 5 5 Dr D Allen 5 5 Mr D Kelly 5 5

4 REMUNERATION REPORT

4.1 Principles of compensation

Remuneration is referred to as compensation throughout this report.

Key management personnel have authority and responsibility for planning, directing and controlling the activities of the Group, including directors of the Company and other executives. Key management personnel comprise the directors of the Company and senior executives for the Group.

Compensation levels for key management personnel and the Company Secretary are competitively set to attract and retain appropriately qualified and experienced directors and executives.

The compensation structures explained below are designed to attract suitably qualified candidates, reward the achievement of strategic objectives, and achieve the broader outcome of creation of value for shareholders. The compensation structures take into account:

the capability and experience of the key management personnel;

the key management personnel’s ability to influence and control performance of the business; and

the Group’s performance including the Group’s earnings, growth in share price and returns on shareholder wealth and amount of incentives within each key management person’s compensation.

Shares and options may only be issued to directors subject to approval by shareholders in general meeting. The Board has no established retirement or redundancy schemes.

Fixed compensation

Fixed compensation consists of base compensation as well as employer contributions to superannuation funds.

Non-executive directors

Total compensation for all non-executive directors is not to exceed $150,000 per annum and is set with reference to fees paid to other non-executive directors of comparable companies. Non-executive directors may receive performance related compensation for particular board approved objectives.

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

3 | Page

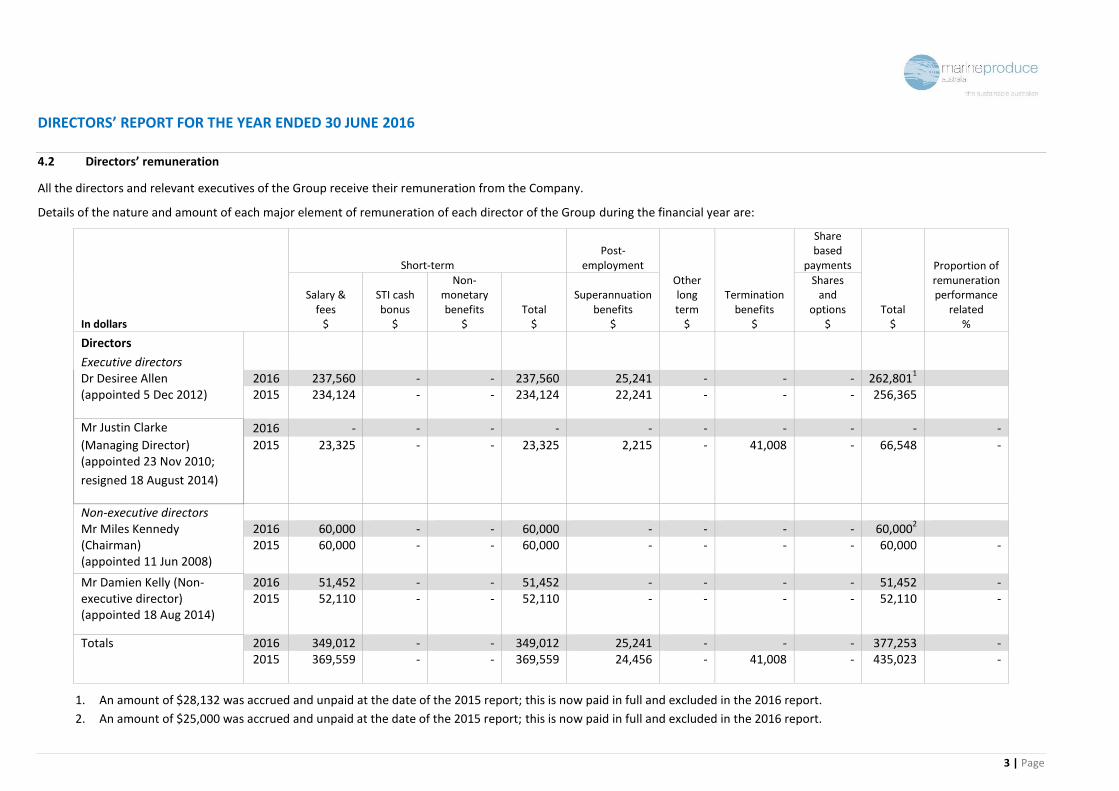

4.2 Directors’ remuneration

All the directors and relevant executives of the Group receive their remuneration from the Company.

Details of the nature and amount of each major element of remuneration of each director of the Group during the financial year are:

In dollars

Short-term Post-

employment

Other long term

$

Termination benefits

$

Share based

payments

Total $

Proportion of remuneration performance

related %

Salary & fees

$

STI cash bonus

$

Non-monetary benefits

$ Total

$

Superannuation benefits

$

Shares and

options $

Directors

Executive directors Dr Desiree Allen (appointed 5 Dec 2012)

2016 237,560 - - 237,560 25,241 - - - 262,8011

2015

234,124

-

-

234,124

22,241

-

-

-

256,365

Mr Justin Clarke 2016 - - - - - - - - - -

(Managing Director) 2015 23,325 - - 23,325 2,215 - 41,008 - 66,548 - (appointed 23 Nov 2010;

resigned 18 August 2014)

Non-executive directors Mr Miles Kennedy (Chairman)

2016 60,000 - - 60,000 - - - - 60,0002

2015 60,000 - - 60,000 - - - - 60,000 - (appointed 11 Jun 2008)

Mr Damien Kelly (Non-executive director)

2016 51,452 - - 51,452 - - - - 51,452 - 2015 52,110 - - 52,110 - - - - 52,110 -

(appointed 18 Aug 2014)

Totals 2016 349,012 - - 349,012 25,241 - - - 377,253 - 2015

369,559

-

-

369,559

24,456

-

41,008

-

435,023

-

1. An amount of $28,132 was accrued and unpaid at the date of the 2015 report; this is now paid in full and excluded in the 2016 report.

2. An amount of $25,000 was accrued and unpaid at the date of the 2015 report; this is now paid in full and excluded in the 2016 report.

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

4 | Page

In dollars

Short-term Post-

employment

Other long term

$

Termination benefits

$

Share based

payments

Total $

Proportion of remuneration performance

related %

Value of options as

proportion of remuneration

%

Salary & fees

$

STI cash bonus

$

Non-monetary benefits

$ Total

$

Superannuation benefits

$

Shares and

options $

Executives

Mark Clements (Company 2016 36,000 - - 36,000 - - - - 36,000 - - Secretary) 2015 13,500 - - 13,500 - - - - 13,500 - - (appointed 16 February 2015)

Tamar Kennedy (Company 2016 - - - - - - - - - - - Secretary) (appointed 3 June 2013, resigned 16 February 2015)

2015 20,061 - - 20,061 1,801 - - - 21,862 - -

Totals 2016 36,000 - - 36,000 - - - - 36,000 - - 2015 33,561 - - 33,561 1,801 - - - 35,362 - -

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

5 | Page

4.3 Equity instruments

(i) Options and rights over equity instruments granted as compensation

On 23 November 2015, 2,200,000 unlisted $0.75 options expiring 30 November 2018 were issued to the Directors following shareholder approval at the Company’s Annual General meeting held 23 November 2015.

(ii) Exercise of options granted as compensation

No options were exercised during the reporting period or the prior period. No options lapsed in the current or prior period.

5 PRINCIPAL ACTIVITIES

This past year has been one of ongoing progress and development for MPA. We continue to focus on our production expansion plans, with improved equipment, greater fish inputs, key staff appointments, and continued development of workplace health and safety and staff training.

(i) OPERATING REVIEW

- Applied for, and were granted, a new Department of Fisheries Licence that allows the production of up to 15,000 tonnes finfish per annum. This approval includes additional 644 hectares of lease area adjacent to our existing 699 hectare water lease.

- Strengthened our farm management team with the promotion of Alasdair Connor to co-Manager of Marine Farming, and Nick Brearley to Innovator Skipper (Master IV).

- Expanded our farming capacity with the addition of new infrastructure, including:

o New 10-cage capacity anchoring system (now have 3 anchoring systems on our lease)

o 12 additional 80m cages (now have 34 cages in total).

- Improved our cage cleaning options with two new pressure washers and disk-drive cleaners

- Commissioned our first automated feed delivery system (feed barge), and updated our feed delivery equipment on existing boats

- Ongoing research into: feeding behaviour for optimal feed conversion and growth; cage materials for stock security; nursery conditions and fingerling genetics for improved production; and environmental conditions for optimising growth.

- Streamlined the cage building process in Derby with the continued assistance of the Derby Shire (with special thanks to all involved).

- Filed a trademark application for “Cone Bay” in relation to fish production – to ensure our iconic name, as we are known throughout Australia, is secured, and the value of that brand retained for our shareholders.

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

6 | Page

(ii) REVIEW OF FINANCIAL RESULTS

Results from Operating Activities and Loss for the Period

The Group’s profit for the period was $3,530,000 (2015: $2,401,701). There was no impairment of property, plant and equipment or intangible assets in the year (2015: $516,787) and depreciation and amortisation was $398,106 (2015: $169,589).

Net cash provided by operating activities was ($2,659,141) (2015: $246,376).

The results from operating activities (excluding impairment and depreciation) included:

12 months

ended June 2016

12 months ended

June 2015 Profit / (loss) from farming operations (excluding impairment and depreciation) 1,368,297 (502,494) Administration and marketing expenses (1,857,847) (2,715,726) Other income 76,120 4,085 Other expense - -

Results from operating activities excluding impairment and depreciation (413,430) (3,214,135)

Impairment and depreciation (398,106) (686,376)

Loss before tax (811,536) (3,900,511)

Non IFRS unaudited

12 months

ended June 2016

12 months ended

June 2015 Farm cash operating costs (AUD) 13,154,499 10,719,168 Fish biomass growth before harvest (kg) 1,410,329 969,523

Farm cash operating cost per kg 9.33 11.06

Revenue

Revenue from sales

Revenue from the sale of fish was $7,253,391 for the period from the sale of 638,805kg. A total of 641,078kg of fish was harvested for the period. As part of the production planning, the harvest volume was intentionally kept low for part of the year so as to ensure we are able to attain the preferred size of our harvestable fish.

(iii) REVIEW OF FINANCIAL CONDITION

At 30 June 2016, the Group had a working capital surplus of $19,741,261 represented significantly by biological assets of $16,141,615 and cash and cash equivalents of $1,473,322.

The Group’s working capital will be utilised to fund operating and capital expenditure to continue to develop the Cone Bay farm site and increase profitability with scale.

The Group has the ability to slow its expansion strategy and/or harvest fish at less than the targeted harvest size to maintain sufficient cash reserves, with a resulting delay in the growth of the scale of the operations. The Group also has the ability, and is planning, to raise new equity or debt capital and to seek research and development tax refunds as it has in prior years.

The financial statements have been prepared on a going concern basis which the directors believe to be appropriate. The directors are confident that the Group will maintain sufficient levels of working capital to continue as a going concern and continue to pay its debts as and when they fall due.

If the Group is unable to continue as a going concern, it will be required to realise its assets and extinguish its liabilities other than in the ordinary course of business and at amounts that may be different to those stated in the financial statements.

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

7 | Page

(iv) SIGNIFICANT CHANGES IN THE STATE OF AFFAIRS

In the interval between the end of the financial year and the date of this report, there has not been any item, transaction or effect of a material or unusual nature likely, in the opinion of the directors of the Company, to affect significantly the operations of the Group, the results of those operations, or the state of affairs of the Group, in future financial years.

6 DIVIDENDS

No dividends were paid or declared during the current or prior financial years.

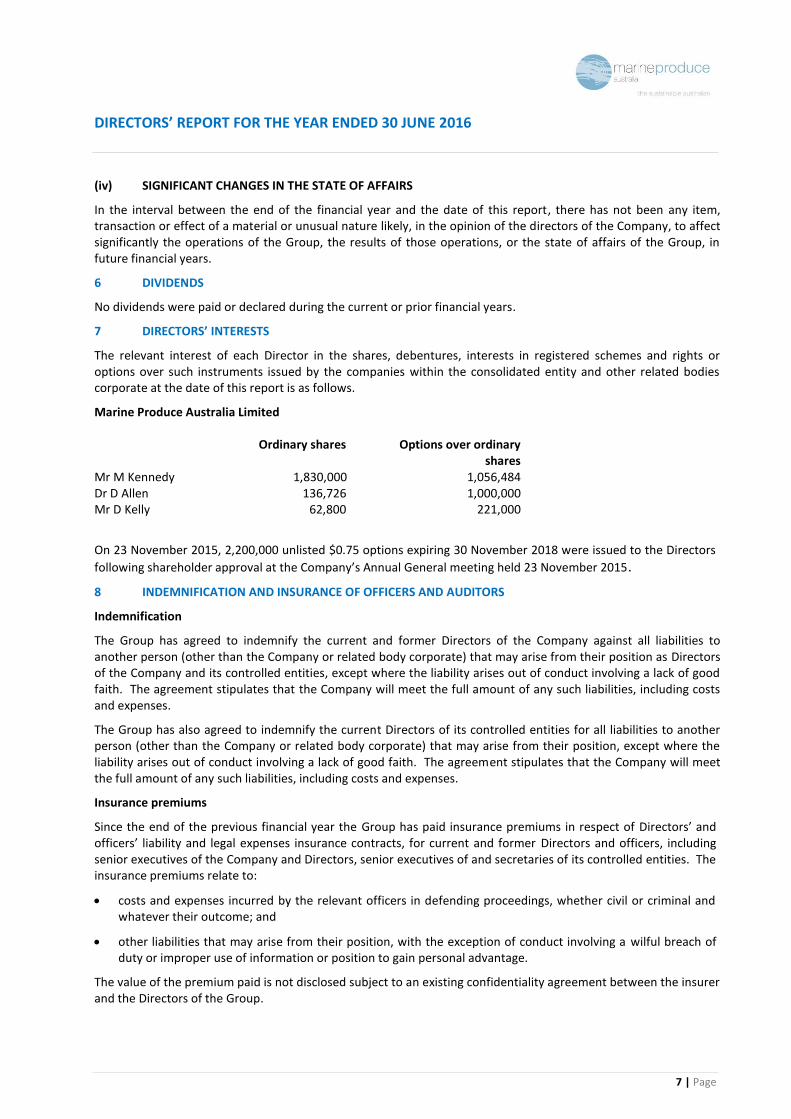

7 DIRECTORS’ INTERESTS

The relevant interest of each Director in the shares, debentures, interests in registered schemes and rights or options over such instruments issued by the companies within the consolidated entity and other related bodies corporate at the date of this report is as follows.

Marine Produce Australia Limited

Ordinary shares Options over ordinary shares

Mr M Kennedy 1,830,000 1,056,484 Dr D Allen 136,726 1,000,000 Mr D Kelly 62,800 221,000

On 23 November 2015, 2,200,000 unlisted $0.75 options expiring 30 November 2018 were issued to the Directors

following shareholder approval at the Company’s Annual General meeting held 23 November 2015.

8 INDEMNIFICATION AND INSURANCE OF OFFICERS AND AUDITORS

Indemnification

The Group has agreed to indemnify the current and former Directors of the Company against all liabilities to another person (other than the Company or related body corporate) that may arise from their position as Directors of the Company and its controlled entities, except where the liability arises out of conduct involving a lack of good faith. The agreement stipulates that the Company will meet the full amount of any such liabilities, including costs and expenses.

The Group has also agreed to indemnify the current Directors of its controlled entities for all liabilities to another person (other than the Company or related body corporate) that may arise from their position, except where the liability arises out of conduct involving a lack of good faith. The agreement stipulates that the Company will meet the full amount of any such liabilities, including costs and expenses.

Insurance premiums

Since the end of the previous financial year the Group has paid insurance premiums in respect of Directors’ and officers’ liability and legal expenses insurance contracts, for current and former Directors and officers, including senior executives of the Company and Directors, senior executives of and secretaries of its controlled entities. The insurance premiums relate to:

costs and expenses incurred by the relevant officers in defending proceedings, whether civil or criminal and whatever their outcome; and

other liabilities that may arise from their position, with the exception of conduct involving a wilful breach of duty or improper use of information or position to gain personal advantage.

The value of the premium paid is not disclosed subject to an existing confidentiality agreement between the insurer and the Directors of the Group.

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

8 | Page

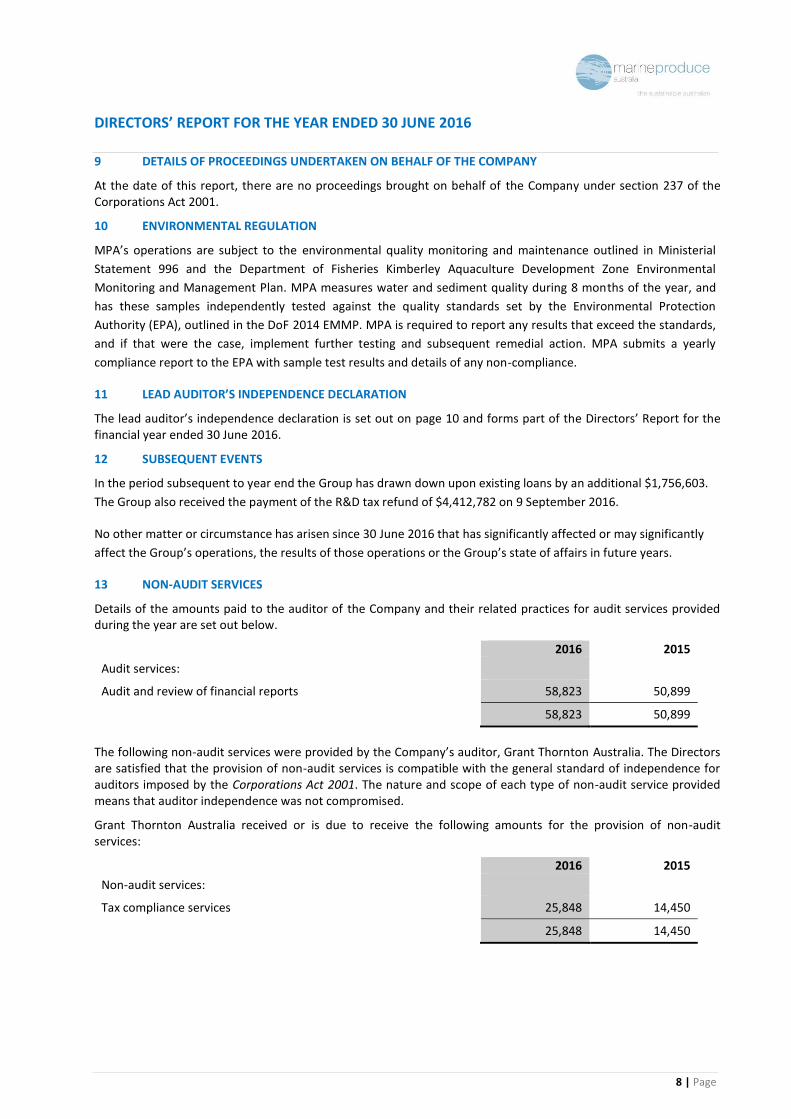

9 DETAILS OF PROCEEDINGS UNDERTAKEN ON BEHALF OF THE COMPANY

At the date of this report, there are no proceedings brought on behalf of the Company under section 237 of the Corporations Act 2001.

10 ENVIRONMENTAL REGULATION

MPA’s operations are subject to the environmental quality monitoring and maintenance outlined in Ministerial

Statement 996 and the Department of Fisheries Kimberley Aquaculture Development Zone Environmental

Monitoring and Management Plan. MPA measures water and sediment quality during 8 months of the year, and

has these samples independently tested against the quality standards set by the Environmental Protection

Authority (EPA), outlined in the DoF 2014 EMMP. MPA is required to report any results that exceed the standards,

and if that were the case, implement further testing and subsequent remedial action. MPA submits a yearly

compliance report to the EPA with sample test results and details of any non-compliance.

11 LEAD AUDITOR’S INDEPENDENCE DECLARATION

The lead auditor’s independence declaration is set out on page 10 and forms part of the Directors’ Report for the financial year ended 30 June 2016.

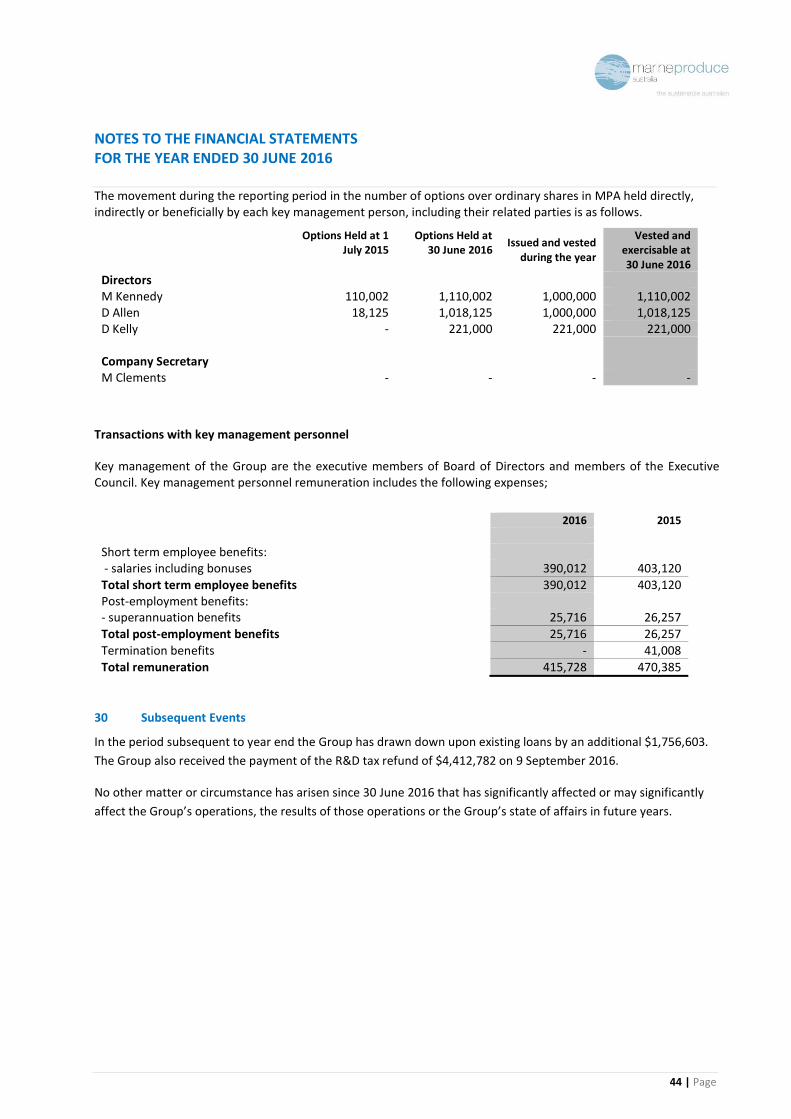

12 SUBSEQUENT EVENTS

In the period subsequent to year end the Group has drawn down upon existing loans by an additional $1,756,603.

The Group also received the payment of the R&D tax refund of $4,412,782 on 9 September 2016.

No other matter or circumstance has arisen since 30 June 2016 that has significantly affected or may significantly

affect the Group’s operations, the results of those operations or the Group’s state of affairs in future years.

13 NON-AUDIT SERVICES

Details of the amounts paid to the auditor of the Company and their related practices for audit services provided during the year are set out below.

2016 2015

Audit services:

Audit and review of financial reports 58,823 50,899

58,823 50,899

The following non-audit services were provided by the Company’s auditor, Grant Thornton Australia. The Directors are satisfied that the provision of non-audit services is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001. The nature and scope of each type of non-audit service provided means that auditor independence was not compromised.

Grant Thornton Australia received or is due to receive the following amounts for the provision of non-audit services:

2016 2015

Non-audit services:

Tax compliance services 25,848 14,450

25,848 14,450

DIRECTORS’ REPORT FOR THE YEAR ENDED 30 JUNE 2016

9 | Page

Signed in accordance with a resolution of the Directors.

DESIREE ALLEN MANAGING DIRECTOR Dated at Subiaco 29

th September 2016.

Level 1

10 Kings Park Road

West Perth WA 6005

Correspondence to:

PO Box 570

West Perth WA 6872

T +61 8 9480 2000

F +61 8 9322 7787

W www.grantthornton.com.au

Grant Thornton Audit Pty Ltd ACN 130 913 594 a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389

‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the

context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm

is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and

are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its

Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited.

Liability limited by a scheme approved under Professional Standards Legislation. Liability is limited in those States where a current scheme applies.

Auditor’s Independence Declaration

To the Directors of Marine Produce Australia Limited

In accordance with the requirements of section 307C of the Corporations Act 2001, as lead

auditor for the audit of Marine Produce Australia Limited for the year ended 30 June 2016, I

declare that, to the best of my knowledge and belief, there have been:

a no contraventions of the auditor independence requirements of the Corporations Act

2001 in relation to the audit; and

b no contraventions of any applicable code of professional conduct in relation to the

audit.

GRANT THORNTON AUDIT PTY LTD Chartered Accountants

M A Petricevic

Partner - Audit & Assurance

Perth, 29 September 2016

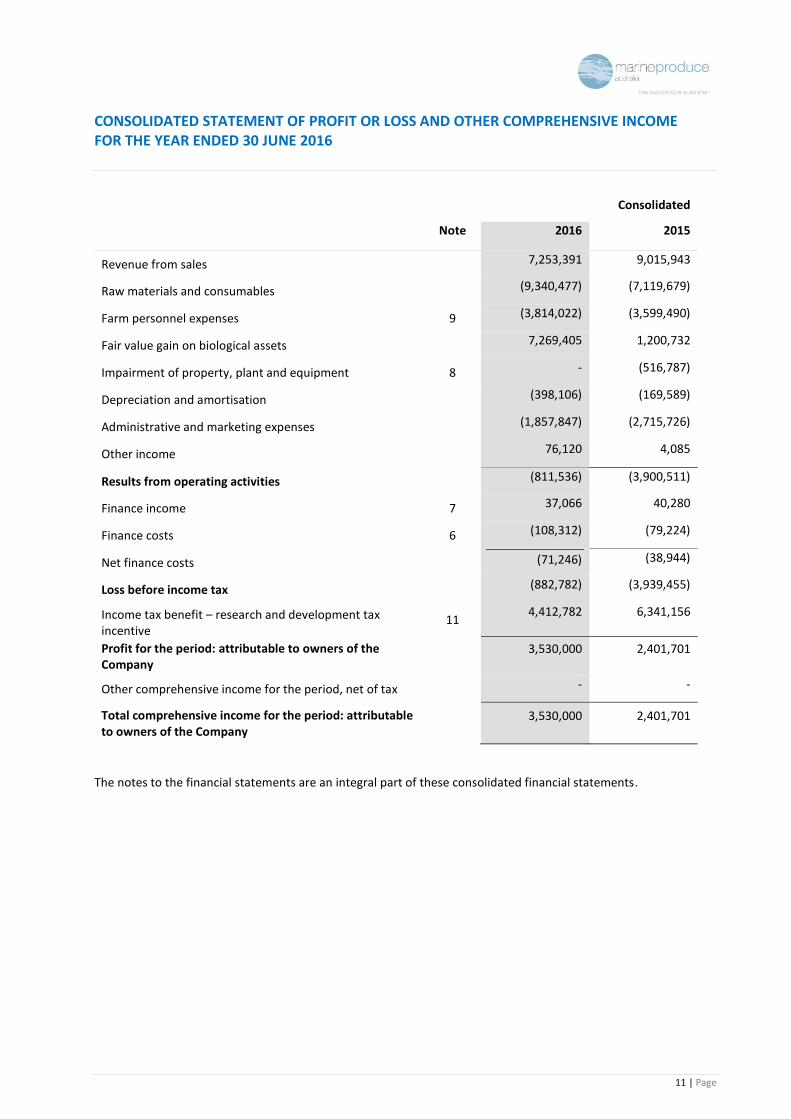

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME FOR THE YEAR ENDED 30 JUNE 2016

11 | Page

Consolidated

Note 2016 2015

Revenue from sales 7,253,391

9,015,943

Raw materials and consumables (9,340,477)

(7,119,679)

Farm personnel expenses 9 (3,814,022)

(3,599,490)

Fair value gain on biological assets 7,269,405

1,200,732

Impairment of property, plant and equipment 8 -

-

-

(516,787)

-

-

Depreciation and amortisation (398,106)

(169,589)

Administrative and marketing expenses (1,857,847)

(2,715,726)

Other income 76,120

4,085

Results from operating activities (811,536)

(3,900,511)

Finance income 7 37,066

40,280

Finance costs 6 (108,312)

(79,224)

Net finance costs (71,246)

-879,412

(38,944)

-879,412

Loss before income tax (882,782)

(3,939,455)

Income tax benefit – research and development tax incentive

11 4,412,782

3,533,370

6,341,156

3,533,370

Profit for the period: attributable to owners of the Company

3,530,000 2,401,701

Other comprehensive income for the period, net of tax -

-

Total comprehensive income for the period: attributable to owners of the Company

3,530,000 2,401,701

The notes to the financial statements are an integral part of these consolidated financial statements.

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2016

12 | Page

Consolidated

Note 2016 2015

Assets

Cash and cash equivalents 12 1,473,322

2,063,069

Trade and other receivables 13 5,688,011

760,308

4,837,960

Inventories 14 760,308

441,489

Biological assets 15 16,141,615

8,658,598

Total current assets 24,063,256

16,001,116

Property, plant and equipment 8/17 4,949,139

2,914,323

Other assets 94,737 91,380

Biological assets 15 70,716

284,329

Total non-current assets 5,114,592

3,290,032

Total assets 29,177,848

19,291,148

Liabilities

Trade and other payables 20 3,509,439

471,702

2,066,503

471,702

Loans and borrowings 21 471,702

1,164,310

Employee benefits 22 340,854

226,331

Total current liabilities 4,321,995

3,457,144

Loans and borrowings 21 1,182,965

691,359

Provision for restoration 19 119,586

110,384

Employee benefits 22 60,230 -

Total non-current liabilities 1,362,781

801,743

Total liabilities 5,684,776

4,258,887

Net assets 23,493,072

15,032,261

Equity

Share capital 23 60,505,645

55,699,560

Reserves 124,726

-

Accumulated losses (37,137,299)

(40,667,299)

Total equity 23,493,072

15,032,261

The notes to the financial statements are an integral part of these consolidated financial statements.

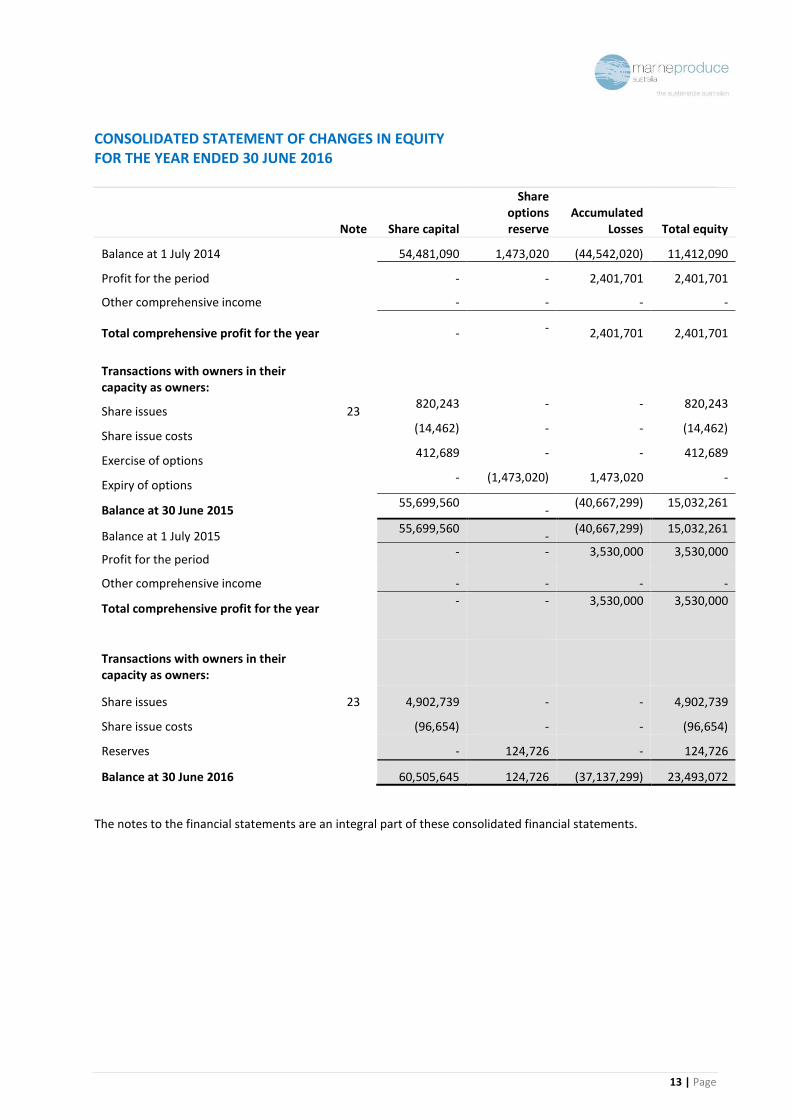

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 30 JUNE 2016

13 | Page

Note Share capital

Share options reserve

Accumulated Losses Total equity

Balance at 1 July 2014 54,481,090 1,473,020 (44,542,020) 11,412,090

Profit for the period - - 2,401,701 2,401,701

Other comprehensive income - - - -

Total comprehensive profit for the year - - 2,401,701 2,401,701

Transactions with owners in their capacity as owners:

Share issues 23 820,243

- - 820,243

Share issue costs (14,462)

- - (14,462)

Exercise of options 412,689

- - 412,689

Expiry of options - (1,473,020)

1,473,020

-

Balance at 30 June 2015 55,699,560

- (40,667,299)

15,032,261

Balance at 1 July 2015 55,699,560

- (40,667,299)

15,032,261

Profit for the period - - 3,530,000

3,530,000

Other comprehensive income - - - -

Total comprehensive profit for the year - - 3,530,000

3,530,000

Transactions with owners in their capacity as owners:

Share issues 23 4,902,739 - - 4,902,739

Share issue costs (96,654) - - (96,654)

Reserves - 124,726 - 124,726

Balance at 30 June 2016 60,505,645 124,726 (37,137,299) 23,493,072

The notes to the financial statements are an integral part of these consolidated financial statements.

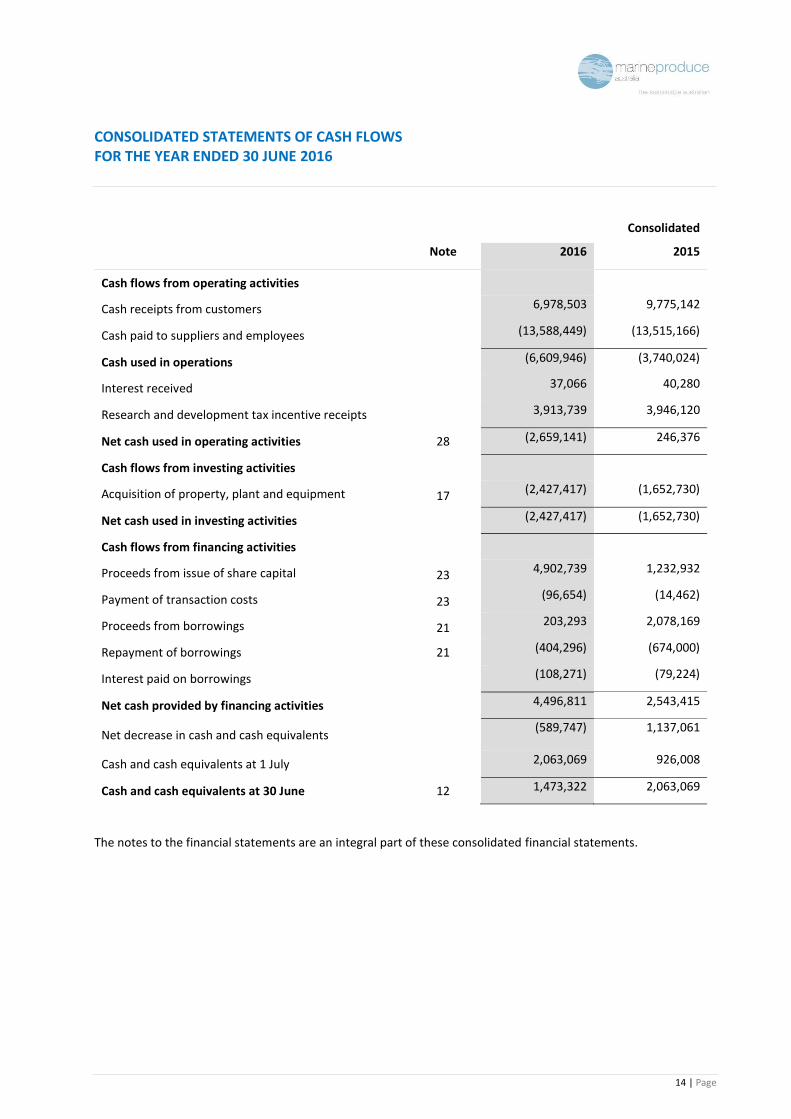

CONSOLIDATED STATEMENTS OF CASH FLOWS FOR THE YEAR ENDED 30 JUNE 2016

14 | Page

Consolidated

Note 2016 2015

Cash flows from operating activities

Cash receipts from customers 6,978,503

9,775,142

Cash paid to suppliers and employees (13,588,449)

(13,515,166)

Cash used in operations (6,609,946)

(3,740,024)

Interest received 37,066

40,280

Research and development tax incentive receipts 3,913,739

3,946,120

Net cash used in operating activities 28 (2,659,141)

246,376

Cash flows from investing activities

Acquisition of property, plant and equipment 17 (2,427,417)

(1,652,730)

Net cash used in investing activities (2,427,417)

(1,652,730)

Cash flows from financing activities

Proceeds from issue of share capital 23 4,902,739

-96,654

1,232,932

-96,654

Payment of transaction costs 23 (96,654)

(14,462)

Proceeds from borrowings 21 203,293

2,078,169

Repayment of borrowings 21 (404,296)

(674,000)

Interest paid on borrowings (108,271)

(79,224)

Net cash provided by financing activities 4,496,811

2,543,415

Net decrease in cash and cash equivalents (589,747) 1,137,061

Cash and cash equivalents at 1 July 2,063,069

926,008

Cash and cash equivalents at 30 June 12 1,473,322

2,063,069

The notes to the financial statements are an integral part of these consolidated financial statements.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

15 | Page

1 Reporting entity

Marine Produce Australia Limited (the Company) is a company domiciled in Australia. The address of the Company’s registered office is 34 Bagot Road, Subiaco WA 6008. The consolidated financial statements of the Group as at and for the year ended 30 June 2016 comprise the Company and its subsidiaries (together referred to as the ‘Group’ and individually as ‘Group entities’).

The Group is a for-profit entity involved in the seafood and aquaculture industry, specifically including the farming of fin fish (Barramundi) in sea cages.

2 Basis of preparation

(a) Statement of compliance

The financial report is a general purpose financial report which has been prepared in accordance with Australian Accounting Standards (AASBs) (including Australian Interpretations) adopted by the Australian Accounting Standards Board (AASB) and the Corporations Act 2001 (Cth). The consolidated financial report of the Group complies with International Financial Reporting Standards (IFRSs) and interpretations adopted by the International Accounting Standards Board (IASB).

The consolidated financial statements were approved and authorised for issue by the Board of Directors on 29th September 2016.

(b) Basis of measurement

The consolidated financial statements have been prepared on the historical cost basis except for the following material items in the statement of financial position:

biological assets are measured at fair value less costs to sell;

property plant and equipment are measured at cost less accumulated depreciation and accumulated impairment losses; and

share based payments are measured at fair value of services provided.

The methods used to determine fair values are discussed further in Note 3 (m).

(c) Functional and presentation currency

These consolidated financial statements are presented in Australian Dollars, which is the Group’s functional currency.

(d) Use of estimates and judgements

The preparation of financial statements in conformity with IFRS requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from those estimates.

Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimates are revised and in any future periods affected.

Information about critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the financial statements is included in the following notes:

Note 8 - Impairment of property, plant and equipment and intangible assets

Note 15 - Biological assets

Note 23 - Share Capital

Note 3(b) - Depreciation methods and rates

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

16 | Page

(e) Going concern

The financial statements have been prepared on a going concern basis which the Directors believe to be

appropriate. The Directors are confident that the Group will be able to maintain sufficient levels of working capital

to continue as a going concern and continue to pay its debts as and when they fall due.

For the period ended 30 June 2016, the Group made a profit of $3,530,000 (2015: $2,401,701). At 30 June 2016,

the Group had a working capital surplus of $19,741,261 represented significantly by biological assets of

$16,141,615 and cash and cash equivalents of $1,473,322.

The Directors are confident that the Group can continue as a going concern and as such are of the opinion that the

financial report has been appropriately prepared on a going concern basis.

The Group’s 2017 cash flow forecast assumes an increase in the working capital spending required to support its

ongoing expansion plans. These increased costs specifically include feeding and growing the fish biomass to sustain

increasing harvest volumes. This ongoing expansion is expected to be funded by sales of fish, further research and

development tax refunds, and some equity and/or debt investment. During 2016 the Group also secured an

additional rolling capital expenditure loan from National Australia Bank.

Key risks associated with Barramundi farming and the ability to successfully grow and harvest fish for sale are

discussed in Note 15.

The directors believe that it is appropriate to prepare the financial statements using the going concern basis as the

Group has the ability to slow its expansion strategy and/or harvest fish at less than the targeted harvest size to

maintain sufficient cash reserves, with a resulting delay in the growth of the scale of the operations. In any case,

the Group is planning to raise new equity or debt capital.

Should the Group be unable to undertake the initiatives disclosed above, there is uncertainty which may cast

doubt as to whether or not the Group will be able to continue as a going concern and whether it will realise its

assets and extinguish its liabilities in the normal course of business and at the amounts stated in the financial

statements.

The financial statements do not include any adjustments relating to the recoverability and classification of

recorded asset amounts nor to the amounts and classification of liabilities that might be necessary should the

Group not continue as a going concern.

3 Significant accounting policies

The accounting policies set out below have been applied consistently to all periods presented in these consolidated financial statements, and have been applied consistently by Group entities.

(a) Basis of consolidation

Subsidiaries

Subsidiaries are entities controlled by the Group. During the reporting period the Company had a 100% interest in the following subsidiaries:

MPA Fish Farms Pty Ltd; MPA Marketing Pty Ltd;

The financial statements of subsidiaries are included in the consolidated financial statements from the date that control commences until the date that control ceases. The accounting policies of subsidiaries have been changed when necessary to align them with the policies adopted by the Group.

In the Company’s financial statements, investments in subsidiaries are carried at cost.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

17 | Page

Transactions eliminated on consolidation

Intra-group balances and transactions, and any unrealised income and expenses arising from intra-group transactions, are eliminated in preparing the consolidated financial statements.

(b) Property, plant and equipment

Recognition and measurement

Items of property, plant and equipment are measured at cost less accumulated depreciation and accumulated impairment losses.

Cost includes expenditure that is directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials; direct labour;; and, an appropriate proportion of production overheads.

When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment.

Gains and losses on disposal of an item of property, plant and equipment are determined by comparing the proceeds from disposal with the carrying amount of property, plant and equipment and are recognised net within other income in profit or loss.

Subsequent costs

Subsequent expenditure is capitalised only when it is probable that the future economic benefits associated with the expenditure will flow to the Group. Ongoing repairs and maintenance is expensed as incurred.

Depreciation

Depreciation is calculated over the depreciable amount, which is the cost of an asset, or other amount substituted for cost, less its residual value.

Depreciation is recognised in profit or loss on an adjusted reducing balance basis over the estimated useful lives of each part of an item of property, plant and equipment, since this most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset.

The estimated useful lives for the current and comparative periods are as follows:

Plant and equipment 5 – 15 years Fixtures and fittings 5 – 10 years Major components 3 – 5 years Boats 15 years Depreciation methods, useful lives and residual values are reviewed at each financial year end and adjusted if appropriate.

(c) Intangible assets

Research and development

Expenditure on research activities, undertaken with the prospect of gaining new scientific or technical knowledge and understanding, is recognised in the profit or loss as incurred.

Development activities involve a plan or design for the production of new or substantially improved products and processes. Development expenditure is capitalised only if development costs can be measured reliably, the product or process is technically and commercially feasible, future economic benefits are probable, and the Group intends to and has sufficient resources to complete development and to use or sell the asset. The expenditure capitalised includes the cost of materials, direct labour and overhead costs that are directly attributable to preparing the asset for its intended use. Other development expenditure is recognised in profit or loss as incurred. Capitalised development expenditure is stated at cost less accumulated amortisation and accumulated impairment losses.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

18 | Page

Subsequent costs

Subsequent expenditure is capitalised only when it increases the future economic benefits embodied in the specific asset to which it relates. All other expenditure is recognised in profit or loss as incurred.

Amortisation

Amortisation is calculated over the costs of the asset, less its residual value.

Amortisation is recognised in profit or loss on a straight-line basis over the estimated useful lives of intangible assets from the date that they are available for use, since this most closely reflects the expected pattern of consumption of the future economic benefits embodied in the asset. The estimated useful lives for the current and comparative periods is 10 years.

Amortisation methods, useful lives and residual values are reviewed at each financial year end and adjusted if appropriate.

(d) Biological assets

Biological assets (fish 400 grams and larger) are measured at fair value less costs to sell, with any change therein recognised in profit or loss. Fair value is determined based on average market sales price. Costs to sell include all costs that are necessary to sell the assets, including costs necessary to get the assets to market.

As the fair value of the assets is based on its present location and condition, the Group applies direct costing to estimate fair value of fish in cages where they have not yet reached a saleable size:

Fish up to 400 grams are measured at cost plus direct feed cost and direct fish management costs.

(e) Inventories

Inventories are measured at the lower of cost and net realisable value. Net realisable value is the estimated selling price in the ordinary course of business, less the estimated costs of completion and costs to sell.

The cost attributed to harvested fish is equal to the fair value less estimated selling costs previously recorded in biological assets at the date of harvest, determined in accordance with the accounting policy for biological assets. Any change in value at the date of harvest is recognised in the income statement. Once harvested, fish inventories are accounted for as normal inventories.

The cost of other inventories is based on the first-in first-out principle and includes expenditure incurred in acquiring the inventories and bringing them to their existing location and condition. Cost includes an appropriate share of overheads based on normal operating capacity.

(f) Impairment

Non-derivative financial assets (including receivables)

The carrying amounts of the Group’s non-derivative financial assets, other than biological assets (see accounting policy (d)), inventories (see accounting policy (e)) and deferred tax assets (see accounting policy (k)) are reviewed at each balance sheet date to determine whether there is any indication of impairment. If any such indication exists, the asset’s recoverable amount is estimated.

For intangible assets that are not yet available for use, the recoverable amount is estimated at each balance sheet date.

An impairment loss is recognised whenever the carrying amount of an asset or its cash-generating unit exceeds its recoverable amount. Impairment losses are recognised in the income statement, unless an asset has previously been revalued, in which case the impairment loss is recognised as a reversal to the extent of that previous revaluation with any excess recognised through profit or loss.

Impairment losses recognised in respect of cash-generating units are allocated first to reduce the carrying amount of any goodwill allocated to cash-generating units (group of units) and then, to reduce the carrying amount of the other assets in the unit (group of units) on a pro rata basis (except for individual assets or groups of assets have been valued separately).

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

19 | Page

Calculation of recoverable amount

The recoverable amount of the Group’s investments and receivables carried at amortised cost is calculated as the present value of estimated future cash flows, discounted at the original effective interest rate (i.e. the effective interest rate computed at initial recognition of these financial assets). Receivables with a short duration are not discounted.

Impairment of receivables is not recognised until objective evidence is available that a loss event has occurred. Significant receivables are individually assessed for impairment. Impairment testing of receivables that are not impaired individually is performed by placing them into portfolios of receivables with similar risk profiles and undertaking a collective assessment of impairment. Non-significant receivables are not individually assessed. Instead, impairment testing is performed by placing non-significant receivables in portfolios of similar risk profiles based on objective evidence from historical experience adjusted to for any effects of conditions existing at each balance sheet date.

Non-financial assets

The carrying amounts of the Group’s non-financial assets, other than biological assets, investment property, inventories and deferred tax assets, are reviewed at each reporting date to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. Goodwill and indefinite life intangible assets are tested annually for impairment. An impairment loss is recognised if the carrying amount of an asset or its related cash-generating unit (CGU) exceeds its recoverable amount.

The recoverable amount of an asset or CGU is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. For the purpose of impairment testing, assets that cannot be tested individually are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or CGUs. Subject to an operating segment ceiling test, CGUs to which goodwill has been allocated are aggregated so that the level at which impairment is tested reflects the lowest level at which goodwill is monitored for internal reporting purposes. Goodwill acquired in a business combination is allocated to groups of CGUs that are expected to benefit from the synergies of the combination.

Impairment losses are recognised in profit or loss. Impairment losses recognised in respect of CGUs are allocated first to reduce the carrying amount of any goodwill allocated to the CGU (or group of CGUs), and then to reduce the carrying amounts of the other assets in the CGU (or group of CGUs) on a pro rata basis (except for individual assets or groups of assets have been valued separately).

An impairment loss in respect of goodwill is not reversed. For other assets, an impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortisation, if no impairment loss had been recognised.

(g) Employee benefits

Defined contribution plans

A defined contribution plan is a post-employment benefit plan under which an entity pays fixed contributions into a separate entity and will have no legal or constructive obligation to pay further amounts. Obligations for contributions to defined contribution superannuation funds are recognised as an employee benefit expense in profit or loss in the periods during which services are rendered by employees.

Short-term benefits

Liabilities for employee benefits for wages, salaries and annual leave that are expected to be settled within 12 months of the reporting date represent present obligations resulting from employees’ services provided to reporting date, are calculated at undiscounted amounts based on remuneration wage and salary rates that the Group expects to pay as at the reporting date including related on-costs, such as workers compensation, insurance and payroll tax. Non-monetary benefits, such as medical care, housing, cars and free or subsidised goods and services, are expensed based on the net marginal cost to the Group as the benefits are taken by the employees.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

20 | Page

Termination benefits

Termination benefits are recognised as an expense when the Group is demonstrably committed, without realistic possibility of withdrawal, to a formal detailed plan to terminate employment before the normal retirement date. Termination benefits for voluntary redundancies are recognised if the Group has made an offer encouraging voluntary redundancy, it is probable that the offer will be accepted, and the number of acceptances can be estimated reliably.

(h) Provisions

A provision is recognised in the Statement of Financial Position when the Group has a present legal or constructive obligation as a result of a past event, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability.

(i) Revenue

Sale of goods

Revenue from the sale of goods is recognised in profit or loss when persuasive evidence exists that the significant risks and rewards of ownership have been transferred to the buyer. No revenue is recognised if there are significant uncertainties regarding recovery of the consideration due, the costs incurred or to be incurred cannot be measured reliably, there is a risk of return of goods or there is continuing management involvement with the goods.

Transfers of risks and rewards vary depending on the individual terms of the contract of sale. For sales of Barramundi, transfer usually occurs when the product is received by the customer.

Gain from change in fair value of biological assets

Biological assets relating to aquaculture activities and products are stated at fair value less estimated point-of-sale costs, with any resultant gain or loss recognised in the income statement. Point-of-sale costs include all costs that would be necessary to sell the assets, including costs necessary to get the assets to market.

As the fair value of the assets is based on its present location and condition, the Company applies direct costing to estimate fair value of Barramundi in cages where they have not yet reached a saleable size of 400 grams.

(j) Expenses

Financing income and expenses

Financing costs comprise interest payable on borrowings (calculated using the effective interest method), facilities and interest receivable on funds invested that are recognised in the income statement. Borrowing costs are expensed as incurred and included in financing costs.

Interest income is recognised in the income statement as it accrues, using the effective interest method.

(k) Income tax

Income tax on profit or loss for the year comprises current and deferred tax. Income tax is recognised in the income statement except to the extent that it relates to items recognised directly in equity, in which case it is recognised in equity.

Current tax is the expected tax payable on the taxable income for the year, using tax rates enacted or substantively enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

Research and development incentive is recognised as an income tax benefit in the year in which it is earned. The corresponding receivable is held within other receivables.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

21 | Page

Deferred tax is provided using the balance sheet liability method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. The following temporary differences are not provided for: initial recognition of goodwill, the initial recognition of assets or liabilities that affect neither accounting nor taxable profit, and differences relating to investments in subsidiaries to the extent that they will probably not reverse in the foreseeable future. The amount of deferred tax provided is based on the expected manner of realisation or settlement of the carrying amount of assets and liabilities, using tax rates enacted or substantively enacted at the balance sheet date.

A deferred tax asset is recognised only to the extent that it is probable that the future taxable profits will be available against which the asset can be utilised. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit will be realised.

Tax consolidation

The Company and its wholly-owned Australian resident entities have formed a tax-consolidated group with effect from 1 July 2004 and are therefore taxed as a single entity from that date. The head entity within the tax-consolidated group is Marine Produce Australia Limited.

Current tax expense/income and deferred tax assets arising from unused tax losses of the subsidiaries is assumed by the head entity and are recognised in the separate financial statements of the members of the tax consolidated group using the “separate tax payer within group” approach by reference to the carrying amount of assets and liabilities in the separate financial statements of each entity and the tax values applying under tax consolidation.

Any current tax liabilities (or assets) and deferred tax assets arising from unused tax losses of the subsidiaries is assumed by the head entity in the tax consolidated group and are recognised as amounts payable (receivable) to (from) other entities in the tax-consolidated group in conjunction with any tax funding arrangement amounts (refer below). Any difference between these amounts is recognised by the Company as an equity contribution or distribution.

The Company recognises deferred tax assets arising from unused tax losses of the tax-consolidated group to the extent that it is probable that future taxable profits of the tax-consolidated group will be available against which the asset can be utilised.

Any subsequent period adjustments to deferred tax assets arising from unused tax losses as a result of revised assessments of the probability of recoverability is recognised by the head entity only.

Nature of tax funding arrangements and tax sharing arrangements

The head entity, in conjunction with other members of the tax-consolidated group, has not entered into a tax funding or sharing arrangement with members of the tax-consolidated group in respect of tax amounts.

(l) Goods and services tax

Revenue, expenses and assets are recognised net of the amount of goods and services tax (GST), except where the amount of GST incurred is not recoverable from the taxation authority. In these circumstances, the GST is recognised as part of the cost of acquisition of the asset or as part of the expense.

Receivables and payables are stated with the amount of GST included. The net amount of GST recoverable from, or payable to, the ATO is included as a current asset or liability in the balance sheet.

Cash flows are included in the statement of cash flows on a gross basis. The GST components of cash flows arising from investing and financing activities which are recoverable from, or payable to, the ATO are classified as operating cash flows.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

22 | Page

(m) Determination of fair values

A number of the Group’s accounting policies and disclosures require the determination of fair value, for both financial and non-financial assets and liabilities. Fair values have been determined for measurement and/or disclosure purposes based on the following methods. When applicable, further information about the assumptions made in determining fair values of assets and liabilities are disclosed in the notes specific to that asset or liability.

Biological assets

The fair value of fish is set out in Note 3(d).

Trade and other receivables

The fair value of trade and other receivables is estimated as the present value of future cash flows, discounted at the market rate of interest at the reporting date.

(n) Financial instruments

Non-derivative financial assets

The Group initially recognises loans and receivables and deposits on the date that they are originated. All other financial assets (including assets designated at fair value through profit and loss) are recognised initially on the trade date at which the Group becomes a party to the contractual provisions of the instrument.

The Group derecognises a financial asset when the contractual rights to the cash flows from the asset expire, or it transfers the rights to receive the contractual cash flows on the financial asset in a transaction in which substantially all the risks and rewards of ownership of the financial asset are transferred. Any interest in transferred financial assets that is created or retained by the Group is recognised as a separate asset or liability.

The Group has the following non-derivative financial assets: trade and other receivables, and cash and cash equivalents.

Trade and other receivables are financial assets with fixed or determinable payments that are not quoted in an active market. Such assets are recognised initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition loans and receivables are measured at amortised cost using the effective interest method, less any impairment losses.

Cash and cash equivalents comprise cash balances and call deposits with original maturities of three months or less. Bank overdrafts that are repayable on demand and form an integral part of the Group’s cash management are included as a component of cash and cash equivalents for the purpose of the statement of cash flows.

Non-derivative financial liabilities

The Group initially recognises debt securities issued and subordinated liabilities on the date that they are originated. All other financial liabilities (including liabilities designated at fair value through profit or loss) are recognised initially on the trade date at which the Group becomes a party to the contractual provisions of the instrument. The Group derecognises a financial liability when its contractual obligations are discharged or cancelled or expire. Financial assets and liabilities are offset and the net amount presented in the Statement of Financial Position when, and only when, the Group has a legal right to offset the amounts and intends either to settle on a net basis or to realise the asset and settle the liability simultaneously.

The Group has the following non-derivative financial liabilities: loans and borrowings, and trade and other payables.

Such financial liabilities are recognised initially at fair value plus any directly attributable transaction costs. Subsequent to initial recognition these financial liabilities are measured at amortised cost using the effective interest rate method.

Financial assets and liabilities are offset and then net amount presented in the Statement of Financial Position when, and only when, the Group has a legal right to offset the amounts and intends either to settle on a net basis or to realise the asset and settle the liability simultaneously.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

23 | Page

Share capital

Ordinary shares

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares and share options are recognised as a deduction from equity, net of any tax effects.

Dividends

Dividends are recognised as a liability in the period in which they are declared.

(o) Government grants

An unconditional government grant is recognised in profit or loss as other income when the grant becomes receivable.

Grants that compensate the Group for expenses incurred are recognised in profit or loss as other income on a systematic basis in the same period in which the expenses are recognised.

Research and development tax incentives are recognised in the statement of profit or loss when received or when the amount to be received can be reliably estimated.

4 New standards and interpretations not yet adopted

A number of new and revised standards are effective for the current reporting period, however there was no need

to change accounting policies or make retrospective adjustments as a result of adopting these standards.

Information on these new standards is presented below.

AASB 2015-1 Amendments to Australian Accounting Standards – Annual Improvements to Australian Accounting Standards 2012-2014 Cycle

These amendments arise from the issuance of Annual Improvements to IFRS 2012-2014 Cycle in September 2014

by the IASB.

Among other improvements, the amendments clarify that when an entity reclassifies an asset (or disposal group)

directly from being held for sale to being held for distribution (or vice-versa), the accounting guidance in

paragraphs 27-29 of AASB 5 Non-current Assets Held for Sale and Discontinued Operations does not apply. The

amendments also state that when an entity determines that the asset (or disposal group) is no longer available for

immediate distribution or that the distribution is no longer highly probable, it should cease held-for-distribution

accounting and apply the guidance in paragraphs 27-29 of AASB 5.

AASB 2014-3 Amendments to Australian Accounting Standards – Accounting for Acquisitions of Interests in Joint Operations

The amendments to AASB 11 Joint Arrangements state that an acquirer of an interest in a joint operation in which

the activity of the joint operation constitutes a ‘business’, as defined in AASB 3 Business Combinations, should;

apply all of the principles on business combinations accounting in AASB 3 and other Australian Accounting

Standards except principles that conflict with the guidance of AASB 11. This requirement also applies to the

acquisition of additional interests in an existing joint operation that results in the acquirer retaining joint

control of the joint operation (note that this requirement applies to the additional interest only, i.e., the

existing interest is not re-measured) and to the formation of a joint operation when an existing business is

contributed to the joint operation by one of the parties that participate in the joint operation; and

provide disclosures for business combinations as required by AASB 3 and other Australian Accounting

Standards.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

24 | Page

AASB 2014-4 Amendments to Australian Accounting Standards – Clarification of Acceptable Methods of Depreciation and Amortisation

The amendments to AASB 116 prohibit the use of a revenue-based depreciation method for property, plant and

equipment. Additionally, the amendments provide guidance in the application of the diminishing balance method

for property, plant and equipment.

The amendments to AASB 138 present a rebuttable presumption that a revenue-based amortisation method for

intangible assets is inappropriate. This rebuttable presumption can be overcome (ie., a revenue-based

amortisation method might be appropriate) only in two (2) limited circumstances:

intangible asset is expressed as a measure of revenue, for example when the predominant limiting factor

inherent in an intangible asset is the achievement of a revenue threshold; or

when it can be demonstrated that revenue and the consumption of the economic benefits of the intangible

asset are highly correlated.

AASB 2014-9 Amendments to Australian Accounting Standards – Equity Method in Separate Financial Statements

The amendments introduce the equity method of accounting as one of the options to account for an entity’s

investments in subsidiaries, joint ventures and associates in the entity’s separate financial statements.

AASB 2015-2 Amendments to Australian Accounting Standards – Disclosure Initiative: Amendments to AASB 101

The Standard makes amendments to AASB 101 Presentation of Financial Statements arising from the IASB’s

Disclosure Initiative project. The amendments:

Clarify the materiality requirements in AASB 101, including an emphasis on the potentially detrimental effect

of obscuring useful information with immaterial information

Clarify that AASB 101’s specified line items in the statement(s) of profit or loss and other comprehensive

income and the statement of financial position can be disaggregated

Add requirements for how an entity should present subtotals in the statement(s) of profit and loss and other

comprehensive income and the statement of financial position

clarify that entities have flexibility as to the order in which they present the notes, but also emphasise that

understand-ability and comparability should be considered by an entity when deciding that order

remove potentially unhelpful guidance in AASB 101 for identifying a significant accounting policy

AASB 2015- 4 Amendments to Australian Accounting Standards – Financial Reporting Requirements for Australian Groups with a Foreign Parent

AASB 2015-4 amends AASB 128 Investments in Associates and Joint Ventures to ensure that its reporting

requirements on Australian groups with a foreign parent align with those currently available in AASB 10

Consolidated Financial Statements for such groups. AASB 128 will now only require the ultimate Australian entity

to apply the equity method in accounting for interests in associates and joint ventures, if either the entity or the

group is a reporting entity, or both the entity and group are reporting entities.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

25 | Page

AASB 1057 Application of Australian Accounting Standards

In May 2015, the AASB decided to revise Australian Accounting Standards that incorporate IFRSs to minimise

Australian specific wording even further. The AASB noted that IFRSs do not contain application paragraphs that

identify the entities and financial reports to which the Standards (and Interpretations) apply. As a result, the AASB

decided to move the application paragraphs previously contained in each Australian Accounting Standard (or

Interpretation), unchanged, into a new Standard AASB 1057 Application of Australian Accounting Standards.

AASB 2015-9 Amendments to Australian Accounting Standards – Scope and Application Paragraphs removes the

application paragraphs from each Australian Accounting Standard.

Impact of standards issued but not yet applied

New and revised accounting standards and amendments that are currently issued for future reporting periods that

are relevant to the Company include:

AASB 9 Financial Instruments

AASB 9 introduces new requirements for the classification and measurement of financial assets and liabilities.

These requirements improve and simplify the approach for classification and measurement of financial assets

compared with the requirements of AASB 139.

The effective date is for annual reporting periods beginning on or after 1 January 2018.

The Company is yet to undertake a detailed assessment of the impact of AASB 9. However, based on the

Company’s preliminary assessment, the Standard is not expected to have a material impact on the transactions

and balances recognised in the financial statements when it is first adopted for the year ending 30 June 2019.

AASB 15 Revenue from Contracts with Customers

AASB 15 replaces AASB 118: Revenue, AASB 111 Construction Contracts and some revenue-related Interpretations. In summary, AASB 15:

establishes a new revenue recognition model;

changes the basis for deciding whether revenue is to be recognised over time at a point in time;

provides a new and more detailed guidance on specific topics (eg multiple element arrangements, variable

pricing, rights of return and warranties); and

expands and improves disclosures about revenue.

The Company is yet to undertake a detailed assessment of the impact of AASB 15. However, based on the Company’s preliminary assessment, the Standard is not expected to have a material impact on the transactions and balances recognised in the financial statements when it is first adopted for the year ending 30 June 2018.

AASB 16 Leases

AASB 16 replaces AASB 117 Leases and some lease-related Interpretations. In summary, AASB 16:

requires all leases to be accounted for ‘on-balance sheet’ by lessees, other than short-term and low value asset leases;

provides new guidance on the application of the definition of lease and on sale and lease back accounting;

largely retains the existing lessor accounting requirements in AASB 117; and

requires new and different disclosures about leases.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

26 | Page

The Company is yet to undertake a detailed assessment of the impact of AASB 16. However, based on the

Company’s preliminary assessment, the Standard is not expected to have a material impact on the transactions

and balances recognised in the financial statements when it is first adopted for the year ending 30 June 2020.

AASB 2014-3 Amendments to Australian Accounting Standards – Accounting for Acquisitions of Interests in Joint

Operations

This amendment impacts on the use of AASB 11 when acquiring an interest in a joint operation.

The effective date is for annual reporting periods beginning on or after 1 January 2016. When these amendments

are first adopted for the year ending 30 June 2017, there will be no material impact on the transactions and

balances recognised in the financial statements.

AASB 2014-4 Amendments to Australian Accounting Standards – Clarification of Acceptable Methods of

Depreciation and Amortisation

The amendments to AASB 116 prohibit the use of a revenue-based depreciation method for property, plant and

equipment. Additionally, the amendments provide guidance in the application of the diminishing balance method

for property, plant and equipment.

The effective date is for annual reporting periods beginning on or after 1 January 2016. When these amendments

are first adopted for the year ending 30 June 2017, there will be no material impact on the transactions and

balances recognised in the financial statements.

AASB 2014-9 Amendments to Australian Accounting Standards – Equity Method in Separate Financial

Statements

The amendments introduce the equity method of accounting as one of the options to account for an entity’s

investments in subsidiaries, joint ventures and associates in the entity’s separate financial statements.

The effective date is for annual reporting periods beginning on or after 1 January 2016. When these amendments

are first adopted for the year ending 30 June 2017, there will be no material impact on the financial statements.

AASB 2014-10 Amendments to Australian Accounting Standards – Sale or Contribution of Assets between an

Investor and its Associate or Joint Venture

The amendments address a current inconsistency between AASB 10 Consolidated Financial Statements and AASB

128 Investments in Associates and Joint Ventures (2011). The amendments clarify that, on a sale or contribution of

assets to a joint venture or associate or on a loss of control when joint control or significant influence is retained in

a transaction involving an associate or a joint venture, any gain or loss recognised will depend on whether the

assets or subsidiary constitute a business, as defined in AASB 3 Business Combinations. Full gain or loss is

recognised when the assets or subsidiary constitute a business, whereas gain or loss attributable to other

investors’ interests is recognised when the assets or subsidiary do not constitute a business.

The effective date is for annual reporting periods beginning on or after 1 January 2016. When these amendments

are first adopted for the year ending 30 June 2017, there will be no material impact on the financial statements.

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

27 | Page

5 Parent company disclosure

As at, and throughout, the financial year ending 30 June 2016 the parent company of the Group was Marine Produce Australia Limited.

Company 2016 2015

Result of the parent entity Profit for the period 3,530,000 2,401,701 Other comprehensive income - - Total comprehensive income for the period 3,530,000 2,401,701 Financial position of parent entity at year end

Current assets 5,505,234 5,924,891 Total assets 26,153,569 18,249,235 Current liabilities (159,319) (306,014) Total liabilities (2,660,497) (3,216,974) Total equity of the parent entity comprising of:

Share capital 60,505,645 55,699,560 Option reserve 124,726 - Accumulated losses (37,137,299) (40,667,299)

Total equity 23,493,072 15,032,261

Marine Produce Australia Limited has a guarantee in place under a facility agreement – refer to Note 21. For disclosures of capital and operating commitments refer Note 25 and Note 26, respectively. 6 Finance costs

2016 2015

Interest expense 108,312 79,224

108,312 79,224

Interest expense

Interest charges for Capital Finance and NAB Finance, for the provision of secured working capital facilities – refer to Note 21 for further details of movements, terms and conditions of these facilities.

7 Finance income

2016 2015

Interest income from cash and cash equivalents 37,066 40,280

37,066 40,280

NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 JUNE 2016

28 | Page

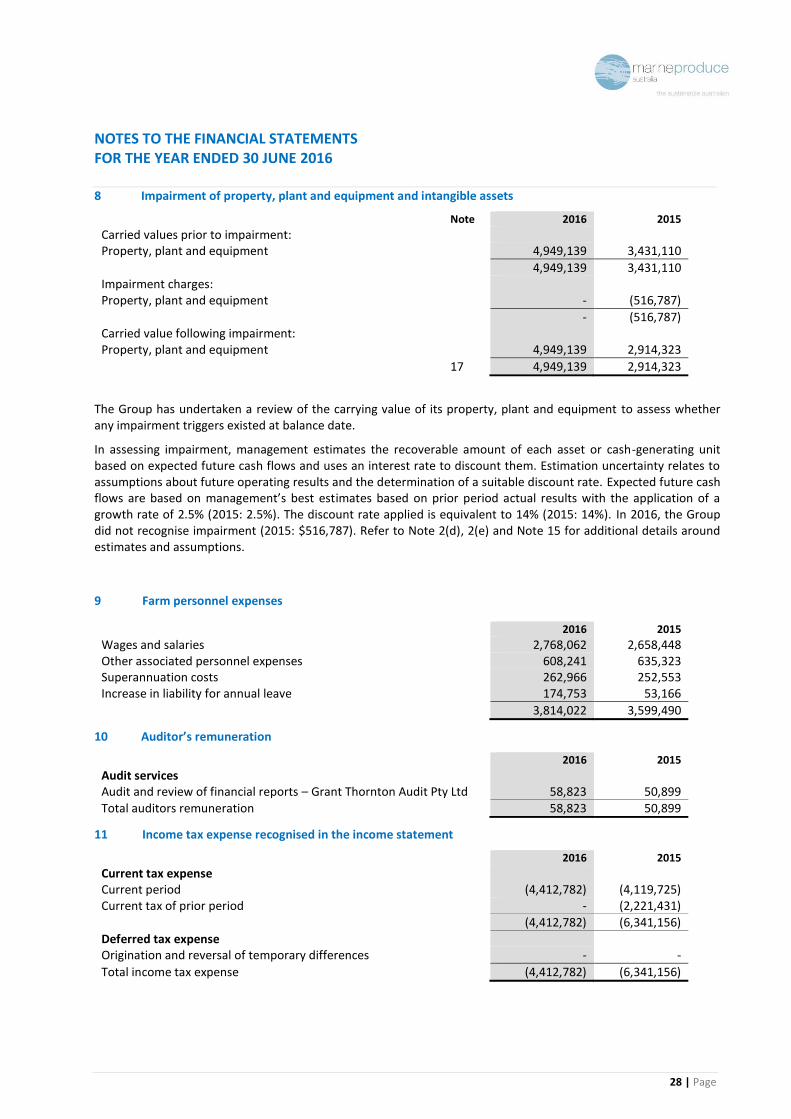

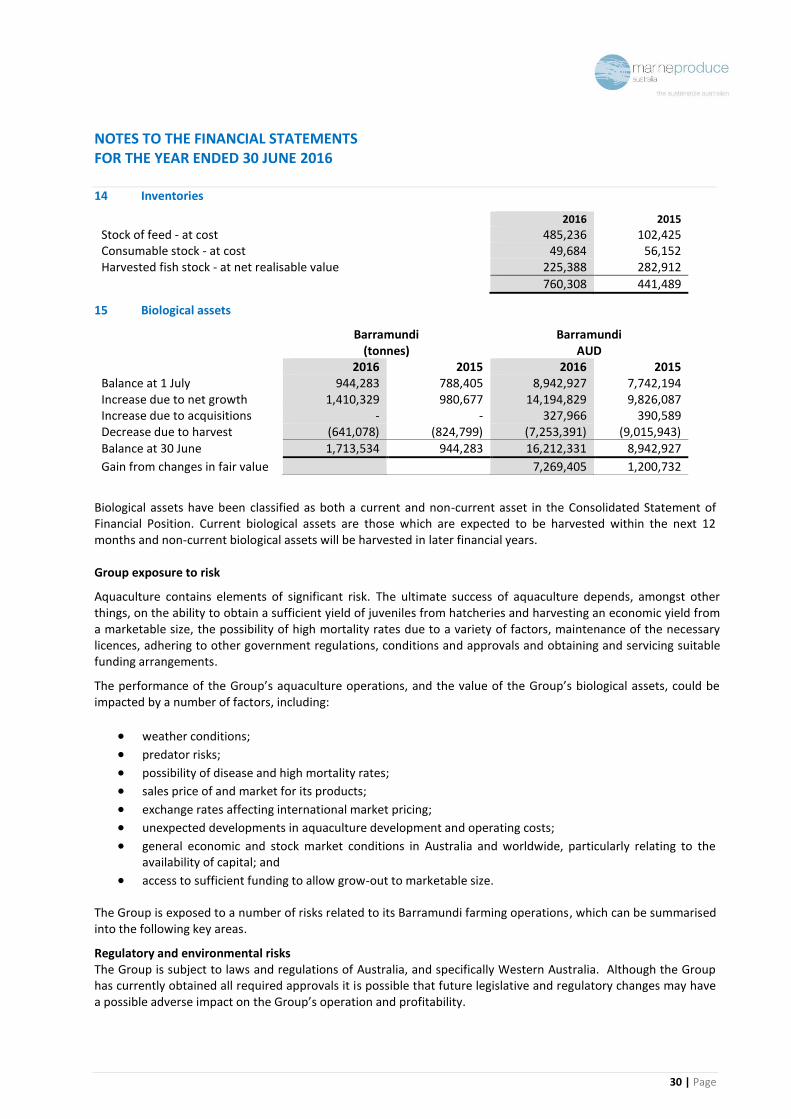

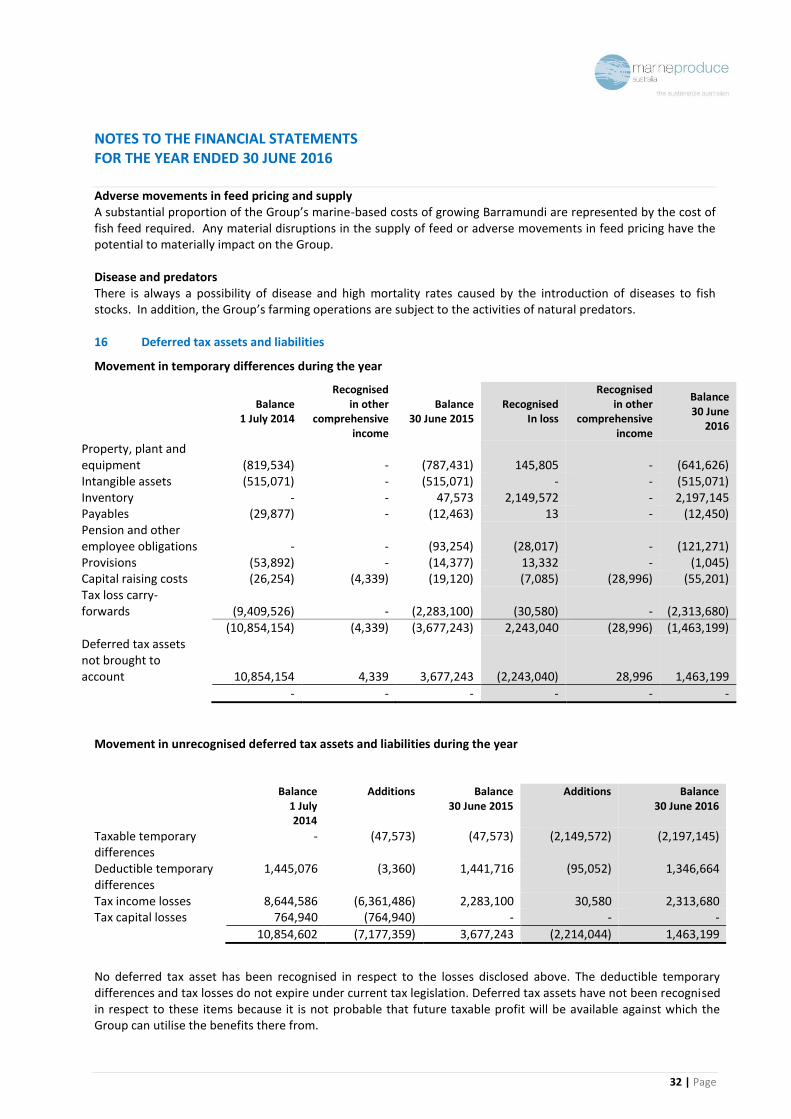

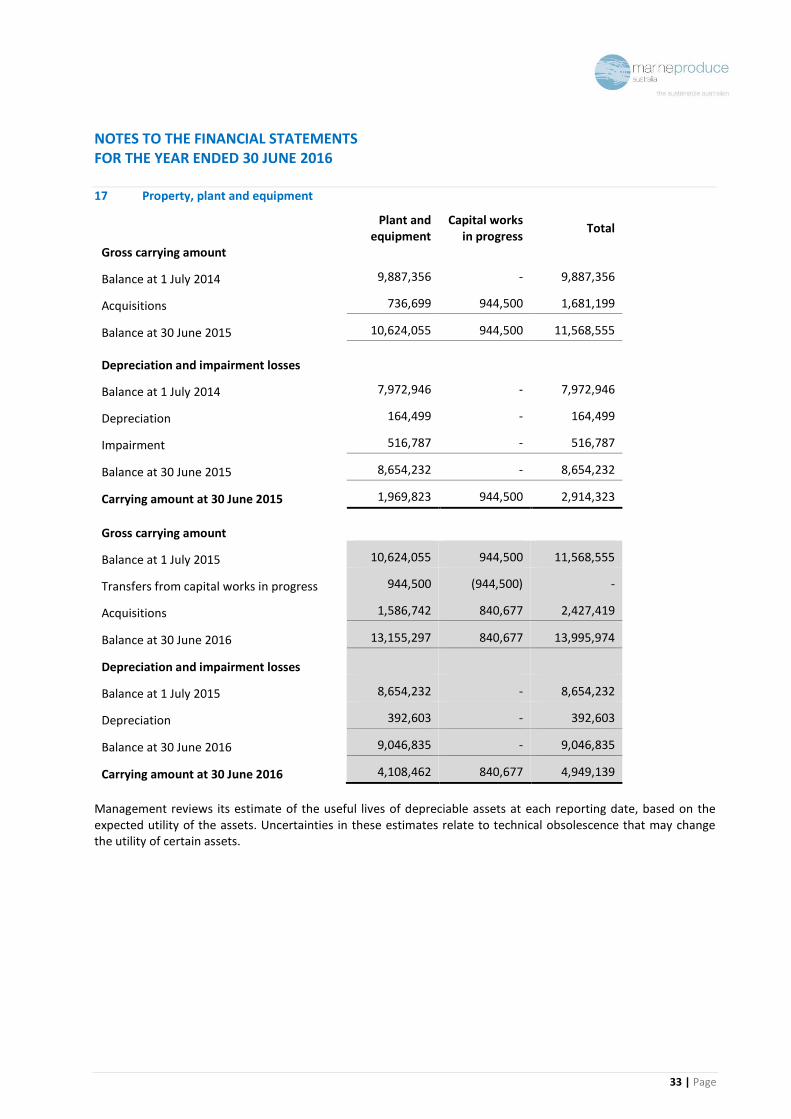

8 Impairment of property, plant and equipment and intangible assets

Note 2016 2015

Carried values prior to impairment: Property, plant and equipment 4,949,139 3,431,110

4,949,139 3,431,110 Impairment charges: Property, plant and equipment - (516,787)

- (516,787) Carried value following impairment: Property, plant and equipment 4,949,139 2,914,323

17 4,949,139 2,914,323

The Group has undertaken a review of the carrying value of its property, plant and equipment to assess whether any impairment triggers existed at balance date.

In assessing impairment, management estimates the recoverable amount of each asset or cash-generating unit based on expected future cash flows and uses an interest rate to discount them. Estimation uncertainty relates to assumptions about future operating results and the determination of a suitable discount rate. Expected future cash flows are based on management’s best estimates based on prior period actual results with the application of a growth rate of 2.5% (2015: 2.5%). The discount rate applied is equivalent to 14% (2015: 14%). In 2016, the Group did not recognise impairment (2015: $516,787). Refer to Note 2(d), 2(e) and Note 15 for additional details around estimates and assumptions.

9 Farm personnel expenses

2016 2015

Wages and salaries 2,768,062 2,658,448 Other associated personnel expenses 608,241 635,323 Superannuation costs 262,966 252,553 Increase in liability for annual leave 174,753 53,166

3,814,022 3,599,490

10 Auditor’s remuneration

2016 2015

Audit services Audit and review of financial reports – Grant Thornton Audit Pty Ltd 58,823

50,899

Total auditors remuneration 58,823 50,899

11 Income tax expense recognised in the income statement

2016 2015

Current tax expense Current period (4,412,782) (4,119,725) Current tax of prior period - (2,221,431)

(4,412,782) (6,341,156)

Deferred tax expense Origination and reversal of temporary differences - -