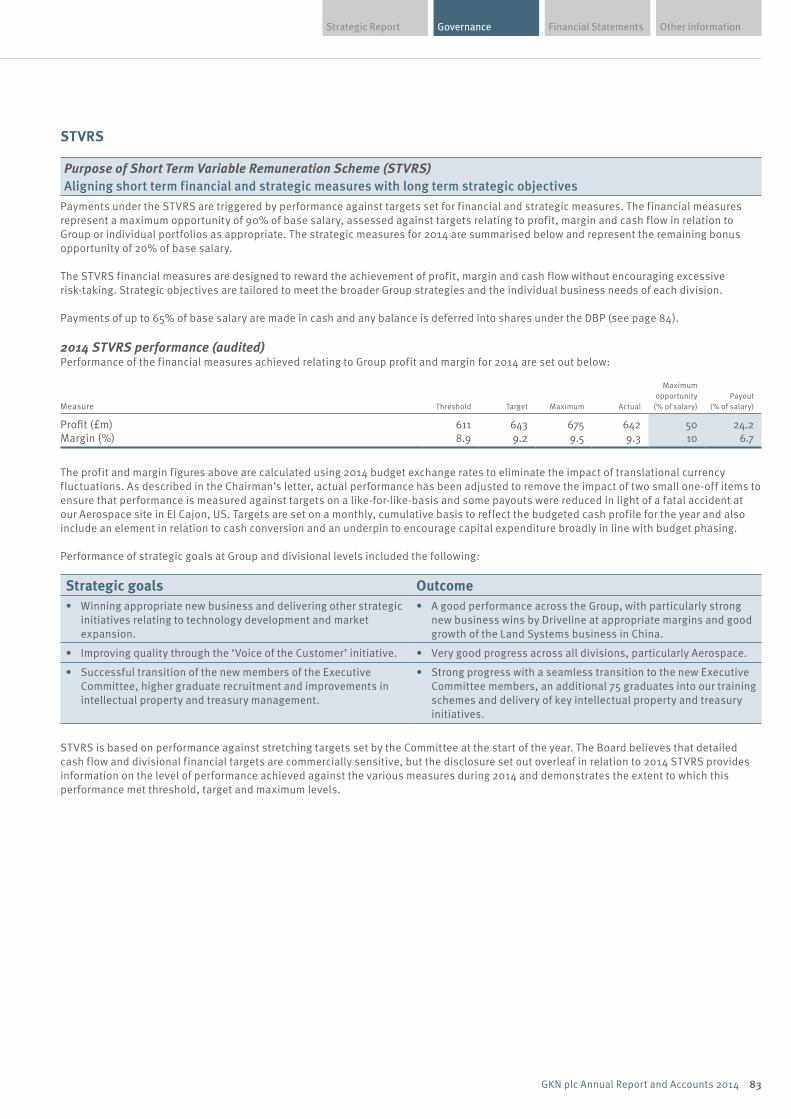

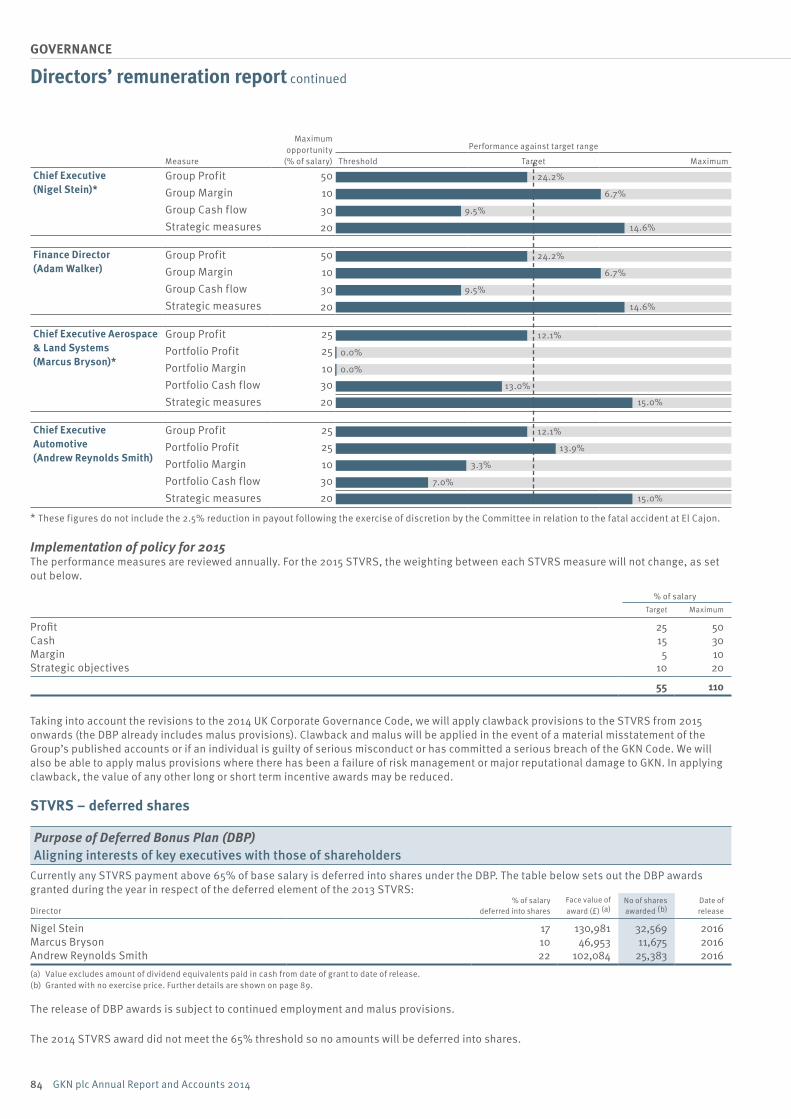

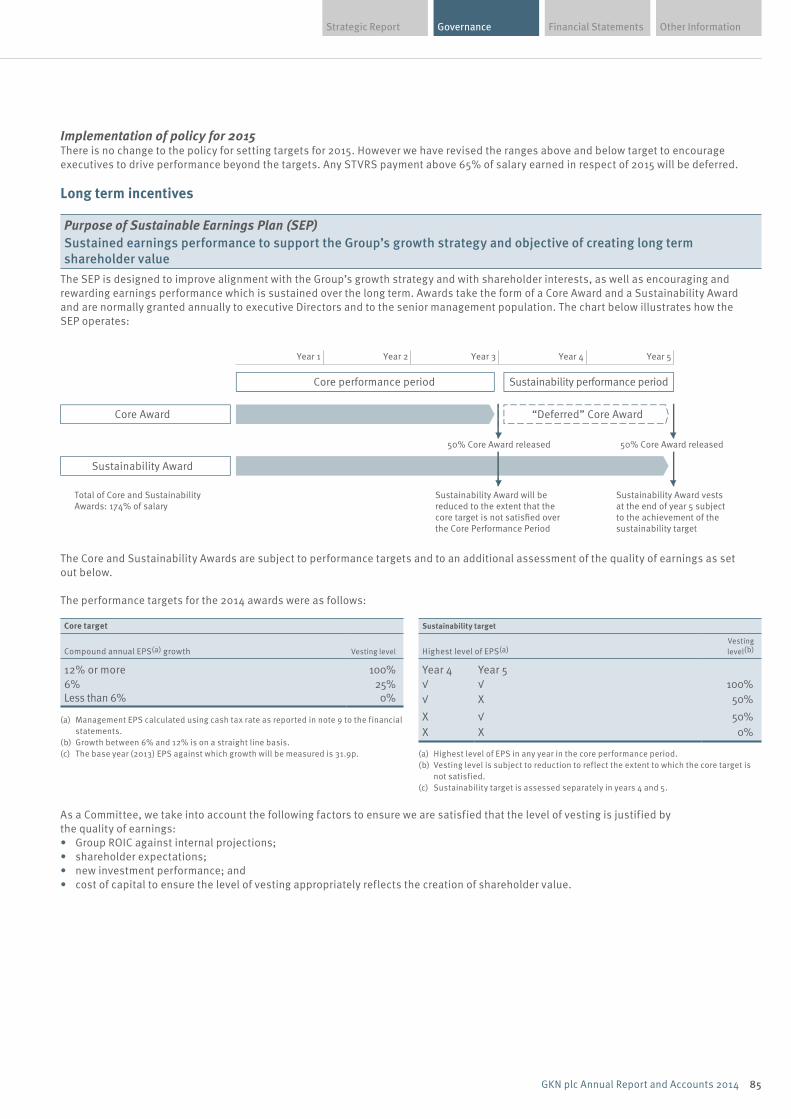

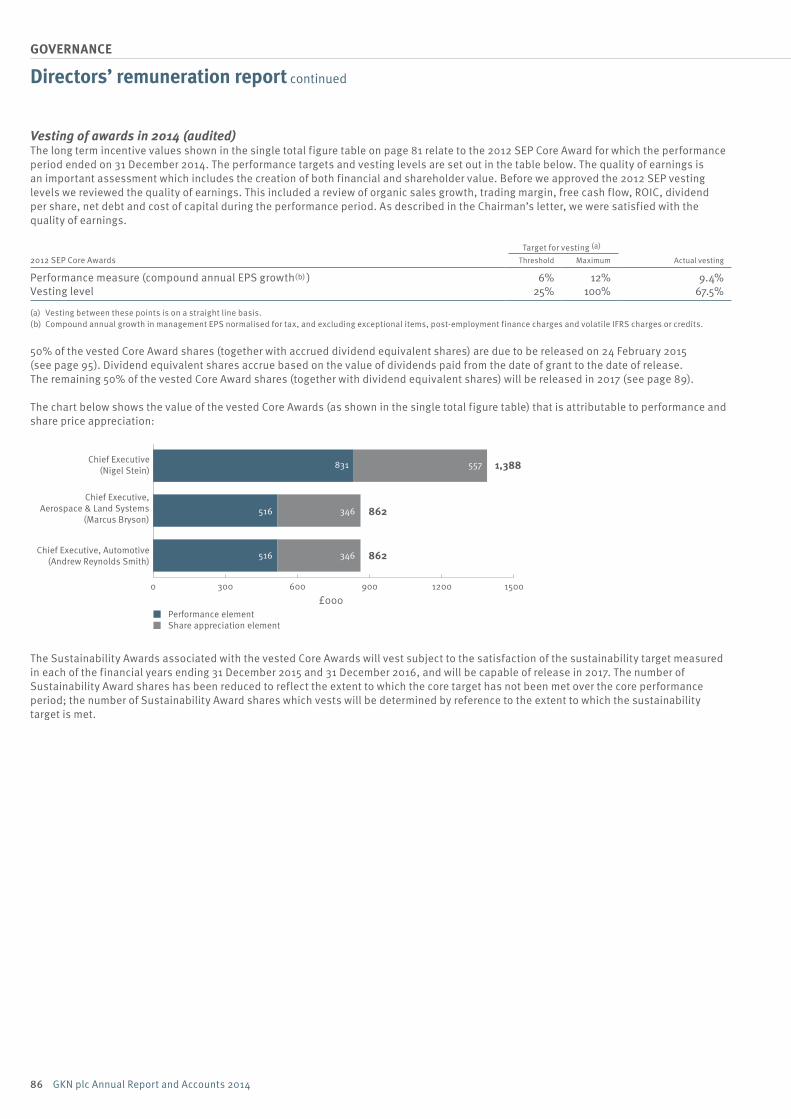

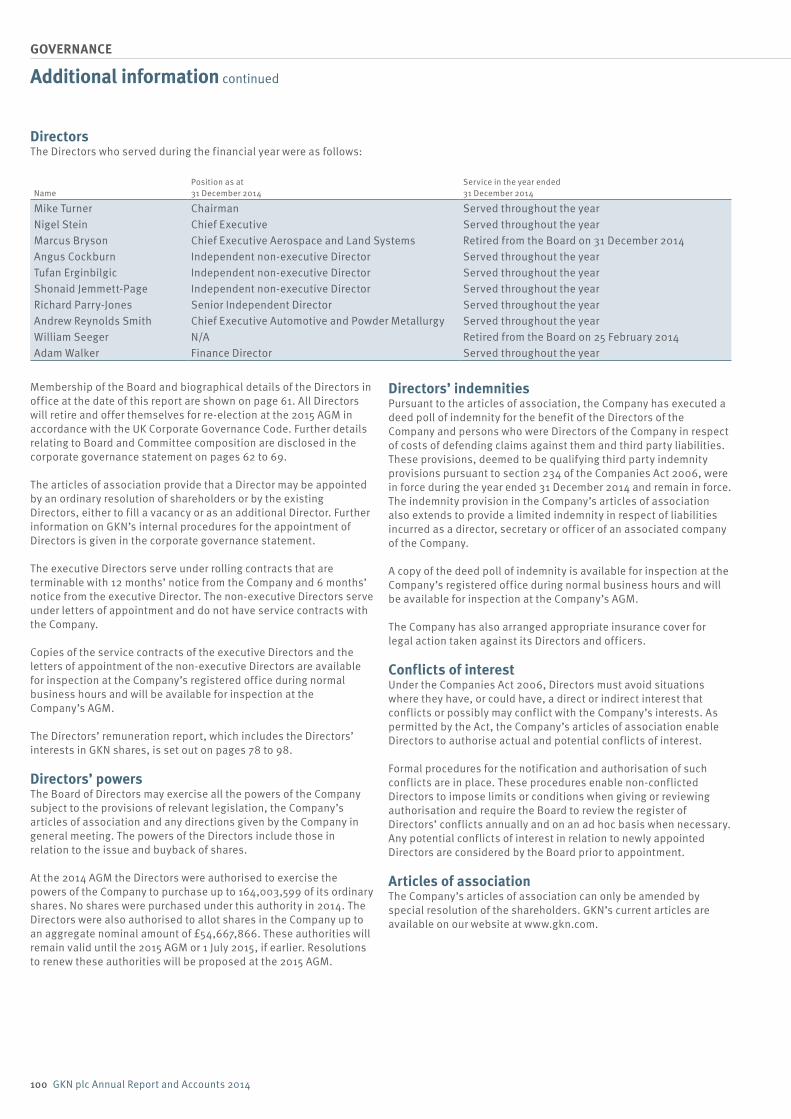

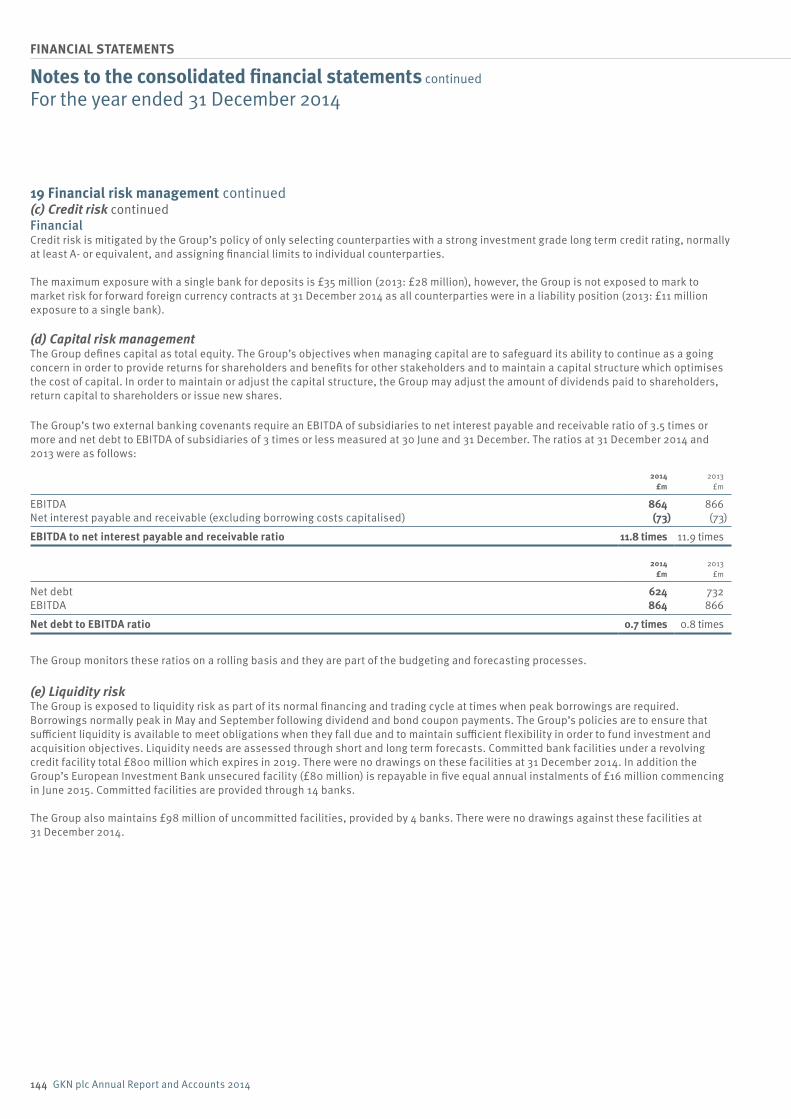

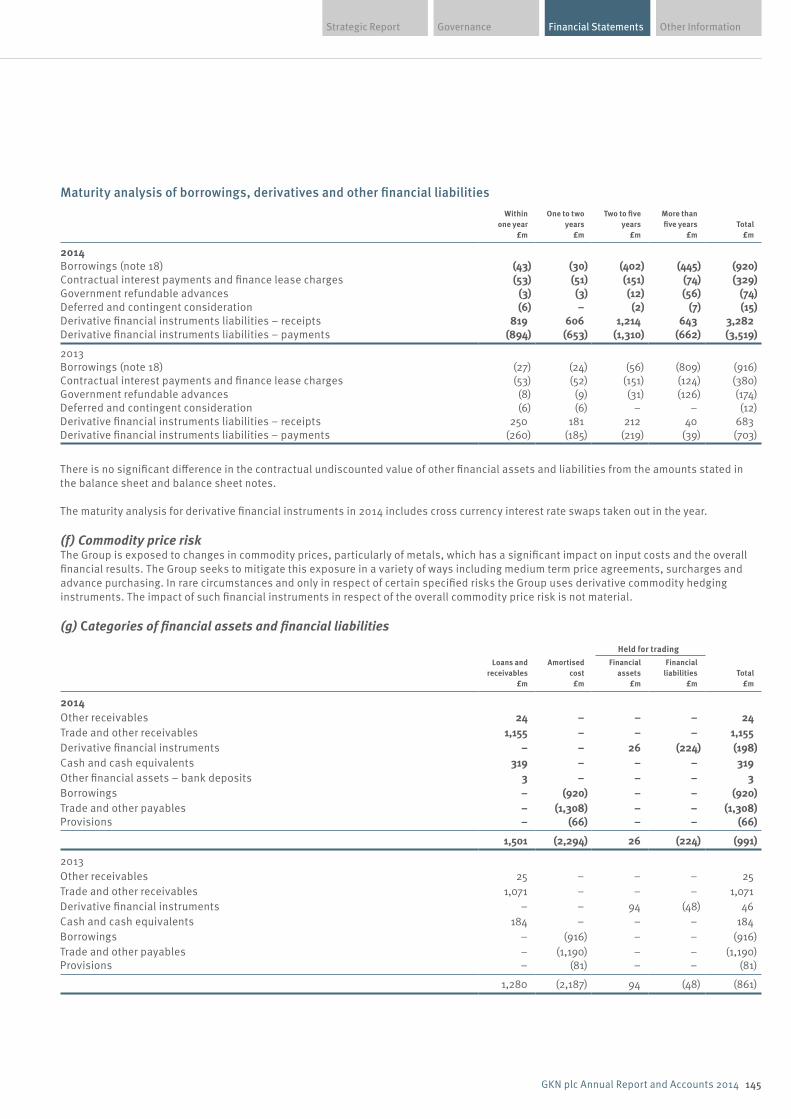

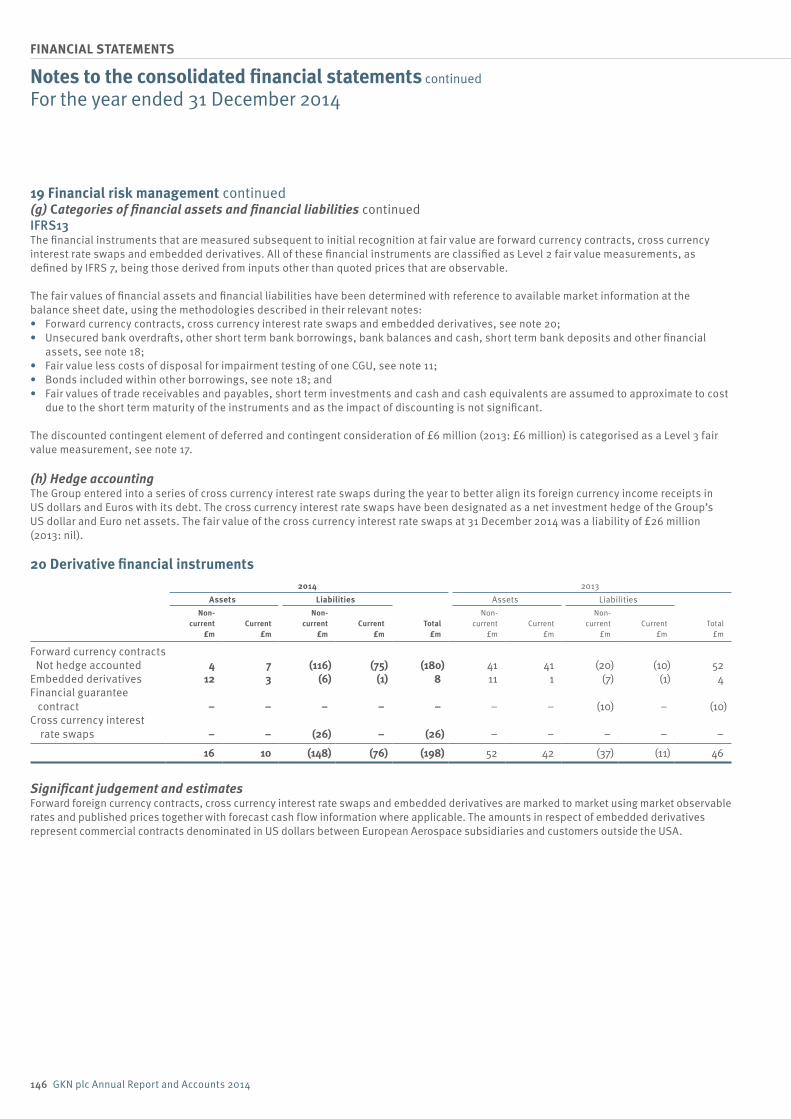

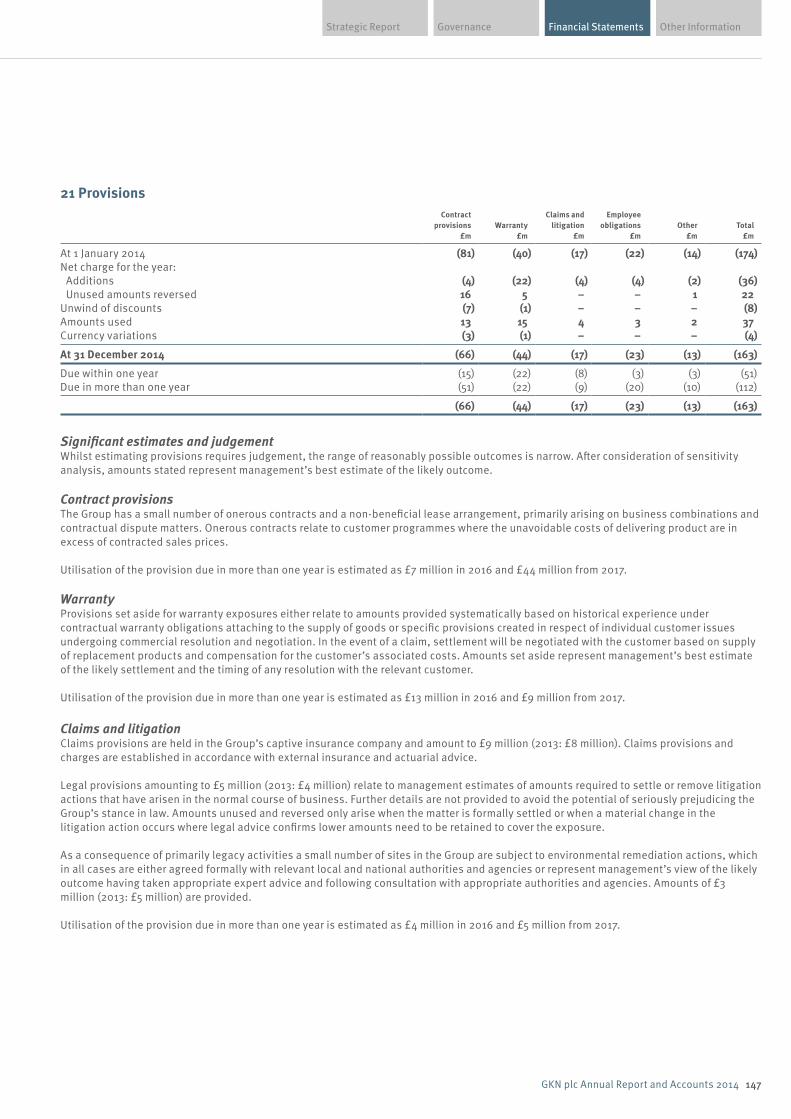

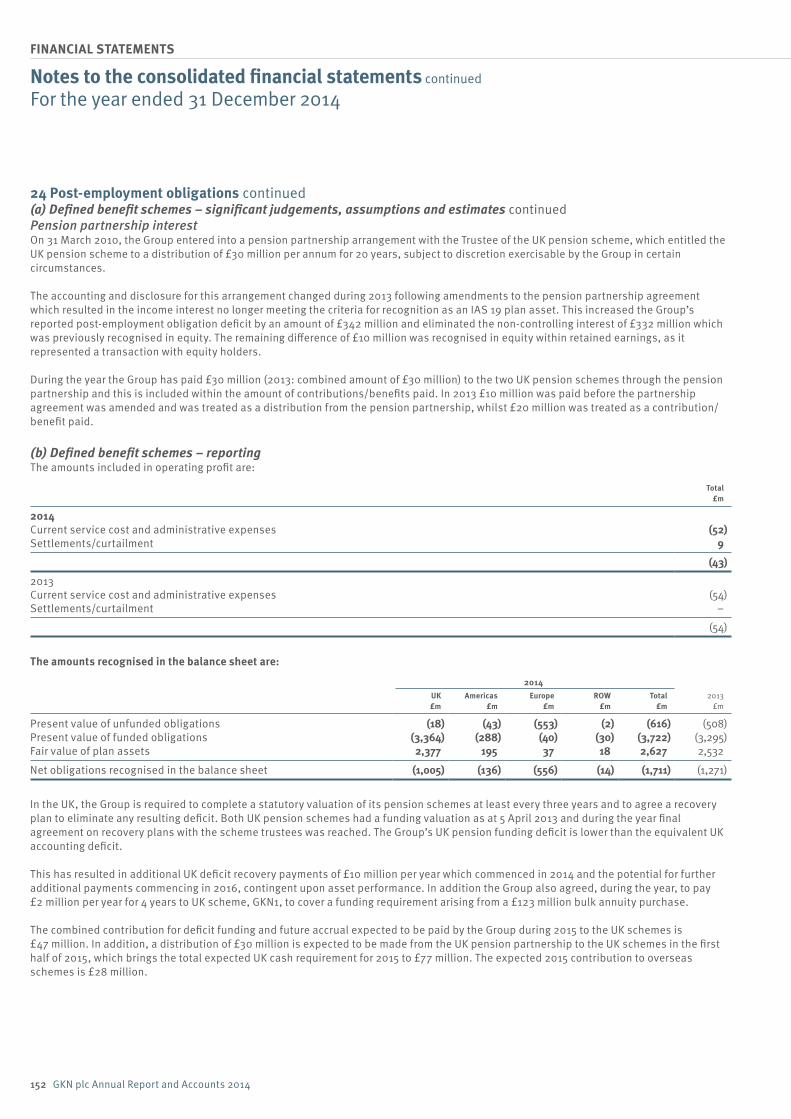

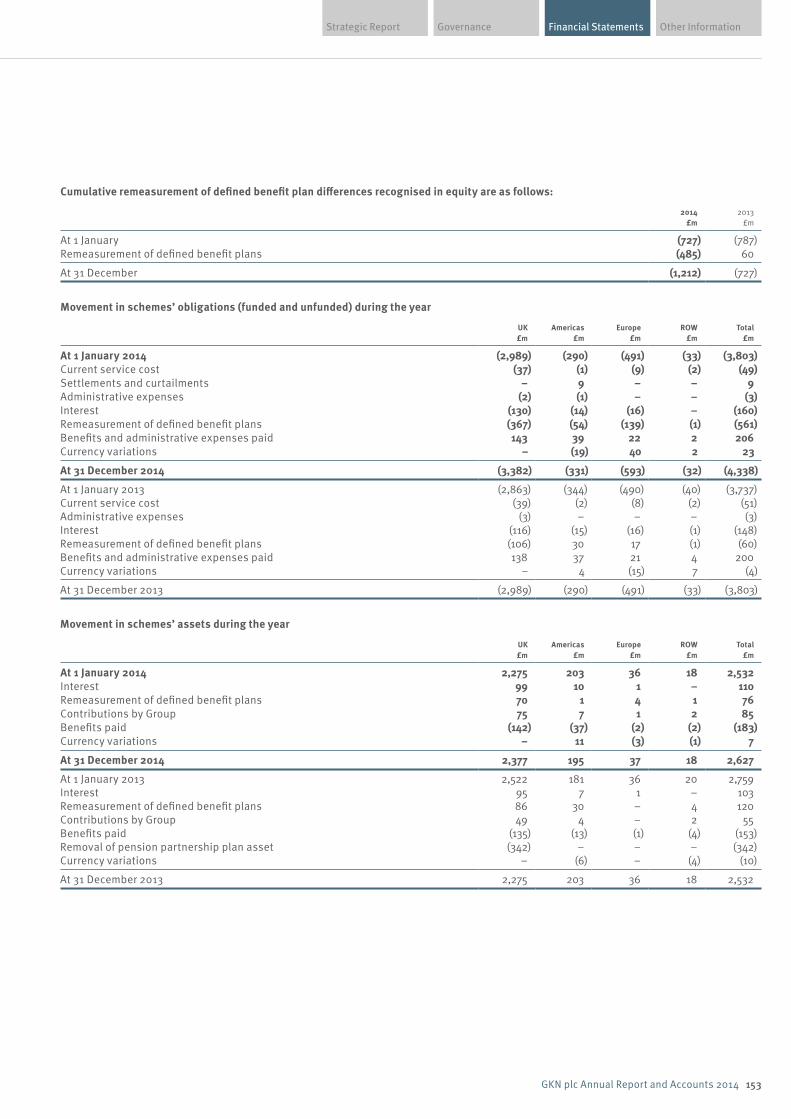

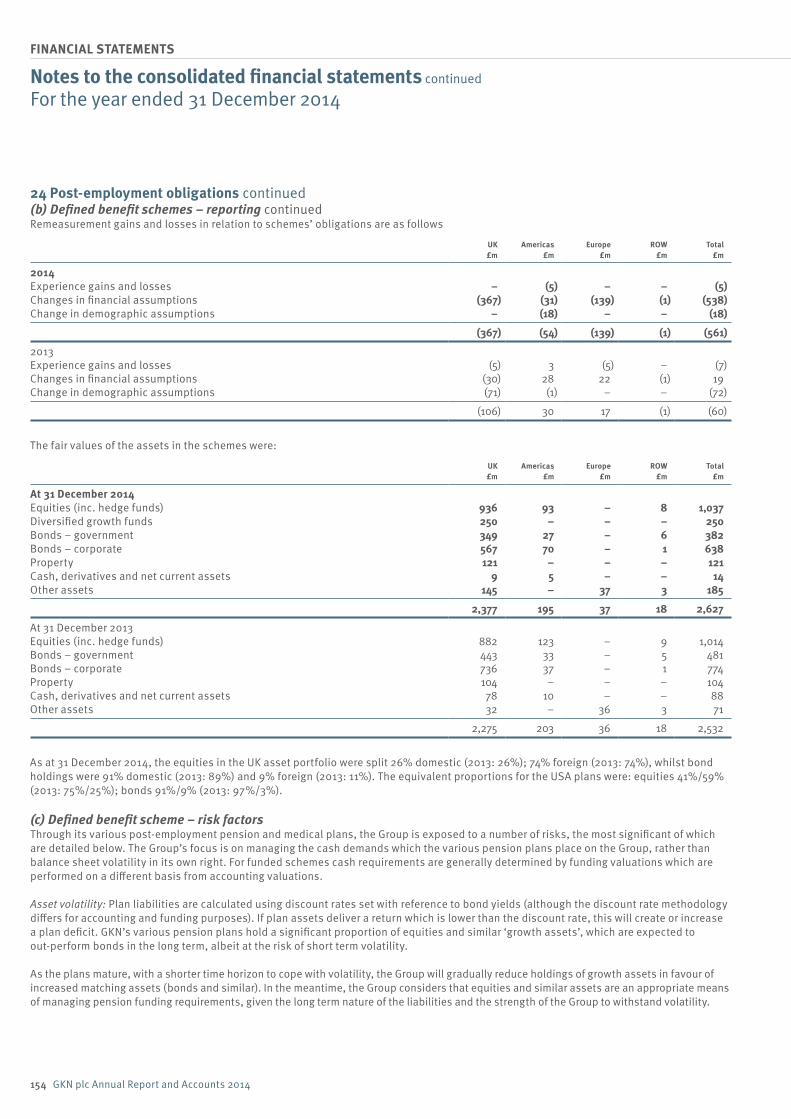

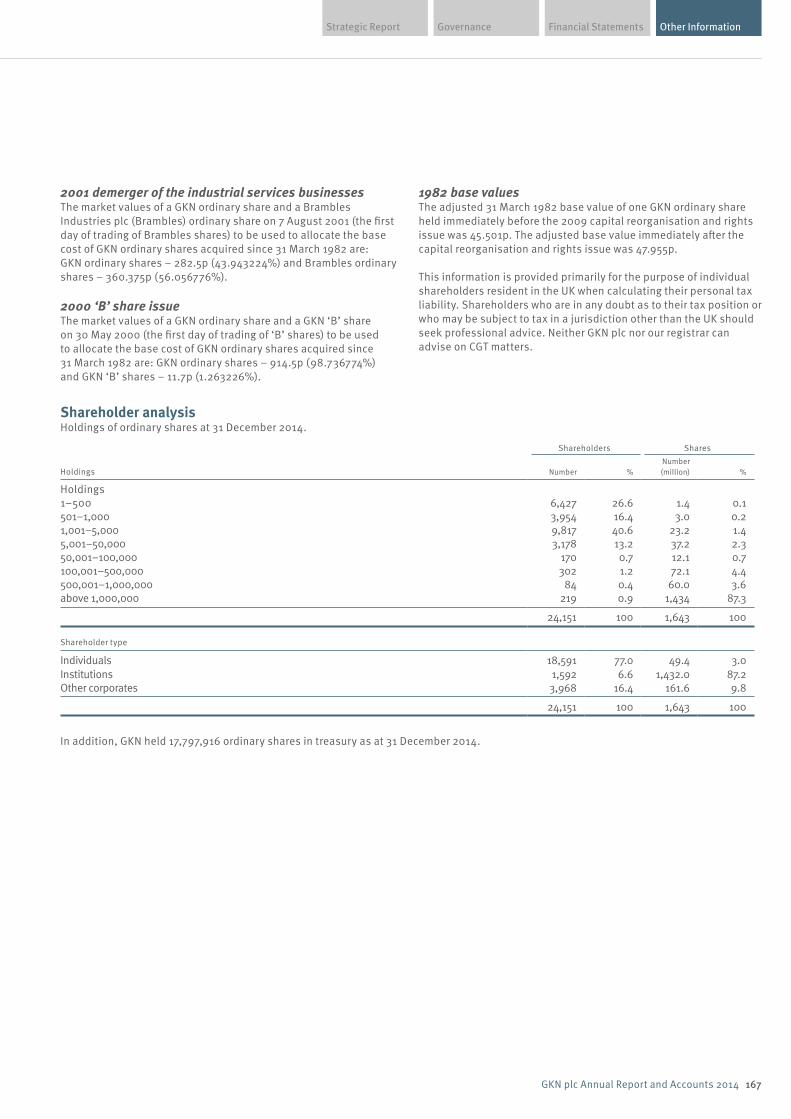

annual report and accounts 2014 - gkn have continued with our progressive dividend policy and are...

TRANSCRIPT

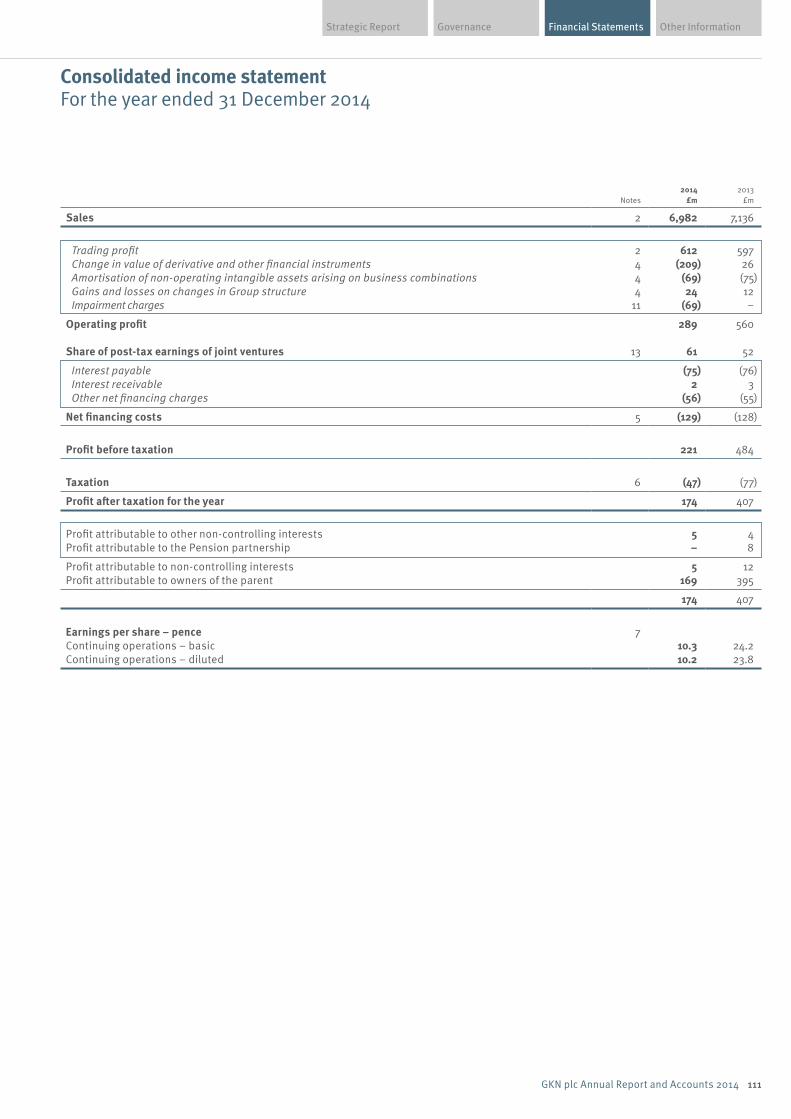

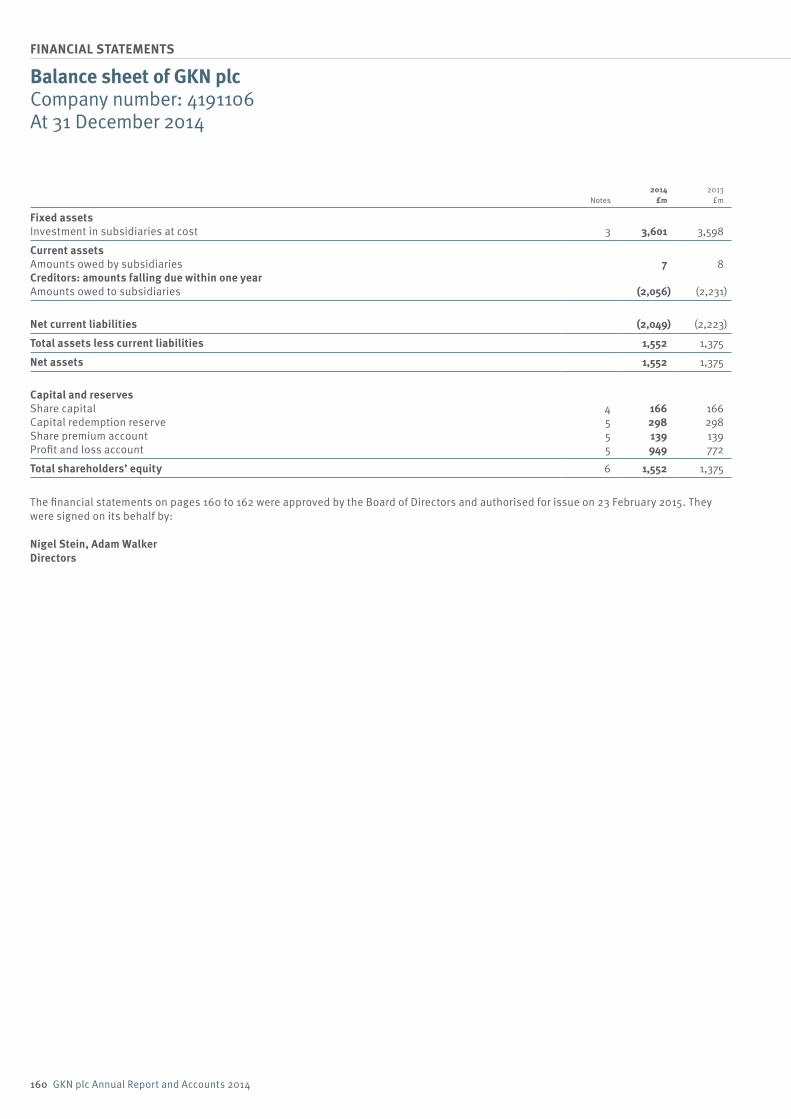

ENGINEERING THAT MOVES THE WORLD

ENGINEERING THAT MOVES THE WORLD

ENGINEERING THAT MOVES THE WORLD

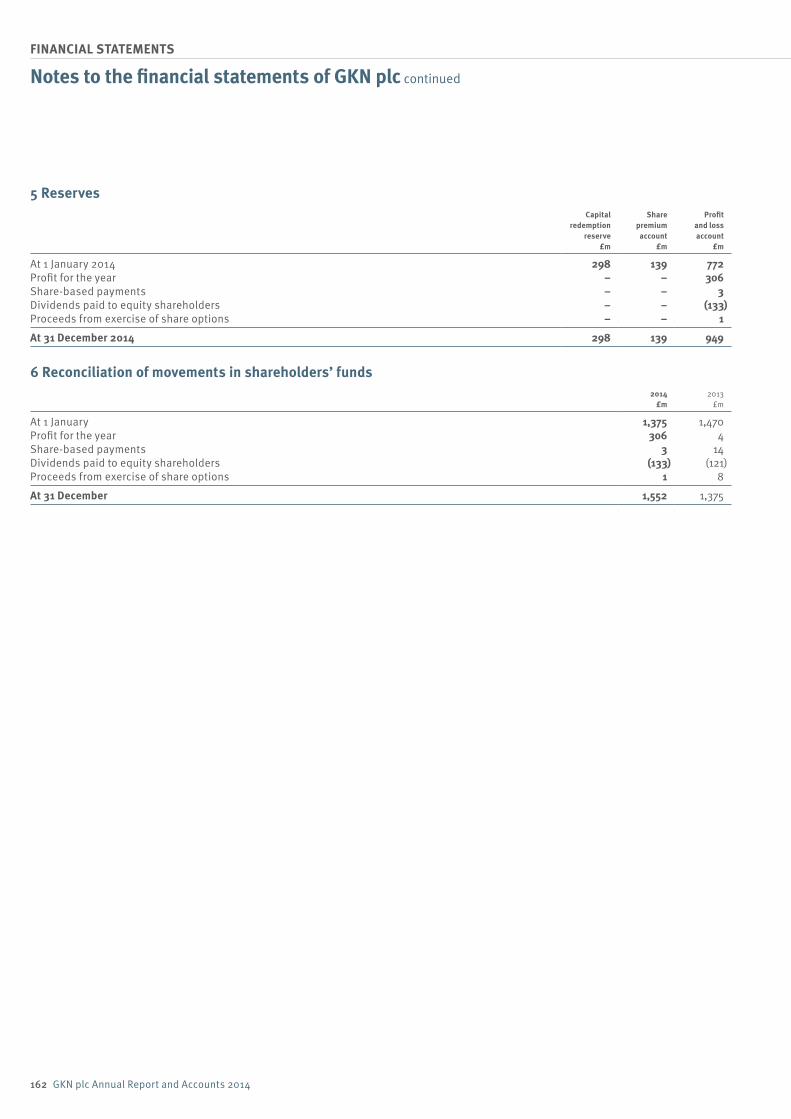

ENGINEERING THAT MOVES THE WORLD

Annual Report and Accounts 2014

ENGINEERING THAT MOVES THE WORLD

ENGINEERING THAT MOVES THE WORLD

→ Visit our website for more information www.gkn.com

GKN

plc Annual Report and Accounts 2014

Engineering that moves the world

Visit our website for more information www.gkn.com

GKN is a global engineering business. Every day we drive the wheels of hundreds of millions of cars, we help thousands of aircraft to fly, we deliver the power to move earth and harvest crops, and we make essential components for industries that touch lives across the globe.

GKN plc PO Box 55 Ipsley House Ipsley Church Lane Redditch Worcestershire B98 0TL Tel +44 (0)1527 517715 Fax +44 (0)1527 517700

London Office 50 Pall Mall London SW1Y 5JH Tel +44 (0)20 7930 2424Fax +44 (0)20 7930 3255

[email protected] www.gkn.com Registered in England No. 4191106

This annual report is available on our website.

Registrar Equiniti Aspect HouseSpencer RoadLancingWest SussexBN99 6DA

Tel 0871 384 2962* (+44 121 415 7039 from outside UK)

Fax 0871 384 2100 (+44 1903 833113 from outside UK)

www.equiniti.com www.shareview.co.uk

* Calls to this number cost 8p per minute plus network extras. Lines are open 8.30 am to 5.30 pm, Monday to Friday, excluding bank holidays.

Cautionary statement This annual report and accounts has been prepared for the members of GKN plc and should not be relied upon by any other party or for any other purpose. It contains forward looking statements which are made in good faith based on the information available at the time of its approval. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a number of risks and uncertainties that are inherent in any forward looking statement which could cause actual results to differ materially from those currently anticipated. Nothing in this document should be regarded as a profits forecast.

Contact information

Financial Statements Other InformationGovernanceStrategic Report

01GKN plc Annual Report and Accounts 2014

Chief Executive’s reviewPage 16

Our strategic framework Page 08

Key performance indicators Page 14

GlobalfootprintPage 04

Chairman’s statement Page 06

ContentsSTRATEGIC REPORTGKN at a glance 022014 at a glance 03Global footprint 04Chairman’s statement 06Our strategic framework 08Our business model 10Our business model / Global markets 12Key performance indicators 14Chief Executive’s review 16Business review / Group performance 20Business review / GKN Aerospace 22Business review / GKN Driveline 26Business review / GKN Powder Metallurgy 30Business review / GKN Land Systems 34Business review / Other financial information 38Risk management 42Sustainability report 52

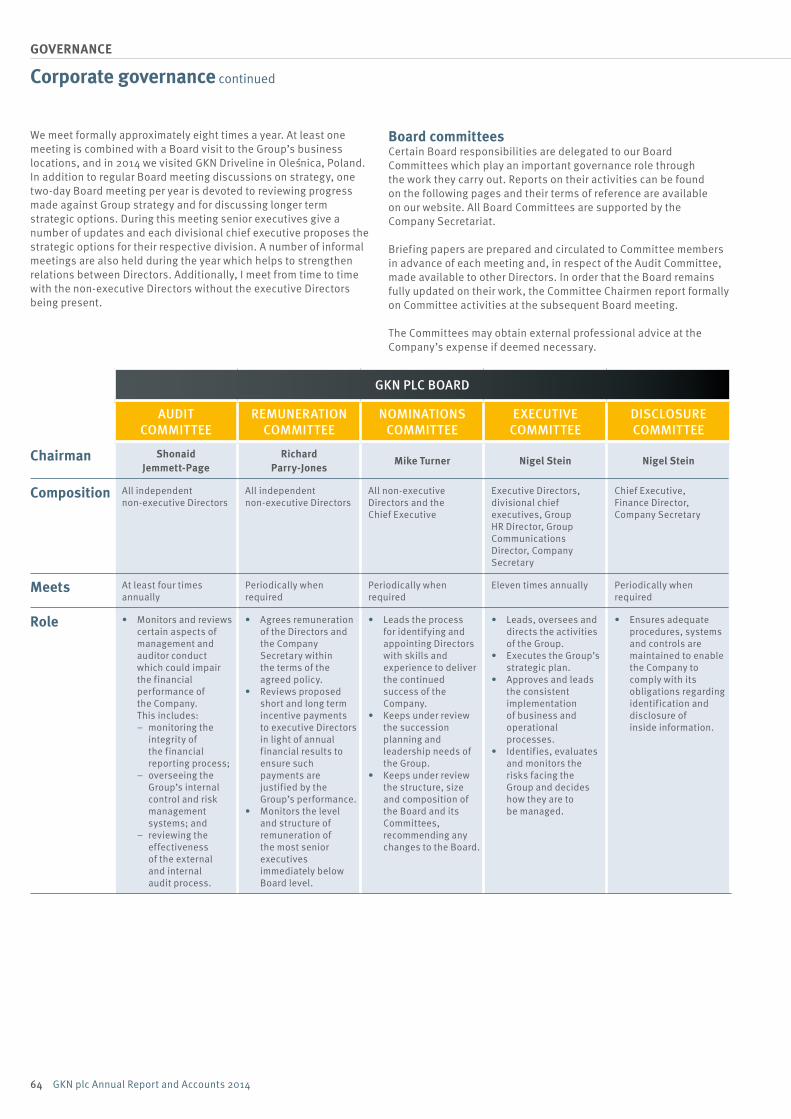

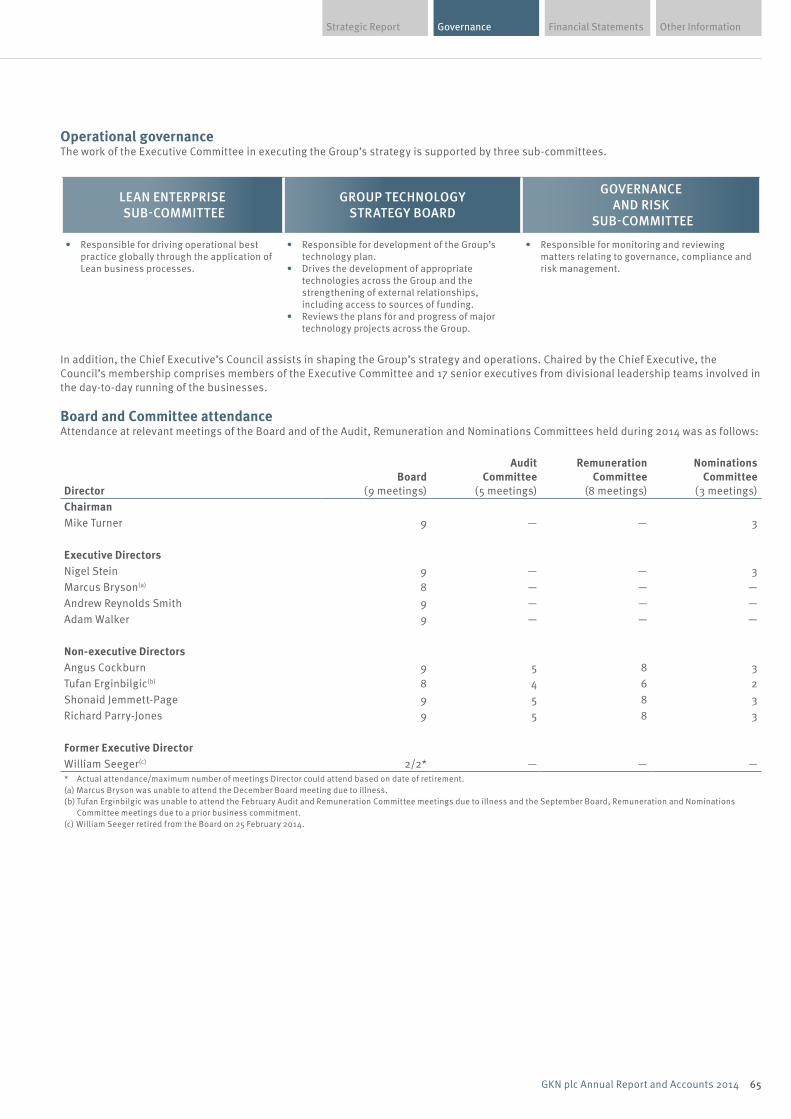

GOVERNANCEBoard of Directors 60Chairman’s introduction to governance 62Corporate governance 63Nominations Committee report 70Audit Committee report 72Directors’ remuneration report 78Additional information 99Statement of Directors’ responsibilities 102

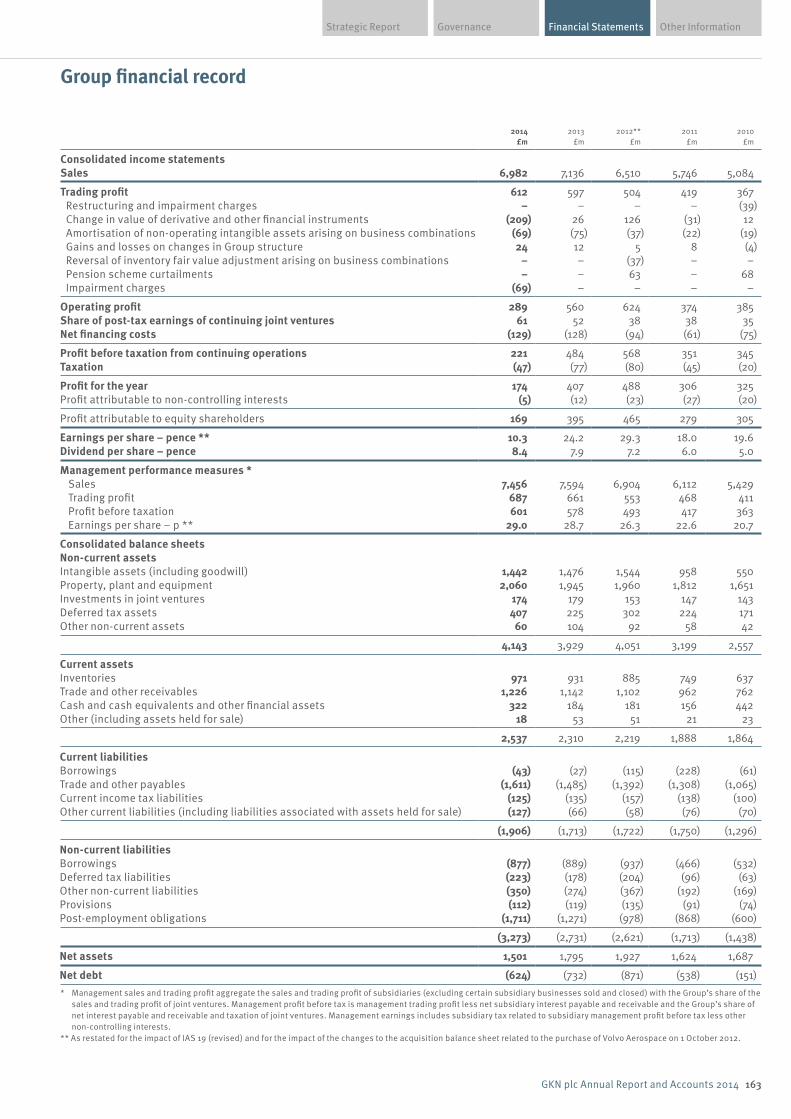

FINANCIAL STATEMENTSIndependent auditors’ report (Group) 103Group financial statements 111Independent auditors’ report (Company) 158Company financial statements 160Group financial record 163

OTHER INFORMATIONKey subsidiaries and joint ventures 164Shareholder information 166Contact information IBC

Pages 60 to 102 comprise the Directors’ report.

02 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 22 – 37 for more information on our divisions

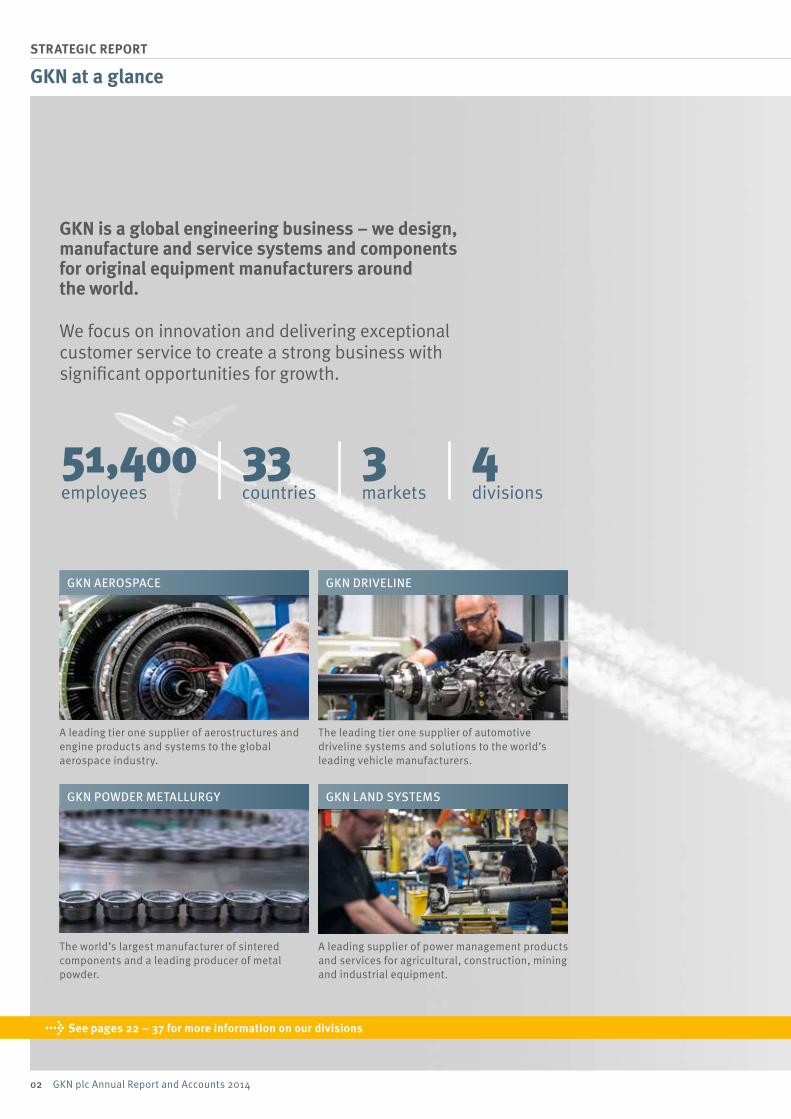

GKN is a global engineering business – we design, manufacture and service systems and components for original equipment manufacturers around the world.

We focus on innovation and delivering exceptional customer service to create a strong business with significant opportunities for growth.

51,400employees

33countries

3markets

4divisions

A leading tier one supplier of aerostructures and engine products and systems to the global aerospace industry.

The world’s largest manufacturer of sintered components and a leading producer of metal powder.

The leading tier one supplier of automotive driveline systems and solutions to the world’s leading vehicle manufacturers.

A leading supplier of power management products and services for agricultural, construction, mining and industrial equipment.

GKN at a glance

GKN DRIVELINEGKN AEROSPACE

GKN POWDER METALLURGY GKN LAND SYSTEMS

Financial Statements Other InformationGovernanceStrategic Report

03GKN plc Annual Report and Accounts 2014

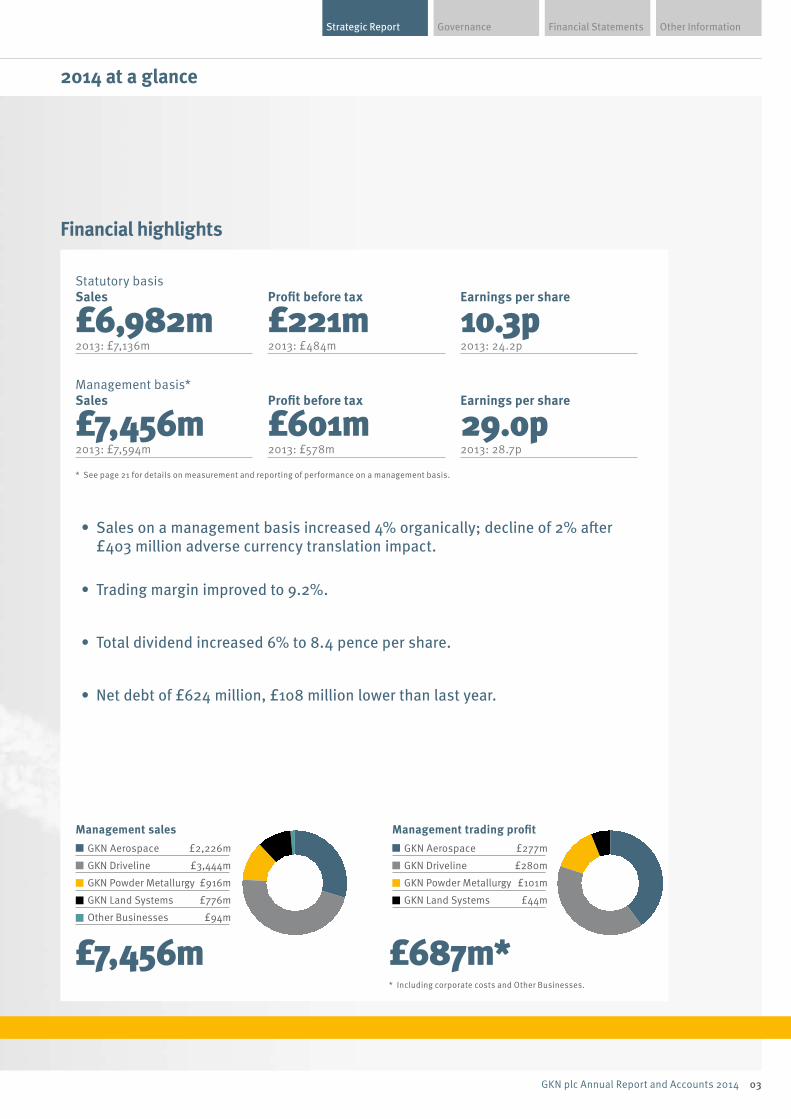

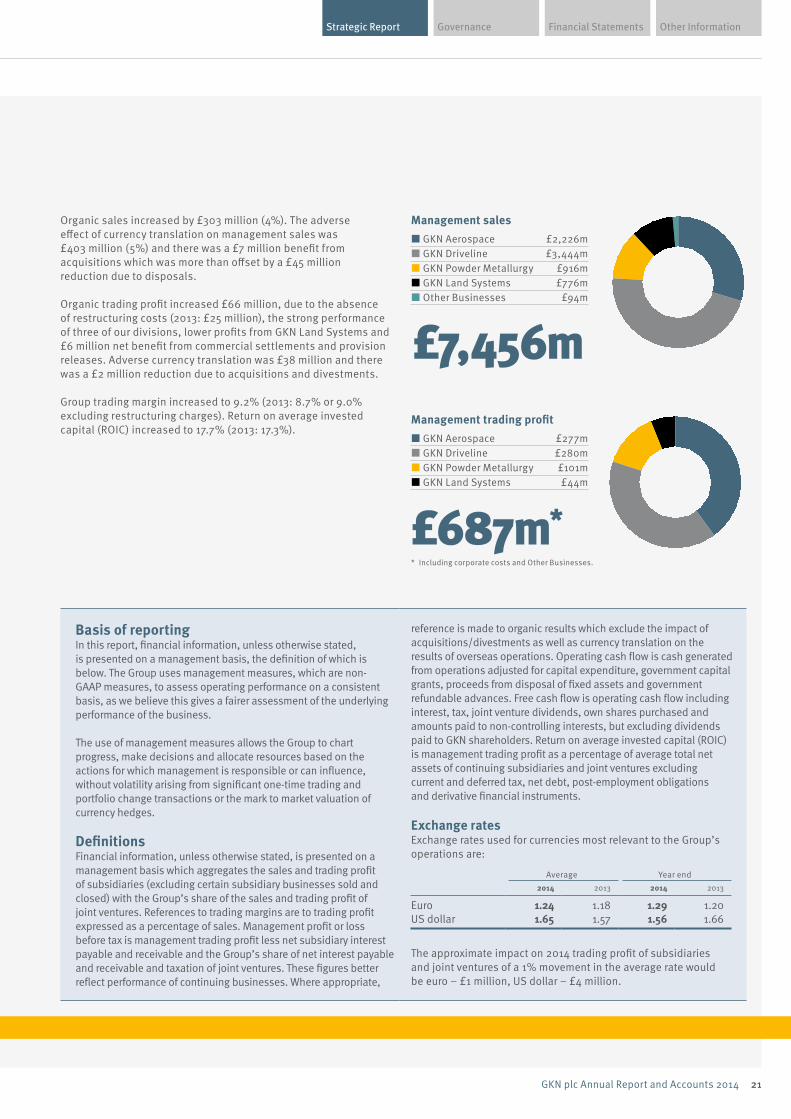

GKN Aerospace £2,226m

GKN Driveline £3,444m

GKN Powder Metallurgy £916m

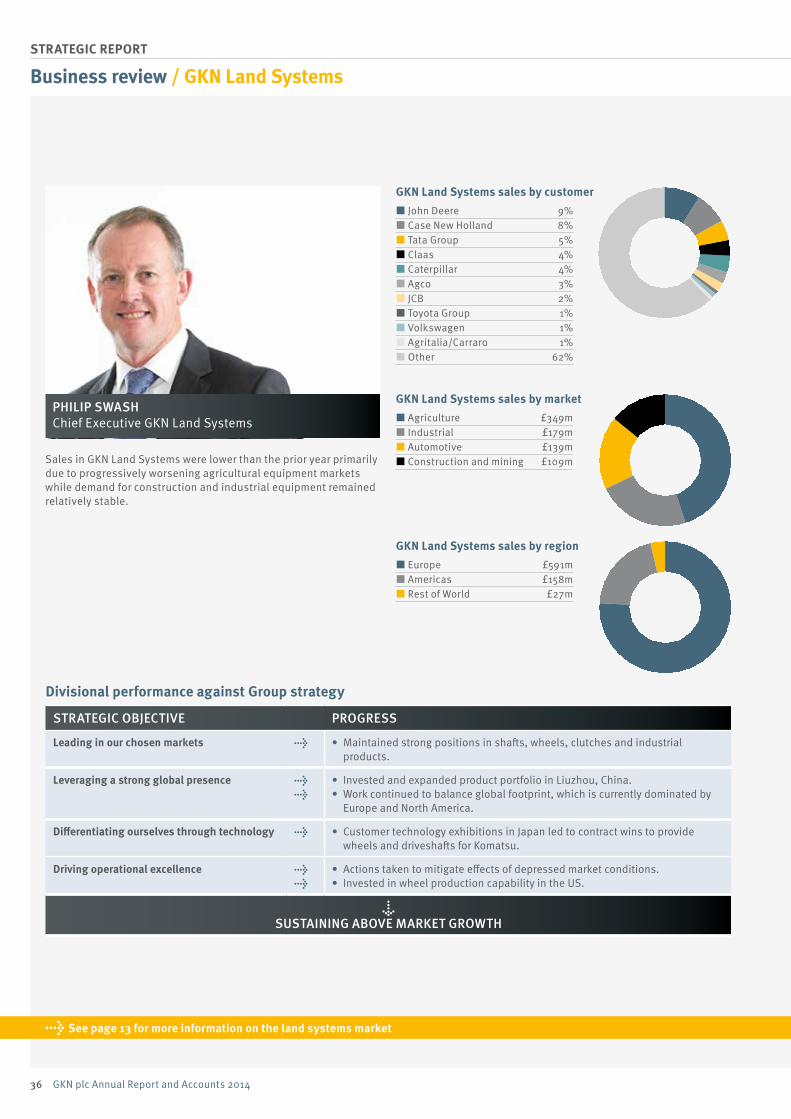

GKN Land Systems £776m

Other Businesses £94m

Management salesGKN Aerospace £277m

GKN Driveline £280m

GKN Powder Metallurgy £101m

GKN Land Systems £44m

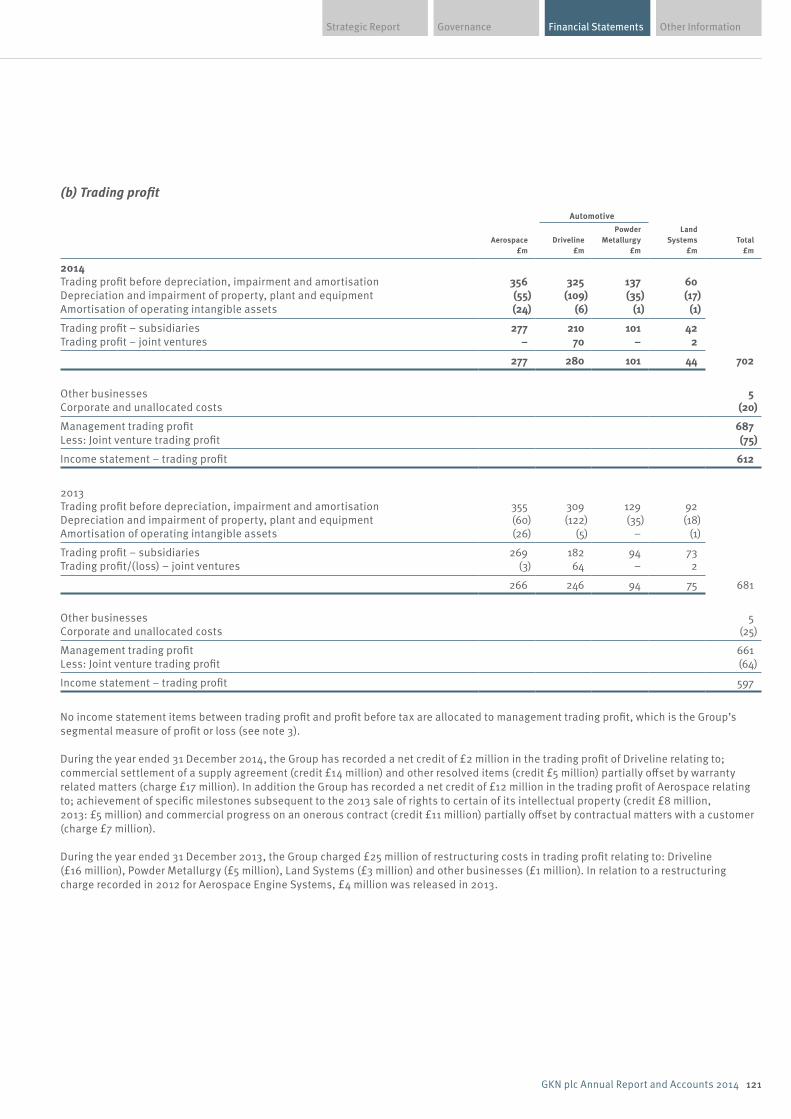

Management trading pro�t

2014 at a glance

Financial highlights

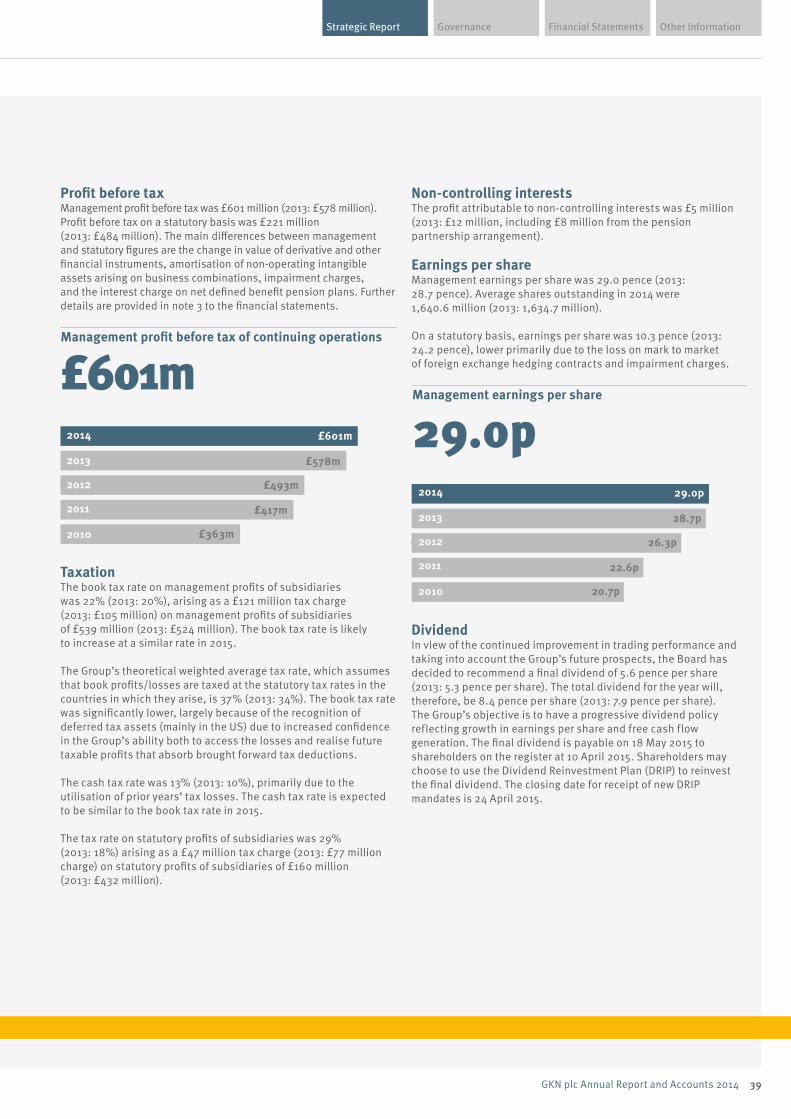

£687m*

Statutory basisSales Profit before tax Earnings per share

£6,982m £221m 10.3p2013: £7,136m 2013: £484m 2013: 24.2p

Management basis*Sales Profit before tax Earnings per share

£7,456m £601m 29.0p2013: £7,594m 2013: £578m 2013: 28.7p

* See page 21 for details on measurement and reporting of performance on a management basis.

£7,456m

• Sales on a management basis increased 4% organically; decline of 2% after £403 million adverse currency translation impact.

• Trading margin improved to 9.2%.

• Total dividend increased 6% to 8.4 pence per share.

• Net debt of £624 million, £108 million lower than last year.

* Including corporate costs and Other Businesses.

04 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

North America 63Asia

South America

1manufacturinglocation

1manufacturinglocations

Australia

Europe

Africa

1manufacturinglocation 5manufacturing

locations

5manufacturinglocations 29 manufacturing

locations

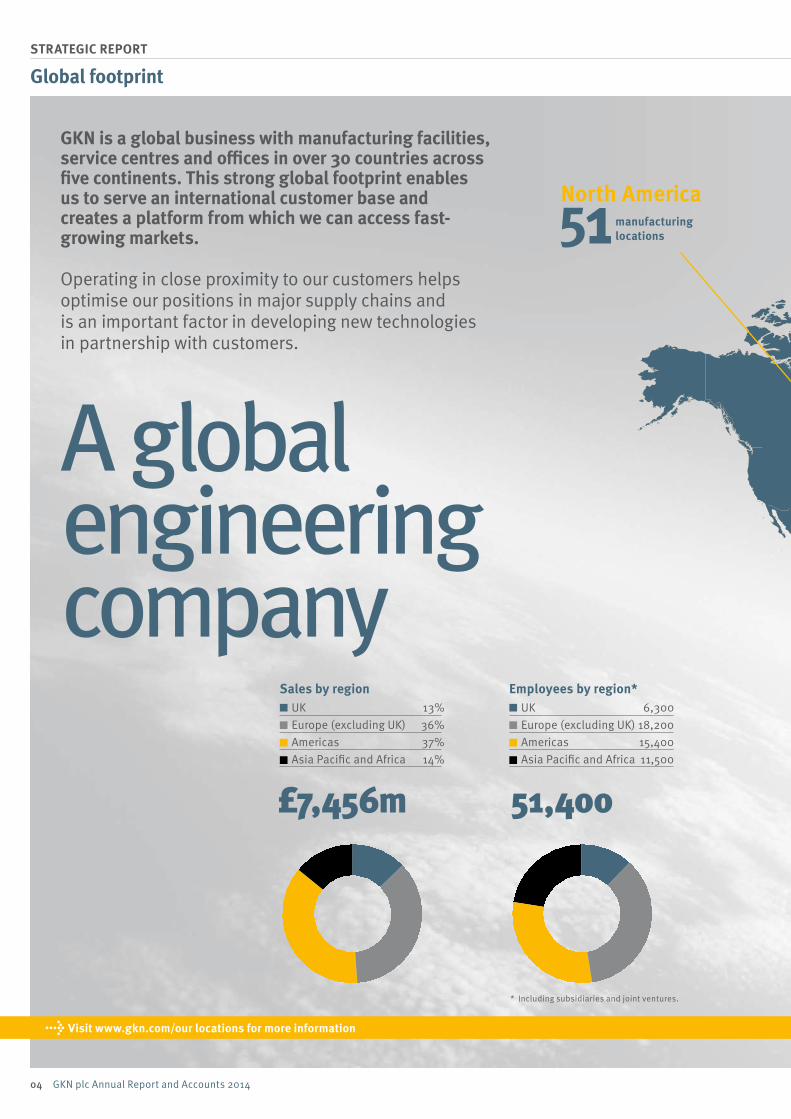

UK 13%Europe (excluding UK) 36%Americas 37%Asia Paci�c and Africa 14%

Sales by regionUK 6,300Europe (excluding UK) 18,200Americas 15,400Asia Paci�c and Africa 11,500

Employees by region*

→ Visit www.gkn.com/our locations for more information

Global footprint

GKN is a global business with manufacturing facilities, service centres and offices in over 30 countries across five continents. This strong global footprint enables us to serve an international customer base and creates a platform from which we can access fast-growing markets.

Operating in close proximity to our customers helps optimise our positions in major supply chains and is an important factor in developing new technologies in partnership with customers.

A global engineering company

£7,456m 51,400

* Including subsidiaries and joint ventures.

Financial Statements Other InformationGovernanceStrategic Report

05GKN plc Annual Report and Accounts 2014

North America 63Asia

South America

1manufacturinglocation

1manufacturinglocations

Australia

Europe

Africa

1manufacturinglocation 5manufacturing

locations

5manufacturinglocations 29 manufacturing

locations

06 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

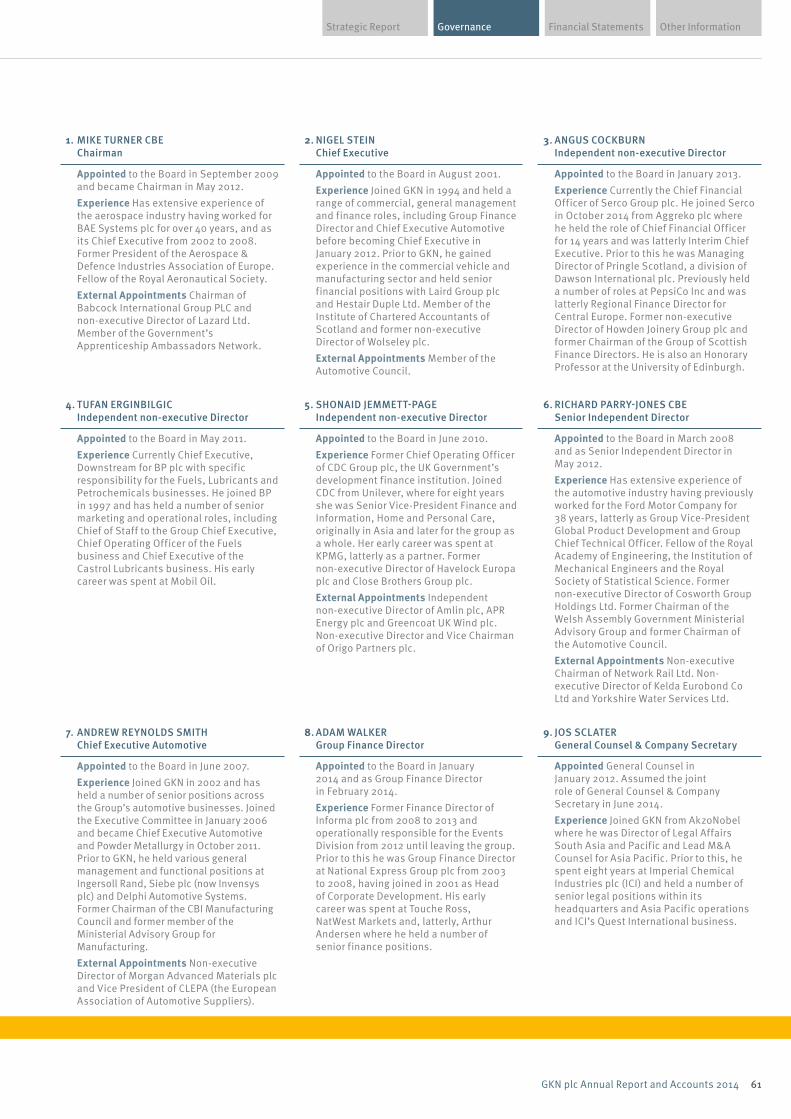

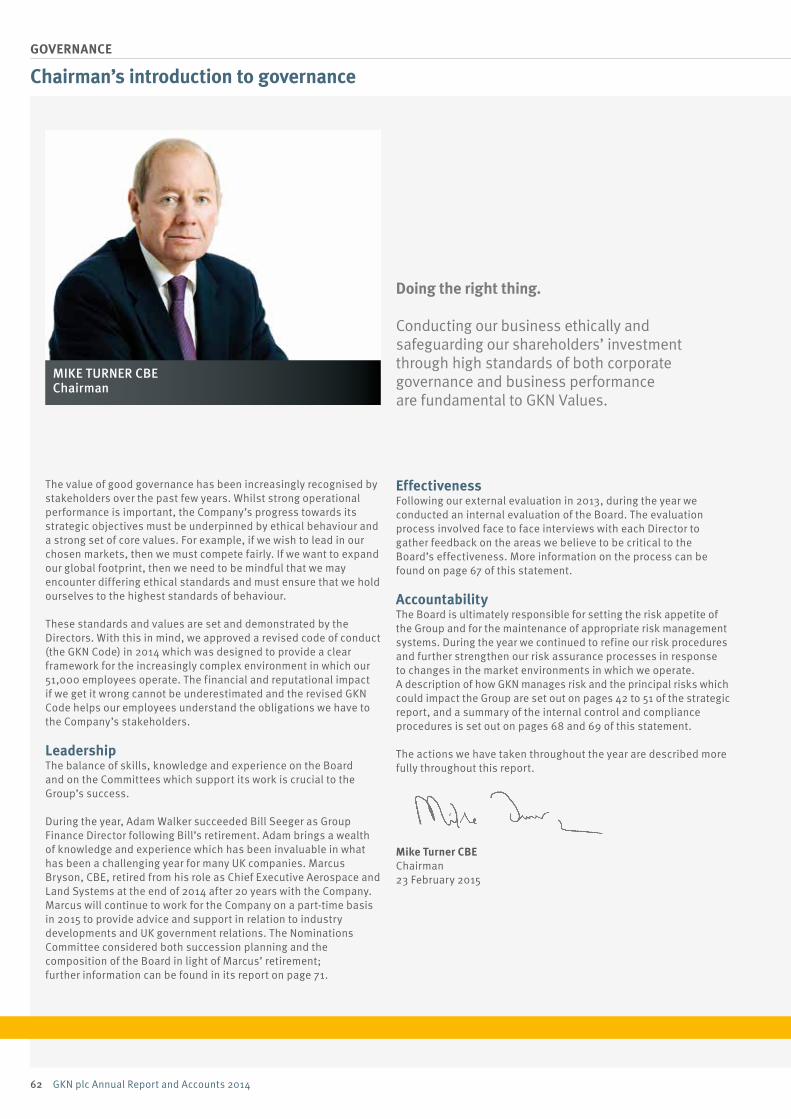

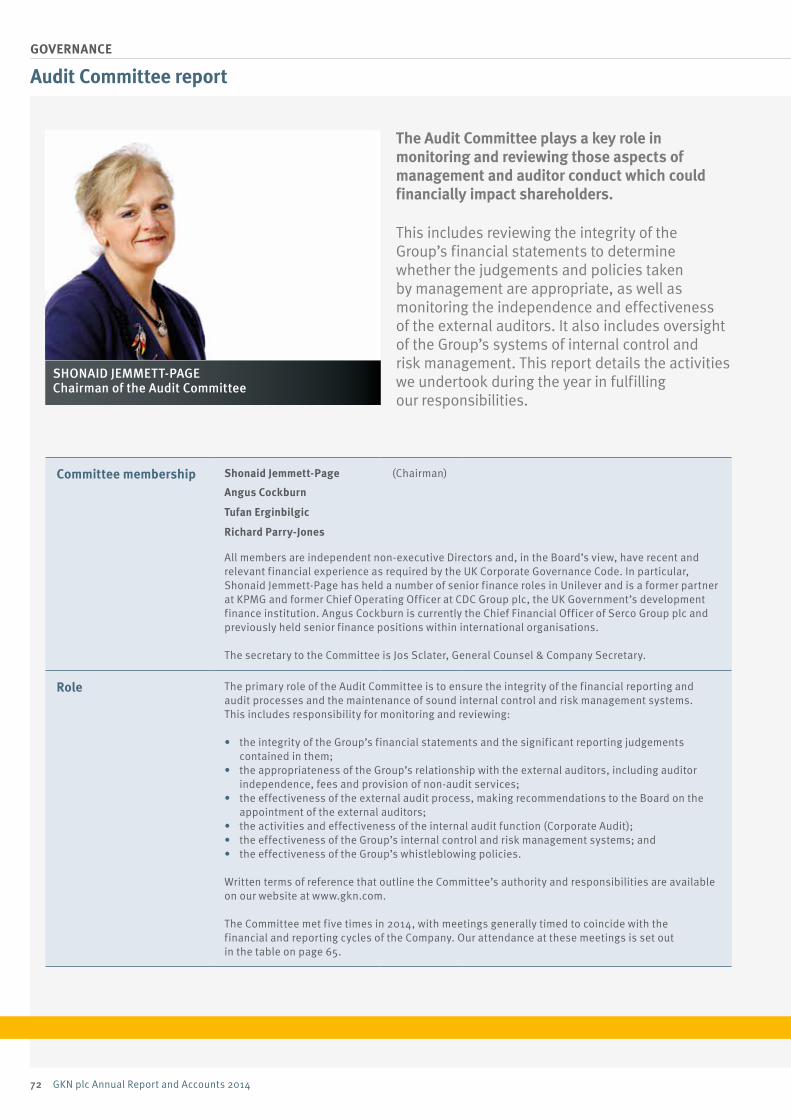

MIKE TURNER CBECHAIRMAN

→ See pages 20-41 for more information on our financial results

Chairman’s statement

Results and dividend2014 was another year of progress for GKN. We have delivered a good set of results. I am particularly pleased with the results because in some respects 2014 was not a straightforward year: we faced considerable currency headwinds with sterling unusually strong against all major currencies for much of the year, the agricultural market fell sharply and the military aerospace market continued to decline. Despite this, we have grown both our organic sales and overall profit. This shows the resilience of our business model and strength of our strategy.

We have continued with our progressive dividend policy and are recommending a final dividend of 5.6 pence per share, making a total of 8.4 pence per share for the year, an increase of 6% over the prior year. Over the course of the past five years we have seen the dividend rise 68% from 5.0 pence per share in 2010 to 8.4 pence in respect of 2014.

Continued progress

Our strategyOur strategy is central to the year’s good results. We successfully positioned our automotive businesses to grow above the market and in 2014 they grew 8% organically compared to market growth of 3%. We have repositioned our aerospace business so that 73% is now in the higher growth commercial sector, compared to just 42% in 2007. Following the successful acquisition and integration as a whole of Volvo Aero, we have a leading aerospace engine systems business with excellent exposure to some fast-growing platforms. In the medium term our aerospace business is very well positioned to take advantage of growing platforms such as the Boeing 787, the A350 and the F-35 Joint Strike Fighter.

Each year we seek to improve our strategy process. In 2014 we refined how we review and develop the Group’s strategic objectives by increasing our focus on long term market, economic and technology trends. There are some exciting changes ahead of us, including the increasing electrification of vehicles and the use of additive manufacturing in aerospace. We continue to invest to take advantage of the opportunities presented by these changes. Our strategic objectives are described in further detail on page 9.

“ We are a long term business with the right strategy.”

Financial Statements Other InformationGovernanceStrategic Report

07GKN plc Annual Report and Accounts 2014

We did not make any major acquisitions in 2014, taking a disciplined approach to potential opportunities and choosing to focus on thoroughly integrating our engine systems business following the acquisition of Volvo Aero in 2012. During 2014 we were awarded investment grade status with all three of the major rating agencies and continued to pay down our debt. We are now in a strong position to make further acquisitions, but will continue to take a focused approach.

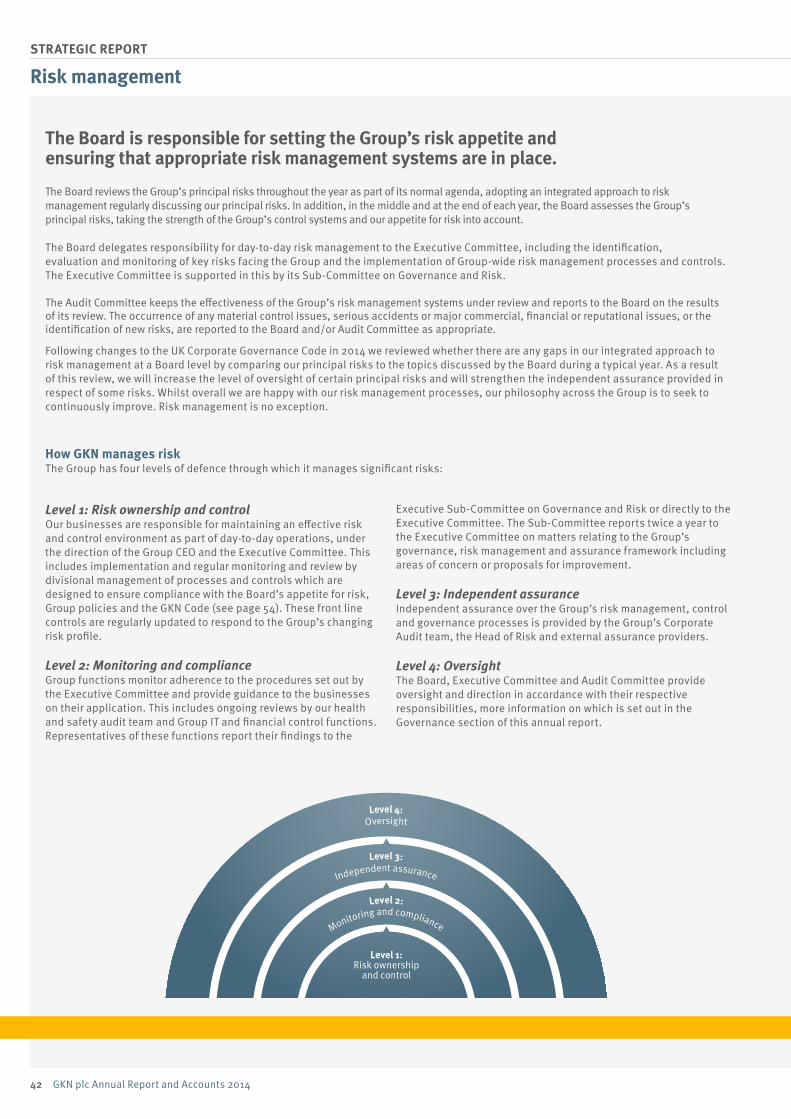

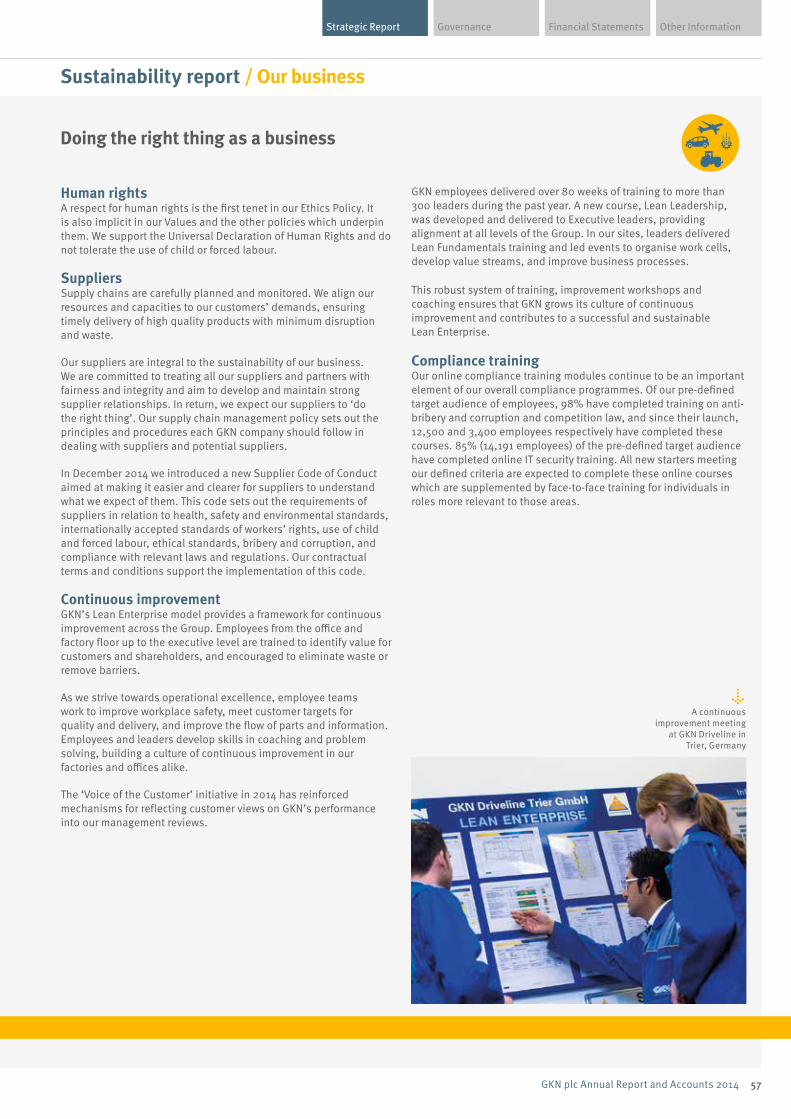

Sustainability and riskGKN has a long history of behaving ethically; of doing the right thing. We recognise that we continuously need to ensure that we set the right tone from the top and engage with our people to ensure that they understand the behaviours that we expect of them. For this reason we revised the GKN Code during 2014, making it clearer and more engaging, and updating it to bring additional focus to areas such as diversity and inclusion, and quality. We have also strengthened our diversity and inclusion programme, which is visibly supported by the Board, and we have worked hard to improve quality and product safety through the ‘Voice of the Customer’ initiative described by Nigel on page 18.

We have well developed risk management processes, but are not complacent and note the emphasis on risk management in the revised 2014 UK Corporate Governance Code. We continue to work to improve our risk management processes and control systems. We have described our work in this area in greater detail on pages 42-51.

The BoardAdam Walker joined the Board at the start of 2014 and quickly became an effective member of the team. I am confident that he will be an asset to the Company. On 31 December 2014 Marcus Bryson CBE retired from his role as Chief Executive Aerospace and Land Systems and from the Board. Marcus joined GKN in 1994 and since then his contribution to the creation of the GKN we see today, and in particular our aerospace division, has been significant. He fully deserves the CBE recently awarded for his contribution to the UK aerospace industry. We have not replaced Marcus on the Board for now and have chosen instead to strengthen the Executive Committee with the appointment of Kevin Cummings, CEO GKN Aerospace, Peter Oberparleiter, CEO GKN Powder Metallurgy, and Philip Swash, CEO GKN Land Systems. They will regularly attend Board meetings to

ensure that the Board continues to have a good feel for what is happening in each division. The Board has real diversity of experience and technical expertise, and the Board dynamic continues to be excellent with all Directors making a valuable contribution.

Our peopleMeeting a wide range of customer expectations is never easy, but GKN’s culture is to persevere and through the commitment of our people we have delivered a good set of results. They have again demonstrated GKN’s resilience and ability to grow above the market. I would like to take this opportunity to thank them for all that they have done.

I have written in the past about a pressing need for a global talent pool that is well stocked with young people with the necessary scientific and mathematical skills. That remains the case and I am glad to report that around the world GKN continues to engage in hundreds of local initiatives designed to encourage young people to choose engineering as a possible future career.

Looking forwardAs we enter 2015, political and economic uncertainty will continue to affect GKN. But we are a long term business with the right strategy. I am therefore confident that the Group will continue to grow and generate sustainable returns for our shareholders during 2015 and beyond.

Mike Turner CBEChairman

08 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 10 – 11 for more information on our business model

Our strategic framework

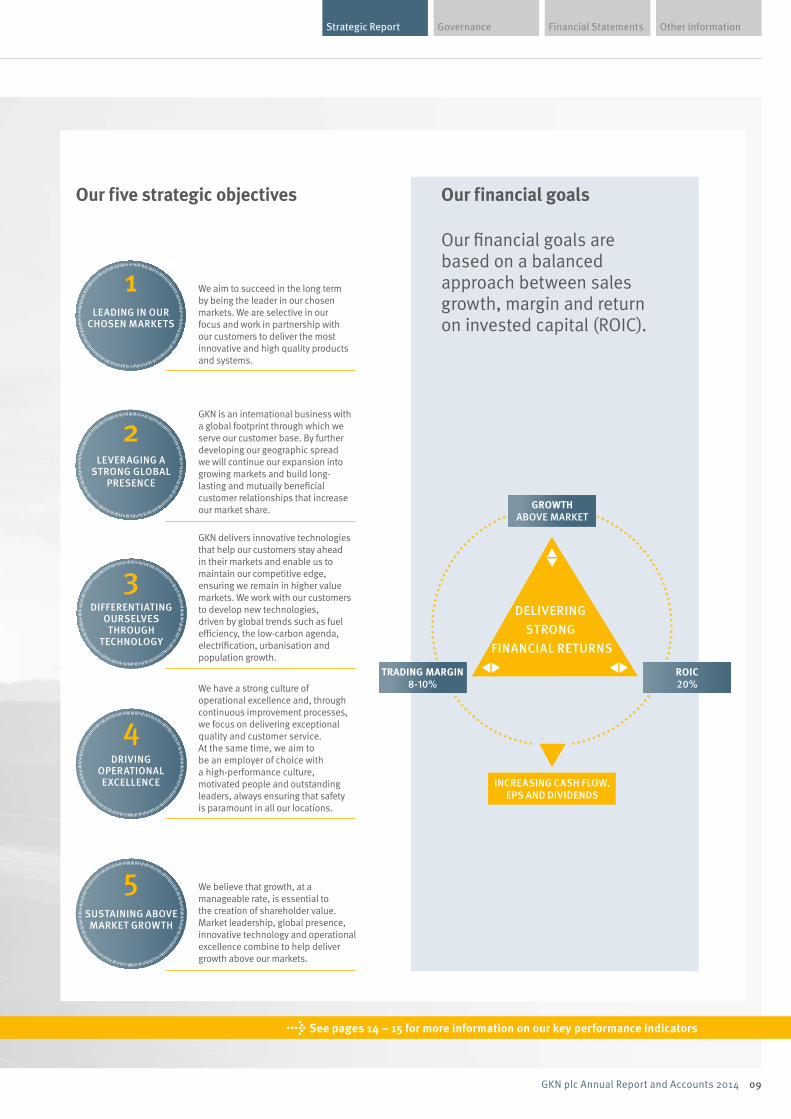

We aim to create long term and sustainable shareholder value in the form of steadily growing earnings and dividends through the delivery of growth in sales, rising profitability and increasing return on invested capital.

We have excellent positions in long term global growth markets and build strong relationships with international original equipment manufacturers (OEMs) and prime contractors. To create value we have five strategic objectives.

Creating sustainable value

Financial Statements Other InformationGovernanceStrategic Report

09GKN plc Annual Report and Accounts 2014

LEVERAGING A STRONG GLOBAL

PRESENCE

2

1LEADING IN OUR

CHOSEN MARKETS

DRIVING OPERATIONAL EXCELLENCE

4

5SUSTAINING ABOVE MARKET GROWTH

DIFFERENTIATING OURSELVESTHROUGH

TECHNOLOGY

3DELIVERING

STRONG FINANCIAL RETURNS

TRADING MARGIN8-10%

GROWTHABOVE MARKET

INCREASING CASH FLOW,EPS AND DIVIDENDS

ROIC20%

→ See pages 14 – 15 for more information on our key performance indicators

Our financial goals are based on a balanced approach between sales growth, margin and return on invested capital (ROIC).

Our five strategic objectives

We aim to succeed in the long term by being the leader in our chosen markets. We are selective in our focus and work in partnership with our customers to deliver the most innovative and high quality products and systems.

GKN is an international business with a global footprint through which we serve our customer base. By further developing our geographic spread we will continue our expansion into growing markets and build long-lasting and mutually beneficial customer relationships that increase our market share.

We believe that growth, at a manageable rate, is essential to the creation of shareholder value. Market leadership, global presence, innovative technology and operational excellence combine to help deliver growth above our markets.

We have a strong culture of operational excellence and, through continuous improvement processes, we focus on delivering exceptional quality and customer service. At the same time, we aim to be an employer of choice with a high-performance culture, motivated people and outstanding leaders, always ensuring that safety is paramount in all our locations.

GKN delivers innovative technologies that help our customers stay ahead in their markets and enable us to maintain our competitive edge, ensuring we remain in higher value markets. We work with our customers to develop new technologies, driven by global trends such as fuel efficiency, the low-carbon agenda, electrification, urbanisation and population growth.

Our financial goals

10 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 8 – 9 for more information on our strategic framework

Our business model

Our business model supports our strategy to create long term and sustainable value for shareholders. It highlights how we combine our advanced engineering value chain in global markets with our strong core competencies and clear values.

Our business modelStrong core competencies GKN’s extensive industry know-how, engineering capability and strong customer relationships are central to our value chain and ensure we are well positioned to sustain above market growth and deliver strong financial returns.

Industry know-howUnderstanding our markets and working closely with our customers, academic institutions and government agencies to identify future technology requirements gives us the expertise to deliver market-leading solutions and provides continued opportunities for sustainable growth.

Engineering capabilityWe are committed to developing and maintaining a diverse range of engineering talent across the Group and continually investing in technology to enable the efficient design and delivery of high quality, innovative solutions.

Strong customer relationshipsWe work in partnership with our customers, wherever they are in the world, to deliver customer-valued innovation and exceptional service. Listening to feedback and constantly striving to improve our products and processes helps us build and maintain these strong relationships.

Financial Statements Other InformationGovernanceStrategic Report

11GKN plc Annual Report and Accounts 2014

STRONG CORE COMPETENCIES

• Industry know-how• Engineering capability

• Strong customer relationships

GLOBAL MARKETS• Aerospace• Automotive

• Land systems

CLEAR VALUES• By our people• As a business• In our world

→ P.52–59

DELIVERING STRONG

FINANCIAL RETURNS

→ P.10 → P.12–13

DESIGNING NEW PRODUCTS AND SOLUTIONS

Investment in technology, together with an understanding of market

trends and customer needs, helps GKN create innovative high quality products that are efficient, sustainable and cost effective for our customers, and that deliver

benefits to end consumers.

WINNING NEW BUSINESSOur strong engineering capability,

global footprint and innovative solutions enable us to win

business by offering value to our customers.

SOURCING MATERIALS AND PRODUCTS

Our well-developed supply chain provides GKN with a reliable

source of key raw materials and components, and is supported

by processes that assist the decision to make in-house or

buy externally.

APPLYING LEAN MANUFACTURINGWe focus on continuous

improvement and reducing waste in our production processes around

the world, as well as providing a safe working environment and minimising our impact on our

environment.

DELIVERING HIGH QUALITY PRODUCTS

We deliver high quality products to the right place at the right time all over the world. These products

meet specific consumer needs, which help us to build strong

customer relationships.

12 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

GLOBAL MARKETS• Aerospace

• Automotive • Land systems

→ See pages 24, 28 and 36 for more information on our markets

The world population is expected to reach over nine billion by 2050, an increase of more than two billion from today’s level, with growth mainly in urban areas.

Our business model / Global markets

Population growth drives change across our markets: increased demand for flights and larger aircraft, changes in the types of car people drive and the number of cars on the roads, a requirement for increased farming efficiency to help double global agricultural production, as well as infrastructure development in cities. All of this influences our product development and offers significant growth opportunities.

There is also the continual drive to improve the fuel efficiency of aircraft, cars and other vehicles, while at the same time increasing manufacturing efficiency and product safety. Demand for fuel-efficient solutions remains high due to concerns over CO2 emissions and air quality. Advanced electric and hybrid alternatives are replacing traditional mechanical processes and GKN has specific expertise in electric and hybrid vehicle technology and electrically-driven machinery which help our customers meet this challenge.

Manufacturers are increasingly opting for lightweight designs and materials. Composite aerostructures and engine components are already relatively common on new platforms, while in the automotive industry, components are being designed to reduce weight and size. Development work is underway in both sectors to increase the opportunities for lightweight materials. GKN has significant know-how in lightweight materials and increasingly in advanced production technologies such as ‘Design for Powder Metallurgy’ and additive manufacturing that offer the opportunity to optimise product design.

9.6bn Global population by 2050(a)

Global markets

Financial Statements Other InformationGovernanceStrategic Report

13GKN plc Annual Report and Accounts 2014

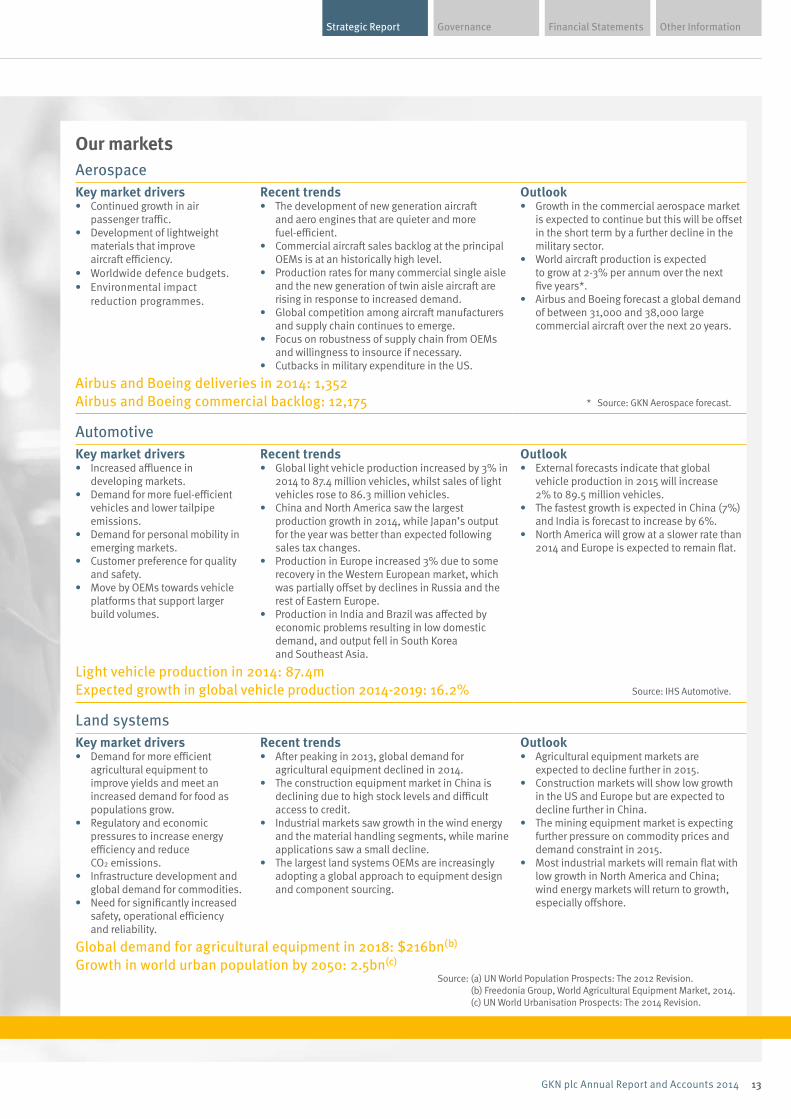

Our marketsAerospaceKey market drivers• Continued growth in air

passenger traffic.• Development of lightweight

materials that improve aircraft efficiency.

• Worldwide defence budgets.• Environmental impact

reduction programmes.

Recent trends• The development of new generation aircraft

and aero engines that are quieter and more fuel-efficient.

• Commercial aircraft sales backlog at the principal OEMs is at an historically high level.

• Production rates for many commercial single aisle and the new generation of twin aisle aircraft are rising in response to increased demand.

• Global competition among aircraft manufacturers and supply chain continues to emerge.

• Focus on robustness of supply chain from OEMs and willingness to insource if necessary.

• Cutbacks in military expenditure in the US.

Outlook• Growth in the commercial aerospace market

is expected to continue but this will be offset in the short term by a further decline in the military sector.

• World aircraft production is expected to grow at 2-3% per annum over the next five years*.

• Airbus and Boeing forecast a global demand of between 31,000 and 38,000 large commercial aircraft over the next 20 years.

Airbus and Boeing deliveries in 2014: 1,352 Airbus and Boeing commercial backlog: 12,175 * Source: GKN Aerospace forecast.

AutomotiveKey market drivers• Increased affluence in

developing markets.• Demand for more fuel-efficient

vehicles and lower tailpipe emissions.

• Demand for personal mobility in emerging markets.

• Customer preference for quality and safety.

• Move by OEMs towards vehicle platforms that support larger build volumes.

Recent trends• Global light vehicle production increased by 3% in

2014 to 87.4 million vehicles, whilst sales of light vehicles rose to 86.3 million vehicles.

• China and North America saw the largest production growth in 2014, while Japan’s output for the year was better than expected following sales tax changes.

• Production in Europe increased 3% due to some recovery in the Western European market, which was partially offset by declines in Russia and the rest of Eastern Europe.

• Production in India and Brazil was affected by economic problems resulting in low domestic demand, and output fell in South Korea and Southeast Asia.

Outlook• External forecasts indicate that global

vehicle production in 2015 will increase 2% to 89.5 million vehicles.

• The fastest growth is expected in China (7%) and India is forecast to increase by 6%.

• North America will grow at a slower rate than 2014 and Europe is expected to remain flat.

Light vehicle production in 2014: 87.4mExpected growth in global vehicle production 2014-2019: 16.2% Source: IHS Automotive.

Land systemsKey market drivers• Demand for more efficient

agricultural equipment to improve yields and meet an increased demand for food as populations grow.

• Regulatory and economic pressures to increase energy efficiency and reduce CO2 emissions.

• Infrastructure development and global demand for commodities.

• Need for significantly increased safety, operational efficiency and reliability.

Recent trends • After peaking in 2013, global demand for

agricultural equipment declined in 2014.• The construction equipment market in China is

declining due to high stock levels and difficult access to credit.

• Industrial markets saw growth in the wind energy and the material handling segments, while marine applications saw a small decline.

• The largest land systems OEMs are increasingly adopting a global approach to equipment design and component sourcing.

Outlook• Agricultural equipment markets are

expected to decline further in 2015.• Construction markets will show low growth

in the US and Europe but are expected to decline further in China.

• The mining equipment market is expecting further pressure on commodity prices and demand constraint in 2015.

• Most industrial markets will remain flat with low growth in North America and China; wind energy markets will return to growth, especially offshore.

Global demand for agricultural equipment in 2018: $216bn(b)

Growth in world urban population by 2050: 2.5bn(c)

Source: (a) UN World Population Prospects: The 2012 Revision. (b) Freedonia Group, World Agricultural Equipment Market, 2014. (c) UN World Urbanisation Prospects: The 2014 Revision.

14 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

2014

2013

2012

2011

2010

£7,456m

£7,594m

£6,904m

£6,112m

£5,429m

2014

2013

2012

2011

2010

29.0p

28.7p

26.3p

22.6p

20.7p

8.4p

7.9p

7.2p

6.0p

5.0p

2014

2013

2012

2011

2010

9.2%

8.7%

8.0%

7.7%

7.6%

17.7%

17.3%

18.0%

18.3%

17.0%

2014

2013

2012

2011

2010

£234m

£346m

£225m

£147m

£188m

2014

2013

2012

2011

2010

2014

2013

2012

2011

2010

2014

2013

2012

[00]

3.2%

3.1%

DELIVERING STRONG

FINANCIAL RETURNS

TRADING MARGIN8-10%

GROWTHABOVE MARKET

INCREASING CASH FLOW,EPS AND DIVIDENDS

ROIC20%

→ See pages 20 – 41 for more information on our financial results

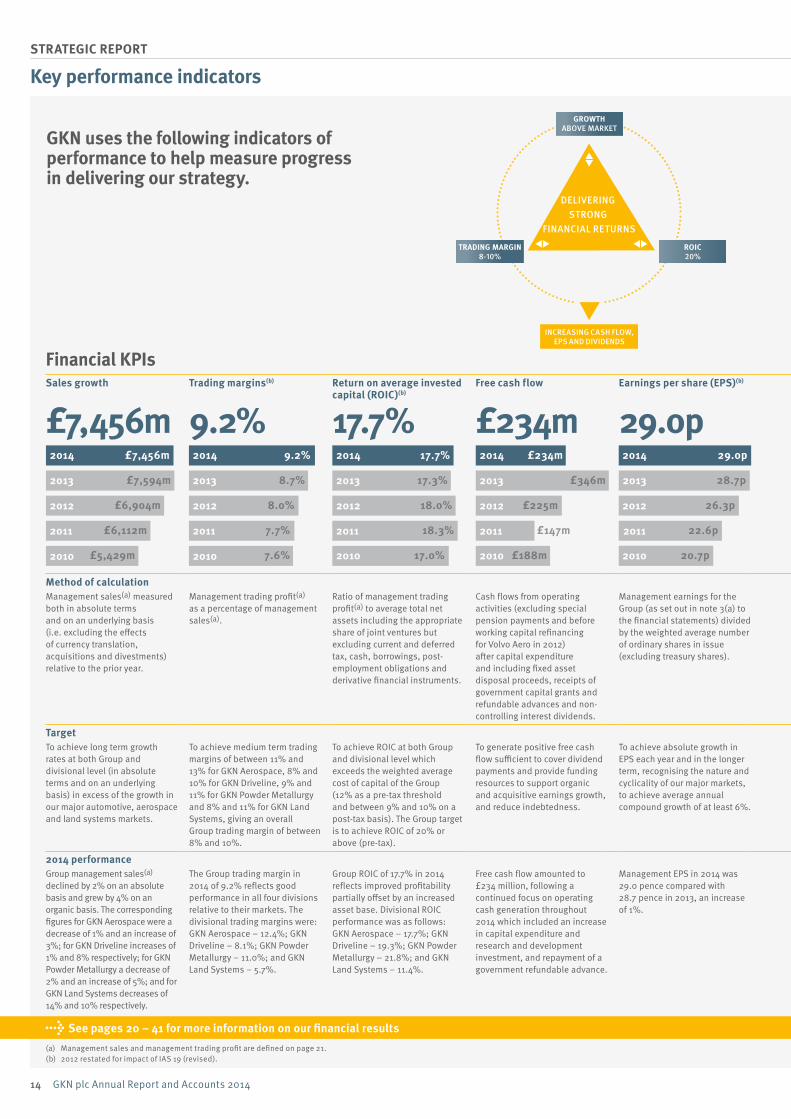

Key performance indicators

GKN uses the following indicators of performance to help measure progress in delivering our strategy.

Financial KPIsSales growth Trading margins(b) Return on average invested

capital (ROIC)(b) Free cash flow Earnings per share (EPS)(b) Dividend per share

£7,456m 9.2% 17.7% £234m 29.0p 8.4p

Method of calculation Management sales(a) measured both in absolute terms and on an underlying basis (i.e. excluding the effects of currency translation, acquisitions and divestments) relative to the prior year.

Management trading profit(a) as a percentage of management sales(a).

Ratio of management trading profit(a) to average total net assets including the appropriate share of joint ventures but excluding current and deferred tax, cash, borrowings, post-employment obligations and derivative financial instruments.

Cash flows from operating activities (excluding special pension payments and before working capital refinancing for Volvo Aero in 2012) after capital expenditure and including fixed asset disposal proceeds, receipts of government capital grants and refundable advances and non-controlling interest dividends.

Management earnings for the Group (as set out in note 3(a) to the financial statements) divided by the weighted average number of ordinary shares in issue (excluding treasury shares).

Amount declared as payable by way of dividend divided by the number of ordinary shares in issue (excluding treasury shares).

Target To achieve long term growth rates at both Group and divisional level (in absolute terms and on an underlying basis) in excess of the growth in our major automotive, aerospace and land systems markets.

To achieve medium term trading margins of between 11% and 13% for GKN Aerospace, 8% and 10% for GKN Driveline, 9% and 11% for GKN Powder Metallurgy and 8% and 11% for GKN Land Systems, giving an overall Group trading margin of between 8% and 10%.

To achieve ROIC at both Group and divisional level which exceeds the weighted average cost of capital of the Group (12% as a pre-tax threshold and between 9% and 10% on a post-tax basis). The Group target is to achieve ROIC of 20% or above (pre-tax).

To generate positive free cash flow sufficient to cover dividend payments and provide funding resources to support organic and acquisitive earnings growth, and reduce indebtedness.

To achieve absolute growth in EPS each year and in the longer term, recognising the nature and cyclicality of our major markets, to achieve average annual compound growth of at least 6%.

To maintain a progressive dividend policy aligning dividends with the long term trend in management earnings and reflecting growth in earnings per share and free cash flow generation.

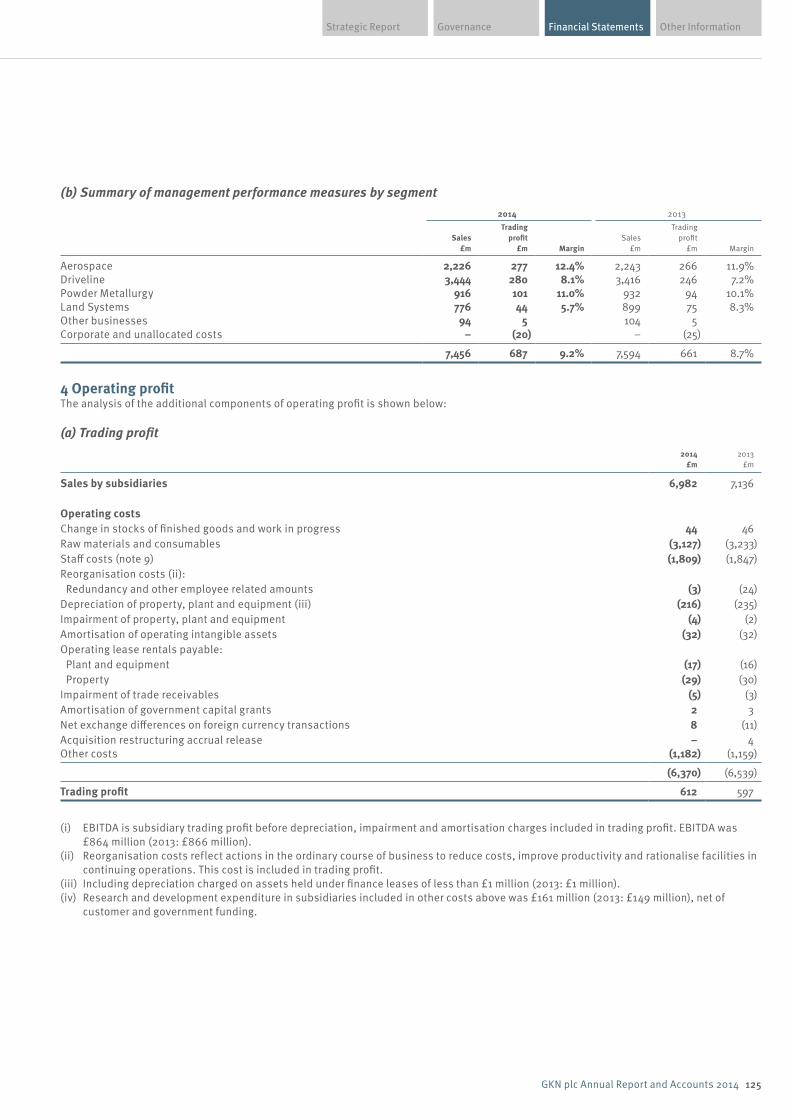

2014 performance Group management sales(a) declined by 2% on an absolute basis and grew by 4% on an organic basis. The corresponding figures for GKN Aerospace were a decrease of 1% and an increase of 3%; for GKN Driveline increases of 1% and 8% respectively; for GKN Powder Metallurgy a decrease of 2% and an increase of 5%; and for GKN Land Systems decreases of 14% and 10% respectively.

The Group trading margin in 2014 of 9.2% reflects good performance in all four divisions relative to their markets. The divisional trading margins were: GKN Aerospace – 12.4%; GKN Driveline – 8.1%; GKN Powder Metallurgy – 11.0%; and GKN Land Systems – 5.7%.

Group ROIC of 17.7% in 2014 reflects improved profitability partially offset by an increased asset base. Divisional ROIC performance was as follows: GKN Aerospace – 17.7%; GKN Driveline – 19.3%; GKN Powder Metallurgy – 21.8%; and GKN Land Systems – 11.4%.

Free cash flow amounted to £234 million, following a continued focus on operating cash generation throughout 2014 which included an increase in capital expenditure and research and development investment, and repayment of a government refundable advance.

Management EPS in 2014 was 29.0 pence compared with 28.7 pence in 2013, an increase of 1%.

Dividend per share increased in 2014 reflecting positive earnings and cash performance. The dividend for the year, at 8.4 pence, is covered 3.4 times by management earnings and 1.7 times by free cash flow.

(a) Management sales and management trading profit are defined on page 21. (b) 2012 restated for impact of IAS 19 (revised).

Financial Statements Other InformationGovernanceStrategic Report

15GKN plc Annual Report and Accounts 2014

2014

2013

2012

2011

2010

£7,456m

£7,594m

£6,904m

£6,112m

£5,429m

2014

2013

2012

2011

2010

29.0p

28.7p

26.3p

22.6p

20.7p

8.4p

7.9p

7.2p

6.0p

5.0p

2014

2013

2012

2011

2010

9.2%

8.7%

8.0%

7.7%

7.6%

17.7%

17.3%

18.0%

18.3%

17.0%

2014

2013

2012

2011

2010

£234m

£346m

£225m

£147m

£188m

2014

2013

2012

2011

2010

2014

2013

2012

2011

2010

2014

2013

2012

[00]

3.2%

3.1%

Non-financial KPIsNon-financial KPIs help measure the sustainability of our business and progress towards operational excellence. We strive to operate in a safe, efficient and ethical manner, and at the same time aim to be an employer of choice and make a positive impact on the environment and the communities in which we operate.

More information can be found in the sustainability report on pages 52-59.

Health and safety performance Per 1,000 employees Method of calculation Accident frequency rate (AFR) measured as the number of lost time accidents per 1,000 employees and accident severity rate (ASR) measured as the number of days/shifts lost due to accidents and occupational ill health per 1,000 employees. TargetZero preventable accidents. 2014 performance AFR reduced to 1.3 (2013: 1.6). However ASR saw a small increase to 46 (2013: 40), primarily due to specific occupational health issues of three employees in North America. More information can be found on page 54.

Environmental performance Main impacts on the environment Method of calculation Energy consumption and associated CO2 emissions, waste generation, waste recycled and water consumption measured on a divisional basis per unit of production and against sales in GKN Aerospace. Target Improved year-on-year performance across all KPIs, with a 15% improvement in energy efficiency from 2009 to 2014. 2014 performance Environmental performance in 2014 was in line with expectations, with most divisions achieving improved results in energy consumption, CO2 emissions, waste and water consumption. Group energy efficiency decreased by 4% over 2013, primarily due to currency fluctuations depressing statutory sales, but improved by 16% since 2009, meeting our target of a 15% improvement over the five years. See page 58 for more information on our environmental performance.

Governance Online compliance trainingCompletion of mandated compliance training on anti-bribery and corruption, competition law and IT security.Method of calculation Measured as a percentage completion against a pre-defined target audience of employees.Target 100% training completion for all employees within the target audience. 2014 performance • 98% (7,284 employees) of the target audience have to date completed our online anti-bribery training

(2013: 84%; 6,302 employees).• 98% (1,575 employees) of the target audience have to date completed our online competition law

training (2013: 98%; 1,594 employees).• 85% (14,191 employees) of the target audience have to date completed our online IT security training

(2013: 37%; 6,273 employees).

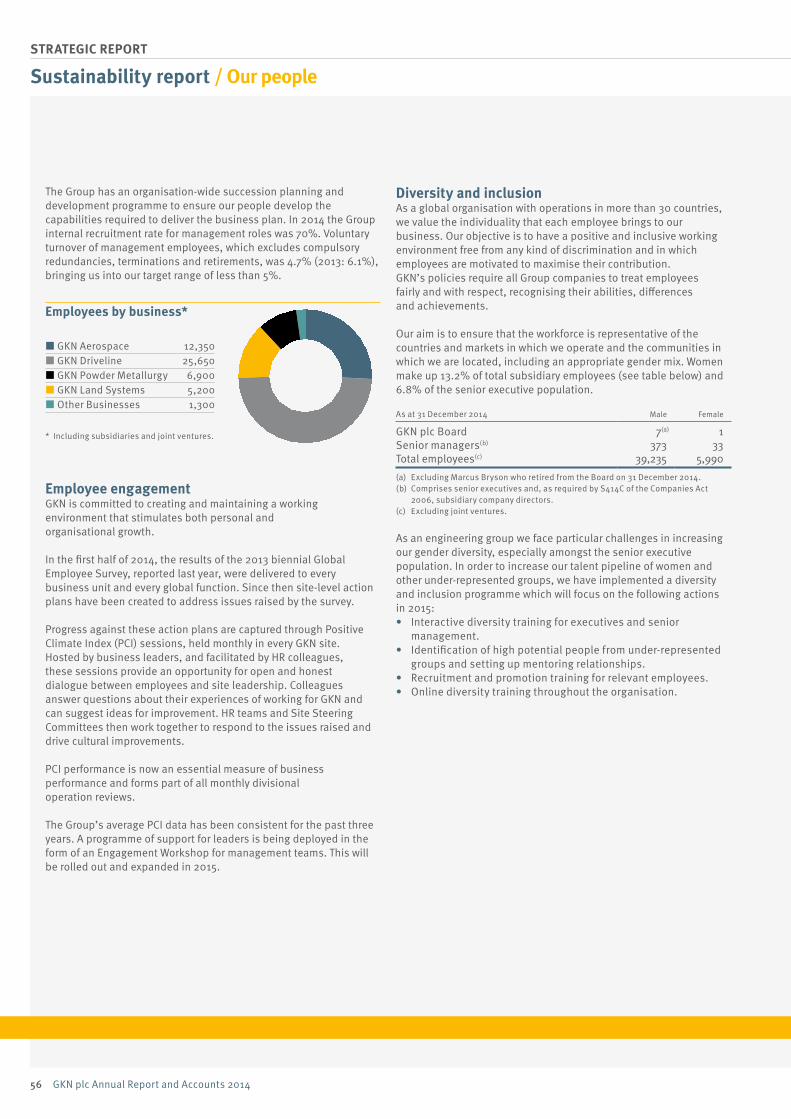

Our people Management turnover Method of calculation Management turnover is a measure of success in retaining our leaders and achieving our goal of being an employer of choice. Voluntary turnover of management employees, which excludes compulsory redundancies, terminations and retirements, is calculated as a percentage of total subsidiary management level employees. TargetVoluntary turnover of less than 5% of management employees.2014 performanceIn 2014, voluntary management turnover was 4.7% (2013: 6.1%), bringing us into our target range of less than 5%.

Financial KPIsSales growth Trading margins(b) Return on average invested

capital (ROIC)(b) Free cash flow Earnings per share (EPS)(b) Dividend per share

£7,456m 9.2% 17.7% £234m 29.0p 8.4p

Method of calculation Management sales(a) measured both in absolute terms and on an underlying basis (i.e. excluding the effects of currency translation, acquisitions and divestments) relative to the prior year.

Management trading profit(a) as a percentage of management sales(a).

Ratio of management trading profit(a) to average total net assets including the appropriate share of joint ventures but excluding current and deferred tax, cash, borrowings, post-employment obligations and derivative financial instruments.

Cash flows from operating activities (excluding special pension payments and before working capital refinancing for Volvo Aero in 2012) after capital expenditure and including fixed asset disposal proceeds, receipts of government capital grants and refundable advances and non-controlling interest dividends.

Management earnings for the Group (as set out in note 3(a) to the financial statements) divided by the weighted average number of ordinary shares in issue (excluding treasury shares).

Amount declared as payable by way of dividend divided by the number of ordinary shares in issue (excluding treasury shares).

Target To achieve long term growth rates at both Group and divisional level (in absolute terms and on an underlying basis) in excess of the growth in our major automotive, aerospace and land systems markets.

To achieve medium term trading margins of between 11% and 13% for GKN Aerospace, 8% and 10% for GKN Driveline, 9% and 11% for GKN Powder Metallurgy and 8% and 11% for GKN Land Systems, giving an overall Group trading margin of between 8% and 10%.

To achieve ROIC at both Group and divisional level which exceeds the weighted average cost of capital of the Group (12% as a pre-tax threshold and between 9% and 10% on a post-tax basis). The Group target is to achieve ROIC of 20% or above (pre-tax).

To generate positive free cash flow sufficient to cover dividend payments and provide funding resources to support organic and acquisitive earnings growth, and reduce indebtedness.

To achieve absolute growth in EPS each year and in the longer term, recognising the nature and cyclicality of our major markets, to achieve average annual compound growth of at least 6%.

To maintain a progressive dividend policy aligning dividends with the long term trend in management earnings and reflecting growth in earnings per share and free cash flow generation.

2014 performance Group management sales(a) declined by 2% on an absolute basis and grew by 4% on an organic basis. The corresponding figures for GKN Aerospace were a decrease of 1% and an increase of 3%; for GKN Driveline increases of 1% and 8% respectively; for GKN Powder Metallurgy a decrease of 2% and an increase of 5%; and for GKN Land Systems decreases of 14% and 10% respectively.

The Group trading margin in 2014 of 9.2% reflects good performance in all four divisions relative to their markets. The divisional trading margins were: GKN Aerospace – 12.4%; GKN Driveline – 8.1%; GKN Powder Metallurgy – 11.0%; and GKN Land Systems – 5.7%.

Group ROIC of 17.7% in 2014 reflects improved profitability partially offset by an increased asset base. Divisional ROIC performance was as follows: GKN Aerospace – 17.7%; GKN Driveline – 19.3%; GKN Powder Metallurgy – 21.8%; and GKN Land Systems – 11.4%.

Free cash flow amounted to £234 million, following a continued focus on operating cash generation throughout 2014 which included an increase in capital expenditure and research and development investment, and repayment of a government refundable advance.

Management EPS in 2014 was 29.0 pence compared with 28.7 pence in 2013, an increase of 1%.

Dividend per share increased in 2014 reflecting positive earnings and cash performance. The dividend for the year, at 8.4 pence, is covered 3.4 times by management earnings and 1.7 times by free cash flow.

(a) Management sales and management trading profit are defined on page 21. (b) 2012 restated for impact of IAS 19 (revised).

16 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 20 – 41 for more information on our financial results

Chief Executive’s review

The Group continued its progress in 2014 helped by good growth in our automotive and aerospace businesses which more than offset the headwinds of adverse currency translation and difficult land systems markets. Although management sales declined to £7,456 million, this represented underlying, organic growth of 4%. Earnings per share increased by 1% and the Board has recommended an increase to the dividend of 0.5 pence.

Our aim is to create long term and sustainable shareholder value through a balanced approach with three elements: growth, trading margin and return on invested capital.

We look to grow sales ahead of our markets, have targeted our Group margin to run in the 8-10% range and have a goal for return on invested capital (ROIC) of around 20%. I am pleased that in 2014 we made progress against all three of these objectives.

NIGEL STEINChief Executive

Moving forward

Our businessOver the course of the year we have seen the benefit of our business model. We are a global engineering business serving the world’s leading original equipment manufacturers in three large markets. But whichever the market, our approach and strategy are the same: using our knowledge of our customers and their needs, combined with our leading technology, excellent global footprint and broad operational excellence, to design, develop and deliver outstanding products. This requires a thorough understanding of market trends and a strong capability for product innovation. There are good examples of both throughout this report including the case studies featured on pages 25-37.

The table opposite summarises some strategic landmarks for the Group and in the business review (pages 22-37) we set out the most noteworthy divisional achievements.

Financial Statements Other InformationGovernanceStrategic Report

17GKN plc Annual Report and Accounts 2014

Leading in our chosen markets – excellent positions in their markets helped all four divisions prove successful in winning new business during 2014. GKN Aerospace won business for both aerostructures and engine systems, with the risk and revenue sharing partnership to supply components for the Pratt & Whitney PurePower PW100 Geared TurbofanTM engine. GKN Driveline won significant sideshaft business with Ford, General Motors, Volkswagen, BMW, Renault Nissan, Mazda and Hyundai whilst successfully designing and launching several all-wheel drive products with Fiat, BMW and Jaguar Land Rover. For GKN Powder Metallurgy, new business wins in the year totalled £165 million, higher than last year’s equivalent and including a good proportion of higher margin ‘Design for Powder Metallurgy’ components. For GKN Land Systems, the tough markets limited options, but its business in the industrial market continued to do well, successfully exploiting its leadership in clutches and brakes.

During the year we sold our stake in the emissions control business Emitec, a good business with sound prospects, but which did not give GKN a route to a leadership position in that market.

Leveraging a strong global presence – having manufacturing plants and design centres located around the world, close to our customers, is an important strategic advantage for GKN. We also use the regional presence of one division to help other divisions enter or expand in that market.

Mexico and Asia in general saw the greatest activity in this respect. Over the course of 2014, Group capital investment in Mexico and Asia was £37 million and £56 million respectively.

China continues to be an important market for GKN. Although the country’s economic growth has eased in recent years, growth of around 7% remains very attractive. We have continued to build our GKN Driveline joint venture company whilst at the same time expanding the activities of GKN Land Systems and GKN Powder Metallurgy in the country. We are also seeking to establish GKN Aerospace in China but this remains a work in progress.

Differentiating ourselves through technology – our excellent technology helped win significant business this year. This was clearly demonstrated through GKN Driveline’s critical role in the Fiat Chrysler small all-wheel drive platform, GKN Powder Metallurgy driving its margin through new ‘Design for Powder Metallurgy’ component wins and GKN Land Systems winning new business with Claas on the back of superior technical offering. GKN Aerospace continued building its position as a technology leader and was pleased to be awarded leadership of a challenging £30 million future wing research programme, backed by the UK’s Aerospace Technology Institute. They also delivered an innovative wing leading edge demonstrator to the Clean Sky programme, helping bring an ultra-high performance, natural laminar flow wing closer to reality.

Increasing investment was made into advanced engineering projects looking to the longer term, including development work on additive manufacturing (also known as 3D printing), the electrification of vehicle powertrains, future wing technologies and energy storage. All look likely to drive significant market changes in the future.

STRATEGIC PROGRESS

Leading in our chosen markets →→

• Organic and add-on opportunities in all divisions.• Sold interest in Emitec.

Leveraging a strong global presence → • Further increased our presence in Mexico and Asia.

Differentiating ourselves through technology → • Increased proportion of investment in advanced engineering.

Driving operational excellence →→ →

• Focus on operational excellence continued.• Used customer data to measure our performance –

‘Voice of the Customer’.• Focused on safety across our operations.

↓SUSTAINING ABOVE MARKET GROWTH

18 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 52 – 59 for more information on ‘doing the right thing’

Operational excellence – is fundamental to what we do and provides the opportunity to differentiate ourselves in our customers’ eyes. Employee safety is our number one priority and our performance is set out on page 54. In general 2014 saw a good reduction in the number of accidents. However, in February 2014 an employee at GKN Aerospace Engine Systems’ El Cajon plant in the US suffered a fatal injury whilst operating a forklift truck. I deeply regret this loss of life and we have provided support to the employee’s family. Lessons have been learned from this and applied elsewhere in the Group.

Across the Group, the GKN Lean manufacturing programme enables us to continue to drive continuous improvement in manufacturing performance and back-office processes.

Listening to the ‘Voice of the Customer’ in a direct way is vital to our success. During 2014 we have implemented improved processes to ensure all employees keep their eyes focused on our customers’ own ratings of us, understand any concerns and work speedily and determinedly to resolve them. Although customers’ views have always been important in GKN, I am confident the positive effect of this direct feedback will prove an advantage in building our business.

Together the successful delivery of these four strategic objectives helped deliver the fifth strategic objective of sustaining above market growth. In 2014 overall Group sales showed an organic increase of 4%, better than average for our markets.

Chief Executive’s review

Doing the right thing Underpinning these results is a strong set of GKN Values. We call this ‘doing the right thing’ and the effects of this are set out in the sustainability report on pages 52-59. At our 2014 internal International Leadership Conference, considerable time was spent discussing how GKN’s most senior people should demonstrate our Group Values.

Supporting this we have introduced new processes for clarifying to managers what is expected of them and getting their acknowledgment they understand this. In the months ahead we will be running a process of re-communicating the GKN Code to every employee wherever they are and no matter which of the 27 Group-wide languages they speak.

SummaryThe continued implementation of our strategy in 2014 delivered organic growth, improved margins and increased ROIC, together bringing increased financial returns to our shareholders. This could not have been achieved without the expertise, focus and sheer hard work of the 51,400 committed GKN people around the world. In closing, I would like to thank everyone in the GKN team for their contribution this year. I would also like to thank my former colleagues Marcus Bryson CBE and Bill Seeger for their support and contribution as members of my Executive team and the Board.

“ The continued implementation of our strategy in 2014 delivered organic growth, improved margins and increased ROIC, together bringing increased financial returns to our shareholders.”

Financial Statements Other InformationGovernanceStrategic Report

19GKN plc Annual Report and Accounts 2014

Looking aheadCommercial aircraft production should continue to be strong whereas military markets are forecast to decline. GKN Aerospace’s 2015 organic sales are expected to be broadly flat, reflecting these differing trends and the phasing of our programmes. However, a strong commercial order book supports attractive growth for GKN Aerospace over the medium term.

In automotive, external forecasts predict growth in global light vehicle production of around 2% with increases in China and North America, and Europe flat. Against this background, GKN Driveline and GKN Powder Metallurgy are expected to continue to grow organically above the market.

Softer global agricultural equipment markets are likely to more than offset the slight improvement in industrial markets. As a result, GKN Land Systems 2015 sales are expected to be lower than 2014 and an £8 million restructuring charge is planned to further reduce the fixed cost base.

Although some markets remain challenging, 2015 is expected to be a year of further growth. Beyond 2015, we are well positioned to outperform in our large global markets.

Nigel SteinChief Executive

→ Visit us at www.gkn.com to see more case studies

GKN DRIVELINE VIGO

Operational excellence founded on Lean manufacturing is a focus for GKN sites across the world. This culture of continuous improvement enables GKN to deliver quality products and exceptional customer service, and GKN Driveline in Vigo, Northern Spain, is one example of a site that has seen significant operational improvements in recent years.

The plant, which supplies sideshafts to European automotive manufacturers, has implemented a system to reduce waste and optimise productivity, created tools for the sharing of knowledge and ideas and provided Lean training for all employees. Maximising employee involvement, both in the office and on the shop floor, has been fundamental in engaging the teams and developing the change in culture.

The site has been recognised by the KAIZEN Institute, a global organisation that specialises in the continuous improvement of people, processes and systems, winning one of its 2014 awards.

Lean manufacturingDelivering operational excellence

20 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 22 – 37 for more information on the financial performance of our divisions

Business review / Group performance

Financial progress

ADAM WALKERGroup Finance Director

Group performanceResults

Change (%)

2014 2013 Headline Organic

Sales (£m) 7,456 7,594 (2) 4

Trading profit (£m) 687 661 4 11

Trading margin 9.2% 8.7%

Return on average invested capital 17.7% 17.3%

The Group has made good progress on its financial targets during 2014 with growth in organic sales, an improved Group margin, and an increase in Group ROIC – all of which support an increase of 6% in the total dividend.

Financial Statements Other InformationGovernanceStrategic Report

21GKN plc Annual Report and Accounts 2014

Management trading profit GKN Aerospace £277m GKN Driveline £280m GKN Powder Metallurgy £101m GKN Land Systems £44m

* Including corporate costs and Other Businesses.

£687m*

Management sales GKN Aerospace £2,226m GKN Driveline £3,444m GKN Powder Metallurgy £916m GKN Land Systems £776m Other Businesses £94m

£7,456m

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Organic sales increased by £303 million (4%). The adverse effect of currency translation on management sales was £403 million (5%) and there was a £7 million benefit from acquisitions which was more than offset by a £45 million reduction due to disposals.

Organic trading profit increased £66 million, due to the absence of restructuring costs (2013: £25 million), the strong performance of three of our divisions, lower profits from GKN Land Systems and £6 million net benefit from commercial settlements and provision releases. Adverse currency translation was £38 million and there was a £2 million reduction due to acquisitions and divestments.

Group trading margin increased to 9.2% (2013: 8.7% or 9.0% excluding restructuring charges). Return on average invested capital (ROIC) increased to 17.7% (2013: 17.3%).

Basis of reportingIn this report, financial information, unless otherwise stated, is presented on a management basis, the definition of which is below. The Group uses management measures, which are non-GAAP measures, to assess operating performance on a consistent basis, as we believe this gives a fairer assessment of the underlying performance of the business.

The use of management measures allows the Group to chart progress, make decisions and allocate resources based on the actions for which management is responsible or can influence, without volatility arising from significant one-time trading and portfolio change transactions or the mark to market valuation of currency hedges.

Definitions Financial information, unless otherwise stated, is presented on a management basis which aggregates the sales and trading profit of subsidiaries (excluding certain subsidiary businesses sold and closed) with the Group’s share of the sales and trading profit of joint ventures. References to trading margins are to trading profit expressed as a percentage of sales. Management profit or loss before tax is management trading profit less net subsidiary interest payable and receivable and the Group’s share of net interest payable and receivable and taxation of joint ventures. These figures better reflect performance of continuing businesses. Where appropriate,

reference is made to organic results which exclude the impact of acquisitions/divestments as well as currency translation on the results of overseas operations. Operating cash flow is cash generated from operations adjusted for capital expenditure, government capital grants, proceeds from disposal of fixed assets and government refundable advances. Free cash flow is operating cash flow including interest, tax, joint venture dividends, own shares purchased and amounts paid to non-controlling interests, but excluding dividends paid to GKN shareholders. Return on average invested capital (ROIC) is management trading profit as a percentage of average total net assets of continuing subsidiaries and joint ventures excluding current and deferred tax, net debt, post-employment obligations and derivative financial instruments.

Exchange rates Exchange rates used for currencies most relevant to the Group’s operations are:

Average Year end2014 2013 2014 2013

Euro 1.24 1.18 1.29 1.20US dollar 1.65 1.57 1.56 1.66

The approximate impact on 2014 trading profit of subsidiaries and joint ventures of a 1% movement in the average rate would be euro – £1 million, US dollar – £4 million.

22 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 24 – 25 for more information on GKN Aerospace

Products • Integrated aerostructures, including wing/empennage and

flight control surface assemblies and fuselage structures. • Fixed and rotating propulsion products for aircraft engines,

fan cases, engine components, exhaust systems and nacelles. • Transparencies including specially coated cockpit and

cabin windows. • Niche products such as ice protection, fuel systems and

flotation devices.

Key strategic activitiesTo support the achievement of the Group’s five strategic objectives, GKN Aerospace is focusing on the following areas:• Exploiting its strong positions on existing programmes for

new aircraft platforms, and pursuing long term contracts on selective high-growth and long-running platforms.

• Deploying new technologies for future commercial and military aircraft, to improve fuel efficiency, reduce emissions and minimise the environmental impact of aviation.

• Expanding into adjacent markets with similar product technologies and manufacturing capabilities; and expanding our global footprint.

Business review / GKN Aerospace

GKN Aerospace

GKN Aerospace is a leading global tier one supplier of airframe and engine structures, components, assemblies and transparencies to a wide range of aircraft and engine prime contractors and other tier one suppliers. It operates in three main product areas: aerostructures, engine components and sub-systems, and special products.

Financial Statements Other InformationGovernanceStrategic Report

23GKN plc Annual Report and Accounts 2014

12,350employees

7countries

33manufacturing locations

24 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

GKN Aerospace sales by customer Airbus 21% GE 13% UTC 13% Boeing 12% Snecma 6% Rolls-Royce 4% Spirit 3% Honeywell 3% MTU 3% Other 22%

GKN Aerospace sales by market Commercial 73% Military 27%

GKN Aerospace sales by product Engine components and sub-systems £1,045m Aerostructures £1,042m Special products £139m

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Business review / GKN Aerospace

Divisional performance against Group strategy STRATEGIC OBJECTIVE PROGRESS

Leading in our chosen markets →

→

• A world leader in aerostructures and number two in the independent aero engine structures market.

• $3 billion new work packages won.

Leveraging a strong global presence →→

• Invested in composite and metallic manufacturing in Mexico.• Construction began of a new manufacturing site in Seattle, US, to support the

Boeing 737 MAX assembly line.

Differentiating ourselves through technology →

→

• Fabricated robotically-welded case technology selected for the Pratt & Whitney PurePower PW1900 Geared Turbofan™ engine.

• Continued to develop strong positions in additive manufacture and future wing design.

Driving operational excellence →

→

• Improved customer scorecard results across the globe through ‘Voice of the Customer’ initiative.

• Received a number of quality awards from customers, including ‘Best performing supplier’ from Airbus.

↓ SUSTAINING ABOVE MARKET GROWTH

KEVIN CUMMINGSChief Executive GKN Aerospace

The overall aerospace market remained positive in 2014 driven by a growing commercial aircraft market partly offset by a declining military market. The division’s commercial sales were 73%, with military representing 27%.

Commercial aircraft production is still growing. Both Airbus and Boeing continue to benefit from higher deliveries and a record order backlog, and both have announced plans to increase production levels for single aisle aircraft in the future. There is also more demand for strong global suppliers to support their expansion plans.

Military spending remains under pressure, largely driven by cutbacks throughout the US and Europe, with the ramp-up of new programmes being delayed and overseas military operations reduced.

→ See page 13 for more information on the aerospace market

Financial Statements Other InformationGovernanceStrategic Report

25GKN plc Annual Report and Accounts 2014

Wings of the futureStrategy in action

→ Visit us at www.gkn.com to see more case studies

GKN AEROSPACE

GKN Aerospace is helping lead the way in wing design for future aircraft. It is participating in a number of UK research programmes focused on using new manufacturing technologies and more cost effective processes to create lighter, more fuel-efficient aircraft.

Together with industrial partners, research institutions and the UK Government, GKN Aerospace is working to develop and demonstrate new manufacturing techniques that will enable the UK aerospace industry to build wings for tomorrow’s aircraft.

It is focusing on creating a new generation of automated processes and technologies that will extend the boundaries of what we are able to manufacture, while at the same time increasing the quality, consistency and speed of production.

The key financial results for the year are as follows:

GKN AerospaceChange (%)

2014 2013 Headline Organic

Sales (£m) 2,226 2,243 (1) 3

Trading profit (£m) 277 266 4 7

Trading margin 12.4% 11.9%

Return on average invested capital 17.7% 17.8%

Overall, GKN Aerospace’s organic sales were £59 million higher (3%). There was an adverse £76 million (3%) impact from currency translation.

Organic commercial aerospace sales were 4% higher, driven by increased demand for the Boeing 787, A350 and engine spares, partly offset by lower A330 and A380 sales and a £17 million reduction due to the previously announced supply chain contract taken back in-house by Airbus in May 2013. Military sales were broadly flat as spares on programmes which ceased production were offset by lower sales for F/A-18 Super Hornet and UH-60 Blackhawk helicopter.

The organic increase in trading profit was £18 million, the impact from currency on translation of results was £10 million adverse (4%) and there was a £3 million benefit relating to losses from the Composite Technology and Applications Limited (CTAL) disposal in 2013.

Each year there are commercial issues and provision movements which impact the results. This year they amounted to a £4 million net benefit, which included a credit of £11 million as progress was made on an onerous contract partly offset by a £7 million charge for customer claims. Trading profit also included income of £8 million (2013: £5 million) for milestones achieved in relation to CTAL, which is not expected to be repeated in 2015.

Other factors included improved commercial spares sales and higher volumes on new programmes offset by lower military sales on mature programmes. Further start-up operating losses at the new A350 facility were £8 million (2013: loss of £11 million). Trading margin was 12.4% (2013: 11.9%).

Return on average invested capital was 17.7% (2013: 17.8%), following the repayment of a Government advance in the first half of the year. During the year a number of important milestones were achieved including: • a new 7% (US$2.5 billion) risk and revenue sharing partnership

(RRSP) with Pratt & Whitney covering the supply of components for the PurePower PW1900 Geared Turbofan™ engine for the Embraer 190 and the 195-E2 narrow body aircraft;

• a long term agreement (LTA) worth more than US$200 million with Rolls-Royce to supply components for the latest version of the Trent 1000 engine, a capability enhancement of the existing Trent 1000 engine for the Boeing 787;

• a contract from Boeing for the final assembly and paint of Advanced Technology (AT) Winglets for the new 737 MAX;

• investment and work being transferred into our low cost manufacturing facilities in Mexico; and

• leading collaborative projects backed by the UK’s Aerospace Technology Institute for additive manufacturing and future wing research.

26 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 28 – 29 for more information on GKN Driveline

GKN Driveline

As a global business serving the world’s leading vehicle manufacturers, GKN Driveline develops, builds and supplies an extensive range of automotive driveline products and systems, for use in everything from the most sophisticated premium vehicles, that demand complex driving dynamics, to the smallest ultra low-cost cars.

Business review / GKN Driveline

Products • Constant velocity jointed systems including CV joints and

sideshafts. • All-wheel drive (AWD) systems including propshafts, couplings

and final drive units. • Trans-axle solutions including open, limited slip and locking

differentials and electronic torque vectoring products. • eDrive systems including electric axles, transmissions

and motors.

Key strategic activitiesTo support the achievement of the Group’s five strategic objectives, GKN Driveline is focusing on the following areas:• Providing innovative driveline systems and solutions,

supporting developing market trends for more fuel-efficient vehicles.

• Increasing business in high growth regions.• Serving the needs of strategic customers through a market-

leading global footprint.

Financial Statements Other InformationGovernanceStrategic Report

27GKN plc Annual Report and Accounts 2014

25,650 employees

22countries

46manufacturing locations

28 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

GKN Driveline sales by customer Volkswagen 15% Fiat Chrysler 11% Ford 10% Renault Nissan 10% General Motors 9% Tata Group 6% BMW Group 6% Toyota Group 5% Mitsubishi 4% Other 24%

GKN Driveline sales by product group CVJ Systems £2,075m AWD and eDrive Systems £1,337m Other £32m

GKN Driveline sales by region of origin Europe £1,312m North America £1,079m China £380m Japan £298m South America £147m India £81m Other £147m

Business review / GKN Driveline

ANDREW REYNOLDS SMITH EXECUTIVE DIRECTORChief Executive GKN Automotive

Divisional performance against Group strategy STRATEGIC OBJECTIVE PROGRESS

Leading in our chosen markets →→

• Number one in driveline and all-wheel drive markets.• £700 million annualised new business won in sideshafts and all-wheel drive.

Leveraging a strong global presence →→

• Further expansion of existing plants in China.• Increased capacity and localised propshaft production in Mexico, and

expanded facility in Newton, North America.

Differentiating ourselves through technology →

→

• Produced the industry’s first two-speed eAxle for electric and hybrid vehicles, which has entered production on the BMW i8.

• Developed the world’s smallest all-wheel drive disconnect system.

Driving operational excellence → • Began implementation of the Driveline Excellence System to ensure consistency in key processes and standards.

↓ SUSTAINING ABOVE MARKET GROWTH

Production in the major automotive markets of China, North America, Europe and Japan increased relative to 2013, while Brazil and India declined. Overall, global production volumes increased 3.1% to 87.4 million vehicles (2013: 84.8 million).

Automotive market

Car and light vehicle production (rounded millions of units) 2014 2013 Growth (%)*

Europe 20.1 19.5 3.3North America 17.0 16.2 5.2Brazil 3.0 3.5 (14.1)Japan 9.2 9.1 2.1China 22.6 20.9 8.1India 3.6 3.7 (1.7)Others 11.9 11.9 0.0

Total – global 87.4 84.8 3.1

* Growth is derived from unrounded production figures.

Source: IHS Automotive.

→ See page 13 for more information on the automotive market

Financial Statements Other InformationGovernanceStrategic Report

29GKN plc Annual Report and Accounts 2014

→ Visit us at www.gkn.com to see more case studies

GKN DRIVELINE

The market for electric and hybrid vehicles is growing and consumers are increasingly looking for dynamic performance, not just exceptional fuel efficiency and low CO2 emissions.

GKN Driveline has developed the industry’s first two-speed eAxle, which delivers electric power throughout a vehicle’s entire speed range. Optimised for weight, packaging and efficiency, the two-speed eAxle supports effective hybridisation, contributing to an outstanding driving experience.

The technology features on the BMW i8 plug-in hybrid sports car, a vehicle that is changing the perception of hybrid vehicles. Working closely with BMW, GKN drew on the expertise and knowledge of its global engineering network to deliver the project from concept to production in just 24 months.

Industry’s first two-speed eAxleStrategy in action

The key financial results for the year are as follows:

GKN DrivelineChange (%)

2014 2013 Headline Organic

Sales (£m) 3,444 3,416 1 8

Trading profit (£m) 280 246 14 23

Trading margin 8.1% 7.2%

Return on average invested capital 19.3% 17.0%

Organic sales increased by £265 million (8%) compared with global vehicle production which was up 3%. The adverse effect of currency translation was £226 million (7%) and the impact from disposals was £11 million, being the proportionate loss of sales from a wholly-owned business in China which was transferred into our Shanghai GKN HUAYU Driveline Systems Co Limited (SDS) joint venture in November 2013. Constant velocity jointed (CVJ) systems accounted for 60% of sales and non-CVJ sales were 40%.

GKN Driveline’s market outperformance was broadly based across the main markets reflecting recent market share gains, a stronger position in premium vehicles, demand for which continued to be good, and GKN Driveline’s broadening product mix, particularly with all-wheel drive (AWD) systems. GKN Driveline slightly underperformed the market in Japan due to our specific programme mix.

The organic improvement in trading profit was £53 million, including the absence of £16 million of restructuring charges reported in 2013. The adverse impact of currency translation on trading profit was £18 million (8%). Each year there are commercial settlements and provision movements which impact the results. In 2014, whilst individually larger than usual, they amounted to a £2 million net benefit. This £2 million included a commercial settlement credit of £14 million and a credit of £5 million as progress was made on an onerous contract, partly offset by a higher than usual £17 million charge for warranty and quality claims. GKN Driveline’s trading margin was 8.1% (2013: 7.2%, or 7.7% excluding restructuring charges), reflecting higher organic revenue growth.

Return on average invested capital increased to 19.3% (2013: 17.0%).

During the year, over £700 million of annualised sales in new and replacement business was secured in CVJ and AWD systems and a number of important milestones were achieved, including:• expanding facilities in Mexico and AWD capacity in Newton, US; • expanding facilities in China with new Power Transfer Unit (PTU)

wins and localisation of AWD products from Europe and North America;

• design and launch of the world’s first integrated disconnect AWD system for Fiat Chrysler’s small SUV platform;

• eAxle new launches on advanced plug-in hybrid supercars, with the world’s first two-speed eTransmission on the BMW i8 and Porsche awarding GKN Driveline ‘Technology Partner’ status for its development of a high-performance eAxle for the 918 Spyder; and

• 11 customer awards, including from Ford, General Motors, Mitsubishi, Nissan and Volvo.

30 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

→ See pages 32 – 33 for more information on GKN Powder Metallurgy

Business review / GKN Powder Metallurgy

GKN Powder Metallurgy

GKN Powder Metallurgy comprises GKN Sinter Metals and Hoeganaes. GKN Sinter Metals is the world’s leading manufacturer of precision automotive components as well as components for industrial and consumer applications. Hoeganaes is one of the world’s largest manufacturers of metal powder, the essential raw material for powder metallurgy.

Products• Sintered components for engines and transmissions, as well

as pumps, bodies and chassis, and compressors.• Sintered bearings and filters.• Metal injection moulded components.• Metal powders.• Soft magnetic components for use in electric motors.• Sintered components for numerous industrial applications.

Key strategic activitiesTo support the achievement of the Group’s five strategic objectives, GKN Powder Metallurgy is focusing on the following areas:• Developing ‘Design for Powder Metallurgy’ applications to

meet the rapidly developing requirements for high efficiency engines, advanced transmission applications, weight reduction and evolving emissions standards.

• Expanding the business in high-growth markets, supporting customers globally.

• Enhancing performance of metal powders.

Financial Statements Other InformationGovernanceStrategic Report

31GKN plc Annual Report and Accounts 2014

6,900 employees

10countries

34manufacturing locations

32 GKN plc Annual Report and Accounts 2014

STRATEGIC REPORT

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

Management sales GKN Aero customer GKN Aero market

GKN Aero productGKN driveline customerGKN driveline productGKN driveline region

management pro�t

metallurgy 2 metallurgy product

landsystems market landsystems region

metallurgy customer landsystems customer

GKN Powder Metallurgy sales by customer Ford 9% General Motors 6% Hilite 4% Fiat Chrysler 4% ZF 4% Schaeffler 3% Borg Warner 2% Linamar 2% Volkswagen 2% Means Industries 2% Other 62%

GKN Powder Metallurgy sales* GKN Sinter Metals Americas £373m Europe £322m Rest of World £73m

Hoeganaes £148m

* GKN Sinter Metals sales by region.

GKN Powder Metallurgy sales by product type

Sintered components Automotive £661m Industrial £107m

Hoeganaes Metal powder £148m

Business review / GKN Powder Metallurgy

Divisional performance against Group strategy

STRATEGIC OBJECTIVE PROGRESS

Leading in our chosen markets →→→

• Global leader in sintered components.• World’s number two manufacturer of metal powder.• £165 million new business won.

Leveraging a strong global presence → • Expanded production facilities in China.

Differentiating ourselves through technology →

→→

• Increased success for ‘Design for Powder Metallurgy’ components such as in variable oil pump applications for automotive engines and transmissions.

• Continued to develop technically enhanced powders.• Technology partnership established to accelerate use of hydrogen storage.

Driving operational excellence →

→

• Roll-out of advanced compaction presses in the US to improve manufacturing efficiency.

• Launched ‘My quality’ programme.

↓ SUSTAINING ABOVE MARKET GROWTH

PETER OBERPARLEITER Chief Executive GKN Powder Metallurgy

→ See pages 13 and 28 for more information on the automotive market

Financial Statements Other InformationGovernanceStrategic Report

33GKN plc Annual Report and Accounts 2014

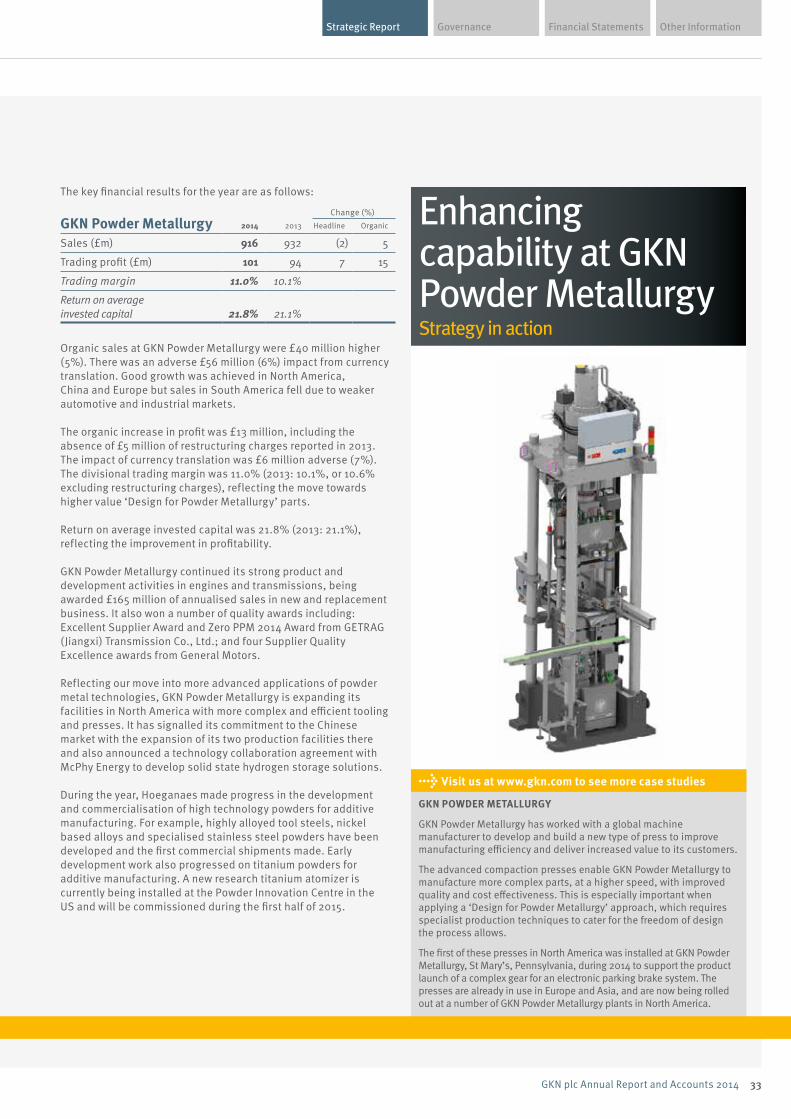

The key financial results for the year are as follows:

GKN Powder MetallurgyChange (%)

2014 2013 Headline Organic

Sales (£m) 916 932 (2) 5

Trading profit (£m) 101 94 7 15

Trading margin 11.0% 10.1%

Return on average invested capital 21.8% 21.1%

Organic sales at GKN Powder Metallurgy were £40 million higher (5%). There was an adverse £56 million (6%) impact from currency translation. Good growth was achieved in North America, China and Europe but sales in South America fell due to weaker automotive and industrial markets.