annual report - j. lauritzen a/sstatic.j-l.com/imce/r2012_final_uk_lores.pdfkls grafisk hus a/s,...

TRANSCRIPT

www.j-lauritzen.com

2012Annual Report

J. Lauritzen a/S · AnnuAl RepoRt 20122

DiScLaimerthis Annual Report contains forward-looking statements about Jl’s future financial position. Such statements are subject to risks and uncertainties as various factors, many of which are beyond the control of Jl, may cause actual developments and actual results to differ materially from expectations contained in the Annual Report. Accordingly, forward-looking statements should not be relied upon as a prediction of actual results.

this report is available in Danish and english. In the event of any discrepancy between the two versions, the Danish version shall pre-vail.

J. lAuRItzen at a gLanceJ.lauritzen (Jl) was founded in 1884 and is owned by the lauritzen Foundation. We have grown and developed our operations consider-ably during the last decade and thus remain one of Denmark’s leading shipping companies.

part of our strategy is to spread risks across the different business areas. today we have four busi-ness units with different growth drivers and cycles and each specifically positioned to their respec-tive markets.

We operate a modern, diversified fleet of bulk car-

riers, gas carriers, product tankers and dynami-cally positioned support vessels for the offshore industry that are all engaged in operations world-wide.

We continuously strive to have a client-oriented approach to the way we do business and our op-erations are conducted by highly skilled staff at sea and ashore.

Jl is headquartered in Copenhagen with overseas offices in China, Japan, philippines, Singapore, Spain and uSA.

pRInteD by: KlS gRAFISK huS A/S, DenmARKS moSt gReen gRAphIC houSe

J. Lauritzen a/S · AnnuAl RepoRt 2012 3

boARD & eXeCutIVe mAnAgement StAtement 4CompAny IntRoDuCtIon 6gRoup Key FIguReS 8hIghlIghtS 2012 AnD outlooK 2013 10lAuRItzen bulKeRS 18lAuRItzen KoSAn 26lAuRItzen tAnKeRS 34lAuRItzen oFFShoRe 40FInAnCe AnD InVeStoR RelAtIonS 42RISK mAnAgement 46CoRpoRAte goVeRnAnCe 50CoRpoRAte ReSponSIbIlIty 54oRgAnISAtIon AnD people 56FInAnCIAl ReVIeW 58boARD oF DIReCtoRS 60mAnAgement 62ACCountS 64mAnAgement StAtement 100InDepenDent AuDItoRS’ RepoRt 101oVeRAll gRoup StRuCtuRe 102lISt oF gRoup CompAnIeS 103

tAble oF contentS

J. Lauritzen a/S · AnnuAl RepoRt 20124

boARD & eXeCutIVe mAnAgementStatementthe business environment for the shipping indus-try has changed substantially during the past few years.

Characterised by oversupply in major shipping markets, surplus shipbuilding capacity, low eco-nomic growth and tight credit conditions, 2012 brought plummeting asset values, with the baltic Freight Index at a 25 year low and further defaults among shipping companies.

Jl was obviously influenced by these circum-stances and with a net loss of uSD (350)m our 2012 result was very unsatisfactory.

In this challenging environment, we continued to develop our different business activities and we made a number of important decisions during the year. of special importance was the joint venture with hitecVision, norway, in the promising off-shore market, the formation of Axis offshore pte. ltd. and the following order for a modern semi-submersible ASV (Accommodation and Support Vessel) for delivery in 2015.

lauritzen bulkers increased its focus on long-term cargo contract business and related market activi-ties.

Capesize bulk carriers left without contract cover due to defaults were sold.

All business units were engaged in an energy sav-ings programme launched in collaboration with classification society DnV (Det norske Veritas).

group finances were further strengthened with a new corporate bond issuance and the bonds were listed on oslo Stock exchange.

In connection with the approval of Jl’s Annual Re-port for 2012, the lauritzen Foundation decided to convert two subordinated loans equivalent to

uSD 160m into equity, thereby increasing Jl’s sol-vency ratio from 37% at year-end 2012 to 44%.

Difficult trading conditions are expected to con-tinue in 2013 as a multitude of risk factors contin-ue to impact global shipping. Surplus capacity will influence most markets during the year. however, we expect global economic growth to gradually strengthen. At the same time, high scrappings and declining deliveries will reduce fleet growth and set the scene for the beginning of a modest recovery towards the end of the year.

more than anything else, Jl stands for accounta-bility. our well-qualified staff will continue to de-liver the services which through our 128 years of history have enabled us to build strong relations with customers, partners and other stakeholders globally no matter which market conditions we have been operating in.

After more than 14 years as president and Ceo, torben Janholt will retire with the release of Jl’s 2012 annual accounts. Jan Kastrup-nielsen, who has been with Jl since 2000 and a member of Jl’s executive management since 2009, will become the new president and Ceo.

Bent Østergaard Chairman of the Board

torben JanholtPresident & CEO 1998-2013

Jan Kastrup-nielsenPresident & CEO2013-

J. Lauritzen a/S · AnnuAl RepoRt 2012 5

From left: Torben Janholt, Bent Østergaard and Jan Kastrup-Nielsen

J. Lauritzen a/S · AnnuAl RepoRt 20126 J. Lauritzen a/S · AnnuAl RepoRt 20116

lAuRItzen BuLKerSDry bulk operations started in the late 1970s when the focus was on handysize bulk carriers/lakers (lakers are special ocean-going vessels capable of also serving the great lakes in north America). today lauritzen bulkers is a major owner and op-erator of bulk carriers engaged in all dry bulk seg-ments.

operations comprise a combined fleet of more than 100 handysize, handymax, panamax and capesize bulk carriers including short-term char-ters.

lAuRItzen KoSanWith the acquisition of Kosan tankers in 1989, Jl entered the market for smaller gas carriers, and today lauritzen Kosan is a leading carrier of liquefied gases, including petrochemical gasses such as ethylene and propylene.

At year-end 2012, lauritzen Kosan controlled a combined fleet of 45 semi-refrigerated/ethylene and fully pressurised gas carriers in the 3,000-10,000 m3 segment.

CompAny introDuction

J. Lauritzen a/S · AnnuAl RepoRt 2012 7

lAuRItzen tanKerSestablished in 2004 with the acquisition of Quan-tum tankers, lauritzen tankers is a provider of medium range (mR) product tankers for ocean transport of oil products ranging from vegetable oils to petroleum products, fuel oils and chemi-cals.

lauritzen tankers controlled 18 modern, medium range product tankers at year-end 2012.

lAuRItzen offShoreoperations started in 2008 with the conversion of a product tanker into a dynamically positioned shuttle tanker. the offshore operation today com-prises three shuttle tankers and part-ownership in the offshore accommodation segment.

In 2012, Axis offshore was established as a 50:50 joint venture with hitecVision to focus on high-end semi-submersible accommodation units also capable of serving clients in the north Sea. the joint venture builds on Jl’s expertise in the off-shore accommodation sector and our first accom-modation unit Dan Swift was transferred to the new operation.

J. Lauritzen a/S · AnnuAl RepoRt 20128

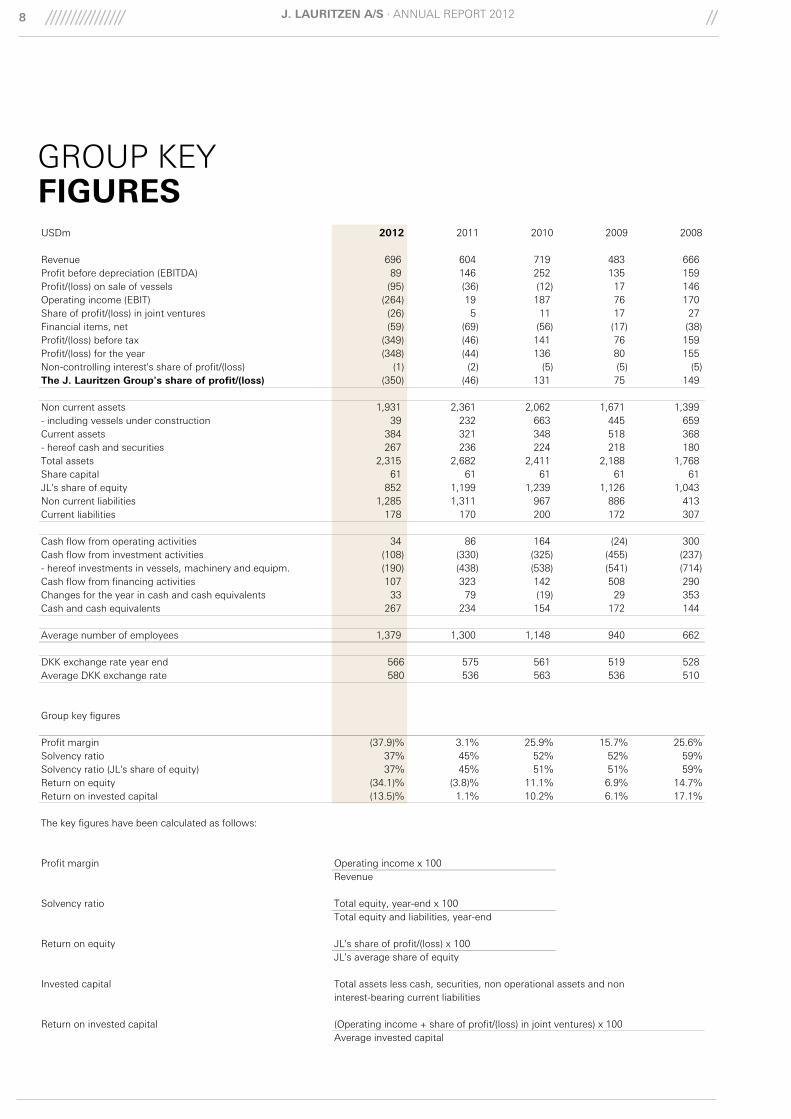

gRoup Key figureSUSDm 2012 2011 2010 2009 2008

Revenue 696 604 719 483 666Profit before depreciation (EBITDA) 89 146 252 135 159Profit/(loss) on sale of vessels (95) (36) (12) 17 146Operating income (EBIT) (264) 19 187 76 170Share of profit/(loss) in joint ventures (26) 5 11 17 27Financial items, net (59) (69) (56) (17) (38)Profit/(loss) before tax (349) (46) 141 76 159Profit/(loss) for the year (348) (44) 136 80 155Non-controlling interest's share of profit/(loss) (1) (2) (5) (5) (5)The J. Lauritzen Group's share of profit/(loss) (350) (46) 131 75 149

Non current assets 1,931 2,361 2,062 1,671 1,399- including vessels under construction 39 232 663 445 659Current assets 384 321 348 518 368- hereof cash and securities 267 236 224 218 180Total assets 2,315 2,682 2,411 2,188 1,768Share capital 61 61 61 61 61JL's share of equity 852 1,199 1,239 1,126 1,043Non current liabilities 1,285 1,311 967 886 413Current liabilities 178 170 200 172 307

Cash flow from operating activities 34 86 164 (24) 300Cash flow from investment activities (108) (330) (325) (455) (237)- hereof investments in vessels, machinery and equipm. (190) (438) (538) (541) (714)Cash flow from financing activities 107 323 142 508 290Changes for the year in cash and cash equivalents 33 79 (19) 29 353Cash and cash equivalents 267 234 154 172 144

Average number of employees 1,379 1,300 1,148 940 662

DKK exchange rate year end 566 575 561 519 528 Average DKK exchange rate 580 536 563 536 510

Group key figures

Profit margin (37.9)% 3.1% 25.9% 15.7% 25.6%Solvency ratio 37% 45% 52% 52% 59%Solvency ratio (JL's share of equity) 37% 45% 51% 51% 59%Return on equity (34.1)% (3.8)% 11.1% 6.9% 14.7%Return on invested capital (13.5)% 1.1% 10.2% 6.1% 17.1%

The key figures have been calculated as follows:

Profit margin Operating income x 100Revenue

Solvency ratio Total equity, year-end x 100Total equity and liabilities, year-end

Return on equity JL's share of profit/(loss) x 100JL's average share of equity

Invested capital Total assets less cash, securities, non operational assets and noninterest-bearing current liabilities

Return on invested capital (Operating income + share of profit/(loss) in joint ventures) x 100Average invested capital

J. Lauritzen a/S · AnnuAl RepoRt 2012 9

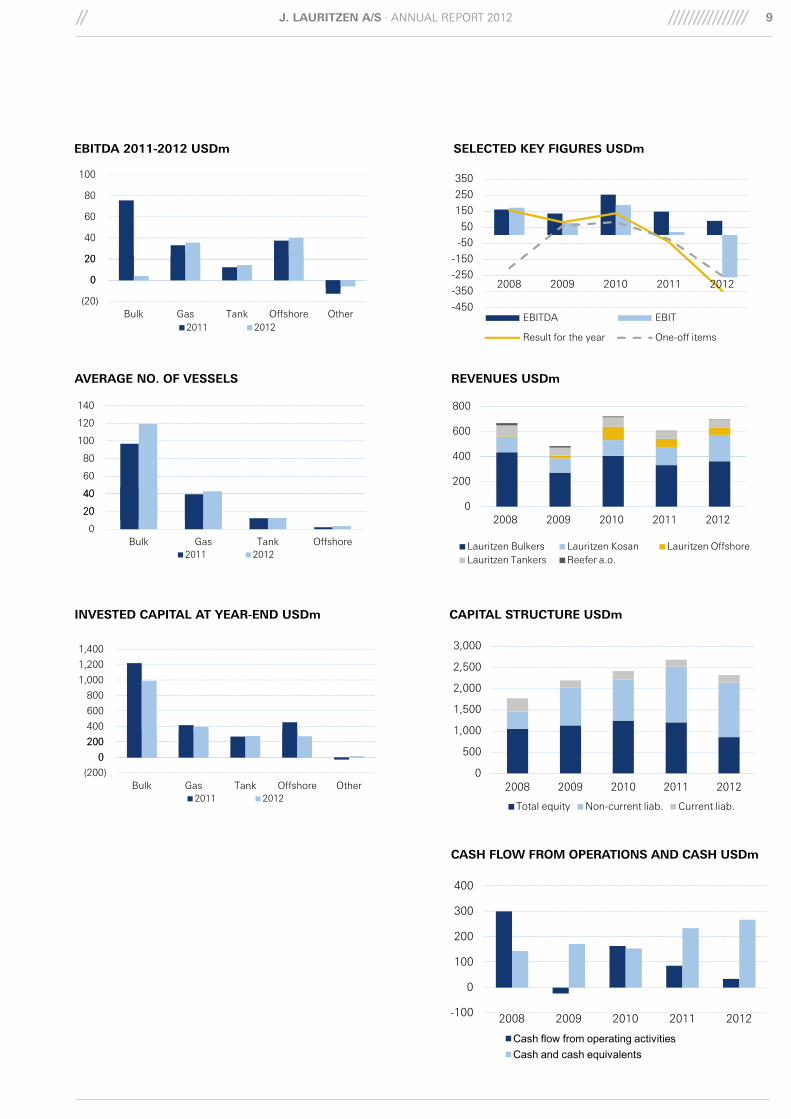

caPitaL Structure uSDm

reVenueS uSDm

SeLecteD KeY figureS uSDm

caSh fLoW from oPerationS anD caSh uSDm

eBitDa 2011-2012 uSDm

aVerage no. of VeSSeLS

inVeSteD caPitaL at Year-enD uSDm

-450

-350

-250

-150

-50

50

150

250

350

2008 2009 2010 2011 2012

EBITDA EBIT

Result for the year One-off items

0

200

400

600

800

2008 2009 2010 2011 2012

Lauritzen Bulkers Lauritzen Kosan Lauritzen OffshoreLauritzen Tankers Reefer a.o.

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012

Total equity Non-current liab. Current liab.

-100

0

100

200

300

400

2008 2009 2010 2011 2012

Cash flow from operating activitiesCash and cash equivalents

0

20

40

60

80

100

(20)

0

20

Bulk Gas Tank Offshore Other2011 2012

20

40

60

80

100

120

140

0

20

40

Bulk Gas Tank Offshore2011 2012

0

200

400

600

800

1,000

1,200

1,400

(200)

0

200

Bulk Gas Tank Offshore Other2011 2012

J. Lauritzen a/S · AnnuAl RepoRt 201210

hIghlIghtS 2012 anD outLooK 2013

figure 1: reSuLt for the Year uSDm

-300

-200

-100

0

100

-400

-300

200

Bulk Gas Tank Offshore

Result before tax Tax a.o. Result for the year

2011 2012

In a year characterised by sustained world eco-nomic decline, generally depressed shipping mar-kets and substantial deliveries of new tonnage to major shipping segments, Jl’s result was uSD (349.7)m compared to uSD (46.2)m in 2011, cf. Figure 1.

the result for 2012 was significantly impacted by one-off items with a net effect of uSD (254.4)m (2011: uSD (25.2)m) comprising write-downs, sale of claims and sales of vessels due to counter-party defaults or strategic initiatives. Adjusted for one-off items, Jl’s result was uSD (95.4)m, down from uSD (21.0)m in 2011 mainly due to income lost as a consequence of counterparty defaults and to the weaker bulk markets.

Return on invested capital was (13.5)% compared to 1.1% in 2011.

the result was in line with expectations stated in our stock exchange announcement to oslo børs in December 2012 but considerably below our ex-pectations at the beginning of the year. the result is regarded as very unsatisfactory.

the BuSineSS enVironment2012 was a very difficult year for practically all shipping markets apart from offshore. the Clark-Sea Index, representing a weighted average of earnings in the bulk, gas, container and product tanker markets declined by 23% in 2012 com-pared to 2011, cf. Figure 2, and was - adjusted for rises in operational costs - at its lowest since 1990. Some markets such as gas carriers wit-nessed periods with acceptable earnings but the trend for most markets was downwards, and for shorter or longer periods heading towards operat-ing costs.

A number of unexpected economic and political factors contributed to reduce growth in world trade in 2012 to a meagre 2.8% with only the bulk market among Jl’s shipping businesses enjoying higher growth in demand, although with supply outpacing bulk demand growth.

the year opened with fairly difficult credit condi-tions which had a detrimental effect, particularly on demand for bulk carriers. tight monetary poli-

cies in China during the first half of 2012 and the increased turmoil in financial markets mainly in the euro zone during the second quarter damp-ened economic growth and limited world trade. tightening sanctions against Iran was another factor that hampered trade in petrochemical gas-es for example.

the following characterized Jl’s main markets in 2012:

• the dry bulk market posted yet another year of unsatisfactory developments in rates and prices with the average baltic Freight Index (bFI) declining by 40% compared to 2011 reaching at its lowest for 25 years. Spot rates were down by 30% on average for handysize and handymax and 50% for cape-size compared to 2011. period rates fell by 20% for capesize and 30% or more for all other segments. After a dismal opening of the year, an im-provement set in for handysize and handy-max in February which ended in August. the normal strengthening for handysize and handymax after the harvest season did not occur. Capesize spot earnings were at very low levels save for a couple of months to-wards the end of the year. Second-hand prices declined by 20-30% de-pending on vessel segment.

• period rates for smaller gas carriers declined slightly to about uSD 540,000 per month for ethylene carriers and uSD 265,000 per month for 3,200 m3 semi-refrigerated carri-ers.

J. Lauritzen a/S · AnnuAl RepoRt 2012 11

SouRCe: Jl buSIneSS AnAlySIS bASeD on DAtA eXtRACt FRom ImF WebSIte

figure 2: cLarKSea inDex 2010-2012 uSD/DaY

Spot rates for ethylene gas carriers were sta-ble throughout the year with spot rates for fully pressurised gas carriers rising in the sec-ond half of 2012. Spot market rates for semi-refrigerated gas carriers in the 3,200-6,500 m3 segment start-ed falling at the beginning of Q2 and declined quite strongly for the balance of the year. Second-hand tonnage prices declined by 5% during the year.

• the product tanker market had a disappoint-ing spot market which saw the three key routes down by 20% for mR product tankers. period markets for mR product tankers lev-elled out at uSD/day 13,500. Second-hand prices for tonnage were down by 5% for a five year-old mR product tanker.

• offshore markets for specialized tonnage in general had another busy year. however, with only a limited number of long-term con-tracts signed, the shuttle tanker market was an exception to this. orders for rigs and other specialized tonnage for the offshore industry continued at a high level.

other commodity shipping markets did not fare better. As a result, demolition increased by about 40% to approximately 60m dwt from 2011 to 2012. Demolition of dry bulk tonnage increased by almost 50% to approximately 35m dwt, where-as demolition of mR products tankers and smaller gas carriers fell to even lower levels than in 2011. Four shuttle tankers were scrapped in 2012 com-pared to one unit in 2010 and 2011.

Contracting for new vessels was down by almost 50% in dwt terms compared to 2011.

International shipping is in the midst of a large supply crisis. heavy deliveries during the past years have lowered the average age of the world merchant fleet in most segments. Additionally, major ship building capacity has been established which current order levels are far from matching. thus, shipyards saw their order books recede by a third in dwt terms from year-end 2011 to year-end 2012. Shipyards’ forward cover is now estimated to be slightly less than two years, implying con-tinuing pressure on newbuilding prices.

JL grouPJl continued developing its business areas and a number of important decisions were taken during the year.

of special importance was the joint venture with hitecVision, norway, in the promising offshore market, the formation of Axis offshore pte. ltd. and the following order for a modern semi-sub-mersible ASV (Accommodation and Support Ves-sel) for delivery in 2015.

lauritzen bulkers increased its focus on long-term cargo contract business and related market activi-ties.

Capesize bulk carriers left without contract cover due to defaults were sold.

0

4000

8000

12000

16000

20000

2010-01 2010-07 2011-01 2011-07 2012-01 2012-07

J. Lauritzen a/S · AnnuAl RepoRt 201212

All business units were engaged in an energy sav-ings programme launched in collaboration with DnV (Det norske Veritas).

group finances were further strengthened with a new corporate bond issuance and the bonds were listed on oslo Stock exchange.

During the year, Jl took delivery of seven new-buildings, including three bulk carriers, one fully pressurized gas carrier, two product tankers and one shuttle tanker. In addition, four bulk carriers, two gas carriers and one product tanker were tak-en on long-term charter. At year-end 2012, Jl had four vessels on order.

During the year, six long-term time-chartered ves-sels were redelivered according to plan.

During 2012, Jl controlled a combined average fleet of 178 vessels compared to 151 vessels in 2011, cf. Figure 3, of which 59 were owned ves-sels (48 in 2011)

total vessel days amounted to 65,073 in 2012 compared to 54,945 days reported in 2011.

Due to our fleet renewal and expansion efforts in recent years, we own a modern, efficient fleet of bulk carriers with an average age of 2.3 years, gas

0

30

60

90

120

150

180

210

2011 2012

Own Part owned Chartered Shared charter Other

z

figure 3: aVerage no. of VeSSeLS

J. Lauritzen a/S · AnnuAl RepoRt 2012 13

figure 4: traDeD Price (noK) for J. Lauritzen noK 700m BonD 2011-2012

SouRCe: oSlo StoCK eXChAnge

carriers 8.6 years, product tankers 3.6 years and shuttle tankers 5.3 years.

aSSetS anD SoLVencYDuring 2012, investments in vessels amounted to uSD 190m compared to uSD 435m in 2011. Sale of vessels totalled uSD 80m compared to uSD 33m in 2011. total invested capital was uSD 1,960m at year-end 2012, down from uSD 2,344m at year-end 2011.

the total book value of vessels amounted to uSD 1,702m, down uSD 267m on 2011 primarily due to sale of assets and write-downs. brokers’ valua-tions of vessels totalled uSD 1,312m down 16% on 2011. the value in use of the vessels, taking contract coverage into account was higher than total book value.

At the end of 2012, Jl’s newbuilding portfolio comprised four owned vessels, three product tankers and one bulk carrier for delivery in 2013

and represented outstanding capital expenditure of uSD 103.9m.

on the final trading day at oslo Stock exchange (29 December 2012), Jl’s unsecured bonds ma-turing in 2015 were trading at noK 102 (noK 100.6 at year-end 2011), cf. Figure 4, and Jl’s un-secured bonds issued in october 2012 (2017 ma-turity) were listed on oslo Stock exchange on 16 January 2013.

At year-end 2012, Jl’s solvency ratio was 37% compared to 45% at year-end 2011.

after Year-enD eVentSIn connection with the approval of Jl’s Annual Re-port for 2012, the lauritzen Foundation decided to convert two subordinated loans of originally DKK 850m into equity. At year-end 2012, the loans in-cluding accrued interest amounted to a total of DKK 903.1m, equivalent to uSD 159.6m. the con-version increases Jl’s solvency ratio from 37% at year-end 2012 to 44%.

95

97

99

101

103

105

107

109

111

2011/01 2011/04 2011/07 2011/10 2012/01 2012/04 2012/07 2012/10

J. Lauritzen a/S · AnnuAl RepoRt 201214

outLooK for 20132013 opened with very low spot earnings in all dry bulk markets, a slight improvement in the market for smaller semi-refrigerated gas carriers and firmness for fully pressurised gas carriers. the stronger spot market for mR product tankers re-corded in late 2012 continued. We expect eco-nomic growth to be somewhat subdued during the first half of 2013. A number of indicators sug-gest that economic growth will strengthen as the year progresses. once economic growth rises, we expect to see inventories rebuilding which will contribute to seaborne trade growth.

Scheduled deliveries of merchant vessels amount to about 175m dwt in 2013. Due to cancellations and slippage which are expected to continue as a result among other things of the tight credit and lending situation in the shipping industry, actual deliveries are likely to be 25% below scheduled deliveries. Dry bulk deliveries are anticipated to fall by about a third to around 70m dwt in 2013. Deliveries of mR product tankers are expected to be of the same order as in 2012, whereas smaller gas carriers are in for a sizeable rise in deliveries. A total of 19 shuttle tankers are scheduled for de-livery in 2013, however with possible delays for a number of these.

Demolition is poised for another record surpass-ing the approximately 60m dwt reported in 2012. bulk carriers will the biggest contributor for the third consecutive year.

on average, the dry bulk market is expected to be below 2012, but with some relief towards the sec-ond half of 2013 when demand growth is expect-ed to exceed supply growth. Smaller gas carriers are forecast to see the spot market weaken slight-ly in 2013 compared to 2012 due to the relatively strong supply growth. the outlook for mR product tankers is unpromising with only modest improve-ments in average spot market rates.

the result for 2013 is anticipated to remain unsat-isfactory with an expected loss of uSD (75-100)m (2012: uSD (350)m).

ebItDA is expected to be in the range of uSD 60–80m (2012: ebItDA of uSD 88.7m). taking the sale of the Accommodation and Support Vessel Dan Swift to the Axis offshore pte. ltd. and one-off items included in the 2012 ebItDA amounting to uSD 33.7m into account, the expectations for 2013 are slightly up compared to 2012. the im-provement primarily relates to lauritzen bulkers’ redelivery of time-charter vessels and increase of lauritzen tankers’ operational fleet.

J. Lauritzen a/S · AnnuAl RepoRt 2012 15

Depreciations are expected to be approximately 10% down compared to 2012 primarily as a con-sequence of the 2012 write-down’s and sale of as-sets.

Income from joint ventures is anticipated to be unsatisfactory but up on 2012. the expected in-come from Axis offshore pte. ltd. will not off-set the forecast loss from other joint ventures.

net finance is expected to be in line with the result in 2012. Currency and interest rate fluctuations may affect the result. tax is expected to be limited and minorities’ share of the result is expected to decrease.

During 2013, Jl will take delivery of the last four vessels on the current newbuilding program, three mR product tankers and one handysize bulk carrier. A part-owned handysize bulk carrier new-building will also be added to the fleet and three mR product tanker newbuildings will enter the fleet on long-term time-charter.

Capital expenditure including dockings amounts to uSD 123m to be financed by at-delivery financ-ing and own funds.

J. Lauritzen a/S · AnnuAl RepoRt 201218

lAuRItzen BuLKerSIn 2012, lauritzen bulkers’ result amounted to uSD (294.5)m compared to uSD (24.7)m in 2011, cf. table 1. the result was significantly impacted by one-off items with a net effect of uSD (200.3)m (2011: uSD (27.7)m) comprising write-downs, sale of claims and sales of vessels due to counter-party defaults. Adjusted for one-off items, the re-sult was uSD (94.2)m, down from uSD 3.0m in 2011 due to the weaker bulk markets and income lost as a consequence of counterparty defaults.

the result was very unsatisfactory.

BuSineSS moDeL anD riSK managementlauritzen bulkers (lb) controls a fleet of more than 100 handysize, handymax, panamax and capesize bulk carriers with a low average age. the fleet comprises a portfolio of owned, part-owned, and time-chartered vessels as well as vessels committed by partners. Active fleet portfolio man-agement via the sale, purchase and time-charter in/out of vessels is an important element of the business model.

the handysize operation, which is lb’s largest business activity, comprises a significant fleet of homogeneous vessels, ensuring economies of scale, operational optimisation and extensive cus-tomer service. 2012 marked a strategic change as focus on long-term cargo contracts was added to

the existing strategy based on spot and short to medium-term cargo contracts.

the handymax fleet is managed similarly to the handysize vessels, whereas most of the fleet of capesize and panamax bulk carrier fleet is em-ployed on long-term time-charter.

the main business risks are market and counter-party risks.

Counterparty risks are managed through continu-ous monitoring and evaluation of charterers’ sub-stance and performance. lower contract cover for the handysize and handymax operations means exposure to short-term market volatility which is to some extent evened out by the size of the controlled fleet. this risk is mitigated by book-ing cargoes for shorter periods (typically up to six months) or longer on affreightment contracts.

main eVentSFleet renewal continued with the aim of building a modern, fuel-efficient, versatile fleet and in 2012 the controlled fleet increased by 15 newbuildings, of which three were owned.

During the year, three long-term time-chartered and four pool vessels were redelivered as planned.

J. Lauritzen a/S · AnnuAl RepoRt 2012 19

2012 2011

Revenue 361.1 330.9 EBITDA 4.0 75.8 Depreciations and write-downs (150.7) (37.9) Profit/(loss) on sale of vessels etc. (96.6) (38.6) Operating income (243.2) (0.7) Share of profit in joint ventures (28.6) 2.3 Finance net (25.0) (18.4) Profit/(loss) before tax (296.8) (16.8) JL's share of profit/(loss) (294.5) (24.7) Invested capital (average) 1,108.3 1,121.5 Return on invested capital (24.5)% 0.1%Average no. of employees 590 493

taBLe 1: KeY figureS uSDm

20

40

60

80

100

120

140

0

20

40

2011 2012

Own Part owned Chartered Shared charter Other

figure 5: aVerage no. of VeSSeLS

the handysize fleet increased by 12 newbuildings, of which three were owned and four were taken on long-term time-charter. pool partners contrib-uted five additional handysize newbuildings and six second-hand handysize bulk carriers to the controlled fleet.

the handymax fleet grew by three newbuildings on long-term time-charter.

lb was severely affected by counterparty defaults with subsequent sales of two capesize bulk carri-ers due to strategic considerations. the risk man-agement desk and risk management procedures were further enhanced during the year, and a car-go desk was established focusing on medium to long-term cargo contracts.

earnings from the handysize operations yet again

outperformed the bhSI (baltic handysize Index). this was achieved through a combination of serv-ing existing and new customers and exploitation of short-term trading opportunities.

towards the end of the year, Island View Shipping announced its withdrawal from the handysize pool, meaning that 14 handysize vessels will leave the pool in the first half of 2013. the withdrawal will not impact the critical mass of lb’s handysize operations.

lb was the runner-up as “Ship operator of the year” in lloyd’s list Awards Asia 2012.

fLeetIn 2012, the total number of ship-days reached 43,539 with 119 vessels on average, 23% up on the figure reported in 2011, cf. Figure 5.

the operational fleet of handysize bulk carriers av-eraged 80 vessels compared to 65 vessels in 2011. At year-end 2012, the controlled handysize fleet comprised 90 vessels.

on average, the handymax fleet comprised 22 vessels in 2012 compared to 14 vessels in 2011, with a further 4 panamax vessels (four in 2011) and 8 capesize vessels (seven in 2011).

At year-end 2012, lb had 43 vessels on long-term time-charter (including two newbuildings for de-livery in 2014), with purchase options for 9 of these.

the owned fleet comprised 25 vessels at the end of 2012 (24 in 2011) with part ownership of a fur-ther 18 vessels (21 in 2011).

At the end of 2012, the average age of the owned fleet was 2.3 years.

fLeet managementtechnical management, including crewing for owned bulk carriers, was undertaken by new Century overseas management Inc., manila, Fleet management ltd., hong Kong and Synergy maritime pte., Singapore.

J. Lauritzen a/S · AnnuAl RepoRt 201220

our technical department works closely with ex-ternal providers on all aspects of achieving safe, cost-effective and reliable vessel operations.

three scheduled dry dockings were completed in 2012. unscheduled off-hire for lb’s owned fleet came to 0.29 % in 2012 (0.31 % in 2011).

hSeeQour in-house technical department monitors overall fleet safety performance and energy effi-ciency in order to comply with applicable national and international rules and regulations as well as increasing client requirements.

We constantly endeavour to minimize risks asso-ciated with our operations. In 2012, we enrolled with ship vetting specialists RightShip’s rating programme and the average risk rating of the owned fleet was 4.9 on the RightShip vetting scale (with 5.0 as best rating) in mid-December 2012.

During 2012, we developed a range of different initiatives to support our ongoing efforts to reduce fuel oil consumption and reduce emissions of Sox, nox and Co2. our specific initiatives are list-ed in Jl’s Corporate Responsibility report 2012 p. 16-17.

gLoBaL marKet DeVeLoPmentSthe period market for bulk carriers had another difficult year with capesize 12 month period rates down by 20% and handysize/handymax down by 30% compared to 2011. panamax bulk carriers suffered even more. the period market decline was due to deteriorating market imbalances which saw second-hand tonnage prices falling by 20% or more from year-end 2011 to year-end 2012.

2012 started with a very weak spot market for all segments, with handysize and handymax recov-ering from end February and peaking in late July. Capesize had stronger markets from September onwards, as did panamax, but the rise could not be sustained. Compared to 2011, the spot market fell by approximately 30% for handysize and handymax in 2012, cf. Figure 6.

DemanD for BuLK carrierSDemand for bulk carriers is estimated to have grown by around 6% in 2012 compared to 7.5% in 2011, cf. Figure 7. many factors contributed to the fairly high, albeit lower than generally expected, demand growth.

J. Lauritzen a/S · AnnuAl RepoRt 2012 21

figure 6: SPot marKet rateS 2010-2012 uSD/DaY

SouRCe: ClARKSon ReSeARCh SeRVICeS

figure 7: DemanD for DrY BuLK carrierS 2003-2012 DWtm

SouRCe: lb buSIneSS AnAlySIS bASeD on DAtA DeRIVeD FRom mSI ltD.

figure 8: SuPPLY of DrY BuLK carrierS 2003-2012 (Beginning of Year) DWtm

SouRCe: lb buSIneSS AnAlySIS bASeD on DAtA DeRIVeD FRom ClARKSon ReSeARCh SeRVICeS

400

500

600

0

100

200

300

003 04 05 06 07 08 09 10 11 12

Iron Coal Grain+Soya Minor Bulks

500

600

700

800

0

100

200

300

400

003 04 05 06 07 08 09 10 11 12

Capesize Panamax Handymax Handysize

2000

3000

4000

5000

18000

24000

30000

36000

0

1000

2000

0

6000

12000

2010/01 2010/07 2011/01 2011/07 2012/01 2012/07

Average of the 6 T/C Routes for the Baltic Handysize IndexAverage of the 6 T/C Routes for the Baltic Handysize IndexAverage of the 6 T/C Routes for Baltic Supramax IndexBaltic Exchange Dry Index (1st November = 1334) - RHS

J. Lauritzen a/S · AnnuAl RepoRt 201222

60.0%

80.0%

100.0%

120.0%

0.0%

20.0%

40.0%

Handysize Handymax Panamax Capesize

25 years or more 15-24 years 0-14 years Order book

SouRCe: lb buSIneSS AnAlySIS bASeD on DAtA DeRIVeD FRom ClARKSon ReSeARCh SeRVICeS

figure 9: BuLK carrier age ProfiLe anD orDer BooK at Year-enD 2012 (% of exiSting fLeet)

uncertainty in credit markets as well as fairly tight monetary policies in for example China in early 2012 led commodity consumers and traders to keep inventories low in many parts of the world, or to actually reduce them. During the following months, economic uncertainties in europe in-creased with negative repercussions for econom-ic growth for the remainder of the year.

A combination of reduced economic activity in mature economies and economic policies to curb inflationary pressures in China led to lower fixed investment growth which in turn reduced growth in imports of iron ore and other minerals.

Coal, mainly steam coal, was the biggest contrib-utor to demand growth for bulk carriers in 2012. Falling prices for coal due to ample supplies in combination with rising electricity production in-creased power plants’ demand for steam coal. this demand was further increased by droughts and high prices for natural gas in europe.

grain shipments were at higher levels during the first half 2012 than in 2011 but due to crop failures in various parts of the world, prices increased to levels that made consumers postpone purchases which had a detrimental impact on demand in late Q3 and Q4, affecting particularly handysize and handymax.

SuPPLY of BuLK carrierSAt the beginning of 2012, the world fleet of bulk carriers amounted to 616m dwt. Deliveries and demolitions both increased in 2012 compared to 2011, leading to net fleet growth of 10.5% (14.7% in 2011) with the world bulk fleet at 680m dwt at year-end 2012, cf. Figure 8.

Fleet growth in the handymax, panamax and capesize segments was 10%, 13% and 12% re-spectively whereas the handysize fleet only in-creased by 2%.

orders for bulk carriers declined for the second consecutive year, and as a result of the heavy de-livery schedule which was characterised by less slippage than expected, the order book was down to approximately 20% of the existing fleet at year-end 2012.

Demolition of bulk carriers amounted to approxi-mately 35m dwt compared to 23.2m dwt in 2011 due to the poor market, low probability of employ-ment and high costs of maintenance.

At year-end 2012, the orderbook for panamax stood at 30% of the existing fleet and 15-18% for the three other segments. taking into consider-ation the age profile and the demand outlook by segment, it would appear that handysize is in a comparatively well-balanced situation.

At year-end 2012, the average age of the world bulk fleet was slightly over 11 years compared to 12.5 years at year-end 2011. there are huge aver-age age differences across segments, cf. Figure 9.

after Year-enD eVentS peter borup took up his position as president of lauritzen bulkers on 1 February 2013.

outLooK for 2013We expect the very low spot market rates charac-terising the end of 2012 to continue into the first part of 2013, partly due to the low level of eco-nomic activity as well as uncertainty in many parts of the world, partly due to continued high delivery schedules in the first part of 2013.

however, 2013 is expected to witness a decelera-tion in supply growth as deliveries are forecast to fall from about 100m dwt in 2012 to about 65-70m dwt in 2013. Demolitions are expected to in-crease slightly from 35m dwt in 2012. Fleet growth is thus projected to fall from 10.5% in 2012 to about 6% in 2013.

J. Lauritzen a/S · AnnuAl RepoRt 2012 23

As in 2012, coal is expected to be a key driver of demand together with iron ore, as fiscal stimulus in China and strengthening economic activity in mature economies gather pace during the year. grain shipments are expected to rise in the sec-ond half of 2013 as crops are expected to return to normal levels. minor bulks are also poised for con-tinued growth. overall, an increase in demand growth is expected for 2013 compared to 2012, particularly in the second half of the year.

We expect the above to stop the decline in the spot market during 2013 with some improve-ments in the second half. With large surplus ship-building capacity, tonnage prices may continue their decline into 2013.

J. Lauritzen a/S · AnnuAl RepoRt 201226

lAuRItzen KoSanthe result was uSD 8.9m, up from uSD 6.5m in 2011 mainly due to improved trading conditions in the first half of 2012 and a larger average fleet of fully pressurised gas carriers, cf. table 2. the result included uSD 1.8m in gains from the sale of vessels, down from uSD 2.3m in 2011.

the result was in line with expectations and ac-ceptable taking the market conditions into consid-eration.

BuSineSS moDeL anD riSK managementlauritzen Kosan (lK) controls a modern fleet of 43 gas carriers with an average age of 8.7 years. the fleet comprises owned, part-owned, chartered vessels and vessels committed by partners. Ac-tive fleet portfolio management via cargo and pe-riod cover and the sale and purchase of vessels constitute key elements in the business model.

Strict health, safety and environmental standards and stringent client requirements are achieved through close in-house collaboration between the technical and commercial departments. Continu-ous improvements through education, innovation and careful implementation of procedures en-hance operational flexibility and higher fleet utili-zation.

As a leading tonnage supplier to the large petro-chemical and oil companies, lK continuously en-

ters into affreightment contracts, seeking to maxi-mise effective fleet cover.

While these contracts provide protection against short-term market fluctuations, due to their struc-ture they do entail some scheduling risks. these risks are connected with the flexibility provided by the affreightment contracts in terms of charterers’ right to manage their flows in accordance with the business cycle and their specific operations.

main eVentSlK took delivery of the last of a series of six 3,600 m3 fully pressurised gas carriers from yangzhou Kejin Shipyard in China designed for the growing Asian gas industry.

two 3,500 m3 fully pressurised gas carrier new-buildings were taken on long-term time-charter from Japanese owners.

A 3,500 m3 fully pressurised gas carrier was sold to Korean interests.

lK moved into its own premises in manila in 2012. the offices will be used for crew-related matters such as training and briefing/debriefing senior of-ficers.

2012 saw the launch of project ReJuICe, a major initiative to reduce fuel consumption and emis-sions.

J. Lauritzen a/S · AnnuAl RepoRt 2012 27

2012 2011

Revenue 210.3 143.2 EBITDA 35.7 33.2 Depreciations and write-downs (27.2) (26.4) Profit/(loss) on sale of vessels etc. 1.8 2.3 Operating income 10.3 9.1 Share of profit in joint ventures 0.7 2.2 Finance net (1.9) (3.7) Profit/(loss) before tax 9.1 7.7 JL's share of profit/(loss) 8.9 6.5 Invested capital (average) 408.3 423.4 Return on invested capital 2.7% 2.7%Average no. of employees 505 403

taBLe 2: KeY figureS uSDm

0

10

20

30

40

50

2011 2012

Own Part owned Chartered Shared charter Other

figure 10: aVerage no. of VeSSeLS

fLeettotal ship-days reached 15,617 for 42.8 vessels on average compared to 14,366 days for the aver-age of 39.4 vessels reported in 2011, cf. Figure 10.

lK’s fleet comprised 35 owned, part-owned and chartered vessels at year-end 2012. the average age of the company’s owned fleet was 8.6 years compared to 8.1 years at year-end 2011. At year-end 2012, the average age of the ethylene fleet was 4.6 years (3.6 years at year-end 2011), with the semi-refrigerated fleet at 16.7 years (15.7 years in 2011) and the fully pressurised fleet at 6.7 years (7.0 years in 2011).

the operated fleet consisted of 29 semi-refrigerat-ed/ethylene gas carriers on average (28 vessels in 2011) and 14 fully pressurized gas carriers (11 in 2011) with a combined capacity of about 221,950 m3 (212,650 m3 in 2011).

fLeet managementDuring the year, lauritzen Kosan Fleet manage-ment (lKFm) handled the technical management for the ethylene and semi-refrigerated gas carri-ers. part-owned Star management Associates, tokyo, handled the technical management for the fully pressurised vessels, although one Fp vessel was moved to lKFm towards the end of the year.

Six scheduled dry-dockings were completed dur-ing 2012 (six in 2011). unscheduled off-hire came to 3.0% in 2012 (2.3% in 2011). technical fleet management is based on health, safety, security, environmental and technical poli-cies to ensure efficient vessel operations in order to comply with international rules and regulations as well as stringent client expectations.

A total of 156 client vetting inspections were per-formed in 2012 (143 in 2011) in order to maintain pertinent client approvals of the vessels. on aver-age, 5.4 observations were received (6.2 in 2011). We focused especially on industry-standard SIRe inspections in which 4.8 observations were re-corded on average per inspection (5.4 in 2011). So-called crew-related observations, which could have been prevented by the crew, continued to decline (2.4 in 2012; 2.8 in 2011). Crew-related observations in SIRe inspections fell from 2.6 in 2011 to 2.3 in 2012.

Vessel crews are in the front line and their perfor-mance and attitude are essential in delivering the expected service. lKFm follows a strategy of training and education combined with perfor-mance incentives. training operations in manila were expanded and for the first time courses were given in bilbao to Spanish and Cuban seafarers. to support our activities in manila, lKFm person-nel moved into the newly established lauritzen Kosan offices in makati.

A new incentive scheme was successfully intro-duced in 2012 for captains and chief engineers in which performance is assessed and rewarded ac-cording to a set of key performance indicators for the vessel under their command. the scheme will be expanded in 2013 to include all officers on board.

J. Lauritzen a/S · AnnuAl RepoRt 201228

hSSeQhealth and safety is about protecting people and our focus on improving the safety culture for all employees is essential for us. During the past years, a broad range of safety initiatives were launched and we will continue to focus on strengthening our culture of embracing safety.

the focus for the 2012 safety campaign was on work routines and factors relating to the preven-tion of fatigue. Fatigue is recognized in the indus-try as a significant contributory factor in breaches of safety. our focus targeted implementation of new user-friendly software, interviews with crew members, changing procedures and responsibili-ties, analyses of work routines and discussions on work and watch schedules. efficient planning and on board resource utilization for our shipboard management are regarded as offering the poten-tial for increased performance. the yardstick for our efforts and ambitions is for zero harm inflicted by lK on any employee.

piracy and robbery unfortunately remain a threat to seafarers although there was a significant de-crease in attacks and hijackings during 2012. Rec-ognising our seafarers as our most important as-sets, lK continues to use private armed security teams on board our vessels operating in high risk areas.

efforts to protect the environment continued in 2012. lKFm maintains ISo 14001 certification with continuous improvement projects.

gLoBaL marKet DeVeLoPmentS After opening on a fairly strong note, the spot market weakened for smaller semi-refrigerated gas carriers from Q2. Smaller fully pressurised gas carriers enjoyed a rising trend throughout the year, whereas ethylene gas carriers witnessed a fairly flat market, cf. Figure 11.

period markets for 2012 were down by about 5% for most types of smaller gas carriers.

Second-hand prices declined marginally, whereas resale and newbuilding prices declined by 5-15% respectively during the year.

DemanD for gaS carrierSDemand for smaller gas carriers almost stagnated in 2012 on a cbm-mile basis after having posted strong growth during 2010 and 2011. petrochemi-cal gases made a negative contribution to de-mand growth with primarily lpg making a posi-tive contribution. transport of ammonia is not a significant part of demand for small gas carriers, and hence provided limited support in 2012, cf. Figure 12.

the key drivers for rising demand for lpg in small-er gas carriers were latin America and parts of Asia. Increased availability of lpg in north Ameri-ca and in Africa with stagnant supplies in the mid-dle east in combination with rising demand both from the household sector and the petrochemical industry were behind the rise in demand for small-er gas carriers transporting lpg.

pRoJeCtreJuiceIn 2012, lauritzen Kosan launched the project ReJuICe, a major initiative focusing on reducing fuel consumption and the environmental impact of our gas carrier operations. Specific initiatives for change have been brought in after a study of current operational practices, such as trim and ballast management, hull cleaning, improved regulation of power consumers and optimization of fleet utilization. together, these initiatives are expected to give a significant reduction in our carbon footprint in the form of emissions.

J. Lauritzen a/S · AnnuAl RepoRt 2012 29

figure 11: SPot marKet rateS 2010-2012 uSD ‘000/month

SouRCe: lK buSIneSS AnAlySIS bASeD on DAtA FRom FeARnley’S

figure 12: DemanD for SmaLLer gaS carrierS 2003-2012 BY ProDuct (miLL tonS)

SouRCe: lK buSIneSS AnAlySIS bASeD on DAtA FRom VIAmAR AS

figure 13: SuPPLY of SmaLer gaS carrierS 2003-2012 BY tYPe in cBmm

SouRCe: lK (23,000 Cbm) buSIneSS AnAlySIS bASeD on DAtA FRom VIAmAR AS

0

100

200

300

400

500

600

700

2010/01 2010/07 2011/01 2011/07 2012/01 2012/07

East (F/P) coaster West (S/R) coaster 6500 S/R 10000 ETH

25

30

35

5

10

15

20

-03 04 05 06 07 08 09 10 11 12

Ethylene Propylene Butadiene VCM LPG Ammonia

3

3.5

4

4.5

5

0 5

1

1.5

2

2.5

3

0

0.5

03 04 05 06 07 08 09 10 11 12

S/R vessels F/P vessels

J. Lauritzen a/S · AnnuAl RepoRt 201230

overall, there was a slight decline in transport of petrochemical gases in 2012 with VCm and ethyl-ene declining, and propylene and butadiene growing. the worsening economic climate, par-ticularly in europe but also in parts of Asia, led to a reduction in demand growth for plastics and thus in petrochemical gases. the production of ethyl-ene in China in 2012 is estimated to have been about 2% below 2011 with production of primary plastics up by 6% during the first 11 months of 2012. this has led to a strong increase in demand for ethylene imports into China.

the severe tightening of sanctions on Iran for pet-rochemical exports with effect from may 2012 af-fected smaller gas carriers severely, as Iran is a key exporter of ethylene, and the disappearance of Iran as a supplier had a detrimental effect on ethylene transportation mileage.

transportation of butadiene benefitted strongly from demand in Asia, whereas movements with propylene increased due to deficits emerging in the uS, partly due to feedstock becoming lighter with the increased use of ethane as feedstock and strongly growing demand in Asia.

SuPPLY of gaS carrierS the fleet of smaller gas carriers in the 3,200-22,999 m3 segment increased by an estimated 4% in 2012 which marked a decline in the growth rate compared to the past five years. At year-end 2012, the fleet was estimated to be slightly above 4.5m m3, cf. Figure 13. total deliveries were estimated at 0.2m m3 with deletions in the order of 0.05m m3

in 2012.

Fully pressurised gas carriers accounted for near-ly two thirds of all deliveries continuing a period of high deliveries, whereas deliveries of semi-refrig-erated and fully-refrigerated carriers declined.

the current order book including options amounts to 0.6m m3 equal to 13% of the existing fleet, of which 85% is semi-refrigerated tonnage. new or-ders increased in 2012 fivefold to almost 0.4m m3 compared to 2011. About 50% of orders in 2012 were for ethylene carriers. All orders are for deliv-ery in 2013-14, including those ordered in 2012. the schedule for delivery is almost evenly spread over the coming two years.

J. Lauritzen a/S · AnnuAl RepoRt 2012 31

figure 14: SmaLLer gaS carrierS age ProfiLe anD orDer BooK at Year-enD 2012 (% of exiSting fLeet)

SouRCe: lK buSIneSS AnAlySIS bASeD on DAtA DeRIVeD FRom ClARKSon ReSeARCh SeRVICeS

total deletions amount to approximately 0.05m m3, equal to 1.5%, with the majority being semi-refrigerated in the 5-15,000 m3 segment. this is the second year with a comparatively low demoli-tion figure which could be ascribed to the firm market with limited fleet growth.

At year-end 2012, the average age of the world fleet of semi-refrigerated gas carriers (including both ethylene and fully-refrigerated units) was 13.8 years and the order book represented 15,6% of the existing fleet. the average age of fully pres-surised gas carriers was 10,6 years and the order book was equal to 9,2% of the existing fleet, cf. Figure 14.

outLooK for 2013Various factors have the potential to keep demand growth for trade in petrochemical gases and en-suing demand for smaller gas carriers low in the first half of 2013 with improvements as the year progresses. these include the continuation of sanctions against Iran, the poor short-term eco-nomic outlook particularly in europe and the pos-sibility of major petrochemical capacity coming on stream in China.

Supply growth before demolitions is estimated at around 6%. Whereas the age profile suggests the potential for higher demolitions in 2013, we ex-pect a net supply growth of 3%. this will be of the same order as forecast demand growth, although with demand growth lagging during the first half of 2013.

60.0%

80.0%

100.0%

120.0%

0.0%

20.0%

40.0%

Semi-Refrigerated Fully-pressurised

25 years or more 15-24 yeas 0-14 years Order book25 years or more 15 24 yeas 0 14 years Order book

J. Lauritzen a/S · AnnuAl RepoRt 201234

lAuRItzen tanKerSIn 2012, lauritzen tankers’ result amounted to uSD (50.6)m compared to uSD (4.0)m in 2011, cf. table 3. the result was significantly impacted by write-downs and other one-off items with a net ef-fect of uSD (46.5)m (2011: uSD 2.5m). Adjusted for one-off items, the result was uSD (4.0)m, up from uSD (6.6)m in 2011.

the result was unsatisfactory.

BuSineSS moDeL anD riSK managementlauritzen tankers (lt) controls a fleet of 18 mod-ern mR product tankers with an average age of 3.6 years. the controlled fleet comprises owned, part-owned, and time-chartered vessels as well as vessels committed by partners.

Vessels employed in the spot market or on CoA are commercially and operationally managed by the mR pool of part-owned hafnia management, Copenhagen. pooling the spot business reduces lt’s market risk, inasmuch as the coverage ob-tained by the pool in terms of meeting customer requirements and being spread across many mar-kets provides better protection against adverse market movements. In 2012, lt remained the largest tonnage provider to this pool.

lt uses its market access to charter in/out ton-nage from/to first class charterers, providing fixed income with limited risk. In addition, sale and pur-

chase of vessels is an integrated part of the busi-ness model.

technical management responsibilities have been outsourced to external service providers.

main eVentStwo 53,500 dwt mR product tanker newbuildings were delivered to the fleet in 2012 and they were both employed on long-term time-charter.

one 50,000 dwt mR product tanker built in 2010 was taken on long-term time-charter with delivery mid-2012 and placed in the hafnia management’s mR pool. fLeetIn 2012, total ship-days reached 4,646 with 12.7 vessels on average compared to the 4,405 days with 12.1 vessels on average reported in 2011, cf. Figure 15.

At year-end 2012, lt controlled a fleet of 18 mR product tankers.

fLeet managementtechnical management of owned ships is provid-ed by Wallem Shipmanagement in hong Kong and bergen as well as mmS in Singapore and lt’s technical department works closely with both suppliers on all aspects of achieving safe, cost-ef-fective, responsible vessel operations.

J. Lauritzen a/S · AnnuAl RepoRt 2012 35

2012 2011

Revenue 61.0 62.0 EBITDA 14.3 12.2 Depreciations and write-downs (55.3) (6.3) Profit/(loss) on sale of vessels etc. - 0.0 Operating income (40.9) 5.9 Share of profit in joint ventures (1.1) 0.2 Finance net (7.6) (5.8) Profit/(loss) before tax (49.5) 0.4 JL's share of profit/(loss) (50.6) (4.0) Invested capital (average) 274.8 222.7 Return on invested capital (15.3)% 2.7%Average no. of employees 154 121

taBLe 3: KeY figureS uSDm

0

2

4

6

8

10

12

14

2011 2012

Own Part owned Chartered Shared charter Other

figure 15: aVerage no. of VeSSeLS

there were zero dry-dockings in 2012 (zero in 2011). the unscheduled off-hire for lt’s owned fleet was 0.8% (1.3% in 2011).

In 2012, seven owned vessels were inspected 23 times by oil majors. During the year, our special focus was on improving vessel performance against the oil Companies International marine Forum’s (oCImF) Ship Inspection Report pro-gramme (SIRe). Accordingly we undertook addi-tional onboard training and development for our vessels and offices. our goals were met by achiev-ing an average of 3.9 observations per vetting, which is better than industry average of 5.7. Crew-related observations accounted for an average of 2.7 of total observations. the remaining 1.2 obser-vations related to our offices and vessel construc-tion.

We continue to engage and encourage crewing by experienced, responsible multinational seafar-ers. Crews are selected for their skills in order to match our business profile and this is done in close collaboration between our external techni-cal management service providers and our tech-nical and operational departments, ensuring good dialogue and mutual understanding.

hSSeQWe are committed to a strict focus on health, safety, security and environmental protection. this is being achieved by comprehensive safety procedures, a focus on security and by maintain-ing energy-efficient operations. We thus work closely with external technical managers and monitor their performance. Consistent dialogue with these providers enables us to meet client ex-pectations for safe and efficient operations.

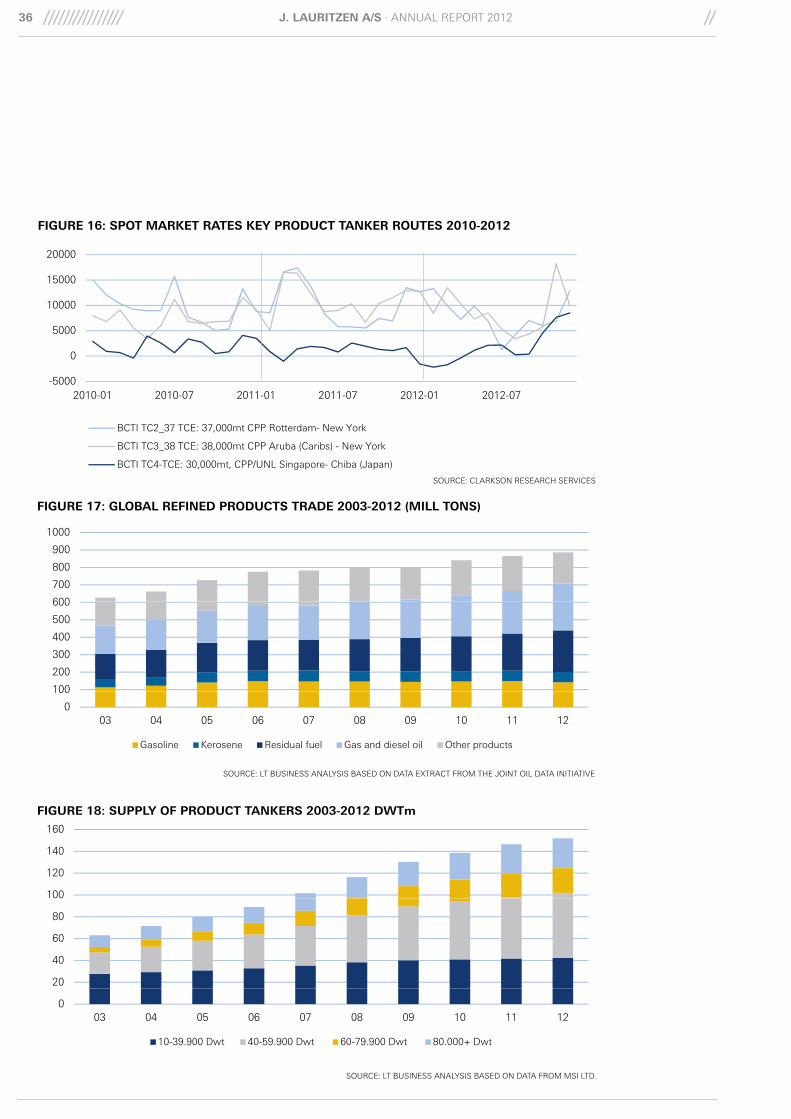

gLoBaL marKet DeVeLoPmentSAverage spot earnings on the three key mR prod-uct tanker routes were down by 20% compared to 2011, cf. Figure 16. unsatisfactory refining mar-gins towards the end of 2011 led refineries to re-duce output which dampened demand for prod-uct tankers in early 2012, mainly in the Far east. Increased economic uncertainty in europe during the summer contributed to depressing the Atlan-tic spot market during Q2 and Q3 before some seasonal strength was noted in Q4.

twelve month period rates for mR product tank-ers were on average at the same level of approxi-mately uSD/day 13,500 in 2012 as in 2011, whereas period rates for lR1 product tankers fell slightly. tonnage prices have fallen since the end of 2011; for a five year-old mR product tanker by almost 5%.

During the first months of 2012, oil prices reached their highest level since 2008 in part due to uncer-tainty relating to the sanctions against Iran, which eventually led Saudi Arabia and Qatar to increase production. With libya resuming production and Iraq steadily increasing its production, oil prices declined slightly during Q3 and then stabilised at approximately uSD 110 per barrel in Q4.

DemanD for ProDuct tanKerSglobal oil consumption grew considerably less than expected due to higher oil prices, but mainly due to less vigorous economic growth than ex-

J. Lauritzen a/S · AnnuAl RepoRt 201236

figure 16: SPot marKet rateS KeY ProDuct tanKer routeS 2010-2012

SouRCe: ClARKSon ReSeARCh SeRVICeS

figure 17: gLoBaL refineD ProDuctS traDe 2003-2012 (miLL tonS)

SouRCe: lt buSIneSS AnAlySIS bASeD on DAtA eXtRACt FRom the JoInt oIl DAtA InItIAtIVe

600

700

800

900

1000

100

200

300

400

500

600

0

100

03 04 05 06 07 08 09 10 11 12

Gasoline Kerosene Residual fuel Gas and diesel oil Other products

figure 18: SuPPLY of ProDuct tanKerS 2003-2012 DWtm

SouRCe: lt buSIneSS AnAlySIS bASeD on DAtA FRom mSI ltD.

100

120

140

160

20

40

60

80

003 04 05 06 07 08 09 10 11 12

10-39.900 Dwt 40-59.900 Dwt 60-79.900 Dwt 80.000+ Dwt

10000

15000

20000

-5000

0

5000

2010-01 2010-07 2011-01 2011-07 2012-01 2012-07

BCTI TC2_37 TCE: 37,000mt CPP Rotterdam- New York

BCTI TC3_38 TCE: 38,000mt CPP Aruba (Caribs) - New York

BCTI TC4-TCE: 30,000mt, CPP/UNL Singapore- Chiba (Japan)

J. Lauritzen a/S · AnnuAl RepoRt 2012 37

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

MR (40-60.000dwt) LR1 (60-80.000dwt)

25 years or more 15-24 years 0-14 years Order book

figure 19: ProDuct tanKerS age ProfiLe anD orDer BooK at Year-enD 2012 (% of exiSting fLeet)

SouRCe: lt buSIneSS AnAlySIS bASeD on DAtA DeRIVeD FRom ClARKSon ReSeARCh SeRVICeS

pected. According to the International energy Agency world oil consumption was up by only 1.1% on 2011.

Consequently, seaborne trade in oil products is estimated to have grown by a modest 2.2% in 2012, similar to the growth in 2011, cf. Figure 17.

trading patterns continued to change in 2012. most notably, uS imports of refined products con-tinued to decline, having fallen by one third in the course of only four years. During the same period, uS exports of refined products almost doubled, leading to net exports of some 0.8m barrels per day in 2012.

europe experienced a slight decline in imports, whereas mature economies in the pacific contrib-uted to rising seaborne trade, partly reflecting the dismantling of old refineries. the same applies to emerging markets in both Asia and in latin Amer-ica.

SuPPLY of ProDuct tanKerSby year-end 2012 the fleet of product tankers (in-cluding chemical/oil tankers) amounted to 152m dwt, up by almost 4% on 2011. the mR segment (40-60,000 dwt) increased by 6% in both 2012 and 2011, whereas the supply of lR1 product tankers (60-80,000 dwt) increased by 4% in 2012 compared to 9% in 2011, cf. Figure 18.

Deliveries of mR product tankers amounted to 3.7m dwt in 2012, similar to deliveries noted in 2011 whereas scrapping fell to 0.2m dwt from 0.5m dwt in 2011.

In general, contracting of product tankers in-creased by 35% in 2012. Contracts for mR prod-uct tankers increased by 15% to 2.6m dwt com-pared to 2011.

At year-end 2012, the average age of mR product tankers was 7.8 years (lR1 6.5 years) and the or-der book for mR product tankers amounted to 10% of the existing fleet (lR1 9%), cf. Figure 19.

outLooK for 2013A combination of weak economic growth and high prices will continue to limit growth in oil con-sumption, whilst at the same time, natural gas is making inroads into markets normally supplied by oil. In 2013 world oil consumption is thus forecast to be another year of low growth of the order of 1%.

this implies the risk of another year of low growth for product tankers in general, however with up-side potential in terms of refinery closures in ma-ture economies that could lift demand due to ad-ditional ton-miles.

For 2013, we expect that the product tanker fleet will only increase by a couple of percent, however with fleet growth of the mR segment expected to be higher.

this suggests that only a minor improvement in the market balance for mR products tankers is to be expected in 2013.

J. Lauritzen a/S · AnnuAl RepoRt 201240

lAuRItzen offShoreIn 2012, lauritzen offshore’s result amounted to uSD 8.8m, up from uSD 3.7m in 2011, cf. table 4. earnings for 2012 were significantly impacted by the formation of Axis offshore including a one-off transaction loss of uSD 7.5m. Adjusted for the one-off transaction loss, the result in 2012 was uSD 16.3m, up from uSD 3.7m in 2011. the in-crease was mainly due to the two shuttle tanker newbuildings delivered late 2011 and early 2012.

the result was in line with expectations and re-garded as acceptable.

BuSineSS moDeL our offshore activities comprise technologically advanced, dynamically positioned Accommoda-tion and Support Vessels (ASV) and shuttle tank-ers for employment in the offshore exploration and production sector. ASV operations are devel-oped as a joint venture whereas the shuttle tanker business is wholly-owned.

As our shuttle tankers are employed on long-term contracts, business risks relate to counterparty risk and the renewal/alternative employment op-tions. We continuously monitor risks and new business opportunities.

main eVentSDan Sabia, a 59,000 dwt shuttle tanker newbuild-ing, was delivered from Cosco nantong Shipyard, China, in early January 2012. on delivery, the ves-sel commenced a 12-year bareboat contract for transpetro, a wholly-owned subsidiary of petro-bras.

Due to growing market potential, a 50/50 joint venture with hitecVision, norway, was estab-lished in the ASV segment with effect from 30 June 2012. the new company, Axis offshore pte. ltd. initially comprises Jl’s monohull ASV Dan Swift currently on long-term contract to the brazil-ian oil major petrobras.

In September 2012, Axis offshore announced an order for a Semi-Submersible accommodation vessel at Cosco Qidong offshore, China, for deliv-ery during the first quarter of 2015 to meet strin-gent north Sea operating requirements. Read more at www.axisoff.com

fLeet managementhigh quality fleet management is vital in the off-shore industry and all issues relating to crewing, health, safety and the environment are managed by in-house experts, providing assurance for com-pliance with the requirements laid down in appli-cable national and international rules and regula-tions.

there were zero dry-dockings 2012 (two in 2011). unscheduled off-hire for the shuttle tanker fleet was zero in 2012 (also zero in 2011).

of the three owned shuttle tankers, only Dan ea-gle had a vetting under the Ship Inspection Report programme (SIRe) in 2012. Four minor observa-tions were made. three were immediately recti-fied but the last related to vessel design. the two shuttle-tankers Dan Cisne (2011) and Dan Sabia (2012) have both been lined up for future SIRe in-spections during the year.

Crew are regarded as a vital resource, so all offi-cers for offshore vessels are selected carefully. Where ratings are concerned, close collaboration with skilled and proven crew managers continued in 2012 to ensure a high level of retention. off-shore is a highly competitive segment for crewing

J. Lauritzen a/S · AnnuAl RepoRt 2012 41

2012 2011

Revenue 60.1 66.2 EBITDA 40.4 37.6 Depreciations and write-downs (16.8) (20.7) Profit/(loss) on sale of vessels etc. (7.5) - Operating income 16.1 16.9 Share of profit in joint ventures 2.7 - Finance net (10.8) (11.6) Profit/(loss) before tax 7.9 5.3 JL's share of profit/(loss) 8.8 3.7 Invested capital (average) 364.6 464.0 Return on invested capital 5.1% 3.6%Average no. of employees 58 126

taBLe 4: KeY figureS uSDm

and so a lot of resources are used to constantly keep officers and ratings updated with specialized courses and training in order to meet our clients’ expectations.

hSSeQlauritzen offshore (lo) is committed to providing safe working conditions in a markedly diverse multicultural and multilingual working environ-ment. We have management systems certified to inter-national standards in place to ensure the well-be-ing of staff, third party contractors and others who may be affected by our activities, in an effort to minimize any impacts.

In 2012, lo continued to implement our health, safety and environment strategy. Results included

a lost time Injury Frequency (ltIF) of zero and a total Recordable Case Frequency (tRCF) of 5.2. gLoBaL marKet DeVeLoPmentSunlike the two previous years, 2012 was a some-what quiet year in terms of new projects being tendered by operators. A 15-year contract for two Suezmaxes in the north Sea was signed, and the market also saw two shuttle tankers obtaining contract extensions.

the huge expansion in the market for shuttle tank-ers in the past couple of years has boosted the or-der book to 35% of the existing fleet. part of the fleet is growing fairly old but we expect that a market for older vessels will develop in Africa and South east Asia, as new and modern Dp2 or Dp3 vessels come on stream.

Including orders (two of which are options), the world fleet comprises almost 100 units. Average vessel age is decreasing, cf. Figure 20. only nine shuttle tankers of the total fleet are less than 60,000 dwt, with seven between 60,000 dwt and 99,000 dwt, with the balance between 100,000 and 165,000 dwt.

outLooK for 2013nineteen shuttle tankers are scheduled for deliv-ery in 2013, of which 15 units are considered firm with the balance possibly subject to delay. With oil prices continuing at uSD 100/ barrel or more in 2013, an increasing number of new deepwater offshore projects are forecast to be initiated with subsequent higher demand for shuttle tankers.

10

11

12

13

40

60

80

100

120

Ave

rag

e ag

e

No. of

vess

els

8

9

10

0

20

40

60

2011 2012 2013 2014 2015

Ave

rag

No. of

v

<<< Fleet <<< Orderbook Average age >>>

figure 20: gLoBaL ShuttLe tanKer fLeet anD age ProfiLe (Beginning of Year)

SouRCe: lAuRItzen oFFShoRe (oWn ReSeARCh)

J. Lauritzen a/S · AnnuAl RepoRt 201242

FInAnCe AnD inVeStor reLationSmaintaining strong and open relations with bond investors and lenders enables Jl to benefit from having access to a range of resources to finance our business activities.

financingReflecting the fact that our business operations are capital intensive, the financing for Jl’s assets comes from different financial resources and our financial policy has three main objectives:

• Secure the necessary liquidity.• Secure the lowest possible cost of debt capi-

tal taking market terms and conditions into consideration.

• maintain financial independency through prudent financial risk management and a di-versified funding base.

Jl’s board of Directors has approved a financial strategy including a set of guidelines for group solvency ratio, liquidity target and policies for fi-nancing debt, including:

• group solvency ratio of at least 35% and pref-erably not less than 40%.

• group liquidity (cash and cash equivalents) of at least uSD 50m plus a buffer to withstand a severe crisis.

• Debt financing for newbuildings to be drawn down at or after delivery of vessels.

• CApeX to be paid out of the group’s cash

holdings (during the construction phase of newbuildings).

• no single bank to contribute more than 25% of total debt.

Jl’s owned fleet is financed with a mix of debt and own funds.

our remaining newbuilding program of owned vessels is fully financed. At year-end 2012, CApeX remaining under the newbuilding program amounted to uSD 104m and committed funding totalled uSD 63m. the newbuilding program comprises four vessels.

Debt financinglong-term debt is generally held by J. lauritzen A/S but in some instances subsidiaries J. laurit-zen Singapore pte. ltd. or lauritzen Shuttletank-ers Singapore pte. ltd. are borrowers of long-term debt.

bank facilities account for the majority of the debt financing. At year-end 2012, bank facilities (amor-tizing term loans and revolving facilities) account-ed for 83% of total debt excluding subordinated loans. bank facilities are secured by mortgages on the vessels being financed. of the 83% bank facilities, 21% percentage points were eCA (ex-port Credit Agency) backed facilities at year-end 2012, cf. Figure 21.

J. Lauritzen a/S · AnnuAl RepoRt 2012 43

Issuer J. Lauritzen A/S J. Lauritzen A/S

ISIn no 001 0572381 no 0010 661846

type Senior unsecured bond Senior unsecured bond

Coupon p.a. Fixed 10.5% Floating rate 8.25% + nIboR 3mths

Issue date 05 may 2010 24 october 2012

maturity date 05 may 2015 24 october 2017

Amount noK 700m noK 500m

Interest payment Annual Quarterly

listing oslo Stock exchange oslo Stock exchange (As from 16 January 2013)

existing term loans (amortizing loans with a bal-loon payment at maturity) mature in 2016 and 2017. existing eCA backed term loans (fully amor-tizing loans) mature in 2021 and 2022. Revolving facilities (partially amortizing credits with a bal-loon payment at maturity) mature between 2014 and 2017.

Jl’s existing bank facilities include covenants on the mortgaged vessels relevant to the ordinary conduct of business. bank facilities also include minimum value requirements (e.g. minimum re-quirements relating to a ratio between the fair market value of the security and outstanding debt in the particular facility) between 100% and 130%. Finally, facilities include financial covenants on Jl’s value-adjusted (taking e.g. vessels at broker valuation) consolidated solvency ratio (minimum 30%), Jl’s consolidated liquidity (minimum uSD

500

750

1000

1250

1500

0

250

500

2013 2014 2015 2016 2017

Term Loan Term Loan ECA backed Revolving

Subordinated Loan Bond UnsecuredSubordinated Loan Bond Unsecured

figure 21: forecaSt outStanDing DeBt Year-enD uSDm

taBLe 5: JL’S corPorate BonD iSSue

50m) and Jl’s consolidated working capital ratio (to be 1:1 or better).

Jl was in compliance with all bank loan and bond debt covenants at year-end 2012.

At year-end 2012, corporate bonds accounted for a further 17% of outstanding debt excluding sub-ordinated loans. Issued bonds include financial covenants on Jl’s consolidated solvency ratio (minimum 30%) and consolidated liquidity (mini-mum uSD 50m).

our strategy is to have approximately uSD 300m or the equivalent in other currencies in outstand-ing debt on a rolling basis, based on corporate bond issuance. the first step was taken in may 2010 with the issuance of noK 700m in corporate bonds (ISIn no0010572381) with maturity in may 2015. the next step was taken in october 2012 when Jl issued noK 500m in a new corporate bond (ISIn no0010661846) with maturity in oc-tober 2017, cf. table 5. We expect to continue to issue additional corporate bonds in the future.

no bank or bond debt requires refinancing until mid-2014, cf. figure 22.

J. Lauritzen a/S · AnnuAl RepoRt 201244

200

250

300

350

400

0

50

100

150

200

2013 2014 2015 2016 2017Bullit Subordinated loan Bullit Bond Bullit Term Loan Repayment

figure 22: rePaYment ProfiLe of outStanDing DeBt

equityJl is a private (non-listed) company owned by the lauritzen Foundation. As a non-listed company Jl has no direct market access to equity.

however, Jl benefits from having an owner with a long-term vested interest in shipping and we have received the following subordinated loans from our owner:

• DKK 600m on 1 April 2009 with an original maturity on 1 April 2014. however, in may 2012 the owner agreed to extend the maturi-ty on this subordinated loan by an additional eight years to 1 April 2022.

• DKK 250m on 7 January 2010 with maturity on 31 January 2015.

early 2013, the lauritzen Foundation decided to convert the two subordinated loans into equity. At year-end 2012, the loans including accrued inter-est amounted to a total of DKK 903.1m, equiva-lent to uSD 159,6m. the conversion increases Jl’s solvency ratio from 37% to 44%.

Joint ventures and part-ownershipJl considers joint-ventures an attractive way to providing access to new markets or increasing our fleet with a view to gaining economies of scale in particular markets or market segments.

Some of the handysize bulk carrier vessels oper-ated by lauritzen bulkers are part-owned vessels,

Note: Bullet payments on existing bank facilities are normally refinanced on or before maturity

by way of pledging the particular financed vessels in a new facility and using proceeds to re-

deem the existing facility.

J. Lauritzen a/S · AnnuAl RepoRt 2012 45

StoCK eXChAnge announcementS 2012the following Stock exchange announcements were made in calendar 2012 via oslo Stock ex-change.

announcement no. 1:Financial report for 2011, 23 February 2012

announcement no. 2:Further strengthening of funding and revised outlook for 2012, 10 may 2012

announcement no. 3:J. lauritzen establishes joint venture with hitecVision, 4 July 2012

announcement no. 4: Interim financial report for the first half of 2012, 14 August 2012

announcement no. 5 :J. lauritzen contemplates bond issue, 10 october 2012

announcement no. 6:J. lauritzen successfully completes noK 500m bond issue, 11 october 2012

announcement no. 7:Kastrup-nielsen will take over as Ceo after Janholt in February 2013, 14 november 2012

announcement no. 8 :lower ebItDA and write-down as result of impairment, 21 December 2012

with lauritzen bulkers having co-ownership. Sim-ilarly a part of lauritzen Kosan’s fleet of ethylene gas carriers is co-owned together with a joint ven-ture partner and operated by lauritzen Kosan.

In 2012, lauritzen offshore formed the AXIS off-shore joint venture together with our norwegian partner, hitecVision, with a view to growing its presence in the offshore accommodation and support vessel segment.

inVeStor reLationSAs mentioned above, an integral part of our finan-cial strategy is to be a recurring issuer of corpo-rate bonds and since may 2010, Jl has had cor-porate bonds listed on oslo Stock exchange. Relations with the investor community are thus important for us.

Jl’s objective is for the market price of securities we issue to fairly reflect the Jl group’s financial performance, our actual and forecast ability to create value and our ability to repay our obliga-tions as they fall due. In doing so, we strive to pro-vide timely, precise and relevant information on Jl group strategy, our business, results and expecta-tions and other matters which affect the percep-tion and assessment of the securities we issue.

Jl seeks to maintain an open dialogue with cur-rent and potential investors, analysts and other market professionals and to provide them with easy and equal access to information from us.

Jl held several investor meetings and conference calls in 2012. presentations from these meetings are available on our website where all announce-ments and financial reports issued by Jl are also available. Investor relations activities in 2012 fo-cused on keeping the investor community updat-ed on developments at Jl but also on exploring our opportunities for issuing further corporate bonds. on the back of these efforts, we success-fully launched and sold a second corporate bond in october 2012.

In order to align Jl’s financial reporting with the standards of other issuers, we will begin releasing quarterly interim financial reports from Q1/2013.

Future investor relations activities are expected to remain at the same level as in 2012.

J. Lauritzen a/S · AnnuAl RepoRt 201246

RISK management

As a cyclical, global industry, shipping is exposed to a large number of diverse risk factors with the potential to heavily impact on the way business is conducted.

the purpose of risk management is to ensure that risks affecting Jl’s operations are identified, moni-tored and dealt with according to the risk toler-ance set for each type of risk.

Jl as a group has identified, monitors and man-ages four main types of risk: business Risks (e.g. freight rates, fuel oil prices, asset values and oper-ating costs), Financial Risks (e.g. interest rates, currencies and liquidity), Credit Risks (e.g. credit rating of counterparties) and operational Risks (e.g. safety, insurance, It and piracy). Risk man-agement is an integral part of Jl’s corporate gov-ernance, see p. 50-53.

As a shipping company we create value by taking calculated risks relating to our core businesses. For operational risks, our risk tolerance is in prin-ciple zero and risks relating to operations, safety, environment and It systems are reduced as much as possible. We have a low risk tolerance related for financial risks and these are managed closely and minimised in order to support our strategy. policies on risk management and risk limitation are approved by the board of Directors. Key risk factors both at group level and for individual busi-ness units are regularly assessed and prioritised

based on how likely they are to occur and their potential impact. the group and individual busi-ness units also have procedures in place to ensure consistent day-to-day risk management.