annual shareholder meeting -...

TRANSCRIPT

ANNUAL SHAREHOLDER MEETINGJANUARY 5, 2016

SAFE HARBOR STATEMENT

Statements in this presentation are "forward-looking statements" within the meaning of the Private Securities Litigation

Reform Act. The forward-looking statements can generally be identified by words such as "believes," "anticipates,"

"expects" or words of similar meaning. Forward-looking statements also include statements relating to the Company's

future performance, such as future prospects, revenues, profits and cash flows. The forward-looking statements are

subject to risks and uncertainties, which may cause actual results to be materially different from any future performance

suggested in the forward-looking statements. Such risks and uncertainties include those factors described in Part 1A of

the Company’s most recent Annual Report on Form 10-K, as such may be amended or supplemented by subsequent

Quarterly Reports on Form 10-Q or other reports filed with the Securities and Exchange Commission. Readers are

cautioned not to place undue reliance on these forward-looking statements. The forward-looking statements are made

only as of the date hereof, and the Company undertakes no obligation to publicly release the result of any revisions to

these forward-looking statements. For more information, please refer to the Company’s filings with the Securities and

Exchange Commission.

During this presentation, we will discuss GAAP measure such as net income, as well as certain non-GAAP measures

such as EBITDA. We have posted on www.investor.arinet.com, a reconciliation of these non-GAAP financial measures

to the most comparable financial measures under GAAP.

1

SHAREHOLDER PROPOSALS

• Proposal # 1: Election of Directors

• Proposal #2: Ratification of Auditors

2

QUESTIONS?

3

REVIEW ACTUAL VS. FY15 “OUTLOOK”

Roy W. Olivier – President & CEO

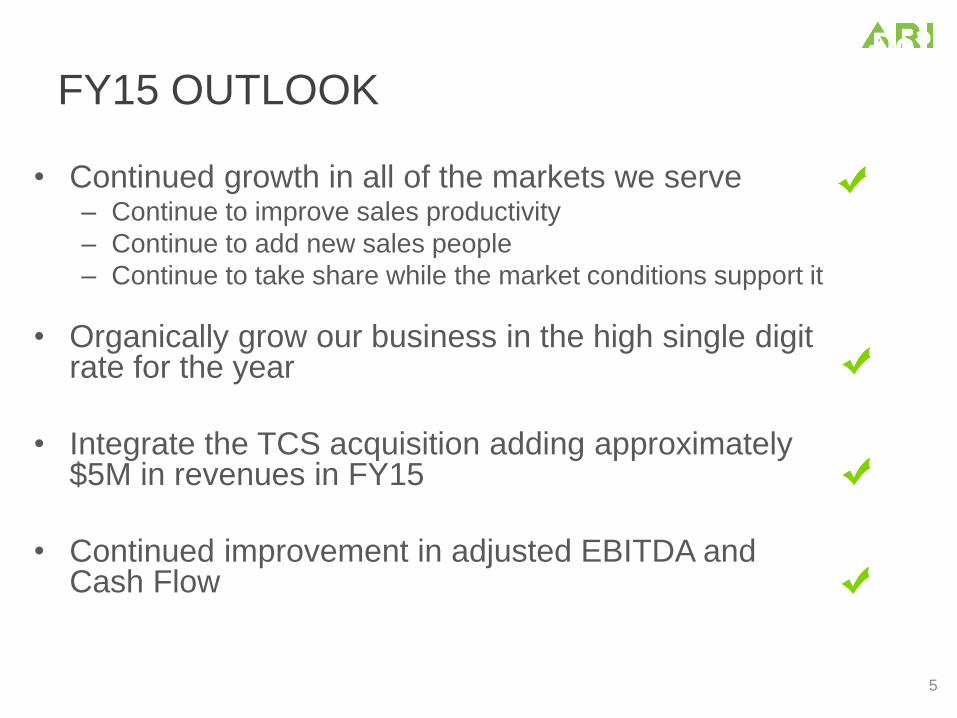

FY15 OUTLOOK

• Continued growth in all of the markets we serve– Continue to improve sales productivity

– Continue to add new sales people

– Continue to take share while the market conditions support it

• Organically grow our business in the high single digit rate for the year

• Integrate the TCS acquisition adding approximately $5M in revenues in FY15

• Continued improvement in adjusted EBITDA and Cash Flow

5

FY15 Outlook – How Did We Do?

INCREASING SHAREHOLDER VALUE

6

Stock Close Gain/Loss ADTV Gain/Loss

Jan 1, 2015 $3.65 22,246

Dec 31, 2015 $4.50 +23% 23,437 +5%

Coverage

Craig Hallum Buy Rating $5.25 Target

Ascendiant Capital Markets, LLC Buy Rating $5.50 Target

H.C. Wainwright & Co. Buy Rating $5.50 Target

Additional Info:

Attended 11 Conferences and conducted 3 Road Shows

Have 20 Institutional Investors vs. 15 in FY14

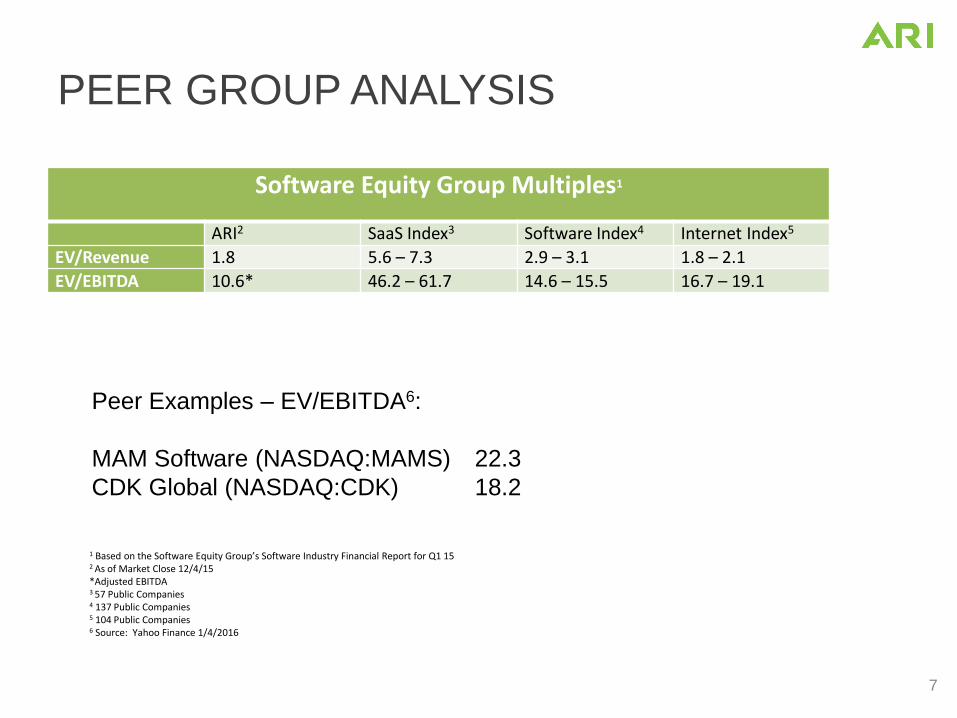

PEER GROUP ANALYSIS

Software Equity Group Multiples1

ARI2 SaaS Index3 Software Index4 Internet Index5

EV/Revenue 1.8 5.6 – 7.3 2.9 – 3.1 1.8 – 2.1

EV/EBITDA 10.6* 46.2 – 61.7 14.6 – 15.5 16.7 – 19.1

7

1 Based on the Software Equity Group’s Software Industry Financial Report for Q1 152 As of Market Close 12/4/15*Adjusted EBITDA3 57 Public Companies4 137 Public Companies5 104 Public Companies6 Source: Yahoo Finance 1/4/2016

Peer Examples – EV/EBITDA6:

MAM Software (NASDAQ:MAMS) 22.3

CDK Global (NASDAQ:CDK) 18.2

FY15 FINANCIAL RESULTS

Bill Nurthen - CFO

8

ANNUAL INCOME STATEMENT SUMMARY

9

(Dollars in Millions, Except Per Share Data)

FY15 FY14 YoY

Revenue $40.4M $33.0M 22.5%

Gross Profit $33.1M $26.6M 24.4%

Operating Income $2.3M $0.4M 550.0%

Net Income $1.1M ($0.1)M 1150.0%

Earnings Per Share $0.07 ($0.01) 800.0%

Adjusted EBITDA* $6.6M $4.4M 48.6%

Gross Margin 81.9% 80.7%

Operating Expenses (as a % of Revenue)

Sales & Marketing 25.8% 28.3%

Customer Operations and Support 19.3% 20.1%

Software Development and Technical Support 10.4% 8.2%

General and Administrative 16.4% 18.8%

Depreciation, Amortization, Other 4.3% 4.1%

Operating Margin 5.7% 1.1%

Adjusted EBITDA Margin 16.3% 13.4%

*Non-Gaap Reconci l iation of Adjusted EBITDA for FY15 and FY14 can be found at investor.arinet.com.

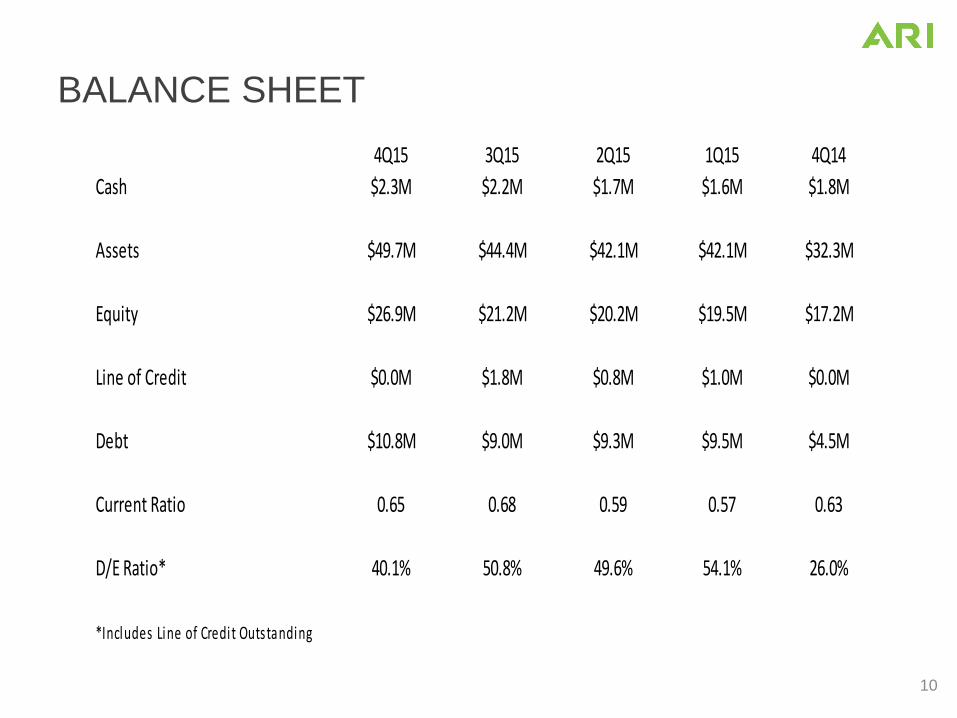

BALANCE SHEET

10

4Q15 3Q15 2Q15 1Q15 4Q14

Cash $2.3M $2.2M $1.7M $1.6M $1.8M

Assets $49.7M $44.4M $42.1M $42.1M $32.3M

Equity $26.9M $21.2M $20.2M $19.5M $17.2M

Line of Credit $0.0M $1.8M $0.8M $1.0M $0.0M

Debt $10.8M $9.0M $9.3M $9.5M $4.5M

Current Ratio 0.65 0.68 0.59 0.57 0.63

D/E Ratio* 40.1% 50.8% 49.6% 54.1% 26.0%

*Includes Line of Credit Outstanding

CASH FLOW SUMMARY

FY15 FY14

Cash Flow Operations $6.3M $2.4M

Capital Expenditures $0.7M $0.6M

Software Development $1.4M $1.8M

Free Cash Flow* $4.2M $0.0M

*Free Cash Flow defined as Cash Flow from Operations less Capital Expenditures and Software Development Capitalized

11

ANNUAL OPERATING METRICS

FY15 FY14

Churn -15.5% -12.6%

CAC Ratio 10.3 12.1

Recurring Revenue % 90.2% 93.6%

Total Dealer Sales Bookings (ACV) $7.0M $6.0M

12

QUARTERLY REVENUE ($ MIL)

13

5.4 5.5 5.7 5.95.9

7.5

8.2 8.5 8.2 8.1 8.28.5

9.1

10.1 10.310.9

0

2

4

6

8

10

12

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15

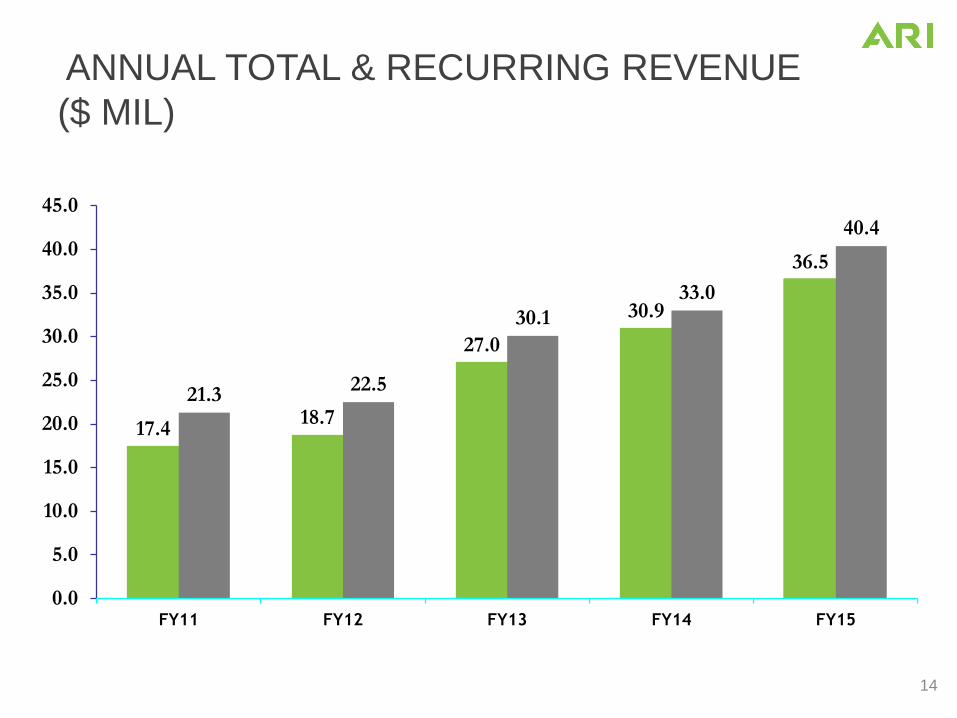

ANNUAL TOTAL & RECURRING REVENUE

($ MIL)

14

17.418.7

27.0

30.9

36.5

21.322.5

30.1

33.0

40.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

FY11 FY12 FY13 FY14 FY15

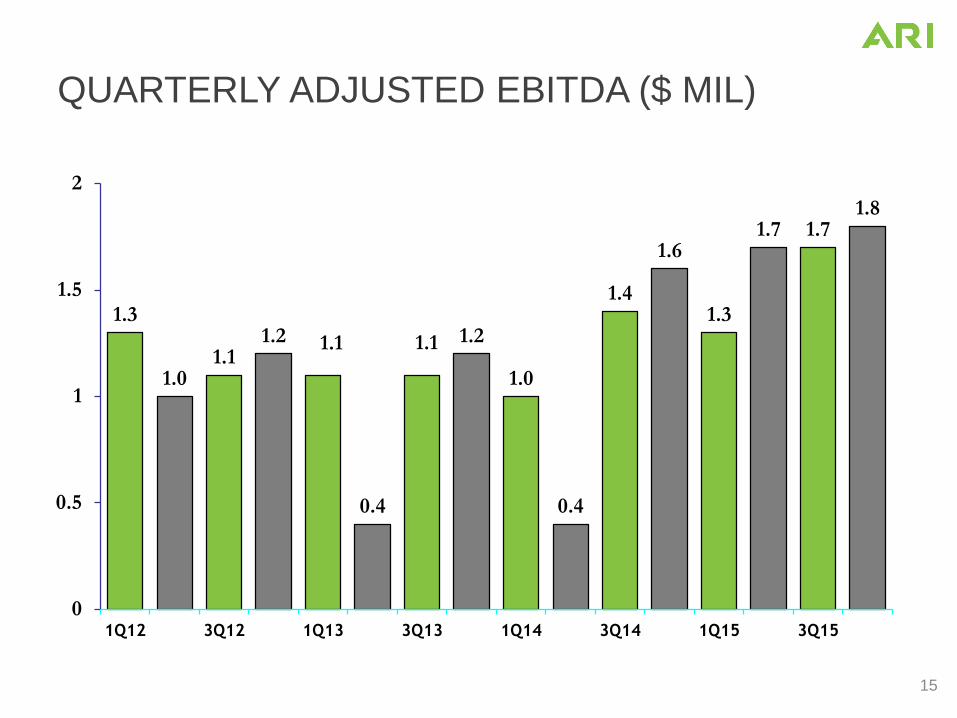

QUARTERLY ADJUSTED EBITDA ($ MIL)

15

1.3

1.01.1

1.2 1.1

0.4

1.1 1.2

1.0

0.4

1.4

1.6

1.3

1.7 1.71.8

0

0.5

1

1.5

2

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15

ANNUAL ADJUSTED EBITDA ($ MIL)

16

5.2

4.6

3.8

4.4

6.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

FY11 FY12 FY13 FY14 FY15

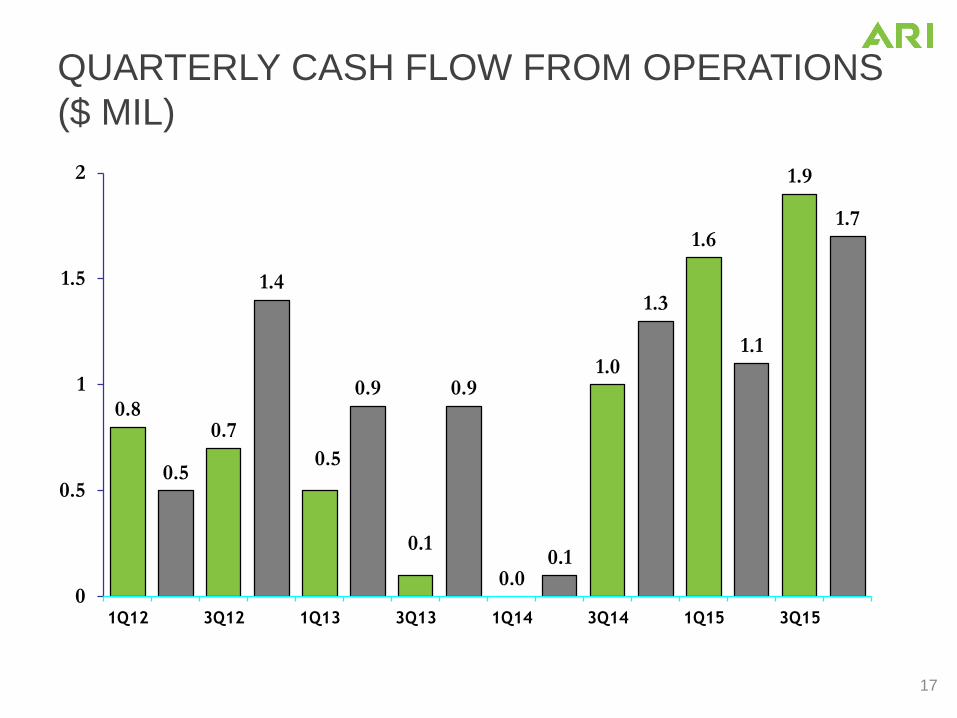

QUARTERLY CASH FLOW FROM OPERATIONS

($ MIL)

17

0.8

0.5

0.7

1.4

0.5

0.9

0.1

0.9

0.00.1

1.0

1.3

1.6

1.1

1.9

1.7

0

0.5

1

1.5

2

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15

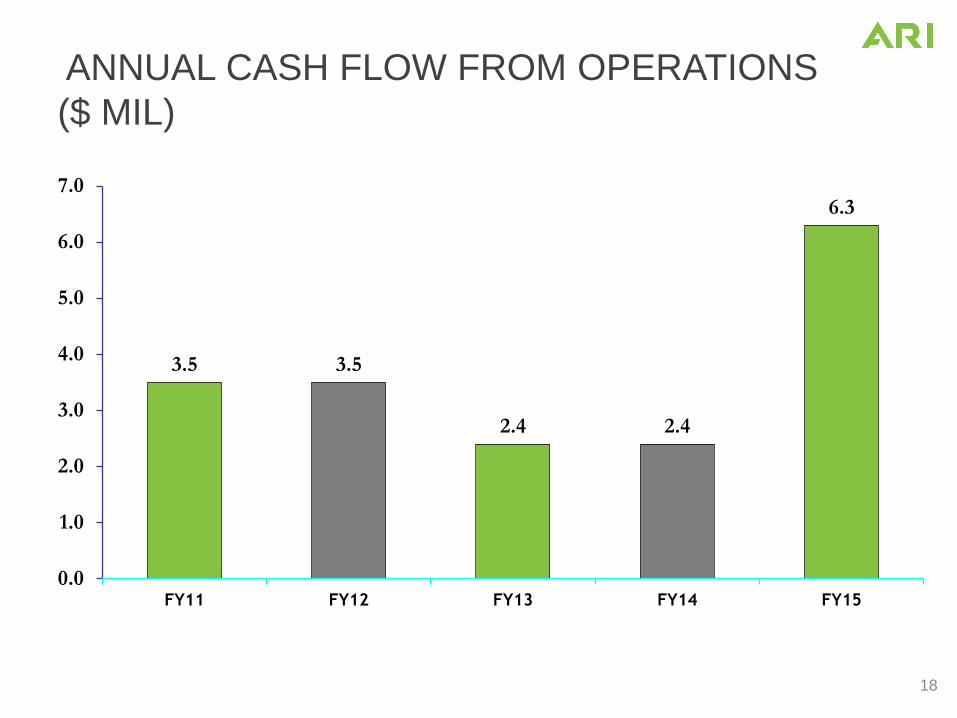

ANNUAL CASH FLOW FROM OPERATIONS

($ MIL)

18

3.5 3.5

2.4 2.4

6.3

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

FY11 FY12 FY13 FY14 FY15

QUARTERLY FREE CASH FLOW ($ MIL)

19

0.2

0.0 0.0

0.8

-0.3

0.4

-0.4

0.2

-0.8 -0.7

0.5

0.9

1.3

0.5

1.4

1.1

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1Q12 3Q12 1Q13 3Q13 1Q14 3Q14 1Q15 3Q15

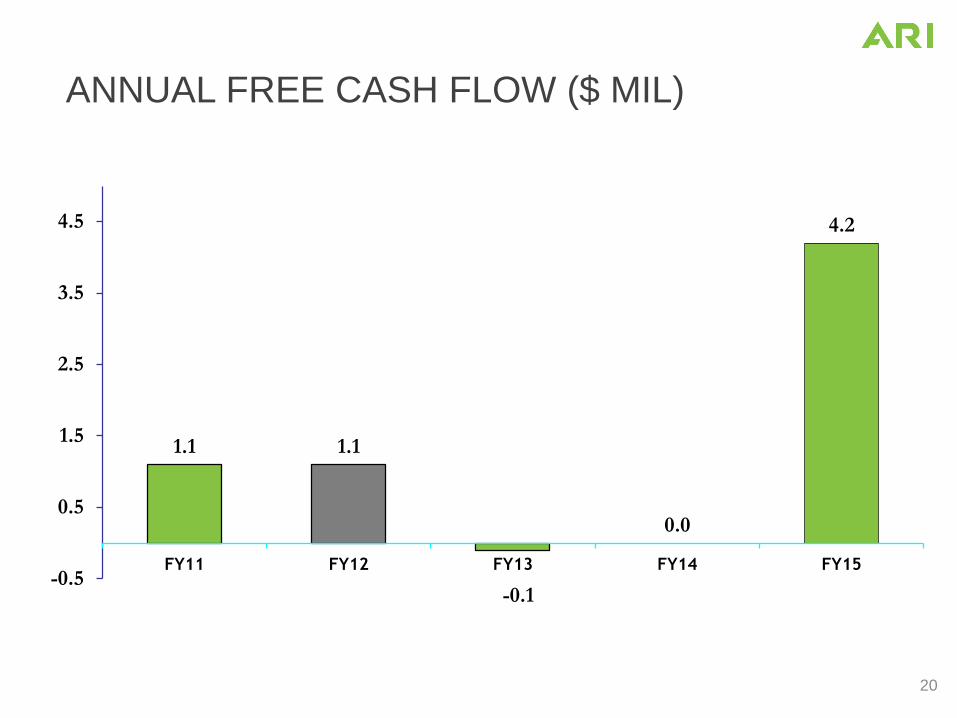

ANNUAL FREE CASH FLOW ($ MIL)

20

1.1 1.1

-0.1

0.0

4.2

-0.5

0.5

1.5

2.5

3.5

4.5

FY11 FY12 FY13 FY14 FY15

$0.0

$10.0

$20.0

$30.0

$40.0

FY2012 FY2013 FY2014 FY2015 TTM

Mill

ion

s

$43.1

$22.5

$33.0

TTM REVENUE ($ MIL)

21

FY = Fiscal Year Ending July 31

$30.1

$40.4

TTM Revenue (Includes 1Q16 Results)

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

FY2012 FY2013 FY2014 FY2015 TTM

Mill

ion

s $4.6

$3.8

$6.6

TTM ADJUSTED EBITDA ($ MIL)

22

FY = Fiscal Year Ending July 31

$4.4

$7.3

TTM Adjusted EBITDA (Includes 1Q16 Results)

-$1.0

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

FY12 FY13 FY14 FY15 TTM

ADJ EBITDA Operating Cash Flow Free Cash Flow

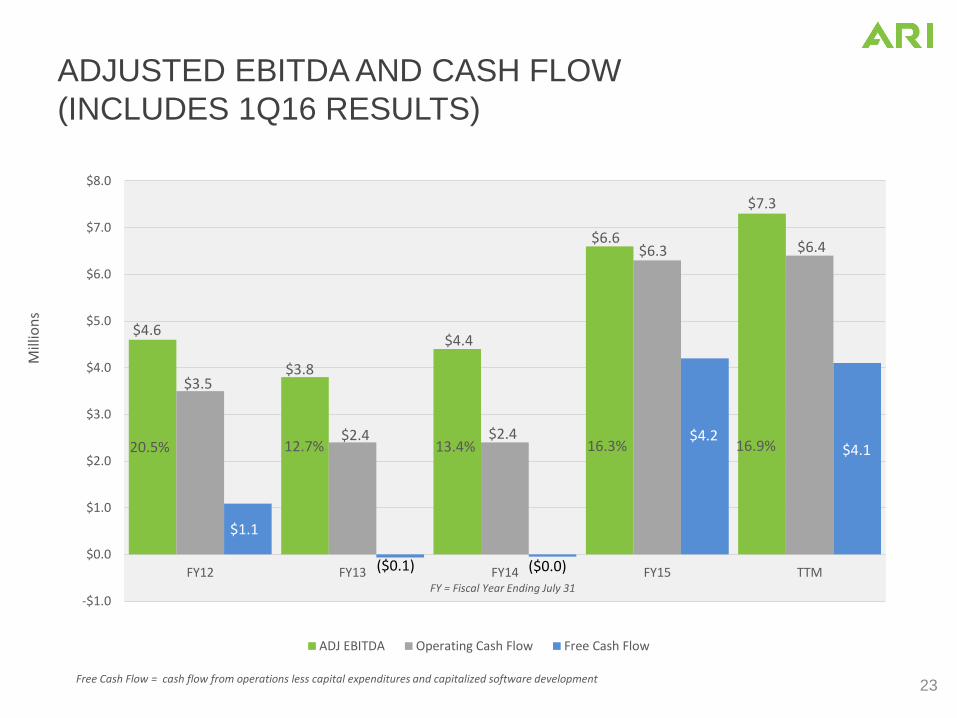

$3.8

$4.4

$6.6

$7.3

Mill

ion

s

20.5% 12.7% 13.4%

FY = Fiscal Year Ending July 31

16.3% 16.9%

$3.5

ADJUSTED EBITDA AND CASH FLOW

(INCLUDES 1Q16 RESULTS)

23

$4.6

$2.4 $2.4

$6.3 $6.4

$1.1

$4.2

($0.1) ($0.0)

$4.1

Free Cash Flow = cash flow from operations less capital expenditures and capitalized software development

STRATEGY

Roy W. Olivier – President & CEO

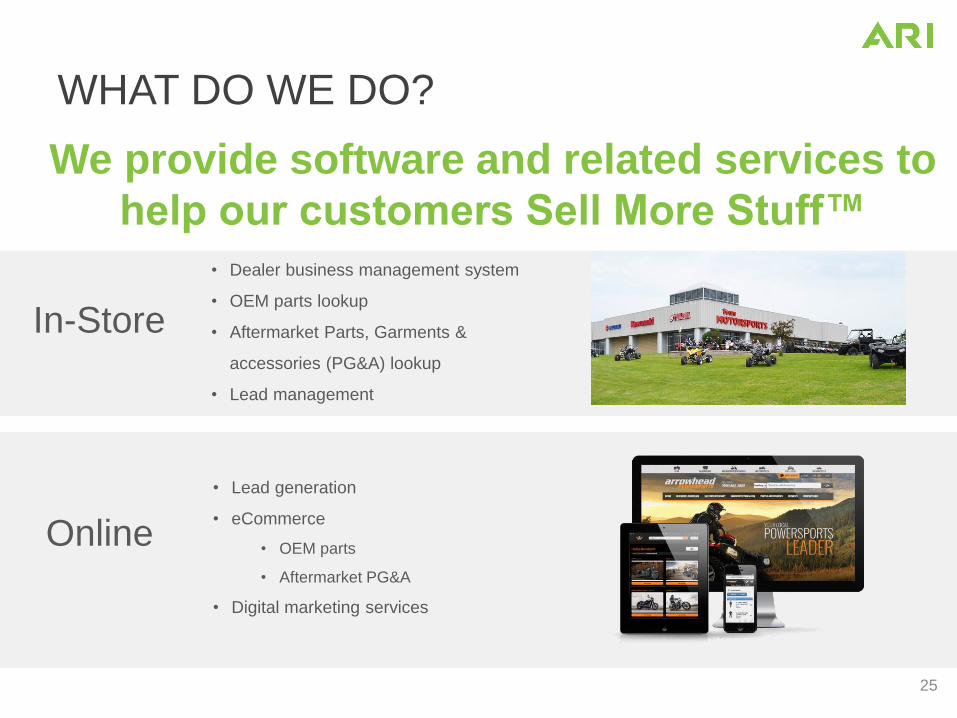

WHAT DO WE DO?

25

We provide software and related services to

help our customers Sell More Stuff™

In-Store

• Dealer business management system

• OEM parts lookup

• Aftermarket Parts, Garments &

accessories (PG&A) lookup

• Lead management

Online

• Lead generation

• eCommerce

• OEM parts

• Aftermarket PG&A

• Digital marketing services

WHO ARE OUR CUSTOMERS

26

Dealers Distributors Manufacturers (OEM)

Our Customers are:

PowersportsOutdoor Power Marine RVAppliances

CORE

Tire & Wheel HME

Markets We Serve:

GROWTH

Aftermarket

Auto Service

What “Stuff”?Whole Goods

(Tires, Bike, Boat,

RV)

OEM PartsAftermarket Parts,

Garments &

Accessories (PG&A)

Service & Tire

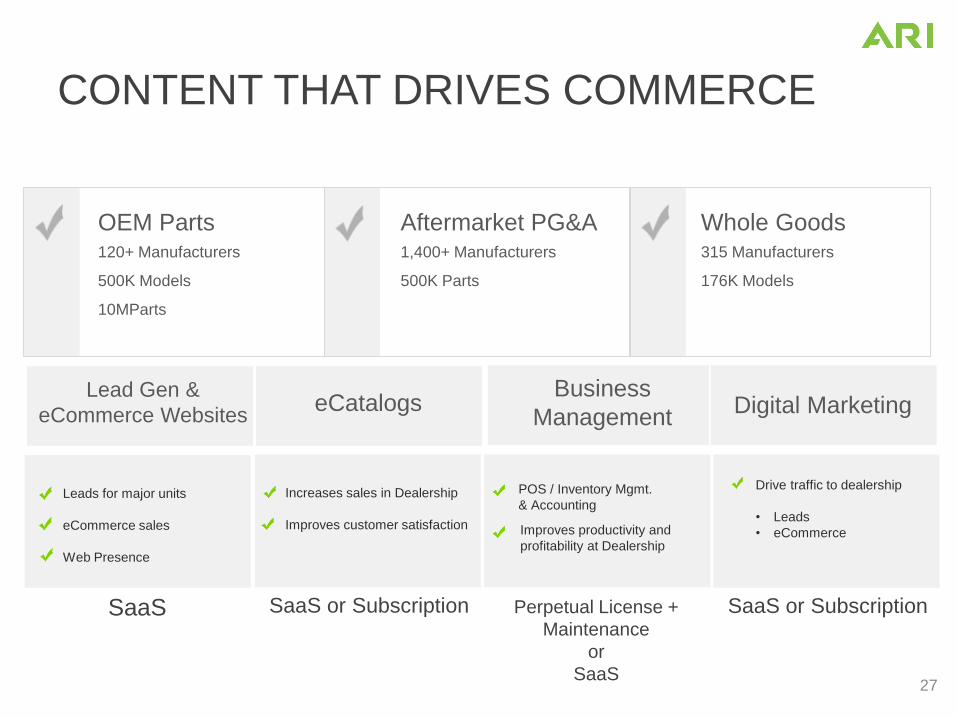

CONTENT THAT DRIVES COMMERCE

27

OEM Parts120+ Manufacturers

500K Models

10MParts

Aftermarket PG&A1,400+ Manufacturers

500K Parts

Whole Goods315 Manufacturers

176K Models

Improves productivity and

profitability at Dealership

Business

Management

POS / Inventory Mgmt.

& Accounting

Drive traffic to dealership

• Leads

• eCommerce

Digital Marketing

Leads for major units

eCommerce sales

Web Presence

Lead Gen &

eCommerce WebsiteseCatalogs

Increases sales in Dealership

Improves customer satisfaction

SaaS or SubscriptionPerpetual License +

Maintenance

or

SaaS

SaaS or SubscriptionSaaS

STRATEGIC GOALS - BACKGROUND

• To be the leader in providing software and services that help our customers Sell More Stuff™.

– Complex equipment will continue to be sold primarily through a dealer network.

– Approximately 7 out of 10 units sold originate as web leads.

– Online shopping is growing faster than in-store.

– Search is now over 50% mobile.

– ARI has a strong online footprint with supporting analytics (7,000+ Dealer Sites).

– We intend to integrate or own in-store systems (Business Management/Point of Sale).

28

STRATEGIC GOALS – THE FUTURE

• We intend to be the leader in helping dealers

capitalize on the convergence of online and in-

store purchases and research.

– Integrate customer search with the dealership’s

location via mobile

– Integrate the customer in-store experience with search

and purchasing history via mobile

– Create personalized shopping experiences based on

models owned, history, etc.

29

STRATEGIC FOUNDATIONS

• Nurture and retain existing customers through world

class customer service and product feature upgrades.

• Drive organic growth through innovative new service

offerings, differentiated content and geographic

expansion.

• Lead the market with open integration to related

platforms.

• Successfully execute acquisitions that align with our core

strategy.

30

FOUR POINT GROWTH STRATEGY

31

• More Markets

¹Total addressable market represented by the green bars . Percentages represent ARI’s market share , or the percentage of U.S. dealers that currently use 1 or more of our products. For example, ARI currently has 40% market-share of the OPE vertical; with 40% of those dealers using 1 or more of ARI’s products.²Average revenue per dealer³Home Medical Equipment

66%

40%

90%10%

25K dealers

MAR

KET

SIZE

66%

40%

90% 10%

2%

17%

0%

25K dealers 125K dealers

GROWTH DRIVERS

32

• More Markets

• More Products• eCatalog

• Lead Gen & eCommerce

• Point of Sale / Dealer

Business Mgmt. Systems (POS/DBMS)

• Digital Marketing Services (DIGMS)

GROWTH DRIVERS

33

• More Markets

• More Products

• Higher ARPD

• eCatalog $1,839

• LeadGen/eCommerce $2,936

• POS/DBMS $4,766

• DIGMS $5,065

GROWTH DRIVERS

34

• More Markets

• More Products

• Higher ARPD

• Acquisitions that align

with our core strategy

• Completed 14

• Fragmented markets with many

small competitors

• We partner with over 90 today

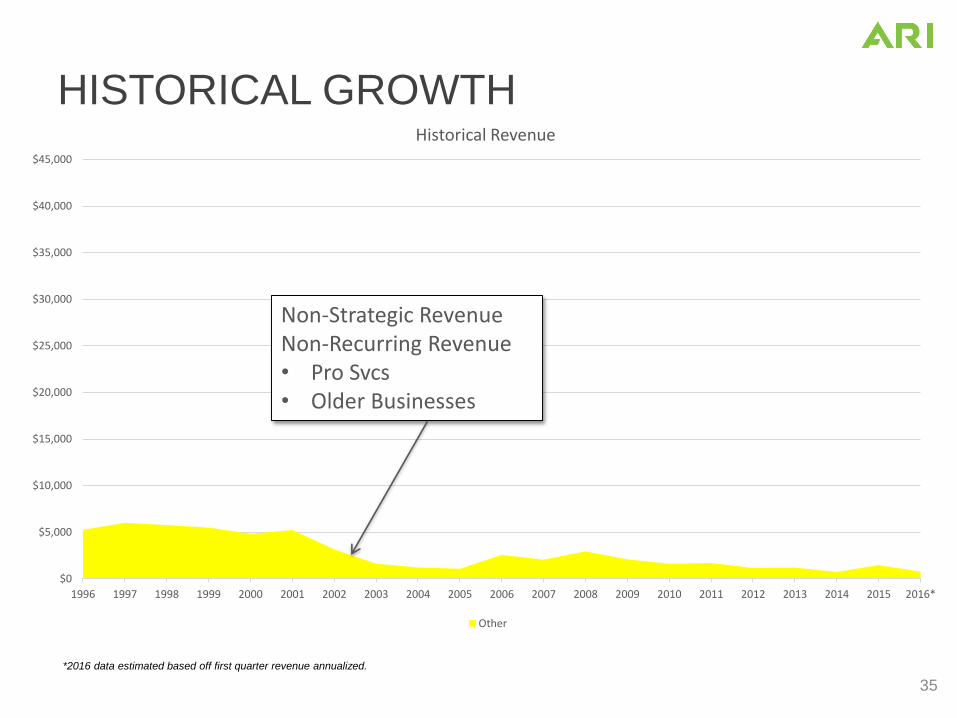

HISTORICAL GROWTH

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Historical Revenue

Other

Non-Strategic RevenueNon-Recurring Revenue• Pro Svcs• Older Businesses

*2016 data estimated based off first quarter revenue annualized.

35

HISTORICAL GROWTH

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Historical Revenue

Other eCatalog*2016 data estimated based off first quarter revenue annualized.

eCatalog• $18M Revenue• 18,000 +Dealers• 100 Countries

36

HISTORICAL GROWTH

In FY13 Q3 we made a change to our lead generation service business model, eliminating the pass-through cost of purchased ad words from the search engine providers on behalf

of our customers.

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Historical Revenue

Other eCatalog Website

Lead Gen/eCom Websites• $23M Revenue• 7,500 Websites

*2016 data estimated based off first quarter revenue annualized. 37

HISTORICAL GROWTH

In FY13 Q3 we made a change to our lead generation service business model, eliminating the pass-through cost of purchased ad words from the search engine providers on behalf

of our customers.

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Historical Revenue

Other eCatalog Website Digital Marketing

Digital Marketing Services• $1M Revenues• 225 Customers

*2016 data estimated based off first quarter revenue annualized. 38

HISTORICAL GROWTH

In FY13 Q3 we made a change to our lead generation service business model, eliminating the pass-through cost of purchased ad words from the search engine providers on behalf

of our customers.

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Historical Revenue

Other eCatalog Website Digital Marketing POS

Business Mgmt System/POS• $3M Revenues• 1,500 Locations

*2016 data estimated based off first quarter revenue annualized. 39

HISTORICAL GROWTH

In FY13 Q3 we made a change to our lead generation service business model, eliminating the pass-through cost of purchased ad words from the search engine providers on behalf

of our customers.

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

$50,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016*

Other eCatalog Website Digital Marketing POS

On track to do $47M - $49M in revenue for FY16

*2016 data estimated based off first quarter revenue annualized. 40

GROWTH OPPORTUNITY

Customer

Count

US TAM

# of

Customers

ARPD TAM Dollars

eCatalog 15,901 20,800 $1,839 $38M

Lead Gen &

eCommerce 7,557 143,800 $2,936 $422M

Point of

Sale/DBMS459 143,800 $4,762 $685M

Digital

Marketing228 143,800 $5,065 $728M

Total US $1.9B

41

After various adjustments we think TAM is $1.5B

eCat – Total includes “Bulk” license agreements without international dealers. ARPD is for dealers billed directly.

TAM – Total Addressable Market or the number of dealers, service locations or service providers.

ARPD– Average Recurring Revenue per dealer, service locations or service providers. Number for FY16Q1 annualized.

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

FY12 FY13 FY14 FY15 FY16 Low End Est.

Mill

ion

s

FY = Fiscal Year Ending July 31

Total Revenue

5 Year CAGR – 17%

3 Year CAGR – 16%

$22.5

$30.1

$47.0

$33.0

REVENUE GROWTH

42

$40.4

TARGET OPERATING MODEL

FY15 Act.FY16 Q1

Annualized

3 Years

FY19

5 Years

FY21

Sales $40M $47M ≅ $75M ≅ $100M

Growth CAGR 16.5% 16.5%

Adj. EBITDA % 16.9% 17.2% 18% - 22% 20% - 24%

Adj. EBITDA $ $7.3M $8M $14M - $17M $20M - $24M

43

NEAR TERM OUTLOOK

• In FY16 deliver $47M - $49M in Revenue– Deliver $50M revenue run rate in a quarter later in the

fiscal year

– Deliver $10M adjusted EBITDA run rate quarterly shortly thereafter

• Continue to integrate the three FY15 acquisitions

• Continued improvement in adjusted EBITDA and Cash Flow

44

QUESTIONS?

45