“k” line fact book 2008 · ④transition of alliance for containership p10 ④car production...

TRANSCRIPT

July, 2008

in English

◇◆◇◆◇◆ INDEX ◆◇◆◇◆◇

1. Management Plan and Improvement of Business Structure P1 3-5. Emerging Markets ① Economig Growth in India(Exports ・Imports) P18

1-1. "K" Line Vision 100 General View P1 (India and Vietnam) ② Economic Growth in Vietnam(Exports・Imports)

1-2. Starting New Management Plan ①"K"Line Vision 2008+ =>"K"Line Vision100 P2 3-6. Emerging Markets ① Exports & Imports of BRICs (ex. China) P19

②Trends of Business Performance (BRICs,VISTA,Turkey) ② Exports & Imports of VISTA

③Improvement in Financial Position ③ Exports & Imports of Turkey

④Fleet Upgrading Plan P3 4. Bulk Carrier Business P20

⑤Newbuildings (Results and Plan) 4-1. "K"Line Fleet ① "K"Line Dry Bulk Fleet P20

1-3. Trends of Financial Indices ①Net Income and Dividend per Share P4 ② Energy Transportation Vessel Fleet

②Consolidated ROE/ROA ③ Ship Price as of Placing Order (Dry Bulkers, Tankers)

③Consolidated Assets Turnover ④ Ship Price as of Completion (Dry Bulkers, Tankers)

④Consolidated EV/EBITDA 4-2. Business Expansion of Drybulk Business into the World P21

⑤Operating Cash Flow 4-3. Demand on Dry Bulk ① Transition of Crude Steel Production P22

⑥Consolidated Interest Coverage Ratio ② World Coal Export (Thermal/Coking Coal) P23

1-4. History of Management Plans P5 ③ World Coal Import in Total

1-5. Restructuring and Scale Expansion ①No. of Seafarers/ "K"Line Employee P6 ④ Iron Ore Import into Major Asian Countries

②Our Fleet Scale, Ordinary Revenures & Income ⑤ World Coal Consumption

1-6. Current Business Composition ①Revenues, Ordinary Income <Division-wise> P7 5. Car Carrier Business P24

②Revenues, Ordinary Income <Segment-wise> 5-1. Fleet and Cargo Movements ① "K"Line PCC Fleet P24

③Fleet Composition ② Cars/Trucks Transported by Our Fleet

2. Comparison to Major Shipping Company P8 ③ Total Cars/Trucks Exported from Japan

2-1. Fleet-scale Ranking ① Major Container Carriers P8 5-2. Demand on Vehicles ① World Automobile Production (2007) P25

② Containership Asia-N.America Loading Volume ② No. of Vehicles Possessed (Cars/1,000 People)

③ Histrical Top 20 Container Carriers P9 ③ Transition of Overseas Production by Japanese Automakers

④ Transition of Alliance for Containership P10 ④ Car Production and Sales in USA

⑤ Cape-size Bulker Owned P11 6. Container Business P26

⑥ Dry Bulkers (All Types) Owned 6-1. Fleet and Cargo Volume ① "K"Line Containership Fleet P26

⑦ PCTC Operated ② "K" Line Average Freight/Volume for All Services

⑧ PCTC Owned ③ "K"Line Volume & Share for Asia-N.America/Europe

⑨ AFRAMAX Tanker Owned ④ Volume & L/F for Asia-N.America/Europe ("K"Line/All) P27

⑩ LNG Fleet (Managed) 6-2. Container Terminal Operated by "K"Line P28

3. World Market P12 6-3. Cargo Movements ① Container Cargo Movements P29

3-1. Fleet Scale by Vessel-type/Age ① Dry Bulk Carriers by Vessel-type/Age P12 ② Asia=>N.America/Europe Country-wise Cargo Volume

② PCC Delivery by Vessel-type/Age P13 6-4. Port-wise Volume ① Port-wise Handling Volume in Asia P30

③ Oil Tanker Delivery by Vessel-type/Age ② Top 10 Ports for 2007 Container Handling

④ Containership Delivery by Vessel-type/AgeP14 ③ Transition of Container Handling among Major Ports in Asia

3-2. Trend of Newbuildings ① Ship Price as of Placing Order P15 6-5. Factory of the World ① Major Electric Device Nation-wise Production P31

② Ship Price as of Delivery ② Trends of Export from Asian Major Nations and Regions

③ World Newbuilding Orders 7. New Businesses P32

④ World Newbuilding Delivery ① Heavy Lift Shipping P32

⑤ World Total Existing Tonnage ② Offshore Support Vessels

⑥ World Total Ship Demolotion ③ Floating LNG Production

3-3. World Cargo Movements ① World Cargo Movements (Ton-mile) P16 8. Financial Data P33

② Dry Bulk Market 9. "K" Line Overview P34

③ Tanker Market 9-1. "K" Line Corporate Governance System P34④ Containership Freight for Our Trunk Lines 9-2. Safety Navigaton P35

3-4. Emerging Markets (China) ① Economic Growth Rate P17 9-3. Enviroment Preservation P36

② Trade Trends for China 9-4. Brief History P37

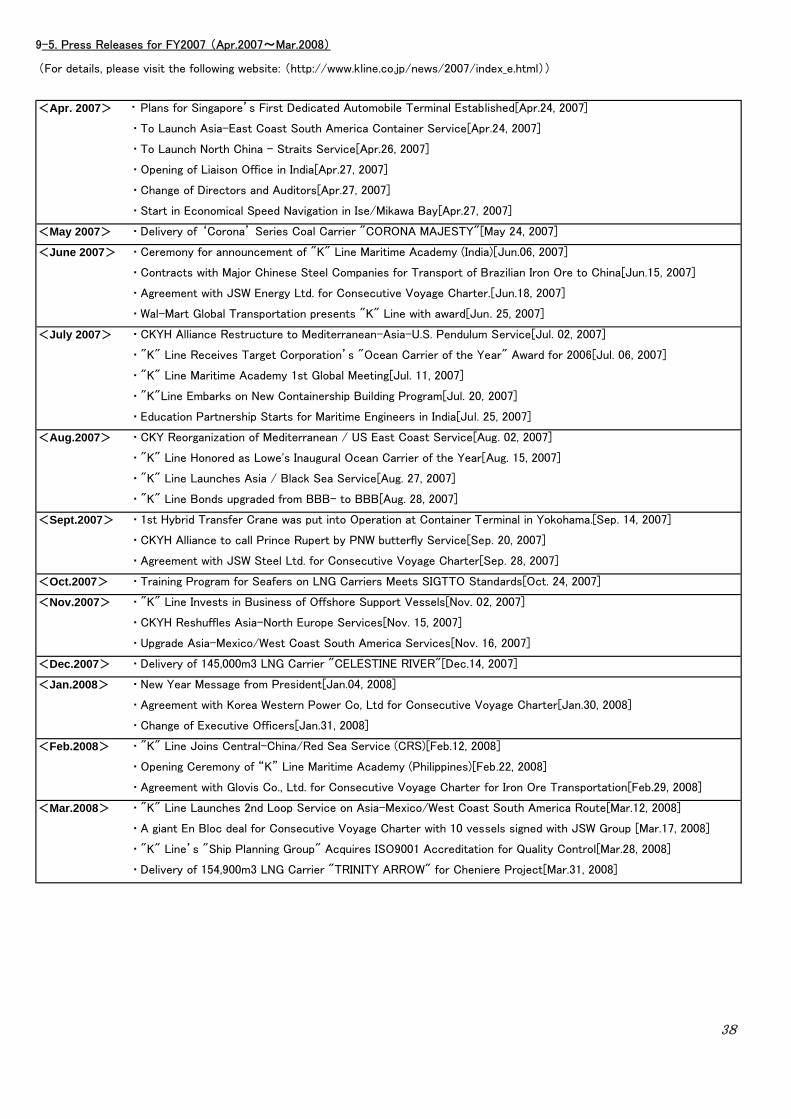

③ Energy Consumption in China 9-5. Press Releases (Apr.2007-Mar.2008) P38

④ Income Gap between Urban and Rural Area 9-6. Certification by Third-party Organization & Information on Convertible Bonds P39

⑤ Per-Capital GDP by Region in China 9-7. Corporate Principles and Charter of Conduct P40

⑥ Earning Gap between Areas

1-1. "K"Line Vision 100 General View

New Midterm Management Plan ("K" LINE Vision 100)Themes: "Synergy for All and Sustainable Growth"

Efforts Toward Synergy for All and Sustainable Growth

Consolidated financial targets (assumptions: exchange rate of 100 Yen = US$1, Dubai oil price at US$100/barrel, fuel-oil price at US$520/MT)(Unit: billion yen) (Unit: trillion yen)

FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 Mid-2010's 100th anniversary

Operating revenues 1,331 1,340 1,450 1,600 1,750Ordinary income 125.9 121 135 145 160Net income 83 78 85 95 105ROA 13% 12% 10% or higher

Shareholders' equity 355.8 426 680 or higherEquity ratio 37% 37% 40% or higherDER 93% 100% 85% or lowerInterest-bearing debt/operating CF 2.3 4.2 3.5 or lowerPayout ratio 20% 22% 25% 30%

Fleet, shipping capacity

End of FY 2007 End of FY 2011 Mid-2010's End of FY 2019

Containership 99 132Dry bulk carriers 169 225Car carriers 102 106LNG carriers 34 48Oil Tankers 28 45Heavy lift /offshore carriers 15 24Coastal/RORO carriers 52 60Total 499 640

(Approx. 1,180 billion yen)

Operaingrevenues: 2.2

Operatingrevenues: 3

Approx. 750vessels

Approx. 900vessels

Corporate Principles of the "K" Line Group:The basic principles of the "K" Line Group as a business organization centering on shipping liein:a. Diligent efforts for safety in navigation and cargo operations as well as for environmentalpreservation;b. Sincere response to customer needs by making every possible effort; andc. Contributing to the world’s economic growth and stability through continual upgrading ofservice quality.

1. Activities to promote environmental protection〇Preventing global warming〇Keeping the sea and air clean

2. Stable safety ship operation administration structure〇Enhancing safety-management systems and strengthening the land-based support structure〇Expanding our ship-management structure〇Hiring and training marine technical personnel

3. Borderless management through the best and strongest organization〇Accelerating borderless management through the spread of "K" Line Standards〇Strengthening overall abilities by bringing together Group knowledge and expertise〇Dramatic improvements in worker productivity〇A bright, vibrant workplace〇Industry-leading competitive strength

4. Strategic investment and proper allocation of management resources〇Establishing a stable profitability structure for existing businesses〇Growing new businesses into revenue-generating ones〇Advancing investment based on internal financial rules 5. Improvement of corporate value and complete risk management〇Enhancing corporate quality and maximizing returns on profits〇Identifying and responding swiftly to potential risks

Group Vision:1. To be trusted and supported by customers in all corners of the world while being able to continue to growglobally with sustainability,2. To build a business base that will be capable of responding to any and all changes in businesscircumstances, and to continually pursue and practice innovation for survival in the global market,3. To create and provide a workplace where each and every employee can have hopes and aspirations for thefuture, and can express creativity and display a challenging spirit.

Society in generalSocial contributions, a focus on the environment,

governanceBuilding relations of trust through actions as a corporate

citizen and contributions to local communities

CustomersProvision of safe logistics services

Building relations of trust through safe and reliabletransportation services

ShareholdersAppropriate returns on profits

Building relations of trust through stable andappropriate returns on profits and fair and accurate

disclosure of information

Business partnersEnhancing partnerships

Building relations of trust through fair transactions

EmployeesRewarding and satisfying work

Building relations of trust through enhancing HRdevelopment and improving both working conditions

and the working environment

ContainershipBusiness

Dry Bulk CarrierBusiness

Car CarrierBusiness

Energy Transportation and TankerBusiness,

Heavy Lift and Offshore SupportBusiness,

New Businesses

Logistics Business, Short Sea and Coastal

Shipping Business

Mobility and high-quality services

* Proposal-based sales that anticipatecustomer needs

* Tailor-made customer-specific services

World-leading transportation qualityand full route network

* High-quality services taking theenvironment and safety into consideration

* Global business expansion respondingswiftly to customer needs

Top class worldwide with safetransportation

* Aggressive efforts to take on newshipping demand

* Pursuing safe and high-quality services

Top class worldwide with cape-size andpost-panamax vessels

* High-quality services suited to diversecustomer needs

* Growing the customer base throughglobal business expansion

* Enhancing a stable profitability structurethrough mid- to long-term contracts

Synergy for All: Mutually beneficial relations

BusinessStrategies

Fleet upgrading plan (FY 2008 - FY 2011) 43 65 27 15 13 13 4

180

Sustainable business growth andefficient business management

* Responding to globalization ofcustomers' businesses throughenhancements to the service network* Enhancing competitive strengthsthrough sustained fleet and terminalimprovements* Pursuing safe transportation with a focuson protecting the environment

11

1-2. Starting New Management Plan "K"Line Vision 100, After "K"Line Vision 2008 +

① From "K"Line Vision 2008+ to "K"Line Vision100 Unit: Billion Yen

FY2006(Plan)

FY2006(Results)

FY2007(Plan)

FY2007(Results)

FY2008(Plan)

Performance

Operating Revenues 970.0 1,085.5 1,050.0 1,331.0 1,100.0 ◎

Ordinary Income 75.0 63.9 90.0 125.9 110.0 ◎

Net Income 53.0 51.5 60.0 83.0 70.0 ◎

ROE 19% 17% 19% 24% 19% ◎

Shareholders' Equity 293.0 344.5 342.0 355.8 400.0 ○

Equity Ratio 35% 38% 37% 37% 39% ○

DER 109% 95% 99% 93% 88% ○

Interest-bearing Debt 320.0 326.2 304.0 329.7 350.0 ◎

Payout Ratio ◎

(Original Assumption: Exchange rate-JPY110/US$, Fuel Oil Price-US$300/MT)

"K" LINE Vision 100 Financial Targets Unit: Billion Yen

FY2007 FY2008 FY2009 FY2010 FY2011Results Plan Plan Plan

Operating Revenues 1,331.0 1,340.0 1,450.0 1,600.0 Operating RevenuesOrdinary Income 125.9 121.0 135.0 145.0 160.0Net Income 83.0 78.0 85.0 95.0 105.0 (Unit: Trillion Yen)ROA 13% 12% over 10%Shareholders' Equity 355.8 426.0 over 680.0Equity Ratio 37% 37% over 40%DER 93% 100% under 85%

2.3 4.2 under 3.5 Payout RatioPayout Ratio 20% 22% 25%

(Assumption of the Plan: Exchange Rate (Yen/US$) 100yen/$, Bunker Oil Price US$520/MT)

(Fiscal Year) '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08-'11 Average Exchange Rate (Yen/US$) 125 108 99 96 113 123 128 112 110 125 122 114 107 113 117 115 100 Average Fuel Price (US$/MT) 99 83 99 108 118 104 76 117 158 134 161 170 192 286 319 407 520

30%

Interest-bearingDebt/Operating CF

20% on consolidated basis

Plan1,750.0

2.2 3.0

100thAnniversaryMid-2010s

2

② Trends of Business Performance (P/L)

-100

300

700

1,100

1,500

1,900

2,300

2,700

3,100

92F93F94F95F96F97F98F99F00F01F02F03F04F05F06F07F08Fe09Fe10Fe11Fe mid-10s

2019F

(Billion Yen)

-10

10

30

50

70

90

110

130

150

170

190

210

(Billion Yen)Operating RevenuesOperating IncomeOrdinary IncomeNet Income

Target 10

K.R Plan

K.R.Phase2Ⅱ

New K-21KV-Plan

"K" Line Vision 2008

"K" Line Vision 2008+

"K" LINE Vision 100

◎ achieved beforehand○ achieved as planned

③ Improvement in Financial Position

0

100

200

300

400

500

600

700

800

92F

93F

94F

95F

96F

97F

98F

99F

00F

01F

02F

03F

04F

05F

06F

07F08

Fe09

Fe10

Fe11

Fe

Equity Ratio Indicated x10(%)↓(Billion Yen)

0%

100%

200%

300%

400%

500%

600%

700%

Interest Bearing Dept Shareholders' Equity Equity Ratio(x10) DER

※We began to record a part of lease obligation in B/S from 1995 because of changes in the accounting system.

Over 680.0 Bln Yen

over40%

under85%

(Year 2019)

④ 【Fleet Upgrading Plan】Toward a Fleet Scale about 900 Vessels in '19F: Investing Approx. 1.18 Trillion Yen on 180 Ships in '08-'11F ⑤ Newbuildings (Results and Plan)

(As of April 2008)

'08F '09F '10F '11F 4-yeartotal

2004FResults

2005FResults

2006FResults

2007FResults

2008FPlan

2009FPlan

Containership 99 4 15 15 9 43 132 Containership 5 5 6 4 4 15Dry Bulker 169 13 16 16 20 65 225 1,700TEU 0 0 3 2 4

PCTC 102 4 10 8 5 27 106 2,400TEU 0 0 0 1 2LNG 34 14 1 0 0 15 48 3,500TEU 3 0 0 0 4

Tanker 28 4 5 0 4 13 45 4,500TEU 2 3 0 0 1Heavy Lifter 15 3 1 3 0 7 18 6,400TEU 0 0 0 0 1

Offshore 0 0 0 3 3 6 6 8,000TEU 0 3 1 1 3Others 52 2 0 1 1 4 60 Dry Bulker 5 19 22 10 13 16Total 499 44 48 46 42 180 640 Capesize 3 8 9 2 4 7

Panamax 2 3 4 4 0 5Handymax 5 4 2 2 0SmallHandy 1 2 1 3 2Chip/Pulp 0 1 0 3 0Corona 2 2 1 1 2

PCTC 3 8 8 4 5 92,000 unit 2 2 0 0 13,800 unit 0 2 1 0 14,000 unit 1 2 0 0 25,000 unit 3 1 0 0 36,000 unit 2 1 4 4 3

LNG 2 4 2 2 14 1

Tanker 3 1 4 3 4 5VLCC 0 1 1 0 4AFRAMAX 1 1 0 2 0LRⅡ 0 2 0 1 1LPG 0 0 2 1 0

Heavy Lifter 0 0 0 1 3 1Others 0 1 5 2 2 0Total 18 38 47 27 44 48

Fleet ofApprox.7

50Vessels

Fleet ofApprox.

900 Vessels

End-'19F(100th

Anniversary)

As ofMar.'08

New Buildings As ofMar.'12

Mid-'10s

No. of Vessels at the End of 2011F (Planned)

(Total 640 Vessels)

Offshore, 6

Others, 60Containers

hip, 132

Dry Bulker,225

HeavyLifter, 18

Tanker, 45

LNG, 48PCTC, 106

No. of Vessels at the End of 2007F(Total 499 Vessels)

Others, 52Containership, 99

DryBulker,

169

PCTC,102

LNG, 34

Tanker, 28

HeavyLifter, 15

3

180 Newbuildings

1-3. Trends of Financial Indices in Recent Years

4

① Net Income and Dividend per Share

0 0 0 0 0

3 3 4 5 35

1016.5 18 18

26

△ 10

0

10

20

30

40

50

60

70

80

90

92F 93F 94F 95F 96F 97F 98F 99F 00F 01F 02F 03F 04F 05F 06F 07F

Unit: Billion Yen

-20

0

20

40

60

80

100

120

140Yen/Share

Net Income Net Income per Share Dividend per Share

② Consolidated ROE, ROA

△ 10

0

10

20

30

40

50

60

70

80

90

92F 93F 94F 95F 96F 97F 98F 99F 00F 01F 02F 03F 04F 05F 06F 07F -10%

0%

10%

20%

30%

40%

50%

Net Income ROE ROA

Unit: Billion Yen

③ Consolidated Assets Turnover

0

200

400

600

800

1,000

1,200

1,400

92F 93F 94F 95F 96F 97F 98F 99F 00F 01F 02F 03F 04F 05F 06F 07F

Unit: Billiion Yen

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

Operating Revenues Assets Turnover

④ Consolidated EV, EBITDA

0

20

40

60

80

100

120

140

160

180

92F 93F 94F 95F 96F 97F 98F 99F 00F 01F 02F 03F 04F 05F 06F 07F

Unit: Billion Yen

0

2

4

6

8

10

12

14

EBITDA EV/EBITDA

⑤ Operanig Cash Flow

△ 10

10

30

50

70

90

110

130

150

92F 93F 94F 95F 96F 97F 98F 99F 00F 01F 02F 03F 04F 05F 06F 07F

Unit: Billion Yen

Net Income Operating Cash Flow

⑥ Consolidated Interest Coverage Ratio

0

20

40

60

80

100

120

140

92F 93F 94F 95F 96F 97F 98F 99F 00F 01F 02F 03F 04F 05F 06F 07F

Unit: Billion Yen

0

5

10

15

20

25

30

Operating Income

Interest Coverage Ratio

1-4. History of Management Plans

Plan name Subjects RemarksNov.1982 Emergency Plan for Strengthening 1st theme: profitability improvement plan Radical improvement in operational structure was targetted,

- the Corporate Foundation 2nd theme: efforts to modernize and increase the efficiency of operational systems feared continued simultaneous slump in three salesAug.1983 ("K" Plan) First Stage 3rd theme: a cost-cutting campaign carried out with the participation of all personnel division and yen rising.

Emergency Plan for Strengthening Reconstruction of system to implement "K"plan, mainly for above 2nd theme (Reference-in June 1983, the Head Office was- the Corporate Foundation Promotion of office automation、Improvement in business procedure, Cost reduction etc relocated to current location )

Mar.1984 ("K" Plan) Second StageApr.1984 Intermediate-term Operational 1) Emergency Measures (disposal of uneconomical ships, establishment land-based and marine personnel plan.) Aimed to establish the capability to resume dividend payment.

Improvement Plan 2) Reinforcement of operational capabilities (development of an internationally competitive fleet, (A part of this plan was named Enhancement of cost control, Promotion of new business) (However, Plaza Accord in 1985 drastically rose yen

- New "K" Plan.) 3) Augmentaton of financial measures to 150 yen per one U.S. dollar, and the U.S. Shipping Act4) Modernization and increasing the efficiency of operational organization (streamlining of land-based of 1984 made container freight fall significantly. operations, reorganization and utilization of an information systems) Our losses were expanded.)

Mar.1987 5)Promotion of safe vessel navigation and cost reduction Apr.1987 Emergency Ratiolization Plan 1) Disposal of uneconomical ships

2) Make the organization more efficient and streamlined. (inc. spinning off our subsidiaries)3) Slashing of both of land and sea workforth with intoroduction of a special retirement policy. Almost all targets completed on schedule.

- <"Emergenvy Employment Measures"(agreed with All Japan Seamen's Union)4) Improvement and reinforcement of operational capabilities =>Once Operating Income moved into the black F88.5) Measures against stronger yen

Mar.1989 6) Implemantation of measures for cost reduction.While we did not have specific management plan during this period, there was a campaign for imporoving customer satisfaction (named 'One for All, All for One', April 1990 - March 1994), and"Project 20・20", an internal campaign in Containership division around 1991 (targeting at total USD 40 min. profit rise through revenue up by 20 mil. and cost down by 20 mil.) , etc.

Dec.1992 Target-10 - Reexamining costs and expenses from every angle '- Around Oct.1993Oct.1993 "K"Line Reengineering Program - Strenghtening international competitiveness through cost-saving and shift as many jobs as possible to overseas

- (K.R. Program) - Establishment of structrure to respond customers' needs and to ensure stable profit even if faced with Mar.1996 exchangerate rate 100 yen per one U.S. dollar,. Apr.1996 K.R.PhaseⅡ - Realization of the situation to implement continual payment of dividends Unfinished targets in K.R. Program. From non-consolidation

- - Reconstruction of operation on a consolidated basis by the entire "K"Line group to consolidation. Aiming for competetiveness matching shipping companies in developing Asia.

Mar.1998 =>In F97 dividend paid after 15 year absenseApr.1998 New"K"Line Spirit for 21(New K-21) - Standing firm in our basic policy of pursuit of profitability while trying to expand scale of business, and Aiming to make containership division move into the black,

*In '00, raised the numerical targets continuing stable payment of dividends which was not achieved in K.R.PhaseII. - *Completed a year ahead of - To expand shipping-based logistics business globally with customer-oriented attitude, and to aim at a corporate group Positive management plan for the first time in many years.

Mar.2002 schedule as most targets achieved which is soild, and fully commited to challenge with courage. =>Most targets achieved, though 9.11changed conditions at all.Apr.2002 KV-Plan 1. Further enhancing of Company’s overall organization through cost reductions and profitable use of IT, etc. Reconstruction of containership business-"Cost Slash 300"

2. Reinforcement of globalization firmly based on regional communities and pursuit of business synergy among business sectors. (Total 30 bln. yen cost reduction plan:- 3. Initiate stronger efforts to implement logistics business. 15 bln. is from deployment of larger ships)

4. Persuit of technical innovations in marine transport, perfection of safety in navigation and cargo operations, In F03 (ends Mar. '04) most of final targets inc. numerical*Completed a year ahead of and further contribution to environmental preservation. ones were atatined a year ahead of schedule.

Mar.2004 schedule as most targets achieved 5. Strengthening of corporate governance aiming at more transparency and greater effectiveness in management. =>"K"Line Vision 2008Apr.2004 "K"LINE Vision 2008 1.Ensuring a stable profitability structure through reinforcing our business base Set a vision for F08, to regard the period from now to F09, our

- -Sustainable Growth and Establish- 2.Creation of a high-level, refined and more matured culture of the "K" Line Group with materialization of dreams 90th anniversary, as a runway.ment of a Stable Profitability Structure and upgrading of the "K" Line Brand As profit targets, set F04, 05 estimation & F08 vision

Mar.2006 (Completed as most targets achieved) 3.Reinforcement of corporate governance and response to risk management Fulfilled most final numerical goals in F05/fuel price hike=>2008+

Apr.2006 "K"LINE Vision 2008+ -Measures to support systematic expansion of business scale (new target) NOT achieved F06 targets due to container freight drop- -Sustainable Growth and Establish- - Response to changes in business enviroments (new target) F07 resuts exceeded most targets for F08 in the plan due to dry

ment of a Stable Profitability Structure- bulk market hike and containership freigt restoration, Mar.2008 (Completed as most targets achieved) & condition change => "K"Line Vision 100Apr.2008 "K"Line Vision 100 1. Activities to promote environmental protection

- Themes: Synergy for All 2. Stable safety ship operation administration structure The plan based on what we will be like in 2019Mar.2012 and Sustainable Growth 3. Borderless management through the best and strongest organization when we celebrate our 100th anniversary.

+ 4. Strategic investment and proper allocation of management resources Detailed targets are set for 4years fom 2008F to 2011FImage for 2019 5. Improvement of corporate value and complete risk management

5

1-5. Effort for Structural Reform and Business Scale Expansion

② Our Fleet-Scale, Operating Revenues, Ordinary Income

-100

100

300

500

700

900

1,100

1,300

65/3 67/3 69/3 71/3 73/3 75/3 77/3 79/3 81/3 83/3 85/3 87/3 89/3 91/3

93/3

95/3

97/3 99/3 01/3 03/3 05/3 07/3

(Operating Revenues (Bln. Yen)/Operating Fleet (No. of Vessels, 100,000 Tons)) (Ordinary Income(Bln. Yen))

-10

10

30

50

70

90

110

130(Non-Consol) Operating Revenues (Consol) Operating Revenues (Non-Consol) Ordinary Income

(Consol) Ordinary Income (Non-Consol) Operating Fleet (Tons) (Non-Consol) No. of Operating Vessels

(Consol) No. of Operating Vessels (Consol) Operating Fleet (Tons)

① No. of Japanese Seafarer/"K"Line Employee

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

65/3 67/3 69/3 71/3 73/3 75/3 77/3 79/3 81/3 83/3 85/3 87/3 89/3 91/3

93/3

95/3

97/3 99/3 01/3 03/3 05/3 07/3

(No. of Consolidated Group Employee, Non-Consolidated Employee)

0

100

200

300

400

500

600

700

800

(Japanese Seafarer (Hundred)/Exchange Rate)

Consolidated Group Employee (Non-Consolidated) Employee on Sea 平均為替レ-ト 海運業収益計 (Non-Consolidated) Employee on Land 経常利益平均燃料油価格 Japanese Seafarer for Overseas Shipping Exchange Rate (\/$)

6

1-6. Current Business Composition

① Operating Revenues, Ordinary Income <Division-wise> ② "K"Line's Operating Revenues/Ordinary Income

(Unit: Billion Yen)

Business Division FY2005 FY2006 FY2007Operating Revenues 451.4 503.5 599.8Ordinary Income 30.5 -7.8 4.7Operating Revenues 468.4 615.8Ordinary Income 66.0 115.3Operating Revenues 289.4 113.6 115.4Ordinary Income 58.1 5.7 5.9Operating Revenues 740.8 1,085.5 1,331.0Ordinary Income 88.6 63.9 125.9

ContainershipBusiness

Other MarineBusiness

Others

Total

Segment-wiseOrdinary Income

Logistics,HarborTransportationBusines

ShippingBusiness,45.136

Others,2.494

Segment-wise Operating Revenues

Logistics,Harbor

Transportation

Business, 127.107

Others,21.488

ShippingBusiness, 936.943

Segment-wise Ordinary Income

Logistics,HarborTransportationBusiness,16.5

ShippingBusiness, 107.6

Others,1.7

Segment-wiseOperating Revenues

ShippingBusiness,

1176.9

Others,22.8

Logistics,Harbor

Transportation

Business,131.3

Division-wiseOperating Revenues

ContainershipBusine

ss,503.45

Others,582.09

7

③ Fleet Composition

Consolidated Ordinary Income 63.9 Bln. Yen

FY2006 Consolidated Operating Revenues: 1,085.5 Bln.

FY2007 Consolidated Operating Revenues: 1,331.0 Bln. Yen

Consolidated Ordinary Income 125.9 Bln. YenDivision-wise

Operating Revenues

Others,731.2

ContainershipBusine

ss,599.8

Division-wiseOrdinary Income

Containership

Business, -7.8

Others,71.8

Other MarineBusiness

Containership

※ Long-term chartered ships are included above fleet

※ For FY2005, we disclosed our total results in two categories: Containership Business and Others

Container 89 Container 99

Bulk Carrier 159 Bulk Carrier 169

PCTC 100PCTC 102

Energy Resource54

Energy Resource62

Heavy Lifter/Coastal/Ferry/Other 51

Heavy Lifter/Coastal/Ferry/Other 67

0

100

200

300

400

500

600

March 2007 March 2008

Total 453 VesselsTotal 499 Vessels

Division-wiseOrdinary Income

Others,121.2

Containership

Business, 4.7

ContainershipBusiness for FY06△7.8 Bln. Yen

2. Comparison to Major Shipping Companies <2-1. Fleet-scale Ranking>

① Major Container Carriers

Top 18 Container Carriers Ranked by Operating Capacity

1 Maersk 1,881,619 456,763 2,338,3822 MSC 1,214,486 619,010 1,833,4963 CMA CGM 891,803 592,747 1,484,5504 EMC 619,462 16,642 636,104 1 Maersk 1,404,8495 HAPAG 494,516 143,235 637,751 2 Evergreen 1,170,7086 CSCL 431,550 219,716 651,266 3 Hanjin 1,131,6847 Cosco 430,472 382,044 812,516 4 APL(NOL) 936,5668 APL 401,625 266,370 667,995 5 CSCL 858,5199 NYK 375,925 255,257 631,182 6 COSCO 806,48810 OOCL 341,583 143,366 484,949 7 YML 767,46411 HANJIN 339,681 283,254 622,935 8 ”K" LINE 754,45612 MOL 333,857 222,927 556,784 9 OOCL 702,42513 K Line 306,486 171,960 478,446 10 Hyndai M.M. 676,40914 Zim 274,828 188,423 463,251 11 NYK 663,40115 Hamburg Süd 273,959 187,235 461,194 12 CSAV 650,39316 YML 272,813 166,508 439,321 13 MSC 598,36217 CSAV 248,987 166,412 415,399 14 MOL 481,29118 HMM 196,782 208,468 405,250 15 Hapag-Lloyd 390,236

Rank Alliance Operating On Order Total Rank Alliance Cargo1 Maersk 1,881,619 456,763 2,338,382 1 CKYH (inc."K"line 3,460,0922 CKYH 1,349,452 1,003,766 2,353,218 2 TNW 2,094,2663 GA 1,294,912 541,858 1,836,770 3 GA (ex.MISC) 1,756,0624 MSC 1,214,486 619,010 1,833,496 4 Maersk 1,404,8495 TNWA 932,264 697,765 1,630,029 5 Evergreen 1,170,7086 CMA 891,803 592,747 1,484,5507 EMC 619,462 16,642 636,104 Source: Piers, as of 2007

Source : AXS Liner (http://www1.axsmarine.com),

CargoLoadedRank Operator

TotalOperatorRankOperating

Fleet'08-'11

Delivery

8

0 500 1000 1500 2000 2500

MaerskMSC

CMA CGMEMC

Hapag-LloydCSCLCosco

APLNYK

OOCLHANJIN

MOLK LINE

ZimHamburg Süd

Yang MingCSAV Group

HMM

1,000 (TEU)

Existing '08 Delivery

'09 Delivery '10 Delivery

'11 Delivery

0 200 400 600 800 1000

MaerskCKYH

GAMSC

TNWACMAEMC

1,000 TEU

Alliance-wise '08-'11Newbuilding Delivery

'08 Delivery

'09 Delivery

'10 Delivery

'11 Delivery

② Containership Asia-N.America Loading Volume Top15 Carriers (Year 2007)

0 300 600 900 1200 1500

Hapag-Lloyd

MOL

MSC

CSAV

NYK

Hyndai M.M.

OOCL

K Line

Yang Ming

COSCO

CSCL

APL(NOL)

Hanjin

Evergreen

Maersk

1,000TEU

2-1. Fleet-scale Ranking

③ Historical Top 20 Container Carriers Ranked by Operating Full Containership Capacity (From 1983, biyearly)

Rank '83 '85 '87 '89 '91 '93 '95 '97 '99 '01 '03 '05 '071 HAPAG EVERGREEN EVERGREEN EVERGREEN EVERGREEN MAERSK MAERSK MAERSK MAERSK/SL MAERSK MAERSK MAERSK MAERSK2 SEA-LAND USL MAERSK MAERSK MAERSK EVERGREEN SEA-LAND SEA-LAND EVERGREEN P&ON MSC MSC MSC3 MAERSK MAERSK NYK SEA-LAND SEA-LAND SEA-LAND EVERGREEN P&ON P&ON EVERGREEN P&O/FARREL EVERGREEN CMA CGM4 OCL SEA-LAND APL APL NYK NYK COSCO EVERGREEN HANJIN/SEN HANJIN EVERGREEN CMA CGM/ANL EVERGREEN5 NYK HAPAG YANGMING NYK COSCO COSCO NYK COSCO MSC MSC HANJIN/SEN HAPAG HAPAG6 OOCL OCL SEA-LAND COSCO APL P&OCL P&OCL HANJIN COSCO APL(NOL) COSCO HANJIN/SEN CHINA SHIPPING7 APL NYK HAPAG OOCL MOL HANJIN NEDLLOYD NOL/APL NOL(APL) COSCO APL COSCO COSCO8 NEDLLOYD OOCL OOCL HAPAG OOCL "K"LINE HANJIN MSC NYK/TSK CP SHIPS CMA CGM/ANL CHINA SHIPPING NYK9 EVERGREEN "K"LINE P&OCL "K"LINE HAPAG NEDLLOYD MOL NYK CMA/CGM NYK "K"LINE APL APL

10 UASC APL "K"LINE YANGMING HANJIN HAPAG APL HMM CP CMA CGM NYK NYK HANJIN11 MOL MOL MOL HANJIN "K"LINE APL HAPAG MOL ZIM MOL CP SHIPS MOL OOCL12 USL COSCO COSCO MOL YANGMING YANGMING DSR-SENATOR ZIM MOL OOCL MOL OOCL "K"LINE13 YANGMING NEDLLOYD NEDLLOYD P&OCL P&OCL MOL "K"LINE YMTC "K"LINE "K"LINE ZIM CSAV MOL14 CGM UASC ZIM NEDLLOYD NOL NOL OOCL OOCL HMM ZIM OOCL "K"LINE ZIM15 ZIM CGM HANJIN ZIM ZIM OOCL YANGMING "K"LINE OOCL HL HAPAG ZIM YANGMING16 "K"LINE ZIM CGM NOL SCANDUTCH ZIM NOL HL YMTC HMM YANGMING YANGMING CSAV17 BALTIC YANGMING UASC CGM UASC HYUNDAI HMM DSR-SENATOR HL UASC CHINA SHIPPING HAMBURG SUD HAMBURG SUD18 W.WILHELMSEN W.WILHELMSEN NOL UASC NEDLLOYD UASC ZIM CMA UASC YANGMING HMM HMM HMM19 NOL BALTIC BSC W.WILHELMSEN CHO YANG CGM CMA WAN HAI CSAV CHINA SHIPPING HAMBURG SUD PIL PIL20 COSCO NOL W.WILHELMSEN BSC CGM CHO YANG MSC CONTSIP CHO YANG HAMBURG SUD CSAV WAN HAI LINES WAN HAI LINES

(Area-wise No. of Companies)U.S.A 3 3 2 2 2 2 2 1 0 0 0 0 0Europe 7 7 7 7 6 5 7 6 5 6 6 5 5Japan 3 3 3 3 3 3 3 3 3 3 3 3 3Asia* 5 5 6 6 7 8 7 9 8 8 8 10 10Others 2 2 2 2 2 2 1 1 4 3 2 2 2

'84 US Shipping Act 1984 '86US Line busted '88 Showa Line withdrew '91 NYK acquirNLS*** '92 HYUNDAI ranked in '96 'CKYH' alliance formed '99 MAERSK acquired '00 China Shipping ranked in '04 MAERSK acquired P&ON*Excluding Japan '85 Plaza Accord '86 HANJIN ranked in '88 NLS established (Japanese 4=>3) '96 P&O and Nedlloyd merged SEALAND '05 HAPAG acquired CP SHIPS

'86 'Emergency Employment (Japanese 6=>4) '97 NOL acquired APL (Americans went away) Measure' ’88 Kaizoshin** Asia-N.America '97 HANJIN acquired majority

route WG's report issued of DSR-SENATOR

1. Top 20 as of '83: U.S.A.: 3, Europe: 7, Japan: 3 , Asia (other than Japan) : 5, Others 2 5. Time-series Major Events '07: Europe: 5, Japan: 3, Asia (other than Japan): 10, Others: 2; U.S. carriers went away, and Asian shipping companies increased '84 U.S. Shipping Act 1984 effective

'85 Plaza Accord2. The No. of European operators reduced, but through M&As after '95, business scale of each was enlarged. In '07, 4 of top 5 were Europeans. '86 US Line busted. (No. of American carriers : 3=>2)

'Emergency Employment Measure' introduced3. Because of Europeans' decrease, Asian companies specialized in containership business (like PIL, WAN HAI.) came into top 20 recently. '88 Kaizoshin** Asia-N.America route Working Group's report issued

Showa Line withdrew, and NLS*** established4. No. of Japanese Containership Operators: (No. of Japanese carriers: 6=>4)

until '87 6 (Existing 3 + Yamashita Shinnihon Steamship Co. Ltd, Japan Line Ltd., Showa Line Ltd.) '91 NYK acquired NLS*** (No. of Japanese carriers: 4=>3)'88 4 ('Showa Line' withdrew, NLS***(Nippon Liner System Co., Ltd.) formed.) '96 P&O and NEDLLOYD merged. 'P&O NEDLLOYD' (P&ON) formed.'91 3 (NYK acquired NLS) '97 NOL acquired APL (No. of American carriers : 2=>1)

'99 MEARSK acquired SEALAND (American carriers disappeared)'04 MAERSK acquired P&ON

*** Joint Venture for containership business spun out of 'Yamashita Shinnihon' and 'Japan Line'. ** Council for Rationalization of Shipping and Shipbuilding Industries ***Joint Venture for containership business spun out of 'Yamashita Shinnihon' and 'Japan Line'.

Data: Containerisation International Yearbook

9

2-1. Fleet-scale Ranking

④ Transition of Alliances for Containership Business

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Maersk Maersk Maersk Maersk-SL Maersk-SL Maersk-SL Maersk-SL Maersk-SL Maersk-SL Maersk(P&ONL) Maersk MaerskSea-Land Sea-Land Sea-Land

NYK NYK NYK NYK NYK NYK NYK NYK NYKNYK NYK NYK Hapag-Lloyd Hapag-Lloyd Hapag-Lloyd Hapag-Lloyd Hapag-Lloyd Hapag-Lloyd Hapag-Lloyd(CP ShipHapag-Lloyd Hapag-LloydHapag-Lloyd Hapag-Lloyd Hapag-Lloyd P&ONL P&ONL P&ONL P&ONL P&ONL P&ONL OOCL OOCL OOCLNOL NOL P&ONL OOCL OOCL OOCL OOCL OOCL OOCL MISC MISC MISCP&O P&ONL OOCL MISC MISC MISC MISC MISC MISC Grand Alliance

MISCCP Ships(Cast) CP Ships(Lykes,Contship) CP Ships CP Ships (TMM,OCA CP Ships CP Ships (Italia LinCP Ships CP Ships

CP Ships(Ivaran, ANZ) The New World AllianceMOL MOL MOL MOL MOL MOL MOL MOL MOL MOL MOLAPL APL MOL APL(NOL) APL(NOL) APL(NOL) APL(NOL) APL(NOL) APL(NOL) APL(NOL) APL(NOL) APL(NOL)OOCL OOCL APL(NOL) HMM HMM HMM HMM HMM HMM HMM HMM HMMNedlloyd (P&ONL) HMMMISC MISC COSCO COSCO COSCO COSCO COSCO COSCO COSCO COSCO COSCO CKYH

COSCO K-Line K-Line K-Line K-Line K-Line K-Line K-Line K-Line K-LineK-Line COSCO K-Line Yangming Yangming Yangming Yangming Yangming Yangming Yangming Yangming YangmingYangming K-Line Yangming Hanjin-Senator Hanjin-Senator Hanjin-Senator Hanjin-Senator Hanjin-Senator Hanjin-Senator

Yangming CSAV CSAV(Norasia) CSAV(Norasia)COSCO CSAV CSAV(Norasia) CSAV(Norasia) CSAV(Norasia) CSAV(Norasia) CSAV(Norasia) CSAV(Norasia)

CSAV NorasiaCSAV Norasia CMA-CGM CMA-CGM CMA-CGM CMA-CGM CMA-CGM CMA-CGM CMA-CGM CMA-CGM CMA-CGM

HMM CMAHMMMSC Norasia Choyang Choyang Hanjin-SenatorNorasia MSC Choyang Hanjin-Senator Hanjin-Senator UASC UASC UASC UASC UASC UASC UASC

Hanjin-Senator UASC UASCDSR-Senator DSR-Senator UASC Evergreen/LT Evergreen/LT Evergreen/LT Evergreen/LT Evergreen/LT Evergreen/IM Evergreen/IMChoyang Choyang Evergreen/LT Evergreen/LTHanjin Hanjin Evergreen MSC MSC MSC MSC MSC MSC MSC

UASC LT MSC MSCUASC CSG CSG CSG CSG CSG CSG CSG

Evergreen MSC CSGEvergreen LTLT

CMACMA

現在のアライアンスの基盤成立

アランアンス安定期、新興勢力台頭

Base leading topresent alliancesformed; (Nedloyd⇒P&O, NOL⇒APL,HJ⇒DSR-Snator)

Maersk⇒Sealand,CMA⇒CGM, EMC⇒Lloyd Triestino,-a series of M&A

Existing alliancesstabilized, newplayers emerging,CSAV=>Norasia

Choyangbankruptcy

Start-up newalliance (CKY+HS)

Maersk⇒P&ONedlloyd

Lloyd Triestino changed thename to Italia Marittima, andthen integrated intoEvergreen

10

2-1. Fleet-scale Ranking

⑧ PCTC Owned

14

18.6

33.5

53.4

62.2

73.8

76.0

82.1

96.1

105.265

58

59

50

33

38

33

21

165.5

0 20 40 60 80 100 120

UECC

Toyofuji Shipping

Eukor Car Carriers

Leif Hoegh & Co.

Ray Shipping

Wallenius Lines AB

Cido Shipping

"K" Line

Mitsui O.S.K. Lines

Nippon Yusen Kaisha

(No. of Vessels, 10,000 DWT)

⑩ LNG Fleet (Managed)

9

9

9

10

10

12

12

22

27

29

24

3.44

3.44

3.44

3.82

3.82

4.58

4.58

8.4

9.16

11.07

10.31

0 5 10 15 20 25 30

Teekay

BP Shipping

"K" Line

BW GS

Ceres

Pronav

Golar

Stasco

MISC

NYK

MOL

No. of Vessels Share(%)

⑤ Cape-size Bulker Owned

23.6

24.5

24.6

28.7

31.0

50.2

54.3

59.2

63.8

66.437

35

33

3331

19

17

15

1414

0 20 40 60 80

Enterprises Shpg.

Cardiff Marine Inc.

China Steel Corp

Angelicoussis Group

Hanjin Shpg Co.

China Ocean (COSCO)

Zodiac Maritime Agy.

Kawasaki Kisen

Mitsui O.S.K. Lines

Nippon Yusen Kaisha

(No. of Vessels, 100,000 DWT)

⑨ AFRAMAX Tanker Owned

1216161927

3856

63.774.6

114.9121.3

128.3179.8

167.5187.4

293.8395.1

67

7

1112

12

70.6

130.7

587.7

0 100 200 300 400 500 600

Kawasaki KisenNippon Yusen Kaisha

- - - - - -Mitsui O.S.K. Lines

- - - - - -- - - - - -- - - - - -

Overseas ShipholdingCentrofin Mngt.

A.P. MollerThenamaris (Mgmt.)

BP PLCMinerva Marine Inc.

Zodiac Maritime Agy.Novorossiysk Shpg.

MISCTeekay Corporation

(No. of Vessels, 10,000 DWT)

⑦ PCTC Operated

55.934

41.075

130.845

138.15

221.985

298.659

417.19

459.911

16

21

31

34

42

54

79

81

85

94

364.5

392.79

0 50 100 150 200 250 300 350 400 450 500

Toyofuji Shipping

UECC

CIDO

GRIMALDI

Leif Hoegh & Co.

Wallenius Lines AB

"K" Line

Eukor Car Carriers

Mitsui O.S.K. Lines

Nippon Yusen Kaisha

(No. of Vessels, 1,000 Cars)

⑥ Dry Bulkers (All Types) Owned

61.2

39.5

51.9

19.7

29.2

103.1

43.3

115.9

135.5

192.9

50

52

53

63

76100

118140

160

326

0 50 100 150 200 250 300 350

Zodiac Maritime Agy.

Excel Maritime Carr.

Cardiff Marine Inc.

Polish Steamship Co.

K. G. JebsenKawasaki Kisen

China Shipping Group

Mitsui O.S.K. Lines

Nippon Yusen Kaisha

China Ocean (COSCO)

(No. of Vessels, 100,000 DWT)

Clarkson Clarkson

Clarkson

"K"Line ProcessedClarkson

Fearnley World PCC Report

11

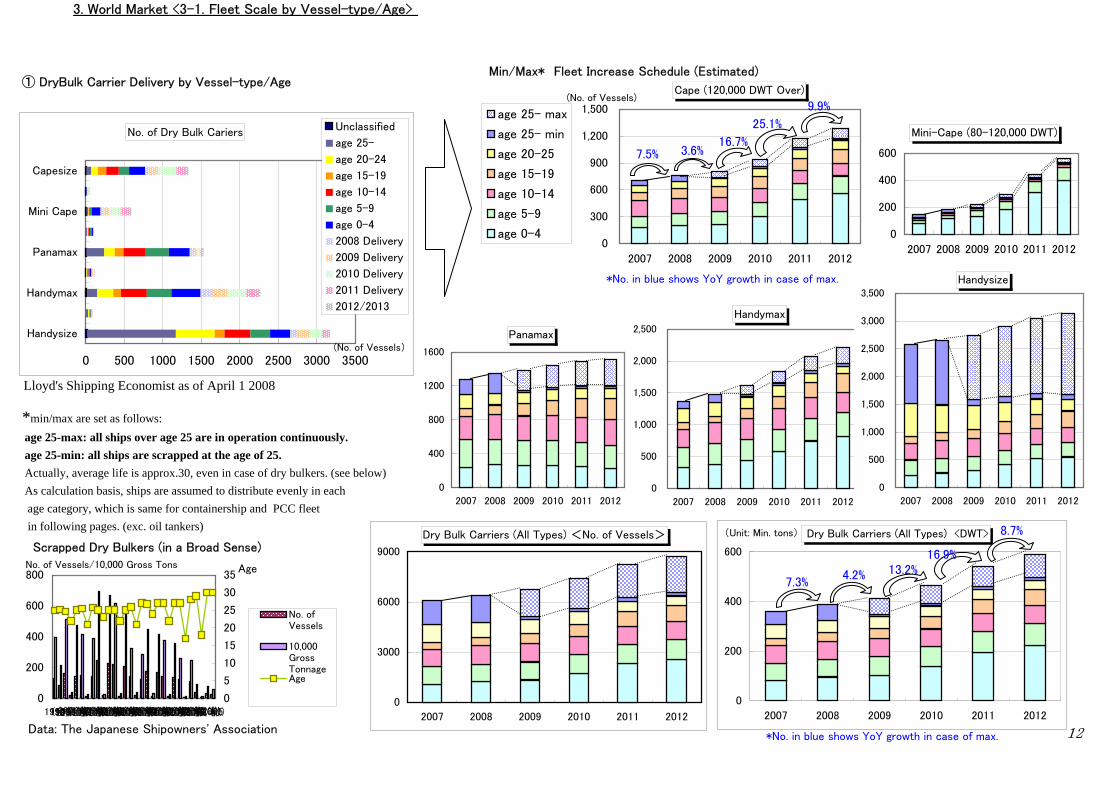

3. World Market <3-1. Fleet Scale by Vessel-type/Age>

① DryBulk Carrier Delivery by Vessel-type/Age

*min/max are set as follows: age 25-max: all ships over age 25 are in operation continuously. age 25-min: all ships are scrapped at the age of 25. Actually, average life is approx.30, even in case of dry bulkers. (see below) As calculation basis, ships are assumed to distribute evenly in each age category, which is same for containership and PCC fleet in following pages. (exc. oil tankers)

Cape (120,000 DWT Over)

0

300

600

900

1,200

1,500

2007 2008 2009 2010 2011 2012

(No. of Vessels)

age 25- max

age 25- min

age 20-25

age 15-19

age 10-14

age 5-9

age 0-4

No. of Dry Bulk Cariers

0 500 1000 1500 2000 2500 3000 3500

Handysize

Handymax

Panamax

Mini Cape

Capesize

(No. of Vessels)

Unclassified

age 25-

age 20-24

age 15-19

age 10-14

age 5-9

age 0-4

2008 Delivery

2009 Delivery

2010 Delivery

2011 Delivery

2012/2013

Min/Max* Fleet Increase Schedule (Estimated)

Scrapped Dry Bulkers (in a Broad Sense)

0

200

400

600

800

199419951996(全損等)(解 撤)1997(全損等)(解 撤)1998(全損等)(解 撤)1999(全損等)(解 撤)2000(全損等)(解 撤)2001(全損等)(解 撤)2002(全損等)(解 撤)2003(全損等)(解 撤)2004(全損等)(解 撤)2005

No. of Vessels/10,000 Gross Tons

0

5

10

15

20

25

30

35Age

No. ofVessels

10,000GrossTonnageAge

Mini-Cape (80-120,000 DWT)

0

200

400

600

2007 2008 2009 2010 2011 2012

Panamax

0

400

800

1200

1600

2007 2008 2009 2010 2011 2012

Handymax

0

500

1,000

1,500

2,000

2,500

2007 2008 2009 2010 2011 2012

Handysize

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2007 2008 2009 2010 2011 2012

Dry Bulk Carriers (All Types) <No. of Vessels>

0

3000

6000

9000

2007 2008 2009 2010 2011 2012

Dry Bulk Carriers (All Types) <DWT>

0

200

400

600

2007 2008 2009 2010 2011 2012

(Unit: Min. tons)

12

7.5% 3.6%16.7%

25.1%

9.9%

7.3%4.2% 13.2%

8.7%

16.9%

*No. in blue shows YoY growth in case of max.

*No. in blue shows YoY growth in case of max.

Lloyd's Shipping Economist as of April 1 2008

Data: The Japanese Shipowners' Association

3. World Market <3-1. Fleet Scale by Vessel-type/Age>

* Data are as of the end of each year. '08 Jan., No. of VLCC: 504 (151 of non-double hull tankers, and 353 of double hull) * Assumptions for no. of non-double hull tankers to be scrapped or converted after '08:

Min. Year '08: Vessels already fixed to be converted, and age over 25 yrs are scrapped Year '09, and '10 : Half of 94 non-double hull ships still existing at the end of '08 will be scrapped by half each year. By the end of '10, all of non-double hull will be demolished.

Max. After year '09, vessels only over 25 year old will be scrapped.

No. of PCC Carriers

0 100 200 300 400 500

-5,000DWT

5,000-9,999DWT

10,000-14,999DWT

15,000DWT-

Unclassified

age 25-

age 20-24

age 15-19

age 10-14

age 5-9

age 0-4

2008 Delivery

2009 Delivery

2010 Delivery

2011/2012

Lloyd's Shipping Economist as of April 1 2008

② PCC Delivery by Vessel-type/Age

No. of Oil Tankers

0 500 1000 1500 2000 2500

No.Handy

No.Panamax

No.Aframax

No.Suexmax

No.VLCC

No.Total Unclassified

age 25-

age 20-24

age 15-19

age 10-14

age 5-9

age 0-4

2008 Delivery

2009 Delivery

2010/11/2012

③ Oil Tanker Delivery by Vessel-type/AgeVLCC min-max* Forecasts

0

100

200

300

400

500

600

700

2000 2002 2004 2006 2008 2010 2012

No. of Vessels

Max.

Min

Newbuilding

PCC<All Types> (DWT)

0

2000

4000

6000

8000

10000

12000

14000

16000

2007 2008 2009 2010 2011

1,000dwt

11.7%7.2%

12.1%12.1%

Lloyd's Shipping Economist as of April 1 2008

"K"Line processedbased on Fearnleys,etc.

13

*No. in blue shows YoY growth in case of max.

PCC<All Types> (No. of Vessels)

0

200

400

600

800

1,000

2007 2008 2009 2010 2011

age25-max

age 25- min

age 20-24

age 15-19

age 10-14

age 5-9

age 0-4

3. World Market <3-1. Fleet Scale by Vessel-type/Age>

④ Containership Delivery by Vessel-type/Age

Min/Max* Fleet Increase Schedule (Estimated)

Lloyd's Shipping Economist as of Mar 1 2007

* Following graphs are based on other data-base to show no. of vessels, etc.

Containership Space (TEU)

0 1000 2000 3000 4000 5000

-1000 TEU-type

1000-1999

2000-2999

3000-3999

4000-4999

5000-5999

6000-7999

8000- TEU-type

1,000 TEUs

age 25-

age 20-24

age 15-19

age 10-14

age 5-9

age 0-4

2008 Delivery

2009 Delivery

2010 Delivery

2011/2012

Containership Delivery Schedule(No. of Vessels)

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 2013

No. ofvessels

~3,100 ~5,100 ~8,200 ~10,000 10,000~

Containership Delivery Schedule(Capacity-base)

0

300

600

900

1200

1500

1800

2008 2009 2010 2011 2012 2013

1,000TEU

~3,100 ~5,100 ~8,200 ~10,000 10,001~

PR News Service

World Continership Increase (Results and Forecasts)

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

'88'89'90'91'92'93'94'95'96'97'98'99'00'01'02'03'04'05'06'07'08'09'10'11

1,000 TEU/Vessel

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

No. of Vessels

Capa.(1,000TEU)

Capa. Growing Ratio

BRS-Alphaliner Annual Report2007 / Data as of 1 Jan. each year

Containerships <All Types> (Capacity)

0

4000

8000

12000

16000

20000

2007 2008 2009 2010 2011

(1,000 TEU)

age 25- max

age 25- min

age 20-24

age 15-19

age 10-14

age 5-9

age 0-4

Lloyd's Shipping Economist as of April 1 2008

14

3-2. Trend of Newbuildings

15

⑤ World Total Existing Tonnage

0

100

200

300

400

500

600

700

800

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Mil. Gross Ton

Tanker Bulk Carrier Others

<Data: Lloyd's Register> *until '91, data as of mid-year, from '92 as of the year-end.Year

④ World Newbuilding Delivery

0

10

20

30

40

50

60

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06Year

Mil. Gross Ton

Japan Korea China World Total

<Data: Lloyd's Register>

⑥ World Total Ship Demolition

05

1015202530354045

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07

Year

Mil. DWT

Tanker Bulk Carrier Combined Carrier Others

<Data: Fearnleys>*Based on ships sold for scrap 3. 2005年は1~3月までの値。

③ World Newbuilding Orders _

0

20

40

60

80

100

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06Year

Mil. Gross Ton

Japan Korea China World Total

<Data: Lloyd's Register>

① Ship Price as of Placing Order (Dry Bulkers, Tankers)

0

30

60

90

120

150

180

92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08Year

Mil. US$

VLCC AframaxCape PanamaxHandy

<Data: Clarkson>

<"K"Line processed based on domestic papers>

②Ship Price as of Delivery (Dry Bulkers, Tankers)

0

20

40

60

80

100

120

140

160

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11Fiscal Year (Apr.-Mar.)

Mil. US$

CAPE PANAMAX

VLCC AFRAMAX

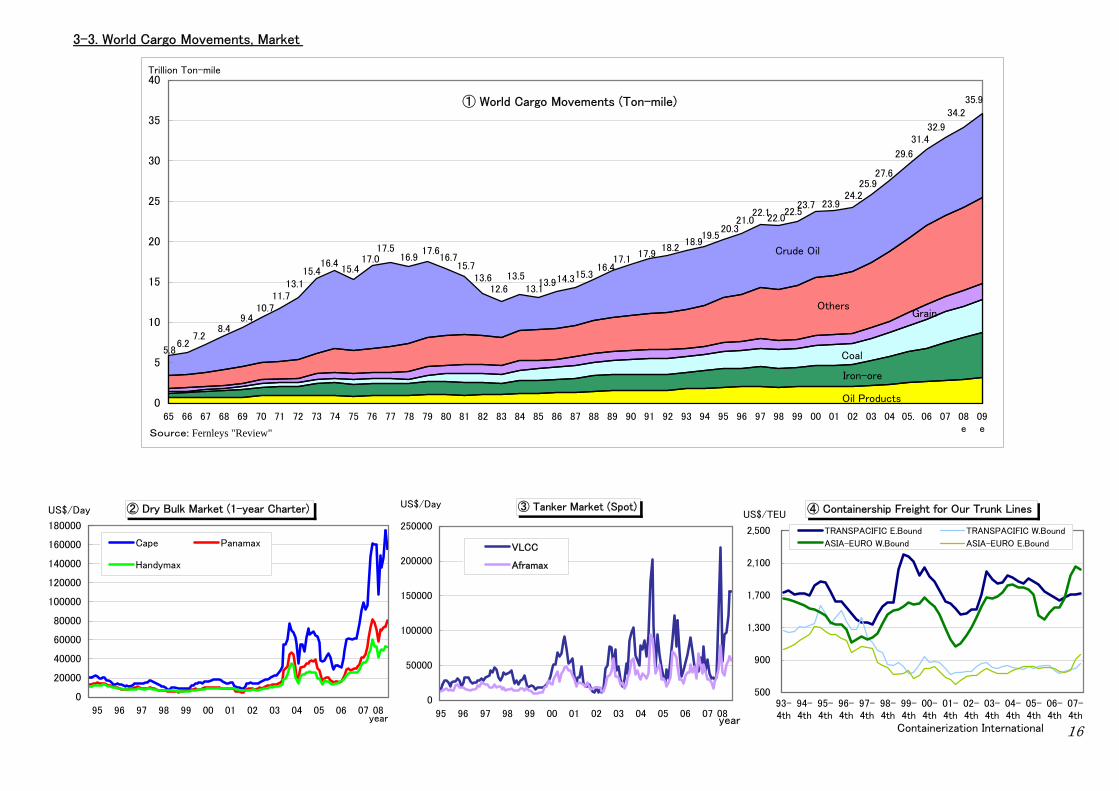

3-3. World Cargo Movements, Market

① World Cargo Movements (Ton-mile)

Oil Products

Iron-ore

Coal

GrainOthers

Crude Oil

35.934.2

32.931.4

29.6

27.625.9

24.223.923.7

22.522.0

22.121.0

20.319.5

18.918.2

17.917.1

16.415.314.313.9

13.113.5

12.613.6

15.716.7

17.616.9

17.517.0

15.416.4

15.413.1

11.710.7

9.48.4

7.2

5.86.2

0

5

10

15

20

25

30

35

40

65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05. 06 07 08e

09e

Trillion Ton-mile

Source: Fernleys "Review"

④ Containership Freight for Our Trunk Lines

500

900

1,300

1,700

2,100

2,500

93-4th

94-4th

95-4th

96-4th

97-4th

98-4th

99-4th

00-4th

01-4th

02-4th

03-4th

04-4th

05-4th

06-4th

07-4th

Containerization International

US$/TEU

TRANSPACIFIC E.Bound TRANSPACIFIC W.Bound

ASIA-EURO W.Bound ASIA-EURO E.Bound

② Dry Bulk Market (1-year Charter)

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

95 96 97 98 99 00 01 02 03 04 05 06 07 08

US$/Day

year

Cape Panamax

Handymax

③ Tanker Market (Spot)

0

50000

100000

150000

200000

250000

95 96 97 98 99 00 01 02 03 04 05 06 07 08year

US$/Day

VLCC

Aframax

16

3-4. Emerging Markets (China)

① Economic Growth Rate

<MOFA "Key Economic Indicator"> *Data After '07 by IMF

<MOFA 'Key Economic Indicator'>

⑤ Per-Capital GDP by Region in China

Yunnan

ZhejiangJiangsu

Shandong

Tianjin

Beijing

Guizhou

HunanJiangxiAnhui

ChongqingXinjiang

NeimengguLiaoning

Hainan

Hebei Jilin

NationalAverage

16,000 yuan

Shanxi

HenanHubei

Guangdong

FujianHeilongjiang

Shanghai

Shaanxi

NingxiaQinhai

SichuanTibet

Guangxi

Gansu

0

1

2

3

4

5

6

10,000 Yuan/Person

② Trade Trends for China

0

200

400

600

800

1000

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06

(Billion Dollars)

0

40

80

120

160

200

Export

Import

Trade Balance

④ Income Gap between Urban and Rural Area

117.59

7.391

35.87

3.976

0

20

40

60

80

100

120

140

'85 '86 '87 '88 '89 '90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06

(100 Yuan/Person)

0

1

2

3

4

5

Disposal Income in Urban Area

Net Revenue in Rural Area

Income Gap (-folds)

Real GDP Growth

-2

0

2

4

6

8

10

12

14

'00 '01 '02 '03 '04 '05 '06 '07 '08-e

'09-e

(%)

Japan

Korea

U.S.

Brazil

Russia

India

China

Germany

France

U.K.

Mining and Industrial Outbut Growth (%)

-10

-5

0

5

10

15

20

2001 2002 2003 2004 2005 2006 2007

(%)

Japan

Korea

USA

Russia

India

China

Germany

France

U.K.

Eastern AreasAvrg 33,000yuan

North-East AreaAvrg 18,000 yuan

Central AreaAvrg 12,000 yuan

Western AreaAvrg 11,000 yuan

⑥ Earning Gap between Areas

15.1

2.6

5.744983288

0

2

4

6

8

10

12

14

16

18

'95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06

(1000 Yuan /Person)

0

1

2

3

4

5

6(-fold)

Earnnig perPerson TheTop 20 Areas

Earnnig perPerson TheBottom 20Areas

Gap betweenthe Top 20and theBottom 20

*Dividing each of 31 provinces and cities nationwide into urban and ruralareas, income (disposal income for urban areas, and net revenue for rural)per-capita at each 62 area is calculated.

17

<METI 'White Paper on International Economy and Trade>

Shanghai57,000yuan

Guizhou6,000yuan

Gap of the No. of Durable Goods Ownedbetween Urban and Rural Area, 2006

0

50

100

150

200

Fan

Bicycle

Color T

VWash

er

Refrigir

ator

Teleph

one

Cell-ph

one

Air Con

dition

ar

Camera PC

Motorbi

ke

No./100 FamiliesUrban Area

Rural Area

*Data for Fan, Bicycle, Camera are as of 2005.

③ Energy Consumption in China

2.5

0.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

'85 '87 '89 '91 '93 '95 '97 '99 '01 '03 '05

(Billion SCEton)

-10

-5

0

5

10

15

20(%)

Energy Consumption

Growth Rate (YoY)

<METI 'White Paper on International Economy and Trade>

*SCE=Standard Coal Equivalent.

<METI 'White Paper on International Economy and Trade>

<METI 'White Paper on International Economy and Trade>

<METI 'White Paper on International Economy and Trade>

<METI 'White Paper on International Economy and Trade>

3-5. Emerging Markets (India, Vietnam)

① India

② Vietnam <Government of India, Ministry of Commerce & Industry, Dept. of Commerce>

<General Statistics Office of Vietnam>

Economic Growth in India

0

5

10

15

20

25

30

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06

(Trillion Rupee) %

0

2

4

6

8

10Real GDP

Real GDP Growth

Economic Growth in Vietnam

0

10

20

30

40

50

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

(Billion U.S.$) %

0

2

4

6

8

10

Real GDP

Real GDP Growth

18

Trends of Exports from India

0

20

40

60

80

100

120

140

1996-1997

1998-1999

2000-2001

2002-2003

2004-2005

2006-2007

(BillionU.S.$)

Japan China ASEAN4 NIEs USA EU15 Others

Trends of Imports into India

0

20

40

60

80

100

120

140

160

180

200

1996-1997

1998-1999

2000-2001

2002-2003

2004-2005

2006-2007

(BillionU.S.$)

Japan China ASEAN4 NIEs USA EU15 Others

Trends of Exports from Vietnam

0

5

10

15

20

25

30

35

40

45

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Prel. 20

06

(Billion U.S.$)

Japan China ASEAN4 NIEs U.S.A EU15※ Others

Trends of Imports into Vietnam

0

5

10

15

20

25

30

35

40

45

50

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Prel. 20

06

(BillionU.S.$)

Japan China ASEAN4 NIEs U.S.A. EU15※ Others

※W/O Data for Luxemburg

3-6. Emerging Markets (BRICs, VISTA, Turkey)

① BRICs (Ex. China)

② VISTA Countries

③ Turkey

Trends of Exports from VISTA Countries

0

20

40

60

80

100

120

2003 2004 2005 2006

(Billion U.S.$) Trends of Imports into VISTA Countries

0

20

40

60

80

100

120

140

160

2003 2004 2005 2006

(Billion U.S.$)

Vietnam

Indonesia

South Africa

Turkey

Argentina

<ジェトロ><JETRO>

Trends of Exports from BRICs Countries(Except China)

0

50

100

150

200

250

300

350

2003 2004 2005 2006

(10 BillionU.S.$)

Brazil

Russia

India

Trends of Imports into BRICs Countries(Except China)

0

50

100

150

200

2003 2004 2005 2006

(10 BillionU.S.$)

Trends of Imports into Turkey

0

20

40

60

80

100

120

140

160

180

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

(Billion U.S.$)

Others

EU15

U.S.A.

NIEs

ASEAN4

China

Japan

Trends of Exports from Turkey

0

20

40

60

80

100

120

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

(Billion U.S.$)

<Turkish Statistical Institute>19

<JETRO>

4. Bulk Carrier Business <4-1. "K"Line Fleet>

① K Line's Dry Bulk Fleet

0103 0203 0303 0403 0503 0603 0703 0803

Cape (DWT 170,000 ton~) 33 33 45 50 51 56 62 61

Over Panamax (DWT abt 100,000 ton) 10 11 12 15 14 12 15 15

Panamax (DWT 6-70,000 ton) 23 23 29 28 40 33 35 42

Handy max (DWT 4-50,000 ton) 13 14 20 16 15 17 21 24

Small Handy (DWT 3-40,000 ton) 19 21 17 17 15 11 11 12

Chip + Pulp 11 11 13 14 14 14 15 15

Total 109 113 136 140 149 143 159 169

*Data for Over Panamax till 0503 show no. of vessels operated by thermal coal carrier division

② K Line's Energy Transportation vessel Fleet

0203 0303 0403 0503 0603 0703 0803

LNG 21 22 24 26 30 31 34

Tankers LPG 2 3 3 3 3 3 5

CLEAN 2 3 3 3 2 5 5

DIRTY 5 5 6 9 10 10 12

VLCC 3 4 4 4 4 5 6

Tankers Total 12 15 16 19 19 23 28

③Ship Price as of Placing Order (Dry Bulkes, Tankers)

0

30

60

90

120

150

92 93 94 95 96 97 98 99 00 01 02 03 04 05 0607 08

Year

Unit: Mil. US$

VLCC Afra

Cape Panamax

Handy

④ Ship Price as of Completion (Dry Bulkers, Tankers)

0

30

60

90

120

150

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Unit: Mil. US$

Fiscal Year (Apr.-Mar.)

CAPE PANAMAX

VLCC AFRAMAX

33 33 45 50 51 56 62 6110 11

12 15 14 1215 15

23 2329

28 40 3335 42

13 14

20 1615 17

2124

19 21

17 1715 11

1112

11 11

13 1414 14

1515

0

30

60

90

120

150

180

0103 0203 0303 0403 0503 0603 0703 0803

Vessels Cape Over Panamax Panamax

Handy max Small Handy Chip + Pulp

21 22 24 26 30 31 342 3 3 3

3 35

2 3 3 32 5

5

55 6

910

1012

34

44

45

6

0

10

20

30

40

50

60

70

0203 0303 0403 0503 0603 0703 0803

Vessels LNG Tankers LPG

Tankers CLEAN Tankers DIRTY

Tankers VLCC

<Data: Clarkson> 20<"K"Line processed based on domestic papers>

4-2. Business Expansion of Drybulk Business into the World

1.Development of Organization2002 May : Establishment of "Bulk & Gas Division" in “K” Line (Europe) Ltd. in UK.2006 Feb.: Dispatch of Resident Officer in Charge of Dry Bulk Business to Shanghai, China.2006 Jul. : Establishment of Drybulk Project Business Division in Headquarters of "K"Line Tokyo 2007 Jul. : Dispatch of Resident Officer in Charge of Dry Bulk Business to Mumbai, India.

2.Business Expansion in China

Contractor Contract Period Cargo, Volume Vessel, Services Trade Routes Date ReleasedJiangsu Shagang Group Co., Ltd 10 Years from 1Q of 2005 Iron Ore, 2 Mil. Tons per Year Consecutive Voyage Charter, Large-sized Bulker West Australia or S.Africa - China 2004/9/9Baoshan Iron & Steel Co., Ltd 3 Years from 4Q of 2006 Iron Ore, 0.5 Mil. Tons per Year 185,000-ton Bulker Brazil - China 2006/11/8Baoshan Iron & Steel Co., Ltd 10 Years from 2H of 2008 Iron Ore, 2.4 Mil. Tons per Year Consecutive Voyage Charter ・200,000-ton Bulker West Australia - China 2006/11/8Baoshan Iron & Steel Co., Ltd 3 Years from 3Q of 2007 Iron Ore, 0.5 Mil. Tons per Year 170,000-ton Bulker Brazil - China 2007/6/15Baoshan Iron & Steel Co., Ltd 15 Years from 1Q of 2011 Iron Ore, 1.2 Mil. Tons per Year Consecutive Voyage Charter ・300,000-ton Bulker Brazil - China 2007/6/15Shougang Corp 5 Years from 3Q of 2007 Iron Ore, 0.5 Mil. Tons per Year 170,000-ton Bulker Brazil - China 2007/6/15Wuhan Iron and Steel Corp 5 Years from 1Q of 2008 Iron Ore, 0.5 Mil. Tons per Year 170,000-ton Bulker Brazil - China 2007/6/15

3.Business Expansion in India

Contractor Contract Period Cargo, Volume Vessel, Services Trade Routes Date ReleasedJSW Steel 7 Years from Jan. 2007 Coking Coal, 0.5 Mil. Tons per Year Panamax 7 Voyages per Year East Australia - India 2006/12/25JSW Energy 15 Years from 2009 Thermal Coal, 2.5 Mil. Tons per Year Consecutive Voyage Charter of 2 Post Panamax Indonesia - India 2007/6/18JSW Steel 15 Years from Apr. 2008 Coking Coal, 0.7 Mil. Tons per Year Consecutive Voyage Charter of a Panamax or Post P'max Australia, S.Africa, China - India 2007/9/28

10 Years from 2008-2009 Consecutive Voyage Charter of 2 Panamax 10 Years from 2012-2014 Consecutive Voyage Charter of 3 Post Panamax 10 Years from 2011-2014 Consecutive Voyage Charter of 5 Capesize

4. Business Expansion in Europe

Contractor Contract Period Cargo, Volume Vessel, Services Trade Routes Date ReleasedILVA(Italy) From 2009 Iron Ore A Long-term Voyage Charter of 300,000-ton Bulker Brazil - Italy 2004/5/24Electricité de France From 2009 A Long-term Time Charter of 170-180,000-ton Bulker 2006/11/17

5. Business Expansion in Other Area

Contractor Contract Period Cargo, Volume Vessel, Services Trade Routes Date ReleasedKorea Western Power Co., Ltd. 10 Years from 2H of 2011 Thermal Coal, 2.5 Mil. Tons per Year Consecutive Voyage Charter of a Capesize & Panamax Australia, S.Africa, Indonesia, Canada, China - S.Korea 2008/1/30Glovis Co., Ltd. 20 Years from 2012 Iron Ore, 3 Mil. Tons per Year Consecutive Voyage Charter of 250,000-ton Bulker West Australia - South Korea 2008/2/29

Coking Coal and Thermal Coal,12 Mil. Tons per Year

Australia, Indonesia, S.Africa , China,etc. - East and West Coast of India

2008/3/17JSW Group

21

4-3. Demand on Dry Bulk

① Transition of World Crude Steel Production

2007 Total 1,344 Million Ton (+8.1% YoY)

Germany

Italia

Spain

CIS(Soviet)

USA

Brazil

OthersJapan,120.2

IndiaFrance

TurkeyEngland

Korea

China,489.2

Japan China Korea India

France Germany Italia Spain

England Turkey CIS(Soviet) USA

Brazil Others

1985 Total 717 Million Ton

Japan

China

Korea

India

France

Germany

CIS(Soviet)

USA

Brazil

Others

Italia

Turkey

EnglandSpain

Japan China KoreaIndia France GermanyItalia Spain EnglandTurkey CIS(Soviet) USABrazil Others

1995 Total 752 Million Ton

Korea

India

France

CIS(Soviet)

USA

Brazil

Others

China, 95.4

Germany

Italia

Spain

Japan,101.6

Turkey England

Japan China Korea India

France Germany Italia Spain

England Turkey CIS(Soviet) USA

Brazil Others

1955 Total 273 Million Ton

CIS(Soviet)

USA

Spain

GermanyItalia

EnglandTurkey

OthersBrazil France

China,KoreaJapanIndia

Japan China KoreaIndia France GermanyItalia Spain EnglandTurkey CIS(Soviet) USABrazil Others

1965 Total 459 Million Ton

France

Germany

Italia

Spain

England

Turkey

USA

Brazil

Others

Japan China

India

Korea

CIS(Soviet)Japan China Korea

India France GermanyItalia Spain EnglandTurkey CIS(Soviet) USABrazil Others

1975 Total 647 Million Ton

Japan

China

Korea

India

France

Germany

Italia

Spain

EnglandCIS(Sovie

t)

USA

Brazil

Others

Turkey

Japan China Korea

India France Germany

Italia Spain England

Turkey CIS(Soviet) USA

Brazil Others

2005 Total 1,138 Million Ton

KoreaIndia

England

CIS(Soviet)

USA

Brazil

OthersJapan,112.5

China,349.4

France

GermanyItalia

Spain

Turkey

Japan China Korea India

France Germany Italia Spain

England Turkey CIS(Soviet) USA

Brazil Others

2006 Total 1,243 Million Ton (+ 9.2% YoY)

USA

Brazil

Others

CIS(Soviet)

India

FranceGermany

ItaliaSpain

EnglandTurkey

Korea

China,422.7

Japan,116.2

Japan China Korea India

France Germany Italia Spain

England Turkey CIS(Soviet) USA

Brazil Others

22

(+3.4%YoY)

(+3.3%YoY)

(+21.0%YoY)

(+15.8%YoY)

4-3. Demand on Dry Bulk

② World Coal Export (Thermal/Coking Coal) ③ World Coal Import in Total (2006) (2006)

Export Import

(2004) (2004)

Export Import

IISI Report', 'Handbook for Iron and Steel Statistics', 'Clarkson', etc.

(2002) (2002)

Export Import

Data: 'Annual Energy Report', etc.

④ Iron Ore Import into Major Asian Countries

0

100

200

300

400

500

600

700

800

900

1996 1998 2000 2002 2004 2006 2008e

Milliion Tons

Japan China

Korea Taiwan

Total

Total Thermal Coal Export

451.3 Mil. Tons

Indonesia

Australia

ChinaSouthAfrica

Russia

Columbia

Others

Poland

USA

Total CokingCoal Export

189.0 Mil. Tons Australia

Canada

USA

Russia

OthersIndonesia

China

Total Import658.6 Mil. Tons

Japan

Korea

Taiwan

Germany

Others

Russia

USA

Canada

Spain

India

UK

⑤ World Coal Consumption

0

200

400

600

800

1,000

1,200

'71 '73 '80 '85 '90 '95 '00 '01 '02 '03 '04 '05

Conversion Volume for Oil / Mil.Tons

USA

EU15

China

Japan

Korea

India

ASEAN7

ex. USSR

Others

Quoted from different sauces, total for 'Export' and 'Import' are not coincident.

Total Thermal Coal Export563 Mil. Tons

Columbia

Russia

SouthAfrica China

Australia

U.S.A

Kazakhstan

OthersIndonesi

a

Total CokingCoal Export

192 Mil. Tons Australia

Canada

U.S.A.

China

Others

Russia

Total Import754 Mil. Tons

Taiwan

Korea

JapanOthers

U.K.

GermanyIndia

U.S.A.Italy

Netherlands

Spain

Total CokingCoal Export220 Mil.Tons

Others

Canada

USA

Indonesia

Australia

Total ThermalCoal Export

593 Mil Tons

Others

China

Columbia

SouthAfrica

Russia

Indonesia

Australia

Italy

RussiaChina

USA

India

Germany

UK

Taiwan

Korea

JapanOthers

Total Import819 Mil.T

23

Data: 'Handbook of Energy & Economic Statics in Japan',etc.

5. Car Carrier Business <5-1."K"Line Fleet and Cargo Movements>

①"K"Line PCC FleetNo. of Cars (RT) 0103 0203 0303 0403 0503 0603 0703 0803

6000 - 3 4 7 10 12 13 17

5000 (4750-5650) 28 28 28 26 26 29 30 32

4000 (3800-4600) 13 13 13 15 17 20 24 25

3000 (2800-3500) 10 8 9 13 13 15 14 11

2000 (1600-2500) 10 8 6 4 2 2 5 5

800 (800-850) 6 5 5 5 10 15 14 12

Total 67 65 65 70 78 93 100 102

Fleet Scale (No of. Vessels)

6 5 5 5 10 15 14 1210 8 6 4

22 5 5

108 9 13 13

15 1411

1313 13 15

17

20 2425

2828 28 26

26

2930 32

3 47

10

1213 17

0

10

20

30

40

50

60

70

80

90

100

110

0103 0203 0303 0403 0503 0603 0703 0803

Vessels 800 2000 3000

4000 5000 6000

Fleet Scale(Estimated Capacity)

0

50

100

150

200

250

300

350

400

450

0103 0203 0303 0403 0503 0603 0703 0803

1000 Cars 800 2000 3000

4000 5000 6000

<Data: JAMA>

③ Total Cars/Trucks Expoted from Japan (Inc. Cars by GM Japan)② Cars/Trucks Transported by Our Fleet (Each Half Year)

24

<自動車工業会>

0

50

100

150

200

250

300

350

400

97/03 98/03 99/03 00/03 01/03 02/03 03/03 04/03 05/03 06/03 07/03 08/03

10,000 CarsJapan/North America Japan/Europe Japan/Others

Others Trade Bound for Japan

0

100

200

300

400

500

600

700

97/03 98/03 99/03 00/03 01/03 02/03 03/03 04/03 05/03 06/03 07/03 08/03

10,000 Cars USA EU Russia Middle East

China Thailand Other Asia Oceania

Central America South America Africa Others

※ 'Others' includes short sea transportation in Europe from 04/09

5-2. Demand on Vehicles

① World Automobile Production (2007) <OICA>

(Data: 'Handbook of Energy & Economic Statics in Japan')

③ Transition of Overseas Vehicle Production by Japanese Automakers <Data: JAMA>

<Data: JAMA>

<Data: JAMA>

Japan38.2%

China29.3%

Korea13.5%

Thailand4.1%

India7.6%

Others1.3%

Makaysia1.4%

Indonesia1.4%

Iran3.3%

25

Breakdown in Asia (2007)

Y1997 Y2007 ASIA 31.2% 41.6% EUROPE 34.2% 31.0% USA 33.2% 26.2%

④ Four-wheel Car Production and Sales in USA

0

5,000

10,000

15,000

20,000

1999 2000 2001 2002 2003 2004 2005 2006 2007

Unit : 1000 Cars

Production Sales (Import in Sales)

0

20

40

60

80

97 98 99 00 01 02 03 04 05 06 07

(Unit: Mil. Cars)CHINA

JAPAN

OTHER ASIA

EUROPE

USA

OCEANIA

AFRICA

Asia

② No. of Vehicles Possessed (Cars/1,000 People)

0

200

400

600

800

1000

1971 1980 1990 2000 2005

USA Brazil Russia Africa Middle East

China Japan Korea EU15 ASEAN9

Overseas Vehicle Production by Japanese Automakers

0

2000

4000

6000

8000

10000

12000

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Unit 1000 Cars USA EU AsiaMiddle East Europe(ex.EU) North America (ex.USA)Latin America Africa Oceania

6. Container Business <6-1. "K"Line Fleet and Cargo Volume>

① "K"Line Containership Fleet0103 0203 0303 0403 0503 0603 0703 0803

5500TEU Over (5500-8000) 0 8 13 13 13 15 21 22

3500TEU Type (3400-4000) 21 16 17 17 22 25 23 24

2800TEU Type (2700-2900) 8 5 5 4 5 5 7 8

2000TEU Type (1500-2500) 10 13 10 13 11 9 11 17

~1400TEU Type 18 19 18 17 22 23 27 28

Total 57 61 63 64 73 77 89 99

③"K"Line Volume, Share for Asia-North America/Europe Routes

② "K" Line Containership Average Freight/Volume for All Services

*As cargo volume for '97 1H-'99 2H, half of the actual data are indicated.

266258277280311

355391413414407426

450435409

556575 566

630661 666

825804763

584 615 617595

667

520

808

657711

732742754

516530504

1299

1301

1349

1220

11431146

1175

11391144

124312501207

117311751178

1108

1000

10501122

925

1044

932

810852

915861

1110

98110371073

1055

10731132

1078

1143

1068

11281194

0

200

400

600

800

1000

97 1H 98 1H 99 1H 00F1Q

00F3Q

01F1Q

01F3Q

02F1Q

02F3Q

03F1Q

03F3Q

04F1Q

04F3Q

05F1Q

05F3Q

06F1Q

06F3Q

07F1Q

07F3Q

USD/TEU

0

200

400

600

800

1000

1200

1400

1000 TEU Volume Average Freight

26

Asia-North America East-bound Volume, Share

0

50000

100000

150000

200000

250000

300000

350000

400000

450000

500000

1000 TEU)

0

0.01

0.02

0.03

0.04

0.05

0.06

(Share)

KL Volume 2E+0 2E+0 2E+0 2E+0 2E+0 3E+0 2E+0 3E+0 3E+0 3E+0 3E+0 4E+0 4E+0 4E+0 4E+0

Share 0.048 0.048 0.049 0.047 0.051 0.048 0.046 0.046 0.048 0.047 0.048 0.049 0.054 0.057 0.054

20011H

20012H

20021H

20022H

20031H

20032H

20041H

20042H

20051H

20052H

20061H

20062H

20071H

20072H

20081He

Asia-Europe West-bound Volume, Share

0

50000

100000

150000

200000

250000

300000

(1000 TEU)

0

0.01

0.02

0.03

0.04

0.05

0.06

(Share)

KL Volume 96613 1E+0 97793 2E+0 2E+0 2E+0 2E+0 2E+0 2E+0 2E+0 2E+0 2E+0 3E+0 3E+0 3E+0

Share 0.037 0.037 0.035 0.05 0.045 0.048 0.044 0.045 0.042 0.04 0.041 0.038 0.04 0.035 0.034

20011H

20012H

20021H

20022H

20031H

20032H

20041H

20042H

20051H

20052H

20061H

20062H

20071H

20072H

20081He

Fleet Scale(No. of Vessels)

19 18 17 22 23 27 28

10 13 10 1311 9

1117

8 55 4

5 5

7

821 1617 17

22 25

23

24

0 8 13 13

1315

21

22

18

0

20

40

60

80

100

0103 0203 0303 0403 0503 0603 0703 0803

Vessel ~1400TEU Type 2000TEU Type

2800TEU Type 3500TEU Type

5500TEU Over

Fleet Scale (Estimated Capacity)

0

50

100

150

200

250

300

350

0103 0203 0303 0403 0503 0603 0703 0803

1000 TEU

~1400TEU Type 2000TEU Type

2800TEU Type 3500TEU Type

5500TEU Over

6-1. "K" Line Fleet and Cargo Volume④ "K"Line/All Line Cargo Volume, Loading Factor for Asia-North America/Europe Services

"K"Line Asia-N. America (East-bound) CargoVolume, L/F

0

50

100

150

200

250

20001H20002H20011H20012H20021H20023Q

20024Q

20031Q

20032Q

20033Q

20034Q

20041Q

20042Q

20043Q

20044Q

20051Q

20052Q

20053Q

20054Q

20061Q

20062Q

20063Q

20064Q

20071Q

20072Q

20073Q

20074Q

1,000 TEU

-20%

0%

20%

40%

60%

80%

100%

120%Cargo Volume L/F L/F Growth

Container Asia Europe Trade (Market) Data: Drewry

0

500

1000

1500

2000

2500

3000

19981H

19992H

20003Q

20012Q

20021Q

20024Q

20033Q

20042Q

20051Q

20054Q

20063Q

20072Q

2008e1Q

1,000 TEU/USD

-20%

0%

20%

40%

60%

80%

100%

120%

CAPA W/B CARGO W/B Loading Factor E/B(%) L/F Growth Freight(USD/TEU)

"K"Line Asia-Europe (West-bound) Cargo Volume, L/F

0

50

100

150

20001H

20002H

20011H

20012H

20021H

20023Q

20024Q

20031Q

20032Q

20033Q

20034Q

20041Q

20042Q

20043Q

20044Q

20051Q

20052Q

20053Q

20054Q

20061Q

20062Q

20063Q

20064Q

20071Q

20072Q

20073Q

20074Q

1,000 TEU

-20%

0%

20%

40%

60%

80%

100%

120%Cargo Volume L/F L/F Growth

Container Transpacific Trade (Market) Data: Drewry

0

500

1000

1500

2000

2500

3000

3500

4000

4500

19962H

19971H

19982H

20001Q

20004Q

20013Q

20022Q

20031Q

20034Q

20043Q

20052Q

20061Q

20064Q

20073Q

2008e2Q