aozora bank fy2014 results analyst meeting · new mid-term plan today’s agenda (note) unless...

TRANSCRIPT

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

~~~~Primary Secondary Bank: An Even More Reliable Partner ~~~~

May 18, 2015

Aozora BankFY2014 Results

Analyst Meeting

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 1

Q&A Session

FY2014 Financial Results

Early and Full Repayment of Public Funds; New Mid-Term Plan

Today’s Agenda(Note) Unless otherwise stated, all figures are on a consolidated basis and amounts

stated in 100 million yen have been rounded to the nearest 100 million yen

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 2

Q&A Session

FY2014 Financial Results

Early and Full Repayment of Public Funds; New Mid-Term Plan

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 3

Summary

Early and Full Repayment of Public Funds

� Early and full repayment of public funds scheduled for June 29, 2015

� Adequate level of capital after full repayment

Strategic Direction

� “Primary Secondary Bank: An Even More Reliable Partner”

� Updated Business Model centered on ‘6 Focuses’

� Differentiated and specialized financial services

Financial Targets� ROE target: mid-term 9% or higher; long-term 10%

� Earnings target: Net revenue 100+ billion yen; Net income 40 billion yen or more

Capital Policy

� Dividend payout ratio: Increase to 50% of consolida ted net income

� Capital adequacy ratio target: 10% or higher (dome stic standard)

� Cancel 467 million of treasury shares (Retain 16.5 million treasury shares after cancella tion)

(Note) From FY2015 onwards, consolidated net income represents ‘profit attributable to owners of parent’ in accordance with the Revised Accounting Standards for Business Combinations and related standards and implementation guidance

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

FY2010 FY2011 FY2012 FY2013 FY2014

Net revenue 779 843 845 858 928

Net Income 328 463 406 423 437

16.93% 17.86% 15.70% 15.13% 14.45% 10.6%Capitaladequacy ratio

FY2010/ FY2011/ FY2012: Basel ll basis, domestic standard ; FY2013/ FY2014: Basel lll basis, domestic standard *2

Based on business-related revenue, including gains on the sale of domestic equity ETFs*1

Fair value of preferred shares: Share price x number of common share equivalents *3

Post-repayment estimate

*2

*1

Early and Full Repayment of Public Funds

The full repayment of the remaining 143.4 billion y en in public funds is scheduled for June 29, following the third installment payment of 20.5 bil lion yen, subject only to the approval of the regulatory authorities

4

< Business Performance >

< Installment Repayment of Public Funds >Share price (yen)

Remaining Amt. of Public funds

Fair value of Pref. Shares*3

3-month avg. share price (2/16 - 5/14)

(Preliminary)

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 5

Management Policy

Differentiated and Specialized Business

Model

� Capitalize on Aozora’s unique position as a mid-sized independent bank with a nationwide branch network, positioned differently from both mega banks and regional banks

� Further strengthen the Bank’s differentiated Business Model and upgrade its products and services, with the aim of providing higher value-added financial services to its customers

Social Responsibilityas a Bank

� Firmly establish new competitive advantages by providing solutions for social challenges, and continue to proactively contribute to the social and economic development of Japan

� Reaffirm the Bank’s commitment to a strong risk management framework and the maintenance of management soundness by properly responding to changes in the internal and external environment

Sustainable Improvement in Corporate Value

Responding to Mandate from Shareholders

� Put more emphasis on communications with shareholders, and pursue a sustainable improvement in corporate value and a stable return to shareholders

� Adopt a highly transparent corporate governance structure distinguished by disciplined management

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 6

‘4 Focuses’ Business Accomplishments

Retail Banking Focusing on Mass Affluent Customers Collaboration with Regional Financial Institutions

Proactive Approach to SME Customers Advanced Services in Specialty Finance Areas

<Increase in cross-selling> <Sales amount of derivative-embedded products to financial institutions >

<Disciplined expansion of overseas business>� Sharp focus on balancing risk-return in lending

operations

� Promotion of sales activities with business solutio ns, leveraging the Bank’s expertise

� Expansion of Asian Network

� Increased sales of derivative-related products to respond to customer needs

� Promoted inter-regional and cross-border business matching

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 7

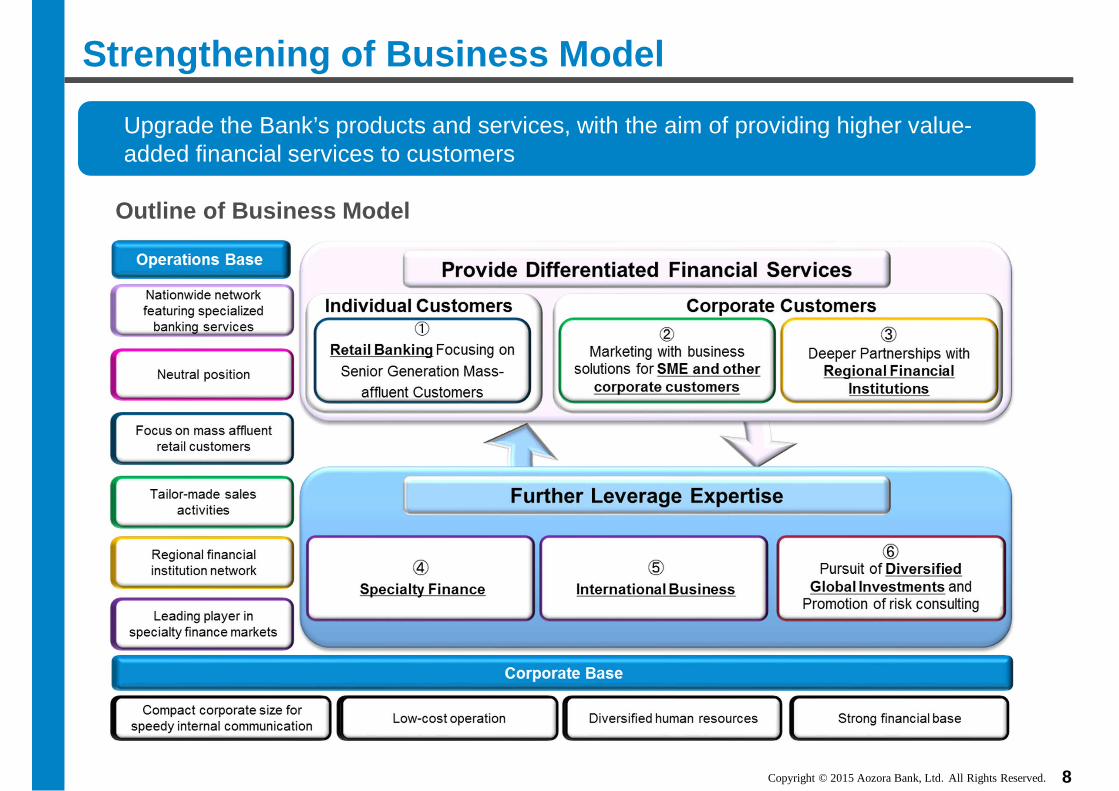

� Expand business base centered on “6 Focuses”

� Continue “selection and concentration” with respect to management resources

� Strengthen the Bank’s differentiated and specialized Business Model

Vision :“:“:“:“Primary Secondary Bank: An Even More Reliable Partner”

Key Points

Business Strategy

4 Focuses 6 Focuses

Specialty Finance

Deeper Partnerships with Regional Financial Institutions

Marketing with business solutions for SME and other corporate customers

Retail Banking Focusing on Senior Generation Mass-affluent

Customers

Pursuit of DiversifiedGlobal Investments and

Promotion of risk consulting

International BusinessCollaboration with Regional Financial Institutions

Proactive Approach to SME Customers

Retail Banking Focusing on Senior Generation Mass-affluent

Customers

Advanced Services in Specialty Finance Areas

Provide DifferentiatedFinancial Services

Further Leverage Expertise

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 8

Strengthening of Business Model

Outline of Business Model

Upgrade the Bank’s products and services, with the aim of providing higher value-added financial services to customers

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 9

‘6 Focuses’

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 10

Investment / M&A Strategy

Investment / M&A Strategy

� Evaluate capital investment or M&A opportunities from a mid- to long-term viewpoint, in accordance with the following basic principles aimed at further growth or new business leading to next generation market segments

� Existence of clear synergy and/or complementary relationship

� Target business should be manageable

� Appropriate investment costs, financially acceptable and future value can be expected

� Timing should be appropriate

Basic Principles

< Ref: Aozora Bank Group >

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 11

Resource Plan

Risk Management Framework

� Implement proactive risk management (management of early indicators)

� Structure/manage a credit portfolio where risk appetite and risk resistance are balanced

� Continue reviewing risk management framework in light of changes in financial regulations including Basel regulation

Human Resources

� Develop human resources and establish reputation as a “Team of highly-motivated and compassionate professionals”

� Foster human resources who have a strong sense of ethics and welcome challenges, and establish a better workplace for people with diverse backgrounds

IT and Facility Investments

� Improve service quality and provide prompt response for customers as well as realize stable system operation by Kanjo-kei System Replacement Project which has been a corporate priority for the Bank

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 12

Post-Repayment Financial Targets

Earnings Target

Key Performance Indicators (KPIs)

FY2012Results

FY2013Results

FY2014Results

Mid-term targets((((FY2015----FY2017)

Net interest margin 1.07% 1.09% 1.21% 1.20%

Non-interest income ratio 46% 46% 46% 40~~~~50%

Overhead ratio (OHR )))) 45.8% 45.8% 43.3% 45% or below

Credit cost ratio 0.09% 0.09% - 0.10~~~~0.20%

ROE 7.1% 8.0% 8.1% 9% or higher

ROA 0.8% 0.9% 0.9% 0.8%

FY2012Results

FY2013Results

FY2014Results

Mid-term targets((((FY2017))))

Net revenue 845 858 928 100+ billion yen

Net income 406 423 437 40 billion yen or more

Credit-related expenses were a net reversal in FY2014.*2Based on business-related revenue, including gains on the sale of domestic equity ETFs*1

*1

*1

*2 Long-term target

10%

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

Number of issued shares after cancellation

1,182.9 million shares

13

� Dividend payout: 50%%%% of consolidated net income (FY2015- FY2017)

� Continue payment of quarterly dividends, unique for a Japanese bank

Shareholder Return Policy Cancellation of Treasury Shares

Revised Capital Policy

*The full -year dividend forecast for FY2015 is based on the total dividend amount, which is 50% of the consolidated net income forecast of 43.0 billion yen for the full-year, divided by the total number of common shares issued, excluding treasury shares, as of March 31, 2015.

< Increase dividend payout ratio>

Adequate Capital

Treasury shares to be cancelled

467.3 million shares

Remaining Treasury shares16.5 million shares

1,166.4 million shares

*

CAR target

10%%%% or higher (FY2015-FY2017)

(yen)

CAR (domestic standard)

CET1 ratioPublic funds (Prefs.)

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 14

Q&A Session

FY2014 Financial Results

Early and Full Repayment of Public Funds; New Mid-Term Plan

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 15

� Net revenue was 92.8 billion yen and net income was 43.7 billion yen, both exceeding the FY2013 results and the FY2014 full-year forecasts

� Both net interest income and non-interest income increased year on year

� Net interest margin increased 12 bps year on year to 1.21%

� The OHR was 43.3%, reflecting the ongoing priority assigned to efficient operations

� Maintained strong financial condition

� Sound asset quality

� Conservative allocation of loan loss reserves

� Adequate capital

� Announced FY2014 full-year common share dividend of 14.90 yen, exceeding the full-year forecast of 14.70 yen

� FY2014 fourth quarter dividend payment : 4.90 yen per common share

ⅠⅠⅠⅠ. Financial highlights(Note) Unless otherwise stated, all figures are on a consolidated basis and amounts

stated in 100 million yen have been rounded to the nearest 100 million yen

: The Financial Reconstruction Law (FRL) ratio (non-consolidated) improved by 1.63 points to 1.35% from end-March 2014

: The ratio of loan loss reserves to total loans remained high at 2.29%

: Capital adequacy ratio (Basel III basis, domestic standard) was 14.45% (preliminary) as of end-March 2015

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

(100 million yen)

3 monthsJan. - Mar.

Full-YearA

3 monthsJan. - Mar.

Full-YearB

Amount %

Net revenue 205 806 231 928 +122 +15.2% 920 100.9%

General & administrative expenses -104 -393 -116 -402 -8 -2.1% -410 97.9%

Business profit 100 413 114 527 +114 +27.6% 510 103.3%

Ordinary profit 109 522 52 597 +75 +14.3% 515 115.9%

Net income 82 423 95 437 +14 +3.2% 430 101.6%

6 -23 -72 47 +70 -

-0 -0 -0 -58 -57 -

Taxes -27 -98 42 -102 -4 -

Achievement

FY2013 Change B-A FY2014full-yearforecast

FY2014

<<<<Reference >>>>

Credit-related expenses

Extraordinary profit

16

ⅡⅡⅡⅡ. PL: Summary

� Net income was 43.7 billion yen, exceeding the FY2013 result and the FY2014 full-year forecast� Net revenue was 92.8 billion yen, an increase of 12.2 billion yen, or 15.2% year on year, and

business profit was 52.7 billion yen, an increase of 11.4 billion yen, or 27.6%, both exceeding the FY2013 results

� Ordinary profit increased 7.5 billion yen, or 14.3%, to 59.7 billion yen

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

3 monthsJan. - Mar.

Full-YearA

3 monthsJan. - Mar.

Full-YearB

Amount %

Net revenue 205 806 231 928 +122 +15.2%

Net interest income 106 437 119 500 +63 +14.4%

Non-interest income 99 369 111 429 +59 +16.1%

Net fees & commissions 32 125 41 145 +20 +16.2%

Net trading revenues 32 98 42 125 +27 +27.4%

34 146 29 158 +12 +8.3%

Gains/losses on bond transactions 9 4 -11 29 +24 +545.4%

25 142 40 130 -12 -8.5%

(100 million yen)

Change B-A

Net other ordinary income

FY2013 FY2014

Net other ordinary incomeexcl. gains/losses on bond transactions

17

ⅡⅡⅡⅡ. PL: Net revenue

� Net revenue increased 12.2 billion yen, or 15.2% year on year, to 92.8 billion yen, exceeding the full-year forecast of 92.0 billion yen� Net interest income was 50.0 billion yen, an increase of 6.3 billion yen, or 14.4%, and non-interest

income was 42.9 billion yen, an increase of 5.9 billion yen, or 16.1%, both exceeding the FY2013 results

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

3 monthsJan. - Mar. A

Full-YearB

3 monthsJan. - Mar. C

Full-YearD C-A D-B

Net interest income 106 437 119 500 +13 +63

Interest income 141 590 152 634 +11 +44Interest on loans and discounts 103 424 110 429 +8 +5Interest and dividends on securities 34 141 38 177 +4 +36Other interest income 3 14 3 23 +1 +9Interest on swaps 2 11 1 5 -1 -6

Interest expenses -35 -153 -33 -134 +3 +19Interest on deposits and NCDs -27 -118 -22 -93 +5 +25Interest on debentures -1 -6 -1 -6 -0 +0Interest on borrowings and rediscount -1 -6 -2 -7 -1 -2Other interest expenses -2 -10 -3 -10 -0 -1Interest on swaps -3 -14 -5 -18 -2 -3

Decreases in expenses are shown as positive

Net interest marginYield on total investments (A) 1.44% 1.49% 1.50% 1.55% +0.06% +0.06%

Yield on loans (B) 1.56% 1.63% 1.61% 1.60% +0.05% -0.03%Yield on securities 1.22% 1.18% 1.38% 1.45% +0.16% +0.27%

Yield on funding (C) 0.37% 0.40% 0.33% 0.34% -0.04% -0.06%Net interest margin (A)-(C) 1.07% 1.09% 1.17% 1.21% +0.10% +0.12%Net loan margin (B)-(C) 1.19% 1.23% 1.28% 1.26% +0.09% +0.03%

(100 million yen)

FY2013 FY2014 Change

18

ⅡⅡⅡⅡ. PL: Net interest income

� Net interest income increased 6.3 billion yen, or 14.4% year on year, to 50.0 billion yen� Net interest margin increased 12 bps to 1.21%

� The yield on total investments increased 6 bps to 1.55% as the Bank continued its disciplined balance sheet management

� Funding costs were reduced 6 bps to 0.34% as a result of our ongoing efforts to reduce funding costs

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

3 monthsJan. - Mar.

A

Full-YearB

3 monthsJan. - Mar.

C

Full-YearD

C-A D-B

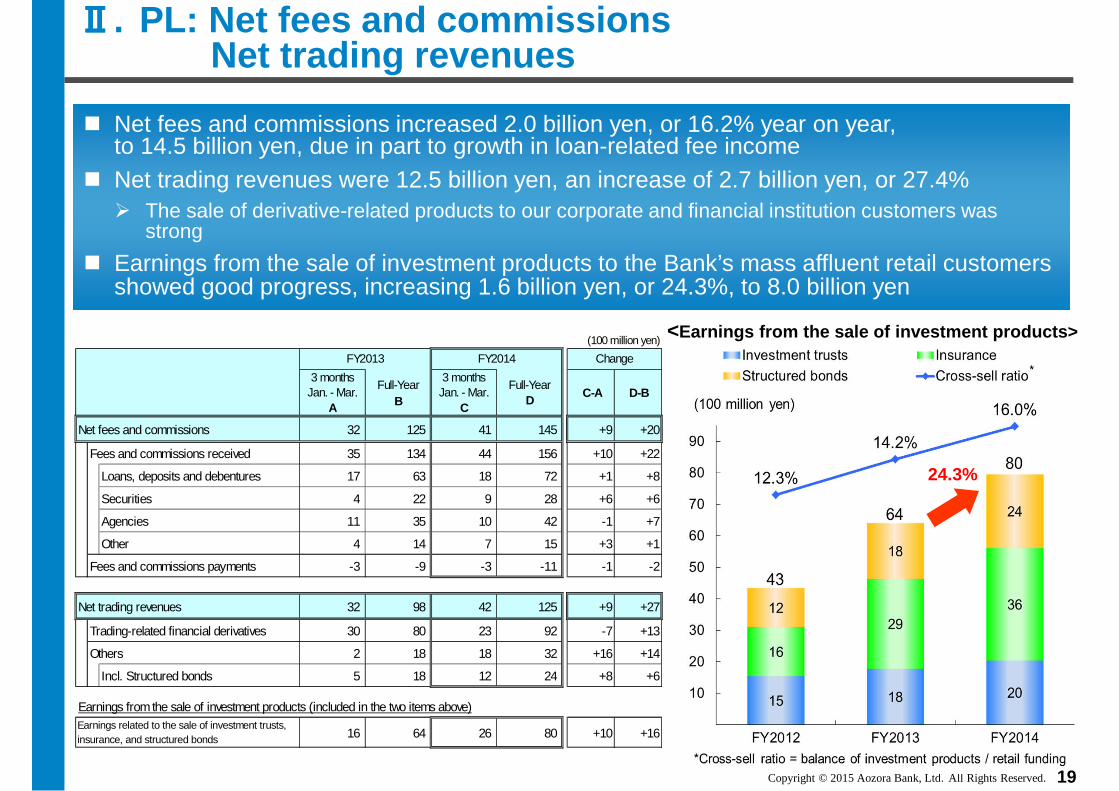

Net fees and commissions 32 125 41 145 +9 +20

Fees and commissions received 35 134 44 156 +10 +22

Loans, deposits and debentures 17 63 18 72 +1 +8

Securities 4 22 9 28 +6 +6

Agencies 11 35 10 42 -1 +7

Other 4 14 7 15 +3 +1

Fees and commissions payments -3 -9 -3 -11 -1 -2

Net trading revenues 32 98 42 125 +9 +27

Trading-related financial derivatives 30 80 23 92 -7 +13

Others 2 18 18 32 +16 +14

Incl. Structured bonds 5 18 12 24 +8 +6

16 64 26 80 +10 +16

(100 million yen)

Change

Earnings related to the sale of investment trusts,insurance, and structured bonds

FY2013 FY2014

Earnings from the sale of investment products (included in the two items above)

19

ⅡⅡⅡⅡ. PL: Net fees and commissionsNet trading revenues

� Net fees and commissions increased 2.0 billion yen, or 16.2% year on year, to 14.5 billion yen, due in part to growth in loan-related fee income� Net trading revenues were 12.5 billion yen, an increase of 2.7 billion yen, or 27.4%

� The sale of derivative-related products to our corporate and financial institution customers was strong

� Earnings from the sale of investment products to the Bank’s mass affluent retail customers showed good progress, increasing 1.6 billion yen, or 24.3%, to 8.0 billion yen

<Earnings from the sale of investment products>

24.3%

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

3 monthsJan. - Mar.

A

Full-YearB

3 monthsJan. - Mar.

C

Full-YearD

C-A D-B

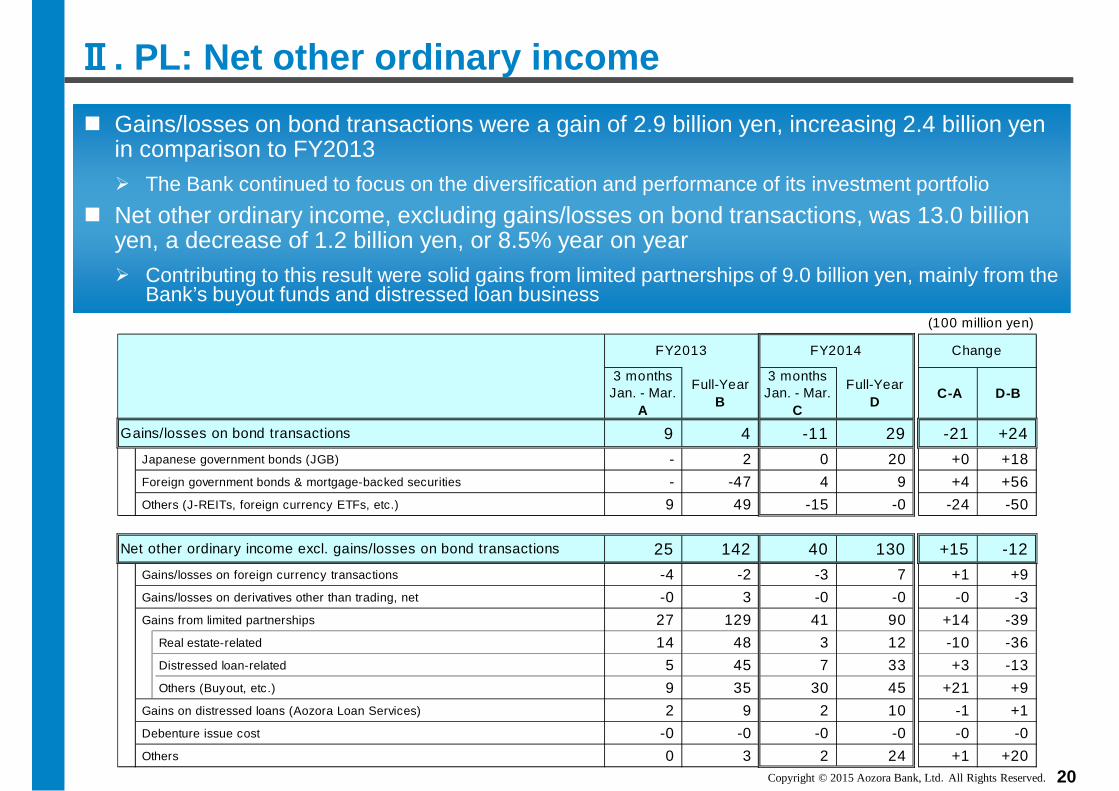

Gains/losses on bond transactions 9 4 -11 29 -21 +24

Japanese government bonds (JGB) - 2 0 20 +0 +18

Foreign government bonds & mortgage-backed securities - -47 4 9 +4 +56

Others (J-REITs, foreign currency ETFs, etc.) 9 49 -15 -0 -24 -50

Net other ordinary income excl. gains/losses on bond transactions 25 142 40 130 +15 -12

Gains/losses on foreign currency transactions -4 -2 -3 7 +1 +9

Gains/losses on derivatives other than trading, net -0 3 -0 -0 -0 -3

Gains from limited partnerships 27 129 41 90 +14 -39

Real estate-related 14 48 3 12 -10 -36

Distressed loan-related 5 45 7 33 +3 -13

Others (Buyout, etc.) 9 35 30 45 +21 +9

Gains on distressed loans (Aozora Loan Services) 2 9 2 10 -1 +1

Debenture issue cost -0 -0 -0 -0 -0 -0

Others 0 3 2 24 +1 +20

FY2013 ChangeFY2014

(100 million yen)

20

ⅡⅡⅡⅡ. PL: Net other ordinary income

� Gains/losses on bond transactions were a gain of 2.9 billion yen, increasing 2.4 billion yen in comparison to FY2013 � The Bank continued to focus on the diversification and performance of its investment portfolio

� Net other ordinary income, excluding gains/losses on bond transactions, was 13.0 billion yen, a decrease of 1.2 billion yen, or 8.5% year on year� Contributing to this result were solid gains from limited partnerships of 9.0 billion yen, mainly from the

Bank’s buyout funds and distressed loan business

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

3 monthsJan. - Mar.

A

Full-YearB

3 monthsJan. - Mar.

C

Full-YearD

C-A D-B

G&A expenses (A) 104 393 116 402 +12 +8

Personnel 52 200 56 204 +4 +4

Non-Personnel 47 175 54 175 +7 -0

Tax 5 19 6 23 +1 +4

205 858 231 928

45.8% 43.3%

FY2013 FY2014 Change

(100 million yen)

Net revenue (B)

OHR (A)/(B)

21

ⅡⅡⅡⅡ. PL: G&A expenses

� G&A expenses were 40.2 billion yen, a year on year increase of 0.8 billion yen, or 2.1%, mainly due to head count increases in our retail staff

� The OHR was 43.3% due to growth in net revenue, as well as the ongoing priority the Bank has assigned to efficient operations

Breakdown of G&A expenses <G&A expenses transition>

*Based on business-related revenue, including gains on the sale of domestic equity ETFs

*

*

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

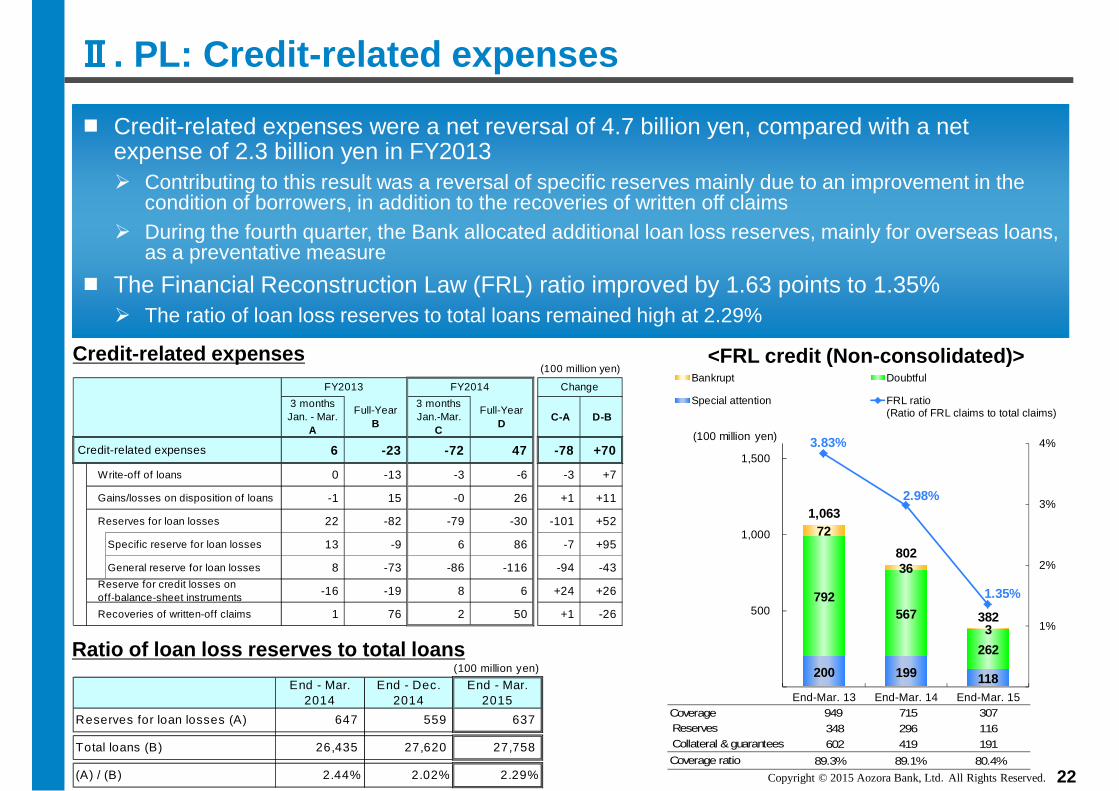

Coverage 949 715 307

348 296 116

602 419 191

89.3% 89.1% 80.4%Coverage ratio

Reserves

Collateral & guarantees

200 199 118

792567

262

72

36

3

1,063

802

382

3.83%

2.98%

1.35%

1%

2%

3%

4%

500

1,000

1,500

End-Mar. 13 End-Mar. 14 End-Mar. 15

Bankrupt Doubtful

Special attention FRL ratio(Ratio of FRL claims to total claims)

(100 million yen)

(100 million yen)

End - Mar.2014

End - Dec.2014

End - Mar.2015

Reserves for loan losses (A) 647 559 637

26,435 27,620 27,758

2.44% 2.02% 2.29%

Total loans (B)

(A) / (B)

3 monthsJan. - Mar.

A

Full-YearB

3 monthsJan.-Mar.

C

Full-YearD

C-A D-B

6 -23 -72 47 -78 +70

Write-off of loans 0 -13 -3 -6 -3 +7

Gains/losses on disposition of loans -1 15 -0 26 +1 +11

Reserves for loan losses 22 -82 -79 -30 -101 +52

Specific reserve for loan losses 13 -9 6 86 -7 +95

General reserve for loan losses 8 -73 -86 -116 -94 -43

-16 -19 8 6 +24 +26

Recoveries of written-off claims 1 76 2 50 +1 -26

(100 million yen)

Reserve for credit losses onoff-balance-sheet instruments

FY2013

Credit-related expenses

FY2014 Change

22

ⅡⅡⅡⅡ. PL: Credit-related expenses

� Credit-related expenses were a net reversal of 4.7 billion yen, compared with a net expense of 2.3 billion yen in FY2013 � Contributing to this result was a reversal of specific reserves mainly due to an improvement in the

condition of borrowers, in addition to the recoveries of written off claims� During the fourth quarter, the Bank allocated additional loan loss reserves, mainly for overseas loans,

as a preventative measure

� The Financial Reconstruction Law (FRL) ratio improved by 1.63 points to 1.35% � The ratio of loan loss reserves to total loans remained high at 2.29%

<FRL credit (Non-consolidated)>

Ratio of loan loss reserves to total loans

Credit-related expenses

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

(100 million yen)

Change

B - A

30,097 29,925 29,847 -250

Debentures 1,976 2,305 2,461 +486

1,588 1,795 1,872 +285

Trading liabilities 3,182 3,852 3,113 -70

Others 6,051 7,645 6,277 +226

Total liabilities 42,894 45,520 43,571 +677

Capital stock 1,000 1,000 1,000 -

Capital surplus 3,102 2,897 2,897 -205

Retained earnings 2,098 2,306 2,350 +252

-993 -993 -993 -

-31 221 349 +380

-69 13 12 +81

Others 53 59 59 +6

Total net assets 5,160 5,502 5,674 +514

Total liabilities and net assets 48,054 51,023 49,245 +1,190

End - Dec.2014

Borrowed money

End - Mar.2014 A

End - Mar.2015 B

Treasury Stock

Valuation difference onavailable-for-sale securities

Foreign currency translation adjustment

Deposits /Negotiable certificates of deposit

Change

B - A

Loans and bills discounted 26,435 27,620 27,758 +1,323

Domestic loans 21,016 20,414 20,197 -818

Overseas loans 5,419 7,206 7,561 +2,141

Securities 11,686 12,580 9,841 -1,846

Incl. JGBs 3,459 3,689 1,940 -1,519

Incl. US Treasury 2,060 2,285 2,066 +7

Cash and due from banks 4,419 3,936 5,505 +1,087

3,529 4,110 3,471 -58

Others 1,986 2,776 2,670 +684

Total assets 48,054 51,023 49,245 +1,190

End - Mar.2014 A

End - Mar.2015 B

End - Dec.2014

Trading assets

23

ⅢⅢⅢⅢ. Balance Sheet: Summary

� Total assets increased 119.0 billion yen, or 2.5%, to 4,924.5 billion yen, as compared with end-March 2014� Loans increased 132.3 billion yen and securities decreased 184.6 billion yen

� Total liabilities were 4,357.1 billion yen, an increase of 67.7 billion yen, or 1.6%, as compared with end-March 2014� Total net assets were 567.4 billion yen, an increase of 51.4 billion yen, or 10.0%,

in comparison with end-March 2014

* With no final risk residing in Japan

*

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

Retail funding ratio 64.6% 63.8% 63.8%

Loan-to-deposit ratio incl. NCDs 89.5% 87.8% 93.0%

20,727 20,463 20,597

7,074 6,503 6,135

4,282 5,107 5,576

32,083 32,073 32,309

10,000

20,000

30,000

40,000

End-Mar. 13 End-Mar. 14 End-Mar. 15

Financial Institutions Corporate and Public Institutions Retail

(100 million yen)

(100 million yen)

5,223 5,052 6,300

End-Mar.2015

Liquidity reserves

End-Dec.2014

End-Mar.2014

(100 million yen)

Change

B-A

30,097 29,925 29,847 -250

1,976 2,305 2,461 +486

End-Mar.2015 B

Deposits/ NCDs

Debentures

End-Dec.2014

End-Mar.2014 A

(100 million yen)

Change

B-A

32,073 32,230 32,309 +236

End-Mar.2015 B

End-Dec.2014

End-Mar.2014 A

Total core funding

24

ⅢⅢⅢⅢ. Balance Sheet: Funding

� Total core funding was 3,230.9 billion yen, an increase of 23.6 billion yen, or 0.7% from end-March 2014

� The percentage of retail funding to total core funding was 63.8%

� Liquidity reserves were at an adequate level of 630.0 billion yen

Funding sources < Funding by customer segment >

<Funding sources by products>

Liquidity reserves

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

(100 million yen)

Balance % Balance % Balance % B -A

Loans by dom estic o ffices (exc lud ing Japan o ffsho re m arke t acco un ts ) 23 ,951 90 .6% 24,187 87 .6% 23,926 86 .2% -25

M anufacturing 2,961 11 .2% 2,720 9 .8% 2,643 9 .5% -318

Agriculture, forestry and fisheries 24 0 .1% 31 0 .1% 31 0 .1% +7

M ining, quarry, gravel extraction 19 0 .1% 18 0 .1% 16 0 .1% -3

Construction 223 0 .8% 254 0 .9% 222 0 .8% -1

Electricity, gas, heat supply and w ater 61 0 .2% 99 0 .4% 143 0 .5% +82

Information and communications 564 2 .1% 427 1 .5% 402 1 .4% -161

Transport, postal services 1,122 4 .2% 1,034 3 .7% 823 3 .0% -299

W holesale and retail sale 1,284 4 .9% 1,246 4 .5% 1,278 4 .6% -6

Financial and insurance 3,840 14 .5% 3,967 14 .4% 4,317 15 .6% +476

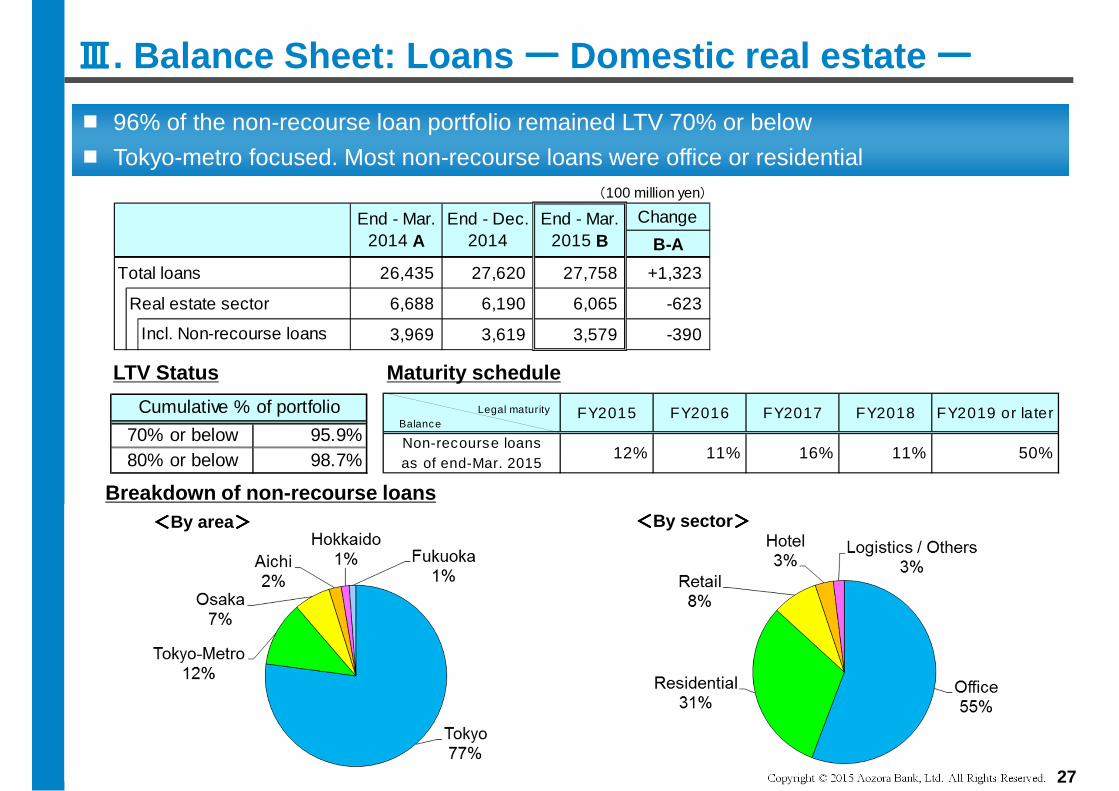

Real estate 6,688 25 .3% 6,190 22 .4% 6,065 21 .8% -623 3,969 59 .3% 3,619 58 .5% 3,579 59 .0% -390

Leasing 1,123 4 .2% 1,217 4 .4% 1,167 4 .2% +44

O ther services 1,590 6 .0% 1,618 5 .9% 1,609 5 .8% +19

Local governments 455 1 .7% 413 1 .5% 404 1 .5% -51

O thers 3,997 15 .1% 4,953 17 .9% 4,806 17 .3% +809 3,426 13 .0% 4,390 15 .9% 4,260 15 .3% +834

2,485 9 .4% 3,434 12 .4% 3,832 13 .8% +1,348

T otal 26,435 100.0% 27,620 100.0% 27,758 100.0% +1,323

Domestic loans 21,016 79 .5% 20,414 73 .9% 20,197 72 .8% -818

O verseas loans (with no final r isk residing in Japa n) 5,419 20 .5% 7,206 26 .1% 7,561 27 .2% +2,141

C hangeLoans and b ills d iscountedby indus try

End - Mar.2014 A

E nd - Mar.2015 B

End - D ec.2014

Incl. Non-recourse loans*

Incl. O verseas (Headquarters booked)

Loans by ov e rse as office s incl. Japan offshore m ark e t accounts

* Non-recourse loans ratio is % of real estate loans 25

ⅢⅢⅢⅢ. Balance Sheet: Loans

� Loans increased 132.3 billion yen, or 5.0%, to 2,775.8 billion yen from end-March 2014

� Overseas loans increased, while domestic loans decreased as the Bank maintained its focus on balancing risk and return

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

(100 million yen)

Change

B - A

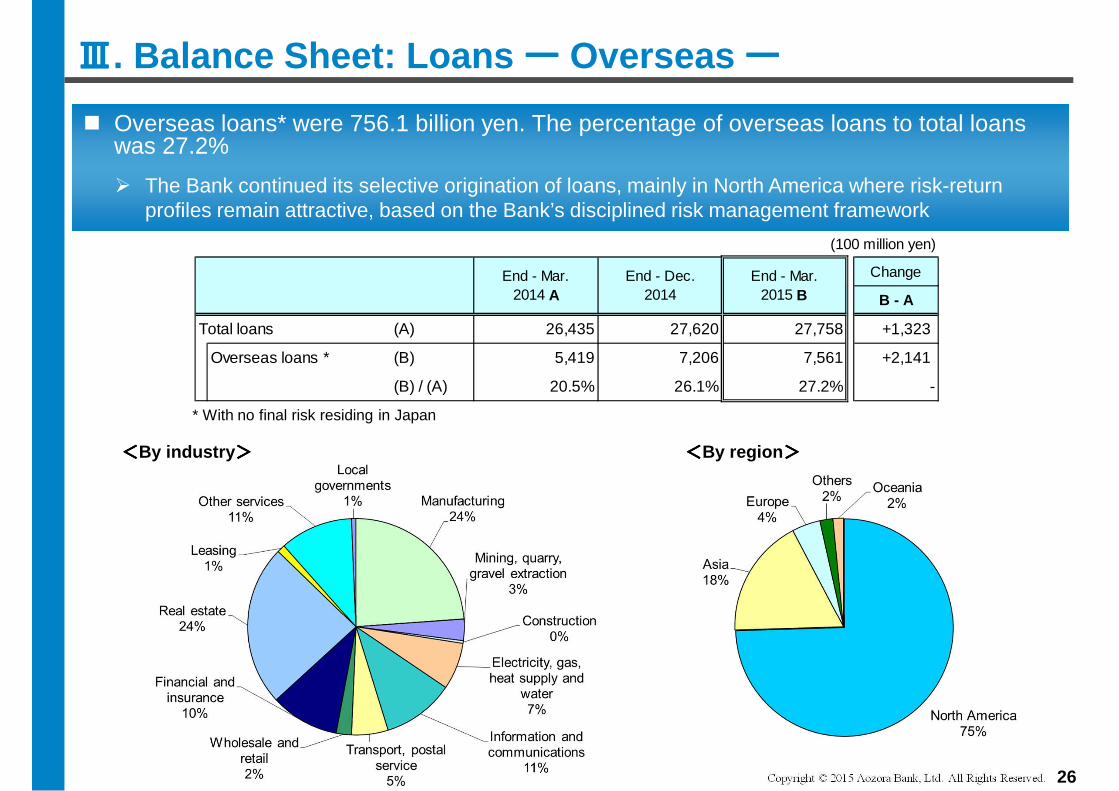

Total loans (A) 26,435 27,620 27,758 +1,323

Overseas loans (B) 5,419 7,206 7,561 +2,141

(B) / (A) 20.5% 26.1% 27.2% -

End - Mar.2015 B

End - Mar.2014 A

End - Dec.2014

26

<<<<By industry >>>> <<<<By region >>>>

ⅢⅢⅢⅢ. Balance Sheet: Loans ーーーー Overseas ーーーー

� Overseas loans* were 756.1 billion yen. The percentage of overseas loans to total loans was 27.2%

� The Bank continued its selective origination of loans, mainly in North America where risk-return profiles remain attractive, based on the Bank’s disciplined risk management framework

* With no final risk residing in Japan

*

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

Breakdown of non-recourse loans

70% or below80% or below

95.9%98.7%

Cumulative % of portfolio

(100 million yen)

Change

B-A

Total loans 26,435 27,620 27,758 +1,323

Real estate sector 6,688 6,190 6,065 -623

3,969 3,619 3,579 -390

End - Mar.2014 A

Incl. Non-recourse loans

End - Mar.2015 B

End - Dec.2014

27

ⅢⅢⅢⅢ. Balance Sheet: Loans ーーーー Domestic real estate ーーーー

� 96% of the non-recourse loan portfolio remained LTV 70% or below

� Tokyo-metro focused. Most non-recourse loans were office or residential

LTV Status Maturity schedule

<<<<By area>>>> <<<<By sector >>>>

Non-recourse loansas of end-Mar. 2015

12% 11% 16% 11% 50%

FY2018 FY2019 or laterFY2015 FY2017FY2016 Legal maturity Balance

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

(100 million yen)

ChangeB - A D - C

JGBs 3,459 3,689 1,940 -1,519 20 8 9 -11 Incl. TDB only 1,702 2,902 1,602 -100 -0 0 0 +0 Incl. 15Y floating rate only 1,453 787 338 -1,115 23 8 9 -14

Municipal bonds 169 159 185 +16 1 2 1 +1 Corporate bonds 575 418 393 -182 3 2 0 -3 Equities 295 381 418 +123 6 229 263 +257 Foreign bonds 3,672 3,856 3,704 +32 -108 -14 36 +143

US Treasury 2,060 2,285 2,066 +7 -48 -10 19 +67 MBS 1,128 801 899 -229 -67 -22 -5 +62 German government bonds - 318 285 +285 - 12 16 +16

485 452 454 -30 8 7 5 -2 Others 3,516 4,077 3,200 -315 38 118 201 +164

Hedge funds 79 76 72 -7 21 24 24 +4 ETFs 1,308 2,118 1,444 +136 6 34 111 +105 Investments in limited partnerships 430 405 675 +244 0 3 6 +5 REIT 349 439 482 +133 14 65 59 +45 Investment trusts 1,247 860 324 -923 -3 -9 -2 +1 Others 102 179 204 +101 -0 1 4 +4

Total 11,686 12,580 9,841 -1,846 -40 345 511 +551

Book value

End - Mar.2014 C

Others

Unrealized gains / lossesEnd - Mar.

2015 DEnd - Dec.

2014ChangeEnd - Mar.

2014 AEnd - Mar.

2015 BEnd - Dec.

2014

28

ⅢⅢⅢⅢ. Balance Sheet: Securities

A portion of beneficial interests in investment trusts within ‘monetary claims bought’ is marked at fair value, but the amounts (balance sheet total 0.7 billion yen; valuation gains of 1 million yen as of end-March 2015) are not included in the table above

� Securities were 984.1 billion yen, a decrease of 184.6 billion yen, or 15.8%, compared with end-March 2014� Total unrealized gains amounted to 51.1 billion yen, increasing 55.1 billion yen from

end-March 2014� Unrealized gains on foreign bonds and ETFs increased, in addition to an increase in unrealized gains

on equities in the third quarter due to the public offering of an unlisted stock

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

(100 million yen)

End-Mar. End-Mar. Change

2014 A 2015 B B - A

Capital adequacy ratio 15.13% 14.45% -0.68%

Regulatory capital (A-B) 5,289 5,429 140

Instruments and reserve (A) 5,289 5,453 164

Shareholders' equity 4,946 4,989 43

Others 343 464 121

Regulatory adjustment (B) - 23 23

Risk-weighted assets 34,956 37,570 2,615

Credit risk assets 32,254 34,614 2,361

Market risk assets 1,368 1,478 110

Operational risk assets 1,334 1,478 144

29

ⅣⅣⅣⅣ. Capital Adequacy Ratio (Preliminary)

� Capital adequacy ratio (Basel III basis, domestic standard) was 14.45% (preliminary) as of end-Mar. 2015, and remained at an adequate level

Basel III basis, domestic standard

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

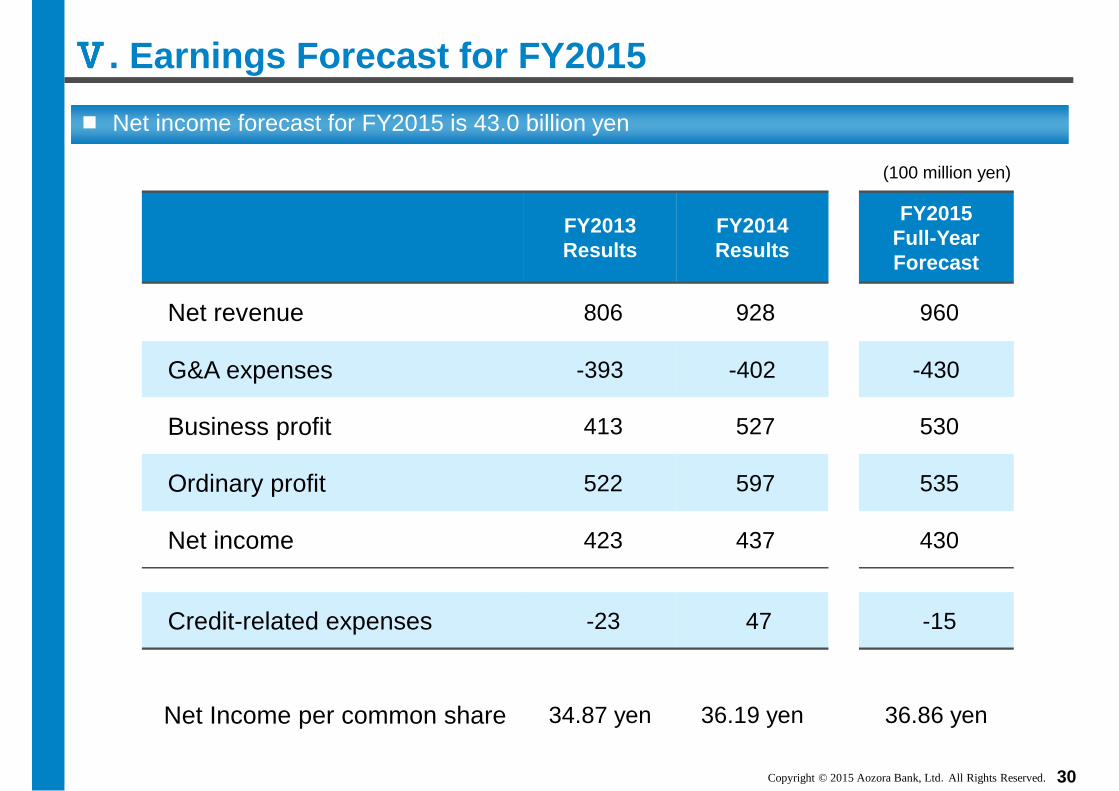

ⅤⅤⅤⅤ. Earnings Forecast for FY2015

� Net income forecast for FY2015 is 43.0 billion yen

(100 million yen)

FY2013Results

FY2014Results

FY2015Full-YearForecast

Net revenue 806 928 960

G&A expenses -393 -402 -430

Business profit 413 527 530

Ordinary profit 522 597 535

Net income 423 437 430

Credit-related expenses -23 47 -15

Net Income per common share 34.87 yen 36.19 yen 36.86 yen

30

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

1st quarter 2nd quarter 3rd quarter Year-end Full-year

Current forecast(FY2015)

18.40 yen

Dividend payment(FY2014)

3.00 yen 3.00 yen 4.00 yen 4.90 yen 14.90 yen

Dividend per common share

31

� Dividend forecast for FY2015 : 18.40 yen per common share� The Bank will continue the payment of quarterly dividends

< Dividend transition >

*The full-year dividend forecast for FY2015 is based on the total dividend amount, which is 50% of the consolidated net income forecast of 43.0 billion yen for the full-year, divided by the total number of common shares issued, excluding treasury stock, as of March 31, 2015

*

ⅥⅥⅥⅥ. Dividend Forecast for FY2015

(Note) From FY2015 onwards, consolidated net income represents ‘profit attributable to owners of parent’ in accordance with the Revised Accounting Standards for Business Combinations and related standards and implementation guidance

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

� FY2014 results

(100 million yen)

RetailBankingGroup

InstitutionalBankingGroup

SpecializedBankingGroup

FinancialMarketsGroup

BusinessGroupTotal

CompanyTotal

RetailBankingGroup

InstitutionalBankingGroup

SpecializedBankingGroup

FinancialMarketsGroup

BusinessGroupTotal

CompanyTotal

Netrevenue 144 223 355 82 804 806 145 266 348 168 927 928

G&Aexpenses -78 -156 -124 -37 -394 -393 -81 -152 -131 -38 -402 -402

Businessprofit 66 67 231 46 410 413 64 114 217 130 525 527

FY2013 Full-Year FY2014 Full-Year

ⅦⅦⅦⅦ. Reference : Results by Business Group

32

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 33

� Non-consolidated net income was 48.3 billion yen, an increase of 6.7 billion yen, or 16.1% year on year� Difference between non-consolidated net income and consolidated net income of 43.7 billion yen

was 4.6 billion yen, mainly due to the recognition in the first quarter of FY2014 of an extraordinary loss of 5.7 billion yen on a consolidated basis only

ⅦⅦⅦⅦ. Reference : Consolidated, Non-consolidated Difference

(100 million yen)

Non-consolidated net income 483

Subsidiaries

Shareholding, etc Net Income

Aozora Trust Bank, Ltd. 100.0% -0

Aozora Securities Co., Ltd. 100.0% 6

Aozora Loan Services Co., Ltd. 67.6% 1

Aozora Regional Consulting Co., Ltd. 100.0% 0

Aozora Investment Management Co., Ltd. 100.0% -2

Aozora Real Estate Investment Advisors Co., Ltd. 100.0% -0

Aozora Asia Pacific Finance Limited (AAPF) 100.0% 4

AZB CLO 1-4 100.0% 1

AZB Funding 1-5 100.0% 1

Aozora Investment, Inc. etc. 100.0% 12

23

-70

Incl. Foreign currency translation adjustment -57

Consolidated net income 437

Difference -46

Company name

Total

Consolidation adjustments

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

� Deferred tax assets were 40.7 billion yen (*1)

(A) Future taxable income for the next 5 years has been conservatively estimated at 183.6 billion yen

(B) The total of future deductible temporary differences realizable within the next 5 years of 109.6 billion yen and tax loss carryforwards of 16.8 billion yen was 126.4 billion yen

Deferred tax assets were calculated at 40.7 billion yen(*1) by multiplying (B), the lesser amount of (A) and (B) above, by the effective tax rate (32.5%)

� Income taxes deferred were a net expense of 6.8 billion yen, which represents the change in the outstanding amount of deferred tax assets from 47.5 billion yen(*2)

as of end-March 2014 to 40.7 billion yen as of end-March 2015

The Bank has been categorized under the ‘proviso of Category No.4 of the judgment guidelines on the realizability of deferred tax assets’

(*1) After deducting deferred tax liabilities of 0.4 billion yen(*2) After deducting deferred tax liabilities of 0.2 billion yen

� Income taxes deferred were a net expense of 6.8 billion yen compared with a net expense of 7.1 billion yen in FY2013 � Income taxes deferred were a net reversal of 5.4 billion yen in the fourth quarter, mainly as a result of

the estimation of taxable losses incurred in previous years as future deductible temporary differences� A net tax expense of approximately 3.9 billion yen was recognized due to a reduction in the corporate

tax rate

ⅦⅦⅦⅦ. Reference : Deferred Tax Assets (Non-consolidated basis)

34

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

@ 1,000

@ 600

Total 1,528 -

24

215

June 2022

June 2022

Conversion price(yen)

200

450

Mandatoryconversion

Current number of commonshares equivalent(million shares)

120

Per share paid-in amount (yen)

Number of shares (million)

286

-- 406

Total paid-in amount (100 million yen)

5th preferred shares 1,287

4th preferred shares 241

(as of end-Mar. 2015)

35

Remaining amount of public funds : 163.9 billion ye n (as of end-Mar. 2015)

Based on the Comprehensive Recapitalization Plan, each June the Bank will make an annual installment repayment of public funds through a super preferred dividend of 20.49 billion yen

<<<<Reference >>>>

� Common shares

� Preferred shares (Public funds)

1,650

-484

1,166

Number of shares issued

Treasury stock

Number of shares(million shares)

Shares outstanding (After deduction of treasury stock)

Common shares

(as of end-Mar. 2015)

ⅦⅦⅦⅦ. Reference : Share Status

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

FY2012Results

FY2013Results

FY2014Results

Net interest margin 1.07% 1.09% 1.21%

Non-interest income ratio 46% 46% 46%

Overhead ratio (OHR) 45.8% 45.8% *1 43.3%

Credit cost ratio 0.09% 0.09% - *2

Retail funding ratio 65% 64% 64%

ROE 7.1% 8.0% 8.1%

ROA 0.8% 0.9% 0.9%

*1 Based on business-related revenue, including gains on the sale of domestic equity ETFs*2 Credit-related expenses were a net reversal in FY2014

ⅦⅦⅦⅦ. Reference : Mid-term KPIs

36

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved. 37

Q&A Session

FY2014 Financial Results

Early and Full Repayment of Public Funds; New Mid-Term Plan

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

Appendix

38

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

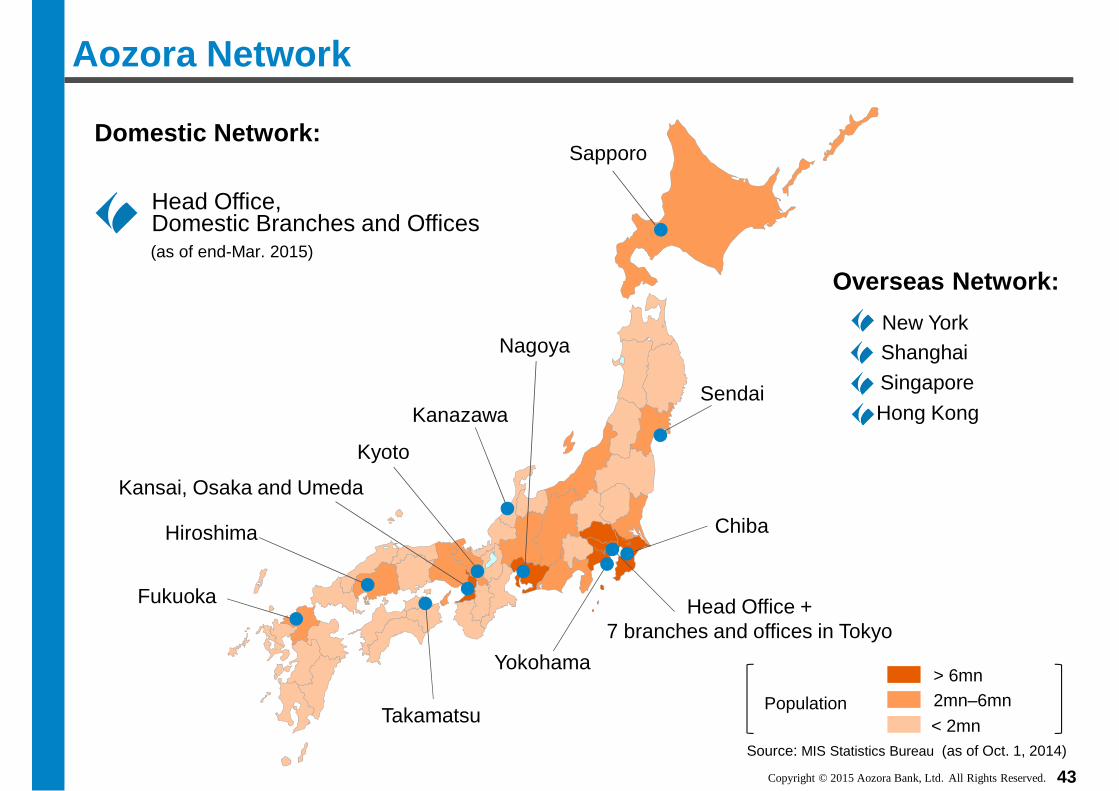

� Headquarters: Chiyoda-ku, Tokyo

� Total Assets: JPY 4,924.5bn

� Credit Ratings: A- / A- / A- / Baa2 (S&P / R&I / JCR / Moody’s)

� Office Network:

� Domestic: 21 offices nationwide� Overseas: New York, Shanghai,

Singapore, Hong Kong

� Major Subsidiaries:

�Aozora Trust Bank, Ltd.

�Aozora Loan Services Co., Ltd.

�Aozora Securities Co., Ltd.

�Aozora Regional Consulting Co., Ltd.

�Aozora Investment Management Co., Ltd.

�Aozora Real Estate Investment Advisors Co., Ltd.

�Aozora Asia Pacific Finance Limited

� Full-time Employees: 1,661

(as of end-Mar. 2015)

� History� Franchise

� 1957: Established as The Nippon Fudosan Bank,Limited

� 1977: Changed name to The Nippon CreditBank, Ltd.

� 1998: Temporarily nationalized

� 2000: Re-privatized

� 2001: Changed name to Aozora Bank, Ltd.

� 2003: Through a common stock tender offer,Cerberus group became the largest shareholder

� 2006: Listed on the First Section of the TokyoStock Exchange

� 2012: Announced ComprehensiveRecapitalization Plan

� 2013: Major shareholder Cerberus group sold itsAozora common shares

Aozora at a Glance

39

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

〔1,166〕 〔1,166〕〔1,166〕〔1,496〕

346 (30%)

524 (45%)

272 (23%)

24 (2%)

293 (25%)

481 (41%)

265 (23%)

97 (8%)

31 (3%)

277 (24%)

518 (44%)

352 (30%)

20 (2%)

104 (7%)

313 (21%)

243 (16%)

821 (55%)

15 (1%)

52,761 64,50832,017 57,908

Shareholder Composition

Unit: Million shares% shows ratio of voting rights

No. of shares outstanding, excl. Treasury stock

# of retailshareholders

40

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

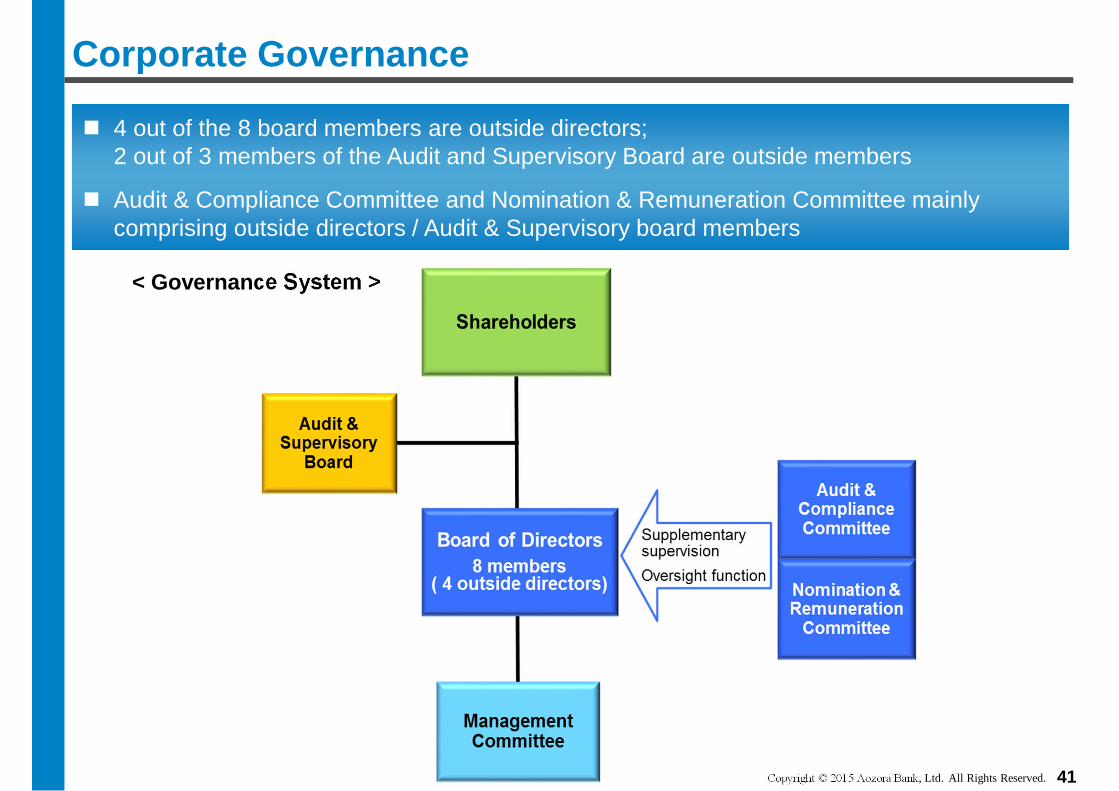

� 4 out of the 8 board members are outside directors; 2 out of 3 members of the Audit and Supervisory Board are outside members

� Audit & Compliance Committee and Nomination & Remuneration Committee mainly comprising outside directors / Audit & Supervisory board members

Corporate Governance

< Governance System >

41

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

Management Team

� Makoto Fukuda Director and ChairmanFormer Deputy Chairman and Senior Managing Director of the Regional Banks Association of Japan

� Shinsuke Baba Representative Director, President and CEO Appointed Representative Director and Deputy President in 2009 and Representative Director, President and CEO in 2012

� Masaki Tanabe Representative Director, Deputy President and CFO Appointed CFO in 2008 and Representative Director and Deputy President in 2013

� Takeo Saito Director, Senior Managing Executive Officer, CRO and CCRO Appointed MEO, Head of Financial Markets Group, in 2013. SMEO, CRO and CCRO in 2014

� Clark D. Graninger MEO, Head of Retail Banking Group

� Katsuya Hosono MEO, Head of Corporate Banking Group

� Kei Tanikawa MEO, Head of Allied Banking Group

� Koji Yamakoshi EO, Head of Specialty Finance Group (Real Estate Finance and Domestic Business)

� Keiichi Asada EO, Head of Business Banking Group

� Masayoshi Ohara EO, Head of Financial Markets Group

� Hideaki Kuraishi EO, Head of International Finance Group (International)

� Masaki Yamagata SMEO, Corporate Strategy Officer and Head of Compliance & Governance

� Masatatsu Ozeki MEO, CTO

� Jorge A. Leon EO

� Tomomi Akutagawa EO, Deputy CFO

� Masaaki Harada EO, Head of Human Resources

� Yukio Sekizawa EO, Deputy CTO

� Fumihiko Hirose EO, Deputy CCRO

42

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

> 6mn2mn–6mnPopulation< 2mn

Source: MIS Statistics Bureau (as of Oct. 1, 2014)

Sapporo

Sendai

Head Office +7 branches and offices in Tokyo

Fukuoka

Hiroshima

Kansai, Osaka and Umeda

Kyoto

Kanazawa

Nagoya

Takamatsu

Yokohama

Chiba

Head Office, Domestic Branches and Offices

Domestic Network:

(as of end-Mar. 2015)

Aozora Network

Overseas Network:

New YorkShanghai

Singapore

Hong Kong

43

Copyright © 2015 Aozora Bank, Ltd.All Rights Reserved.

This presentation contains forward-looking statements regarding the Bank’s financial condition and results of operations. These forward-looking statements, which include the Bank’s views and assumptions with respect to future events, involve certain risks and uncertainties. Actual results may differ from forecasts due to changes in economic conditions and other factors including the effects of changes in general economic conditions, changes in interest rates, stock markets and foreign currency, and any ensuing decline in the value of our securities portfolio, incurrence of significant credit-related cost and the effectiveness of our operational, legal and other risk management policies

< Inquiries >

AOZORA BANK, LTD.

Corporate Communication Division

TEL: 03-5212-9253

FAX: 03-3239-8065

URL: http://www.aozorabank.co.jp/english/

Mr. Hiroyuki Kajitani [email protected]

Ms. Junko Matsumoto [email protected]

Mr. Yasunari Shimizu [email protected]

Mr. Sohei Ito [email protected]

Ms. Yasuko Fukai [email protected]