aplma news - sc lowy news issue no. 55 winter ... project finance michael thorpe commonwealth bank...

TRANSCRIPT

APLMA NewsIssue No. 55 Winter 2014

Follow the latest updates and information at https://www.aplma.com

Features

Contents:

Page

APLMA Events Calendar 2015 5

APLMA Indonesian Loan

Market Seminar 8

APLMA Indian Loan

Market Conference 10

Member News 12

APLMA Singapore Christmas Party 14

APLMA WILMA Series: Diversity in the

Workplace 16

APLMA WILMA Christmas lunch talk 17

APLMA Hong Kong Young Leaders

Christmas Party 21

APLMA Secondary Loan

Market Seminar 22

APLMA Asia Pacifi c Syndicated Loan

Market Outlook Roundtable 30

APLMA Philippines Loan Market

Conference 38

APLMA Hong Kong Christmas Party 44

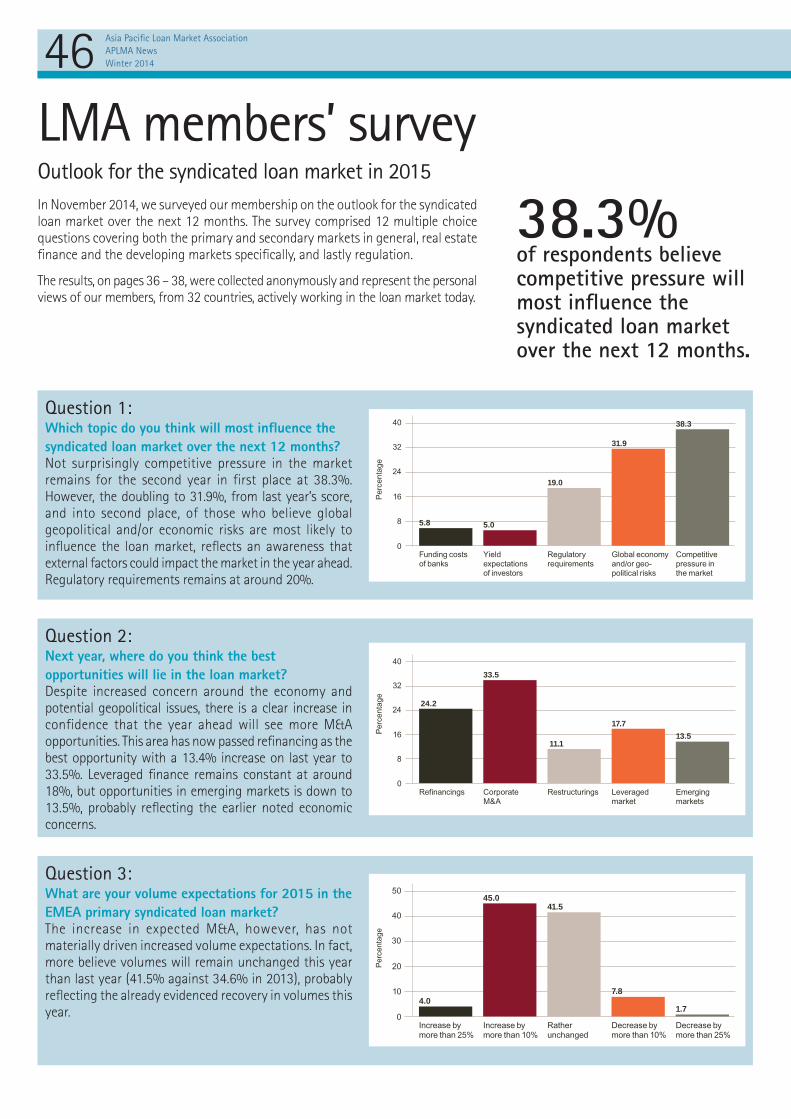

LMA members’ survey 46

Dealogic Asia Pacifi c market wrapPage 3

Outlook for the secondary marketPage 23

Syndicated Lending in Taiwan: opportunity amidst challengesPage 28

A Word from the Managing Director

Happy New YearThe APLMA ended 2014 on a high note. It was a full and active year with

over 80 events and a record 258 members. Our Documentation and Agency

Committees rolled out multiple new and revised documents as well as

guidance notes which are all now available on the APLMA web site. We also

launched our new web site with a host of new and improved features. The

APLMA would like to thank its Board, ExCo and Committee members for

helping to make 2014 our best year ever.

Membership Renewals 2014As we continue to increase the number of events and roll out new documentation, membership of the APLMA

is of even greater benefi t to members, and we hope that all members will renew their subscriptions so that

we can continue to represent the loan market.

Membership fees were due on 1 January, 2015. So please ensure that you pay your membership dues

on time. For enquiries, please contact: [email protected].

APLMA Awards / Global Loan Market SummitVoting for the APLMA Awards closes on 15 January. Winners will be announced at the 4th APLMA Awards

Dinner on 3 February, 2015. There are only a few tables left so please book early to avoid disappointment.

For reservations, please contact: [email protected]. The 4th Annual Global Loan Market Summit will

be held in association with the LMA and the LSTA on 3-4 February, 2015.

Finally, the APLMA would like to take this opportunity to wish all members a very Happy and Prosperous

2015.

Janet FieldManaging Director

Janet Field

Asia Pacifi c loan market –outlook for 2015Page 32

Banks & Borrowers review opportunities in the PhilippinesPage 40

02Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

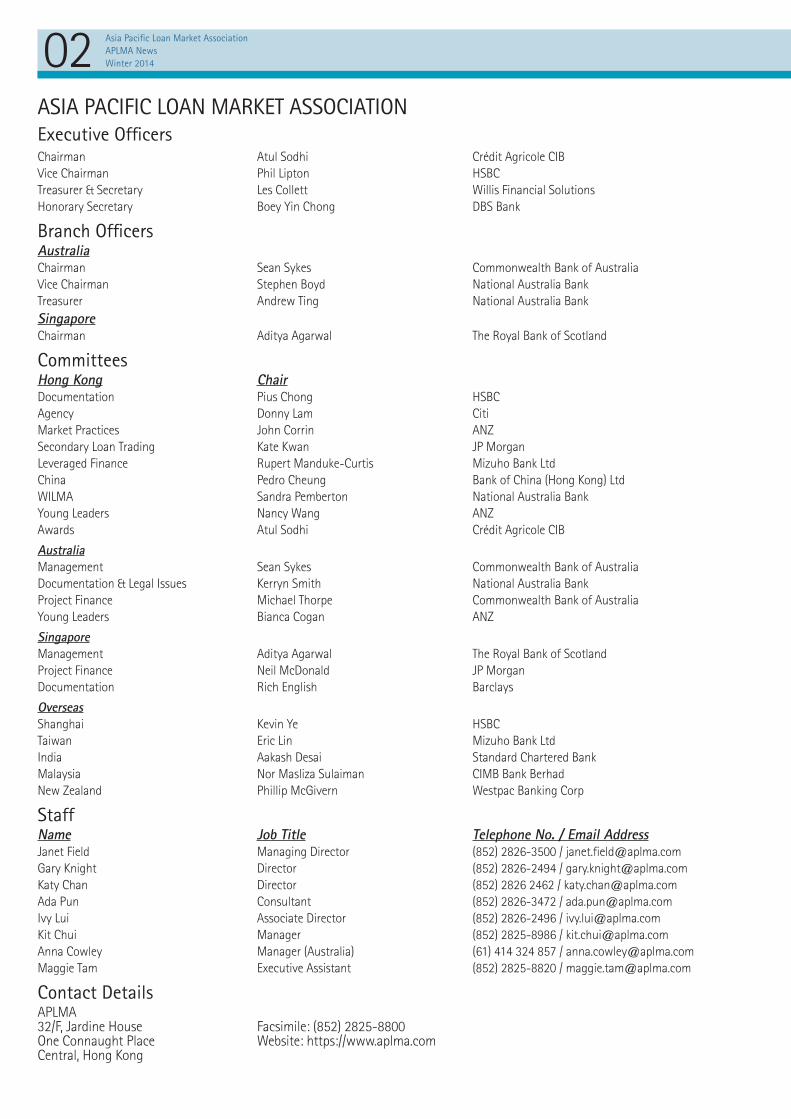

ASIA PACIFIC LOAN MARKET ASSOCIATIONExecutive Offi cersChairman Atul Sodhi Crédit Agricole CIB

Vice Chairman Phil Lipton HSBC

Treasurer & Secretary Les Collett Willis Financial Solutions

Honorary Secretary Boey Yin Chong DBS Bank

Branch Offi cersAustraliaChairman Sean Sykes Commonwealth Bank of Australia

Vice Chairman Stephen Boyd National Australia Bank

Treasurer Andrew Ting National Australia Bank

SingaporeChairman Aditya Agarwal The Royal Bank of Scotland

CommitteesHong Kong ChairDocumentation Pius Chong HSBC

Agency Donny Lam Citi

Market Practices John Corrin ANZ

Secondary Loan Trading Kate Kwan JP Morgan

Leveraged Finance Rupert Manduke-Curtis Mizuho Bank Ltd

China Pedro Cheung Bank of China (Hong Kong) Ltd

WILMA Sandra Pemberton National Australia Bank

Young Leaders Nancy Wang ANZ

Awards Atul Sodhi Crédit Agricole CIB

Australia

Management Sean Sykes Commonwealth Bank of Australia

Documentation & Legal Issues Kerryn Smith National Australia Bank

Project Finance Michael Thorpe Commonwealth Bank of Australia

Young Leaders Bianca Cogan ANZ

Singapore

Management Aditya Agarwal The Royal Bank of Scotland

Project Finance Neil McDonald JP Morgan

Documentation Rich English Barclays

Overseas

Shanghai Kevin Ye HSBC

Taiwan Eric Lin Mizuho Bank Ltd

India Aakash Desai Standard Chartered Bank

Malaysia Nor Masliza Sulaiman CIMB Bank Berhad

New Zealand Phillip McGivern Westpac Banking Corp

StaffName Job Title Telephone No. / Email AddressJanet Field Managing Director (852) 2826-3500 / janet.fi [email protected]

Gary Knight Director (852) 2826-2494 / [email protected]

Katy Chan Director (852) 2826 2462 / [email protected]

Ada Pun Consultant (852) 2826-3472 / [email protected]

Ivy Lui Associate Director (852) 2826-2496 / [email protected]

Kit Chui Manager (852) 2825-8986 / [email protected]

Anna Cowley Manager (Australia) (61) 414 324 857 / [email protected]

Maggie Tam Executive Assistant (852) 2825-8820 / [email protected]

Contact DetailsAPLMA32/F, Jardine House Facsimile: (852) 2825-8800One Connaught Place Website: https://www.aplma.com Central, Hong Kong

03Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

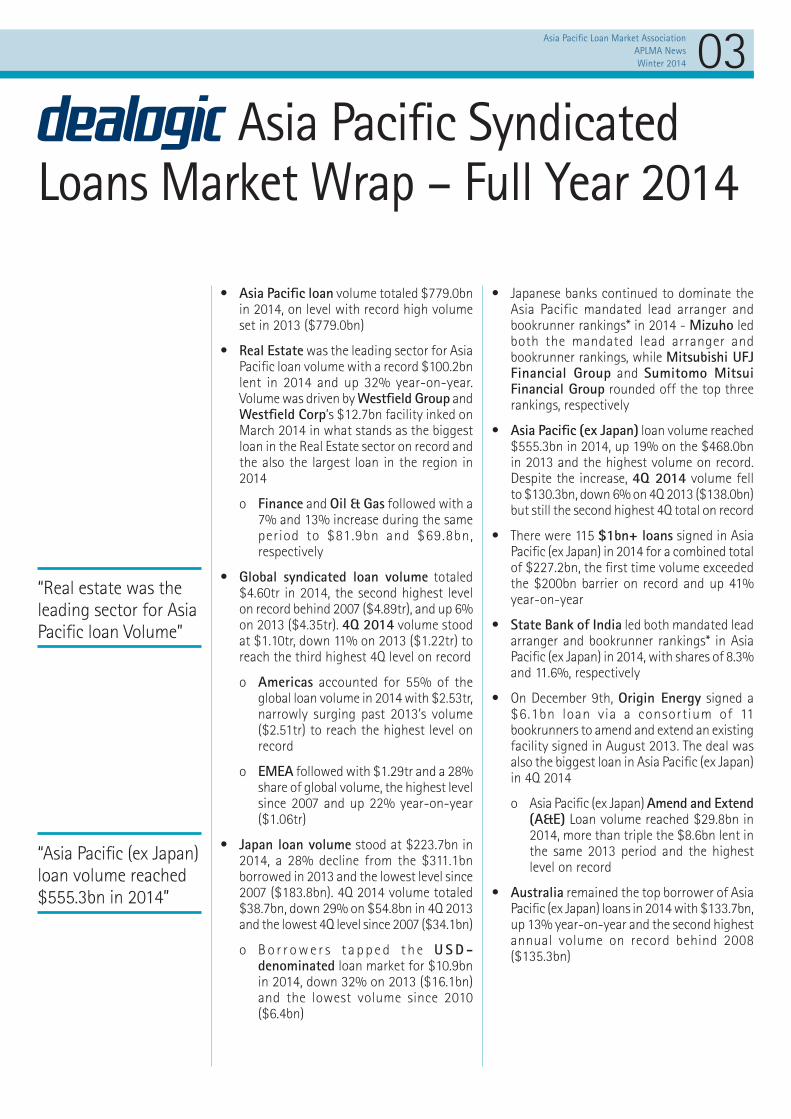

Asia Pacifi c Syndicated Loans Market Wrap – Full Year 2014

• Asia Pacifi c loan volume totaled $779.0bn in 2014, on level with record high volume set in 2013 ($779.0bn)

• Real Estate was the leading sector for Asia Pacifi c loan volume with a record $100.2bn lent in 2014 and up 32% year-on-year. Volume was driven by Westfi eld Group and Westfi eld Corp’s $12.7bn facility inked on March 2014 in what stands as the biggest loan in the Real Estate sector on record and the also the largest loan in the region in 2014

o Finance and Oil & Gas followed with a 7% and 13% increase during the same period to $81.9bn and $69.8bn, respectively

• Global syndicated loan volume totaled $4.60tr in 2014, the second highest level on record behind 2007 ($4.89tr), and up 6% on 2013 ($4.35tr). 4Q 2014 volume stood at $1.10tr, down 11% on 2013 ($1.22tr) to reach the third highest 4Q level on record

o Americas accounted for 55% of the global loan volume in 2014 with $2.53tr, narrowly surging past 2013’s volume ($2.51tr) to reach the highest level on record

o EMEA followed with $1.29tr and a 28% share of global volume, the highest level since 2007 and up 22% year-on-year ($1.06tr)

• Japan loan volume stood at $223.7bn in 2014, a 28% decline from the $311.1bn borrowed in 2013 and the lowest level since 2007 ($183.8bn). 4Q 2014 volume totaled $38.7bn, down 29% on $54.8bn in 4Q 2013 and the lowest 4Q level since 2007 ($34.1bn)

o B o r r o w e r s t a p p e d t h e U S D -denominated loan market for $10.9bn in 2014, down 32% on 2013 ($16.1bn) and the lowest volume since 2010 ($6.4bn)

• Japanese banks continued to dominate the Asia Pacific mandated lead arranger and bookrunner rankings* in 2014 - Mizuho led both the mandated lead arranger and bookrunner rankings, while Mitsubishi UFJ Financial Group and Sumitomo Mitsui Financial Group rounded off the top three rankings, respectively

• Asia Pacifi c (ex Japan) loan volume reached $555.3bn in 2014, up 19% on the $468.0bn in 2013 and the highest volume on record. Despite the increase, 4Q 2014 volume fell to $130.3bn, down 6% on 4Q 2013 ($138.0bn) but still the second highest 4Q total on record

• There were 115 $1bn+ loans signed in Asia Pacifi c (ex Japan) in 2014 for a combined total of $227.2bn, the fi rst time volume exceeded the $200bn barrier on record and up 41% year-on-year

• State Bank of India led both mandated lead arranger and bookrunner rankings* in Asia Pacifi c (ex Japan) in 2014, with shares of 8.3% and 11.6%, respectively

• On December 9th, Origin Energy signed a $6.1bn loan via a consortium of 11 bookrunners to amend and extend an existing facility signed in August 2013. The deal was also the biggest loan in Asia Pacifi c (ex Japan) in 4Q 2014

o Asia Pacifi c (ex Japan) Amend and Extend (A&E) Loan volume reached $29.8bn in 2014, more than triple the $8.6bn lent in the same 2013 period and the highest level on record

• Australia remained the top borrower of Asia Pacifi c (ex Japan) loans in 2014 with $133.7bn, up 13% year-on-year and the second highest annual volume on record behind 2008 ($135.3bn)

“Real estate was the leading sector for Asia Pacifi c loan Volume”

“Asia Pacifi c (ex Japan) loan volume reached $555.3bn in 2014”

04Asia Pacifi c Loan Market Association

APLMA News

Winter 201404Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

• Southeast Asian borrowers tapped the loan volume for a combined total of $119.5bn in 2014, up 38% on 2013 ($86.6bn) and the highest volume on record. Deal activity, however, dropped to 247 deals in 2014, down from 295 deals in 2013 and the fi rst year-on-year decrease since 2009 (168 deals)

o 2H 2014 volume of $59.1bn was up 49% compared to the same 2013 period ($39.7bn) and the highest 2H volume on record. Marina Bay Sands Ptd Ltd completed a $4.1bn loan facility in August 2014 in what is the largest facility completed in the region in 2H 2014

• Singapore loan volume totaled $60.6bn in 2014, surpassing the previous annual record set in 2011 ($36.7bn) and up 71% on the $35.5bn lent in 2013

• Asia Pacifi c (ex Japan) club loans reached $216.4bn in 2014, the highest annual volume on record and up 24% from $174.5bn in 2013. Average deal size reached the highest level on record with $461m

• Asia Pacific (ex Japan) Loans in Local Currencies reached $327.4bn in 2014, up 26% from $260.4bn in 2013 and the highest volume on record. HKD ($39.7bn), NZD ($20.0bn) and PHP ($1.2bn) denominated borrowing all reached new full year record highs

o Similarly, G3-currency denominated loans totaled $221.4bn in 2014, an increase of 8% on the 2013 ($205.8bn). Notably Euro-denominated loan volume was up for the second consecutive year to $7.8bn

• Asia Pacifi c (ex Japan) Acquisition-related loan** reached $73.2bn in 2014, the second highest volume on record behind 2007 ($101.4bn)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014

Deal Value $ (m) No.

* Please note that bookrunner market share is a proportion of bookrunner-led loan volume only** Includes acquisitions, future acquisitions, spin-offs and LBOs

“Asia Pacifi c (ex Japan) club loans reached $216.4bn”

05Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

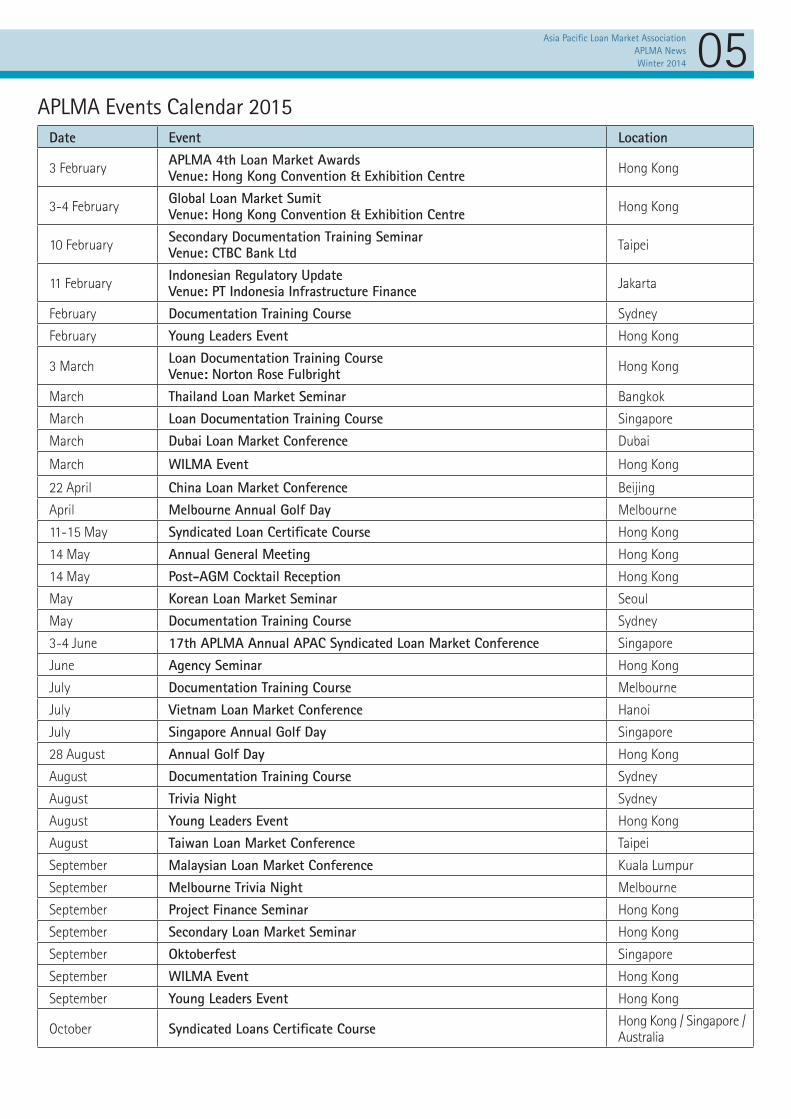

APLMA Events Calendar 2015

Date Event Location

3 FebruaryAPLMA 4th Loan Market AwardsVenue: Hong Kong Convention & Exhibition Centre

Hong Kong

3-4 FebruaryGlobal Loan Market SumitVenue: Hong Kong Convention & Exhibition Centre

Hong Kong

10 FebruarySecondary Documentation Training SeminarVenue: CTBC Bank Ltd

Taipei

11 FebruaryIndonesian Regulatory UpdateVenue: PT Indonesia Infrastructure Finance

Jakarta

February Documentation Training Course Sydney

February Young Leaders Event Hong Kong

3 MarchLoan Documentation Training CourseVenue: Norton Rose Fulbright

Hong Kong

March Thailand Loan Market Seminar Bangkok

March Loan Documentation Training Course Singapore

March Dubai Loan Market Conference Dubai

March WILMA Event Hong Kong

22 April China Loan Market Conference Beijing

April Melbourne Annual Golf Day Melbourne

11-15 May Syndicated Loan Certifi cate Course Hong Kong

14 May Annual General Meeting Hong Kong

14 May Post-AGM Cocktail Reception Hong Kong

May Korean Loan Market Seminar Seoul

May Documentation Training Course Sydney

3-4 June 17th APLMA Annual APAC Syndicated Loan Market Conference Singapore

June Agency Seminar Hong Kong

July Documentation Training Course Melbourne

July Vietnam Loan Market Conference Hanoi

July Singapore Annual Golf Day Singapore

28 August Annual Golf Day Hong Kong

August Documentation Training Course Sydney

August Trivia Night Sydney

August Young Leaders Event Hong Kong

August Taiwan Loan Market Conference Taipei

September Malaysian Loan Market Conference Kuala Lumpur

September Melbourne Trivia Night Melbourne

September Project Finance Seminar Hong Kong

September Secondary Loan Market Seminar Hong Kong

September Oktoberfest Singapore

September WILMA Event Hong Kong

September Young Leaders Event Hong Kong

October Syndicated Loans Certifi cate CourseHong Kong / Singapore / Australia

APLMA 4th Loan Market Awards The APLMA 4th Loan Market Awards will be held on 3 February, 2015 at the Hong Kong Conven on and Exhibi on Centre, Hong Kong.

The APLMA Syndicated Loan Awards are the first Awards that could be deemed to be truly judged by the market, offering a level playing field for key market prac oners to have their deals recognised by their peers based on merit alone.

Vo ng will take place in December and January and we will be using the Bloomberg League Tables as an aide memoire. Detailed informa on is available on the APLMA website .

Special thanks to the Media Partner:

07Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Date Event Location

October Sydney Annual Golf Day Sydney

October Indian Loan Market Conference Mumbai

October Loan Documentation Training Course Hong Kong

October Loan Documentation Training Course Singapore

November Philippines Loan Market Seminar Manila

November Asia Pacifi c Syndicated Loan Market Outlook Roundtable Hong Kong

November Melbourne End of Year Networking Event Melbourne

November SEA Loan Market Seminar Singapore

November Young Leaders Event Hong Kong

November / December

Australian Branch Christmas Party Sydney / Melbourne

December Singapore Branch Christmas Party Singapore

December Hong Kong Branch Christmas Party Hong Kong

Full details of all APLMA events, including Programmes and online registration, can be found on the APLMA website (http://www.aplma.com), under the Events section on the homepage.

To Register Online:

– Log on to the APLMA website (www.aplma.com) with your login name and password;

– Select the event that you would like to attend;

– Click on ‘register’;

– Click on ‘submit’.

NB: If you do not receive an automatic “Registration Confi rmation” you need to re-register

CPT Points - Frequently Asked Questions

1. How do I get CPT points for attending an APLMA seminar or conference? The APLMA issues CPT certifi cates for many of its seminars and conferences. In order to be eligible for CPT points, Members

are required to comply with the following procedures:

i) Sign in:– A CPT attendee list in alphabetical order by company is available on the Registration Desk at all eligible APLMA events;

– Attendees who require CPT points are required to sign in against their name indicating their time of arrival;

ii) Attend the seminar / conference in full:– In order to be eligible for CPT points a Member is required to attend the seminar / conference for the full duration of

the event;

– Members who leave the event before the end or who have to leave early will NOT be eligible for CPT points.

iii) Sign out: – At the end of each seminar / conference, Members are required to sign out indicating their time of departure.

2. What if I forget to sign out?– Members who sign in but forget to sign out will NOT be eligible for CPT points;

– The APLMA regrets that CPT points cannot be issued to any members who forget to sign out. Please note that requests

for CPT points by Members who forget to sign out will be declined.

3. What if I have to leave early? Can I sign out before the conference ends?– Members who leave early will NOT be eligible for CPT points.

– The APLMA regrets that CPT points cannot be issued to any members who leave early. Please note that requests for CPT

points by Members who leave the event before the end will be declined.

08Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Ronny (Sponsor: ANZ)

Ari Soerono (Indonesia Infrastructure Finance)

Edimon Ginting (Asian Development Bank)

Janet Field (APLMA)

Birendra Baid (Deutsche Bank), Boey Yin Chong (DBS), Ashish Sharma (Credit Suisse), Carl Roberts (Sponsor: ANZ), David Sumual (PT Bank Central Asia)

APLMA Indonesian Loan Market SeminarOver 160 members attended the APLMA Indonesian Loan Market Seminar on 9 October, 2014. Speaker presentations are now available on the APLMA web site. Special thanks to sponsors: ANZ and Thomson Reuters.

Birendra Baid (Deutsche Bank), Boey Yin Chong (DBS), Ashish Sharma (Credit Suisse)

Ashish Sharma (Credit Suisse), Carl Roberts (Sponsor: ANZ), David Sumual (PT Bank Central Asia)

Over 160 members attended

09Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

John Corrin (Sponsor: ANZ), Hugeng Gozali (Astra Sedaya Finance), Ashish Saboo (CT Corpora)

Hugeng Gozali (Astra Sedaya Finance), Ashish Saboo (CT Corpora), Anne Patricia Sutanto (PT Pan Brothers Tbk), David Tendian (Adaro Group)

Janet Field (APLMA), Sevianto Nismara (CTBC), Kai Weng Yip (Maybank)

John Corrin (Sponsor: ANZ), Hugeng Gozali (Astra Sedaya Finance), Ashish Saboo (CT Corpora), Anne Patricia Sutanto (PT Pan Brothers Tbk), David Tendian (Adaro Group)

Amerta Mardjono (Wells Fargo), Oswald Tambunan (Bank Negara Indonesia)

APLMA Indonesian Loan Market Seminar

Jessica Teo (Maybank), San Sany Hakim (Standard Chartered), May Ching Lim (Maybank), Kai Weng Yip (Maybank), Joy Li (Standard Chartered)

Donda Hutabarat (Indonesia Eximbank), Adam Hardani (Indonesia Eximbank), Wilsa Arini (Indonesia Eximbank), Mekar Maulina (Indonesia Eximbank)

Ashish Saboo (CT Corpora), Amit Khattar (Deutsche), Birendra Baid (Deutsche), Parag Ranade (VTB Capital)

10Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Rajeev Arora (State Bank of India)

Aditi Nayar (ICRA), Harsha Subramaniam (Sponsor: Bloomberg), Samiran Chakraborty (Standard Chartered)

Atul Sodhi (CACIB), Niraj Shah (ANZ), S M Sundaresan (Standard Chartered), Rahul Shukla (Citi), Brijesh Mehra (RBS)

Janet Field (APLMA)

S M Sundaresan (Standard Chartered), Rahul Shukla (Citi)

APLMA Indian Loan Market ConferenceOver 160 delegates attended the APLMA Indian Loan Market Conference on 29 October, 2014. Speaker presentations are now available on the APLMA web site. The conference focused on trends and opportunities in the Indian loan market. Special thanks to sponsors: Herbert Smith Freehills and Bloomberg.

Atul Sodhi (CACIB), Niraj Shah (ANZ)

Soumya Rao (Sponsor: Herbert Smith Freehills), Siddhartha Sivaramakrishnan (Sponsor: Herbert Smith Freehills), Alexander Aitken (Sponsor: Herbert Smith Freehills)

Nathan Nelson (EDC)

11Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Sanjay Ratra (Standard Chartered)

Yogesh Venkatachalam (ANZ), Aakash Desai (Standard Chartered), Birendra Baid (Deutsche)

Ashish Garg (Vedanta Resources), Vipul Chandra (Larssen & Toubro), Raghav Sud (Tata Steel), Sameer Chandra (Citi)

Aditya Agarwal (RBS), Yogesh Venkatachalam (ANZ), Aakash Desai (Standard Chartered), Birendra Baid (Deutsche), Pankaj Agarwal (DBS)

Vipul Chandra (Larssen & Toubro)

APLMA Indian Loan Market Conference

Vipul Chandra (Larssen & Toubro), Raghav Sud (Tata Steel)

Janet Field (APLMA), Veena Sivaramakrishnan (Juris Corp) Gaurav Shukla (Standard Chartered), Niloufer Lam (Amarchand & Mangaldas & Suresh A. Shroff & Co.), Sonali Mahapatra (Talwar Thakore & Associates)

12Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Member News

APLMA News

APLMA staff changes

The APLMA welcomed Maggie Tam on 3 November, 2014 as a new Executive Assistant – Events. Maggie joins

from Rococco and has many years experience of event organisation and hospitality. Maggie can be contacted

on: [email protected].

The APLMA is also pleased to announce the promotion of Ivy Lui to Associate Director and Kit Chui to Manager.

Membership renewals

Membership renewals for 2015 were due on 1 January, 2015, Renewal notices were sent to all members in

November.

If you have not yet renewed your APLMA membership please do so as soon as possible. Members who have

not yet renewed will not be able to access the APLMA web site for standard documentation and event

registration until their accounts have been settled. Please settle early to avoid disappointment.

New Members

The APLMA warmly welcomes the following new Members who recently joined:

• Chong Hing Bank Limited – Associate

• Hastings & Co – Associate

• Miller Insurance Services LLP – Associate

• Prudential Capital (Singapore) Pte Ltd – Associate

• ICRA Limited – Single Centre

• PT Indonesia Infrastructure Finance – Single Centre

Branch News

Australian Branch celebrates 15th anniversary

2014 was another busy year for the APLMA in Australia. We held over 20 events, courses and seminars for

our members, all of which have been tremendously supported.

Australian Branch celebrated its 15th anniversary which is a great achievement, refl ecting the collective efforts

of so many over this time. To commemorate our birthday, we set aside September for formal recognition of

this milestone, with two events which were great successes. The fi rst of these was the Borrower Update, at

which we had a panel of our lead syndicators provide their perspectives on the main trends in debt markets

and their thoughts on the outlook for the market. Within the attendance of over 200 people we also had over

60 representatives from our client base who attended to hear the perspectives of our panel and to enjoy a

relaxed cocktail party after.

The next night we held our 15 year birthday party at which approximately 300 members and partners attended to celebrate the

achievements of APLMA Australia. To have over 500 people attend these events was tremendously satisfying for our Branch and a

fi tting way to celebrate our milestone. I would like to thank everyone involved with organising our 15 year birthday events.

Australian committee news

Our Documentation Sub-Committee has had a very busy year and made great progress on updating the APLMA Australia standard

documentation. I would like to thank Kerryn Smith (Chairman) and his committee for all their efforts in progressing their agenda so

strongly over the year.

Sean Sykes

Maggie Tam

Ivy Lui

Kit Chui

13Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Our Young Leaders Sub-Committee has again had an outstanding year holding several events in Sydney and Melbourne. The level of

support from members for their events is particularly gratifying. I would like to offer special thanks to Bianca Cogan from ANZ who

has done a great job as Chair over the past year and also to all committee members as the number and quality of events they have

staged has been outstanding. Bianca will be passing the reigns to Grazia Zappia from CBA, to continue the great momentum our

Young Leaders have established. Congratulations to Bianca and Grazia.

Our Project Finance Sub-Committee has also maintained good momentum over the year with the PF Three Cities Seminar a particular

highlight. Thanks to Norm Heavener for his efforts as Chairman and also to the members of their committee.

Management Committee changes

I would also like to acknowledge two people who have been outstanding servants for the APLMA here in Australia and to the APLMA

generally. Firstly Wayne Green, Head of Loan Capital Markets Australia for BNP Paribas, a founding Director of APLMA Australia and

a past Chairman for four years will be moving to Hong Kong to take up a role as Head of Syndication, Asia for BNP Paribas. Wayne

has been a wonderful contributor to APLMA Australia over the last 15 years and we wish him all the very best with his move to Hong

Kong. Similarly Gavin Chappell from Westpac, is taking up a new role heading Structured Asset Finance for Westpac in Australia. Gavin

is also a long standing committee member of APLMA Australia and a Director of the APLMA and was a past Chairman for three years.

Gavin has been a great contributor also and on behalf of everyone I wish Gavin all the very best with his new role. A big thank you

from us to both Wayne and Gavin.

Year ahead

2015 will be another active year for the APLMA in Australia, with our usual number of high quality events, seminars and courses that

are always well supported by our members.

Finally I would like to thank all the members of Australian Branch Management Committee who continue to generously give their

time to serve the APLMA here in Australia. We are fortunate to have so many here who are such great advocates for our Association

and who freely contribute so willingly and positively to all of our events every year.

Wishing you all a great 2015.

Committee News

Australian Project Finance Committee

New chair

Norm Heavener, Head of Project Finance of Westpac, will be stepping down as

Chair of the Project Finance Committee in Australia in January. He will be

succeeded by Michael Thorpe, Managing Director, Project Finance of

Commonwealth Bank in January.

The APLMA would like to thank Norm for his enormous contributions to the

growth and development of this committee as the inaugural chairman. We look

forward to welcoming Michael as the new chair.

Hong Kong Documentation Committee

New documents

The Committee has completed the following new document templates which have been posted to the website

in Q4:

i) Mandate Letter for secured transactions (Hong Kong and English Law);

ii) Term Sheet for secured transactions (Hong Kong and English Law);

iii) Offshore RMB facility agreement (Hong Kong law). A user guide will be provided subsequently.

The Committee has also updated the Unsecured Mandate Letter and Unsecured Term Sheet (to include the

English law option in addition to Hong Kong law) and the APLMA Confi dentiality Letter (Hong Kong Law) for Primary Syndication

(Clean) to refect the change to the reference in the Companies Ordinance.

Norm Heavener Michael Thorpe

Pius Chong

14Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Aditya Shroff (Linklaters), Boey Yin Chong (DBS), Andrew Saw (Linklaters)

Over 120 members attended

Simon Lim (RBS), Sean Liu (UOB), Jesscia Teo (Maybank)

Aditya Agarwal (RBS)

Mike Williams (Westpac), Michael Downes (Babson Capital), Shane Forster (Babson Capital)

APLMA Singapore Christmas PartyOver 120 members attended the Singapore Branch Christmas Party on 27 November, 2014. This event provided an excellent opportunity to network.

Eugene Ooi (Allen & Gledhill LLP), Benny Cheong (Bank of Nova Scotia)

Lishi Fong (Norton Rose Fulbright), Andrew Koh (CCB) Atul Kawatra (Siemens Financial Services), Sujata Bhattacharjee (RBS)

15Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Documents in the pipeline

The Committee is currently working on the following documents which are targeted to be launched in early 2015:

i) Updated version of the Sample Asia Arbitration Clauses to take account of the changes to arbitration law in Hong Kong and China;

ii) Chinese translations of the Hong Kong Law Facility Agreement, Term Sheet and Confi dentiality Letter for primary syndication (NEW documents).

Update on FATCA

In January 2015, the APLMA released a FATCA Note for Agents operating in an IGA Model 2 jurisdiction (ie HK, Japan and Taiwan).

The note provides a sample provision which protects the Agent against any liability which might result from its failure to withhold on

account of FATCA which was caused by a Lender failing to provide accurate information about its FATCA status, or a US or FFI borrower

failing to correctly act on that information.

Agency Committee

Half day HIBOR fi xing

Due to the typhoon season, members have raised concerns about Agents’ duties in respect of the half Business

Day process, especially since the Hong Kong Banking Association is now also publishing HIBOR in the afternoon.

The half Business Day process has already been covered in the existing APLMA standard agreement. Unless

the Agent has obtained all parties’ approval to use the afternoon HIBOR, the APLMA standard agreement

states that the Agent shall obtain the rate from the Reference Banks if no HIBOR appears at 11:00 am Hong

Kong time. Also, as far as it is a Business Day and HKD clearing is working, whether it is a full or half day, the

payment must be settled as normal and if any party cannot arrange payment due to it being a half day, it

shall be treated as non-payment under the agreement. The APLMA will be issuing a new guideline on this in

early 2015.

Inaugural APLMA Agency Seminar

The APLMA will be hosting its fi rst Agency Seminar in 2015. Details will be posted on the APLMA web site in due course.

Shanghai Committee

New chair

Julia Wu of HSBC recently stepped down as Chair of the Shanghai

Committee and has been succeeded by Kevin Ye of HSBC as the

new Chair. The APLMA wishes to thank Julia for her contributions

to the growth and development of the APLMA’s activities in

China and warmly welcomes Kevin aboard.

Event programme

The APLMA Shanghai Committee met on 12 December. Katy Chan

(APLMA), Kevin Ye and members of the committee attended. The

members of the committee suggested preliminary topics and arrangements for the committee’s events and activities for 2015 including

strengthening relationships with local banking associations as a priority and conducting more documentation training on China specifi c

issues. The members also shared their preliminary ideas for the APLMA China Loan Conference.

New committee members

In the meantime, all members agreed to invite additional active market players (both foreign banks and Chinese banks) to join the

Committee so that the Committee can play a more important role in the China syndication community. Any Full members interested

in joining the committee should contact: [email protected].

Kevin Ye Shanghai Committee

Donny Lam

16Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Sophie Guerin (Community Business)

Angie Lau (Sponsor: Bloomberg)

Over 60 members attended

Janet Field (APLMA)

Janet Field (APLMA), Angie Lau (Sponsor: Bloomberg), Dorothy Chan (Sponsor: Bloomberg), Sophie Guerin (Community Business)

APLMA WILMA Series: Diversity in the WorkplaceOver 60 members attended the WILMA workshop on diversity in the workplace on 23 October, 2014. The speaker presentation is now available on the APLMA web site. Special thanks to venue sponsor: Bloomberg.

Lei Zhang (DBS), Katy Chan (APLMA), Janet Field (APLMA)

Katy O’Doherty (Simmons & Simmons), Louisa Ng (Simmons & Simmons)

Georgina Axon (Norton Rose Fulbright), Eleanor Miller (Norton Rose Fulbright)

17Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Over 50 members attended

Janice Gerber (City Style Image Consultants), Paloma Gerber

Martha Fernandez (BBVA) poses a question

Janet Field (APLMA)

Sandra Pemberton (NAB) gives a farewell speech

APLMA WILMA Christmas lunch talkOver 50 members attended the APLMA WILMA Christmas lunch talk on 25 November, 2014 and bid farewell to committee chair, Sandra Pemberton. The new chair will be announced at the next committee meeting.

Janice Gerber (City Style Image Consultants) presents a lucky draw prize to Catherine Lam (Bloomberg)

Kitty Leung (Bank of Nova Scotia), Sylvia Hung (ANZ), Cecily Fan (ANZ), Kate Kwan (JP Morgan)

Anita So (HSBC), Katrina Santos (HSBC)

18Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Malaysia Loan Market and Syndication 2014

The year on year growth of syndicated loan volume in Malaysia increased by 47.6%, with total volume of

USD18.40 billion in 2014 compared to USD12.47 billion in 2013. This volume growth is substantial when

benchmarked against the Malaysia year on year GDP growth of 5.6%-6.00%.

On the other hand, the number of deals completed decreased year on year. There were 29 completed deals in

2014 compared to 46 completed deals in 2013. This signifi es that larger transactions were accomplished in

2014 as compared to 2013.

Major deals concluded in 2014 include Sapura Kencana TMC Sdn Bhd (USD 5.5 billion), Battersea Phase 2 &

Phase 3 Holding Co Ltd (USD 2,176 million), Powertek Investment Holdings Sdn Bhd (USD 1,712 million), 1MDB

Energy Holdings Ltd (USD 975 million) and QSR Brands Bhd (USD 736 million).

WILMA

WILMA chair, Sandra Pemberton will be stepping down as committee in January to

take up a new role at National Australia Bank in Sydney.

The APLMA wishes to thank Sandra for her contributions to the committee and growing

the programme of WILMA events. Sandra’s successor will be announced at the next

committee meeting.

Secondary Loan Trading Committee

Events

The Secondary Loan Trading Committee held an APLMA Secondary Loan Market Conference on 15 October,

2014 sponsored by Clifford Chance. The conference included an “Overview of the Secondary Loan Market” by

Kate Kwan (JPMorgan), “Understanding Delayed Settlement / Buy In Sell Out / Information Sharing” by Dauwood

Malik and Andrew Hutchins of Clifford Chance, and a panel discussion on “Trends, Developments & Opportunities

for Growth” with Kate Kwan, JPMorgan as moderator, and Steve Lyons, SC Lowy, Kevin Tham, Merrill Lynch,

Joe Cheung, Standard Chartered, and Ronnie Mahal, HSBC as panellists.

To summarise, market players see most loan trading activity in countries such as Australia, Hong Kong and

the Middle East. Industries include shipping, aircraft, commodities, mining and mining-services. With Basel III

and portfolio management and control, we see more and more commercial banks coming out to manage their

portfolios by selling loan exposures. Coming into 2015, market participants see that the trend would be more or less in line with 2014

and are hopeful of seeing more secondary loan activity in the region.

Year ahead

The Committee plans to organise seminars in Taiwan and Singapore in 2015. Please stay tuned if you are interested in knowing more

about market developments and the legal aspects of the secondary loan market.

Young Leaders Committee Australia

The Committee was established for young professionals with up to fi ve years experience in banking and

fi nancial services in Australia.

Its prime objective is to provide networking, professional development and market knowledge events where

like-minded young professionals can draw from the expertise of more experienced professionals in the market.

Events include discussions of topical issues and themes, development and advice relating to career progression,

technical and leadership skills and of course networking opportunities.

Sandra Pemberton

Nor Masliza Sulaiman

Kate Kwan

Bianca Cogan

Grazia Zappia

19Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

The APLMA Young Leaders Australian Sub-Committee again had a successful year with 7 events run across Melbourne and Sydney in

2014. The energy, drive and commitment of the committee members have ensured that a new and relevant range of events were

brought to the broader association members.

We were very lucky this year to have a number of institutions sponsor events and a special thank you to Allens Linklaters, Ashurst,

King & Wood Mallesons, and Norton Rose Fulbright.

New Chair

I will be stepping down as chair in January and the committee is pleased to announce that Grazia Zappia will be the incoming Chair

for 2015. Congratulations Grazia. Further appointments on the committee will be released in the next Newsletter.

Finally, a huge thanks and congratulations need to go out to the hard work of the 2014 committee members, without whom we could

not have delivered on the objectives and events we had set out for the year:

Events:

Events held over the past year include:

i) Melbourne

– Networking Event – Lawn Bowls

– Different Debt Platforms and how they fi t into the market

– Lifecycle of a Private Equity deal

ii) Sydney

– Lifecycle of a Private Equity deal

– Development session on “How to give an effective presentation”

– Syndications Roundtable

– Networking Event – Amazing Race

Further information will be provided on events in 2015 and the Committee looks forward to seeing you at these events throughout

the year.

RBC Capital Markets partners with clients t create c se n in a is r an investing opportunities that deliver relevant and easura le outco es ith o ces in

countries we ocus on creating long ter relationships and providing superior service and execution to clients around the globe.

Contact us to discuss how we can assist you.

Execution and Distribution Built on Solid Foundations

o inic udsonInvestment Banking

im allamCorporate Banking

Enrico MassiDebt Capital Markets

rbccm.com

21Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Simon Leung (Taipei Fubon), Heather Lu (Taipei Fubon)

Nancy Wang (ANZ), Danielle Roman (Mourant Ozannes)

Lucas de Olaran (BAML), William Yuen (BAML), Alexandre Sieradzki (DZ Bank)

Over 60 members attended

Lan Feng (China CITIC Bank), Henry Ho (Mizuho), Ivan Cheung (BNP Paribas)

APLMA Hong Kong Young Leaders Christmas PartyOver 60 members attended the Young Leaders’ Christmas Party in Hong Kong on 10 December, 2014. This event provided an excellent opportunity to network with the leaders of the future.

Maureen Gao (CDB), Spring Cheung (CDB), Vivian Wang (CDB), Fang Wang (Kirkland & Ellis)

Clayton Chan (China Merchants Securities), Jinghong Weng (Natixis), Edward Chan (China Merchants Securities)

Alan Yeung (Maybank), Ka Ming Chan (Maybank), Sandeep Patnaik (Axis Bank)

22Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Steve Lyons (SC Lowy), Ronnie Mahal (HSBC), Kate Kwan (JP Morgan), Joe Cheung (Standard Chartered), Kevin Tham (BAML)

Dauwood Malik (Sponsor: Clifford Chance), Andrew Hutchins (Sponsor: Clifford Chance)

Steve Lyons (SC Lowy)

Janet Field (APLMA)

Ronnie Mahal (HSBC), Kate Kwan (JP Morgan)

APLMA Secondary Loan Market SeminarOver 120 members attended the APLMA Secondary Loan Market Seminar on 15 October, 2014. For highlights of this event, please refer

to page 23. Special thanks to venue sponsor: Clifford Chance.

Kevin Tham (BAML)

A full house of over 120 members Timothy Lee (Bank of China), Kate Kwan (JP Morgan), William Wong (RBS)

23Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Outlook for the secondary market

Kwan began by asking: What are the latest trends in Asian loan trading?

Tham: “It is a good question and a question we

often get asked. As everyone knows Asia is a

very episodic market. It is unlike other loan

markets where there is a steady universe of

assets that trade year-in and year-out.”

He said over the last couple of months “trades

due to the Eurozone crisis have fi zzled out”. But,

on the distressed side, he continued to see fl ows

from ‘large-cap situations’, particularly for

names like BrisConnections.

For par-loans he has seen greater balance-sheet

management of shipping names, particularly for

Korean, Japanese and Chinese credits. “Secured

loans trading at 85-90 cents have been

particularly active. And we have even seen

distressed names from Indonesia such as Berlian

Laju Tanker.” He saw the trend continuing as

“some banks – such as German banks – have

portfolios to dispose of”.

Mahal: “As a newcomer to Asia I have found it

very illiquid compared to the US and Europe.”

The APLMA held a Secondary Loan Market Conference on 15 October, 2014 in Hong Kong sponsored by Clifford Chance.

The programme began with Dr Kate Kwan, Executive Director and Head, Secondary Loan Sales Asia Pacifi c at JP Morgan in Hong Kong giving a short Secondary Loan Market Overview presentation.

This was followed by presentations from Dauwood Malik and Andrew Hutchins, both Partners at Clifford Chance. The topics were ‘Understanding Delayed Settlement’, ‘Buy In, Sell Out’ and ‘Information Sharing’.

The afternoon concluded with a panel discussion moderated by Kate Kwan on “Trends, Developments and Opportunities for Growth”.

Panellists were:

• Steve Lyons, COO, SC Lowy, Hong Kong

• Kevin Tham, Managing Director, Global Loans and Special Situations Group, Merrill Lynch (Asia Pacifi c) Ltd, Hong Kong

• Joe Cheung, Executive Director, Loan Syndicate & Distribution, Standard Chartered Bank, Hong Kong

• Ronnie Mahal, Head Trader Secondary Loan Trading, HSBC, Hong Kong

Kate Kwan

Steve Lyons

Kevin Tham

“This is a completely different challenge. What has

kept me busy is not really trading the HSBC

portfolio, but third-party trades. We have set up

a book for event-driven trades of some of the big

names that came out last year, such as Alibaba

and WH Group.”

HSBC has an active global loan trading group

which is headquartered in Europe. Talking to

clients globally is seen as an advantage for the

bank.

Although too late to get involved with much of

the distressed debt that has been traded in Asia,

HSBC has been “pretty busy in the Middle East. In

terms of origination the Middle Eastern market

was huge in 2008, with a lot of Asian banks

involved.”

Kwan then asked Lyons of SC Lowy about his fi rm’s view on the Middle East.

Lyons: “If you go back two or three years we had a

large Australian trading book which was active –

names such as Rivercity – but that has slid off over

the last two to three years.”

24Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Joe Cheung

Ronnie Mahal

“We have moved a lot of resources into the

Middle East. We trade from the Middle East

throughout Asia down to Australia. A lot of the

slack has been picked up by trades in the Middle

East.”

Kwan then focused on industry, noting that besides shipping, mining, and mining services companies are under pressure.

Tham thought that shipping – “particularly in

the container space” – will be an active sector.

“The decline in oil prices will likely mean LNG

tankers, VLCCs and similar classes will be

important for us. Also rig bonds and loans are

interesting in the sense that they are not really

Asian or regional – they are global assets.”

“Australia continues to have a lot of companies

focused on commodities which could present

opportunities, and some South African and

European banks have been running down their

commodity fi nancing books.”

“There are also the junior mining companies and

ancillary businesses that support them –

contractors, infrastructure providers, roads,

ports.”

He said some companies will capitalise on

weakening commodity prices, but that “quite a

few others will enter stress – if you have ten

companies each with US$250-300m of debt,

that gives you a couple of billion dollars to

trade.”

Moving away from the stressed sector, Kwan then asked Cheung of Standard Chartered Bank about opportunities for active primary loan arrangers in the secondary loan market.

Cheung: “Due to Basel III, banks have generally

been more disciplined in their approach to

pricing, fi nal hold, and management of their

credit exposure.” He sees the trend continuing:

“I think, going forward, with more stringent

application of Basel III there will be more

secondary opportunities in the next 12-18

months.”

His other area of focus is on the more lucrative

leveraged or acquisition fi nance transactions

like the recent deals for Alibaba, Focus Media,

Giant and WH Group: “Because these were well

over-subscribed in primary when deal size was

capped. The underlying demand saw asset holders

get scaled down signifi cantly, so we are seeing

banks bidding up the paper and looking for offers

to get more of the asset.”

Kwan then asked Mahal whether being a major player in the primary market helps on the secondary side.

Mahal: “It helps in the sense that I get a lot of

calls from banks asking what HSBC is selling. My

simple answer is usually that we are not selling

anything.”

“But we selectively look to trim exposure and I am

always happy to have a dialogue.”

“Compared with investment banks HSBC is not

an aggressive seller, but the dialogue allows me

to learn who is looking at what. By sharing

information this may help the primary team focus

on the right clients”. A reciprocal relationship with

his syndication team means they keep him

informed about clients and their preferences.

“What do I think about secondary market pricing?

A lot of loans that have been originated here have

relationship pricing and sometimes it does not

accurately refl ect what should be market pricing.”

The moderator then invited Lyons of SC Lowy to talk about the challenges of being broker/dealer.

Lyons: “I have been in the industry for about fi ve

years. Our principals have been in the industry in

Asia for about 15-20 years, and we’ve seen a lot

of players come and go.” He mentioned three main

challenges.

“Firstly, there are fairly signifi cant barriers to entry

to being a successful broker/dealer. You need to

have a balance sheet, because if you are going to

make markets you have to hold inventory. Things

like minimum holds of A$10m in Australia means

if you are going to build up inventory you have

to have capital.”

“A greater barrier to entry is really having in-depth

knowledge – having a strong research team. SC

Lowy has one of the largest fi xed-income research

teams in Asia. For every asset that we either invest

in or trade we get in-depth credit analysis, we

meet CEOs, CFOs and industry experts. We really

understand what we are trading.”

“with more stringent application of Basel III there will be more secondary opportunities”

25Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

“It is hard for those that are just agency trading

or match-principal trading to compete without

the same in-depth knowledge.”

“The third barrier to entry is just experience.

Having an experienced trader on the desk,

someone who has seen the ups and downs in

the market over a long period of time is

invaluable. That experience is very hard to

duplicate.”

Kwan: What are special situations and what opportunities do you see in this area?

Tham: “One of our investment strategies is to

partner with banks to provide capital. This might

be a bit of mezzanine or second-lien to provide

a bit of stretch on the debt funding side to

support corporates in the region.”

“My group runs a balance sheet of close to

US$1bn of which distressed and special

situations form a fairly large component.”

“In special situations when dealing with single-

or double-B corporates we provide very high-

yield loans or equity-linked loans for growth

capital.”

“We have also been particularly active in the

resources sector, both oil and gas, and mining.

Last year there was a US$340m deal for Niko

Resources of Canada. It had production blocks

in India which it owned jointly with Reliance

Industries. The deal paid a 15% coupon as well

as revenue-sharing warrants on top.”

“However we should not overestimate that deal.

I think every dealer would probably do between

three and six special-situation deals a year. It is

not a massive market.”

“Banks in this room are still very liquid and are

able to offer pricing at very attractive levels.

Deals have to be event-driven or regulatory-

driven before someone steps up to pay double-

digit interest rates”

Kwan mentioned that JP Morgan, besides

secondary loans, is also active in private

fi nancings and similar structured deals where

the bank provides loans to an SPV with security

being bonds or convertible bonds – special

structures to enhance the yield on loans.

The moderator then asked Lyons if he is seeing any opportunities in the special situations arena?

Lyons: “It’s just a few transactions each year. We

are very opportunistic and do special situations

for the credits that we get to know very well.”

“Currently, and over the next year, we are investing

in and trading in shipping, mining and those types

of areas. That space is where we will be active for

the moment and see ourselves being active for

the next 12 months.”

Kwan: As we know secondary in Asia is at least 10 years behind what is happening in Europe and the US. What should we do to further develop this market and get more banks or participants to join or churn their assets?

Cheung: “It is tricky because the Asian loan market

is predominantly about banks. Most are still very

low on leverage. Hong Kong banks have a 73%

loan-to-deposit ratio, whereas European banks are

at maybe ~100%, and US banks at 70-90%. Banks

will continue to provide relationship-driven pricing

and that will hinder the growth of the secondary

loan market. This will be very diffi cult to change

until banks get more leveraged.”

He said Standard Chartered has been developing

a non-bank FI investor base from credit funds,

family offi ces and leasing companies in Japan, in

order to develop an alternative source of liquidity.

“A few months ago when the credit spread

between the bonds and loans was much tighter

we sold some China property loans to non-bank

FIs, but now it would be very diffi cult given the

reversal.”

Mahal: “If you look at the growth of secondary

volumes in the US and Europe, it happened

because of the shift in the investor base. The

investor base became more institutional because

of CLOs. It is a topical subject over here: is there

potential for CLOs to be done here? Some

non-banks are looking at these types of

structures. I think that would help increase the

secondary flow. Also more event-driven

fi nancing, such as LBO-type deals. That will

create secondary volume too.”

“Banks will continue to provide relationship-driven pricing and that will hinder the growth of the secondary loan market”

“growth of secondary volumes in the US and Europe...happened because of the shift in the investor base”

Crédit Agricole Corporate and Investment Bank includes social and environmental criteria in its fi nancing policies, proving

its will to act in favor of responsible growth.

www.ca-cib.com

actively promoting

responsible

growth

www.

.com

27Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Kwan: How do we narrow the pricing gap between buyers and sellers? Sellers always want to sell at a lower yield while buyers want it the other way around. How do you overcome this situation?

Lyons thought better research would help. “If

you have buyers who are really knowledgeable

about the credits and what they are purchasing,

then the closer buyers and sellers will get. With

parity of information you suspect that views of

a credit are going to be similar.”

Tham thought that it would help if regulators

and governments got involved. In Singapore,

government-linked institutional investors –

such as ST Asset Management, Seatown

Holdings, GIC and Temasek – have been involved

in the loan market.

Q: Do you think recent regulatory and compliance issues such as onboarding and know-your-client rules have affected the effi ciency of the market?

Mahal: “Yes, but at HSBC we are pretty

fortunate that in APAC we have a lot of

relationships with clients that are already

onboarded. But the process is more onerous

now, so it can have an effect in closing trades.”

Kwan agreed that onboarding requirements

could take a long time for her institution.

Tham said it has not stood in the way of doing

trades, “but it really stands in the way of getting

them closed”.

“BAML has a large middle-offi ce support team

that is needed as a result, so we carry a very

heavy and costly infrastructure.”

“Politically-exposed persons, family offi ces, and

investment vehicles, especially in the distressed

world are challenging and we need to be mindful

of these things before we trade.”

More importantly nowadays, particularly for his

organisation and other US counterparts, the

“optics” or reputational consequences of certain

trades need to be considered as well.

“If something is 100% legal but might not look

great – such as helping the shareholder buy bonds

back or working with a party to accumulate a

stake in a debt structure with the intention of

doing a loan to own – some of these things do

come under more scrutiny than before. We need

to employ more people to make sure we are on

the right side of things.”

Kwan’s last question was about the next year’s market outlook.

Cheung: “There will defi nitely be more China

transactions in both primary and secondary,

especially given some of the corporate scandals

and potential credit issues in POEs.”

“There will be more offers on China property given

what is happening in the market and there should

be growing interest on both the primary and

secondary side.”

He sees a greater focus on onshore / offshore

inter-creditor property structures rather than

China holdcos. “Onshore / offshore is more

favorable from a credit standpoint given the

access to mortgage via an intercreditor between

onshore / offshore. There will be growing interest

in these transactions in secondary and primary.”

Mahal: “I think China is probably the big story –

that is where you will see a lot of volume in 2015.

In terms of favourite jurisdictions, these are

Australia, Korea, Singapore, but the supply has

been pretty tight so we need to see more primary

there before secondary can kick in.”

Written by:Instanter Ltd

“reputational consequences of certain trades need to be considered”

“China is probably the big story – that is where you will see a lot of volume in 2015”

28Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Syndicated lending in Taiwan: opportunity amidst challenges

Crowded banking sector

Taiwan’s banking sector is considered one of the most crowded sectors when compared to others in the region. With 38 domestic banks and almost an equal number of foreign counterparts, banks are competing hard to get a piece of the pie, which has led to margins touching rock bottom.

Taiwan/China pact

The biggest opportunity for Taiwanese banks was the signing of the pact between Taiwan and China, which opened up the China market and gave growth opportunity to Taiwan’s saturated banking sector. Not surprisingly every bank had an aggressive strategy to tap into growing their business in mainland China from bilateral lending deals to complex syndicated deals. The fact that China has become Taiwan’s largest debtor and Taiwanese banks’ exposure was valued close to US 100Bn by the end of Q2 2014 has resulted in increasing concerns from the Central Bank and the Ministry of Finance.

Regulator curbs China lending

With the regulator taking steps to curb lending to Chinese corporate, banks in Taiwan can expect larger scrutiny while doing such deals. The impact has already been seen: In Q3 2014, Taiwan’s syndicated lending witnessed one of the worst quarters in the last six years. With banks fl ush with US dollars, it is becoming imperative for them to look for business in other markets, such as India and Indonesia.

As Taiwanese banks’ foray into more overseas markets to grow their syndicated lending business, they will need to overcome competition not only from local domestic banks but also other foreign banks, which enjoy early mover advantage and are well established. Large foreign banks have continued to use

technology to help them establish themselves in overseas markets. State of the art lending systems implemented by these banks have not only helped them in consolidation but the benefi ts of such systems have been multifold. Banks have witnessed a ten-fold increase in the number of loans and a reduction of up to 85% of servicing these loans leading to higher customer satisfaction. Banks have also experienced a 100% reduction in errors and overall IT savings of more than 40% through reducing the number of systems required to manage loans.

Regulatory changes

Taiwanese banks, like many other Asian banks, continue to support their commercial complex loan business by using their legacy core banking system, single-function secondary systems, and manual processes. While this setup may have been adequate in the past, it is a poor fi t for today’s increasingly complex loans, marketplace dynamics, and regulatory framework, which is becoming tougher to comply with unless banks have complete visibility of their lending books.

Core banking systems are especially weak in the areas of loan pricing and options, and multiple transactions. They also have limited hierarchies and have no syndication capability. This makes it diffi cult for banks which use the core plus add-ons model for their commercial lending business to participate in the growing market for syndicated and other complex loans. It also poses a challenge for banks (especially mid-market ones) who want to enter new geographical markets quickly in order to be able to serve large regional clients.

In addition, the disparateness entails data re-entry to normalise loan data across systems, as well as the use of spreadsheets, paper checklists and external diaries as workarounds and to communicate with clients and internally within the bank. Such data re-processing and manual

Amit Chopra

“The biggest opportunity for Taiwanese banks was the signing of the pact between Taiwan and China”

“the regulator took steps to curb lending to Chinese corprorates”

29Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

patchwork and reporting are inherently error-prone, thus creating a wasteful need to always have to check for accuracy. Furthermore, such practices are not streamlined, redundancy is common, and workfl ow and document tracking capability are poor.

As per Celent’s report on the Top 10 Trends in Corporate Banking for 2014:

“For most banks in the developed world, the technology that supports the commercial lending business is outdated and fragmented, with literally dozens of third-party software packages, homegrown applications, and less than industrial strength database and spreadsheet solutions being used.”

Loan technology

In the syndicated lending world where relationship managers are faced with stiffer targets to increase revenues for the bank, banks also need efficient middle and back office systems to support frontend sales teams by way of up to date systems. The ability of the bank to effi ciently service a loan over its life

span can be a differentiator in this highly competitive market place. Lack of proper systems also poses a reputation risk for the banks among their technologically advanced peers.

Integrated loan technology undoubtedly brings opportunity amidst the various challenges faced by banks. Lending continues to be one of the key revenue generators for banks and commercial lending is one of the few bright spots in banking today. Consumer lending helps banks to establish their presence in the market and commercial lending continues to drive higher revenues for the bank. With the criticality of this business function, commercial lending certainly deserves dedicated and state of the art systems.

About the author

Amit Chopra heads the Syndicated and Corporate Lending Solution team for Misys in the Asia Pacifi c. Amit has over 15 years of experience in the region and in lending in both corporate and retail banking. As part of his role at Misys, Amit Chopra is responsible for FusionBanking Loan IQ, which is the market leading system for Syndicated and Bilateral Lending.

“relationship managers are faced with stiffer targets to increase revenues”

30Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Guy Hargreaves (Moderator), Atul Sodhi (Sponsor: CACIB)

Dariusz Kowalczyk (Sponsor: CACIB)

Guy Hargreaves, Atul Sodhi (Sponsor: CACIB), John Corrin (ANZ)

Janet Field (APLMA)

Siong Ooi (BAML), Phil Lipton (HSBC), Ashish Sharma (Credit Suisse)

APLMA Asia Pacifi c Syndicated Loan Market Outlook RoundtableOver 140 members attended the APLMA Market Outlook Seminar on 26 November, 2014. For an overview of key highlights please refer to page 32. Special thanks to sponsor: Credit Agricole Corporate & Investment Bank.

Atul Sodhi (Sponsor: CACIB), John Corrin (ANZ)

John Corrin (ANZ), Siong Ooi (BAML), Phil Lipton (HSBC) Ashish Sharma (Credit Suisse), Aditya Agarwal (RBS)

31Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Members network at cocktail reception

A full house of over 140 members attended

Dai Chang Song (ADB), Ellie Crespi (Harneys), Chris Raciti (ANZ), John Corrin (ANZ)

Guy Hargreaves, Atul Sodhi (Sponsor: CACIB), John Corrin (ANZ), Siong Ooi (BAML), Phil Lipton (HSBC), Ashish Sharma (Credit Suisse), Aditya Agarwal (RBS)

Jolyon Ellwood-Russell (Simmons & Simmons), Janet Field (APLMA), Theron Alldis (SC Lowy)

APLMA Asia Pacifi c Syndicated Loan Market Outlook Roundtable

Phil Lipton (HSBC), Oliver Huffmann (UniCredit), Mariachiara Cefaratti (UniCredit)

Charmaine Lo (BNP Paribas), Jennifer Chung (BNP Paribas) Teena Jaisinghani (Axis Bank), Kingsley Ong (Eversheds)

32Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Asia Pacifi c loan market – outlook for 2015

Hargreaves began by noting the dominant global market theme appeared to be technology companies, mentioning the world’s biggest IPO for Alibaba and Facebook buying Whatsapp for US$19bn. His fi rst question to the panel was: What was the best syndicated loan this year (preferably one that your bank was not involved in)?

Sodhi chose the global refi nancing for Tata Steel

“as it has a lot of complexity and includes

European and Asian tranches”. “It is challenging

because it is the steel industry – a diffi cult sector

in today’s economic environment. The client put

a good banking group together, covering

differing pockets of liquidity.” “The deal hasn’t

closed yet, but has been very well received by

the market.”

Corrin identifi ed Woolworths as a contender; a

deal done in Australia and syndicated to

insurance companies. It had “a very innovative

The Asia Pacifi c Loan Market Outlook Seminar – held on November 26, 2014 at the JW Marriott Hotel in Hong Kong – included a discussion panel to review the current year and to discuss the outlook for 2015. The moderator was veteran Asian banker Guy Hargreaves.

Panellists were:

• Atul Sodhi, Chairman APLMA, Managing Director & Head, Loan Syndication, Debt Origination and Distribution, Asia Pacifi c, Credit Agricole CIB, Hong Kong

• John Corrin, Global Head of Loan Syndications, ANZ, Hong Kong

• Phil Lipton, Managing Director, Head of Loan Syndications, Asia Pacifi c, HSBC, Hong Kong

• Aditya Agarwal, Chairman APLMA Singapore Branch, Managing Director, Head – Loan Markets, APAC, The Royal Bank of Scotland, Singapore

• Siong Ooi, Managing Director, Head of AP Syndicated & Leveraged Finance, Asia Pacifi c Debt Capital Markets, Bank of America Merrill Lynch, Hong Kong

• Ashish Sharma, Head of Loan Syndications, Asia Pacifi c, Credit Suisse, Hong Kong

Atul Sodhi

Guy Hargreaves

John Corrin

Phil Lipton

structure” and “broke new ground”. He considered

it an impressive deal, one which he wished his

bank had been involved in.

Ooi picked the Goodpack transaction, as it was a

large deal that involved commercial and investment

banks. He believed it to be one of the largest Term

Loan B (TLB) deals taken to the US. It was “an

interesting deal that hopefully leads to the evolution

of the market”. He would like to “see the bank market

in Asia try to bridge some of the gaps that exist

between Asia and the US TLB markets”.

Lipton also opted for Tata Steel for its size and

complexity: “Even though it has not been fully

completed yet, it is already a successful deal going

by the over subscription at the top level”.

Sharma chose CT Corp because of its size, which

was large for an Indonesian borrower at

US$1.275bn. “It was a highly-structured and

complex deal, and syndication was interesting

because it was marketed as a single transaction,

but had three different credits; one of which was

a holding company. A ground-breaking deal

considering it was a refi nancing of the deal done

only the year before”. He said it “set the tone for

the Indonesian loan market in general.”

33Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Aditya Agarwal

Siong Ooi

Ashish Sharma

Agarwal also liked Tata Steel and CT Corp, but

picked Huawei Technologies: “A largely European

syndication for a Chinese issuer, a fi ve-plus-one-

plus-one structure, and a size of US$1.5bn is

unprecedented.”

Hargreaves conducted an audience poll on expected loan volumes for next year in the Asia-Pacifi c. Volumes year-to-date are around US$368bn, compared to US$461bn for full-year 2013. The audience polling result was for around US$400bn or slightly more, a relatively bearish view for next year. What did the panellists think?

Lipton: “Volumes have slowed signifi cantly

coming into the fourth quarter this year, after

a very strong fi rst six months. Loan volumes in

October are meaningfully down in comparison

to last year. Last December was a very strong

month, with around US$50bn in volumes, so

this last quarter may look quite weak in

comparison. The pipeline now leading to Chinese

New Year looks okay, but it’s a question of will

this be as good as the past few years?”

Ooi thought that: “There aren’t the 2013-type

volumes in the pipeline now.” He expected

volumes for 2015 to be at around the US$400-

450bn level.

Hargreaves: How does the panel see the market? Is it in healthy shape – any negative structural trends to watch out for?

Corrin began by saying the market is very

healthy, stating that almost all this year’s deals

have been successfully syndicated: “A good

barometer of how the market stands”. However,

he believed it is going to get tougher, as even

with high volumes of business, banks will

probably be “getting paid less, as everything is

being squeezed very hard”. Despite this, the

market is “in very good shape” and has been able

to co-exist well with the bond market.

Sodhi expected a 5-7% change, either an increase

or a decrease, in loan volumes next year. The

number of arranger banks is increasing and deals

are usually over-subscribed. But retail liquidity is

not growing and remains low in many parts of

the region. This was a worry because arranging

banks tend to make their returns by taking skim

from these sorts of deals.

Ooi added that a challenge faced by arranging

banks is the increase in self-arranged deals owing

to strong liquidity. He agreed with Corrin: “While

volumes are high, banks arranging deals and

seeking underwriting income will be dramatically

impacted by such strong liquidity.”

Hargreaves asked Sharma: Are banks below the top-level at risk from how much liquidity there is?

Sharma agreed with the statement, as around

75% of the deals are very “clubbish in nature”.

They might not be branded as clubs, but selling

only around 5% into the market should not be

regarded as a syndicated deal. However, a positive

result of strong liquidity is that some banks and

funds are now more willing to “play outside their

comfort zones with deals that are higher yield or

more structured”. “At the same time there are

funds that previously wanted double-digit yields

that are now willing to look at deals at Libor plus

6-7%.”

Agarwal made a distinction between loan volume

and syndicated loan volume. He gave as an

example the WH Group refi nancing that closed a

few weeks ago. “The deal last year was syndicated

and well received. The refinancing was still

US$1bn, but was closed as a large club. In regards

to volumes, a lot of these loan volumes don’t

translate over to syndicated loan volumes.” He

further added that he believed real syndicated

loan volumes for 2015 will be down.

Audience poll: What will pricing be like for 2015? Audience polling resulted in most believing pricing will decrease by up to 10%. Hargreaves asked Lipton for his view.

Lipton “It is diffi cult to tell, as unexpected events

can make an impact – in India a few years back

“a challenge faced by arranging banks is the increase in self-arranged deals”

34Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

pricing went up as a result of a few economic

setbacks. Pricing has also gone up quite

signifi cantly this year in China and Hong Kong

(with the exception of the blue-chips) because

of factors such as the higher cost of funds for

Taiwanese banks and increased supply. However,

the general trend is now downwards as the

market is very competitive. This is despite

upward pressure from regulatory issues like

Basel III starting to make an impact. In addition,

the cost of funds for banks is higher than it used

to be, so that helps create a pricing fl oor.”

Hargreaves asked Ooi: If US interest rates go higher next year, how will that affect pricing?

Ooi “Talking about credit spreads, as opposed

to bond-market yields, I don’t see much impact.

But we need to look at two segments: There are

investment-grade blue-chips where we have

seen a lot of spread compression that has

bottomed out.” “The chase for yield is now at

the higher spreads. There is increased competition

for sub-investment-grade credits paying

spreads of 2-4%, and we may see some spread

compression here.”

Sodhi thought there are a few trends that could

impact pricing such as Japanese and European

central banks putting more money into the

banking system, which helps compress credit

spreads. He doesn’t believe corporates will

borrow more in the next year since economic

activity is not strong. “But on the fl ipside, there

are regulatory pressures such as Basel III to push

pricing up.” Overall, he believes pricing will

remain about the same, at least in the early part

of 2015.

Corrin said he does not understand why

investment-grade credits in Asia are priced so

much higher than in America or Europe.

“European pricing is signifi cantly lower than in

Asia, but largely with the same Japanese and

European banks involved.” Using Alibaba as an

example he believed pricing will decrease:

“When Alibaba initially borrowed, it had very

attractive pricing, but this subsequently came

down signifi cantly for the current revolving

credit. Banks moan about the decrease in

pricing, yet they continue to support these

deals.” He doesn’t see many “voting with their

feet”. He noted that often there is no difference

between blue- or red-chip pricing and he remains

quite pessimistic about the pricing trend.

Hargreaves: Do you think pricing levels are supportive of jumbo deals?

Sharma defi ned jumbo as US$5bn or more. He

agreed with Corrin’s thinking that pricing will go

down for investment-grade credits, with pricing

impacted by lower rates paid in the bond market.

“The bond market today offers overall better

pricing than the loan market, especially for longer

maturities.” “However, at higher yields, companies

don’t have access to the bond market.” He thought

“the interesting space to watch is LBO pricing,

where pricing has remained stable at 4% or

higher.”

Agarwal said most Asian borrowers are quasi-

BBB- credits. There is also a small market for

leveraged-fi nance or high-yield deals; but “that

volume is signifi cantly smaller than for good

corporates with which banks have a good

relationship.” “It is a combination of factors

already mentioned that infl uence pricing. Nobody

wants to miss a deal, so instead of having fi ve or

six arranging banks – now it can be 12 or 13 – then

the client might only want to have a club, because

a syndicated deal would be considered too

expensive.”

Audience poll: Taiwanese banks have been important contributors to liquidity in the market. Going forward, do you expect them to be more aggressive, no change, or less aggressive and retreat to the home market? Audience polling results in fairly equal results.

Sodhi noted that it has been a tough year for the

Taiwanese going back to when they had liquidity

problems and a high cost of funds. “The cost of

funds problem has eased off, but their regulator

has been clamping down on overseas exposure.”

He believed they will be a little more cautious, but

will not retreat to home; they will become more

focused on top-tier names. “They will remain an

important source of liquidity, indeed, they appear

to be the only signifi cant source of retail liquidity

in the market. The question is: Where will other

sources come from in the next few years?”

“investment grade credits in Asia are priced so much higher than in America or Europe”

“the interesting space to watch is LBO pricing”

35Asia Pacifi c Loan Market Association

APLMA News

Winter 2014

Hargreaves then asked: On that note, are there regions where lenders are becoming more aggressive?

Corrin remarked that institutions such as

Babson are more active than before, particularly

from Australia: “But the obvious area where

liquidity is coming from is the Gulf, where banks

have a lot of money and some are expanding in

Asia”. He expects they will be “quite signifi cant

lenders in 2015.” However, they can be “in and

out” investors: “When liquidity is good they pile

in, but the current declining price of oil might

curb their enthusiasm for joining deals.”

Ooi saw the Taiwanese as becoming more

aggressive in terms of structures and pricing,

and also, increasingly, leading deals. He also

mentioned Middle Eastern banks as a pocket of

liquidity, though: “the ones to look out for are

Japanese banks, especially second-tier ones.”

“They are sitting on a lot of liquidity and are a

good source of low-cost funding.”

Hargreaves: Last year was about recovery for European banks, do you believe that will be the trend in the future?

Sodhi said “2011 and 2012 were tough years for

European banks because of the Eurozone Crisis.

The situation is back to normal now, due to

actions by the regulators and banks. For the

foreseeable future, European banks will continue

to be very involved in Asia.”

Agarwal said RBS was ranked the seventh most

active bank in Asia and that only one other

European bank was in the top ten. “All banks can

have weak quarters and there is always someone

waiting to take that space, so at times you will see

Middle Eastern banks at the top, or Korean banks,