appeal procedure under income tax act (1)

TRANSCRIPT

APPEAL PROCEDURE UNDER INCOME TAX ACT

R.Ravichandran

Why the process of appeal necessary?

Powers to make tax payers comply with their tax obligations and to investigate those who do not

Tax authorities have discretion to make ‘best judgement assessment’ and to pass orders as they ‘may think fit’ in the circumstances of the case.

Exercise of such powers and discretion by tax authorities is likely to generate tax payer grievances on ground either that the tax authority misunderstood the law or incorrectly inferred facts or misapplied the law to the facts of the case had not afforded a reasonable opportunity of hearing to the tax

payer may also be voiced.

Why the process of appeal necessary?

In case of obvious or prime facie mistakes, the tax payer can approach the concerned authority for rectification of the order. Such mistakes may be as to facts as well as of law.

The tax payer can also approach the Commissioner of Income-tax for revision of the orders of the authority administratively subordinate to him where he does not file appeal against this order.

In order that the tax payers have confidence in the fair play, credibility and impartiality of the tax administration, Direct Tax laws have provided for independent appellate fora.

Ravichandran/NADT/Appeal Procedures

Right of Appeal Statutory Right Appeal against the order of Assessing officer lies

with the CIT(Appeal) under S.246A to S.251 of the IT Act Only by the assessee

Appeal against the order of the CIT(Appeal) lies with the appellate tribunal By assessee or IT Department

Appeal against the order of the Income tax Appellate Tribunal (ITAT) lies with the High Courts and thereafter the Supreme Court

Ravichandran/NADT/Appeal Procedures

Alternate modes of redressal of grievances

In case of obvious or prime facie mistakes, the tax payer can approach the concerned authority for rectification of the order.

Such mistakes may be as to facts as well as of law.

The tax payer can also approach the Commissioner of Income-tax for revision of the orders of the authority administratively subordinate to him where he does not file appeal against this order.

Ravichandran/NADT/Appeal Procedures

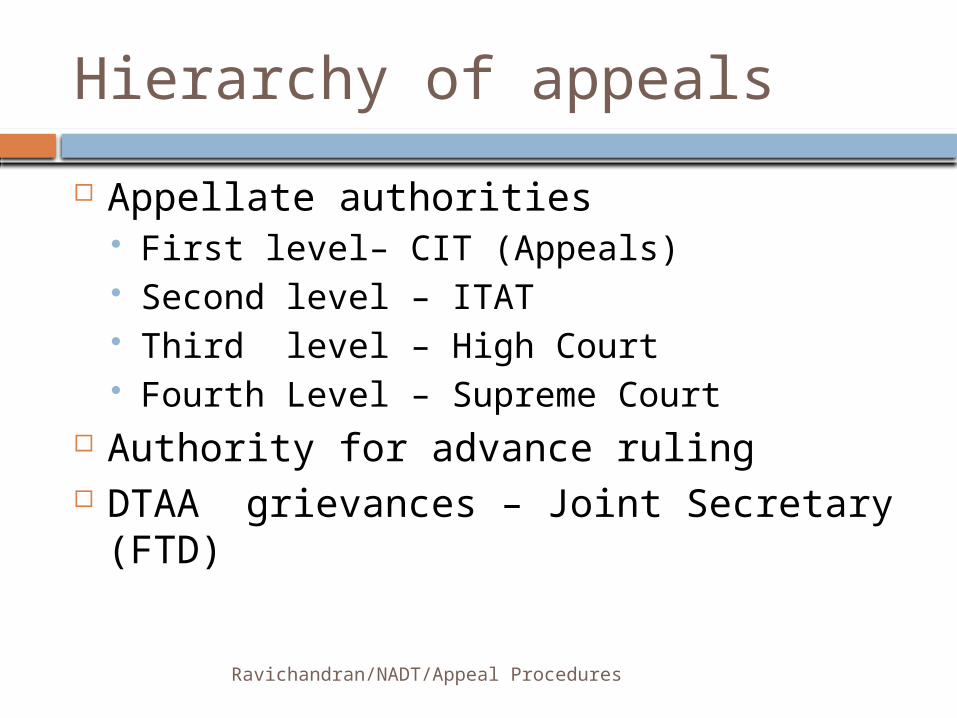

Hierarchy of appeals Appellate authorities

First level– CIT (Appeals) Second level – ITAT Third level – High Court Fourth Level – Supreme Court

Authority for advance ruling DTAA grievances – Joint Secretary (FTD)

Appeal under Income Tax Act,1961

Sections Covered

246A: CIT (Appeals) 254: ITAT ---Final Fact Finding Authority 260A: High Court ---On substantial Question of Law 261:SupremeCourt

Orders not appealable

Orders passed U/s 234A, B, and C for levying Interest Orders passed U/s 264 rejecting Revision Petition Orders of AAR (Authority for Advance Ruling) Orders of Settlement Commission

Particulars 246A 254 260A 261

Appellate Authority CIT (A) ITAT High Court Supreme Court

Time limit for Appeal30 days from the receipt of the order

60 days from the communication of the Order

120 days from the communication of the order of ITAT

90 days from the date of Order of High Court

Time limit for disposal of Appeal

1 Year from the end of the FY

4 Year from the end of the FY

As per Court procedure

As per Court procedure

Application Form 35 36As per Court procedure

As per Court procedure

Procedure of Appeal

Stamps to be affixed 0.50P 0.50P

As per Court procedure

As per Court procedure

Fees to be Paid

Returned Income upto Rs1 Lac Rs 250 Rs 500

As per Court procedure

As per Court procedure

More than 1 lac upto Rs 2 Lac Rs 500 Rs 1500

As per Court procedure

As per Court procedure

More than 2 lac Rs 10001 % of income Max Rs (10,000)

As per Court procedure

As per Court procedure

Appeal for other than Income Rs 250 Rs 500

As per Court procedure

As per Court procedure

Stay of Demand Not PossiblePossible against order of CIT(A)

Possible Possible

Recovery of TaxNo power to stay the recovery of Tax

Final order should be passed within 180 days from the stay order so passed

- -

Minimum Tax to be paid for filling appeal

If Return is Filled: Tax due on Returned IncomeIf Return not Filled: At least the Advance tax payable

Rs 2,00,000/-+ Question of Law

Rs 4,00,000/-+ Question of

Law

Rs 10,00,000/-+ Question of

Law

SECTION 246A- APPEAL TO COMMISSIONER (APPEALS)

Appealable orders Orders against the Assessee Where the assessee denies his liability to be

assessed under IT Act assessed under Assessment Order U/s 143 (3), 144

Where the assessee objects to the income assessed amount of tax determined amount of loss computed status under which he is assessed

SECTION 246A- APPEAL TO COMMISSIONER (APPEALS)…

Order of Assessment / Re-assessment U/s 147,153A

Orders made U/s 154,155 enhancing the assessment reducing a refund refusing to allow a claim

Orders made U/s 163 ---treating Assessee as an agent of NR

Orders made U/s 170 (2) / (3) on succession of Business or Profession

Ravichandran/NADT/Appeal Procedures

SECTION 246A- APPEAL TO COMMISSIONER (APPEALS)…

Orders made U/s 171-----refusing Partition of HUF Orders made U/s 201----levying interest for delay

in remitting TDS / TCS Orders made U/s 206C (6A)---levying penalty for

failure to collect or delay in remitting TDS /TCS Order made U/s 237----Refund Order imposing penalty U/s 221, 271, 271A,

271AAA, 271F, 271FB, 271B, 271BB, 271C, 271CA, 271D, 271E, 272A, 272AA, 272BB, 158BFA, Chapter XXI

SECTION 246A- APPEAL TO COMMISSIONER (APPEALS)….

Order imposing / enhancing penalty U/s 275 (1A)

Order made U/s 158BC ( c) for search initiated U/s 132 or requisition of books U/s 132A

Orders made U/s 115VP Orders made U/s 115WE/ WF for value of

Fringe Benefits Orders made U/s 115 WG for re-assessment

of FBT

Powers of CIT (A) To Condone the Delay as regards limitation of

time limit for filling Appeal beyond 30 days if he is satisfied that the appellant or the

Assessee has sufficient reason to file the appeal after the due date.

To inquire into the matters as he thinks fit, before disposing the Appeal.

To direct the Assessing officer to make such inquiry and report the same, as he thinks fit.

Powers of CIT (A)…. Can confirm, reduce, enhance or

annul the assessment -----if the Appeal is against the Order of Assessment.

Can confirm, cancel, and vary the Order -----if the Order is against the Order of Penalty. (can not set aside)

Pass such Order as he thinks fit.

Ravichandran/NADT/Appeal Procedures

ITAT

SECTION 253: APPEAL TO INCOME TAX APPELLATE TRIBUNAL (ITAT)

Appealable orders Orders Passed by COMMISSIONER

(APPEALS) Orders passed U/s 115 VZC refusing

applicability of tonnage tax Scheme. Orders passed U/s 154 Orders passed u/s 250 Orders passed u/s 271, 271A, 272A

SECTION 253: APPEAL TO INCOME TAX APPELLATE TRIBUNAL

Orders passed by Commissioner Orders passed U/s 12 AA refusing registration of a

Trust as religious or charitable or Cancellation of registration of a Trust.

Orders passed U/s 80G (5) (vi) refusing to register a Trust U/s 80G

Orders passed U/s 263, 271, 272 A Order passed U/s 154 amending order U/s 263

Order passed U/s 154 amending order passed U/s 272A originally passed by Chief Commissioner, DG or Director

Powers of ITAT To Condon the Delay as regards limitation of

time limit for filling Appeal beyond 120 days if he is satisfied that the appellant or the

Assessee has sufficient reason to file the appeal after the due date

To accept additional evidence Under Rule 46A. To make necessary inquiry, wherever

necessary To rectify the mistake apparent from record

Powers of ITAT….

Rectify ( can not REVIEW ) its own order at any time ---within 4 years from the date of the Order---with a view to rectify any mistake apparent from record. (if any order is prejudicial to the interest of the Assessee then shall give opportunity of being heard).

ITAT is the final fact finding authority i.e, on a question of fact, the Order of ITAT are final and no appeal against the said order can be filed at Supreme Court

On a question of Law the Order of ITAT is final until appeal is not filed at Supreme Court against the said Order

APPEAL AGAINST ITAT

On a question of Fact A WRIT PETITION can be filed to the

Supreme Court, challenging the fact finding process adopted by ITAT.

If the Supreme Court is satisfied that the Fact Finding process is not proper, then the Order of ITAT shall be quashed and a direction shall be issued by the Supreme Court to the ITAT to do the Fact Finding in a proper manner and /or as per the direction

Appeal against ITAT…. If the WRIT PETITION filed by assessee is

dismissed by SUPREME COURT The assessee can file a SPECIAL LEAVE

PETITION to the SUPREME COURT challenging the Fact Finding process of ITAT.

If the Supreme Court is satisfied that the Fact Finding process is not proper, then the Order of ITAT shall be quashed and a direction shall be issued by the Supreme Court to the ITAT to do the Fact Finding in a proper manner and /or as per the direction

Ravichandran/NADT/Appeal Procedures

Procedure

Ravichandran/NADT/Appeal Procedures

Procedure for filing of appeals before CIT(A) &ITAT

The Income-tax Rules, 1962 provides that an appeal to the Commissioner (Appeals) shall be made in Form No. 35

Form of verification shall be signed and verified by the person who is authorized to sign the return of income under section 140 of the Income-tax Act, 1961 (the Act) (Rule 45) .

Income-tax (Appellate Tribunal ) Rules, 1963 specifies as to the contents of the memorandum of appeal.

Ravichandran/NADT/Appeal Procedures

Procedure for filing of appeals before CIT(A) &ITAT

Rule 8 mandates that every memorandum of appeal shall be written in English and shall set forth, concisely and under distinct heads the grounds of appeal without any argument or narrative and such grounds shall be numbered consecutively.

Rule 47 of the Rules prescribes Form No. 36 for an appeal to the Income-tax Appellate Tribunal and Form No. 36A for filing memorandum of cross-objections

Ravichandran/NADT/Appeal Procedures

Procedure for filing of appeals before CIT(A) &ITAT…..

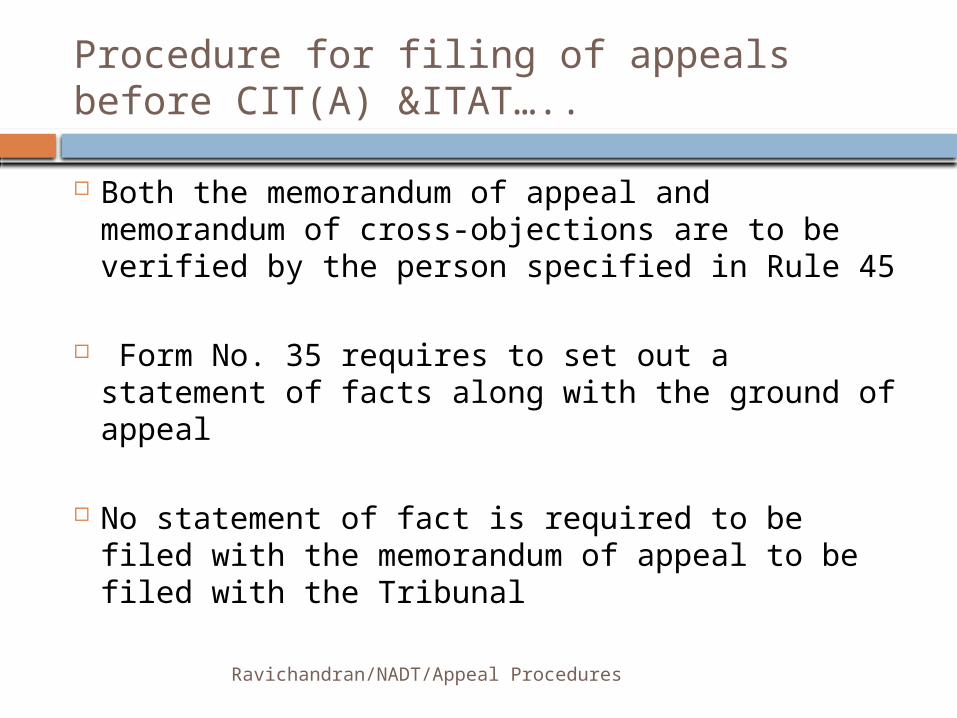

Both the memorandum of appeal and memorandum of cross-objections are to be verified by the person specified in Rule 45

Form No. 35 requires to set out a statement of facts along with the ground of appeal

No statement of fact is required to be filed with the memorandum of appeal to be filed with the Tribunal

Ravichandran/NADT/Appeal Procedures

Procedure for filing of appeals before CIT(A) &ITAT…..

Annexure to the memorandum of appeal to be filed before the Tribunal should include Form No. 35 in which statement of facts are narrated.

Statement of facts should be in such a manner so as to clearly bring out the issues in the assessment/penalty proceedings leading to the order under challenge.

Rule 22 of the Tribunal Rules provides that memorandum of cross-objection shall be numbered as an appeal and all the rules so far as may be, shall apply to such appeal.

Ravichandran/NADT/Appeal Procedures

Draft of grounds of appeal

"On the facts and in the circumstances of the case and in law the Assessing Officer (or ‘ the Commissioner of Income–tax (Appeals)’ where an appeal is filed before the Tribunal against the order of Commissioner (Appeals)) erred in …….without appreciating …………".

A prayer should be made for deletion or addition/disallowance after taking relevant ground as under :

"The Appellant prays that the addition/ disallowance of Rs. _________ made in respect of/out of ……………. be deleted."

Ravichandran/NADT/Appeal Procedures

Draft of grounds of appeal… And at the end the Appellant should

crave leave for variation or withdrawal of grounds of appeal as under:

"The Appellant craves leave to add, amend , alter vary and / or withdraw any or all the above grounds of Appeal."

If the statement of facts /grounds of appeal are separately annexed then the same should be signed by the Appellant.

Ravichandran/NADT/Appeal Procedures

Detailed process… Appeal to the Commissioner (Appeals) is to be filed

in Form No. 35 and to the Tribunal in Form No. 36. Cross-objections are to be filed in Form No. 36A. As per notes to the Form No. 35 the memorandum

of appeal, statement of facts and the grounds of appeal must be in duplicate and should be accompanied by a copy of the order appealed against and the notice of demand in original, if any.

The memorandum of appeal should be accompanied by the prescribed fee.

Ravichandran/NADT/Appeal Procedures

Detailed Process… Where the appeal is filed against an order imposing

penalty under section 271(1)(c) of the Act , a copy of assessment order must also be attached.

Rule 9 of the Tribunal Rules provides that every memorandum of appeal to be filed before the Tribunal shall be in triplicate and shall be accompanied by two copies (at least one of which is a certified copy) of the order appealed against, two copies of the order of the assessing officer, two copies of the grounds of appeal, before the first Appellate authority and two copies of statement of facts, if any, filed before the said Appellate Authority.

Ravichandran/NADT/Appeal Procedures

Detailed process… In a case of appeal against the order of penalty,

the memorandum of appeal shall also be accompanied by two copies of the assessment order.

Where an assessment order is passed under section 143(3) rws 144B or under section 143(3) rws 144A or under section 143(3) rws 147, the memorandum of appeal shall also be accompanied by the two copies of the draft assessment order under section 144B or directions under section 144A or the original assessment order as the case may be.

Ravichandran/NADT/Appeal Procedures

Detailed Process… The memorandum of appeal before the Tribunal

shall also be accompanied by the prescribed fees. Four identical sets consisting of memorandum of

appeal in Form No. 36, order of Commissioner (Appeals), Form No. 35 with annexures and the assessment/penalty order from which the appeal arises are generally prepared

Explanation to Rule 9 clarifies that "certified copy " will include the copy which was originally supplied to the assessee as well as photostat copy thereof duly authenticated by the assessee or his authorised representative as a true copy.

Ravichandran/NADT/Appeal Procedures

Beware The Supreme Court in CIT vs. Calcutta

Discount Co. Ltd., (1973) 91 ITR 8 (SC) observed that in considering an appeal the Appellate Authority should deal with the substance of the matter at issue and not be unduly influenced by mere procedural technicalities, for example, whether the memo of appeal was or was not in proper form etc.

Ravichandran/NADT/Appeal Procedures

Appeal Fees Fee must be paid for admitting the appeal The Hyderabad Bench of the Tribunal in

Andhra Pradesh State Electricity Board vs. ITO (1994) 49 ITD 552 (Hyd) have held that even where total income is computed at a loss and such loss exceeds Rs.1 lakh, the fees payable would be as per the slab prescribed for the income more than Rs. 1 lakh and therefore fees are to be determined on the basis as if loss determined is income.

Ravichandran/NADT/Appeal Procedures

Appeal fees… The Mumbai Bench of the Tribunal in Chiranjilal S.

Goenka vs. WTO (2000) 66 TTJ (Mum) 728 have held that the stay application for more than one year or for more than one order for the same assessment year can be made on payment of fees of Rs. 500/- only.

The Mumbai Bench of Tribunal in Amruta Enterprises vs. Dy. CIT (2003) 84 ITD 172 (Mum) have held that the quantum of penalty under section 271(1)(c) cannot be linked with the assessed income and therefore the fees payable is as per the provisions of section 253 (6)(d). Also, in Narendra Valji Shah vs. ACIT (ITA/3545/M/99 dated 24-5-2000).

Ravichandran/NADT/Appeal Procedures

Appeal Fees… In Mrs. Nimu R. Thodani vs. Jt. CIT

(ITA/5437/M/97 dated 1-2-2000) the Tribunal held that in cases filed with respect to interest under sections 234A, 234B, 234C or any other interest appeal fee would be Rs. 500/- as per section 253(6)(d) because interest is in no way related to the assessed income but is linked with tax payable.

The ratio of the above decisions will also apply to the appeals to be filed before Commissioner (Appeals).

Ravichandran/NADT/Appeal Procedures

Appeal fees… The Tribunal (Mumbai Bench C) held that

the levy of penalty u/s. 271B is not in any way related to the total income and hence fees would be Rs. 500/- as contemplated in section 253(6)(d). A similar view was taken in Chromatte India Ltd. vs. ITO (ITA/3486-87/M/02 dated 12-2-2002)

where the Tribunal held that in an appeal against an order u/s 263 the fees are to be paid as per section 253(6)(d).

Ravichandran/NADT/Appeal Procedures

Signing of appeal the form of appeal is to be signed and

verified by the person who is authorised to sign the return of income under section 140 of the Act.

As such the appeal to be filed by an individual must be signed and verified (i) by the individual himself, (ii) where he is absent from India, by the

individual himself or by some person duly authorised by him in this behalf (a valid Power of Attorney should be attached with the appeal)

Ravichandran/NADT/Appeal Procedures

Signing of Appeal… (iii) where he is mentally incapacitated from

attending to his affairs, by his guardian or any other person competent to act on his behalf.,

where, for any other reason, it is not possible for the individual to sign the appeal, by any person duly authorised by him in this behalf (a valid Power of Attorney should be attached with the appeal).

Therefore, unless any of such exceptional circumstances be present, an appeal in order to be valid, has to be signed by the individual himself.

Ravichandran/NADT/Appeal Procedures

Signing of appeal….. In case of the Hindu undivided family, the appeal is to

be signed by the Karta and where the Karta is absent from India or he is mentally incapacitiated from attending to his affairs, the appeal is to be signed and verified by any other adult member of such family. If the Hindu undivided family has no major member as Karta, appeal may be validly signed by any male adult member of the family who is in receipt of the income.

In the case of Shridhar Uday Narayan vs. CIT (1962) 45 ITR 577(All)]. "Adult "is a person who has attained the age of discretion which in India is 16 years. A person attains majority at the age of 18 years.

Ravichandran/NADT/Appeal Procedures

Signing of appeal… In a case of a company an appeal is to be signed and

verified by the Managing Director thereof or where for any unavoidable reason, such Managing Director is not able to sign, by any Directors thereof or where there is no Managing Director by any Director thereof.

The Calcutta High Court in National Insurance Co. Ltd vs. CIT (1995) 213 ITR 862 (Cal) held that the return signed by a Director and not by the Managing Director was invalid in absence of any explanation.

A company which is being wound up or for whose assets any person has been appointed as a receiver, the appeal is to be signed and verified by the liquidator referred to in section 178(1).

Ravichandran/NADT/Appeal Procedures

Signing of Appeal…. In case of a firm the appeal is to be signed by the

Managing Partner thereof or where for any unavoidable reason, such Managing Partner is not able to sign, by any partner thereof not being a minor or where there is no Managing Partner as such, by any partner thereof not being a minor.

In other cases, it is the principal officer who has to sign the appeal. The Bombay Bench of the Tribunal in Mrs. Leezo Salidan vs. CIT 16 TTJ 243 (Bom) , Pyrkashim Stores vs. CIT 9 ITD 93(Bom) and Hariledge vs. ITO 29 Taxman 122 (Bom) as also the Gujarat High Court in Rajendrakumar Maneklal Sheth( HUF) vs. CIT (1995) 213 ITR 715 (Guj) have held that the appeal signed by an advocate / Chartered Accountant is valid.

Ravichandran/NADT/Appeal Procedures

Signing of appeal…

The Madras High Court in Arunachalam Chettiar vs. CIT (1962) 45 ITR 407 (Mad) and Andhra Pradesh High Court in Chelamala Setti Adeyya vs. CGT (1964) 54 ITR 339 (AP) held that failure to attach notice of demand to memorandum of appeal is mere irregularity which can be subsequently rectified.

The above view was held by Gyan Manjari Kuari vs. CIT (1944) 12 ITR 59 (Pat); Ag IT v. Keshab Chandra Madanlal (1950) 18 ITR 569, 573(SC)].

The Bombay High Court in Malani Trading Co. vs. CIT (2001) 252 ITR 670 (Bom) have held that merely because there is defect in the memo of appeal, dismissal of appeal without giving opportunity to cure said defect will be improper.

Ravichandran/NADT/Appeal Procedures

Presentation of Appeal Where revenue filed appeal without including

therein grounds of appeal and statement of facts as required and Tribunal did not issue defect memo, the Gauhati Bench of the Tribunal in Asst. CIT vs. Rayang Timber Products (P) Ltd. (2002) 82 ITD 73 (Gau)(TM) held that appeal was to be deemed to have been accepted and it had to be further presumed that Tribunal had already exercised its discretion under sub-rule (3) of rule 9 of ITAT rules in favour of appellant

Ravichandran/NADT/Appeal Procedures

Presentation of appeal A memorandum of appeal to the Commissioner (Appeals)

must be presented to the office of the Commissioner in person or by an agent or sent by Registered Post addressed to the Office of the Commissioner (Appeals).

A memorandum of appeal to the Tribunal must be presented by the Appellant in person or by an agent to the Registrar at the Head Quarters of the Tribunal at Bombay or to an Officer authorised in this behalf by the Registrar or sent by Registered Post addressed to the Registrar or to such officer.

Vide order No. 1 of 1973 dated 1.10.1973, the Registrar of the Tribunal has authorised Asst. Registrars of the Appellate Tribunal situated at different places to be the authorised Officer to receive the appeals or applications as per Rule 7 of the Tribunal Rules.

Ravichandran/NADT/Appeal Procedures

Presentation of appeal… In the case the applicant apprehends that it is last day

of the limitation for presentation of his appeal and application, he may present it to the Assistant Registrar at his residence or any other place wherever he may be or to Member of the Tribunal at his residence or wherever he may be.

If an appeal is send by post it shall be deemed to have been presented on that day on which it is received by the office of the Commissioner (Appeals) or the Tribunal (pl.see Rule 6(2) of the Tribunal Rules and F.N.Roy vs. Collector of Customs AIR 1957 (SC) 648 – postal authorities are not considered as a agents of the addressee but are the agents of the sender).

Ravichandran/NADT/Appeal Procedures

Decisions on Time limit An appeal to the Commissioner (Appeals) should be

filed within a period of 30 days of the service of the order against which the appeal is preferred.

The Calcutta High Court in Charki Mica Mining Co. Ltd. vs. CIT (1978) 111 ITR 193 (Cal) has held that the period of limitation for filing an appeal to the Commissioner (Appeals) is to be computed from the date of the receipt of demand by the assessee and not from the date of receipt of assessment order by the assessee.

An appeal to the Tribunal should be filed within a period of 60 days from the date on which the order sought to be appealed against is communicated.

Ravichandran/NADT/Appeal Procedures

Decisions on Time limit… Where the assessment order was served on the person

who was not an authorised agent of the assessee, and later on, the assessee applied for and obtained a copy of the assessment order for purpose of filing an appeal, it was held that the time limit for filing the appeal should be reckoned from the date on which the assessee obtained the copy of the assessment order and notice of demand and not from the earlier date of service of the assessment order – CIT vs. Prem Kumar Rastogi (1980) 124 ITR 381 (All). Also see, Jayalakshmi Cloth Stores vs ITO (1981) 132 ITR 764 (AP), Rasipuram vs. CIT (1956) 30 ITR 687 (Mad) and Malayalam Plantations Ltd vs. CIT (1959) 36 ITR 205 (Ker).

Ravichandran/NADT/Appeal Procedures

Decisions on Time limit… Where postal acknowledgment in file of

Assessing Officer did not bear signature of any person and so also it did not bear any date of service, it was reasonable to believe that the assessee was not served with the order of assessment and the demand notice and in such case appeal filed by the assessee on 10-8-1980 against the order of assessment for the assessment year 1981-82 could not be said to be barred by limitation. (Badri Singh Thakur vs. ITO (1995) 78 Taxman 206(Jab).

Ravichandran/NADT/Appeal Procedures

Delay in filing the appeal Section 249 (3) gives a power to the Commissioner

(Appeals) to condone the delay in filing the appeal to the Commissioner (Appeals).

Section 253(5) empowers the Tribunal to admit an appeal or permit the filing of memorandum of cross-objection after the expiry of the relevant period if it is satisfied that there was sufficient cause for not presenting it within that period.

When an application for condonation of delay in filing an appeal is preferred, it is statutory obligation of the appellate authority to consider whether sufficient cause for not presenting the appeal in time was shown by the appellant – Shrimant Govindrao Narayanrao Ghorpade vs. CIT (1963) 48 ITR 54(Bom).

Ravichandran/NADT/Appeal Procedures

Delay in filing the appeal… An assessee has a statutory right to present an appeal

within prescribed period without any order being required from the Appellate Authority for admission of the appeal.

After the expiry of the prescribed period, an appeal can be entertained only if it is admitted by the appellate authority after condoning the delay [CIT vs. Mysore Iron & Steel Ltd. (1949) 17 ITR 478, 480 (Bom)].

The power to condone the delay is discretionary and the discretion must be judicially exercised. (J & K Small Scale Industries Development Corpn Ltd., v. Dy. CIT (1949) 71 ITD 367 (Asr).

Ravichandran/NADT/Appeal Procedures

Delay in filing the appeal… The Supreme Court in Collector of Land Acquisition vs. Mrs.

Katiji & Others (1987)167 ITR 471(SC), held that Court should have pragmatic and liberal approach. [Also see Raja Jagadambika Pratap Narain Singh vs. CBDT 100 ITR 698 (SC)]

The Supreme Court in N. Balkrishnan vs. M. Krishnamurthy (1998) 7 SCC 123 had condoned a delay of 833 days. It was observed that condonation of delay is a matter of discretion of the Court and the only criterion is the acceptability of explanation irrespective of the length of delay.

A subsequent decision of the Supreme Court/High Court was considered as sufficient cause for condoning delay in filing the appeal. (State of Andhra Pradesh vs. Venkataramana Chudava & Muramura Merchant (1986) 159 ITR 59 (AP).

Ravichandran/NADT/Appeal Procedures

Delay in filing the appeal… The Courts have also held that the mistake of an Advocate

or Chartered Accountant is a reasonable cause for delay in filing an appeal. (pl. see Rafiq C. Munshilal AIR 1981 SC 1400 (1401), Mahavir Prasad Jain vs. CIT (1988) 172 ITR 331 (MP), Concord of India Insurance Co. Ltd. vs. Smt. Nirmaladevi & Sons (1979) 118 ITR 507 (SC). Punam Singh vs. ITO (2002) 257 ITR 38 (Chennai) ( Trib). Shakti Clearing Agency P. Ltd. vs. ITO (127 Taxman 49 (Mag) (Raj.).

Revenues petition for condonation of delay was dismissed in Asst. CIT vs. Taggas Industries Development Ltd. (2002) 80 ITD 21 (Cal); Asst. CIT vs. Punna Textiles Industries P. Ltd., (2002) 122 Taxman 264 (Cal) (Mag), Asst. CIT vs. Mahadeo Agarwalla (2002) 125 Taxman 229 (Cal) (Mad).

Ravichandran/NADT/Appeal Procedures

Payment of admitted tax… Section 249 (4) provides that no appeal shall be entertained

under chapter XX unless at the time of filing the appeal the assessee has paid

(a) the taxes due on the returned income or (b) where no return is filed, an amount equal to the amount of

advance tax which was payable by him. The Commissioner (Appeals) is empowered, for any good and

sufficient reason, to exempt the assessee from operation of this provision in case of (b).

Prior to amendment from 1-4-1989 the Commissioner (Appeals) had power to exercise his power to exempt in case (a) also.

Order refusing to exercise such discretion is an appealable order – CIT vs. Smt. Nanhibai Jaiswal (1988) 171 ITR 646 (M.P.).

Ravichandran/NADT/Appeal Procedures

Payment of admitted tax… Filing of appeal before Tribunal also falls

under chapter XX , hence provisions of section 249(4) are applicable to an appeal filed before the Tribunal. (V. Baskaran vs. Asst. CIT (1998) 62 TTJ (Chennai) 698).

The Indore Bench of the Tribunal in Pawan Kumar Lodha vs. ACIT (2003) 78 TTJ (Ind) 983 held that prepayment of tax does not apply to appeal filed before the Tribunal.

Ravichandran/NADT/Appeal Procedures

Payment of admitted tax… It does not apply to appeals filed to the Tribunal

from assessment framed under Chapter XIV B. [V.S.N. Sudhakaran vs. Asst. CIT (2002) 83 ITD 159 (Chennai); Anil Sanghi vs. ACIT (85 ITD 73 (Del) (SB)].

The Madras High Court in CIT vs. Smt. G.A. Somanth Kamani (2002) 125 Taxman 424 (Mad) held that section 249 (4) cannot be read down so as to restrict it to appeal against assessment only it will be applicable in case of appeal against penalty also.

Ravichandran/NADT/Appeal Procedures

Maintainability of appeals… Appeal is not maintainable

where tax is not deducted at source from payment made to non-resident and is not paid to the Govt. prior to filing of appeal (ITO vs. Tata Iron & Steel Co. Ltd. (2001) 71 TTJ (Cal) 323.

Crucial date for deciding the applicability of amended provisions to section 249(4) was the date of issue of notice under section 143(2) and not date of filing return. (Satyendra Pal Chaudhary vs. Asst. CIT (2002) 74 TTJ (Mum) 741) .

Where despite adjustment of seized amount full amount of tax due from assessee was not paid before filing appeal, assessee’s appeal was not maintainable (Bharatkumar Sekhsaria vs. Dy. CIT (2002) 82 ITD 512 (Mum) ( CIT vs. Smt. G.A. Samonthakamani (2002) 125 Taxman 424 (Mad).)

Ravichandran/NADT/Appeal Procedures

Maintainability of appeals… In Shri Parasram G. Purohit vs. ACIT, ITA

No. 2689/Bom/93 Bench ‘B’ Assessment year 1989-90, the Hon’ble Bombay Tribunal, held that once the tax required to be paid u/s. 249(4) has been paid before the final date of hearing, it is incumbent to consider the appeal having been filed on the date of payment. (Decision of Supreme Court in CIT vs. Filmistan 42 ITR 163 referred to).

Ravichandran/NADT/Appeal Procedures

Maintainability of appeals… Where appellant was ‘notified entity under the Special Court (Trial of

offences relating to Transactions in Securities) Act, 1992 and all properties had been attached, in view of this fact that the Appellant had requested the Assessing Officer to approach special Court to release amount of self assessment tax payable and such request had been made by Assessing Officer, assessee could be said to have made implied compliance with the provisions of section 249(4). (Divine Holdings (P) Ltd vs. Dy. CIT (2001) 119 Taxman 27 (Mum) (Mag) (Also see, Ashwin S. Mehta (HUF) vs. Asst CIT (2002) 75 TTJ (Mum) 960).

Where assessee filed appeal on 2.4.1976 and 4.11.1997 was last date on which AAC heard appeal by which time assessee had paid entire tax due, the Delhi High Court in CIT vs. Rama Body Builders (2001) 250 ITR 825 (Del), AAC was not justified in refusing to entertain appeal on the ground that tax due had not been paid by 2.4.1976, the date on which the appeal was filed, [also see S. Venkatesh vs. Asst. CIT (2000) 112 Taxman 31 (Chennai) (Mag)].

Ravichandran/NADT/Appeal Procedures

Death of Assessee Where an assessee to an appeal dies or is adjudicated

insolvent or in the case of the company wound up, the appeal will not abate and will continue against the executor, administrator or other legal representatives of the assessee or by or against the assignee, receiver or liquidator as the case may be.

In case of a death of assessee, the legal heirs of the assessee must file copy of death certificate and an affidavit of they being the legal heirs.

A fresh memorandum of appeal signed by the legal heirs must be filed before the Commissioner (Appeals) or the Tribunal as the case may be where the assessee is the appellant so that the legal heirs are brought on record.

Ravichandran/NADT/Appeal Procedures

High Court

Ravichandran/NADT/Appeal Procedures

High Courts

The High Court stands at the head of a State's judicial administration.

There are 18 High Courts in the country, three having jurisdiction over more than one State.

Among the Union Territories Delhi alone has a High Court of its own. Other six Union Territories come under the jurisdiction of different State High Courts.

.

Ravichandran/NADT/Appeal Procedures

Powers of HC Each High Court has power to issue to any person

within its jurisdiction directions, orders, or writs including writs which are in the nature of habeas corpus, mandamus, prohibition, quo warranto and certiorari for enforcement of Fundamental Rights and for any other purpose.

This power may also be exercised by any High Court exercising jurisdiction in relation to territories within which the cause of action, wholly or in part, arises for exercise of such power, notwithstanding that the seat of such Government or authority or residence of such person is not within those territories.

Ravichandran/NADT/Appeal Procedures

Powers of HC…. Each High Court has powers of

superintendence over all Courts within its jurisdiction.

It can call for returns from such Courts, make and issue general rules and prescribe forms to regulate their practice and proceedings and determine the manner and form in which book entries and accounts shall be kept.

Ravichandran/NADT/Appeal Procedures

Supreme Court

Ravichandran/NADT/Appeal Procedures

Supreme Court Original, appellate and advisory jurisdiction. exclusive original jurisdiction extends to any dispute between

the Government of India and one or more States or between the Government of India and any State or States on one side and one or more States on the other or between two or more States, if and insofar as the dispute involves any question (whether of law or of fact) on which the existence or extent of a legal right depends.

Article 32 of the Constitution gives an extensive original jurisdiction to the Supreme Court in regard to enforcement of Fundamental Rights.

It is empowered to issue directions, orders or writs, including writs in the nature of habeas corpus, mandamus, prohibition, quo warranto and certiorari to enforce them.

Ravichandran/NADT/Appeal Procedures

Supreme Court… The Supreme Court has been conferred with power to direct

transfer of any civil or criminal case from one State High Court to another State High Court or from a Court subordinate to another State High Court.

The Supreme Court, if satisfied that cases involving the same or substantially the same questions of law are pending before it and one or more High Courts or before two or more High Courts and that such questions are substantial questions of general importance, may withdraw a case or cases pending before the High Court or High Courts and dispose of all such cases itself.

Under the Arbitration and Conciliation Act, 1996, International Commercial Arbitration can also be initiated in the Supreme Court.

Ravichandran/NADT/Appeal Procedures

Powers of Supreme Court Appellate jurisdiction of the Supreme Court can be

invoked by a certificate granted by the High Court concerned under Article 132(1), 133(1) or 134 of the Constitution in respect of any judgement, decree or final order of a High Court in both civil and criminal cases, involving substantial questions of law as to the interpretation of the Constitution.

Appeals also lie to the Supreme Court in civil matters if the High Court concerned certifies : (a) that the case involves a substantial question of law of

general importance, and (b) that, in the opinion of the High Court, the said question

needs to be decided by the Supreme Court.

Ravichandran/NADT/Appeal Procedures

Powers of Supreme Court…. In criminal cases, an appeal lies to the Supreme Court if the

High Court (a) has on appeal reversed an order of acquittal of an accused

person and sentenced him to death or to imprisonment for life or for a period of not less than 10 years, or

(b) has withdrawn for trial before itself any case from any Court subordinate to its authority and has in such trial convicted the accused and sentenced him to death or to imprisonment for life or for a period of not less than 10 years, or

(c) certified that the case is a fit one for appeal to the Supreme Court. Parliament is authorised to confer on the Supreme Court any further powers to entertain and hear appeals from any judgement, final order or sentence in a criminal proceeding of a High Court.

Ravichandran/NADT/Appeal Procedures

Powers of Supreme Court…. Appellate jurisdiction over all Courts and

Tribunals in India in as much as it may, in its discretion, grant special leave to appeal under Article 136 of the Constitution from any judgment, decree, determination, sentence or order in any cause or matter passed or made by any Court or Tribunal in the territory of India.

Special advisory jurisdiction in matters which may specifically be referred to it by the President of India under Article 143 of the Constitution.

Ravichandran/NADT/Appeal Procedures

Reference to SC There are provisions for reference or

appeal to this Court under Article 317(1) of the Constitution,

Section 257 of the Income Tax Act, 1961, Section 7(2) of the Monopolies and Restrictive Trade Practices Act, 1969, Section 130-A of the Customs Act, 1962, Section 35-H of the Central Excises and Salt Act, 1944 and Section 82C of the Gold (Control) Act, 1968.

Ravichandran/NADT/Appeal Procedures

Appeals to SC Appeals also lie to the Supreme Court under the

Representation of the People Act, 1951 Monopolies and Restrictive Trade Practices Act, 1969 Advocates Act, 1961 Contempt of Courts Act, 1971 Customs Act, 1962 Central Excises and Salt Act, 1944 Enlargement of Criminal Appellate Jurisdiction Act, 1970 Trial of Offences Relating to Transactions in Securities

Act, 1992, Terrorist and Disruptive Activities (Prevention) Act, 1987

Consumer Protection Act, 1986

Ravichandran/NADT/Appeal Procedures

Enabling provision in IT act (i) Section 257 of Income-tax Act, provides that the

Income-tax Appellate Tribunal can, through its President, refer to the Supreme Court, any question of law on which there is difference of opinion between different High Courts and the question requires to be resolved by the Supreme Court.

Section 261 of Income-tax Act provides for an appeal to the Supreme Court from any judgment of the High Court (delivered on a reference made under Section 256 against an order made under section 254 before 1st October, 1998 or on appeal made to the High Court in respect of an order passed under section 254 on or after that date), in any case which the High Court certifies to be a fit one for appeal to the Supreme Court.

Name Year Territorial establishment jurisdiction Seat

Allahabad 1866 Uttar Pradesh Allahabad (Bench at Lucknow)

Andhra Pradesh 1956 Andhra Pradesh Hyderabad

Bombay 1862 Maharashtra, Goa, Dadra and Nagar Haveli and Daman and Diu

Bombay (Benches at Nagpur, Panaji and Aurangabad)

Calcutta 1862 West Bengal Calcutta (Circuit Bench at Port Blair)

Delhi 1966 Delhi Delhi

Guwahati(2) 1948Assam, Manipur, Meghalaya,

Nagaland,Tripura, Mizoram and Arunachal Pradesh

Guwahati (Benches at Kohima, Aizwal & Imphal. Circuit Bench at Agartala &

Shillong)

Gujarat 1960 Gujarat Ahmedabad

JURISDICTION AND SEAT OF HIGH COURTS

Himachal Pradesh 1971 Himachal Pradesh Shimla

Jammu & Kashmir 1928 Jammu & Kashmir Srinagar & Jammu

Karnataka(3) 1884 Karnataka Bangalore

Kerala 1958 Kerala & Lakshadweep Ernakulam

Madhya Pradesh 1956 Madhya Pradesh Jabalpur (Benches at Gwalior and Indore)

Madras 1862 Tamil Nadu & Pondicherry Madras

Orissa 1948 Orissa Cuttack

Patna 1916 Bihar Patna (Bench at Ranchi)

Punjab & Haryana(4) 1975 Punjab, Haryana & Chandigarh Chandigarh

Rajasthan 1949 Rajasthan Jodhpur (Bench at Jaipur)

Sikkim 1975 Sikkim Gangtok

Ravichandran/NADT/Appeal Procedures

Thank You

Ravichandran/NADT/Appeal Procedures

NTT

Backlog in Indian courts At the current speed, the lower courts, may take 124 years for

clearing 2,50,000 cases. In the last seven years, the disposal rate has increased by 48 per

cent in the high courts and by 28 per cent in the subordinate courts, but the pendency has increased.

The Chief Justices’ Conference has recommended increasing in the working hours of high courts to clear the huge backlog of cases.

Most high courts work for 210 days in a year and it has been recommended to increase it up to 215 or 220

Setting up 463 family courts, one in each district, to deal with matrimonial cases

Setting up one CBI court in each state. There were about 13,000 cases under the Prevention of Corruption Act pending in various high courts out of which 6,100 were CBI cases

Backlog…. Indian judiciary would take 320 years to

clear the backlog of 31.28 million cases pending in various courts including High courts in the country "If one considers the total pendency of cases in the Indian judicial system, every judge in the country will have an average load of about 2,147 cases,”

Backlog… A recent study indicated that the

number of new cases has direct relationship with increasing literacy rate and awareness

Citing example of Kerala, a high literacy state with awareness has 28 new cases per 1000 population per annum have been added, whereas, Bihar with relatively low literacy rate the figure stands at just three

Backlog… India has 14,576 judges as against the sanctioned

strength of 17,641 including 630 High Court Judges. This works out to a ratio of 10.5 judges per million

population The Apex court in 2002 had suggested 50 judges

per million population If the norm of 50 judicial officers per million

becomes reality by 2030 when the country's population would be 1.5 to 1.7 billion, the number of judges would go upto 1.25 lakh dealing with 300 million case.

Article 32… Things had come to a pass in the Supreme Court of

India, when Justice E.S. Venkataramiah in P.N. Kumar v. Municipal Corporation of Delhi, (1987) 4 SCC 609 relegated the writ petitioner under Article 32 to the High Court, without deciding whether any fundamental rights were violated or not, giving, among others, the following reason: “This Court has no time today even to dispose of cases which have to be decided by it alone and by no other authority. A large number of cases are pending from 10 to 15 years. Even if no new case is filed in this Court hereafter, with the present strength of Judges it may take more than 15 years to dispose of all the pending cases.”

Workload of SC Justice P.N. Bhagwati, in Bihar Legal Support Authority

v. Chief Justice of India and Anr., (1986) 4 SCC 767 had this to say: “The Supreme Court of India was never intended to be a regular court of appeal against orders made by the High Court or the sessions court of the magistrates. It was created for the purpose of laying down the law for the entire country and the extraordinary jurisdiction of granting special leave was conferred upon it under Article 136 of the Constitution so that it could interfere whenever it found that the law was not correctly enunciated by the lower courts or tribunals and it was necessary to pronounce the correct law on the subject.”

National Court of Appeals The Constitution Bench had itself felt the need to set up a

National Court of Appeal and observed in the very same judgment thus: “We think that it would be desirable to set up a National Court of Appeal which should be in a position to entertain appeals by special leave from the decisions of the high courts and tribunals in the country in civil, criminal, revenue and labour cases and so far as the present apex court is concerned, it should concern itself only with entertaining cases involving questions of constitutional law and public law.”

Law Commission of India in its 229th Report (2009) recommended the setting up of a Cour de Cassation in each of the four regions to act as a final court with regard to the matters entrusted to it.

Distance to SC Nick Robinson, a Yale Law School Research

Fellow, that 10 per cent of the cases filed in the Supreme Court emanate from Delhi, 6.2 per cent from Punjab and Haryana, and 6.2 per cent from Uttarakhand, with only 1.1 per cent and 2.4 per cent coming from large States like Tamil Nadu and Karnataka.

This would imply that the distance of the Supreme Court from the southern States would, in fact, be an impediment to access to the Supreme Court in Delhi.

Disposal by SC in India, USA &UK

Supreme Court disposes of about 50,000 cases a year

Falls short of the filings that year by about 3,000 to 4,000 cases

U.S. Supreme Court with nine judges sitting en banc is able to dispose of only 80 to 100 cases a year

Erstwhile Judicial Committee of the House of Lords was able to dispose of only about 180 cases a year

NTT Passing of the Forty Second Amendment to the Constitution of India in 1976,

tribunals became key dramatis personae in the justice delivery system For speedy disposal of cases, an array of tribunals were set up. Administrative Tribunals, the Rent Control Tribunals and also Tax Tribunals. Constitution of the National Tax Tribunals, through the passing of the National

Tax Tribunal Act, 2005 in pursuance of Article 323-B (1) (a). Act provides a machinery for the adjudication by the National Tax Tribunal of

disputes with respect to levy, assessment, collection and enforcement of direct taxes and also to provide for the adjudication by that Tribunal of disputes with respect to the determination of the rates of duties of customs and central excise on goods and the valuation of goods for the purposes of assessment of such duties as well as in matters relating to levy of tax on service.

The Act is bound to raise constitutional issues of immense significance as to validity of conferral of the power and functions of the Tribunal, the exercise of such powers and functions, and the concept of judicial review under the Constitution.

Ravichandran/NADT/Appeal Procedures

Thank You