(applicable to with-profits business issued by the prudential group to uk policyholders) · ·...

TRANSCRIPT

Principles & Practicesof Financial Management(Applicable to With-Profits business issuedby the Prudential Group to UK policyholders)

Principles & Practices of Financial Management 3

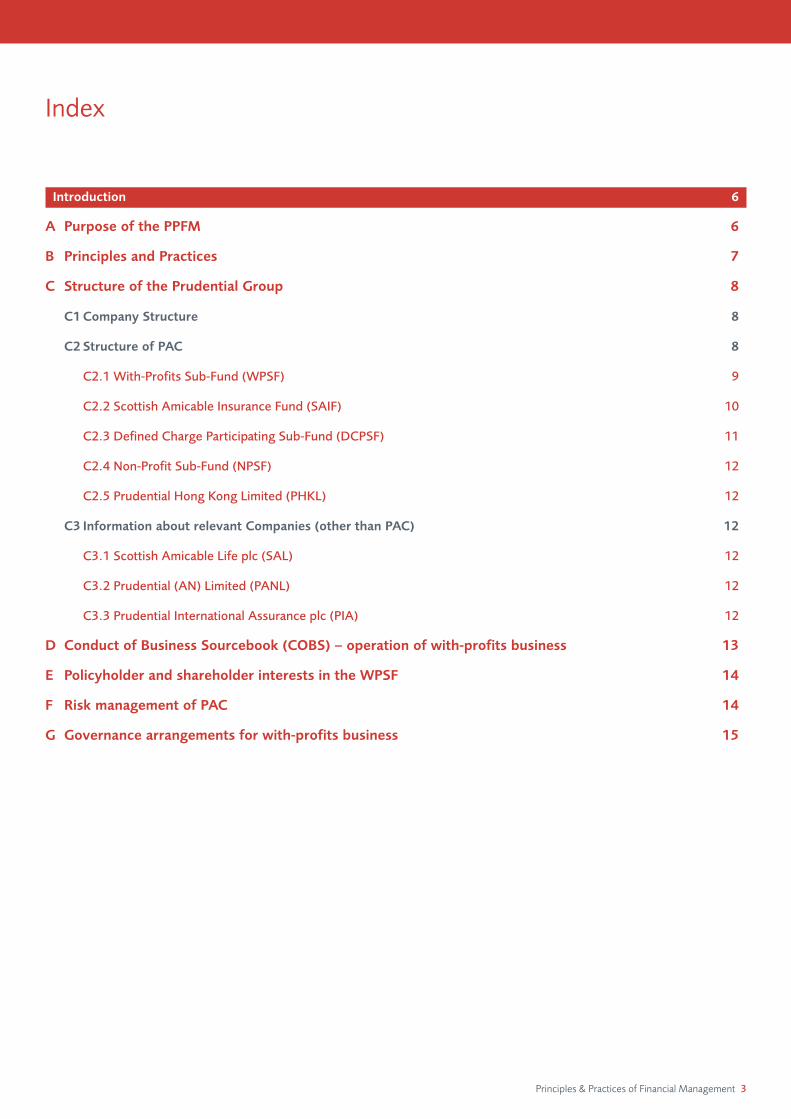

Introduction 6

A Purpose of the PPFM 6

B Principles and Practices 7

C Structure of the Prudential Group 8

C1Company Structure 8

C2 Structure of PAC 8

C2.1 With-Profits Sub-Fund (WPSF) 9

C2.2 Scottish Amicable Insurance Fund (SAIF) 10

C2.3 Defined Charge Participating Sub-Fund (DCPSF) 11

C2.4 Non-Profit Sub-Fund (NPSF) 12

C2.5 Prudential Hong Kong Limited (PHKL) 12

C3 Information about relevant Companies (other than PAC) 12

C3.1 Scottish Amicable Life plc (SAL) 12

C3.2 Prudential (AN) Limited (PANL) 12

C3.3 Prudential International Assurance plc (PIA) 12

D Conduct of Business Sourcebook (COBS) – operation of with-profits business 13

E Policyholder and shareholder interests in the WPSF 14

F Risk management of PAC 14

G Governance arrangements for with-profits business 15

Index

4 Principles & Practices of Financial Management

Principles and Practices of Financial Management 16

1. Determining With-Profits Policy Values 16

1.1 Introduction 16

1.2 Principles 17

1.3 Practices 18

1.3.1 Pay-out values 18

1.3.2 Regular Bonus Rates 18

1.3.3 Final Bonus Rates 19

1.3.4 Smoothing of Maturity and Death Benefits 19

1.3.5 Target ranges for Maturity Benefits 20

1.3.6 Surrender Values and Market Value Reductions (MVRs) 20

1.3.6.1 Accumulating with-profits policies 20

1.3.6.2 Conventional with-profits policies 20

1.3.6.3 Target ranges for surrender benefits 21

1.3.7 Asset share approach 21

1.3.7.1 Overview 21

1.3.7.2 Investment Return 21

1.3.7.3 Tax 21

1.3.7.4 Guarantees and Smoothing 22

1.3.7.5 Mortality and Morbidity 22

1.3.7.6 Shareholder Profit 22

1.3.7.7 Miscellaneous Profits and Losses 23

1.3.7.8 Expenses and Commission 23

1.3.8 Significant variations in practice for specific types of PAC policy 23

1.3.8.1 Business originally issued by Scottish Amicable Life plc (SAL) 23

1.3.8.2 With-Profits Annuity 24

1.3.8.3 Defined Charge Participating Sub-Fund (DCPSF) business (non ELAS) 24

1.3.8.4 Defined Charge Participating Sub-Fund (DCPSF) business (ELAS) 24

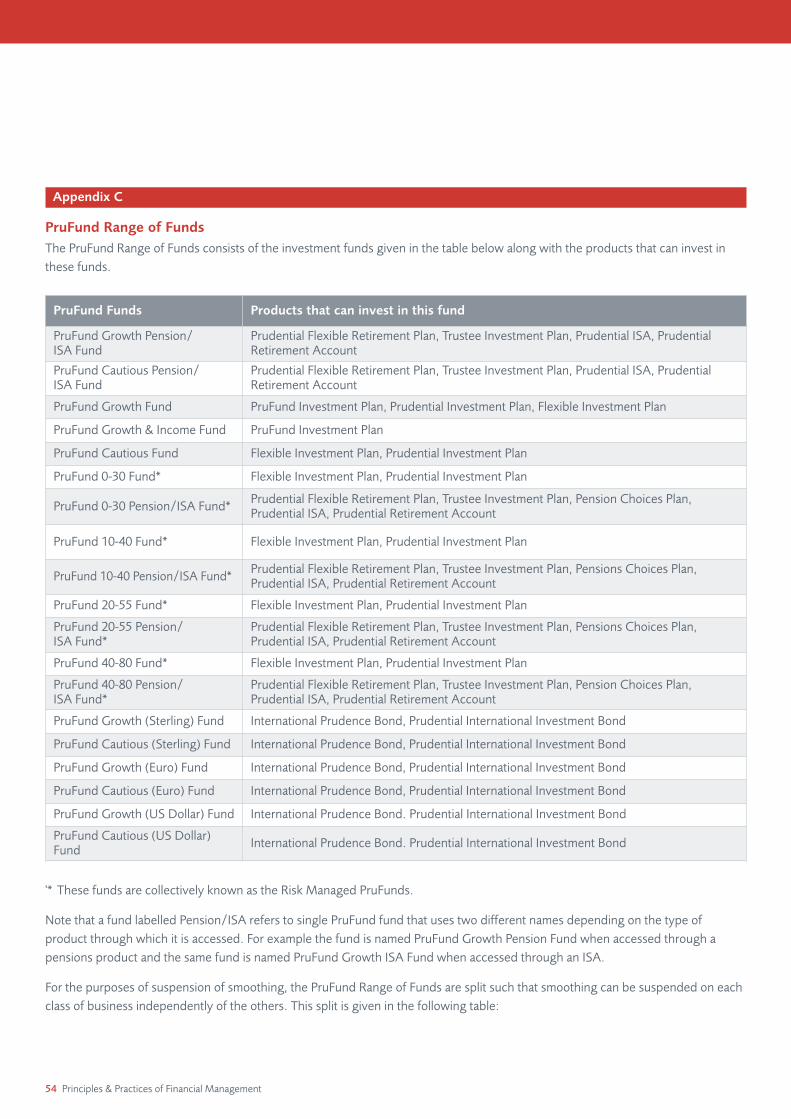

1.3.8.5 PruFund Range of Funds 26

1.3.8.6 Income Choice Annuity 27

1.3.9 New bonus series 28

1.4 Variations for Scottish Amicable Insurance Fund (SAIF) and Scottish Amicable Account (SAA) with-profits policies 30

2. Investment strategy 30

2.1 Introduction 30

2.2 Principles 30

2.3 Practices 30

Principles & Practices of Financial Management 5

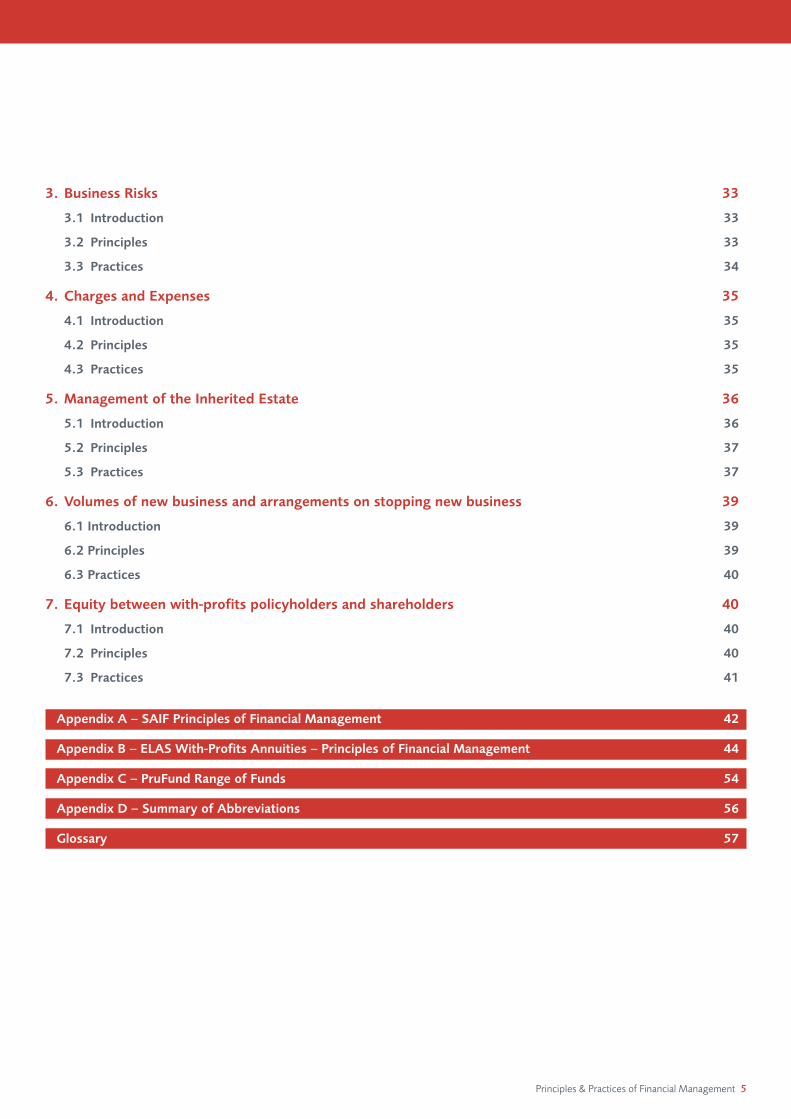

3. Business Risks 33

3.1 Introduction 33

3.2 Principles 33

3.3 Practices 34

4. Charges and Expenses 35

4.1 Introduction 35

4.2 Principles 35

4.3 Practices 35

5. Management of the Inherited Estate 36

5.1 Introduction 36

5.2 Principles 37

5.3 Practices 37

6. Volumes of new business and arrangements on stopping new business 39

6.1 Introduction 39

6.2 Principles 39

6.3 Practices 40

7. Equity between with-profits policyholders and shareholders 40

7.1 Introduction 40

7.2 Principles 40

7.3 Practices 41

Appendix A – SAIF Principles of Financial Management 42

Appendix B – ELAS With-Profits Annuities – Principles of Financial Management 44

Appendix C – PruFund Range of Funds 54

Appendix D – Summary of Abbreviations 56

Glossary 57

6 Principles & Practices of Financial Management

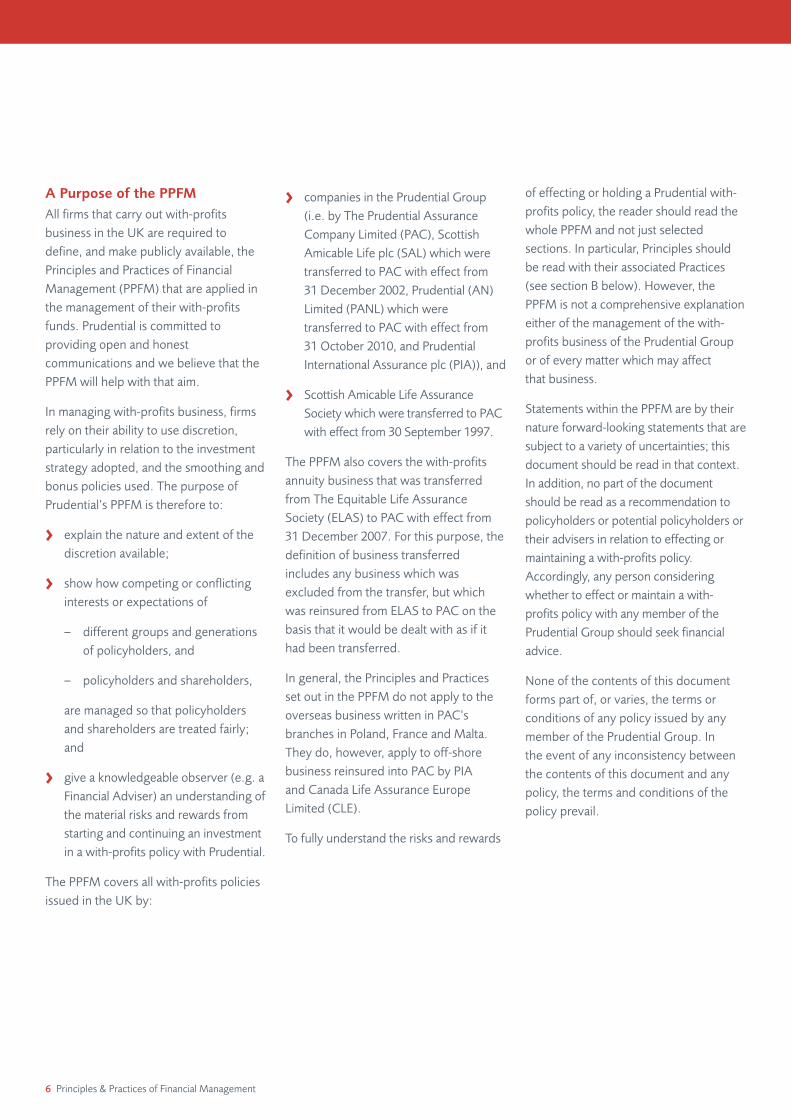

A Purpose of the PPFMAll firms that carry out with-profitsbusiness in the UK are required todefine, and make publicly available, thePrinciples and Practices of FinancialManagement (PPFM) that are applied inthe management of their with-profitsfunds. Prudential is committed toproviding open and honestcommunications and we believe that thePPFM will help with that aim.

In managing with-profits business, firmsrely on their ability to use discretion,particularly in relation to the investmentstrategy adopted, and the smoothing andbonus policies used. The purpose ofPrudential’s PPFM is therefore to:

> explain the nature and extent of thediscretion available;

> show how competing or conflictinginterests or expectations of

− different groups and generationsof policyholders, and

− policyholders and shareholders,

are managed so that policyholdersand shareholders are treated fairly;and

> give a knowledgeable observer (e.g. aFinancial Adviser) an understanding ofthe material risks and rewards fromstarting and continuing an investmentin a with-profits policy with Prudential.

The PPFM covers all with-profits policiesissued in the UK by:

> companies in the Prudential Group(i.e. by The Prudential AssuranceCompany Limited (PAC), ScottishAmicable Life plc (SAL) which weretransferred to PAC with effect from 31 December 2002, Prudential (AN)Limited (PANL) which weretransferred to PAC with effect from 31 October 2010, and PrudentialInternational Assurance plc (PIA)), and

> Scottish Amicable Life AssuranceSociety which were transferred to PACwith effect from 30 September 1997.

The PPFM also covers the with-profitsannuity business that was transferredfrom The Equitable Life AssuranceSociety (ELAS) to PAC with effect from31 December 2007. For this purpose, thedefinition of business transferredincludes any business which wasexcluded from the transfer, but whichwas reinsured from ELAS to PAC on thebasis that it would be dealt with as if ithad been transferred.

In general, the Principles and Practicesset out in the PPFM do not apply to theoverseas business written in PAC’sbranches in Poland, France and Malta.They do, however, apply to off-shorebusiness reinsured into PAC by PIAand Canada Life Assurance EuropeLimited (CLE).

To fully understand the risks and rewards

of effecting or holding a Prudential with-profits policy, the reader should read thewhole PPFM and not just selectedsections. In particular, Principles shouldbe read with their associated Practices(see section B below). However, thePPFM is not a comprehensive explanationeither of the management of the with-profits business of the Prudential Groupor of every matter which may affect that business.

Statements within the PPFM are by theirnature forward-looking statements that aresubject to a variety of uncertainties; thisdocument should be read in that context.In addition, no part of the documentshould be read as a recommendation topolicyholders or potential policyholders ortheir advisers in relation to effecting ormaintaining a with-profits policy.Accordingly, any person consideringwhether to effect or maintain a with-profits policy with any member of thePrudential Group should seek financialadvice.

None of the contents of this documentforms part of, or varies, the terms orconditions of any policy issued by anymember of the Prudential Group. In the event of any inconsistency betweenthe contents of this document and anypolicy, the terms and conditions of thepolicy prevail.

Principles & Practices of Financial Management 7

B Principles and PracticesIn the PPFM we define the Principles andPractices used in managing the UK with-profits business of PAC, which includesoff-shore business acquired by orreinsured into the company (see sectionC below) by PIA and CLE.

> The Principles define the overarchingstandards adopted in managing PAC’swith-profits business to maintain thelong-term solvency of the fund forcurrent and future policyholders anddescribe the approach used:

− in meeting our duty to with-profitspolicyholders, and

− in responding to longer-termchanges in the business andeconomic environment.

> The Practices describe the approachused:

− in managing PAC’s with-profitsbusiness, and

− in responding to changes in thebusiness and economicenvironment in the shorter-term.

The contents of the PPFM are normallyreviewed on a half-yearly basis. Thecontents of the PPFM may be amendedfollowing such a review, either as thecircumstances of the Prudential Groupchange or business or economicenvironments alter, or to reflect newproduct launches, or to reflect changes inthe management of the with-profitsbusiness. Any proposed changes arereviewed by PAC’s With-ProfitsCommittee (WPC) (details of which aregiven in section G below) and are subjectto approval by the PAC Board.

In normal circumstances we would expectto give affected policyholders writtennotice at least 3 months in advance of theeffective date of any material change tothe Principles. However, there may becircumstances when changes will be madewithout notice with the agreement of ourregulators, the Financial ConductAuthority (FCA) and Prudential RegulatoryAuthority (PRA), or their successors.

We expect our Practices to be revisedfrom time to time as both circumstancesand the business environment change.We will notify affected policyholders in areasonable period after the effective dateof any such change, generally in theirnext annual statement.

The most important aspects of the PPFMhave been summarised in customerfriendly form called a Consumer FriendlyPPFM (CFPPFM). We have a smallnumber of different versions, eachappropriate to particular products. All UKwith-profits policyholders who receivedan annual statement following theFebruary 2006 bonus declaration, and allnew UK with-profits policyholders from 1 January 2006, received or will receive aCFPPFM. Policyholders will subsequentlybe notified of any significant changes inthe relevant CFPPFM made as a result ofchanges to the PPFM.

8 Principles & Practices of Financial Management

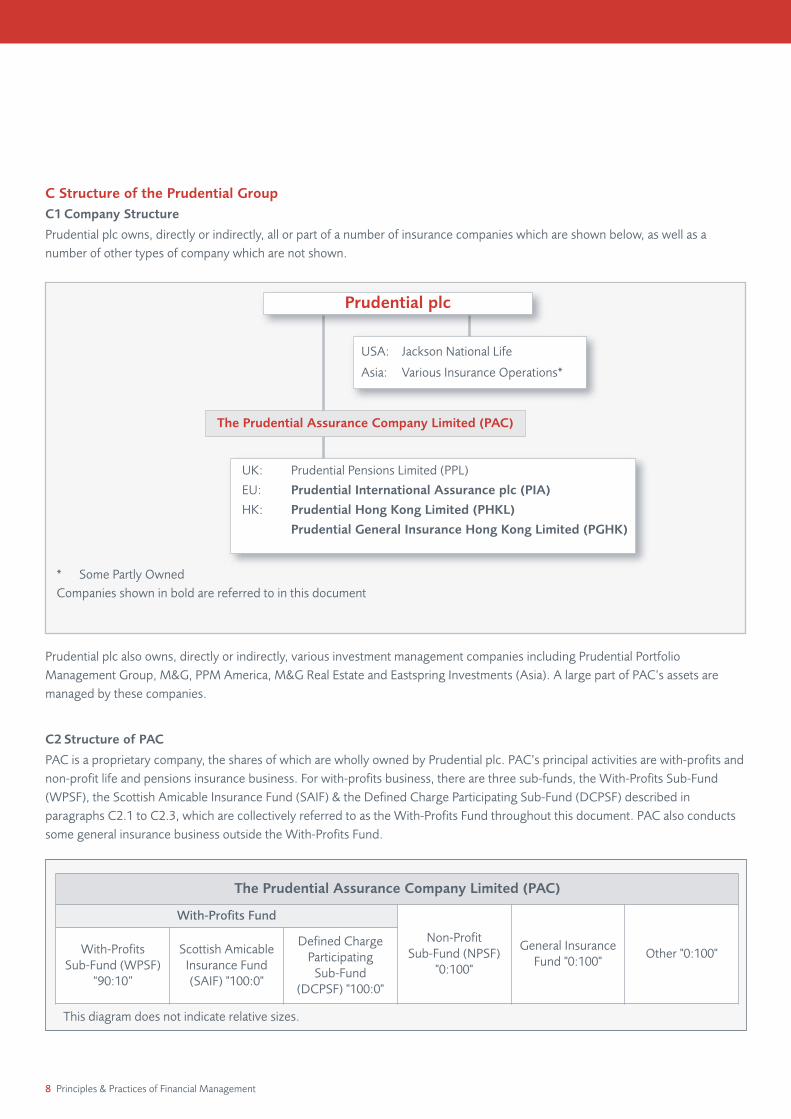

The Prudential Assurance Company Limited (PAC)

With-Profits Fund

Non-Profit Sub-Fund (NPSF)

"0:100"

General InsuranceFund "0:100"

Other "0:100"With-ProfitsSub-Fund (WPSF)

“90:10”

Scottish AmicableInsurance Fund(SAIF) "100:0"

Defined ChargeParticipating Sub-Fund

(DCPSF) "100:0"

This diagram does not indicate relative sizes.

Prudential plc also owns, directly or indirectly, various investment management companies including Prudential PortfolioManagement Group, M&G, PPM America, M&G Real Estate and Eastspring Investments (Asia). A large part of PAC’s assets aremanaged by these companies.

* Some Partly OwnedCompanies shown in bold are referred to in this document

UK: Prudential Pensions Limited (PPL)

EU: Prudential International Assurance plc (PIA)

HK: Prudential Hong Kong Limited (PHKL)

Prudential General Insurance Hong Kong Limited (PGHK)

The Prudential Assurance Company Limited (PAC)

USA: Jackson National Life

Asia: Various Insurance Operations*

Prudential plc

C Structure of the Prudential GroupC1Company Structure

Prudential plc owns, directly or indirectly, all or part of a number of insurance companies which are shown below, as well as anumber of other types of company which are not shown.

C2 Structure of PAC

PAC is a proprietary company, the shares of which are wholly owned by Prudential plc. PAC’s principal activities are with-profits andnon-profit life and pensions insurance business. For with-profits business, there are three sub-funds, the With-Profits Sub-Fund(WPSF), the Scottish Amicable Insurance Fund (SAIF) & the Defined Charge Participating Sub-Fund (DCPSF) described inparagraphs C2.1 to C2.3, which are collectively referred to as the With-Profits Fund throughout this document. PAC also conductssome general insurance business outside the With-Profits Fund.

Principles & Practices of Financial Management 9

PAC’s life and pensions business istransacted mainly in the UK and ispredominantly with-profits.

The UK with-profits business consists of business:

> written directly in PAC,

> transferred into PAC from the ScottishAmicable Life Assurance Society(SALAS) on 30 September 1997 andfrom SAL on 31 December 2002,

> transferred into PAC from ELAS on 31 December 2007, and

> transferred into PAC from PANL on31 October 2010.

PAC also contains with-profits businesswritten outside the UK, comprisingbusiness:

> written by branches of PAC in Poland,France and Malta,

> reinsured into PAC by

– other Prudential Group insurancecompanies, such as PIA, or

– Canada Life Assurance (Europe)Ltd (see paragraph C3.3 below),and

> written by branches of ELAS andtransferred into PAC from ELAS on 31 December 2007.

With-profits business is written in theWith-Profits Fund and consists of with-profits policies which share in the divisibleprofit of PAC as determined each year inaccordance with the company’s Articlesof Association. The constituents of thedivisible profit and the proportionattributable to policyholders may vary byproduct type; the proportion attributableto policyholders in the With-Profits Sub-Fund (see paragraph C2.1 below) may be

varied by the company over time. TheWith-Profits Fund is divided into sub-funds to facilitate the management of thevarious risk-bearing and profit-sharingarrangements that apply.

The profits (if any) available topolicyholders and/or shareholdersvary between the sub-funds asdescribed below.

C2.1 With-Profits Sub-Fund (WPSF)

The With-Profits Sub-Fund (WPSF)consists mainly of with-profits business,which is/was written by:

> PAC, both Ordinary Branch (including Poland and Malta) andIndustrial Branch,

> SAL, and transferred into PAC, and

> PANL, and transferred into PAC.

The WPSF also contains a significantamount of non-profit business, whichconsists of:

> non-profit annuity business that hasarisen from with-profits pensionpolicies that were originally written inthe WPSF,

> non-profit immediate and deferredannuities originally written byPrudential Annuities Limited (PAL)and transferred into the WPSF,

> other non-profit (including unit-linked) business written by PAC thatis not allocated by the Directors to theNon-Profit Sub-Fund (see paragraphC2.4 below), and

> certain types of business originallywritten by SALAS and now containedin the Scottish Amicable Account(SAA), which are:

− the unitised with-profits lifebusiness, other than itsinvestment content which was

transferred to the ScottishAmicable Insurance Fund (SAIF)(see paragraph C2.2 below),

− the non-profit life business, and

− the unit-linked life business.

Prior to 1 October 2014, the WPSFowned PAL, a subsidiary companywriting non-profit annuity business. PAL was established in 1992, but closedto new business in July 2004 as a result of the WPSF reaching its risk limits inrelation to the credit and longevity risksassociated with non-profit annuitybusiness. The long-term insurancebusiness of PAL was transferred to theWPSF on 1 October 2014.

The WPSF contains the PAC inheritedestate. This is the amount of money inthe sub-fund in excess of that which theDirectors of PAC expect to be paid out tomeet obligations to existing policyholders(see sections D and E below). Thebusiness written by PAC’s Polish andMaltese branches is treated on equalterms with PAC’s UK business in relationto the support it receives from the PACinherited estate.

Divisible profit arising in the WPSF,including profit that arises on the non-profit business, is divided between with-profits policyholders and shareholders.The Articles of Association permit up to 5%of the divisible profit to be transferred to acontingency fund before the balance isdivided between policyholders andshareholders. The proportion of divisibleprofit attributable to with-profitspolicyholders in the WPSF is defined bythe Articles of Association as being at least90%, with the balance attributable toshareholders. For virtually all business, thepolicyholders’ proportion is currently 90%.Thus the WPSF is a “90:10” sub-fund.

10 Principles & Practices of Financial Management

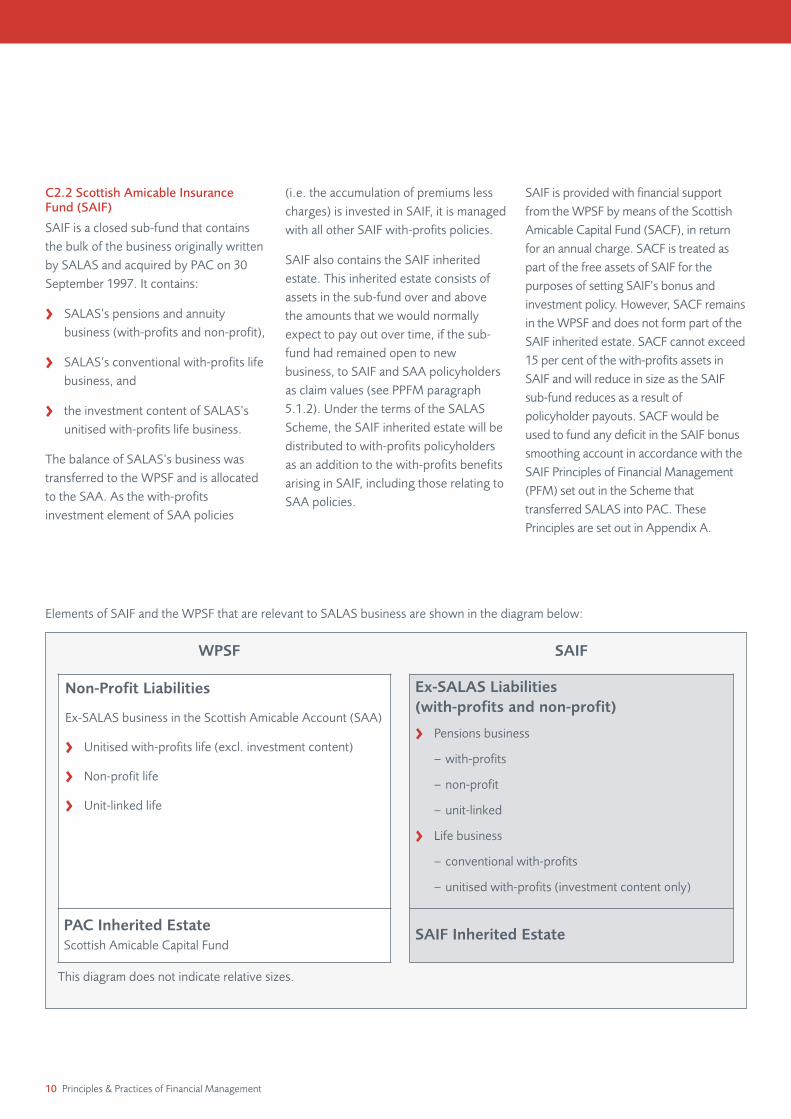

C2.2 Scottish Amicable InsuranceFund (SAIF)

SAIF is a closed sub-fund that containsthe bulk of the business originally writtenby SALAS and acquired by PAC on 30September 1997. It contains:

> SALAS’s pensions and annuitybusiness (with-profits and non-profit),

> SALAS’s conventional with-profits lifebusiness, and

> the investment content of SALAS’sunitised with-profits life business.

The balance of SALAS’s business wastransferred to the WPSF and is allocatedto the SAA. As the with-profitsinvestment element of SAA policies

(i.e. the accumulation of premiums lesscharges) is invested in SAIF, it is managedwith all other SAIF with-profits policies.

SAIF also contains the SAIF inheritedestate. This inherited estate consists ofassets in the sub-fund over and abovethe amounts that we would normallyexpect to pay out over time, if the sub-fund had remained open to newbusiness, to SAIF and SAA policyholdersas claim values (see PPFM paragraph5.1.2). Under the terms of the SALASScheme, the SAIF inherited estate will bedistributed to with-profits policyholdersas an addition to the with-profits benefitsarising in SAIF, including those relating toSAA policies.

SAIF is provided with financial supportfrom the WPSF by means of the ScottishAmicable Capital Fund (SACF), in returnfor an annual charge. SACF is treated aspart of the free assets of SAIF for thepurposes of setting SAIF’s bonus andinvestment policy. However, SACF remainsin the WPSF and does not form part of theSAIF inherited estate. SACF cannot exceed15 per cent of the with-profits assets inSAIF and will reduce in size as the SAIFsub-fund reduces as a result ofpolicyholder payouts. SACF would beused to fund any deficit in the SAIF bonussmoothing account in accordance with theSAIF Principles of Financial Management(PFM) set out in the Scheme thattransferred SALAS into PAC. ThesePrinciples are set out in Appendix A.

Non-Profit Liabilities

Ex-SALAS business in the Scottish Amicable Account (SAA)

> Unitised with-profits life (excl. investment content)

> Non-profit life

> Unit-linked life

PAC Inherited EstateScottish Amicable Capital Fund

Ex-SALAS Liabilities(with-profits and non-profit)

> Pensions business

– with-profits

– non-profit

– unit-linked

> Life business

– conventional with-profits

– unitised with-profits (investment content only)

SAIF Inherited Estate

WPSF SAIF

This diagram does not indicate relative sizes.

Elements of SAIF and the WPSF that are relevant to SALAS business are shown in the diagram below:

Principles & Practices of Financial Management 11

The Scheme which transferred SALASinto PAC states that the ScottishAmicable Funds (i.e. SAIF and SACF)must be managed in accordance with thespecified SAIF PFM. These Principles:

> include the over-arching provisionthat the Scottish Amicable Fundsshould be managed in a sound andprudent fashion,

> provide a framework for settingbonus and investment policy for theScottish Amicable Funds on a basisthat is fair to both SAIF and SAApolicyholders and other PACpolicyholders, and

> require that the SAIF inherited estatebe distributed over time to with-profits policyholders in SAIF and SAA.

The whole of the profit arising in SAIF,including profits or losses on its non-profit business, will be allocated to with-profits policyholders in SAIF and SAA(i.e. SAIF is a “100:0” sub-fund).

C2.3 Defined Charge ParticipatingSub-Fund (DCPSF)

The Defined Charge Participating Sub-Fund (DCPSF) consists of two types of business.

The first type of business is theaccumulated investment content ofpremiums paid (i.e. the accumulation ofpremiums less explicit charges) in respectof the Defined Charge Participatingbusiness, which is either:

> reinsured into PAC from PIA or othercompanies, or

> written through PAC’s French branch(between 1 January 2001 and 31December 2003).

This business is defined as with-profitsbusiness on which policyholders incuronly the charges stated explicitly in thepolicy (which include an annualmanagement charge on the assets heldwithin the DCPSF). The charges on thereinsured PIA business accrue to PIA,which bears all of the correspondingexpenses. The charges on the PACFrance Branch business accrue to theNon-Profit Sub-Fund (NPSF), which bearsall of the corresponding expenses.Hence, the shareholders receive anyprofits or losses arising from thedifference between the charges andexpenses on this business.

Bonus smoothing accounts for businessreinsured in from PIA, and for businesswritten by the French branch, aremaintained in the inherited estate withinthe WPSF. These bonus smoothingaccounts are credited or debited asappropriate with any difference betweenclaim payments made from the DCPSFand the relevant policies’ underlyingasset shares. For International PrudenceBond and Prudential InternationalInvestment Bond business invested in thePruFund Range of Funds (as defined inparagraph 1.3.8.5), the smoothingaccounts are credited or debited asappropriate with any difference betweenthe unit price and the net asset value perunit when units are created or cancelledas a result of premiums being received orclaims being paid. It is intended thatthese smoothing transfers shouldgenerate no net gain to either sub-fundover the long term.

The second type of business in theDCPSF is the with-profits annuitiesbusiness transferred from ELAS on31 December 2007.

For this business, the charges taken aredefined within the ELAS Scheme oftransfer. There is a 1% per annumdeduction from the gross investmentreturn credited to asset shares. Thischarge accrues to the NPSF, which bearsall expenses; hence the shareholdersreceive any profits or losses arising fromthe difference between this charge andthe expenses (including the capitalcharge payable by the NPSF to theWPSF) on this business. In addition,there is a maximum deduction of 0.5%per annum from the gross investmentreturn per annum for the expected costof guarantees. This charge accrues to theinherited estate within the WPSF, whichbears the cost of the guarantees; hencethe inherited estate within the WPSFreceives any profits or losses arising fromthe difference between this charge andthe actual cost of guarantees.

A separate bonus smoothing account forthis business is maintained in the inheritedestate within the WPSF. It is intended thattransfers to and from this account shouldgenerate no net gain or loss to either theWPSF or DCPSF over the long term.Further information on the operation ofthe bonus smoothing account is includedin paragraph 1.3.8.4 of this document.

The profits allocated to the transferringELAS annuities arise from the investmentreturns earned on the underlying assetshares (less the charges described above).

The profit in the DCPSF arises solely frominvestment performance and is entirelyattributable to DCPSF policyholders (i.e.the DCPSF is a “100:0” sub-fund).

12 Principles & Practices of Financial Management

C2.4 Non-Profit Sub-Fund (NPSF)

The NPSF consists of such non-profit andunit-linked business as has been explicitlyallocated to this sub-fund by the Directors.

It also includes non-PIA Defined ChargeParticipating business, excluding thebusiness which was transferred fromELAS. The investment content of theDefined Charge Participating businessheld in the NPSF is allocated to theDCPSF. All charges for the DefinedCharge Participating business held in theNPSF are credited to the NPSF, whichbears all of the expenses of this business.

For the business transferred from ELAS(and which is allocated to the DCPSF), theNPSF is credited with the value of a 1%per annum deduction from the grossinvestment return credited to the ELASasset shares and bears all the expenses ofthis business. The NPSF pays an annualcharge to the PAC inherited estate withinthe WPSF for the use of the economiccapital supporting the business transferredfrom ELAS. This charge is calculated as0.14% per annum of asset shares.

All the profit of the NPSF is attributable to shareholders (i.e. the NPSF is a“0:100” sub-fund).

C2.5 Prudential Hong Kong Limited(PHKL)

Following court approval in Hong Kongand the UK, on 1 January 2014, PACtransferred its existing Hong Kongbranch business to two new Hong Kongincorporated Prudential companies, oneproviding life insurance and oneproviding general insurance, so that theHong Kong business could work moreclosely with Prudential’s other Asianoperations. Following the transfer, PAC ceased to write business in HongKong. All Hong Kong based business

sold from 1 January 2014 is writtendirectly into the Hong Kong incorporatedPrudential companies.

Life insurance policies that were originallytaken out by customers of PAC’s HongKong branch were transferred to the newHong Kong based life insurance company,Prudential Hong Kong Limited (PHKL),together with an appropriate amount ofPAC's assets and liabilities. In practicalterms, since the Hong Kong branch hadboth with-profit and non-profit policies, anappropriate amount was transferred fromboth the WPSF and the NPSF, asnecessary, to cover the requisite assetsand liabilities of those policies. As part of the transfer, Prudential split the inherited estate of the WPSF andtransferred an appropriate amount of it toPHKL. PHKL is a wholly owned subsidiaryof PAC.

The WPSF contains certain non-profitannuity business that was previouslyreinsured to PAL by the WPSF but wasrecaptured in August 2011. In order toachieve an equitable sharing of the risksand rewards of this business betweenPAC and PHKL, as part of the HongKong transfer, a reinsurancearrangement was put in place on 1January 2014 between PAC and PHKLwhereby PAC reinsured a proportionateshare of the PAL and recaptured PALbusiness to PHKL. Following the transferof the long-term insurance business ofPAL to the WPSF on 1 October 2014,this business, which is now in the WPSF,remains reinsured to PHKL.

Following the transfer, the vast majorityof the PAC With-Profits Fund remains inthe UK and in particular, neither SAIF northe DCPSF was split.

General insurance policies sold by theHong Kong branch were transferred toPrudential General Insurance Hong KongLimited (PGHK).

C3 Information about relevantCompanies (other than PAC)

C3.1 Scottish Amicable Life plc (SAL)

SAL was a wholly owned subsidiary of PACuntil it was liquidated in 2011. SAL wroteunit-linked, non-profit and with-profitsbusiness from 1 October 1997 until 31December 2002. At 31 December 2002, its business was transferred into the NPSFwith the with-profits element allocated tothe WPSF. All references in this PPFM toWPSF with-profits business apply to SALwith-profits business unless there is aspecific reference to SAL business.

C3.2 Prudential (AN) Limited (PANL)

PANL was a wholly owned subsidiary ofPAC until it was liquidated in 2012. PANLwrote new with-profits life business from10 December 2002 to 11 August 2004and wrote unit-linked pensions businessuntil 31 October 2010. At 31 October2010 its with-profits business wastransferred into the WPSF and its non-profit business was transferred into theNPSF. Prior to the transfer, its with-profitsbusiness was wholly reinsured to theWPSF and its policies shared in thedivisible profits of the WPSF alongsidePAC policies. All references in this PPFMto WPSF business also apply to thetransferred PANL with-profits business.

C3.3 Prudential InternationalAssurance plc (PIA)

PIA is a wholly owned subsidiary of PACwhich has transacted Defined ChargeParticipating business since March 2002.All of PIA’s with-profits policies(including those written in Germanywhich were transferred to Canada Life

Principles & Practices of Financial Management 13

Assurance (Europe) Ltd with effect from1 January 2003) are reinsured into PAC.The investment content of the reinsuredbusiness is invested in the DCPSF. PIAand CLE pay an annual charge to the PACinherited estate within the WPSF for theuse of the economic capital supportingthis business.

D Conduct of BusinessSourcebook (COBS) – operationof with-profits business”The operation of with-profits business isregulated by the rules and guidance setout in Chapter 20 of the Conduct ofBusiness Sourcebook (COBS) of the FCAHandbook (formerly the FinancialServices Authority). With effect from 1 April 2012, the FSA (our regulator atthat time) made certain changes to therules and guidance set out in Chapter 20of COBS in relation to protecting with-profits policyholders. PAC soughtclarification from the FSA following thesechanges and received IndividualGuidance in relation to the factors it isrequired to take account of on twospecific issues:

> the writing of new business; and

> setting the risk appetite of its With-Profits Fund.

Following handover from the FSA to theFCA, the FCA confirmed during 2013that the Individual Guidance previouslyissued by the FSA remained valid.

On the first issue of factors relevant tothe writing of new business, the FSAconfirmed that PAC is not generallyconstrained in its use of the inheritedestate to support the writing of newbusiness by any requirement to take intoaccount the prospect that existingpolicyholders may otherwise have of

receiving a distribution, or a greaterdistribution, from the inherited estate.The FSA, however, identified thefollowing as constraints on the use of aninherited estate by a with-profits firmsuch as PAC:

> writing new business that is priced onterms that are unlikely to allow theproducts to be self-supporting overtheir duration;

> writing new business that at the timeit is written is self-supporting but willnot foreseeably be sold in sufficientquantities such that the economicvalue of the future margins expectedto emerge is not enough to cover thecosts incurred in acquiring thebusiness; and

> writing new business in volumes thatincrease at such a rapid rate that inthe long term it has an adverse effecton a firm’s financial strength.

In applying the above constraints on theuse of an inherited estate for writing newbusiness, the FSA noted that aproprietary with-profits fund such asPAC’s is not required to take account ofthe tax liability arising on transfers toshareholders from the fund. The FSAfurther clarified that new business is notrequired to be self-supporting in theperiod temporarily following a materialchange in the business environment thatis outside of a firm’s control.

On the second issue, the FSA confirmedthat in setting risk appetite anddetermining its approach to the cost ofguarantees for its with-profits fund, PACis generally not required to take intoaccount the prospect of existingpolicyholders receiving a distribution out of the inherited estate. However, the

FSA identified the following factors asrelevant to the setting of a with-profitsfund’s risk appetite in this context:

> risk appetite should be understood tomean a firm’s long term targetposition for the strength of its with-profits fund, underpinning its bonusand investment policy, which inconjunction with its available workingcapital, defines its ability to take riskfrom time to time;

> the risk appetite of a with-profits fundsuch as PAC’s has to have regard notonly to the financial strength of thefund, but also to representations that have been made by a firm to policyholders;

> whilst there is no requirement to takeaccount of any interest ofpolicyholders in a distribution ofexcess surplus when setting the riskappetite of a with-profits fund such asPAC’s, a firm should not deliberatelyset or change its approach to riskappetite in order to prevent theemergence of excess surplus; and

> if a policy contains a guarantee, thepricing of the product should makeproper allowance at the time it iswritten for the foreseeable cost of the guarantee(s).

Taking into account the IndividualGuidance received from the FSA referredto above, PAC believes that its With-ProfitsFund complies with the rules and guidancein Chapter 20 of COBS. PAC will thereforeinterpret the COBS rules and guidance,and operate the With-Profits Fund, havingregard to the Individual Guidance. Thecomments made in sections E and F belowtake into account the Individual Guidance,and the discussions that accompanied it.

14 Principles & Practices of Financial Management

E Policyholder and shareholderinterests in the WPSFPAC is, and always has been, a proprietarycompany, and the whole of the WPSF islegally and beneficially owned by PAC.

PAC’s WPSF includes an inherited estate.This is the amount of money in the sub-fund in excess of that which PAC expectsto pay out to meet its obligations toexisting policyholders.

The inherited estate represents the majorpart of the working capital of the WPSF. Itis available to support both current andfuture new business in PAC’s with-profitssub-funds, and is used to provide solvencysupport, to allow investment freedom forpolicyholders’ asset shares, and to providethe smoothing and guarantees associatedwith with-profits business. The Directorsseek to manage the PAC inherited estateso that it continues to provide adequateworking capital for the future security andongoing solvency of PAC’s with-profitsbusiness. There is no specific target for thesize of the PAC inherited estate.

Whilst the WPSF remains open and theinherited estate remains fully utilised insupporting current and expected futurenew business, PAC believes thatpolicyholders’ reasonable expectations,and the fair treatment of policyholders,requires that:

(i) policyholders should receive benefitsin line with smoothed asset shares (asdefined in section 1 of the PPFM), orguaranteed benefits if higher, and

(ii) PAC should seek to manage its with-profits business in such a way as tomaintain a strong enough inheritedestate in the WPSF to help protect thesecurity of policyholders’ contractualbenefits, and to allow the continuation

of investment freedom, smoothing andthe meeting of guarantees. It should benoted that, although PAC seeks tomaintain a strong inherited estatethrough the prudent management ofthe risks that it takes on, a reduction inthe size of the inherited estate as aproportion of the WPSF couldnevertheless occur, for example as aresult of adverse market conditions.

In the circumstances where the inheritedestate is fully utilised in supporting currentand expected future new business, PACdoes not consider that policyholders haveany expectation of a distribution of theinherited estate, other than through thenormal process of smoothing and meetingguarantees in adverse investmentconditions. In addition, and as is set out inmore detail in sections 5 and 6 of thePPFM, in such circumstances PAC is not:

(i) required to take into account in settingrisk appetite, and in its approach to thecosts of guarantees, the prospect ofexisting policyholders receiving adistribution out of the inherited estate;or

(ii) constrained in the use of the inheritedestate to support the writing of newbusiness by a requirement to take intoaccount the prospect that existingpolicyholders might otherwise have ofreceiving a distribution, or a greaterdistribution, from the inherited estate.

The approach taken by PAC in relation toconflicts of interest between policyholdersand shareholders in relation to themanagement of the inherited estate isdescribed in section 7 of the PPFM.

The WPSF exists for the purpose of writingnew with-profits business, and managingthe risks inherent in this business for the

benefit of both policyholders andshareholders. On this basis, PAC continuesto write new with-profits business, and tomanage the associated risks within thewith-profits sub-funds, providing that theDirectors of PAC are satisfied that the newbusiness is properly priced, the risks areproperly managed, and the new businessis likely to have no adverse impact on thereasonable benefit expectations of thecompany’s in-force policyholders.

F Risk management of PACIn managing risk, the PAC Board isresponsible for:

(i) determining the company’s riskappetite which, in conjunction with theavailable working capital, determinesthe company’s risk capacity from timeto time, and

(ii) determining the financial managementframework within which the overall risklevel of the company is managed,having regard to that risk capacity, and

(iii) managing the overall risk level of thecompany and the With-Profits Fund,including its three sub-funds, havingregard to that risk capacity and thefinancial management framework.

The WPSF’s risk appetite defines therange of acceptable levels for the sub-fund’s financial strength, and,together with the financial managementframework, underpins how PAC managesits with-profits business, including settingbonus and investment policy (asdescribed in sections 1 and 2 of thePPFM) and the maximum limits, if any,which may be placed on new businessvolumes (as described in section 6 of thePPFM). The risk appetite and financialmanagement framework thereforeprovide the context within which

Principles & Practices of Financial Management 15

decisions in relation to the managementof PAC’s with-profits business, includingthose which may involve conflicts ofinterest between policyholders andshareholders, are taken. Since, asdiscussed in section C above, the DCPSFand SAIF rely on the WPSF’s inheritedestate for capital support, decisions takenby PAC’s Directors regarding the WPSF’srisk appetite, risk capacity and risk level may affect all of PAC’s with-profitspolicyholders.

The WPSF’s risk appetite is set havingregard to policyholders’ reasonableexpectations, based on PAC’s policydocuments, marketing information andother relevant materials. As noted insection E above, whilst the WPSF remainsopen and the inherited estate continues tobe fully utilised in supporting current andexpected future new business, PAC doesnot consider policyholders’ reasonableexpectations to extend to any expectationof a distribution of the inherited estate,other than through the normal process ofsmoothing benefits and meetingguarantees in adverse investmentconditions. Consequently, when settingthe WPSF’s risk appetite, PAC is notrequired to take into account the prospectof existing policyholders receiving adistribution out of the PAC inheritedestate. Although the firm’s risk appetite isnot set having regard to policyholders’contingent interest in any possibledistribution, or greater distribution, of theinherited estate, neither is it set so as todeliberately prevent any possibility of sucha distribution being made.

The WPSF’s risk appetite may be amendedin response to significant changes in thecompany’s long-term financial strength orbusiness environment (such as following achange in the WPSF’s regulatory solvency

requirements). However, the Directorswould consider with-profits policyholders’reasonable expectations at the time ofmaking any change.

With-profits policyholders may beexposed to a range of business andinvestment risks specific to the type ofproduct held; further details are providedin various sections of the PPFM as follows:

> The overall risk level of the With-Profits Fund reflects bothinvestment risk and business risks,which are described in sections 2and 3 respectively.

> The level of investment-related riskfor all business depends on the extentto which the future asset and liabilitycash flows may differ, including theextent to which the capital value ofassets may differ from the value ofthe underlying policy guaranteeswhen those assets are realised to paypolicy benefits. For with-profitsbusiness, this risk is closely inter-related with the bonus distributionpolicy which is described in section 1.

> The risk capacity of the With-ProfitsFund depends on the amount ofworking capital available, which isprovided primarily by the PACinherited estate as described insection 5.

> The amount of working capitalrequired is affected by the type andvolume of new business written, asdescribed in section 6.

The key risk for the With-Profits Fundresults from holding a high proportion ofreal assets (e.g. equities and property) toback smoothed liabilities whichincorporate guarantees (mainly in theform of basic sums assured and theaccumulated regular bonus additions).

As discussed in section 5, the PACinherited estate provides capital supportfor both UK and overseas business, andthe risk level of the WPSF thus reflectsthe aggregate risk level of all of the sub-fund’s with-profits business, includingthat arising in its overseas branches. TheDirectors of PAC seek to ensure the fairtreatment of policyholders in eachterritory, including that:

(i) the business written in each territoryhas a similar aggregate level ofrisk, and

(ii) an appropriate proportion of theinherited estate (which will generallybe held in the UK) is denominated inthe currency of the relevant territory.

G Governance arrangements forwith-profits business In addition to its other responsibilities,the PAC Board is responsible for themanagement of the company’s with-profits business, including investmentand bonus distribution policy. However,the SALAS Scheme established theScottish Amicable Board to beresponsible for the management(including investment and bonus policy)of the Scottish Amicable Funds. TheSALAS Scheme also requires that aMonitoring Actuary be appointed inorder to advise the Scottish AmicableBoard as to the proper operation of theScottish Amicable Funds in order tosafeguard the interests and reasonableexpectations of policyholders invested in SAIF.

16 Principles & Practices of Financial Management

In line with industry-wide regulatoryrequirements, the PAC Board hasappointed:

> a Chief Actuary that provides the PACBoard with certain actuarial advice,and fulfills various statutory dutiesunder the new regulatory reportingregime introduced on 1 January 2016,

> a With-Profits Actuary, who reviewsmaterial relevant to the operation ofthe with-profits business, with thespecific duty to advise the PAC Boardon the reasonableness of howdiscretion has been exercised inapplying the PPFM and how anyconflicting interests have beenaddressed, and

> a With-Profits Committee (WPC),comprising at least three members, all of whom are independent ofPrudential, which provides anindependent assessment of the wayin which Prudential manages its with-profits business and how Prudentialbalances the rights and interests ofpolicyholders and shareholders inrelation to its With-Profits Fund.

The company prepares an annual reportto with-profits policyholders setting outhow it has complied with the PPFM. Thisreport, which is available on request andat www.pru.co.uk/ppfm, includesdetails of how discretion has beenexercised, how any conflicts of interestbetween different groups or generationsof policyholders, and betweenpolicyholders and shareholders, havebeen addressed and a report from theWith-Profits Actuary which stateswhether he or she considers that thereport and the discretion exercised bythe company in the year may beregarded as taking policyholders’interests into account in a reasonable and proportionate manner.

The WPC has the duty to report to thePAC Board, providing an assessment ofcompliance with the PPFM and how anyconflicting rights have been addressed. Ifthe WPC wishes to make a statement towith-profits policyholders in addition tothe company’s report described above,the company will make that reportavailable. In addition, under the Schemethat transferred ELAS business to PAC,the WPC has responsibility for theapplication of some elements ofdiscretion as defined by the Scheme.

Principles and Practices of Financial Management

Section 1 – DeterminingWith-Profits Policy Values1.1 Introduction

1.1.1 The amount of profit available for distribution among with-profitspolicyholders and shareholders, thedivisible profit, is determined annually by the Directors of PAC in accordancewith its Articles of Association.Policyholders receive their distribution of profits by means of bonuses, or other methods as specified in therelevant policy documentation.

1.1.2 Accumulating with-profitspolicyholders (i.e. holders of unitised andcash accumulation products, excludingPruFund) and conventional with-profitspolicyholders receive their share of thedivisible profit by way of bonuses whichare declared, generally yearly, in thefollowing form:

> a regular bonus (also known as anannual or reversionary bonus) whichmay be added during the lifetime of a policy, so gradually increasing theguaranteed benefits, for example thebenefit payable on death, and

> a final bonus (also known as aterminal or additional bonus) whichmay be added to policies when aclaim is paid in a specified period.

The rates of regular and final bonusdeclared are generally different for eachtype of policy. Final bonus rates for eachtype of policy generally vary by referenceto the period, usually a year, in which the policy commenced or each premiumwas paid.

The bonus rates applied to the with-profits annuities transferred from ELASconsist of a regular bonus which is usedto determine the guaranteed annuity, anda combination of an Overall Rate ofReturn (ORR) and an Interim Rate ofReturn (IRR) which is used to determinethe non guaranteed annuity. For thisbusiness the bonus rates do not varyaccording to the period in which thepolicy commenced. Depending on thelevel of regular bonus, ORR and IRRdeclared, the guaranteed annuity andnon-guaranteed annuity may fall afterapplication of the Anticipated Bonus Rate(ABR), and in respect of the non-guaranteed annuity, the GuaranteedInterest Rate (GIR).

PruFund policyholders receive their shareof the divisible profit by means of anincrease in the unit price at the ExpectedGrowth Rate applicable to the selectedfund, subject to adjustments when theunit price moves outside specified limits.Further information on Expected GrowthRates and the returns received byPruFund policyholders is given inparagraph 1.3.8.5 below.

The bonus rates applied to the IncomeChoice Annuity take the form of aSmoothed Return that is used todetermine the non-guaranteed incomeand, if applicable, any increase in theguaranteed income (the Secure Level) as described in paragraph 1.3.8.6.

Principles & Practices of Financial Management 17

1.1.3 A bonus becomes a contractualright only when it has been added to apolicy but it remains subject to thePrinciples and Practices set out below(see in particular paragraph 1.3.6).

1.1.4 This section sets out the Principlesand Practices we use to work out thepay-out values including:

> the methods we use to work out theamount to pay to with-profitspolicyholders,

> the approach we take when we setregular bonus rates.

> the approach we take when we setfinal bonus rates, and

> the approach we take when we setExpected Growth Rates for PruFundbusiness.

1.1.5 The practices set out in paragraphs1.3.1 to 1.3.7 below cover the majority ofwith-profits policies. There are somedifferences in approach for:

> SAIF with-profits policies,

> SAA with-profits policies, and

> some other types of with-profitspolicy, namely:

− policies originally issued by SAL,

− with-profits annuities,

− policies in the DCPSF,

− policies invested in the PruFundRange of Funds, and

− Income Choice Annuity.

Significant differences in practices aresummarised in paragraph 1.4 for SAIFand SAA policies, and in paragraph 1.3.8for other with-profits policies.

1.2 Principles

1.2.1 The company seeks to treat all with-profits policyholders fairly. We aim toprovide:

> pay-out values on death or maturity that are fair between different policy typesand different generations of policyholder, and

> pay-out values on surrender, transfer or retirement (other than at the selectedretirement date) that are also fair between those policyholders leaving and thoseremaining in the sub-fund.

1.2.2 Pay-out values are managed through the bonus declaration process (oralternative profit distribution mechanisms as described in the policy document), withadjustments for surrender and transfer values being made through Market ValueReductions (MVRs) or the surrender value bases, as appropriate.

The main objectives of the company’s bonus distribution policy are:

> to give each with-profits policyholder a return on the premiums paid reflectingthe return on the underlying investments over the time the policyholder has heldthe policy, smoothing the peaks and troughs of investment performance, and

> to ensure that with-profits policyholders in each sub-fund receive a fair share of theprofits distributed from that sub-fund by way of bonus additions to their policies.

1.2.3 To retain flexibility in our investment policy and to protect the With-ProfitsFund, for most types of with-profits product we aim to keep a substantial proportionof pay-out values in non-guaranteed form (i.e. payable as final bonus) and determineregular bonus rates accordingly.

1.2.4We set pay-out values by reference to the earnings of the underlyinginvestments, except where guaranteed minimum benefits increase the total amountpayable.

1.2.5 Final bonus rates are set so that in normal investment conditions pay-outvalues change only gradually over time (i.e. we provide smoothed benefits). Ourapproach to smoothing is not dependent on the type of claim except when an MVRis applied or a change in surrender bases is made.

1.2.6 Our intention is that smoothing profits and losses should balance out overtime, so that in the long run with-profits policyholders in each sub-fund, or within aproduct group with a specific smoothing account, neither gain nor lose as a result ofour smoothing policy. The cumulative cost of smoothing is monitored. The short-term cost of smoothing is constrained only by the impact that smoothing costs haveon the risk level of the sub-fund and hence on the security and reasonable benefitexpectations of continuing policyholders.

1.2.7 Any change to the company’s objectives and the methods used to achievethem, or any material change to the historical assumptions or parameters relevant tothose methods (for example, previously applied investment returns, charges, orallocations of miscellaneous surplus), will be made as and when they are consideredto be appropriate and compatible with treating customers fairly, and only with theapproval of the Directors. Any change in respect of SAIF or SAA policies would alsobe approved by the Scottish Amicable Board and, in addition, court approval may berequired if the SAIF Principles of Financial Management need to be changed. Certainchanges in respect of the with-profit annuities transferred from ELAS would require

18 Principles & Practices of Financial Management

in investment returns associated withinflation rates that were generally lowerthan had been experienced in the 1970sand 1980s.

1.3.2.2 Regular bonus rates aredeclared, normally in February, for theforthcoming bonus declaration year for:

> all WPSF unitised with-profitsproducts (except SAA and SALunitised life with-profits products),

> DCPSF unitised with-profits products,and

> SAIF unitised with-profits pensionproducts.

These bonuses are added daily to eachpolicy but the rates of future accrual maybe changed at any time during the bonusdeclaration year.

Regular bonus rates are declared,normally in February, in respect of theprevious calendar year for:

> WPSF conventional with-profitsproducts,

> SAA and SAL unitised life with-profitsproducts,

> SAIF conventional with-profitsproducts, and

> With-profit annuities transferred from ELAS.

For these latter products (except thosewith-profit annuities transferred fromELAS) an interim bonus rate is alsodeclared for claims arising after the endof the calendar year but prior to thedeclaration for that year. For annuitiestransferred from ELAS, an IRR is declared

review and approval by the With-ProfitsCommittee, and in certain circumstancescourt approval may be needed.

1.3 Practices

1.3.1 Pay-out values

1.3.1.1 To meet our objectives for pay-out values, we target them on the assetshares (see paragraph 1.3.7) of samplepolicies or groups of sample policies. Ingeneral, and where appropriate, eachsample policy represents only thosepolicies which share a common rate offinal bonus (i.e. policies of a particulartype which were either issued in thesame year or for which a premium waspaid in that year). However, where suchsample policies would each represent acomparatively small number of policies,we produce scales of final bonus ratesthat are targeted on the aggregate assetshares across groups of sample policies.Asset shares are calculated for allsignificant blocks of business.

1.3.1.2 The asset share of a samplepolicy is a fair value of the assets backingthe policy, and is calculated byaccumulating the premiums paid (lessallowance for expenses and/or charges)at the actual rates of investment returnearned on the underlying assets over thelifetime of the policy (allowing for theeffect of tax on the investment returnsand of tax relief on expenses for lifebusiness), making appropriate allowancefor miscellaneous profits and losses.

1.3.1.3 When the Ordinary Branch (OB)assets and the Industrial Branch (IB)assets were merged in 1988, thecompany undertook to link IB policybonuses to OB policy bonuses as follows:

> for IB policies issued before July1988, total bonus additions will not beless than 90% of those oncorresponding OB policies; and

> for IB policies issued from July 1988,total bonus additions will be 100% ofthose on corresponding OB policies.

Hence IB pay-out values depend on thecorresponding OB pay-out values and donot reflect the IB asset shares, unless theIB value would produce a higher amountfor business issued before July 1988. Therelationship between IB and OB assetshares is reviewed annually.

1.3.2 Regular Bonus Rates

1.3.2.1 Rates of regular bonus aredetermined for each type of policyprimarily by targeting them at a prudentproportion of the long-term expectedfuture investment return on theunderlying assets. The expected futureinvestment return is reduced asappropriate for each type of policy toallow for items such as expenses,charges, tax and shareholders’ transfers.However, the rates declared may differby product type, or by date of paymentof the premiums or date of issue of thepolicy, if the accumulated annual bonusesare particularly high or low relative to aprudent proportion of the achievedinvestment return.

When target bonus levels change, thePAC Board has regard to the overallfinancial strength of the With-ProfitsFund when determining the length oftime over which it will seek to achieve theamended prudent target bonus level.Regular bonuses were gradually reducedbetween 1991 and 2004 to reflect the fall

Principles & Practices of Financial Management 19

which is intended to give credit for theexpected investment return after the end of the calendar year until the nextpolicy anniversary.

For WPSF cash accumulation products,the regular bonus rates declared,normally in February, apply for the yearending on the scheme revision datewhich falls in the next bonus year.

1.3.2.3 In normal investmentconditions, we expect changes to regularbonus rates to be gradual over time andchanges are not expected to exceed 1%p.a. over any year. However, theDirectors retain the discretion whether ornot to declare a regular bonus each year,and there is no limit on the amount bywhich regular bonus rates can change. Ifthe WPSF was operating materiallyoutside of its risk appetite, the PAC Boardwould expect to take a range ofmanagement actions to address this.Reductions in annual bonuses wouldtypically be one of the actions that wouldbe taken.

1.3.3 Final Bonus Rates

1.3.3.1 A final bonus, which is normallydeclared yearly, may be added when aclaim is paid, or when units of a unitisedproduct are realised.

> Final bonus scales for WPSF andDCPSF unitised with-profits productsand all SAIF and SAA products maybe varied at any time. In particular,additional bonus declarations toreduce these bonus scales might benecessary (as part of a range ofmanagement actions) if the WPSFwas operating materially outside of itsrisk appetite.

> Final bonus scales for WPSFconventional with-profits products aredeclared for policies becoming claimsin the forthcoming bonus period,usually a year.

1.3.3.2 The rates of final bonus usuallyvary by type of policy and by referenceto the period, usually a year, in which thepolicy commenced or each premium waspaid. These rates of final bonus aredetermined by reference to the assetshares for the sample policies or groupsof sample policies described in paragraph1.3.1.1, but subject to the smoothingapproach described in paragraphs1.3.4.1, and 1.3.4.2.

In general the same final bonus scaleapplies to maturity, death and surrenderclaims except that:

> the total surrender value may beimpacted by the application of anMVR (for accumulating with-profitsbusiness) and is affected by thesurrender bases (for conventionalwith-profits business), and

> for SAIF and SAA policies, andpolicies transferred from SAL, thefinal bonus rates applicable onsurrender may be adjusted to reflectexpected future bonus rates.

Further details are given in paragraphs1.3.6 and 1.3.8.1 below.

1.3.3.3 There may be an additionalbonus on retirement for certainconventional with-profits deferredannuity contracts. Any additional bonus,which is dependent on sex and age atretirement, would increase the annuity.The rate of additional bonus for futureretirements may be varied at any time.

1.3.4 Smoothing of Maturity andDeath Benefits

1.3.4.1 The smoothing approach differsbetween accumulating and conventionalwith-profits policies as follows:

For accumulating with-profits policies(i.e. unitised and cash accumulation with-profits policies):

> Pay-out values are smoothed primarilyby looking at the change in the pay-out value on sample policies from oneyear to the next. However, we mayalso consider the change in pay-outvalues on sample policies of the sameduration from one year to the next.

For conventional with-profits policies:

> Pay-out values are smoothed primarilyby looking, for sample policies, at thechange from one year to the next inthe maturity values of correspondingpolicies of the same duration.However, we may also consider thechange in the pay-out value on samplepolicies from one year to the next and,for deferred annuity policies, in thepension payable at vesting.

1.3.4.2 In normal circumstances we donot expect most pay-out values onpolicies of the same duration to changeby more than 10% up or down from oneyear to the next, although some largerchanges may occur to balance pay-outvalues between different policies.Greater flexibility may be required incertain circumstances, for examplefollowing a significant rise or fall inmarket values (either sudden or over aperiod of years), and in such situationsthe PAC Board may decide to vary the

20 Principles & Practices of Financial Management

standard bonus smoothing limits toprotect the overall interests ofpolicyholders. Such a situation arose inFebruary 2009 when pay-out values onmost equivalent policies were reduced byamounts greater than 10% (i.e. outside ofthe normal limits).

1.3.5 Target ranges for MaturityBenefits

1.3.5.1 We set a target range for thematurity payments that we shall make onour with-profits policies, expressed as apercentage of asset shares. The targetrange we use is 80% – 120%.

1.3.5.2 We have set this range as itallows us to target stable bonus rates andallows a reasonable degree of flexibilityto smooth returns in periods of marketvolatility. It also provides greater certaintyto policyholders and minimises the risk ofcustomers not receiving their fair share ofthe fund return or of receiving paymentswhich are more than the fund can affordto the detriment of the remainingpolicyholders.

1.3.5.3 For all policies where it isreasonable to determine payouts basedon asset shares we manage our businesswith the aim of ensuring that maturitypayments for at least 90% of with-profitspolicies fall within the target range. In certain circumstances it is notreasonable to determine payouts basedon asset shares (e.g. for IB policies, see paragraph 1.3.1.3).

1.3.5.4 In setting target ranges, we usesample policies for all product types. Thisapproach is consistent with the approachoutlined in 1.3.1. We do not expect therange of maturity benefits relative toasset shares to be materially differentfrom the range that would apply if allpolicies were considered.

1.3.5.5 Bonus declarations are normallymade with the intention that at least 90%of maturity payments are expected to fallwithin the target range in the periodcovered by the declaration. However,any substantial movement in the marketvalue of the assets of the relevant with-profits sub-fund may take a significantproportion of pay-out values outside thetarget ranges. This may lead to a mid-year bonus declaration to bring morepay-out values within the target range.

1.3.6 Surrender Values and MarketValue Reductions (MVRs)

The approach to surrender values differsbetween accumulating and conventionalwith-profits policies.

1.3.6.1 Accumulating with-profitspolicies

> Surrender values are generally thepay-out values described in paragraph1.3.4, less any discontinuance charge(also known as an early cash-in charge)that may be applied in accordancewith the policy provisions. However,we may then apply an MVR to ensurethat neither the security of the sub-fund nor the return to continuingpolicyholders is affected by payingsurrender values significantly in excessof the value of the underlying assets.

> An MVR may apply if:

− a policy is surrendered (partly or wholly),

− benefits are taken from a pensionpolicy either before or after theselected retirement date,

− an investment is switched out of a with-profits investment fund into another fund (including theconversion of a with-profitsannuity (issued by PAC) to a non-profit annuity), or

− regular withdrawals are taken.

> The amount of any MVR on a policywill vary as the value of the sub-fund’s assets changes.

> It is not our practice to apply MVRswhich reduce surrender values belowan amount fairly reflecting the valueof the assets underlying the policy.

> On some policies, the impact of anyMVR is reduced as policies approachmaturity with the aim of ensuring thatsurrender values progress smoothlyinto maturity values. Typically, this isdone over the last 5 years of thepolicy.

> All accumulating with-profits policiesprovide some specific guarantees atcertain times – for example on death,terminal illness or the pre-selectedretirement date. At these times noMVR can apply.

> Partial withdrawals are normallysubject to an MVR; however, regularautomatic withdrawals may have beenset up with a guarantee that no MVRwill apply. On a partial withdrawal, theasset share of the remaining part ofthe policy is not adjusted to reflect anydifference between the surrendervalue and the asset share of the partsurrendered (i.e. the asset share isreduced by the proportion that thewithdrawal amount bears to the policyvalue before any MVR deduction).

1.3.6.2 Conventional with-profitspolicies

> Surrender values are derived by wayof a formula, the parameters of whichare set to broadly target asset shares– over the long term, less anydeductions necessary to protect theinterests of existing policyholders.The formula is based on the sum

Principles & Practices of Financial Management 21

1.3.7 Asset share approach

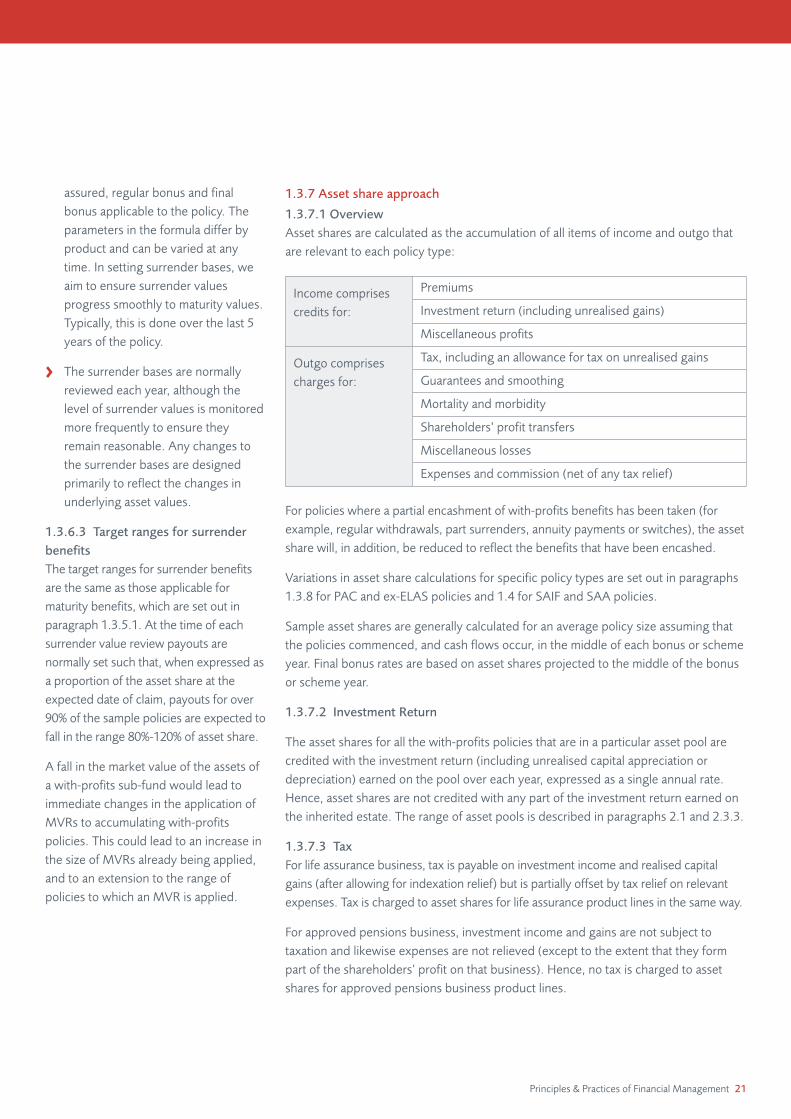

1.3.7.1 OverviewAsset shares are calculated as the accumulation of all items of income and outgo thatare relevant to each policy type:

Income comprisescredits for:

Premiums

Investment return (including unrealised gains)

Miscellaneous profits

Outgo comprisescharges for:

Tax, including an allowance for tax on unrealised gains

Guarantees and smoothing

Mortality and morbidity

Shareholders’ profit transfers

Miscellaneous losses

Expenses and commission (net of any tax relief)

assured, regular bonus and finalbonus applicable to the policy. Theparameters in the formula differ byproduct and can be varied at anytime. In setting surrender bases, weaim to ensure surrender valuesprogress smoothly to maturity values.Typically, this is done over the last 5years of the policy.

> The surrender bases are normallyreviewed each year, although thelevel of surrender values is monitoredmore frequently to ensure theyremain reasonable. Any changes tothe surrender bases are designedprimarily to reflect the changes inunderlying asset values.

1.3.6.3 Target ranges for surrenderbenefitsThe target ranges for surrender benefitsare the same as those applicable formaturity benefits, which are set out inparagraph 1.3.5.1. At the time of eachsurrender value review payouts arenormally set such that, when expressed asa proportion of the asset share at theexpected date of claim, payouts for over90% of the sample policies are expected tofall in the range 80%-120% of asset share.

A fall in the market value of the assets ofa with-profits sub-fund would lead toimmediate changes in the application ofMVRs to accumulating with-profitspolicies. This could lead to an increase inthe size of MVRs already being applied,and to an extension to the range ofpolicies to which an MVR is applied.

For policies where a partial encashment of with-profits benefits has been taken (forexample, regular withdrawals, part surrenders, annuity payments or switches), the assetshare will, in addition, be reduced to reflect the benefits that have been encashed.

Variations in asset share calculations for specific policy types are set out in paragraphs1.3.8 for PAC and ex-ELAS policies and 1.4 for SAIF and SAA policies.

Sample asset shares are generally calculated for an average policy size assuming thatthe policies commenced, and cash flows occur, in the middle of each bonus or schemeyear. Final bonus rates are based on asset shares projected to the middle of the bonusor scheme year.

1.3.7.2 Investment Return

The asset shares for all the with-profits policies that are in a particular asset pool arecredited with the investment return (including unrealised capital appreciation ordepreciation) earned on the pool over each year, expressed as a single annual rate.Hence, asset shares are not credited with any part of the investment return earned onthe inherited estate. The range of asset pools is described in paragraphs 2.1 and 2.3.3.

1.3.7.3 TaxFor life assurance business, tax is payable on investment income and realised capitalgains (after allowing for indexation relief) but is partially offset by tax relief on relevantexpenses. Tax is charged to asset shares for life assurance product lines in the same way.

For approved pensions business, investment income and gains are not subject totaxation and likewise expenses are not relieved (except to the extent that they formpart of the shareholders’ profit on that business). Hence, no tax is charged to assetshares for approved pensions business product lines.

22 Principles & Practices of Financial Management

PAC is assessed for tax as a singleshareholder-owned entity and the taxapportioned to sub-funds fairly, subject tothe requirements that:

> the amount charged to SAIF is theamount that SAIF would pay if it weretaxed as a mutual life assurancecompany. In effect any differencebetween the tax otherwise fairlyapportionable to SAIF and the amountcharged to SAIF falls to the PACinherited estate, and

> the amounts charged to each of theWPSF and DCPSF are not greater thanthose which would be charged if eachsub-fund individually comprised theentire with-profits fund of a UKproprietary life insurance company.

Any difference between the tax charged toasset shares in each sub-fund and theoverall amount of tax charged to that sub-fund falls into the PAC inherited estate orthe SAIF inherited estate as appropriate.

The tax rates assumed in calculating assetshares are amended when tax rateschange. They are also reviewedperiodically and may be retrospectivelyadjusted to reflect any significantcumulative difference between the tax charged to asset shares and the total tax paid in respect of thecorresponding policies.

1.3.7.4 Guarantees and SmoothingFor new WPSF business, an analysis iscarried out from time to time to determinecharges for smoothing and guarantees thatthe Directors of PAC believe arereasonable and fair for each type ofproduct. The resulting charges arededucted in calculating asset shares andcredited to the PAC inherited estate, whichbears the costs of smoothing andguarantees as they emerge.

On policies other than with-profits annuity,Income Choice Annuity or those investedin the PruFund Range of Funds, the totaldeduction charged to asset shares over thelifetime of each policy is not currently morethan 2% of asset shares, with the deductionbuilding up to this level over the first fewyears of the policy.

For with-profits annuity contracts providedby PAC a deduction is made from theinvestment return credited to asset shareseach year. This deduction is derived so thatin aggregate its value is expected to coverthe costs of guarantees over the lifetime ofthe portfolio of this business.

For Income Choice Annuity a deduction ismade from the investment return creditedto asset shares each year and anadjustment may also be made to the levelof starting income. This adjustment may bepositive or negative. The deduction fromthe investment return and the adjustmentsto starting income levels are derived sothat, in aggregate, their value is expectedto cover the cost of guarantees over thelifetime of the policy.

The deductions made to cover the cost ofsmoothing and guarantees for newbusiness are regularly reviewed and maybe adjusted, for example in line withmarket conditions, changes in assetallocation and/or changes in business mix.The level of these charges can rise or fall asa result of these reviews.

For in-force business, the company keepsthe level of charges under review and mayalter these if necessary to protect thesolvency of the With-Profits Fund.

For investments in the PruFund Range ofFunds, see 1.3.8.5 for further information.

For the business transferred from ELASand allocated to the DCPSF, a deduction ofup to 0.5% p.a. is made from the

investment return credited to asset shares.This charge is transferred from the DCPSFto the WPSF and, in return, the WPSFmeets the cost of guarantees. This chargeis kept under review and may be amendedbut cannot exceed 0.5% p.a.

1.3.7.5 Mortality and MorbidityFor WPSF, SAIF and SAA business, amortality charge is deducted in calculatingasset shares. This charge is calculated byapplying a mortality rate to the excess ofthe benefit on death over the current valueof the policy. Any difference between theaggregate mortality charge and the cost ofdeath claims each year accrues to theappropriate inherited estate. A similarapproach applies for morbidity costs.

For the business transferred from ELAS, tothe extent that actual payments of incomeare less or more than expected in anycalendar year because of heavier or lightermortality than expected, the profit or losswill accrue to the WPSF. Should Prudentialadopt a different mortality basis for thisbusiness, the effect of this change on theasset shares is subject to certain limitswhich are described in Appendix B.

1.3.7.6 Shareholder ProfitFor a WPSF with-profits policy, the amounttransferred to shareholders in respect ofthe bonuses credited to the policy isdeducted in calculating asset shares. Thebasis of determining the amount to betransferred is described in paragraph7.3.1. There is no such charge to the assetshare of a DCPSF, SAIF or SAA policy.

Additional tax is payable as a consequenceof the transfer of shareholder profits out ofthe WPSF. This has always been chargedto the PAC inherited estate and it isexpected that this will continue subject tothe security of the sub-fund remainingsatisfactory when the tax is paid (seeparagraph 5.3.2.1).

Principles & Practices of Financial Management 23

1.3.7.7 Miscellaneous Profitsand Losses For WPSF business, miscellaneous profitsand losses are reflected in asset shares as follows:

> Profits and losses from:

> non-profit annuity business, written inthe WPSF and also that transferred tothe WPSF from PAL, written between 1January 2000 and 30 June 2004, withthe exception of Prudential PersonalRetirement Plan (PPRP) vestings, and

> certain other non-profit UK businesswritten in the WPSF

are allocated each year to all UK with-profits product lines (other than thePruFund Range of Funds) as an addition ordeduction in the calculation of asset shares.

> Aggregate profits, or losses, ondiscontinuance of with-profits policies(other than profits or losses fromsmoothing) are calculated each year forcertain product groups and credited tosurviving policies in the calculation ofasset shares for that product group.This aggregate profit or loss is thedifference, in respect of discontinuingpolicies, between the asset shareallowing for the expenses incurred inrunning the business and the assetshare allowing for the charges taken to cover these expenses. Theseexpenses include the actual cost ofshareholder transfers.

> Aggregate profits, or losses, that mayemerge from any other UK businessrisk will be credited each year to assetshares across all UK product lines(other than the PruFund Range ofFunds), unless the Directors havedecided that specific losses should beborne by the PAC inherited estate (seeparagraph 3.3.4).

1.3.7.8 Expenses and Commission As described in paragraphs 1.3.7.6 and3.3.4, certain costs allocated to the WPSFare charged to the PAC inherited estateand not to asset shares.

All other expenses, including commission,allocated to the WPSF are split intoacquisition and administration expenses,and expressed as some or all of a rate per policy, a rate per cent of premium,a rate per cent of sum assured and as a reduction in the investment return. Therelevant combination of these expenserates is normally deducted in calculatingasset shares.

However, the net impact of the charges toasset shares for expenses and for items 1.3.7.5 to 1.3.7.7 above is limited as follows:

> for all new business since 1997, theaggregate projected deductions equalsthe aggregate projected policy-specificcharges used when illustrating benefitsat point of sale, while

> for many pension contracts, the netimpact of these deductions has beenlimited to 1% p.a. since April 2001; thislevel of charge is not guaranteed toapply in future, and

> for certain other personal pension andcorporate pension policies, an annualrate of charge is applied; the currentlevel of charge is not guaranteed toapply in future.

Up to 31 December 2011 the excess ofany costs incurred in excess of theamounts charged to asset shares (alsoreferred to as cost over-runs) was borne bythe PAC inherited estate. However, from 1January 2012 onwards, the PAC Board hasdecided that new business in the WPSFshould be priced such that it is expected tobe financially self supporting over the

lifetime of the business at the point thepricing assumptions are set. Where thebusiness is not expected to be financiallyself-supporting at the point the pricingassumptions are set, shareholders willmake an appropriate contribution to theWPSF. In considering whether newbusiness is self-supporting, it should benoted that:

(i) the test of self-supporting does notinclude the tax liability arising fromshareholder transfers on that business.As described in section 5.3.2.1 of thePPFM, this tax will be charged to thePAC inherited estate subject to thesecurity of the sub-fund remainingsatisfactory when the tax is paid; and

(ii) new business may temporarily not beself-supporting, resulting in cost over-runs which are borne by the PACinherited estate, following a materialchange in the business environmentwhich is outside of the firm’s control.This reflects the fact that businesscannot necessarily be re-pricedimmediately, and that the change inbusiness environment (for example amarket fall) may, in good faith, bebelieved to only be temporary.

1.3.8 Significant variations in practicefor specific types of PAC policy

1.3.8.1 Business originally issued byScottish Amicable Life plc (SAL)In calculating asset shares:

> the only relevant items of income andoutgo are premiums, investmentreturn, charges for tax, guarantees andsmoothing, mortality and morbidity,and the explicit charges for expensesand profit specified on similar unit-linked policies; and

24 Principles & Practices of Financial Management

> credit for miscellaneous profit will be given only if the asset sharescalculated using explicit charges with no allowance for miscellaneousprofit are less than the asset sharescalculated using actual expenses withallowance for miscellaneous profit andthe distribution of profit to PAC shareholders.

If the difference between the chargesdeducted and the expenses incurred is less than the actual shareholder transfer,then this deficit accrues to the PACinherited estate.

The final bonus rates for surrenders maydiffer from those for death or maturityclaims to reflect expected future bonus rates.

1.3.8.2 With-Profits Annuity Asset shares are calculated by means of aretrospective accumulation of premiumspaid, allowing for actual investmentreturns (net of charges, including thosetaken to cover the cost of guarantees)and the deduction of unsmoothedannuity payments. Asset shares are alsoadjusted to reflect the respreading ofmortality surplus each year arising fromreleases of asset shares on deaths (theamount which is respread is based on thedifference between the actual andexpected mortality experience for theperiod under review). The unsmoothedannuity represents the annuity that wouldbe paid before smoothing is applied andwithout allowance for any minimumguarantee that might apply.

The regular bonus declared each year hasa permanent effect on the incomereceived. This income will increase if thebonus declared is higher than theanticipated bonus rate selected by the

policyholder or (subject to the minimumincome guarantee) decrease if the bonusdeclared is lower than the anticipated rate.