applied finance centre faculty of business …...2018/07/17 · applied finance centre faculty of...

TRANSCRIPT

1

1APPLIED FINANCE CENTRE

APPLIED FINANCE CENTREFaculty of Business and Econom ics

FTAWebinarWeightedAverageCostofCapital:Part217July,2018

Presentedby:TonyCarltonAssociateProfessor&ProgramDirector,CorporateFinanceMacquarieAppliedFinanceCentre

2APPLIED FINANCE CENTRE

Tony CarltonApplied Finance Centre, Macquarie UniversityAssociate Professor & ProgramDirector, Corporate Finance

Tony is responsible for managing the Corporate Finance stream in the prestigiousMaster of Applied Finance. Prior to joining the Applied Finance Centre Tony had over25 years' experience in the manufacturing, resource and agricultural industries. Hisexperience includes all aspects of corporate finance and strategy, including projectevaluation, strategic portfolio analysis and restructuring, and the development andexecution of growth strategies. He managed a number of large acquisitions anddivestments both in Australia and overseas, and a number of large scale balancesheet restructurings.

In the Masters of Applied Financeprogram, Tony presents the CoreCorporate Finance course, andelective subjects including AdvancedValuation, Managing ShareholderValue and Corporate Fin ancialStrategy. He completed his PhD atMacquarie University in 2015.

2

3APPLIED FINANCE CENTRE

ü RecapofPart1

q ChallengesinapplyingWACC(continued)

q WACCandFinancialStrategy

q IssuesinestimatingWACC

q SourcesofinformationforcalculatingWACC

Agenda

Part2

4APPLIED FINANCE CENTRE

WACCmeasuresthereturnsrequiredbyinvestorsinanasset

RecapofPart1

q UsedinDiscountedCashFlow(DCF)valuations

q TheWACCisdeterminedby thecharacteristicsofthecashflowsbeingvalued– primarilyrisk anddebtcapacity

q OperatingFreeCashFlowsdiscountedatWACCtogiveEnterprise (orAsset)Value

q EnterpriseValue =Equity+ Debt

q WhenusingWACC,EquityValueisdeterminedasaResiduali.e.Equity=EnterpriseValue – Debt

3

5APPLIED FINANCE CENTRE

WACCmeasuresthereturnsrequiredbyinvestorsinanasset

Where:Re istheCostofEquity forthecashflowsbeingvalued;

Rd istheCostofDebtusuallyestimatedascurrentborrowingrate;

Tisthemarginalcorporatetaxrate,importantbecauseinterestistaxdeductibleandequityisnot.Thismeansthat,forsensibledebtlevels,WACCreducesduetotaxbenefitofinterestdeductions;

D/V isthetargetdebtcapacityofthecashflowsbeingvalued,,whereDisDebtisexpressedaspercentageofEnterpriseValue,V.Targetgearingisexpressedinmarketvalueterms

RecapofPart1

6APPLIED FINANCE CENTRE

CostofEquityiskeyinputintoWACCcalculation

Costof equityisestimatedusingtheCapitalAssetPricingModel

Where:

Re istheCostOfEquity:returnrequiredbyshareholdersallowingfortheriskinessoftheproject;

Rf istheRiskFreeRate:usuallyestimatedascurrentlongtermgovernmentbondyield,ideallytomatchthetermoftheinvestment.

istheinvestment’sBeta.Itmeasuresthesensitivityofaninvestment’sreturnstochangesintheoverallmarket,andisameasureofrelativerisk.AnassetwiththesameriskasthemarkethasaBetaof 1.Thisistheriskthatcannotbeeliminatedbydiversification;

MRPistheMarketRiskPremium,anestimateoftheadditionalreturnsthatinvestorsrequiretoinvestintheoverallmarketcomparedtoinvestinginriskfreeassets(whichhaveaBetaofzero).InAustralia,anMRPof6%ismostcommonlyused.

Re = Rf + β x MRP

RecapofPart1

4

7APPLIED FINANCE CENTRE

SampleCalculation:WACCforNewCrest

Input Data Weighted InputtoWACC

TargetGearing 11%

CostofDebtx(1– Taxrate)

6%x(1– 0.30) 4.20% 4.20%x11% 0.46%

CostofEquity 3%+0.73x6.5%

7.75% 7.75%x89% 6.90%

WACC 7.36%

RecapofPart1

8APPLIED FINANCE CENTRE

WACCbasedvaluationsusedinwiderangeofapplications

Application Whichmeans Howused

CapitalAllocation

EquityValuation

Impairment Testing

Performance measurement

RegulatoryPricing

RecapofPart1

5

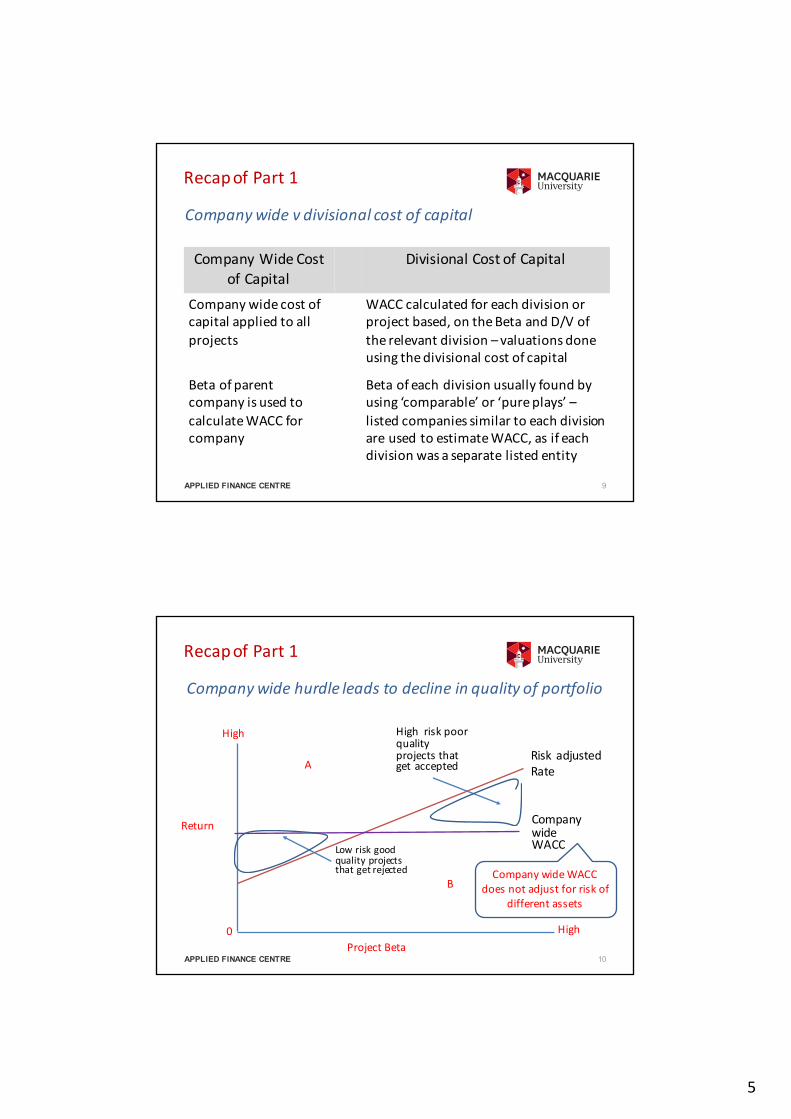

9APPLIED FINANCE CENTRE

Companywidevdivisionalcostofcapital

Company WideCostofCapital

DivisionalCostofCapital

Company widecostofcapitalappliedtoallprojects

WACCcalculatedforeachdivisionorprojectbased,ontheBetaandD/V oftherelevantdivision– valuationsdoneusingthedivisionalcostofcapital

Betaofparentcompanyis usedtocalculateWACCforcompany

Betaofeachdivisionusuallyfoundbyusing‘comparable’or‘pureplays’–listedcompaniessimilartoeachdivisionareusedtoestimateWACC,asifeachdivisionwasaseparatelistedentity

RecapofPart1

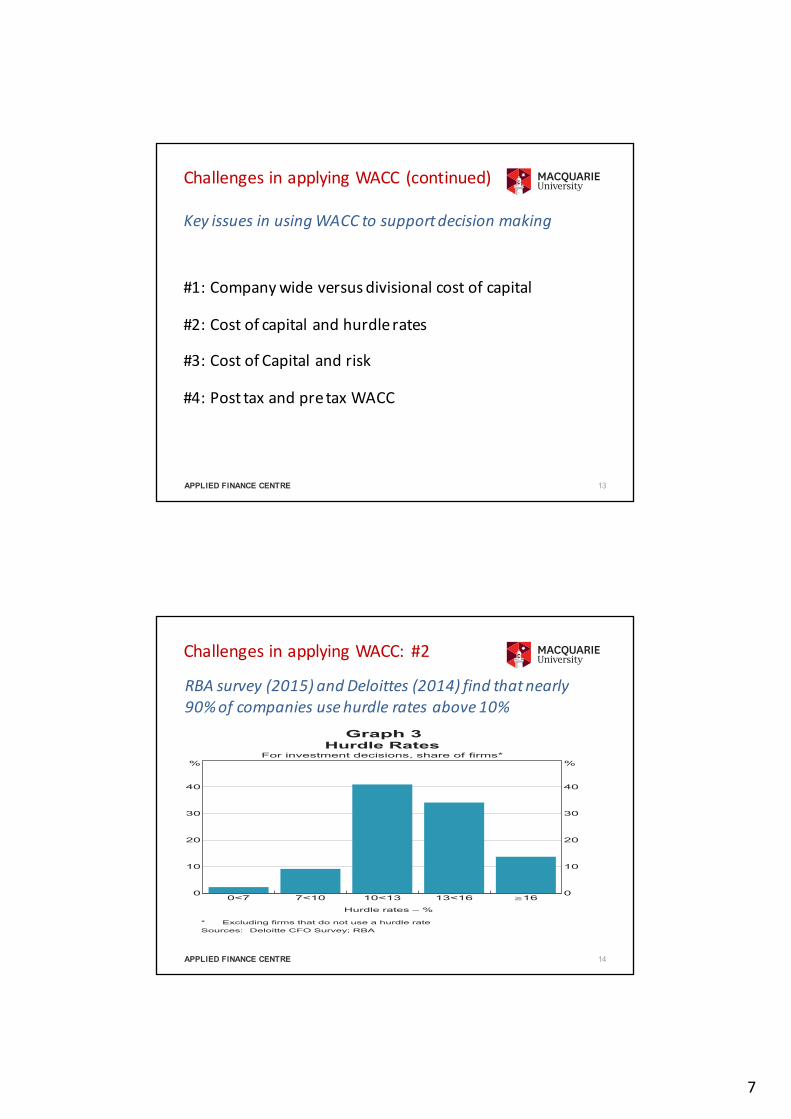

10APPLIED FINANCE CENTRE

Companywidehurdleleadstodeclineinqualityofportfolio

ProjectBeta

Return

0

High

High

CompanywideWACC

RiskadjustedRate

Lowriskgoodqualityprojectsthatgetrejected

HighriskpoorqualityprojectsthatgetacceptedA

BCompanywideWACC

doesnotadjustforriskofdifferentassets

RecapofPart1

6

11APPLIED FINANCE CENTRE

Companywidevdivisionalcostofcapital- example

Calculatethecostofcapitalforaprospective investmentintheaquacultureindustry.Assumethisinvestmenthasatarget[Debt/Value]ratioof10%;

Step: Result

[1]Findcomparables Threegoodcomparables inAustralia:Tassal,HuonandCleanSeas

[2]Calculatethe‘Ungeared’or‘Asset’Beta

AssetBetais0.59- refernextslide#1.Thisisthesystematicriskoftheassetwithzerodebt

[3]Calculatethe“Geared’or‘equity’Beta,uisng thetargetgearing

Regeared Betais0.63 - referfollowingslide#2.ThisisanEquityBetawithDebt/ValueRatioequalto10%[Note:D/E=10/90]

[4]CalculateWACC ofTargetAsset WACCis6.80% - referfollowingslide #2

RecapofPart1

12APPLIED FINANCE CENTRE

q RecapofPart1

ü ChallengesinapplyingWACC(continued)

q WACCandFinancialStrategy

q IssuesinestimatingWACC

q SourcesofinformationforcalculatingWACC

Agenda

Part2

7

13APPLIED FINANCE CENTRE

KeyissuesinusingWACCtosupportdecisionmaking

ChallengesinapplyingWACC (continued)

#1:Companywideversusdivisionalcostofcapital

#2:Costofcapitalandhurdlerates

#3:CostofCapitalandrisk

#4:PosttaxandpretaxWACC

14APPLIED FINANCE CENTRE

RBAsurvey(2015)andDeloittes (2014)findthatnearly90%ofcompaniesusehurdleratesabove10%

3BULLETIN | J U N E Q UA R T E R 2015

FIRMS’ INVESTMENT DECISIONS AND INTEREST RATES

of years it would take for the capital outlay to be returned by the cash flows generated by the project. Although the payback period is intuitive and easy to communicate, it does not take into account the time value of money and ignores cash flows beyond the chosen cut-off date.

Evidence from Australian FirmsA typical firm in the Bank’s liaison program evaluates discretionary capital expenditure by using DCF analysis, and also by considering the payback period as a supporting consideration. This is in line with the evidence from other advanced economies such as the United States and the United Kingdom (see below) and is also in line with earlier survey evidence for Australia. For instance, a survey of Australian firms conducted by academics in 2004 also found that the vast majority of firms used both methods, which, according to other surveys, had become more popular over the preceding decades (Graph 2).

These observations are broadly in line with recent evidence from the Deloitte CFO Survey, which found that nearly 90 per cent of the Australian corporations that responded used hurdle rates exceeding 10 per cent, and around half of the corporations used a hurdle rate exceeding 13 per cent (Deloitte 2014; Graph 3). Liaison contacts reason that the hurdle rate is often set above the cost of capital to account for uncertainty about the cash flow projections. Contacts also note that there is likely to be an optimism bias in these cash flow projections. As a result, setting a hurdle rate above the cost of capital is likely to improve the chances that investments add value to the firm on a risk-adjusted basis.4

Many liaison contacts also report that hurdle rates are not changed very often and in some instances have not been altered for at least several years. These observations are also reflected in the recent survey by Deloitte; two-thirds of corporations indicated their hurdle rate was updated less frequently than their formal review of the WACC, and nearly half reported the level of their hurdle rate was changed ‘very rarely’ (Graph 4). For these firms, changes in

4 Adjusting for risk by using a higher discount rate rather than by probability weighting the cash flows introduces a bias against longer-term projects, since the present value of a longer-dated cash flow is more sensitive to changes in the discount rate.

Graph 2

Discounted cash flow analysis

Liaison contacts indicate that the hurdle rates used to evaluate business investment opportunities are often several percentage points above the WACC. Hurdle rates of around 15 per cent are quite common, though the range of rates reported is relatively wide, from a little less than 10 per cent up to 30 per cent.

Graph 3

0<7 7<10 10<13 13<16 !160

10

20

30

40

%

0

10

20

30

40

%

Hurdle RatesFor investment decisions, share of firms*

Hurdle rates – %

* Excluding firms that do not use a hurdle rateSources: Deloitte CFO Survey; RBA

ChallengesinapplyingWACC: #2

8

15APPLIED FINANCE CENTRE

q USFederalReserve (2013)reportthatasampleofUScompanieshaveaveragehurdlerateof14.1%(whenBBByieldswere4%)

q ForUS,Jagannathan etal(2013)findhurdleratesexceedWACCbyupto8%

q Hurdlerateshashardlychangedinprevious10years,inspiteofinterestratedeclines– impliesitisusedasa“ruleofthumb”ratherthanavaluationtool

q Highergrowthfirmshavehigherhurdlerates,andarelesssensitivetointerestratechanges– becausemarginalreturnsarerelativelyattractive

q Investmentplansnotsensitivetochangesininterestrates

Pervasiveroleofhurdlerates

ChallengesinapplyingWACC: #2

16APPLIED FINANCE CENTRE

Pervasiveroleofhurdlerates–OECDfindadeclineinUserCostofCapitalhasnotdrivenuptickinG7capital investment

Source:OECDEconomic Outlook,Vol 2015, Issue1,Chapter3“LiftingInvestmentforHigherSustainable Growth”

ChallengesinapplyingWACC: #2

9

17APPLIED FINANCE CENTRE

q Allowanceforoptimism:Ø BuildsingamingØ BiasesagainstlongtermprojectsØ NotsupportedbyevidenceØ Doesitixtheissue?

q Allowanceforrisk:

Ø NobasisforadjustmentØ LosesTransparency

q DesiretoearngreaterthanWACCØ Valuemaximisedbymaximisingvaluecreation(i.e.acceptallpositive

NPVprojects.TryingtomaximiseROICorotherratiosdoesnotmaximiseVALUECREATION

q Ruleofthumbthathasworked

(Dubious)Rationalesforhurdlerates

ChallengesinapplyingWACC: #2

18APPLIED FINANCE CENTRE

q Preservefinancialflexibilitybyavoidinggoingtocapitalmarkets,especiallyformarginalprojects:

Ø Costofaccessingmarketseasilyadds1%- 1.5%torequiredreturn

Ø USsurveyfindsfinanciallyconstrainedcompaniestendtohavelowerhurdlerates

q Allowanceforoptionality:

Ø Decisionrulesforoptionsgrossuprequiredreturnforvolatility,soonlyveryinthemoneyprojectsgetaccepted,othersdelayed

Ø Decisionrulesincorporatingoptionsjustifypremiumof2%- 4%overWACC

q Allowanceforoperationalconstraints– I.E.ITISPRIMARILYAMANAGERIALDEVICERATHERTHANAVALUATIONTOOL

Ø USsurveyfindsthistobemostsignificantexplanation

(Justifiable)Rationalesforhurdlerates

ChallengesinapplyingWACC: #2

10

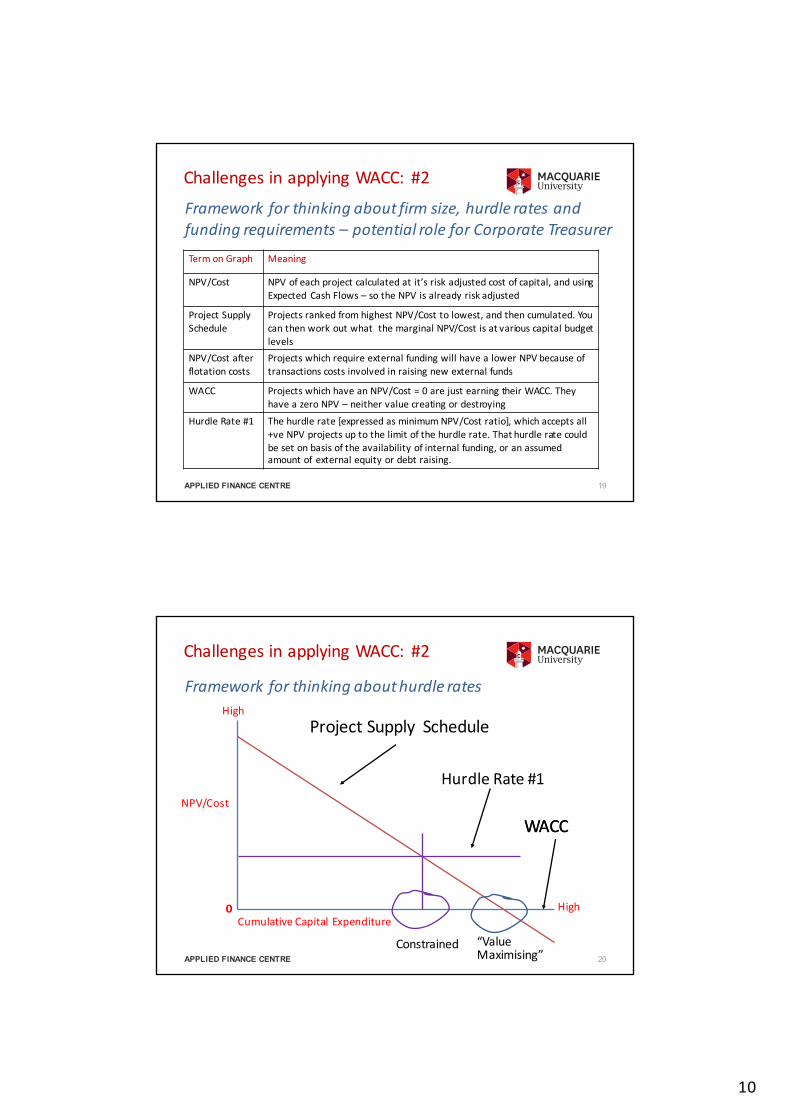

19APPLIED FINANCE CENTRE

TermonGraph Meaning

NPV/Cost NPVofeachprojectcalculatedatit’sriskadjustedcostofcapital,andusingExpected Cash Flows– sotheNPVisalreadyriskadjusted

ProjectSupplySchedule

ProjectsrankedfromhighestNPV/Cost tolowest,andthencumulated.YoucanthenworkoutwhatthemarginalNPV/Costisatvariouscapitalbudgetlevels

NPV/Costafterflotationcosts

ProjectswhichrequireexternalfundingwillhavealowerNPVbecauseoftransactionscostsinvolvedinraisingnewexternalfunds

WACC Projects whichhaveanNPV/Cost=0arejustearningtheirWACC.TheyhaveazeroNPV– neithervaluecreatingordestroying

HurdleRate#1 Thehurdle rate[expressedasminimumNPV/Costratio],whichacceptsall+ve NPVprojectsuptothelimitofthehurdlerate.Thathurdleratecouldbesetonbasisoftheavailabilityofinternalfunding,oranassumedamountof externalequityordebtraising.

Frameworkforthinkingaboutfirmsize,hurdleratesandfundingrequirements– potentialroleforCorporateTreasurer

ChallengesinapplyingWACC: #2

20APPLIED FINANCE CENTRE

Frameworkforthinkingabouthurdlerates

CumulativeCapitalExpenditure

NPV/Cost

00

High

High

ProjectSupply Schedule

WACC

HurdleRate#1

WACC

“ValueMaximising”

Constrained

ChallengesinapplyingWACC: #2

11

21APPLIED FINANCE CENTRE

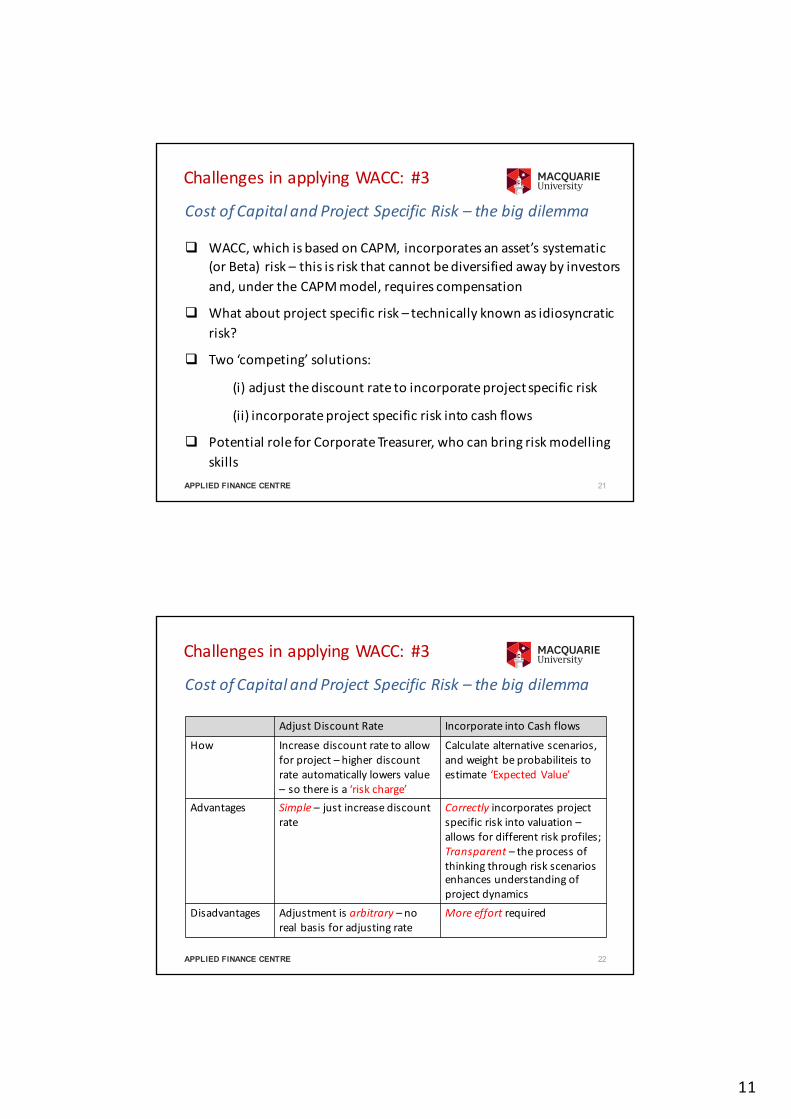

q WACC,whichisbasedonCAPM,incorporatesanasset’ssystematic(orBeta) risk– thisisriskthatcannotbediversifiedawaybyinvestorsand,undertheCAPMmodel,requirescompensation

q Whataboutprojectspecificrisk– technicallyknownasidiosyncraticrisk?

q Two‘competing’solutions:

(i)adjustthediscountratetoincorporateprojectspecificrisk

(ii)incorporateprojectspecificriskintocashflows

q PotentialroleforCorporateTreasurer,whocanbringriskmodellingskills

CostofCapitalandProjectSpecificRisk– thebigdilemma

ChallengesinapplyingWACC: #3

22APPLIED FINANCE CENTRE

CostofCapitalandProjectSpecificRisk– thebigdilemma

AdjustDiscountRate IncorporateintoCashflows

How Increasediscountrateto allowforproject– higherdiscountrateautomaticallylowersvalue– sothereisa‘riskcharge’

Calculate alternativescenarios,andweightbeprobabiliteis toestimate ‘ExpectedValue’

Advantages Simple – justincreasediscountrate

Correctly incorporatesprojectspecificriskintovaluation–allows fordifferentriskprofiles;Transparent – theprocessofthinkingthroughriskscenariosenhancesunderstandingofprojectdynamics

Disadvantages Adjustmentisarbitrary– norealbasisforadjustingrate

Moreeffortrequired

ChallengesinapplyingWACC: #3

12

23APPLIED FINANCE CENTRE

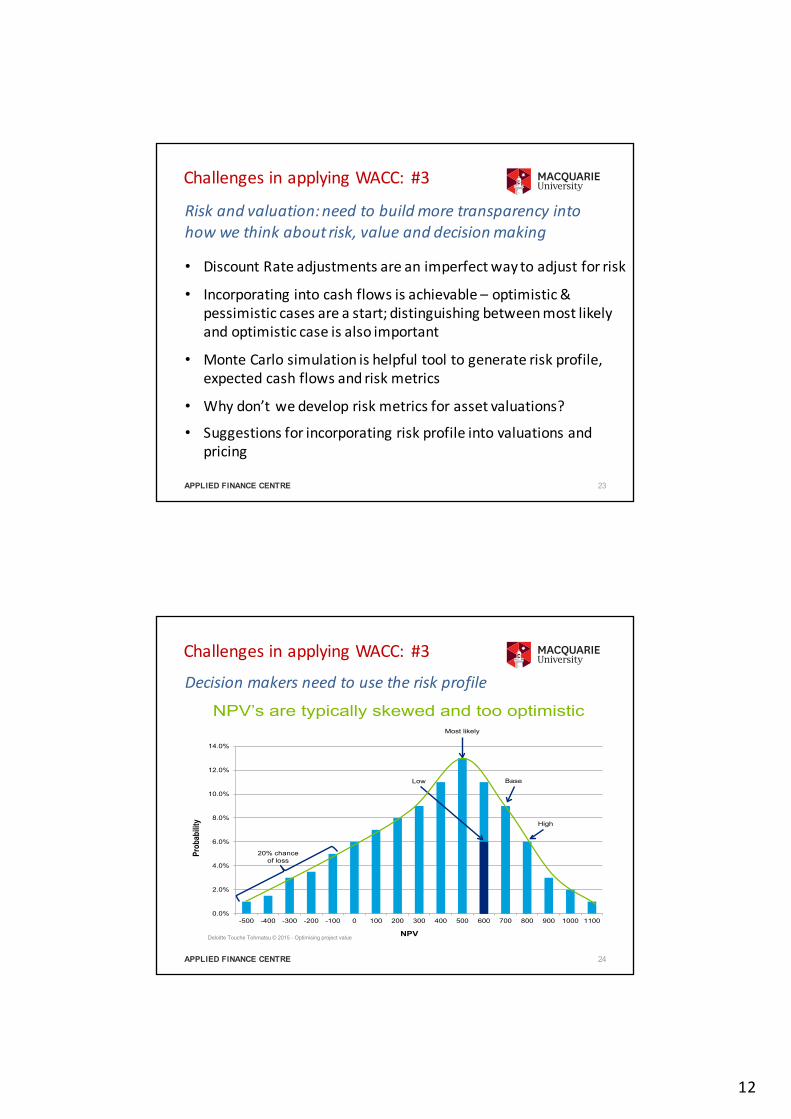

Riskandvaluation:needtobuildmoretransparencyintohowwethinkaboutrisk,valueanddecisionmaking

ChallengesinapplyingWACC: #3

• DiscountRateadjustmentsareanimperfectwaytoadjustforrisk

• Incorporatingintocashflowsisachievable– optimistic&pessimisticcasesareastart;distinguishingbetweenmostlikelyandoptimisticcaseisalsoimportant

• MonteCarlosimulationishelpfultooltogenerateriskprofile,expectedcashflowsandriskmetrics

• Whydon’twedevelopriskmetricsforassetvaluations?

• Suggestionsforincorporatingriskprofileintovaluationsandpricing

24APPLIED FINANCE CENTRE

Decisionmakersneedtousetheriskprofile

Deloitte Touche Tohmatsu © 2015 - Optimising project value

NPV’s are typically skewed and too optimistic

6

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-500 -400 -300 -200 -100 0 100 200 300 400 500 600 700 800 900 1000 1100

Prob

abili

ty

NPV

Most likely

High

Low Base

20% chance of loss

Deloitte Touche Tohmatsu © 2015 - Optimising project value

NPV’s are typically skewed and too optimistic

6

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

-500 -400 -300 -200 -100 0 100 200 300 400 500 600 700 800 900 1000 1100

Pro

bab

ility

NPV

Most likely

High

Low Base

20% chance of loss

ChallengesinapplyingWACC: #3

13

25APPLIED FINANCE CENTRE

Mostrequireuseofprobabilitydistributionofvalue,andthereforesomeriskmodelling

Suggestions DefinitionSharpestyleratio EnterpriseValue/𝜎"#MorganStanleyBull&Bearprice BaseCase isprobabilityweighted,usingResidualIncome

valuation;Downside&Upside scenariospublished

Ruback Incorporatesdownsidescenariointoforecasts

Bancel & Tierney[Cash Flow@Risk]

ValueMinimumCashFlow@debtrate+Excess cashflows@CostofEconomic Capital

Deduct Economic CapitalfromValue

Determine Economic Capitaltocoverspecificdownsideanddeductfrom value;Downsidecanbemeasuredintermsofvalueor‘x’yearsahead

ChallengesinapplyingWACC: #3

26APPLIED FINANCE CENTRE

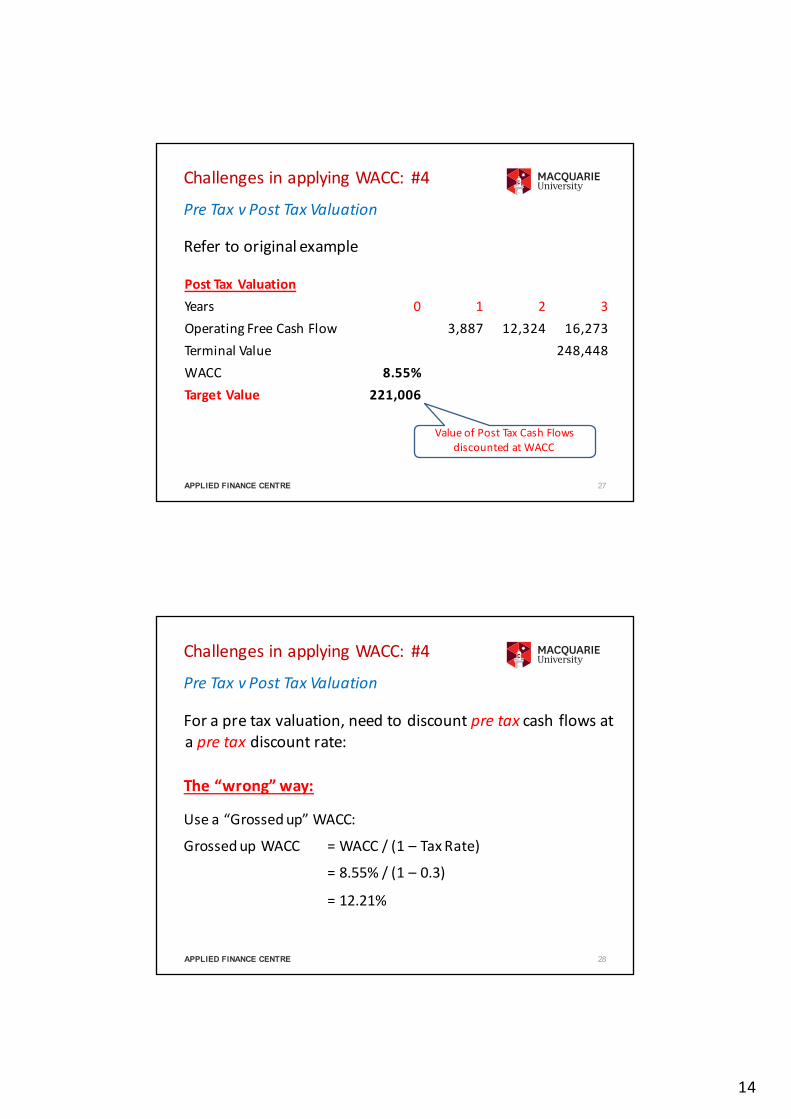

q Pretaxvaluationshouldusepretaxcashflowsatapretaxdiscountrate,andstillgivethesameresult

q Grossingupisdifficult.Simplydividingby(1-T)israrelycorrect:

o Taxpaidrarelyequalsstatutorytaxrateat30%;

o Needtodoagrossupforeachyear;

o CashFlowdifferentbasistoprofitanyway,sogrossingupCashFlowdoesnotmakesense.

ü C

PreTaxvPostTaxValuation

ChallengesinapplyingWACC: #4

14

27APPLIED FINANCE CENTRE

PostTaxValuationYears 0 1 2 3OperatingFreeCashFlow 3,887 12,324 16,273TerminalValue 248,448WACC 8.55%TargetValue 221,006

Refertooriginalexample

ValueofPostTaxCashFlowsdiscountedatWACC

PreTaxvPostTaxValuation

ChallengesinapplyingWACC: #4

28APPLIED FINANCE CENTRE

Forapretaxvaluation,needtodiscountpretaxcashflowsatapretaxdiscountrate:

The“wrong”way:

Usea“Grossedup”WACC:

GrossedupWACC =WACC/(1– TaxRate)

=8.55%/(1– 0.3)

=12.21%

PreTaxvPostTaxValuation

ChallengesinapplyingWACC: #4

15

29APPLIED FINANCE CENTRE

PreTaxValuation– thewrongway

PreTaxValuationYears 0 1 2 3OperatingFreeCashFlow 3,887 12,324 16,273TaxPaid 1,507 582 (307)PreTaxOperatingFreeCashFlow 5,394 12,906 15,966PreTaxTerminalValue 253,140PreTaxCashFlowsfordiscounting 5,394 12,906 269,106

GrossedUpWACC 12.21%ValueatGrossedupWACC 205,505Error -7.0%

ChallengesinapplyingWACC: #4

30APPLIED FINANCE CENTRE

PreTaxValuation– correctpretaxratecanbebacksolved –butwhybother?

PreTaxValuationYears 0 1 2 3OperatingFreeCashFlow 3,887 12,324 16,273TaxPaid 1,507 582 (307)PreTaxOperatingFreeCashFlow 5,394 12,906 15,966PreTaxTerminalValue 253,140PreTaxCashFlowsfordiscounting 5,394 12,906 269,106

CorrectPreTaxRate 9.44%ValueatGrossedupWACC 221,006 Backsolved – findingtherate

thatgivestheoriginalvalue.Willvarywithproject

characteristics

ChallengesinapplyingWACC: #4

16

31APPLIED FINANCE CENTRE

q RecapofPart1

q ChallengesinapplyingWACC(continued)

ü WACCandFinancialStrategy

q IssuesinestimatingWACC

q SourcesofinformationforcalculatingWACC

Agenda

Part2

32APPLIED FINANCE CENTRE

q UnderlyingfinancialstrategyspecifiedbytheWACC- afixedDebt/Value ratio,andaResidualDividendPolicywhichassumespayoutofcashflowstomaintaintargetD/V

q WACCnothelpfultodeterminefinancialstructure

q WACCandassetbasedfinancing

q SituationswhereWACCnotappropriate

WACC andFinancialStructure

WACCmakesveryspecificassumptionsaboutunderlyingfinancialstrategy

17

33APPLIED FINANCE CENTRE

Refertooriginalexample

UnderlyingFinancial Strategy

FinancialStrategyUnderlyingWACCValuation

Years 0 1 2 3

AssumedTargetDebt/Value ratio 25% 25% 25% 25%

EstimatedEnterpriseValue@Yearend 221,006 236,016 243,870 248,448

AssumedDebtBalance[EVxTarget D/V] 55,252 59,004 60,968 62,112AssumedEquityValue[EV- DebtBalance] 165,755 177,012 182,903 186,336

$amountofdebtalwaysadjuststomaintaintheTargetD/Vratioovertheforecastperiod

34APPLIED FINANCE CENTRE

Refertooriginalexample

DebtProfileYears 0 1 2 3

OpeningBalance - 55,252 59,004 60,968Plus Drawdown/(Repayment) 55,252 3,752 1,964 1,144Equals ClosingBalance 55,252 59,004 60,968 62,112

InterestPayments 3,315 3,540 3,658Less: InterestTaxShelter [InterestxTaxRate] 995 1,062 1,097Equals AfterTaxInterestPayment - 2,321 2,478 2,561

UnderlyingFinancial Strategy

Sothedebtscheduleandinterestpaymentsarepredetermined

18

35APPLIED FINANCE CENTRE

Refertooriginalexample

CashFlowstoEquity[BasedonEV]

Years 0 1 2 3

OperatingFree CashFlow* (221,006) 3,887 12,324 16,273

Plus DebtDrawdown/(Repayment) 55,252 3,752 1,964 1,144

Less AfterTaxInterestPayment 2,321 2,478 2,561

Equals CashFlowtoEquity (165,754) 5,319 11,810 14,857

Plus Valueatendofforecastperiod 186,336

UnderlyingFinancial Strategy

asisthedividendpolicy.Anysurpluscashdistributedtoshareholders

36APPLIED FINANCE CENTRE

WACCnothelpfulfordeterminingcapitalstructureDecidingthetargetmixofdebtandequity– temptingtocalculateWACCatdifferentgearinglevels

Gearing

Rating

HighLow

AAA AA A BBB BB B CCC

%

Interestrate

CostofEquity

WACCAlthoughitdoesalignwith‘optimum’ratingatlowinvestmentgrade,whichisthemostcommon

rating

19

37APPLIED FINANCE CENTRE

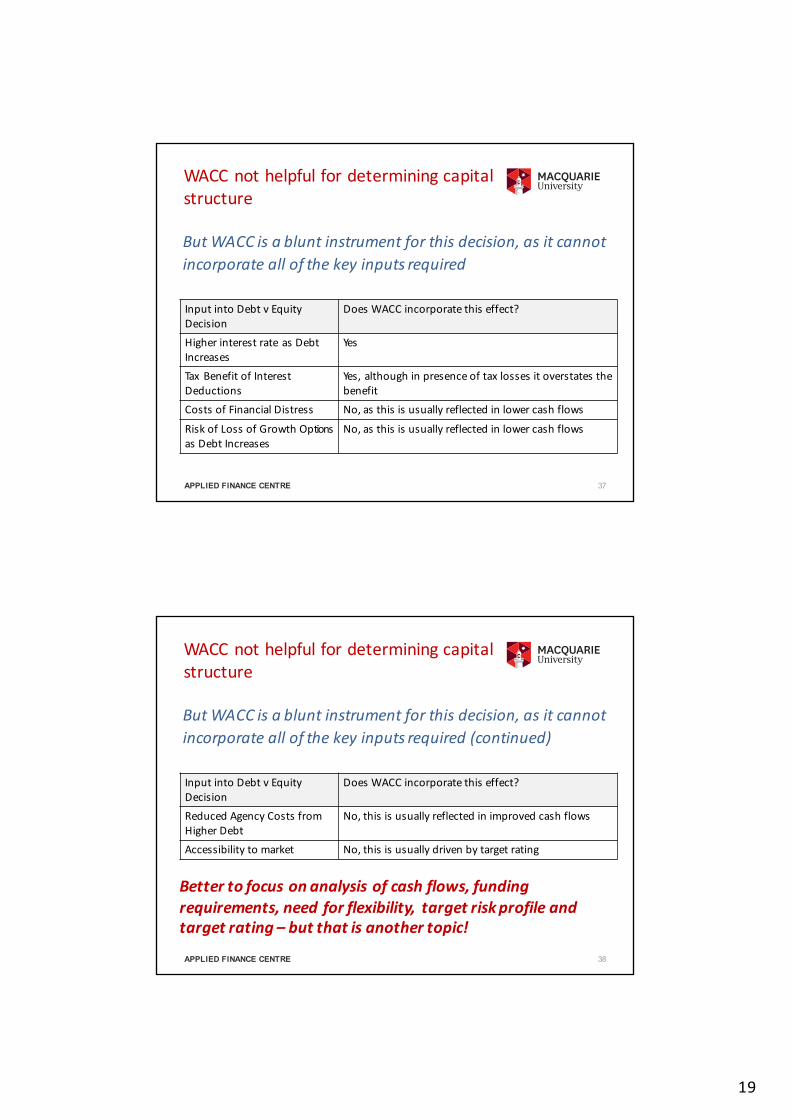

WACCnothelpfulfordeterminingcapitalstructure

ButWACCisabluntinstrumentforthisdecision,asitcannotincorporateallofthekeyinputsrequired

InputintoDebtvEquityDecision

DoesWACCincorporatethiseffect?

HigherinterestrateasDebtIncreases

Yes

TaxBenefit ofInterestDeductions

Yes,althoughinpresence oftaxlossesitoverstatesthebenefit

CostsofFinancial Distress No,asthisisusuallyreflected inlowercashflows

RiskofLossofGrowthOptionsasDebtIncreases

No,asthisisusuallyreflected inlowercashflows

38APPLIED FINANCE CENTRE

WACCnothelpfulfordeterminingcapitalstructure

ButWACCisabluntinstrumentforthisdecision,asitcannotincorporateallofthekeyinputsrequired(continued)

InputintoDebtvEquityDecision

DoesWACCincorporatethiseffect?

ReducedAgencyCostsfromHigherDebt

No,thisisusuallyreflected inimprovedcashflows

Accessibilitytomarket No,thisisusually drivenbytargetrating

Bettertofocusonanalysisofcashflows,fundingrequirements,needforflexibility, targetriskprofileandtargetrating– butthatisanothertopic!

20

39APPLIED FINANCE CENTRE

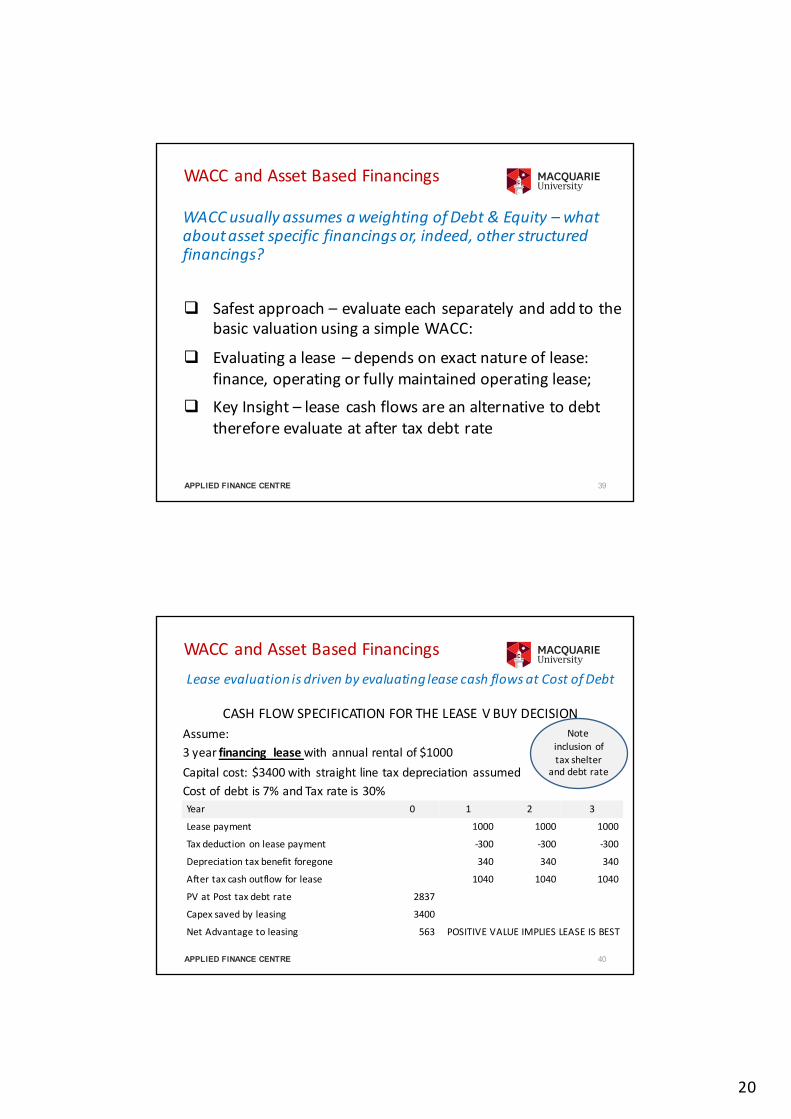

q Safestapproach– evaluateeachseparatelyandaddtothebasicvaluationusingasimpleWACC:

q Evaluatingalease – dependsonexactnatureoflease:finance,operatingorfullymaintainedoperatinglease;

q KeyInsight– lease cashflowsareanalternativetodebtthereforeevaluateataftertaxdebtrate

WACC andAssetBasedFinancings

WACCusuallyassumesaweightingofDebt&Equity– whataboutassetspecificfinancingsor,indeed,otherstructuredfinancings?

40APPLIED FINANCE CENTRE

LeaseevaluationisdrivenbyevaluatingleasecashflowsatCostofDebt

CASHFLOWSPECIFICATIONFORTHELEASEVBUYDECISIONAssume:3yearfinancing leasewith annualrentalof$1000Capitalcost:$3400with straightlinetaxdepreciation assumedCostofdebtis7%andTaxrateis30%Year 0 1 2 3

Leasepayment 1000 1000 1000

Taxdeduction onleasepayment -300 -300 -300

Depreciationtaxbenefitforegone 340 340 340

Aftertaxcashoutflowforlease 1040 1040 1040

PVatPosttaxdebtrate 2837

Capex savedbyleasing 3400

NetAdvantagetoleasing 563 POSITIVEVALUEIMPLIESLEASEISBEST

Noteinclusion oftaxshelter

anddebtrate

WACC andAssetBasedFinancings

21

41APPLIED FINANCE CENTRE

CASHFLOWSPECIFICATIONFORTHELEASEVBUYDECISIONAssume:Samedealexceptitisanoperatinglease Expectedsalvagevalueis$600.WACCis10%Year 0 1 2 3

Leasepayment 1000 1000 1000

Taxdeduction onleasepayment -300 -300 -300

Depreciationtaxbenefitforegone 340 340 340

Aftertaxcashoutflowforlease 1040 1040 1040

PVatPosttaxdebtrate 2837

SalvageValue(after tax) 420

PVofsalvagevalue 316

Capex savedbyleasing 3400

NetAdvantagetoleasing 247 POSITIVEVALUEIMPLIESLEASEISBEST

Salvagevaluediscounted atWACC

WACC andAssetBasedFinancings

42APPLIED FINANCE CENTRE

Evaluationofleasesdependsonnatureoflease– formulaegiveninAppendix

Operatinglease:NETADVANTAGETO(Operating)LEASING=

FinanceLease:NETADVANTAGETO(Finance)LEASING=

InvestmentOutlay

- Present valueofAfterTaxLeasePayments@AfterTaxCostofDebt

- DepreciationTaxShelterForegone@AfterTaxCostofDebt

InvestmentOutlay

- Present valueofAfterTaxLeasePayments@AfterTaxCostofDebt

- DepreciationTaxShelterForegone@AfterTaxCostofDebt

- Present ValueofForegoneAfterTaxSalvageValueatendoflease:SalvageValue@WACC;BookValuexT@Rd(1-T)

WACC andAssetBasedFinancings

22

43APPLIED FINANCE CENTRE

Evaluationofleasesdependsonnatureoflease(cont)

InvestmentOutlay

- Present valueofAfterTaxLeasePayments@AfterTaxCostofDebt

- DepreciationTaxShelterForegone@AfterTaxCostofDebt

- Present ValueofForegoneAfterTaxSalvageValueatendoflease:SalvageValue@WACC;BookValuexT@Rd(1-T)

+ Present ValueofAfterTaxcashflowssavedfrommaintenanceetc,@WACC

FullymaintainedoperatingleaseNETADVANTAGETO(FullyMaintainedOperating)LEASING=

WACC andAssetBasedFinancings

44APPLIED FINANCE CENTRE

WhenisWACCnotappropriate?

Situationswheretheunderlyingassumptionabout financialstrategydoesnotmatch requiresanalternativetoWACC

ViolationofWACCAssumption Response

PrivateEquity investmentsdonotuseaconstantDebt/Value ratio,butusuallynegotiateafixeddebtschedule

UseFlowtoEquity,method wherecashflowsarediscountedatCostofEquity

International investments,structurescomplicatedbymultipletaxrates,anddebtstructuring

UseAdjustedPresentValuemethod,whichdirectlycalculatescosts&benefitsoffinancingstructures.WACChasthefinancingbenefitsembedded intheRd(1-T)term

Infrastructrue &Property Investments–tendnotto useaconstantDebt/Valueratio,butusuallynegotiatea fixeddebtschedule

UseFlowtoEquitymethod,wherecashflowsarediscountedatCostofEquity

23

45APPLIED FINANCE CENTRE

q RecapofPart1

q ChallengesinapplyingWACC(continued)

q WACCandFinancialStrategy

ü IssuesinestimatingWACC

q SourcesofinformationforcalculatingWACC

Agenda

Part2

46APPLIED FINANCE CENTRE

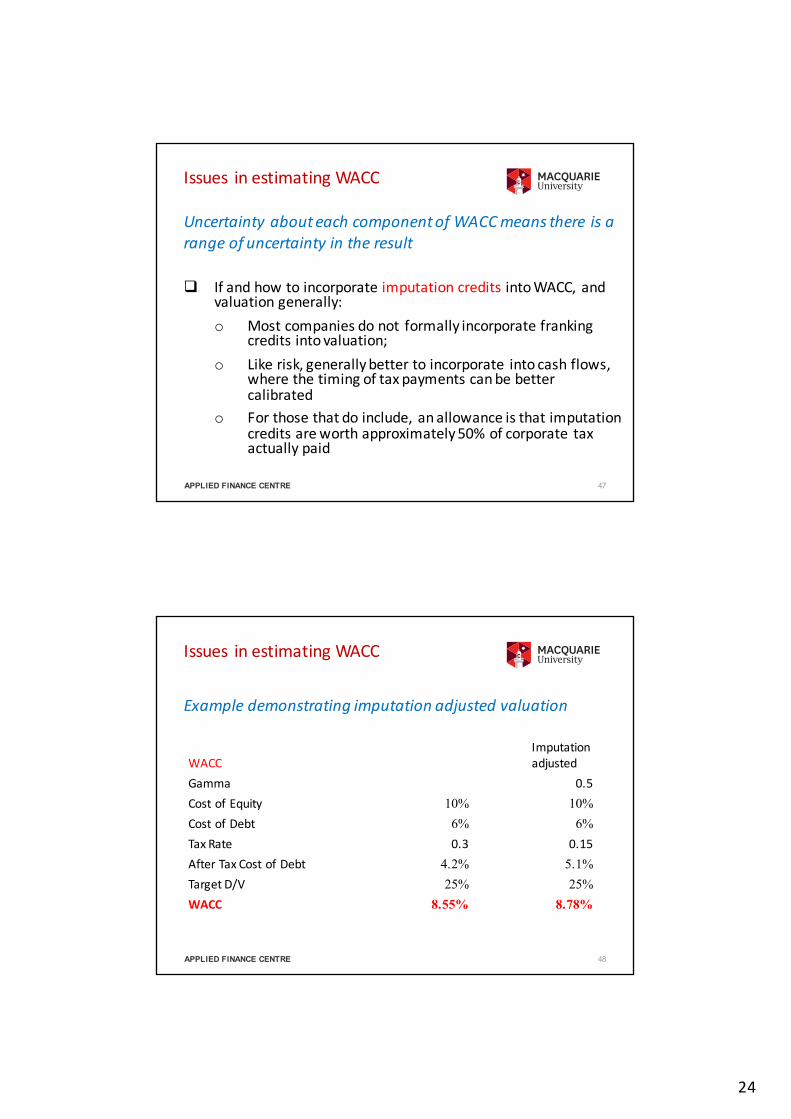

UncertaintyabouteachcomponentofWACCmeansthereisarangeofuncertaintyintheresult

Issues inestimatingWACC

q MarketRiskPremiumdebate– historyvimpliedforward

o RangeinAustraliaisbetween5%- 7%

q EstimatingBeta– especiallyforthinlytradedstocks,andlimitednumberofcomparables,esp inAustralia

o Justifyby fundamentals,notstatistics

o Fundamentalsimplycyclicalityofrevenues,leveloffixedcosts,durationofassets,degreeofgrowthoptions

24

47APPLIED FINANCE CENTRE

UncertaintyabouteachcomponentofWACCmeansthereisarangeofuncertaintyintheresult

Issues inestimatingWACC

q IfandhowtoincorporateimputationcreditsintoWACC,andvaluationgenerally:o Mostcompaniesdonot formallyincorporatefranking

creditsintovaluation;o Likerisk,generallybettertoincorporate intocashflows,

wherethetimingoftaxpaymentscanbebettercalibrated

o Forthosethatdoinclude,anallowanceisthatimputationcreditsareworthapproximately50%ofcorporate taxactuallypaid

48APPLIED FINANCE CENTRE

Exampledemonstratingimputationadjustedvaluation

Issues inestimatingWACC

WACCImputationadjusted

Gamma 0.5CostofEquity 10% 10%CostofDebt 6% 6%TaxRate 0.3 0.15AfterTaxCostofDebt 4.2% 5.1%TargetD/V 25% 25%WACC 8.55% 8.78%

25

49APPLIED FINANCE CENTRE

Exampledemonstratingimputationadjustedvaluation

Issues inestimatingWACC

ReworkedforImputation

OperatingFree cashFlow 5,394 12,906 269,106

Add ImputationCreditValue (753) (291) 154

Terminal Value 2,346

ImputationadjustedOFCF 4,640 12,615 271,605

ImputationadjustedEV $225,961

OriginalE.V. $221,006

50APPLIED FINANCE CENTRE

UncertaintyabouteachcomponentofWACCmeansthereisarangeofuncertaintyintheresult

Issues inestimatingWACC

q Howtoallowforchangesingearingbetweenprojects–deleveraging&releveraging:o RefertoexampleinPart1forexpressionsfordeleveragingand

releveragingo TechnicalissueaboutwhetheranassumptionofDebtBeta=0–

verycommon,butincorrect,assumptionq Isthereasmallstockpremium– premiumincostofequityforsmall

capstockswillresultinlowervaluationso Smallcapstockscommonlyattractahigherdiscountrate,called

smallcappremium– inorderof5%;o Relevantforvaluinglistedsmallcapsandprivatebusinesses,not

usedinprojectevaluation

26

51APPLIED FINANCE CENTRE

q RecapofPart1

q ChallengesinapplyingWACC(continued)

q WACCandFinancialStrategy

q IssuesinestimatingWACC

q SourcesofinformationforcalculatingWACC

Agenda

Part2

52APPLIED FINANCE CENTRE

Widerangeofsourcesofinformationavailable

SourcesofInformationforWACC

Information Source

Usefulgeneral sourcesofinformationonWACC

KPMGAnnualValuationPracticesSurvey;

Independent Expert reportsonM&Atransactions

AustralianEnergyRegulator

Integrated sourcesprovideanoverallWACCresult

Bloomberg;

MarketRiskpremium AustralianEnergyRegulator

IndependentExpertReports

27

53APPLIED FINANCE CENTRE

Widerangeofsourcesofinformationavailable

SourcesofInformationforWACC

SourcesforIndividualbuilding blocks

Source

RiskFreeRate RBA:https://www.rba.gov.au/statistics/tables/

Betas Bloomberg

AGSMRiskMeasurementService

DirectcalculationusingCapIQ

Datastream

YahooFinance

54APPLIED FINANCE CENTRE

WACCisakeymetric incorporatefinance,butstillmanyissues,withscopeforcontributionbyCoprorate Treasurer

Conclusions

q Primarily usedinawidevarietyofvaluationapplications

q WACCshould bebasedonassetspecificcharactistics, especially(systematic)riskanddebtcapacity, butcompanywideWACCcommonlyused(incorrectly)

q Italsocompetesagainsttheuseofahurdle rate– moreatool forrationingcapitalandresources

q Incorporating project specific risk– manyaddan(arbitrary) premiumtodiscount rate.Better way--- incorporate project specific risksinto cashflows

q Generallynotappropriate formakingfinancial strategydecisions

q Anumber ofestimation &application issuessuggesthandlewithcare

28

55APPLIED FINANCE CENTRE

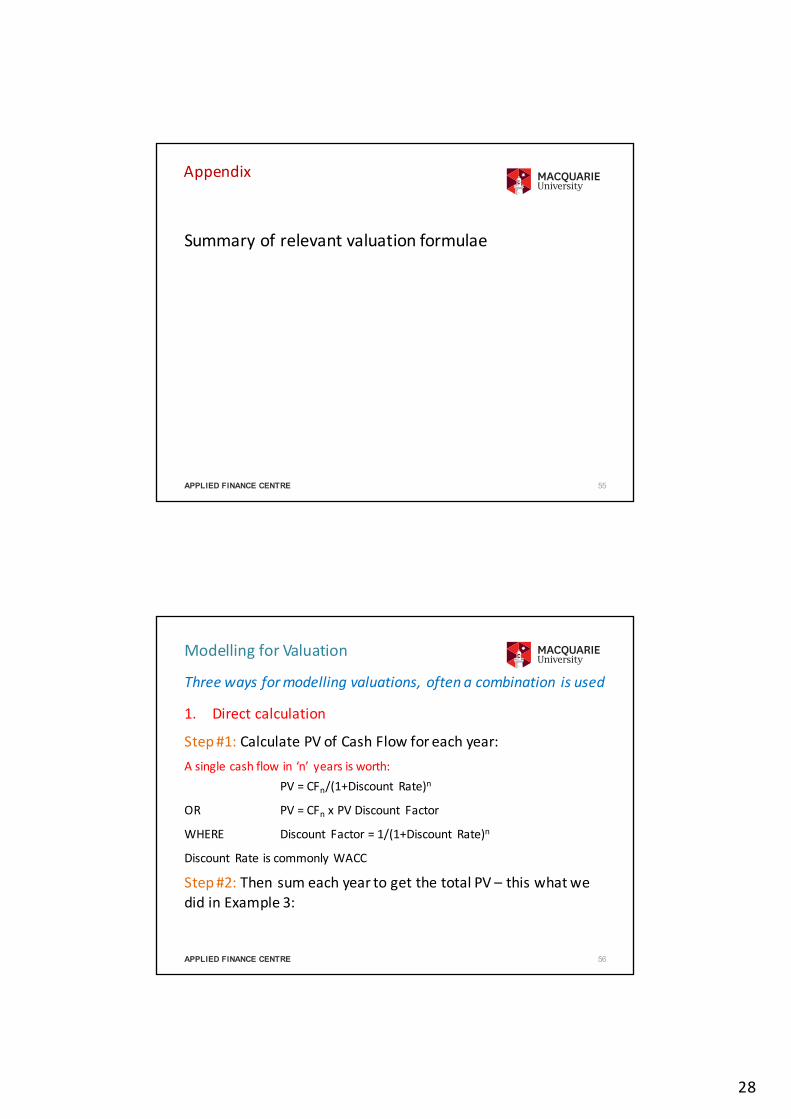

Summaryofrelevantvaluationformulae

Appendix

56APPLIED FINANCE CENTRE

Threewaysformodellingvaluations,oftenacombination isused

1. Directcalculation

Step#1:CalculatePVofCashFlowforeachyear:Asinglecashflowin‘n’ yearsisworth:

PV=CFn/(1+Discount Rate)n

OR PV=CFn xPVDiscount Factor

WHERE Discount Factor=1/(1+Discount Rate)n

Discount RateiscommonlyWACC

Step#2: ThensumeachyeartogetthetotalPV– thiswhatwedidinExample3:

ModellingforValuation

29

57APPLIED FINANCE CENTRE

Threewaysformodellingvaluations,oftenacombination isused

2. Excelformulae

NPV(rate,values….)foraseries of(changing)valuesoverafixedperiodo Rate=DiscountRateorWACCo Valuesiscellreferencesforcashflows:

o Assumesnoblankcells;o ExcludetheTime=0CashFlow[Excelassumescashflowsatendofeach

period];o Assumesequalperiods

PV(rate,nper,pmt)forafixedtermlevelannuityo Nper isnumberof(equal)periodso Pmt isthe(equal)amountoftheannuity

ModellingforValuation

58APPLIED FINANCE CENTRE

Threewaysformodellingvaluations,oftenacombination isused

3. “Shortcut”formulaeCommonformulaeforperpetuities[PART#1]:Levelperpetuity: PV=CFt /WACC

OR PV=CFt xMultiple

WHERE Multiple=1/WACC

Growingperpetuity: PV=CFt+1/(WACC – g)

OR PV=CFt+1 xMultiple

WHERE Multiple=1/(WACC– g)

AND gisgrowthrateinperpetuity

ModellingforValuation

30

59APPLIED FINANCE CENTRE

Threewaysformodellingvaluations,oftenacombination isused

3. “Shortcut” formulaeCommonformulaeforfixedtermannuities[PART#2]:FixedTerm(Level)Annuity:

𝑃𝑉 = 𝐶𝐹)*

+,--− *+,--/ *0+,-- 1

FixedTermGrowingAnnuity:

𝑃𝑉 = 𝐶𝐹)0*1

𝑊𝐴𝐶𝐶 − 𝑔−

1𝑊𝐴𝐶𝐶 − 𝑔

𝑥1 + 𝑔 9

1 + 𝑊𝐴𝐶𝐶 9

WHERE‘T’ isthenumber ofyearsforwhichtheannuityoperates, afterwhich cashflowsarezero.

ModellingforValuation

60APPLIED FINANCE CENTRE

Forthosethatlikeformulae!!!

Operatinglease:NETADVANTAGETO(Operating)LEASING=

FinanceLease:NETADVANTAGETO(Finance)LEASING=

Note:theseformulaworkwhenthere arenotaxlosses.Theyneedadjustment inthepresence oftaxlosses

Lease EvaluationFormulae

+I; −<L> − T@L> + T@Dep>[1 + RF 1 − T@ ]>

−EMVK(1 − T@)[1 + WACC]K

K

>Q;

−BVKT@

[1 +RF 1− T@ ]K

+I;−<L>− T@L> + T@Dep>[1 + RF 1 − T@ ]>

K

>Q;

31

61APPLIED FINANCE CENTRE

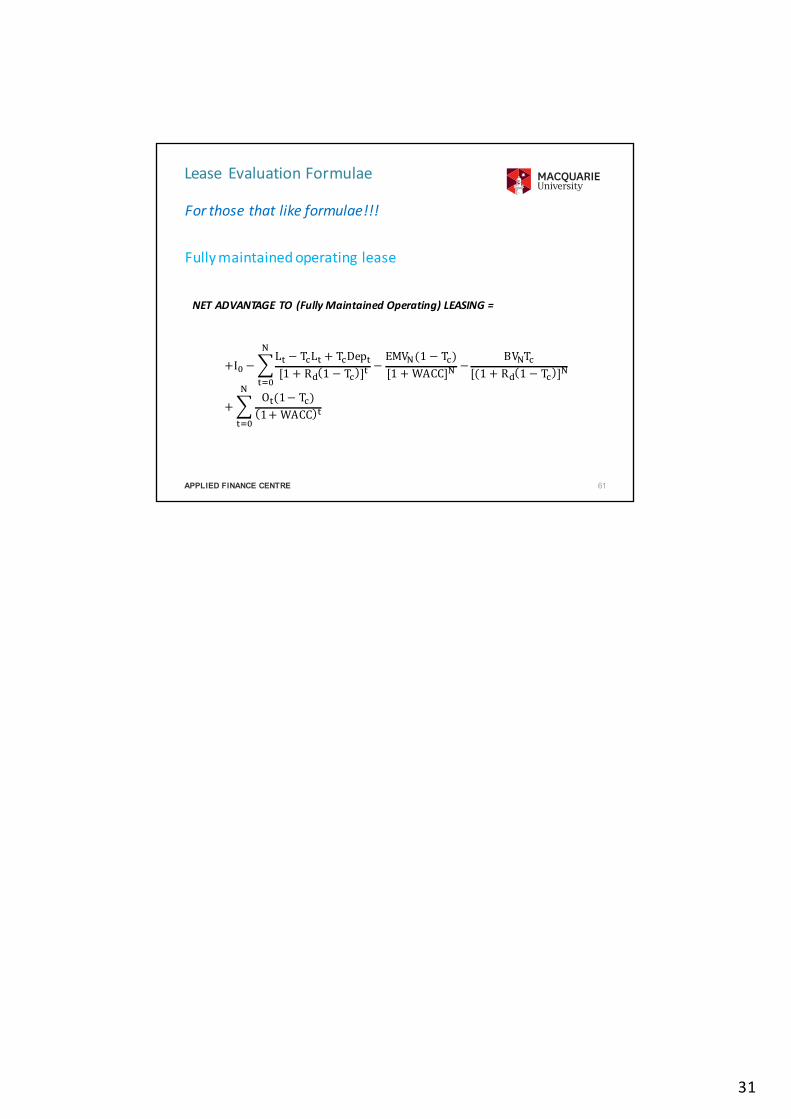

NETADVANTAGETO (FullyMaintainedOperating)LEASING=

Fullymaintainedoperatinglease

Forthosethatlikeformulae!!!

Lease EvaluationFormulae

+I; −<L> − T@L> + T@Dep>[1 + RF 1 − T@ ]>

−EMVK(1 − T@)[1 + WACC]K

K

>Q;

−BVKT@

[(1 + RF 1 − T@ ]K

+<O>(1− T@)1+ WACC >

K

>Q;