apresentação do powerpoint - copelir.copel.com/enu/9077/roadshow_ing.pdf · mata de santa genebra...

TRANSCRIPT

August 2017

Disclaimer

2

Any statements made during this event involving Copel’s business outlook or financial

and operating forecasts and targets constitute the beliefs and assumptions of the

Company’s Management, and the information currently available. Forward-looking

statements are not guarantees of performance and involve risks, uncertainties and

assumptions, given that they refer to future events, and thus are dependent on

circumstances that may or may not occur. The general economic conditions, industry

conditions and other operating factors could come to affect the future performance of

Copel and lead to results that are materially different from those expressed in said

forward-looking statements.

3

Agenda

About Sector

About Copel

Main Strategic Objectives

Leverage Analysis

Budget Supplementation

Startup New Assets

70

90

110

130

150

170

Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16 Jan-17 Mar-17 May-17 Jul-17

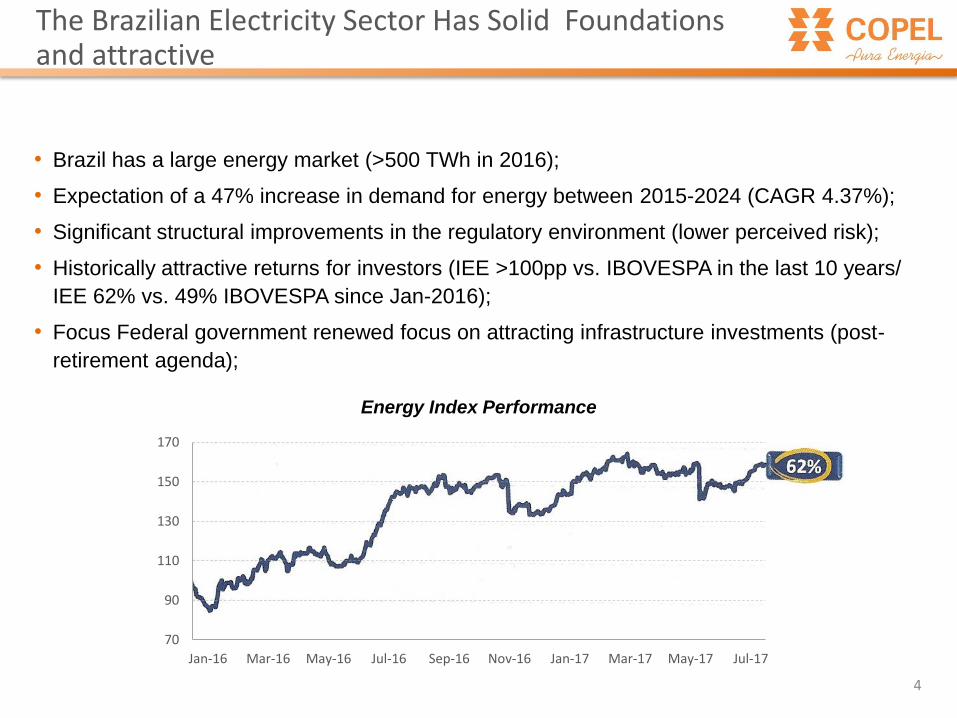

The Brazilian Electricity Sector Has Solid Foundations and attractive

4

• Brazil has a large energy market (>500 TWh in 2016);

• Expectation of a 47% increase in demand for energy between 2015-2024 (CAGR 4.37%);

• Significant structural improvements in the regulatory environment (lower perceived risk);

• Historically attractive returns for investors (IEE >100pp vs. IBOVESPA in the last 10 years/

IEE 62% vs. 49% IBOVESPA since Jan-2016);

• Focus Federal government renewed focus on attracting infrastructure investments (post-

retirement agenda);

Energy Index Performance

... And It Has A Prospect To Evolve Even More...

5

Privatization of hydroelectric palnts;

Enlargement of the free market;

Solve court issues of the sector;

Allocation of costs and rationalization;

Resumption of stability and credibility of the legal-regulatory framework;

Proposal for measures to improve the legal framework of the electricity sector - Public Consultation

Reduction of obstacles to the capture of investments in energy;

Expansion of energy commercialization;

New rules for conducting new and existing energy auctions;

Possibility of distributors negotiating with free consumers and other agents of the Free

Market contracts of sale of excess contracted energy.

Decree 9,143/2017

Agricultural 9.7% Industries

15.8%

Utilities 3.4%

Construction 5.8%

Commerce 16.1%

Services 49.2%

6

State of Paraná: Highlight in Growth

Geographic Information

Area: 199,000 km2 (2.3% of the country)

Population: 11 million (5.5% of Brazil´s population)

Cities: 399

Economic Data

GDP 2015: R$ 366 billion (6% of Brazilian GDP)

GDP 2016: R$ 387 billion (6% of Brazilian GDP)

GDP 1Q17: R$ 107 billion (+ 2.5% vs. 1Q16)

Breakdown by Income Segment

7

Companhia Paranaense de Energia - Copel

Head office: Curitiba/PR

62 years in the industry

Integrated Company - Generation, Transmission,

Distribution, Energy Trading and Telecommunication

Since 1994 on the B3

23 years of listing

20 years of listing on the NYSE

The first of the brazilian electric sector

Present in the European Union

15 years listed on Latibex

1On 08.18.2017

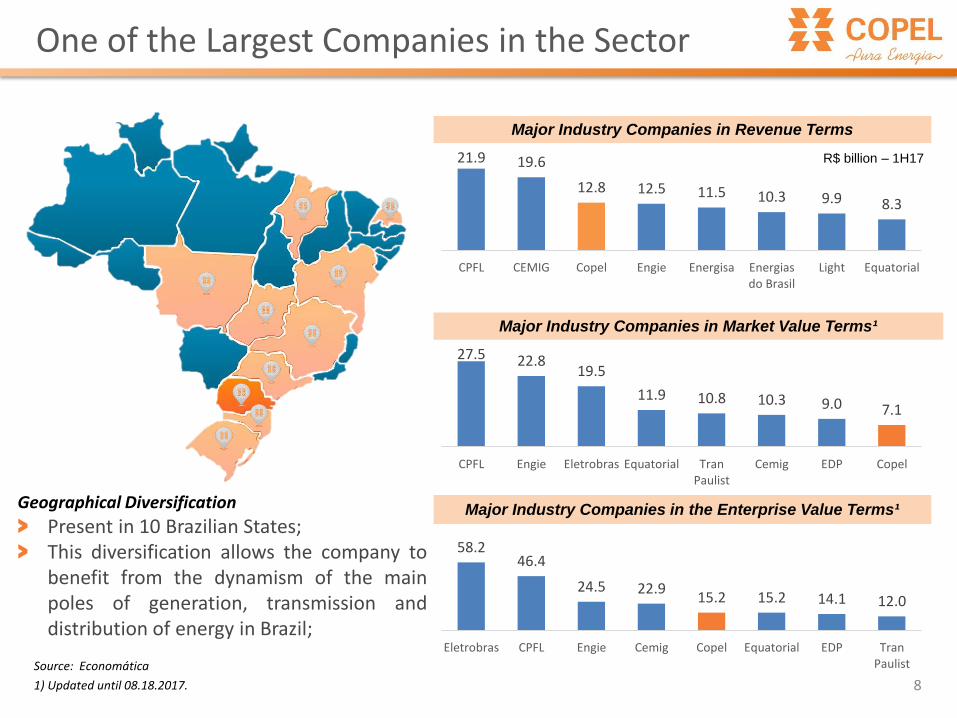

One of the Largest Companies in the Sector

8

Geographical Diversification

> Present in 10 Brazilian States; > This diversification allows the company to

benefit from the dynamism of the main poles of generation, transmission and distribution of energy in Brazil;

Source: Economática

1) Updated until 08.18.2017.

Major Industry Companies in Revenue Terms

21.9 19.6

12.8 12.5 11.5 10.3 9.9 8.3

CPFL CEMIG Copel Engie Energisa Energiasdo Brasil

Light Equatorial

R$ billion – 1H17

27.5 22.8 19.5

11.9 10.8 10.3 9.0 7.1

CPFL Engie Eletrobras Equatorial TranPaulist

Cemig EDP Copel

Major Industry Companies in Market Value Terms¹

Major Industry Companies in the Enterprise Value Terms¹

58.2 46.4

24.5 22.9 15.2 15.2 14.1 12.0

Eletrobras CPFL Engie Cemig Copel Equatorial EDP TranPaulist

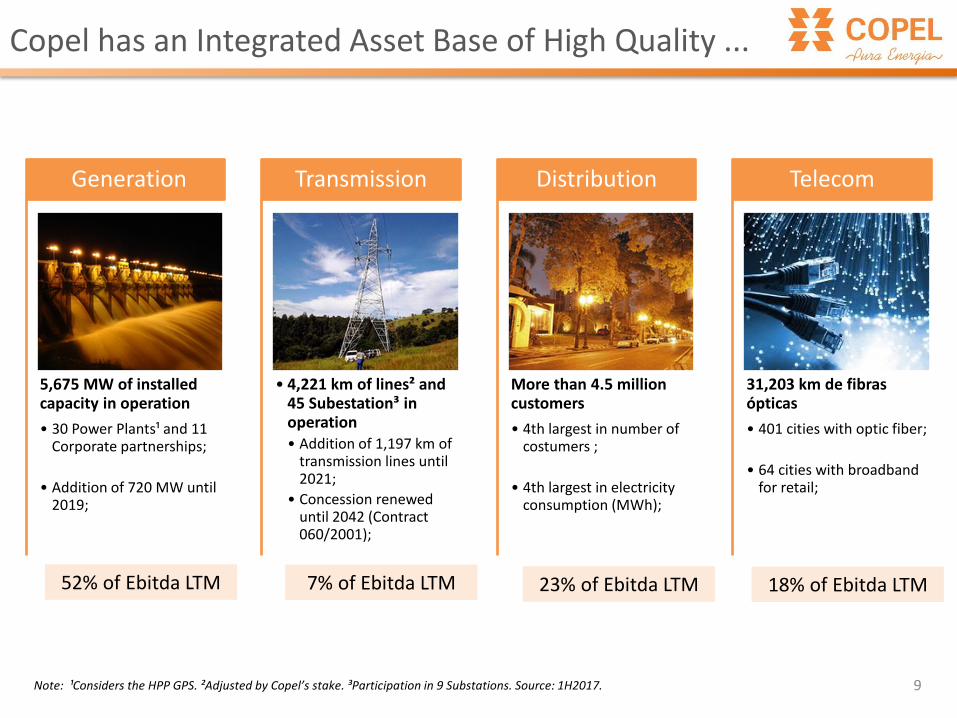

5,675 MW of installed capacity in operation

• 30 Power Plants¹ and 11 Corporate partnerships;

• Addition of 720 MW until 2019;

Generation

• 4,221 km of lines² and 45 Subestation³ in operation • Addition of 1,197 km of

transmission lines until 2021;

• Concession renewed until 2042 (Contract 060/2001);

Transmission

More than 4.5 million customers

• 4th largest in number of costumers ;

• 4th largest in electricity consumption (MWh);

Distribution

31,203 km de fibras ópticas

• 401 cities with optic fiber;

• 64 cities with broadband for retail;

Telecom

Copel has an Integrated Asset Base of High Quality ...

9

52% of Ebitda LTM 7% of Ebitda LTM 23% of Ebitda LTM 18% of Ebitda LTM

Note: ¹Considers the HPP GPS. ²Adjusted by Copel’s stake. ³Participation in 9 Substations. Source: 1H2017.

10

Copel Distribuição – The Best Of Latam

Customers’ satisfaction;

Quality in energy supply;

Better Communication;

Excellence in customer

service;

Valuing the company image;

Image only portuguese.

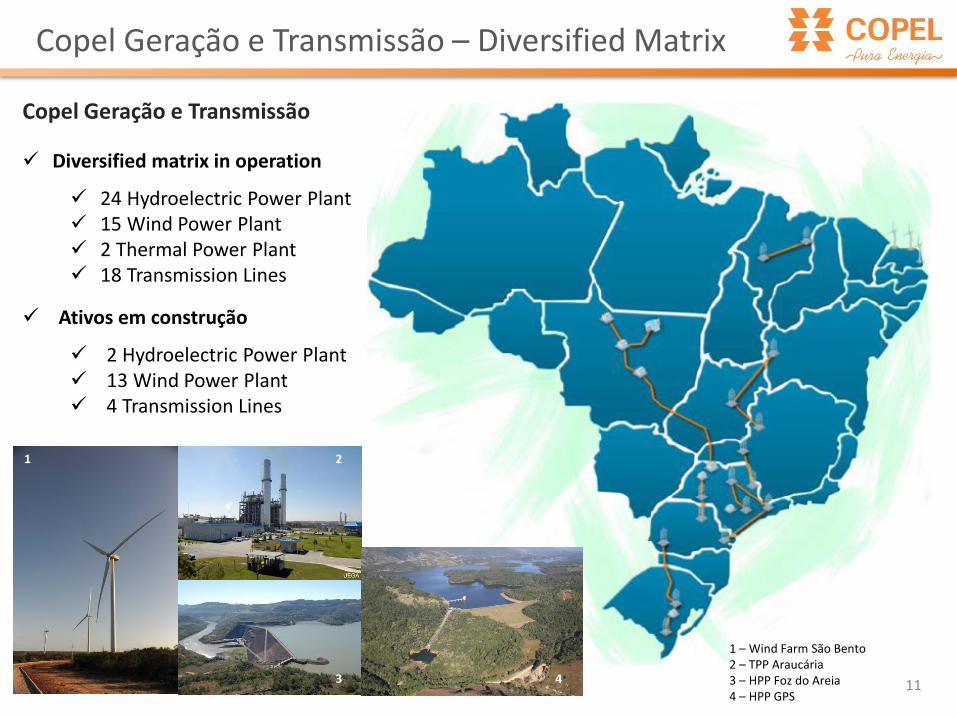

Diversified matrix in operation

24 Hydroelectric Power Plant 15 Wind Power Plant 2 Thermal Power Plant 18 Transmission Lines

Ativos em construção

2 Hydroelectric Power Plant 13 Wind Power Plant 4 Transmission Lines

11

Copel Geração e Transmissão – Diversified Matrix

Copel Geração e Transmissão

1 2

3 4

1 – Wind Farm São Bento 2 – TPP Araucária 3 – HPP Foz do Areia 4 – HPP GPS

Copel has an Experienced Team and Already Adopts the Best Practices of Corporate Governance of the Sector ...

12

• Strong presence of corporate committees and councils: Committee for Disclosure of

Material Acts and Facts, Customer Council and Ethics Guidance Council;

• Risk and Integrity Management Actions: integrity program, programa de integridade,

code of conduct, risk assessment and channels of complaint;

• Sarbanes Oxley

• Strongly committed to sustainability and social programs:

– Signatory of the Global Compact since 2000;

– Participation in the Corporate Sustainability Index (ISE) of B3;

– 11 years adopting the guidelines of the GRI - Global Reporting Initiative;

– 2 years adopting Integrated Reporting Guidelines - IIRC - International Integrated

Reporting Council;

– 10 years in the Top 10 of the Abradee Social Responsibility Award;

– Participation in the Global Sustainability Index - MSCI since 2014 and FTSE4GOOD

Emerging Index;

Copel Has Some Additional Competitive Advantages ...

13

Power generation leadership in Paraná (~ 30%) with growth above the national

average (9.4 GW of unexplored market);

Greater exposure to the Spot Market among peers (22% of energy not contracted

in 2017 and 36% in 2018, reaching 78% in 2021);

Diversified energy matrix, with significant portions of its production coming from

non-hydro sources (~ 11% thermal and 7% wind);

High operational efficiency in distribution (DEC and FEC better than regulatory

limits);

Relevant long-term cash flow generation in transmission concessions (stable

long-term APR profile of the sector)

Demand in the concession area is stable and shows growth above the national

average (less importance of industrial consumption in the portfolio 23.3% vs.

35.6% in Brazil);

Copel is Currently Valued Below the Industry Average ...

14

Firm Value/ EBITDA (CY18E)

8.8

7.7

4.1

5.2 4.9

4.0

5.8

CPFL Eletrobras Cemig Energias do Brasil Copel LightCopel

4.9

Copel

7.0

Potential

Copel

+ ~43%

• Our Strategic Plan will be based on the recovery of the Company's value.

Main short-term strategic objectives ... Focus on cash flow generation ...

15

• Maintenance of cash flow generation for all current business (GeT, Dis, Telecom and

Commercialization);

• Priorization of investment plan to finalize projects in progress, in the shortest possible time,

ensuring the expected chash flow generation;

• Renegociation of short-term debt;

• Review of funding plan (BNDES, bond, monetization of CRC, etc);

• Optimization of costs (PDV, review of contracts, management of delinquency, judicial

deposits, etc);

• Sale of non-strategic assets (SPCs, land, properties, obsolete products in stock);

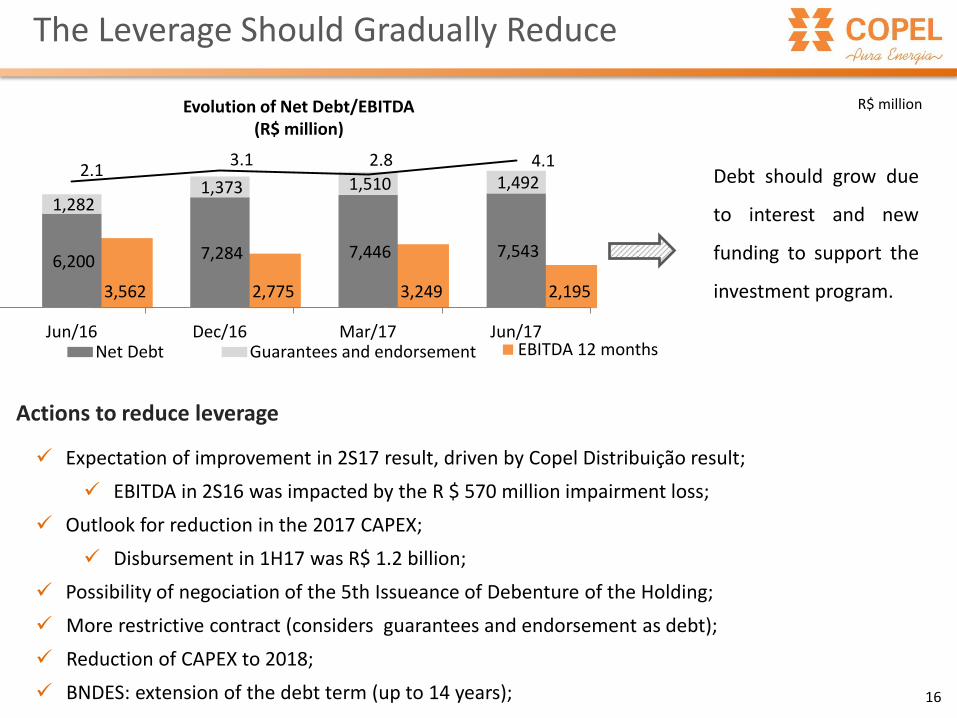

The Leverage Should Gradually Reduce

16

Evolution of Net Debt/EBITDA (R$ million)

Expectation of improvement in 2S17 result, driven by Copel Distribuição result;

EBITDA in 2S16 was impacted by the R $ 570 million impairment loss;

Outlook for reduction in the 2017 CAPEX;

Disbursement in 1H17 was R$ 1.2 billion;

Possibility of negociation of the 5th Issueance of Debenture of the Holding;

More restrictive contract (considers guarantees and endorsement as debt);

Reduction of CAPEX to 2018;

BNDES: extension of the debt term (up to 14 years);

R$ million

Actions to reduce leverage

3,562 2,775 3,249 2,195

EBITDA 12 months

6,200 7,284 7,446 7,543

1,282 1,373 1,510 1,492

2.1 3.1 2.8 4.1

Jun/16 Dec/16 Mar/17 Jun/17Net Debt Guarantees and endorsement

Debt should grow due

to interest and new

funding to support the

investment program.

Main Risks and Oportunities

17

Lower pace of economic recovery (delayed further reforms);

Sectorial issues (GSF and PLD);

Performance of energy consumption;

Possible impacts of impairment of generation assets (final adjustments of works);

Oportunities

Cut of costs;

81 identified actions; Review of third-party service contracts; Redundancy plan without the replacement of vacancies; Overtime cut; Review of provisions for litigation;

Sale of non-strategic assets;

Sanepar; Others;

Focus on reducing delinquency;

Risks

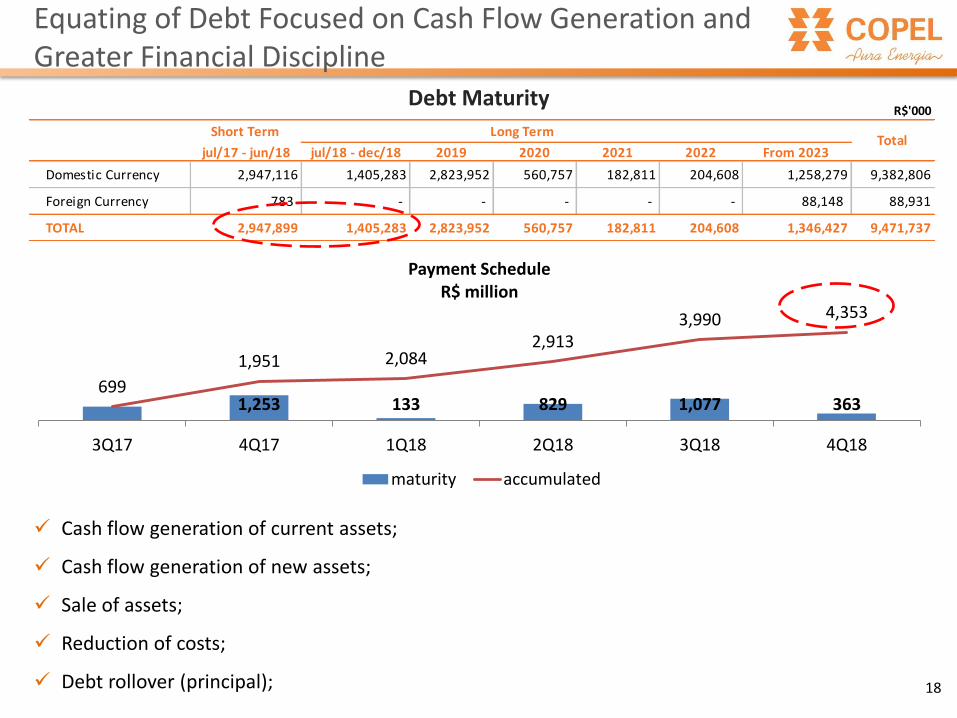

R$'000

Short Term

jul/17 - jun/18 jul/18 - dec/18 2019 2020 2021 2022 From 2023

Domestic Currency 2,947,116 1,405,283 2,823,952 560,757 182,811 204,608 1,258,279 9,382,806

Foreign Currency 783 - - - - - 88,148 88,931

TOTAL 2,947,899 1,405,283 2,823,952 560,757 182,811 204,608 1,346,427 9,471,737

Long TermTotal

Equating of Debt Focused on Cash Flow Generation and Greater Financial Discipline

18

Debt Maturity

1,253 133 829 1,077 363 699

1,951 2,084 2,913

3,990 4,353

3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

Payment Schedule R$ million

maturity accumulated

Cash flow generation of current assets;

Cash flow generation of new assets;

Sale of assets;

Reduction of costs;

Debt rollover (principal);

Budget Supplementation

19

Investment Program 2017

Efforts in the works in progress to start up assets under construction

R$ million

Original Revised

Copel Geração e Transmissão 230.3 503.3 570.3 1,024.5

HPP Colíder2 44.5 50.9 24.1 125.3

HPP Baixo Iguaçu2 50.9 98.7 20.5 253.1

TL Araraquara / Taubaté 34.0 111.3 137.9 137.9

TL Foz do Chopim - Realeza 0.5 2.9 9.5 9.5

TL Assis - Londrina 11.9 24.6 20.4 20.4

TL Curitiba Leste / Blumenau 6.4 9.8 32.1 32.1

Mata de Santa Genebra Transmissão3 48.1 151.8 101.1 176.9

Cantareira Transmissora2 23.0 23.0 - 42.6

Paranaíba Transmissora2 - 2.1 - 2.1

Others 11.0 28.3 224.7 224.6

Copel Distribuição 148.7 283.0 629.6 649.2

Copel Telecomunicações 62.8 103.0 164.3 214.3

Copel Comercialização - - 0.2 0.2

Copel Renováveis - - 1.5 1.5

Holding - - 1.6 1.6

Cutia Wind Farm Complex 200.0 340.0 638.6 967.5

Other Invesment4 - - 28.8 18.7

TOTAL 641.8 1,229.3 2,034.9 2,877.5

2 Planned CAPEX under review.3 Regarding the participation of Copel in Enterprises.4 Includes Voltalia São Miguel do Gostoso I Participações among others.

1 Capital budget originally approved by the Board of Directors. These values do not consider appropriation due to own

labor, interest and others.

Scheduled 20171

Subsidiary / SPCCarried

1H17

Carried

2Q17

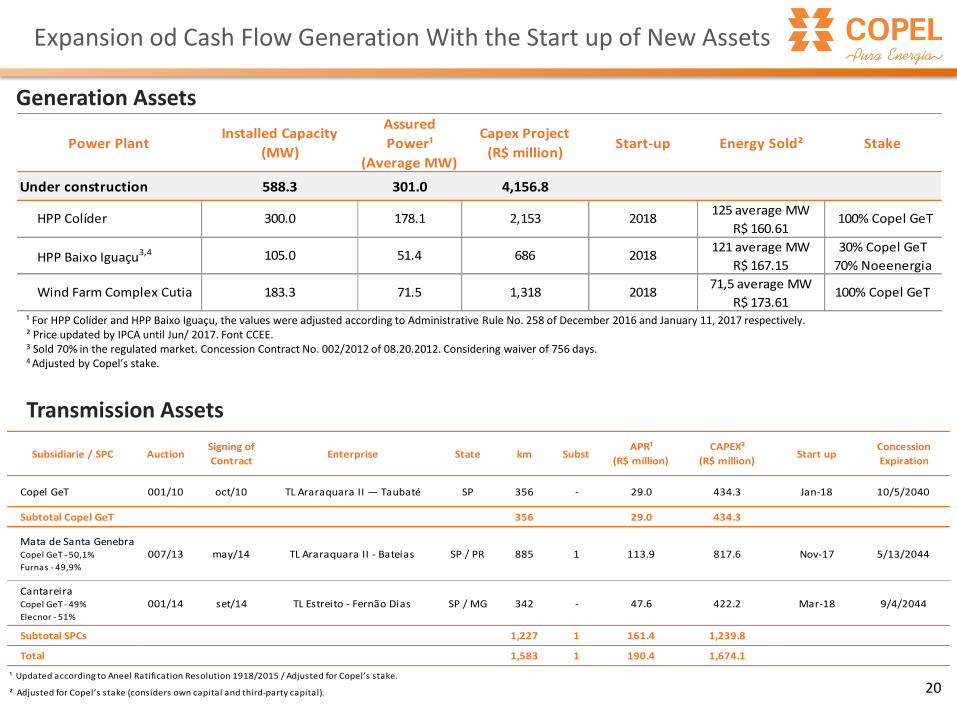

Expansion od Cash Flow Generation With the Start up of New Assets

20

Generation Assets

Power PlantInstalled Capacity

(MW)

Assured

Power¹

(Average MW)

Capex Project

(R$ million)Start-up Energy Sold² Stake

Under construction 588.3 301.0 4,156.8

125 average MW

R$ 160.61

121 average MW 30% Copel GeT

R$ 167.15 70% Noeenergia

71,5 average MW

R$ 173.61100% Copel GeTWind Farm Complex Cutia 183.3 71.5 1,318 2018

HPP Baixo Iguaçu3,4 2018105.0 51.4

HPP Colíder 300.0 178.1 100% Copel GeT20182,153

686

Transmission Assets

Subsidiarie / SPC AuctionSigning of

ContractEnterprise State km Subst

APR¹

(R$ million)

CAPEX²

(R$ million)Start up

Concession

Expiration

Copel GeT 001/10 oct/10 TL Araraquara II — Taubaté SP 356 - 29.0 434.3 Jan-18 10/5/2040

Subtotal Copel GeT 356 29.0 434.3

Mata de Santa GenebraCopel GeT - 50,1%

Furnas - 49,9%

007/13 may/14 TL Araraquara II - Bateias SP / PR 885 1 113.9 817.6 Nov-17 5/13/2044

CantareiraCopel GeT - 49%

Elecnor - 51%

001/14 set/14 TL Estreito - Fernão Dias SP / MG 342 - 47.6 422.2 Mar-18 9/4/2044

Subtotal SPCs 1,227 1 161.4 1,239.8

Total 1,583 1 190.4 1,674.1

¹ Updated according to Aneel Ratification Resolution 1918/2015 / Adjusted for Copel’s stake.

² Adjusted for Copel’s stake (considers own capital and third-party capital).

¹ For HPP Colíder and HPP Baixo Iguaçu, the values were adjusted according to Administrative Rule No. 258 of December 2016 and January 11, 2017 respectively. ² Price updated by IPCA until Jun/ 2017. Font CCEE. 3 Sold 70% in the regulated market. Concession Contract No. 002/2012 of 08.20.2012. Considering waiver of 756 days. 4 Adjusted by Copel’s stake.