apresentação do powerpointir.marfrig.com.br/en/documentos/3591_institutional... · 2q14 (%) 78%...

TRANSCRIPT

1Focus to Win

INSTITUTIONAL

PRESENTATION September, 2014

FOCUS TO WIN

2Focus to Win

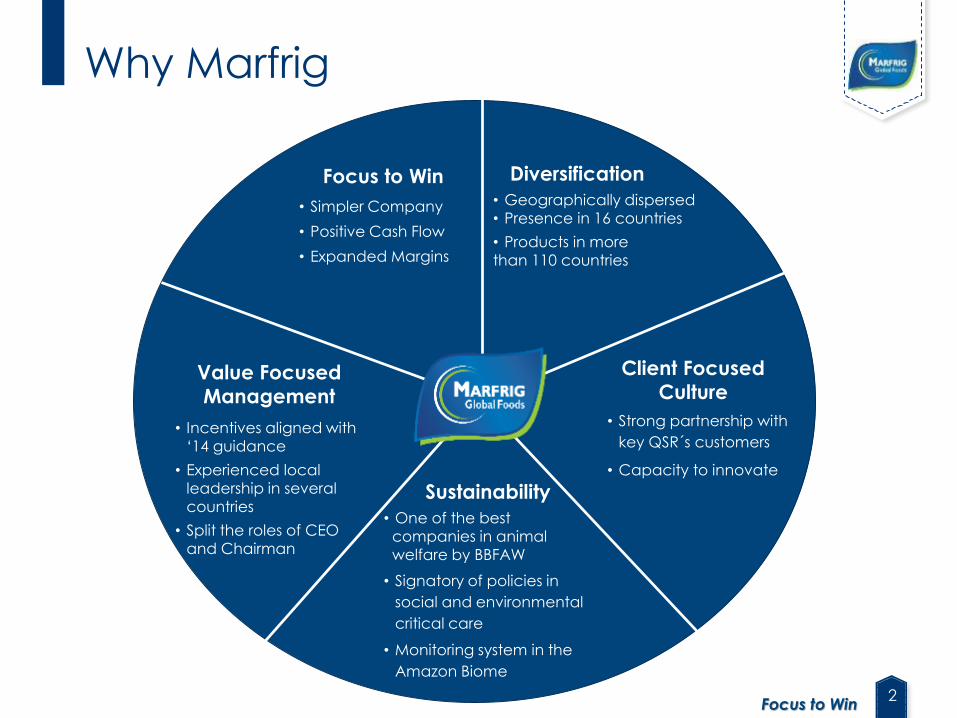

Why Marfrig

Focus to Win

• Simpler Company

• Positive Cash Flow

• Expanded Margins

Diversification

• Geographically dispersed

• Presence in 16 countries

• Products in more

than 110 countries

Value Focused

Management

• Incentives aligned with

‘14 guidance

• Experienced local

leadership in several

countries

• Split the roles of CEO

and Chairman

Sustainability

• One of the best

companies in animal

welfare by BBFAW

• Signatory of policies in

social and environmental

critical care

• Monitoring system in the

Amazon Biome

Client Focused

Culture

• Strong partnership with

key QSR´s customers

• Capacity to innovate

3Focus to Win

STRATEGIC

OVERVIEW

4Focus to Win

2Q14 breakdownby business

2Q14 breakdownby currency

2Q14 breakdownby product

Who we are | Marfrig at a glance

Net Revenue(R$ bn)

28%

29%

43%

MOY PARKKEYSTONEMARFRIG BEEF

45%

44%

9%

FURTHER PROCESSED

FRESH

OTHER

One of the world’s

largest providers of

processed food to

major restaurant

chains

FoodService

One of the largest

poultry-based

processed products

suppliers in the UK

and Europe

Retail and Food Service

World’s 3rd largest beef

producer and one of

South America’s largest

lamb suppliers

Diversified

DiversifiedAnimal

Protein Player

Strong focuson Food Service

Marfrig Group

Main Sales

Channels

Business

Description

44%

25%

20%

12%

USDEURO/POUNDREALOTHER

45%

26%

21%

9%

4.5

5.1

2Q13 2Q14

+ 15%

5Focus to Win

Non-financial Highlights

Corporate Governance: conclusion of the

transition process to separate the roles of

Chief Executive Officer and Chairman of

the Board of Directors.

Animal Welfare: Marfrig was recently

elected one the world’s best companies

in animal welfare (source: Business

Benchmark on Farm Animal Welfare,

2013), which reflects our firm commitment

to sustainability in our business chain.

6Focus to Win

STRATEGIES AND

OBJECTIVES

7Focus to Win

High single digit margins in beef business. Consistent cash generation and stricter cost management

Solid beef business

Who we were

Strong customer focus but keeping a tight grip on margins

Strong customer focus

Rapid growth Focus on profitable growth and margin expansion

Debt financed acquisitions

Accelerated organic growth

Broad based meat company

Easier to connect and to focus

Earnings volatility Earnings stability

Cash consumption Positive free cash flow

Where we are headed What have we

done so far

Uruguay returned to profitability, reduced losses in Argentina

Destination channels are being optimized

Significant margin expansion in both Moy Park and Keystone

Working to finalize JV in Indonesia and in the Middle East (Keystone)

SKU simplification in Beef Brazil, Uruguay makes up 100% ofKeystone China’s South American beef purchases

Results in line over the lastthree quarters

Cash consumption cut by R$ 1.5 billion from 1H13 to 1H14

Strategy | Business Transformation

8Focus to Win

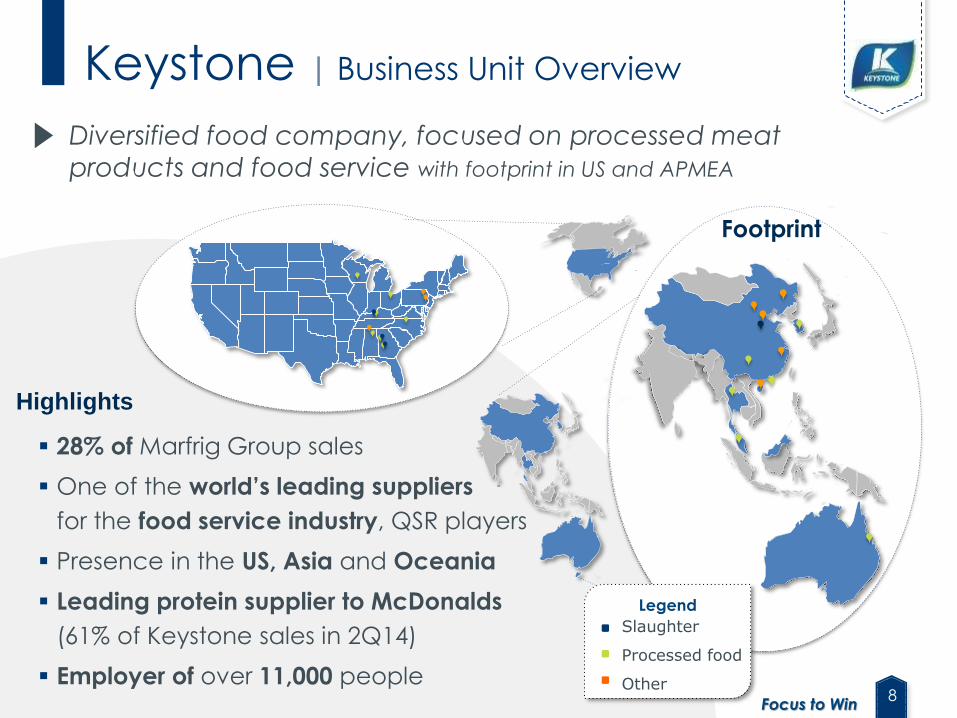

Highlights

28% of Marfrig Group sales

One of the world’s leading suppliers

for the food service industry, QSR players

Presence in the US, Asia and Oceania

Leading protein supplier to McDonalds

(61% of Keystone sales in 2Q14)

Employer of over 11,000 people

Keystone | Business Unit Overview

Footprint

Diversified food company, focused on processed meat

products and food service with footprint in US and APMEA

Legend

Slaughter

Processed food

Other

9Focus to Win

Keystone | Business Unit Overview

Geographic Presence

Geographic Coverage

Production Infrastructure

Sales ChannelsProductsProduction Structure

ProductsSales

Channels

• 13 further processing

plants

• 3 poultry vertical

integration complexes

• 1 primary processing

plant + 1 grain operation

• 1 research &

development facility

• 19 pullet farms + 61

breeder farms + 296

broiler farms

• Focused on food

service channel and

developing retail

channels

• Leading supplier to

McDonald´s

USA: #1 beef, #2

poultry and #2 fish

APMEA: #2 protein

supplier in China, sole

protein supplier to

Malaysia, Thailand

and Korea; #2 in

Australia

• Poultry, beef and fish

processed products

2Q14(%)

2Q14(%)

78%

20%

2%

Poultry

Beef

Fish

USA

APMEA

74%

26%

10Focus to Win

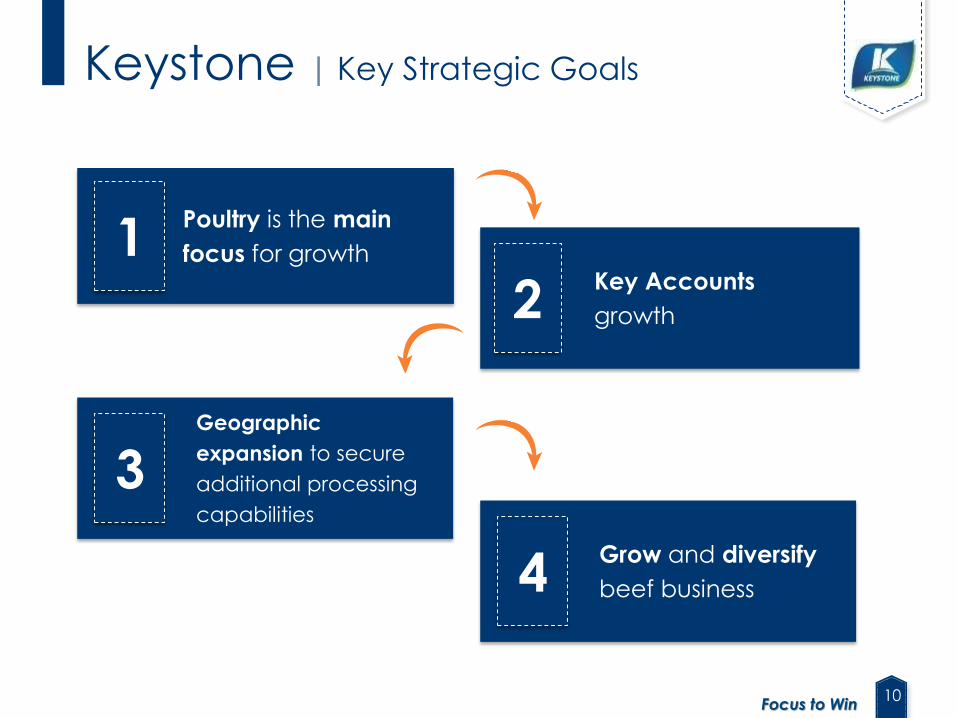

Poultry is the main

focus for growth1Key Accounts

growth2

Geographic

expansion to secure

additional processing

capabilities

3

Grow and diversify

beef business4

Keystone | Key Strategic Goals

11Focus to Win

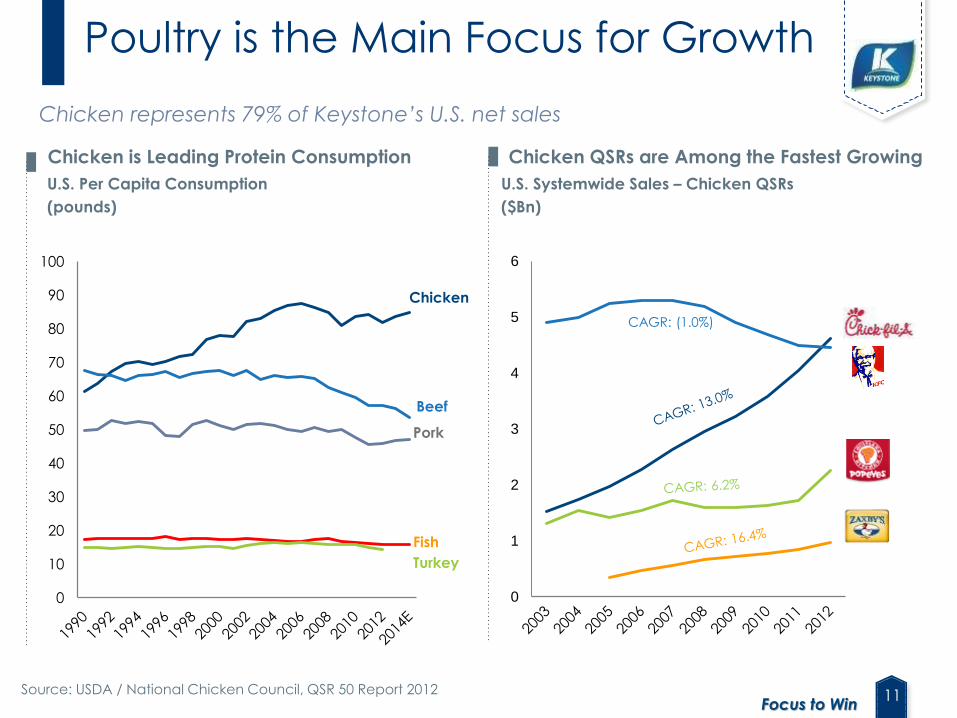

Poultry is the Main Focus for Growth

0

1

2

3

4

5

6

U.S. Systemwide Sales – Chicken QSRs

($Bn)

0

10

20

30

40

50

60

70

80

90

100

U.S. Per Capita Consumption

(pounds)

Chicken

Fish

Turkey

Pork

Beef

Chicken represents 79% of Keystone’s U.S. net sales

CAGR: (1.0%)

Chicken is Leading Protein Consumption

Source: USDA / National Chicken Council, QSR 50 Report 2012

Chicken QSRs are Among the Fastest Growing

12Focus to Win

Key Accounts Growth

Strong reputation with a diverse and high quality customer base

225 232 273362 402

39 4954

5773

264 281327

419475

2009 2010 2011 2012 2013

U.S. APMEA

16.8%

CAGR

15.6%

CAGR

Select

Key

Accounts

Attractive Growth in Key Account Sales

($MM)

13Focus to Win

Geographic Expansion to Secure

Additional Processing CapabilitiesKeystone supplies the rapidly growing QSR industry in APMEA

APMEA Overview: 4,000+ restaurants served; Facilities: 6 further processing plants; 1 primary processing plant

30%

13%12%

12%

11%

8%

6%5%

2%

1% 0%

Japan

Thailand

China

Malaysia

Korea

(%), by End-Market Country 2013

Australia

Singapore

EUOthers

Middle East

Growth Across All Markets

(MM pounds)

0

50

100

150

200

250

300

350

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

109

137

168

196

226239

257

274299

313

APMEA Growth History (Volume)

14Focus to Win

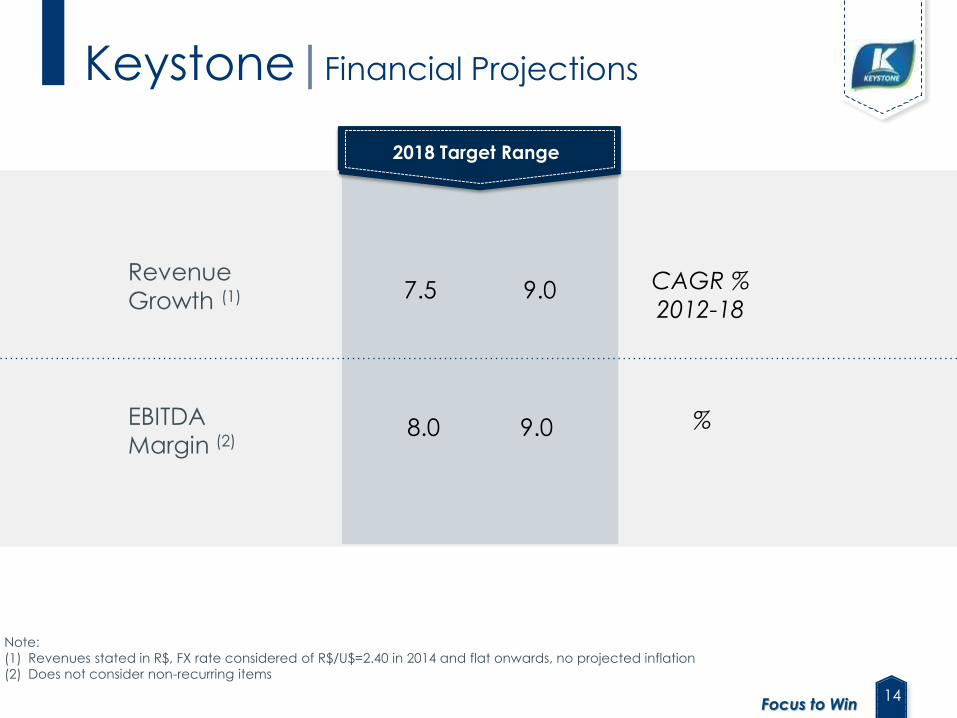

Keystone|Financial Projections

Revenue

Growth (1)

EBITDA

Margin (2)

Note:

(1) Revenues stated in R$, FX rate considered of R$/U$=2.40 in 2014 and flat onwards, no projected inflation

(2) Does not consider non-recurring items

%

CAGR %

2012-18

Faixa Alvo 2018

7.5 9.0

8.0 9.0

Faixa-alvo 2018

%

CAGR %

2012-187.0 9.0

8.0 10.0

Faixa Alvo 2018

7.5 9.0

8.0 9.0

Revenue

Growth (1)

EBITDA

Margin (2)

2018 Target Range

15Focus to Win

LegendSlaughter

Processed food

Other

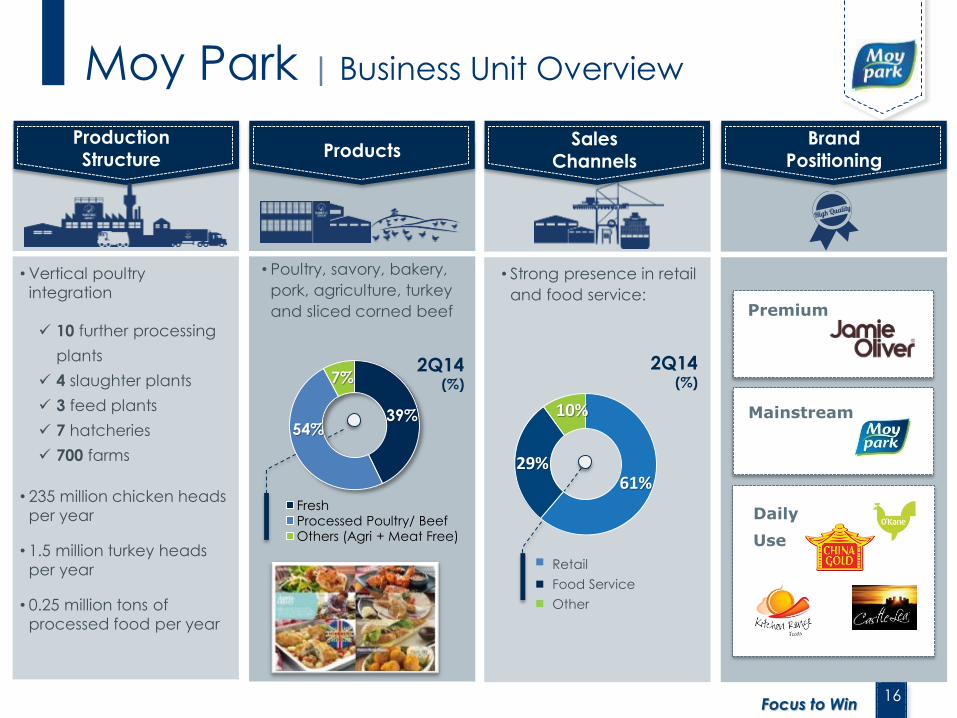

Moy Park | Business Unit Overview

26% of Marfrig Group sales

One of Europe’s leading poultry companies

Top 20 UK food business and leader in

convenience products

Northern Ireland’s largest company

Presence in the UK, Northern Ireland, France

and Holland

70 years of history

Employer of more than 8,000 people

HighlightsFootprint

Diversified protein based food company with

presence in poultry, turkey, beef and pork

16Focus to Win

Moy Park | Business Unit Overview

Production Structure

Products

• Poultry, savory, bakery,

pork, agriculture, turkey

and sliced corned beef

Brand Positioning

Premium

Mainstream

Daily

Use

Sales Channels

• Vertical poultry

integration

10 further processing

plants

4 slaughter plants

3 feed plants

7 hatcheries

700 farms

• 235 million chicken heads

per year

• 1.5 million turkey heads

per year

• 0.25 million tons of

processed food per year

2Q14(%)

• Strong presence in retail

and food service:

2012

2Q14(%)

39%54%

7%

FreshProcessed Poultry/ BeefOthers (Agri + Meat Free)

61%29%

10%

Retail

Food Service

Other

17Focus to Win

Continue expansion of

multi protein retail sales

in markets across UK,

Ireland and

Continental Europe

2

Boost presence in

the food service

distribution channel

in the UK, Ireland

and Continental

Europe

3

Moy Park | Key Strategic Goals

1

Grow core UK &

Ireland retail fresh

poultry and

convenience food

sales ahead of the

market

4Become Marfrig

global distribution

platform in Europe

18Focus to Win

Key Strengths and Investment

Positioned in the attractive UK poultry market…1

... Moy Park is a leading player in both Fresh Poultry and Convenience Food

2The company enjoys strong relationships with UK and European retailers and QSR operators…

3

Most consumed animal protein in the

UK with 728 kton sold in 2013A

Fastest growing animal protein and the

most affordable (£1,300 per ton vs.

£4,420 for Beef)

Preference for local products: 8 out of

10 shoppers would buy British when

available

#1 producer of fresh coated and

ready-to-eat poultry

It is the second largest producer in the

UK

Moy Park has brands covering the full

market

Poultry has higher growth

UK poultry production

Fresh coated poultry

Ready-to-eat poultry

#2

#1

#1

(2012A–17E CAGR in consumption volume) Retail Food Service

Larger market share in “winning”

categories and formats

Supplier to the major UK and French

QSR operators

Fast growing QSR market in France and

UK with 13-17E CAGR of 5.6% and 1.3%

Customized product solutions with Moy

Park personnel located on site of largest

clients’ facilities

1.62% 1.60%

0.13% 0.09%

Poultry Fish Pork Beef and

Veal

19Focus to WinSource: Euromonitor

UK convenience

Agri-fresh

EU convenience

Breeding Grounds

Geographical location of breeding

farms in West-Europe ensures for a

“natural” biosecurity barrier

Track record: 14% sales CAGR

since 2008 / +2.7% EBITDA margin

uplift since 2011

Strong operating cash flows

generated and re-invested to

drive future growth

Combined, the team has over

100 years of food industry

knowledge

InitiativesRelevance for

investors

Leverage poultry and beef footprint in Europe acrossUK franchise

2. Increase Presence inFood Service

Explore an increasing sales channel that will lead to sustainable growth

Tap significant opportunity with low risk and investment

1. Grow Core Business

Grow core retailfresh poultry and conveniencefood sales

3. Innovation and ChannelDevelopment

Outpace competition and increase profitability

Deliver leading consumer insights to customersDrive growth via new channels

Key Strengths and Investment

...underpinned by a strong management team with proven track-record

4Clear strategy of organic growth with multiple levers for further upside…

5…on the back of an efficient and well-invested production base6

integrated production platform

including unique poultry rearing

ensuring integrity of supply

Production footprint in Ireland

acting as natural bio-security barrier

£180m invested over the last 5 years

20Focus to Win

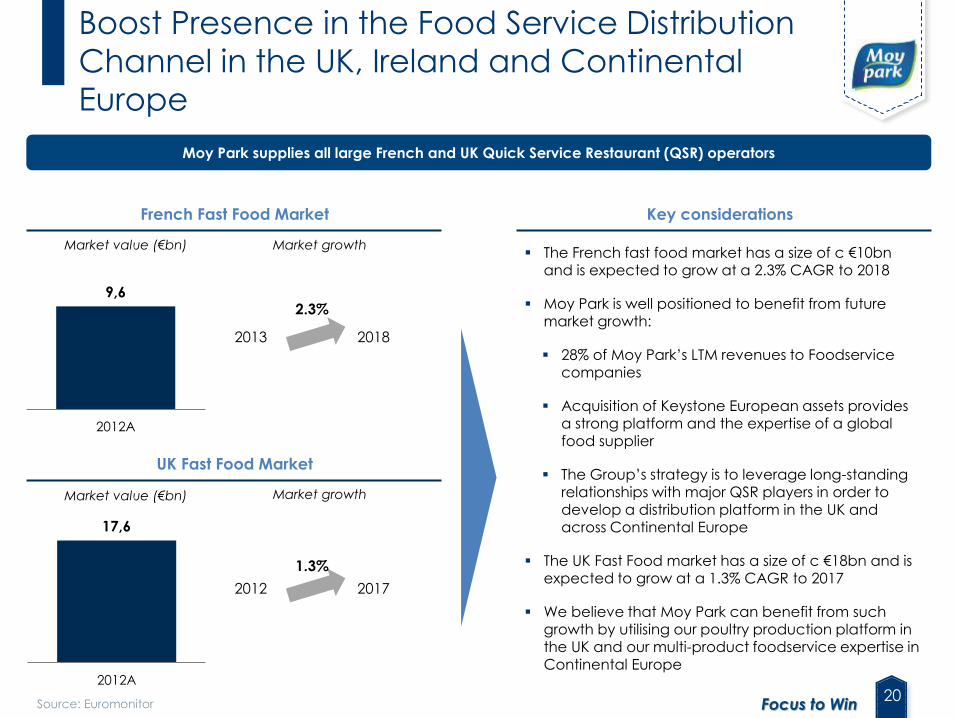

Boost Presence in the Food Service Distribution

Channel in the UK, Ireland and Continental

Europe

9,6

2012A

French Fast Food Market Key considerations

Market value (€bn)

Moy Park supplies all large French and UK Quick Service Restaurant (QSR) operators

Source: Euromonitor

The French fast food market has a size of c €10bn and is expected to grow at a 2.3% CAGR to 2018

Moy Park is well positioned to benefit from future market growth:

28% of Moy Park’s LTM revenues to Foodservice companies

Acquisition of Keystone European assets provides a strong platform and the expertise of a global food supplier

The Group’s strategy is to leverage long-standing relationships with major QSR players in order to develop a distribution platform in the UK and across Continental Europe

The UK Fast Food market has a size of c €18bn and is expected to grow at a 1.3% CAGR to 2017

We believe that Moy Park can benefit from such growth by utilising our poultry production platform in the UK and our multi-product foodservice expertise in Continental Europe

UK Fast Food Market

Market growth

17,6

2012A

Market value (€bn) Market growth

2013 2018

2.3%

2012 2017

1.3%

21Focus to Win

2nd Largest Overall Poultry Producer in the UK

and More Than Twice the Size of the Number 3

25%

B

C

D

E

A

% of total UK average bird processing per week

Market Share of Total UK Poultry Production

Source: DEFRA UK broiler slaughter, rolling 12 months to December 2013, averaged per week

Market shares are Company estimates based on third-party industry sources

Total: 17.4m birds per week

Key observations

#2 UK poultry producer provides scale and efficiency benefits which enhance Moy Park’s competitive position

Integrated supply of British-produced poultry into the convenience retail and foodservice markets provides a competitive advantage as well as a driver for growth, as end consumers value British-sourced meat

Our market share in the sale of fresh poultry to retailers offers attractive opportunities for future growth

22Focus to Win

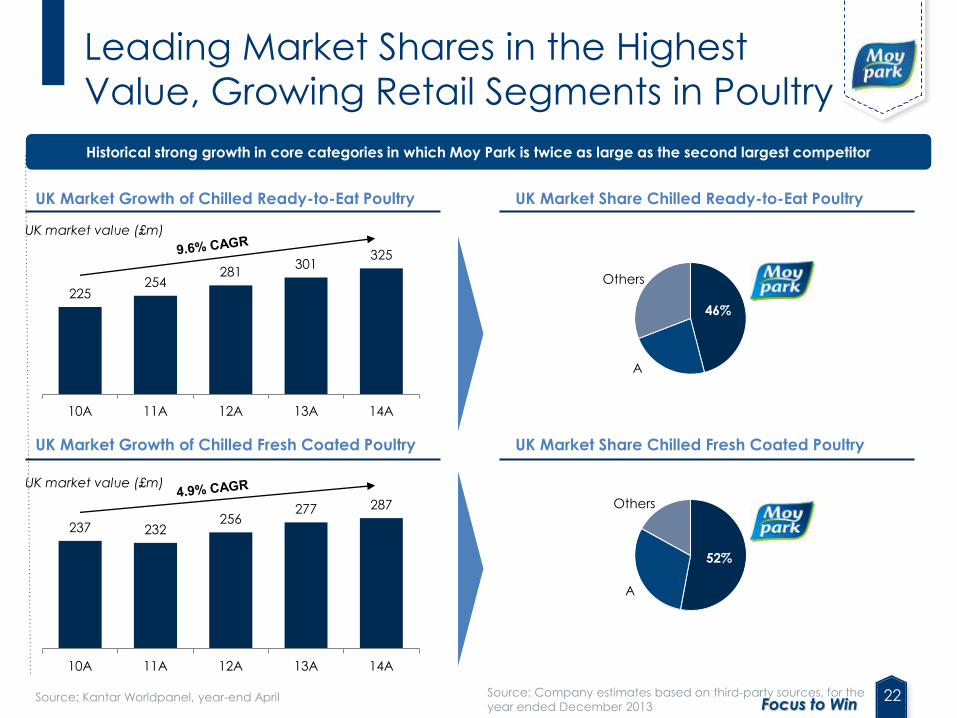

Leading Market Shares in the Highest

Value, Growing Retail Segments in Poultry

UK Market Growth of Chilled Ready-to-Eat Poultry UK Market Share Chilled Ready-to-Eat Poultry

UK Market Growth of Chilled Fresh Coated Poultry UK Market Share Chilled Fresh Coated Poultry

Source: Kantar Worldpanel, year-end April

Historical strong growth in core categories in which Moy Park is twice as large as the second largest competitor

UK market value (£m)

52%

Others

A

46%

Others

A

UK market value (£m)

Source: Company estimates based on third-party sources, for the

year ended December 2013

225254

281301

325

10A 11A 12A 13A 14A

237 232256

277 287

10A 11A 12A 13A 14A

23Focus to Win

Moy Park | Financial Projections

Note:

(1) Revenues stated in R$, FX rate considered of R$/£=3.80 in 2014 and flat onwards, no projected inflation

(2) Does not consider non-recurring items

%

CAGR %

2012-187.0 9.0

8.0 10.0

Faixa Alvo 2018

8.5 10.0

7.5 8.5

2018 Target Range

Revenue

Growth (1)

EBITDA

Margin (2)

24Focus to Win

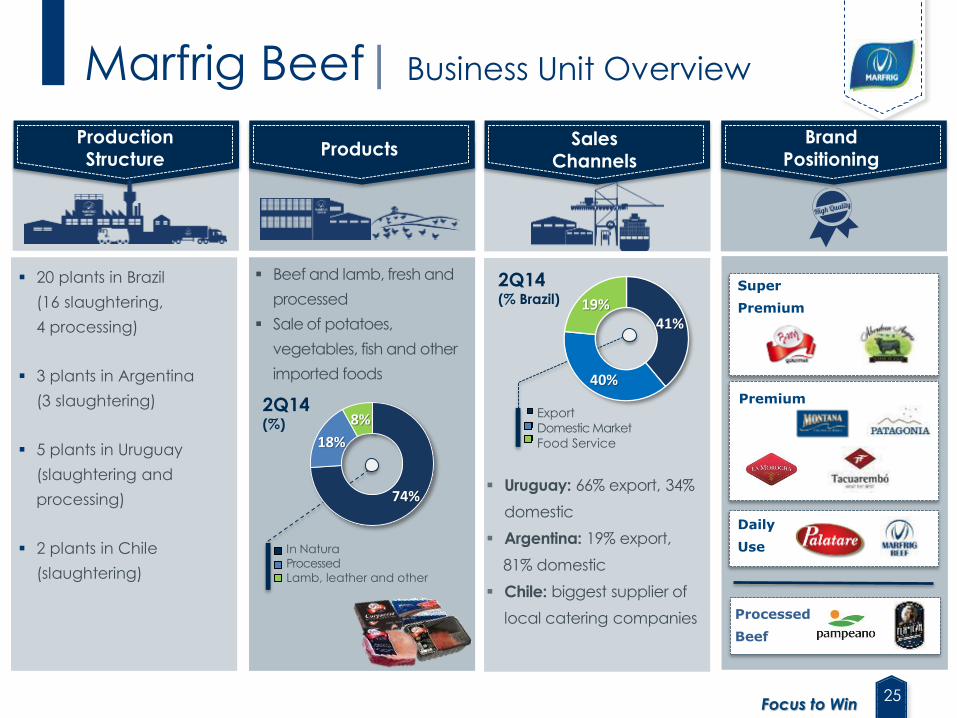

Marfrig Beef | Business Unit Overview

Highlights

46% of Marfrig Group sales

(c.36% in Brazil)

Focus on beef and lamb

Products sold in the local and

international markets

Presence in Brazil, Argentina, Uruguay

and Chile

2nd largest beef operation in Brazil

Leader in Uruguay slaughter

#1 Chilean meat importer

+22,000 employees

Legend:

Slaughter

Processed food

Other

25Focus to Win

Marfrig Beef| Business Unit Overview

Beef and lamb, fresh and

processed

Sale of potatoes,

vegetables, fish and other

imported foods

Uruguay: 66% export, 34%

domestic

Argentina: 19% export,

81% domestic

Chile: biggest supplier of

local catering companies

20 plants in Brazil

(16 slaughtering,

4 processing)

3 plants in Argentina

(3 slaughtering)

5 plants in Uruguay

(slaughtering and

processing)

2 plants in Chile

(slaughtering)

Production Structure

ProductsBrand

PositioningSales

Channels

Super

Premium

Premium

Daily

Use

Processed

Beef

Export

Domestic Market

Food Service

In Natura

Processed

Lamb, leather and other

2Q14(% Brazil)

2Q14(%)

74%

18%

8%

41%

40%

19%

26Focus to Win

Improve cash

conversion – drive

efficiencies and asset

optimization

1Top line profitable

growth – focus on

strategic distribution

channels

2

Leverage our beef

sourcing potential in

South America to

increase sales to US,

Europe and Asia

3

Marfrig Beef|Key Strategic Goals

Grow in the

value added

product segment4

27Focus to Win

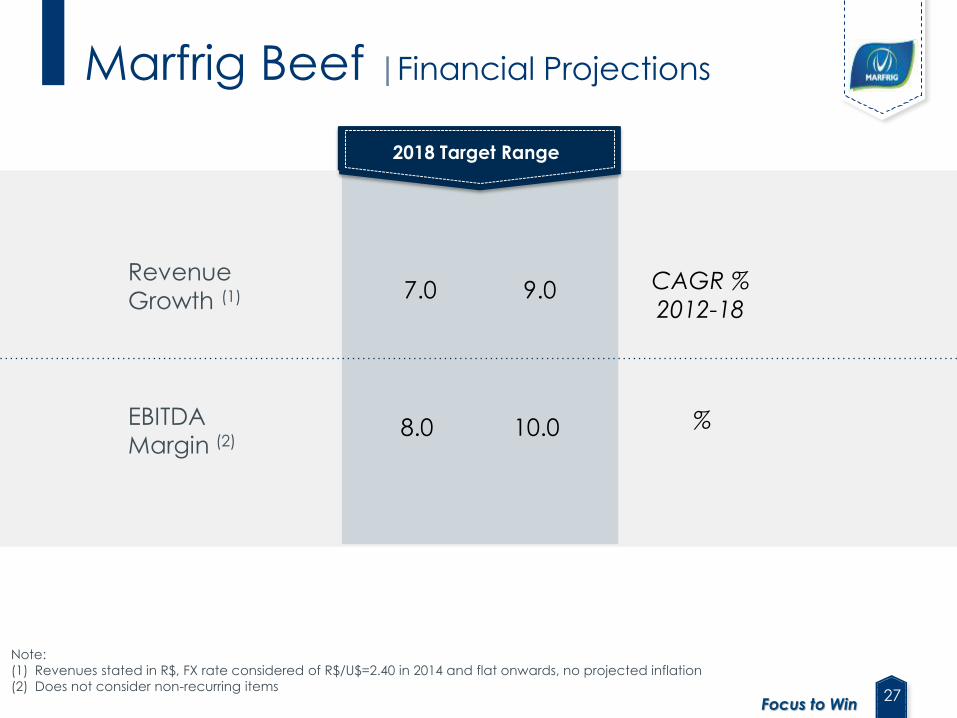

Marfrig Beef |Financial Projections

Revenue

Growth (1)

EBITDA

Margin (2)

Note:

(1) Revenues stated in R$, FX rate considered of R$/U$=2.40 in 2014 and flat onwards, no projected inflation

(2) Does not consider non-recurring items

%

CAGR %

2012-18

Faixa Alvo 2018

7.5 9.0

8.0 9.0

Faixa-alvo 2018

%

CAGR %

2012-187.0 9.0

8.0 10.0

Faixa Alvo 2018

7.0 9.0

8.0 10.0

Revenue

Growth (1)

EBITDA

Margin (2)

2018 Target Range

28Focus to Win

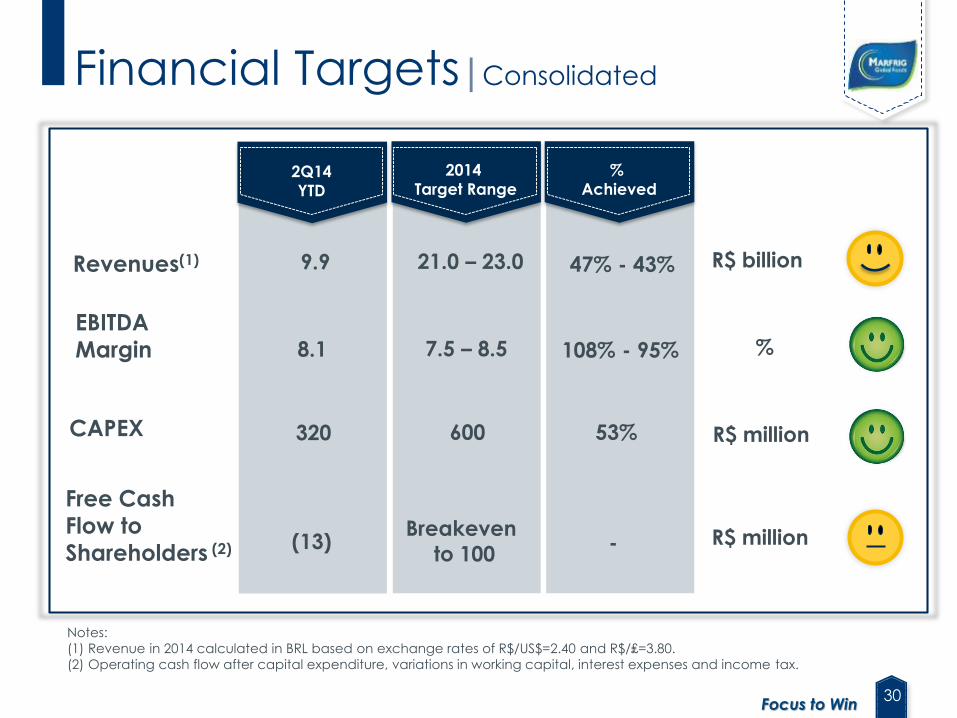

2Q14

FINANCIAL

PERFORMANCE

29Focus to Win

Main Accomplishments in 2Q14

• We remain on track to meeting our guidance for the year in all financial

indicators, which is an important step towards consolidating our operational

performance in line with our Focus to Win strategy.

• Sales above R$5.0 billion based on organic growth.

• EBITDA margins stable at levels above 7% in all business units for the third straight

quarter, despite the more challenging domestic market in Brazil.

• The net loss fell by 43% compared to 1Q14 and by more than 88% compared to

2Q13, representing the best result in the Company's recent history.

• Most balance sheet indicators remained stable, with the cash position

strengthening to close the quarter at over R$2.6 billion.

• Average debt cost down 90 bps, with the positive impacts observed already this

quarter.

30Focus to Win

Notes:

(1) Revenue in 2014 calculated in BRL based on exchange rates of R$/US$=2.40 and R$/₤=3.80.

(2) Operating cash flow after capital expenditure, variations in working capital, interest expenses and income tax.

21.0 – 23.0

2014

Target Range

7.5 – 8.5

%

Achieved

%

R$ billion

Financial Targets|Consolidated

2Q14

YTD

47% - 43%

108% - 95%

9.9

8.1

Breakeven

to 100

R$ million

(13)

600 53%320

R$ million

EBITDAMargin

Revenues(1)

Free Cash Flow to

Shareholders (2)

CAPEX

-

31Focus to Win

2Q14 Highlights

Net Revenue / Margin

• Net Revenue in the quarter topped R$5.1 billion, with a strong performance by

exports from Brazil and solid sales growth in the international business units:

• Consolidated sales grew 14.9% from 2Q13, despite the challenging scenario in

the beef segment in Brazil's domestic market.

• The strong performance is explained in part by a record quarter in Uruguay, the

stronger sales at Moy Park and the exchange variation gain in the period.

• Moy Park: + 18.2% vs. 2Q13

• Keystone: + 10.0% vs. 2Q13

• Marfrig Beef: + 16.1% vs. 2Q13

32Focus to Win

2Q14 Highlights

Performance of Business Units

• EBITDA margin in excess of 7% at all business units for the third consecutive

quarter, signaling a new level of profitability in the Company’s operations:

• The good performance of the international operations (Moy Park and

Keystone), which accounted for 54% of consolidated revenue and 49% of

EBITDA.

• Excellent performance by Marfrig Beef in Uruguay, which counterbalanced

the challenging scenario in Brazil's domestic market.

• Moy Park: 7.0% vs. 5.9% in 2Q13

• Keystone: 7.1%, vs. 5.3% in 2Q13

• Marfrig Beef: 8.6% vs. 7.1% in 2Q13

33Focus to Win

2Q14 Highlights

Balance Sheet

• We successfully conducted a number of liability management exercises

throughout 6M14 that enabled the group to bring down its overall average

debt cost by 90 bps, from 7.9% p.y. in 1Q14 to 7% p.y. this quarter, whichgenerated annualized savings of R$60.0 million in financial expenses.

• Balance sheet ratios remained unchanged for the most part, with Net Debtdeclining from R$6.9 billion in 1Q14 to R$6.7 billion this quarter.

• All our bonds are trading in the secondary market at yields of under 7.9%.

• The cash position strengthened from R$1.8 billion at year-end 2013 to over

R$2.6 billion at the end of 6M14.

• The leverage ratio was relatively unchanged at 4x.

34Focus to Win

2Q14 HighlightsCash Flow

• Cash flow in the quarter was negative R$29.7 million, which is explained primarilyby the weaker operating performance in Brazil's domestic market, the

seasonality of investment projects that increased capital expenditure this quarter

and the reduction in interest expenses.

• This quarter, we also developed a receivables securitization vehicle (FIDC) that

we now can use as a conduit to sell non-recourse domestic receivables at

competitive interest rates.

• Moy Park and Keystone maintained positive free cash flow in the first half of2014.

• Our free cash flow position ended the first half at negative R$13.4 million.

• The reduction of over R$26 million in interest expenses in the second quarter

helped the group to cut by 43% the net loss posted in the first quarter.

• We remain committed to delivering on our 2014 Guidance.

35Focus to Win

4,455

4,944 4,9784,788

5,118

2Q13 3Q13 4Q13 1Q14 2Q14

Financial Performance|Consolidated

Net Revenue(R$ million)

Breakdown by Business(%)

2Q13 2Q14

Growth versus 2Q13:

Keystone: +10.0%

Marfrig Beef: +16.1%

Moy Park: +18.2%

25%

29%

46%

+ 14.9%

36Focus to Win

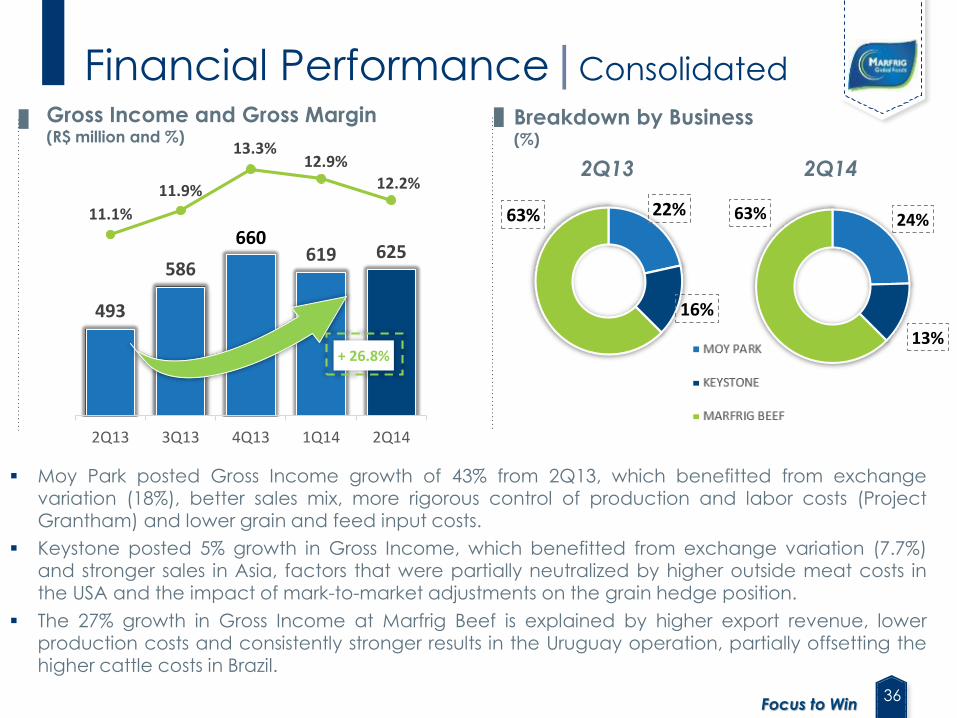

493

586

660619 625

11.1%

11.9%

13.3%12.9%

12.2%

2Q13 3Q13 4Q13 1Q14 2Q14

Breakdown by Business(%)

2Q13 2Q14

Moy Park posted Gross Income growth of 43% from 2Q13, which benefitted from exchangevariation (18%), better sales mix, more rigorous control of production and labor costs (ProjectGrantham) and lower grain and feed input costs.

Keystone posted 5% growth in Gross Income, which benefitted from exchange variation (7.7%)and stronger sales in Asia, factors that were partially neutralized by higher outside meat costs inthe USA and the impact of mark-to-market adjustments on the grain hedge position.

The 27% growth in Gross Income at Marfrig Beef is explained by higher export revenue, lowerproduction costs and consistently stronger results in the Uruguay operation, partially offsetting thehigher cattle costs in Brazil.

Financial Performance|Consolidated

Gross Income and Gross Margin(R$ million and %)

22%

16%

63% 24%

13%

63%

+ 26.8%

37Focus to Win

331 342373

357 369

7.4%

6.9%

7.5% 7.5%

7.2%

2Q13 3Q13 4Q13 1Q14 2Q14

Reduction of 20 bps in SG&A/NOR compared to 2Q13.

Moy Park registered an increase of 110 bps on higher freight and export expenses andcommercial and marketing investments to strengthen commercial ties with Key Accountsand support continued growth.

Keystone registered a drop of 220 bps in 2Q14, due to the revision of the provision for healthplans and receipt of insurance premiums, coupled with the continuous cost cutting initiatives.

Marfrig Beef registered an increase of 10 bps on increased selling expenses, driven mainly byhigher marketing expenses, which were partially offset by lower administrative expenses (e.g.,personnel and travel).

2Q13 2Q14

Breakdown by Business(%)

SG&A and SG&A/NOR(R$ million and %)

Financial Performance|Consolidated

27%

14%

59%32%

6%

62%

+ 11.4%

38Focus to Win

280

375

422403 398

6.3%

7.6%

8.5% 8.4%7.8%

2Q13 3Q13 4Q13 1Q14 2Q14

Breakdown by Business (%)

2Q13 2Q14

Consolidated Adjusted EBITDA Margin of 8.1%, in line with the target of our FOCUS TO WIN strategy

Financial Performance|Consolidated

Adjusted EBITDA and Margin(R$ million and %)

24%

24%

52%24%

25%

51%

Compared to 2Q13:

110 bps increase at Moy Park to 7.0%.

180 bps increase at Keystone to 7.1%.

150 bps increase at Marfrig Beef to 8.6%.

+ 42.1%

39Focus to Win

Net Debt – 1Q14 vs. 2Q14(R$ million)

Liquidity and Debt|Consolidated

6,8626,733

175

239

11

Dívida

Líquida1T14

Fluxo de Caixa

antes do

Capex

Capex Juros

Provisionados

Var. Cambial

da Dívida e

Caixa

Outros Dívida Líquida

2T14

(377)

(197)

38

230

177

Net Debt Cash Flow Capex Provisioned FX Variation on Other Net Debt

1Q14 before Capex Interest Cash and Debt 2Q14

40Focus to Win

* Current Liquidity = Current Assets / Current Liabilities

** Excludes the interest paid on the mandatorily

convertible debenture

Indicator 2Q14 1Q14

LTM EBITDA 1,813.6 2,275.4

Net Debt / LTM EBITDA 3.71x 3.02x

Net Debt / Annualized

Adj. EBITDA4.23x 4.25x

Net Debt / Total Assets 0.36x 0.38x

Cash and Eq. / Short

Term Debt2.52x 1.85x

Current Liquidity (*) 2.2 2.1

Duration (months) 54 52

Avg. Cost ** (p.a.) 7.0% 7.9%

Short Term (%) 11.2% 14.0%

Long Term (%) 88.8% 86.1%

In R$ (%) 4.1% 3.8%

Other Currencies (%) 95.9% 96.2%

Debt(R$ million)

Liquidity and Debt|Consolidated

2,169 1,492 1,123 1,295 1,054

6,733

8,928 7,635 7,817 7,960 8,336

2,657

11,097

9,127 8,940 9,255 9,390

Gross Debt2Q13

Gross Debt3Q13

Gross Debt4Q13

Gross Debt1Q13

Gross Debt2Q14

Cash andEquivalent

Net Debt2Q14

Long Term

Short Term

41Focus to Win

Maturity Schedule in 2Q14(R$ million)

Maturity Schedule in 1Q14(R$ million)

Short Term: R$ 1.1 billion

Liquidity and Debt|Consolidated

Short Term: R$ 1.3 billion

42Focus to Win

Cash Flow Bridge – 2Q14 (R$ million)

Cash Flow|Consolidated

As part of the ongoing efforts to improve working capital management, in 2Q14 we

focused on the line suppliers and lengthened the payment term while reducing

inventories, which dropped from 49 days in 1Q14 to 45 days this quarter. We also

recorded an impact from longer receivable terms at Marfrig Beef due to increased

exports.

(55.1)

427.0

(17.2)(26.4)

228.8

(127.6)(52.0)

377.4

(176.9)

200.6

(230.3)(29.7)

ResultadoLíquido

Itens que nãoafetam caixa

Contas areceber

de clientes

Estoques Fornecedores Outros Tributos FC Oper.antes de

Capex e Juros

Capex FC Oper. DespesaFinanceira

Fluxo decaixa livre

43Focus to Win

We recorded negative Free cash flow of R$29.7 million this quarter, which is primarily

explained by the seasonality of investment projects (R$30 million increase in capital

expenditure compared to 1Q14). On the other hand, the reduction in interest

expenses due to the liability management transactions made a positive contribution

to the result.

Free Cash Flow (after CAPEX and Interest)

(R$ million)

Cash Flow|Consolidated

44Focus to Win

6678

101 95 94

5.9%6.4%

7.6% 7.2% 7.0%

2Q13 3Q13 4Q13 1Q14 2Q14

Growth in sales revenue, influenced by the gain from exchange variation in the period (18%) and

the better domestic sales mix, especially in the UK and Ireland, with a higher concentration ofconvenience ready to eat and frozen coated poultry products.

Gross income growth of 43% from 2Q13, reflecting the investment in the Grantham Project(optimizing this processed food unit in England) that has been reducing production and laborcosts, combined with lower grains and feed input prices.

Growth of 41% in adjusted EBITDA, accompanied by margin expansion of 110 bps from 2Q13.

Moy Park 2Q14 Highlights

Net Revenue(R$ million)

Adjusted EBITDA and Margin(R$ million and %)

+ 18.2% + 41.4%

45Focus to Win

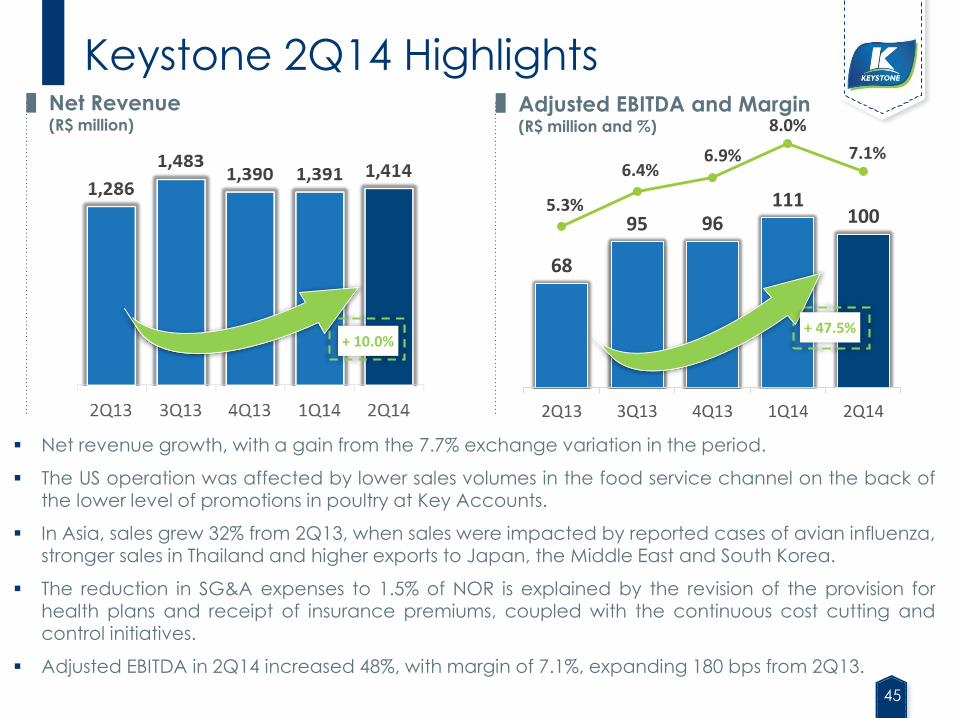

68

95 96111

1005.3%

6.4%6.9%

8.0%

7.1%

2Q13 3Q13 4Q13 1Q14 2Q14

Net revenue growth, with a gain from the 7.7% exchange variation in the period.

The US operation was affected by lower sales volumes in the food service channel on the back ofthe lower level of promotions in poultry at Key Accounts.

In Asia, sales grew 32% from 2Q13, when sales were impacted by reported cases of avian influenza,stronger sales in Thailand and higher exports to Japan, the Middle East and South Korea.

The reduction in SG&A expenses to 1.5% of NOR is explained by the revision of the provision forhealth plans and receipt of insurance premiums, coupled with the continuous cost cutting andcontrol initiatives.

Adjusted EBITDA in 2Q14 increased 48%, with margin of 7.1%, expanding 180 bps from 2Q13.

Keystone 2Q14 HighlightsNet Revenue(R$ million)

Adjusted EBITDA and Margin(R$ million and %)

+ 10.0%+ 47.5%

46Focus to Win

2,038

2,240 2,256

2,075

2,365

2Q13 3Q13 4Q13 1Q14 2Q14

145

202

226

197 203

7.1%

9.0%

10.0%9.5%

8.6%

2Q13 3Q13 4Q13 1Q14 2Q14

Net revenue growth of 16% from 2Q13, driven by the better performance of the food servicechannel in Brazil, the focus on growing exports and the average depreciation in the BRL againstthe USD of 7.7%.

Gross income grew 26.7% compared to 2Q13, mainly due to the consistent improvements in theUruguay operation and the gross income growth in the Brazilian operations due to the greaterfocus on exports.

Increase of 40% in adjusted EBITDA, with margin expansion of 150 bps from 2Q13, due to thebetter performance of the Uruguay operation and the restructuring of the Argentina operation.

Marfrig Beef 2Q14 Highlights

Net Revenue(R$ million)

Adjusted EBITDA and Margin(R$ million and %)

+ 16.1% + 39.9%

47Focus to Win

Net Income (Loss)(R$ million)

Financial Performance|Consolidated

+ 88.5%

The reduction in financial expenses contributed to reductions in the Net Loss of

43% compared to 1Q14 and 88% compared to 2Q13.

48Focus to Win

BONDS AND

EQUITY

49Focus to Win

Shareholder Structure|July, 2014

Total capital

520,747,405 shares49% Free float

253,939,253 shares

Source: Marfrig

BNDES

19.6%

MMS Part.

31.5%

Treasury0.1%

Board/Management

0.1%

6.3%

Other

42.4%

Others

1.4%

1.0%

1.3%

28.9%

26.8%

15.9%

1.4%

8.8%2.0%

0.6%

0.4%

2.2%

0.7%

8.6%

50Focus to Win

Bonds Performance| 2014

Source: Bloomberg

To Sep. 1st 2014

2020 2021

2017 2018

Repurchase

MRFG 2017

Repurchase

MRFG 2021

Retap

MRFG 2020

YTM Marfrig

51Focus to Win

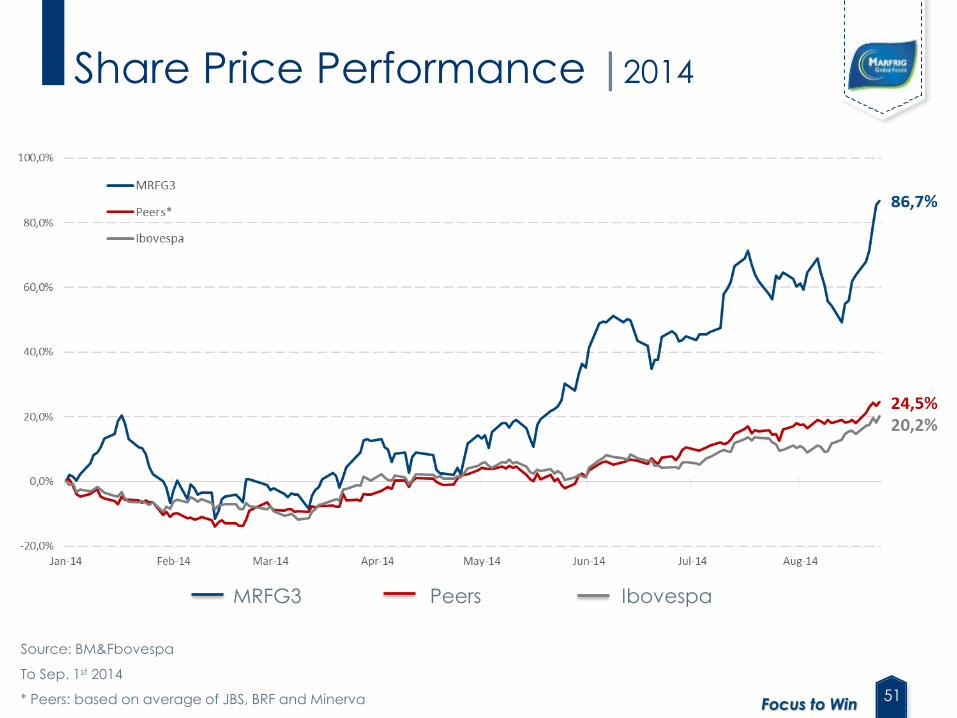

Share Price Performance |2014

MRFG3 Peers Ibovespa

Source: BM&Fbovespa

To Sep. 1st 2014

* Peers: based on average of JBS, BRF and Minerva

52Focus to Win

FINAL REMARKS

53Focus to Win

Final Remarks

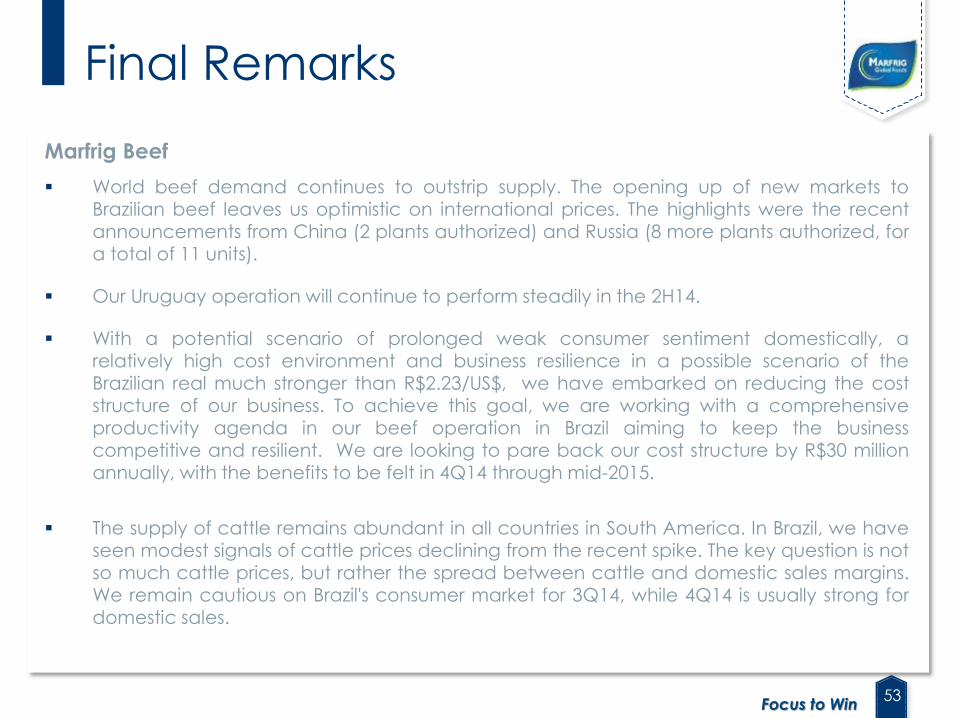

Marfrig Beef

World beef demand continues to outstrip supply. The opening up of new markets toBrazilian beef leaves us optimistic on international prices. The highlights were the recent

announcements from China (2 plants authorized) and Russia (8 more plants authorized, fora total of 11 units).

Our Uruguay operation will continue to perform steadily in the 2H14.

With a potential scenario of prolonged weak consumer sentiment domestically, arelatively high cost environment and business resilience in a possible scenario of the

Brazilian real much stronger than R$2.23/US$, we have embarked on reducing the coststructure of our business. To achieve this goal, we are working with a comprehensiveproductivity agenda in our beef operation in Brazil aiming to keep the businesscompetitive and resilient. We are looking to pare back our cost structure by R$30 millionannually, with the benefits to be felt in 4Q14 through mid-2015.

The supply of cattle remains abundant in all countries in South America. In Brazil, we haveseen modest signals of cattle prices declining from the recent spike. The key question is notso much cattle prices, but rather the spread between cattle and domestic sales margins.We remain cautious on Brazil's consumer market for 3Q14, while 4Q14 is usually strong fordomestic sales.

54Focus to Win

Final Remarks

Moy Park

The business remains strong and is gaining new momentum among both existing and newclients, as shown by the recent sales trajectory.

To continue sustaining and uplifting margins, we will focus on three fronts:

improving the profitability of our convenience business by reducing SG&A expenses toeliminate unnecessary complexity;

continuing to focus on improving the profitability of our plants in France, which todayare running at EBITDA margins of around 4%, compared to negative margins a yearago;

analyzing how to best take advantage of a grain environment with structurally lower

prices, especially in 4Q14.

Our attention to customer service, responsiveness and quality will continue to receive ourutmost attention as part of our promise to our clients.

The greater exposure of the Moy Park brand during the World Cup should lead to gains in

regions where the brand carries a relevant position (United Kingdom and Ireland).

55Focus to Win

Final Remarks

Keystone

Given the current grain environment, there is no pressure on margins coming from this end.

Keystone continues to lead with best-in class SG&A management, with a ratio to sales of well below 4%.

The price scenario for third-party sourced chicken meat in the United States (we are 70%

integrated in the country) could remain challenging, though some recent signs indicate that price pressure might abate.

Our Asia operation is doing well and operating at full steam, benefitting from the impeccable track record in customer service and flawless execution in the industrial operations.

56Focus to Win

Final Remarks

Strategy

We continue to improve the group's operating performance and remain committed to our guidance. Margins have risen and remained reasonably stable for the third consecutive quarter.

We have seen a great level of interest in the beef supply chain from international investors. The current US beef picture should not change much in the near future and Australia will not be able to supply Asia by itself, given that demand continues to grow. At the same time, the industry has reached mature levels of consolidation in South America.

We continue to exploit alternatives to accelerate growth at both Moy Park and Keystone:

Moy Park successfully tapped the sterling bond market in May 2014, opening up ourstory to a host of new and important UK investors. We believe Moy Park could be well

positioned for an IPO if we decide to pursue that path.

Keystone’s growth remains centered on Asia and with a number of new selectiveclients. We have entertained a number of constructive discussions with several investorsinterested in taking a minority stake in the company in view of its prosperous future, butwe have not yet decided which path to ultimately take.

57Focus to Win

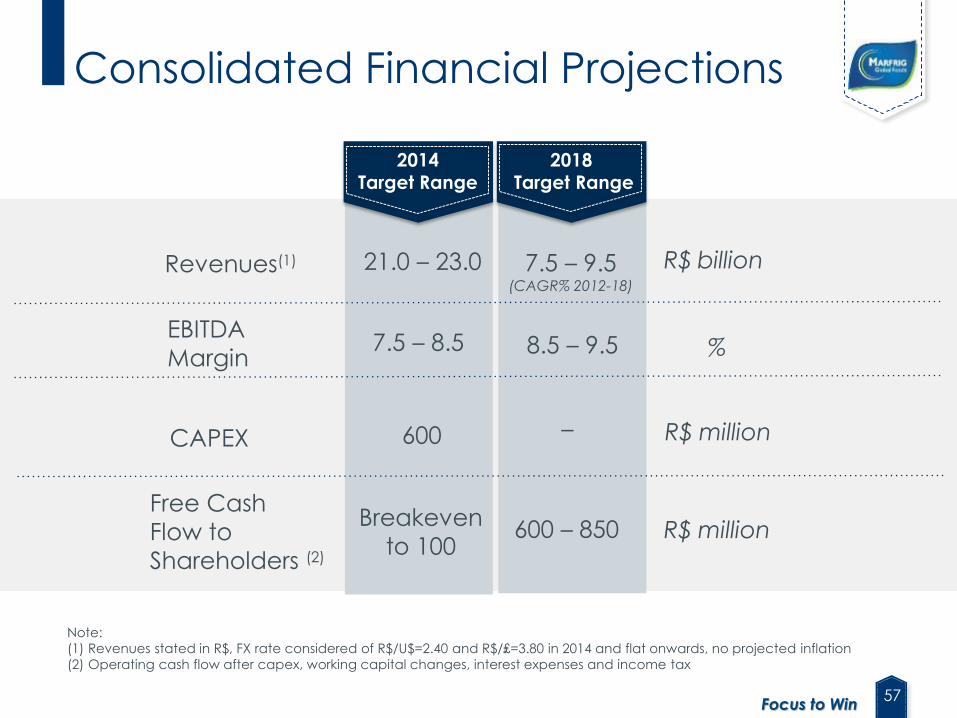

EBITDA

Margin

Note:

(1) Revenues stated in R$, FX rate considered of R$/U$=2.40 and R$/₤=3.80 in 2014 and flat onwards, no projected inflation

(2) Operating cash flow after capex, working capital changes, interest expenses and income tax

Revenues(1) 21.0 – 23.0

2014Target Range

7.5 – 9.5(CAGR% 2012-18)

7.5 – 8.5 8.5 – 9.5

2018Target Range

Free Cash

Flow to

Shareholders (2)

600 –

%

R$ billion

R$ millionCAPEX

Breakeven

to 100600 – 850 R$ million

Consolidated Financial Projections

58Focus to Win

Disclaimer

This material is a presentation of general information about MarfrigGlobal Foods S.A. and its consolidated subsidiaries (jointly the“Corporation”) on the date hereof. The information is presented insummary form and does not purport to be complete.

No representation or warranty, either expressed or implied, ismade regarding the accuracy or scope of the information herein.Neither the Company nor any of its affiliated companies,consultants or representatives undertake any responsibility for anylosses or damages arising from any of the information presented orcontained in this presentation. The information contained in thispresentation is up to date as of June 30, 2014, and, unless statedotherwise, is subject to change without prior notice. Neither theCorporation nor any of its affiliated companies, consultants orrepresentatives have signed any commitment to update suchinformation after the date hereof. This presentation should not beconstrued as a legal, tax or investment recommendation or anyother type of advice.

The data contained herein were obtained from various externalsources and the Corporation has not verified said data throughany independent source. Therefore, the Corporation makes nowarranties as to the accuracy or completeness of such data,which involve risks and uncertainties and are subject to changebased on various factors.

This presentation includes forward-looking statements. Suchstatements do not constitute historical fact and reflect the beliefsand expectations of the Corporation’s management. The words“anticipates,” “hopes,” “expects,” “estimates,” “intends,”“projects,” “plans,” “predicts,” “projects,” “aims” and other similarexpressions are used to identify such statements.

Although the Corporation believes that the expectations andassumptions reflected by these forward-looking statements arereasonable and based on the information currently available to itsmanagement, it cannot guarantee results or future events. Suchforward-looking statements should be considered with caution,since actual results may differ materially from those expressed orimplied by such statements. Securities are prohibited from beingoffered or sold in the United States unless they are registered orexempt from registration in accordance with the U.S. SecuritiesAct of 1933, as amended (“Securities Act”). Any future offering ofsecurities must be made exclusively through an offeringmemorandum. This presentation does not constitute an offer,invitation or solicitation to subscribe or acquire any securities, andno part of this presentation nor any information or statementcontained herein should be used as the basis for or considered inconnection with any contract or commitment of any nature. Anydecision to buy securities in any offering conducted by theCorporation should be based solely on the information containedin the offering documents, which may be published or distributedopportunely in connection with any security offering conductedby the Company, depending on the case.

59Focus to Win

IR Contacts

Website

www.marfrig.com.br/ir

Address

Avenida

Chedid Jafet, 222

Bloco A - 5th floor

São Paulo - SP - Brasil

+55 (11)

3792-8650

3792-8600

Telephone

@