april 2013 - hsbc global asset management · hsbc flexi debt fund pg 44 ... are gaining ground on a...

TRANSCRIPT

April 2013

Index

1

In this Issue ...

Fund Manager Commentary Pg 2

HSBC Equity Fund Pg 6

HSBC India Opportunities Fund Pg 8

HSBC Midcap Equity Fund Pg 10

HSBC Progressive Themes Fund Pg 12

HSBC Tax Saver Equity Fund Pg 14

HSBC Unique Opportunities Fund Pg 16

HSBC Dynamic Fund Pg 18

HSBC Emerging Markets Fund Pg 20

HSBC Small Cap Fund Pg 21

HSBC Brazil Fund Pg 23

Fund Managers - Equity Pg 24

Comparative Performance of Equity Schemes Pg 26

HSBC MIP - Savings Plan Pg 29

HSBC MIP - Regular Plan Pg 31

HSBC Income Fund - Investment Plan Pg 33

HSBC Income Fund - Short Term Plan Pg 35

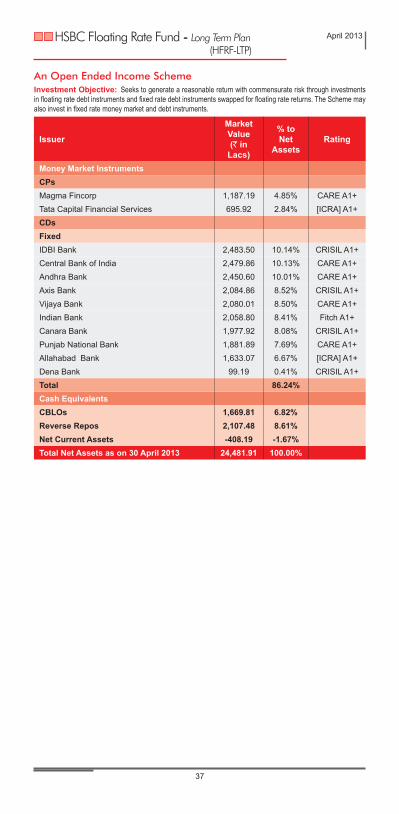

HSBC Floating Rate Fund - Long Term Plan Pg 37

HSBC Cash Fund Pg 39

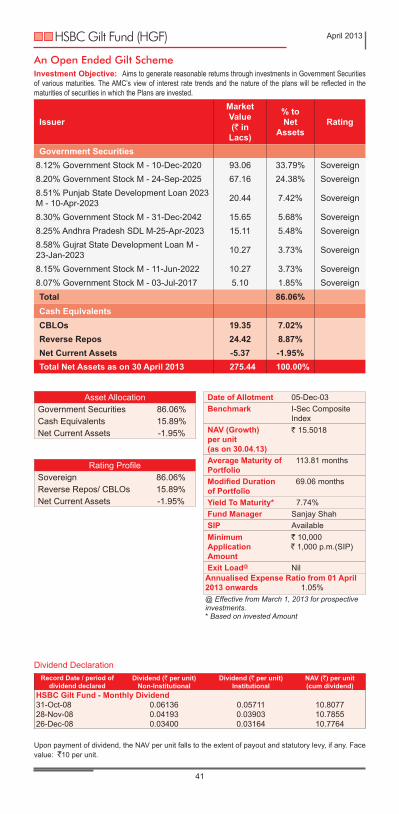

HSBC Gilt Fund Pg 41

HSBC Ultra Short Term Bond Fund Pg 42

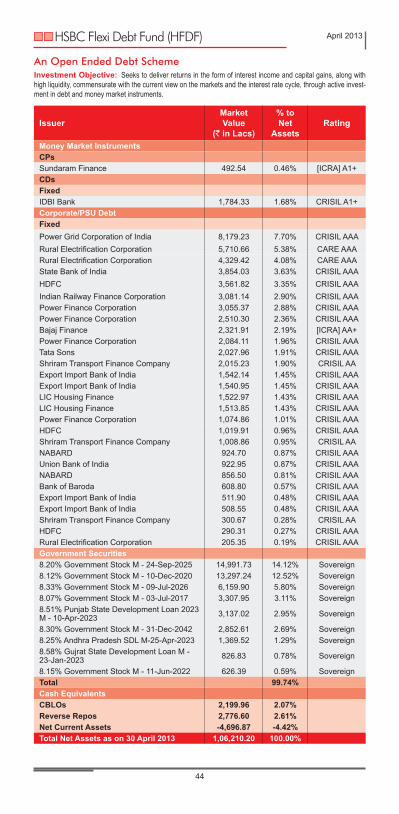

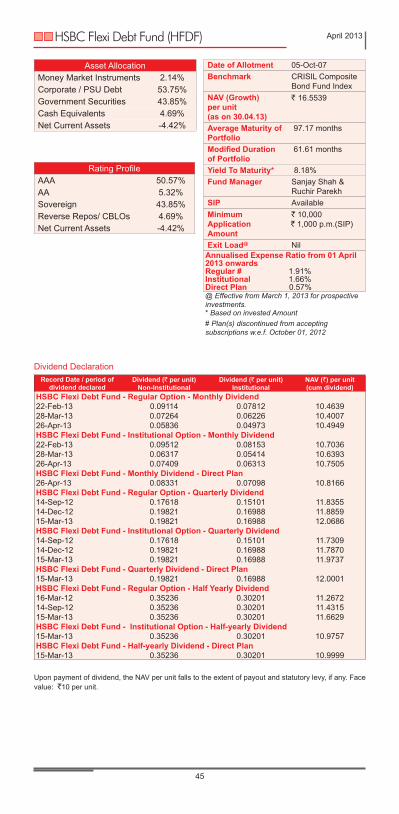

HSBC Flexi Debt Fund Pg 44

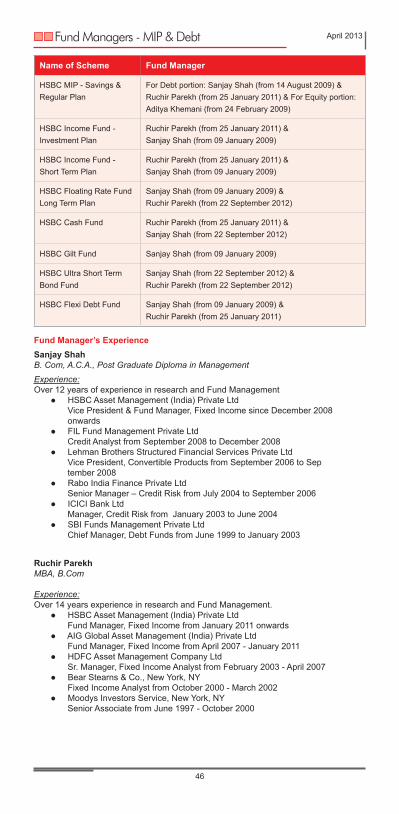

Fund Managers - MIP & Debt Pg 46

Comparative Performance of MIP & Debt Schemes Pg 47

Fund Manager Commentary April 2013

2

Equity & MIP

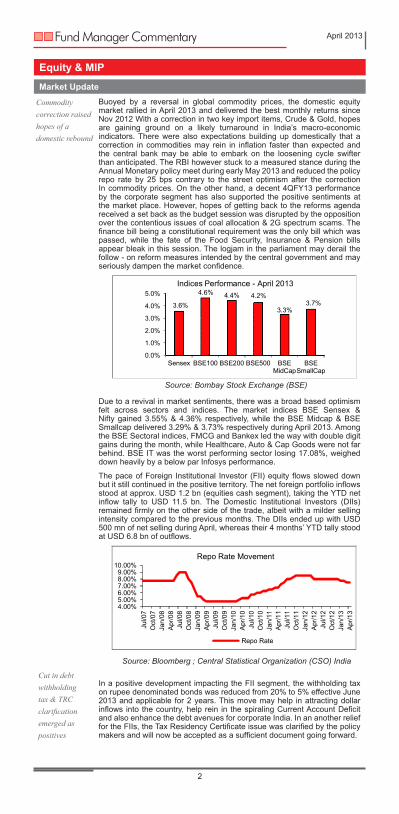

Market UpdateBuoyed by a reversal in global commodity prices, the domestic equity market rallied in April 2013 and delivered the best monthly returns since Nov 2012 With a correction in two key import items, Crude & Gold, hopes are gaining ground on a likely turnaround in India’s macro-economic indicators. There were also expectations building up domestically that a correction in commodities may rein in inflation faster than expected and the central bank may be able to embark on the loosening cycle swifter than anticipated. The RBI however stuck to a measured stance during the Annual Monetary policy meet during early May 2013 and reduced the policy repo rate by 25 bps contrary to the street optimism after the correction In commodity prices. On the other hand, a decent 4QFY13 performance by the corporate segment has also supported the positive sentiments at the market place. However, hopes of getting back to the reforms agenda received a set back as the budget session was disrupted by the opposition over the contentious issues of coal allocation & 2G spectrum scams. The finance bill being a constitutional requirement was the only bill which was passed, while the fate of the Food Security, Insurance & Pension bills appear bleak in this session. The logjam in the parliament may derail the follow - on reform measures intended by the central government and may seriously dampen the market confidence.

Due to a revival in market sentiments, there was a broad based optimism felt across sectors and indices. The market indices BSE Sensex & Nifty gained 3.55% & 4.36% respectively, while the BSE Midcap & BSE Smallcap delivered 3.29% & 3.73% respectively during April 2013. Among the BSE Sectoral indices, FMCG and Bankex led the way with double digit gains during the month, while Healthcare, Auto & Cap Goods were not far behind. BSE IT was the worst performing sector losing 17.08%, weighed down heavily by a below par Infosys performance.

The pace of Foreign Institutional Investor (FII) equity flows slowed down but it still continued in the positive territory. The net foreign portfolio inflows stood at approx. USD 1.2 bn (equities cash segment), taking the YTD net inflow tally to USD 11.5 bn. The Domestic Institutional Investors (DIIs) remained firmly on the other side of the trade, albeit with a milder selling intensity compared to the previous months. The DIIs ended up with USD 500 mn of net selling during April, whereas their 4 months’ YTD tally stood at USD 6.8 bn of outflows.

In a positive development impacting the FII segment, the withholding tax on rupee denominated bonds was reduced from 20% to 5% effective June 2013 and applicable for 2 years. This move may help in attracting dollar inflows into the country, help rein in the spiraling Current Account Deficit and also enhance the debt avenues for corporate India. In an another relief for the FIIs, the Tax Residency Certificate issue was clarified by the policy makers and will now be accepted as a sufficient document going forward.

Cut in debt withholding tax & TRC clarification emerged as positives

Commodity correction raised hopes of a domestic rebound

Source: Bloomberg ; Central Statistical Organization (CSO) India

Source: Bombay Stock Exchange (BSE)

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Sensex BSE100 BSE200 BSE500 BSEMidCap

BSESmallCap

3.6%

4.6% 4.4% 4.2%

3.3% 3.7%

Indices Performance - April 2013

4.00%5.00%6.00%7.00%8.00%9.00%

10.00%

Jul/0

7O

ct/0

7Ja

n/08

Apr

/08

Jul/0

8O

ct/0

8Ja

n/09

Apr

/09

Jul/0

9O

ct/0

9Ja

n/10

Apr

/10

Jul/1

0O

ct/1

0Ja

n/11

Apr

/11

Jul/1

1O

ct/1

1Ja

n/12

Apr

/12

Jul/1

2O

ct/1

2Ja

n/13

Apr

/13

Repo Rate Movement

Repo Rate

Inflation & Industrial Growth

Headline Inflation falls further

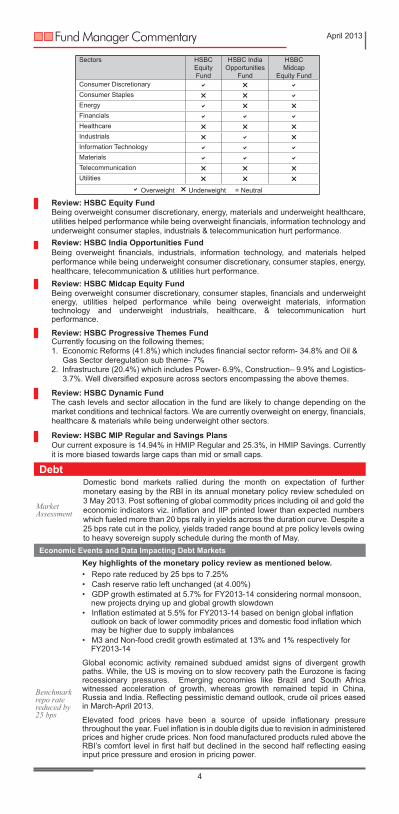

The headline Wholesale Price Index (WPI) figure for Mar 2013 came in at 5.96% YoY (6.84% in Feb 2013) its lowest reading for close to 3.5 years. Following on the downward trend, the core inflation also eased further to 3.5% YoY (3.8% in Feb 2013). Though, these better readings on the inflation may provide room for the RBI to ease policy rates in the near term, they continued on a relatively hawkish view as gauged from the 03 May 2013 policy meet. The Consumer Price Index (CPI) remained in double digit range for Mar 2013 (at 10.4% vs. 10.9% in Mar 2013) and that may be a key variable to look out for in the radar of RBI

IIP growth remained in the positive zone

The Index of Industrial Production (IIP) for February 2013 recorded a growth of 0.6% YoY (2.4% in January 2013). The growth was led by an expansion in manufacturing sector (up 2.2%), while both mining and electricity contracted by -8.1% & -3.2% respectively. While the growth trend in IIP though being marginal is still encouraging, a few more months of sustained growth may be needed to exude enough optimism.

Global Economic Scenario

Strong US data & ECB rate cut revived sentiments

April 2013 turned out to be a strong month for most of the global markets with the release of positive macro data supporting the performance, especially in the US. The US equities extended their recent rally with the S&P 500 reaching a fresh record high. The US unemployment rate fell to a four year low of 7.5% for April 2013 and this may be reinforcing the faith that the recovery in the economy is steady. Elsewhere in Eurozone, an accommodative monetary policy stance by the European Central Bank (ECB) boosted the confidence of the market participants. The ECB reduced its main refinancing rate by 25 bps to a historical low of 0.5%, its marginal lending facility rate by 50 bps to 1%, while kept the deposit rate unchanged at 0%. The ECB commentary gave enough hints on continuing with their accommodative monetary policy and did not rule out further cuts in the refinancing rate.

Going ForwardAfter a worrisome month of March when the macro data raised alarm in the form of an all-time high current account deficit, April brought some hopes to the table. The price correction in global commodities, especially that of Oil & Gold would be a silver lining for an economy like India with a high proportion of those imports. However it is important to note that the reversal in the commodity prices should be structural and the prices should sustain at these levels or below for any meaningful benefit for the economy in the medium term. On the other hand, the reforms push has lost its momentum as the government may find it difficult to pass and implement key policy measures owing to the parliament stalemate and electoral compulsions. The relatively hawkish commentary of the RBI notwithstanding, the monetary easing exercise may have already started albeit at a slower pace. The retreating core inflation may mean that the room for policy support from the RBI has increased and the recent fall in commodity prices may help to stimulate the process further. We remain firm believers in the long term growth potential of the Indian economy, given that the structural growth levers of the economy are all intact. As a fund house, we follow a selective bottom-up strategy to identify stocks that are at the same time cheap and profitable. We thus advise investors to stay invested & continue with their allocation into equities and not get too much perturbed by the market volatility.

Source: Bloomberg, for all data except where mentioned otherwise

Fund Manager Commentary April 2013

3

Source: Bloomberg ; Central Statistical Organization (CSO) India

Source: Bloomberg ; Central Statistical Organization (CSO) India

9.7%

9.7%

9.6%

9.5%

9.4%

9.8%

10.0%

9.9%

9.5%

7.7%

7.2%

7.6%

7.7%

7.5%

7.6% 7.6%

7.5%

8.0% 8.1%

7.3% 7.2%

7.3% 7.3% 6.8%

6.0% 5.0%6.0%7.0%8.0%9.0%

10.0%11.0%

Mar

/11

Apr

/11

May

/11

Jun/

11Ju

l/11

Aug

/11

Sep

/11

Oct

/11

Nov

/11

Dec

/11

Jan/

12Fe

b/12

Mar

/12

Apr

/12

May

/12

Jun/

12Ju

l/12

Aug

/12

Sep

/12

Oct

/12

Nov

/12

Dec

/12

Jan/

13Fe

b/13

Mar

/13

Wholesale Price Index Inflation (WPI)

WPI YoY growth (New series; base 2004-05)

7.5%

6.7%

9.4%

5.3%

6.2% 9.5%

3.7% 3.4%

2.5% -5.0%

6.0% 2.7%

1.0%

4.3%

-2.8% -1.3%

2.5%

-2.0%

-0.1% 2.0%

-0.7%

8.4%

-1.0%

-0.5%

-10.0%-5.0%0.0%5.0%

10.0%15.0%

Mar

/11

Apr

/11

May

/11

Jun/

11Ju

l/11

Aug

/11

Sep

/11

Oct

/11

Nov

/11

Dec

/11

Jan/

12Fe

b/12

Mar

/12

Apr

/12

May

/12

Jun/

12Ju

l/12

Aug

/12

Sep

/12

Oct

/12

Nov

/12

Dec

/12

Jan/

13Fe

b/13

Index of Industrial Production (IIP)

IIP YoY Growth (New Series; base 2004- 05)

Fund Manager Commentary April 2013

4

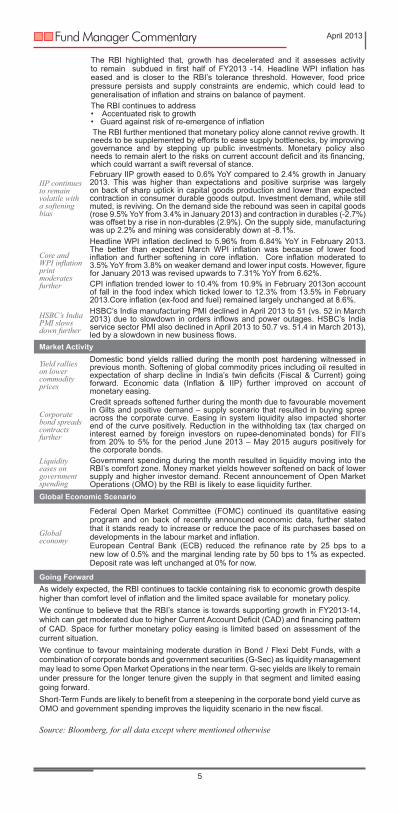

Review: HSBC Progressive Themes FundCurrently focusing on the following themes; 1. Economic Reforms (41.8%) which includes financial sector reform- 34.8% and Oil & Gas Sector deregulation sub theme- 7%2. Infrastructure (20.4%) which includes Power- 6.9%, Construction– 9.9% and Logistics- 3.7%. Well diversified exposure across sectors encompassing the above themes.

Review: HSBC Dynamic FundThe cash levels and sector allocation in the fund are likely to change depending on the market conditions and technical factors. We are currently overweight on energy, financials, healthcare & materials while being underweight other sectors.

Review: HSBC MIP Regular and Savings PlansOur current exposure is 14.94% in HMIP Regular and 25.3%, in HMIP Savings. Currently it is more biased towards large caps than mid or small caps.

Review: HSBC Midcap Equity FundBeing overweight consumer discretionary, consumer staples, financials and underweight energy, utilities helped performance while being overweight materials, information technology and underweight industrials, healthcare, & telecommunication hurt performance.

Sectors HSBC Equity Fund

HSBC India Opportunities

Fund

HSBCMidcap

Equity FundConsumer Discretionary Consumer Staples Energy Financials Healthcare Industrials Information Technology Materials Telecommunication Utilities

Overweight Underweight = Neutral

Review: HSBC India Opportunities FundBeing overweight financials, industrials, information technology, and materials helped performance while being underweight consumer discretionary, consumer staples, energy, healthcare, telecommunication & utilities hurt performance.

Review: HSBC Equity FundBeing overweight consumer discretionary, energy, materials and underweight healthcare, utilities helped performance while being overweight financials, information technology and underweight consumer staples, industrials & telecommunication hurt performance.

Debt

Market Assessment

Domestic bond markets rallied during the month on expectation of further monetary easing by the RBI in its annual monetary policy review scheduled on 3 May 2013. Post softening of global commodity prices including oil and gold the economic indicators viz. inflation and IIP printed lower than expected numbers which fueled more than 20 bps rally in yields across the duration curve. Despite a 25 bps rate cut in the policy, yields traded range bound at pre policy levels owing to heavy sovereign supply schedule during the month of May.

Economic Events and Data Impacting Debt Markets

Benchmark repo rate reduced by 25 bps

Key highlights of the monetary policy review as mentioned below.• Repo rate reduced by 25 bps to 7.25%• Cash reserve ratio left unchanged (at 4.00%)• GDP growth estimated at 5.7% for FY2013-14 considering normal monsoon, new projects drying up and global growth slowdown• Inflation estimated at 5.5% for FY2013-14 based on benign global inflation outlook on back of lower commodity prices and domestic food inflation which may be higher due to supply imbalances• M3 and Non-food credit growth estimated at 13% and 1% respectively for FY2013-14 Global economic activity remained subdued amidst signs of divergent growth paths. While, the US is moving on to slow recovery path the Eurozone is facing recessionary pressures. Emerging economies like Brazil and South Africa witnessed acceleration of growth, whereas growth remained tepid in China, Russia and India. Reflecting pessimistic demand outlook, crude oil prices eased in March-April 2013.

Elevated food prices have been a source of upside inflationary pressure throughout the year. Fuel inflation is in double digits due to revision in administered prices and higher crude prices. Non food manufactured products ruled above the RBI’s comfort level in first half but declined in the second half reflecting easing input price pressure and erosion in pricing power.

The RBI highlighted that, growth has decelerated and it assesses activity to remain subdued in first half of FY2013 -14. Headline WPI inflation has eased and is closer to the RBI’s tolerance threshold. However, food price pressure persists and supply constraints are endemic, which could lead to generalisation of inflation and strains on balance of payment.The RBI continues to address• Accentuated risk to growth• Guard against risk of re-emergence of inflation The RBI further mentioned that monetary policy alone cannot revive growth. It needs to be supplemented by efforts to ease supply bottlenecks, by improving governance and by stepping up public investments. Monetary policy also needs to remain alert to the risks on current account deficit and its financing, which could warrant a swift reversal of stance.

IIP continues to remain volatile with a softening bias

February IIP growth eased to 0.6% YoY compared to 2.4% growth in January 2013. This was higher than expectations and positive surprise was largely on back of sharp uptick in capital goods production and lower than expected contraction in consumer durable goods output. Investment demand, while still muted, is reviving. On the demand side the rebound was seen in capital goods (rose 9.5% YoY from 3.4% in January 2013) and contraction in durables (-2.7%) was offset by a rise in non-durables (2.9%). On the supply side, manufacturing was up 2.2% and mining was considerably down at -8.1%.

Core and WPI inflation print moderates further

Headline WPI inflation declined to 5.96% from 6.84% YoY in February 2013. The better than expected March WPI inflation was because of lower food inflation and further softening in core inflation. Core inflation moderated to 3.5% YoY from 3.8% on weaker demand and lower input costs. However, figure for January 2013 was revised upwards to 7.31% YoY from 6.62%.CPI inflation trended lower to 10.4% from 10.9% in February 2013on account of fall in the food index which ticked lower to 12.3% from 13.5% in February 2013.Core inflation (ex-food and fuel) remained largely unchanged at 8.6%.

HSBC’s India PMI slows down further

HSBC’s India manufacturing PMI declined in April 2013 to 51 (vs. 52 in March 2013) due to slowdown in orders inflows and power outages. HSBC’s India service sector PMI also declined in April 2013 to 50.7 vs. 51.4 in March 2013), led by a slowdown in new business flows.

Market Activity

Yield rallies on lower commodity prices

Domestic bond yields rallied during the month post hardening witnessed in previous month. Softening of global commodity prices including oil resulted in expectation of sharp decline in India’s twin deficits (Fiscal & Current) going forward. Economic data (Inflation & IIP) further improved on account of monetary easing.

Corporate bond spreads contracts further

Credit spreads softened further during the month due to favourable movement in Gilts and positive demand – supply scenario that resulted in buying spree across the corporate curve. Easing in system liquidity also impacted shorter end of the curve positively. Reduction in the withholding tax (tax charged on interest earned by foreign investors on rupee-denominated bonds) for FII’s from 20% to 5% for the period June 2013 – May 2015 augurs positively for the corporate bonds.

Liquidity eases on government spending

Government spending during the month resulted in liquidity moving into the RBI’s comfort zone. Money market yields however softened on back of lower supply and higher investor demand. Recent announcement of Open Market Operations (OMO) by the RBI is likely to ease liquidity further.

Global Economic Scenario

Global economy

Federal Open Market Committee (FOMC) continued its quantitative easing program and on back of recently announced economic data, further stated that it stands ready to increase or reduce the pace of its purchases based on developments in the labour market and inflation. European Central Bank (ECB) reduced the refinance rate by 25 bps to a new low of 0.5% and the marginal lending rate by 50 bps to 1% as expected. Deposit rate was left unchanged at 0% for now.

Going ForwardAs widely expected, the RBI continues to tackle containing risk to economic growth despite higher than comfort level of inflation and the limited space available for monetary policy. We continue to believe that the RBI’s stance is towards supporting growth in FY2013-14, which can get moderated due to higher Current Account Deficit (CAD) and financing pattern of CAD. Space for further monetary policy easing is limited based on assessment of the current situation.We continue to favour maintaining moderate duration in Bond / Flexi Debt Funds, with a combination of corporate bonds and government securities (G-Sec) as liquidity management may lead to some Open Market Operations in the near term. G-sec yields are likely to remain under pressure for the longer tenure given the supply in that segment and limited easing going forward. Short-Term Funds are likely to benefit from a steepening in the corporate bond yield curve as OMO and government spending improves the liquidity scenario in the new fiscal.

Source: Bloomberg, for all data except where mentioned otherwise

Fund Manager Commentary April 2013

5

An Open Ended Diversified Equity SchemeInvestment Objective: Aims to generate long term capital growth from an actively managed portfolio of equity and equity related securities.

Issuer Market Value(` in Lacs)

% to NetAssets

Auto Bajaj Auto 1,504.32 2.75%Tata Motors 1,275.00 2.33%Hero Motocorp 1,184.00 2.16%Auto AncillariesApollo Tyres 1,158.80 2.11%Banks ICICI Bank 4,375.32 7.98%HDFC Bank 3,002.12 5.48%State Bank of India 1,811.44 3.31%Federal Bank 1,369.35 2.50%Bank of Baroda 1,223.16 2.23%CementGrasim Industries 2,344.76 4.28%Construction ProjectsLarsen & Toubro 2,117.08 3.86%Consumer Non DurablesI T C 3,946.20 7.20%Fertilisers Coromandel International 593.00 1.08%Finance HDFC 2,881.84 5.26%LIC Housing Finance 730.95 1.33%Gas GAIL (India) 948.11 1.73%Industrial Capital GoodsBharat Heavy Electricals 578.25 1.06%Minerals/Mining Coal India 957.60 1.75%Non Ferrous Metals Hindustan Zinc 2,025.55 3.70%Oil Oil & Natural Gas Corporation 2,613.60 4.77%Cairn India 1,092.00 1.99%Petroleum Products Reliance Industries 2,758.70 5.03%Bharat Petroleum Corporation 1,242.75 2.27%Pharmaceuticals Dr Reddy’s Laboratories 2,007.92 3.66%Cadila Healthcare 785.25 1.43%Power NTPC 1,101.45 2.01%Software Infosys 2,570.77 4.69%Tata Consultancy Services 1,791.92 3.27%Tech Mahindra 1,239.43 2.26%

HSBC Equity Fund (HEF) April 2013

6

Issuer Market Value(` in Lacs)

% to NetAssets

Telecom - Services Bharti Airtel 1,115.63 2.04%Textile Products Arvind 1,113.25 2.03%Total 97.55%CBLOs 1,662.31 3.03%Other Equity Investments 627.65 1.15%Net Current Assets -947.40 -1.73%Total Net Assets as on 30 April 2013 54,802.06 100.00%

Asset AllocationAuto 7.23%Auto Ancillaries 2.11%Banks 21.50%Cement 4.28%Construction Projects 3.86%Consumer Non Durables 7.20%Fertilisers 1.08%Finance 6.59%Gas 1.73%Industrial Capital Goods 1.06%Minerals/Mining 1.75%Non - Ferrous Metals 3.70%Oil 6.76%Petroleum Products 7.30%Pharmaceuticals 5.10%Power 2.01%Software 10.22%Telecom - Services 2.04%Textile - Products 2.03%Reverse Repos/CBLOs 3.03%Net Current Assets -1.73%Other Equity Investments 1.15%Total Net Assets 100.00%

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC Equity Fund - Dividend28-May-10 1.50 1.50 26.691119-Nov-10 2.00 2.00 29.324422-Feb-13 2.50 2.50 26.1962HSBC Equity Fund - Dividend Direct Plan22-Feb-13 2.50 2.50 26.2505

Date of Allotment 10-Dec-02Benchmark S&P BSE 200NAV (Growth) per unit(as on 30.04.13)

` 103.4724

Fund Manager Tushar PradhanSIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 0.86%R-Squared 0.9627Beta (Slope) 0.9102Sharpe Ratio -0.0229Annualised Expense Ratio from 01 April 2013 onwards 2.65%Portfolio Turnover 0.12

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments. Risk free rate: 7.73% as on April 30, 2013.

HSBC Equity Fund (HEF) April 2013

7

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

An Open Ended Flexi-Cap Equity SchemeInvestment Objective: Seeks long term capital growth through investments across all market capitalisations, including small, mid and large cap stocks. It aims to be predominantly invested in equity & equity related securities. However it could move a significant portion of its assets towards fixed income securities if the fund manager becomes negative on equity markets.

Issuer Market Value(` in Lacs)

% to NetAssets

Auto Tata Motors 600.00 2.83%Eicher Motors 591.68 2.79%Auto Ancillaries Bosch 622.86 2.94%Apollo Tyres 579.60 2.73%Banks ICICI Bank 1,369.03 6.46%HDFC Bank 852.88 4.02%State Bank of India 600.49 2.83%Punjab National Bank 499.14 2.35%Bank of Baroda 489.27 2.31%Cement Shree Cements 607.74 2.87%ChemicalsSupreme Industries 511.61 2.41%Construction ProjectsLarsen & Toubro 684.27 3.23%Consumer Non Durables I T C 892.83 4.21%Finance HDFC 674.69 3.18%LIC Housing Finance 661.51 3.12%Power Finance Corporation 617.67 2.91%CRISIL 402.08 1.90%GasPetronet LNG 523.31 2.47%Industrial Capital GoodsCrompton Greaves 599.30 2.83%Industrial ProductsCarborundum Universal 398.72 1.88%Sintex Industries 361.15 1.70%Minerals/Mining Gujarat Mineral Development Corporation 244.27 1.15%Non - Ferrous Metals Hindalco Industries 389.00 1.83%Hindustan Zinc 235.92 1.11%Oil Oil & Natural Gas Corporation 591.33 2.79%PesticidesUnited Phosphorus 635.18 3.00%Petroleum Products Reliance Industries 713.32 3.36%Pharmaceuticals Divi's Laboratories 537.43 2.54%Dr Reddy’s Laboratories 405.64 1.91%Software Infosys 809.23 3.82%Tech Mahindra 571.95 2.70%Eclerx Services 499.65 2.36%Polaris Software Lab 432.08 2.04%Tata Consultancy Services 413.52 1.95%Telecom - ServicesBharti Airtel 350.63 1.65%Total 94.19%

HSBC India Opportunities Fund (HIOF) April 2013

8

Issuer Market Value(` in Lacs)

% to NetAssets

CBLOs 1,262.52 5.96%Other Equity Investments 521.83 2.46%Net Current Assets -553.21 -2.61%Total Net Assets as on 30 April 2013 21,200.11 100.00%

Asset AllocationAuto 5.62%Auto Ancillaries 5.67%Banks 17.98%Cement 2.87%Chemicals 2.41%Construction Projects 3.23%Consumer Non Durables 4.21%Finance 11.11%Gas 2.47%Industrial Capital Goods 2.83%Industrial Products 3.58%Minerals/Mining 1.15%Non - Ferrous Metals 2.95%Oil 2.79%Pesticides 3.00%Petroleum Products 3.36%Pharmaceuticals 4.45%Software 12.86%Telecom - Services 1.65%Reverse Repos/CBLOs 5.96%Net Current Assets -2.61%Other Equity Investments 2.46%Total Net Assets 100.00%

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC India Opportunities Fund - Dividend11-Dec-09 1.00 1.00 16.901319-Nov-10 1.00 1.00 18.23134-Feb-13 1.50 1.50 17.7319HSBC India Opportunities Fund - Dividend Direct Plan4-Feb-13 1.50 1.50 17.7519

Date of Allotment 24-Feb-04Benchmark S&P BSE 500NAV (Growth) per unit(as on 30.04.13)

` 35.8201

Fund Manager Tushar PradhanSIP AvailableMinimumApplication Amount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 0.80%R-Squared 0.9459Beta (Slope) 0.8551Sharpe Ratio -0.0229Annualised Expense Ratio from 01 April 2013 onwards 2.78%Portfolio Turnover 0.39

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments.Risk free rate: 7.73% as on April 30, 2013.

HSBC India Opportunities Fund (HIOF) April 2013

9

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

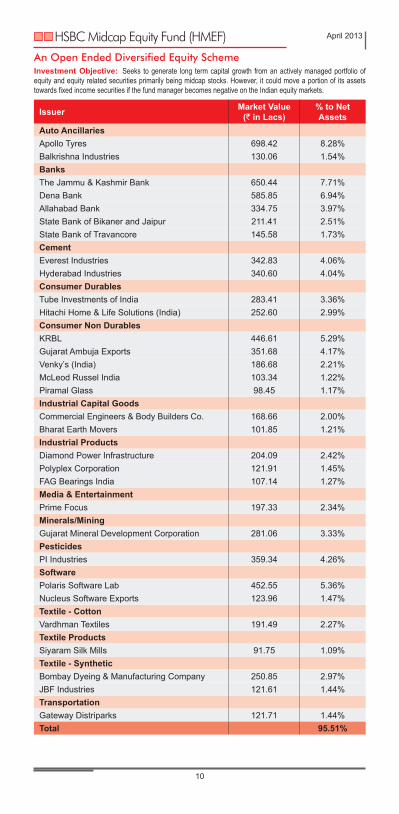

An Open Ended Diversified Equity SchemeInvestment Objective: Seeks to generate long term capital growth from an actively managed portfolio of equity and equity related securities primarily being midcap stocks. However, it could move a portion of its assets towards fixed income securities if the fund manager becomes negative on the Indian equity markets.

Issuer Market Value(` in Lacs)

% to NetAssets

Auto Ancillaries Apollo Tyres 698.42 8.28%Balkrishna Industries 130.06 1.54%Banks The Jammu & Kashmir Bank 650.44 7.71%Dena Bank 585.85 6.94%Allahabad Bank 334.75 3.97%State Bank of Bikaner and Jaipur 211.41 2.51%State Bank of Travancore 145.58 1.73%CementEverest Industries 342.83 4.06%Hyderabad Industries 340.60 4.04%Consumer Durables Tube Investments of India 283.41 3.36%Hitachi Home & Life Solutions (India) 252.60 2.99%Consumer Non DurablesKRBL 446.61 5.29%Gujarat Ambuja Exports 351.68 4.17%Venky’s (India) 186.68 2.21%McLeod Russel India 103.34 1.22%Piramal Glass 98.45 1.17%Industrial Capital GoodsCommercial Engineers & Body Builders Co. 168.66 2.00%Bharat Earth Movers 101.85 1.21%Industrial Products Diamond Power Infrastructure 204.09 2.42%Polyplex Corporation 121.91 1.45%FAG Bearings India 107.14 1.27%Media & EntertainmentPrime Focus 197.33 2.34%Minerals/Mining Gujarat Mineral Development Corporation 281.06 3.33%PesticidesPI Industries 359.34 4.26%Software Polaris Software Lab 452.55 5.36%Nucleus Software Exports 123.96 1.47%Textile - CottonVardhman Textiles 191.49 2.27%Textile ProductsSiyaram Silk Mills 91.75 1.09%Textile - Synthetic Bombay Dyeing & Manufacturing Company 250.85 2.97%JBF Industries 121.61 1.44%Transportation Gateway Distriparks 121.71 1.44%Total 95.51%

HSBC Midcap Equity Fund (HMEF) April 2013

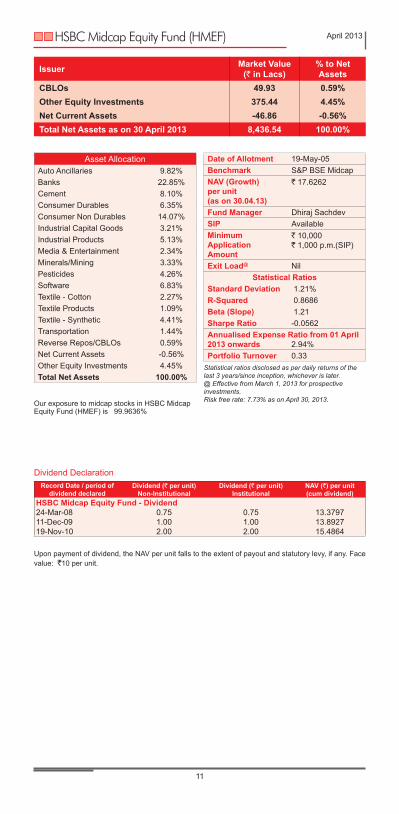

10

Issuer Market Value(` in Lacs)

% to NetAssets

CBLOs 49.93 0.59%Other Equity Investments 375.44 4.45%Net Current Assets -46.86 -0.56%Total Net Assets as on 30 April 2013 8,436.54 100.00%

Asset AllocationAuto Ancillaries 9.82%Banks 22.85%Cement 8.10%Consumer Durables 6.35%Consumer Non Durables 14.07%Industrial Capital Goods 3.21%Industrial Products 5.13%Media & Entertainment 2.34%Minerals/Mining 3.33%Pesticides 4.26%Software 6.83%Textile - Cotton 2.27%Textile Products 1.09%Textile - Synthetic 4.41%Transportation 1.44%Reverse Repos/CBLOs 0.59%Net Current Assets -0.56%Other Equity Investments 4.45%Total Net Assets 100.00%

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC Midcap Equity Fund - Dividend24-Mar-08 0.75 0.75 13.379711-Dec-09 1.00 1.00 13.892719-Nov-10 2.00 2.00 15.4864

Date of Allotment 19-May-05Benchmark S&P BSE MidcapNAV (Growth) per unit(as on 30.04.13)

` 17.6262

Fund Manager Dhiraj SachdevSIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 1.21%R-Squared 0.8686Beta (Slope) 1.21Sharpe Ratio -0.0562Annualised Expense Ratio from 01 April 2013 onwards 2.94%Portfolio Turnover 0.33

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments.Risk free rate: 7.73% as on April 30, 2013.

HSBC Midcap Equity Fund (HMEF) April 2013

11

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

Our exposure to midcap stocks in HSBC Midcap Equity Fund (HMEF) is 99.9636%

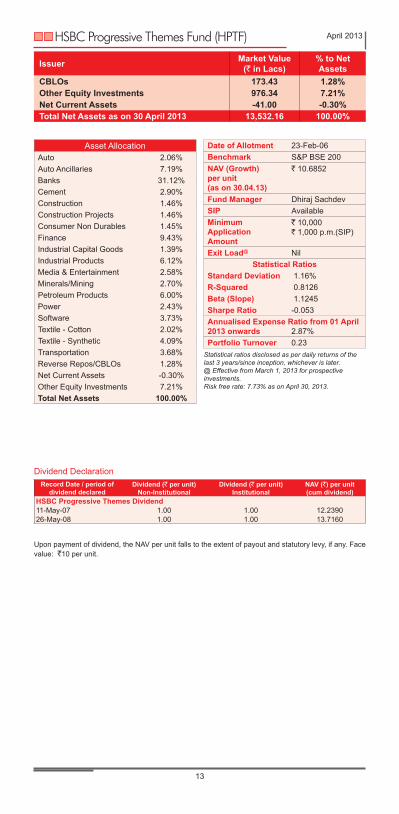

An Open Ended Flexi-Theme Equity SchemeInvestment Objective: Seeks to generate long term capital growth from an actively managed portfolio of equity and equity related securities by investing primarily in sectors, areas and themes that play an important role in, and/or benefit from India’s progress, reform process and economic development.

Issuer Market Value(` in Lacs)

% to NetAssets

Auto Tata Motors DVR 278.29 2.06%Auto Ancillaries Apollo Tyres 972.76 7.19%Banks The Jammu & Kashmir Bank 1,267.31 9.37%Dena Bank 645.39 4.77%ICICI Bank 581.83 4.30%Indian Bank 451.44 3.34%The Karnataka Bank 419.30 3.10%Allahabad Bank 325.72 2.41%Union Bank of India 318.24 2.35%United Bank of India 202.61 1.50%CementEverest Industries 392.80 2.90%ConstructionIRB Infrastructure Developers 197.46 1.46%Construction ProjectsGammon Infrastructure Projects 197.04 1.46%Consumer Non DurablesGujarat Ambuja Exports 196.80 1.45%Finance Rural Electrification Corporation 493.68 3.65%Aditya Birla Nuvo 445.59 3.29%Rane Holdings 337.00 2.49%Industrial Capital GoodsBharat Heavy Electricals 187.93 1.39%Industrial Products FAG Bearings India 425.67 3.15%Diamond Power Infrastructure 248.45 1.84%Polyplex Corporation 154.22 1.14%Media & EntertainmentPrime Focus 349.77 2.58%Minerals/MiningGujarat Mineral Development Corporation 365.08 2.70%Petroleum Products Hindustan Petroleum Corporation 610.93 4.51%Indian Oil Corporation 201.20 1.49%Power Reliance Infrastructure 328.26 2.43%Software Polaris Software Lab 504.27 3.73%Textile - Cotton Vardhman Textiles 272.80 2.02%Textile - Synthetic Bombay Dyeing & Manufacturing Company 409.46 3.03%JBF Industries 144.61 1.07%TransportationGateway Distriparks 497.48 3.68%Total 91.81%

HSBC Progressive Themes Fund (HPTF) April 2013

12

Issuer Market Value(` in Lacs)

% to NetAssets

CBLOs 173.43 1.28%Other Equity Investments 976.34 7.21%Net Current Assets -41.00 -0.30%Total Net Assets as on 30 April 2013 13,532.16 100.00%

Asset AllocationAuto 2.06%Auto Ancillaries 7.19%Banks 31.12%Cement 2.90%Construction 1.46%Construction Projects 1.46%Consumer Non Durables 1.45%Finance 9.43%Industrial Capital Goods 1.39%Industrial Products 6.12%Media & Entertainment 2.58%Minerals/Mining 2.70%Petroleum Products 6.00%Power 2.43%Software 3.73%Textile - Cotton 2.02%Textile - Synthetic 4.09%Transportation 3.68%Reverse Repos/CBLOs 1.28%Net Current Assets -0.30%Other Equity Investments 7.21%Total Net Assets 100.00%

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC Progressive Themes Dividend11-May-07 1.00 1.00 12.239026-May-08 1.00 1.00 13.7160

Date of Allotment 23-Feb-06Benchmark S&P BSE 200NAV (Growth) per unit(as on 30.04.13)

` 10.6852

Fund Manager Dhiraj SachdevSIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 1.16%R-Squared 0.8126Beta (Slope) 1.1245Sharpe Ratio -0.053Annualised Expense Ratio from 01 April 2013 onwards 2.87%Portfolio Turnover 0.23

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments. Risk free rate: 7.73% as on April 30, 2013.

HSBC Progressive Themes Fund (HPTF) April 2013

13

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

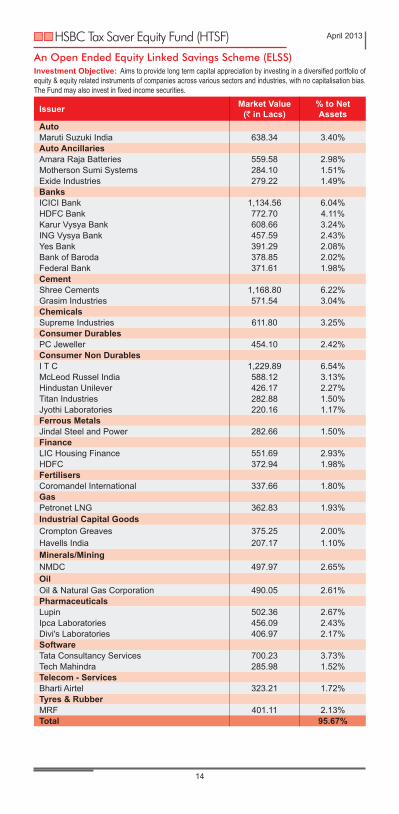

An Open Ended Equity Linked Savings Scheme (ELSS)Investment Objective: Aims to provide long term capital appreciation by investing in a diversified portfolio of equity & equity related instruments of companies across various sectors and industries, with no capitalisation bias. The Fund may also invest in fixed income securities.

Issuer Market Value(` in Lacs)

% to NetAssets

Auto Maruti Suzuki India 638.34 3.40%Auto Ancillaries Amara Raja Batteries 559.58 2.98%Motherson Sumi Systems 284.10 1.51%Exide Industries 279.22 1.49%Banks ICICI Bank 1,134.56 6.04%HDFC Bank 772.70 4.11%Karur Vysya Bank 608.66 3.24%ING Vysya Bank 457.59 2.43%Yes Bank 391.29 2.08%Bank of Baroda 378.85 2.02%Federal Bank 371.61 1.98%Cement Shree Cements 1,168.80 6.22%Grasim Industries 571.54 3.04%ChemicalsSupreme Industries 611.80 3.25%Consumer DurablesPC Jeweller 454.10 2.42%Consumer Non DurablesI T C 1,229.89 6.54%McLeod Russel India 588.12 3.13%Hindustan Unilever 426.17 2.27%Titan Industries 282.88 1.50%Jyothi Laboratories 220.16 1.17%Ferrous Metals Jindal Steel and Power 282.66 1.50%Finance LIC Housing Finance 551.69 2.93%HDFC 372.94 1.98%Fertilisers Coromandel International 337.66 1.80%GasPetronet LNG 362.83 1.93%Industrial Capital GoodsCrompton Greaves 375.25 2.00%Havells India 207.17 1.10%Minerals/MiningNMDC 497.97 2.65%OilOil & Natural Gas Corporation 490.05 2.61%Pharmaceuticals Lupin 502.36 2.67%Ipca Laboratories 456.09 2.43%Divi's Laboratories 406.97 2.17%Software Tata Consultancy Services 700.23 3.73%Tech Mahindra 285.98 1.52%Telecom - Services Bharti Airtel 323.21 1.72%Tyres & RubberMRF 401.11 2.13%Total 95.67%

HSBC Tax Saver Equity Fund (HTSF) April 2013

14

Date of Allotment 05-Jan-07Benchmark S&P BSE 200NAV (Growth) per unit(as on 30.04.13)

` 16.2609

Fund Manager Aditya KhemaniSIP AvailableMinimumApplicationAmount

` 500(Lumpsum & SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 0.82%R-Squared 0.9259Beta (Slope) 0.8511Sharpe Ratio -0.0138Annualised Expense Ratio from 01 April 2013 onwards 2.82%Portfolio Turnover 0.76

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments. Risk free rate: 7.73% as on April 30, 2013.

Issuer Market Value(` in Lacs)

% to NetAssets

CBLOs 653.03 3.47%Other Equity Investments 303.50 1.61%Net Current Assets -143.53 -0.76%Total Net Assets as on 30 April 2013 18,797.15 100.00%

Asset AllocationAuto 3.40%Auto Ancillaries 5.97%Banks 21.89%Cement 9.26%Chemicals 3.25%Consumer Durables 2.42%Consumer Non Durables 14.62%Ferrous Metals 1.50%Finance 4.92%Fertilisers 1.80%Gas 1.93%Industrial Capital Goods 3.10%Minerals/Mining 2.65%Oil 2.61%Pharmaceuticals 7.26%Software 5.25%Telecom - Services 1.72%Tyres & Rubber 2.13%Reverse Repos/CBLOs 3.47%Net Current Assets -0.76%Other Equity Investments 1.61%Total Net Assets 100.00%

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC Tax Saver Equity Dividend19-Feb-10 1.00 1.00 12.8713

HSBC Tax Saver Equity Fund (HTSF) April 2013

15

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

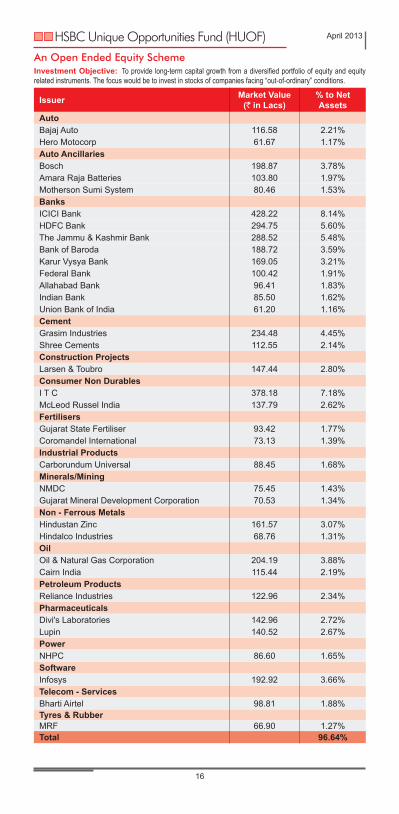

An Open Ended Equity SchemeInvestment Objective: To provide long-term capital growth from a diversified portfolio of equity and equity related instruments. The focus would be to invest in stocks of companies facing “out-of-ordinary” conditions.

Issuer Market Value(` in Lacs)

% to NetAssets

Auto Bajaj Auto 116.58 2.21%Hero Motocorp 61.67 1.17%Auto Ancillaries Bosch 198.87 3.78%Amara Raja Batteries 103.80 1.97%Motherson Sumi System 80.46 1.53%Banks ICICI Bank 428.22 8.14%HDFC Bank 294.75 5.60%The Jammu & Kashmir Bank 288.52 5.48%Bank of Baroda 188.72 3.59%Karur Vysya Bank 169.05 3.21%Federal Bank 100.42 1.91%Allahabad Bank 96.41 1.83%Indian Bank 85.50 1.62%Union Bank of India 61.20 1.16%CementGrasim Industries 234.48 4.45%Shree Cements 112.55 2.14%Construction ProjectsLarsen & Toubro 147.44 2.80%Consumer Non DurablesI T C 378.18 7.18%McLeod Russel India 137.79 2.62%FertilisersGujarat State Fertiliser 93.42 1.77%Coromandel International 73.13 1.39%Industrial Products Carborundum Universal 88.45 1.68%Minerals/MiningNMDC 75.45 1.43%Gujarat Mineral Development Corporation 70.53 1.34%Non - Ferrous Metals Hindustan Zinc 161.57 3.07%Hindalco Industries 68.76 1.31%Oil Oil & Natural Gas Corporation 204.19 3.88%Cairn India 115.44 2.19%Petroleum Products Reliance Industries 122.96 2.34%Pharmaceuticals Divi's Laboratories 142.96 2.72%Lupin 140.52 2.67%PowerNHPC 86.60 1.65%Software Infosys 192.92 3.66%Telecom - Services Bharti Airtel 98.81 1.88%Tyres & RubberMRF 66.90 1.27%Total 96.64%

HSBC Unique Opportunities Fund (HUOF) April 2013

16

Issuer Market Value(` in Lacs)

% to NetAssets

CBLOs 121.53 2.31%Other Equity Investments 26.60 0.51%Net Current Assets 28.52 0.54%Total Net Assets as on 30 April 2013 5,263.85 100.00%

Asset AllocationAuto 3.39%Auto Ancillaries 7.28%Banks 32.54%Cement 6.59%Construction Projects 2.80%Consumer Non Durables 9.80%Fertilisers 3.16%Industrial Products 1.68%Minerals/Mining 2.77%Non - Ferrous Metals 4.38%Oil 6.07%Petroleum Products 2.34%Pharmaceuticals 5.39%Power 1.65%Software 3.66%Telecom - Services 1.88%Tyres & Rubber 1.27%Reverse Repos/CBLOs 2.31%Net Current Assets 0.54%Other Equity Investments 0.51%Total Net Assets 100.00%

Date of Allotment 21-Mar-07Benchmark S&P BSE 200NAV (Growth) per unit(as on 30.04.13)

` 11.0465

Fund Manager Gaurav Mehrotra & Amaresh Mishra

SIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 0.88%R-Squared,m 0.9312Beta (Slope) 0.909Sharpe Ratio -0.028Annualised Expense Ratio from 01 April 2013 onwards 2.93%Portfolio Turnover 0.26

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments. Risk free rate: 7.73% as on April 30, 2013.

HSBC Unique Opportunities Fund (HUOF) April 2013

17

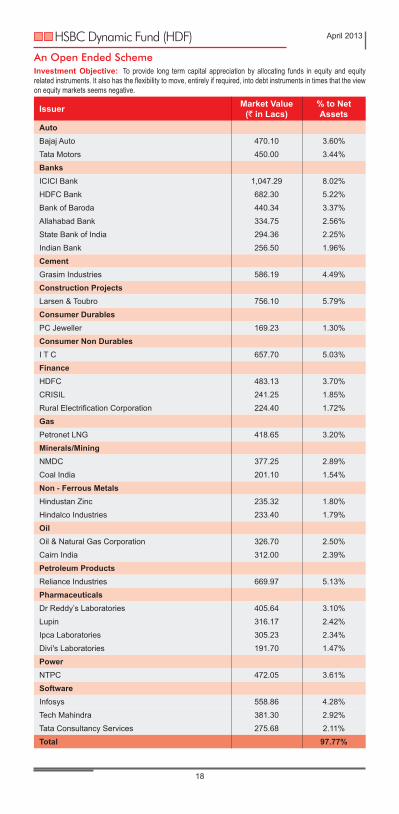

An Open Ended SchemeInvestment Objective: To provide long term capital appreciation by allocating funds in equity and equity related instruments. It also has the flexibility to move, entirely if required, into debt instruments in times that the view on equity markets seems negative.

Issuer Market Value(` in Lacs)

% to NetAssets

AutoBajaj Auto 470.10 3.60%

Tata Motors 450.00 3.44%

Banks ICICI Bank 1,047.29 8.02%

HDFC Bank 682.30 5.22%

Bank of Baroda 440.34 3.37%

Allahabad Bank 334.75 2.56%

State Bank of India 294.36 2.25%

Indian Bank 256.50 1.96%

CementGrasim Industries 586.19 4.49%

Construction ProjectsLarsen & Toubro 756.10 5.79%

Consumer DurablesPC Jeweller 169.23 1.30%

Consumer Non DurablesI T C 657.70 5.03%

Finance HDFC 483.13 3.70%

CRISIL 241.25 1.85%

Rural Electrification Corporation 224.40 1.72%

GasPetronet LNG 418.65 3.20%

Minerals/Mining NMDC 377.25 2.89%

Coal India 201.10 1.54%

Non - Ferrous Metals Hindustan Zinc 235.32 1.80%

Hindalco Industries 233.40 1.79%

Oil Oil & Natural Gas Corporation 326.70 2.50%

Cairn India 312.00 2.39%

Petroleum Products Reliance Industries 669.97 5.13%

Pharmaceuticals Dr Reddy’s Laboratories 405.64 3.10%

Lupin 316.17 2.42%

Ipca Laboratories 305.23 2.34%

Divi's Laboratories 191.70 1.47%

PowerNTPC 472.05 3.61%

Software Infosys 558.86 4.28%

Tech Mahindra 381.30 2.92%

Tata Consultancy Services 275.68 2.11%

Total 97.77%

HSBC Dynamic Fund (HDF) April 2013

18

Issuer Market Value(` in Lacs)

% to NetAssets

CBLOs 789.19 6.04%Net Current Assets -497.42 -3.81%Total Net Assets as on 30 April 2013 13,066.42 100.00%

Asset AllocationAuto 7.04%Banks 23.38%Cement 4.49%Construction Projects 5.79%Consumer Durables 1.30%Consumer Non Durables 5.03%Finance 7.26%Gas 3.20%Minerals/Mining 4.43%Non - Ferrous Metals 3.59%Oil 4.89%Petroleum Products 5.13%Pharmaceuticals 9.33%Power 3.61%Software 9.31%Reverse Repos/CBLOs 6.04%Net Current Assets -3.81%Total Net Assets 100.00%

Date of Allotment 24-Sep-07Benchmark S&P BSE 200NAV (Growth) per unit(as on 30.04.13)

` 10.0821

Fund Manager Tushar Pradhan(for Equity portion)Sanjay Shah(for Debt portion)

SIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 0.84%R-Squared 0.9497Beta (Slope) 0.8783Sharpe Ratio -0.031Annualised Expense Ratio from 01 April 2013 onwards 2.85%Portfolio Turnover 0.29

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments. Risk free rate: 7.73% as on April 30, 2013.

HSBC Dynamic Fund (HDF) April 2013

19

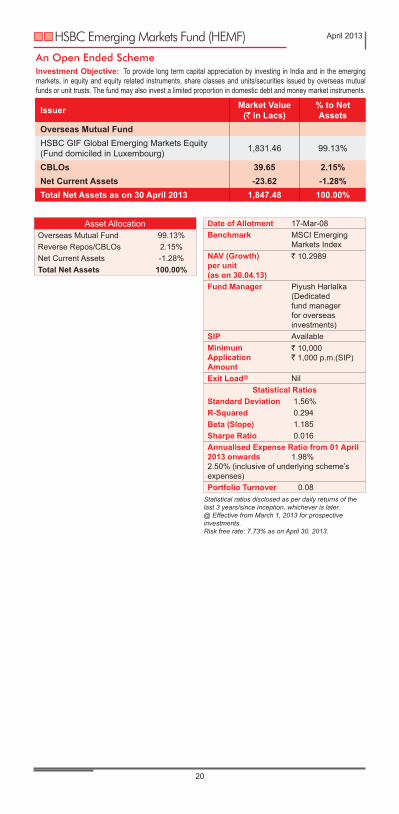

Date of Allotment 17-Mar-08Benchmark MSCI Emerging

Markets IndexNAV (Growth) per unit(as on 30.04.13)

` 10.2989

Fund Manager Piyush Harlalka (Dedicated fund manager for overseas investments)

SIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 1.56%R-Squared 0.294Beta (Slope) 1.185Sharpe Ratio 0.016Annualised Expense Ratio from 01 April 2013 onwards 1.98% 2.50% (inclusive of underlying scheme’s expenses)Portfolio Turnover 0.08

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments. Risk free rate: 7.73% as on April 30, 2013.

Asset AllocationOverseas Mutual Fund 99.13%Reverse Repos/CBLOs 2.15%Net Current Assets -1.28%Total Net Assets 100.00%

Issuer Market Value(` in Lacs)

% to NetAssets

Overseas Mutual FundHSBC GIF Global Emerging Markets Equity (Fund domiciled in Luxembourg) 1,831.46 99.13%

CBLOs 39.65 2.15%Net Current Assets -23.62 -1.28%Total Net Assets as on 30 April 2013 1,847.48 100.00%

An Open Ended SchemeInvestment Objective: To provide long term capital appreciation by investing in India and in the emerging markets, in equity and equity related instruments, share classes and units/securities issued by overseas mutual funds or unit trusts. The fund may also invest a limited proportion in domestic debt and money market instruments.

HSBC Emerging Markets Fund (HEMF) April 2013

20

An Open Ended Equity SchemeInvestment Objective: To provide long term capital appreciation primarily from a diversified portfolio of equity and equity related instruments of small cap companies.

Issuer Market Value(` in Lacs)

% to NetAssets

Auto Ancillaries Pricol 89.86 6.18%Majestic Auto 31.30 2.15%Balkrishna Industries 18.39 1.27%Banks State Bank of Travancore 77.74 5.35%State Bank of Bikaner and Jaipur 69.03 4.75%The Karnataka Bank 46.42 3.19%Cement Orient Cement 112.47 7.74%Orient Paper & Industries 14.99 1.03%Chemicals India Glycols 57.55 3.96%Consumer Durables IFB Industries 66.72 4.59%Hitachi Home & Life Solutions (India) 45.53 3.13%Tube Investments of India 23.20 1.60%Consumer Non DurablesGujarat Ambuja Exports 85.46 5.88%KRBL 61.92 4.26%Globus Spirits 61.50 4.23%Greenply Industries 38.65 2.66%Lakshmi Energy and Foods 31.05 2.14%FinanceRane Holdings 99.58 6.85%Industrial Capital GoodsSanghvi Movers 39.20 2.70%Indo Tech Transformers 32.65 2.25%TIL 28.67 1.97%Industrial Products Ador Welding 49.30 3.39%PesticidesPI Industries 22.87 1.57%Software Nucleus Software Exports 128.54 8.85%Textile - Cotton RSWM 71.26 4.90%SRF 25.54 1.76%Total 98.37%

HSBC Small Cap Fund (HSCF) April 2013

21

Issuer Market Value(` in Lacs)

% to NetAssets

CBLOs 72.85 5.01%Other Equity Investments 23.09 1.59%Net Current Assets -72.20 -4.97%Total Net Assets as on 30 April 2013 1,453.11 100.00%

Asset AllocationAuto Ancillaries 9.60%Banks 13.30%Cement 8.77%Chemicals 3.96%Consumer Durables 9.32%Consumer Non Durables 19.17%Finance 6.85%Industrial Capital Goods 6.92%Industrial Products 3.39%Pesticides 1.57%Software 8.85%Textile - Cotton 6.66%Reverse Repos/CBLOs 5.01%Net Current Assets -4.97%Other Equity Investments 1.59%Total Net Assets 100.00%

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC Small Cap Fund - Dividend19-Nov-10 1.00 1.00 14.3053

Date of Allotment 24-Mar-08

Benchmark S&P BSE Small Cap Index

NAV (Growth) per unit(as on 30.04.13)

` 9.1804

Fund Manager Dhiraj SachdevSIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 1.08%R-Squared 0.8454Beta (Slope) 0.9895Sharpe Ratio -0.0881Annualised Expense Ratio from 01 April 2013 onwards 2.99%Portfolio Turnover 0.11

Statistical ratios disclosed as per returns of the last 3 years/since inception, whichever is later.@ Effective from March 1, 2013 for prospective investments.Risk free rate: 7.73% as on April 30, 2013.

HSBC Small Cap Fund (HSCF) April 2013

22

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

Our exposure to small cap stocks in HSBC Small Cap Fund (HSCF) is 92.2155%

Date of Allotment 06-May-11Benchmark MSCI Brazil

10/40 IndexNAV (Growth) per unit(as on 30.04.13)

` 9.633

Fund Manager Piyush Harlalka (Dedicated fund manager for overseas investments)

SIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilStatistical Ratios

Standard Deviation 1.20%R-Squared 0.312Beta (Slope) 0.482Sharpe Ratio -0.033Annualised Expense Ratio from 01 April 2013 onwards* 1.98% 2.50% (inclusive of underlying scheme’s expenses)Portfolio Turnover 0.05

Statistical ratios disclosed as per daily returns of the last 3 years/since inception, whichever is later. @ Effective from March 1, 2013 for prospective investments. Risk free rate: 7.73% as on April 30, 2013.* Accrual & Average Net Assets are for the period 05-May-11 to 31-Mar-12.

Asset AllocationOverseas Mutual Fund 98.51%Reverse Repos/CBLOs 2.89%Net Current Assets -1.40%Total Net Assets 100.00%

Issuer Market Value(` in Lacs)

% to NetAssets

Overseas Mutual FundHSBC GIF Brazil Equity Fund (Fund domiciled in Luxembourg) 17,486.75 98.51%

CBLOs 487.35 2.89%

Net Current Assets -256.50 -1.40%

Total Net Assets as on 30 April 2013 17,717.60 100.00%

An Open-Ended Fund of Funds SchemeInvestment Objective: The primary investment objective of the Scheme is to provide long term capital appreciation by investing predominantly in units/shares of HSBC Global Investment Funds (HGIF) Brazil Equity Fund. The Scheme may, at the discretion of the Investment Manager, also invest in the units of other similar overseas mutual fund schemes, which may constitute a significant part of its corpus. The Scheme may also invest a certain proportion of its corpus in money market instruments and/or units of liquid mutual fund schemes, in order to meet liquidity requirements from time to time.

HSBC Brazil Fund (HBF) April 2013

23

Name of Scheme Fund Manager

HSBC Equity Fund Tushar Pradhan (from 29 September 2011)

HSBC India Opportunities Fund Tushar Pradhan (from 29 September 2011)

HSBC Midcap Equity Fund Dhiraj Sachdev (from 01 December 2009)

HSBC Progressive Themes Fund Dhiraj Sachdev (from 01 December 2009)

HSBC Tax Saver Equity Fund Aditya Khemani (from 24 February 2009)

HSBC Unique Opportunities Fund Gaurav Mehrotra and Amaresh Mishra (from 02 July 2012)

HSBC Dynamic Fund For Equity portion: Tushar Pradhan (from 29 September 2011) & For Debt portion: Sanjay Shah (from 14 August 2009)

HSBC Emerging Markets Fund Piyush Harlalka (from 02 July 2012)

HSBC Small Cap Fund Dhiraj Sachdev (from 01 December 2009)

HSBC Brazil Fund Piyush Harlalka (from 02 July 2012)

Fund Manager’s ExperienceTushar Pradhan Chief Investment Officer MBA (USA), B. Com.

Experience: Over 17 years of experience in Fund Management

l HSBC Asset Management (India) Private Ltd Chief Investment Officer since June 2009 onwards l AIG Global Asset Management Company (India) Private Ltd Chief Investment Officer – Equities from December 2006 to June 2009 l HDFC Asset Management Company Private Ltd Senior Fund Manager from July 2000 to Dec. 2006 l HDFC Ltd Manager – Treasury from April 1995 to June 2000

Dhiraj Sachdev B.Com., ACA, Grad CWA, Diploma in Foreign Trade Management (DFTM)

Experience:Over 16 years experience in Equity Research and Fund Management. This involved analysing various sectors and companies and presenting investment ideas to fund man-agers in India and abroad.

l HSBC Asset Management (India) Private Ltd Senior Fund Manager from December 2009 to present l HSBC Asset Management (India) Private Ltd Head of Equity-Portfolio Management Services from October 2005 to November 2009 l ASK Raymond James Securities India Private Ltd Portfolio Manager from October 2003 to September 2005 l HDFC Bank Ltd Senior Manager Equities from November 1999 to September 2003 l DSQ Software Ltd Business Analyst from June 1999 to November 1999 l Probity Research & Services Ltd (India Infoline Ltd) Research Analyst from November 1998 to May 1999 Ford Brothers Capital Services (P) Ltd Manager Research from July 1996 to Sept 1998

Fund Managers - Equity April 2013

24

l

Gaurav MehrotraPost Graduate Diploma in Business Management, Bachelor of Engineering

Experience: Over 6 years experience in research. HSBC Asset Management (India) Private Ltd Associate Vice president from September 2007 to present JPMorgan Services India Private Ltd Equity Research from August 2005 to September 2007 Tata Consultancy Services Ltd Business Analyst from June 2004 to July 2005

Aditya KhemaniB.Com. (Hons.), Post Graduate Diploma in Business Management

Experience: Over 7 years experience in research. HSBC Asset Management (India) Private Ltd Assistant Fund Manager, Equities from February 2009 to present Associate Vice President - Investment Management from October 2007 to February 2009 SBI Funds Management India Private Ltd Senior Manager - Equity Research from March 2007 to September 2007 Prudential ICICI Asset Management Company India Private Ltd Assistant Manager - Equity Research from December 2005 to February 2007 Morgan Stanley Advantage Services India Private Ltd Research Associate from May 2005 to November 2005

Amaresh Mishra Post Graduate Diploma in Business Manager Management Bachelor of Engineering (Chemical)

Experience: Over 7 years of experience in Equities & Sales l HSBC Asset Management (India) Private Ltd Assistant Fund Manager, from April 2012 till date l HSBC Asset Management (India) Private Ltd Associate Vice President - Investment Management from April 2008 to March 2012 l HSBC Asset Management (India) Private Ltd Associate Vice President - Equities from October 2007 to March 2008 l HSBC Asset Management (India) Private Ltd Associate Vice President - Sales and Distribution from March 2005 to September 2007 l Centre for Science and Environment Trainee Researcher from July 2001 to July 2002

Piyush Harlalka M.B.A, (Finance), C.A., C.S.

Experience:Over 6 years of experience in Fund Management & Research l HSBC Asset Management (India) Private Ltd Vice President – Fixed Income from April 2012 till date l HSBC Asset Management (India) Private Ltd Associate Vice President-Fixed Income from October 2010 till March 2012 l HSBC Asset Management (India) Private Ltd Associate Vice President - Investment Management, PMS, from April 2008 to October 2010 l HSBC Asset Management (India) Private Ltd Research Analyst from July 2007 to March 2008 l Batlivala & Karanai Securities Pvt. Ltd., Research Analyst from April 2006 to June 2007

Fund Managers - Equity April 2013

25

l

l

l

l

l

l

l

Funds Managed by Tushar Pradhan.

Comparative Performance of Equity Schemes April 2013

HSBC Equity Fund Date of Inception : 10 Dec 02Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Equity Fund - Growth 4.20% -8.90% 9.67% 24.76%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 17.41%S&P BSE 200 (Scheme Benchmark) 5.41% -9.55% 7.27% 18.68%`10,000, if invested in HSBC Equity Fund - Growth, would have become `10,420 `9,110 `10,967 `98,173

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `52,409

`10,000, if invested in S&P BSE 200 , would have become `10,541 `9,045 `10,727 `58,573

HSBC India Opportunities Fund Date of Inception : 24 Feb 04Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC India Opportunities Fund - Growth 0.21% -3.60% 11.00% 14.45%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 13.06%S&P BSE 500 (Scheme Benchmark) 4.14% -9.47% 6.55% 13.22%`10,000, if invested in HSBC India Opportunities Fund - Growth, would have become `10,021 `9,640 `11,100 `34,233

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `30,608

`10,000, if invested in S&P BSE 500 , would have become `10,414 `9,053 `10,655 `31,023

26

Data for the period April to March has been considered in all cases, except for ‘Since Inception’ returns. ‘Since Inception’ (%) returns are compounded annualised, other % returns are absolute. ‘Since inception’ returns are calculated on `10 invested at inception. Standard benchmark is prescribed by SEBI for long-term equity schemes and is used for comparison purposes. Returns on `10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be minor differences between point-to-point returns vis-a-vis returns indicated above.

Past performance may or may not be sustained in the future. Refer note below.

Past performance may or may not be sustained in the future. Refer note below.

Past performance may or may not be sustained in the future. Refer note below.

HSBC Dynamic Fund Date of Inception : 24 Sep 07Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Dynamic Fund - Growth 1.59% -8.24% 8.77% -0.65%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 2.24%S&P BSE 200 (Scheme Benchmark) 5.41% -9.55% 7.27% 1.55%`10,000, if invested in HSBC Dynamic Fund - Growth, would have become `10,159 `9,176 `10,877 `9,648

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `11,303

`10,000, if invested in S&P BSE 200 , would have become `10,541 `9,045 `10,727 `10,889

Comparative Performance of Equity Schemes April 2013

27

Data for the period April to March has been considered in all cases, except for ‘Since Inception’ returns. ‘Since Inception’ (%) returns are compounded annualised, other % returns are absolute. ‘Since inception’ returns are calculated on `10 invested at inception. Standard benchmark is prescribed by SEBI for long-term equity schemes and is used for comparison purposes. Returns on `10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be minor differences between point-to-point returns vis-a-vis returns indicated above.

HSBC Brazil Fund Date Of Inception : 06 May 11Scheme Name & Benchmarks Apr 12 - Mar 13 Since InceptionHSBC Brazil Fund - Growth -2.50% -1.68%MSCI Brazil 10/40 Index -14.53% -12.43%CNX Nifty Index (Standard Benchmark) 6.93% 0.22%`10,000, if invested in HBF, would have become `9,750 `9,681

`10,000, if invested in MSCI Brazil 10/40 Index, would have become `8,547 `7,772

`10,000, if invested in CNX Nifty Index , would have become `10,693 `10,042

Past performance may or may not be sustained in the future. Refer note below.

HSBC Emerging Markets Fund Date of Inception : 17 Mar 08Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Emerging Markets Fund - Growth 4.55% -6.74% 11.30% 0.70%MSCI Emerging Market Index 1.77% -7.26% 9.33% 1.25%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 4.32%`10,000, if invested in HMEF, would have become `10,455 `9,326 `11,130 `10,360

`10,000, if invested in MSCI Emerging Market Index, would have become `10,177 `9,274 `10,933 `10,646

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `12,380

Past performance may or may not be sustained in the future. Refer note below.

Funds Managed by - Piyush Harlalka.

HSBC Unique Opportunities Fund Date of Inception : 21 Mar 07Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Unique Opportunities Fund - Growth 4.82% -9.79% 8.92% 0.79%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 6.71%S&P BSE 200 (Scheme Benchmark) 5.41% -9.55% 7.27% 6.52%`10,000, if invested in HSBC Unique Opportunities Fund - Growth, would have become

`10,482 `9,021 `10,892 `10,486

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `14,808

`10,000, if invested in S&P BSE 200 , would have become `10,541 `9,045 `10,727 `14,648

Past performance may or may not be sustained in the future. Refer note below.

Fund Managed by Gaurav Mehrotra and Amaresh Mishra.

HSBC Tax Saver Equity Fund Date of Inception : 05 Jan 07Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Tax Saver Equity Fund - Growth 11.90% -4.42% 4.41% 7.00%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 5.53%S&P BSE 200 (Scheme Benchmark) 5.41% -9.55% 7.27% 4.99%`10,000, if invested in HSBC Tax Saver Equity Fund - Growth, would have become `11,190 `9,558 `10,441 `15,263

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `13,995

`10,000, if invested in S&P BSE 200 , would have become `10,541 `9,045 `10,727 `13,556

Past performance may or may not be sustained in the future. Refer note below.

Fund Managed by - Aditya Khemani.

Comparative Performance of Equity Schemes April 2013

28

Data for the period April to March has been considered in all cases, except for ‘Since Inception’ returns. ‘Since Inception’ (%) returns are compounded annualised, other % returns are absolute. ‘Since inception’ returns are calculated on `10 invested at inception. Standard benchmark is prescribed by SEBI for long-term equity schemes and is used for comparison purposes. Returns on `10,000 are point-to-point returns for the specific time period, invested at the start of the period. The returns provided above have been rounded off and hence there may be minor differences between point-to-point returns vis-a-vis returns indicated above.

HSBC Small Cap Fund Date of Inception : 24 Mar 08Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Small Cap Fund - Growth -6.02% -18.39% 0.04% -2.47%S&P BSE Small Cap (Standard Benchmark) 6.93% -9.13% 10.27% 3.85%CNX Nifty (Scheme Benchmark) -14.05% -20.74% -6.06% -3.13%`10,000, if invested in HSCF, would have become `9,398 `8,161 `10,004 `8,819

`10,000, if invested in S&P BSE Smallcap, would have become `10,693 `9,087 `11,027 `12,093

`10,000, if invested in CNX Nifty, would have become `8,595 `7,926 `9,394 `8,522

Past performance may or may not be sustained in the future. Refer note below.

HSBC Progressive Themes Fund Date of Inception : 23 Feb 06Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Progressive Themes Fund - Growth -10.58% -4.28% -11.23% 0.30%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 8.79%S&P BSE 200 (Scheme Benchmark) 5.41% -9.55% 7.27% 8.29%`10,000, if invested in HSBC Progressive Themes Fund - Growth, would have become `8,942 `9,572 `8,877 `10,215

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `18,206

`10,000, if invested in S&P BSE 200 , would have become `10,541 `9,045 `10,727 `17,624

Past performance may or may not be sustained in the future. Refer note below.

Funds Managed by - Dhiraj Sachdev.

HSBC Midcap Equity Fund Date of Inception : 19 May 05Scheme Name & Benchmarks Apr 12 -

Mar 13Apr 11 - Mar 12

Apr 10 - Mar 11

Since Inception

HSBC Midcap Equity Fund - Growth -8.82% -8.51% -10.38% 7.17%CNX Nifty Index (Standard Benchmark) 6.93% -9.13% 10.27% 13.96%S&P BSE MID CAP (Scheme Benchmark) -4.30% -9.14% 0.11% 8.43%`10,000, if invested in HSBC Midcap Equity Fund - Growth, would have become `9,118 `9,149 `8,962 `17,263

`10,000, if invested in CNX Nifty Index , would have become `10,693 `9,087 `11,027 `28,002

`10,000, if invested in S&P BSE MID CAP , would have become `9,570 `9,086 `10,011 `18,919

Past performance may or may not be sustained in the future. Refer note below.

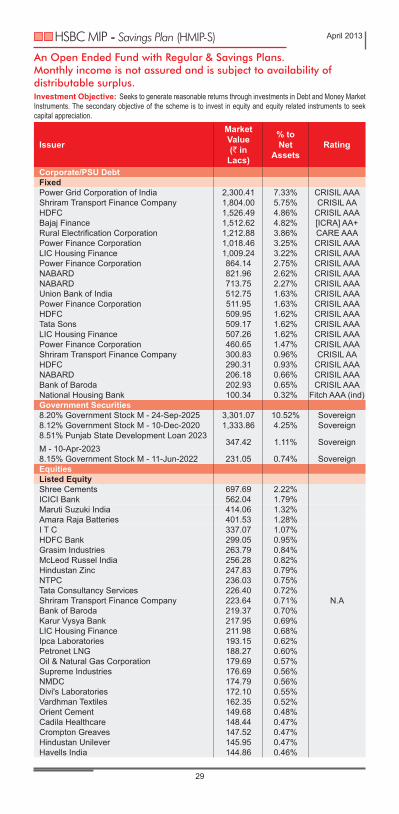

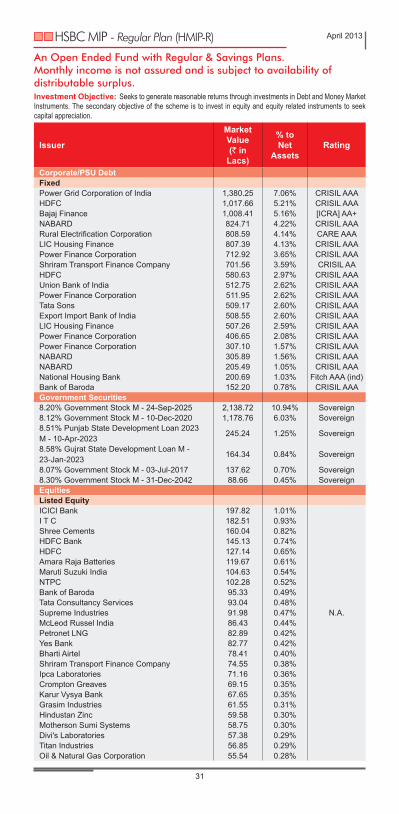

An Open Ended Fund with Regular & Savings Plans.Monthly income is not assured and is subject to availability of distributable surplus.Investment Objective: Seeks to generate reasonable returns through investments in Debt and Money Market Instruments. The secondary objective of the scheme is to invest in equity and equity related instruments to seek capital appreciation.

Issuer

MarketValue(` in

Lacs)

% toNet

AssetsRating

Corporate/PSU DebtFixedPower Grid Corporation of India 2,300.41 7.33% CRISIL AAAShriram Transport Finance Company 1,804.00 5.75% CRISIL AAHDFC 1,526.49 4.86% CRISIL AAABajaj Finance 1,512.62 4.82% [ICRA] AA+Rural Electrification Corporation 1,212.88 3.86% CARE AAAPower Finance Corporation 1,018.46 3.25% CRISIL AAALIC Housing Finance 1,009.24 3.22% CRISIL AAAPower Finance Corporation 864.14 2.75% CRISIL AAANABARD 821.96 2.62% CRISIL AAANABARD 713.75 2.27% CRISIL AAAUnion Bank of India 512.75 1.63% CRISIL AAAPower Finance Corporation 511.95 1.63% CRISIL AAAHDFC 509.95 1.62% CRISIL AAATata Sons 509.17 1.62% CRISIL AAALIC Housing Finance 507.26 1.62% CRISIL AAAPower Finance Corporation 460.65 1.47% CRISIL AAAShriram Transport Finance Company 300.83 0.96% CRISIL AAHDFC 290.31 0.93% CRISIL AAANABARD 206.18 0.66% CRISIL AAABank of Baroda 202.93 0.65% CRISIL AAANational Housing Bank 100.34 0.32% Fitch AAA (ind)Government Securities8.20% Government Stock M - 24-Sep-2025 3,301.07 10.52% Sovereign8.12% Government Stock M - 10-Dec-2020 1,333.86 4.25% Sovereign8.51% Punjab State Development Loan 2023 M - 10-Apr-2023

347.42 1.11% Sovereign

8.15% Government Stock M - 11-Jun-2022 231.05 0.74% SovereignEquitiesListed EquityShree Cements 697.69 2.22%ICICI Bank 562.04 1.79%Maruti Suzuki India 414.06 1.32%Amara Raja Batteries 401.53 1.28%I T C 337.07 1.07%HDFC Bank 299.05 0.95%Grasim Industries 263.79 0.84%McLeod Russel India 256.28 0.82%Hindustan Zinc 247.83 0.79%NTPC 236.03 0.75%Tata Consultancy Services 226.40 0.72%Shriram Transport Finance Company 223.64 0.71% N.ABank of Baroda 219.37 0.70%Karur Vysya Bank 217.95 0.69%LIC Housing Finance 211.98 0.68%Ipca Laboratories 193.15 0.62%Petronet LNG 188.27 0.60%Oil & Natural Gas Corporation 179.69 0.57%Supreme Industries 176.69 0.56%NMDC 174.79 0.56%Divi's Laboratories 172.10 0.55%Vardhman Textiles 162.35 0.52%Orient Cement 149.68 0.48%Cadila Healthcare 148.44 0.47%Crompton Greaves 147.52 0.47%Hindustan Unilever 145.95 0.47%Havells India 144.86 0.46%

HSBC MIP - Savings Plan (HMIP-S) April 2013

29

Date of Allotment 24-Feb-04Benchmark CRISIL MIP

Blended IndexNAV (Growth) per unit(as on 30.04.13)

` 22.987

Average Maturity of Portfolio

67.00 months

Modified Durationof Portfolio

45.72 months

Fund Manager Aditya Khemani(for Equity portion)Sanjay Shah &Ruchir Parekh(for Debt portion)

SIP AvailableMinimum Application AmountGrowth `10,000Quarterly Dividend `10,000Monthly Dividend `25,000SIP `1,000 p.m.Exit Load@ NilAnnualised Expense Ratio from 01 April 2013 onwards 2.46%

@ Effective from March 1, 2013 for prospective investments.

Asset AllocationCorporate/ PSU Debt 53.84%Government Securities 16.61%Cash Equivalents 0.47%Net Current Assets 3.78%Other Equity Investments 25.30%Total Net Assets 100.00%

Issuer

MarketValue(` in

Lacs)

% toNet

AssetsRating

Bharti Airtel 142.80 0.46%Titan Industries 140.76 0.45%Coromandel International 136.26 0.43%Tech Mahindra 133.46 0.43%Motherson Sumi Systems 122.10 0.39%Punjab National Bank 122.10 0.39% N.AJindal Steel and Power 101.42 0.32%PC Jeweller 97.00 0.31%Sanghvi Movers 96.60 0.31%Hindustan Dorr-Oliver 28.01 0.09%Orient Paper & Industries 19.95 0.06%Total 95.75%Cash EquivalentsCBLOs 147.31 0.47%Net Current Assets 1,187.72 3.78%Total Net Assets as on 30 April 2013 31,383.36 100.00%

Rating ProfileAAA 42.31%AA+/ AA-/ AA 11.53%Sovereign 16.61%Reverse Repo/CBLOs 0.47%Net Current Assets 3.78%Other Equity Investments 25.30%Total Net Assets 100.00%

HSBC MIP - Savings Plan (HMIP-S) April 2013

30

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC MIP - Savings Plan - Monthly Dividend22-Feb-13 0.05285 0.04530 12.331628-Mar-13 0.05285 0.04530 12.179626-Apr-13 0.05256 0.04478 12.3492HSBC MIP - Savings Plan - Monthly Dividend - Direct Plan22-Feb-13 0.05285 0.04530 12.353028-Mar-13 0.05285 0.04530 12.210226-Apr-13 0.05256 0.04478 12.3856HSBC MIP - Savings Plan - Quarterly Dividend14-Sep-12 0.17618 0.15101 12.040614-Dec-12 0.17618 0.15101 12.435515-Mar-13 0.17618 0.15101 12.3803HSBC MIP - Savings Plan - Quarterly Dividend - Direct Plan15-Mar-13 0.08809 0.07550 12.4028

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

An Open Ended Fund with Regular & Savings Plans. Monthly income is not assured and is subject to availability of distributable surplus.Investment Objective: Seeks to generate reasonable returns through investments in Debt and Money Market Instruments. The secondary objective of the scheme is to invest in equity and equity related instruments to seek capital appreciation.

Issuer

MarketValue(` in

Lacs)

% toNet

AssetsRating

Corporate/PSU DebtFixedPower Grid Corporation of India 1,380.25 7.06% CRISIL AAAHDFC 1,017.66 5.21% CRISIL AAABajaj Finance 1,008.41 5.16% [ICRA] AA+NABARD 824.71 4.22% CRISIL AAARural Electrification Corporation 808.59 4.14% CARE AAALIC Housing Finance 807.39 4.13% CRISIL AAAPower Finance Corporation 712.92 3.65% CRISIL AAAShriram Transport Finance Company 701.56 3.59% CRISIL AAHDFC 580.63 2.97% CRISIL AAAUnion Bank of India 512.75 2.62% CRISIL AAAPower Finance Corporation 511.95 2.62% CRISIL AAATata Sons 509.17 2.60% CRISIL AAAExport Import Bank of India 508.55 2.60% CRISIL AAALIC Housing Finance 507.26 2.59% CRISIL AAAPower Finance Corporation 406.65 2.08% CRISIL AAAPower Finance Corporation 307.10 1.57% CRISIL AAANABARD 305.89 1.56% CRISIL AAANABARD 205.49 1.05% CRISIL AAANational Housing Bank 200.69 1.03% Fitch AAA (ind)Bank of Baroda 152.20 0.78% CRISIL AAAGovernment Securities8.20% Government Stock M - 24-Sep-2025 2,138.72 10.94% Sovereign8.12% Government Stock M - 10-Dec-2020 1,178.76 6.03% Sovereign8.51% Punjab State Development Loan 2023 M - 10-Apr-2023

245.24 1.25% Sovereign

8.58% Gujrat State Development Loan M - 23-Jan-2023

164.34 0.84% Sovereign

8.07% Government Stock M - 03-Jul-2017 137.62 0.70% Sovereign8.30% Government Stock M - 31-Dec-2042 88.66 0.45% SovereignEquitiesListed EquityICICI Bank 197.82 1.01%I T C 182.51 0.93%Shree Cements 160.04 0.82%HDFC Bank 145.13 0.74%HDFC 127.14 0.65%Amara Raja Batteries 119.67 0.61%Maruti Suzuki India 104.63 0.54%NTPC 102.28 0.52%Bank of Baroda 95.33 0.49%Tata Consultancy Services 93.04 0.48%Supreme Industries 91.98 0.47% N.A.McLeod Russel India 86.43 0.44%Petronet LNG 82.89 0.42%Yes Bank 82.77 0.42%Bharti Airtel 78.41 0.40%Shriram Transport Finance Company 74.55 0.38%Ipca Laboratories 71.16 0.36%Crompton Greaves 69.15 0.35%Karur Vysya Bank 67.65 0.35%Grasim Industries 61.55 0.31%Hindustan Zinc 59.58 0.30%Motherson Sumi Systems 58.75 0.30%Divi's Laboratories 57.38 0.29%Titan Industries 56.85 0.29%Oil & Natural Gas Corporation 55.54 0.28%

HSBC MIP - Regular Plan (HMIP-R) April 2013

31

Date of Allotment 24-Feb-04Benchmark CRISIL MIP

Blended IndexNAV (Growth) per unit(as on 30.04.13)

` 20.1484

Average Maturity of Portfolio

70.02 months

Modified Durationof Portfolio

47.64 months

Fund Manager Aditya Khemani(for Equity portion)Sanjay Shah &Ruchir Parekh(for Debt portion)

SIP AvailableMinimum Application AmountGrowth `10,000Quarterly Dividend `10,000Monthly Dividend `25,000SIP `1,000 p.m.Exit Load@ NilAnnualised Expense Ratio from 01 April 2013 onwards 2.51%@ Effective from March 1, 2013 for prospective investments.

Asset AllocationCorporate/ PSU Debt 61.23%Government Securities 20.22%Cash Equivalents 3.70%Net Current Assets -0.09%Other Equity Investments 14.94%Total Net Assets 100.00%

Issuer

MarketValue(` in

Lacs)

% toNet

AssetsRating

Jindal Steel and Power 54.82 0.28%Tech Mahindra 54.34 0.28%Infosys 53.87 0.28%Hindustan Unilever 50.79 0.26%NMDC 46.53 0.24%Havells India 46.09 0.24% N.A.Vardhman Textiles 40.12 0.21%Cadila Healthcare 39.19 0.20%Orient Cement 37.86 0.19%LIC Housing Finance 36.55 0.19%Punjab National Bank 34.56 0.18%PC Jeweller 20.64 0.11%Sanghvi Movers 8.87 0.05%Hindustan Dorr-Oliver 8.40 0.04%Orient Paper & Industries 5.05 0.03%Total 96.39%Cash EquivalentsCBLOs 723.29 3.70%Net Current Assets -17.38 -0.09%Total Net Assets as on 30 April 2013 19,548.95 100.00%

Rating ProfileAAA 52.48%AA+/ AA-/ AA 8.75%Sovereign 20.22%Reverse Repo/CBLOs 3.70%Net Current Assets -0.09%Other Equity Investments 14.94%Total Net Assets 100.00%

HSBC MIP - Regular Plan (HMIP-R) April 2013

32

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC MIP - Regular Plan - Monthly Dividend22-Feb-13 0.05285 0.04530 11.337528-Mar-13 0.05285 0.04530 11.261726-Apr-13 0.05256 0.04478 11.3867HSBC MIP - Regular Plan - Quarterly Dividend14-Sep-12 0.17618 0.15101 11.472214-Dec-12 0.17618 0.15101 11.664815-Mar-13 0.17618 0.15101 11.6883

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

An Open Ended Income SchemeInvestment Objective: Aims to provide reasonable income through a diversified portfolio of fixed income securities. The AMC’s view of interest rate trends and the nature of the Plans will be reflected in the type and maturities of securities in which the Short Term and Investment Plans are invested.

Issuer

MarketValue(` in

Lacs)

% toNet

AssetsRating

Securitised DebtFixedIndia MBS 2002 Series I-D (LIC Housing Finance) PTC 27.71 0.28% CRISIL

AAA(SO)Corporate/PSU DebtFixedPower Grid Corporation of India 920.16 9.41% CRISIL AAAState Bank of India 709.95 7.26% CRISIL AAARural Electrification Corporation 656.98 6.72% CARE AAAIndian Railway Finance Corporation 513.52 5.25% CRISIL AAAExport Import Bank of India 511.90 5.23% CRISIL AAAHDFC 508.83 5.20% CRISIL AAAPower Finance Corporation 305.54 3.12% CRISIL AAARural Electrification Corporation 254.67 2.60% CARE AAAPower Finance Corporation 204.73 2.09% CRISIL AAAPower Finance Corporation 203.33 2.08% CRISIL AAABajaj Finance 201.91 2.06% [ICRA] AA+LIC Housing Finance 201.85 2.06% CRISIL AAAShriram Transport Finance Company 200.44 2.05% CRISIL AANABARD 102.74 1.05% CRISIL AAAUnion Bank of India 102.55 1.05% CRISIL AAANABARD 101.96 1.04% CRISIL AAABank of Baroda 50.73 0.52% CRISIL AAAGovernment Securities8.20% Government Stock M - 24-Sep-2025 1,715.11 17.54% Sovereign8.12% Government Stock M - 10-Dec-2020 1,158.08 11.84% Sovereign8.51% Punjab State Development Loan 2023 M - 10-Apr-2023 337.20 3.45% Sovereign

8.30% Government Stock M - 31-Dec-2042 172.10 1.76% Sovereign8.15% Government Stock M - 11-Jun-2022 159.17 1.63% Sovereign8.25% Andhra Pradesh State Development Loan M-25-Apr-2023 125.88 1.29% Sovereign

8.07% Government Stock M - 03-Jul-2017 117.23 1.20% Sovereign8.33% Government Stock M - 09-Jul-2026 104.41 1.07% Sovereign8.58% Gujrat State Development Loan M - 23-Jan-2023 25.68 0.26% Sovereign

5.59% Government Stock M - 04-Jun-2016 0.38 0.00% SovereignTotal 99.14%Cash EquivalentsCBLOs 280.14 2.86%Reverse Repos 353.57 3.62%Net Current Assets -549.37 -5.62%Total Net Assets as on 30 April 2013 9,779.09 100.00%

HSBC Income Fund - Investment Plan (HIF-IP) April 2013

33

Date of Allotment 10-Dec-02Benchmark CRISIL Composite

Bond Fund IndexNAV (Growth) per unit(as on 30.04.13)

` 20.7725

Average Maturity of Portfolio

99.33 months

Modified Durationof Portfolio

64.11 months

Yield To Maturity* 8.23%Fund Manager Ruchir Parekh &

Sanjay ShahSIP AvailableMinimumApplicationAmount

` 10,000` 1,000 p.m.(SIP)

Exit Load@ NilAnnualised Expense Ratio from 01 April 2013 onwards Regular 1.92%Direct Plan 0.67%

@ Effective from March 1, 2013 for prospective investments.* Based on invested Amount

Asset AllocationSecuritised Debt 0.28%Corporate / PSU Debt 58.82%Government Securities 40.04%Cash Equivalents 6.48%Net Current Assets -5.62%

Dividend DeclarationRecord Date / period of

dividend declaredDividend (` per unit)

Non-InstitutionalDividend (` per unit)

InstitutionalNAV (`) per unit(cum dividend)

HSBC Income Fund - Investment Plan - Regular Option - Quarterly Dividend14-Sep-12 0.22023 0.18876 11.452314-Dec-12 0.22023 0.18876 11.453315-Mar-13 0.22023 0.18876 11.6100HSBC Income Fund - Investment Plan - Institutional Option - Quarterly Dividend12-Jun-09 0.11387 0.10598 11.029411-Sep-09 0.11387 0.10598 10.996011-Dec-09 0.11387 0.10598 11.0973

Rating ProfileAAA 54.99%AA 4.11%Sovereign 40.04%Reverse Repos/ CBLOs 6.48%Net Current Assets -5.62%

HSBC Income Fund - Investment Plan (HIF-IP) April 2013

34

Upon payment of dividend, the NAV per unit falls to the extent of payout and statutory levy, if any. Face value: `10 per unit.

An Open Ended Income SchemeInvestment Objective: Aims to provide reasonable income through a diversified portfolio of fixed income securities. The AMC’s view of interest rate trends and the nature of the Plans will be reflected in the type and maturities of securities in which the Short Term and Investment Plans are invested.

Issuer

MarketValue(` in

Lacs)

% toNet

AssetsRating

Money Market InstrumentsCPsSundaram Finance 1,970.15 1.81% [ICRA] A1+Kotak Mahindra Prime 258.41 0.24% CRISIL A1+CDsFixedOriental Bank of Commerce 6,651.54 6.12% CRISIL A1+State Bank of Mysore 4,689.25 4.31% [ICRA] A1+Punjab National Bank 2,375.55 2.19% CARE A1+Corporation Bank 2,375.03 2.18% CRISIL A1+Central Bank of India 2,371.94 2.18% CARE A1+Oriental Bank of Commerce 2,336.31 2.15% CRISIL A1+Punjab National Bank 2,335.81 2.15% CARE A1+UCO Bank 2,332.95 2.15% CRISIL A1+IDBI Bank 2,327.98 2.14% CRISIL A1+Bank of Maharashtra 1,961.93 1.80% CRISIL A1+State Bank of Patiala 1,905.83 1.75% [ICRA] A1+Andhra Bank 1,633.07 1.50% CARE A1+Kotak Mahindra Bank 916.83 0.84% CRISIL A1+Axis Bank 496.30 0.46% CRISIL A1+Indusind Bank 495.22 0.46% CRISIL A1+Vijaya Bank 494.69 0.46% CARE A1+Oriental Bank of Commerce 422.38 0.39% CRISIL A1+United Bank of India 99.78 0.09% [ICRA] A1+ICICI Bank 74.36 0.07% [ICRA] A1+Yes Bank 65.01 0.06% [ICRA] A1+Corporate/PSU Debt