a.r.a.s. 3.1 valuation guidelines life insurance annual statement composition and valuation...

Post on 21-Dec-2015

226 views

TRANSCRIPT

A.R.A.S. 3.1 valuation guidelines

Life Insurance Annual Statement Composition and Valuation Guidelines

Life insurance companies

Table of Contents Consolidation Affiliates ARAS work papers File description and valuation Admissibility Assets Provision for doubtful collection Technical provisions Life Accident & Sickness provision

Table of Contents (cont’d) External auditor’s role External auditor’s opinion External actuary’s role Reconciliation sheet Access to guidelines Call for comments

Consolidation Line-by-line consolidation of fully or partially

owned (majority interest) insurance subsidiaries is not permitted

These should be reported as an asset (line 2.2) on the balance sheet and valued based on the equity method

Line-by-line consolidation is allowed for fully or partially owned (majority interest) subsidiaries not engaged in the insurance business

Affiliates Affiliates are defined to be:

entities that are fully or partially owned by the company

entities that fully or partially own stocks of the company

entities on which the full or partial owners of the company have control

entities of which the majority of the supervisory and/ or managing directors also represent the majority of the supervisory and/ or managing directors of the company

Affiliates (cont’d) The respective balances with affiliates should be

reported on one of the following accounts, without netting: Loans and other interest bearing receivables due

from affiliates Non-interest bearing receivables due from affiliates Payable to affiliates

Except: Balances with affiliated (re)insurance companies

regarding reinsurance business Balances with affiliated brokerage companies

regarding sale of insurance policies

ARAS work papers Work papers used to complete ARAS should be

kept on site These work papers include a reconciliation of

accounts in the company’s general ledger/ trial balance to accounts in ARAS

Work papers should be kept at a minimum for Files 103, 105 and 110.

Work papers should be kept for a minimum of 2 years

File description and valuation All Files in ARAS have been described

Detailed description of accounts in Files 103, 105 and 106

Valuation guidelines provided for each account in File 103

A Glossary of terms is provided

Admissibility of Assets Admissibility requirements are imposed on the

following balance sheet asset accounts: Intangibles: non-admissible International stocks: only investment grade

admissible International bonds: only investment grade

admissible International investment funds/ pools: only

investment grade admissible Local investments (stocks, bonds, funds):

admissibility subject to impairment test

Admissibility of Assets (cont’d) Admissibility requirements are imposed:

Mortgage loans: excess balance above 70% of current appraised market value is non-admissible except excess ≤ amount secured by Guarantee

Fund Collateral loans: excess of outstanding balance

above fair value of pledged assets is non-admissible

Interest and non-interest bearing due from affiliates: excess above applicable limits is non-admissible

Admissibility of Assets (cont’d) Admissibility requirements are imposed :

Deposits at foreign banks: only deposits at banks rated investment grade are admissible

Reinsurance recoverable on paid claims: amounts non-admissible if the insurer may not receive them due to insolvency of reinsurer or disputes about amount of coverage

Company should report in File 102, line 1: total balance of non-admitted assets that weren’t

reported in the Statement, divided between the several asset classes

Provision for doubtful collection Agents & Brokers Debit Balances:

not less than those receivables which are in excess of 90 days past due.

Uncollected premium/ term life & health insurance policies: non-installment premium: not less than those

receivables which are in excess of 90 days past due. installment premium: which are not paid on the

agreed installment date, the provision should not be less than those installments which are in excess of 90 days past due.

Technical provisions Life Principles based approach Generally accepted actuarial method Based on prudent, reliable and consistently

applied principles, including: Probability weighted future contract CF Discounting of CF at market interest rate Up-to-date objective data and realistic

assumptions Current mortality & morbidity tables All expenses that will be incurred in servicing

insurance obligations

Technical provisions Life (cont’d) Unamortized deferred acquisition cost:

equally amortized over the life of the policy to match the premium income stream, with a maximum of 10 years

Unamortized capitalized premium reduction: fully amortized within 8 years as follows:

In the year that the reduction was granted and the 3 following years by 15% each year;

In the last 4 years by 10% each year.

Technical provisions Life (cont’d) Ceded provisions

non-admissible if the insurer may not receive these amounts due to insolvency of reinsurer or disputes about amount of coverage

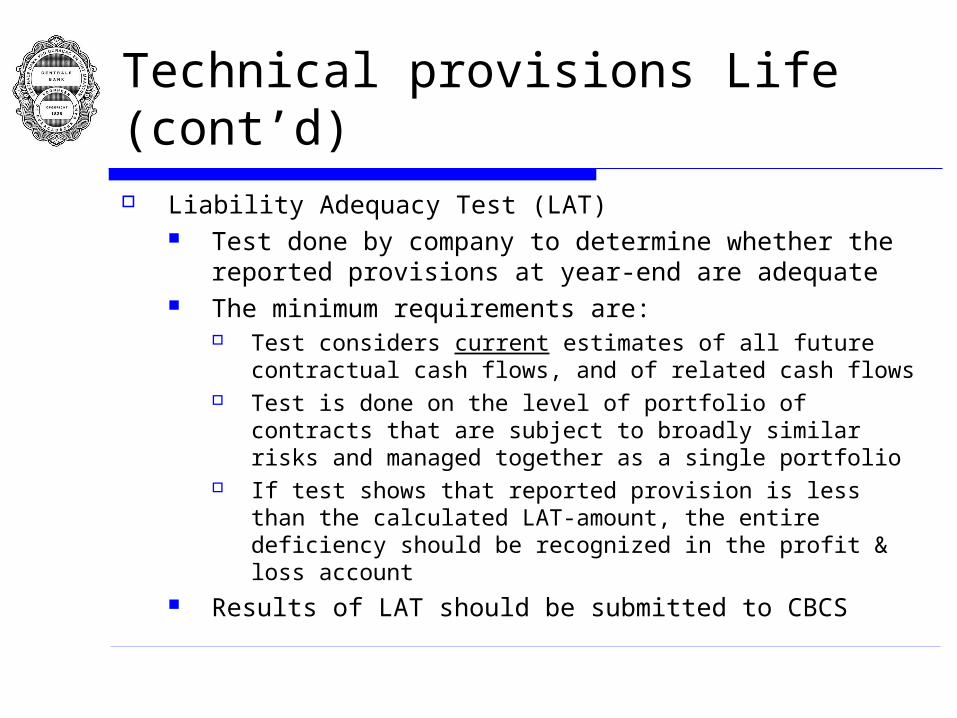

Technical provisions Life (cont’d) Liability Adequacy Test (LAT)

Test done by company to determine whether the reported provisions at year-end are adequate

The minimum requirements are: Test considers current estimates of all future

contractual cash flows, and of related cash flows Test is done on the level of portfolio of contracts that

are subject to broadly similar risks and managed together as a single portfolio

If test shows that reported provision is less than the calculated LAT-amount, the entire deficiency should be recognized in the profit & loss account

Results of LAT should be submitted to CBCS

Accident & Sickness Provision Calculation based on a non-actuarial approach

is permitted

The actuarial approach is preferred when it involves periodic payments caused by long tail claims due to for example critical illnesses

Liability Adequacy Test (LAT)

External auditor’s role Article 26, paragraph 2 of National Ordinance:

Provide auditor’s opinion on the Life Statement

Mark hard copy Life statement for identification purposes

External auditor’s role (cont’d) The external auditor should be authorized by

the company by a provision in the contract to: Supply the CBCS with written information about

the company reasonably considered necessary in order for the CBCS to comply with her duties. [when asked by CBCS]

Agree with the CBCS on the conditions or circumstances encountered during his duties which warrant informing the CBCS a.s.a.p. [voluntarily supplied to CBCS]

CBCS will send copy of received info to the company

External auditor’s opinion The Statement is based on own accounting

and reporting principles Certification of the Statement should be based

on the Life valuation guidelines! ‘According to notes’ opinion CBCS proposed a standard unqualified

‘according to notes’ opinion to be issued on the Statement

External actuary’s role Issuance of opinion on

the value at year-end of all technical provisions the fact that the comparison of mortality

experience have been reproduced correctly

Signing of the hard copy files 117 and 125

Reconciliation sheet Regards a reconciliation of the reported Total

Assets, Total Equity and/ or Net Results in the Statement with corresponding values in the company’s own financial statement

To be submitted with the Statement if a difference exists

Not applicable to local branch offices which don’t issue own financial statement

Access to guidelines Go to www.centralbank.an ‘Click’ on the ‘Login’ icon on the ribbon

Username: autoflow Password: CentralBank2

‘Click’ on link ‘Annual Reports Automated Statements (ARAS)’

Access folder ‘ARAS 3.1’

Call for comments 6 weeks available to submit comments

starting today Only via [email protected] Proposal:

Onshore insurers: joint response via N.A.V.V. Int’l insurers: joint response via C.I.A.C. Non-affiliated insurers: separate response External auditors: joint response via N.A.V.A. External actuaries: separate response

Questions??