arch and garch models - wordpress.com overview of arima models arch model garch model garch-m model...

TRANSCRIPT

ARCH AND GARCH MODELS

Phung Thanh Binh

▪ An overview of ARIMA models

▪ ARCH model

▪ GARCH model

▪ GARCH-M model

▪ T-GARCH/EGARCH models

▪ Factors of volatility

▪ MGACH model

OUTLINE

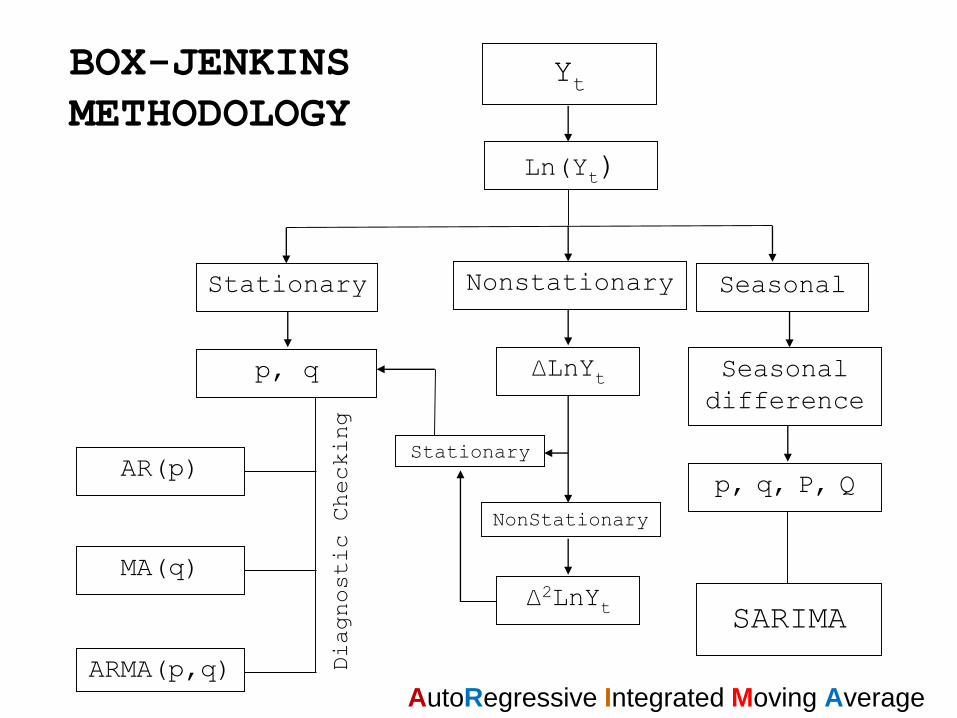

Ln(Yt)

Stationary Seasonal

Yt

Nonstationary

p, q

AR(p)

MA(q)

ARMA(p,q) Diagnostic Checking

∆LnYt

Stationary

NonStationary

∆2LnYt

Seasonal

difference

p, q, P, Q

SARIMA

BOX-JENKINS

METHODOLOGY

AutoRegressive Integrated Moving Average

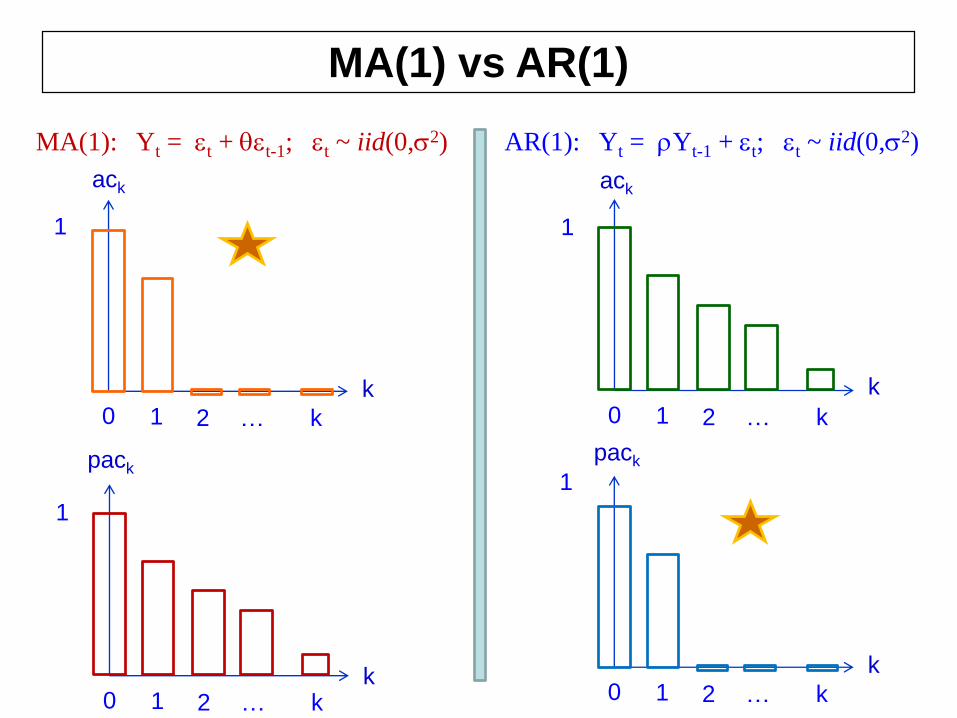

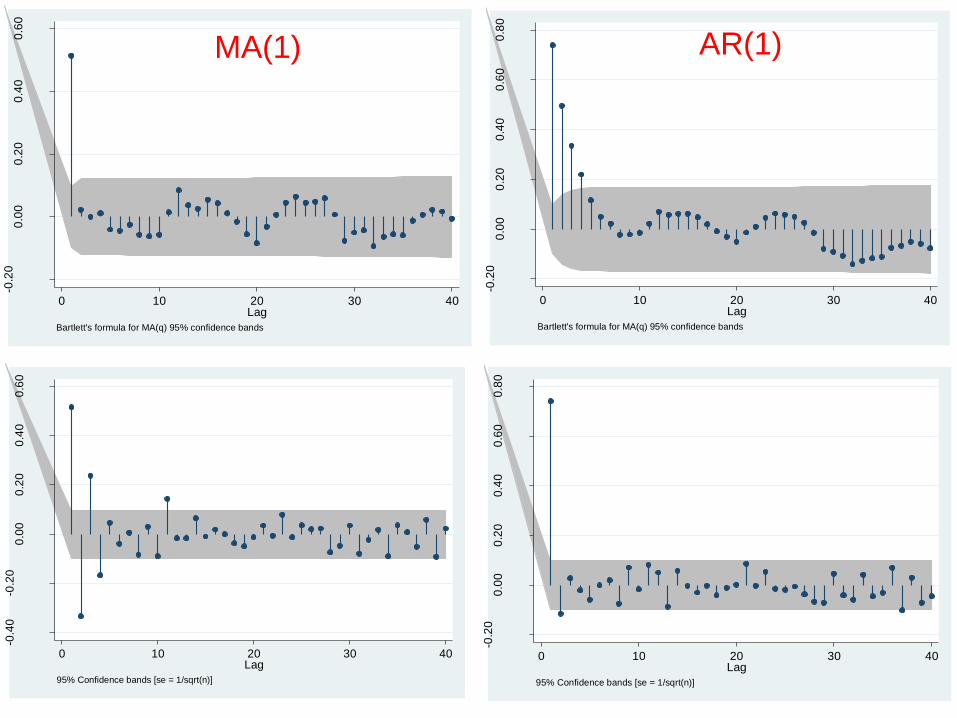

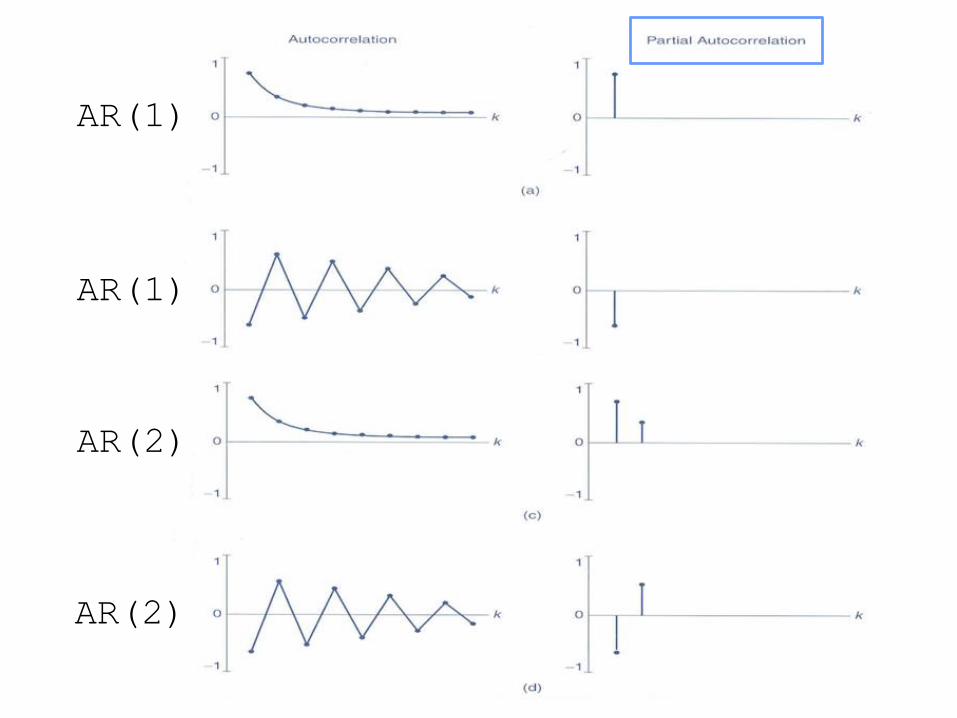

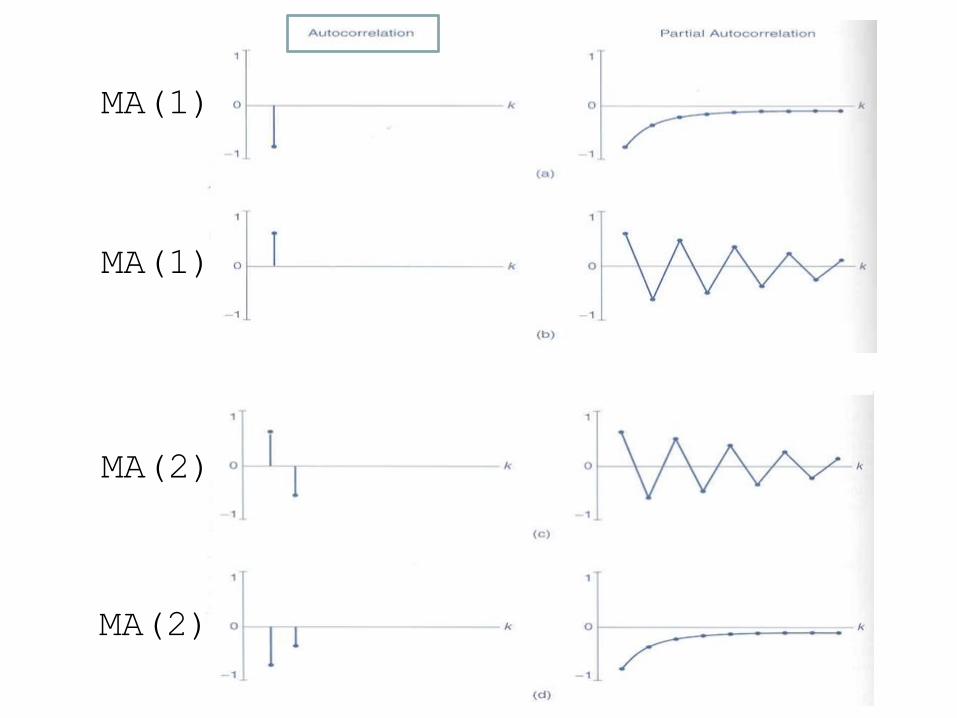

MA(1) vs AR(1)

MA(1): Yt = t + t-1; t ~ iid(0,2) AR(1): Yt = Yt-1 + t; t ~ iid(0,2)

ack

k0

1

1 2 k…

ack

k

0

1

1 2 k…

pack

k0

1

1 2 k…k

0

1

1 2 k…

pack

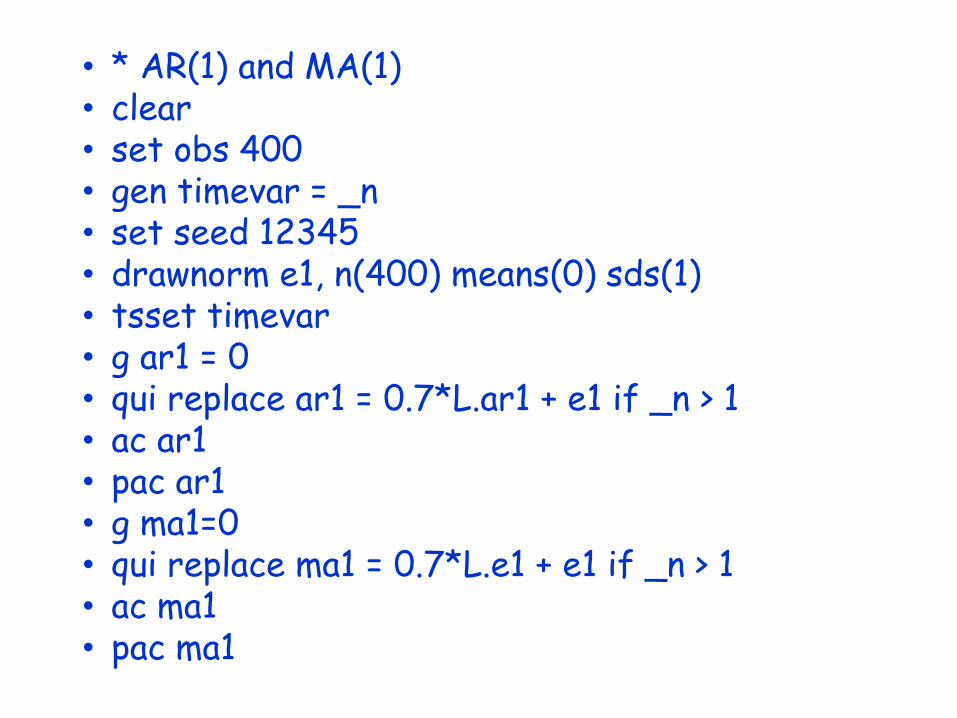

• * AR(1) and MA(1)• clear• set obs 400• gen timevar = _n• set seed 12345• drawnorm e1, n(400) means(0) sds(1)• tsset timevar• g ar1 = 0• qui replace ar1 = 0.7*L.ar1 + e1 if _n > 1• ac ar1• pac ar1• g ma1=0• qui replace ma1 = 0.7*L.e1 + e1 if _n > 1• ac ma1• pac ma1

-0.2

00

.00

0.2

00

.40

0.6

00

.80

Pa

rtia

l a

uto

co

rrela

tio

ns o

f a

r1

0 10 20 30 40Lag

95% Confidence bands [se = 1/sqrt(n)]

-0.2

00

.00

0.2

00

.40

0.6

00

.80

Au

tocorr

ela

tion

s o

f ar1

0 10 20 30 40Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.2

00

.00

0.2

00

.40

0.6

0

Au

tocorr

ela

tion

s o

f m

a1

0 10 20 30 40Lag

Bartlett's formula for MA(q) 95% confidence bands

AR(1)MA(1)

-0.4

0-0

.20

0.0

00

.20

0.4

00

.60

Pa

rtia

l a

uto

co

rrela

tio

ns o

f m

a1

0 10 20 30 40Lag

95% Confidence bands [se = 1/sqrt(n)]

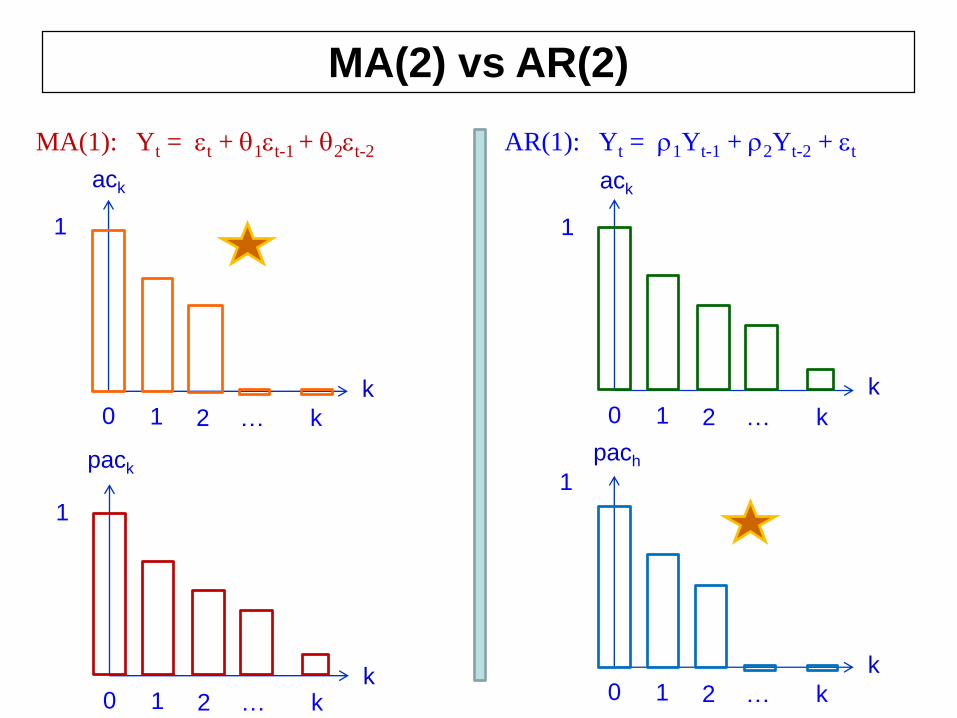

MA(2) vs AR(2)

MA(1): Yt = t + 1t-1 + 2t-2 AR(1): Yt = 1Yt-1 + 2Yt-2 + t

ack

k0

1

1 2 k…

ack

k

0

1

1 2 k…

pach

k0

1

1 2 k…k

0

1

1 2 k…

pack

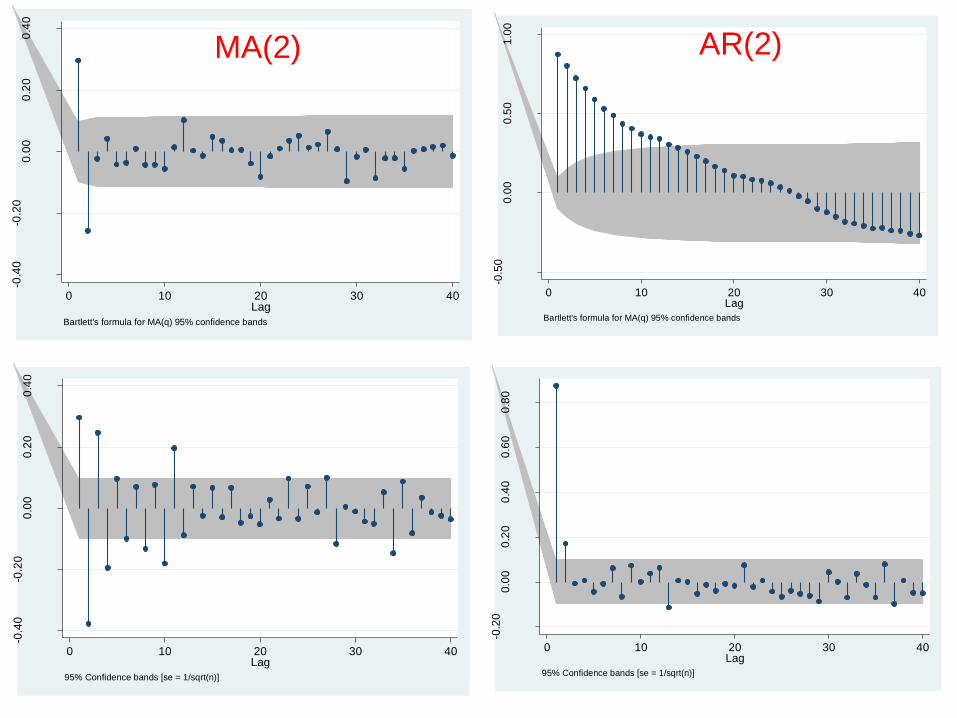

• * AR(2) and MA(2)• clear• set obs 400• gen timevar = _n• set seed 12345• drawnorm e1, n(400) means(0) sds(1)• tsset timevar• g double ar2 = 0• qui replace ar2 in 3/l = 0.6*L.ar2 + 0.3*L2.ar2 + e1• ac ar2• pac ar2• g double ma2=0• qui replace ma2 in 3/l = 0.6*L.e1 - 0.4*L2.e1 + e1• ac ma2• pac ma2

-0.4

0-0

.20

0.0

00

.20

0.4

0

Au

tocorr

ela

tion

s o

f m

a2

0 10 20 30 40Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.4

0-0

.20

0.0

00

.20

0.4

0

Pa

rtia

l a

uto

co

rrela

tio

ns o

f m

a2

0 10 20 30 40Lag

95% Confidence bands [se = 1/sqrt(n)]

-0.5

00

.00

0.5

01

.00

Au

tocorr

ela

tion

s o

f ar2

0 10 20 30 40Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.2

00

.00

0.2

00

.40

0.6

00

.80

Pa

rtia

l a

uto

co

rrela

tio

ns o

f a

r2

0 10 20 30 40Lag

95% Confidence bands [se = 1/sqrt(n)]

AR(2)MA(2)

AR(1)

AR(1)

AR(2)

AR(2)

MA(1)

MA(2)

MA(2)

MA(1)

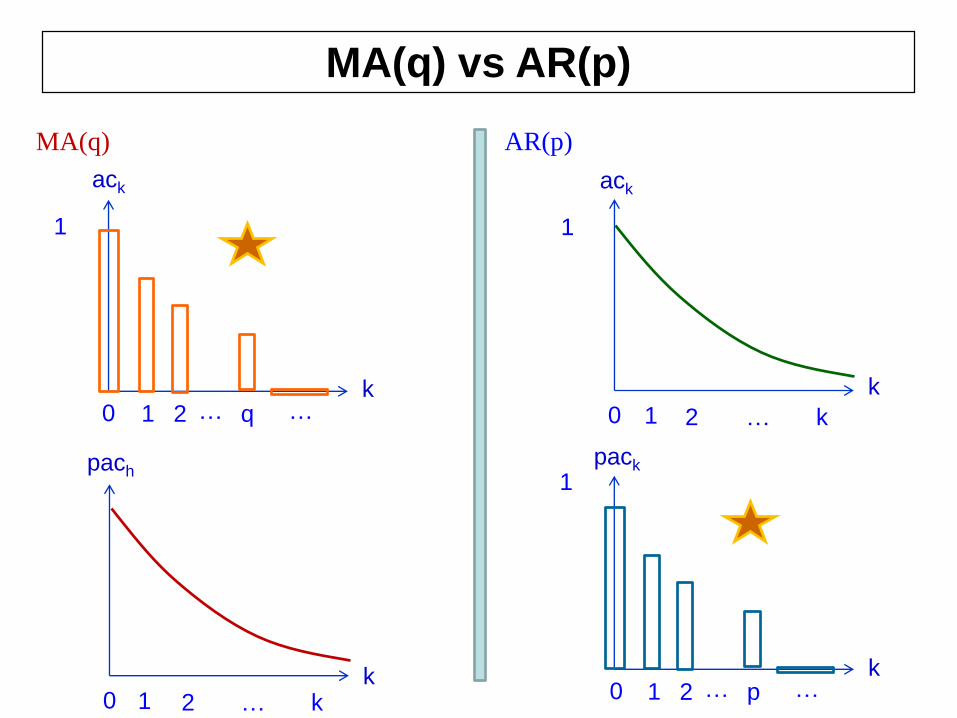

MA(q) vs AR(p)

MA(q) AR(p)

ack

k0

1

1 2 …

ack

k

0

1

1 2 k…

pack

k

1

k0 1 2 k…

pach

q …

0 1 2 … p …

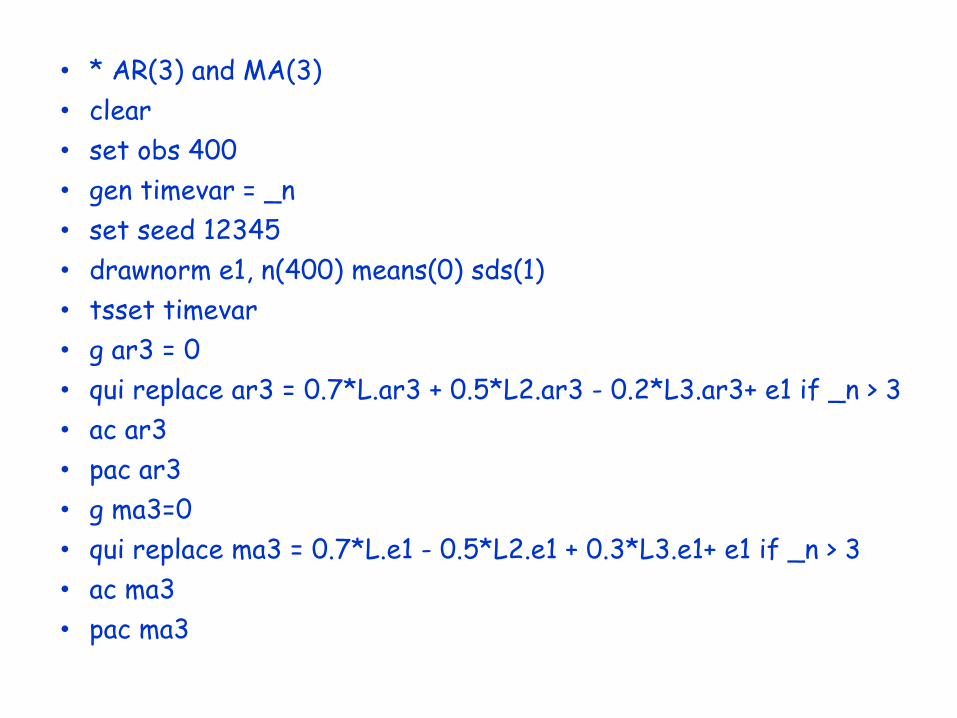

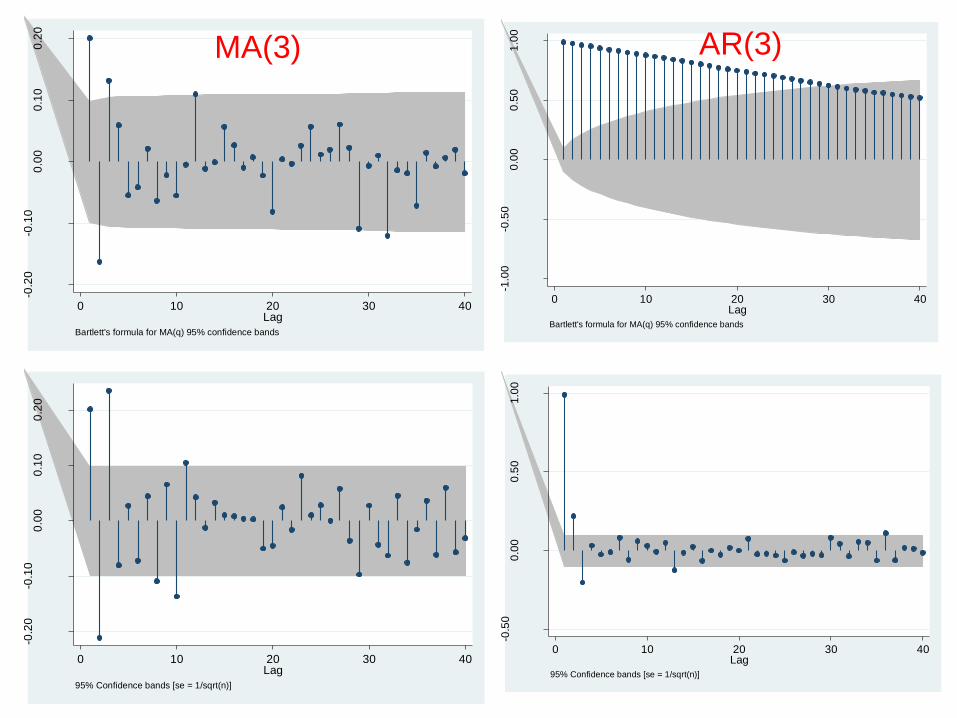

• * AR(3) and MA(3)

• clear

• set obs 400

• gen timevar = _n

• set seed 12345

• drawnorm e1, n(400) means(0) sds(1)

• tsset timevar

• g ar3 = 0

• qui replace ar3 = 0.7*L.ar3 + 0.5*L2.ar3 - 0.2*L3.ar3+ e1 if _n > 3

• ac ar3

• pac ar3

• g ma3=0

• qui replace ma3 = 0.7*L.e1 - 0.5*L2.e1 + 0.3*L3.e1+ e1 if _n > 3

• ac ma3

• pac ma3

-0.2

0-0

.10

0.0

00

.10

0.2

0

Au

tocorr

ela

tion

s o

f m

a3

0 10 20 30 40Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.2

0-0

.10

0.0

00

.10

0.2

0

Pa

rtia

l a

uto

co

rrela

tio

ns o

f m

a3

0 10 20 30 40Lag

95% Confidence bands [se = 1/sqrt(n)]

-1.0

0-0

.50

0.0

00

.50

1.0

0

Au

tocorr

ela

tion

s o

f ar3

0 10 20 30 40Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.5

00

.00

0.5

01

.00

Pa

rtia

l a

uto

co

rrela

tio

ns o

f a

r3

0 10 20 30 40Lag

95% Confidence bands [se = 1/sqrt(n)]

AR(3)MA(3)

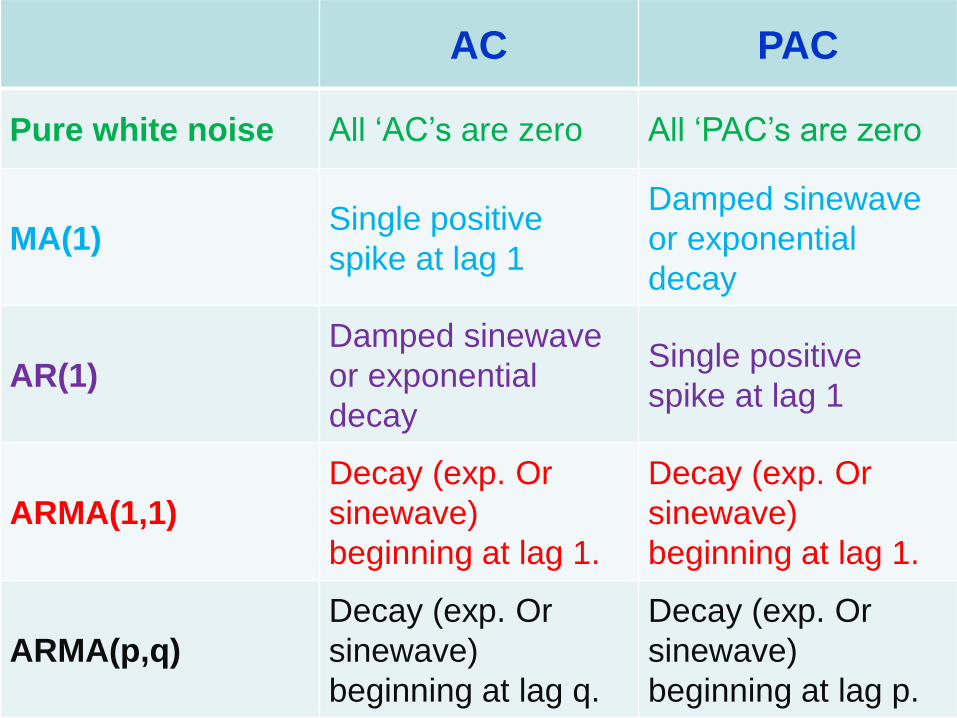

AC PAC

Pure white noise All ‘AC’s are zero All ‘PAC’s are zero

MA(1)Single positive

spike at lag 1

Damped sinewave

or exponential

decay

AR(1)

Damped sinewave

or exponential

decay

Single positive

spike at lag 1

ARMA(1,1)

Decay (exp. Or

sinewave)

beginning at lag 1.

Decay (exp. Or

sinewave)

beginning at lag 1.

ARMA(p,q)

Decay (exp. Or

sinewave)

beginning at lag q.

Decay (exp. Or

sinewave)

beginning at lag p.

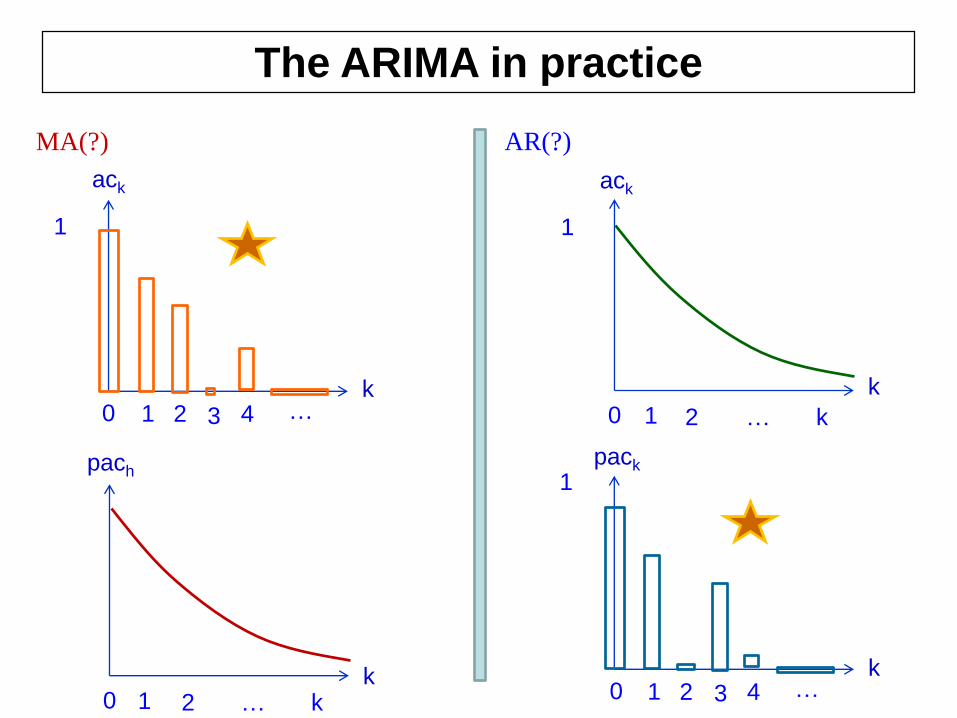

The ARIMA in practice

MA(?) AR(?)

ack

k0

1

1 2

ack

k

0

1

1 2 k…

pack

k

1

k0 1 2 k…

pach

4 …

0 1 2 4 …

3

3

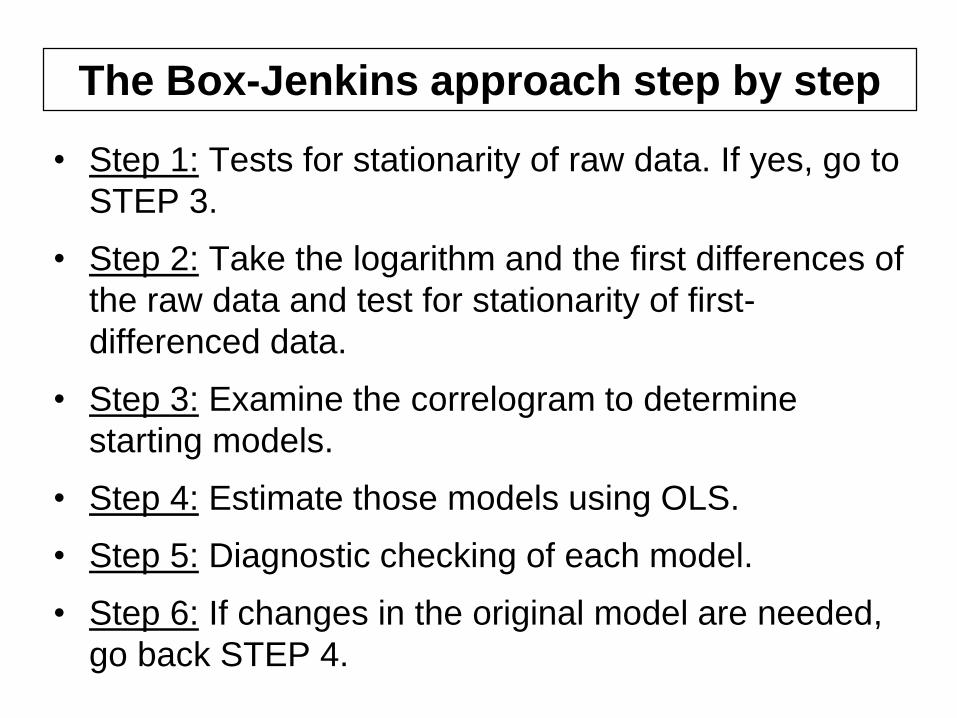

• Step 1: Tests for stationarity of raw data. If yes, go to

STEP 3.

• Step 2: Take the logarithm and the first differences of

the raw data and test for stationarity of first-

differenced data.

• Step 3: Examine the correlogram to determine

starting models.

• Step 4: Estimate those models using OLS.

• Step 5: Diagnostic checking of each model.

• Step 6: If changes in the original model are needed,

go back STEP 4.

The Box-Jenkins approach step by step

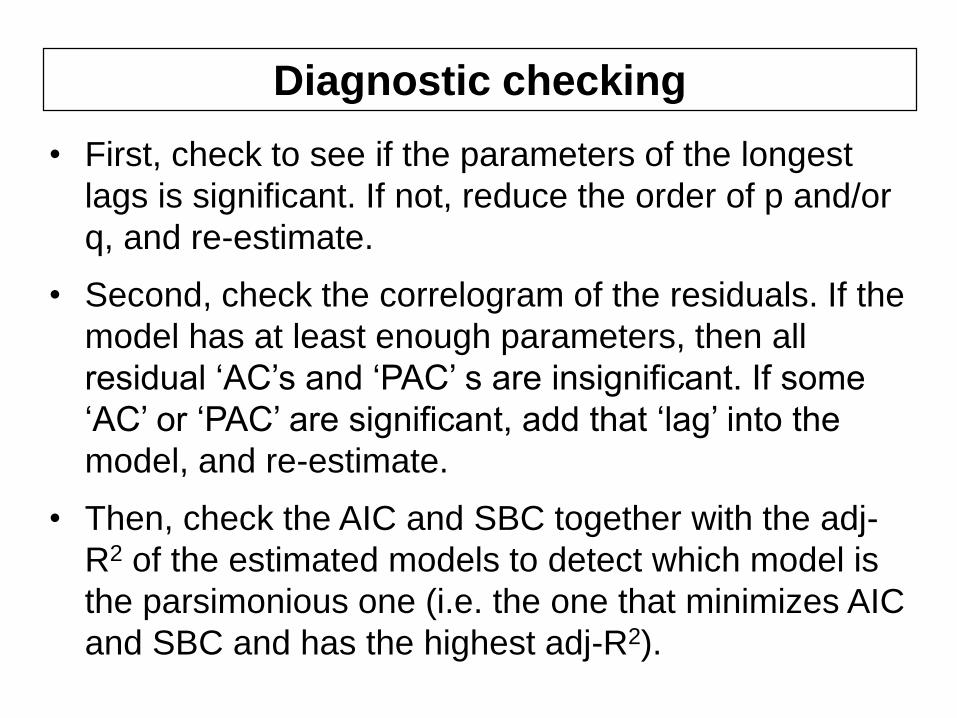

• First, check to see if the parameters of the longest

lags is significant. If not, reduce the order of p and/or

q, and re-estimate.

• Second, check the correlogram of the residuals. If the

model has at least enough parameters, then all

residual ‘AC’s and ‘PAC’ s are insignificant. If some

‘AC’ or ‘PAC’ are significant, add that ‘lag’ into the

model, and re-estimate.

• Then, check the AIC and SBC together with the adj-

R2 of the estimated models to detect which model is

the parsimonious one (i.e. the one that minimizes AIC

and SBC and has the highest adj-R2).

Diagnostic checking

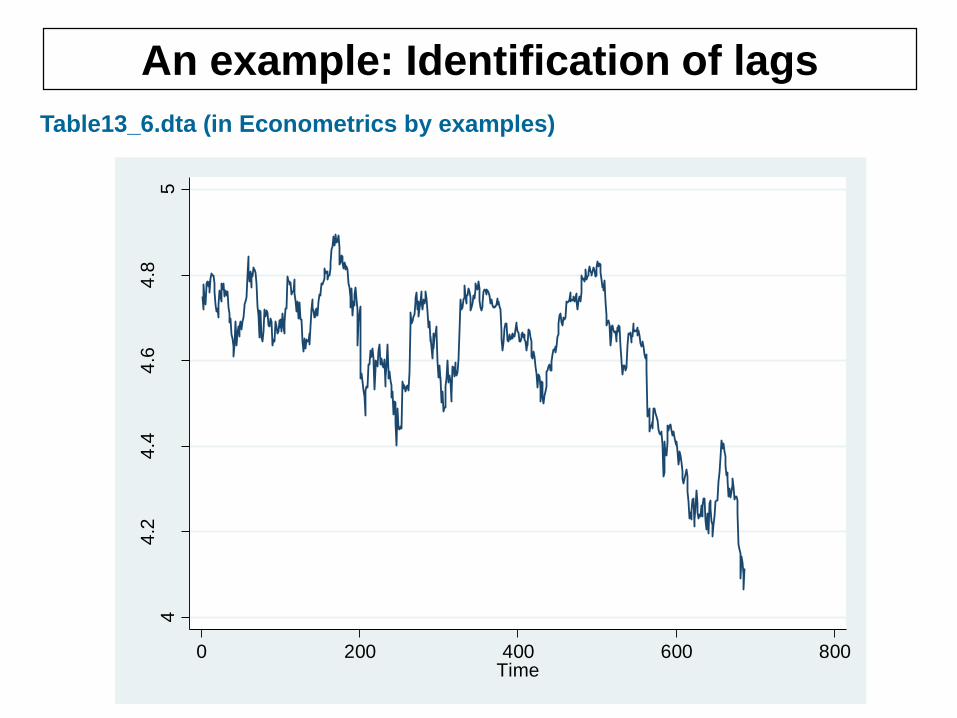

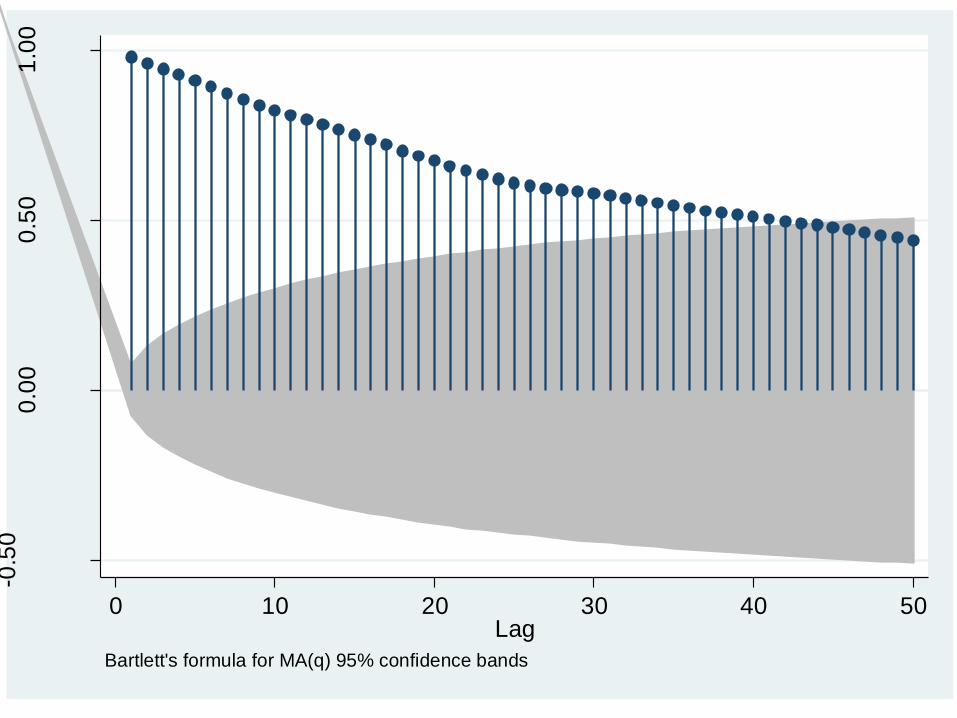

An example: Identification of lags

Table13_6.dta (in Econometrics by examples)

44

.24

.44

.64

.85

ln(c

lose

)

0 200 400 600 800Time

-0.5

00

.00

0.5

01

.00

Au

tocorr

ela

tion

s o

f ln

clo

se

0 10 20 30 40 50Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.1

0-0

.05

0.0

00

.05

0.1

0

Au

tocorr

ela

tion

s o

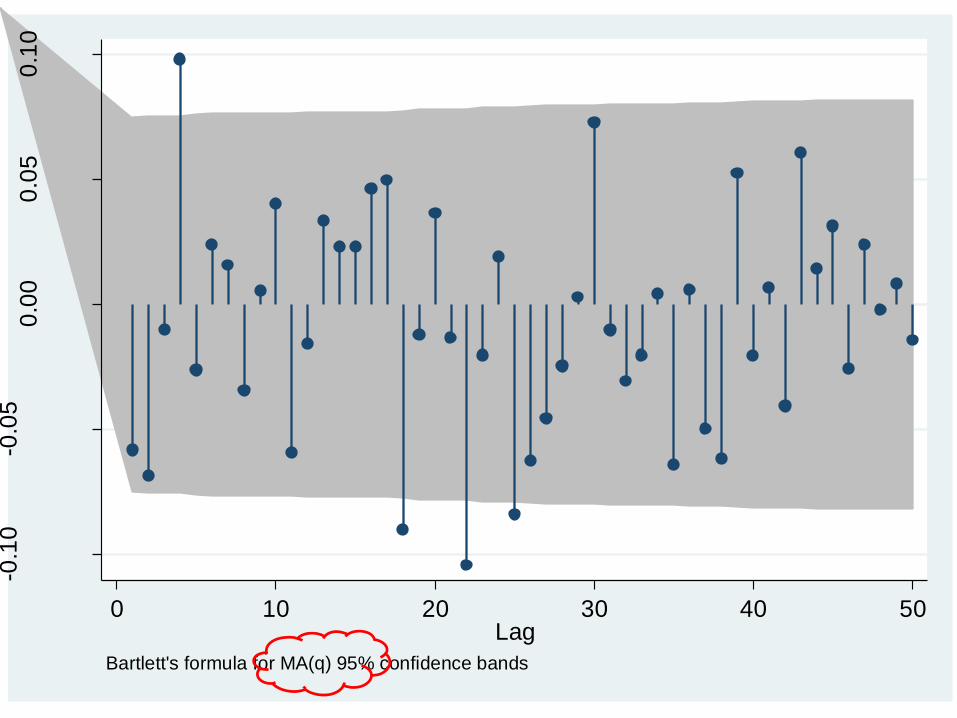

f D

.ln

clo

se

0 10 20 30 40 50Lag

Bartlett's formula for MA(q) 95% confidence bands

-0.1

0-0

.05

0.0

00

.05

0.1

0

Au

tocorr

ela

tion

s o

f D

.ln

clo

se

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50Lag

Bartlett's formula for MA(q) 95% confidence bandsac d.lnclose, lags(50)

q = (4, 18, 22, 25)

-0.1

0-0

.05

0.0

00

.05

0.1

0

Pa

rtia

l a

uto

co

rrela

tio

ns o

f D

.lnclo

se

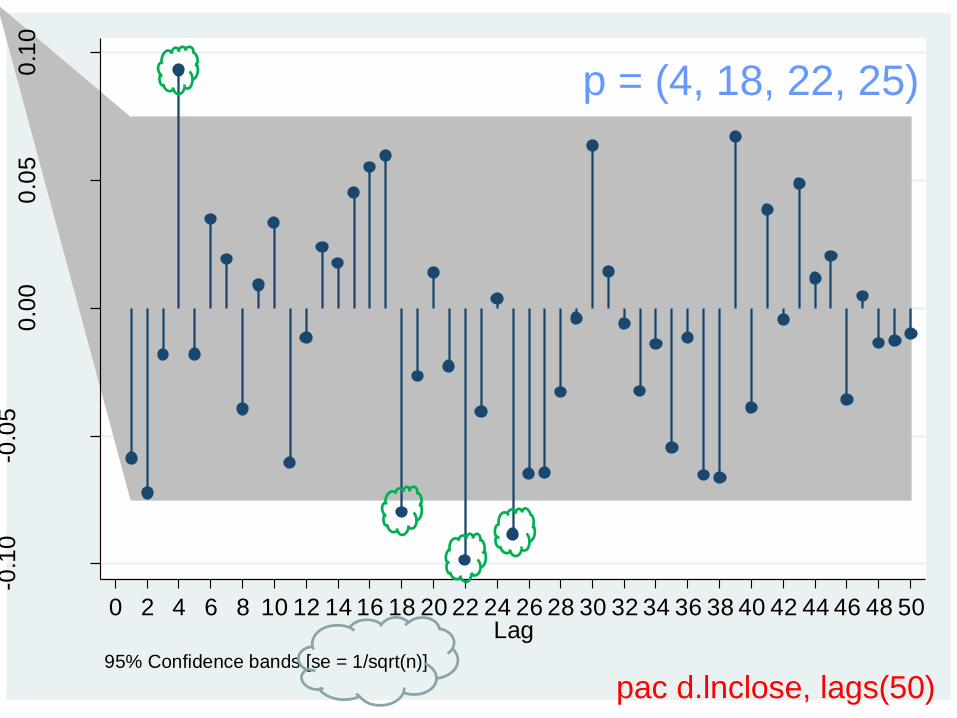

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46 48 50Lag

95% Confidence bands [se = 1/sqrt(n)]

p = (4, 18, 22, 25)

pac d.lnclose, lags(50)

Technical notes:

Current Stata versions can not estimate

models with more than 20 lagged

variables.

Identification of p and q by using Stata

could be better than using other

softwares.

Stata commands:

arima d.lnclose, ar(1/3) ma(1/4)

arima lnclose, arima(3,1,4)

arima d.lnclose, ar(1 2 5) ma(1 3 4)

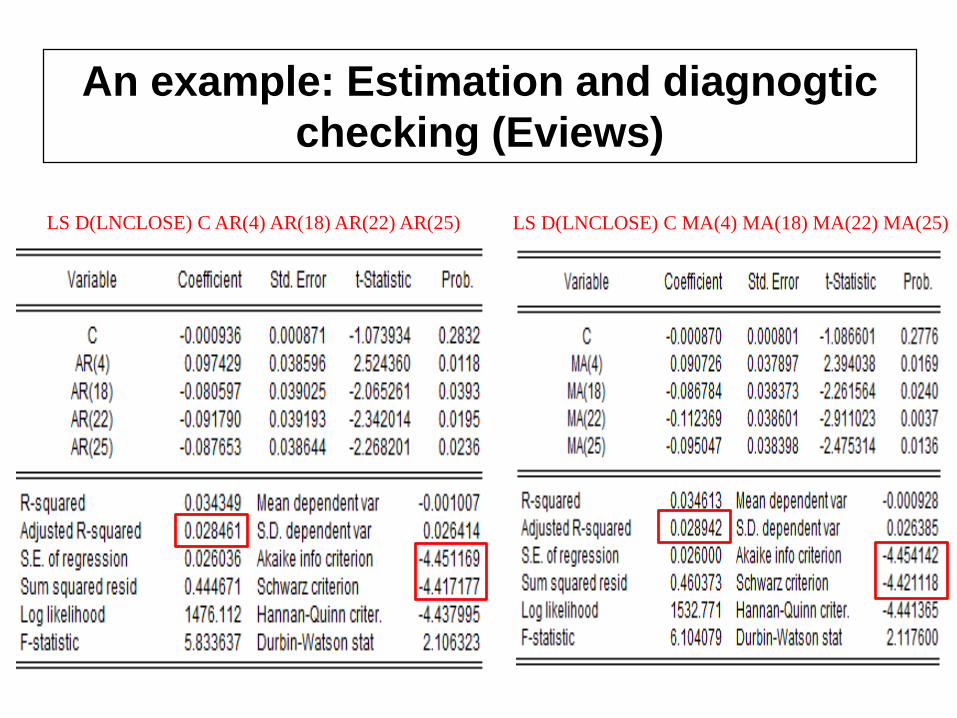

An example: Estimation and diagnogtic

checking (Eviews)

LS D(LNCLOSE) C AR(4) AR(18) AR(22) AR(25) LS D(LNCLOSE) C MA(4) MA(18) MA(22) MA(25)

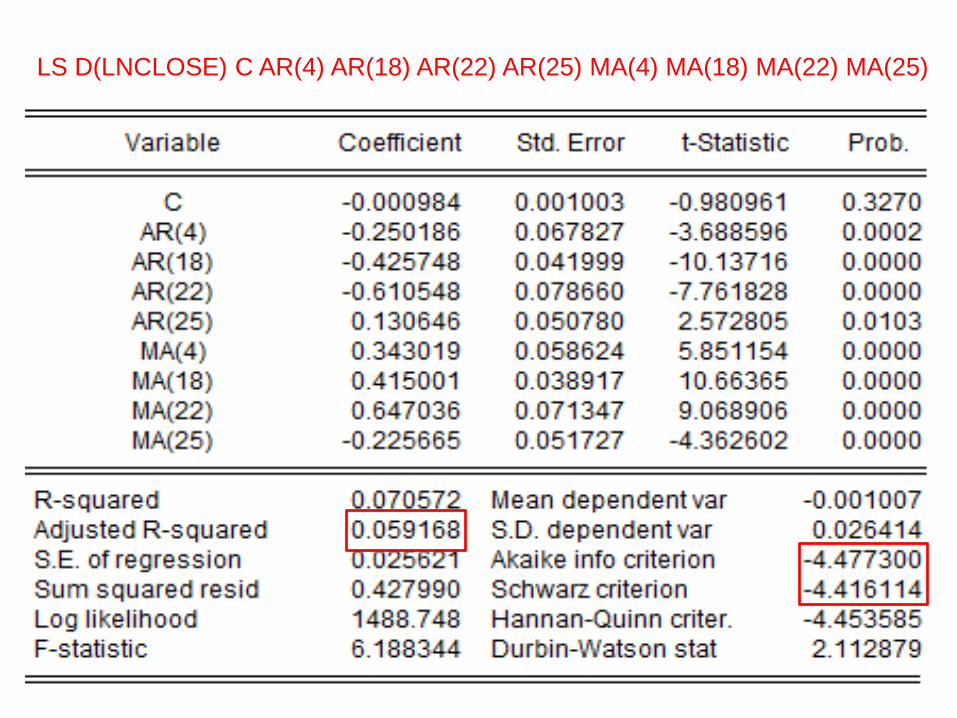

LS D(LNCLOSE) C AR(4) AR(18) AR(22) AR(25) MA(4) MA(18) MA(22) MA(25)

• Conventional econometric analysis views the

variance of the disturbance as constant over

time (‘homoscedasticity’).

• But, many economic time series exhibit

periods of unusually ‘high volatility’ (wild)

followed by more tranquil periods of ‘low

volatility’ (calm).

• Financial econometrics: model the attitude of

investors not only towards expected returns,

but towards risk (variance).

The ARCH/GARCH models

The ARCH model

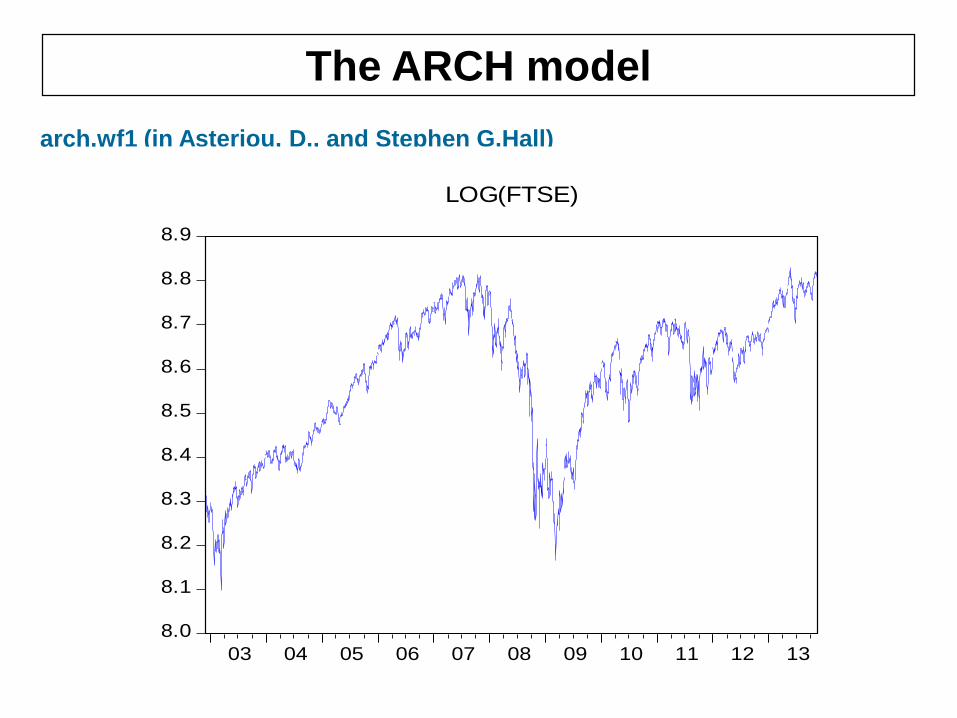

arch.wf1 (in Asteriou, D., and Stephen G.Hall)

8.0

8.1

8.2

8.3

8.4

8.5

8.6

8.7

8.8

8.9

03 04 05 06 07 08 09 10 11 12 13

LOG(FTSE)

-.100

-.075

-.050

-.025

.000

.025

.050

.075

.100

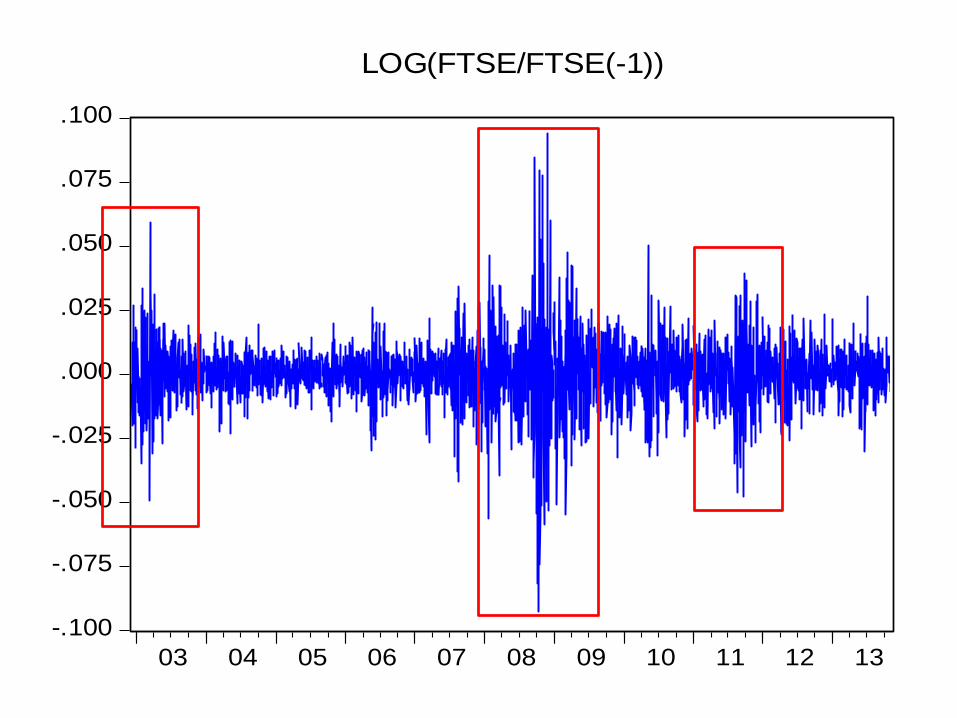

03 04 05 06 07 08 09 10 11 12 13

LOG(FTSE/FTSE(-1))

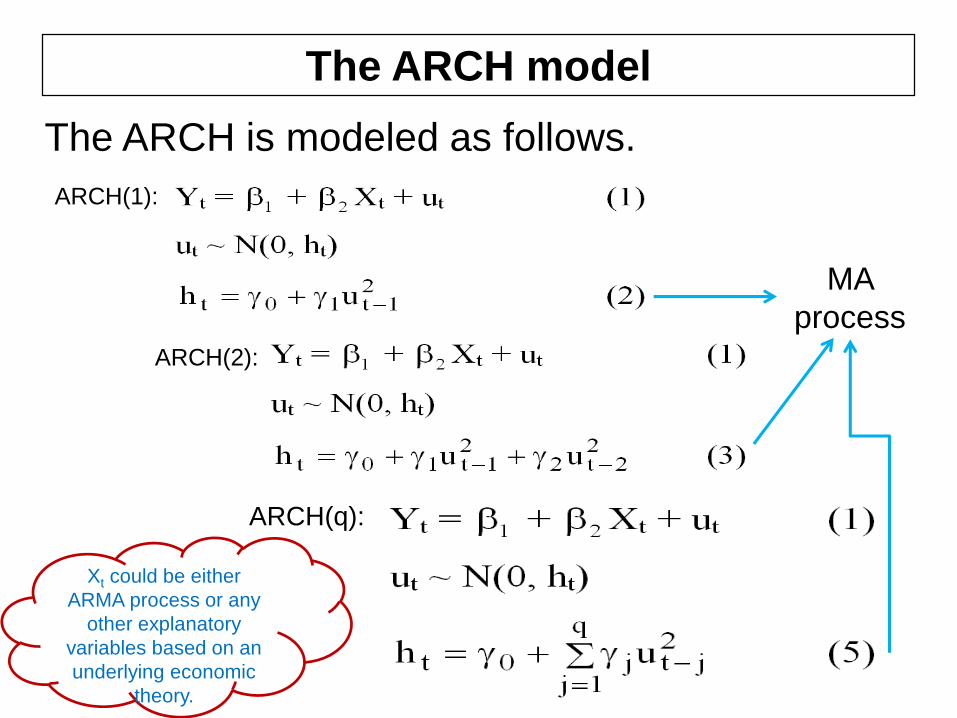

The ARCH model

The ARCH is modeled as follows.

ARCH(1):

ARCH(2):

ARCH(q):

MA

process

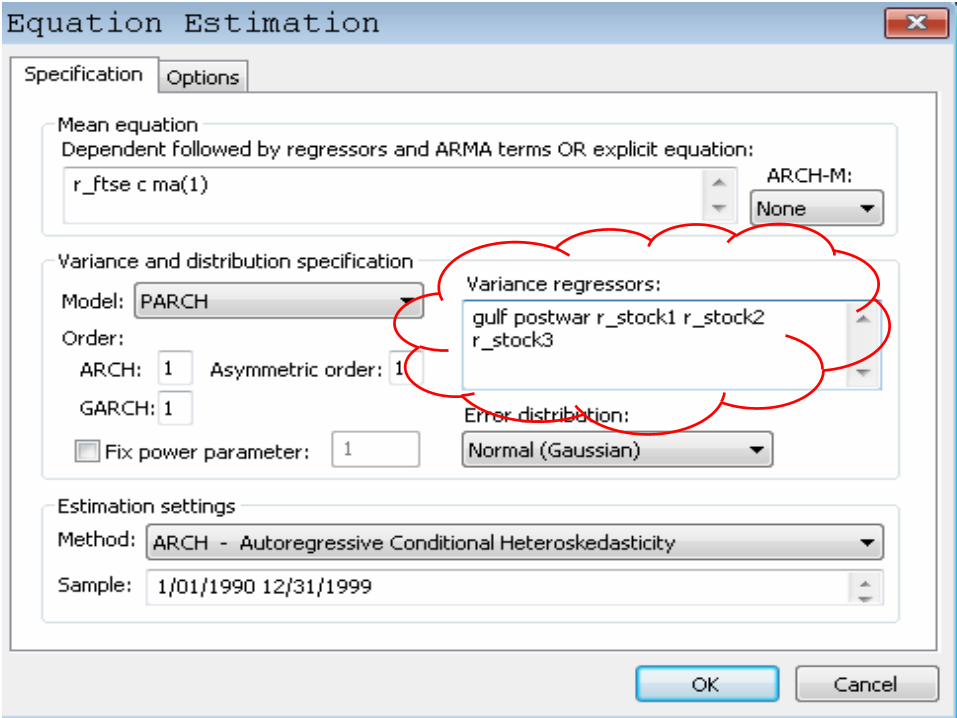

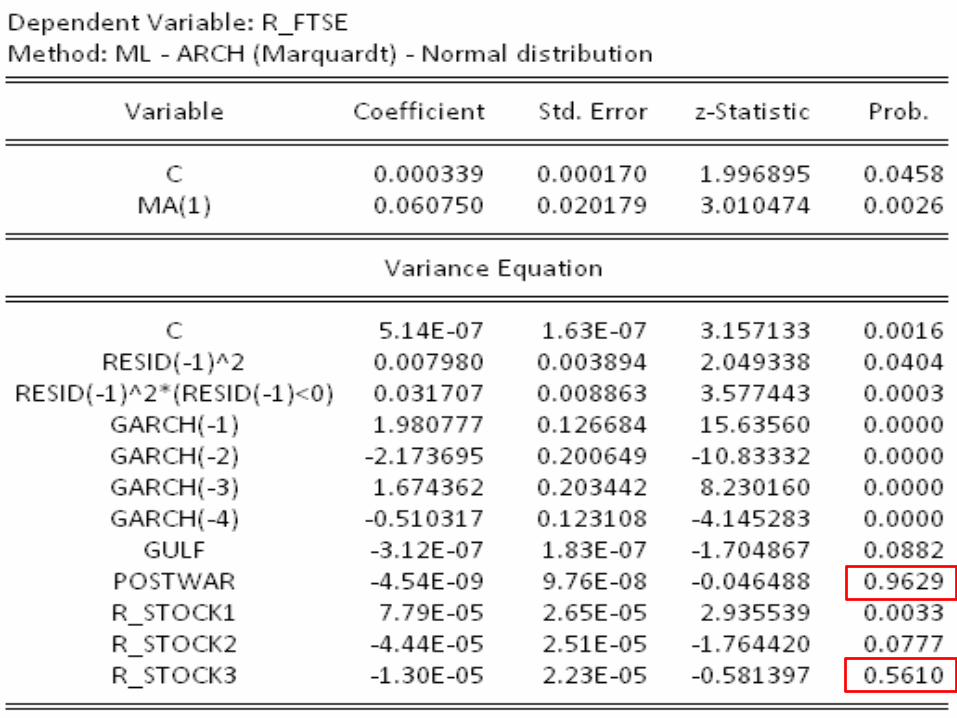

Xt could be either

ARMA process or any

other explanatory

variables based on an

underlying economic

theory.

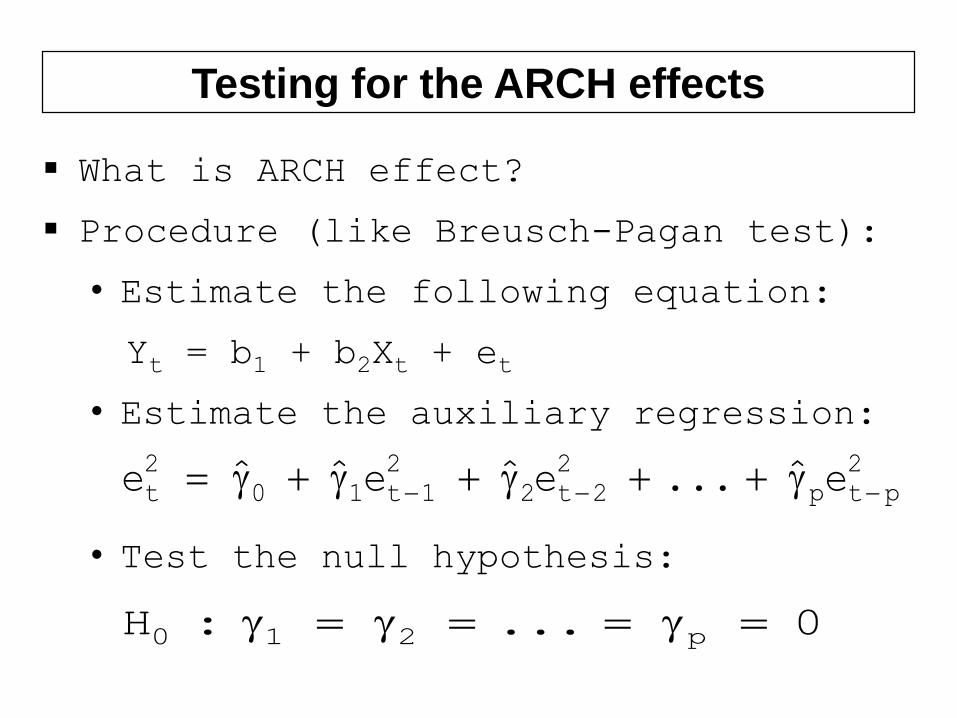

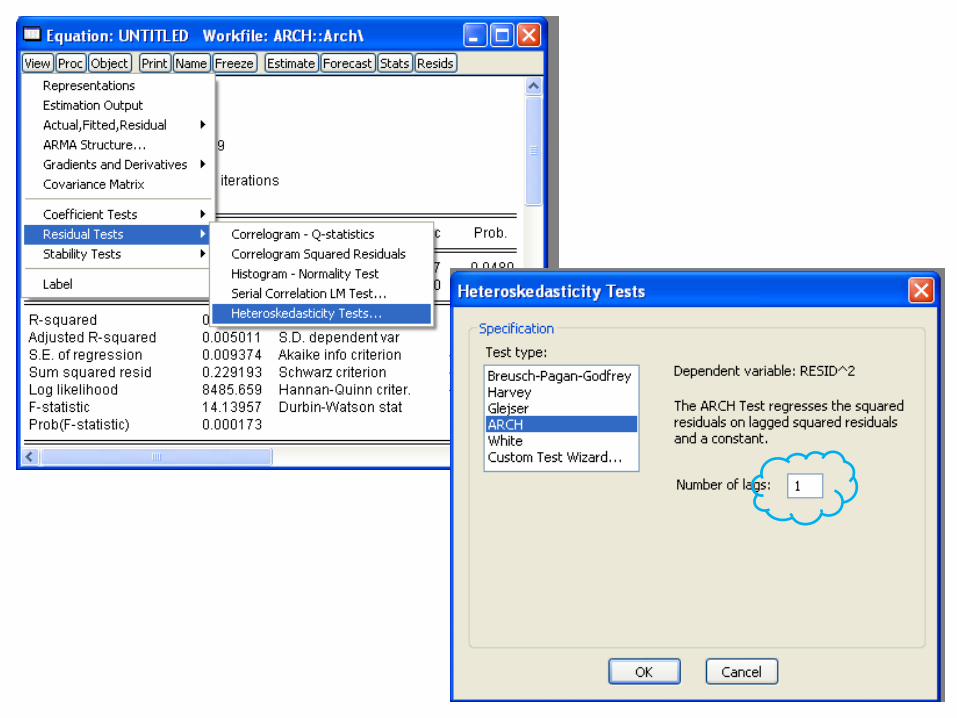

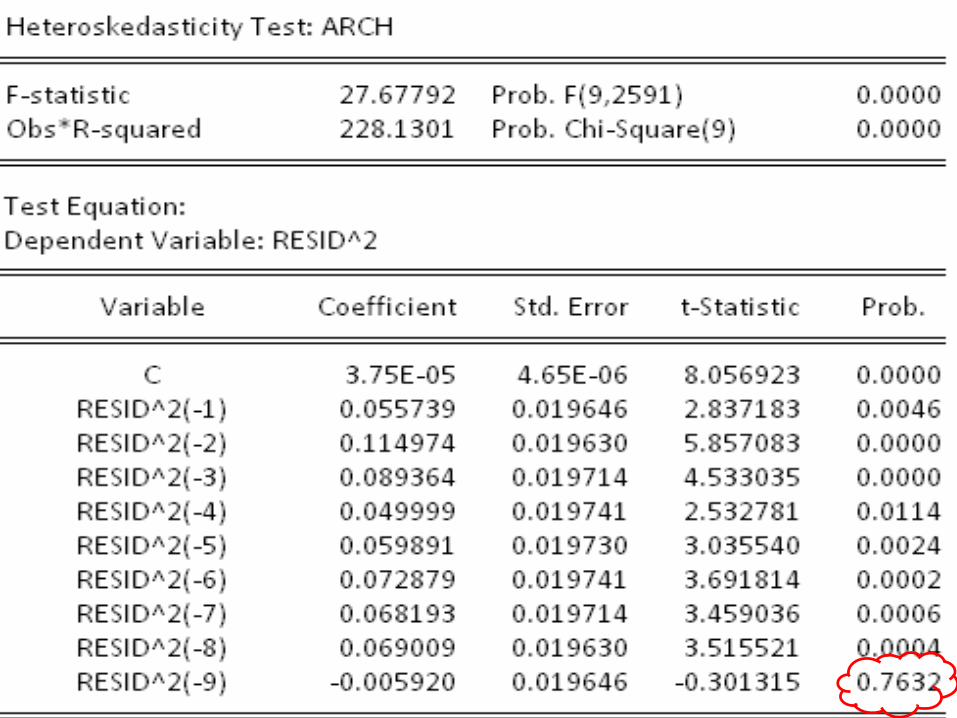

Testing for the ARCH effects

▪ What is ARCH effect?

▪ Procedure (like Breusch-Pagan test):

• Estimate the following equation:

Yt = b1 + b2Xt + et

• Estimate the auxiliary regression:

• Test the null hypothesis:

2

ptp

2

2t2

2

1t10

2

t eˆ...eˆeˆˆe

0...:H p210

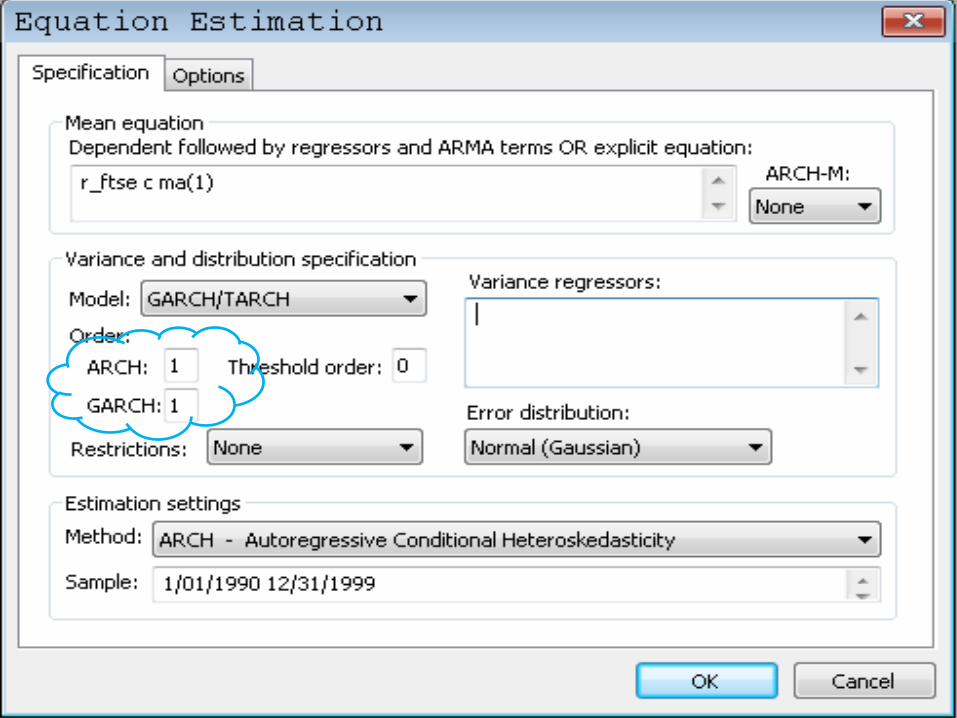

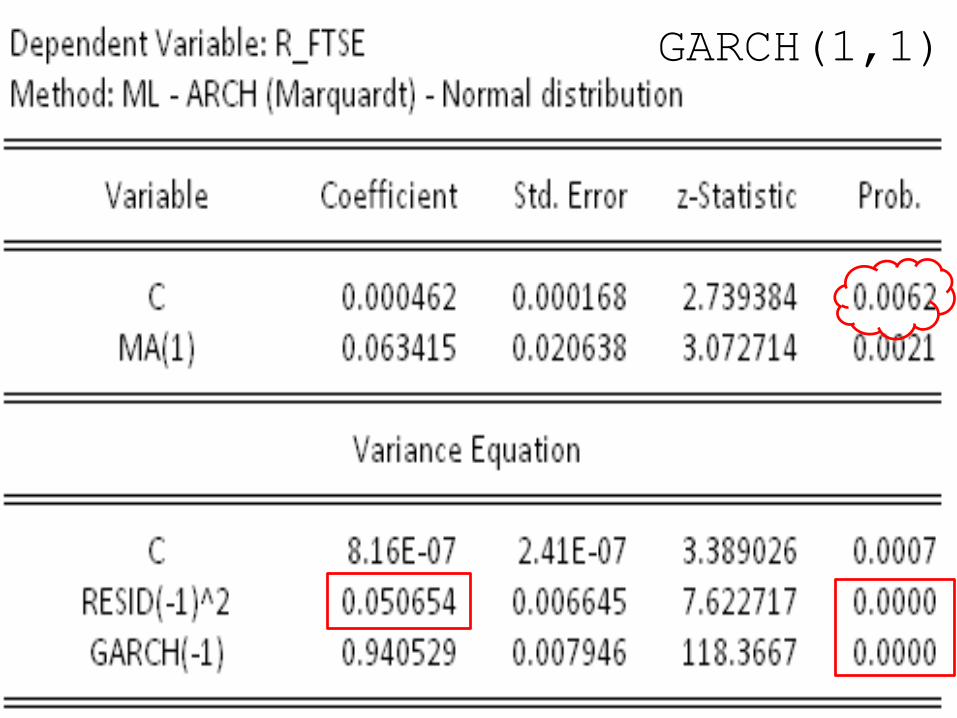

An example: FTSE volatility

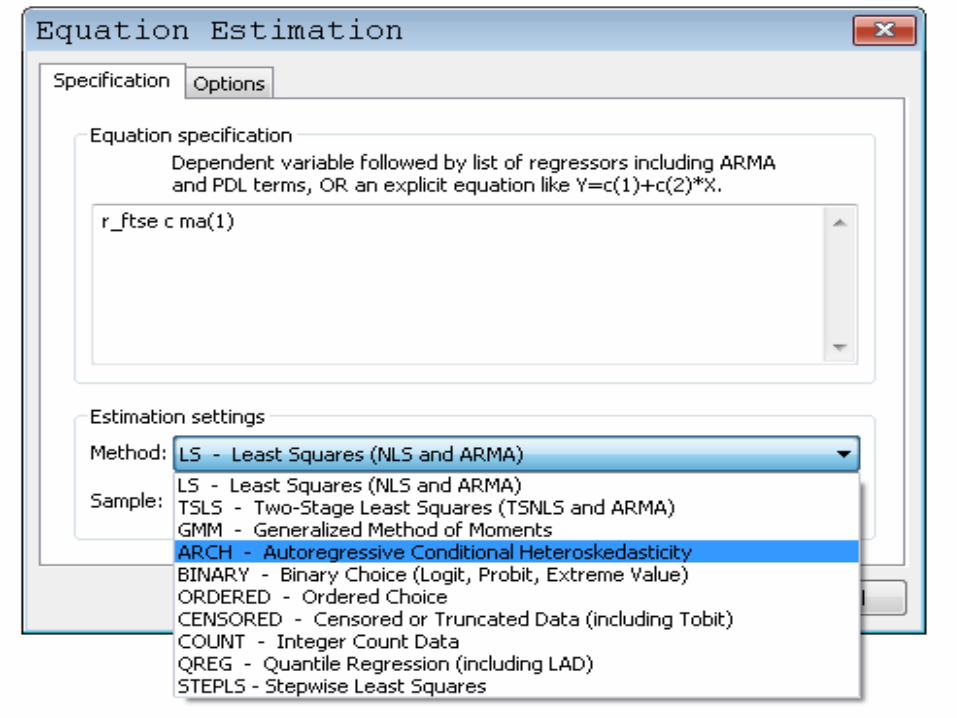

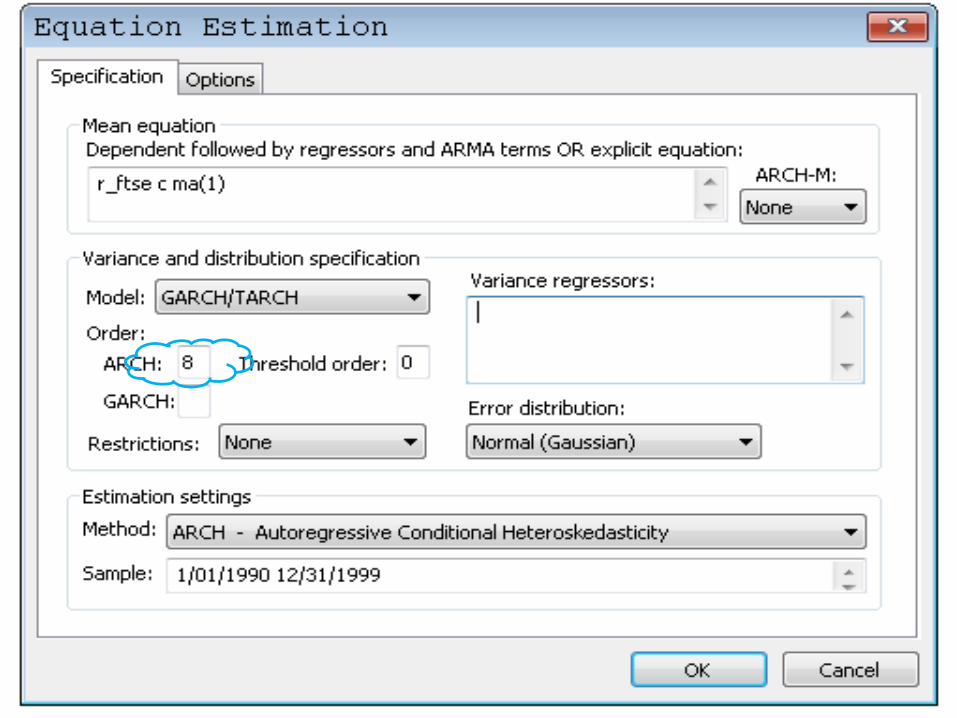

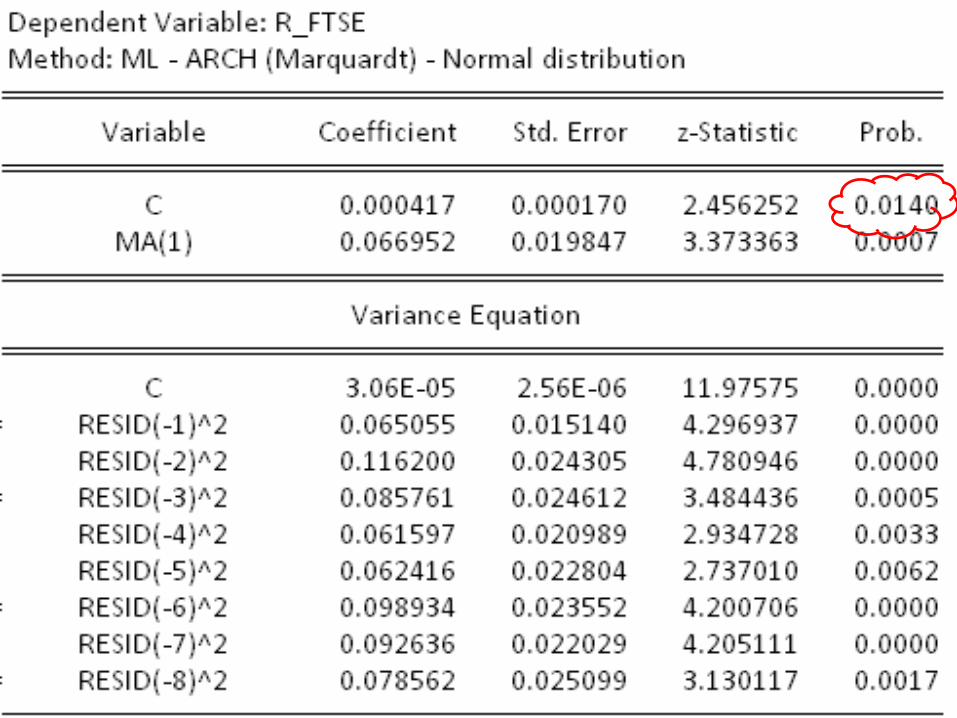

▪ Suppose the series FTSE follows

ARIMA(0,1,1) model:

.0000

.0001

.0002

.0003

.0004

.0005

.0006

.0007

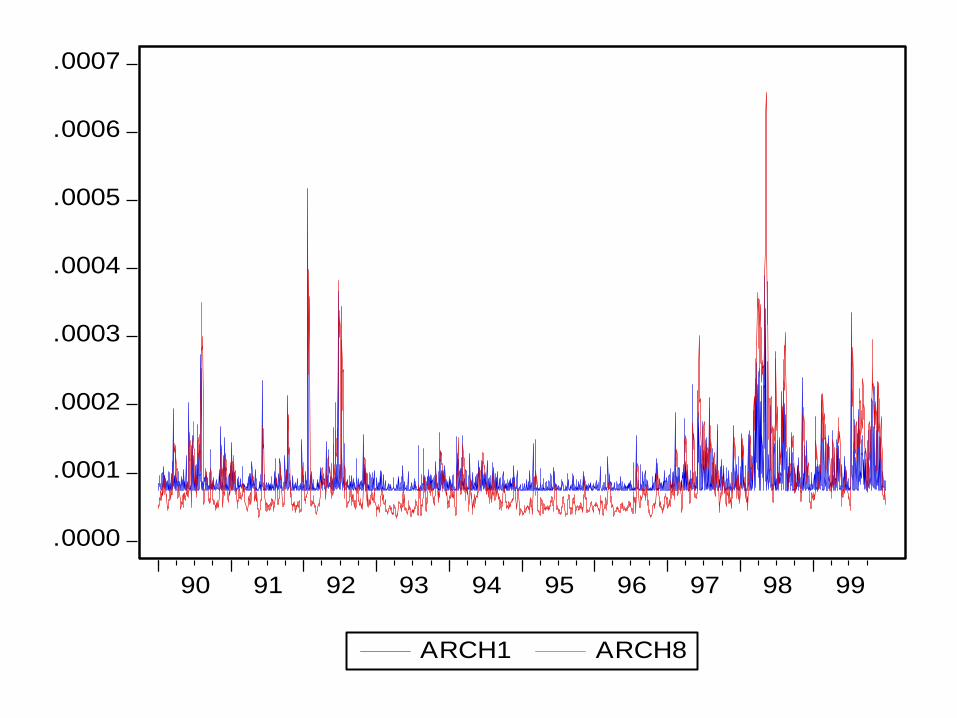

90 91 92 93 94 95 96 97 98 99

ARCH1 ARCH8

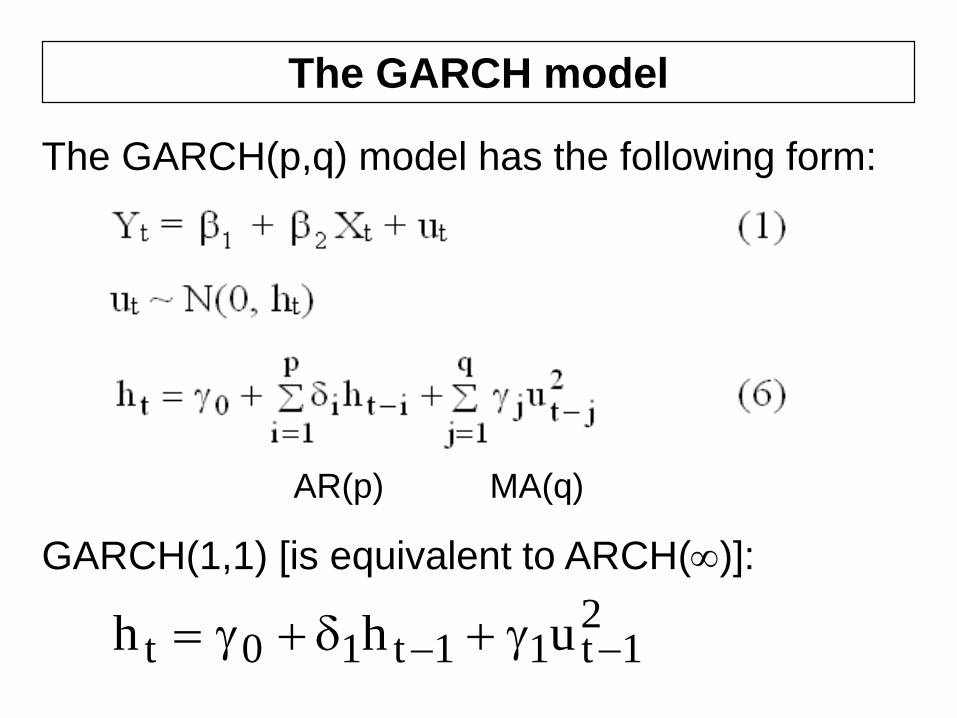

The GARCH model

The GARCH(p,q) model has the following form:

GARCH(1,1) [is equivalent to ARCH()]:

21t11t10t uh h

AR(p) MA(q)

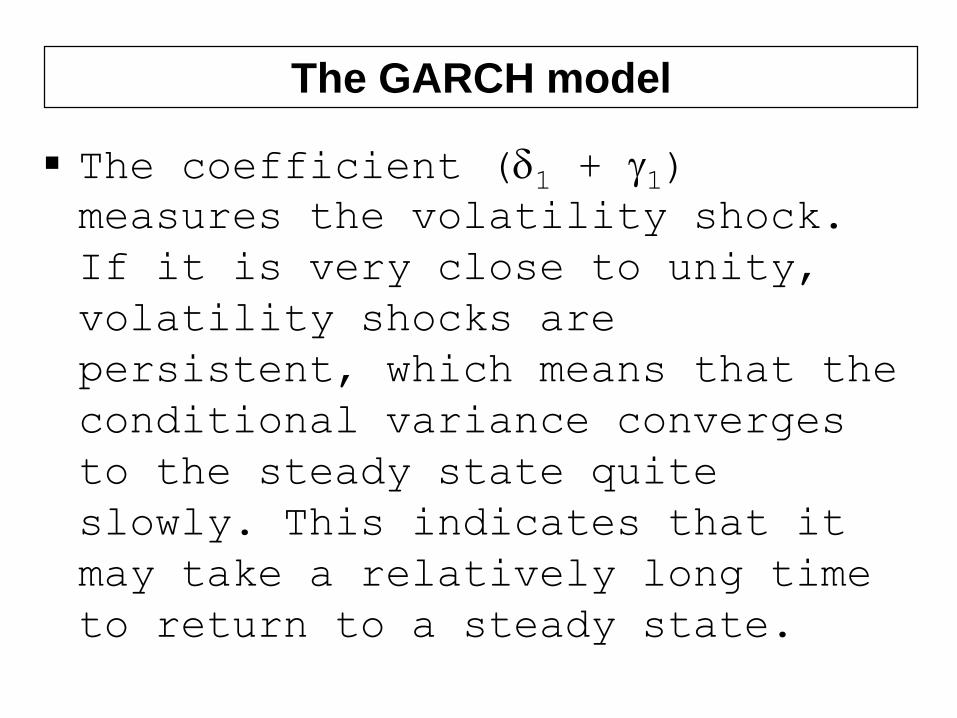

▪ The coefficient (1 + 1)

measures the volatility shock.

If it is very close to unity,

volatility shocks are

persistent, which means that the

conditional variance converges

to the steady state quite

slowly. This indicates that it

may take a relatively long time

to return to a steady state.

The GARCH model

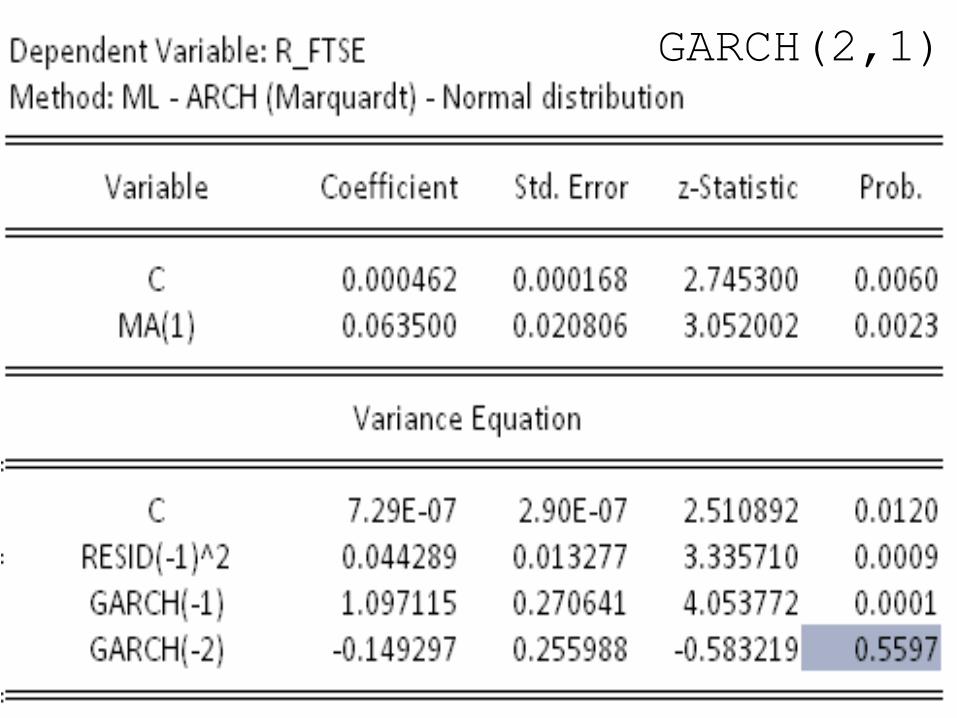

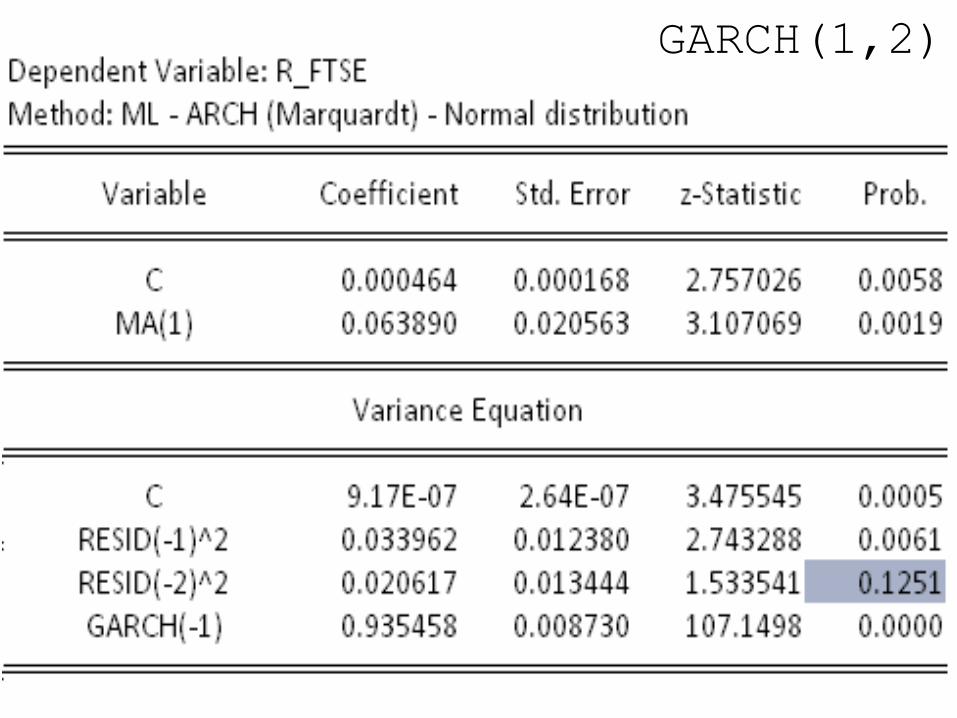

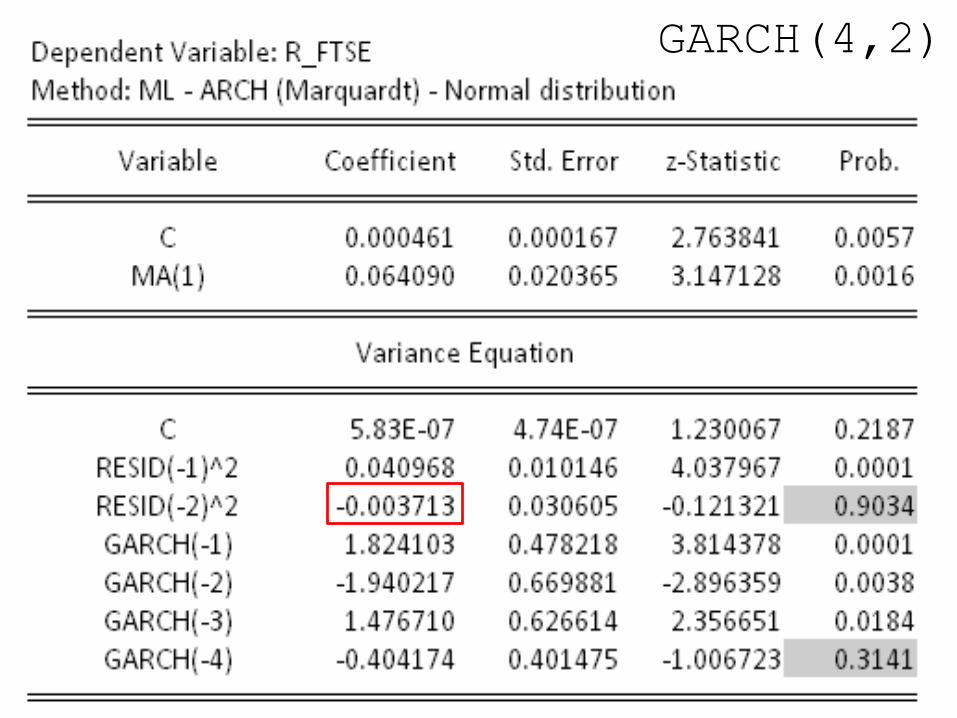

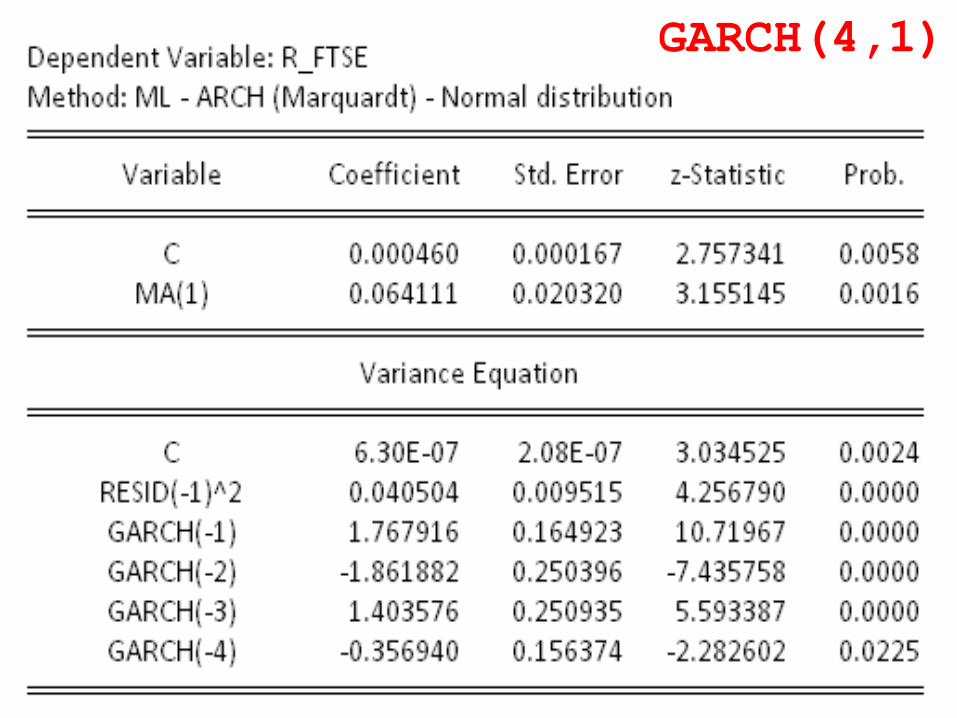

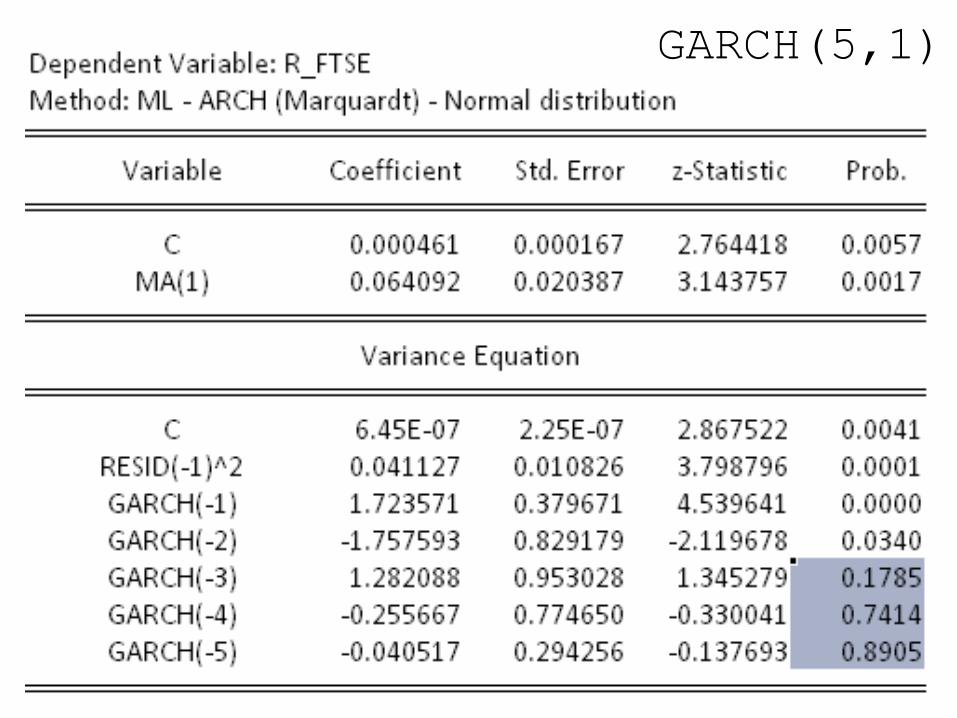

GARCH(1,1)

GARCH(2,1)

GARCH(1,2)

GARCH(3,2)

GARCH(4,2)

GARCH(4,1)

GARCH(5,1)

.0000

.0001

.0002

.0003

.0004

.0005

.0006

.0007

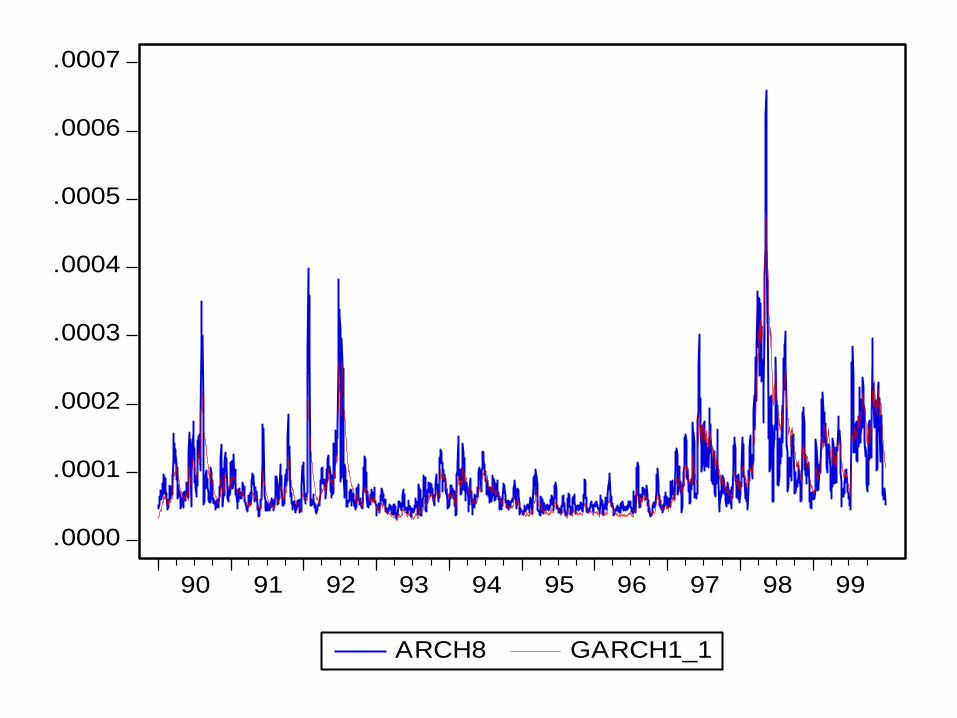

90 91 92 93 94 95 96 97 98 99

ARCH8 GARCH1_1

.0000

.0001

.0002

.0003

.0004

.0005

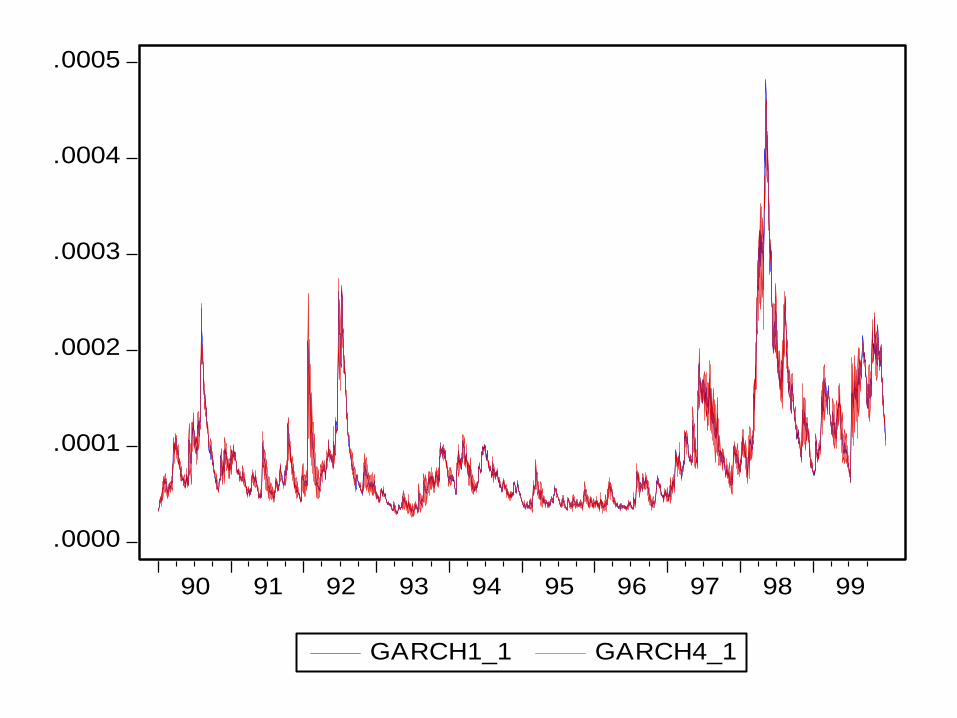

90 91 92 93 94 95 96 97 98 99

GARCH1_1 GARCH4_1

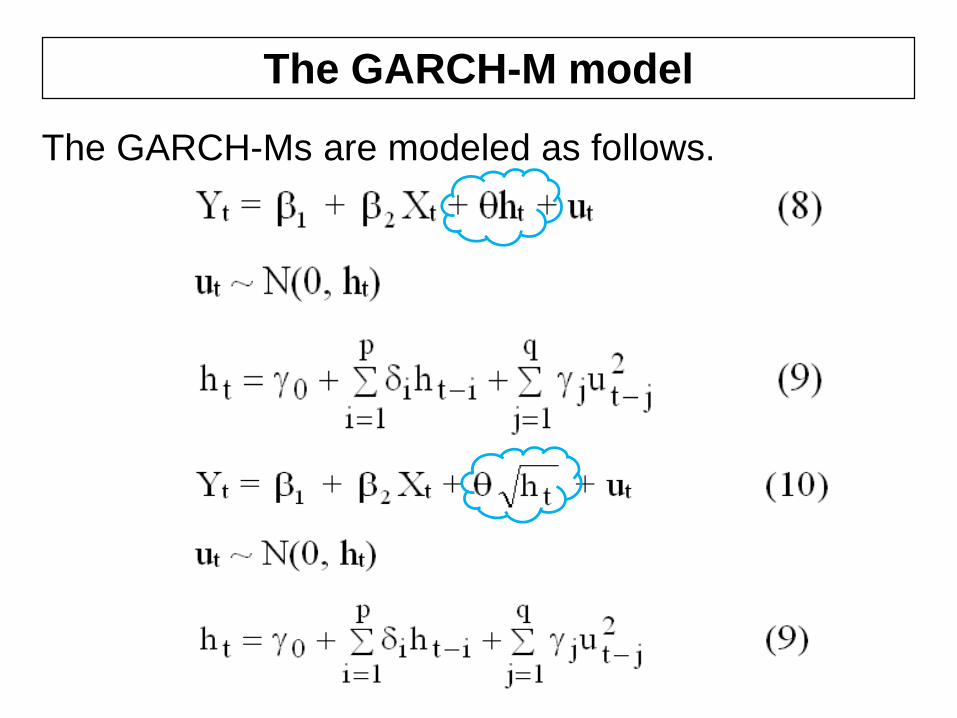

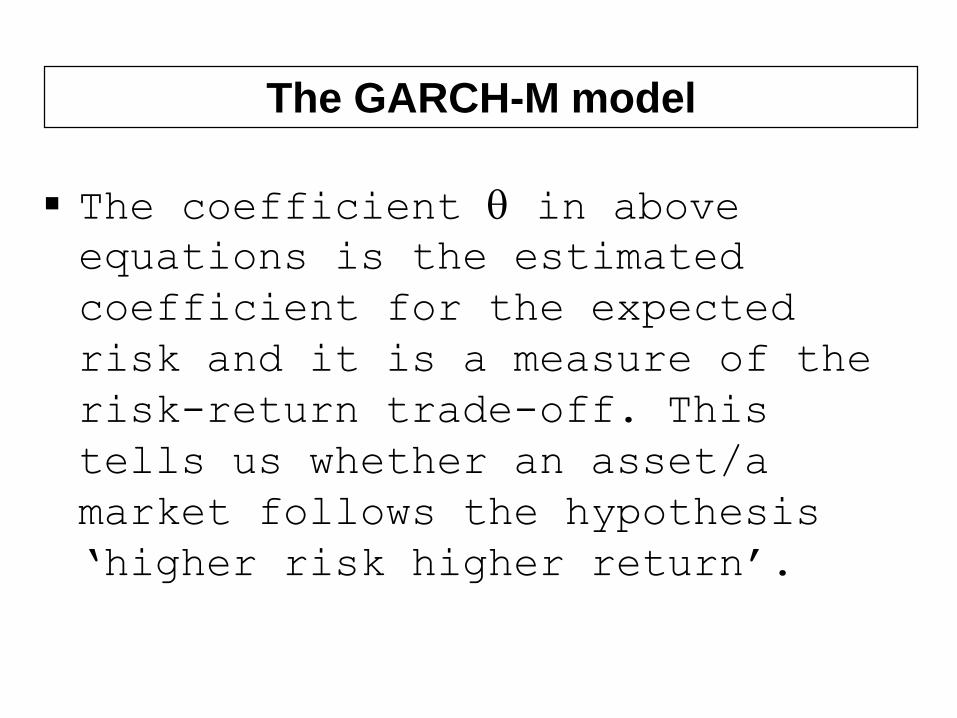

The GARCH-M model

The GARCH-Ms are modeled as follows.

▪ The coefficient in above

equations is the estimated

coefficient for the expected

risk and it is a measure of the

risk-return trade-off. This

tells us whether an asset/a

market follows the hypothesis

‘higher risk higher return’.

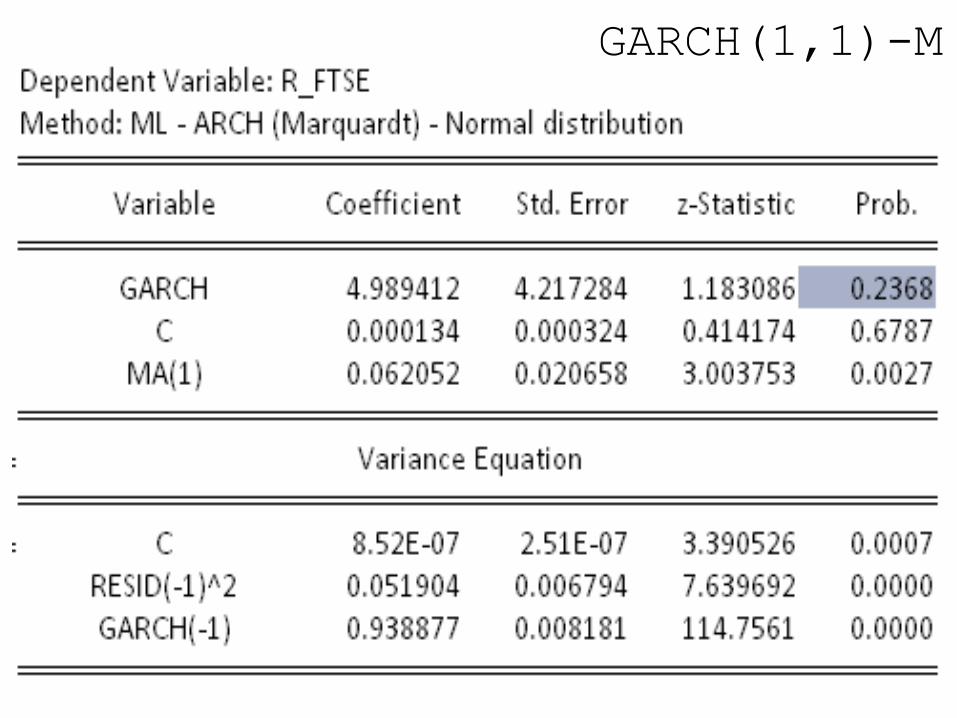

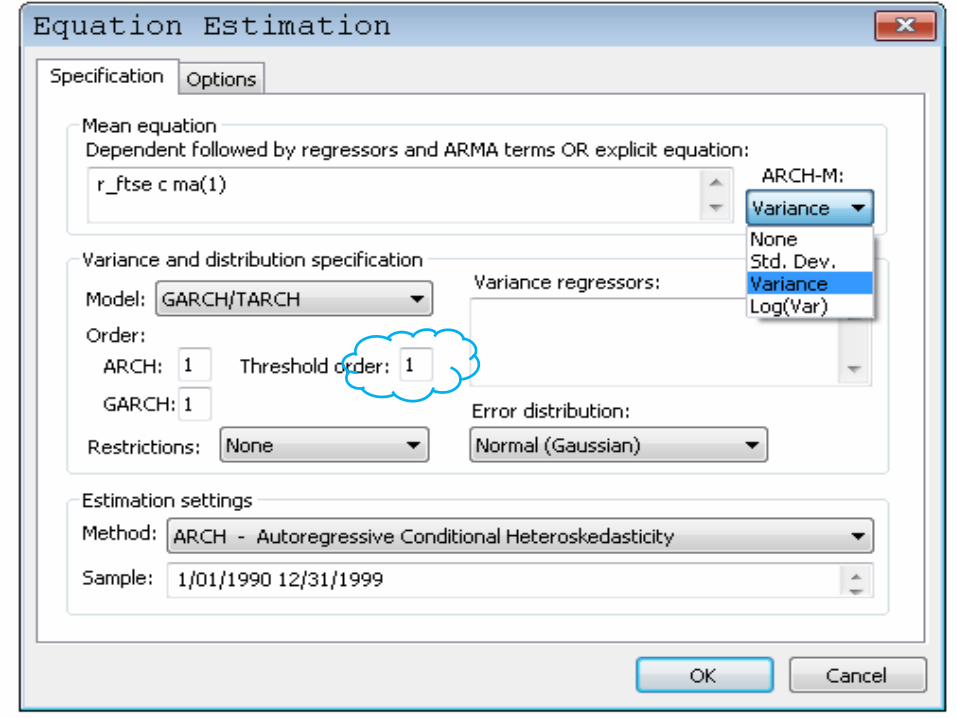

The GARCH-M model

GARCH(1,1)-M

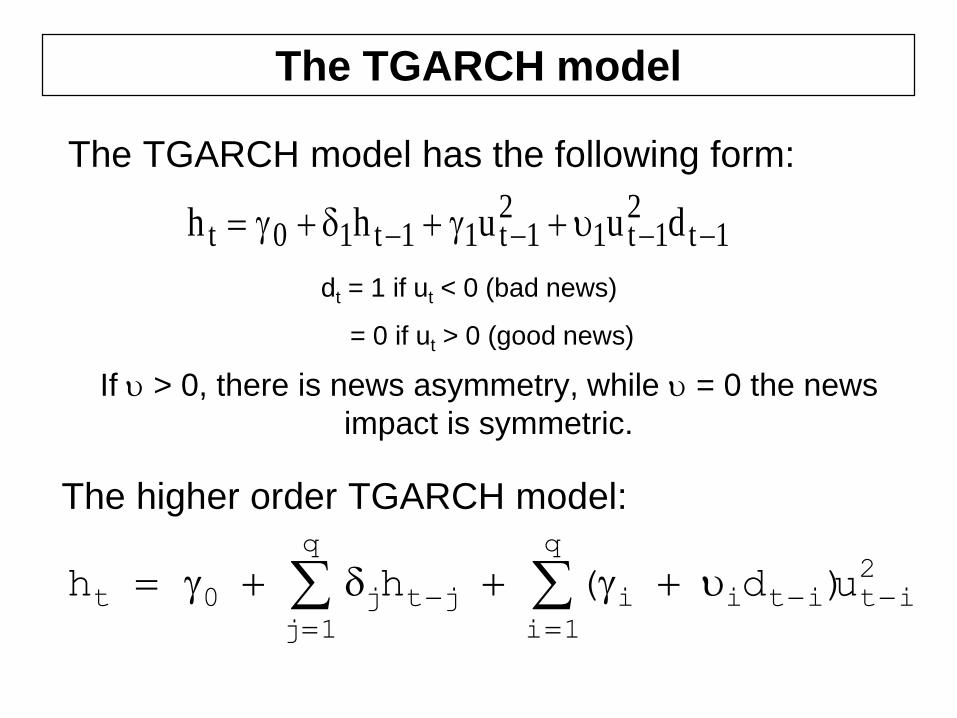

The TGARCH model

1t2

1t12

1t11t10t duuh h

The TGARCH model has the following form:

If > 0, there is news asymmetry, while = 0 the news

impact is symmetric.

The higher order TGARCH model:

2

it

q

1i

itiijt

q

1j

j0t u)d(h h

dt = 1 if ut < 0 (bad news)

= 0 if ut > 0 (good news)

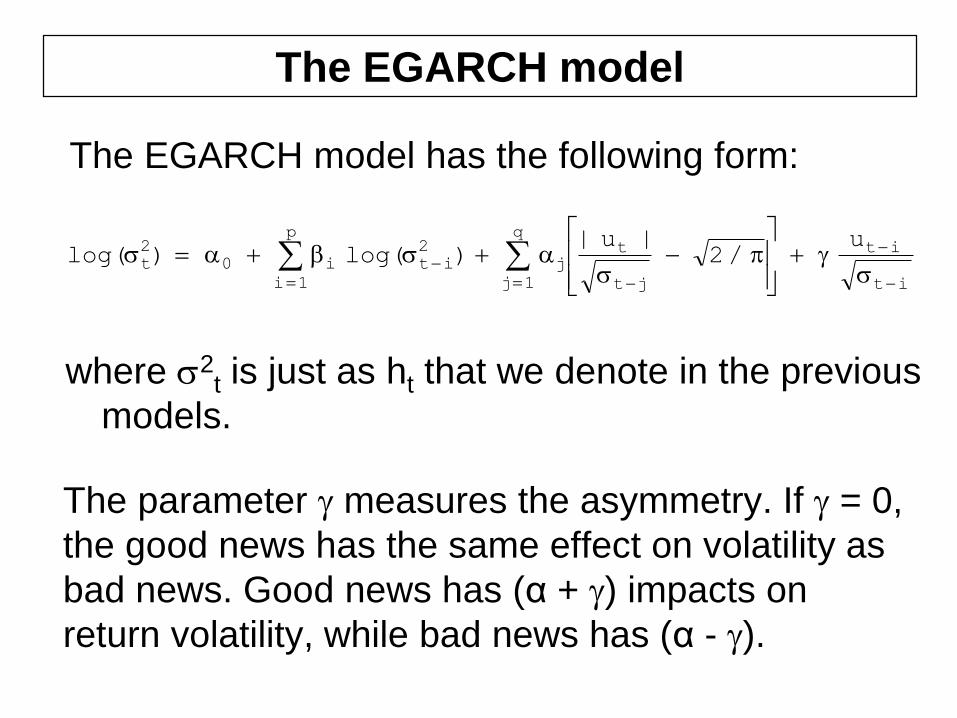

The EGARCH model

The EGARCH model has the following form:

it

it

jt

tq

1j

j

2

it

p

1i

i0

2

t

u/2

|u|)log()log(

where 2t is just as ht that we denote in the previous

models.

The parameter measures the asymmetry. If = 0,

the good news has the same effect on volatility as

bad news. Good news has (α + ) impacts on

return volatility, while bad news has (α - ).

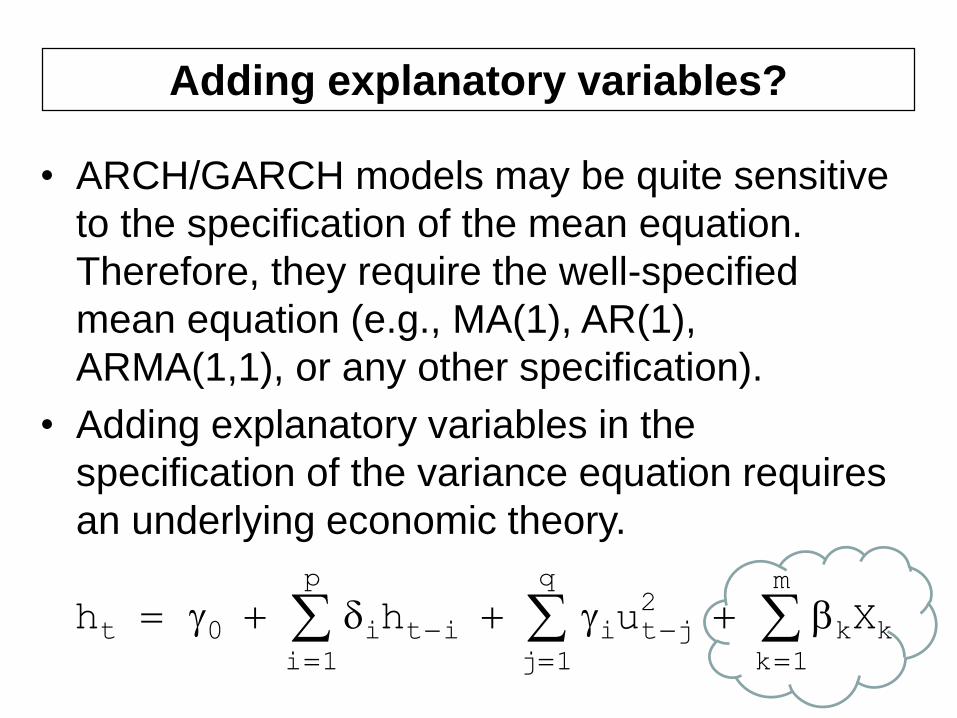

• ARCH/GARCH models may be quite sensitive

to the specification of the mean equation.

Therefore, they require the well-specified

mean equation (e.g., MA(1), AR(1),

ARMA(1,1), or any other specification).

• Adding explanatory variables in the

specification of the variance equation requires

an underlying economic theory.

Adding explanatory variables?

k

m

1k

k

2

jt

q

1j

iit

p

1i

i0t Xuh h

• The above models are univariate ARCH-type models. For

doing research, it’s better to use multivariate GARCH

(MGARCH) models. These models have various

applications:

• Volatility of a market leads to volatility of other markets.

• Volatility of an asset leads to volatility of other assets.

• Shock on a market increases the volatility on another

market.

• Impact of volatility in financial markets on real economic

variables.

• The computation of time-varying hedge ratios.

• The estimation of time-varying beta coefficient in asset

pricing models, etc.

Multivariate GARCH model