argus fmb nitrogen...2012/09/27 · bcic awards 187,500t of urea ethiopia to tender for 100,000t of...

TRANSCRIPT

Copyright © 2012 Argus Media Ltd

Argus FMB NitrogenFormerly FMB Weekly Nitrogen Report

price guidemarket summary

Market stable to firmUrea prices have changed little over the past week, but the outlook remains firm heading into Q4. Yuzhny urea traded down to $382/t fob as suppliers sold for prompt loading to clear stocks, but that level should represent the floor for prices in October and probably for Q4 as a whole.

An Egyptian tender for granular urea saw a price $3/t lower than last week, at $459/t fob, reflecting the difficulty of raising prices in the European market. The US market is firm for the nearby as the closure date for the Upper Mississippi approaches, but is weaker for October-November and will not support Egyptian prices at present.

The start up date of the new plant in Algeria remains shrouded in uncertainty and has pushed OCI into the market to buy granular urea to cover sales in Europe, lending support to prices. This situation may be repeated in October, but will not last for ever.

The prilled urea market has shrugged off the failure of the Indian tender to secure any worthwhile quantities. The counterbid by STC was too low to be of interest: traders reckon that a new tender will be issued very soon and that India will have to pay up to buy the large tonnage of urea it needs. Moreover, in an unexpected twist, another Indian buyer stepped in for 200,000t of Chinese urea to cover an old tender award dating from March this year.

An Argus Media company View the methodology used to assess nitrogen prices at www.argusmedia.com/methodology. Your feedback is always welcome at [email protected]

argus FmB Nitrogen

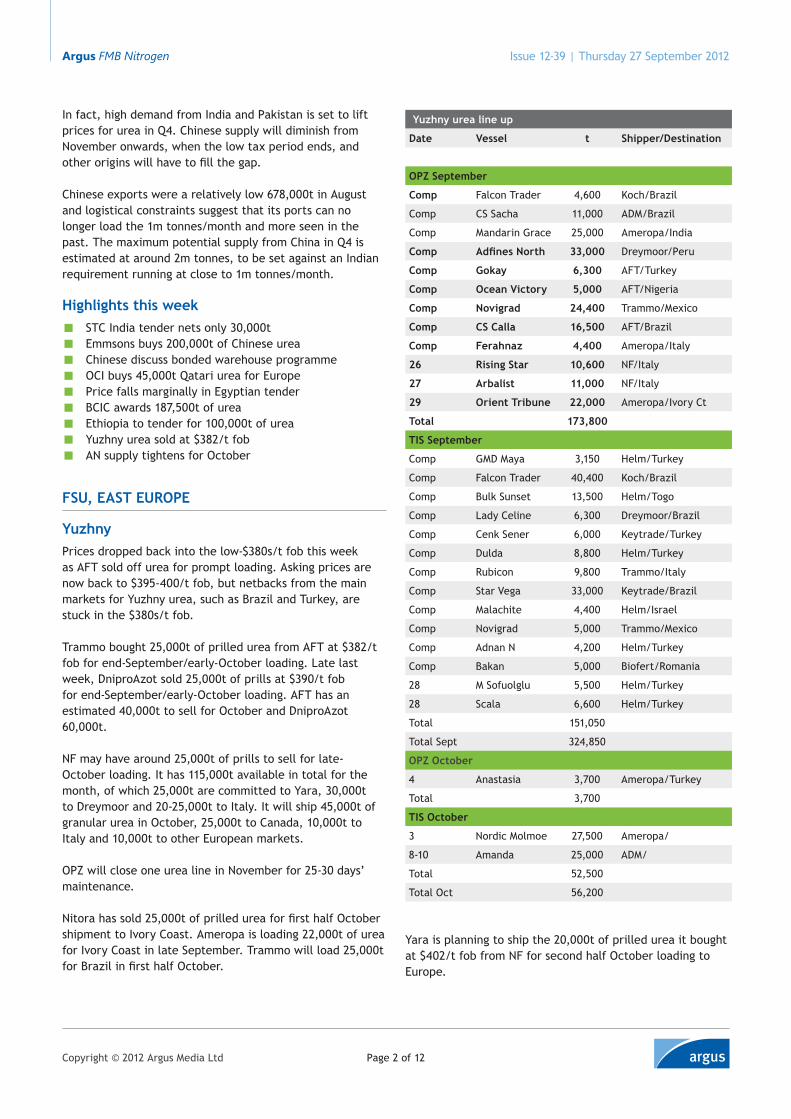

argus NitrOgeN iNdeX

Issue 12-39 | Thursday 27 September 2012

FMB nitrogen fertilizer price guide

27-sep 20-sep

Prilled urea – fob bulkYuzhny 382-390 380-402Baltic 385-390 390-395Croatia/Romania 412-417 410-415Arabian Gulf 390-395 390-395Arabian Gulf (fob bagged) 400-405 400-405China 375-377 370-380Brazil (cfr) 414-418 415-418Granular urea – fob bulkArabian Gulf all netbacks 415-454 385-452Arabian Gulf – US netback* 434-454 446-452Arabian Gulf – non US netbacks 415-423 385-423Iran 380-385 370-375Egypt 459 445-462Indonesia/Malaysia 410-437 437-449Southeast Asia (cfr) 425-430 420-430Venezuela/Trinidad 415-438 425-456US Gulf (pst barge) 422-440 433-439US Gulf (cfr metric) 460-480 472-478* Basis 35-45,000t freightAmmonium sulphate – bulkfob Baltic (Caprolactam) 235-238 230-235fob Blk Sea (Caprolactam) 235-240 230-235fob Kherson (steel grade) 200-203 192-195cfr S.E. Asia 238-240 238-240Ammonium nitratefob bulk Baltic 295-305 280-290fob bulk Black Sea 305-310 275-280UAN (32%)Nola (short ton) 305-308 295-305Rouen 30% N fot (€ Euros) 246-247 245-248fob Black Sea 303-305 300-305Argus nitrogen indexArgus nitrogen index 278.382 275.946* Composite based on Argus FMB assessments for a basket of nitrogen-based fertilizers. The index is calculated such that 3 January 2009 = 100 for each component class of fertilizers.

iNdeX rises 2.5 ON Firmer urea/aN/as prices

100

150

200

250

300Argus Nitrogen Index

Copyright © 2012 Argus Media Ltd Page 2 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

In fact, high demand from India and Pakistan is set to lift prices for urea in Q4. Chinese supply will diminish from November onwards, when the low tax period ends, and other origins will have to fill the gap.

Chinese exports were a relatively low 678,000t in August and logistical constraints suggest that its ports can no longer load the 1m tonnes/month and more seen in the past. The maximum potential supply from China in Q4 is estimated at around 2m tonnes, to be set against an Indian requirement running at close to 1m tonnes/month.

Highlights this week

▪ STC India tender nets only 30,000t

▪ Emmsons buys 200,000t of Chinese urea

▪ Chinese discuss bonded warehouse programme

▪ OCI buys 45,000t Qatari urea for Europe

▪ Price falls marginally in Egyptian tender

▪ BCIC awards 187,500t of urea

▪ Ethiopia to tender for 100,000t of urea

▪ Yuzhny urea sold at $382/t fob

▪ AN supply tightens for October

Fsu, east eurOpe

yuzhnyPrices dropped back into the low-$380s/t fob this week as AFT sold off urea for prompt loading. Asking prices are now back to $395-400/t fob, but netbacks from the main markets for Yuzhny urea, such as Brazil and Turkey, are stuck in the $380s/t fob.

Trammo bought 25,000t of prilled urea from AFT at $382/t fob for end-September/early-October loading. Late last week, DniproAzot sold 25,000t of prills at $390/t fob for end-September/early-October loading. AFT has an estimated 40,000t to sell for October and DniproAzot 60,000t.

NF may have around 25,000t of prills to sell for late-October loading. It has 115,000t available in total for the month, of which 25,000t are committed to Yara, 30,000t to Dreymoor and 20-25,000t to Italy. It will ship 45,000t of granular urea in October, 25,000t to Canada, 10,000t to Italy and 10,000t to other European markets.

OPZ will close one urea line in November for 25-30 days’ maintenance.

Nitora has sold 25,000t of prilled urea for first half October shipment to Ivory Coast. Ameropa is loading 22,000t of urea for Ivory Coast in late September. Trammo will load 25,000t for Brazil in first half October.

Yara is planning to ship the 20,000t of prilled urea it bought at $402/t fob from NF for second half October loading to Europe.

yuzhny urea line up

date Vessel t shipper/destination

OPZ September

Comp Falcon Trader 4,600 Koch/Brazil

Comp CS Sacha 11,000 ADM/Brazil

Comp Mandarin Grace 25,000 Ameropa/India

Comp Adfines North 33,000 Dreymoor/Peru

Comp gokay 6,300 AFT/Turkey

Comp Ocean Victory 5,000 AFT/Nigeria

Comp Novigrad 24,400 Trammo/Mexico

Comp cs calla 16,500 AFT/Brazil

Comp Ferahnaz 4,400 Ameropa/Italy

26 rising star 10,600 NF/Italy

27 arbalist 11,000 NF/Italy

29 Orient tribune 22,000 Ameropa/Ivory Ct

total 173,800

TIS September

Comp GMD Maya 3,150 Helm/Turkey

Comp Falcon Trader 40,400 Koch/Brazil

Comp Bulk Sunset 13,500 Helm/Togo

Comp Lady Celine 6,300 Dreymoor/Brazil

Comp Cenk Sener 6,000 Keytrade/Turkey

Comp Dulda 8,800 Helm/Turkey

Comp Rubicon 9,800 Trammo/Italy

Comp Star Vega 33,000 Keytrade/Brazil

Comp Malachite 4,400 Helm/Israel

Comp Novigrad 5,000 Trammo/Mexico

Comp Adnan N 4,200 Helm/Turkey

Comp Bakan 5,000 Biofert/Romania

28 M Sofuolglu 5,500 Helm/Turkey

28 Scala 6,600 Helm/Turkey

Total 151,050

Total Sept 324,850

OpZ October

4 Anastasia 3,700 Ameropa/Turkey

Total 3,700

tis October

3 Nordic Molmoe 27,500 Ameropa/

8-10 Amanda 25,000 ADM/

Total 52,500

Total Oct 56,200

Copyright © 2012 Argus Media Ltd Page 3 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

tuapseEurochem will load 15,000t of granular urea and 15,000t of prilled urea in Tuapse for the US in October. It has also sold 25,000t of prills for shipment to West Africa (carryover from end September), 12,000t to Romania\Bulgaria and will supply 8,000t to Ukraine by rail .

RomaniaInteragro has sold prilled urea for October at $412-417/t fob Constantza. Prices have moved up during the week. Several traders are inquiring for urea for Turkey and other Med destinations.

Interagro is selling most of the output from its Turnu Magurele plant into Central Europe, moving up the Danube

by barge and giving higher netbacks. It is loading an average of 3,000t/day on barges.

BaLtic

Prices are in the range $385-390/t fob, with traders obliged to pay the top end of the range for full cargoes.

sBu azot - Has sold 25,000t of prilled urea to Indagro at $390/t fob for early-October shipment.

Eurochem - Has committed 72,000t of granular urea for October shipment from Klaipeda as follows:

5,000t to Ameropa for the UK12,000t to the Netherlands for sale from its terminal at Terneuzen30,000t to Canada for mid-October shipment25,000t to Canada for second half October shipment

In addition it has sold 9-10,000t of prilled urea for October shipment to Germany.

Eurochem fixed a vessel to load 25,000t of urea in Klaipeda prompt for Sillery and Hamilton, east coast Canada, at about $37/t.

Uralchem - Says it has one cargo of urea to sell for second half October loading.

phosagro - maintenance work on one plant has reduced availability of urea from Cherepovets in October and the two cargoes moving under frame agreements to Trammo and Keytrade will account for most of the tonnage available.

Baltic Urea Export Sales – September

supplier Buyer market ‘000t

Phosagro Keytrade Brazil ? 25

Phosagro Trammo 40

Agronova Trader Peru 6

SBU Azot Dreymoor Brazil 25

Trammo Europe 10

trader Europe 10

Uralchem Gavilon Brazil 27

Brazil 25

Eurochem trader Brazil 25

Grodno trader TBC 5

Biofert Nitron Peru 12

Ameropa sold via Yuzhny

total 211available 30-35

Bagging Terminal Management Bulk Handling Equipment Sales Consultancy Expediting

B U L K H A N D L I N G S P E C I A L I S T S

www.nectargroup.net Nectar Group Ltd Email: [email protected] Tel: +44 1708 386 555

Copyright © 2012 Argus Media Ltd Page 4 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

eurOpe

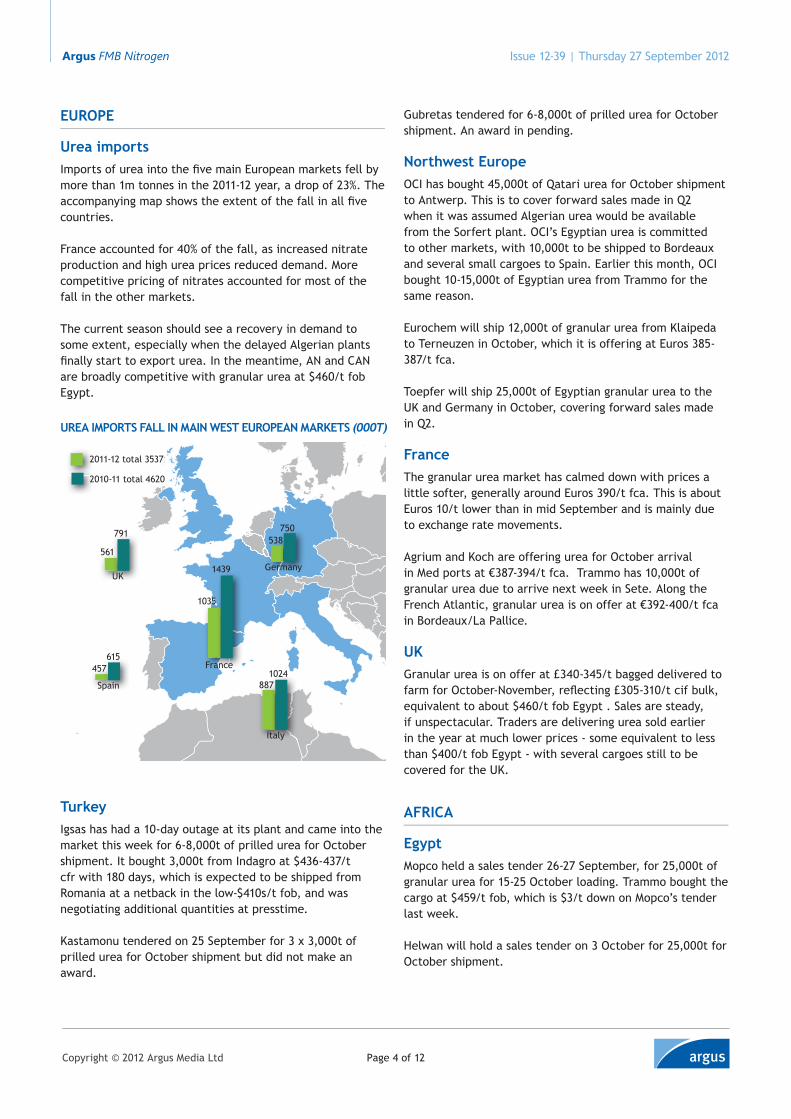

Urea importsImports of urea into the fi ve main European markets fell by more than 1m tonnes in the 2011-12 year, a drop of 23%. The accompanying map shows the extent of the fall in all fi ve countries.

France accounted for 40% of the fall, as increased nitrate production and high urea prices reduced demand. More competitive pricing of nitrates accounted for most of the fall in the other markets.

The current season should see a recovery in demand to some extent, especially when the delayed Algerian plants fi nally start to export urea. In the meantime, AN and CAN are broadly competitive with granular urea at $460/t fob Egypt.

urea impOrts FaLL iN maiN West eurOpeaN markets (000T)

1035

1439

France

538750

Germany

8871024

Italy

457615

Spain

561

791

UK

2011-12 total 3537

2010-11 total 4620

turkeyIgsas has had a 10-day outage at its plant and came into the market this week for 6-8,000t of prilled urea for October shipment. It bought 3,000t from Indagro at $436-437/t cfr with 180 days, which is expected to be shipped from Romania at a netback in the low-$410s/t fob, and was negotiating additional quantities at presstime.

Kastamonu tendered on 25 September for 3 x 3,000t of prilled urea for October shipment but did not make an award.

Gubretas tendered for 6-8,000t of prilled urea for October shipment. An award in pending.

Northwest europeOCI has bought 45,000t of Qatari urea for October shipment to Antwerp. This is to cover forward sales made in Q2 when it was assumed Algerian urea would be available from the Sorfert plant. OCI’s Egyptian urea is committed to other markets, with 10,000t to be shipped to Bordeaux and several small cargoes to Spain. Earlier this month, OCI bought 10-15,000t of Egyptian urea from Trammo for the same reason.

Eurochem will ship 12,000t of granular urea from Klaipeda to Terneuzen in October, which it is offering at Euros 385-387/t fca.

Toepfer will ship 25,000t of Egyptian granular urea to the UK and Germany in October, covering forward sales made in Q2.

FranceThe granular urea market has calmed down with prices a little softer, generally around Euros 390/t fca. This is about Euros 10/t lower than in mid September and is mainly due to exchange rate movements.

Agrium and Koch are offering urea for October arrival in Med ports at €387-394/t fca. Trammo has 10,000t of granular urea due to arrive next week in Sete. Along the French Atlantic, granular urea is on offer at €392-400/t fca in Bordeaux/La Pallice.

ukGranular urea is on offer at £340-345/t bagged delivered to farm for October-November, refl ecting £305-310/t cif bulk, equivalent to about $460/t fob Egypt . Sales are steady, if unspectacular. Traders are delivering urea sold earlier in the year at much lower prices - some equivalent to less than $400/t fob Egypt - with several cargoes still to be covered for the UK.

aFrica

egyptMopco held a sales tender 26-27 September, for 25,000t of granular urea for 15-25 October loading. Trammo bought the cargo at $459/t fob, which is $3/t down on Mopco’s tender last week.

Helwan will hold a sales tender on 3 October for 25,000t for October shipment.

Copyright © 2012 Argus Media Ltd Page 5 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

LibyaOne ammonia plant is running at Marsa el Brega, but urea production will begin only in November as further work is required on the cooling system.

ethiopiaAISE will hold a tender on behalf of the ministry of agriculture on 2 October for 100,000t of urea, for shipment in four lots, two in November and two in December.

West africaBauche has purchased 25,000t of prilled from Nitora for early-October shipment from Yuzhny to Abidjan, Ivory Coast.

Keytrade is in the freight market for a 25,000t urea/MOP combination cargo loading in the Baltic for Dakar, Senegal.

middLe east

QatarQafco has sold 45,000t of granular urea to OCI at $423/t fob for October shipment to northwest Europe. This adds to an already heavy line up of contract shipments: Yara/US 100,000t; Yara/Thailand 50,000t; Yara/Brazil 45,000t; Yara/Philippines 15-20,000t; IPL/Australia 100,000t; Yara/South Africa 40,000t; 150,000t for Pakistan; and a possible cargo for New Zealand.

kuwaitNitron will load 25,000t of granular urea for Argentina in October. GPIC Bahrain will close its urea plant for turnaround in November.

OmanGavilon will load 45-50,000t of granular urea in Sohar 8-12 October for the US Gulf, bought a couple of weeks ago.

FertilFertil’s Ruwais plants began a 40-45 day turnaround this week. Exports will not resume until late November due to work to extend the loading facilities at Fertil’s berth.

asia

indiaSTC countered suppliers in its 20 September tender for urea at $390.97-394/t cfr but received no acceptances in that range. The counters were equivalent to break even cost from China and traders were not interested in selling at that level.

As a result, STC bought only 30,000t from ETA and a new tender is expected to close in the coming week for IPL. India has an urgent need for urea and prices will have to be higher in the next tender to ensure timely supplies.

middle east export sales

supplier Buyer/market ‘000t month

granular

sabic Thailand 50-60 Sept

Avail 240kt Australia 35-40 Sept

balance 0-15kt New Zealand 25 Sept

US 55 Sept

S Africa 30 Sept

Sudan 15 Sept

Bangladesh 15 Sept

Qafco Yara/US 100 Sept

Avail 400kt Australia 25 Sept

balance 55kt S Africa 25 Sept

Yara/Brazil 45 Sept

CHS/Pakistan 50 Sept

Indagro/Pakistan 100 Sept

pic Ameropa/Am 25 Sept

Avail 135kt Indagro/S Am 30 Sept

Balance 0kt Koch/Australia 30 Sept

Gavilon/US 45 Sept

Oman Toepfer/ 30 Sept

avail 110kt Koch/ 45 Sept

balance 0kt CHS/US 40

Fertil Sri Lanka 24 August

Avail 70kt Trammo/US 25 August

balance 0kt Bangladesh 24 August

prilled

sabic South Africa 15 Sept

Avail 50kt domestic 15 Sept

balance 3kt Bangladesh 15 Sept

Qafco India 20-25 Sept

Avail 75-80kt Bangladesh 24 Sept

balance 5-10kt Philippines 20 Sept

india - urea balance sheet april-august

2012-13 2011-12 % change

Production 8,915 9,056 -1.6Imports 1,734 2,549 -32.3Sales 10,866 11,297 -3.8Closing stock 172 228 -24.6

Copyright © 2012 Argus Media Ltd Page 6 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

In the meantime, Emmsons is to supply another 200,000t of urea under its award in IPL’s March tender. Emmsons has so far supplied 83,000t of Iranian urea against its contract for 500,000t with IPL at $387/t cfr. The latest 200,000t have been sourced in China and will be shipped in three vessels in October.

indian urea situationUrea supply is tight in India judging from the statistics for April-August issued by FAI. Closing stocks dropped to just 172,000t at the end of August, equivalent to less than one percent of annual usage.

Production is running at annual level of 21-22m tonnes. Sales in kharif were down 3-4% but are expected to have caught up some ground in September. Overall usage in 2012-13 should exceed 30m tonnes.

pakistanLatest estimates from NFDC put opening stocks for rabi 2012 at 440,000t of urea. Production in rabi is projected at 1.9m tonnes, based on the continued closure of plants on the SNGPL network and a 12% cutback on other units. Imports contracted to date are 300,000t, giving a total supply figure of 2.64m tonnes.

FMB Spot Sales Selection – 27 September 2012

product Origin supplier Buyer destination ’000t $pt bulk Shipment

prilled urea

China ETA STC India 30 390.97 cfr October

China Helm SE Asia 25 400-402 cfr October

China various Emmsons India 200 October

China trader India 30 377 fob October

Yuzhny AFT Trammo 25 382 fob Sept/Oct

Yuzhny DniproAzot trader 25 390 fob Sept/Oct

Yuzhny Nitora Bauche Ivory Coast 25 October

Baltic SBU Indagro 25 390 fob October

Baltic? Fertipar Brazil 25 410 cfr October

Romania Interagro trader Turkey 5-10 417.50 fob October

granular urea

Qatar Qafco OCI Europe 45 423 fob October

Kuwait Nitron Argentina 25 460 cfr October

Egypt Mopco Trammo 25 459 fob October

Indonesia Indevco Australia 30 October

China Keytrade Nidera Argentina 10-15 450 cfr Oct/Nov

China Desh BCIC Bangladesh 37.5 438.64 cfrlo Oct/Nov

China Wilson BCIC Bangladesh 12.5 452.87 cfrlo Oct/Nov

China Hydrocarbon BCIC Bangladesh 25 455.50 cfrlo Oct/Nov

China Olam BCIC Bangladesh 25 456.82 cfrlo Oct/Nov

China Desh BCIC Bangladesh 25 443.14 cfrlo Oct/Nov

China Olam BCIC Bangladesh 25 454.41 cfrlo Oct/Nov

China Wilson BCIC Bangladesh 12.5 456.67 cfrlo Oct/Nov

China Hydrocarbon BCIC Bangladesh 25 460.50 cfrlo Oct/Nov

aN

Russia Uralchem Brazil 20-25 325 cfr October

Amsul

Russia KuAz trader Brazil 10 240 fob November

Baltic Grodno trader Brazil 25 235 fob November

uaN

Russia Eurochem US 30 330-335 cfr October

Copyright © 2012 Argus Media Ltd Page 7 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

Rabi demand is forecast at about 3m tonnes, leaving a minimum shortfall of 360,000t to be covered by additional imports. In fact, the requirement could run as high as 600,000t due to the need to maintain some stocks and the possibility of further gas curtailments in winter.

BangladeshBCIC has made awards totalling 187,500t under its 3 September tenders for 2 x 100,000t of granular urea for shipment to Chittagong and Mongla. Awards are as follows, prices in $/t cfrlo.

chittagong - 100,000tDesh Trading China/Indo 37,500t $438.64Wilson Intl China/Egypt 12,500t $452.87Hydro Carbon China/Egy/Rus 25,000t $455.50Olam Intl China/M East 25,000t $456.82

mongla - 87,500tDesh Trading China/Indo 25,000t $443.14Olam Intl China/M East 25,000t $454.41Wilson Intl China/Egypt 12,500t $456.67Hydro Carbon China/Egy/Rus 25,000t $460.50

sri LankaThe Ministry of Agriculture closed a tender for 12,000t of bagged urea on 26 September. Offers were as follows, prices in $/t cfr bagged.

Sri Lanka - MoA Urea tender 26 September - 12,000t

supplier Origin cfr 180d cfr 270d

Agricom China/M East 437.78 442.08

Blue Deebaj Iran/Chi/CIS/Uzbek 444.96 451.44

Valency Uzbek 449.44 453.48

ETA China 459.97 464.97

Dragon Asia China 464.00 470.50

Swiss Singapore Chi/Iran/ME/Indo 472.00 479.00

chinaPrilled urea prices have risen this week as Emmsons stepped in to buy 200,000t of urea for October shipment to India, compensating to some extent for the disappointment of the STC tender. Sales took place at $375-378/t fob and asking prices have now moved above $380/t fob.

Emmsons has fixed the m/v Chanchal Prem to load about 80,000t and the m/v Vinalines Global to load about 60,000t. Freight for the Chanchal Prem is reported in the low-$10s/t. It is one of the largest vessels ever employed to ship fertilizer.

Port stocks of prilled urea are estimated at about 450,000t and granular at about 250,000t.

Asking prices for granular urea have moved above $400/t fob, with some suppliers indicating $410/t fob for October. Earlier this month prices bottomed out at $393-395/t fob. Fudao sold its September cargoes at $415/t fob but is seeking above $420/t fob for October.

Bonded warehouse programmeProducers are discussing deliveries of urea to bonded warehouses for export after the low tax period ends on 31 October. The level of interest outweighs the capacity of the main ports to handle urea and port authorities are screening customers. Interest is high because international prices are likely to move up in November-December.

It is estimated that about 1m tonnes of urea can be accommodated in bonded warehouses, mostly in Yantai (600,000t) and Bayuquan (200,000t). There is a limited time available to fill this capacity but, unlike last year, there are no rail restrictions as movement of other commodities, notably coal, is running at a lower level.

Urea exports were 678,000t in August, an increase of 38% on August 2011. Exports since the start of the low tax window in July total 1.03m tonnes, one third higher than last year. Some 300,000t of urea were loaded for India in August, Mexico took 85,000t, the US 65,000t, South Korea and the Philippines each took 51,000t.

chinese urea production 2012 - ‘000 tonnes

month NBs cNFia difference

Jan 5,254 4,791 463

Feb 5,352 4,602 750

Mar 5,167 4,728 439

Apr 5,372 4,800 572

May 5,693 4,728 965

June 5,809 4,890 919

July 5,613 4,790 823

Aug 6,404 4,832 1,572

ytd 44,665 38,162 6,503

china urea productionFigures from the National Bureau of Statistics show a huge increase in urea production in August, with monthly output estimated at 6.4m tonnes, the largest ever total and an increase of 38% over last year. However, there appears to be an error in the NBS figures as production in Xinjiang province is shown increasing by 750,000t over July. The nitrogen producers’ association, CNFIA, estimates August production at 4.8m tonnes of urea, 10.2% higher than in August 2011.

Copyright © 2012 Argus Media Ltd Page 8 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

2012 Argus FMB Europe Fertilizer Conference and Exhibition3-5 October, Madrid, Spain Register online here www.eventsforce.net/FMBEurope

thailandContract deliveries from Saudi Arabia, Qatar and Malaysia will cover demand for granular urea for October. Prices for Middle East urea remain in the $420s/t cfr. Heavy rain in the northeast has led to flooding, which may eventually affect the centre and south of the country, limiting demand.

philippinesYara will load 20,000t of mainly granular urea in Qatar for the Philippines in October.

indonesiaPusri cancelled a sales tender planned for 25 September for 60,000t of granular and 20,000t of prilled urea. A date for a new tender has still to be set.

Quantum will combine its last two purchases of granular urea and load 45,000t in Bontang for Australia in early October. Indevco has also sold the 30,000t of granular urea it bought in the last Pusri tender to Australia.

malaysiaThe PKF plant remains down for turnaround and is expected to resume production on schedule around 8 October. Petronas has only about 15,000t of granular urea for export to Thailand in October due to domestic market commitments and production lost from the turnaround. Netbacks on the sales to Thailand are in the range $410-415/t fob.

VietnamUrea imports were 59,000t in August, slightly less than half the tonnage imported in August 2011. Cumulative imports January-August were 325,000t, down from 555,000t in the first eight months of 2011.

americas

us Prices for prompt granular urea barges are firm in the range $437-440/st fob Nola for loading pre-river close. Trading has been limited due to a lack of barges on offer; most shippers are looking to move product before 5 October and the tonnage of urea available before then is small.

US gran urea imports from offshore

month Origin 000t Comments

July arrivals – all sources 105august 490September 688Gavilon Egypt 25CHS Oman 45Sabic S Arabia 60Yara Qatar 100CHS Kuwait 45 contractGavilon Bahrain 45 contractGavilon Kuwait 33 spotEurochem Russia 50Trammo Egypt 25Toepfer Oman 45CHS Indonesia 30Trammo China 25 Fudao cargoTrammo UAE 25PCS Trinidad 25Koch Oman 45Dreymoor China 40 west coastMarubeni China 25October 419Yara Qatar 100Sabic S Arabia 55Ameropa Kuwait 25Trammo China 50PCS Trinidad 50Koch Egypt 25Gavilon Bahrain 40Ameropa Indonesia 30 west coastCHS Oman 44November 340cHs Kuwait 45 spotSabic S Arabia 55Yara Qatar 100CHS Kuwait 45 contractGavilon Oman 45Eurochem Russia 15PCS Trinidad 35

ytd total 2042July-Nov 2011 1680change 362

Copyright © 2012 Argus Media Ltd Page 9 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

Post river close, deals have been concluded at $420-425/st fob Nola. Further out, prices for December firmed from $425/st fob Nola late last week to $428/st fob earlier this week.

Prices are higher for Q1, with traders asking prices of $445/st and above. One April barge was sold at $452/st fob Nola. Heavy demand for spring 2013 should lead to a pick up in buying from December onwards. Buyers waited too long to step in for spring 2012 and most will aim to avoid the additional costs associated with waiting too long again.

egyptiaN prices tOO HigH FOr tHe us

400

420

440

460

480

500

520US Gulf Egypt

According to our calculations, offshore granular urea imports are running close to 400,000t ahead of last year for July-November. The latest additions to the list are a 45,000t Omani cargo for Gavilon and a 15,000t part cargo from Eurochem. Chinese granular cargoes may be added to the line up for November arrival as traders are bidding for Fudao tonnage at present.

Two more nitrogen projects announcedAdding to the growing list of ammonia/urea projects planned for North America, Ohio Valley Resources (OVR) announced this week that it intends to build a new $1bn nitrogen plant in Spencer County, Indiana. KBR will provide the ammonia process production units while Weatherly, Inc will supply the design on the UAN plant. Capacity is expected to be 2,420st/day ammonia and 3,000st/day UAN. Expected completion is in 2016.

Also, Farmers of North America (FNA) are seeking investment for a new nitrogen plant in Canada, according to Grainews. FNA does not intend to own the plant. It announced on Wednesday the launch of Fertilizer Limited Partnership, which is leading “ProjectN” – the efforts of FNA to see a new plant come to fruition.

ColombiaIncofe will next be in the market in October for a cargo of granular urea for December delivery to Buenaventura.

ecuadorFertisa received offers this week for a combination cargo of prilled urea and AN but had yet to make a decision at presstime.

chileAnagra is seeking 25,000t of granular urea for October shipment.

Brazil Prilled urea prices have firmed marginally this week. Traders have sold part cargoes at $414-415/t cfr for October shipment and bids for small lots have risen to $418/t cfr. There are, however, unconfirmed reports that Fertipar was able to buy a cargo at $410/t cfr early in the week.

Demand is estimated at around 700,000t of urea for the balance of the year, but sales are fairly slow at present.

argusmedia.com

For more information please contact our conference department at +7 495 933 75 71 or by email: [email protected]

Argus FMB FSU Regional Fertilizer Conference and Exhibition 201228–30 November, 2012, Bristol Hotel, Odessa, Ukraine

Book before 13 October and save €200

Registration Program request

Copyright © 2012 Argus Media Ltd Page 10 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

The granular urea market is becoming increasingly influenced by formula pricing. Since Yara started to offer monthly cargoes of Qatari urea on a Yuzhny-linked formula similar to that used by Profertil, other suppliers have begun to offer in the same way.

This has led to some low prices for granular. Based on the current FMB Yuzhny mid-point, plus freight of $29-31/t and a premium of $20-22/t, granular urea would be priced at $436-438/t cfr this week. Suppliers have been trying to sell at $455/t cfr on a fixed priced basis, but buyers will obviously prefer formula pricing.

argentina/uruguaySeveral granular urea cargoes have been booked or are under negotiation for October-December arrival, as shown below. Demand in Argentina is largely covered for this year and Profertil is embarking on its export programme for the period through to March/April.

Venezuela - around 15,000t of granular urea arrived in Montevideo, Uruguay, recently from Venezuela under a government-government deal. The urea is in the hands of Alcoles del Uruguay, which is not a regular fertilizer seller, and being offered at $470/t cfr equivalentprofertil - 10-15,000t are under negotiation for October shipment to Uruguay, based on a formula price. Profertil has indicated that it will load one cargo/month for Uruguay October through Aprilindagro - 15,000t sold in Uruguay from a Qatari vessel arriving around 10 October, the balance is likely to be sold in BrazilNitron - has sold 25,000t of Kuwaiti granular urea around $460/t cfr in Argentina for October shipment, plus 10,000t of Russian urea

keytrade - has sold 10-15,000t of Chinese granular urea in Argentina and Uruguay at $450/t cfr from a cargo for December arrival.

ammONium Nitrates/suLpHate

▪ OCI, Eurochem raise CAN prices for October

▪ GrowHow UK announces Q4 AN prices

▪ AN tight for October

▪ Abu Qir to retender UAN

Germany/NetherlandsOCI and Eurochem have announced a Euros 7/t increase in their CAN 27 list prices for October, taking the official level to Euros 265/t cif inland.

This is Euros 5/t lower than Yara’s October price. The Euros 10/t price increase announced by Yara last week has so far not been implemented and market prices have not moved up above Euros 260/t cif.

Distributors are suspicious about price developments this year and are unwilling to accept a large monthly increase that they cannot pass on to farmers.

FranceOther suppliers have responded to the AN price increase announced by Yara on 17 September and the major producers are now all between Euros 345 and 350/t bulk delivered.

Borealis followed suit announcing the same level as Yara of Euros 350/t. Borealis has announced that its Pec-Rhin plant will close for 12-15 days’ maintenance in October.

FMB Fertilizer Reports - now available on a dashboard

FMB has launched the world’s first dashboard for international fertilizer markets. The new dashboard facility is available for all our weekly reports, phosphates, nitrogen, sulphur, ammonia and potash. Subscribers can define their own online list of key prices, set up graphs and create feeds of relevant news. Dashboard users have access to historical price data and can set up email alerts to receive automatic reminders with market updates and price news. Subscrib-ers can set up multiple dashboards to create windows into different markets, or compare trends for two or more types of fertilizer.

argusmedia.com/fertilizer

For more information or to request an online demonstration email us at [email protected]

Copyright © 2012 Argus Media Ltd Page 11 of 12

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

Eurochem is understood to be at Euros 345/t. GPN earlier declared a new price of Euros 345/t, but several customers report limited quantities available at this new level, and some backlog in deliveries.

ukGrowHow announced new prices for AN 34.5 on 27 September as follows, prices are for AN in bags delivered to merchant:

£291/t October£296/t November£301/t December

This is up from £289/t in September and £285/t for most of the summer. The increases are relatively modest and merchants expect to be able to pass them on to farmers. The UK price for October is around Euros 10/t lower than the Yara AN price in France.

Black sea/BalticAN is tight from the main Russian and Ukrainian suppliers, with few offers in the market. Prices are put at $305-310/t fob for October, but producers will seek higher for November.

NF is sold out on AN for October and says it has sold 25,000t for early-November shipment. Production of AN has been reduced at Gorlovka in favour of ammonia exports and is also cutback at Cherkassy.

Eurochem has committed 140,000t of AN for October as follows:

Russian market - 110,000tLithuania – 10,000tLatvia – 5,000t Ukraine – 15,000t

No additional exports are planned for the month and Eurochem is telling traders that it is unlikely to sell for deep sea export in Q4.

Amsul prices are firm in the range $235-240/t fob. Kuaz is claiming a sale at $240/t fob for end-November and a trader bought 25,000t from Grodno at $235/t fob in its most recent sale.

BulgariaAgropolychim has restarted production at its plant at Varna following conversion from stabilised to straight AN. The plant can produce about 30,000t/month of AN, of which 80% will be used to supply the domestic market in Q4.

BrazilRecent AN business has taken place at $325/t cfr, with Uralchem reported to have sold a cargo at that level for October shipment.

The line up of vessels waiting to discharge at Paranagua has diminished following a quiet period for new purchases. There are seven vessels either berthed or waiting to discharge at the port with a total of 129,000t of AN.

Far eastCapro Corp held a sales tender on 27 September for 25,000t of amsul for October shipment to the Americas. Bids are reported in the high-$230s/t fob.

uaN

usThe Nola market is quiet, although price indications have firmed slightly on improved sentiment for the spring season and the urea market. There is still a standoff between buyers and sellers with buyers more interested in levels around $290-300/st fob Nola and buyers more solidly at $310-315/st fob Nola, hence the range this week is assessed at $305-308/st fob Nola.

Prices on the east coast are in the range $330-335/t cfr for October shipments.

FranceOffer prices for UAN 30 are Euros 247/t fca Rouen and Euros 245/t fca Ghent for October, having firmed a little since mid September. Demand from farmers is light and distributors have stopped buying temporarily.

russiaEurochem has committed 88,000t of UAN 32 for export in October as follows:

25,000t to Canada loading in Klaipeda33,000t to Australia loading in Novorossisk30,000t to the US (Nola and/or US Gulf) from Novorossisk

RomaniaInteragro sold 25,000t of UAN 32 to a trader late last week at $305/t fob for October loading. Asking prices are now around $310/t fob for the remaining October tonnage.

Koch will load a cargo for Rouen in the first week of October and Gavilon has 25,000t to load for the US later in October.

Fertilizer

Argus FMB Nitrogen Issue 12-39 | Thursday 27 September 2012

Registered officeArgus House, 175 St John St, London, EC1V 4LW Tel: +44 20 7780 4200 Fax: +44 870 868 4338 email: [email protected]

ISSN: 2050-3571copyright noticeCopyright © 2012 Argus Media Ltd. All rights reserved. All intellectual property rights in this publication and the information published herein are the exclusive property of Argus and/or its licensors and may only be used under licence from Argus. Without limiting the foregoing, by reading this publication you agree that you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatsoever without the prior written consent of Argus.

publisher:Adrian Binks

Chief operating officer:Neil Bradford

Global compliance officer:Jeffrey Amos

Commercial manager:Jo Loudiadis

editor in chief:Ian Bourne

managing editor:Cindy Galvin

editor:Stephen MitchellTel: +44 20 8979 [email protected]

Customer support and sales:email: [email protected]

London, ukTel: +44 20 7780 4200

moscow, russiaTel: +7 495 933 7571

singaporeTel: +65 6496 9966

tokyo, JapanTel: +81 3 3561 1805

argus media inc, Houston, usTel: +1 713 968 0000

argus media inc, Washington dc, usTel: +1 202 775 0240

Argus FMB Nitrogen is published by Argus Media Ltd.

Trademark noticeARGUS, ARGUS MEDIA, the ARGUS logo, FMB, ARGUS FMB PHOSPHATES, other ARGUS publication titles and ARGUS index names are trademarks of Argus Media Ltd. Visit www.argusmedia.com/trademarks for more information.

DisclaimerThe data and other information published herein (the “Data”) are provided on an “as is” basis. Argus makes no warranties, express or implied, as to the accuracy, adequacy, timeliness, or completeness of the Data or fitness for any particular purpose. Argus shall not be liable for any loss or damage arising from any party’s reliance on the Data and disclaims any and all liability related to or arising out of use of the Data to the full extent permissible by law.

egyptAbu Qir held a sales tender on 25 September for 15,000t UAN for shipment 29 September-1 October. Bids were lower than anticipated, or not for the full quantity, so Abu Qir did not sell. It has issued a new tender closing on 2 October for 25,000t for 6-8 October loading.

2013 Argus FMB Asia Fertilizer Conference and Exhibtion24-26 April, Beijing, China Save the date! More details on the conference will be released shortly.

argusmedia.com/fertilizer-asia

FertiLiZer deriVatiVes

FIS Cash Settled swaps – 27 September 2012

month Bid Offer mid Basis

Urea (Prill) fob Yuzhny (mt)

Oct 393 397 395 5 mt

Nov 395 400 398 5 mt

Dec 393 400 397 5 mt

urea (gran) fob barge NOLa (s ton)

Oct 426 432 429 3 st

Nov 425 432 429 1.5 st

Dec 425 433 429 1.5 st

Urea (gran) fob Egypt (mt)

Oct 455 462 459 5 mt

Nov 450 460 455 5 mt

Dec 450 460 455 5 mt

For further swaps information contact:

Ron Foxon & Alexey Paliy,

FIS Ltd - Office : +44 207 090 1122 or

Cell: +44 7738726557 [email protected]