arm 54 assignment 13-14 -...

TRANSCRIPT

6/27/2012

1

Associate in Risk Management

ARM 54 – Chapters 13 & 14

Understanding & Applying

Cash Flow Analysis

Presented by:

Lynne Lovell RHU CLU ChFC CIC CRM ARM CPCU AFSB ASLI AINS MLIS CRIS

Understanding Cash Flow Analysis

Chapter 13 Educational Objectives:

1. Explain why net cash flows are important

2. Explain why money has a “time value” & how to determine present value

3. Calculate present values of future single payments or streams of future payments

using present value tables

Understanding Cash Flow Analysis

Chapter 13 Educational Objectives:

4. Explain how to use net present value &

internal rate of return methods to evaluate

capital investment proposals

5. Apply net present value & internal rate of

return methods to rank capital investment proposals

6/27/2012

2

Understanding Cash Flow Analysis

Chapter 13 Educational Objectives:

6. Calculate internal rate of return for a

capital investment proposal using

interpolation

7. Explain how to calculate differential annual

after tax net cash flows for investment proposal

8. Case study (on your own)

Valid financial criteria for choosing proposals that provide the greatest financial benefit

Cash flow – the money generated by an investment in assets or activities– can be negative or positive–Net cash flow (NCF)

#1 Why Net Cash Flows are Important

Time value of money = ability to invest & generate income over time on a dollar available today–Dollar today is worth more than a dollar to be received in the future•Investing money over time in an asset/activity can generate income

#2 Why Money Has a Time Value

6/27/2012

3

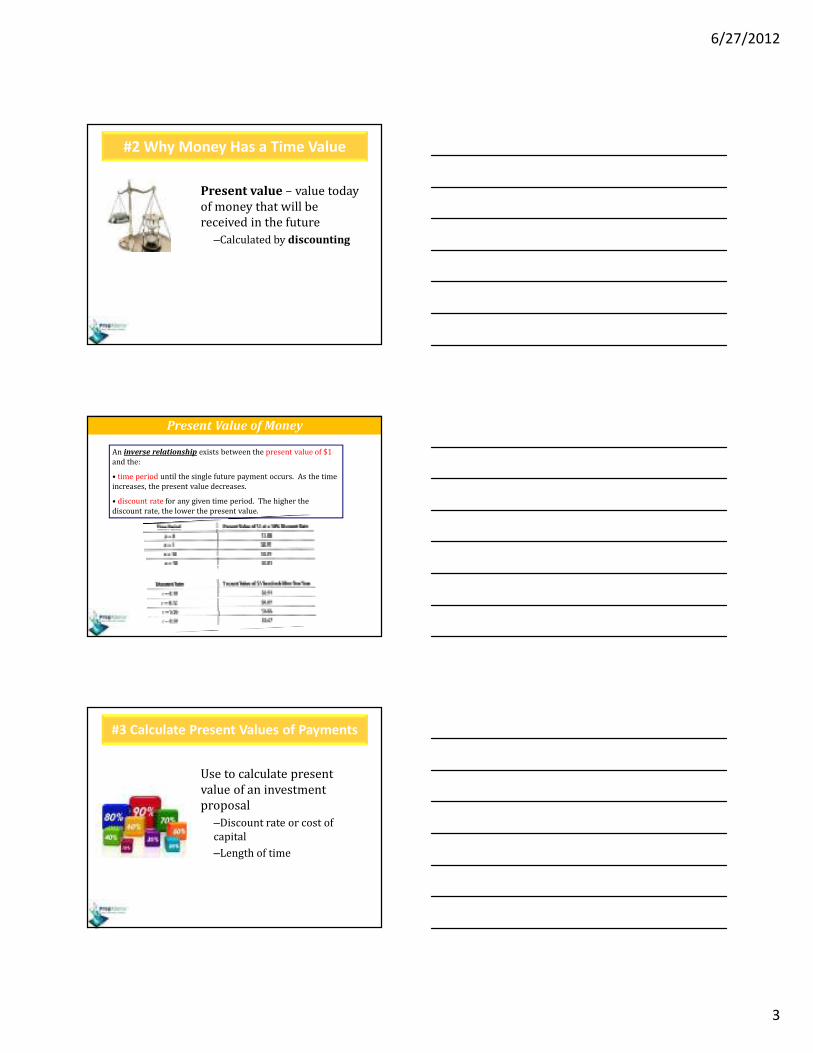

Present value – value today

of money that will be received in the future

–Calculated by discounting

#2 Why Money Has a Time Value

An inverse relationship exists between the present value of $1

and the:

• time period until the single future payment occurs. As the time

increases, the present value decreases.

• discount rate for any given time period. The higher the

discount rate, the lower the present value.

Present Value of Money

Use to calculate present

value of an investment proposal

–Discount rate or cost of

capital

–Length of time

#3 Calculate Present Values of Payments

6/27/2012

4

Present payment –Simply the value today of that payment (in the present)

Single future payment –One payment at some future date•Ex: Salvage or resale value

Present value factorPVFa = 1/(1+r)ⁿ

–PVFa single future payment–PVFb stream of future payments

#3 Calculate Present Values of Payments

PVFa indicates amount invested today at a given rate for a given time period to receive $1 as single payment at end of period

PVFa X (1+r)ⁿ = $1

PVFa is amount of money todaythat would grow to $1 at the end of the time period

•Other than $1 at end of period

#3 Calculate Present Values of Payments

Stream of equal future payments

–Annuity - Present value of a

stream of future payments

–Equal to the sum of present

value of each separate payment

•Appendix A

•Appendix B

#3 Calculate Present Values of Payments

6/27/2012

5

Stream of unequal future payments

–Cannot use Appendix B!

–Use Appendix A and calculate separately then add together

#3 Calculate Present Values of Payments

Using Net Present Value (NPV) and Internal Rate of

Return (IRR) to evaluate capital expenditure proposals

–Exhibit 13-4 – NPV method

–Exhibit 13-5 – IRR method

#4 Using NPV & IRR

Net Present Value (NPV) method

–Use only when minimum acceptable rate of return is predetermined (would most likely get this from CFO)

NPV = PV (sum of future net cash flows) – PV (initial investment)

•If NPV is negative do not accept

•If NPV is positive should be considered

#4 Using NPV & IRR

6/27/2012

6

Internal Rate of Return (IRR) Method

–Discount rate at which net present value of all net cash flows equals zero

PVF = Initial Investment/Differential Cash Flow

#4 Using NPV & IRR

•Objective is to choose the proposals with the highest NPV or IRR to maximize organization's

value

–If initial investment - same choose highest IRR to maximize value

–If initial investment is different and limitations on available capital (resources) - develop a profitability index - higher profitability indices are preferred

Profitability Index = PV (NCF)/PV (Initial Investment)

#5 Using NPV/IRR to Rank Proposals

Interpolating

–Provides a more exact rate of return

–P 13.20

#6 Internal Rate of Return

6/27/2012

7

Differential–The difference the investment will make on revenue and expenses•For-profit – income taxes are cash outflows

–Percentage of taxable income

–Non-cash revenue and expenses

»Depreciation allocates cost of long-term assets over multiple accounting periods

•Straight-line depreciation (used in the book and on the exam)

–Exhibit 13-8 – purchase of RMIS

#7 Differential After-tax NCF

Application questions in course guide – apply

methods learned

#8 Evaluate Investment Proposals

6/27/2012

8

Associate in Risk Management

ARM 54 – Chapter 14

Applying Cash Flow Analysis

Applying Cash Flow Analysis

Chapter 14 Educational Objectives:

1. How recognition of expected losses alters

cash flows

2. Effect various risk control techniques have

on net cash flows

3. Calculate NPV & IRR on capital investment

when using various risk control techniques

Applying Cash Flow Analysis

Chapter 14 Educational Objectives:

4. Effect various risk financing techniques

have on net cash flows

5. Calculate NPV & IRR on capital investment

proposal using various risk financing

techniques

6. Effect combination of RM techniques has

on net cash flows

6/27/2012

9

Applying Cash Flow Analysis

Educational Objectives:

7. Calculate NPV & IRR on capital investment

proposal using combination of RM

techniques

8. Consider uncertainty in cash flow analysis

9. Select RM technique offering highest NPV

& IRR for given investment proposal

Differential Annual After-Tax Net Cash Flow

#1 Expected Losses Alter Cash Flows

• Incorporate all costs and benefits including RM techniques implemented– Add one-time costs should be added to initial

investment

– On-going RM costs should be deducted from projected annual NCFs

– Expected losses – when recognized NPV & IRR will change – Exh 14-2

– Compare Exh 14-1 to Exh 14-3

6/27/2012

10

#2 Effect of RC Techniques on CF

• Consider effect of

– Avoidance – all benefits of activity are foregone

– Prevention or reduction of losses

– Separation of loss exposures

#3 NPV & IRR Using RC Techniques

• Adjustments to

– Present Value of the initial investment

– Differential cash expenses

• Expected losses

• Maintenance

• Depreciation

#4 Effect of RF Techniques on NCF

• Captive Insurer– Established insurance subsidiary

–May or may not be retention depending upon tax & regulatory issues• If legally considered to be retention (no risk transfer

taken place) premiums paid are not tax-deductible & cash flows similar for loss retention with a funded retention

• If considered insurance premiums then tax deductible

6/27/2012

11

#4 Effect of RF Techniques on NCF

• Risk Financing techniques - Loss transfer

through unrelated insurer

– Insurance most common

– Hold-harmless agreement

– Hedging for business risks

#4 Effect of RF Techniques on NCF

• RF Techniques Cont’d

– Loss retention with current funding

– Loss retention with unfunded reserve

• Same as current funding except possible extra administrative costs

– Loss retention with prefunded reserve

– Loss retention with post-funding (borrowing)

#5 Calculate NPV & IRR Using Various RF

• Adjustments to proposal

– Adjust PV of initial investment

– Adjust differential cash revenues

– Adjust differential cash expenses

6/27/2012

12

#6 Combination of RM Techniques

• Apply several RM techniques to each

significant loss exposure

– Reduces COR more than using any single RM technique

• Separation & a funded reserve to pay losses

– Increase initial investment

– Not change in cash outflows

– Creates earnings on fund held in reserve

– Benefits must outweigh higher initial investment

#7 NPV & IRR Using RM Techniques

• Adjustments

– PV of the initial investment

– Differential cash revenues

– Differential cash expenses

#8 Uncertainty in Cash Flow Analysis

• Corporation with common stock– If no greater risk use normal cost of capital

– Can increase required rate of return

• Identify and quantify possible effect of large losses– Can reduce risk through insurance, hedging,

other RM techniques reducing expected losses

– Quantify effects & incorporate costs into NPV & IRR calculations but hard to measure

6/27/2012

13

#8 Uncertainty in Cash Flow Analysis

• When difficult to measure assign “price tag”

– Cost of uncertainty

• Provides straightforward & understandable method reflecting uncertainty

– Treat like any other cost/cash outflow

• Greater risk of large loss, greater cost assigned

• More insurance purchased, lower cost assigned

• Deduct from after-tax cash inflow or add to after-tax net cash outflow

• Calculate NPV & IRR based on adjustment

#9 RM Technique w/Highest NPV - IRR

• To maximize organization's value use NPV &

IRR to select RM Techniques

– RM techniques promising highest positive NPV and IRR above minimum rate of return

– Consider all relevant possibilities

• Evaluate each proposal coupled with RM technique

Quiz Questions

6/27/2012

14

Sample Test Questions – Chapter 13

3. Maria has a table listing the present value factors for $1

received at the end of each year for four years shown below. She needs to calculate the present value of a stream of four

equal payments of $5,000 to be received at the end of each of

the next four years. The discount rate is 8 percent. What is the present value of this stream of payments?

a. $4,630

b. $16,560

c. $42,990

d. $66,240

Sample Test Questions – Chapter 13

4. A proposed project requires an initial investment of $60,000. The project will have a useful life of four years with no salvage value and will generate a

differential annual after-tax cash flow of $20,000. The minimum acceptable rate of return is 10 percent. Which one of the following correctly evaluates the

proposal using the net present value method?

a. The NPV is $41,480 so the proposal would reduce the organization’s value.

b. The NPV is $110,200 so it should be undertaken.

c. The NPV is $3,400 so it is acceptable by the NPV method.

d. The NPV is $63,400, which is more than the initial investment so the project should be rejected.

Sample Test Questions – Chapter 13

6/27/2012

15

5. A proposed project requires an initial investment of

$15,000. It has a useful life of two years and will generate $8,500 differential annual after-tax cash flow.

What is the interpolated rate of return for the

proposal?

a. 1.77%

b. 8.02%

c. 8.77%

d. 10.38%

Sample Test Questions – Chapter 13

Sample Test Questions – Chapter 14

1. When calculating net cash flow, differential annual expenses resulting from expected losses are:

a. Added to differential depreciation.

b. Deducted from differential cash revenues.

c. Deducted from taxable income.

d. Divided into the initial investment amount to determine the present value factor.

Sample Test Questions – Chapter 14

6/27/2012

16

2. The Barnes Company has signed a hold-harmless agreement

for property loss exposures. Barnes is reimbursed for a portion of each fire loss to its properties. Annual

reimbursements for property losses are projected at $2,000

and additional administrative costs for the agreement are $250. In calculating cash flows related to this hold-harmless

agreement,

a. The $250 administrative cost are not considered in cash

flow and analysis.

b. The $250 administrative cost are treated as a source of incremental revenues.

c. The $2,000 projected reimbursements are treated as an expense and deducted from differential cash revenues.

d. The $2,000 projected reimbursements are treated as a

source of incremental revenues.

Sample Test Questions – Chapter 14

3. Pinewood Manufacturing’s management team is evaluating a proposal to build an addition to the plant. The NPV and IIR of the

proposal are less than they had anticipated. However, the company’s risk manager explains the installation of a sprinkler system in the

building can make the proposal more attractive. All of the following correctly describe the effect the sprinkler system on the proposal’s

net cash flow, EXCEPT:

a. The sprinkler would reduce the expected value of fire losses.

b. The maintenance expenses for the sprinkler system would be

added to the cost of the proposal’s initial investment.

c. The system’s initial cost would be added to the cost of the

proposal’s initial investment.

d. The depreciation expenses for the sprinkler system are considered in calculating after-tax net cash flows each year.

Sample Test Questions – Chapter 14

Sandy’s Missed Quiz Question Ch. 13

Heywood Company is considering two loss control investments.

Project #1 is a sprinkler system. This project has an internal rate of

return of 7.5 percent. All net cash flows after the initial investment are positive. Project #2 is camera monitoring system. This project

has an internal rate of return of 14 percent. All net cash flows after

the initial investment are positive. Heywood uses a 10 percent

interest rate to evaluate capital budgeting projects of this degree of

risk. Which of the following statements concerning the net present

value (NPV) of these projects is true? A. The NPV of Project #1 is positive and the NPV of Project

#2 is negative.

B. The NPV of Project #1 is negative and the NPV of

Project #2 is positive.

C. Both projects have a positive NPV.

D. Both projects have a negative NPV.

6/27/2012

17

"Change is a dragon. You can

ignore it, which is futile. You

can fight it, in which case you

will lose. Or you can ride it."

- Anonymous

Thank you! Now it’s time for “Open Mic” Q&A