as march online - aviation strategy · pdf filecountries, summer 2008 vs. summer 2007 source:...

TRANSCRIPT

Aviation EconomicsJames House, 1st Floor 22/24 Corsham Street

London N1 6DRTel: +44 (0) 20 7490 5215Fax: +44 (0) 20 7490 5218e-mail: [email protected]

Issue No: 125 March 2008

Aviation Strategy

Analysis

All change at Heathrow?1-2

Briefing

Tougher times ahead forAirAsia Group?

3-9

Has Alitalia picked the right saviour?

10-16

JetBlue: slower growthand new revenue strategy

17-23

Databases 24-27

Airline traffic and financials

Regional trends

Orders

CONTENTS

PUBLISHER

www.aviationeconomics.com

Will it be all change at London Heathrow?Frantic buying of slots at London Heathrow in time for the

2008 summer season has resulted in the four US non-Bermuda II carriers gaining access to Heathrow to varyingdegrees.

Continental has reported in a SEC filing that it paid $209mfor its four daily (28 weekly) slot pairs to operate Newark andHouston flights; Delta (JFK and Atlanta) and Northwest (Detroit,Minneapolis and Seattle) have acquired three daily slot pairswhile US Airways has acquired a single daily slot to operate aPhiladelphia service.

Sellers of slots at LHR include: GB Airways (four), Alitalia(three), KLM (two) and Air France (two). The chart below showsthat the European flag carriers retain a sizeable presence atHeathrow should they wish to either sell their slots, operatelong-haul services in conjunction with alliance partners or - asin the case of Air France with its new Los Angeles service -operate their own metal, gate permitting.

The two most interesting slot portfolios to keep an eye on for2009 are bmi and Alitalia, the former of which may be about toembark on a transformational transaction that may see itbecome part of the Lufthansa group, and the latter of which islikely to become part of the Air France/KLM empire (seeBriefing, page 10).

BA; 41.4%

BMI; 11.2%Lufthansa ; 4.3%Virgin Atlantic; 3.4%

Aer Lingus ; 3.2%

SAS ; 2.9%

American; 2.5%

Iberia ; 2.2%

Air Canada ; 2.1%

KLM; 1.9%United; 1.5%

Air France ; 1.5%Alitalia; 1.3%

TAP; 0.9%

Others; 19.7%

Source: Airports Coordination Limited, Aviation Economics estimates

HEATHROW’S SLOT PIE, SUMMER 2008

Aviation StrategyAnalysis

2

Aviation Strategyis published 10 times a yearby Aviation Economics

Publisher:Keith McMullan

Editor:Nick Moreno

Contributing Editors:Heini Nuutinen

Robert Cullemore

Sub-editor: Julian Longin

Subscriptions:[email protected]

Tel: +44 (0)20 7490 5215

Copyright:Aviation Economics

All rights reserved

Aviation EconomicsRegistered No: 2967706

(England)

Registered Office:James House, 1st Floor

22/24 Corsham St London N1 6DR

VAT No: 701780947

ISSN 1463-9254

The opinions expressed in this publica-tion do not necessarily reflect the opin-

ions of the editors, publisher or contribu-tors. Every effort is made to ensure thatthe information contained in this publica-tion is accurate, but no legal reponsibilityis accepted for any errors or omissions.

The contents of this publication, either inwhole or in part, may not be copied,

stored or reproduced in any format, print-ed or electronic, without the written con-

sent of the publisher.

March 2008

While planned capacity and move-ments from London Heathrow to the UShave increased by a headline inducinglevel of more than 20% in the summer of2008 compared with the summer of 2007,the total capacity between all five Londonairports and the US has increased by justover 9%, reflecting the fact that many air-lines have shifted certain Gatwick-USoperations that could not operate ex-Heathrow due to Bermuda II (e.g.Houston, Dallas and Atlanta).

Price warsThere has been a considerable amount

of speculation about a transatlantic pricewar. We're not sure what form, if any, thiswill take. Yield per RPK for BA on USroutes has historically been lower thanthat of Air France and Lufthansa operatingfrom their respective continental hubs.There isn't therefore much incentive forthe continental network carriers to engagein a price war in order to attract economyleisure passengers, who are profit neutralat best. The UK to US and continental toUS markets are in any case largely sepa-rate.

However, there is a concern that themere presence of Delta, Northwest,Continental and US Airways at Heathrowcould shut the door for what has been hith-erto been a lucrative source of revenue forVirgin and BA: employees of US firms with

corporate contracts with one of the fournon-LHR US carriers who could exploit thefact that their 'designated carrier' did notserve Heathrow by taking their business toone of the two UK carriers.

These passengers were often bookingunrestricted premium travel tickets, andthis option may no longer be available tothem. This could also impact Eos as well,and Silverjet to a lesser extent.

While the macro-economic indicatorsare pointing south, the relatively strongpound against the US$ should help tocompensate as the number of UK out-bound passengers on transatlantic flightsis higher than US outbound passengers,and for 2007 remained very strong.

Lastly, Terminal 5 opens on March27th. We have some concerns about T5 asthere seem to be niggling issues with bag-gage handling systems. Furthermore,there is considerable doubt that passen-gers are going to be enthused about thenewly introduced biometric testing, evenfor domestic flights.

However, the facility should be impres-sive, but so too will be the amount of freespace in the other terminals created byBA's withdrawal - starting with Terminal 1at the outset and followed by Terminal 4once BA has moved across its long-hauloperations to Terminal 5 on the planneddate of April 30th. It's set to be an inter-esting summer season at LondonHeathrow.

-20%

-10%

0%

10%

20%

30%

40%

UAEUSA

Russia

Ind

ia

Denmark

UK

German

y

Sweden

Switzerl

and

Norway

Hong K

ong

Austria

Canad

a

Belgium

Spa

in

Netherl

ands

Portug

al Italy

Irelan

d

Franc

e

ATM CHANGES BETWEEN LHR AND OTHERCOUNTRIES, SUMMER 2008 vs. SUMMER 2007

Source: Airports Coordination Limited, Aviation Economics estimates

With a massive 140 A320s on firm order,the AirAsia Group is set to become the

largest operator in the world of the model.But while the self-styled "lowest cost airlinein the world" has a significant advantageover MAS and other legacy carriers, willAirAsia be able to place these new aircraftprofitably once ASEAN countries adopt anopen skies regime, after which existing andnew LCCs are certain to increase theircapacity too?

AirAsia was launched by a government-owned conglomerate in 1996 as a regionalairline, but operations were scaled back todomestic services before Tune Air - a hold-ing company owned by AirAsia Group CEOTony Fernandes and ex-Ryanair directorConor McCarthy - bought the loss-makingand heavily indebted airline in September2001 for a nominal fee of RM 1 (US$0.27).The airline was relaunched as an LCC inJanuary 2002, and the AirAsia Group raisedUS$227m in an IPO on the Kuala Lumpurmarket in November 2004.

Today the shareholders include not onlyTune Air (which has a 30.9% stake) but alsoa number of investment companies and pri-vate shareholders, and they have seen theKuala Lumpur-based AirAsia Group rack upsubstantial profits over the last few years(see charts, page four). In the 2006/07 finan-cial year (ending June 30th), AirAsia Grouprecorded a 50% increase in revenue to RM1.6bn (US$463m), and a net profit of RM498m (US$144m), compared with RM 202min 2005/06. The group carried 14m passen-gers in the 12 month period, 51% up year-on-year, with load factor up 2.1 percentagepoints to 79.6%. Yield rose 11% in 2006/07(although the average fare was down 2%,due largely to a 6% reduction in average triplength). However, cost per ASK rose 7% dueto rising fuel prices and higher average userand station charges from more internationalroutes, though after stripping out fuel, unitcosts fell by 4% thanks to the effect of fewerleased aircraft in the fleet, the impact of lowcost terminals at Kuala Lumpur and Kota

Kinabalu (the latter opening in February2007), and productivity improvements (seechart, page six). Impressively, net marginrose from 18.8% in 2005/06 to 31.1% in2006/07.

Today the AirAsia Group operates 90routes to 11 countries: the three "homecountries" of Malaysia, Indonesia andThailand, plus China, Myanmar, Philippines,Vietnam, Laos, Cambodia, Brunei andSingapore. The group employs 3,000, mostof which are stationed at six bases: KualaLumpur, Kuching, Kota Kinabalu and JohurBahru in Malaysia, with Jakarta in Indonesiaand Bangkok in Thailand.

The stunning success enjoyed by theAirAsia Group since 2002 has been duelargely to the problems at the legacy carrier,Malaysia Airlines (MAS), where a high struc-tural cost base and ineffective managementjust couldn't compete with an aggressiveLCC that quickly became profitable in thedomestic and international Malaysian mar-ket. But AirAsia Group has wider ambitionsthan just the Malaysian market, since theAsia/Pacific region has 250 cities with a pop-ulation of half a million or more, few of whichhave any significant international routes, letalone an LCC service. Furthermore, withinsouth-east Asia a large majority of theregion's population has never travelled byair, so the AirAsia Group wants to create theso-called "Ryanair effect", with low faresencouraging people to fly who have neverpreviously flown.

Aviation StrategyBriefing

March 20083

Fleet Orders OptionsAirAsia (Malaysia)A320-200 32 140 50737-300 9Thai AirAsiaA320-200 3737-300 14Indonesia AirAsia737-300 10AirAsiaXA330-300 1 15Total 69 155 50

AIRASIA GROUP FLEET

Tough times ahead for AirAsia Group?

This analysis encouraged the group toset up subsidiaries in Indonesia andThailand (see below), and build a huge orderbook. The first A320 order (for 60 aircraft)was only placed in March 2005, so the orderbook has built up rapidly, with the latest addi-tion coming in December 2007 when theAirAsia Group ordered another 25 A320s(firmed up from existing options), bringingtotal orders for the model to 175 aircraft (ofwhich 140 are outstanding), with another 50on option.

The first two A320s arrived in December2005, and the group will receive 23 aircraft inthe 2008 financial year, 14 in 2009, 23 in2010, 24 in 2011, 24 in 2012, 24 in 2013 and10 in 2014. Of the 175, just under half will beused for "frequency additions", 33 willreplace the 737s that the group currentlyoperates, while the rest will be put onto newroutes.

Even given the potential of theAsia/Pacific market, that's a large amount ofadditional capacity - particularly since thegroup has experienced different levels ofsuccess in the three main markets it hasalready entered. Whereas in the Malaysianmarket the group has faced weak competi-

tion, in both Thailand and Indonesia thegroup's subsidiaries have been exposed tofar greater competition - and in both coun-tries the subsidiaries have found it difficult tomake a profit.

IndonesiaThe Indonesian subsidiary was launched

as Awair in 2000 before becoming IndonesiaAirAsia in December 2005, a year afterAirAsia Group made a 49% investment (theother 51% is owned by Indonesianinvestors).

The Jakarta-based carrier operates afleet of 10 737-300s, with a final 737 trans-ferring from the Malaysian AirAsia in Marchbefore the airline starts receiving A320s asdirect replacements for the 737s, with thefirst coming in the summer. IndonesiaAirAsia serves 10 domestic and three for-eign destinations out of Jakarta (to KualaLumpur, Johor Bahru and Bangkok), and asecond hub is being set up at Bali thisMarch, which will develop domestic routes toeastern Indonesia and international servicesto destinations such as Malaysia, Thailandand even Australia.

Indonesia AirAsia made an operatingloss in the 2005/06 financial year but - frus-tratingly - AirAsia Group gave little detail ofresults at subsidiaries in its 2006/07 annualreport, and the group even stopped reportingpassenger numbers at its subsidiaries afterSeptember 2007 (see chart, page seven).The lack of information can only raise doubton AirAsia Group's previous prediction thatthe Indonesian affiliate was "turning around"and would break even in 2006/07, eventhough the airline was boosted significantlyin 2006 by the government's allowing of fareadvertising for the first time, which enabledIndonesia AirAsia to launch aggressive pro-motions and advertising. However, it isknown that AirAsia suffered a high number ofunscheduled maintenance and aircraftdelays and cancellations at the Indonesianoperation in 2006/07, and so it's unlikely thatthe Indonesian operation has broken evenyet - and this was confirmed in Februarywhen AirAsia said that its "portion of losses"at the Indonesian operation for October-

Aviation StrategyBriefing

March 20084

0

500

1,000

1,500

2,000

02/03 03/04 04/05 05/06 06/07

RM m AIRASIA GROUP REVENUE..

0

100

200

300

400

500

02/03 03/04 04/05 05/06 06/07

..AND FINANCIAL RESULTSRM m

Netprofit

Op.profit

Note: FY ends June 30

December 2007 was RM 3.3m (US$1m).Additionally, Indonesian LCC Lion Airlines isexpanding rapidly: it currently operates afleet of 28 aircraft, but it has a hefty 178 737-900ERs on order. The carrier will base 60aircraft in Indonesia and the rest across theAsia/Pacific region - including Thailand - andwill prove a major challenge to AirAsiaGroup in the region.

ThailandThai AirAsia was launched in November

2003, and AirAsia Group currently holds a49% stake. Already though, the Bangkok-based airline has had a chequered history. Itwas launched as a joint venture with theShin Corporation, a telecommunicationsgroup owned by the family of formerThailand prime minister Thaksin Shinawatra(who was deposed by a military coup inSeptember 2006 after allegations of corrup-tion) that subsequently sold part of its 50%stake to Thai businessmen SittichaiVeerathummanoon in order to get aroundforeign ownership limits (since Shinawatra’sstake was bought by Temasek Holdings, theSingapore government's investment vehiclein January 2006). Sittichai and Shin thensold their entire shareholding to six of ThaiAirAsia's management team in the summerof last year.

The airline received its first A320 at endof 2007 and Thai AirAsia will be an all-A320operation sooner than originally plannedthanks to rising fuel prices, with the last of itscurrent 14 737-300s leaving the fleet in2010.

Within the Group (and prior to the ASEANopen skies agreement) Thai AirAsia wasoriginally seen as a "launch pad" for newroutes into Indo-China, as Thailand has aseries of open skies deals with countriesthroughout the region, and Thai AirAsiabecame the first LCC to operate into China,from 2005. But, although Thai AirAsia ishelped considerably by a 50% discount onairport fees in the country as well as an eightyear tax exemption, like its Indonesiancousin the Thai subsidiary is struggling tomake a positive contribution to AirAsiaGroup.

While Thai AirAsia currently operates to10 domestic and nine foreign destinations,most new routes have been put on hold forat least 18 months thanks to rising fuelprices. The situation hasn't been helped bythe rise of other LCCs in Thailand, includingNok Air (a subsidiary of Thai AirwaysInternational that has 12 aircraft) and One-Two-Go (owned by Orient Thai Airlines).Additionally, the political situation in Thailandhas affected demand there, both from Thaitravellers and from visiting tourists, and for2006/07 AirAsia said that the "financial resultfrom the operations in Thailand is not signif-icant compared with the Malaysian opera-tions".

According to Tassapon Bijleveld - ThaiAirAsia's CEO - revenue rose by 40% in2007 (the calendar year), but the carrier stillcould not post a profit. Figures just releasedshow a RM 8.2m (US$3m) loss for ThaiAirAsia in the October-December 2007 peri-od, although Bijleveld insists that the airlinewill make a profit in January-December2008. The airline has also been hit hard byfinancial penalties for breaking leases on737-300s returned to lessors, while Bijleveldalso blames "intense competition in Thailandthrough rampant undercutting". But althoughthe group adds that the "current operationalpressure" at the subsidiary airlines "is a tem-porary blip", the medium-term goal for ThaiAirAsia of an IPO around 2010 or 2011 mustbe in some doubt.

Other countriesThe AirAsia Group has been linked to a

large number of new subsidiaries in otherAsian countries - although many of its planshave come to nothing:

• Sri LankaIn 2006 the group was reported to be innegotiations to buy 49% of Sri Lankan carri-er Holiday Air, an LCC that planned tolaunch operations to domestic and interna-tional destinations out of Colombo in 2007. A"technical partnership" was agreed wherebyHoliday Air changed its name to AirAsiaLanka, with AirAsia Group agreeing to trainthe pilots of Air Asia Lanka and with the Sri

Aviation StrategyBriefing

March 20085

Lankan airline also using AirAsia's internetbooking system, but despite plans for a fleetof seven aircraft, this project did notprogress.• BangladeshAgain in 2006 an MoU was signed with theOrion Group - a Bangladeshi conglomerate -to analyse a joint venture carrier provisional-ly called East West Airlines. This venturealso appears to have come to nothing.• SingaporeAirAsia Group seriously considered buyingSingaporean LCC Valuair in 2005, and anoffer was put to Valuair's shareholders in thatyear. However, some of Valuair's sharehold-ers were unhappy with the price and withAirAsia's plan to drop some of Valuairroutes, and instead Valuair merged withJetstar Asia.• The PhilippinesNegotiations have also been held betweenthe AirAsia Group and Manila-based AsianSpirit over establishing Philippine AirAsia atClark airport (which is close to Manila), butapparently any potential deal collapsed fol-lowing Asian Spirit's insistence that aPhilippine AirAsia should focus on domestictrunk routes, leaving Asian Spirit to continueits regional routes. • VietnamAn LoI was signed with the VietnamShipbuilding Industry Group (also known asVinashin, and which is owned by theVietnamese state) in August 2007. Althoughthe idea is still subject to formal Vietnamesegovernment approval, the so-called Hanoi-

based Vinashin AirAsia would operate initial-ly on domestic routes before expanding intointernational services.

But unless the Vietnamese governmentchanges the current limits on foreign owner-ship (which it says its is considering), theAirAsia Group will be restricted to a 30%ownership stake in the Vietnamese carrier -and in any case reports out of Asia suggestthe plans are facing considerable oppositionfrom both Vietnam Airlines and PacificAirlines (the former of which is owned 100%by the state, and the latter 82% by state bod-ies and 18% by Qantas). Currently ThaiAirAsia operates between Bangkok andHanoi and has been trying - unsuccessfully -to win permission from the Vietnameseauthorities to operate routes to Ho Chi MinhCity. • ChinaLaunching an airline in China is believed tobe at the very top of AirAsia Group's wishlist, but Fernandes believes that the politicalpower held by the Big Three Chinese airlinesmeans that no local AirAsia subsidiary willbe possible within the next five years atleast.

Given this reality, the group is making dowith a furious expansion on routes into thecountry, and most of the 15 routes beinglaunched by the group in 2007/08 are toChina, with new services to Hong Kong,Haikou, Guilin, Xiamen and Shenzhen fromKuala Lumpur, Bangkok or Kota Kinabalu. AKuala Lumpur-Guangzhou route waslaunched this January, where it competesagainst China Southern and MAS (whichcodeshare with each other). The airlineexpects to carry 130,000 passengers a yearon the route, which is the fourth Chinesedestination out of Kuala Lumpur, joining ser-vices to Shenzhen, Xiamen and Macau, andwith routes to Hainan, Gueling and HongKong also being planned.

AirAsia XLong-haul LCC AirAsia X was set up last

year as a separate company from theAirAsia Group, although it is now owned48% by Aero Ventures (which includes manyof the main shareholders in AirAsia Group,

Aviation StrategyBriefing

March 20086

0

1,000

2,000

3,000

01/02 02/03 03/04 04/05 05/06 06/072,000

3,000

4,000

5,000

‘000sAIRASIA GROUP EMPLOYEESAND PRODUCTIVITY

Employees

ASKsper emp.

including CEO Tony Fernandesand deputy CEO KamarudinMeranun), while 16% is held direct-ly by the AirAsia Group and 16% bythe Virgin Group. AirAsia Grouppaid RM 26.7m (US$7.6m) for itsinitial 20% stake, while the VirginGroup is believed to have paid asimilar sum for its initial 20%. Theoriginal investors have now beendiluted but in return experienced amassive paper profit because inFebruary this year the ManaraConsortium - a Bahrain-basedinvestment company - and Japan-based financial services group OrixCorporation (which owns Dublin-basedlessor ORIX Aviation) each bought a 10%stake, for RM 125m (US$39m) each. AirAsiaX considers these as "strategic investors",and the funds raised will be used to financeaircraft purchases.

Sarawak-based AirAsia X launched aninitial four-flights-a-week route betweenKuala Lumpur and the Gold Coast inAustralia in November 2007, chosen partlybecause it is close to Brisbane, at which theLCC Virgin Blue (in which the Virgin Grouphas a 25% stake) is based. Fernandes saysthat links with Virgin Atlantic may be devel-oped in the future, though this would stopshort of codesharing.

A second route was launched thisFebruary: a five-times-a-week servicebetween Kuala Lumpur and Hangzhou (nearShanghai) in China, which is operated withthe single A330 that is AirAsia X's only air-craft so far. This is on a six-year lease fromAWAS, but in January the airline said it haddecided against expanding its fleet in theshort-term thanks to a shortage of availableA330s, and with those that are availablehaving lease rates that are too expensive.

This is obviously a blow to the carrier'slong-term plan to build up a network of up to50 destinations in the Asia/Pacific andEuropean regions, and further routes willnow have to wait until AirAsia X receives thefirst aircraft from its order for 15 A330-300s(in a high density, 400-seat configuration),the first two of which are due to be deliveredin the fourth quarter of this year, after which

two more will come in 2009, three in 2010,four in 2011 and four in 2012. But it's possi-ble that alongside this delivery scheduleAirAsia could lease more A330s if leaserates start to come down (which should hap-pen once airlines start replacing the modelwith 787s).

Ten A330-300s are also under option andthese are expected to be upgraded to firmorders at some point in 2008. AirAsia X willplace an order for 25 further aircraft (plus 25options) in the second half of this year, withnegotiations to buy A350s or 787-900salready under way.

Among routes believed to be under con-sideration at AirAsia X are other Chinesedestinations (such as Tianjin), Japan andservices to the UK via the Middle East (prob-ably Dubai or Sharjah). While Fernandeshas hinted that an interline agreement is outof the question, AirAsia X may co-ordinate itsflight times in order to connect in with otherEuropean LCCs. However, a stopover in theMiddle East will bring AirAsia X into compe-tition with Emirates and others, although theLCC is confident this will not be a problemthanks to the feed it has in Asia. Routes arealso planned to India, and AirAsia X hasalready carried out negotiations with the air-port authority at Amritsar.

Despite these ambitions, and althoughAirAsia X expects to be profitable in its sec-ond year of operation, there are questionmarks over how much of the LCC businessmodel can be applied to long-haul. Whilepassengers have to pay for frills such as

Aviation StrategyBriefing

March 20087

0

100200

300400

500

600700

800900

1,000

Jul 0

4

Sep 04

Nov 04

Jan 0

5

Mar 05

May 05

Jul 0

5

Sep 0

5Nov

05

Jan 0

6

Mar 06

May 06

Jul 0

6

Sep 06

Nov 06

Jan 0

7

Mar 07

May 07

Jul 0

7

Sep 0

7

‘000s AIRASIA GROUP PASSENGER BREAKDOWN

Malaysia

Thailand

Indonesia

food and in-seat entertainment, AirAsia Xoperates alongside Air Asia out of KualaLumpur's Low-Cost Carrier Terminal(LCCT), which is 20km away from the air-port's main terminal. AirAsia X obviouslybelieves it is crucial to connect with short-and medium-haul AirAsia Group passen-gers, but Air Asia X must lose some passen-gers who would prefer to connect at themain terminal.

And whereas the various AirAsia airlineshave turnaround times of around 25 min-utes, AirAsia X has a turnaround time of atleast 75 minutes. Curiously, as part of an"agreement", AirAsia X has vowed never tooperate competing flights of less than fourhours duration, while the AirAsia Group willnot operate competing flights longer thanfour hours. This will lead to the strange situ-ation in India that AirAsia will serve destina-tions only in the south of the country, whilenorthern cities will be served by AirAsia X. Atleast four destinations will be served in Indiaby each of AirAsia and AirAsia X by 2010,Fernandes says.

While AirAsia X is a separate operation tothe AirAsia Group, it is doubtless distractingthe attention of Fernandes and others fromfocussing 100% on AirAsia Group. The long-term intentions of Fernandes and the otherinvestors for AirAsia X is almost certainly tomake a profitable exit once (or if) the long-haul LCC is established and profitable, andFernandes has already mentioned a possi-ble float by 2010 at the very earliest.

Cost leadershipAssuming AirAsia X does not become a

distraction, the key to AirAsia Group's con-tinued success will be to maintain its lowcost base and place its new aircraft suc-cessfully, with ASEAN being the immediatefocus for AirAsia Group according toFernandes, as bilateral restrictions areeased ahead of ASEAN open skies.

On the former issue, the group still claimsto have the "lowest unit cost in the world",thanks to its location and LCC strategy.Taking a closer look, by far the biggest dif-ference between AirAsia Group's unit costsand its LCC peers is in two key areas:

employees and aviation charges. At 0.33 UScents/ASK in 2006/07, AirAsia Group's staffcosts are around 0.8-0.9 US cents/ASKlower than the average of rival LCCs Gol,JetBlue, Southwest, Air Tran, EasyJet,Ryanair, WestJet and Virgin Blue - thanksentirely to Asia being such a low cost region.That's a huge cost advantage, and in addi-tion the group's user station/aviation chargesof 0.22 US Cents/ASK are 0.7-0.8 US centslower than the same LCC peer group,thanks again to lower Asian user charges.

But AirAsia Group is not competingagainst these other LCCs, but against air-lines in the Asia/Pacific region, and while thelocal legacy carriers will never be able tomatch the unit costs of AirAsia, the region'slower structural costs are available to allLCCs - so the real test of AirAsia Group willcome once the challenge from Asian LCCsincreases. With roughly the same unit costsas AirAsia Group, the other LCCs will be rac-ing to place capacity on the key Asia/Pacificroutes under ASEAN open skies - and so thekey indicator for AirAsia Group will be howits yields hold up as it places its massiveA320 order into the market.

A foretaste of what AirAsia Group will facewill be shown on the Kuala Lumpur-Singapore route, on which AirAsia started adaily service this February after the Malaysiaand Singapore governments partially easedthe restrictions on their existing air servicesagreement, in order to allow LCCs to operateon this key route against Singapore Airlinesand Malaysia Airlines.

All restrictions on the route will be lifted byDecember (when the open skies dealbetween the 10 ASEAN countries - whichhave a combined population of 500m - startsto come into effect). AirAsia had been lobby-ing hard to get onto this lucrative route, butwhile AirAsia Group is undercutting the lega-cy carriers' fares substantially, it also facescompetition from Jetstar Asia and TigerAirways (owned 49% by SIA), and as HSBCsays, "we anticipate Air Asia struggling torival the more efficient full service carriersand differentiating itself from the other lowcost carriers which will also gain access tothe routes". There may also be competitionfrom Firefly, a domestic LCC set up by MAS

Aviation StrategyBriefing

March 20088

that aims to launch international services,including Kuala Lumpur-Singapore.

Certainly until recently the AirAsia Grouphas faced little or no LCC competition in itsmain markets, but that is changing, and thiswill inevitably result in yield erosion. SIA'sTiger Airways, for example, started aSingapore-Kuala Lumpur route in Februarythis year, and has 58 A320s on order.

AirAsia Group faces other challenges too,including constraints at its key operationalbase, at Kuala Lumpur. An LCC terminalcosting US30m was only built in 2006, butnow that AirAsia has transferred all its opera-tions there from the main terminal (chargesare 40% lower at the LCC terminal than themain one), the LCC terminal has already fullyused up its capacity of 10m passengers ayear, and Malaysia Airports Holding (the gov-ernment-controlled airport operator) is franti-cally increasing the capacity to 15m at themoment. But that too is likely to prove insuf-ficient within a few years, so there are furtherplans to increase annual capacity to 30m.

Fuel challengePerhaps the biggest short-term challenge

to AirAsia Group comes from rising fuelprices. The group previously forecast higherprofits in 2007/08 as long as fuel price riseswere not too high - but this is exactly whathas happened, and to make matters worse,the group's management of this risk hasbeen nothing short of disastrous. Essentially,Air Asia Group sold call options that bet thatoil prices would not break through the US$90per barrel, but the group called this wrong,and one analyst predicts that Air Asia's"wrong" bets on the price is cutting groupprofits by around US$3m a month.Fernandes says that although in the pasthedging had "ultimately benefited the compa-ny", the current volatility of oil prices "is anightmare".

The group's wish to mitigate risk here isunderstandable, as each extra US$1 changein the actual price per barrel paid by AirAsiatranslates into a RM10m (US$3.1m) fall inprofits before tax, but the group's hedging ofthis risk has simply been erroneous.Additionally, the group's hedging policy has

led to some investors selling the group'sshares, leading to a 15% fall in the shareprice at the end of 2007, and to some down-grading by analysts.

AirAsia's senior executives were unhappyat the group's share price fluctuation in late2007, but although Fernandes says that "thestock market needs to understand AirAsiabetter", the market is only reflecting concernthat the group's derivative trading was welloutside its area of expertise.

Shareholders should also be concernedthat AirAsia Group is benefiting tremendous-ly from the weak US dollar, as only a tiny per-centage of its revenue is in dollars, whereasat least 60% of its costs are dollar based. Atsome point in the future that advantage maydisappear, and this will have a significantimpact on the profit level.

In the second quarter of 2007/08(October-December 2007 - although fromnow on the group will change its FY toJanuary-December) Air Asia Group recordeda 43% rise in revenue to RM 632.8m(US$197m), with operating profit of RM154.8m (US$48m), compared with RM86.8m in 2Q 2006/07. Net profit was RM245.7m (US$76m), compared with RM142.1m in 2Q 2006/07. It's an excellentresult, and furthermore the AirAsia Group isstrong financially. Cash and cash equivalentsstood at RM 426m (US$132m) at December31st 2007, while long-term debt rose fromRM 2.3bn (US$714m) at June 30th 2007 toRM 3.4bn (US$1.1bn) as at the end of 2007,thanks largely to aircraft purchases.

Nevertheless, it's the medium-term chal-lenge of placing the huge increase in capac-ity that is the real test of AirAsia Group'sstrategy. Though Fernandes says that risingcosts will slow the establishment of LCCs inthe region, he acknowledges that competi-tion is increasing. As the group's track recordhas shown, entering new markets will not beeasy, and Mark Webb of HSBC GlobalResearch says AirAsia yields are expected:"to remain flat amid a saturated domesticmarket and stiff competition outside Malaysia….if [Asian economic] growth slows signifi-cantly, AirAsia - with its aggressive expansionplans - may find itself unable to generate sus-tainable levels of return".

Aviation StrategyBriefing

March 20089

The prolonged and inept attempt to sellthe Italian state's remaining 49.9% stake

in Alitalia finally appears to be reaching aconclusion, with preferred bidder AirFrance/KLM set to complete the deal immi-nently. But although most analysts believethe Franco-Dutch group is the best acquirerof an airline that is losing at least €1m a day,has the ailing Italian flag carrier reallypicked the best white knight?

The need for Alitalia to be rescued isobvious. Today the airline employs 11,000and its fleet of 148 aircraft carried 24.6mpassengers in 2007, but despite this scaleand the prestige of being a flag carrier, theairline has racked up more than €3bn of netlosses since 2000 and last made an operat-ing profit back in 1998 (see charts, page12).

In 2007 Alitalia reported a 2.8% rise inrevenue to €4.9bn, with the operating lossfalling from €466m in 2006 to €203m in2007. While no net figure is available untilMay (Alitalia had a net loss of €626m in2006), at the pre-tax level the airline report-ed a €364m net loss in 2007, compared witha €605m pre-tax net loss in 2006. But thisreduction in losses was due largely to thefalling away of almost €200m of write-downs of aircraft values included in the2006 results. Ominously, Alitalia says its2007 net figure will include the result ofanother revaluation of its fleet, and thedirection of any adjustment will only bedownwards.

As at the end of 2007, Alitalia has short-term debt of €147m and long-term debt of€1,419m (see chart, right), and after cashand short-term financial credits of €367mare taken away, this leaves the group withnet debt of €1.2bn. Alitalia is believed tohave enough financial resources to keepgoing only until the summer of 2008, andcertainly does not have enough cash torepay €320m of debt due in 2008 and 2009.

Alitalia's yield fell 3.4% in 2007, thanks

largely to LCC competition, and the airlinenow warns that its 2008 financial results willbe worse than it previously forecast, whichwill mean even deeper cuts into its costbase.

The airline's management blames theusual problems of competition, labourunrest and high fuel costs for recent losses,but the underlying reason for Alitalia'sabysmal performance over the years hasbeen a combination of poor managementand weak leadership by the Italian govern-ment. Incredibly, Alitalia has had nine CEOsin 10 years and there have been at least fivemajor restructuring attempts at Alitalia since2003, each one associated with a differentset of top management. None have suc-ceeded, and in the meantime debts havemounted and the airline is losing at least€1m a day.

A new beginning?While its predecessors dithered, the cen-

tre-left government of Romano Prodi (elect-ed in May 2006) quickly decided to offloadthe government's remaining 49.9% stake inthe flag carrier. Yet the first Prodi attempt tosell the stake - by July 2007 - was a disas-ter and the government had no choice but tobegin the process all over again. MaurizioPrato, previously head of Fintecna - thestate holding company - was appointedpresident of Alitalia in August, and wasgiven a range of executive powers. Hedescribed Alitalia's condition as "comatose",and added that he had "been surprised bythe general refusal to accept the reality ofhow critical the situation is".

At the end of August a new plan wasunveiled for Alitalia. The so-called "plan forsurvival/transition" covers the 2008-2010period (and is being implemented fromMarch 2008) in an attempt to achieve anoperating profit in 2010. At its core is ashrinking of operations, with reductions in

Aviation StrategyBriefing

March 200810

Has Alitalia pickedthe right saviour?

routes and an unspecified number of jobcuts, with the airline admitting openly that itcannot continue to rack up the losses it iscurrently incurring.

In essence the plan admits that the air-line is weak strategically thanks to the poorgeographical position of Italy, where it haslittle catchment area other than Italy itself(and even here these catchment areas arewidely dispersed), and being sub-optimallyplaced for all the major international aviationsectors. The plan says it would be almostimpossible to close the competitive gap withits major rivals based on the realities ofAlitalia today, and if it did try to continue tocompete in all current routes and markets inan attempt to remain an independent hubairline, "the only result of this attempt wouldbe to confirm Alitalia's current role as a mar-ginal and 'regional' airline."

Therefore Alitalia believes it has nochoice but to scale down its operations,closing both short- and long-haul routeswhere there is no chance of making a profitin the short-term. This means building upthe Rome hub as the prime hub for Alitaliaat the expense of Milan Malpensa, which isbeing downgraded into a point-to-point air-port servicing routes not already covered byMilan Linate, and being used much more forAlitalia's LCC Volareweb and charter carrierAir Europe. According to Alitalia, "the com-pany is no longer able to operate efficientlyout of two hubs", but providing RomeFiumicino can cut its charges to Alitalia andimprove its infrastructure, Alitalia wouldincrease routes out of the Rome hub.

The survival plan also envisages a sig-nificant capital increase over that period bywhoever takes over the government's stake,since by 2010 the cash position would oth-erwise not be "adequate". When the 2007results were announced, the airline said itwould probably need at least €750m offresh capital in 2008 in order to maintainsufficient liquidity, and the situation will getworse if there are any further delays inimplementation of the planned restructuringof Alitalia.

How many redundancies this survivalplan will lead to was unknown at the time itwas unveiled, but not surprisingly the plan

attracted plenty of criticism within Italy, fromall political spectrums and from Alitalia'sunions. And it's this plan that has - contro-versially - effectively framed the govern-ment's second attempt to sell off its 49.9%stake, which Prato promised would be com-pleted by the end of 2007 given the extremeurgency of Alitalia's financial position. Withthe government sticking to its message thatit will not put any more funds into the airline,the explicit approval of the survival plan bythe government signalled that it now accept-ed a scaling down of Alitalia was inevitable,and that whoever buys Alitalia would begiven a free hand to do whatever they need-ed to. But with the government "presenting"such a plan as coming from Alitalia's man-agement, those who currently oppose theAir France/KLM bid complain bitterly (andwith some justification) that the governmenthas effectively pushed a contraction ofAlitalia as being the only possible agendafor a successful bidder.

The new attempt…For the latest attempt to sell the govern-

ment stake, the six short-listed candidatesnamed by Alitalia in November 2007 were:Aeroflot, Lufthansa, TPG, Air France/KLM,AP Holdings/Air One and a consortium ledby Antonio Baldassarre, an Italian lawyer.However, the process continued to beshambolic, with the deadline for the latestround of bids somehow slipping fromNovember to December. And by the reviseddeadline - December 7th - only three poten-tial acquirers remained. TPG withdrew inOctober when it could not put together an

Aviation StrategyBriefing

March 200811

-

500

1,000

1,500

2,000

2,500

2Q04

3Q-04

4Q04

1Q05

2Q05

3Q-05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

€mALITALIA GROUP DEBT

Medium/long-term debt

Short-termdebt

appropriate consortium with enough Italianpartners, while Aeroflot withdrew inNovember, saying that acquiring Alitaliawould be unprofitable. Lufthansa - whichwas widely expected to enter the formal bid-ding process - at the last minute didn't makea bid, stating that "the risks outweighed thepositives" and that any investment in itsSkyTeam partner would affect Lufthansainvestment rating negatively.

The list of potential acquirers was downto three: Air France/KLM, AP Holdings/AirOne and the Baldassarre consortium (head-ed by Antonio Baldassarre, who was previ-ously chairman of RAI, the state televisionstation), the latter of which had little chanceof success, given its lack of aviation experi-ence.

The original plan was to narrow the fieldof three down to one for exclusive negotia-tions by mid-December but - unsurprisingly- after yet another delay, on December 28thAlitalia's board of directors unanimouslychoose Air France/KLM as their preferredbidder, citing its "highly credible" businessplan - a plan remarkably similar to the sur-

vival plan unveiled by Alitalia back inAugust.

Unconfirmed Italian reports suggestedPrato threatened to resign if Air France/KLMwas not chosen as the preferred bidder(which perhaps explains the unanimousnature of the decision by the Alitalia board),and the decision was fully backed by theProdi government. While Prodi had previ-ously said that best bidder should winAlitalia regardless of its "nationality", thefinance minister declared the APHoldings/Air One bid was "excessively opti-mistic"; while other government sourceshinted that an Air One deal may have led toantitrust problems.

An eight-week exclusive negotiationperiod between the two airlines formallybegan on January 11th, (expiring on March11th) at the end of which the governmenthopes agreement on the details of the dealwill have been reached, with AirFrance/KLM then taking up its option to sub-mit a binding offer to buy the 49.9% stake,subject to approval by the government.

The Air France/KLM bidAir France/KLM's shares rose sharply

after its bid was confirmed, a reflection ofthe airline's close links with Alitalia and thegeneral opinion of investors that a merger ofthe two SkyTeam partners makes sense.Essentially, the Franco-Dutch group - whichalready owns 2% in Alitalia, acquired backin 2003 - offers Alitalia scale, deep pocketsand the experience of integrating KLM, andthe deal delivers significant political capitaland kudos to the Italian governmentthroughout the EU.

Air France/KLM promises a large expan-sion of routes out of Rome Fiumicino, mak-ing it the third hub for the group and provid-ing a southern European base alongsideParis CDG and Schiphol. Alitalia would pro-vide Air France/KLM feed out of the Italiandomestic market, as well as on routes tosouthern and central Europe, and down tonorth Africa. While there would continue tobe some medium-and long-haul servicesout of Milan, Malpensa would no longer bea major hub airport, and Air France/KLM

Aviation StrategyBriefing

March 200812

4,000

4,500

5,000

5,500

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

€m ALITALIA GROUP REVENUE..

-1,000

-800

-600

-400

-200

0

200

400

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

€m ..AND FINANCIAL RESULTS

Operatingresult

Net result

says it would support Alitalia's plan toexpand Volareweb flights out of Milan. WithAlitalia saying that 92% of passengers orig-inating from northern Italy do not useMalpensa as their departure airport for long-haul flights, Air France/KLM says that "if theMalpensa hub is not significantly down-sized, we don't see a reason for a deal".

Jean-Cyril Spinetta, CEO of AirFrance/KLM, says that "a big majority" ofAlitalia's losses arise from the Malpensaoperation, with the other major source oflosses being long-haul routes. Under AirFrance/KLM's plans, Italian passengers toNorth America could travel via Amsterdamand Paris, allowing Alitalia's long-haul oper-ation to refocus on eastward routes to theMiddle East and Asia.

With reductions at Malpensa and onlong-haul, Air France/KLM plans 1,700 jobcuts at Alitalia, equivalent to 15% of the11,000 workforce - although the governmentis making it clear that it will finance unem-ployment benefits for those made redun-dant.

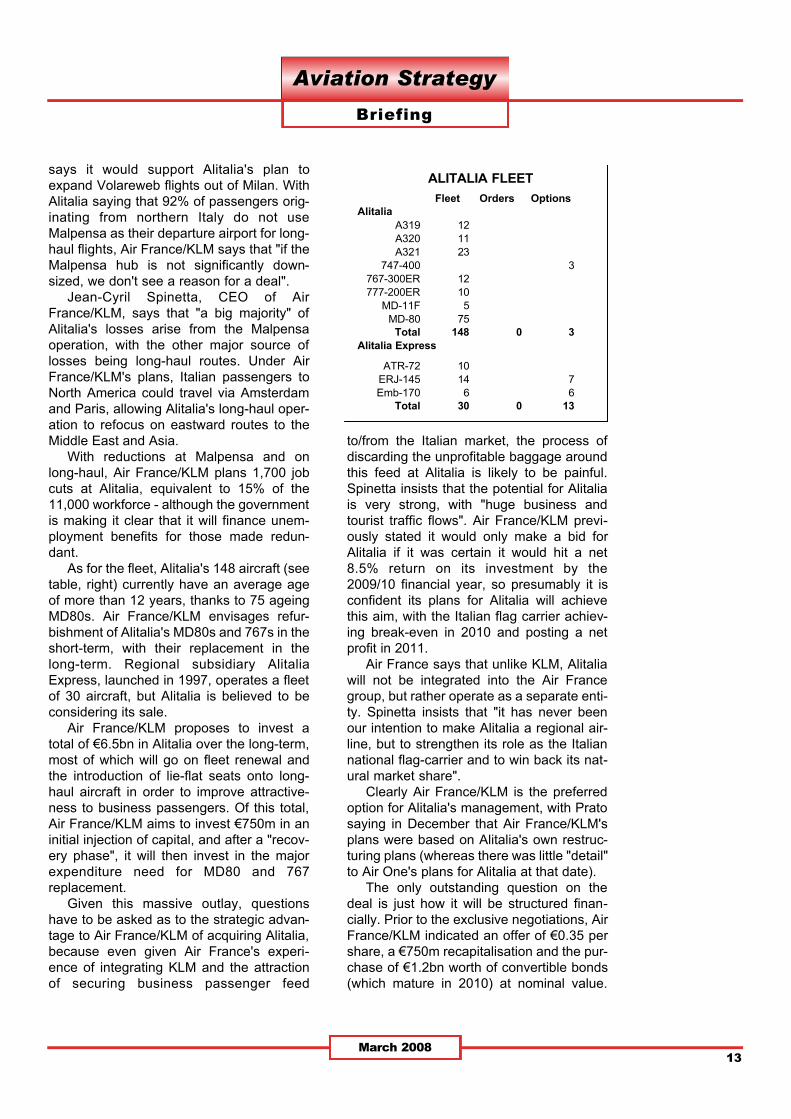

As for the fleet, Alitalia's 148 aircraft (seetable, right) currently have an average ageof more than 12 years, thanks to 75 ageingMD80s. Air France/KLM envisages refur-bishment of Alitalia's MD80s and 767s in theshort-term, with their replacement in thelong-term. Regional subsidiary AlitaliaExpress, launched in 1997, operates a fleetof 30 aircraft, but Alitalia is believed to beconsidering its sale.

Air France/KLM proposes to invest atotal of €6.5bn in Alitalia over the long-term,most of which will go on fleet renewal andthe introduction of lie-flat seats onto long-haul aircraft in order to improve attractive-ness to business passengers. Of this total,Air France/KLM aims to invest €750m in aninitial injection of capital, and after a "recov-ery phase", it will then invest in the majorexpenditure need for MD80 and 767replacement.

Given this massive outlay, questionshave to be asked as to the strategic advan-tage to Air France/KLM of acquiring Alitalia,because even given Air France's experi-ence of integrating KLM and the attractionof securing business passenger feed

to/from the Italian market, the process ofdiscarding the unprofitable baggage aroundthis feed at Alitalia is likely to be painful.Spinetta insists that the potential for Alitaliais very strong, with "huge business andtourist traffic flows". Air France/KLM previ-ously stated it would only make a bid forAlitalia if it was certain it would hit a net8.5% return on its investment by the2009/10 financial year, so presumably it isconfident its plans for Alitalia will achievethis aim, with the Italian flag carrier achiev-ing break-even in 2010 and posting a netprofit in 2011.

Air France says that unlike KLM, Alitaliawill not be integrated into the Air Francegroup, but rather operate as a separate enti-ty. Spinetta insists that "it has never beenour intention to make Alitalia a regional air-line, but to strengthen its role as the Italiannational flag-carrier and to win back its nat-ural market share".

Clearly Air France/KLM is the preferredoption for Alitalia's management, with Pratosaying in December that Air France/KLM'splans were based on Alitalia's own restruc-turing plans (whereas there was little "detail"to Air One's plans for Alitalia at that date).

The only outstanding question on thedeal is just how it will be structured finan-cially. Prior to the exclusive negotiations, AirFrance/KLM indicated an offer of €0.35 pershare, a €750m recapitalisation and the pur-chase of €1.2bn worth of convertible bonds(which mature in 2010) at nominal value.

Aviation StrategyBriefing

March 200813

Fleet Orders OptionsAlitalia

A319 12A320 11A321 23

747-400 3767-300ER 12777-200ER 10

MD-11F 5MD-80 75

Total 148 0 3Alitalia Express

ATR-72 10ERJ-145 14 7Emb-170 6 6

Total 30 0 13

ALITALIA FLEET

But although Alitalia's shares have plungedover the last year (see chart, page 15), theyare still substantially above €0.35 per share,so it's no surprise that the governmentwants Air France/KLM to increase its bid. InFebruary Air France/KLM said it wouldinvest €3bn in Alitalia over the next five orsix years (and €6.5bn in the long-term), andthat it wanted to acquire 100% of the airlineand then de-list it, subject to agreement bythe Italian government to make a full bid.

Given this level of investment andAlitalia's current financial position, a sub-stantial increase in Air France/KLM's bid isunlikely. A way out of this problem may be ashare swap, which is being considered byboth the government and Air France/KLM.Unconfirmed reports say that the govern-ment's stake in Alitalia could be exchangedfor a 3% stake in the enlarged AirFrance/KLM/Alitalia, and this could evenrise to 5% if Alitalia bought back the gov-ernment's 51% stake in Servizi, the formerAlitalia engineering and ground servicesdivision that is now owned 51% by stateholding company Fintecna.

Servizi employs 8,500 and Alitalia'smanagement is urging the Franco-Dutchgroup to reintegrate the ground servicesbusiness, but whether Air France/KLMwould really want to be burdened with a100% stake in the service unit (which someanalysts believe is substantially over-manned) remains to be seen.

AP HoldingsThe bid from Italian LCC Air One for

Alitalia is being carried out through APHoldings, its parent company, which is in aconsortium that also includes four banks -Italian-based retail bank Intesa Sanpaolo, aswell as Nomura, Goldman Sachs andMorgan Stanley.

Carlo Toto, chairman and founder ofRome-based Air One, says that its bid forAlitalia would "preserve its national identity",although it is rumoured that an Air One-con-trolled Alitalia might draw close to Lufthansain the future (speculation that in Januaryprompted Lufthansa to deny it would be join-ing the Air One bid for Alitalia).

Air One's ambitious five-year plan forAlitalia targets a breakeven in 2009 and aprofit in 2010, with the consortium investingup to €4bn in the airline, largely for medium-haul fleet renewal that would be at the heartof an expansion of business routes out ofRome-Fiumicino. But in contrast with AirFrance, Air One says that Milan Malpensawould remain a hub airport under its plans,which envisage an eventual Alitalia fleet of215-222 aircraft.

While there would be 40 long-haul air-craft, Alitalia's long-haul slots might be soldoff unless they complemented or enhancedAir One's existing plans to launch long-haulroutes in 2008. Up to 20 long-haul aircraft willbe leased by Air One over the next four orfive years, with approximately four new air-craft a year entering its fleet.

Key to Air One's initial plans for the flagcarrier would be renewal of Alitalia's regionaland medium-haul A320 and A330 fleet, withup to 130 new aircraft coming in at a cost of€3bn. In particular, Air One is looking to shoreup Alitalia's domestic market share, whichhas fallen to 40% (compared with the 25% ofAir One), and there would be rationalisationwith Air One's existing domestic network. AirOne has 90 A320s on order, and with theplanned new aircraft for Alitalia, an AirOne/Alitalia group would have large amountsof new aircraft coming on stream over thenext few years.

Air One indicated that Alitalia's interna-tional services would be run primarily onpoint-to-point routes between Italian andEuropean destinations, while businessroutes will be concentrated on MilanMalpensa and leisure routes at RomeFiumicino - although the number of routeswill be roughly equal out of each of these air-ports. By integrating the networks of Alitaliaand Air One, AP Holdings says it will take16% out of Alitalia's cost base. Its forecastssee revenue reaching €6.2bn by 2012 (withpassengers carried of 34.4m), with an EBITin that year of €375m.

But AP Holdings is offering just €0.01 foreach Alitalia share, well below the currentshare price and the Air France/KLM offer,although this is a more sensible price thanthe Air France/KLM bid as it allows AP to

Aviation StrategyBriefing

March 200814

maximise investment on the airline going for-ward.

Still in the gameAlthough Alitalia's choice of Air

France/KLM was a huge blow to the APHoldings consortium, Carlo Toto is still confi-dent that his bid is not yet dead as hebelieves it is in the best long-term interests ofthe airline and the country, and there arereports of at least five new private investorsjoining the bid since the start of 2008.

Indeed while senior Alitalia managementand most of the Prodi government prefers theAir France/KLM bid, and while Air One's bidto buy its much bigger rival appears to bevery ambitious, AP Holdings does have somekey allies on its side: the unions (althoughsome of them are now starting to come roundto supporting Air France/KLM, after the lat-ter's lobbying offensive), most of the Alitaliaworkforce and some powerful political forces,such as the Lombardy regional government.This support is based on Air One's plans tomaintain the size of the Milan Malpensaoperation, even though Air One says that itwould still need to cut a substantial amount ofpositions at Alitalia (though less than AirFrance/KLM).

Air One has long been interested inexpanding its presence in Milan's airportsand has been a fierce critic of Alitalia'stakeover of the collapsed Italian Volare groupin July 2006. Although the Italian regulatorruled that Alitalia had to give up four pairs ofslots at Milan Linate as a condition of itsapproval, that did not satisfy Air One, whichhas been pursuing the case legally eversince.

In the latest twist, in early March anItalian appeals court agreed with Air One andruled that a new tender must be held forVolare. But Volare, which includes chartercarrier Air Europe and LCC Volareweb, hasalready been absorbed into Alitalia as itsresponse to the challenge of the LCCs, andVolareweb is now expanding fast, with itscurrent fleet of four A320s set to increase to10 by the summer of 2008, most of which arelikely to be A319s. It's clear that if Air Oneloses out to Air France/KLM, then it will battle

hard against expansion of Volareweb opera-tions at Milan Malpensa - notwithstanding therecent court ruling, which may completelythrow the future of Volare into doubt again.

The future?If - as seems likely - the Italian govern-

ment's 49.9% stake is bought by AirFrance/KLM, the future for Alitalia will stillremain uncertain. Most pressingly, the AirFrance bid has divided Alitalia staff, and theunions at Alitalia may react badly to the newowners of the flag carrier. Securing a dealwith staff is the number one priority for AirFrance/KLM, and Spinetta has already metAlitalia unions, including the key UGL union,since if they cannot be persuaded of themerit of an Air France/KLM takeover thenindustrial action to prevent the cut-backs ofroutes and staff is inevitable.

But assuming a scenario of labour unrestdoesn't happen, a key problem for Alitalia/AirFrance/KLM will be what the competitiondoes at Milan Malpensa as Alitalia reducesits presence at the airport. Air One is likely topile into Malpensa if the flag carrier leavesthe door open there, and just how many ofthe slots will be turned over to Alitalia's char-ter or LCC operation remains to be seen:LCC subsidiary Volareweb is already startingto increase European routes out of Milan, butfollowing the release of Alitalia's summerschedule, slots Alitalia is no longer using atMalpensa have been released back to the

Aviation StrategyBriefing

March 200815

0.5

0.6

0.7

0.8

0.9

1.0

1.1

1.2

€ ALITALIA SHARE PRICE

airport operator - which is infuriating oppo-nents of Alitalia's strategy.

While Alitalia's summer schedule is basedaround the Rome Fiumicino hub, even atRome some routes have been closed (suchas to Shanghai, Mumbai and Delhi on long-haul, and to Zagreb, Minsk, Lyon andCopenhagen in Europe), although frequencyis being increased at certain other routes.From the summer Alitalia will operate to 83destinations, of which 77 are served out ofRome, 38 from Milan Malpensa and 18 fromMilan Linate.

More worrying perhaps for Alitalia is thespectre of Ryanair, which has ambitious plansfor Milan Malpensa. The LCC is urging theairport to turn itself into a low-cost hub, andpromises hundreds of millions of Euros ofinvestment into Malpensa if the airport doesso. Ryanair has long been keen to win morepassengers within and to/from Italy, and inDecember 2007 Ryanair asked the EuropeanCommission to block Air France/KLM's bid forAlitalia until both airlines pay back a total of€2.7bn in "illegal state aid" from the Italianand French governments (of which the Alitaliaportion is €1.7bn).

If the Air France/KLM deal does go ahead,regional politicians in the north of Italy maywell persuade the airport to open itself up toAir One or even Ryanair, and while this willsecure local jobs, substantial competition outof Milan Malpensa would have unknowneffects on Air France/KLM's projections forAlitalia. The threat to Alitalia of Malpensabeing opened up became even more likelyonce a small but key political partner left thecentre-left government coalition in January,leaving Prodi without a working majority in theItalian senate. That development hit the shareprice of Alitalia in January and it fell by almost10% on one day, prompting a brief suspen-sion on the Milan market. As of early Marchthe share price had dipped under €0.6, givingAlitalia a market cap of around €820m.

The election...Alitalia insists the talks with Air

France/KLM will not be affected by the uncer-tainty over the future of the Prodi govern-ment, but with a general election scheduled

for April 13th and 14th, the political impera-tive has shifted. The centre-right parties areahead in the opinion polls, and they are firm-ly opposed to Air France/KLM's takeover.Forza Italia - the largest centre-right wingparty, led by Silvio Berlusconi - is very criticalof the current situation, and may preferAlitalia to go bankrupt and for a new nationalairline to be launched with new labour agree-ments. Another right-wing party is theNorthern League, which is fiercely opposedto Alitalia cutting back its presence at MilanMalpensa. AP Holdings/Air One's hopes aretherefore not yet dead even though a legalchallenge launched in January by AP Holdingagainst the government's decision to allowexclusive negotiations between Alitalia andAir France/KLM was rejected by an Italiancourt in late February (although that decisionis being appealed by AP).

Crucially (and slightly confusingly) in mid-February Air France/KLM said that while itwill make a decision on whether to make abinding offer by mid-March (well before theItalian general election in mid-April) it addedthat it would only go ahead with the deal if thenew Italian government approved theFranco-Dutch takeover, which might not hap-pen if the centre-right coalition wins the elec-tion.

In any case, while Air France/KLM hasexperience of going through a mergerprocess before, and this is likely to make itaggressive in cutting back Alitalia into theshape it needs to fit into the new Alitalia/AirFrance/KLM giant, the advantages of the APHoldings/Air One bid may have been under-estimated by many analysts.

Crucially, under AP Holdings the airlinewould retain the goodwill of unions and politi-cians alike, and the changes that still need tobe made at Alitalia could be carried out in afar less aggressive and much more achiev-able way by Italian owners than by AirFrance/KLM. With short-term financial andlabour stability assured, an Air One-ownedAlitalia would then be in a much strongerposition to link up (even with equity) with oneof Europe's larger airlines - and preferablyLufthansa. The Air France/KLM bid may offerscale and kudos, but it may not necessarilybe the best option in the long-term for Alitalia.

Aviation StrategyBriefing

March 200816

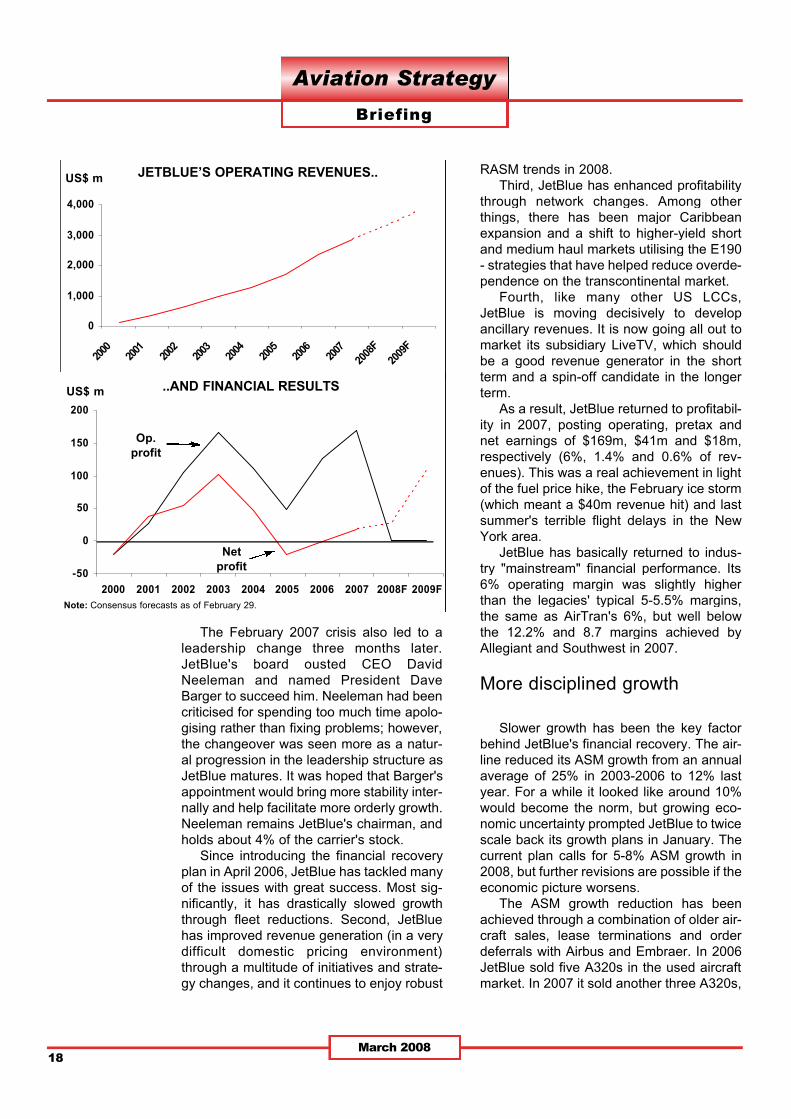

JetBlue Airways, the largest of the new-generation US LCCs, is in the middle of

a financial turnaround, thanks to two yearsof restructuring and strategy refinements.The New York City-based airline hasretained its superior product and low coststructure, but in other ways it looks very dif-ferent: a new leadership team, more sophis-ticated revenue management, a disciplinedgrowth strategy, new types of markets and afocus on high-yield passengers and interna-tional alliances. Will this new type of hybridLCC/traditional model work for JetBlue?

JetBlue, which commenced operationsfrom New York JFK in February 2000, hadperfect credentials: ample start-up funds, astrong management team and a promisinggrowth niche. It succeeded in attainingSouthwest's efficiency levels, despite itshigh-cost Northeast environment, muchsmaller fleet and a more up-market product.JetBlue became profitable after only sixmonths of operation and went on to achievespectacular 17% operating margins in 2002and 2003.

With its new A320 fleet, state-of-the-arttechnology and superior in-flight product,JetBlue also set new standards in airlineservice quality in the US. Like Southwest, itquickly built a "cult following", which hasenabled it to attract price premiums andconsiderable customer loyalty.

JetBlue also grew extremely rapidly,achieving "major carrier" status, with $1bn-plus annual revenues, in 2004 - its fifth yearof operation, which is by far the fastest-trackto a major ever seen in the US. Last yearJetBlue had $2.8bn of revenues, making itthe eighth largest US passenger carrier.

However, after the spectacular start,JetBlue stumbled financially just as the restof the US airline industry began to see lightat the end of the tunnel. In two years,JetBlue literally went from the industry'sbest to worst in terms of financial results. Itsoperating margin plummeted from 17% in

2003 to 8.8% in 2004 and 2.8% in 2005.2005 and 2006 saw net losses of $20m and$1m, respectively.

The main reason for the losses, ofcourse, was the hike in fuel prices. Likemost US airlines, JetBlue did not have sig-nificant fuel hedges in place. Like otherLCCs, JetBlue also found it harder than thelegacies to deal with the weak domesticpricing environment. It had no lucrativeinternational operations. Its simple pricingmodel meant that it had few fare buckets toplay with. And its aggressive growth planrequired it to focus on filling aircraft ratherthan pricing for profitability.

JetBlue was the fastest-growing US LCCin the first half of this decade. It continued togrow ASMs by 21-25% annually in 2005 and2006, despite the financial losses, becausethere was no demand problem and becauseit did not want to forego good growth oppor-tunities.

Although JetBlue began to tackle itsproblems in the spring of 2006 with a "returnto profitability" plan, the most visible actionscame following an operational meltdown onValentine’s Day in February 2007 that high-lighted serious shortcomings in the airline'sability to deal with operational issues. An icestorm in the Northeast grounded 1,000-plusflights, and because JetBlue had a policy ofnot cancelling flights ahead of bad weather,thousands of people were trapped in aircraftfor hours or stranded in terminals for days.JetBlue did not fly a full schedule for days.There was a massive outcry from air trav-ellers and calls from Congress for legisla-tion to protect passengers' rights.

JetBlue averted the crisis - and fortu-nately suffered no lasting negative impacton image or customer loyalty - by takingdecisive action. The airline made importantchanges in the way it responds to weatherand other operational irregularities, draftedits own "customer bill of rights" andstrengthened its operations team.

Aviation StrategyBriefing

March 200817

JetBlue: slower growthand new revenue strategies

The February 2007 crisis also led to aleadership change three months later.JetBlue's board ousted CEO DavidNeeleman and named President DaveBarger to succeed him. Neeleman had beencriticised for spending too much time apolo-gising rather than fixing problems; however,the changeover was seen more as a natur-al progression in the leadership structure asJetBlue matures. It was hoped that Barger'sappointment would bring more stability inter-nally and help facilitate more orderly growth.Neeleman remains JetBlue's chairman, andholds about 4% of the carrier's stock.

Since introducing the financial recoveryplan in April 2006, JetBlue has tackled manyof the issues with great success. Most sig-nificantly, it has drastically slowed growththrough fleet reductions. Second, JetBluehas improved revenue generation (in a verydifficult domestic pricing environment)through a multitude of initiatives and strate-gy changes, and it continues to enjoy robust

RASM trends in 2008.Third, JetBlue has enhanced profitability

through network changes. Among otherthings, there has been major Caribbeanexpansion and a shift to higher-yield shortand medium haul markets utilising the E190- strategies that have helped reduce overde-pendence on the transcontinental market.

Fourth, like many other US LCCs,JetBlue is moving decisively to developancillary revenues. It is now going all out tomarket its subsidiary LiveTV, which shouldbe a good revenue generator in the shortterm and a spin-off candidate in the longerterm.

As a result, JetBlue returned to profitabil-ity in 2007, posting operating, pretax andnet earnings of $169m, $41m and $18m,respectively (6%, 1.4% and 0.6% of rev-enues). This was a real achievement in lightof the fuel price hike, the February ice storm(which meant a $40m revenue hit) and lastsummer's terrible flight delays in the NewYork area.

JetBlue has basically returned to indus-try "mainstream" financial performance. Its6% operating margin was slightly higherthan the legacies' typical 5-5.5% margins,the same as AirTran's 6%, but well belowthe 12.2% and 8.7 margins achieved byAllegiant and Southwest in 2007.

More disciplined growth

Slower growth has been the key factorbehind JetBlue's financial recovery. The air-line reduced its ASM growth from an annualaverage of 25% in 2003-2006 to 12% lastyear. For a while it looked like around 10%would become the norm, but growing eco-nomic uncertainty prompted JetBlue to twicescale back its growth plans in January. Thecurrent plan calls for 5-8% ASM growth in2008, but further revisions are possible if theeconomic picture worsens.

The ASM growth reduction has beenachieved through a combination of older air-craft sales, lease terminations and orderdeferrals with Airbus and Embraer. In 2006JetBlue sold five A320s in the used aircraftmarket. In 2007 it sold another three A320s,

Aviation StrategyBriefing

March 200818

0

1,000

2,000

3,000

4,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

F20

09F

-50

0

50

100

150

200

2000 2001 2002 2003 2004 2005 2006 2007 2008F 2009F

US$ m

Note: Consensus forecasts as of February 29.

..AND FINANCIAL RESULTS

Op.profit

Net profit

US$ m JETBLUE’S OPERATING REVENUES..

returned one leased A320, deferred fourA320 deliveries from 2009 to 2012 anddeferred 16 E190 deliveries from 2007-2012to 2013 and beyond. In January JetBlue dis-closed that it had deferred the delivery of 16A320s from 2010-2011 to 2012-2013. It alsocurrently has commitments to sell six A320sin 2008 and is open to selling more, if nec-essary.

The airline also intends to managecapacity through aircraft gauge reductions(substituting E190s for the A320s) and byreducing utilisation in off-peak periods.JetBlue is lucky to have one of the highestaircraft utilisation rates in the industry - stillaveraging 12.8 hours daily on the A320s -which gives it flexibility in the current fuelenvironment.

The A320 and E190 options help JetBluemaintain flexibility to accelerate fleet growthand respond to market opportunities. Forexample, in December the airline exercisedthree E190 options for 2009 delivery.

JetBlue is scheduled to take delivery of12 A320s and six E190s this year. Assumingsix A320s are sold, the year-end 2008 fleetwould be 110 A320s and 36 E190s.Including the effects of the January Airbusorder amendments, at the end of 2007JetBlue had 70 A320s and 74 E190s on firmorder for delivery through 2015, plus 32A320 options and 91 E190 options for 2009-2015 delivery. The firm order deliveriesamount to 18-25 annually in the next sixyears.

Improved revenue generation

The April 2006 recovery plan instigatedfundamental changes to JetBlue's revenuestrategy. In David Neeleman's words at thattime, fuel simply changed the way the airlinelooked at the world. The premise of the pre-vious model, which worked well when crudeoil was at $20-30 a barrel, was to keep costsand prices low and make substantial profitson volume and growth. Now the time hadcome to sacrifice some load factor to theyield.

The aim was to get the system averagefare of $105 up by "a few more dollars" to

cover the increase in fuel prices. JetBlue didnot want to change its low fare structure;rather, it wanted to improve the fare mix.

This meant a move towards convention-al yield management and more complexityin the pricing model - strategies thatEuropean LCCs like Ryanair have usedsuccessfully since their inception. JetBlueupgraded its yield management systemsand revamped its revenue managementteam. The spring and summer of 2006 sawa multitude of revenue initiatives, includingselective capacity cuts, scheduling adjust-ments, adjustments to fare buckets, elimina-tion of some of the cheapest fares and newcorporate booking tools.

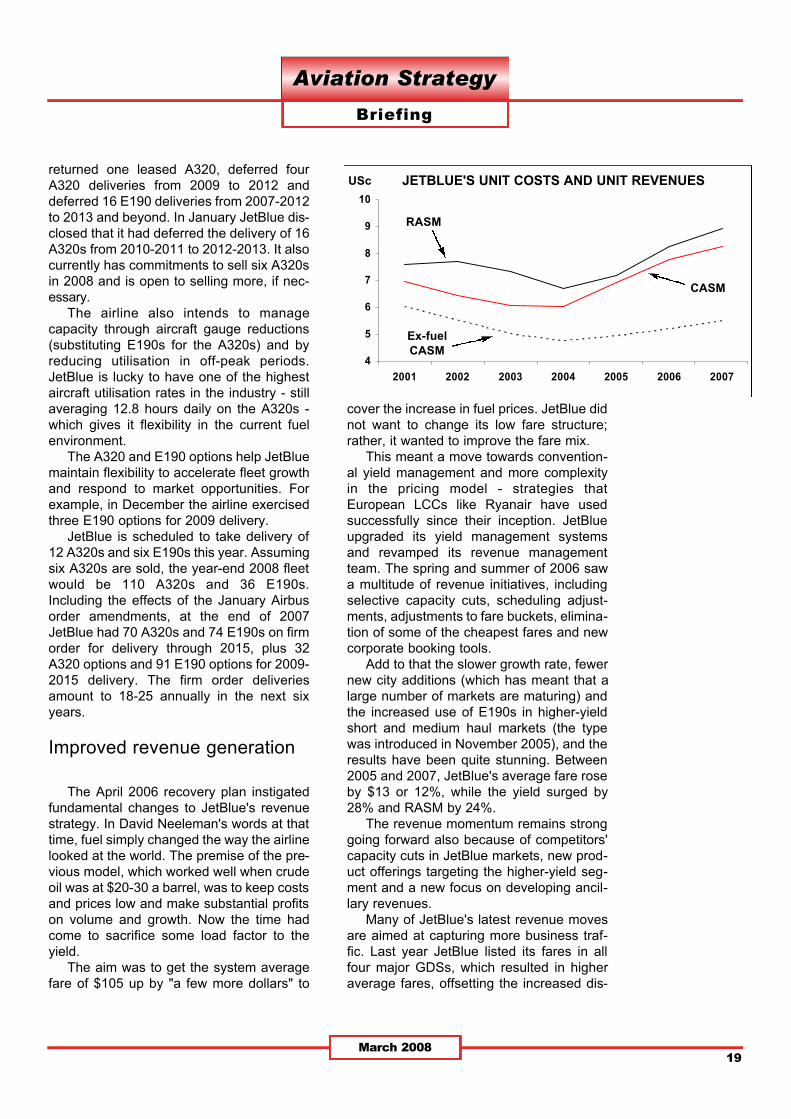

Add to that the slower growth rate, fewernew city additions (which has meant that alarge number of markets are maturing) andthe increased use of E190s in higher-yieldshort and medium haul markets (the typewas introduced in November 2005), and theresults have been quite stunning. Between2005 and 2007, JetBlue's average fare roseby $13 or 12%, while the yield surged by28% and RASM by 24%.

The revenue momentum remains stronggoing forward also because of competitors'capacity cuts in JetBlue markets, new prod-uct offerings targeting the higher-yield seg-ment and a new focus on developing ancil-lary revenues.

Many of JetBlue's latest revenue movesare aimed at capturing more business traf-fic. Last year JetBlue listed its fares in allfour major GDSs, which resulted in higheraverage fares, offsetting the increased dis-

Aviation StrategyBriefing

March 200819

4

5

6

7

8

9

10

2001 2002 2003 2004 2005 2006 2007

JETBLUE'S UNIT COSTS AND UNIT REVENUESUSc

RASM

CASM

Ex-fuelCASM

tribution costs. In January the airlinelaunched refundable fares - a fare class witha $50-100 premium for passengers needingextra flexibility.

In the second quarter JetBlue will unveila new "front cabin" product, aimed at mon-etising the increased pitch on its A320sespecially against competitors such asVirgin America. About a year ago, JetBlueremoved a row of seats from its A320s,reducing the seating from 156 to 150, whichenabled it to operate the aircraft with two(rather than three) flight attendants. Thereconfiguration also meant that seats in thefirst 11 rows (44% of total seats) have anindustry-leading 36-inch pitch, while theremaining seats have at least 34-inch pitch.JetBlue planned to reserve some of thefront seats for last-minute or first-class typecustomers and said that it would later rollout "exciting programmes" to boost rev-enues. The product to be unveiled in thecoming months is the result of those efforts.It will not involve removing more seats fromthe A320s.

JetBlue's management has indicatedthat developing ancillary revenues will be amajor focus in 2008. Last year the airlineincreased its change fees, began collectinga $10 fee for reservations over the phoneand launched a "cashless cabin", which willprovide a platform for further developingsales onboard aircraft. The result was anencouraging 50% increase in "other" rev-enues in 2007. Like Southwest, JetBlueneeds to invest in some technologicalenhancements to be able to fully meet itsancillary revenue goal.

Selling LiveTV products to other airlinesis a highly promising "other" revenuesource. A wholly owned subsidiary thatJetBlue acquired in 2002, LiveTV had $40mrevenues in 2007. At year-end contractswere in place with seven airlines, involving372 aircraft.

Until recently, JetBlue was careful not togive direct competitors access to the prod-uct; however, Continental, JetBlue's primarycompetitor in New York, is now the latestLiveTV customer, having signed a long-termcontract for its 737s and 757-300s. This rep-resents an interesting shift of strategy on

JetBlue's part. CEO Dave Barger explainedrecently that JetBlue believed that domesticpassengers in the US would soon expectsome form of in-flight entertainment andconnectivity on flights, so having a LiveTV-type product would be necessary just tokeep up with competition. Since the productno longer offers a distinct competitiveadvantage, JetBlue has decided to beginaggressively pursuing sales opportunitieswith any airlines.

Unique business modelIn the past couple of years, it has often

been suggested that JetBlue is movingtowards a conventional business model,"toward something decidedly traditional", asone analyst put it. Multiple fleet types, mod-est growth, GDS participation, internationalpartners, emphasis on high-yield passen-gers and refundable tickets all point in thatdirection.

However, JetBlue has always beenupscale and it remains one of the lowest-cost US carriers and committed to low fares,so nothing has fundamentally changed.

JetBlue's key value proposition and mar-keting message, as stated in its 2007 annu-al report, is the same it has always been:"Low fares and quality air travel need not bemutually exclusive". And as CEO DaveBarger put it recently, "our ability to deliverexceptional service at a low cost differenti-ates us from the rest of the industry".

Back in October, Barger stressed thatJetBlue remained a "discretionary airline, aleisure airline by and large" but that therewere opportunities to "mine the corporatecustomer" and that JetBlue needed to goafter those opportunities.

JetBlue is merely doing what it needs todo to remain viable in the current fuel envi-ronment. Southwest is moving in the samedirection, one difference being that it needsto move cautiously because of its egalitari-an image. AirTran, in turn, has had a busi-ness class product for about a decade.

That said, JetBlue does seem to have abrisker attitude to doing business than theother LCCs - its CEO has used the term"can do" airline. It is less averse to doing

Aviation StrategyBriefing

March 200820

unusual deals, such as accepting an invest-ment from Lufthansa.

JetBlue has not departed from itsSouthwest-style growth strategy of focusingon markets that have high average faresand then stimulating demand with lowfares.

Most significantly, JetBlue has retainedits low cost structure, despite the increasingmix of the shorter-haul E190s in the fleetand rising A320 maintenance costs, in addi-tion to the fuel price pressures. Asset andlabour productivity are high and the lattercontinues to improve. The managementbelieves that the cost initiatives launched in2006 have "helped institutionalise JetBlue'slow-cost culture". That said, AirTran hasabout 10% lower CASM on a stage lengthand density adjusted basis.

Route network strategy

JetBlue is primarily a point-to-point car-rier, earning 90% of its revenues from suchoperations in 2007. Most of the flights areto or from New York JFK or the other focuscities of Boston, Fort Lauderdale, LongBeach and Washington DC. The carrierserves about 53 cities in 21 states, PuertoRico, Mexico and the Caribbean.International services accounted for 4% oftotal revenues last year.

Route expansion in the past couple ofyears has had three main themes. First,there has been significant Caribbeanexpansion. Second, there has been a mod-est shift away from transcontinental to shortand medium haul routes, associated withthe introduction and growth of the E190fleet (though just last month JetBlueannounced significant new transcon andWest Coast expansion). Third, JetBlue isincreasingly overflying JFK due to conges-tion issues; for example, operating upstateNY to Florida point-to-point services withthe E190s.

However, JetBlue is also determined tomaintain its leading position in New York. Inaddition to growing JFK outside the dailypeak periods, it has added service fromLaGuardia and Newark, as well as the two

satellite airports of Stewart Field andWestchester County. About 66% of its dailyflights have one of those airports as eitherorigin or destination.

As a result of the new strategies, in thepast two years East-West services' share ofJetBlue's total capacity has fallen from55.1% to 47.4%, while Caribbean's sharehas increased from 6.4% to 10.6%.Northeast-Florida has declined slightly from33.5% to 31.8%.

Reflecting its more disciplined approachto route profitability, JetBlue is, first of all,adding fewer new cities. After launching 16new destinations in 2006, last year saw justfive and 2008 will also see only five. Thefocus will be on connecting the dots andboosting frequencies. Second, as a resultof a network profitability review, JetBluerecently exited two cities (Nashville andColumbus) and discontinued FortLauderdale-Oakland service.

The Caribbean expansion has beenfrom JFK, Boston, Fort Lauderdale andOrlando and has taken JetBlue to placessuch as Cancun in Mexico, Bermuda, SanJuan, Santo Domingo and Aruba. JetBluecalls the Caribbean "a natural out of NewYork". The markets are strong, have year-round demand, have matured quickly, gen-erally require minimal up-front capital and,in spite of limited daily frequencies, are rel-atively low-cost.

Encouraged by the Caribbean experi-ence, JetBlue has applied to serve Bogota(Colombia) from both Fort Lauderdale andOrlando (pending approval). It would be thefirst US LCC in that competitive market.JetBlue is not planning major expansioninto South America but believes that thereare opportunities for an LCC to serve theregion from the Northeast or Florida.

Both the A320 and the E190 are over-water-equipped, long range aircraft.JetBlue believes that the E190, with itsnear-2,000-mile range, is "perfectly situat-ed as a pathfinder in many of those mar-kets, say Florida-Caribbean". The airline isalso considering utilising the E190 in off-peak periods in the Caribbean.