documentas

DESCRIPTION

sdsdTRANSCRIPT

Negotiations and Agreements VUB Advanced Starter Seminars

By Mike Truyen (Eubelius) 9 October 2014

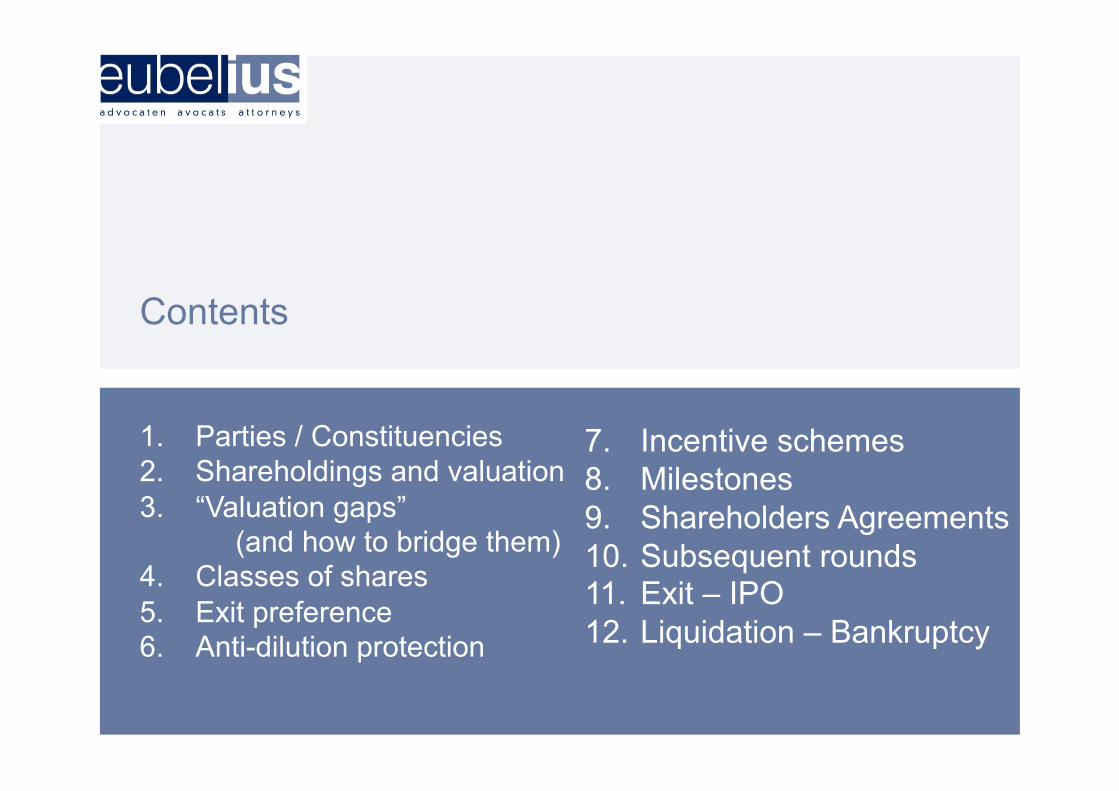

Contents

1. Parties / Constituencies 2. Shareholdings and valuation 3. “Valuation gaps”

(and how to bridge them) 4. Classes of shares 5. Exit preference 6. Anti-dilution protection

7. Incentive schemes 8. Milestones 9. Shareholders Agreements 10. Subsequent rounds 11. Exit – IPO 12. Liquidation – Bankruptcy

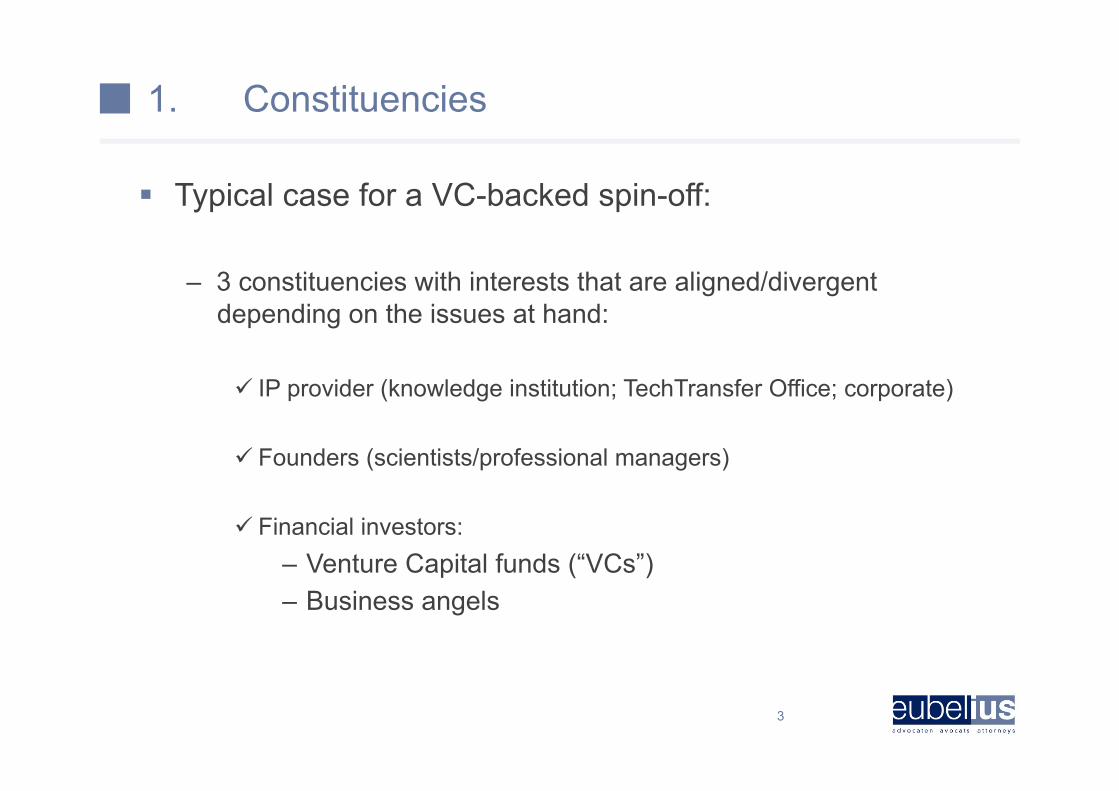

1. Constituencies

! Typical case for a VC-backed spin-off:

– 3 constituencies with interests that are aligned/divergent depending on the issues at hand:

" IP provider (knowledge institution; TechTransfer Office; corporate)

" Founders (scientists/professional managers)

" Financial investors: – Venture Capital funds (“VCs”) – Business angels

3

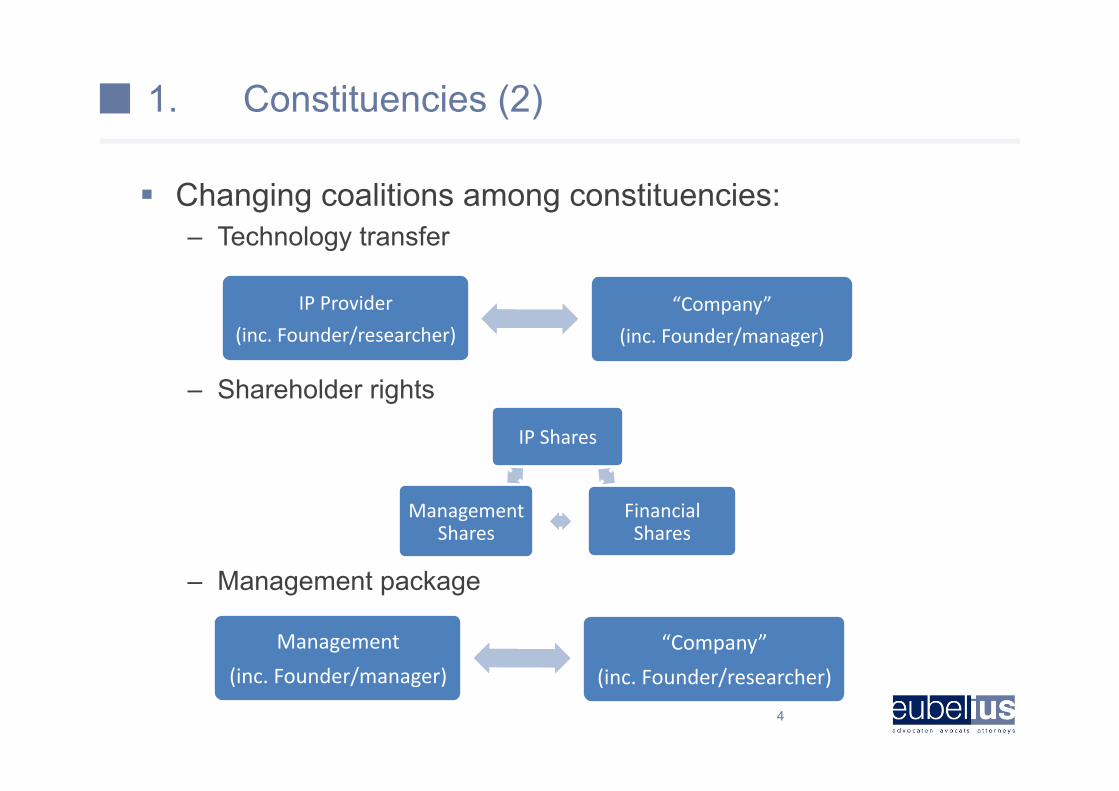

1. Constituencies (2)

! Changing coalitions among constituencies: – Technology transfer

– Shareholder rights

– Management package

4

IP Provider

(inc. Founder/researcher)

“Company”

(inc. Founder/manager)

Management

(inc. Founder/manager)

“Company”

(inc. Founder/researcher)

IP Shares

Financial Shares

Management Shares

1. Constituencies (3)

! Types of financial investors:

– Venture Capital funds

– Seed funds

– Business Angels

5

6

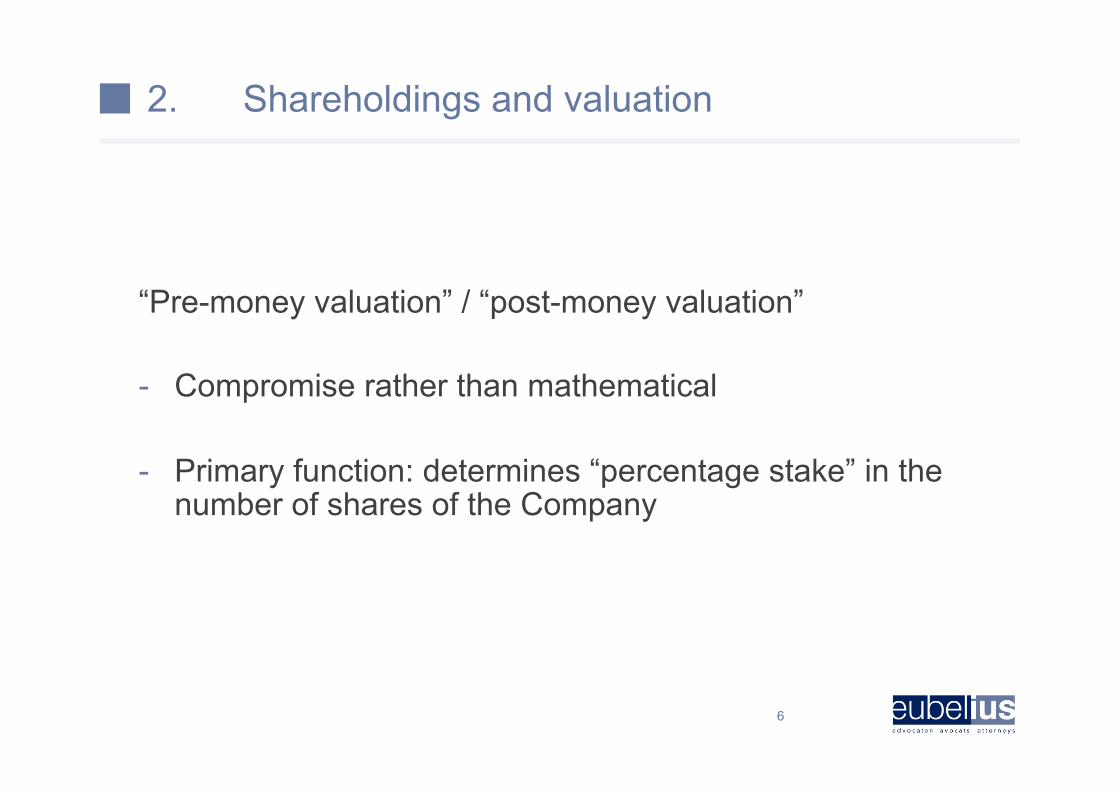

2. Shareholdings and valuation

“Pre-money valuation” / “post-money valuation”

- Compromise rather than mathematical

- Primary function: determines “percentage stake” in the number of shares of the Company

2. Shareholdings and valuation (2)

Valuation “step-ups” between consecutive financing rounds are therefore largely “paper money”

7

Seed financing: EUR 1.00 per share

1,000,000 shares

Round A: EUR 1.50 per share,

1,500,000 addiJonal investment

Total: 2 mio shares

Round B: EUR 2.00 per share,

5,000,000 addiJonal invested.

Total: 4.5 mio shares

Total in: 6.5 mio

Post money:

9 Mio

2. Shareholdings and valuation (4)

! Principle: each share has the same rights

! But: each of these matters is typically heavily modified in the contractual provisions governing the investment

! Therefore: do not over-estimate the importance of valuations

8

3. “Valuation gaps” – bridging

! Discussions on valuation of IP can become a numbers game

! However:

– This “number” is only a means to an end (relative stakes)

– While this must be “fixed” when the contribution of IP is made, it is not cast in stone

9

3. “Valuation gaps” – bridging (2)

Perennial debate: does an “IP euro” equal a “cash euro”?

Does a “manager euro” deserve/ need to be treated differently?

From the viewpoint of the financial investors: IP/Management “value” is a “risk”: proof of the pudding…

=> Get to “de-risking” events: events which prove the value, which solidify it, or (ideally) which allow the investors to cash in on it

10

11

3. “Valuation gaps” – bridging (3)

Legal forms of technology transfer:

! Sale

! License

! Contribution of ownership (“sale” of IP in consideration for shares)

! Contribution in enjoyment

! Mixed contribution in enjoyment/license (“equity component”)

! Warrant (on top of license) (“equity kicker”)

3. “Valuation gaps” – bridging (4)

Combinations are possible

Balancing act between FTO and rights of IP creators

12

4. Classes of shares

! Typical distinction: – Preferred Shares

– Common Shares

– Where do IP shares, cash contributions from knowledge institutions and contributions from mamagement come in?

! Preferences trump valuations!

13

14

4. Classes of shares (2)

! A range of rights and obligations are typically linked to “classes of shares: – Liquidation/ Trade Sale preference – Transfer restrictions – Board seats – Vetoes / special majorities – Information

! New financing rounds => usually new preferred class of shares (LIFO, “on top” of all that comes before it)

5. Exit preferences

! Exit = all events that lead to the investors being able to “cash in” on their investment (for better or worse): – Liquidation – “M&A” (Shares/assets/merger etc.)

! Exit preference = specific entitlement to portion of Exit proceeds for a certain class of shares

! Typical components

– “Multiple” (1x, 2x, 3x investment) – IRR (internal rate of return) – Catch-up? Full or only 1x? None (“double dip”)?

15

16

5. Exit preferences (2)

! Typical VC way of looking at this: – New money > older money > IP > Management/Founders

! Exit preference can be structured in many different ways (convertible class of shares vs. preferences), but principle, and intended end result is identical

5. Exit preferences (3)

! Ultimate goal =

– “Bad” scenario

" Not enough money to repay every VC share (1x)

" VCs will receive the exit proceeds

" Penalizes Management (and IP provider) for “failure”

17

5. Exit preferences (4)

– “Moderate” scenario

" Make sure VCs at least meet their internal goals for “success/non-failure” of a project, prior to allowing Management and IP provider to cash in

" “Multiple” or IRR in addition to “money back”

" Sets a “hurdle” which will define a successful Exit

18

5. Exit preferences (5)

– “Success” scenario

" Ideally the Exit preference then becomes irrelevant

" Catch-up or no Exit preferences anymore.

" However, in practice, this tends to be a negotiation point

19

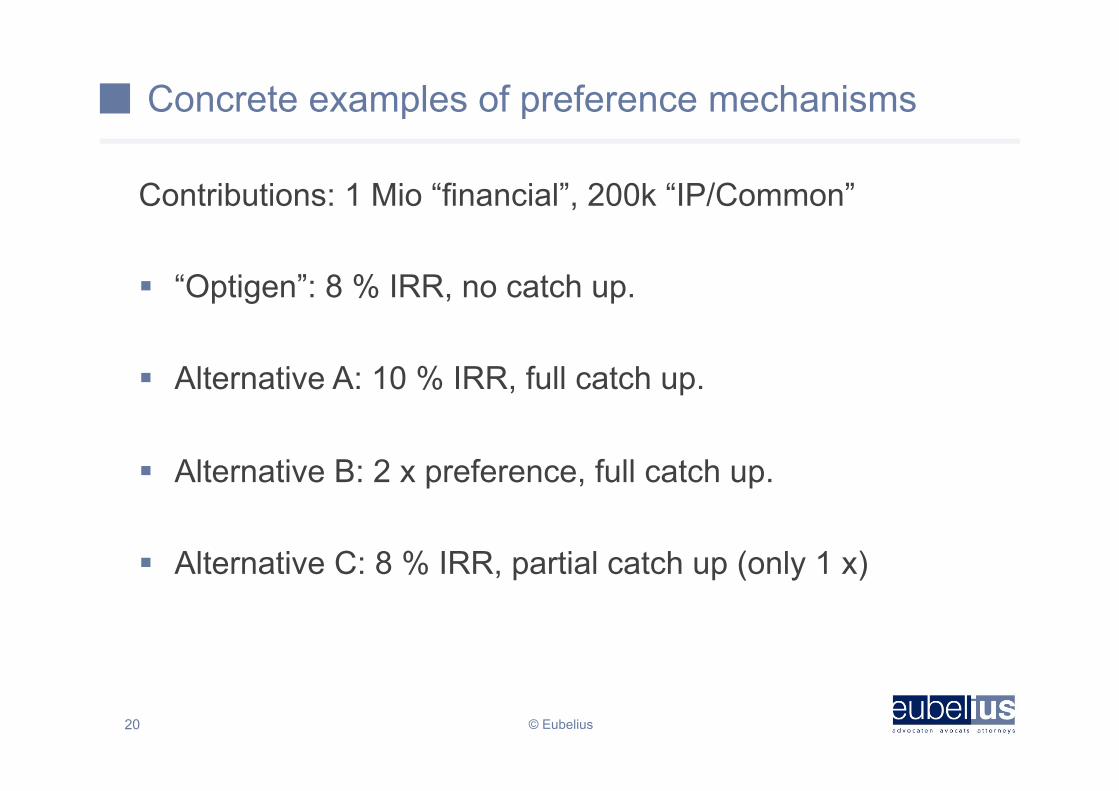

Concrete examples of preference mechanisms

Contributions: 1 Mio “financial”, 200k “IP/Common”

! “Optigen”: 8 % IRR, no catch up.

! Alternative A: 10 % IRR, full catch up.

! Alternative B: 2 x preference, full catch up.

! Alternative C: 8 % IRR, partial catch up (only 1 x)

20 © Eubelius

Trade sale at 1 year – proceeds to investors

21 © Eubelius

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Trade sale proceeds:

"Pro rata"

8% (no)

10% (full)

2x

8% + parJal

Trade sale at 5 years – proceeds to investors

22 © Eubelius

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Trade sale proceeds:

Pro Rata

8% (no)

10% (full)

2x

8% + parJal

6. Anti-dilution Protection

! Principle: – Protection for financial investors against (financial) dilution in

“down round”

! Mechanism: – Issue more shares to protected investor free of charge

! True effect: – “Corporate nuclear bomb” – Veto right against down round

23

6. Anti-dilution Protection (2)

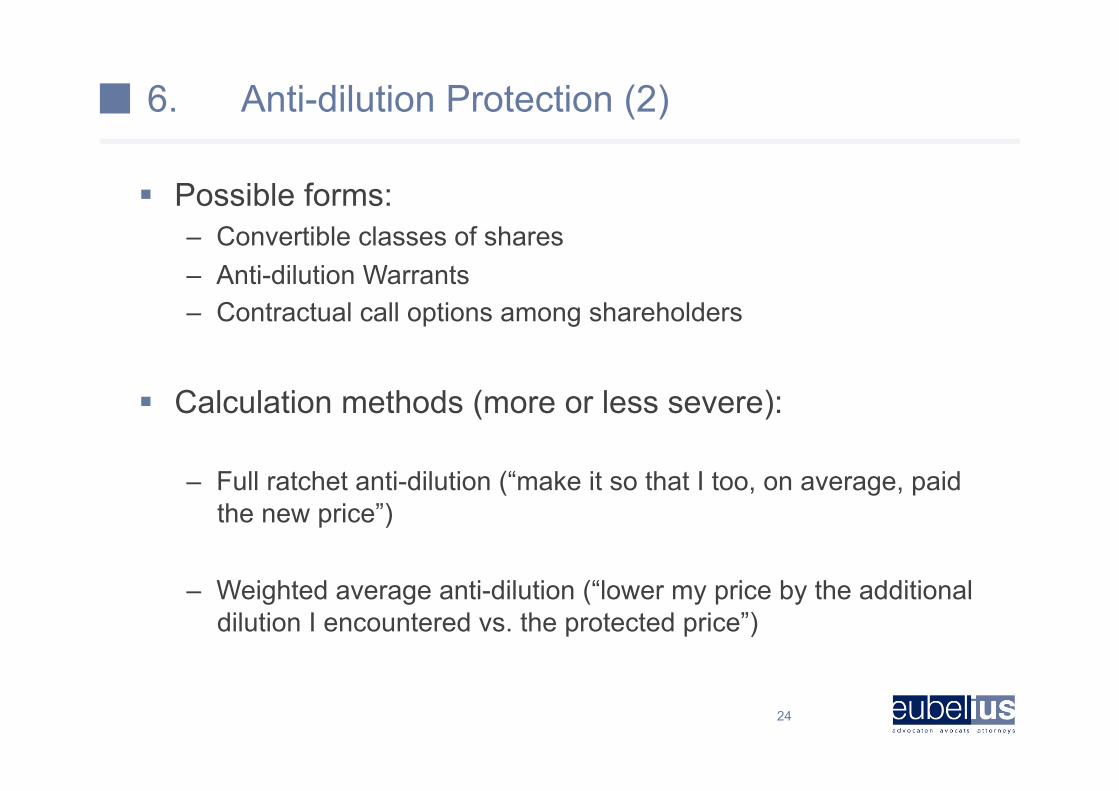

! Possible forms: – Convertible classes of shares – Anti-dilution Warrants – Contractual call options among shareholders

! Calculation methods (more or less severe):

– Full ratchet anti-dilution (“make it so that I too, on average, paid the new price”)

– Weighted average anti-dilution (“lower my price by the additional dilution I encountered vs. the protected price”)

24

6. Anti-dilution Protection (3)

! Potential corrective mechanisms – Pay-to-Play (incentive to participate) – Tapers – Internal Round exemption

! Important: this “protection” (and its corrective mechanisms) can influence “down”/”distress” round discussions

25

7. Incentive schemes

! How to reward Founders, Management, employees

! Heavily tax-driven (tax consequences / tax risks)

! Possibilities (with a corporate component): – Grant of stock options

– Subscribe for “cheap stock/Founder Shares”

– Grant of “profit certificates”

26

8. Milestones

! Further capital calls (staggered investment / tranching)

! Re-adjustment of valuation (“bridging the valuation gap”)

! Vesting of stock options/sweet equity

! “Pull the plug” scenarios for the spin-off: voting agreement to liquidate

27

9. Shareholders Agreements

! Agreement among shareholders to regulate voting, exercise of rights vis-à-vis Company and other shareholders, etc.

! Subscription Agreement: often includes Representations and Warranties (Company/Founders/Management) => potential liability

28

29

9. Shareholders Agreements (2)

! Transfer restrictions: – Lock-up – Pre-emption Right (“Right of First Refusal”) – Tag Along – Drag Along – Exemptions (important)

30

9. Shareholders Agreements (3)

! Director proposal rights (no direct appointment possible)

! Supermajorities (decisions at Board level and by shareholders meeting) – For matters of prime importance – Vetoes – Avoid deadlock

! Exit Preference

9. Shareholders Agreements (4)

! Stock options (reserved warrant pool)

! Protective covenants: – IP protection

" Confidentiality " Non-compete " Assignment of inventions

31

9. Shareholders Agreements (5) - Practicalities of negotiations

! Logical progression (although, in practice…): – Term Sheet – Shareholders Agreement / Subscription Agreement – Ancilliary contractual documentation (management contracts,

licensing agreements, service agreements, side letters) – Corporate documents (reports, Articles, deeds) – Notary

! Timing: can range from very quick (6 weeks) to drawn out (2 years +). Deciding factor? MOMENTUM

! Legal Support? Important to have support that understands the economics, manages the process, “translates” between constituencies and has access to a wide range of specialized knowledge.

32 © Eubelius

10. Subsequent capital rounds

! “The 3 constituencies” again, but with twists: – Founders/Management/scientists – IP provider – Financials (existing/new)

! “Layering” of preferences, valuation step-up (?) ! Anti-dilution protection

– Effect in case of down round: disastrous – Corporate WMDs

! In case down round needed: – Numerous possibilities for parties to impede can come from

“innocuous looking” provisions – Division “believers”/”non-believers”

33

10. Subsequent capital rounds (2)

Prior agreements (existing Shareholders Agreement, Articles of Association, etc.) can try to provide for this (and usually do) but, in the end, in many cases, “all bets are off”

34

11. Exit – IPO

! “Exit” = – Liquidation

– Share deal (acquirer – shareholders)

– Asset deal (acquirer – Company)

– Corporate restructuring (acquirer – Company)

– IPO?

35

11. Exit – IPO (2)

! Share Purchase Agreement: – Representations & Warranties (again):

" Price adjustment " Escrow / partially deferred payment? " R&W insurance?

– Earn-out? – Usually triggers incentive schemes (vesting of warrants etc.) – Inter-Seller Arrangements

36

37

11. Exit – IPO (4)

IPO: – “Going public” => selling shares to the public and listing on a

stock exchange

– Afterwards: listed company (different level of requirements)

– FSMA oversees listing and requirements for listed companies

– Keep this in mind in negotiations! Small provisions can make this a lot easier, or a lot harder…

38

12. Liquidation – Bankruptcy

! Bankruptcy

– Failure to meet current due debt – Inability to obtain further funding (“shocked credit”) – Possibly, “suspicious period” – Potential liabilities and even criminal sanctions

⇒ Board and management need to be aware of this possibility in “run-up” to funding (“business judgment rule”: reasonable director in same position; ex ante)

39

12. Liquidation – Bankruptcy (2)

! Liquidation

– Following decision to wind up the Company

– Solvent or insolvent liquidation

– Insolvent liquidation may still lead to bankruptcy