asc 606 webinar: the impact is on your whole organization

TRANSCRIPT

ASC-606 New Revenue Recognition Rules

Impact the entire company

This is BIG!!! Do you know why?!

About Jade

Pune

San Jose

San DiegoNoida

Atlanta

Hyderabad

Reading

10 Offices

Worldwide

5 Global

Delivery Centers

Services High-Tech Manufacturing Energy Social Media & Entertainment

Boston

Los Angeles

Philadelphia

ASC-606 Caveats

Agenda

Introductions

ASC-606 Caveats

It is all about Revenue

New Opportunities

Taking Charge

Automation to assist in transition

Summary

ASC-606 Items to Call Out

May 28, 2014, FASB and IASB issued, ASC 606 and IFRS 15

Public companies - FY/CY 2018

Non-public companies - FY/CY 2019

Entities may elect either of two transition options:

Full Retrospective Method

Modified Retrospective Method

ASC-606 Greatly Expands the Scope of Disclosures

Contractual Cost Tracking/Matching:

ASC-606: Revenue is King

ASC-606 will affect all companies to some degree

Revenue Recognition is a key metric

Revenue is the bases for many business decisions

Areas of Changes in ASC-606 Elimination of software

guidance

No VSOE Limitation

Residual Approach

Contingencies

Roadmaps

Ratable revenue may

change

Vendor protection clauses

Time value of money

Extended payment terms

Certain Subscriptions

Cash Cap guidance

Funded R&D

arrangements

Distributor revenues

Contract modifications

Bill and hold

arrangements

Term licenses

Sales Commissions

Other contract costs

Volume Discounts

Extended warranties

Judgement & Estimates

ASC-606 Beyond Accounting Change ASC-606’s pervasive changes will be across the company:

Key Financial Metrics

Management/ Sales Compensation

Debt Covenants

Tax Payments

Investor Relations

IT Systems/ Processes/ Controls

ASC-606 Creates Opportunities

Business models, now have a fresh look

Business Practices

Contract Terms

Go-to-Market Strategies

Sales Compensation

Tax Matters

ASC-606 If You Have Not Started, You Are Late

Per PWC

Public Companies - 8%, not started, 75% assessing, 8% implementing

Private Companies – 47% not started, 45% assessing, 7% implementing

http://www.pwc.com/us/en/audit-assurance-services/accounting-

advisory/revenue-recognition-survey.html

For Full Retrospective method, the transition has begun

For Modified Retrospective method, data gathering has begun

Transition to ASC-606 timeline: 6 to 9 months, depending

3 to 6 months to assess and implement

3 months to run in parallel

ASC-606 Here is What You Can Do!!

Starting today, make ASC-606 Top Priority,

TAKE CHARGE!!

Practically/Actively what to do: “12 steps program”

“Accept the Old Methods are not Compliant”

Get Priority from the Very Top

Select a Cross-Functional Team

Educate the Team

Team Assesses the Situation/Sets Roadmap

Design & Implement: new Policies, Process and Systems

Next Steps

Don’t underestimate the potential impact or level of effort required

Complete your assessment soon

Consider the pros and cons of each adoption method and plan for

SAB 74 disclosures

Develop a detailed plan for implementation

Addressing These Challenges

Addressing These Challenges

Tools Focus in Automation

There are multiple automation tools in the market and these are

Stand alone tools that consume data from your transactional systems

Build on rules that you configure to

Manage revenue contracts (RC)

Identify configurable performance obligations (PoB)

Determine in arriving at transaction price (TP)

Allocate transaction price to separate performance obligations

Manage events or triggers to release revenue

Manage operational, accounting and disclosure reporting

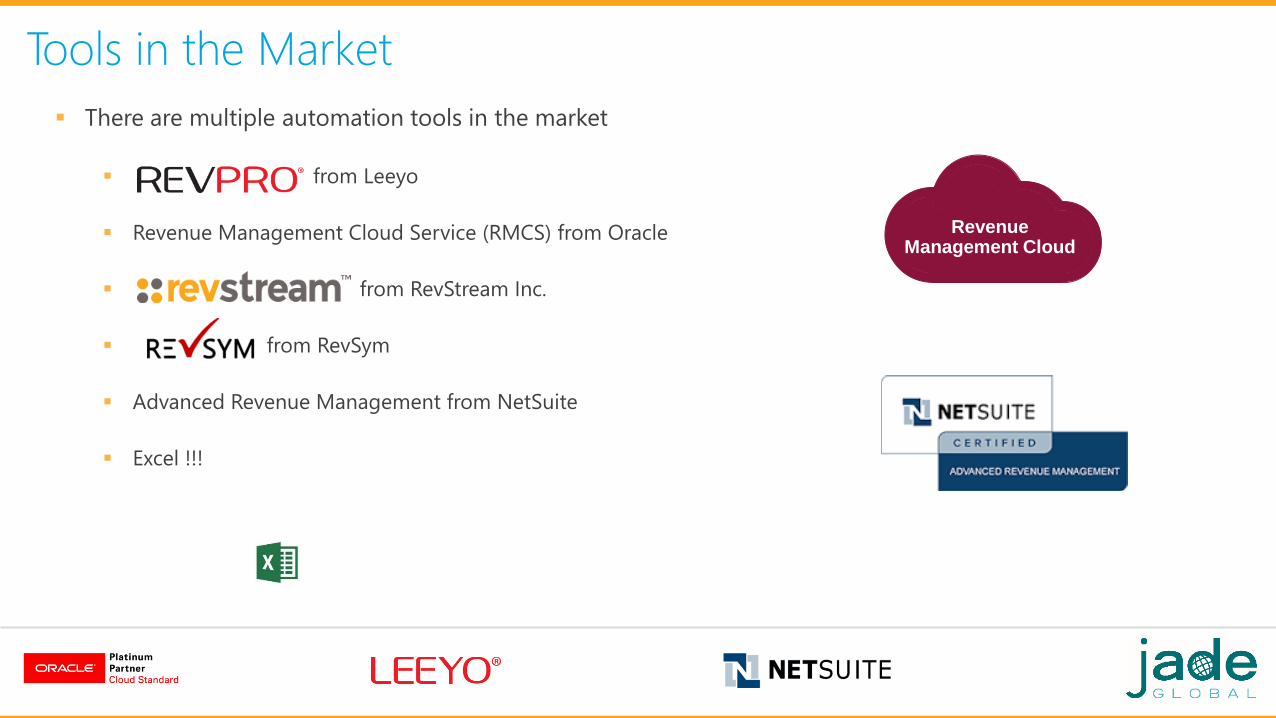

There are multiple automation tools in the market

from Leeyo

Revenue Management Cloud Service (RMCS) from Oracle

from RevStream Inc.

from RevSym

Advanced Revenue Management from NetSuite

Excel !!!

Revenue Management Cloud

Tools in the Market

Transaction Lifecycle In Revpro – ASC 606

Transaction Grouping

Assign POB Templates

Calculate Variable

Consideration SSP Assignment

Create/Modify Revenue Contract

Revenue Release

Accounting Reporting

Calculate Other Costs

Forecasting

Bundle Explosion

No

Bundle Config Exists? Yes

Revenue Allocation

Contracts Orders Projects Billing Revenue Events

Identify Customer

Contract

(Step 1)

Identify

Performance

Obligations

(Step 2)

Determine

Transaction

Price (Step 3)

Allocate

Transaction

Price (Step 4)

Recognize

Revenue

(Step 5)

Post and

Report

GAAP Guidance

RevPro - Main Menu

RevPro - Main Menu

RMCS - Revenue Management Cloud Service

RMCS – Co-existence

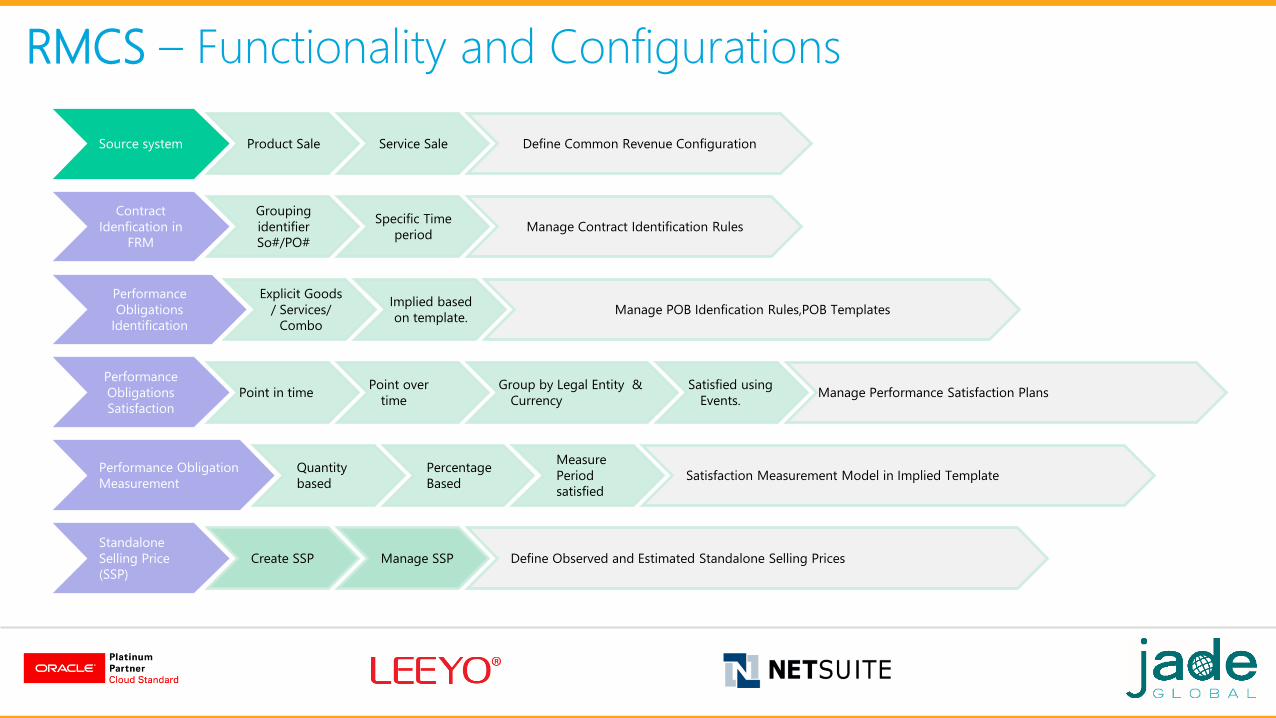

RMCS – Functionality and Configurations

Source system Product Sale Service Sale Define Common Revenue Configuration

Contract

Idenfication in

FRM

Grouping

identifier

So#/PO#

Specific Time

periodManage Contract Identification Rules

Performance

Obligations

Identification

Explicit Goods

/ Services/

Combo

Implied based

on template.Manage POB Idenfication Rules,POB Templates

Performance

Obligations

Satisfaction

Point in time Point over

time

Group by Legal Entity &

Currency

Satisfied using

Events.Manage Performance Satisfaction Plans

Performance Obligation

Measurement

Quantity

based

Percentage

Based

Measure

Period

satisfied

Satisfaction Measurement Model in Implied Template

Standalone

Selling Price

(SSP)

Create SSP Manage SSP Define Observed and Estimated Standalone Selling Prices

RMCS – Main Menu

Challenges with Revenue Recognition using Excel

Pros

Spreadsheets are blank slates

Easy to use

Cons

Not secure

Heavily dependent on the user

Manual and error prone

Limited in functionality

Summary

Critical considerations towards ASC-606

Are you currently working with spreadsheets?

What option is best for you to comply with the new guidance?

Have you analyzed your business processes?

Review your ERP/systems footprint

Analyze your current transactional sources and processes

Are you clear on the data sources to support compliance with the new

guidance

Trusted tools & methodologies

Automate your revenue recognition data collection activity

Process revenue recognition tasks with rules based engine

ASC-606 Jade Global

“We are Ready to Help Today!” Help You TAKE CHARGE!!

Jade Global

Oracle Platinum Cloud Standard Partner

13 years in business

200+ Customers with 800+ technology projects

600+ Employees

We do Services:

Advisory Implementation/ Upgrades

Managed Services

Mobile & Custom Development

Integration

Analytics and BI

Contact us

Connect With Us

Visit us at www.jadeglobal.com

Email us at [email protected]

Call us at 1-877-JADE4IT