asda income trackeryour.asda.com/media... · unit 1, 4 bath street, london ec1v 9dx ......

TRANSCRIPT

© Centre for Economics and Business Research 2013

Asda Income Tracker Report: September 2013 Released: October 2013

Centre for Economics and Business Research ltd Unit 1, 4 Bath Street, London EC1V 9DX t 020 7324 2850 w www.cebr.com

M a k i n g B u s i n e s s S e n s e

© Centre for Economics and Business Research 2013

Contents Introduction 03 Headlines 04 Constructing the Income Tracker 05 Dashboard 06 Income Tracker trends 07 Cost of living 09 Labour market 11 Regional trends 12 Fuel price trends 15 Contact 17 Data charts & tables 18 Method 23 Disclaimer 25

Asda Income Tracker

2

© Centre for Economics and Business Research 2013

“It's encouraging to see that inflation in essential items is heading in the right direction. However, it is becoming even more evident that action needs to be taken to address widespread regional discrepancies. “Aside from overall household spending power being at a six month low and the rising cost of energy bills adding extra pressure , when you look beyond the capital and South East the situation across the regions gets steadily worse – with families in Northern Ireland and the North East still squeezed to a far greater degree. “We can only celebrate the full benefits of an economic recovery if it is a fair recovery for all and the continued shortfall for millions of households is a worrying and unacceptable reality.”

Introduction Asda Income Tracker

Andy Clarke Asda President and CEO

3

© Centre for Economics and Business Research 2013

Headlines – Asda Income Tracker The average UK household had £157 a week of discretionary income in September 2013, down from £159 in the same month a year before and moving further below the 2010 peak of £165. Average household net income growth remained on hold, continued to be held back by historically low wage increases, stubbornly high unemployment and the effect of the ongoing cap in the growth of working age benefits. However, the gap between income growth and increases in the cost of living narrowed in September, as essential item inflation slowed to 2.8 per cent, largely due to reductions in clothing price and mortgage interest inflation.

Headlines

“The UK economic recovery continues to gain momentum in 2013, as growth picks up pace and business confidence has reached its highest level in years. “However, as the Asda Income Tracker highlights, the effects of this recovery are not translating into growth in purchasing power for the average UK household. Inflation on essential items continues to stand well below income growth, which is being held back by spare capacity in the labour market.” Rob Harbron, Senior Economist, Cebr

Asda family spending

power was down by £2

a week year on year

(a 1.1% annual

decline)

4

© Centre for Economics and Business Research 2013

Constructing the Asda Income Tracker

Total household income £707 per week e.g. wages, investment income, pensions, social security, self employment earnings

e.g. national insurance contributions, income tax

e.g. holidays, cinema, theatre, eating out, toys, sports, savings, jewellery, national lottery and other gambling payments, computer software and games

e.g. food, clothing, housing costs, bills, transport, communication costs, health, children’s schooling, house maintenance and repair

i.e. take home pay

i.e. take home pay

Taxes £118 per week

= - Net income

£589 per week

Cost of living £432 per week

= - Net income £589 per week

Average family spending power

£157 per week

Model

5

© Centre for Economics and Business Research 2013

Asda Income Tracker Dashboard: September Annual percentage change Indicator

0.8% (excl. bonuses) Regular earnings growth* (Aug)

7.7% (-0.2 % points on year) Unemployment rate** (Aug)

Latest trend

2.1% Net income

2.3% Mortgage costs

4.3% Food

-1.6% Vehicle fuels

7.7% Home electricity, gas & fuel

2.8% Essential item inflation

-1.1% Family spending power KEY IMPROVEMENT NO SIGNIFICANT CHANGE DETERIORATION

Dashboard

* three months to month stated **unemployment rate for three months to month stated

0.9% (+279,000 employment on year) Employment growth* (Aug)

6

© Centre for Economics and Business Research 2013

Discretionary spending power continues to see declines in September

• In September 2013, household discretionary incomes fell back by 1.1 per cent compared to a year before, in the third consecutive month of year-on-year decreases. • As illustrated by the chart opposite, household finances are have deteriorated in 2013, losing some of the gains made in 2012. • The ongoing pressure on household incomes comes from the effects of very weak wage growth, high unemployment and the cap on growth in working age benefits. Growth in the cost of living remains well above income increases, eroding household spending power. • When the effects of bonus payments are included, average weekly discretionary incomes also declined by £2, or 1.3 per cent.

Income Tracker Trends

Year-on-year change in Asda income tracker, £ The Asda Income Tracker was £2 a week lower in September 2013 than a year before

-£15

-£10

-£5

£0

£5

£10

£15

£20

£25

£30

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

7

© Centre for Economics and Business Research 2013

• The average UK household had £157 a week in discretionary income in September 2013, down from £159 in the same month a year before, and moving further away from the peak of £165 in early 2010. • Household net income growth remained unchanged at 2.1 per cent over the year to September, held back by historically very weak wage growth, little change in the unemployment rate and the ongoing effects of the cap on increases in working age benefits. However despite these challenges, net incomes continue to be supported by April’s increase in the personal tax allowance. • Although income growth is on hold, the gap with growth in the cost of living has narrowed, as essential price inflation came down to 2.8 per cent. • Once bonus payments are included, average weekly household discretionary income stood at £181 in September 2013.

Contributions to annual change in the Income Tracker (excluding bonuses), September 2013

Income growth stagnant but growth in cost of living starting to come down

-£20 -£15 -£10 -£5 £0 £5 £10 £15

Income Tracker

Essential spending

Net Income

Income Tracker Trends

The Asda Income Tracker was £2 a week lower in September 2013 than a year before

8

© Centre for Economics and Business Research 2013

Essential item inflation falls back but remains well above income growth

• Annual inflation on the overall consumer price index (CPI) stood at 2.7 per cent in September, unchanged from August’s reading. • Contributions to changes in the headline index were relatively small in September, with an upward contribution from air fares being offset by a downward effect from a fall in the cost of filling up at the pump. • However, inflation on the cost of essential items came down in September to 2.8 per cent, a decrease from 2.9 per cent in August and July and 3.0 per cent in June. • Meanwhile, inflation on the broader retail price index (RPI) stood at 3.2 per cent in September – a level around which RPI inflation has fluctuated only marginally in the past 12 months.

Cost of living

The cost of essential items rose year on year in August by 2.8 per cent

Annual inflation on the consumer price index and essential item annual inflation

0%

1%

2%

3%

4%

5%

6%

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Essential items CPI

9

© Centre for Economics and Business Research 2013

Cost of living Clothing price growth eases and mortgage interest inflation continues to fall back The main factors putting pressure on family discretionary income in September were: • Annual clothing price inflation fell back to 1.1 per cent in September, down from 1.6 per cent in August to its lowest in four months. • In addition, inflation on mortgage interest payments slid back for the sixth consecutive month, reaching 2.3 per cent in the year to September. This is down from a high of 4.6 per cent in the year to March. • Further downward pressure on the cost of living came from petrol & diesel prices, which fell back year on year by 1.6 per cent. • However, food price inflation climbed to 4.3 per cent, up from 4.1 per cent in August to its highest since 3.8 per cent. • In addition, annual price inflation on electricity and gas tariffs remains high – at 8.1 per cent and 8.3 per cent respectively.

Inflation of selected goods, annual change to September 2013

-2%

0%

2%

4%

6%

8%

10%

10

© Centre for Economics and Business Research 2013

Labour Market

UK unemployment rate (LHS), per cent and 3-month annual growth in regular pay (RHS), per cent

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Feb-

08

Aug

-08

Feb-

09

Aug

-09

Feb-

10

Aug

-10

Feb-

11

Aug

-11

Feb-

12

Aug

-12

Feb-

13

Aug

-13

Unemployment rate Regular Earnings growth

• Annual growth in average regular pay fell to just 0.8 per cent during the three months to August. Wage growth has not been lower than this since comparable data began in 2001 – illustrating the extent of the current squeeze on household incomes. • The rate of unemployment stood on hold at 7.7 per cent, just 0.2 percentage points lower than a year ago. • However, even within those that are employed, the rate of underemployment has reached an all-time high; the proportion of those working part-time because they could not find full-time work reached 18.5 during the three months to August, the highest since data began in 1992. • As a result, workers find themselves without much bargaining power, limiting the pace of wage growth.

While the unemployment rate remains on hold at 7.7 per cent

Regular pay growth falls back to historic lows

11

© Centre for Economics and Business Research 2013

Gross income growth falls back across much of the UK

Regional Trends

Regional gross income, annual change to quarter indicated Only the East of England sees a growth uptick, boosted by local labour market

• Every country and region of the UK, with the exception of the East of England, saw annual household gross income growth slow between Q2 and Q3 2013. • This was driven by a slowdown in employment growth across much of the UK, combined with the effects of the cap in working age benefit increases continuing to feed through. • However, the labour market of the East of England strengthened notably, as the unemployment rate fell back by 0.7 percentage points in the three months to August 2013 compared to both the previous quarter and the same period a year before. • At the other end of the scale, the West Midlands saw the slowest growth in household gross incomes at just 0.9% over the year, as the unemployment rate climbed by 0.8 points in the three months to August 2013 compared to a year before.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Q2 2013 Q3 2013

12

© Centre for Economics and Business Research 2013

Household finances now deteriorating around the UK

Regional Trends

Asda Income Trackers by region, annual change to quarter indicated

Weak income growth and elevated inflation continues to erode family spending power

• Spending power is now falling back year on year in every region of the UK except for the East of England and Scotland. The East saw a 1.2 per cent annual uptick in discretionary incomes, while Scotland experienced 0.6 per cent growth, largely thanks to strengthening local labour markets. • However, the effects of weak wage growth, the cap in benefits increases and high inflation in the cost of living are being felt across the rest of the UK. • The West Midlands and Northern Ireland faced the sharpest annual declines in discretionary spending power in Q3 2013. Unemployment jumped in the West Midlands over the past year, holding back income growth, while those in Northern Ireland are particularly exposed to the cap on benefits growth.

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

Q2 2013 Q3 2013

13

© Centre for Economics and Business Research 2013

Spending power in Northern Ireland falls further behind the UK average

Regional Trends

Asda Income Trackers by region, £ per week in quarter indicated Weekly discretionary incomes fell back in Q3 2013 compared to Q2 across much of the UK • Family spending power was reduced in most regions of the UK in Q3 compared to the previous quarter. • Households in Northern Ireland had £60 of discretionary income a week in Q3 2013, compared to the UK average of £158 for the quarter. • The UK average is now 2.64 times higher than that of Northern Ireland, compared to 2.63 in Q2 2013 and 2.58 a year ago. • Meanwhile, households in London had £235 a week of discretionary income in Q3 2013, down from £237 the previous quarter and £239 in the same quarter a year before. • Discretionary income in Scotland held broadly stable at £161 in Q3 2013.

£0

£50

£100

£150

£200

£250

Q2 2013 Q3 2013

14

© Centre for Economics and Business Research 2013

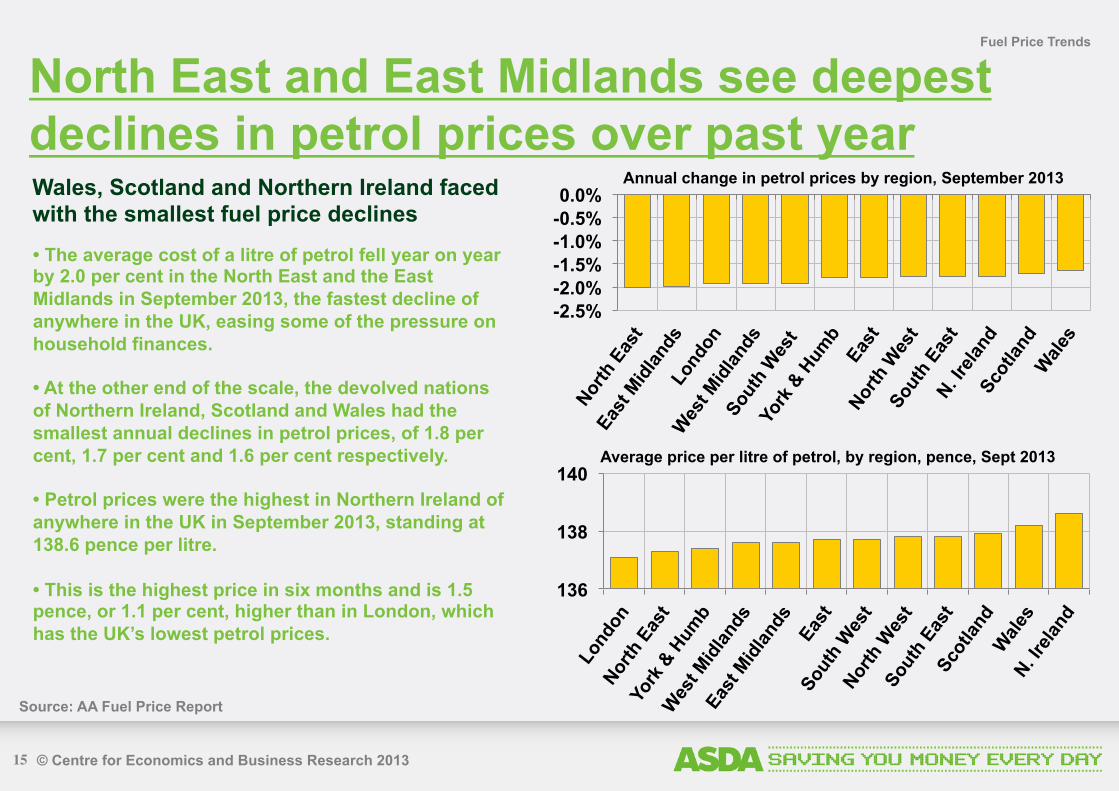

North East and East Midlands see deepest declines in petrol prices over past year

Fuel Price Trends

Annual change in petrol prices by region, September 2013 Wales, Scotland and Northern Ireland faced with the smallest fuel price declines

• The average cost of a litre of petrol fell year on year by 2.0 per cent in the North East and the East Midlands in September 2013, the fastest decline of anywhere in the UK, easing some of the pressure on household finances. • At the other end of the scale, the devolved nations of Northern Ireland, Scotland and Wales had the smallest annual declines in petrol prices, of 1.8 per cent, 1.7 per cent and 1.6 per cent respectively. • Petrol prices were the highest in Northern Ireland of anywhere in the UK in September 2013, standing at 138.6 pence per litre. • This is the highest price in six months and is 1.5 pence, or 1.1 per cent, higher than in London, which has the UK’s lowest petrol prices.

-2.5% -2.0% -1.5% -1.0% -0.5% 0.0%

Average price per litre of petrol, by region, pence, Sept 2013

136

138

140

Source: AA Fuel Price Report

15

© Centre for Economics and Business Research 2013

Households in Northern Ireland spending almost double those in London on filling up

Fuel Price Trends

Average weekly household spend on vehicle fuel by region Cost of vehicle fuel rises around the UK between Q2 and Q3 2013

• Households in Northern Ireland on average were spending £36.40 a week in Q3 2013, up from £36 a week in Q2. • This leaves these households spending more on fuel than anywhere else in the UK – partly due to the higher cost of petrol in Northern Ireland and in part because of more litres being bought. • This compares to a UK-wide average of £25.60 in Q3 2013, and just £18.50 a week for households in London – again partly because of London having the lowest petrol prices and purchasing the fewest litres a week on average. • Despite the year-on-year decline in petrol prices, the cost of filling up was higher in Q3 2013 than in the previous quarter around the entire UK.

£0

£5

£10

£15

£20

£25

£30

£35

£40

Q2 2013 Q3 2013

16

© Centre for Economics and Business Research 2013

Data and Method Please find attached method notes and the tabulated date. Asda produces a monthly income tracker report with a more comprehensive report every quarter. For press enquiries please contact:

Bee Rycroft, PR Manager, [email protected] ; 0113 826 3448 Amy Garbutt, PR Manager, [email protected] ; 0113 826 3369 For data enquiries please contact: Bethan Ellis, Insight Planning Manager, [email protected] ; 0113 826 2198 Rob Harbron, CEBR Senior Economist, [email protected] ; 020 7324 2864

Appendix

© Centre for Economics and Business Research 2012 17

© Centre for Economics and Business Research 2013

Monthly Asda Income Tracker Asda Income Tracker tables

Asda Income Tracker (LHS) Asda Income Tracker annual % change (RHS)

Figure 1: Asda Income Tracker and year-on-year change (excluding bonuses)

18

-10%

-5%

0%

5%

10%

15%

20%

25%

£120

£125

£130

£135

£140

£145

£150

£155

£160

£165

£170

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

© Centre for Economics and Business Research 2013

Monthly Asda Income Tracker Figure 2: Comparison of year-on-year change in Asda Income Tracker including and excluding bonuses

Asda Income Tracker tables

-£20

-£15

-£10

-£5

£0

£5

£10

£15

£20

£25

£30

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9 Se

p-09

N

ov-0

9 Ja

n-10

M

ar-1

0 M

ay-1

0 Ju

l-10

Sep-

10

Nov

-10

Jan-

11

Mar

-11

May

-11

Jul-1

1 Se

p-11

N

ov-1

1 Ja

n-12

M

ar-1

2 M

ay-1

2 Ju

l-12

Sep-

12

Nov

-12

Jan-

13

Mar

-13

May

-13

Jul-1

3 Se

p-13

Asda Income Tracker including Bonuses Asda Income Tracker excluding Bonuses

19

© Centre for Economics and Business Research 2013

Monthly Asda Income Tracker Figure 3: Twelve-month moving average of Income Tracker (excl. bonuses) level

£100

£110

£120

£130

£140

£150

£160

£170Sep-08

Dec-08

Mar-09

Jun-09

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

Jun-13

Sep-13

Asda Income Tracker tables

20

© Centre for Economics and Business Research 2013

Monthly Asda Income Tracker Month Income tracker Month Income tracker Month Income tracker Month Income tracker

Table 1: Average UK household Income Tracker, £ per week, current prices, excluding bonuses Income tracker Month

Asda Income Tracker tables

January 2009 £159 January 2010 £165 January 2011 £162 January 2012 £154 January 2013 £157

February 2009 £157 February 2010 £165 February 2011 £159 February 2012 £153 February 2013 £154

March 2009 £159 March 2010 £164 March 2011 £159 March 2012 £153 March 2013 £153

April 2009 £163 April 2010 £162 April 2011 £155 April 2012 £156 April 2013 £159

May 2009 £162 May 2010 £162 May 2011 £155 May 2012 £158 May 2013 £158

June 2009 £163 June 2010 £162 June 2011 £155 June 2012 £160 June 2013 £160

July 2009 £164 July 2010 £164 July 2011 £155 July 2012 £161 July 2013 £160

August 2009 £163 August 2010 £163 August 2011 £153 August 2012 £160 August 2013 £158

September 2009 £163 September 2010 £164 September 2011 £151 September 2012 £159 September 2013 £157

October 2009 £164 October 2010 £164 October 2011 £152 October 2012 £158

November 2009 £164 November 2010 £163 November 2011 £152 November 2012 £158

December 2009 £164 December 2010 £160 December 2011 £151 December 2012 £155

2009 Average £162 2010 Average £163 2011 Average £155 2012 Average £157

21

© Centre for Economics and Business Research 2013

Quarterly ASDA Income Tracker

Region

© Centre for Economics and Business Research 2012

Q3 2011 Q3 2012 Q3 2013

Table 2: Average household Income Tracker, £ per week, current prices, excluding bonuses Asda Income Tracker tables

Northern Ireland 61 62 60

Yorkshire & Humber 121 128 127

North East 122 133 130

North West 131 135 133

West Midlands 136 142 137

East Midlands 137 141 139

South West 137 145 140

Wales 140 148 146

Scotland 155 160 161

South East 165 169 168

East 177 183 185

London 229 239 235

22

© Centre for Economics and Business Research 2013

Total household income for the United Kingdom is derived from the Living Costs and Food Survey 2011 (released December 2012). This is updated on a monthly basis using official statistics on average earnings, unemployment, social security payments, interest rates and pension income. Earnings data from the Office for National Statistics that is released in the month of the report refers to the previous month. We forecast earnings data for the month of the report. Taxes are subtracted from total household income to estimate the actual amount that can be spent on goods and services, i.e. net income or disposable income. The average amount of tax paid is calculated using the latest version of the Living Costs and Food Survey. This is updated on a monthly basis using Office for National Statistics data and Cebr modelling.

Method The Asda income tracker is calculated from the following equations: • Total household income minus taxes

equals net income • Net income minus basic spend equals

Asda income tracker

Method notes

23

© Centre for Economics and Business Research 2013

Method

Net income is calculated by deducting our tax estimate from our total household income estimate. Basic spend (cost of living) figures are updated using monthly consumer price data and the trend growth rate in the volume of essential goods and services purchased over the most recent ten year period. A full list of items constituting basic (or ‘essential’) spending was created in collaboration between Asda and Cebr when the income tracker concept was originally formed in 2008. This list is available on request. The Asda income tracker is a measure of ‘discretionary income’, reflecting the amount remaining after the average UK household has had taxes subtracted from their income and bought essential items such as: groceries, electricity, gas, transport costs and mortgage interest payments or rent. The income tracker measures the amount left over to spend on discretionary purchases such as leisure and recreation goods and services.

These components are based on official statistics and Cebr calculations.

Method notes

24

© Centre for Economics and Business Research 2013

Disclaimer

This report was produced by the Centre for Economics and Business Research (Cebr), an independent economics and business research consultancy established in 1993 providing forecasts and advice to City institutions, government departments, local authorities and numerous blue-chip companies throughout Europe. The main contributors to this report are Cebr economists Rob Harbron, Scott Corfe and Charles Davis. Whilst every effort has been made to ensure the accuracy of the material in this report, the authors and Cebr will not be liable for any loss or damages incurred through the use of this report. London, October 2013

Disclaimer

25