asean and global rice situation and outlook, 2011–2022

DESCRIPTION

This paper documents the current and projected status until 2022 of ASEAN rice economies as well as other neighboring Asian countries by assessing their potential rice supply and demand paths over the next decade. Despite aggressive campaigns for rice self-sufficiency, Indonesia and the Philippines are expected to remain important rice importers.TRANSCRIPT

ASEAN and Global Rice Situation and Outlook, 2011–2022

Eric J. Wailes

and Eddie C. Chavez

The lead author, Eric J. Wailes, is Distinguished Professor at the Department of Agricultural Economics and Agribusiness, University of Arkansas

Contents

Abbreviations .............................................................................................................................. v

Executive Summary ................................................................................................................... 1

1. Overview ............................................................................................................................... 2

1.1 Purpose of this Outlook and its Significance for ASEAN ................................................. 2 1.2 The Arkansas Global Rice Model Framework ................................................................. 2

2. ASEAN Rice Outlook ............................................................................................................ 4

2.1 Rice Harvested Area and Production .............................................................................. 4 2.2 Rice Consumption .......................................................................................................... 5 2.3 Rice Exports ................................................................................................................... 5 2.4 Rice Imports ................................................................................................................... 7 2.5 Rice Stocks .................................................................................................................... 7

3. ASEAN Country Rice Outlook ............................................................................................... 7

3.1 Brunei Darussalam .......................................................................................................... 7 Economy ...................................................................................................................... 7 Rice Supply and Demand ............................................................................................ 8

3.2 Cambodia ........................................................................................................................ 8 Economy ...................................................................................................................... 8 Rice Supply and Demand ............................................................................................ 8

3.3 Indonesia ......................................................................................................................... 9 Economy ...................................................................................................................... 9 Rice Supply and Demand ............................................................................................ 9

3.4 Lao People’s Democratic Republic .................................................................................10 Economy .....................................................................................................................10 Rice Supply and Demand ...........................................................................................10

3.5 Malaysia .........................................................................................................................10 Economy .....................................................................................................................10 Rice Supply and Demand ...........................................................................................10

3.6 Myanmar ........................................................................................................................11 Economy .....................................................................................................................11 Rice Supply and Demand ...........................................................................................11

3.7 Philippines ......................................................................................................................12 Economy .....................................................................................................................12 Rice Supply and Demand ...........................................................................................12

3.8 Singapore .......................................................................................................................12 Economy .....................................................................................................................12 Rice Supply and Demand ...........................................................................................13

3.9 Thailand .........................................................................................................................13 Economy .....................................................................................................................13 Rice Supply and Demand ...........................................................................................13

3.10 Viet Nam ......................................................................................................................14 Economy .....................................................................................................................14 Rice Supply and Demand ...........................................................................................14

4. Global Rice Outlook .............................................................................................................14

4.1 International Rice Prices .................................................................................................14 4.2 Global Rice Supply and Demand ....................................................................................15

4.3 Key Global Policy Assumptions ......................................................................................16 4.4 Global Rice Trade...........................................................................................................17 4.5 Key Non-ASEAN Rice Countries ....................................................................................17 4.6 People’s Republic of China .............................................................................................18

Economy .....................................................................................................................18 Rice Supply and Demand ...........................................................................................18

4.7 Japan .............................................................................................................................18 Economy .....................................................................................................................18 Rice Supply and Demand ...........................................................................................19

4.8 Republic of Korea ...........................................................................................................19 Economy .....................................................................................................................19 Rice Supply and Demand ...........................................................................................19

4.9 India ...............................................................................................................................20 Economy .....................................................................................................................20 Rice Supply and Demand ...........................................................................................20

4.10 Pakistan .......................................................................................................................20 Economy .....................................................................................................................20 Rice Supply and Demand ...........................................................................................21

5. Stochastic Analysis ...............................................................................................................21

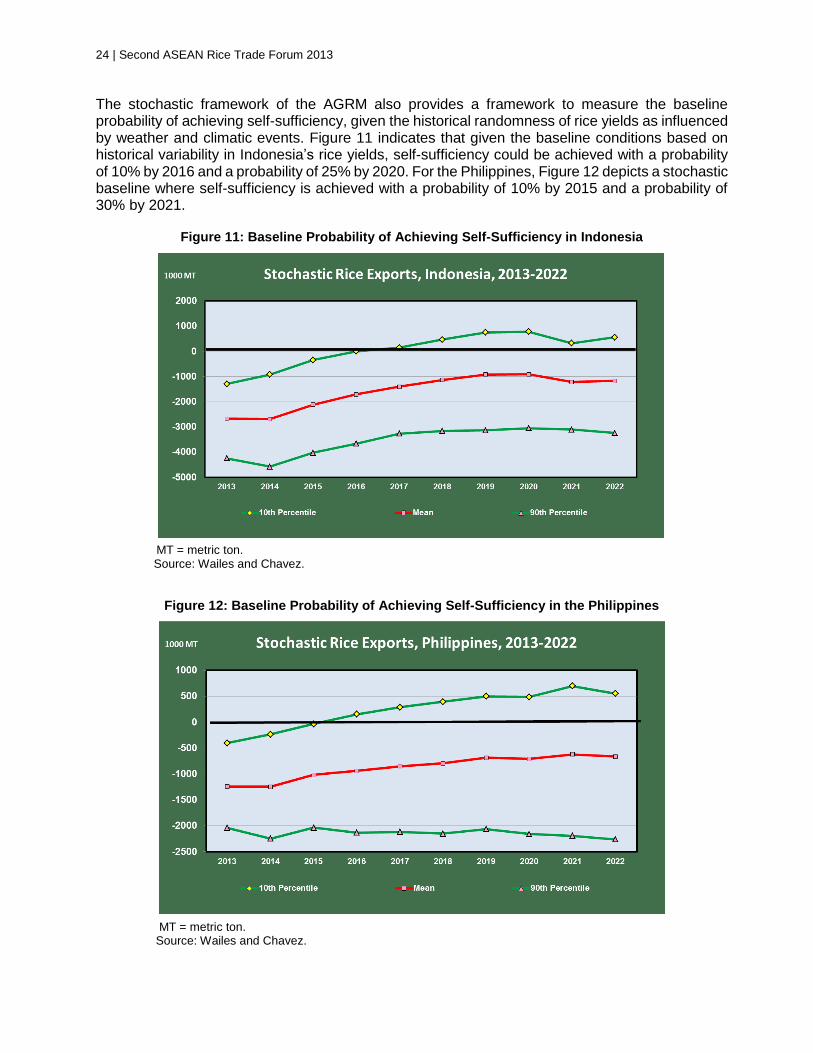

5.1 Baseline Results .............................................................................................................21 5.2 Use of the Baseline for Assessing Self-Sufficiency and Trade Impacts ...........................23

6. Conclusion ............................................................................................................................25

References ...............................................................................................................................27

Appendixes

1. Rice Models of the Arkansas Global Rice Economics Program ............................................29

Arkansas Global Rice Model ................................................................................................29 Riceflow Model .....................................................................................................................30

2. Aggregate Rice Supply and Utilization Tables for ASEAN Countries .....................................32

3. ASEAN Rice Supply and Utilization Tables by Country .........................................................37

4. Other Non-ASEAN Country Rice Supply and Utilization Tables from 2011–2012 to 2022–2023 ........................................................................................................................42

5. World Net Rice Trade, Per Capita Use, and Average Yield Tables by Country ...............................45

Tables

Table 1: World Rice Supply and Utilization, 2011–2022 .............................................................. 16 Table 2: Impact of Self-Sufficiency in Indonesia and the Philippines on Baseline Rice Exports from Viet Nam ................................................................................ 25 Table 3: Impact of Self-Sufficiency in Indonesia and the Philippines on Baseline World Long-Grain Rice Reference Price ............................................................. 25

Appendix 2 Table A2.1: ASEAN Rice Supply and Utilization .......................................................................... 32 Table A2.2: ASEAN Rice Trade .................................................................................................. 33 Table A2.3: ASEAN Rice Area Harvested ................................................................................... 34 Table A2.4: ASEAN Rice Yield per Hectare ................................................................................ 34 Table A2.5: ASEAN Rice Production ........................................................................................... 35 Table A2.6: ASEAN Rice Consumption ....................................................................................... 35

Table A2.7: ASEAN Per Capita Rice Consumption ..................................................................... 36 Table A2.8: ASEAN Rice Ending Stocks ..................................................................................... 36

Appendix 3 Table A3.1: Brunei Darussalam Rice Supply and Utilization ........................................................ 37 Table A3.2: Cambodia Rice Supply and Utilization ..................................................................... 37 Table A3.3: Indonesia Rice Supply and Utilization ...................................................................... 38 Table A3.4: Lao PDR Rice Supply and Utilization ....................................................................... 38 Table A3.5: Malaysia Rice Supply and Utilization ........................................................................ 39 Table A3.6: Myanmar Rice Supply and Utilization ....................................................................... 39 Table A3.7: Philippines Rice Supply and Utilization .................................................................... 40 Table A3.8: Singapore Rice Supply and Utilization ..................................................................... 40 Table A3.9: Thailand Rice Supply and Utilization ........................................................................ 41 Table A3.10: Viet Nam Rice Supply and Utilization ..................................................................... 41

Appendix 4 Table A4.1: People’s Republic of China Rice Supply and Utilization ........................................... 42 Table A4.2: Japan Rice Supply and Utilization ............................................................................ 43 Table A4.3: Republic of Korea Rice Supply and Utilization.......................................................... 43 Table A4.4: India Rice Supply and Utilization .............................................................................. 44 Table A4.5: Pakistan Rice Supply and Utilization ........................................................................ 44

Appendix 5 Table A5.1: World Net Rice Trade by Selected Countries and Prices ......................................... 45 Table A5.2: Per Capita Rice Consumption, World and Selected Countries ................................. 46 Table A5.3: Rice Yield per Hectare, World and Selected Countries ............................................ 47

Figures

Figure 1: Projections of Population Growth and Gross Domestic Product ..................................... 4 Figure 2: ASEAN Rice Area Harvested, Yield, Supply and Utilization ........................................... 5 Figure 3: ASEAN Rice Trade ........................................................................................................ 6 Figure 4: World Rice Prices, 1995–2022 ..................................................................................... 15 Figure 5: World Rice Area Harvested, Yield, Supply and Utilization ............................................ 16 Figure 6: Regional Shares of World Net Rice Trade, 2011–2022 ................................................ 17 Figure 7: Long-Grain Rice International Reference Prices (Stochastic Projection) ...................... 22 Figure 8: ASEAN Rice Ending Stocks (Stochastic Projection) ..................................................... 22 Figure 9: Indonesia’s Baseline Yield Gap to Achieve Self-Sufficiency ......................................... 23 Figure 10: Philippines’ Baseline Yield Gap to Achieve Self-Sufficiency ....................................... 23 Figure 11: Baseline Probability of Achieving Self-Sufficiency in Indonesia .................................. 24 Figure 12: Baseline Probability of Achieving Self-Sufficiency in the Philippines........................... 24

Appendix 6 Figure A6.1: Medium-Grain Rice Prices, FOB California (Stochastic Projection) ......................... 48 Figure A6.2: World Net Rice Trade (Stochastic Projection) ......................................................... 48 Figure A6.3: ASEAN Total Rice Area Harvested (Stochastic Projection) ..................................... 49 Figure A6.4: ASEAN Total Rice Production (Stochastic Projection) ............................................ 49 Figure A6.5: ASEAN Total Rice Consumption (Stochastic Projection) ........................................ 50 Figure A6.6: ASEAN Net Rice Exports (Stochastic Projection) .................................................... 50 Figure A6.7: ASEAN Net Rice Imports (Stochastic Projection) .................................................... 51 Figure A6.8: ASEAN Rice Stocks-to-Use Ratio (Stochastic Projection) ....................................... 51

Abbreviations ADB AGRM ASEAN FAPRI GDP kg Lao PDR PRC US USDA USDA FAS WTO

Asian Development Bank Arkansas Global Rice Model Association of Southeast Asian Nations Food and Agricultural Policy Research Institute gross domestic product kilograms Lao People's Democratic Republic People's Republic of China United States United States Department of Agriculture United States Department of Agriculture Foreign Agricultural Service World Trade Organization

Unless otherwise noted, “$” refers to US dollars.

Executive Summary Member states of the Association of Southeast Asian Nations (ASEAN) play a major role in the global rice market. Over the next decade, the ASEAN region is projected to account for 53% of net rice exports, 18% of net rice imports, 29% of harvested area, 25% of total rice production, and 22% of total rice consumption. Rice is the major food staple in ASEAN countries and thus plays a significant role in the food security concerns of the region. The rice price crisis that occurred in 2007–2008 has created a widespread sense of urgency among policy makers and other rice stakeholders to coordinate domestic policies and rice trade. This paper documents the current and projected status until 2022 of the rice economies in ASEAN countries by assessing their potential supply and demand paths over the next decade.1 Other Asian nations that have a significant role in the behavior and performance of the global rice economy are also discussed—the People’s Republic of China (PRC), Japan, the Republic of Korea, as well as India and Pakistan. While the ASEAN and global rice economies are always subject to uncertainties in weather and policies, abundant rice supplies and slow growth in rice consumption have resulted in downward pressure on prices. Driven by the use of higher-yielding rice varieties and other improved production technologies, the outlook for the rice economies is expected to follow this trend. The focus on self-sufficiency by major rice-consuming countries is expected to restrain rice trade and dampen international rice prices over the next decade. Domestic price policy supports, coupled with good weather, have resulted in strong rice harvests in India and Thailand and large stock inventories. Import demand growth in other ASEAN countries is limited for similar reasons. Much of the projected growth in rice trade is expected to come from other regions, particularly Africa. Despite the desire for self-sufficiency and a trend for production to grow faster than demand, major ASEAN rice importers—the Philippines and Indonesia—are expected to remain important importers. Expected expansion in rice exports from Cambodia and Myanmar will add to competitive price pressures that will result in lower international prices over time. Results of stochastic analysis, based on uncertainties associated with production, show that international long-grain rice reference prices are expected to range from $368 per ton to as high as $506 per ton, a gap of $138. Volatility in prices as a result of uncertain weather and policies thus remains a persistent food security concern with the ASEAN and global rice economies.

1 This report was prepared for the Second ASEAN Rice Trade Forum on 4–5 June 2013 in Yogyakarta, Indonesia. The

Asian Development Bank (ADB) provided technical assistance under TA-REG 7495: Support for the Association of Southeast Asian Nations Plus Three Integrated Food Security Framework, with financing from the Japan Fund for Poverty Reduction. The lead author, Eric J. Wailes, is Distinguished Professor and L. C. Carter Endowed Chair at the Department of Agricultural Economics and Agribusiness, Division of Agriculture, University of Arkansas, Fayetteville. Eddie C. Chavez is Senior Program Associate and a member of Dr. Wailes’ team that developed and maintains the Arkansas Global Rice Model and Riceflow model. This report does not necessarily reflect the views of ADB or the Government concerned, or the institutions at which the consultant works, and ADB and the Government and these institutions cannot be held liable for its contents.

2 | Second ASEAN Rice Trade Forum 2013

1. Overview 1.1 Purpose of this Outlook and its Significance for ASEAN Member nations of the Association of Southeast Asian Nations (ASEAN) play a major role in the global rice market. Over the next decade, the region’s rice output is projected to account for 53% of net exports, 18% of net imports, 29% of harvested area, 25% of total production, and 22% of total consumption of world rice. Rice is the major food staple in ASEAN and thus plays a very important role in the food security concerns of the region. The rice price crisis that occurred in 2007–2008 has catalyzed renewed interest and a widespread sense of urgency among policy makers and other rice stakeholders to forge more coordinated efforts to avoid a repeat of such an occurrence. The purpose of this outlook is to document the current state and the expected directions of the rice economies in ASEAN countries by assessing their potential supply and demand paths over the next decade. As the ASEAN region is a net rice exporter to the world, the region is influenced by factors prevailing in the global rice economy and cannot be looked at in isolation. An overview of the global rice sector is hence included in this report. It is important to note that over the last couple of years, the international rice market has been dominated by twin events. First is India’s official lifting of its ban on non-basmati rice exports as of September 2011. Second is Thailand’s implementation of its paddy pledging scheme in October 2011, a price-floor support policy for Thai farmers. The outlook is not a prediction but rather a framework to be used to discuss the management of risks of rice price volatility and their causes, including policies, supply distortions, and climate change. The Arkansas Global Rice Model (AGRM) framework provides the ASEAN region with functional structural models that can be used to assess intermediate and longer-term challenges faced by the region, which meet the goal of designing a set of coherent and coordinated policy actions to address emerging issues proactively. 1.2 The Arkansas Global Rice Model Framework The 10-year baseline deterministic and stochastic estimates presented in this report are generated using the AGRM. The AGRM is one of the two global rice modeling frameworks maintained by the University of Arkansas Global Rice Economics Program. The AGRM is a partial, nonspatial, multicountry statistical simulation, and econometric analytical framework. The other model, Riceflow, is a spatial equilibrium framework that tracks bilateral trade flows and rice value chain adjustments (Appendix 1). These models are updated on a regular basis and have been used to provide analyses for the Asian Development Bank, Food and Agriculture Organization of the United Nations, International Rice Research Institute (IRRI), Organisation for Economic Co-operation and Development, United States Department of Agriculture, the World Bank as well as many national governments and research institutes. All ASEAN member nations are modeled individually in AGRM. This model links all countries through rice prices and trade (Wailes 2012). The AGRM is disaggregated into 45 of the major rice-producing, -consuming and -trading countries; and five rest-of-the-world regional aggregations: Africa, the Americas, Asia, Europe, and Oceania. Each country and regional model includes a supply sector, a demand sector, trade, stocks, and price linkage equations.

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 3

The AGRM and Riceflow are research application tools that provide frameworks of the global rice economy and ASEAN countries as a system. They can thus address a wide range of issues and questions regarding price risks, policies, and supply and demand distortions (Wailes 2012). The 10-year baseline deterministic and stochastic estimates presented in this report are generated using the AGRM. The baseline assumes the following:

a continuation of existing rice sector policies;

macroeconomic projections from Global Insight, a global information company that provides economic forecasts, industry analysis, and market intelligence for over 200 countries and 170 industries;

no Doha Development Round of World Trade Organization (WTO) trade reforms; and

average weather conditions.

The stochastic component of the analysis provides a range of possible outcomes (confidence intervals) as opposed to the deterministic analysis that generates average point estimates. The stochastic framework is generated using multivariate empirical distributions of the rice yield for each of the 50 countries/regions in the model. Yield is used because it is the variable that not only varies by year and by country but is also very sensitive to changes in weather conditions and water availability—factors that are critical for rice production. A total of 200 random draws for each year are implemented using a 28-year empirical distribution of historical yields generated by the software Simulation and Econometrics to Analyze Risk (SIMETAR) developed by Richardson et al. (2008). Stochastic estimates are useful because underlying assumptions in the deterministic baseline usually do not hold true in reality, i.e., actual market outcomes deviate from average estimates. The theoretical structure, general equations, and other details of the AGRM can be found in the online documentation by Wailes and Chavez (2011). The AGRM has benefited from working closely with the Food and Agricultural Policy Research Institute (FAPRI) based at the University of Missouri, Columbia, which maintains United States (US) agricultural and other commodity models. FAPRI provided data on commodity prices and net returns projections, which are transmitted into the different AGRM country models. In particular, the prices and net returns for corn, soybeans, and wheat are relevant, considering that these commodities are substitute crops for rice in the US and other countries. Rice area competes with a number of crops, including soybeans, corn, and cotton in the rice-producing states in the US (Arkansas, California, Louisiana, Mississippi, Missouri, and Texas). In the People’s Republic of China (PRC), rice competes with corn in the provinces of Guangxi, Heilongjiang, Jilin, and Liaoning; with wheat in the province of Jiangsu; and with both corn and wheat in the provinces of Anhui, Chongqing, Guizhou, Hubei, Ningxia, Sichuan, and Yunnan. In India, rice competes with wheat, particularly in the northern states (Carriquiry et al. 2012 as cited by Wailes and Chavez 2013). The historical rice data are obtained from the Production, Supply, and Distribution report (Rice Outlook) of the United States Department of Agriculture (USDA) Foreign Agricultural Service (FAS) and Economic Research Service as of March 2013. The AGRM rice marketing years by country generally follow the USDA system. For example, the year 2012 or marketing year 2012–2013 in the model refers to January 2013–December 2013 for Indonesia, Thailand, and Viet Nam; October 2012–September 2013 for India; July 2012–June 2013 for the Philippines; and April 2012–March 2013 for South American countries. Hence, supply values for 2012 are fixed for some countries

4 | Second ASEAN Rice Trade Forum 2013

while still dynamic for a number of countries.2 As such, the annual cumulative growth rates as well as the total growth presented in this document are reckoned from 2011 and cover the 11-year period of 2011–2022. For the most part, the data on the economies of individual countries came from the online Central Intelligence Agency World Fact Book (2013).

2. ASEAN Rice Outlook3 2.1 Rice Harvested Area and Production The conditioning macroeconomic environment for the rice outlook is based on projections of population growth and economic growth (gross domestic product [GDP]) for the region. While the ASEAN population growth has historically exceeded world averages, it is expected to converge to the global average of approximately 1% until 2022. Projections for ASEAN and the ASEAN Plus Three,4 and for India and Pakistan, have slightly declining GDP growth but are clearly more robust than for the rest of the world (Figure 1). Appendix 2 provides the estimates for the ASEAN region, Appendix 3 for the 10 ASEAN member nations, Appendix 4 for the non-ASEAN countries (PRC, Japan, Republic of Korea, as well as India and Pakistan), and Appendix 5 for the world net rice trade, per capita use, and average rice yield tables by country.

Figure 1: Projections of Population Growth and Gross Domestic Product

ASEAN = Association of Southeast Asian Nations; Plus3 = People's Republic of China, Japan, Republic of Korea;

IN = India; PK = Pakistan. Source: Wailes and Chavez.

Total ASEAN rice output is projected to expand by a total of 15.9 million tons over the baseline period, growing at 1.2% annually, from nearly 114.6 million tons in 2011 to 128.8 million tons in 2022—with the growth coming mainly from yields as area harvested gains only marginally (Figure 2 and Table A2.1). The ASEAN region contributes just under 25.0% of global rice production. The ASEAN rice harvested area accounts for 29.0% of the global total. The region’s rice area harvested is projected to expand by a total of 414,000 hectares over the next decade, reaching 46.66 million hectares in

2 For details, see the USDA Foreign Agricultural Service site: http://www.fas.usda.gov/psdonline/psdAvailability.aspx 3 An extended version of the AGRM baseline is available upon request. The extended version, World Rice Situation and

Outlook 2012-2022, provides detailed tables and projections for all key individual rice-importing and rice-exporting countries for all regions of the world.

4 The ASEAN Plus Three is composed of the 10 member nations of ASEAN—Brunei Darussalam, Cambodia, Indonesia, the Lao People’s Democratic Republic, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Viet Nam—plus the three East Asian nations of the People’s Republic of China, Japan, and the Republic of Korea.

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 5

2022. This is equivalent to a marginal growth of 0.08% per year. The average rice yield of the region is projected to improve from 2.47 tons per hectare in 2011 to 2.76 tons per hectare in 2022—a total increase of 319 kilograms (kg) per hectare, equivalent to an annual growth of 1.12% (Appendix 2).

Figure 2: ASEAN Rice Area Harvested, Yield, Supply and Utilization

Source: Wailes and Chavez.

The region’s average rice yield level is lower than the world average by about 15%. However, the yield gap is projected to narrow down to 403 kg per hectare in 2022 from 493 kg per hectare in 2011, primarily as more countries in the region expand the use of hybrid rice varieties. Thus, improving farm productivity is the most promising direction that countries in the region need to focus on, which entails expanding the use of high-yielding hybrids and improved production technologies. This should be the priority both of countries aiming for rice self -sufficiency and those that are trying to expand exports in the face of limited land and other production resources. Challenges for rice expansion in the region include constraints on land and water resources; competition from other crops and uses; high input prices; farm demographics; climate change; and the emerging issue on rice carbon and water footprints. Another concern that has implications for the future of rice farming is the migration of people from rural areas to urban centers in search of alternative non-farm income opportunities. In conjunction with aging farmers, this situation can aggravate labor scarcity in the agricultural sector of the region. 2.2 Rice Consumption Rice consumption is driven by income, population, and other demographics. Rising incomes dampen rice demand in some Asian countries where rice is considered an inferior good. Other factors include aging populations and increasing health consciousness that shift diet preferences away from carbohydrates and toward protein-based foods. The ASEAN rice total consumption accounts for 22.1% of the world total. Over the next decade, ASEAN rice total use will expand from 100.7 million tons in 2011 to 113.5 million tons in 2022, attaining a growth of 1.10 % annually (Figure 2). The average ASEAN rice per capita use has been 2.5 times the world average (164 kg versus 65 kg over the last decade). The growth in the region’s total rice consumption over the baseline period is driven by a population growth of 1.06% annually (Table A2.6) as the average per capita use of rice is projected to be flat (Table A2.7). 2.3 Rice Exports ASEAN net rice exports declined 16.9% in 2011 from the 2010 level of 18.6 million tons, largely due to the 4.1-million ton or 39.3% drop in Thai exports as a result of the country’s paddy pledging

6 | Second ASEAN Rice Trade Forum 2013

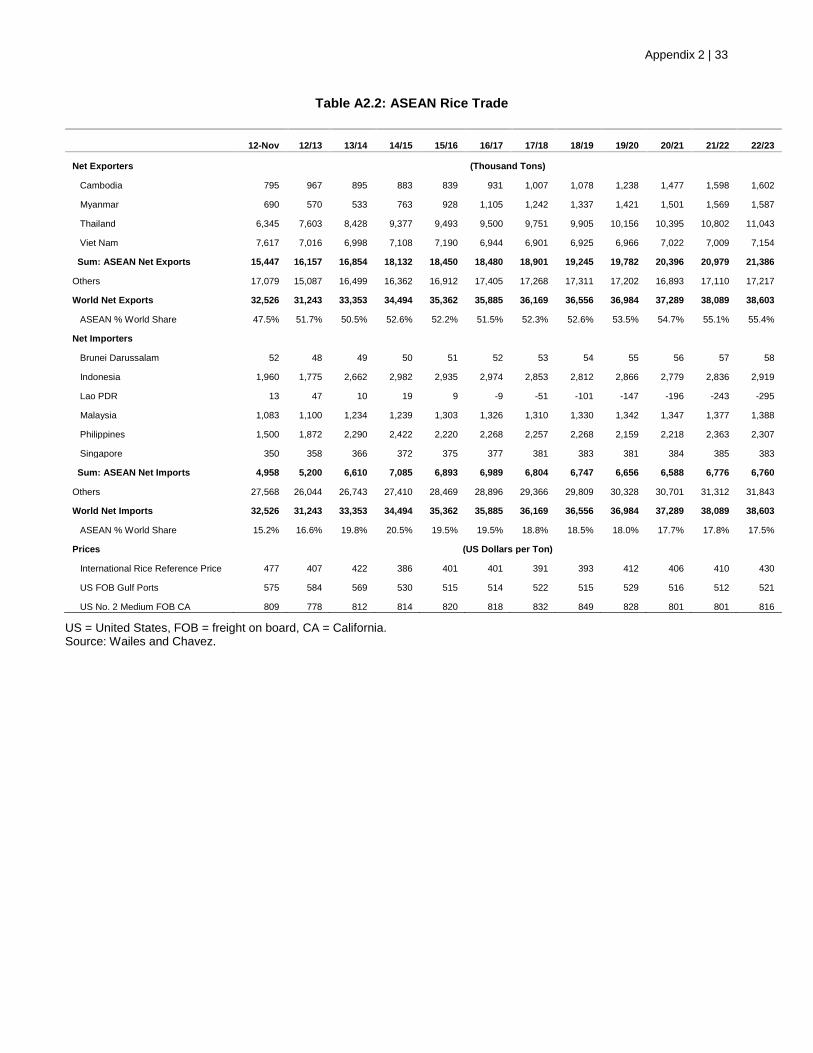

program that made its quoted export prices much higher than its competitors’ prices. The region’s net rice exports went up 4.6% in 2012 as Thailand’s export shipments gained 19.8%, mainly through government-to-government sales. Reflecting the same historical average share, the total ASEAN net rice exports are expected to account for 52.6% of the total global volume over the projection period (2011–2022). The combined net rice exports of ASEAN are projected to grow at 3.0% per year, from 15.4 million tons in 2011 to 21.4 million tons in 2022 over the same period. Two of the top five world rice exporters, Thailand and Viet Nam, are both ASEAN members, which are projected to jointly account for about 47% of the growth of global net exports during the same period (Figure 3 and Table A2.2).

Figure 3: ASEAN Rice Trade

Lao PDR = Lao People's Democratic Republic. Source: Wailes and Chavez.

Despite Thailand’s unpopular and controversial paddy pledging program, the country is expected to reestablish its strong presence in the global rice market over the next decade. Recent government pronouncements indicate that the country has decided to sell its mounting rice stockpile both into the open market and through government-to-government sales. The Thai government is expected to incur substantial financial losses in the short term as it sells its high-priced rice at competitively lower prices. Cambodia and Myanmar are projected to increase their rice exports steadily as production continues to exceed consumption. Good availability of land and water resources in these two countries offers opportunities to expand rice production and rice exports. This, however, is subject to their ability to build the necessary infrastructure and institutional support to export larger volumes on a sustained basis. Over the last few years of the baseline, both countries are projected to reach a similar magnitude of rice exports of approximately 1.6 million tons. The Lao People's Democratic Republic (Lao PDR) also has the potential to become an important rice exporter in the region, subject likewise to its ability to successfully undertake infrastructure capacity and institutional building. Over the last half of the baseline period, the country is projected to shift from being a net rice importer to a net rice exporter, reaching nearly 200,000 tons of net rice exports by 2022. The issue of unofficial cross-border trade of rice in the ASEAN region remains unresolved. The total elimination of this problem is challenging. However, minimizing it will improve transparency in rice trade and prices, and will contribute to generating more reliable market information for better decision-making purposes.

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 7

2.4 Rice Imports The average share of ASEAN net rice imports to total world trade is projected to expand from 16.5% over the last decade to 18.3% over the next decade—growing from just under 5.0 million tons in 2011 to 6.8 million tons in 2022 (Figure 3 and Table A2.2). The combined ASEAN net rice imports declined 15.9% in 2011 from the 2010 level as a result of a 36.7% reduction in Indonesia’s imports, as the country supplies its domestic rice needs from expanded production and withdrawal from its stocks. The region’s net rice imports recovered by 4.9%, from 4.96 million tons in 2011 to 5.2 million tons in 2012, as the projected increase in Philippine imports for stock replenishment more than compensates for the decline in Indonesia’s imports—as the latter opts to continue withdrawing from its stocks. Over the last few years, the Indonesian and Philippine governments have focused on their goal of rice self-sufficiency and their efforts should be commended. As a result, the two countries are projected to make gains in productivity, raising output mostly from increased yields with the expanded use of high-yielding hybrids as area harvested remains relatively flat. Over the projection period, the average rice yields are projected to grow annually by 1.1% for Indonesia, and by 1.8% for the Philippines. However, attaining rice self-sufficiency presents a daunting challenge for the two countries, considering that the historical average annual production gap for Indonesia stands at 7% (equivalent to 2.9 million tons) of annual consumption, and that of the Philippines is 16% (about 2.2 million tons). Estimates indicate that if Indonesia and the Philippines were to prioritize maintaining relatively safe stock levels over the baseline period—even lower than the historical path—chances are they will remain the top rice importers in ASEAN: Indonesia will rank second, and the Philippines, third, with a combined share of 13.6% of global net rice import volume. The region’s growth in rice demand is driven mainly by population growth, as per capita use in most countries is on the decline, with per capita use in a few countries either flat or with marginal gains over the projection period. 2.5 Rice Stocks The ASEAN average rice stocks-to-use ratio is projected to increase from 16.9% during the last decade to 24.4% over the next decade due to the paddy pledging-related buildup in Thai stocks. The annual stocks-to-use ratio will increase steadily from 19.3% in 2011 to 28.1% in 2022. The average share of ASEAN rice stocks to the global total is estimated to go up from 17.2% during the last decade to 21.1% over the baseline period. For the projection period, the annual share of the region’s rice stocks in the global total would expand from 18.3% in 2011 to 22.2% in 2022 (Table A2.8).

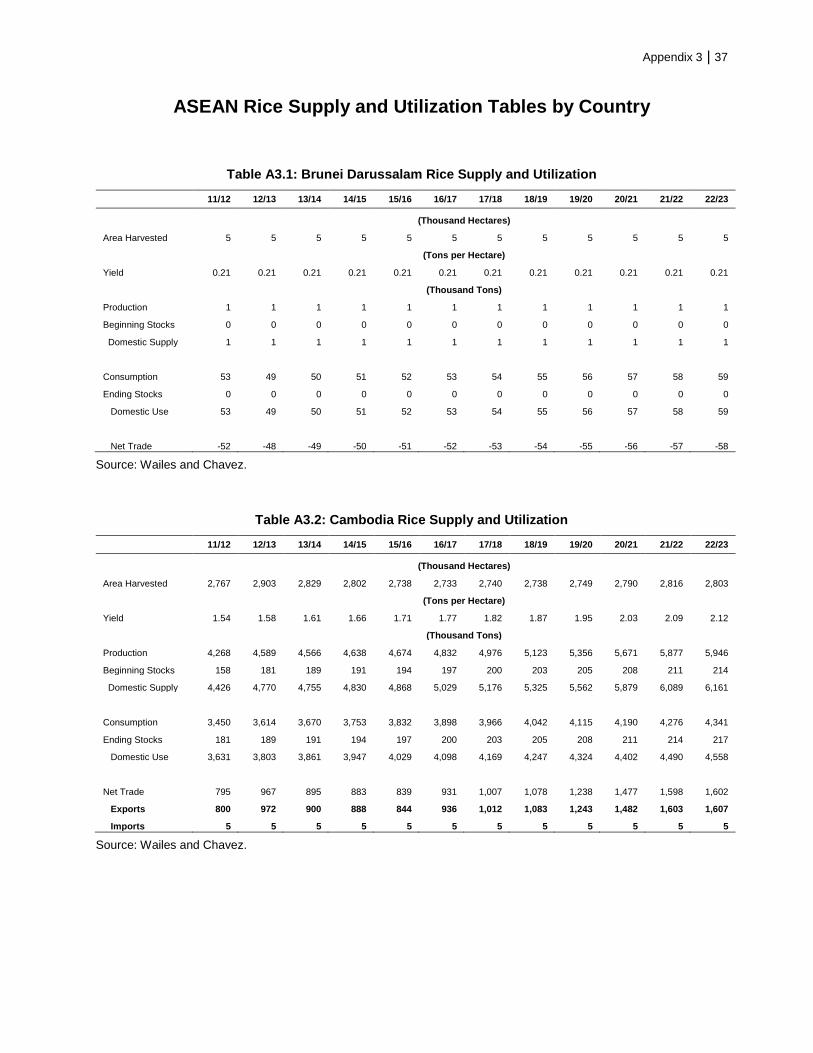

3. ASEAN Country Rice Outlook5 3.1 Brunei Darussalam

Economy Brunei Darussalam’s economy is projected to grow at 2.7% per year in real terms. It is heavily

5 See Appendix 2 for individual ASEAN country rice situation and outlook supply and utilization estimates.

8 | Second ASEAN Rice Trade Forum 2013

dependent on revenues from crude oil and natural gas, which account for 60% of GDP and 90% of exports. The country is the third largest oil producer in Southeast Asia and the fourth largest producer of liquefied natural gas in the world. By sector, the country’s GDP is composed of 0.6% agriculture, 71.7% industry, and 27.7% services. The country’s population is 415,717 and grows at 1.69% per year; 89% is under 55 years old. Per capita income, at $50,500 in 2012, is one of the highest in the world. The labor force totals 205,800, with 4.2% in agriculture, 62.8% in industry, and 33.0% in services. The local currency, the Brunei dollar (BND or B$), had an exchange rate of B$1.25 in 2012 and is projected to appreciate relative to the US dollar over the baseline period.

Rice Supply and Demand The country consumed 53,000 tons of milled rice in 2011, with about 97% coming from imports. Rice per capita use generally ranges from 120 kg to 123 kg per year over the projection period. Given the population growth, this translates to an annual increase of about 2.0% in total rice consumption. To meet this demand, net rice imports are seen to grow by just under 1.0% per year (Table A3.1). Only 2.1% of the country’s 5,765-square kilometer land area is considered arable. The USDA reports that the country produces 1,000 tons of milled rice from 1,000 harvested hectares. Eventually, the government plans to increase the area planted to rice to 5,000 hectares, depending on the availability of suitable land that can be developed without damaging the ecological balance. To improve food security, the country has a goal of 60% self-sufficiency in rice by 2015 despite its limited land. The government has been seriously exploring ways to increase rice output since 1978, and indications are that it will continue to do so. Recent efforts are focused on availing of rice technical assistance and training from neighboring countries. Another option mentioned is entering into joint venture agreements with neighboring rice-producing countries to own and operate rice farms. 3.2 Cambodia

Economy Garments, construction, agriculture, and tourism have been driving Cambodia’s economic growth since 2004, causing real GDP to grow over 6% per year in 2010–2012, among the strongest in Southeast Asia. The garment industry accounts for 70% of the country’s total exports. The economy is composed of 34.7% agriculture, 24.3% industry, and 41% services. The population is 15.2 million and grows at 1.69% per year; 91% is below 55 years old. Per capita income is $2,400. Out of its labor force of 7.9 million, 55.8% is in agriculture, 16.9% in industry, and 27.3% in services. The local currency, the riel (KHR or KR), had an exchange rate of KR4,075 in 2012 and is projected to depreciate relative to the US dollar over the baseline, which will improve the country’s export competitiveness

Rice Supply and Demand The country harvested 2.77 million hectares of rice in 2011, yielding an average of 1.54 tons per hectare. Total milled rice production stands at 4.27 million tons, growing at 3.0% per year, mainly from yield growth (2.9%) as area is up only marginally (0.1%). Total rice consumption (3.45 million tons in 2011) grows at 2.1% annually and is projected to reach 4.34 million tons in 2022, mainly as a result of 1.5% population growth as per capita use increases only 0.60% per year. The country’s

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 9

rice exports expand at 6.6% per year, which are estimated to double from 795,000 tons in 2011 to 1.6 million tons in 2022. The USDA’s rice export figures for Cambodia are much higher than those quoted or reported elsewhere because the USDA includes both the estimated cross-border trade and the official trade for rice. This reportedly involves some information gathering and verification from the ground. The USDA believes this approach makes the supply and demand data more realistic. As Cambodia attains improvements in yields and continues to have production surplus, rice exports are projected to expand steadily, doubling from 800,000 tons in 2011 to 1.61 million tons by 2022 (Table A3.2). However, to accelerate official rice exports at a sustained level, Cambodia needs to accomplish two things: to invest in infrastructure development, and to control and manage the reportedly rampant unofficial cross-border trade of unmilled rice into its neighboring countries. In so doing, the country’s farmers can benefit from improved value-added revenues by directly exporting milled rice. The settlement of the cross-border trade issue will require strong political will from top-level officials of the countries involved in formulating well-coordinated and implementable diplomatic solutions. 3.3 Indonesia

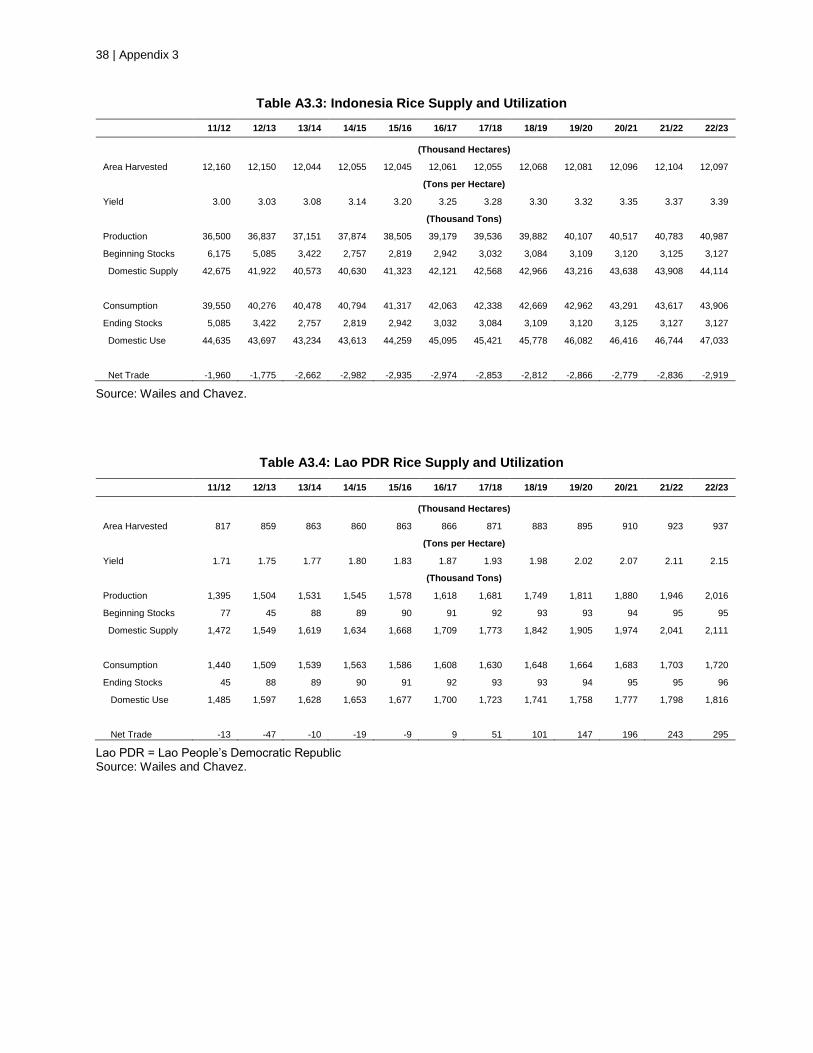

Economy During the global financial crisis, Indonesia outperformed its regional neighbors and joined the PRC and India as the only Group of 20 members that posted growth in 2009. Introducing a number of significant financial reforms and conservative fiscal policies, the country’s economy grew over 6% in 2010 and 2011. Estimated real GDP growth in 2012 is 6%. By sector, the country’s economy is composed of 15.4% agriculture, 46.5% industry, and 38.1% services. The country’s population is 251.2 million and projected to grow at 1.03% annually; 86% is under 55 years old. Per capita income is $5,000. Its labor force stands at 118 million, with 38.9% in agriculture, 22.2% in industry, and 47.9% in services. The local currency, the rupiah (IDR or Rp), had an exchange rate of Rp9,670 in 2012 and is projected to depreciate relative to the US dollar over the baseline period.

Rice Supply and Demand The country’s 12.16 million hectares of harvested rice produced 36.50 million tons of milled rice in 2011 at an average yield of 3.0 tons per hectare. Total rice production is projected to grow at 1.1% annually, solely from yield gain. The rate of land conversion to non-agricultural uses near urban areas in Java is at a reported high rate of 100,000 hectares per year. This has made it difficult to expand the rice area, which does not augur well for the country’s rice self-sufficiency goal. Total rice consumption (39.55 million tons in 2011) grows at 0.95% per year, mainly as a result of population growth as per capita consumption gains under 0.1% annually (Table A3.3). Indonesia sources about 6% of its domestic rice requirement from imports and its government has been constantly trying to limit importation. Recently, however, the country signed a 5-year agreement with Viet Nam to import 1.5 million tons of rice annually starting in 2013. The country’s rice imports recently declined dramatically, from 3.1 million tons in 2010 to under 2.0 million tons in 2011, due to the combination of increased domestic production and withdrawal from its stocks. During the same period, while the total area harvested increased by 85,000 hectares and the average yield improved by 60 kg per hectare, there was also a substantial decline of 18% (or 1.1 million tons) in its stocks. Rice imports are estimated to further contract to 1.8 million tons in 2012 as the country continues to resort to withdrawing from its stocks. Assuming a stock level equivalent to 26 days of

10 | Second ASEAN Rice Trade Forum 2013

consumption, annual rice imports are projected to remain around 2.8 million tons. This estimate is relatively low compared to the historical level of about 49 days during the last decade, but this is consistent with the stock management style shown recently by the Indonesian government. 3.4 Lao People’s Democratic Republic

Economy Still a one-party communist state, the country began decentralizing control and encouraging private enterprise in 1986, causing its economy to attain a robust growth north of 7% from 2008–2012, albeit from a low base. The Lao PDR, however, is heavily dependent on capital-intensive natural resource exports and is constrained by underdeveloped infrastructure especially in rural areas. By sector, the country’s economy is composed of 26.0% agriculture, 34.0% industry, and 40.0% services. The country’s population is 6.70 million and projected to grow at 1.65% per year; 91% is under 55 years old. Per capita income is $3,000. Out of its labor force of 3.7 million, 75.1% is in agriculture, and the rest in industry and services. Agriculture labor is dominated by rice cultivation in lowland areas. The local currency, the kip (LAK or KN), had an exchange rate of KN8,018 in 2012 and is expected to depreciate relative to the US dollar over the projection period.

Rice Supply and Demand The country has 817,000 hectares of rice, producing 1.4 million tons of milled rice in 2011 at an average yield of 1.71 tons per hectare. Total rice production is estimated at 3.4% per year, of which 2.1% comes from yield and 1.3% from the annual gain in area harvested. Total rice consumption (1.44 million tons in 2011) grows at 1.63% per year, resulting mainly from population growth as per capita rice consumption grows only 0.09% annually over the baseline period. With production growing faster than consumption, the country is expected to become a minor rice exporter over the next decade, with shipments projected to grow from 9,000 tons in 2016 to 295,000 tons by 2022 (Table A3.4). 3.5 Malaysia

Economy Malaysia’s economy is driven by exports, mainly electronics, oil and gas, palm oil, and rubber. However, the current government is reportedly trying to boost domestic demand and reduce dependence on exports. The country’s economy grew by 4.5% in 2012. By sector, the country’s economy is composed of 11.9% agriculture, 41.2% industry, and 46.8% services. The population is 29.63 million and projected to grow at 1.54% per year; 87% is under 55 years old. Per capita income is $16,900. The labor force stands at 12.92 million, with 11.1% in agriculture, 36.0% in industry, and 53.5% in services. The local currency, the ringgit (MYR or RM), is projected to have a stable exchange rate of around RM3.07 to the US dollar over the baseline period.

Rice Supply and Demand The country harvested 675,000 hectares of rice in 2011, producing 1.69 million tons of milled rice at an average yield of 2.50 tons per hectare. Total rice production grows at 1.33% annually, coming from yield improvement of 0.98% and an increase in area harvested of 0.34%. For the longer term, the government is reportedly encouraging large-scale private-sector commercial paddy production, especially in the states of Sabah and Sarawak where land is still abundant.

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 11

The government has reportedly reduced the rice self-sufficiency target to 70% from the original goal of 90%. Under the new food security policy, the government’s strategies are designed to ensure a sufficient supply of rice that include maintaining a government rice stockpile equivalent to 45 days of consumption, entering into long-term contract agreements to import rice, and increasing the productivity of existing rice areas through infrastructure upgrade, without developing new areas. Total rice consumption (2.71 million tons in 2011) grows at 1.90% per year, which is largely due to population growth as per capita consumption is up only 0.50% annually. Rice self-sufficiency is currently around 60%. The balance of Malaysia’s rice needs is sourced mainly from Viet Nam, Thailand, and Pakistan, in that order. The country’s net rice imports are estimated to grow by 2.3% per year, from 1.08 million tons in 2011 to 1.39 million tons by 2022 (Table A3.5). 3.6 Myanmar

Economy Myanmar is a resource-rich country but its economy is reportedly constrained by pervasive government controls, inefficient economic policies, and rural poverty. While the government has good economic relations with neighboring countries, significant improvements are needed in the business climate and the political situation to attract serious foreign investments. Despite the constraints, however, the country’s economy attained real growth of 5.5% in 2011 and 6.2% in 2012. By sector, the country’s economy is composed of 38.8% agriculture, 19.3% industry, and 41.8% services. The country’s population is 55.17 million and grows at 1.07% per year; 88% is under 55 years old. Per capita income is $1,400. The labor force totals 33.41 million, with 70.0% in agriculture, 7.0% in industry, and 23.0% in services. The local currency, the kyat (MMK or MK), had an exchange rate of MK868 in 2012 and is projected to have a relatively stable exchange rate with the US dollar over the baseline.

Rice Supply and Demand The country’s harvested rice area is projected to expand at 0.65% per year, from 6.5 million hectares in 2011 to nearly 7.0 million hectares in 2022. Total milled rice production reached 10.82 million tons in 2011 and is growing at 1.94% per year, 1.29% of which comes from yield growth. Average yield is forecasted to improve from 1.66 tons per hectare in 2011 to 1.92 tons per hectare in 2022. Total rice consumption will increase from 10.2 million tons in 2011 to 11.7 million tons in 2022, equivalent to a growth of 1.25% annually, with nearly 1.0% resulting from population growth and 0.26% from per capita consumption (Table A3.6). As Myanmar’s yield-based growth in domestic rice output continues to exceed that of domestic consumption, rice exports are projected to expand steadily over the baseline, from 690,000 tons in 2011 to 1.59 million tons by 2022. As in the case of Cambodia, adequate investments in infrastructure development will be required to achieve this level of growth. The country has promising opportunities to expand its rice exports due to substantial improvements in milling facilities. Since 1990, the number of rice mills reportedly increased from 225 to 1,230, rice polishers from 10 to 28, and color sorters from 1 to 9. These improvements should support postharvest quality and loss reduction, which would augur well for expanding the country’s presence in the global rice market.

12 | Second ASEAN Rice Trade Forum 2013

3.7 Philippines

Economy Driven by consumer demand, exports, investments, and election-related spending, the Philippine economy expanded by 7.6% in 2010. Growth slowed to 3.9% in 2011 but recovered and grew by 6.6% in 2012. The country weathered the recent global recession better than most of its Asian neighbors due to its minimal exposure to troubled international investments, lower dependence on exports, relatively resilient domestic consumption, a growing outsourcing industry on business processing, and strong support from the dollar remittances of overseas workers. By sector, the country’s GDP is composed of 11.9% agriculture, 31.1% industry, and 57.0% services. The country’s population is 105.72 million and grows at 1.87% per year; 90% is under 55 years old. Per capita income stands at $4,300. The country has a labor force of 40.36 million, with 32.0% in agriculture, 15.0% in industry, and 53.0% in services. The exchange rate of the Philippine peso (PHP or P), the local currency, was P42.23 in 2012 and is projected to depreciate slightly relative to the US dollar over the baseline

Rice Supply and Demand The country produced 10.70 million tons of milled rice from 4.58 million hectares in 2011, based on an average yield of 2.34 tons per hectare. Total rice production is projected to grow at 1.91% annually, largely from yield improvements (1.80%) by using more hybrids, as potential expansion in harvested area is limited. Rice faces land use competition from industrialization and the growth of the real estate sector in the country (Oryza 2013). This makes rice area expansion and the attainment of the country’s rice self-sufficiency goal much more challenging. Total rice consumption is estimated to grow at 1.71% per year, from 12.85 million tons in 2011 to 15.48 million tons in 2022, solely as a result of population growth as per capita consumption declines marginally (Table A3.7). The Philippines imports about 14% of its domestic rice requirement, and the government tries to limit importation in line with its self-sufficiency target in 2013. The government planned to reduce rice imports from 1.5 million tons in 2011 to 0.5 million tons in 2012 by increasing support to farmers and encouraging the use of hybrids. However, to maintain a reasonable stock level, it is assessed that the country has to import an estimated 1.9 million tons in 2012. Assuming that a stock level equivalent to 50 days of consumption is maintained, annual rice imports are projected to remain around 2.2 million tons. This amount is below the country’s historical stock level of about 126 days during the last decade—or even the Philippine government’s 90-day buffer stock policy. However, this is in line with the recent practice of the government to minimize rice importation in support of the country’s self-sufficiency goal. 3.8 Singapore

Economy Singapore has a very successful free market economy that depends heavily on the exportation of consumer electronics, information technology products, pharmaceuticals, and financial services. The country’s average real GDP grew above 8% in the 4 years preceding the global financial crisis, but contracted as exports weakened during the crisis, then recovered in 2010 and 2011, before declining again to 1.3% in 2012 as a result of the recession in Europe. Singapore’s economy is composed of 26.8% industry, 73.2% services, and marginal agriculture. The country’s per capita

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 13

income is $60,900, the seventh highest in the world. In Asia, only Qatar has a higher level of income at $102,800, which is also the highest in the world. The country’s population is 5.46 million and grows at 1.99% per year; 82% is under 55 years old. Out of its labor force of 3.62 million, 0.1% is in agriculture, 19.6% in industry, and 80.3% in services. The local currency, the Singapore dollar (SGD or S$), had an exchange rate of S$1.25 in 2012 and is projected to appreciate slightly relative to the US dollar over the next decade.

Rice Supply and Demand The country does not produce rice, depending entirely on the international market for its domestic rice needs. The USDA does not show any rice stocks for the country, so imports are assumed to simply match total consumption. The country’s imports are projected to grow at 0.83% annually, from 350,000 in 2011 to 383,000 by 2022 (Table A3.8). To ensure food security, the country is reportedly aiming to transform itself from being a passive food importer to a more active contributor to the regional and global food system through urban agribusiness, realizing that it has little land to grow its own food. The strategy has four prongs: (i) to accelerate research and development; (ii) to turn Singapore into an agribusiness hub where the private sector will play a key role; (iii) to develop Singapore’s own domestic market into a “test lab” for urban agriculture (e.g., “rooftop farming”); and (iv) to shift toward greater local production of three key food items—eggs, leafy vegetables, and fish (Kassim 2011). 3.9 Thailand

Economy Growth in Thailand’s economy is driven by industrial and agricultural exports, consisting mainly of electronics, agricultural commodities, automobiles and parts, and processed foods. Thailand’s economy expanded 7.8% in 2010, but growth was interrupted in the last quarter of 2011 by historic flooding in the industrial areas of Bangkok and the surrounding provinces. The economy recovered in 2012, with the GDP growing at 5.5%. The economy is composed of 8.6% agriculture, 39.0% industry, and 52.4% services. The population is 67.45 million and growing at 0.54% per year; 80% is under 55 years old. Per capita income is $10,000. The country has a labor force of 39.77 million, with 38.2% in agriculture, 13.6% in industry, and 48.2% in services. The local currency, the baht (THB or B), had an exchange rate of B31.09 in 2012 and is projected to be stable relative to the US dollar over the baseline.

Rice Supply and Demand The country harvested 11.0 million hectares of rice in 2011, yielding 1.86 tons per hectare on average. Total milled rice production is 20.46 million tons, growing at 0.89% per year, which solely comes from yield growth as area harvested is flat over the projection period. Total rice consumption (10.40 million tons in 2011) is projected to grow at 0.41% annually, solely due to population growth as per capita use declines marginally over the same period (Table A3.9). The rice pledging scheme implemented by the government starting in October 2011 has constrained Thai rice exports, causing a substantial decline in shipments and a consequent excessive buildup in stocks. The government announced recently that a portion of the rice stocks, especially the old crop, will be sold through the open market and government-to-government

14 | Second ASEAN Rice Trade Forum 2013

arrangements—even at a loss. The country has to do this not only to get rid of the deteriorating old rice crops in storage but also to recoup its top position in global rice trade, which it has recently lost to India. The country’s chances are favorable, given its good infrastructure resources and concerted focus on developing a strong presence in branded high-quality rice (Wailes and Chavez 2013b). The baseline thus projects that Thailand will eventually regain its leading market share in the international rice market. 3.10 Viet Nam

Economy In recent years, the Vietnamese government has reaffirmed its commitment to economic modernization. Membership in the WTO in January 2007 has promoted export-driven industries. Vietnam also became an official negotiating partner in the Trans-Pacific Partnership trade agreement in 2010. The global recession hurt Viet Nam's export-oriented economy, with the GDP growing at only 5%, its slowest rate of growth since 1999. In 2012, however, annual exports recovered and expanded more than 18%. The country’s economy is projected to have a robust growth of about 6.5% over the projection period—one of the strongest among the ASEAN economies. Viet Nam’s economy is composed of 21.5% agriculture, 40.7% industry, and 37.7% services. The country’s population is 92.48 million and growing at 1.05% annually; 87% is under 55 years old. Per capita income is $3,500. The labor force of 39.77 million constitutes 48.0% in agriculture, 21.0% in industry, and 31.0% in services. The local currency, the dong (VND or D), had an exchange rate of D20,828 in 2012 and is projected to depreciate relative to the US dollar over the baseline.

Rice Supply and Demand The country harvested 7.74 million hectares and produced 27.08 million tons of milled rice in 2011, or an average yield of 3.50 tons per hectare, which grows at 0.83% annually. Total milled rice production grows at 0.57% per year, all of which comes from yield growth as area harvested contracts by 0.26% annually. Total rice consumption (19.65 million tons in 2011) grows at 0.90% per year, solely due to population growth as per capita consumption declines by 0.04% per year (Table A3.10). Taking advantage of reduced rice exports from Thailand as a result of the paddy pledging scheme, Viet Nam (along with India and Pakistan) has expanded its rice exports and pegged its price at very competitive world reference levels. As a result, Viet Nam’s net rice exports in 2011 exceeded that of Thailand’s by 1.3 million tons. The country aims to strengthen its presence in the international market by focusing on improved rice quality and by expanding export opportunities to new markets such as the PRC. An issue that the country may have to address is the reported unofficial cross-border rice trade coming from its neighboring countries. As growth in Viet Nam’s total domestic rice consumption exceeds domestic output, the country’s exports are projected to be relatively flat, around 7.0 million tons over the baseline.

4. Global Rice Outlook 4.1 International Rice Prices The international rice prices are highly volatile due to a number of reasons. Rice has inelastic supply

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 15

and demand throughout much of Asia, where it is the dominant food staple. While rice is the primary staple for half of the world’s population, it is thinly traded. Only about 7% of rice production is traded as opposed to 10% for coarse grains and 16% for wheat (Wailes and Chavez 2012). The international rice trade is highly concentrated, with five dominant players—Thailand, India, Viet Nam, Pakistan, and the US, in that order—accounting for 89% of global net trade. Despite slow growth in rice consumption, increased rice output, driven by the use of higher-yielding varieties and hybrids and other improved production technologies as well as the more focused self-sufficiency programs of major rice-consuming countries, is expected to expand supply. This will dampen international rice prices over the next decade. The situation is beneficial for food-deficit rice-importing countries in the developing world but could have uncertain response from rice producers and exporters (Wailes and Chavez 2013b). The average international long-grain rice reference price is projected to decline steadily from $477 per ton in 2011 to $430 per ton in 2022. The average medium-grain rice price, however, would be generally stable above $800 per ton over the same period (Figure 4).

Figure 4: World Rice Prices, 1995–2022

LG = long-grain (rice), MG = medium-grain (rice), FOB = freight on board, CA = California. Source: Wailes and Chavez.

4.2 Global Rice Supply and Demand Rice is the most important food crop of the developing world and the staple food of more than half of the world's population, accounting for more than 20% of daily caloric requirement (IRRI 2013). World rice production, rice consumption, rice stocks, and rice trade projections are shown in Table 1. The stocks-to-use ratio is projected to increase to more than 28% over the projection period, providing a potential improvement in global rice and food security. Over the baseline period (2011–2022), the world rice output grows at 0.8% per year, with 0.7% coming from yield improvement and 0.1% from slight growth in area harvested (Figure 5 and Table 1). Driven solely by population growth, the total global rice consumption gains 0.9% annually as the average world per capita rice use declines slightly (Figure 5 and Table A5.2).

16 | Second ASEAN Rice Trade Forum 2013

Table 1: World Rice Supply and Utilization, 2011–2022

11/12 12/13 13/14 14/15 15/16 16/17 17/18 18/19 19/20 20/21 21/22 22/23

(Thousand Hectares)

Area Harvested 159,173 159,036 160,083 160,188 160,435 160,913 160,848 160,981 161,007 160,976 160,888 160,720

(Tons per Hectare)

Yield 2.93 2.95 2.97 3.00 3.03 3.04 3.06 3.08 3.10 3.12 3.14 3.16

(Thousand Tons)

Production 467,043 469,431 475,486 481,114 485,700 489,882 492,108 495,391 498,816 502,278 505,734 508,407

Beginning Stocks 98,821 106,100 105,798 108,486 112,694 117,169 122,489 126,835 130,941 134,467 138,124 141,160

Domestic Supply 565,863 575,531 581,285 589,599 598,394 607,051 614,597 622,225 629,757 636,745 643,858 649,567

Consumption 458,248 470,038 473,070 477,129 481,434 484,761 487,984 491,526 495,525 498,834 502,922 506,084

Ending Stocks 106,100 105,798 108,486 112,694 117,169 122,489 126,835 130,941 134,467 138,124 141,160 143,695

Domestic Use 564,349 575,837 581,555 589,823 598,603 607,250 614,818 622,467 629,991 636,958 644,082 649,778

Total Trade 39,335 36,496 37,883 39,146 39,893 40,449 40,779 41,189 41,649 42,039 42,872 43,371

(Percent)

Stocks-to-Use Ratio 23.15 22.51 22.93 23.62 24.34 25.27 25.99 26.64 27.14 27.69 28.07 28.39

Source: Wailes and Chavez.

Figure 5: World Rice Area Harvested, Yield, Supply and Utilization

Source: Wailes and Chavez.

4.3 Key Global Policy Assumptions Two recent events have had significant impacts on the dynamics of the global rice market: one is India’s official lifting of its ban on non-basmati rice exports on September 2011, and the other is Thailand’s implementation of its paddy pledging scheme in October 2011. India’s return as a major rice exporter was motivated by the need to reduce excessive rice stocks that accumulated as a result of the export ban and by good weather conditions in 2009 and 2010. The Thai price-floor support policy for Thai farmers guarantees minimum prices for paddy rice that results in a long-grain milled rice price. Since the policy’s initial implementation, the paddy pledging price continues to be 30%–50% higher than trading prices offered by other export competitors such as Viet Nam as well as India and Pakistan. While Thailand’s intervention program is market distorting because producers are paid higher than world market prices, the policy has not adversely affected international rice trade as much as initially anticipated. This is because of abundant exportable rice stocks and increased price competition from the other major rice-exporting countries—India, Pakistan, Viet Nam, and

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 17

increasingly, Cambodia and Myanmar. Consequently, Thailand’s rice export volumes in 2011 declined dramatically by 44% while rice export supplies from the other major exporters dominated international trade (Figure 3). Thailand’s share of global net rice exports declined to 19% in 2011 compared to a historical average of 34% during the 5-year period of 2006–2010 (Wailes and Chavez 2013b). 4.4 Global Rice Trade While criticism and opposition to the Thai pledging scheme abound, the government of Thailand has reauthorized the extension of the program for marketing years 2012–2013 and 2013–2014. As expected, with Thailand’s mounting rice stocks, burdensome costs of storage, and limited export shipments because of non-competitive high prices, Thailand recently announced a plan to release a portion of its stocks from previous seasons to the international market at a loss (The New York Times 2013). The baseline assumes a continuation of this policy and the willingness of the Thai government to export at a loss. As depicted in Figure 6, the baseline projects a return to a larger export share for Thailand and to a consequent increase in the global share of ASEAN net rice exports from 47% in 2011–2012 to 55% by 2021–2022 (Table A2.2 and Table A5.1).

Figure 6: Regional Shares of World Net Rice Trade, 2011–2022

Source: Wailes and Chavez.

The bulk of the world net rice imports are shipped to countries in Africa, ASEAN, and other Asian regions (Table A5.1). Figure 6 also shows the projected shifts in regional rice import shares. The projections suggest that ASEAN net rice import shares will increase slightly from 15% in 2011–2012 to 17% by 2021–2022 as efforts to attain self-sufficiency are offset by population growth in Indonesia, Malaysia, and the Philippines (Table A2.5). The dominant rice-importing region, Africa, will maintain an import share of 40% over the projection period. Significant growth is projected for other Asian regions (Bangladesh, the PRC, and the Middle Eastern countries), increasing from 27% in 2011–2012 to 32% by 2021–2022. Accessing other markets in Africa and Asia will thus provide a growth opportunity for ASEAN rice-exporting countries. 4.5 Key Non-ASEAN Rice Countries There is no doubt that the resumption of India’s long-grain rice exports, which began in September 2011, has had substantial effects on international rice trade and prices. To a large extent, it has neutralized the potential upward price impact of Thailand’s paddy pledging scheme. As a result, global rice prices have remained stable at relatively lower levels—benefiting consumers especially in food-deficit countries. A relatively recent development in global trade is the emergence of the

18 | Second ASEAN Rice Trade Forum 2013

PRC as a major rice importer, which has been taking advantage of attractive lower rice prices over the last couple of years. Hence, a baseline outlook for other key Asian countries is useful. 4.6 People’s Republic of China

Economy Since the PRC has restructured its economy from a closed, centrally-planned system to greater market orientation in the late 1970s, the efficiency gains have caused its GDP to expand over tenfold since 1978. The country became the world’s largest merchandise exporter in 2010. The economy grew by 7.8% in 2012, albeit lower than the 9.3% growth registered in 2011 and 10.4% in 2010. The economy is projected to have robust growth over the next decade, although at a pace slightly lower than in previous years. The economy is composed of 10.1% agriculture, 45.3% industry, and 44.6% services. The PRC is the world’s most populous country, with a population of 1,349,600, which is only growing at 0.48% per year; 79% of the population is under 55 years. Per capita income is $9,100. The country has a massive labor force of 795.4 million, with 34.8% in agriculture, 29.5% in industry, and 35.7% in services. The local currency, the renminbi (RMB) or yuan (CNY), had an exchange rate of CNY6.31 in 2012 and is projected to appreciate relative to the US dollar over the baseline.

Rice Supply and Demand The PRC harvested 30.06 million hectares of rice and produced 140.7 million tons of milled rice in 2011 at an average yield of 4.68 tons per hectare. Yields are expected to grow at 0.66% annually. Total milled rice production declines at 0.17% per year, as a 0.82% annual contraction in area exceeds gains in average yield. The total rice area is projected to contract by 2.6 million hectares over the next decade as the country’s agricultural economy diversifies. Total rice consumption is estimated to decline by 0.17% per year, as the population growth of 0.36% per year is not enough to compensate for the annual decline in per capita use of 0.53%. The country was a net rice exporter of about 633,000 tons per year during 2005–2009. But in reaction to lower international rice prices, it became a significant net rice importer in 2011 (with 1.79 million tons of rice imports and 0.44 million tons of rice exports) and in 2012 (with 2.42 million tons of rice imports and 0.50 million tons of rice exports). Over the baseline, the country is projected to remain a net rice importer by an average of 1.0 million tons. The PRC maintains a relatively high stocks-to-use ratio of 0.32 to 0.50, which augurs well for its food security (Table A4.1). 4.7 Japan

Economy Government stimulus spending helped the economy recover in late 2009 and 2010 from the recession in 2008. However, the economy contracted again in 2011 as the massive 9.0 magnitude earthquake and subsequent tsunami hit Japan’s northeast Pacific coastal region on 11 March 2011, disrupting the manufacturing sector. The USDA reported that the disaster took the lives of over 24,000 people, and damaged about 23,600 hectares of arable land. Estimates of physical and infrastructural damages to the agriculture, fishery, and forestry sectors have reached $30 billion. According to the USDA, “During this unprecedented crisis, Japan’s food supply system demonstrated remarkable resilience and strength in its ability to secure ample, undisrupted supplies of food for people in the affected regions and feed for livestock animals—attesting to the robustness of Japan’s food security system, which relies on both domestic production and the availability of

ASEAN and Global Rice Situation and Outlook, 2011–2022 | 19

reliable imports” (USDA FAS 2012). Japan’s real GDP contracted by 0.8% in 2011 from a growth of 4.5% in 2010, and is estimated to be relatively flat at 0.2% in 2012. By sector, the economy is composed of 1.2% agriculture, 27.5% industry, and 71.4% services. The country’s population is 127.25 million, which is declining at 0.08% per year; 61% is under 55 years old. Per capita income stands at $36,200. The labor force is 65.02 million, 3.9% of which is in agriculture, 26.2% in industry, and 69.8% in services. The local currency, the yen (JPY or ¥), had an exchange rate of ¥79.42 in 2012 and is projected to appreciate relative to the US dollar over the next decade.

Rice Supply and Demand The country harvested 1.58 million hectares of rice in 2011, producing 7.65 million tons of milled rice at an average yield of 4.85 tons per hectare. The model assumes the country to be an entirely medium-grain rice market. Total rice production is estimated to decline by 0.94% annually, as the area harvested contracts by 0.89% and the yield declines marginally. Total rice consumption declines by 0.76% per year due to the combined effects of contraction in both the population level (0.20%) and per capita use (0.56%). Bread consumption has taken dietary share from rice as a main source of carbohydrates as Japanese tastes have increasingly shifted to more Western diets. As a result of the sharp rise in US corn prices since the summer of 2012, the ratio of corn used in compound feeds in the country decreased in favor of nonconventional grains such as rice, wheat, and sorghum (USDA FAS 2012b). The country’s net rice imports remain generally stable at the WTO minimum access level of 482,000 tons over the projection period (Table A4.2). 4.8 Republic of Korea

Economy High-tech and industrialized, the economy of the Republic of Korea is the 12th largest in the world.The country has adopted a number of economic policies and reforms, including the promotion of importation of raw materials and technology at the expense of consumer goods; the encouragement of savings and investments over consumption; and greater openness to foreign investments and imports. However, real GDP growth slowed from 6.3% in 2010 to 3.6% in 2011, and was estimated to further weaken to 2.0% in 2012, as the country relies heavily on exports that have contracted in recent years due to the financial crisis. By sector, the economy is composed of 2.7% agriculture, 39.8% industry, and 57.5% services. The population is 48.95 million and growing at 0.2% per year; 76% is under 55 years old. Per capita income is $32,400. Out of the labor force of 25.5 million, 6.2% is in agriculture, 23.8% in industry, and 70.0 % in services. The local currency, the won (KRW or W) has an exchange rate of W1,127 and is projected to appreciate relative to the US dollar over the baseline period.

Rice Supply and Demand The country harvested 854,000 hectares of rice in 2011, producing 4.22 million tons of milled rice at an average yield of 4.95 tons per hectare. As in the case of Japan, the Republic of Korea’s rice market is assumed to be all medium grain. Total rice production is projected to decline at 0.24% annually, as the yield growth of 0.47% is not enough to compensate for an annual decline of 0.71% in area harvested. The government is reportedly encouraging rice farmers to plant other crops due to bumper rice crops in recent years. Total rice consumption is calculated to decline by 1.03% per

20 | Second ASEAN Rice Trade Forum 2013

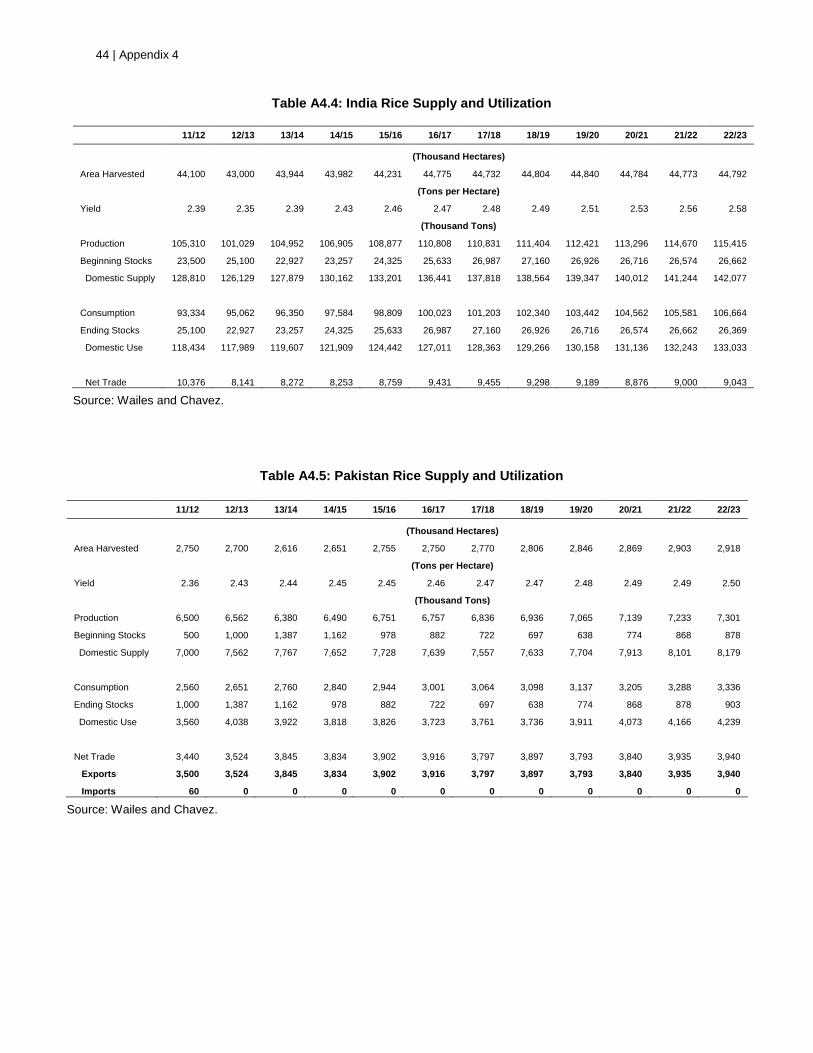

year, from 4.98 million tons in 2011 to 4.44 million tons in 2022, as the slight population growth of 0.12% partially offsets the decline in per capita consumption of 1.15% per year. The country’s annual rice imports are generally stable based on the preset WTO minimum access level (Table A4.3). 4.9 India