asia-pacific development bank

TRANSCRIPT

ASIA-PACIFIC DEVELOPMENT BANK

Annual Report

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

CONTENTS Pages

CEO Statement ..................................................................................................................... 1

Corporate Information ........................................................................................................... 2

Vision, Mission and Core Value ............................................................................................ 3

Organization Chart ............................................................................................................... 4

Management Team .......................................................................................................... 5 - 8

Audited Financial Statements in accordance with Cambodian International Financial Reporting Standards

Report of The Board Of Directors .................................................................................. 9 - 12 Independent Auditor’s Report ...................................................................................... 13 - 15 Statement of Financial Position .......................................................................................... 16 Statement of Profit Or Loss And Other Comprehensive Income ........................................ 17 Statement of Changes In Equity .................................................................................. 18 - 19 Statement of Cash Flows .................................................................................................... 20 Notes to the financial statements ................................................................................ 21 – 70

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

1

CEO STATEMENT

Global economy 2019 has virtually ground to a halt, recording its slowest growth since the Financial Crisis a decade ago. While economic outlook becoming uncertain and unpredictable, businesses and investments take cautious measures to sustain themselves and maintain their pace in this unprecedented situation. Thanks to stable political environment and social stability in Cambodia leading a sustainable economic growth of 7%, these have assured investors to continue their investment agenda and to reinvent new opportunities. To facilitate these investments, the banking sector in Cambodia continues play a crucial role through the mobilization and allocation of financial resources to fuel and support our economy.

Over the past years we have strived enormously to achieve a momentous milestone by successfully upgrading ourselves to commercial bank. Our total assets have jumped significantly from USD24million in 2018 to USD80.47million this year. Meanwhile, our gross loans increased more than 3 folds from USD21.49million to USD70.80million. Together with these growths, the Bank has enforced stringent assets management; hence, there is no non-performing loan for 4 consecutive years. As of May 2020, despite global economic recession due to Covid-19 and uncertainties pertaining withdrawal of EBA (Everything But Arms) from Cambodia, our assets quality remains sound and healthy. Moving forward, while constantly securing strong financial and operational foundation, APD Bank is equipping ourselves to embark greater journey of commercial bank.

We aim to be at the forefront in introducing cutting-edge digital banking technology and solutions to Cambodia. Focusing on technological innovation for financial services, APD Bank will vigorously develop mobile banking in the future, prioritizing on mobile account opening, remittance, payment and other innovative services, and implementing new technological financial experience to our remote customers. We also provide Internet and online banking services for local and international customers convenience.

We aim to achieve our goal of "being in Cambodia and serving the whole Asia-Pacific" by providing comprehensive cross-border financial services to the entire Asia-Pacific region including China, Hong Kong, Taiwan, Singapore, Thailand, Malaysia, etc.

We will continue to prioritize full compliance and to build a strong governance and robust risk management culture. APD Bank places the highest priority in making sure all requirements are met and all internal policies and processes are adhered to at all times. We will keep ourselves abreast to the latest development of the regulatory requirements and regulations.

To all my beloved colleagues, I would like to express my sincere thanks and recognition for all your hard-work, commitments and initiatives to betterment of APD Bank. I firmly believe 2020 comes with another exciting chapter for our commercial banking journey, a remarkable journey to be filled with challenges, opportunities, excitements and growth.

Finally, we would like to express our gratitude to our shareholders and Board of Directors for their attentive guidance in positioning APD Bank. We also thank our customers for their trust and cooperation. Last but not least, our utmost appreciation goes to the National Bank of Cambodia and other regulatory authorities for their ongoing guidance and supports. Hsiao Charng Geng, Chief Executive Officer Phnom Penh, 8 June 2020

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

2

CORPORATE INFORMATION

Bank Asia-Pacific Development Bank Plc. Registration No 00007514 Registered office Lot No.132, Street no. 294 (Corner Norodom Blvd) Sangkat Tonle Bassac, Khan Chamkarmorn Phnom Penh, Kingdom of Cambodia Shareholders Mr. Vong Pech Mr. Lau Yao Zhong Board of Directors Mr. Vong Pech Chairman Mr. Lau Yao Zhong Vice Chairman Mr. Zhao Wen Qing Director Mr. Lonh Hay Director Mr. Yu Yongshun Director Management team Mr. Hsiao Charng Geng Chief Executive Officer Ms. Chen Ya-Duan Deputy CEO Mr. Svay Pisal Head of Risk Management Ms. Saing Manita Head of Compliance Mr. Thol Lyna Head of Internal Audit Mr. Chheu Tech Head of Finance and Accounting Ms. Thai Sreymom Head of Admin and HR and Secretariat Auditors Ernst & Young (Cambodia) Ltd

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

3

VISION, MISSION AND CORE VALUE

Vision

APD Bank’s vision is to be one of the leading financial institutions offering quality service to fulfill dreams across generations, beyond borders.

Mission

APD Bank is committed to delivering a whole range of international quality financial services that will create value and enrich the lives of our customers, employees, shareholders and the communities we serve.

Core Value

Accountability : We are active and accountable in our customers’, employees’ and shareholders’ best interests.

Passion : We put our soul into our work and stamp it with our own personality to accomplish our customer’s objective. Enthusiasm is very important for our achievement.

Diligence : We understand what a priority is, and we are committed to doing the best of our ability by whatever means necessary.

Best : We strive to get better, smarter and more innovative and be the best in everything we do.

Acumen : We master market trends and use our operational knowledge and strategic thinking to provide high quality service to our customers.

Network : We achieve our goals and objectives by collaborating and working together. We will also use the resources from our Group efficiently and effectively with full cooperation and effective communication to yield greater results.

Knowledge : We believe in knowledge orientation, specialized employees, up-to-date technology, creativity, and innovation in our activities.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

4

ORGANIZATIONAL CHART

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

5

MANAGEMENT TEAM

MR. HSIAO CHARNG GENG AKA JOE HSIAO

CHIEF EXECUTIVE OFFICER

Mr. Joe Hsiao has more than 35 years of banking experience in various banks across Taiwan, China and Southeast Asia. In 2015, he was appointed as CEO to establish APD Specialized Bank and subsequently upgraded the Bank to full-fledged Commercial Bank in 2019.

Prior to joining APD Bank, Mr. Joe worked for Fubong Commercial Bank, Mega International Commercial Bank and Taiwan Shin Kong Commercial Bank. In addition to working in Taiwan, he was dispatched to work in Manila (Philippines), Ningbo, Dongguan, Shenzhen and Hong Kong for almost 20 years. His main fields of expertise include operations, business promotion and marketing, loans/credit, foreign exchange, trade finance, securities, trust, overseas branch operation and management.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

6

MS. CHEN YA-DUAN (ELAINE) DEPUTY CEO

Ms. Chen Ya-Duan has more than 30 years banking experience in Information Technology and Business Administration with various banks. She joined APD Bank in 2019 as deputy CEO specializing in digitalization transformation.

Prior to joining APD Bank, she was Professor of FinTech in Soochow University, Taiwan. She was also our consultant during the establishment of IT infrastructure for APD Specialized Bank in 2016. Before this, she worked for CitiBank Taiwan, Mega International Commercial Bank, ANZ Taiwan, DBS Taiwan and Taiwan Shin Kong Commercial Bank.

Ms. Chen Ya-Duan holds Master of Computer Science from Florida Institute of Technology (FIT), USA and Bachelor of Business Administration from National Taiwan University (NTU).

MR. SVAY PISAL HEAD OF RISK MANAGEMENT

Mr. Pisal is currently the Head of Risk Management responsible for overall risk managements of the Bank. He is one of core management team joining APD Bank since the first day of operations in June 2016 as Operation Manager.

Along the way of banking career, Mr. Pisal has come across with varieties of roles and responsibilities from very junior to managerial levels including Customer Services, Sales and Marketing, Operations, Loans/Credits and Branch Management. He started his first Banking job in 2005 as a junior staff in Card Business Department with a local Bank. In late 2005, he moved to a leading Malaysian-owned Bank as an Authorizer of Card Centre in Head Office and subsequently be promoted as Branch Manager in 2009. He remained with the same Bank until end of 2014 with his last role as Branch Manager before moving to another Malaysian-owned Bank in 2015 in the position of Branch Manager of Head Office Branch.

Mr. Pisal holds a Master of Finance from National University of Management (NUM), Phnom Penh. He graduated Bachelor’s degree of Management from the same university in 2004.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

7

MS. SAING MANITA

HEAD OF COMPLIANCE

Ms. Saing Manita, Head of Compliance, is responsible for overall management of the Bank’s Compliance function and works as the principal liaison with the NBC and other regulators. She joined APD Bank in 2017 and subsequently obtained official approval from the National Bank of Cambodia (NBC) as Head of Compliance.

Ms. Nita has accumulated 6 years of working experience in banking, starting her first job in 2014 specializing in risk and compliance at a local MDI. During her career path, she has attended various workshops and seminars in banking and finance industry. Moreover, she has obtained Certificate of Regulatory Compliance from Institute of Banking and Finance (IBF), Cambodia.

Ms. Nita is currently pursuing Master of Risk Management in Insurance, Banking and Finance at Royal University of Law and Economics (RULE). She holds double bachelor degrees in Accounting from National University of Management (NUM) and English Education from Institute of Foreign Languages (IFL).

MR. THOL LYNA

HEAD OF INTERNAL AUDIT

Mr. Thol Lyna, Head of Internal Audit, is responsible for overall management of the Bank’s audit and internal control functions. He joined APD Bank in 2019 and obtained official approval from the National Bank of Cambodia (NBC) as Head of Internal Audit in the same year.

Mr. Lyna has more than 10 years of working experience. He experienced with a “big four” international accounting and audit firm and promoted to Senior Auditor prior to moving to his banking journey with one of the leading banks as Assistant Finance Manager and subsequently upgraded to Head of Taxation. In 2018, he moved to a local MDI to pursue his audit career as Internal Audit Manager. With his diverse background in finance, audit and banking, he is able to bring innovation and carry out any task required for his position.

Mr. Lyna is pursuing a UK-based ACCA Program at CamEd Business School. He holds bachelor degree in Business Administration majoring in Finance and Banking from the National University of Management (NUM). In addition, he was a four-year scholarship awardee from a France Organization majoring in Management.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

8

MR. CHHEU TECH

HEAD OF FINANCE AND

ACCOUNTING

Mr. Tech, Head of Finance and Accounting, is responsible for planning, executing, managing all finance and accounting activities of the Bank. He is one of core management team joining APD Bank since 2017 as Head of Internal Audit.

Prior to his current position, Mr. Tech worked for one of the “big four” international audit firms for 3 years with his last position as Senior Auditor. During his service, he has performed audit in various industries such as banks, MFIs, insurance, manufacturing, companies and NGOs.

Mr. Tech is an Affiliate of the UK-based Association of Chartered Certified Accountants (ACCA). He also holds Bachelor of Finance and Banking from Royal University of Law and Economics (RULE) and Bachelor of Education from Institute of Foreign Languages (IFL).

MS. THAI SREYMOM

HEAD OF ADMIN AND HR &

SECRETARIAT

Ms. Thai Sreymom, Head of Admin and Human Resource & Secretariat, is responsible for managing the administrative tasks as well as HR strategies involving talent acquisition, staff consultation, capacity building and resource development. She joined APD Bank in March 2020.

Ms. Sreymom has 11 years of banking experience with a number of local, Malaysian-owned and Taiwanese-owned banks. She started her banking career in 2009 and exposed herself to many fields such as finance, accounting, budgeting, administration, procurement, human resources and management. Prior to joining APD Bank, she was one of the core management team members in setting up a newly-incorporated local bank.

Ms. Sreymom holds Bachelor Degree in Accounting and Finance from Vanda Institute of Accounting. She also attended various courses and trainings on taxation, human resource management and leadership skills.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.)

9

AUDITED FINANCIAL STATEMENTS

REPORT OF THE BOARD OF DIRECTORS The Board of Directors of Asia-Pacific Development Bank Plc. (“the Bank”) presents its report and the Bank’s financial statements as at 31 December 2019 and for the year then ended. THE BANK The Bank was incorporated in the Kingdom of Cambodia and registered with the Ministry of Commerce as a public limited company under registration number 00007514 dated 5 April 2016. The Bank obtained its specialized banking license from the National Bank of Cambodia (“NBC”) on 16 June 2016 to operate as a specialized bank with a permanent validity and officially commenced its operations on 11 July 2016. On 26 June 2019, the Bank obtained a commercial bank license from the NBC and changed its name from Asia-Pacific Development Specialized Bank Plc to Asia-Pacific Development Bank Plc. The amendments of the Bank’s legal documents submitted to relevant authorities following the change of the Bank’s status were fully completed on 13 February 2020. The Bank is principally engaged in commercial banking business and provision of related financial services in the Kingdom of Cambodia. The Bank’s registered office address is located at No. 132, Street no. 294 (Corner Norodom Blvd), Sangkat Tonle Bassac, Khan Chamkarmorn, Phnom Penh, Kingdom of Cambodia. FINANCIAL RESULTS The financial performance of the Bank is set out in the statement of profit or loss and other comprehensive income. DIVIDENDS No dividend was declared or paid and the Board of Directors do not recommend any dividend to be paid for the year (2018: nil). SHARE CAPITAL The paid-up capital of the Bank as at 31 December 2019 was US$77.49 million or KHR 309.96 billion (2018: US$15 million or KHR60.00 billion). WRITTEN OFF OF AND ALLOWANCE FOR FINANCIAL ASSETS Before the financial statements were prepared, the Board of Directors took reasonable steps to ascertain that action had been taken in relation to the writing off of financial assets that have no reasonable expectations of recovering the contractual cash flows in their entirety or a portion thereof and making of allowance for expected credit losses on financial assets, and satisfied themselves that there all known financial assets that have no reasonable expectations of recovering the contractual cash flows were written off and that adequate allowance for expected credit losses on financial assets have been made. At the date of this report and on the best of knowledge, the Board of Directors is not aware of any circumstances which would render the amount of the allowance for expected credit losses on financial assets in the financial statements of the Bank inadequate to any material extent.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) REPORT OF THE BOARD OF DIRECTORS (continued)

10

ASSETS Before the financial statements of the Bank were prepared, the Board of Directors ascertained that management took reasonable steps to ensure that any current assets, which were unlikely to be realised in the ordinary course of business at their values as shown in the accounting records of the Bank had been written down to amounts which they might be expected to realise. VALUATION METHODS At the date of this report, the Board of Directors is not aware of any circumstances that have arisen which render adherence to the existing method of valuation of assets and liabilities in the financial statements of the Bank misleading or inappropriate. CONTINGENT AND OTHER LIABILITIES At the date of this report, there does not exist:

(a) any charge on the assets of the Bank which has arisen since the end of the financial year which secures the liabilities of any other person; and

(b) any contingent liability in respect of the Bank that has arisen since the end of the financial year other than in the ordinary course of its business operations.

No contingent or other liability of the Bank has become enforceable, or is likely to become enforceable within the period of 12 months after the end of the financial year which, in the opinion of the Board of Directors, will or may have a material effect on the ability of the Bank to meet its obligations as and when they fall due. CHANGE OF CIRCUMSTANCES At the date of this report, the Board of Directors is not aware of any circumstances, not otherwise dealt with in this report or the financial statements of the Bank, which would render any amount stated in the financial statements misleading. ITEMS OF AN UNUSUAL NATURE The results of the operations of the Bank for the year were not, in the opinion of the Board of Directors, substantially affected by any item, transaction or event of a material and unusual nature. There has not arisen in the interval between the end of the financial year and the date of this report any item, transaction or event of a material and unusual nature likely, in the opinion of the Board of Directors, which affect substantially the financial performance of the Bank for the current financial year in which this report is made. EVENTS AFTER THE REPORTING DATE At the date of this report, to the best knowledge of the Board of Directors, there have been no significant events occurring after reporting date which would require adjustments or disclosures to be made in the financial statements.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) REPORT OF THE BOARD OF DIRECTORS (continued)

11

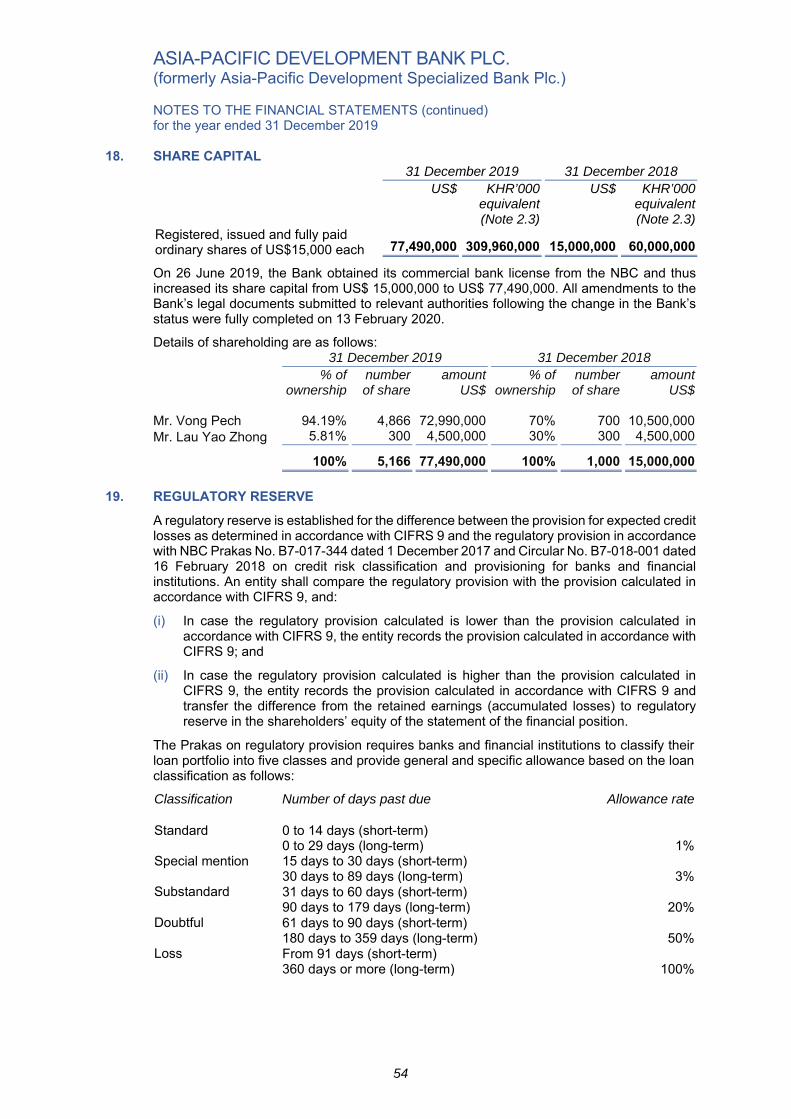

THE BOARD OF DIRECTORS The members of the Board of Directors holding office during the year and at the date of this report are: Name Position Mr. Vong Pech ChairmanMr. Lau Yao Zhong Vice-ChairmanMr. Zhao Wenqing DirectorMr. Lonh Hay DirectorMr. Yu Yongshun Director (appointed on 27 June 2019) DIRECTORS’ INTERESTS The directors who held office at the end of the financial year and their interests in the shares of the Bank are as follows:

31 December 2019 31 December 2018

% of

ownership Number

of sharesAmount

US$% of

ownershipNumber

of shares Amount

US$ Mr. Vong Pech 94.19% 4,866 72,990,000 70% 700 10,500,000Mr. Lau Yao Zhong 5.81% 300 4,500,000 30% 300 4,500,000

100% 5,166 77,490,000 100% 1,000 15,000,000 Other than the directors disclosed above, the other directors did not have any interest in the ordinary shares of the Bank during the financial year. DIRECTORS’ BENEFITS During and at the end of the year, no arrangement existed to which the Bank was a party with the objective of enabling the directors of the Bank to acquire benefits by means of the acquisition of shares in or debentures of the Bank or any other body corporate. During the financial year, no director of the Bank has received or become entitled to receive any benefit (other than a benefit include in the aggregate amount of emoluments receivable by the directors as disclosed in the financial statements) by reason of a contract made by the Bank or a related corporation with a firm of which the director is a member, or with a company in which the director has substantial financial interest other than as disclosed in the financial statements. RESPONSIBILITIES OF THE BOARD OF DIRECTORS IN RESPECT OF THE FINANCIAL STATEMENTS The Board of Directors is responsible for ascertaining that the financial statements present fairly, in all material respects, the financial position of the Bank as at 31 December 2019, and its financial performance and its cash flows for the year then ended. In preparing these financial statements, the Board of Directors ensures that:

adopts appropriate accounting policies which are supported by reasonable and prudent judgments and estimates and then apply them consistently;

comply with the disclosure requirements of Cambodian International Financial Reporting Standards (“CIFRSs”), or if there have been any departures in the interest of fair true and fair presentation, ensure that these have been appropriately disclosed, explained and quantified in the financial statement;

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) REPORT OF THE BOARD OF DIRECTORS (continued)

12

RESPONSIBILITIES OF THE BOARD OF DIRECTORS IN RESPECT OF THE FINANCIAL STATEMENTS (continued)

oversee the Bank’s financial reporting process and maintains adequate accounting records and an effective system of internal controls;

assess the Bank’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Bank or to cease operations, or has no realistic alternative but to do so; and

effectively control and direct effectively the Bank in all material decisions affecting the operations and performance and ascertain that such have been properly reflected in the financial statements.

The Board of Directors confirms that they have fulfilled and complied with the above responsibilities in preparing the financial statements. APPROVAL OF THE FINANCIAL STATEMENTS We hereby approve the accompanying financial statements which give a true and fair view of the financial position of the Bank as at 31 December 2019, and its financial performance and its cash flows for the year then ended in accordance with Cambodian International Financial Reporting Standards. On behalf of the Board of Directors:

Vong Pech Chairman Phnom Penh, Kingdom of Cambodia 26 March 2020

13

Reference: 61552160/21288598

INDEPENDENT AUDITOR’S REPORT To: The Shareholders of Asia-Pacific Development Bank Plc. Opinion We have audited the accompanying financial statements of Asia-Pacific Development Bank Plc. (“the Bank”) which comprise the statement of financial position as at 31 December 2019, and the statement of profit or loss and other comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies. In our opinion, the financial statements give a true and fair view of the financial position of the Bank as at 31 December 2019, and its financial performance and its cash flows for the year then ended in accordance with Cambodian International Financial Reporting Standards (“CIFRSs”). Basis for Opinion We conducted our audit in accordance with Cambodian International Standards on Auditing (“CISAs”). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Bank in accordance with the sub-decree on the Code of Ethics for Professional Accountants and Auditors promulgated by the Royal Government of Cambodia, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Other Matter The financial statements of the Bank as at and for the year ended 31 December 2018 were audited by another auditor who expressed an unmodified opinion on those financial statements on 26 March 2019. Information Other than the Financial Statements and Auditor’s Report Thereon The other information obtained at the date of the auditor’s report comprises the Report of the Board of Directors as set out in pages 1 to 4. Management is responsible for the other information. Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon. In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

14

Responsibilities of Management and Those Charged with Governance for the Financial Statements Management is responsible for the preparation of financial statements that give a true and fair view in accordance with CIFRSs, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. In preparing the financial statements, management is responsible for assessing the Bank’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Bank or to cease operations, or has no realistic alternative but to do so. Those charged with governance are responsible for overseeing the Bank’s financial reporting process. Auditor’s Responsibilities for the Audit of the Financial Statements Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor’s report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with CISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements. As part of an audit in accordance with CISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Bank’s internal control.

Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Bank’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor’s report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’s report. However, future events or conditions may cause the Bank to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

15

Auditor’s Responsibilities for the Audit of the Financial Statements (continued) We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Ernst & Young (Cambodia) Ltd. Certified Public Accountants Registered Auditors Phnom Penh, Kingdom of Cambodia 26 March 2020

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) STATEMENT OF FINANCIAL POSITION as at 31 December 2019

16

Notes 31 December 2019 31 December 2018 1 January 2018

US$ KHR’000

equivalent US$ KHR’000

equivalent US$ KHR’000

equivalent (Note 2.3) (Note 2.3) (Note 2.3) (As restated - Note 3) (As restated - Note 3) ASSETS Cash on hand 6 18,701 76,207 343,507 1,380,211 2,000 8,074 Balance with National Bank of Cambodia 7 122,502 499,196 100,517 403,877 96,462 389,417 Balances with other banks 8 1,060,822 4,322,850 283,967 1,140,979 500,948 2,022,327 Loans and advances to customers 9 70,358,681 286,711,625 21,282,410 85,512,723 21,080,223 85,100,860 Statutory deposit 10 7,750,000 31,581,250 750,000 3,013,500 750,000 3,027,750 Other assets 11 22,145 90,240 27,335 109,832 28,075 113,340 Software 12 357,808 1,458,068 230,148 924,735 306,716 1,238,212 Property and equipment 13 456,162 1,858,860 677,993 2,724,176 929,564 3,752,650 Right-of-use asset 14 214,338 873,427 313,264 1,258,695 412,190 1,664,011 Deferred tax assets 15 (iii) 114,000 464,550 - - - -

TOTAL ASSETS 80,475,159 327,936,273 24,009,141 96,468,728 24,106,178 97,316,641

LIABILITIES AND SHAREHOLDERS’ EQUITY LIABILITIES Current income tax liability 15 (i) 582,067 2,371,923 47,705 191,679 2,284 9,221 Other liabilities 16 194,324 791,871 590,470 2,372,508 170,699 689,112 Lease liability 14 246,952 1,006,329 352,231 1,415,264 452,386 1,826,282 Borrowing 17 - - 8,300,000 33,349,400 8,800,000 35,525,600

TOTAL LIABILITIES 1,023,343 4,170,123 9,290,406 37,328,851 9,425,369 38,050,215 SHAREHOLDERS’ EQUITY Share capital 18 77,490,000 309,960,000 15,000,000 60,000,000 15,000,000 60,000,000 Retained earnings (accumulated losses) 1,259,662 5,100,919 (503,115) (2,030,808) (542,921) (2,191,772) Regulatory reserve 19 702,154 2,852,883 221,850 895,644 223,730 903,198 Cumulative exchange differences on translation - 5,852,348 - 275,041 - 555,000

TOTAL SHAREHOLDERS’ EQUITY 79,451,816 323,766,150 14,718,735 59,139,877 14,680,809 59,266,426 TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY 80,475,159 327,936,273 24,009,141 96,468,728 24,106,178 97,316,641

The accompanying notes from 1 to 29 form an integral part of these financial statements.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME for the year ended 31 December 2019

17

Notes For the year ended 31 December 2019

For the year ended 31 December 2018

US$ KHR’000

equivalent US$

KHR’000

equivalent (Note 2.3) (Note 2.3) (As restated - Note 3) Operating income

Interest income 20 4,437,820 17,982,047 2,051,369 8,297,788 Interest expense 20 (120,777) (489,388) (488,886) (1,977,544)

Net interest income 4,317,043 17,492,659 1,562,483 6,320,244

Other operating income 21 51,414 208,330 9,652 39,042 Personnel expenses 22 (825,459) (3,344,760) (764,406) (3,092,022)Depreciation and amortisation 12,13,14 (451,583) (1,829,814) (442,968) (1,791,806)Other operating expenses 23 (315,379) (1,277,916) (264,462) (1,069,749)(Provision for) reversal of

provision for expected credit losses 24 (25,429) (103,038) 2,387 9,655

Profit before income tax 2,750,607 11,145,461 102,686 415,364

Income tax expense 15 (507,526) (2,056,495) (64,760) (261,954)

Net profit 2,243,081 9,088,966 37,926 153,410

Other comprehensive income item: Exchange difference on translation - 5,577,307 - (279,959)

Total comprehensive income for the year 2,243,081 14,666,273 37,926 (126,549)

The accompanying notes from 1 to 29 form an integral part of these financial statements.

ASIA-PACIFIC DEVELOPMENT BANK PLC.(formerly Asia-Pacific Development Specialized Bank Plc.)

STATEMENT OF CHANGES IN EQUITY for the year ended 31 December 2019

18

Share capital Retained earnings Regulatory reserve

Cumulative exchange

differenceson translation Total

US$ KHR’000equivalent

US$ KHR’000equivalent

US$ KHR’000equivalent

KHR’000equivalent

US$ KHR’000 equivalent

(Note 2.3) (Note 2.3) (Note 2.3) (Note 2.3) (Note 2.3)

As at 1 January 2019 (as restated - Note 3) 15,000,000 60,000,000 (503,115) (2,030,808) 221,850 895,644 275,041 14,718,735 59,139,877

Additional share capital 62,490,000 249,960,000 - - - - - 62,490,000 249,960,000 Net profit for the year - - 2,243,081 9,088,966 - - - 2,243,081 9,088,966 Transfer to regulatory reserve - - (480,304) (1,957,239) 480,304 1,957,239 - - - Exchange difference on

translation - - - - - 5,577,307 - 5,577,307

As at 31 December 2019 77,490,000 309,960,000 1,259,662 5,100,919 702,154 2,852,883 5,852,348 79,451,816 323,766,150

The accompanying notes from 1 to 29 form an integral part of these financial statements.

-

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) STATEMENT OF CHANGES IN EQUITY (continued) for the year ended 31 December 2019

19

Share capital Accumulated losses Regulatory reserve

Cumulative exchange

differenceson translation Total

US$ KHR’000

equivalent US$ KHR’000

equivalent US$ KHR’000

equivalent KHR’000

equivalent US$ KHR’000

equivalent (Note 2.3) (Note 2.3) (Note 2.3) (Note 2.3) (Note 2.3) As at 1 January 2018

(as previously reported) 15,000,000 60,000,000 (267,023) (1,077,972) - - 555,000 14,732,977 59,477,028 Effect of transition to CIFRSs

(Note 3) - - (52,168) (210,602) - - - (52,168) (210,602) Transfer to regulatory reserve - - (223,730) (903,198) 223,730 903,198 - - -

As at 1 January 2018 (as restated - Note 3) 15,000,000 60,000,000 (542,921) (2,191,772) 223,730 903,198 555,000 14,680,809 59,266,426

Net profit for the year (as restated - Note 3) - - 37,926 153,410 - - - 37,926 153,410

Transfer to regulatory reserve - - 1,880 7,554 (1,880) (7,554) - - - Exchange difference on

translation - - - - - - (279,959) - (279,959)

As at 31 December 2018 (as restated - Note 3) 15,000,000 60,000,000 (503,115) (2,030,808) 221,850 895,644 275,041 14,718,735 59,139,877

The accompanying notes from 1 to 29 form an integral part of these financial statements.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) STATEMENT OF CASH FLOWS for the year ended 31 December 2019

20

For the year ended 31 December 2019

For the year ended 31 December 2018

US$ KHR’000

equivalent US$

KHR’000

equivalent (Note 2.3) (Note 2.3) (As restated - Note 3) OPERATING ACTIVITIES

Profit before income tax 2,750,607 11,145,461 102,686 415,364 Adjustments for:

Depreciation and amortisation 451,583 1,829,814 442,968 1,791,806 Expected credit losses on:

Loans and advances 7,174 29,069 (2,200) (8,899)Balances with other banks 18,270 74,030 (75) (303)

Loss on disposal of property and equipment 1,564 6,337 2,349 9,502

Provision for employee benefits (22,118) (89,622) 54,020 218,511 Changes in:

Statutory deposit (7,000,000) (28,364,000) - -Loans and advances to customers (49,083,445) (198,886,119) (199,988) (808,951)Other assets 5,190 21,030 740 2,993 Other liabilities (359,307) (1,455,912) 385,597 1,559,740

Cash used in operations (53,230,482) (215,689,912) 786,097 3,179,763 Income tax paid (87,164) (353,189) (19,339) (78,226)

Net cash (used in) generated from operating activities (53,317,646) (216,043,101) 766,758 3,101,537

INVESTING ACTIVITIES Purchase of property and equipment (40,968) (166,002) (8,930) (36,122)Purchase of software (219,082) (887,720) (9,413) (38,076)Proceeds from disposal of property and

equipment - - 91 368

Net cash used in investing activities (260,050) (1,053,722) (18,252) (73,830) FINANCING ACTIVITIES Proceed from additional share capital 62,490,000 253,209,480 - -Lease payments (120,000) (486,240) (120,000) (485,400)Repayment of borrowing (8,300,000) (33,631,600) (5,300,000) (21,438,500)Proceeds from borrowing - - 4,800,000 19,416,000

Net cash generated from (used in) financing activities 54,070,000 219,091,640 (620,000) (2,507,900)

Net increase in cash and cash equivalents 492,304 1,994,817 128,506 519,807

Cash and cash equivalents at the beginning of year 728,193 2,925,879 599,687 2,420,936

Exchange difference on translation - 52,830 - (14,864)

Cash and cash equivalents at the end of year 1,220,497 4,973,526 728,193 2,925,879

The accompanying notes from 1 to 29 form an integral part of these financial statements.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS for the year ended 31 December 2019

21

1. CORPORATE INFORMATION

Asia-Pacific Development Bank Plc (“the Bank”) was incorporated in the Kingdom of Cambodia and registered with the Ministry of Commerce as a public limited company under registration number 00007514 dated 5 April 2016. The Bank obtained its specialized banking license from the National Bank of Cambodia (“NBC”) on 16 June 2016 to operate as a specialized bank with a permanent validity and officially commenced its operations on 11 July 2016. On 26 June 2019, the Bank obtained a commercial bank license from the NBC and changed its name from Asia-Pacific Development Specialized Bank Plc to Asia-Pacific Development Bank Plc. The Bank is principally engaged in commercial banking business and provision of related financial services in the Kingdom of Cambodia. The Bank’s registered office address is located at No. 132, Street no. 294 (Corner Norodom Boulevard), Sangkat Tonle Bassac, Khan Chamkarmorn, Phnom Penh, Kingdom of Cambodia. As at 31 December 2019, the Bank had 30 employees (2018: 21 employees).

2. BASIS OF PREPARATION OF THE FINANCIAL STATEMENTS

The financial statements, expressed in United States dollar (“US$”), have been prepared on a historical cost basis, except otherwise indicated.

2.1. Basis of preparation

This is the first set of financial statements of the Bank prepared in accordance with the Cambodian International Financial Reporting Standards (“CIFRSs”). The Bank’s date of transition to CIFRSs is 1 January 2018. The financial statements for the year ended 31 December 2018 were prepared in accordance with Cambodian Accounting Standards (“CASs”) and relevant regulations and guidelines issued by the NBC, collectively referred to as the previous generally accepted accounting principles (“previous GAAP”). The transition to the CIFRSs has resulted to a number of changes in the Bank’s accounting policies compared to those used when applying previous GAAP. Note 3 to the financial statements describes the differences between the equity and profit or loss presented under previous GAAP and the newly presented amounts under CIFRSs for the reporting year ended at 31 December 2018, as well as the equity presented in the opening statement of financial position as at 1 January 2018. It also describes all the required changes in accounting policies made on first-time adoption of the CIFRSs.

2.2 Fiscal year The Bank’s fiscal year starts on 1 January and ends on 31 December.

2.3 Functional and presentation currency

Presentation currency

The financial statements are presented in US$, which is the Bank’s functional and presentation currency.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

22

2. BASIS OF PREPARATION OF THE FINANCIAL STATEMENTS (continued)

2.3 Functional and presentation currency (continued)

Transactions and balances

Transactions in currencies other than US$ are translated into US$ at the foreign exchange rate ruling at the date of the transaction. Monetary assets and liabilities denominated in currencies other than US$ which are outstanding at the reporting date are translated into US$ at the rate of exchange ruling at that date. Exchange differences arising on translation are recognized in profit or loss. Translation of US$ in KHR

The translation of the US$ amounts into thousands KHR (“KHR’000”) is presented in the financial statements to comply with the Law on Accounting and Audit dated 11 April 2016 using the closing and average rates for the year then ended, as announced by the General Department of Taxation.

Assets and liabilities included in the statement of financial position are translated at the closing rate prevailing at the end of each reporting date, whereas income and expense items presented in the statement of profit or loss and other comprehensive income are translated at the average rate for the year then ended. All resulting exchange differences are recognized in the statement of profit or loss and other comprehensive income. Such translation should not be construed as a representation that the US$ amounts represent, or have been or could be, converted into KHR at that or any other rate. All values in KHR are rounded to the nearest thousand (“KHR’000”), except if otherwise indicated.

The financial statements are presented in KHR based on the applicable exchange rates per US$1 as follows:

2019 2018 2017 Closing rate 4,075 4,018 4,037Average rate 4,052 4,045 4,045

2.4 Rounding of amounts

Except as indicated otherwise, amounts in the financial statements have been rounded off to the nearest dollar for US$ amounts and nearest thousand for KHR amounts.

2.5 Standards issued but not yet effective

The standards and amendments that are issued, but not yet effective, up to the date of issuance of the Bank’s financial statements are disclosed below. These standards and amendments to CIFRSs issued but not yet effective are not expected to have a significant impact on the financial position or performance of the Bank.

CIFRS 17, Insurance

Amendments to CIFRS 3: Definition of Business

Amendments to CIAS 1 and CIAS 8: Definition of Material

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

23

3. RECONCILIATION BETWEEN PREVIOUS GAAP AND NEW PRESENTATION UNDER CIFRSs

As a first-time adopter of CIFRSs, the Bank has applied retrospectively accounting policies based on each CIFRS effective as at end of the first CIFRSs reporting period (31 December 2019), except for areas of exceptions and optional exemptions set out in CIFRS 1. In the table below, equity determined in accordance with CIFRSs is reconciled to equity determined in accordance with the previous GAAP at both 1 January 2018 (the date of transition to the CIFRSs) and 31 December 2018 (the end of the latest period presented in the most recent financial statements prepared in accordance with the previous GAAP). 1 January 2018 31 December 2018 Previous GAAP Reclassification Remeasurement CIFRSs Previous GAAP Reclassification Remeasurement CIFRSs US$ US$ US$ US$ US$ US$ US$ US$ ASSETS Cash on hand 2,000 - - 2,000 343,507 - - 343,507 Balances with the NBC 96,462 - - 96,462 100,517 - - 100,517 Balances with other banks (a) 501,225 - (277) 500,948 281,327 - 2,640 283,967 Loans and advances to customers (a) 21,014,596 77,197 (11,570) 21,080,223 21,196,479 81,137 4,794 21,282,410 Statutory deposit 750,000 - - 750,000 750,000 - - 750,000 Other assets (a) 105,272 (77,197) - 28,075 108,472 (81,137) - 27,335 Intangible assets 306,716 - - 306,716 230,148 - - 230,148 Property and equipment 929,564 - - 929,564 677,993 - - 677,993 Right-of-use asset (b) - - 412,190 412,190 - - 313,264 313,264

TOTAL ASSETS 23,705,835 - 400,343 24,106,178 23,688,443 - 320,698 24,009,141

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

24

3. RECONCILIATION BETWEEN PREVIOUS GAAP AND NEW PRESENTATION UNDER CIFRSs (continued)

1 January 2018 31 December 2018 Previous GAAP Reclassification Remeasurement CIFRSs Previous GAAP Reclassification Remeasurement CIFRSs US$ US$ US$ US$ US$ US$ US$ US$

LIABILITIES AND SHAREHOLDERS’ EQUITY LIABILITIES Current income tax liability 2,284 - - 2,284 47,705 - - 47,705 Other liabilities (a) 170,574 - 125 170,699 590,457 - 13 590,470 Borrowings 8,800,000 - - 8,800,000 8,300,000 - - 8,300,000 Lease liability (a) - - 452,386 452,386 - - 352,231 352,231

TOTAL LIABILITIES 8,972,858 - 452,511 9,425,369 8,938,162 - 352,244 9,290,406 SHAREHOLDERS’ EQUITY Share capital 15,000,000 - 15,000,000 15,000,000 - - 15,000,000 Accumulated losses (267,023) (223,730) (52,168) (542,921) (249,719) (221,850) (31,546) (503,115) Regulatory reserve (e) - 223,730 - 223,730 - 221,850 - 221,850

TOTAL SHAREHOLDERS’ EQUITY 14,732,977 - (52,168) 14,680,809 14,750,281 - (31,546) 14,718,735

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY 23,705,835 - 400,343 24,106,178 23,688,443 - 320,698 24,009,141

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

25

3. RECONCILIATION BETWEEN PREVIOUS GAAP AND NEW PRESENTATION UNDER CIFRSs (continued)

The table below summarises the differences between the profit or loss presented under previous GAAP and the newly-presented amounts under the CIFRSs for the year ended 31 December 2018:

Note Previous GAAP Reclassification Remeasurement CIFRSs US$ US$ US$ US$ Interest income 1,873,064 171,032 7,273 2,051,369 Interest expense (d) (469,041) - (19,845) (488,886)

Net interest income 1,404,023 171,032 (12,572) 1,562,483

Other operating income (c) 180,684 (171,032) - 9,652 (Provision for) reversal of provision

for expected credit losses (a) (9,733) - 12,120 2,387 Personnel expenses (764,406) - - (764,406) Depreciation and amortisation (d) (344,042) - (98,926) (442,968) Other expenses (d) (384,462) - 120,000 (264,462)

Profit before income tax 82,064 - 20,622 102,686

Income tax expense (64,760) - - (64,760)

Profit for the year 17,304 - 20,622 37,926

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

26

3. RECONCILIATION BETWEEN PREVIOUS GAAP AND NEW PRESENTATION UNDER

CIFRSs (continued) Explanatory notes to the reconciliation tables (a) Financial assets and liabilities impacted by the transition to CIFRSs

1 January 2018

Note

Original classification under previous GAAP

New classification under CIFRS 9

Original carrying

amount under previous

GAAP

New carryingamount under

CIFRS 9 US$ US$ Financial assets Balances with other banks (i) Cost Amortised cost 501,225 500,948 Loans and advances to

customers (ii) Carrying amount Amortised cost 21,014,596 21,080,223 Other assets (iii) Carrying amount Amortised cost 105,272 28,075

Financial liabilities Lease liability (iv) Cost Amortised cost - 452,386 Other liabilities (v) Cost Amortised cost 170,574 170,699

(i) As at 1 January 2018, balances with other banks decreased by US$ 277 to recognise

cumulative transition adjustment for expected credit loss (“ECL”) on balances with other banks following the requirement of CIFRS 9.

(ii) Under previous GAAP, the Bank recognised loans and advances at carrying amount

while they are now recognised at amortized cost using EIR method. Loans and advances decreased by US$ 65,627 due to the following:

- Reclassification of accrued interest receivable of US$ 77,197 from other assets to loans and advances.

- Under previous GAAP, loan processing fees were fully recognized in the profit or loss for the year ended on and before 31 December 2018. As at 1 January 2018, cumulative transition adjustment of unamortized loan processing fees was recognised which decreased loans and advances by US$ 220,843.

- Under previous GAAP, the Bank determined the allowance for losses on loans and advances based on impairment provisioning mandated by NBC Prakas No. B7-017-344 for the year ended on and before 31 December 2018. As at 1 January 2018, loans and advances increased by US$ 209,273 due to the cumulative transition adjustment following CIFRS 9 because ECL on loans and advances to customers was lower than the regulatory provision by that amount.

(iii) Other assets decreased by US$ 77,197 because accrued interest receivable was reclassified from other assets to loans and advances as explained in (ii) above.

(iv) As at 1 January 2018, there was no recognition of lease liability under previous

GAAP. A cumulative transition adjustment to lease liability amounting to US$ 452,386 was recognised under CIFRS 16.

(v) As at 1 January 2018, a cumulative transition adjustment of US$ 125 as provision for

off-balance sheet items was recognized under other liabilities following CIFRS 9.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

27

3. RECONCILIATION BETWEEN PREVIOUS GAAP AND NEW PRESENTATION UNDER

CIFRSs (continued) Explanatory notes to the reconciliation tables (continued)

(b) Lease

As at 1 January 2018, cumulative transition adjustment to recognise the right-of-use asset amounting to US$ 412,190 and lease liability amounting to US$ 452,386 was made based on CIFRS16, with the difference adjusted in the opening retained earnings.

(c) Interest income and other operating income

Interest income for the year ended 31 December 2018 increased by US$178,305 due to amortisation of loan processing fees reclassified from other operating income.

(d) Lease expense

(i) Interest expense increased by US$ 19,845 to recognise accretion of interest on lease

liability for the year ended 31 December 2018. (ii) For the year ended 31 December 2018, depreciation and amortisation increased by

US$ 98,926 for the amortisation of right-of-use asset following the requirement of CIFRS 16. Other operating expenses decreased by US$ 120,000 to derecognise lease expenses based on actual payments.

(e) The transfer from retained earnings to regulatory reserve based on NBC requirement

(Note 19).

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES

4.1 Cash and cash equivalents Cash and cash equivalents consist of notes on hand, unrestricted balances the NBC, balances with other banks and highly-liquid financial assets with original maturities of three months or less from the date of acquisition that are subject to an insignificant risk of changes in their fair value, and are used by the Bank in the management of its short-term commitments.

4.2 Financial instruments

The Bank’s financial assets and liabilities include cash on hand, balances with the NBC (except statutory deposit), balances with other banks, loans and advances to customers, other assets (except for non-refundable deposits and prepayments), borrowings and other liabilities (except for income tax payable) which are measured at amortised cost following the business model discussed in Note 4.2.1.

Initial recognition and measurement

Financial assets and financial liabilities are recognised in the Bank’s statement of financial position when the Bank becomes a party to the contractual provisions of the instruments.

Financial assets and financial liabilities are initially measured at fair value. Transaction costs that are directly attributable to the acquisition or issue of financial assets and financial liabilities (other than financial assets and financial liabilities at fair value through profit or loss) are added to or deducted from the fair value of the financial assets or financial liabilities, as appropriate, on initial recognition.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

28

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued)

Initial recognition and measurement (continued) If the transaction price differs from fair value at initial recognition, the Bank will account for such difference as follows:

If fair value is evidenced by a quoted price in an active market for an identical asset or liability or based on a valuation technique that uses only data from observable markets, then the difference is recognised in profit or loss on initial recognition (i.e. day 1 profit or loss);

In all other cases, the fair value will be adjusted to bring it in line with the transaction price (i.e. day 1 profit or loss will be deferred by including it in the initial carrying amount of the asset or liability).

4.2.1 Business model

The Bank measures balances with the NBC (except for statutory deposit), balances with other banks, loans and advances to customers, and other assets (except for non-refundable deposits and prepayments) at amortised cost based on the business model or management of the asset’s contractual term when the following conditions are met:

The financial assets is held within a business model with the objective to hold financial assets in order to collect contractual cash flow

The contractual terms of the financial asset give rise on a specified date to cash flows that are solely payment of principal and interest (SPPI) on the principal amount outstanding

The details of these conditions are outlined below. The Bank makes an assessment of the objective of a business model in which an asset is held at a portfolio level that best reflects how the assets are managed. Factors considered includes:

the stated policies and objectives for the portfolio and the operation of those policies in practice. In particular, whether management’s strategy focuses on earning contractual interest revenue, maintaining a particular interest rate profile, matching the duration of the financial assets to the duration of the liabilities that are funding those assets or realizing cash flows through the sale of the assets;

how the performance of the portfolio is evaluated and reported to the Bank’s management;

the risks that affect the performance of the business model (and the financial assets held within that business model) and its strategy for how those risks are managed;

how managers of the business are compensated (e.g. whether compensation is based on the fair value of the assets managed or the contractual cash flows collected); and

the frequency, volume and timing of sales in prior periods, the reasons for such sales and its expectations about future sales activity. However, information about sales activity is not considered in isolation, but as part of an overall assessment of how the Bank’s stated objective for managing the financial assets is achieved and how cash flows are realized.

Financial assets that are held for trading or managed and whose performance is evaluated on a fair value basis are measured at FVTPL because they are neither held to collect contractual cash flows nor held both to collect contractual cash flows and to sell financial assets.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

29

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued)

4.2.2 Solely payments of principal and interest (“SPPI”) test

As a second step of its classification process, the Bank assess the contractual terms of the financial asset to identify whether they meet the SPPI test.

For purposes of this assessment, ‘principal’ is defined as the fair value of the financial asset on initial recognition. ‘Interest’ is defined as consideration for the time value of money and for the credit risk associated with the principal amount outstanding during a particular period of time and for other basic lending risks and costs (e.g. liquidity risk and administrative costs), as well as profit margin.

In assessing whether the contractual cash flows are SPPI, the Bank considers the contractual terms of the instrument. This includes assessing whether the financial asset contains a contractual term that could change the timing or amount of contractual cash flows such that it would not meet this condition.

In making the assessment, the Bank considers:

• contingent events that would change the amount and timing of cash flows;

• leverage features;

• prepayment and extension terms;

• terms that limit the Bank’s claim to cash flows from specified assets (e.g. non-recourse loans); and

• features that modify consideration of the time value of money (e.g. periodical reset of interest rates).

Non-recourse loans

In some cases, loans made by the Bank that are secured by collateral of the borrower limit the Bank’s claim to cash flows of the underlying collateral (non-recourse loans). The Bank applies judgment in assessing whether the non-recourse loans meet the SPPI criterion. The Bank typically considers the following information when making this judgement:

• whether the contractual arrangement specifically defines the amounts and dates of the cash payments of the loan;

• the fair value of the collateral relative to the amount of the secured financial asset;

• the ability and willingness of the borrower to make contractual payments, notwithstanding a decline in the value of collateral;

• whether the borrower is an individual or a substantive operating entity or is a special-purpose entity;

• the Bank’s risk of loss on the asset relative to a full-recourse loan;

• the extent to which the collateral represents all or a substantial portion of the borrower’s assets; and

• whether the Bank will benefit from any upside from the underlying assets.

Reclassification of financial assets and liabilities

Financial assets are not reclassified subsequent to their initial recognition, except in the period after the Bank changes its business model for managing financial assets.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

30

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued) 4.2.3 Derecognition of financial assets and liabilities

Financial assets

The Bank derecognises a financial asset when the contractual rights to the cash flows from the financial asset expire, or it transfers the rights to receive the contractual cash flows in a transaction in which substantially all of the risks and rewards of ownership of the financial asset are transferred or in which the Bank neither transfers nor retains substantially all of the risks and rewards of ownership and it does not retain control of the financial asset. On derecognition of a financial asset, the difference between the carrying amount of the asset (or the carrying amount allocated to the portion of the asset derecognised) and the sum of (i) the consideration received (including any new asset obtained less any new liability assumed) and (ii) any cumulative gain or loss that had been recognized in OCI is recognized in profit and loss. Financial liabilities

A financial liability is derecognised when the obligation under the liability is discharged, cancelled or expires. Where an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability. The difference between the carrying value of the original financial liability and the consideration paid is recognised in profit or loss.

4.2.4 Modifications and forbearance of financial assets

If the terms of a financial asset are modified, then the Bank evaluates whether the cash flows of the modified asset are substantially different.

If the cash flows are substantially different, then the contractual rights to cash flows from the original financial asset are deemed to have expired. In this case, the original financial asset is derecognized and a new financial asset is recognized at fair value plus any eligible transaction costs. Any fees received as part of the modification are accounted for as follows:

• fees that are considered in determining the fair value of the new asset and fees that represent reimbursement of eligible transaction costs are included in the initial measurement of the asset; and

• other fees are included in profit and loss as part of the gain or loss on derecognition.

• If cash flows are modified when the borrower is in financial difficulties, then the objective of the modification is usually to maximize recovery of the original contractual terms rather than to originate a new asset with substantially different terms. If the Bank plans to modify a financial asset in a way that would result in forgiveness of cash flows, then it first considers whether a portion of the asset should be written off before the modification takes place (see below for write-off policy). This approach impacts the result of the quantitative evaluation and means that the derecognition criteria are not usually met in such cases.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

31

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued)

4.2.4 Modifications of financial assets and financial liabilities (continued)

• If the modification of a financial asset measured at amortised cost or FVOCI does not result in derecognition of the financial asset, then the Bank first recalculates the gross carrying amount of the financial asset using the original effective interest rate of the asset and recognises the resulting adjustment as a modification gain or loss in profit and loss. For floating-rate financial assets, the original effective interest rate used to calculate the modification gain or loss is adjusted to reflect current market terms at the time of the modification. Any costs or fees incurred and fees received as part of the modification adjust the gross carrying amount of the modified financial asset and are amortised over the remaining term of the modified financial asset.

• If such a modification is carried out because of financial difficulties of the borrower, then the gain or loss is presented together with impairment losses. In other cases, it is presented as interest income calculated using the effective interest rate method.

4.2.5 Offsetting

Financial assets and financial liabilities are offset and the net amount presented in the statement of financial position when, and only when, the Bank has a legal right to set off the amounts and it intends either to settle them on a net basis or to realize the asset and settle the liability simultaneously.

4.2.6 Fair value measurement

‘Fair value’ is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date in the principal or, in its absence, the most advantageous market to which the Bank has access at that date. The fair value of a liability reflects its non-performance risk. When one is available, the Bank measures the fair value of an instrument using the quoted price in an active market for that instrument. A market is regarded as ‘active’ if transactions for the asset or liability take place with sufficient frequency and volume to provide pricing information on an ongoing basis.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

32

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued)

4.2.6 Fair value measurement (continued)

If there is no quoted price in an active market, then the Bank uses valuation techniques that maximize the use of relevant observable inputs and minimize the use of unobservable inputs. The chosen valuation technique incorporates all of the factors that market participants would take into account in pricing a transaction.

The best evidence of the fair value of a financial instrument on initial recognition is normally the transaction price – i.e. the fair value of the consideration given or received. If the Bank determines that the fair value on initial recognition differs from the transaction price and the fair value is evidenced neither by a quoted price in an active market for an identical asset or liability nor based on a valuation technique for which any unobservable inputs are judged to be insignificant in relation to the measurement, then the financial instrument is initially measured at fair value, adjusted to defer the difference between the fair value on initial recognition and the transaction price. Subsequently, that difference is recognized in profit and loss on an appropriate basis over the life of the instrument but no later than when the valuation is wholly supported by observable market data or the transaction is closed out.

If an asset or a liability measured at fair value has a bid price and an ask price, then the Bank measures assets and long positions at a bid price and liabilities and short positions at an ask price.

Portfolios of financial assets and financial liabilities that are exposed to market risk and credit risk that are managed by the Bank on the basis of the net exposure to either market or credit risk are measured on the basis of a price that would be received to sell a net long position (or paid to transfer a net short position) for the particular risk exposure. Portfolio-level adjustments – e.g. bid-ask adjustment or credit risk adjustments that reflect the measurement on the basis of the net exposure – are allocated to the individual assets and liabilities on the basis of the relative risk adjustment of each of the individual instruments in the portfolio.

The fair value of a financial liability with a demand feature (e.g. a demand deposit) is not less than the amount payable on demand, discounted from the first date on which the amount could be required to be paid.

The Bank recognizes transfers between levels of the fair value hierarchy as of the end of the reporting period during which the change has occurred.

4.2.7 Expected credit losses (“ECLs”) The Bank recognises allowance for ECLs on the following financial instruments that are not measured at FVTPL:

• Balances with other banks;

• Loans and advances to customers; and

• Loan commitments and financial guarantee contracts issued. ECLs are required to be measured through a loss allowance at an amount equal to:

• 12-month ECL, i.e. lifetime ECL that result from those default events on the financial instrument that are possible within 12 months after the reporting date, (referred to as Stage 1); or

• full lifetime ECL, i.e. lifetime ECL that result from all possible default events over the life of the financial instrument, (referred to as Stage 2 and Stage 3).

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

33

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued) 4.2.7 Expected credit losses (“ECLs”) (continued)

A loss allowance for full lifetime ECL is required for a financial instrument if the credit risk on that financial instrument has increased significantly since initial recognition. For all other financial instruments, ECLs are measured at an amount equal to the12-month ECL. More details on the determination of a significant increase in credit risk are provided below.

ECLs are a probability-weighted estimate of the present value of credit losses. These are measured as the present value of the difference between the cash flows due to the Bank under the contract and the cash flows that the Bank expects to receive arising from the weighting of multiple future economic scenarios, discounted at the asset’s EIR.

• for undrawn loan commitments, the ECL is the difference between the present value of the difference between the contractual cash flows that are due to the Bank if the holder of the commitment draws down the loan and the cash flows that the Bank expects to receive if the loan is drawn down; and

• for financial guarantee contracts, the ECL is the difference between the expected payments to reimburse the holder of the guaranteed debt instrument less any amounts that the Bank expects to receive from the holder, the debtor or any other party.

The Bank measures ECL on an individual basis, or on a collective basis for portfolios of loans that share similar economic risk characteristics. The measurement of the loss allowance is based on the present value of the asset’s expected cash flows using the asset’s original EIR, regardless of whether it is measured on an individual basis or a collective basis. Credit-impaired financial assets

A financial asset is ‘credit-impaired’ when one or more events that have a detrimental impact on the estimated future cash flows of the financial asset have occurred. Credit-impaired financial assets are referred to as Stage 3 assets. Evidence of credit-impairment includes observable data about the following events:

• significant financial difficulty of the borrower or issuer;

• a breach of contract such as a default or past due event;

• the lender of the borrower, for economic or contractual reasons relating to the borrower’s financial difficulty, having granted to the borrower a concession that the lender would not otherwise consider;

• the disappearance of an active market for a security because of financial difficulties; or

• the purchase of a financial asset at a deep discount that reflects the incurred credit losses. It may not be possible to identify a single discrete event- instead, the combined effect of several events may have caused financial assets to become credit-impaired. The Bank assesses whether debt instruments that are financial assets measured at amortised cost or FVTOCI are credit-impaired at each reporting date. To assess if sovereign and corporate debt instruments are credit impaired, the Bank considers factors such as bond yields, credit ratings and the ability of the borrower to raise funding.

A loan is considered credit-impaired when a concession is granted to the borrower due to a deterioration in the borrower’s financial condition, unless there is evidence that as a result of granting the concession the risk of not receiving the contractual cash flows has reduced significantly and there are no other indicators of impairment. For financial assets where concessions are contemplated but not granted the asset is deemed credit impaired when there is observable evidence of credit-impairment including meeting the definition of default.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

34

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued)

4.2.7 Expected credit losses (“ECLs”) (continued)

The definition of default (see below) includes unlikeliness to pay indicators and a backstop if amounts are overdue for 90 days or more. Definition of default

Critical to the determination of ECL is the definition of default. The definition of default is used in measuring the amount of ECL and in the determination of whether the loss allowance is based on 12-month or lifetime ECL, as default is a component of the probability of default (“PD”) which affects both the measurement of ECLs and the identification of a significant increase in credit risk.

The Bank considers the following as constituting an event of default:

• the borrower is past due more than 90 days on any material credit obligation to the Bank; or

• the borrower is unlikely to pay its credit obligations to the Bank in full.

This definition of default is used by the Bank for accounting purposes as well as for internal credit risk management purposes and is broadly aligned to the regulatory definition of default. The definition of default is appropriately tailored to reflect different characteristics of different types of assets. Overdrafts are considered as being past due once the customer has breached an advised limit or has been advised of a limit smaller than the current amount outstanding.

When assessing if the borrower is unlikely to pay its credit obligation, the Bank takes into account both qualitative and quantitative indicators. The information assessed depends on the type of the asset, for example in corporate lending a qualitative indicator used is the breach of covenants, which is not relevant for retail lending. Quantitative indicators, such as overdue status and non-payment on another obligation of the same counterparty are key inputs in this analysis. The Bank uses a variety of sources of information to assess default which are either developed internally or obtained from external sources. As noted in the definition of credit impaired financial assets above, default is evidence that an asset is credit impaired. Therefore, credit impaired assets will include defaulted assets, but will also include other non-defaulted given the definition of credit impaired is broader than the definition of default. Significant increase in credit risk

The Bank monitors all financial assets, issued loan commitments and financial guarantee contracts that are subject to the impairment requirements to assess whether there has been a significant increase in credit risk since initial recognition. If there has been a significant increase in credit risk, the Bank will measure the loss allowance based on lifetime rather than 12-month ECL. The Bank’s accounting policy is not to use the practical expedient that financial assets with ‘low’ credit risk at the reporting date are deemed not to have had a significant increase in credit risk. As a result, the Bank monitors all financial assets, issued loan commitments and financial guarantee contracts that are subject to impairment for significant increase in credit risk.

ASIA-PACIFIC DEVELOPMENT BANK PLC. (formerly Asia-Pacific Development Specialized Bank Plc.) NOTES TO THE FINANCIAL STATEMENTS (continued) for the year ended 31 December 2019

35

4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICES (continued)

4.2 Financial instruments (continued)

4.2.7 Expected credit losses (“ECLs”) (continued)