asia pacific: textile, apparel & footwear -...

TRANSCRIPT

December 1, 2016

Asia Pacific: Textile, Apparel & Footwear

Equity Research

When the going gets tough: Buy Shenzhou (CL), Yue Yuen

Three debates facing Greater China exporters

China is the largest exporter of apparel and footwear to the US, accounting for

36% and 63% of US imports in 2015, respectively. In this report, we examine

the potential impact of possible changes to US trade policy on exporters in

Greater China, under three potential scenarios: 1) Production move back to

the US: Textile and footwear are labor intensive industries, employing c.23mn

in China. Average hourly wages in China are US$3-4 vs. US$19 in the US. This

makes it difficult to move these jobs back to the US in a big way, in our view.

2) Tariff increase: We estimate that the imposition of an additional tariff of

45% on textile imports would increase US retail prices by 11% on a full pass-

through basis with most of the costs borne by retailers/brands. We estimate

OEMs' earnings for China exports to the US would be cut 30-60% if they take

on 10-20% of the tax duty increase. 3) Future of TPP: If the US withdraws from

the TPP, it could impact brands’ sourcing strategies in the near term. However,

we believe Vietnam, a key production base for many Greater China exporters,

still enjoys cost advantages and preferential duties through FTAs with the EU.

US exposure and production allocation to determine impact

We do stress tests to analyze the potential impact on exporters and

conclude that it largely depends on exporters’ end-market exposures and

production base allocations. Shenzhou has the lowest US exposure (13% of

sales in 2015) but the biggest production base in China (82% of production)

within our coverage. Makalot has high US market exposure (77%) but low

China production (8%). Stella has relatively high US exposure (53%) as well as

high China production (73%) and will likely be impacted the most if it needs to

share a part of potential additional duties on US imports from China.

Shenzhou added to CL (Buy), Yue Yuen up to Buy, Eclat to Neutral

With market concerns on global trade and demand uncertainties, we

recommend investing in quality names with healthy earnings outlooks. We

add Shenzhou to our Conviction List (Buy), on 1) low US exposure, 2)

strong client mix and share gains, 3) integrated business model, 4) Vietnam

capacity ramp-up, and 5) margin upside from product mix and cost

management. Yue Yuen up to Buy from Neutral on 1) stabilized

operation/margin trend, 2) balanced market/client exposure, and 3) rising

contribution from Pou Sheng. Eclat down to Neutral from Buy as: 1) we

forecast EPS recovery to be lower than what we had previously expected, and

2) see uncertainties from US retail clients (26% of 2016E sales) on inventory

control/slower SSSG. We update estimates/target price across our coverage.

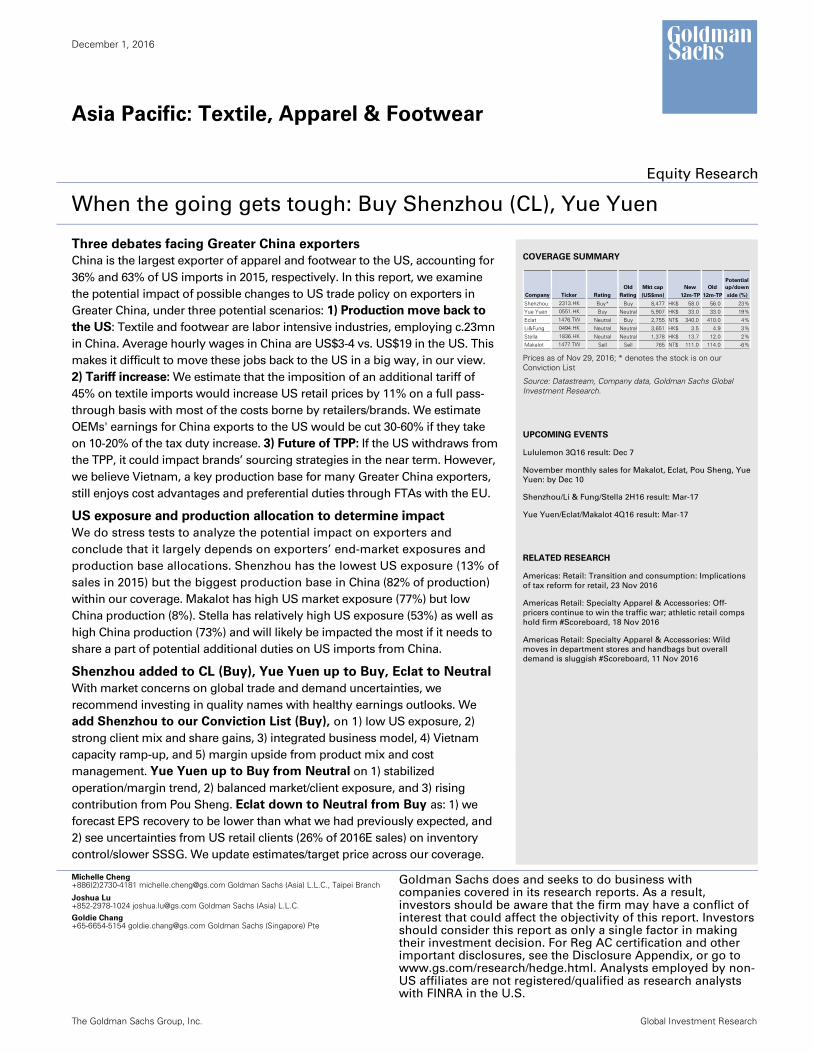

COVERAGE SUMMARY

Prices as of Nov 29, 2016; * denotes the stock is on our Conviction List

Source: Datastream, Company data, Goldman Sachs Global Investment Research.

UPCOMING EVENTS

Lululemon 3Q16 result: Dec 7

November monthly sales for Makalot, Eclat, Pou Sheng, Yue

Yuen: by Dec 10

Shenzhou/Li & Fung/Stella 2H16 result: Mar-17

Yue Yuen/Eclat/Makalot 4Q16 result: Mar-17

RELATED RESEARCH

Americas: Retail: Transition and consumption: Implications

of tax reform for retail, 23 Nov 2016

Americas Retail: Specialty Apparel & Accessories: Off-

pricers continue to win the traffic war; athletic retail comps

hold firm #Scoreboard, 18 Nov 2016

Americas Retail: Specialty Apparel & Accessories: Wild

moves in department stores and handbags but overall

demand is sluggish #Scoreboard, 11 Nov 2016

Michelle Cheng +886(2)2730-4181 [email protected] Goldman Sachs (Asia) L.L.C., Taipei Branch Goldman Sachs does and seeks to do business with

companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not registered/qualified as research analysts with FINRA in the U.S.

Joshua Lu +852-2978-1024 [email protected] Goldman Sachs (Asia) L.L.C. Goldie Chang +65-6654-5154 [email protected] Goldman Sachs (Singapore) Pte

The Goldman Sachs Group, Inc. Global Investment Research

Old Mkt cap New Old

Potential

up/down

Company Ticker Rating Rating (US$mn) 12m-TP 12m-TP side (%)

Shenzhou 2313.HK Buy* Buy 8,477 HK$ 58.0 56.0 23%Yue Yuen 0551.HK Buy Neutral 5,907 HK$ 33.0 33.0 19%

Eclat 1476.TW Neutral Buy 2,755 NT$ 340.0 410.0 4%

Li&Fung 0494.HK Neutral Neutral 3,651 HK$ 3.5 4.9 3%

Stella 1836.HK Neutral Neutral 1,378 HK$ 13.7 12.0 2%Makalot 1477.TW Sell Sell 765 NT$ 111.0 114.0 -6%

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 2

Table of contents

Overview: Focus on earnings quality amid looming uncertainty; Buy Shenzou (CL), Yue Yuen 3

Potential impact of additional duties on US imports from China 5

US heavily reliant on imports; challenges in moving back production 7

Free trade agreements impact sourcing strategies 10

Near-term uncertainty, but longer-term concerns overdone 12

Earnings revisions and valuation 14

Shenzhou: Buy on share gains, defensive market exposure; to CL 18

Yue Yuen: Stabilized margins and rising retail mix; up to Buy 22

Eclat: Down to Neutral as EPS recovery appears priced in 25

Appendix 1: Share price performance 28

Appendix 2: Lukewarm US apparel demand vs. inventory control 29

Disclosure Appendix 31

All prices in this report are as of November 29, 2016 unless otherwise stated.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 3

Overview: Focus on earnings quality amid looming uncertainty;

Buy Shenzou (CL), Yue Yuen

US trade policy key for Chinese exporters

US President-elect Donald Trump has a significantly more hawkish stance than that of the

current administration and may impose new tariffs on imports from China and Mexico, up

to 45%/35%, respectively. Besides, Mr. Trump opposes the Trans-Pacific Partnership (TPP),

which has been one of the most important FTA under negotiation globally, involving the

US, Japan, and another 10 countries including Vietnam. His stance on global trade has

raised concerns among Asian manufacturers. In this report, we analyse the following

possibilities:

1. Imposition of additional tariffs: Chinese players could lose their competitiveness if

brands alter their sourcing strategies and start sourcing from other countries. This

would put pressure on production in China and could speed up a move out of China.

2. Future of TPP: Brands could change their sourcing strategy for import to the US in the

near term, without incurring an immediate duty benefit. Vietnam still enjoys cost

advantages, on top of free trade agreements with other countries.

3. Production move back to the US: With higher labor costs and insufficient labor

supply, production is unlikely to move back to the US immediately. We believe

technology upgrade/automation will determine the feasibility of moving production

back to the US.

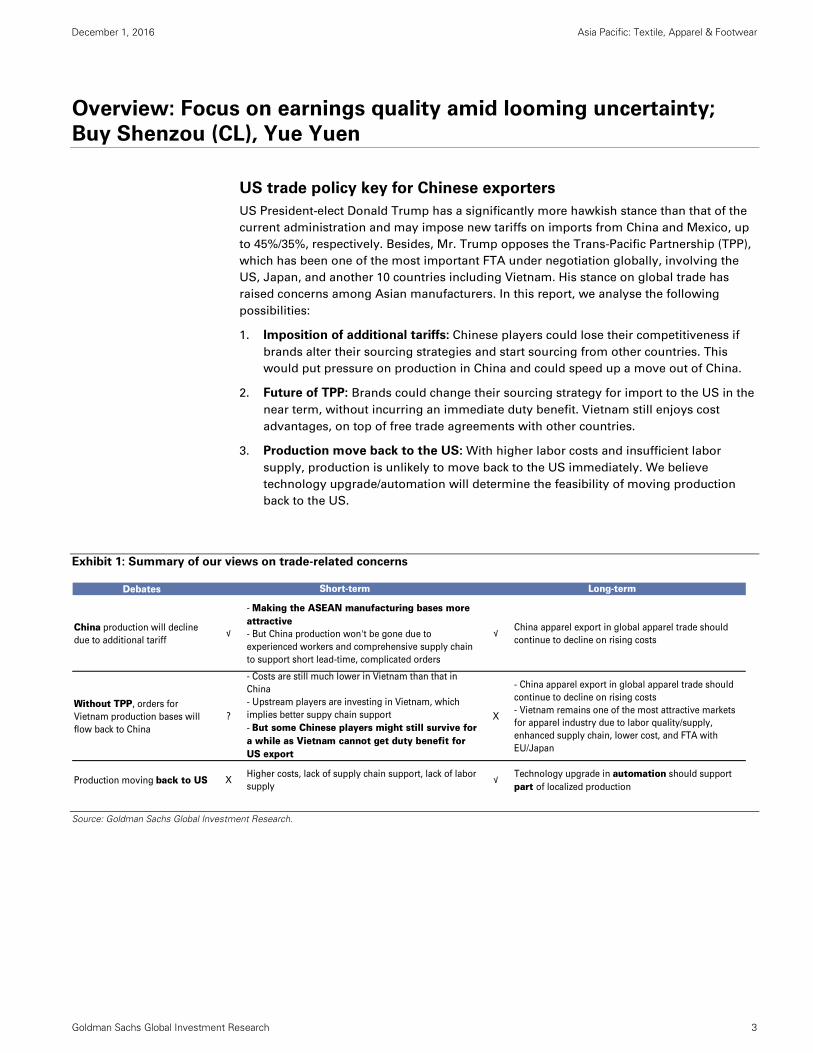

Exhibit 1: Summary of our views on trade-related concerns

Source: Goldman Sachs Global Investment Research.

Debates

China production will decline

due to additional tariff√

- Making the ASEAN manufacturing bases more attractive- But China production won't be gone due to

experienced workers and comprehensive supply chain

to support short lead-time, complicated orders

√China apparel export in global apparel trade should

continue to decline on rising costs

Without TPP, orders for

Vietnam production bases will

flow back to China

?

- Costs are still much lower in Vietnam than that in

China

- Upstream players are investing in Vietnam, which

implies better suppy chain support

- But some Chinese players might still survive for a while as Vietnam cannot get duty benefit for US export

X

- China apparel export in global apparel trade should

continue to decline on rising costs

- Vietnam remains one of the most attractive markets

for apparel industry due to labor quality/supply,

enhanced supply chain, lower cost, and FTA with

EU/Japan

Production moving back to US XHigher costs, lack of supply chain support, lack of labor

supply√

Technology upgrade in automation should support

part of localized production

Short-term Long-term

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 4

Four factors drive our stock picks: Buy Shenzhou (CL), Yue Yuen

Over the long term, we believe industry consolidation and tougher supply chain control

would enable leading OEMs to gain market share. However, to deal with the near-term

uncertainties, we prefer companies with:

1. A more balanced end-market exposure (less US): Shenzhou has the lowest US

exposure at 13% of total sales (2015).

2. Benefiting from China growth story: Yue Yuen has rising contribution from Pou

Sheng (10% in 2015 to 16% in 2018E); Shenzhou is likely to benefit from

Nike/Adidas/Uniqlo’s growth in China.

3. Better client mix: Shenzhou’s key clients (Nike, Uniqlo, Adidas, Puma) are on a solid

track, especially in China; Yue Yuen has diversified sports shoe clients (Nike/Adidas

27%/23% of 2015 OEM sales.

4. Company-specific margin expansion potential: Shenzhou on product mix and

Vietnam capacity ramp-up; Yue Yuen on stabilized operations following relocation

pressures in 2013-15.

Accordingly, we maintain our Buy rating on Shenzhou and add it to our Conviction List,

and upgrade Yue Yuen to Buy from Neutral. We also move Shenzhou (2313.HK), Yue Yuen

(0551.HK), Eclat (1476.TW); Li & Fung (0494.HK), Stella (1836.HK) and Makalot (1477.HK) to

the “Greater China Retail” Coverage Group (Coverage View: Neutral) from the ”TW and HK

Retail” Coverage Group (Coverage View: Neutral).

Exhibit 2: Comparison of OEMs in terms of business model, market/client/production exposure

Source: Company data, Goldman Sachs Global Investment Research.

Makalot Eclat Shenzhou Yue Yuen Feng Tay Stella Li & Fung

Ticker 1477.TW 1476.TW 2313.HK 0551.HK 9910.TW 1836.HK 494.HK

Business description Garment OEM/ODMFabric, garment OEM/ODM

Fabric, garment OEM/ODM

Footwear OEM/ODM Footwear OEM/ODM Footwear OEM/ODM Trading and logistics

Degree of integration5% of fabric supplied from its JV

35% of the fabric is for internal garment manufacturing

100% NA NA NA NA

Sales breakdown by

client (2015)

Gap (23%), Kohl's (23%), Target (15%), GU (12%), Hanesbrands (5%)

Nike (10-15%), lululemon(7-8%), Under Armour (7-8%), JC Penny, Macy's

Nike (30%), Uniqlo (30%), adidas (22%), Puma (8%)

Nike (27% of OEM), adidas (23%)

Nike (80%)UGG, Nike, Clarks, VFC, WWW (c.70%)

Kohl's, Macy, JC Penney

Sales breakdown by

businesses (2015)Garment: 100%

Garment: 65%Fabric: 35%

Garment: 100%OEM: 73%Retail: 27%

Shoes manufacturing and selling:90%Shoes material trade: 1%Others: 9%

Footwear: 100%Trading: 95%Logistics: 5%

Sales breakdown by

product (2015)

Fashion: 58%Active: 15%Sleepwear: 15%Functional sports: 12%

Mostly functional sportswear

Sportswear: 64%Casual wear: 28%Lingerie: 8%Other knitting: 1%

For OEM:Sports shoes: 73%Casual & outdoors: 27%

Sport shoes: 83%Casual shoes and equipment: 10%Wholesale on daily necessities: 5%Ball: 2%

Dress/Casual shoes: c.85%Sports shoes: c.15%

Soft goods: 59%Hard goods:36%Logistics: 5%

Sales breakdown by

geography (2015)

US: 77%Asia:18%Europe:1%Others: 4%

US: 52%Canada: 5%Cambodia: 6%China: 4%Others: 33%

Japan: 23%China: 22%Europe: 18%US: 13%Others: 24%

For OEM: China: 10%US: 35%Europe: 27%Others: 28%

US: 52%Europe: 19%China: 4%Others: 25%

North America: 53%Europe: 26%China: 13%Asia: 6%Others: 2%

US: 62%Europe: 17%Asia: 15%Others: 7%

Production base

breakdown (2015)

Indonesia: 31%Vietnam:33%Cambodia: 23%China: 8%Philippines: 6%

-FabricVietnam: 54%Taiwan: 46%- GarmentVietnam: 63%Lesotho: 16%Cambodia: 11%China: 5%Taiwan: 5%

-FabricChina: 77%Vietnam: 23%- GarmentChina: 82%Cambodia: 16%Vietnam: 2%

Vietnam: 42%Indonesia: 32%China: 25%Others: 1%

Vietnam: 53%India: 20%China: 14%Indonesia: 13%

China: 73%South East Asia: 27%

Sourcing areas: China (50+% of sourcing unit volume), followed by Vietnam, then Bangladesh

Gross margin (2015) 23.6% 28.0% 30.5%23.4% (total company); 19.7% (OEM only)

21.1% 21.0% 11.5%

EBIT margin (2015) 11.3% 19.0% 20.8%5.1% (total company); 5.4% (OEM only)

9.9% 6.4% 2.7%

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 5

Potential impact of additional duties on US imports from China

While US trade policies remain unclear, we conduct a stress test to assess the impact of

potential additional duties on companies under our coverage.

Based on our analysis, we estimate a cotton T-shirt sold at a retail price of US$12 has an

FOB price of c.US$3 per piece. Currently, we estimate duties paid by brands/retailers

amount to c.US$0.5/piece (subject to 16.5% duties).

If imports from China incur an additional 45% duty, it would imply an additional US$1.35

per piece. We summarize three scenarios below (Exhibit 3):

1. If additional duties are fully passed on to the retail price, we estimate retail ASP will

increase by 11%. Considering apparel imports to the US from China and Mexico make

41% of total imports (2015) and assuming an additional 35-45% tariff on apparel

imports from Mexico and China with all tariff increases reflected in ASP, we calculate

5.7% higher costs for consumers’ apparel consumption, or 0.2% of the total per capita

spending. A 5-6% impact is significant in our view given the US apparel market had a

sales CAGR of 1-2% in the past decade.

2. If an OEM making OP margin of 15% (integrated player producing both fabric and

garment) shares 10% of the additional duties, it would imply a 30% hit to profits per

our calculation.

3. If an OEM shares 20% of the additional duties, we estimate earnings will be hurt by

60%.

Exhibit 3: For a cotton T-shirt sold at USD12 per piece, we estimate FOB price at c.US$3.0

Apparel value chain

Source: US ITC, Goldman Sachs Global Investment Research.

Garment FOB, $3.00

Current duty, $0.50

Other handing fee/freight,

$0.11

Wholesaler's GP, $3.00

Retailer's GP, $5.40

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

Apparel value chain, assuming retail ASP of US$12

Retail ASP US$12

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 6

Exhibit 4: If additional duties are fully passed on, we estimate retail ASP will rise by 11%. If

OEMs absorb 10-20% of additional duties, assuming an OPM of 15%, we expect earnings

to be hit by 30-60% Scenario analysis on retail price and OEMs’ profits

Source: US ITC, Goldman Sachs Global Investment Research.

Exhibit 5: Assuming OEMs absorb 20% of the additional duties on US imports from China,

NI would decline 1-48% within our coverage NI analysis if OEMs share 20% of the additional duties

Source: Company data, Goldman Sachs Global Investment Research.

In addition to NI impact, if PE de-rates due to earnings cut and slower NI growth, implied

valuations will lower. Assuming lower NI based on 20% sharing of the additional duties

and lower PE multiples, implied valuations for our OEM coverage slide 20-55%.

T‐Shirt made of cotton

Imported garment value chain

Garment FOB $3.00

Current duty $0.50

Other handing fee/freight $0.11

Wholesaler's GP $3.00

Retailer's GP $5.40

Retail price / piece $12.00

Current duty for import to US

without trade benefits 16.5%Additional duty of 45% imposed

on China import 45%

Additional duty per piece $1.35

OEM's OPM (Garment + fabric) 15.0%

OEM's OP / piece $0.45

Scenario 1) additional duty fully refected on retail ASP, impact on consumers

New retail price / piece $13.35

Upside vs original retail price 11.3%

Scenario 2) OEMs take 10% of the hit from additional duties

OEM's new OP / piece $0.32

vs original OP ‐30.0%

New OPM 10.5%

vs original OPM ‐4.5%

Scenario 3) OEMs take 20% of the hit from additional duties

OEM's new OP / piece $0.18

vs original OP ‐60.0%

New OPM 6.0%

vs original OPM ‐9.0%

US sales as % of total sales China as % of total production OPM

Using 2015 as reference 2018E 2018E 2018E

Shenzhou 13% 71% 23% ‐4%

Yue Yuen 35% 19% 7% ‐7%

Eclat 58% 3% 20% ‐1%

Stella 53% 60% 6% ‐48%

Makalot 77% 8% 8% ‐6%

NI impact

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 7

Exhibit 6: Potential impact on valuations Implied valuations assuming OEMs share 20% of the additional duties and PE multiples de-rate

Source: Datastream, Goldman Sachs Global Investment Research.

US heavily reliant on imports; challenges in moving back production

US imported 97% of its apparel/footwear consumption in 2015

We believe a large-scale production move back to the US would be difficult given higher

costs and a lack of labor supply. US textile industry workers earn an hourly salary of

c.US$19 vs the minimum wage of c.US$2 in China, or total hourly salary of c.US$3-4. There

are only 0.3m workers in the US textile industry vs 23m in China and 2.5m in Vietnam.

US imported 97% of its apparel/footwear consumption in 2015. China is the largest

exporter to the US, accounting for 39%/63% of total US apparel/footwear imports in 2015.

Due to rising costs and a shrinking labor supply in China, China has been losing its cost

advantage while Vietnam has been consistently gaining share in recent years.

Exhibit 7: China accounts for the highest imports to the

US for apparel, but the ratio is declining… US apparel import breakdown by country

Exhibit 8: … same for footwear import

US footwear import breakdown by country

Source: ITA.

Source: Eurostat.

NI impact on OEMs under our coverage, if assuming OEMs absorb 20% of the additional duties

GS target multiple TP Current PE

(X) (LLC) (X)Average since

2011 +1SD ‐1SD

Ave. PE since

2011PE +1SD PE ‐1SD

Ave. PE since

2011PE +1SD PE ‐1SD

Shenzhou 18 58.0 16 12.1 15.7 8.4 37.4 48.8 26.1 ‐35% ‐16% ‐55%

Yue Yuen 13 33.0 12 12.0 13.4 10.6 29.2 32.7 25.8 ‐11% ‐1% ‐22%

Eclat 18 340.0 20 18.7 28.5 8.8 349.4 532.5 164.4 3% 57% ‐52%

Stella 14 13.7 14 16.4 19.3 13.4 8.7 10.2 7.1 ‐36% ‐25% ‐48%Makalot 14 111.0 16 17.1 22.7 11.6 131.7 174.8 89.3 19% 57% ‐20%

Implied valuation based on Change vs current TPPE

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

9M16

US apparel import breakdown

China Vietnam CAFTA Indonesia Bangladesh

NAFTA India EU Others

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010

2011

2012

2013

2014

2015

9M16

US footwear import breakdown

China Vietnam Indonesia Italy India

Mexico CAFTA-DR Bangladesh Others

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 8

Exhibit 9: Vietnam is consistently gaining share in the US apparel import… Yoy value change for apparel import to the US by country

Source: ITA.

Exhibit 10: …same for footwear market

Yoy value change for footwear import to the US by country

Source: ITA.

Cost structure and labor supply drive production base allocation

China’s rising production costs (labor and utility) and difficulties in recruiting workers in

labor-intensive manufacturing industries are making it gradually lose its cost advantage to

other emerging countries including ASEAN. Vietnam has been the biggest beneficiary on

the back of lower costs, labor supply, government support, preferential duty treatment, and

access to upstream material supplies. Not only are downstream garment factories moving

to Vietnam, we see upstream/integrated players including Shenzhou, Far Eastern New

Century (1402.TW), Formosa Group investing. A better industry cluster for textile industry

would also help drive cost efficiency and lead-time management for all players.

Even though labor costs in ASEAN countries including Vietnam have risen by 15-20%

CAGR in recent years, the cost advantage still persists. For example, we estimate

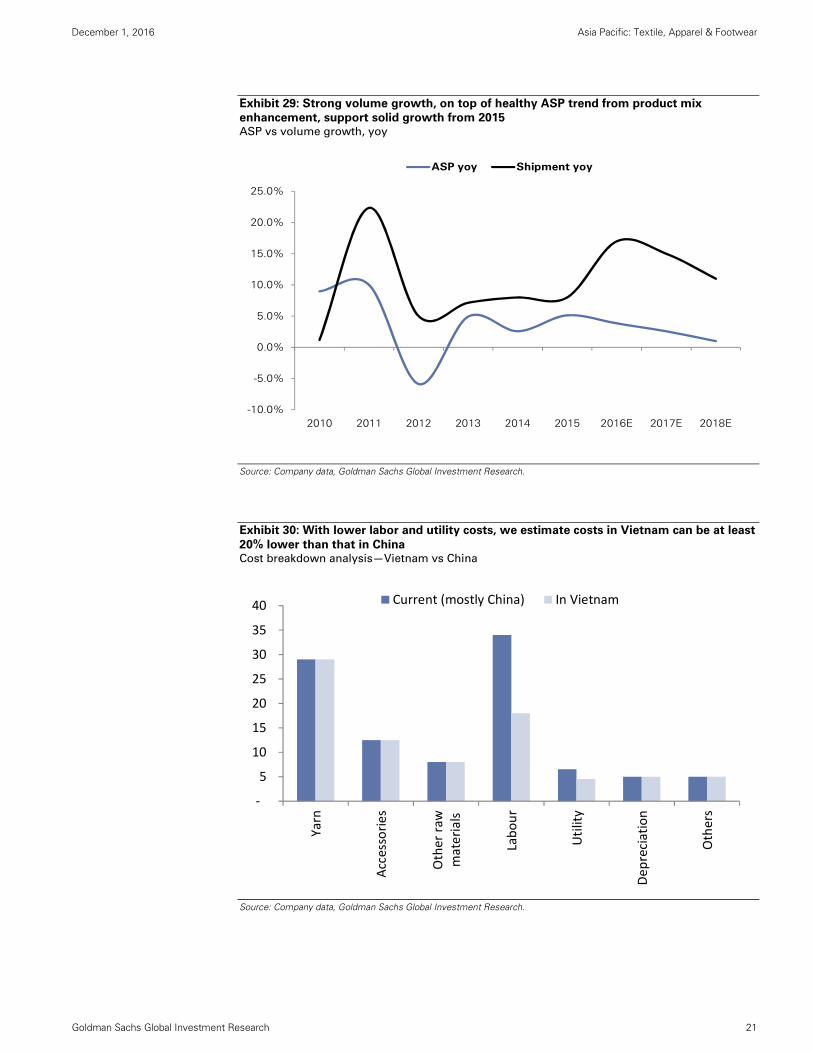

Shenzhou’s production costs in Vietnam are c.20% lower than China assuming similar

productivity (Exhibit 15).

YoY 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 9M16

Total 6% 4% 3% -3% -12% 13% 9% -1% 4% 2% 4% -5%

China 70% 22% 23% 1% 3% 19% 5% -1% 2% 0% 3% -9%Vietnam 6% 18% 35% 20% -3% 16% 13% 7% 14% 14% 14% 2%CAFTA -4% -8% -6% -4% -19% 14% 12% -1% 1% 4% 2% -1%Indonesia 20% 28% 8% 1% -4% 15% 14% -2% 1% -3% 2% -3%Bangladesh 20% 23% 6% 11% -1% 15% 15% -1% 11% -2% 12% 1%NAFTA -10% -12% -15% -14% -18% 4% 7% -2% 0% 2% -4% -7%India 34% 7% -1% -3% -7% 9% 7% -8% 6% 6% 8% 0%EU -9% -4% 6% -8% -32% 5% 22% 7% 8% 10% -4% -5%Others -10% -3% -10% -12% -30% 4% 9% -4% 2% 2% 3% -7%

YoY 2011 2012 2013 2014 2015 9M16

Total 9% 5% 4% 5% 6% -8%

China 6% 2% -1% 0% 1% -15%Vietnam 25% 18% 21% 23% 22% 10%Indonesia 28% 23% 23% 6% 16% -2%Italy 24% 8% 11% 9% -2% -3%India 8% 34% 10% 18% 32% 12%Mexico 21% 30% 12% -8% 0% -17%CAFTA-DR 39% 22% 4% 13% 14% 0%Bangladesh 177% 16% 25% 84% 71% -4%Others -3% -3% 6% 17% 15% 9%

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 9

Exhibit 11: Labor cost differences remain big, driving

production allocation Min. wage comparison across different countries - 2015

Exhibit 12: Labor costs rising significantly in ASEAN Min. wage increase, 2009-2015 CAGR

Source: CEIC

Source: CEIC

Exhibit 13: Shrinking youth also implies a smaller worker base in China

Population distribution by year born, indexed to 1970s, China vs Vietnam

Source: Euromonitor

0 100 200 300 400 500

ChinaVietnam

IndonesiaThailand

PhilippinesMalaysiaCambodia

BangladeshIndiaLaos

MexicoHondurasEl Salvador

TurkeyMoroccoTunisia

Min monthly wage (US$, 2015)

‐5% 0% 5% 10% 15% 20% 25%

China

Vietnam

Indonesia

Thailand

Philippines

Cambodia

Bangladesh

India

Laos

Mexico

Honduras

El Salvador

Turkey

Morocco

TunisiaMin wage: 2009‐2015 CAGR

2000s

2000s1990s

1990s

1980s

1980s

1970s 1970s1960s

1960s

1950s

1950s

1940s

1940s1930s 1930s

0%

20%

40%

60%

80%

100%

120%

140%

China Vietnam

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 10

Exhibit 14: China is expensive, not only for labor, but also

for utility costs Water and electricity costs comparison, China vs Vietnam

Exhibit 15: We estimate Shenzhou can save c.20% of

COGS from lower labor and utility costs if productivity in

Vietnam is at a level similar to China COGS comparison

Source: CEIC

Source: Company data, Goldman Sachs Global Investment Research.

Free trade agreements impact sourcing strategies

Apparel products are subject to import tariffs in the US market ranging from 0% to 32%

while footwear import duties range from 0% to 48%, depending on material, product type,

and import value (exhibit 16). Brands/retailers pay duties with various free trade

agreements and cost structures impacting their sourcing strategies.

There are various FTAs globally/regionally (Exhibit 17). In the US, only c.15% of apparel

import was duty free in 2015. Of these, CAFTA-DR accounted for 62% of duty-free imports

to the US, followed by NAFTA (21%). The major apparel countries that the US imports from,

including China, Vietnam, Indonesia, and Bangladesh (60% of US imports), do not have any

preferential duty treatment in the US.

‐

5

10

15

20

25

30

35

40

Yarn

Accessories

Other raw

materials

Labour

Utility

Depreciation

Others

Current (mostly China) In Vietnam

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 11

Exhibit 16: Apparel/footwear imports into the US incur 0-32%/0-48% duties, depending on material, type and value Illustration of US apparel/footwear import duties on different categories

Source: US ITC.

Exhibit 17: Below we highlight the major global free trade agreements (FTA). In addition to these, there are FTAs

between countries like Bangladesh/Cambodia/Vietnam and the EU

Source: Goldman Sachs Global Investment Research.

Tariffs % HS Chapter/subheading US

Apparel 61-62 0 - 32 *-Women's or girls' blouses and shirts, knitted or crocheted

- Silk 6106.90.15 0.9 - 5.6- Wool 6106.90.10 13.6- Cotton 6106.10.00 19.7- Man-made fibers 6106.20 14.9 - 32-T-shirts, singlets, tank tops and similar garments, knitted or crochete

- Silk 6109.90.40 2.6- Wool 6109.90.15 5.6- Cotton 6109.10.00 16.5- Man-made fibers 6109.90.10 32-Men's or boys' shirts

- Silk 6205.90.10/6205.90.30 1.1 -7.1- Wool 6205.90.05/6205.90.07 9.2 - 17.5- Cotton 6205.20 8.7 - 19.7- Man-made fibers 6205.30 12.2 - 25.9%+29.1¢/kg-Jeans 6201- 6204 8.2 - 16.6

Footwear 64 0 - 48- Footwear with outer soles of rubber, plastics, leather or composition leather and uppers of leather

- Sports footwear 6403.12/ 6403.19 0 - 10- Others 6403.40/ 6403.51/ 6403.59/ 6403.91/ 6403.99 0 - 10- Footwear with outer soles of rubber, plastics, leather or composition leather and uppers of textile materials

- Sports footwear 6404.11 7.5 - 48 *- Others 6404.19 7.5 - 48*Depend on raw materials/types of apparel or footwear/import value; lower for silk and higher for man-made fibers generally in apparel category;lower for vegetable fibers/leather and higher for other materials generally in footwear category

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 12

Exhibit 18: Only c.15% of apparel imports into the US are under FTA and enjoy preferential

duty treatment US apparel imports by FTA—2015

Source: USFIA

Near-term uncertainty, but longer-term concerns overdone

Although uncertainty in the near term will likely impact brands’ sourcing strategies and

impact the cost advantage among different production bases, investor concerns over the

longer-term appear overdone. Key points to consider:

Costs in China are high, in terms of labor and utility, which implies production moving out to

lower cost ASEAN countries is unlikely to reverse.

Costs in the US are even higher with labor in short supply, making a large-scale production move

to the US difficult unless there is a break-through in automation technology.

Additional duties’ impact on consumers’ spending power and OEMs’ margins could be significant,

hurting overall retail market and brands’ profitability.

a. An additional tariff of 35-45% on China/Mexico imports implies 5-6% cost increase

for consumers’ apparel consumption, assuming all else equal. If the additional

duties are fully passed on, it could impact consumer spending power in the US.

b. Given leading OEMs are making 5-20% OPM (in 2015), our analysis shows that

sharing of additional duties will impact some players’ NI significantly (for example,

Stella; Exhibit 5) . If the additional duties are not passed on, we could see huge

margin contractions leading to more aggressive industry consolidation.

How bad can it get from here?

1. If US brands/retailers further destock before a clearer picture emerges on trade policies,

companies suffering from slower order growth from the US, especially from retailers, could see more pressure.

CAFTA FTA62%

NAFTA FTA21%

Jordan FTA6%

QIZ‐Egypt6%

Peru FTA2%

South Korea FTA1%

Colombia FTA1% Others

1%

US FTA World Apparel Imports 2015

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 13

2. If additional duties are imposed on imports from China, suppliers in China will get hurt

while production moving out from China will accelerate.

3. If US officially withdraws from the TPP and China is not subject to additional duties,

competition may intensify as some Chinese local players may survive for a bit longer

as they won’t have duty disadvantage. But, YTD data suggests that China’s exports to

the US dropped the most among major countries although a depreciating RMB favors

Chinese makers.

Long-term industry trends appear intact

Key industry development trends remain unchanged or may speed up, favoring leading

players:

Brands like Nike, Adidas have been highlighting their investments in automation. OEMs with the

ability to work with brands on further cost efficiency improvement will likely gain shares.

OEMs with multi-national operations will have better capabilities to accommodate brands’

sourcing strategies, in our view.

Based on our conversation with OEMs, we summarize several key strategies:

Vietnam remains an important country for future investment given its cost advantage, industry

supply chain, trade benefit (i.e. EU).

OEMs are also surveying other countries like Myanmar, Laos, etc. to diversify risks.

Without TPP, production allocation for different items will be re-organized because synthetic

materials were to get higher duty savings under the TPP framework. OEMs can potentially re-

arrange production lines based on scale or manufacturing costs.

Investment in automation, production efficiency improvement, and materials will continue to

drive differentiation and enable share gains, in our view.

Exhibit 19: Vietnam is still small in terms of apparel export to EU (3% in 2015), but could

pick up if an FTA is signed in 2018 EU apparel import breakdown by country

Source: Eurostat.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

8M16

EU apparel import breakdown

Others

Tunisia

Morocco

Cambodia

Vietnam

India

Turkey

Bangladesh

China

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 14

Earnings revisions and valuation

Our top pick among OEMs is Shenzhou. We believe Shenzhou is the most defensive OEM

as it has the lowest exposure to the US, a balanced market/client base, is gaining market

share in key accounts, and has potential for margin upside from product mix and Vietnam

capacity ramp-up. We reiterate Buy on Shenzhou and add it to our Conviction List as we

note increased upside following the recent market pullback (down 10% over last three

months vs. the Hang Seng index down 0.4%). We also like Yue Yuen and upgrade it to Buy

from Neutral given its stabilized margin trend, balanced market/clients mix, and rising

contribution from Pou Sheng. We downgrade Eclat on Neutral from Buy, as we forecast

earnings recovery from 4Q16 to be lower than what we had previously expected due to

uncertainties in global trade and US retailers’ destocking. Moreover, we believe this

recovery is already priced in with its shares currently trading at 20.5X vs. its historical

average of 19X (since 2011). Li & Fung, Stella and Makalot remain more challenging given

high casual/fashion and private label clients’ exposure. However, we remain Neutral-rated

on Li & Fung and Stella as valuations appear fair at current levels. We maintain Sell on

Makalot as its private label clients (Kohl’s and Target) could see significant order

contraction due to muted sales growth.

In this note, we roll over our valuation base from 2017/18PE average to 2018 PE. Our PE

multiples still take into account EPS growth and CROCI, and are benchmarked to global

peers.

Shenzhou (CL-Buy; TP: HK$58): Most defensive OEM with solid

brand/market exposure

We reiterate our Buy on Shenzhou and add it to our regional Conviction list. We think the

13% pullback in its share price since its Sept. peak, driven by market concerns over global

trade and demand, offers a good opportunity to accumulate. Shenzhou is the most

defensive name among our covered exporters due to: 1) balanced market exposure with

less exposure to the US (10% in 1H16); 2) strong client mix and share gains; 3) integrated

business model to support clients’ short lead-time orders; 4) volume growth with rising

contribution from Vietnam capacity; 5) margin upside from product mix and cost mgmt.

We expect EPS growth of 24%/20% in 2H16 and 2017E. We fine tune 2016-18E EPS by -

0.5%-2% to factor in latest FX trend. Our 12-m TP rises to HK$58 from HK$56 as we roll

over to 2018. Our target multiple remains 18x, benchmarked vs global peers on earnings

growth and CROCI. Risks: 1) Slower sportswear demand growth, 2) higher-than-expected

labor costs increase, 3) slower ramp-up in production in Vietnam, 4) FX.

Yue Yuen (Buy; TP: HK$33): Stabilized margins and rising

contribution from Pou Sheng

We upgrade Yue Yuen to Buy from Neutral on: 1) stabilized operations with decent

margin improvement from 4Q15, after relocation issues dragged down efficiency in China;

2) balanced client and market exposure for OEM business; 3) rising contribution from

Pou Sheng. We fine tune our 2016-18E EPS by 1-5% to factor in the latest 3Q16 result and

FX trend (RMB against USD at 6.9 from 4Q16-2017). Our 12-month SOTP-based target price

is unchanged at HK$33. We roll over our valuation base to 2018E and derive our target

price by applying 14X P/E to value Pou Sheng (down from 16X, as we believe the easiest

path to margin expansion, from 4.2% in 2015 to 6.5% in 2016E, is almost done and further

re-rating to previous peak PE of 16X requires stronger execution on margin beat in our

view) and 13X P/E (unchanged) to the OEM business. Risks: 1) Worse-than-expected

production efficiency in China, 2) weaker-than-expected volume growth in sports and

casual shoes, 3) rising raw material costs in the near term, and 4) lower contribution from

Pou Sheng.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 15

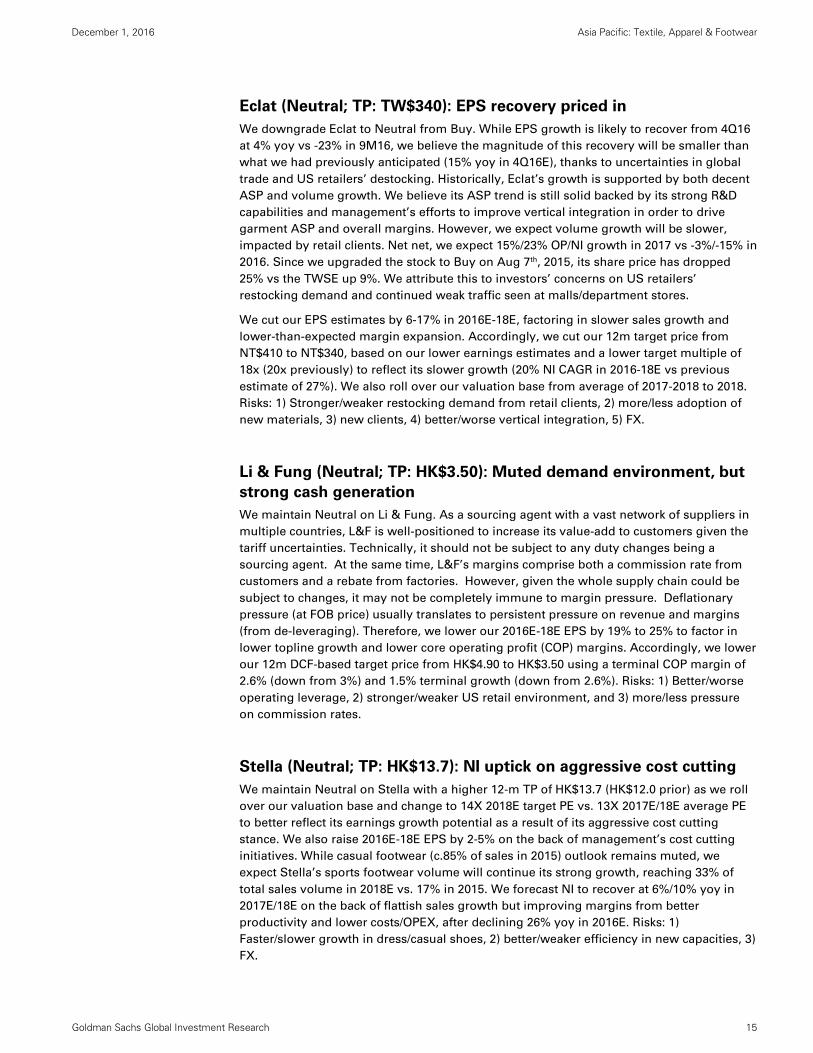

Eclat (Neutral; TP: TW$340): EPS recovery priced in

We downgrade Eclat to Neutral from Buy. While EPS growth is likely to recover from 4Q16

at 4% yoy vs -23% in 9M16, we believe the magnitude of this recovery will be smaller than

what we had previously anticipated (15% yoy in 4Q16E), thanks to uncertainties in global

trade and US retailers’ destocking. Historically, Eclat’s growth is supported by both decent

ASP and volume growth. We believe its ASP trend is still solid backed by its strong R&D

capabilities and management’s efforts to improve vertical integration in order to drive

garment ASP and overall margins. However, we expect volume growth will be slower,

impacted by retail clients. Net net, we expect 15%/23% OP/NI growth in 2017 vs -3%/-15% in

2016. Since we upgraded the stock to Buy on Aug 7th, 2015, its share price has dropped

25% vs the TWSE up 9%. We attribute this to investors’ concerns on US retailers’

restocking demand and continued weak traffic seen at malls/department stores.

We cut our EPS estimates by 6-17% in 2016E-18E, factoring in slower sales growth and

lower-than-expected margin expansion. Accordingly, we cut our 12m target price from

NT$410 to NT$340, based on our lower earnings estimates and a lower target multiple of

18x (20x previously) to reflect its slower growth (20% NI CAGR in 2016-18E vs previous

estimate of 27%). We also roll over our valuation base from average of 2017-2018 to 2018.

Risks: 1) Stronger/weaker restocking demand from retail clients, 2) more/less adoption of

new materials, 3) new clients, 4) better/worse vertical integration, 5) FX.

Li & Fung (Neutral; TP: HK$3.50): Muted demand environment, but

strong cash generation

We maintain Neutral on Li & Fung. As a sourcing agent with a vast network of suppliers in

multiple countries, L&F is well-positioned to increase its value-add to customers given the

tariff uncertainties. Technically, it should not be subject to any duty changes being a

sourcing agent. At the same time, L&F’s margins comprise both a commission rate from

customers and a rebate from factories. However, given the whole supply chain could be

subject to changes, it may not be completely immune to margin pressure. Deflationary

pressure (at FOB price) usually translates to persistent pressure on revenue and margins

(from de-leveraging). Therefore, we lower our 2016E-18E EPS by 19% to 25% to factor in

lower topline growth and lower core operating profit (COP) margins. Accordingly, we lower

our 12m DCF-based target price from HK$4.90 to HK$3.50 using a terminal COP margin of

2.6% (down from 3%) and 1.5% terminal growth (down from 2.6%). Risks: 1) Better/worse

operating leverage, 2) stronger/weaker US retail environment, and 3) more/less pressure

on commission rates.

Stella (Neutral; TP: HK$13.7): NI uptick on aggressive cost cutting

We maintain Neutral on Stella with a higher 12-m TP of HK$13.7 (HK$12.0 prior) as we roll

over our valuation base and change to 14X 2018E target PE vs. 13X 2017E/18E average PE

to better reflect its earnings growth potential as a result of its aggressive cost cutting

stance. We also raise 2016E-18E EPS by 2-5% on the back of management’s cost cutting

initiatives. While casual footwear (c.85% of sales in 2015) outlook remains muted, we

expect Stella’s sports footwear volume will continue its strong growth, reaching 33% of

total sales volume in 2018E vs. 17% in 2015. We forecast NI to recover at 6%/10% yoy in

2017E/18E on the back of flattish sales growth but improving margins from better

productivity and lower costs/OPEX, after declining 26% yoy in 2016E. Risks: 1)

Faster/slower growth in dress/casual shoes, 2) better/weaker efficiency in new capacities, 3)

FX.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 16

Makalot (Sell; TP: TW$111): Private label clients still a drag

We remain Sell-rated on Makalot given 1) lower visibility of client orders due to weak performance of retail clients (Kohl’s and Target) and some fashion brands (Gap); 2) unfavorable product mix as new products/clients take time to contribute

meaningfully; 3) margin contraction as management targets to secure volumes through

price cuts. We cut our 2016-18E EPS by 0%-6% to factor in price cuts and margin

contraction. Accordingly, we revise our 12m target price down from NT$114 to NT$111. We

roll over our valuation to 2018E, but maintain our PE multiple at 14X. Risks: 1) Stronger

apparel consumption, 2) faster capacity ramp-up at the new sportswear plant in Vietnam, 3)

better product mix, 4) higher contribution from new clients, 5) FX.

Exhibit 20: Earnings revision summary Greater China exporters’ earnings revision vs. consensus

Source: Company data, Goldman Sachs Global Investment Research.

Exhibit 21: 12m TPs for our Greater China exporters: CL-Buy on Shenzhou, Buy Yue Yuen, Neutral on Eclat 12-m TP revision summary

Source: Company data, Datastream Goldman Sachs Global Investment Research.

EPS % % % GSe vs. Consensus

Ticker Currency New Old chg New Old chg New Old chg 16E 17E 18E 16E 17E 18E 16E 17E 18E

Exporters

Shenzhou 2313.HK Rmb 1.68 2.13 2.14 -0.5% 2.57 2.52 2.1% 2.86 2.80 2.0% 27% 20% 11% 4% 5% 0% 2.05 2.44 2.86Eclat 1476.TW NT$ 15.52 13.18 14.05 -6.2% 16.26 18.20 -10.7% 18.84 22.69 -17.0% -15% 23% 16% -1% -2% -7% 13.3 16.6 20.2Makalot 1477.TW NT$ 10.48 7.64 7.64 0.0% 7.20 7.50 -3.9% 8.19 8.74 -6.3% -27% -6% 14% -10% -12% -14% 8.4 8.2 9.6 Yue Yuen 0551.HK US$ 0.24 0.30 0.28 4.9% 0.31 0.30 1.3% 0.34 0.34 0.8% 25% 4% 10% 4% 0% -9% 0.29 0.31 0.33Stella 1836.HK US$ 0.15 0.11 0.11 5.0% 0.12 0.12 2.4% 0.13 0.13 2.2% -26% 6% 10% 5% 0% -13% 0.11 0.12 0.13Li & Fung 0494.HK US$ 0.05 0.03 0.04 -22.1% 0.03 0.04 -18.8% 0.03 0.04 -24.8% -36% 4% -3% -10% -9% -16% 0.04 0.04 0.04

Consensus2015 2016E 2017E 2018E YoY%

Valuations (on 2018E EPS)

New target

P/E (X)

Old target

P/E (X)

2018E

EPSCurr

12m TP

(New)

Price

Nov-29

Up/down

sideRating (New) TP (Old)

TP

change

Rating

(Old)

Exporters

Shenzhou 18 18 3.21 HK$ 58.00 47.00 23% Buy* 56.00 4% BuyYue Yuen 13 14 2.62 HK$ 33.00 27.75 19% Buy 33.00 0% NeutralEclat 18 20 18.84 NT$ 340.00 325.50 4% Neutral 410.00 -17% BuyLi & Fung *14 15 0.25 HK$ 3.50 3.39 3% Neutral 4.90 -29% NeutralStella 14 13 1.01 HK$ 13.70 13.46 2% Neutral 12.00 14% NeutralMakalot 14 14 8.19 NT$ 111.00 118.00 -6% Sell 114.00 -3% SellNote: We refer to implied P/E for Li & Fung and Yue Yuen, as they are based on DCF valuation and SOTP, respectively. For Yue Yuen, we use 13X/14X 2018E target P/E for OEM/retail business (Pou Sheng)*denotes that the stock is on our Conviction List

Decem

ber 1, 2016 A

sia Pacific: Textile, Apparel &

Footwear

Goldm

an Sachs Global Investm

ent Research

17

Exhibit 22: Peers’ valuation

*denotes stock is on our regional Conviction List; all target prices mentioned above are on a 12-month timeframe. NC=Not Covered; NA=Not Applicable.

Source: Company data, Goldman Sachs Global Investment Research.

Stock Market cap Price Pricing TargetPotentialupside/ P/B (X) ROE

DivYield

FCF Yield

EV/EBITDA

(X)Net debt/Equity CROCI

Company Ticker Rating (US$mn) 29-Nov-2016 currency Price downside 2016E 2017E 2018E 2016 2017E 2018E 2016E 2017E 2018E 2016E 2017E 2018E 2017E 2017E 2017E 2017E 2017EChina sports brands & apparel/footwear OEMs

Shenzhou International Group 2313.HK Buy* 8,477 47.00 HKD 58.0 23% 27% 20% 11% 19.6 16.3 14.6 4.0 3.5 3.1 21% 23% 22% 3.3% 3% 11.7 -13% 24%Pou Sheng International Holdings 3813.HK Buy 1,600 2.33 HKD 3.0 29% 60% 16% 21% 15.4 13.2 10.9 1.8 1.6 1.5 12% 13% 14% 1.7% 8% 7.3 -7% 12%Yue Yuen Industrial 0551.HK Buy 5,907 27.75 HKD 33.0 19% 25% 4% 10% 12.0 11.6 10.6 1.2 1.2 1.1 11% 11% 11% 5.2% 7% 6.8 -9% 10%Li Ning Co. 2331.HK Buy 1,003 5.68 HKD 6.5 14% NM 11% 31% 20.8 18.7 14.2 2.7 2.3 1.9 16% 16% 18% 0.0% 5% 8.9 -34% 12%Eclat Textile Co. 1476.TW Neutral 2,755 325.50 TWD 340.0 4% -15% 23% 16% 24.7 20.0 17.3 5.8 5.2 4.6 26% 27% 28% 3.5% 3% 13.3 -32% 26%Anta Sports Products 2020.HK Neutral 6,895 21.45 HKD 22.6 5% 16% 17% 10% 20.1 17.2 15.6 5.1 4.7 4.3 27% 29% 29% 4.1% 5% 12.9 -62% 26%Belle International Holdings 1880.HK Neutral 4,828 4.44 HKD 4.7 6% 4% -1% -5% 10.2 10.2 10.7 1.2 1.2 1.1 13% 12% 11% 6.0% 6% 5.1 -27% 14%Li & Fung 0494.HK Neutral 3,652 3.39 HKD 3.5 3% -36% 4% -3% 13.5 12.9 13.4 1.4 1.4 1.4 11% 11% 11% 6.8% 6% 7.5 0% 9%Stella International Holdings 1836.HK Neutral 1,378 13.46 HKD 13.7 2% -26% 6% 10% 15.4 14.6 13.3 1.4 1.4 1.4 9% 10% 10% 6.9% 5% 9.2 -13% 11%Makalot Industrial Co 1477.TW Sell 765 118.00 TWD 111.0 -6% -27% -6% 14% 15.4 16.4 14.4 2.8 2.8 2.6 18% 17% 19% 5.3% 6% 10.6 -16% 19%Median 4% 8% 11% 15.4 15.4 13.8 2.3 2.0 1.7 15% 15% 16% 4.6% 5.4% 9.0 -14% 13%

Apparel OEM/ODM peers

Regina Miracle 2199.HK NC 1,214 7.69 HKD NA NA -61% 80% 72% 47.5 26.4 15.4 3.4 3.1 2.6 11% 12% 18% 0.9% NA 17.9 17% NALuen Thai 0311.HK NC 428 3.21 HKD NA NA 91% 31% NA 18.0 13.8 NA 1.1 1.0 NA 6% 7% NA 2.4% NA 2.6 NA NAPacific Textiles 1382.HK NC 1,675 8.98 HKD NA NA -5% 5% 8% 12.6 12.0 11.1 3.9 3.9 3.8 31% 33% 36% 8.2% NA 9.4 -18% NATexwinca 0321.HK NC 1,003 5.63 HKD NA NA -13% -22% 3% 9.7 12.5 12.1 1.3 1.3 1.3 12% 10% 10% 8.9% NA 6.1 -40% NABest Pacific 2111.HK NC 843 6.36 HKD NA NA 25% 18% 26% 15.1 12.8 10.2 3.2 2.8 2.4 23% 23% 25% 2.6% NA 10.0 3% NADe Licacy 1464.TW NC 233 26.70 TWD NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NAEverest Textile 1460.TW NC 255 17.25 TWD NA NA 10% NA NA 15.2 NA NA 1.6 NA NA 10% NA NA NA NA NA NA NAYoungone 111770.KS NC 1,056 27,900 KRW NA NA 6% 9% 12% 9.0 8.2 7.3 1.0 0.9 0.8 11% 11% 11% 0.7% NA 5.3 -7% NAHansae 105630.KS NC 764 22,350 KRW NA NA -20% 16% 13% 12.2 10.5 9.3 1.8 1.6 1.4 16% 16% 16% 1.1% NA 8.9 34% NAWillbes 008600.KS NC 128 2,635 KRW NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NA NAPan Brothers PBRX.JK NC 208 434 IDR NA NA NM NA NA 11.4 NA NA 1.0 NA NA 9% NA NA NA NA 6.0 NA NAMedian 1% 16% 13% 12.6 12.5 10.7 1.6 1.6 1.9 11% 12% 17% 2.4% NA 7.5 -2% NA

Global apparel brands- Casual & fashion

Global Brands Group 0787.HK Buy 1,215 1.14 HKD 1.40 23% 9% 88% 55% 18.0 9.5 6.2 0.5 0.5 0.4 3% 5% 7% 0.0% 13% 6.5 30% 5%L Brands Inc. LB Buy 20,885 71.8 USD 86.0 20% -6% 4% 15% 19.4 18.7 16.2 NA NA NA NA NA NA 3.7% 3% 9.3 NA 16%Inditex ITX.MC Buy* 106,315 32.2 EUR 37.0 15% 12% 11% 12% 31.7 28.5 25.4 7.9 7.1 6.4 26% 26% 27% 2.3% 3% 16.2 -53% 14%Ralph Lauren Corp. RL Buy* 9,727 110.9 USD 127.0 15% -15% 2% 12% 19.5 19.0 17.0 2.6 2.5 2.3 13% 13% 14% 1.5% 4% 9.4 -13% 11%Urban Outfitters Inc. URBN Neutral 4,230 32.4 USD 36.0 11% 9% 11% 9% 16.8 15.1 13.8 2.9 2.6 2.3 19% 18% 18% 0.0% 6% 6.2 -26% 12%Gap Inc. GPS Neutral 10,804 25.5 USD 27.0 6% -19% 2% 3% 12.9 12.5 12.2 3.5 3.0 2.7 29% 26% 23% 3.0% 7% 5.0 -10% 11%Hennes & Mauritz HMb.ST Neutral 48,067 267.9 SEK 275.0 3% -11% 14% 10% 24.1 21.2 19.2 7.3 6.8 6.2 31% 33% 34% 3.8% 3% 12.2 -5% 10%PVH Corp. PVH Neutral 8,775 108.1 USD 108.0 0% -5% 7% 10% 16.2 15.2 13.7 1.8 1.6 1.5 11% 11% 11% 0.2% 6% 9.6 38% 12%Fast Retailing 9983.T Neutral 36,467 40,200 JPY 34,000 -15% -25% 53% 8% 57.2 37.3 34.6 6.9 6.1 5.5 11% 17% 17% 0.9% 2% 18.5 -14% 12%American Eagle Outfitters Inc. AEO Sell 3,575 18.4 USD 12.0 -35% 13% -6% -1% 15.6 16.6 16.7 2.8 2.5 2.3 19% 16% 15% 3.3% 6% 5.9 -39% 12%Median -6% 9% 10% 18.7 17.6 16.5 2.9 2.6 2.3 19% 17% 17% 1.9% 5% 9.3 -13% 12%

Global sportwear & functional brands

adidas ADSGn.DE Buy 29,418 137.6 EUR 181.0 32% 42% 15% 19% 27.5 24.0 20.1 4.4 3.9 3.5 17% 17% 18% 1.7% 2% 12.8 4% 14%Nike Inc. NKE Buy 86,941 51.0 USD 62.0 22% 10% 8% 13% 22.9 21.2 18.8 6.8 6.5 6.1 31% 32% 34% 1.5% 4% 14.1 -23% 24%Columbia Sportswear Co. COLM Buy* 4,174 59.6 USD 71.0 19% 8% 10% 11% 22.5 20.5 18.4 2.7 2.4 2.2 13% 13% 13% 1.2% 4% 9.8 -36% 17%Under Armour Inc. UA Neutral 13,334 31.2 USD 35.0 12% 21% 13% 13% 49.0 43.3 38.2 6.7 5.8 5.0 15% 15% 14% 0.0% -2% 19.8 32% 18%VF Corp. VFC Buy 24,192 56.9 USD 63.0 11% 2% 11% 14% 18.1 16.4 14.4 4.8 5.0 4.9 26% 29% 33% 2.8% 5% 11.4 39% 20%Puma PUMG.DE Neutral 3,700 234.0 EUR 242.0 3% 59% 57% 29% 59.4 37.9 29.4 2.1 1.9 1.8 4% 5% 6% 0.4% 2% 13.2 -18% 10%Asics Corp. 7936.T Buy 4,115 2,434.0 JPY 2,500.0 3% 26% 22% 13% 35.8 29.2 26.0 2.2 2.1 2.0 6% 7% 8% 1.2% 3% 11.2 -21% 8%lululemon athletica inc. LULU Sell 8,121 57.2 USD 46.0 -20% 10% 10% 9% 28.0 25.4 23.4 0.0 0.2 3.7 25% 22% 20% 0.0% 2% 13.2 -51% 25%Median 16% 12% 13% 29.3 25.2 22.4 3.8 3.7 3.5 14% 14% 13% 1.2% 4% 12.3 -19% 18%

US department stores & discount stores

TJX Cos. TJX Buy 52,727 78.7 USD 89.0 13% 5% 6% 11% 22.5 21.2 19.0 11.5 11.1 10.5 53% 54% 58% 1.4% 4% 10.9 6% 26%Burlington Stores Inc. BURL Buy 6,234 87.4 USD 98.0 12% 37% 21% 18% 28.0 23.2 19.7 NA NA NA NA NA NA 0.0% 6% 10.7 NA 12%Macy's Inc. M Neutral 13,284 43.1 USD 44.0 2% -15% 17% -6% 13.2 11.3 12.0 3.3 3.5 3.5 25% 30% 29% 3.5% 8% 6.3 202% 8%Ross Stores Inc. ROST Neutral 27,263 68.4 USD 69.0 1% 12% 12% 13% 24.5 21.8 19.3 9.7 7.9 6.4 42% 40% 37% 0.8% 5% 11.1 -33% 38%Nordstrom Inc. JWN Neutral 9,850 56.1 USD 49.0 -13% -6% 5% 5% 18.6 17.7 16.8 8.4 7.0 5.9 50% 44% 38% 2.7% 4% 6.9 124% 12%Kohl's Corp. KSS Sell 9,848 54.1 USD 35.0 -35% -2% -7% -8% 13.7 14.8 16.0 1.9 1.7 1.7 13% 12% 11% 3.8% 8% 5.0 43% 11%Median -1% 14% 4% 18.8 16.6 15.7 6.5 5.7 4.9 34% 35% 33% 2.2% 6% 8.7 84% 23%

EPS growth P/E (X)

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 18

Shenzhou: Buy on share gains, defensive market exposure; to CL

Source of opportunity

We reiterate our Buy on Shenzhou and add it to our regional Conviction

list. We think the 13% pullback in its share price since its Sept. peak,

driven by market concerns over global trade and demand, offers a good

opportunity to accumulate. Shenzhou is the most defensive name

among our covered exporters due to: 1) balanced market exposure with

less exposure to the US (10% in 1H16); 2) strong client mix and share

gains; 3) integrated business model to support clients’ short lead-time

orders; 4) volume growth with rising contribution from Vietnam

capacity; 5) margin upside from product mix and cost mgmt. We expect

EPS growth of 24%/20% in 2H16 and 2017E.

Catalyst

1) Less impacted by uncertain US trade policies: Shenzhou is down

7% and peers down 3% in the past month on concerns on US trade

policies. Even though key accounts are Uniqlo/Nike/Adidas/Puma, we

believe potential impact should be smaller for Shenzhou as it sells to

diversified markets especially in Asia, unlike many other OEMs like

Makalot/Eclat/Stella. Shenzhou has North America exposure of only

13% vs c.77%/57%/53% in 2015.

2) Resilient growth prospects: Shenzhou’s sales growth from its top

four clients grew at an avg. of 25% in 1H16. We expect growth of 17%

yoy for 2H16E and 2017E on market share gains, given its strong

production efficiency, product upgrade, and its capability to fulfill short

lead-time orders. Also, Shenzhou has been ramping up its capacity in

Vietnam and we expect this to support 15%/11% volume growth for the

group in 2017/18E. On top of that, we believe an improved product mix

and better efficiency in Vietnam imply further margin upside for

Shenzhou.

Valuation

We fine tune 2016-18E EPS by -0.5%-2% to factor in latest FX trend. Our

12-m TP rises to HK$58 from HK$56 as we roll over to 2018. Our target

multiple remains 18x, benchmarked vs global peers on earnings growth

and CROCI.

Key risks

1) Slower sportswear demand growth, 2) higher-than-expected labor

costs increase, 3) slower ramp-up in production in Vietnam, 4) Changes

in FX.

INVESTMENT LIST MEMBERSHIP

Asia Pacific Buy list

Asia Pacific Conviction Buy list

Coverage View: Neutral

Growth

Returns *

Multiple

Volatility Volatility

Multiple

Returns *

Growth

Investment Profile

Low High

Percentile 20th 40th 60th 80th 100th

* Returns = Return on Capital For a complete description of the investment

profile measures please refer to the

disclosure section of this document.

Shenzhou International Group (2313.HK)

Asia Pacific Consumer Peer Group Average

Key data Current

Price (HK$) 47.00

12 month price target (HK$) 58.00

Market cap (HK$ mn / US$ mn) 65,753.0 / 8,477.6

Foreign ownership (%) --

12/15 12/16E 12/17E 12/18E

EPS (Rmb) 1.68 2.13 2.57 2.86

EPS growth (%) 14.0 26.7 20.4 11.2

EPS (diluted) (Rmb) 1.68 2.13 2.57 2.86

EPS (basic pre-ex) (Rmb) 1.68 2.13 2.57 2.86

P/E (X) 17.5 19.6 16.3 14.6

P/B (X) 3.2 3.9 3.5 3.1

EV/EBITDA (X) 12.8 14.0 11.7 10.2

Dividend yield (%) 3.1 2.7 3.3 3.7

ROE (%) 18.9 21.4 22.7 22.4

CROCI (%) 22.4 22.5 24.0 23.7

7,500

8,500

9,500

10,500

11,500

12,500

35

40

45

50

55

60

Nov-15 Mar-16 Jun-16 Sep-16

Price performance chart

Shenzhou International Group (L) Hang Seng China Ent. Index (R)

Share price performance (%) 3 month 6 month 12 month

Absolute (6.4) 22.0 17.2

Rel. to Hang Seng China Ent. Index (9.2) 7.9 16.6

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 11/30/2016 close.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 19

*Closing price as of Nov 30th, 2016

Shenzhou International Group: Summary financials

Profit model (Rmb mn) 12/15 12/16E 12/17E 12/18E Balance sheet (Rmb mn) 12/15 12/16E 12/17E 12/18E

Total revenue 12,639.3 15,356.2 18,113.0 20,306.5 Cash & equivalents 4,880.0 5,757.5 6,330.1 6,451.0

Cost of goods sold (8,790.4) (10,449.6) (12,307.5) (13,777.6) Accounts receivable 2,001.8 2,303.4 2,717.0 3,046.0

SG&A (1,217.6) (1,504.9) (1,738.9) (1,949.4) Inventory 3,232.8 3,448.4 4,061.5 4,546.6

R&D 0.0 0.0 0.0 0.0 Other current assets 796.8 796.8 796.8 796.8

Other operating profit/(expense) 0.0 0.0 0.0 0.0 Total current assets 10,911.5 12,306.2 13,905.3 14,840.4

EBITDA 3,133.1 4,055.7 4,819.6 5,396.5 Net PP&E 5,549.8 6,400.8 6,953.1 7,258.1

Depreciation & amortization (501.7) (654.0) (752.9) (817.0) Net intangibles 109.5 99.8 90.1 80.4

EBIT 2,631.4 3,401.7 4,066.7 4,579.5 Total investments 4.7 4.7 4.7 4.7

Interest income 153.7 140.6 110.0 116.9 Other long-term assets 1,786.2 1,786.2 1,786.2 1,786.2

Interest expense (30.0) (30.0) (30.0) (30.0) Total assets 18,361.6 20,597.7 22,739.4 23,969.8

Income/(loss) from uncons. subs. (1.0) (1.0) (1.0) (1.0)

Others 132.8 147.0 237.0 207.0 Accounts payable 678.5 806.6 950.0 1,063.5

Pretax profits 2,886.9 3,658.3 4,382.8 4,872.5 Short-term debt 656.9 956.9 956.9 3,200.0

Income tax (532.1) (674.2) (788.9) (877.0) Other current liabilities 819.4 819.4 819.4 819.4

Minorities (0.2) (0.2) (0.2) (0.2) Total current liabilities 2,154.8 2,582.8 2,726.3 5,082.9

Long-term debt 3,117.0 3,200.0 3,200.0 0.0

Net income pre-preferred dividends 2,354.7 2,983.9 3,593.7 3,995.3 Other long-term liabilities 0.0 0.0 0.0 0.0

Preferred dividends 0.0 0.0 0.0 0.0 Total long-term liabilities 3,117.0 3,200.0 3,200.0 0.0

Net income (pre-exceptionals) 2,354.7 2,983.9 3,593.7 3,995.3 Total liabilities 5,271.8 5,782.8 5,926.3 5,082.9

Post-tax exceptionals 0.0 0.0 0.0 0.0

Net income 2,354.7 2,983.9 3,593.7 3,995.3 Preferred shares 0.0 0.0 0.0 0.0

Total common equity 13,074.1 14,798.9 16,797.1 18,870.7

EPS (basic, pre-except) (Rmb) 1.68 2.13 2.57 2.86 Minority interest 15.7 15.9 16.1 16.3

EPS (basic, post-except) (Rmb) 1.68 2.13 2.57 2.86

EPS (diluted, post-except) (Rmb) 1.68 2.13 2.57 2.86 Total liabilities & equity 18,361.6 20,597.7 22,739.4 23,969.8

DPS (Rmb) 0.90 1.14 1.37 1.53

Dividend payout ratio (%) 53.5 53.5 53.5 53.5 BVPS (Rmb) 9.35 10.58 12.01 13.49

Free cash flow yield (%) 0.5 2.8 3.5 4.9

Growth & margins (%) 12/15 12/16E 12/17E 12/18E Ratios 12/15 12/16E 12/17E 12/18E

Sales growth 13.5 21.5 18.0 12.1 CROCI (%) 22.4 22.5 24.0 23.7

EBITDA growth 20.1 29.4 18.8 12.0 ROE (%) 18.9 21.4 22.7 22.4

EBIT growth 20.4 29.3 19.6 12.6 ROA (%) 13.7 15.3 16.6 17.1

Net income growth 14.0 26.7 20.4 11.2 ROACE (%) 19.7 21.8 23.9 24.4

EPS growth 14.0 26.7 20.4 11.2 Inventory days 121.2 116.7 111.4 114.0

Gross margin 30.5 32.0 32.1 32.2 Receivables days 52.6 51.2 50.6 51.8

EBITDA margin 24.8 26.4 26.6 26.6 Payable days 23.8 25.9 26.0 26.7

EBIT margin 20.8 22.2 22.5 22.6 Net debt/equity (%) (8.5) (10.8) (12.9) (17.2)

Interest cover - EBIT (X) NM NM NM NM

Cash flow statement (Rmb mn) 12/15 12/16E 12/17E 12/18E Valuation 12/15 12/16E 12/17E 12/18E

Net income pre-preferred dividends 2,354.7 2,983.9 3,593.7 3,995.3

D&A add-back 501.7 654.0 752.9 817.0 P/E (analyst) (X) 17.5 19.9 16.5 14.8

Minorities interests add-back 0.2 0.2 0.2 0.2 P/B (X) 3.2 4.0 3.5 3.1

Net (inc)/dec working capital (773.6) (389.1) (883.2) (700.7) EV/EBITDA (X) 12.8 14.2 11.8 10.4

Other operating cash flow 176.1 (110.6) (80.0) (86.9) EV/GCI (X) 2.8 3.5 3.1 2.7

Cash flow from operations 2,259.1 3,138.4 3,383.5 4,024.8 Dividend yield (%) 3.1 2.7 3.2 3.6

Capital expenditures (2,037.8) (1,500.0) (1,300.0) (1,116.9)

Acquisitions 0.0 0.0 0.0 0.0

Divestitures 0.0 0.0 0.0 0.0

Others 643.2 115.2 84.6 91.5

Cash flow from investments (1,394.7) (1,384.8) (1,215.4) (1,025.4)

Dividends paid (common & pref) (1,103.7) (1,259.1) (1,595.6) (1,921.7)

Inc/(dec) in debt 862.4 383.0 0.0 (956.9)

Common stock issuance (repurchase) 0.0 0.0 0.0 0.0

Other financing cash flows (629.5) 0.0 0.0 0.0

Cash flow from financing (870.7) (876.1) (1,595.6) (2,878.5)

Total cash flow (6.3) 877.5 572.5 120.9 Note: Last actual year may include reported and estimated data.

Source: Company data, Goldman Sachs Research estimates.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 20

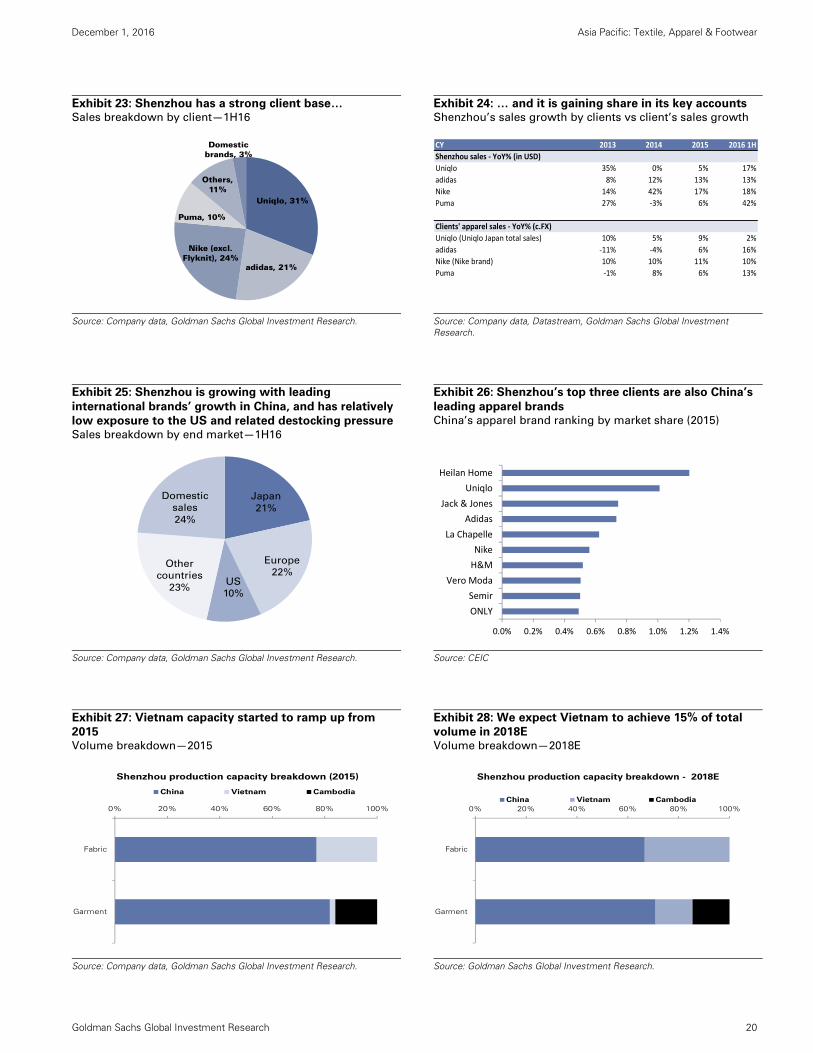

Exhibit 23: Shenzhou has a strong client base… Sales breakdown by client—1H16

Exhibit 24: … and it is gaining share in its key accounts Shenzhou’s sales growth by clients vs client’s sales growth

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Datastream, Goldman Sachs Global Investment Research.

Exhibit 25: Shenzhou is growing with leading

international brands’ growth in China, and has relatively

low exposure to the US and related destocking pressureSales breakdown by end market—1H16

Exhibit 26: Shenzhou’s top three clients are also China’s

leading apparel brands China’s apparel brand ranking by market share (2015)

Source: Company data, Goldman Sachs Global Investment Research.

Source: CEIC

Exhibit 27: Vietnam capacity started to ramp up from

2015 Volume breakdown—2015

Exhibit 28: We expect Vietnam to achieve 15% of total

volume in 2018E Volume breakdown—2018E

Source: Company data, Goldman Sachs Global Investment Research.

Source: Goldman Sachs Global Investment Research.

Uniqlo, 31%

adidas, 21%

Nike (excl. Flyknit), 24%

Puma, 10%

Others, 11%

Domestic brands, 3%

CY 2013 2014 2015 2016 1H

Shenzhou sales ‐ YoY% (in USD)

Uniqlo 35% 0% 5% 17%

adidas 8% 12% 13% 13%

Nike 14% 42% 17% 18%

Puma 27% ‐3% 6% 42%

Clients' apparel sales ‐ YoY% (c.FX)

Uniqlo (Uniqlo Japan total sales) 10% 5% 9% 2%

adidas ‐11% ‐4% 6% 16%

Nike (Nike brand) 10% 10% 11% 10%

Puma ‐1% 8% 6% 13%

Japan

21%

Europe

22%US

10%

Other

countries

23%

Domestic

sales

24%

0.0% 0.2% 0.4% 0.6% 0.8% 1.0% 1.2% 1.4%

ONLY

Semir

Vero Moda

H&M

Nike

La Chapelle

Adidas

Jack & Jones

Uniqlo

Heilan Home

0% 20% 40% 60% 80% 100%

Fabric

Garment

Shenzhou production capacity breakdown (2015)

China Vietnam Cambodia

0% 20% 40% 60% 80% 100%

Fabric

Garment

Shenzhou production capacity breakdown - 2018E

China Vietnam Cambodia

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 21

Exhibit 29: Strong volume growth, on top of healthy ASP trend from product mix

enhancement, support solid growth from 2015 ASP vs volume growth, yoy

Source: Company data, Goldman Sachs Global Investment Research.

Exhibit 30: With lower labor and utility costs, we estimate costs in Vietnam can be at least

20% lower than that in China Cost breakdown analysis—Vietnam vs China

Source: Company data, Goldman Sachs Global Investment Research.

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2010 2011 2012 2013 2014 2015 2016E 2017E 2018E

ASP yoy Shipment yoy

‐

5

10

15

20

25

30

35

40

Yarn

Accessories

Other raw

materials

Labour

Utility

Depreciation

Others

Current (mostly China) In Vietnam

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 22

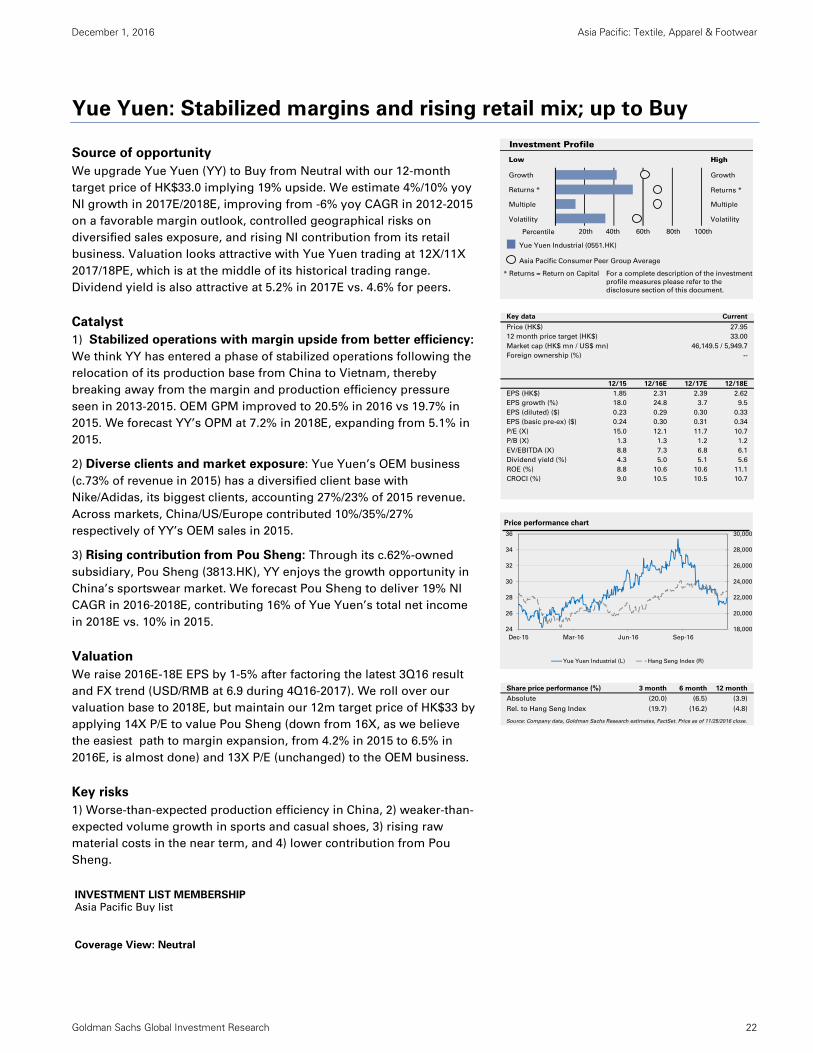

Yue Yuen: Stabilized margins and rising retail mix; up to Buy

Source of opportunity

We upgrade Yue Yuen (YY) to Buy from Neutral with our 12-month

target price of HK$33.0 implying 19% upside. We estimate 4%/10% yoy

NI growth in 2017E/2018E, improving from -6% yoy CAGR in 2012-2015

on a favorable margin outlook, controlled geographical risks on

diversified sales exposure, and rising NI contribution from its retail

business. Valuation looks attractive with Yue Yuen trading at 12X/11X

2017/18PE, which is at the middle of its historical trading range.

Dividend yield is also attractive at 5.2% in 2017E vs. 4.6% for peers.

Catalyst

1) Stabilized operations with margin upside from better efficiency:

We think YY has entered a phase of stabilized operations following the

relocation of its production base from China to Vietnam, thereby

breaking away from the margin and production efficiency pressure

seen in 2013-2015. OEM GPM improved to 20.5% in 2016 vs 19.7% in

2015. We forecast YY’s OPM at 7.2% in 2018E, expanding from 5.1% in

2015.

2) Diverse clients and market exposure: Yue Yuen’s OEM business

(c.73% of revenue in 2015) has a diversified client base with

Nike/Adidas, its biggest clients, accounting 27%/23% of 2015 revenue.

Across markets, China/US/Europe contributed 10%/35%/27%

respectively of YY’s OEM sales in 2015.

3) Rising contribution from Pou Sheng: Through its c.62%-owned

subsidiary, Pou Sheng (3813.HK), YY enjoys the growth opportunity in

China’s sportswear market. We forecast Pou Sheng to deliver 19% NI

CAGR in 2016-2018E, contributing 16% of Yue Yuen’s total net income

in 2018E vs. 10% in 2015.

Valuation

We raise 2016E-18E EPS by 1-5% after factoring the latest 3Q16 result

and FX trend (USD/RMB at 6.9 during 4Q16-2017). We roll over our

valuation base to 2018E, but maintain our 12m target price of HK$33 by

applying 14X P/E to value Pou Sheng (down from 16X, as we believe

the easiest path to margin expansion, from 4.2% in 2015 to 6.5% in

2016E, is almost done) and 13X P/E (unchanged) to the OEM business.

Key risks

1) Worse-than-expected production efficiency in China, 2) weaker-than-

expected volume growth in sports and casual shoes, 3) rising raw

material costs in the near term, and 4) lower contribution from Pou

Sheng.

INVESTMENT LIST MEMBERSHIP

Asia Pacific Buy list

Coverage View: Neutral

Growth

Returns *

Multiple

Volatility Volatility

Multiple

Returns *

Growth

Investment Profile

Low High

Percentile 20th 40th 60th 80th 100th

* Returns = Return on Capital For a complete description of the investment

profile measures please refer to the

disclosure section of this document.

Yue Yuen Industrial (0551.HK)

Asia Pacific Consumer Peer Group Average

Key data Current

Price (HK$) 27.95

12 month price target (HK$) 33.00

Market cap (HK$ mn / US$ mn) 46,149.5 / 5,949.7

Foreign ownership (%) --

12/15 12/16E 12/17E 12/18E

EPS (HK$) 1.85 2.31 2.39 2.62

EPS growth (%) 18.0 24.8 3.7 9.5

EPS (diluted) ($) 0.23 0.29 0.30 0.33

EPS (basic pre-ex) ($) 0.24 0.30 0.31 0.34

P/E (X) 15.0 12.1 11.7 10.7

P/B (X) 1.3 1.3 1.2 1.2

EV/EBITDA (X) 8.8 7.3 6.8 6.1

Dividend yield (%) 4.3 5.0 5.1 5.6

ROE (%) 8.8 10.6 10.6 11.1

CROCI (%) 9.0 10.5 10.5 10.7

18,000

20,000

22,000

24,000

26,000

28,000

30,000

24

26

28

30

32

34

36

Dec-15 Mar-16 Jun-16 Sep-16

Price performance chart

Yue Yuen Industrial (L) Hang Seng Index (R)

Share price performance (%) 3 month 6 month 12 month

Absolute (20.0) (6.5) (3.9)

Rel. to Hang Seng Index (19.7) (16.2) (4.8)

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 11/25/2016 close.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 23

*Closing price as of Nov 30th, 2016

Yue Yuen Industrial: Summary financials

Profit model ($ mn) 12/15 12/16E 12/17E 12/18E Balance sheet ($ mn) 12/15 12/16E 12/17E 12/18E

Total revenue 8,434.9 8,375.4 8,616.7 9,033.5 Cash & equivalents 1,046.6 1,503.9 1,632.4 1,761.4

Cost of goods sold (6,462.6) (6,276.0) (6,424.2) (6,697.1) Accounts receivable 1,413.8 1,403.8 1,444.2 1,514.1

SG&A (1,302.8) (1,300.8) (1,356.6) (1,429.6) Inventory 1,254.2 1,217.9 1,246.7 1,299.7

R&D (157.1) (156.0) (160.5) (168.3) Other current assets 22.2 22.2 22.2 22.2

Other operating profit/(expense) (83.8) (97.4) (87.3) (87.9) Total current assets 3,736.7 4,147.8 4,345.5 4,597.4

EBITDA 678.3 814.9 875.7 955.7 Net PP&E 1,945.2 2,018.1 2,039.6 2,058.2

Depreciation & amortization (249.7) (269.7) (287.7) (305.1) Net intangibles 375.0 367.5 359.9 352.3

EBIT 428.5 545.2 588.0 650.6 Total investments 865.9 937.1 1,013.9 1,097.0

Interest income 9.3 10.0 14.4 15.7 Other long-term assets 341.6 341.6 341.6 341.6

Interest expense (19.4) (20.5) (24.2) (24.2) Total assets 7,264.5 7,812.1 8,100.5 8,446.5

Income/(loss) from uncons. subs. 82.2 71.1 76.8 83.1

Others (16.4) 15.0 0.0 0.0 Accounts payable 1,482.0 1,439.2 1,473.2 1,535.8

Pretax profits 484.2 620.8 655.1 725.1 Short-term debt 433.2 433.2 433.2 433.2

Income tax (66.3) (87.9) (95.9) (107.9) Other current liabilities 76.7 76.7 76.7 76.7

Minorities (27.7) (45.3) (51.2) (61.0) Total current liabilities 1,991.9 1,949.1 1,983.1 2,045.7

Long-term debt 370.0 720.0 720.0 720.0

Net income pre-preferred dividends 390.2 487.6 507.9 556.2 Other long-term liabilities 36.3 36.3 36.3 36.3

Preferred dividends 0.0 0.0 0.0 0.0 Total long-term liabilities 406.3 756.3 756.3 756.3

Net income (pre-exceptionals) 390.2 487.6 507.9 556.2 Total liabilities 2,398.3 2,705.5 2,739.5 2,802.1

Post-tax exceptionals 0.0 0.0 0.0 0.0

Net income 390.2 487.6 507.9 556.2 Preferred shares 0.0 0.0 0.0 0.0

Total common equity 4,498.6 4,693.6 4,896.8 5,119.3

EPS (basic, pre-except) ($) 0.24 0.30 0.31 0.34 Minority interest 367.6 413.0 464.2 525.2

EPS (basic, post-except) ($) 0.24 0.30 0.31 0.34

EPS (diluted, post-except) ($) 0.23 0.29 0.30 0.33 Total liabilities & equity 7,264.5 7,812.1 8,100.5 8,446.5

DPS ($) 0.15 0.18 0.19 0.20

Dividend payout ratio (%) 64.9 60.0 60.0 60.0 BVPS ($) 2.73 2.85 2.97 3.11

Free cash flow yield (%) 6.2 6.3 6.8 7.2

Growth & margins (%) 12/15 12/16E 12/17E 12/18E Ratios 12/15 12/16E 12/17E 12/18E

Sales growth 5.3 (0.7) 2.9 4.8 CROCI (%) 9.0 10.5 10.5 10.7

EBITDA growth 5.2 20.1 7.5 9.1 ROE (%) 8.8 10.6 10.6 11.1

EBIT growth 5.0 27.2 7.9 10.6 ROA (%) 5.4 6.5 6.4 6.7

Net income growth 17.9 25.0 4.2 9.5 ROACE (%) 9.1 11.6 11.8 12.6

EPS growth 18.0 25.0 4.2 9.5 Inventory days 72.7 71.9 70.0 69.4

Gross margin 23.4 25.1 25.4 25.9 Receivables days 61.0 61.4 60.3 59.8

EBITDA margin 8.0 9.7 10.2 10.6 Payable days 79.8 84.9 82.7 82.0

EBIT margin 5.1 6.5 6.8 7.2 Net debt/equity (%) (5.0) (6.9) (8.9) (10.8)

Interest cover - EBIT (X) 42.5 51.9 60.0 76.0

Cash flow statement ($ mn) 12/15 12/16E 12/17E 12/18E Valuation 12/15 12/16E 12/17E 12/18E

Net income pre-preferred dividends 390.2 487.6 507.9 556.2

D&A add-back 249.7 269.7 287.7 305.1 P/E (analyst) (X) 15.0 12.1 11.7 10.7

Minorities interests add-back 27.7 45.3 51.2 61.0 P/B (X) 1.3 1.3 1.2 1.2

Net (inc)/dec working capital 197.0 3.4 (35.2) (60.2) EV/EBITDA (X) 8.8 7.3 6.8 6.1

Other operating cash flow (77.0) (71.1) (76.8) (83.1) EV/GCI (X) 0.8 0.8 0.7 0.7

Cash flow from operations 787.6 734.8 734.9 779.0 Dividend yield (%) 4.3 5.0 5.1 5.6

Capital expenditures (398.1) (335.0) (301.6) (316.2)

Acquisitions 0.0 0.0 0.0 0.0

Divestitures 0.0 0.0 0.0 0.0

Others 0.0 0.0 0.0 0.0

Cash flow from investments (398.1) (335.0) (301.6) (316.2)

Dividends paid (common & pref) (242.8) (292.6) (304.8) (333.7)

Inc/(dec) in debt (143.0) 350.0 0.0 0.0

Common stock issuance (repurchase) 0.0 0.0 0.0 0.0

Other financing cash flows 73.5 0.0 0.0 0.0

Cash flow from financing (312.3) 57.4 (304.8) (333.7)

Total cash flow 77.2 457.3 128.5 129.1 Note: Last actual year may include reported and estimated data.

Source: Company data, Goldman Sachs Research estimates.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 24

Exhibit 31: Optimizing production in China still continues, but margin impact stabilized Production volume change by country

Source: Company data.

Exhibit 32: GPM/OPM has bottomed out and should

improve on better efficiency and geographical mix Yue Yuen’s OEM GPM and OPM

Exhibit 33: Contribution from Pou Sheng increasing to

16% of YY’s NI in 2018E Pou Sheng’s contribution

Source: Company data, Goldman Sachs Global Investment Research.

Source: Company data, Goldman Sachs Global Investment Research.

Exhibit 34: We use 13X PE to value the OEM business and 14X PE to value Pou Sheng

SoTP valuation

Source: Company data, Goldman Sachs Global Investment Research.

% of volume 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

PRC 34% 29% 29% 32% 26% 25% 25% 25% 25% 22% 22% 19%Vietnam 34% 39% 39% 39% 39% 41% 43% 42% 42% 43% 43% 46%Indonesia 31% 31% 31% 28% 34% 33% 31% 32% 32% 33% 33% 33%Others 1% 1% 1% 1% 1% 1% 1% 1% 1% 2% 2% 2%Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Volume (mn pairs) 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

PRC 28.4 22.0 23.8 22.8 20.4 18.6 21.2 18.1 21.5 17.6 18.8 13.1 Vietnam 28.4 29.6 32.0 27.6 30.5 30.5 36.3 30.4 36.2 34.5 36.8 32.6 Indonesia 25.9 23.6 25.4 19.7 26.6 24.6 26.3 23.1 27.6 26.5 28.2 23.2 Others 0.8 0.8 0.8 0.7 0.8 0.7 0.8 0.7 0.9 1.6 1.7 1.4 Total 83.4 76.0 82.0 70.8 78.3 74.5 84.6 72.3 86.1 80.2 85.5 70.4

Volume YoY 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

PRC -28% -15% -11% -21% 5% -5% -11% -27%Vietnam 8% 3% 13% 10% 18% 13% 1% 7%Indonesia 3% 4% 4% 18% 4% 8% 7% 0%Others -6% -2% 3% 2% 10% 115% 102% 95%Total -6% -2% 3% 2% 10% 8% 1% -3%

=

-

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

16.0%

17.0%

18.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

25.0%

OEM's GPM OEM's OPM (RHS)

-5.5%

0.9%

10.2%

13.2%15.1%

16.4%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

2013 2014 2015 2016E 2017E 2018E

Pou Sheng as % of YY's NI

NI breakdown PE (x) EPS (HK$) Implied value (HK$)OEM 83.7% 13 2.19 27.4 Pou Sheng 16.3% 14 0.43 6.0

TP (HK$) 33.0

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 25

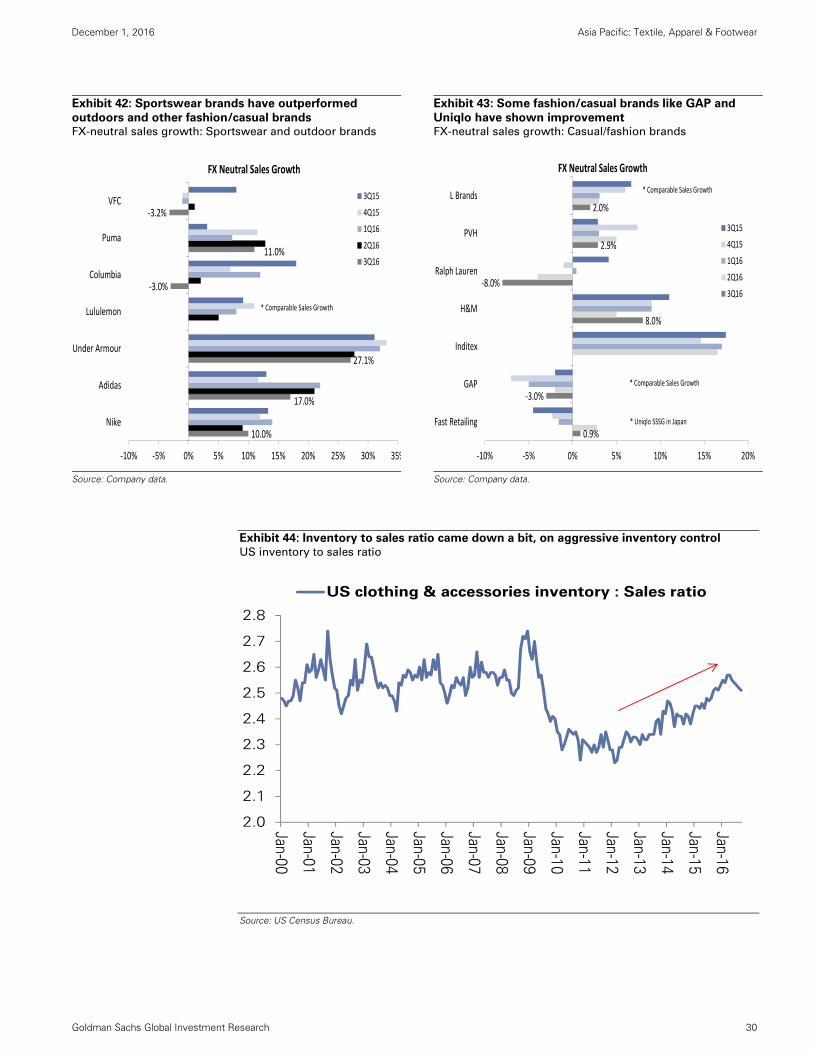

Eclat: Down to Neutral as EPS recovery appears priced in

What happened

We downgrade Eclat to Neutral from Buy. While EPS growth is likely to

recover from 4Q16 at 4% yoy vs -23% in 9M16, we believe the

magnitude of this recovery will be smaller than what we had previously

anticipated (15%), thanks to uncertainties in global trade and US

retailers’ destocking. Fundamentally, we still see solid trend for ASP,

but lower visibility on volume growth. We lower our 2016-18E EPS by

6-17% to reflect weaker sales/margins. Accordingly, we cut our 12m

target price from NT$410 to NT$340, based on our lower earnings

estimates and a lower target multiple of 18x (20x previously) to reflect

its slower growth (20% NI CAGR in 2016-18E vs previous estimate of

27%). We also roll over our valuation base from average 2017 and 2018

PE to 2018 PE. Since we upgraded the stock to Buy on Aug 7th, 2015, its

share price is down 25% vs the TWSE up 9%. We attribute this to

investors’ concerns on inventory control and weak traffic at US

retailers.

Current view

1) ASP growth is likely to remain solid on contribution from new

materials backed by superior R&D on stretchable functional products.

2) Vertical integration by adopting more fabric internally allows

Eclat to strive for value growth given its superior fabric development

track record. More services provided in the supply chain and

production efficiency also help realize clients’ design ideas into

products and strengthen the relationship with clients. Eclat’s market

share in US apparel imports has more than doubled in the past five

years. 3) We see headwinds in volume growth as retail clients’

restocking demand remains slow. Retail clients still represented c.25%

of Eclat’s 3Q16 sales although client mix is improving (c.27% retail

clients in 1H16 and c.35% in 2015). 4) If US brand/retailers continue destocking before a clearer picture emerges on trade policies, volume

growth for Eclat would be hurt as direct orders from the US represent c.

52% of total sales and indirect orders could be even higher.

Valuation

We cut our 2016-18E sales by 3-12% and net margins by 0.5-1pp to

factor in lower demand from US retailer clients. Valuation wise, we roll

over our valuation base to 2018E and cut our target multiple from 20X

to 18X on the back of its weaker EPS outlook and on a par with

Shenzhou’s multiple.

Key risks

Risks: 1) Stronger/weaker restocking demand from retail clients, 2)

more/less adoption for new materials, 3) new clients, 4) better/worse

vertical integration, 5) FX.

INVESTMENT LIST MEMBERSHIP

Neutral

Coverage View: Neutral

Growth

Returns *

Multiple

Volatility Volatility

Multiple

Returns *

Growth

Investment Profile

Low High

Percentile 20th 40th 60th 80th 100th

* Returns = Return on Capital For a complete description of the investment

profile measures please refer to the

disclosure section of this document.

Eclat Textile Co. (1476.TW)

Asia Pacific Consumer Peer Group Average

Key data Current

Price (NT$) 325.50

12 month price target (NT$) 340.00

Market cap (NT$ mn / US$ mn) 87,555.3 / 2,752.5

Foreign ownership (%) 42.4

12/15 12/16E 12/17E 12/18E

EPS (NT$) 15.52 13.18 16.26 18.84

EPS growth (%) 39.0 (15.1) 23.4 15.9

EPS (diluted) (NT$) 15.52 13.18 16.26 18.84

EPS (basic pre-ex) (NT$) 15.52 13.18 16.26 18.84

P/E (X) 27.8 24.7 20.0 17.3

P/B (X) 9.8 5.8 5.2 4.6

EV/EBITDA (X) 20.5 15.2 13.3 11.4

Dividend yield (%) 2.4 2.8 3.5 4.1

ROE (%) 39.3 26.4 27.3 28.2

CROCI (%) 37.2 24.7 25.5 25.8

7,600

8,100

8,600

9,100

9,600

10,100

250

300

350

400

450

500

Dec-15 Mar-16 Jun-16 Sep-16

Price performance chart

Eclat Textile Co. (L) Taiwan SE Weighted Index (R)

Share price performance (%) 3 month 6 month 12 month

Absolute (17.9) (5.7) (24.4)

Rel. to Taiwan SE Weighted Index (19.4) (12.9) (31.9)

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 11/30/2016 close.

December 1, 2016 Asia Pacific: Textile, Apparel & Footwear

Goldman Sachs Global Investment Research 26

*Closing price as of Nov 30th, 2016

Eclat Textile Co.: Summary financials