asian development bank ppa: nep 18030 project … · ppar – project performance audit report ta...

TRANSCRIPT

ASIAN DEVELOPMENT BANK PPA: NEP 18030

PROJECT PERFORMANCE AUDIT REPORT

ON THE

FIFTH AND SIXTH POWER PROJECTS (Loans 670 and 708-NEP[SF])

IN

NEPAL

December 1999

CURRENCY EQUIVALENTS Currency Unit – Nepalese Rupee/s (NRe/NRs)

At Appraisal

Fifth Power Project (Loan 670-NEP)

(October 1983) Sixth Power Project (Loan 708-NEP)

(October 1984)

NRe1.00 = $0.068 NRe1.00 = $0.058 $1.00 = NRs14.800 $1.00 = NRs17.300

At Project Completion

Fifth Power Project (November 1997)

Sixth Power Project (August 1996)

At Operations Evaluation (November 1999)

NRe1.00 = $0.018 NRe1.00 = $0.020 NRe1.00 = $0.014 $1.00 = NRs55.750 $1.00 = NRs49.480 $1.00 = NRs70.1

ABBREVIATIONS

ADB – Asian Development Bank EIRR – economic internal rate of return FIRR – financial internal rate of return NEA – Nepal Electricity Authority OEM – Operations Evaluation Mission PCR – project completion report PPAR – project performance audit report TA – technical assistance WTP – willingness to pay

NOTES

(i) The fiscal year (FY) of the Government agencies and the Nepal Electricity Authority ends on 15 July.

(ii) In this report, "$" refers to US dollars.

WEIGHTS AND MEASURES

A (ampere) - unit of current V (volt) - unit of voltage kV (kilovolt) - 1,000 volts W (watt) - unit of power kW (kilowatt) - 1,000 watts MW (megawatt) - 1,000,000 watts Wh (watt-hour) - unit of energy kWh (kilowatt- hour) - 1,000 Wh MVA (megavolt-ampere) - 1,000,000 volt-amperes

Operations Evaluation Office, PE-543

CONTENTS

Page BASIC DATA ii EXECUTIVE SUMMARY iv MAPS Error! Bookmark not defined. I. BACKGROUND 1

A. Rationale 1 B. Formulation 1 C. Objectives and Scope at Appraisal 1 D. Financing Arrangements 2 E. Completion 3 F. Operations Evaluation 3

II. IMPLEMENTATION PERFORMANCE 1

A. Design 1 B. Contracting, Construction, and Commissioning 2 C. Organization and Management 3 D. Actual Cost and Financing 4 E. Implementation Schedule 4 F. Technical Assistance 5 G. Compliance with Loan Covenants 5

III. PROJECT RESULTS 7

A. Operational Performance 7 B. Institutional Development 9 C. Performance of Asian Development Bank 9 D. Financial Performance 10 E. Economic and Financial Reevaluation 10 F. Socioeconomic Results 11 G. Gender and Development 12 H. Environmental Impact and Control 12 I. Sustainability 13

IV. KEY ISSUES FOR THE FUTURE 1 V. CONCLUSIONS 1

A. Overall Assessment 1 B. Lessons Learned 1 C. Follow-Up Actions 2

APPENDIXES 3

BASIC DATA Fifth Power Project (Loan 670-NEP[SF])

PROJECT PREPARATION/INSTITUTION BUILDING TA No. Project Title Type Amount ($) Approval Date 478-NEP Formulation of Fifth Power PPTA1 50,000 23 Aug 1982 KEY PROJECT DATA ($ million)

As Per ADB

Loan Documents

Actual Total Project Cost 25.70 23.75 Foreign Exchange Cost 18.40 23.10 Local Currency Cost 7.30 0.65 ADB Loan Amount/Utilization ($) 20.00 23.75 (SDR million) 18.88 17.73 ADB Loan Amount/Cancellation ($) — 1.60 (SDR million) 1.15 KEY DATES Expected Actual Fact-Finding 14–18 Mar 1983 Appraisal 28 May–9 Jun 19832 Loan Negotiations 7–10 Nov 1983 Board Approval 14 Dec 1983 Loan Agreement 19 Dec 1983 Loan Effectiveness 19 Mar 1984 18 Sep 1984 First Disbursement 30 Jul 1985 Project Completion 31 Mar 1988 31 Dec 1996 Loan Closing 31 Dec 1988 23 Jun 1997 Months (Effectiveness to Completion) 42 147 KEY PERFORMANCE INDICATORS (%)

Appraisal (1983)

PCR (1997)

PPAR (1999)

Economic Internal Rate of Return 13.0 29.2 15.3 Financial Internal Rate of Return 12.3 8.3 7.7 Borrower The Kingdom of Nepal Executing Agency Nepal Electricity Authority MISSION DATA Type of Mission No. of Missions Person-Days Fact-Finding 1 5 Appraisal 1 14 Project Administration - Special Loan Administration 1 4 - Review 12 62 - Project Completion Review 1 9 Operations Evaluation 1 34

ADB = Asian Development Bank, PCR = project completion report, PPAR = project performance audit report. 1 Project preparatory technical assistance. 2 A Follow-Up Mission was fielded from 28 September to 6 October 1983.

iii

BASIC DATA Sixth Power Project (Loan 708-NEP[SF])

KEY PROJECT DATA ($ million)

As Per ADB

Loan Documents

Actual Total Project Cost 41.70 53.80 Foreign Exchange Cost 28.60 36.98 Local Currency Cost 13.10 16.82 ADB Loan Amount/Utilization ($) 28.10 37.05 (SDR million) 28.13 27.47 ADB Loan Amount/Cancellation ($) — 0.99 (SDR million) — 0.66

KEY DATES Expected Actual

Appraisal 14-28 Jul 1984 Loan Negotiations 11-13 Oct 1984 Board Approval 20 Nov 1984 Loan Agreement 17 Jan 1986 Loan Effectiveness 17 Apr 1986 15 Apr 1986 First Disbursement 25 Jun 1986 Project Completion 30 Nov 1988 26 May 1996 Loan Closing 30 Jun 1989 16 Nov 1995 Months (Effectiveness to Completion) 32 121 KEY PERFORMANCE INDICATORS (%)

Appraisal (1984)

PCR (1996)

PPAR (1999)

Economic Internal Rate of Return n.c.1 12.4-13.35 15.3 Financial Internal Rate of Return n.c. 4.2 7.7 Borrower The Kingdom of Nepal Executing Agency Nepal Electricity Authority MISSION DATA Type of Missions No. of Missions Person-Days Fact-Finding 1 36 Appraisal 1 90 Project Administration - Review 12 46 - Project Completion Review 1 26 Operations Evaluation 1 34

1 n.c. = overall rate of return was not calculated.

EXECUTIVE SUMMARY

Asian Development Bank (ADB) assistance for the Fifth and Sixth Power projects in

Nepal were designed to meet increased demand for electricity (outside the Kathmandu valley) until the mid-1990s, improve the quality and reliability of power supply, reduce energy losses, and reduce oil imports, so as to support economic growth and improve the standard of living, particularly in the rural areas. The principal components of the Fifth Power Project (Fifth Project) as approved in 1983 comprised: Part A (i) construction of a 132-kilovolt (kV) line and substations, (ii) subtransmission (33kV) distribution system rehabilitation and extension; (iii) consulting services for project implementation, and staff training in construction work; and Part B (i) institution building of the Nepal Electricity Authority, Executing Agency (EA) of the Project. On the other hand, the follow-up Sixth Power Project (Sixth Project) was directed at transferring full energy output from the 69-megawatt (MW) Marsyangdi hydropower station to the main 132 kV grid, in addition to, reinforcing and expanding the subtransmission and distribution networks in secondary towns and rural areas adjacent to the main grid.

The rationale and mix of components for both projects were sound. During project appraisal, there was a need to transmit the hydropower generated in the central area to the Terai region to replace imported power from India and power derived from isolated diesel sets. The 132 kV extensions and the 33 kV lines under the Fifth Project provided the means to transmit hydropower and to supply load centers which earlier utilized other modes of power generation. Rehabilitation of the existing distribution system and the increased power supply to more rural areas under the Sixth Project attracted additional consumers and established the potential to enhance the living standards in those areas. Further to this, several components were modified based on reassessments of evolving sector requirements. In October 1991, envisaged training assistance under Part B of the Fifth Project was modified to include the installation and commissioning of a computerized billing system. A year later, the Project was again modified to provide consultant inputs for preparing the Kali Gandaki "A" Hydropower Project (Part C). Correspondingly, an added objective to the Sixth Project following a change in scope approved in November 1990, was to expand the hydropower generating capacity in Marsyangdi.

Actual ADB assistance for both projects amounted to $60.8 million equivalent. The cost of the Fifth Project at appraisal was estimated at $25.7 million of which $18.4 million was in foreign currency. To meet the foreign currency requirement, ADB provided a loan equivalent to SDR1 18.9 million ($20 million) in December 1983. At loan closing, the resulting dollar equivalent of the loan was about $25.4 million, of which about $23.8 million was disbursed. The cost of the Sixth Project at appraisal totaled to $41.7 million equivalent, of which $28.6 million was in foreign currency. During project implementation, the value of the dollar again depreciated against the SDR, and at loan closure, the resulting dollar equivalent of the loan was about $38.0 million, of which about $37.0 million had been disbursed. Part A of the Fifth Project, scheduled to be completed by April 1988, was completed only in September 1991, more than three years after the target completion date. Part B was completed ahead of schedule, but only the first of three phases was actually carried out. The additional work under Part C was completed only in December 1996. Submission of the final

1 special drawing rights.

v

detailed engineering design for Kali Gandaki was submitted at the end of February 1997 for a further 27 months. The Sixth Project was significantly delayed by about eight years. Implementation schedules are detailed in Appendix 1. Despite the significant delays, overall implementation of the two projects can be considered successful. A notable exception is the commissioning of certain facilities, especially the substations, which was poorly carried out. Construction quality was generally good with the exception of the work of the contractor for the 33 kV substations under the Fifth Project and four of the nine contractors for the Tatopani hydropower extensions under the Sixth Project. The Government complied with majority of the loans' covenants. At loan closing, the exceptions covered two common conditions: (i) a reduction on energy losses to 20 percent or less, and (ii) an annual rate of return of not less than 6 percent. A rate of return of 8.5 percent had been achieved (in FY1995 following project completion), but electricity losses continue to remain above 20 percent through FY1999.

Both projects generated economic opportunities within areas served by the transmission and distribution network. Increased access to electricity allowed cottage-type industries to develop and helped improve living standards (e.g., use of household appliances). The joint economic internal rate of return (based on a time slice analysis) for the two projects is recalculated at 15.3 percent. This is lower than estimates at project appraisal and completion due to a scaled down benefit stream focussing on the spatial location of beneficiary users connected to the grid in the Terai area in both Eastern and Western regions. The reestimated financial internal rate of return is also lower due to uneconomical tariffs charged for power sales, combined with a reduced scale of beneficiary user groups. In addition, the longer-than-expected completion period contributed to reducing both internal rates of return relative to the appraisal estimates.

Sustainability of project facilities under the Fifth and Sixth projects depends primarily on the (i) financial and technical adequacy of future maintenance and upgrading efforts, principally of the subtransmission and distribution facilities; and (ii) general level of maintenance at some, if not all, of the 33-11 kV, substations which is currently very substandard. At present, the Operations Evaluation Mission considers the physical sustainability of the transmission poles and substations as very much in doubt. Lack of tools and maintenance manuals, and the inadequate or dangerous repair techniques all further contribute to compromising the integrity of the transmission system. Overall, the sustainability of the current network, therefore, appears weak in several respects, but it is not beyond redress if given a greater allocation of maintenance effort. In retrospect, the two projects were successfully implemented and the transmission and distribution system is operational, although with severe constraints in the subtransmission gear. Both projects have generated positive socioeconomic impacts and an acceptable economic internal rate of return even though financially, the results were less robust. Keeping in mind the aforementioned sustainability risks related to several ADB-funded components of the transmission network, the Fifth and Sixth projects are nevertheless rated generally successful on account of the significant economic benefits generated by an adequate power supply for a rapidly growing consumer base.

Project experience demonstrated the need to constantly monitor maintenance efforts of the EA once a project is completed. This issue has already been emphasized in past observations with regard to ADB-funded projects, but both ADB and the EA must still exercise greater vigilance in ensuring strict adherence to minimum maintenance standards and practices as a precondition for further investments in the expansion of the system. Another lesson is the necessity for the EA to have a more rigorous accountability in carrying out rural electrification

vi

programs as evidenced by the absence of adequate monitoring data on project achievements for this major component of the Sixth Project. Equally important is the application of an objective criteria of either cost-effectiveness considerations and/or economic feasibility for the socioeconomic evaluation of rural electrification schemes.

I. BACKGROUND

A. Rationale

1. The rationale for the two projects was sound. At appraisal, there was a need to extend hydropower generated in the central area to the areas of the Terai to replace power imported from India and from isolated diesel sets. The 132-kilovolt (kV) extensions under the Fifth Project provided the means to transmit hydropower, the 33 kV lines supplied the load centers previously utilizing other modes of generation, and the rehabilitation of the existing distribution system and the increased power supply to more rural areas pursued under the Sixth Project attracted additional consumers and established a potential to enhance the living standards in those areas. 2. The projects were designed to help meet the increasing demand for electricity in the country until the mid-1990s, improve the quality and reliability of the power supply, reduce energy losses, and reduce oil imports, with the view to supporting economic growth and improving the standard of living, particularly in the rural areas.

B. Formulation

3. The Fifth Project was designed in response to an assessment carried out by Nepal Electricity Authority’s (NEA’s) predecessor, the Electricity Department,1 which felt the need to extend the transmission and distribution network of the national grid to reach out to the outlying areas of the country, following an initial significant buildup of generation capacity, initially earmarked for the Kathmandu Valley area. The projects were formulated in clear recognition of the need to expand the transmission and distribution system for development of the grid.2

C. Objectives and Scope at Appraisal

4. The overall objective of the Fifth Power Project was to (i) reinforce and expand the transmission and distribution network in main load centers outside the Kathmandu Valley, (ii) reduce losses and improve the quality of supply, and (iii) meet the load forecast up to 1993.

(i) Transmission and distribution design. For the procurement and installation of the transmission and distribution facilities, Asian Development Bank (ADB)-funded consultants prepared an extensive design manual complete with a listing of major equipment. For the rehabilitation of four urban distribution systems and

1 The Nepal Electricity Authority (NEA) was founded in 1985 by merging the Electricity Department and Nepal

Electricity Corporation. 2 It should be noted that the preparatory technical assistance (TA) project did not formally provide for a least-cost

master plan design for expansion of the national network.

2

establishment of a new distribution system (at Damak), the consultants also prepared a satisfactory design report of the proposed work and a market study so as to estimate the growth to be met by the installed facilities. A review of these reports indicates that the designs were generally well-prepared and suitable for the intended works.

(ii) Computerized billing component. This addressed two of the objectives of the

Project: reducing nontechnical systems losses and improving the quality of electricity supply.

(iii) Engineering services for Kali Gandaki “A” hydroelectric project. The ADB-

financed component of the Kali Gandaki hydropower generation facility consisted of the preparation of designs and tender documents for the generating plant.

5. The main objectives of the Sixth Power Project were to (i) transfer the full output of energy from the 69 megawatt Marsyangdi hydropower station to the main 132 kV grid, and (ii) reinforce and expand the subtransmission and distribution networks in various secondary towns and rural areas adjacent to the main grid. Subsequently, ADB approved a change in scope of Part B to include two additional components: the 33-kilowatt Lahan-Jaljale transmission line (approved in February 1989) and addition of four 250 kW generating units at the Tatopani hydropower station, including an expansion of the local distribution network and connection to the main grid (approved in November 1990). An added objective, following a change in scope approved in November 1990, was to expand the hydropower generating capacity at Marsyangdi. 6. The Rural Electrification Program under the Sixth Project consisted of six rural electrification schemes in the Terai, targeting approximately 500 villages in the region.

D. Financing Arrangements

7. The overall project cost of the Fifth Power Project was estimated at $25.70 million, of which $18.40 million was in foreign currency and $7.30 million equivalent in local currency3 (Appendix 1). To meet the foreign currency requirement, ADB approved a loan of SDR18.88 million ($20 million) in December 1983. At the closure of the accounts on 23 June 1997, the resulting dollar equivalent of the loan was about $25.4 million, of which about $23.8 million had been disbursed and $1.60 million (SDR1.15 million) was canceled. The Sixth Power Project was estimated to cost $41.70 million equivalent, of which $28.60 million was in foreign currency and $13.10 million equivalent in local currency. During project implementation, the value of the dollar depreciated against the SDR, and at loan closure in November 1995 the dollar equivalent of the loan was about $38.0 million, of which about $37.05 million had been disbursed and about $0.99 million (equal to SDR0.66 million) was canceled. Previous ADB involvement in the development of the national electricity sector amounted to $55.3 million in loans, and $3.81 million in technical assistance (TAs). Subsequent to the Fifth and Sixth Power projects, ADB extended further loans to the NEA under the Seventh Power Project. The total sector assistance to date amounts to $189.5 million.

3 As the NEA did not provide the local cost it actually disbursed, actual local cost includes only the portion disbursed

by ADB under the loan.

3

E. Completion

8. Part A of the Fifth Power Project was scheduled to be completed by March 1988, but was significantly delayed. The final component was completed in October 1991, more than three years after its target completion date. Part B was completed ahead of schedule, but only the first of three phases scheduled for completion was actually carried out. The consulting services originally allocated for the implementation of all three phases of the Project were thus used for the implementation of the pilot system alone. Due to appreciable changes in the scope of services, the work planned for Part C was completed only in December 1996 and the final version of the detailed engineering design for Kali Gandaki was submitted at the end of February 1997, representing an additional 27-months delay. The Sixth Project was delayed by eight years (Appendix 2). 9. The project completion reports (PCRs) were prepared by ADB’s Infrastructure Energy Division (West) and circulated to the Board in August 1996 (Sixth Power Project) and November 1997 (Fifth Power Project), respectively. The PCRs were based on a comprehensive assessment of completed works, with a detailed account of the scope, costs, implementation, and operational aspects of the projects at that stage. For the Fifth Power Project, the recalculated financial rate of return (FIRR) was 8.3 percent and the economic internal rate of return (EIRR) was at 29.2 percent; the corresponding figures for the Sixth Project were 4.2 percent and 13.35 percent, respectively. Both projects were rated as generally successful. The Operations Evaluation Mission (OEM) found the PCRs to be straightforward in their assessment of the project implementation and physical achievements as well as underlying shortcomings during the implementation cycle.

F. Operations Evaluation

10. The project performance audit report assesses the projects’ effectiveness in terms of appropriateness of formulation and design, progress and quality of implementation, degree of achievement of their objectives, and sustainability. It presents the findings of the OEM that visited project sites in Nepal from 27 October to 13 November 1999. The PPAR is based on a review of the appraisal reports (for the Fifth and Sixth Power projects), the corresponding PCRs, and materials from ADB’s files, and those at NEA.

II. IMPLEMENTATION PERFORMANCE

A. Design

1. Kali Gandaki

11. Consultants from Finland, Norway, and the United States selected in accordance with ADB’s Guidelines on the Use of Consultants, performed the engineering services for the Kali Gandaki hydropower station design and tendering. Despite minor problems due to replacement of expert personnel during project implementation, the performance of the consultants during project preparation is rated as generally satisfactory. The items of design unforeseen prior to implementation are noted in the consultant’s report (Appendix 3). The Kali-Gandaki design has proven to be adequate and implementation of the works is under way and cofinanced under ADB Loan 1452-NEP(SF).1

1 Loan 1452-NEP(SF): Kali-Gandaki A Hydropower Station, for $160 million, approved on 23 July 1996.

2

2. Computerized Billing System

12. The attempts of the selected software supplier to develop a custom software for the billing system resulted in long delays and prevented the original scope of works—extending the pilot program to additional branch offices—to be implemented. At design, the consultants had assumed the use of a commercially available software. It could not have been foreseen that the successful bidder would propose to develop a custom software. 13. While the covenants of the loans included a reduction system losses to less than 20 percent, no design feature other than the computerized billing system and the rehabilitation of some villages included in the projects would tend to reduce losses. The previous losses were at least 26.3 percent. It is not reasonable to expect that more than 6 percent of the entire system losses were to be found in the combination of rehabilitation and computerized billing implementation.2 The design of the projects should have included the means to enable the Executing Agency (EA) to meet technical conditions. 14. At the time of the Mission, computerized billing pilot program had been in operation for about two years. The system is functioning well and start-up problems in hardware and software have been rectified. Customer satisfaction is perceived to be higher than at the other offices. Software developmental problems of database errors and those associated with changes in procedures have been addressed.

3. Rural Electrification Program

15. Implementation of the Rural Electrification Program, the largest financial component of the Sixth Project, was plagued by significant delays, requiring more than seven years to complete instead of the three and a half years initially envisaged. The reasons for the delay include the trade blockade between India and Nepal and the alleged mismatch between the supply and construction contracts. In the end, important achievements did occur by way of line installation and consumer connections and, according to the NEA PCR prepared in 1995, the following outputs were produced: (i) 33 kV lines: 279.5 kilometers (km) compared with the 240 km envisaged; (ii) 11 kV lines: 986 km compared with 530 km; (iii) .4/.23 kV lines: 1,212 km compared with 530 km; and (iv) electrification of 511 villages and rehabilitation of four major towns in addition to smaller areas.

B. Contracting, Construction, and Commissioning

16. Materials procurement under international competitive bidding for the Fifth Power Project was mostly satisfactory, with 26 packages awarded for the transmission, distribution, rehabilitation, and generation facilities. Local competitive bidding was utilized for vehicles and

2 The project covenanted target for loss reduction implied a corresponding effort by NEA to reduce system losses

above and beyond what was achievable through the computerized billing component alone. The issue of nontechnical loss reduction is being further addressed by a component of Loan 1452-NEP (footnote 3).

3

office equipment for the pilot project. The contract for the erection of the 132 kV substations and transmission line was awarded on a turnkey basis. The balance of the transmission and distribution facilities and the rehabilitation work were covered through the separate installation and procurement of materials. 17. The Mission observed that commissioning of the facilities especially the substations was poor. Some relaying installations were never put into service and there is a total lack of records, manuals, as-built drawings, circuit diagrams, etc. for much of the equipment installed. As no records or anecdotal evidence could be located, it is not known if the problem originated at commissioning or if all such missing items were merely lost since. On the other hand, the pilot computerized billing system was successfully commissioned, and all necessary manuals are on hand. 18. Quality control during procurement was not effective in preventing substandard materials, i.e., steel poles and 11 kV class circuit breakers, from being utilized.3 Construction quality was partly satisfactory. NEA personnel cited the poor work of the contractor for the 33 kV substations under the Fifth Project and four of the nine contractors for the Tatopani hydropower additions. 19. Tatopani Hydroelectric. The project component, implemented under the Sixth Power Project, provided for the addition of four generating units at the Tatopani site, an associated distribution system, and a grid connection. Previous construction had provided for these units to be added to the site. The consultant was selected according to the ADB guidelines for detailed design and assisted the NEA during tendering. The design separated the procurement into 12 tender packages to decrease the weight of each shipment to the remote site. Most of the reported4 shortcomings of the facility do not seem to be solely due to the design or specification of equipment procured by the Sixth Project, but first and foremost to prior civil design and other station features. Units 5 and 7, which were provided by the Sixth Project have had long outages due to mechanical problems. Quality control for the procurement or the commissioning process may have been less than required for this application.

C. Organization and Management

20. Prior to 1985, planning for power generation and construction of transmission systems in Nepal were the responsibility of the Electricity Department. The operation of facilities after completion and all distribution functions were under the Nepal Electricity Corporation. To improve the management of the electrical system, the NEA was created in 1985 after many years of policy dialogue and delay. Although improvements were made, many problems remained. These included long delays in project implementation, weak financial controls, and poor planning. The failure of NEA’s new management to establish an efficient workforce during the coincident early years of the projects contributed to the delays encountered.5 3 The Mission was not able to determine if this resulted primarily from inadequate quality control or from specification

weakness. 4 This site had been reviewed by an ADB OEM on the Small Hydroelectric Project. 5 The Fifth Project loan was approved in December 1983, the loan agreement was delayed to September 1984, and

the consultant for the initial works appointed in July 1985. The Sixth Project loan was approved in November 1984, became effective in April 1986, and the initial consultant appointed in September 1986.

4

21. NEA’s problems with project management procedures contributed to (i) delays in procurement, (ii) lack of details as to disbursement categories, and (iii) lack of records of installed facilities utilization. These problems were encountered both by the Review Mission as well as the PCR team. The NEA’s PCRs are not adequate to reconstruct the expenditures by location, which compromises the evaluation of results. Considering the foregoing, the management of both projects can be considered substandard.

D. Actual Cost and Financing

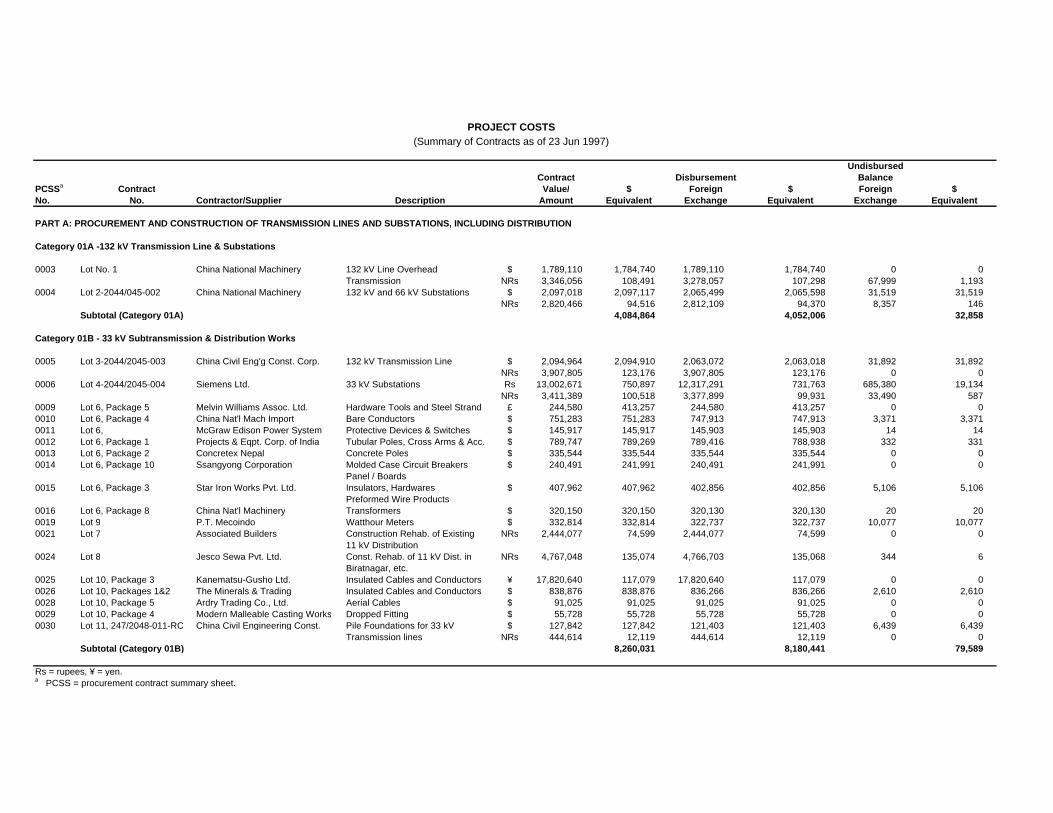

22. The appraised cost (foreign plus local cost) of the combined projects was $67.4 million equivalent with changes and additions increasing the estimated final cost to $82.493 million equivalent. At closing, the actual cost was $77.545 million, of which ADB-financed $60.795 million. Under the Fifth Project, $1.60 million was undisbursed. Details on each major component are in Table 1. A summary of the contracts per loan category is given in Appendix 1.

Table 1: Estimated and Actual Cost ($ million)

Estimated Actual

Item

FX

LC Total Cost

FX

LC

Total Cost

A. Procurement and Construction of

Transmission Lines and Substations, Including Distributiona

18.00 7.10 25.10 15.40 0.70 16.10

B. Management Training Assistance for NEA, Including a Computerized Consumer and Commercial Accounting System

na na 1.70 1.90 0.00 1.90

C. Engineering Services for Kali Gandaki “A” Hydroelectric Project

5.00 0.80 5.80 5.80 0.00 5.80

FX = foreign exchange, LC = local cost, na = not available, NEA = Nepal Electricity Authority. a appraisal.

23. Given the total disarray of NEA’s records, ADB’s efforts in preparing the PCR were commendable. Future loans to Nepal involving the NEA should covenant a more acceptable method and performance in maintaining records of expenditures as to category and amounts.

E. Implementation Schedule

24. For the Fifth Project, the schedule according to the project appraisal report included loan approval in November 1983, and completion of construction and training in March 1988 for a

5

duration of some 52 months. The loan was approved in December 1983, but became effective in September 1984. Construction and training for the 132 kV works were completed in July 1990, and that for distribution in October 1991 about 43 months later than expected. The primary reasons for these delays were (i) the initial delay for the consultancy, (ii) delays in tendering, and (iii) a blockade of customs entry points between India and Nepal. The delay due to the blockade was beyond the control of the NEA, but other delays were due to internal processes in the NEA. 25. In November 1991, at the request of His Majesty’s Government, ADB approved the inclusion of the computerized consumer billing system in the Project. Due to a delay in appointing the consultants, this component was not initiated until April 1994. Implementation of the pilot program was delayed by the software supplier to the point that only the pilot installation was completed. 26. Loan savings from the Fifth Project were utilized to finance the engineering services for the Kali Gandaki subproject. These services were added to the loan as of December 1992 and extended up to December 1996. With the loan modification, the estimated term of services was to extend to the end of July 1994 or for some 20 months. Due to appreciable changes in the scope of work as the Project became better defined, the term was extended by 27 months. Several valid reasons were advanced for the additional time. Among these were the changes found in geology, unforeseen environmental considerations addressed, and the need to evaluate bids received from 36 prospective contractors. 27. The Sixth Project was also delayed, in this case by about eight years. Initial delays were due to the delays caused by the creation of the NEA and the resulting tendering delays, the trade dispute with India, the addition of another 33 kV line with two substations, and the addition of the Tatopani generating units and local distribution system in January 1991. The Sixth Project loan was closed on 16 November 1995 (the original closing data was 30 June 1989).

F. Technical Assistance

28. The Fifth Project was preceded by a project preparatory TA; however, no mention is made of the outputs of the TA in any of the project planning, implementation, or completion reports. The ongoing TA 1267-NEP: Institutional Support for Distribution Planning and Commercial Operations in NEA,6 served as the catalyst for the addition of the computerized consumer and commercial accounting system.

G. Compliance with Loan Covenants

29. Each loan contained several key conditions and covenants: 12 for the Fifth and 14 for the Sixth. 30. At closing, two common conditions had not been fully met. These were to reduce losses to 20 percent or less and to produce an annual rate of return of not less than 6 percent. Per the

6 For $780,000, approved on 11 January 1990.

6

(unaudited) NEA financial statement for FY1995, the rate of return was 8.5 percent. Therefore, the condition was achieved, after the project was effectively completed. However, electricity losses, although decreasing, have remained greater than 20 percent through FY1999.

7

III. PROJECT RESULTS

A. Operational Performance

1. Transmission Lines

31. Construction of the 132 kV transmission lines reviewed by the OEM appears to be of good quality and the line is sustainable for its expected life—provided adequate (normal) preventive maintenance of the towers and adjacent right-of-way continues (Appendix 3). The installation of the 132 kV facilities7 appears to have been designed and with good workmanship. The towers are in good condition and have no broken insulators. 32. The 33 kV lines are in generally good condition and should perform up to their expected life or to the point where their load reaches capacity with normal maintenance practices. The 33-11 kV substations, on the other hand, suffer from poor maintenance and their ability to sustain service without rehabilitation is questionable. Their condition is similar to those of the Fifth Power Project (para. 31). Rehabilitation of the substations is required to prevent near-term outages. In their present condition, most are not sustainable.

2. Subtransmission Lines

33. The 11 kV feeder breakers have also suffered premature failures and need replacement to ensure sustainability of the transmission system. Technical details regarding the condition of the lines are provided in Appendix 3. 34. The 33-11 kV distribution substations constructed under the Sixth Project were well designed, but suffer from numerous common problems. These include inoperative air conditioners, inoperative relaying, never commissioned relaying, lack of spare parts, inoperative meters, problems with the breakers (Pokhara), inadequate gravel cover, failed carrier systems, etc. Many examples of dangerous repair techniques were noted. 35. Line personnel have demonstrated a high level of adaptability to the lack of equipment and tools even to the point of transporting poles by bicycle and installing transformers with pulleys, but these techniques inevitably compromise the levels of maintenance and expansion that the distribution system needs to become viable in scope and revenue-generation potential.8 36. The general level of maintenance at the substations is very poor. For the most part, the personnel are willing to perform maintenance and repair and have demonstrated a high degree 7 Based on observations of the line in the vicinity of Balaju. 8 Except for Pokhara, the substations are operating without the full complement of 11 kV circuit breakers and they

have no spare parts and no manuals. The remaining breakers though still serviceable will probably fail after interrupting a few faults and/or after an indeterminable number of open/close operations.

8

of ingenuity in maintaining the service with few spare parts, no tools, no manuals, and a very low level of funding for maintenance activities. In their present condition, the 11 kV substation switchgear cannot support any significant additional distribution expansion. 37. The Fifth Power Project-funded 132-11 kV substation in Pokhara reviewed by the Mission has a peak demand that is equal to the installed transformer capacity. Continued operation requires installation of additional capacity or moving the distribution load supply to an alternative substation.9 The station is sustainable at present loading, assuming adequate maintenance is provided and the current problems are rectified. 38. Rehabilitation initiatives undertaken under the Fifth Project have been overshadowed by subsequent projects and further area expansion or rehabilitation efforts, and are difficult to discern. The resulting growth has engendered 11 kV feeders that are much too long to serve future increases in load, as are many of the 400/230 circuits. The 400/230-volt distribution feeders also suffer from the same excessive length problem as their 11 kV counterparts. They should be limited to about 300 meters. 39. Proper tools for maintenance of the distribution facilities are lacking. ‘’Hot sticks’’ are mostly absent and, where used, are too short for safety and effective operation. As protection from unintended reenergizing and from induced voltages, grounding jumpers, installed with hot sticks, should be used on all de-energized lines while overhead work is being performed. 40. Vehicle availability must be increased in the distribution offices to maintain the lines so as to retain the normal life of the equipment, maximize service, and reduce losses. The lack of vehicles will eventually lead to a collapse of service in the more remote regions as there will be no means of addressing multiple failures of lines and distribution transformers.

3. Rural Electrification Program

41. The operational performance of the rural electrification component is difficult to assess in empirical or economic terms, given the absence of either a baseline survey or project monitoring data over the entire project implementation cycle. Moreover, candidate schemes for rural electrification were not systematically selected according to formal socioeconomic criteria as was the case for a similar rural electrification scheme recently carried out for Sri Lanka (Power System Expansion).10 Discussions with various NEA officials also revealed that political considerations were not uncommon in the selection of zones slated for electrification, and the criterion of cost-effectiveness was clearly not retained—as evidenced by the Mission observation of a very low customer base for some locations. 42. The NEA PCR, however, mentions that the full quota of 55,000 consumer connections envisaged during project inception has not materialized. At project completion, only 30,000 new consumers had been connected. The shortfall can be partially attributable to the relatively onerous start-up connection charges and expenses (meter acquisition and connection fees in

9 The Kali Gandaki “A” Hydroelectric Project includes a 132 kV line to the vicinity of Pokhara. If timely, the resulting

substation could include distribution (11 kV) facilities to serve the area loads. 10 Source: PCR:SRI 21201: Power System Expansion Project, May 1990.

9

particular), which have dissuaded a large contingent of potential new customers located in the vicinity of the distribution lines developed under the rural electrification scheme. 43. The NEA kept the records of outputs from this component in Kathmandu, and very little information pertaining to the results of the rural electrification component were made available to the OEM during their Mission’s visits to various locations serviced by the Project.

B. Institutional Development

44. The NEA was created in 1985, following extensive policy dialogue with ADB. Although a number of institutional improvements had been made, much still remains to be done within the NEA. Long delays in project implementation have persisted, financial performance and control are weak, and planning has been carried out largely on an ad hoc basis. Consequently, although the Fifth Project loan was approved in December 1983, the loan agreement became effective only in September 1984, and the consultant for transmission and distribution work was appointed only in July 1985. However, problems persisted and in 1987, after the joint mission of the International Development Association and ADB for power subsector review visited Nepal, a matrix of issues11 was developed and discussed with the Government. The failure of NEA's new management to establish a cohesive and efficient workforce during the initial years of the Project contributed to the delays. 45. Through successive ADB and World Bank projects initiated after the Fifth and Sixth Power projects, the NEA has made progress toward becoming a more efficient utility. Financial covenants were met in FY1995, tariffs were increased in FY1994 in anticipation of the Arun III Project (which did not materialize). Audited accounts were submitted on time. Systems losses, however, did not decrease to the covenanted 20 percent. To assist the NEA, ADB included a nontechnical loss reduction component costing $2.3 million in Loan 1452-NEP (footnote 4). ADB and other external agencies have been actively involved in providing TA to strengthen the NEA's institutional capability as it moves toward becoming a commercially oriented utility. To improve the NEA's operational performance and to introduce modern utility management practices, a twinning arrangement was established with Electricité de France in October 1989. Staff retrenchments brought the total down from 9,775 in 1991 to 7,457 in 1995. In February 1994, a revised organization structure was approved. Under an ADB TA,12 consulting services were provided to improve the NEA's distribution planning capability and to enhance its commercial operations. However, the OEM feels that much still remains to be done to effectively reorient NEA management practices and corporate culture toward a fully commercialized approach in providing cost-effective services.

C. Performance of the Asian Development Bank

11 The main elements raised included overstaffing, lack of well-defined corporate goals, and shortage of technical

manpower. 12 TA 1267-NEP: Institutional Support for Distribution Planning and Commercial Operations, for $780,000, approved

on 11 January 1990.

10

46. ADB cooperated well with the Borrower and the EA in formulating the Project and processing the loan. During implementation, ADB closely monitored and supported the Project, thus contributing significantly to its successful completion. 47. ADB controllers, however, did not properly book contracts financed under the Sixth Power Project to loan categories, which severely hampered PCR preparation. ADB may not have properly reviewed the periodic status and progress reports submitted by the NEA project manager. Such submissions could have alerted ADB to the fact that certain records were not being maintained. 48. Regular missions from ADB staff during the various phases of implementation appreciated the different problems faced during implementation, and provided advice and solutions. Regular monthly meetings in the Nepal Resident Mission in Kathmandu also provided valuable support to the NEA. Because these meetings were attended by project managers of various ADB-assisted projects, the exchange of experiences, and discussions of problems and solutions were very helpful. Apart from these meetings, the Nepal Resident Mission was always available for further advice and support. A training program in ADB procedures, conducted in Kathmandu under Part B of the loan, was deemed very helpful in the administration of the Project.

D. Financial Performance

49. The financial profile of the NEA is presented in Appendix 4. The profit and loss statement presented its annual report indicates a marked improvement in the financial performance of the utility: operating losses/deficits registered during the early 1990s converted to net surpluses beginning in 1993 onward. The principal financial indicators pertaining to the utility’s performance indicate a gradual improvement in the key ratios.

E. Economic and Financial Reevaluation

50. The Fifth and Sixth projects constituted a major portion of the NEA’s capital investment program for transmission and distribution in the areas of the grid located outside the Kathmandu Valley (notably the Terai region) for the period 1985-1991. Since this component is a relatively small portion of the overall investment program, it was decided to perform a time/area slice analysis of the NEA’s national investment program over the period of project implementation. This approach is similar to what was used for the PCR for both the Fifth and Sixth projects. However, the consumer base used for projecting financial and economic benefits is limited to power consumption and revenue generation outside the Kathmandu Valley (Eastern, Western, and Far Western Regions). 51. The capital costs of the investment program were assumed as the actual costs less interest during construction for the financial analysis. Operation and maintenance costs were assumed at 1.5 percent of capital costs for transmission and distribution investments and 1 percent of the capital cost for generation investments. For the economic analysis, taxes and

11

duties were excluded, and local capital costs were converted to border prices at a standard conversion factor of 0.9.13 52. For the financial analysis, the benefits were in terms of incremental sales revenues for 1985-1996 as provided by the NEA, and then adjusted to constant mid-1999 price levels (Appendix 5). The projected growth of revenues beyond 1999 was based on a more moderate expansion of the consumer base than what was observed in the recent past. 53. For the economic analysis, the benefits from electricity consumption for each major consumer category were based on (i) the alternative economic costs of other energy sources such as kerosene lighting or diesel generator sets that will be displaced by the use of electricity, and (ii) valuing the additional or induced energy consumption at the estimated average willingness to pay for electricity based on a weighted average of the alternative costs of providing similar energy-related services, and the current electricity tariff. The benefits valued on the basis of resource cost savings for the diverted market and consumers’ willingness to pay for the generated market. Further details on the valuation methodology are in Appendix 5. 54. A summary of the results of the sensitivity analysis is in Table 2, and the cost/benefit cash flows are in Appendix 5. The resulting base case EIRR is 15.3 percent, which is above the 20 percent opportunity cost of capital in Nepal.

Table 2: FIRR and EIRR Sensitivity Analysis

Item

FIRR (%)

EIRR (%)

Base Case 7.7 15.3 Incremental Sales less 10 percent 6.7 13.7 Incremental Sales less 20 percent 5.7 12.0

EIRR = economic internal rate of return, FIRR = financial internal rate of return. 55. The FIRR of the projects—using NEA's overall investment program as the cost stream within the time-slice approach—is 7.7 percent. This poor result is largely a reflection of the impact of low electricity tariffs during the early years of the project when financial covenants were not being met. However, subsequent pressure from ADB and other external funding agencies resulted in tariff increases that allowed the NEA to meet its financial covenants, although still insufficient to generate a financially acceptable FIRR.14

F. Socioeconomic Results

13 For purposes of evaluation throughout the economic analysis, all local costs were assumed to be nontraded goods

and services. Separate shadow wage rate factors were not available at the time of evaluation. 14 Average tariff was increased by 20 percent in 14 May 1996. The most recent increase was 27.6 percent, which took

effect in 17 November 1999.

12

56. The primary socioeconomic impact of both projects is the generation of economic opportunities for cottage-type industries located within the areas serviced by the transmission and distribution network. The primary vector for increased socioeconomic activity is the rural electrification program; increased access to power allowed cottage industries to develop as well as provided for increased use of household amenities such as electric appliances that were hitherto unavailable. The absence of socioeconomic data documenting the changes that have occurred in the impacted areas following implementation of the rural electrification component of the Sixth Power Project prevents any meaningful analysis of the quantitative impacts generated.

G. Gender and Development

57. There was no specific effort to gauge the projects’ effect on women. However, as the women of Nepal perform much of the water gathering, rice milling, etc., the advent of electric power facilitated and lessened the physical demands, and time requirements of these activities.

H. Environmental Impact and Control

58. The environmental impacts of the distribution and rural electrification components of the Fifth and Sixth projects were minor or insignificant. 59. While land was acquired for the substation construction, the affected land was minimal. Most of the right-of-way for the 33 kV lines is still in productive use. The incremental impact of the 11 kV lines was slight because they generally follow existing roadways. Concrete and steel poles were utilized in lieu of wood. 60. The NEA does not utilize herbicides for vegetation control in its substations or along the rights-of-way. Its tree-trimming activities are so infrequent and so minimal in the amount of limb growth removed that the consequence to the environment is marginal. 61. The design and specification of the Kali Gandaki “A” Hydroelectric facility had the potential for significant environmental impact. This potential was addressed by an extensive Environmental Impact Assessment study15 and comprehensive planning for monitoring and abatement of any adverse effects or impacts. In addition, an ADB TA-financed the strengthening of NEA’s Environmental Division.16 This division is participating in monitoring and mitigation of adverse project effects. 62. The other activities of the projects had no discernible environmental impact.

15 The Environmental Impact Assessment was per Nepal’s and ADB’s guidelines. 16 TA 2613-NEP: Institutional Strengthening of NEA’s Environmental Division, for $534,000, approved on 23 July

1996.

13

I. Sustainability

63. The 132 kV lines can be sustained with attention to recommended periodic maintenance practices. Rehabilitation of the distribution in the secondary towns can be effective and sustainable with proper maintenance and upgrading at adequate levels. 64. On the other hand, failure to properly measure loading and take appropriate steps to add transformers and upgrade conductor capacity will cause the losses to remain high and even increase. The full impact of several of the upgrades is not being realized for lack of meters for additional connections. Some areas17 have initiated meter repair and procurement to effectively utilize the additional capacity. 65. The distribution steel poles and pin insulators procured under the Sixth Power Project are superior to those of the previous projects, and are much more sustainable. 66. With increased maintenance, the rural area distribution schemes constructed by the Sixth Power Project are sustainable—provided they are not extended beyond their design capacity and length by the NEA or by subsequent assistance projects. 67. The tubular steel poles used in the Fifth Power Project for 11 kV lines were extremely prone to corrosion; many have already failed and all need to be replaced.18 To the extent that the 33 kV lines utilize these poles,19 this is a major problem in the sustainability of these facilities. This problem is being partially redressed through a pole replacement program undertaken by the regional divisions of the NEA. 68. The computerized billing pilot system is sustainable as a stand-alone system with routine repair/replacement of the hardware, provision of consumable supplies, and database and software maintenance. Replacements of personnel will require training and competent maintenance personnel must be retained as the system ages. However, the system software is not standard and the database included is outmoded. As the remaining offices receive a standardized system, the pilot facility will be nonstandard in the NEA system, and will require significant software changes at a minimum to remain viable when these offices are networked. 69. The equipment of the Sixth Project (Tatopani units 5-8) is sustainable provided (i) preventive maintenance procedures (as per the manufacturer’s recommendations) are followed, (ii) training in operation and maintenance techniques is obtained, and (iii) rocks and other debris due to rack failure are not allowed to strike the turbines. 70. The transmission/distribution line at the local Tatopani area has a very high rate of outages due to momentary contact with trees, bamboo, etc. This condition can be cured and sustainability enhanced by a simple right-of-way clearing and/or a recloser installation.

17 Nepalganj town and surrounding areas. 18 These poles have corroded to the point of collapse, which is a public safety concern as well as a potential cause of

extended wide-area outages in the distribution system. While several area offices have initiated repair by extending the concrete foundation, this will only delay the failure, and is not a permanent repair.

19 The pervasive failure of the steel poles used for 11 kV installations were not noted on the 33 kV lines.

14

71. The most likely scenario for a complete failure of the transmission and distribution lines would arise from the lack of protection for faults as no sectionalizing fusing has been installed.

IV. KEY ISSUES FOR THE FUTURE

72. The project management skills of the NEA, and its personnel must be improved further to prevent delays in procurement and project implementation. Similarly, project reporting formats and record maintenance practices need to be rigorously implemented. 73. The NEA needs to carefully consider the capacity of existing facilities before embarking on future expansion. It is not proper to extend distribution if the existing system cannot support such. The Mission clearly recognizes that certain vital components of the existing distribution system are unsustainable, especially if of use of the line network were further expanded or intensified. 74. To ensure the financial sustainability of operations, tariffs must be maintained at levels that will support adequate maintenance as well as comply with the financial covenants. This activity should include the active maintenance of an accurate cost-of-service determination and its update at least on a quarterly basis. 75. The NEA should be ready to periodically submit the tariffs required to meet its current cost of service and targeted rate of return to the regulatory body. The latter body should be made aware of gaps in tariff implementation even if revision applications are denied. 76. The planning1 abilities of the NEA and the facilities required, i.e., software, hardware, mapping, etc., must be developed to the point where planning can be pursued internally and continually updated.

1 In both least-cost system plans and distribution design.

V. CONCLUSIONS

A. Overall Assessment

77. Exception for delays beyond the control of the NEA and the cancellation of phases 2 and 3 of the computerized billing component, the Fifth Project was implemented successfully. The Project has a positive impact on Nepal’s economy because it facilitated the provision of a power supply to the load centers through the construction of transmission and subtransmission lines from the main grid. The benefits from the Sixth Project as reassessed after its completion also indicate that the Project has a positive impact on Nepal's economy, bearing in mind the lower-than-expected outcomes but subsequent positive impacts of the rural electrification component. Both projects can be considered generally successful on the basis of the consolidated EIRR. The sustainability of the system is a real concern, but ultimately the project components are deemed sustainable in a “status-quo” scenario where no further additions are made to the distribution capacity; otherwise, further efforts at major rehabilitation are indispensable to ensure the functioning of the expanded systems.

B. Lessons Learned

1. Project Implementation

78. Delays in project implementation resulted in losses of revenue and deviations from the originally planned project scope. These delays were perhaps due to the NEA’s difficulties in following ADB’s procurement procedures and in a possible lack of foresight by ADB of the difficulties of project implementation given the local institutional context of Nepal. It is recommended that NEA’s senior personnel participate in training courses at ADB, and that when planning projects, NEA managers take a broader view, thus minimizing the likelihood of difficulties. 79. The EA’s recognition of the need for rigorous maintenance needs enhancement. Adherence to minimum maintenance standards and practices should be a pre-condition for further investments in the expansion of the system. 80. Another lesson is the need to provide for more rigorous accountability in carrying out rural electrification programs as evidenced by the absence of adequate monitoring data on project achievements for this significant component of the Sixth Project. Equally important is the application of proper screening criteria based on either cost-effectiveness considerations and/or economic feasibility, where warranted, for the socioeconomic evaluation of rural electrification schemes.

2

C. Follow-Up Actions

81. Problems related to a lack of adequate funding, priorities, and training give rise to deficiencies in general maintenance and avoidable1 nontechnical loss problems in the NEA distribution system. Such issues require monitoring and training to improve the situation. 82. NEA technical staff should conduct an exhaustive review of the status and conditions regarding the operational status and long-term sustainability of the transmission and distribution components funded by the Fifth and Sixth projects. This review should be carried out on a priority basis to prepare a rehabilitation and/or equipment replacement plan. Implementation of this rehabilitation program should constitute a precondition for future aid agency involvement in the country’s power sector development. 83. Several items of additional assistance that the NEA needs are being addressed through various ongoing loans and TA projects.2 Computerized billing is to be implemented under a current pending loan. In addition, the NEA recognizes the need for TA for strengthening its capacity in the environmental and social areas, and for upgrading its system planning capability to formulate a comprehensive power system master plan. 84. Particular care should be taken for ADB to monitor and supervise future loans more closely during implementation, and for contracts with contractors and suppliers to be carried out in accordance with the description of the various categories of the loans. Issues and problems surrounding the implementation of procurement and their quality control should be more effectively addressed by prequalification of suppliers or short-listing during the international competitive bidding.3

85. The issue of conformity with the loan covenant on systems losses that has still to be satisfied by the NEA must be pursued under the current and forthcoming ADB loans to the power sector.

1 For example, lack of metering at the consumer and distribution feeder levels. 2 TA 1746-NEP: Enhancement of Project Implementation Efficiency, for $366,000, approved on 18 August 1992. The

TA was to support Government efforts at strengthening overall implementation capacity. It sought to identify the constraints at the national, sectoral and individual project level, and suggest remedial measures.

3 This aspect was discussed at length with NEA management and former project managers who were in agreement on the potential benefit.

3

APPENDIXES

Number

Title

Page

Cited on (page, para.)

1 Project Costs 18 2, 7

2 Implementation Schedule 22 3, 8

3 Consultant’s Report on Operational Performance

28 3,11

4 Nepal Electricity Authority: Financial Highlights 1988/89

31 11,49

5 Economic and Financial Evaluation attachments\pe543-app5a.xls attachments\pe543-app5b.xls

33 11,52

ContractPCSSa Contract Value/No. No. Contractor/Supplier Description Amount

PART A: PROCUREMENT AND CONSTRUCTION OF TRANSMISSION LINES AND SUBSTATIONS, INCLUDING DISTRIBUTION

Category 01A -132 kV Transmission Line & Substations

0003 Lot No. 1 China National Machinery 132 kV Line Overhead $ 1,789,110 1,784,740 1,789,110 1,784,740 0 0Transmission NRs 3,346,056 108,491 3,278,057 107,298 67,999 1,193

0004 Lot 2-2044/045-002 China National Machinery 132 kV and 66 kV Substations $ 2,097,018 2,097,117 2,065,499 2,065,598 31,519 31,519NRs 2,820,466 94,516 2,812,109 94,370 8,357 146

Subtotal (Category 01A) 4,084,864 4,052,006 32,858

Category 01B - 33 kV Subtransmission & Distribution Works

0005 Lot 3-2044/2045-003 China Civil Eng'g Const. Corp. 132 kV Transmission Line $ 2,094,964 2,094,910 2,063,072 2,063,018 31,892 31,892NRs 3,907,805 123,176 3,907,805 123,176 0 0

0006 Lot 4-2044/2045-004 Siemens Ltd. 33 kV Substations Rs 13,002,671 750,897 12,317,291 731,763 685,380 19,134NRs 3,411,389 100,518 3,377,899 99,931 33,490 587

0009 Lot 6, Package 5 Melvin Williams Assoc. Ltd. Hardware Tools and Steel Strand £ 244,580 413,257 244,580 413,257 0 00010 Lot 6, Package 4 China Nat'l Mach Import Bare Conductors $ 751,283 751,283 747,913 747,913 3,371 3,3710011 Lot 6, McGraw Edison Power System Protective Devices & Switches $ 145,917 145,917 145,903 145,903 14 140012 Lot 6, Package 1 Projects & Eqpt. Corp. of India Tubular Poles, Cross Arms & Acc. $ 789,747 789,269 789,416 788,938 332 3310013 Lot 6, Package 2 Concretex Nepal Concrete Poles $ 335,544 335,544 335,544 335,544 0 00014 Lot 6, Package 10 Ssangyong Corporation Molded Case Circuit Breakers $ 240,491 241,991 240,491 241,991 0 0

Panel / Boards0015 Lot 6, Package 3 Star Iron Works Pvt. Ltd. Insulators, Hardwares $ 407,962 407,962 402,856 402,856 5,106 5,106

Preformed Wire Products0016 Lot 6, Package 8 China Nat'l Machinery Transformers $ 320,150 320,150 320,130 320,130 20 200019 Lot 9 P.T. Mecoindo Watthour Meters $ 332,814 332,814 322,737 322,737 10,077 10,0770021 Lot 7 Associated Builders Construction Rehab. of Existing NRs 2,444,077 74,599 2,444,077 74,599 0 0

11 kV Distribution0024 Lot 8 Jesco Sewa Pvt. Ltd. Const. Rehab. of 11 kV Dist. in NRs 4,767,048 135,074 4,766,703 135,068 344 6

Biratnagar, etc.0025 Lot 10, Package 3 Kanematsu-Gusho Ltd. Insulated Cables and Conductors ¥ 17,820,640 117,079 17,820,640 117,079 0 00026 Lot 10, Packages 1&2 The Minerals & Trading Insulated Cables and Conductors $ 838,876 838,876 836,266 836,266 2,610 2,6100028 Lot 10, Package 5 Ardry Trading Co., Ltd. Aerial Cables $ 91,025 91,025 91,025 91,025 0 00029 Lot 10, Package 4 Modern Malleable Casting Works Dropped Fitting $ 55,728 55,728 55,728 55,728 0 00030 Lot 11, 247/2048-011-RC China Civil Engineering Const. Pile Foundations for 33 kV $ 127,842 127,842 121,403 121,403 6,439 6,439

Transmission lines NRs 444,614 12,119 444,614 12,119 0 0Subtotal (Category 01B) 8,260,031 8,180,441 79,589

Rs = rupees, ¥ = yen.a PCSS = procurement contract summary sheet.

(Summary of Contracts as of 23 Jun 1997)PROJECT COSTS

$Equivalent

DisbursementForeign

Exchange

UndisbursedBalanceForeign

Exchange$

Equivalent$

Equivalent

ContractPCSSa Contract Value/No. No. Contractor/Supplier Description Amount

$Equivalent

DisbursementForeign

Exchange

UndisbursedBalanceForeign

Exchange$

Equivalent$

Equivalent

Category 01C - Equipment & Materials & Vehicles

0007 Lot 5, 044/45 ADB V-1 Hyosung Corp. Distribution Materials (Package A&B) $ 971,005 966,290 971,005 966,290 0 00008 Lot 5, 044/45 ADB V-2 Toyota Tsusho Corp. Crane Auger Truck, Crane Truck, ¥ 73,946,800 589,173 73,946,800 589,173 0 0

Pickup (D)0020 Lot 5 (C), Package C LGZ Landis & Gyr Zug Corp. Watthour Meter (Transformer rated) SwF 229,059 143,144 229,059 143,144 0 00023 Lot 5, Package A P.T. Mecoindo 600 V Current Transformers $ 7,758 7,758 7,758 7,758 0 00027 Lot 5(C), Package D Dongfang Electric Co. Inst. Transformer for Metering Unit $ 405,913 405,913 405,913 405,913 0 0

Subtotal- Category 01C 2,112,278 2,112,278 0

Category 01D - Consulting Services

0001 Hyundai Engineering Co. Consulting Services for Part A $ 1,842,970 1,843,626 1,720,442 1,721,098 122,528 122,528

Subtotal (Category 01D) 1,843,626 1,721,098 122,528

Category 01E - Training for Trade Staff

0017 M. Tuladhar Travel Expenses RM 1,343 535 1,343 535 0 00018 M. Tuladhar Travel Expenses $ 227 227 227 227 0 0

0034 Rabin Shrestha Training $ 3,600 3,600 2,940 2,940 660 660

Subtotal (Category 01E) 4,362 3,702 660

TOTAL (Part A) 16,305,161 16,069,524 235,636

RM = ringgit, SwF= Swiss franc, ¥ = yen.

ContractPCSSa Contract Value/No. No. Contractor/Supplier Description Amount

$Equivalent

DisbursementForeign

Exchange

UndisbursedBalanceForeign

Exchange$

Equivalent$

Equivalent

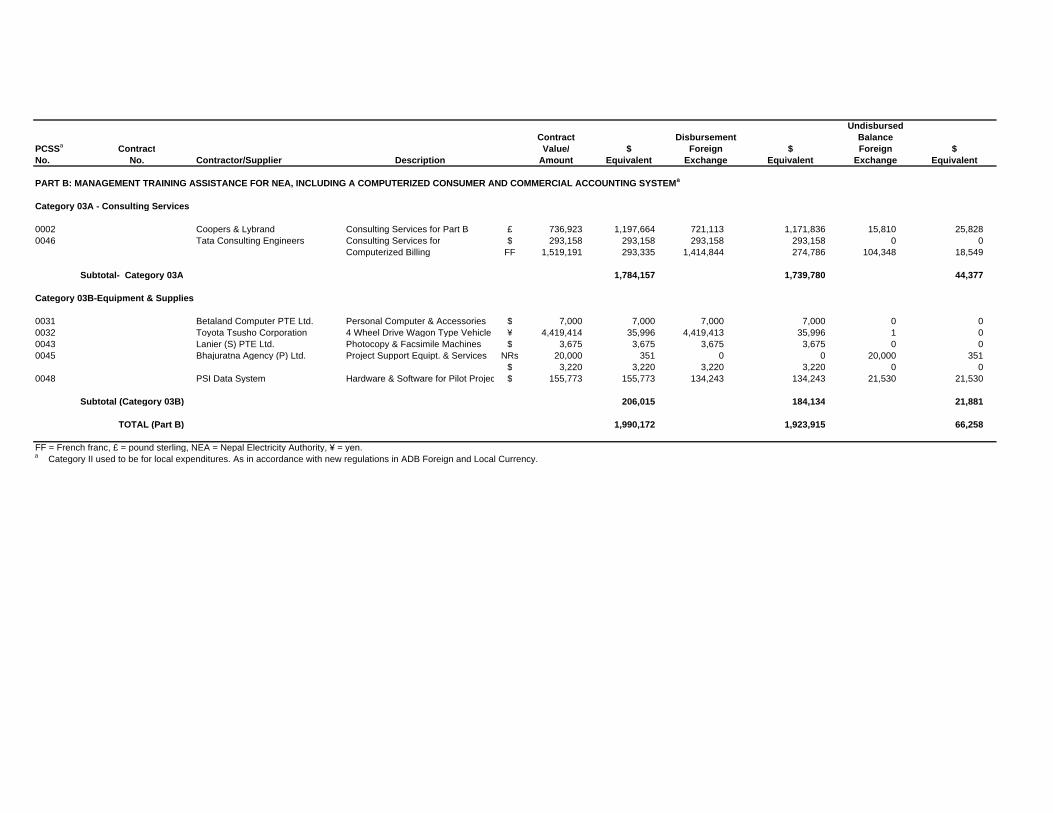

PART B: MANAGEMENT TRAINING ASSISTANCE FOR NEA, INCLUDING A COMPUTERIZED CONSUMER AND COMMERCIAL ACCOUNTING SYSTEMa

Category 03A - Consulting Services

0002 Coopers & Lybrand Consulting Services for Part B £ 736,923 1,197,664 721,113 1,171,836 15,810 25,8280046 Tata Consulting Engineers Consulting Services for $ 293,158 293,158 293,158 293,158 0 0

Computerized Billing FF 1,519,191 293,335 1,414,844 274,786 104,348 18,549

Subtotal- Category 03A 1,784,157 1,739,780 44,377

Category 03B-Equipment & Supplies

0031 Betaland Computer PTE Ltd. Personal Computer & Accessories $ 7,000 7,000 7,000 7,000 0 00032 Toyota Tsusho Corporation 4 Wheel Drive Wagon Type Vehicle ¥ 4,419,414 35,996 4,419,413 35,996 1 00043 Lanier (S) PTE Ltd. Photocopy & Facsimile Machines $ 3,675 3,675 3,675 3,675 0 00045 Bhajuratna Agency (P) Ltd. Project Support Equipt. & Services NRs 20,000 351 0 0 20,000 351

$ 3,220 3,220 3,220 3,220 0 00048 PSI Data System Hardware & Software for Pilot Project $ 155,773 155,773 134,243 134,243 21,530 21,530

Subtotal (Category 03B) 206,015 184,134 21,881

TOTAL (Part B) 1,990,172 1,923,915 66,258

FF = French franc, £ = pound sterling, NEA = Nepal Electricity Authority, ¥ = yen.a Category II used to be for local expenditures. As in accordance with new regulations in ADB Foreign and Local Currency.

ContractPCSSa Contract Value/No. No. Contractor/Supplier Description Amount

$Equivalent

DisbursementForeign

Exchange

UndisbursedBalanceForeign

Exchange$

Equivalent$

Equivalent

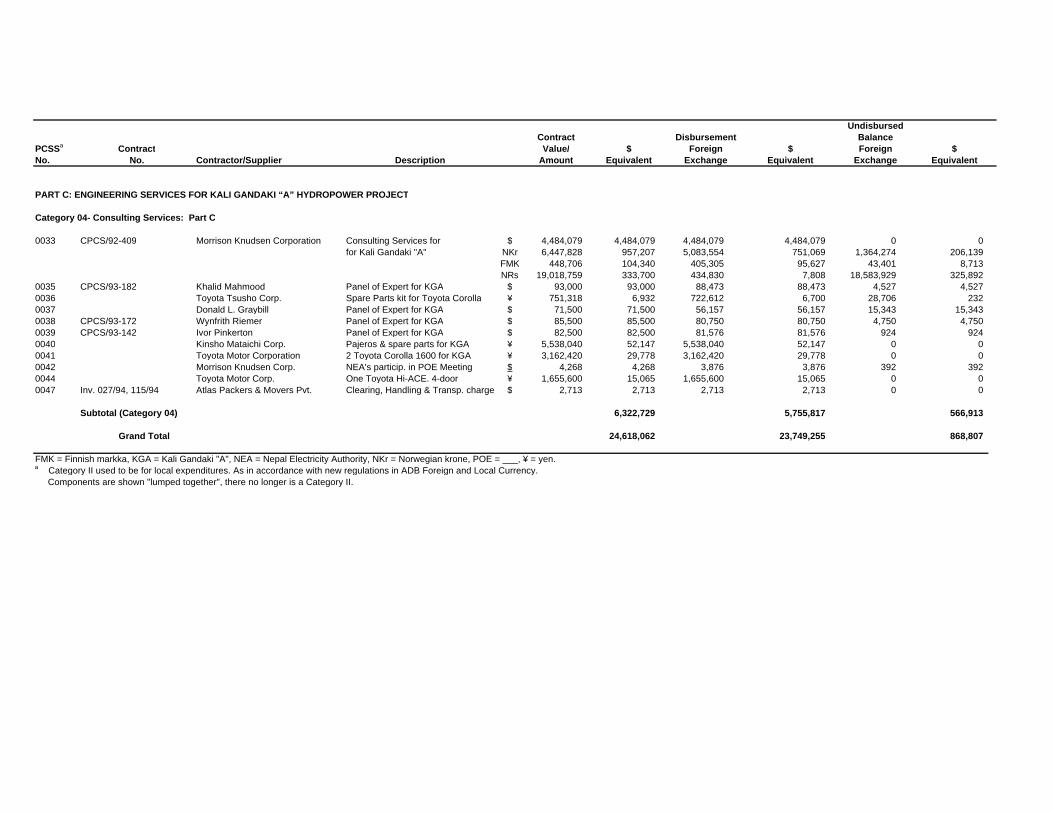

PART C: ENGINEERING SERVICES FOR KALI GANDAKI “A” HYDROPOWER PROJECT

Category 04- Consulting Services: Part C

0033 CPCS/92-409 Morrison Knudsen Corporation Consulting Services for $ 4,484,079 4,484,079 4,484,079 4,484,079 0 0for Kali Gandaki "A" NKr 6,447,828 957,207 5,083,554 751,069 1,364,274 206,139

FMK 448,706 104,340 405,305 95,627 43,401 8,713NRs 19,018,759 333,700 434,830 7,808 18,583,929 325,892

0035 CPCS/93-182 Khalid Mahmood Panel of Expert for KGA $ 93,000 93,000 88,473 88,473 4,527 4,5270036 Toyota Tsusho Corp. Spare Parts kit for Toyota Corolla ¥ 751,318 6,932 722,612 6,700 28,706 2320037 Donald L. Graybill Panel of Expert for KGA $ 71,500 71,500 56,157 56,157 15,343 15,3430038 CPCS/93-172 Wynfrith Riemer Panel of Expert for KGA $ 85,500 85,500 80,750 80,750 4,750 4,7500039 CPCS/93-142 Ivor Pinkerton Panel of Expert for KGA $ 82,500 82,500 81,576 81,576 924 9240040 Kinsho Mataichi Corp. Pajeros & spare parts for KGA ¥ 5,538,040 52,147 5,538,040 52,147 0 00041 Toyota Motor Corporation 2 Toyota Corolla 1600 for KGA ¥ 3,162,420 29,778 3,162,420 29,778 0 00042 Morrison Knudsen Corp. NEA's particip. in POE Meeting $ 4,268 4,268 3,876 3,876 392 3920044 Toyota Motor Corp. One Toyota Hi-ACE. 4-door ¥ 1,655,600 15,065 1,655,600 15,065 0 00047 Inv. 027/94, 115/94 Atlas Packers & Movers Pvt. Clearing, Handling & Transp. charge $ 2,713 2,713 2,713 2,713 0 0

Subtotal (Category 04) 6,322,729 5,755,817 566,913

Grand Total 24,618,062 23,749,255 868,807

FMK = Finnish markka, KGA = Kali Gandaki "A", NEA = Nepal Electricity Authority, NKr = Norwegian krone, POE = ___, ¥ = yen.a Category II used to be for local expenditures. As in accordance with new regulations in ADB Foreign and Local Currency. Components are shown "lumped together", there no longer is a Category II.

Appendix 3, page 1

CONSULTANT’S REPORT ON OPERATIONAL PERFORMANCE A. Transmission Lines 1. The construction of the 132-kilovolt (kV) transmission line from Dubi to Anarmani (approximately 75 kilometers [km]) substations appears to be of good quality, and the line is sustainable for its expected life if adequate (normal) preventive maintenance for the towers and right-of-way is provided. Various spare parts are available at Anarmani. No damaged insulators or corrosion of the lattice works was noted. Ground resistance of the tower footings should be checked on a regular basis because of the changing pattern of land use and subsequent moisture levels around the towers. 2. The 132 kV facilities1 appear to have been installed as designed and have good workmanship. The towers are in good condition and no broken insulators were observed. 3. The Anarmani facility includes spare 132 kV parts but few tools, and has problems with the installed metering as few of them are functioning. The major equipment is maintainable and receives routine testing periodically. The current peak demand was recorded as 12.0 megawatts with an installed transformer capacity of about 12.75 megavolt-ampere (MVA).2 Continued operation without load shedding will require additional transformer capacity and/or reactive correction in the very near future. 4. The present Pokhara 132-11 kV substation peak demand is equal to the installed transformer capacity. Continued operation requires the additional capacity be installed or that the distribution load supply be moved to an alternative substation.3 The station also has problems with the SF6 circuit breaker and relaying. The station is sustainable at present loading, assuming adequate maintenance is provided, and the current problems are rectified, especially the circuit breaker gas leaks and nonuniform pole opening. 5. The capacity of the Marsyangdi-Bharatpur 132 kV circuit should be confirmed by load-flow studies to assess the need for increases depending on the timing and location of additional generation facilities and for load center increases. 6. The 33 kV lines are in generally good condition and should perform up to their expected life or to the point where their load reaches capacity with normal maintenance practices. The 33-11 kV substations suffer from poor maintenance and their ability to sustain service without rehabilitation is questionable. Their condition is similar to those of the Fifth Project. Rehabilitation is required to prevent near-term outages. In their present condition, most are not sustainable. B. Subtransmission Lines 7. The 11 kV feeder breakers are in a condition similar to those of the Fifth Project. They have also suffered premature failures and need replacement to ensure the sustainability of the transmission system.

1 Based on observations of the line in the Balaju vicinity. 2 Assuming a power factor of 0.85 with nameplate capacity of 15 MVA (2 x 7.5 MVA units) 3 The Kali Gandaki Hydroelectric Project includes a 132 kV line to the Pokhara vicinity. If timely, the resulting

substation could include distribution (11 kV) facilities to serve area loads.

Appendix 3, page 2

8. The 33-11 kV distribution substations constructed under the Sixth Project were well designed, but suffer from numerous common problems. These include inoperative air conditioners, inoperative relaying, never commissioned relaying, lack of spare parts, inoperative meters, problems with the SF6 breakers (Pokhara), inadequate gravel cover, failed carrier systems, etc. Many examples of dangerous repair techniques were noted, including the use of wire to bypass failed breakers and combining feeders onto single breakers. 9. The most pressing problem is the 11 kV feeder circuit breakers, regardless of the Project. In most of the areas visited (Pokhara being an exception), the majority of these breakers have failed to the point that the few surviving feeder breakers are now supplying several circuits. The breakers suffer from poor phase separation, which has resulted in flashover, fragile arc chambers made of glass, lack of spare parts (except at Pokhara), and lack of manuals. In fact, there appears to be no manuals for any of the substation equipment anywhere. This should be a correctable problem that the Nepal Electricity Authority should immediately address. Equipment of this nature cannot be properly maintained without manuals. 10. The general level of maintenance at the substations is very poor. The personnel are, for the most part, willing to perform maintenance and repair, and have demonstrated a high degree of ingenuity in maintaining service with few spare parts, no tools, no manuals, and a very low level of funding for maintenance activities.4 In their present condition, the 11 kV substation switchgear cannot support any significant additional distribution expansion. 11. As in the substations, the line personnel have demonstrated a high level of adaptability to the lack of equipment and tools even to the point of transporting the PSC poles by bicycle and installing transformers with pulleys, but these techniques inevitably compromise the levels of maintenance and expansion that the distribution system needs to become viable in scope and revenue-generation potential.5 12. The distribution circuit rehabilitation6 appears to have been adequately implemented. These efforts have expanded to the point that rehabilitation initiatives undertaken under the Fifth Project have been overshadowed by subsequent projects and further area expansion or rehabilitation efforts, and are therefore difficult to discern. The resulting growth has, however, engendered 11 kV feeders, which are much too long (many are over 12 km and some are over 25 km) to serve future increases in load as are many of the 400/230 circuits.7 The typical long 11 kV feeder serves only about 350 kV at present, which effectively disguises the fact that they are much too long to be economical and technically sound.8 13. The 400/230-volt distribution feeders also suffer from the same excessive length problem as their 11 kV counterparts. These should be limited to about 300 meters. Several

4 As an example of precarious maintenance and repair procedures, some of the “spot” repairs are dangerous to

personnel and have increased the probability of catastrophic failure of the 11 kV system in the event of a close in fault, which the paralleled equipment would not be able to interrupt.

5 Except for Pokhara, the substations are operating without the full complement of 11 kV circuit breakers, and have no spare parts and no manuals. The remaining breakers, though still serviceable, will probably fail after interrupting a few faults and/or after an indeterminable number of open/close operations.

6 The Fifth Project included the rehabilitation of four existing distribution systems, and the creation of a new system at Damak.

7 The 11 kV feeders would normally be limited to about 12 km with “Dog” conductor for proper voltage regulation and optimization of losses.

8 These overly long feeders are typically installed as a result of political and social pressures to provide electricity to outlying areas. As a result, these long 11 kV lines are consuming resources and generating losses, the costs of which far exceed the resulting revenue.

Appendix 3, page 3