aspi 3% 5% 11% fc research eps (lkr) adj for … · initiating coverageanalyst fc research :...

TRANSCRIPT

Initiating Coverage

FC Research Analyst: Michelle Weerasinghe

SRI LANKA

CEYLON TOBACCO COMPANY PLC BUY

CTC.N0000 JULY 2015

“Fags Drive Healthy Profits”

Current Price: LKR 890.0 Fair Value: LKR 1,000.0

Ceylon Tobacco Company PLC, member of British American Tobacco is expected

to accelerate its earnings potential to achieve a CAGR of 16% 2015E-2017E. CTC

is expected to generate higher sales volumes through reversing its historical

volume trend attributing to higher domestic purchasing power, prospects in

tourism and increased raids curtailing spread of illicit tobacco products while

margins are likely to expand via price increases over and above the tax increase.

CTC trades at expensive multiples justified by stronger growth leading to our

fair value of LKR 1,000.0 providing an overall return of 23% over 18 months. BUY

Boost in per capita income to drive revenue to 14% CAGR 2015E-2017E: Sri

Lanka’s increasing disposable income resulting from higher GDP per capita and

lower cost of living are likely to support volumes with tourist arrivals expected to

grow by c.15% p.a. Increased efforts by government in limiting the spread of

unauthorized and illicit tobacco products may further boost volumes. We expect

volumes to grow by c.4% through 2015E and 2016E (tobacco production

increased by 12% during Jan-Apr 2015). We expect revenue to grow 49% in

2015E-2017E growing 17% each in 2015E and 2016E and 9% in 2017E.

Margins to expand over cost pass through effect: We expect CTC’s margins

(Operating Profit / Gross Revenue) to reach 18% by 2017E as CTC’s monopoly

status allowing the company pass on the cost increases and levy increases on to

the consumer which had an only exception in 2014. Further, margins are

expected to expand with consumers switching to higher branded products

resulting from growing affordability.

CTC to provide a 23% return over 18 months period: Our fair value for CTC stands

at LKR 1,000.0 [DCF based LKR 971.7, PER based LKR 1,047.1 and DDM based LKR

956.1]. CTC is expected to provide a total return of 23% including a DY of 11%.

Risks: A significant increase in tax would drive prices over and above what

consumers can afford affecting both volumes and margins.

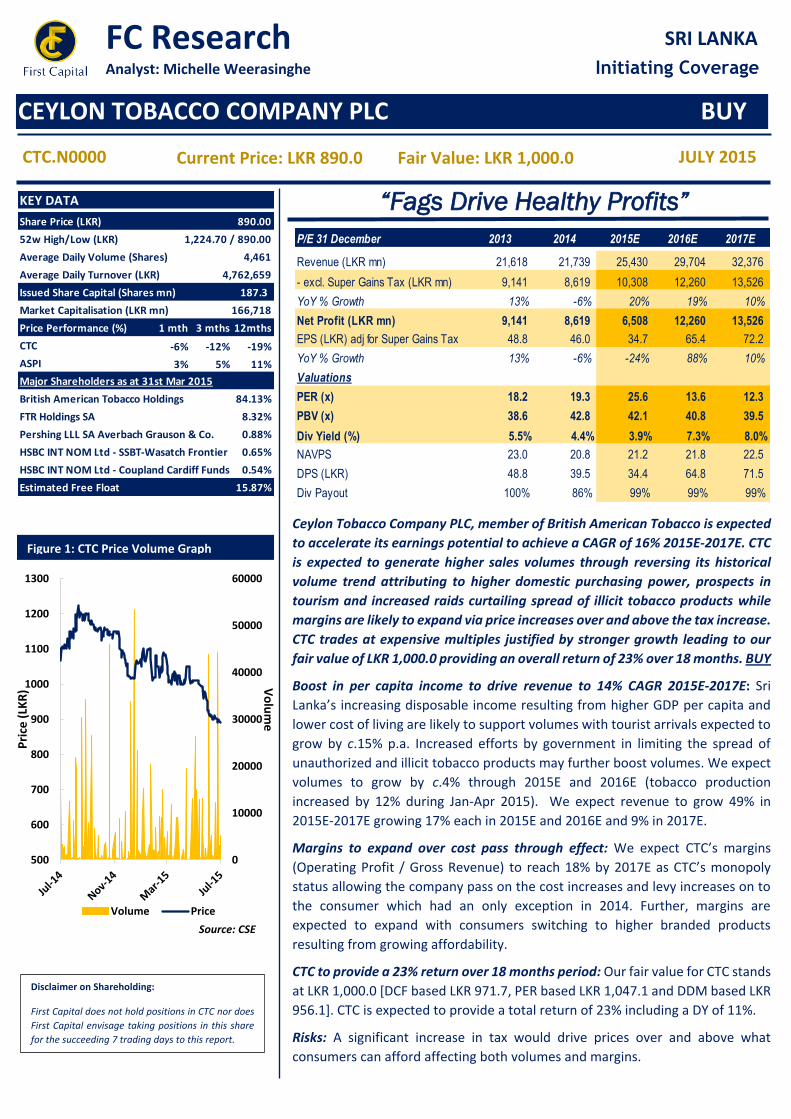

Figure 1: CTC Price Volume Graph

Disclaimer on Shareholding:

First Capital does not hold positions in CTC nor does

First Capital envisage taking positions in this share

for the succeeding 7 trading days to this report.

Source: CSE

0

10000

20000

30000

40000

50000

60000

500

600

700

800

900

1000

1100

1200

1300

Vo

lum

e

Pri

ce (

LKR

)

Volume Price

KEY DATA

Share Price (LKR)

52w High/Low (LKR)

Average Daily Volume (Shares)

Average Daily Turnover (LKR)

187.3

Price Performance (%) 1 mth 3 mths 12mths

CTC -6% -12% -19%

ASPI 3% 5% 11%

84.13%

8.32%

0.88%

0.65%

0.54%

4,762,659

890.00

4,461

1,224.70 / 890.00

HSBC INT NOM Ltd - Coupland Cardiff Funds PLC

Issued Share Capital (Shares mn)

Market Capitalisation (LKR mn) 166,718

Major Shareholders as at 31st Mar 2015

British American Tobacco Holdings

FTR Holdings SA

Pershing LLL SA Averbach Grauson & Co.

HSBC INT NOM Ltd - SSBT-Wasatch Frontier

Estimated Free Float 15.87%

P/E 31 December 2013 2014 2015E 2016E 2017E

Revenue (LKR mn) 21,618 21,739 25,430 29,704 32,376

- excl. Super Gains Tax (LKR mn) 9,141 8,619 10,308 12,260 13,526

YoY % Growth 13% -6% 20% 19% 10%

Net Profit (LKR mn) 9,141 8,619 6,508 12,260 13,526

EPS (LKR) adj for Super Gains Tax 48.8 46.0 34.7 65.4 72.2

YoY % Growth 13% -6% -24% 88% 10%

Valuations

PER (x) 18.2 19.3 25.6 13.6 12.3

PBV (x) 38.6 42.8 42.1 40.8 39.5

Div Yield (%) 5.5% 4.4% 3.9% 7.3% 8.0%

NAVPS 23.0 20.8 21.2 21.8 22.5

DPS (LKR) 48.8 39.5 34.4 64.8 71.5

Div Payout 100% 86% 99% 99% 99%

FC Research

2

“Fags Driving Healthy Profits”

1.0 Introduction

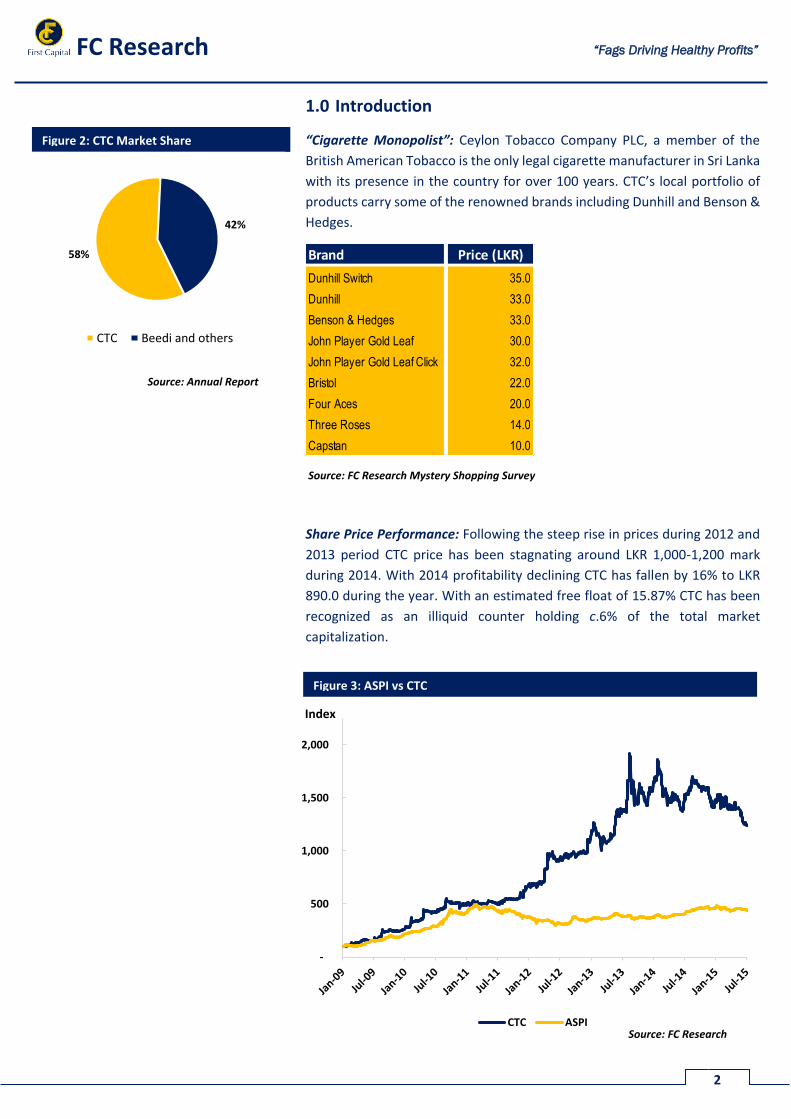

“Cigarette Monopolist”: Ceylon Tobacco Company PLC, a member of the

British American Tobacco is the only legal cigarette manufacturer in Sri Lanka

with its presence in the country for over 100 years. CTC’s local portfolio of

products carry some of the renowned brands including Dunhill and Benson &

Hedges.

Share Price Performance: Following the steep rise in prices during 2012 and

2013 period CTC price has been stagnating around LKR 1,000-1,200 mark

during 2014. With 2014 profitability declining CTC has fallen by 16% to LKR

890.0 during the year. With an estimated free float of 15.87% CTC has been

recognized as an illiquid counter holding c.6% of the total market

capitalization.

Figure 3: ASPI vs CTC

Figure 2: CTC Market Share

58%

42%

CTC Beedi and others

Source: FC Research Mystery Shopping Survey

Source: Annual Report

-

500

1,000

1,500

2,000

Index

CTC ASPI

Brand Price (LKR)

Dunhill Switch 35.0

Dunhill 33.0

Benson & Hedges 33.0

John Player Gold Leaf 30.0

John Player Gold Leaf Click 32.0

Bristol 22.0

Four Aces 20.0

Three Roses 14.0

Capstan 10.0

Source: FC Research

FC Research

3

“Fags Driving Healthy Profits”

2.0 Boost in per capita income to drive revenue to 14%

CAGR 2015E-2017E

Volumes to grow in 2015E and 2016E before reverting back to declines: We

expect CTC volumes to grow c.4% each in 2015E and 2016E reversing the

continuous declines, primarily led by higher disposable income levels and

tourism. Following the temporary growth in volumes we expect CTC to revert

back to a declining with 2.5% decline expected in 2017E.

Source: CBSL and www.priu.gov.lk

Figure 4: Growth in GDP per capita

3,625

6,000

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

6,500

USD

CAGR 8%

Figure 5: Cigarette Volumes

-11%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

-11,000

-9,000

-7,000

-5,000

-3,000

-1,000

1,000

3,000

5,000

GrowthSticks ('m)

Quantity of Cigarettes Issued by Customs (LHS)

Growth in Cigarettes Issued (RHS)Source: Sri Lanka Customs, FC Research Estimates

FC Research

4

“Fags Driving Healthy Profits”

GDP per capita to grow at 8%: We expect Sri Lanka’s per capita GDP to grow

at an annual average of 8% during 2014-2020E. Mean household income has

increased at a 12% CAGR 2007-10 and 8% CAGR 2010-13. We expect the

household income to grow at 8% level, which in turn would enable more

consumer affordability of purchasing CTC brands.

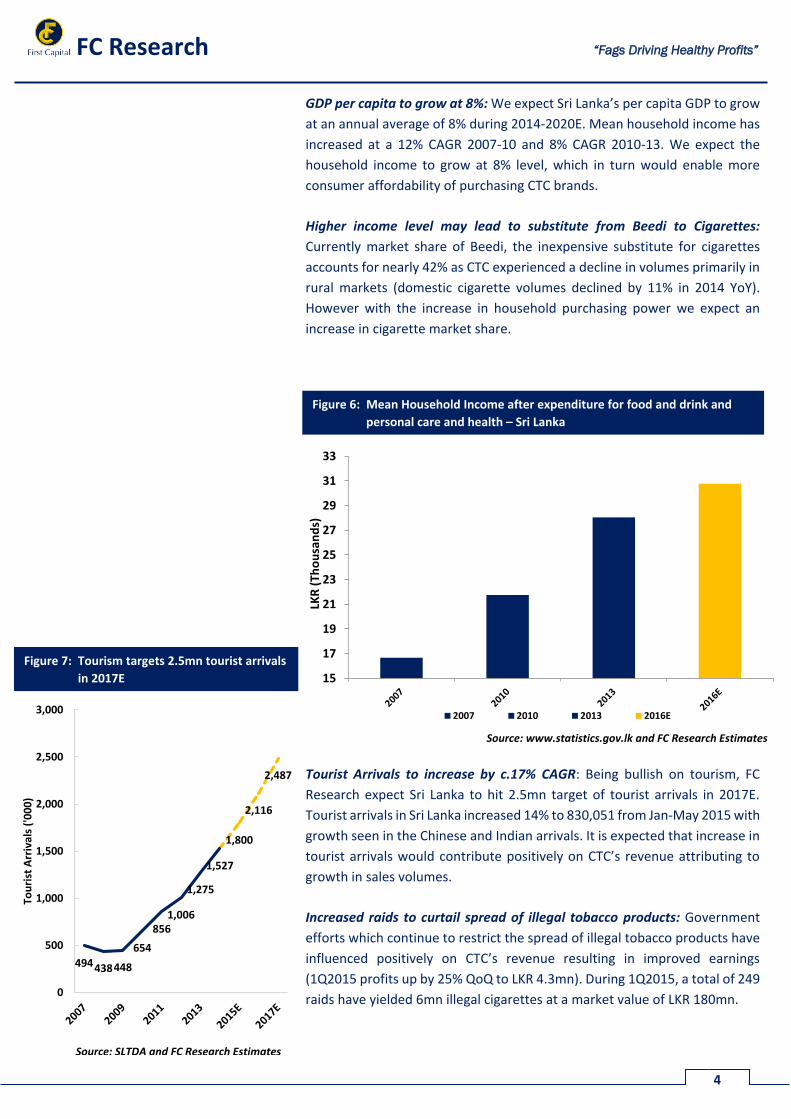

Higher income level may lead to substitute from Beedi to Cigarettes:

Currently market share of Beedi, the inexpensive substitute for cigarettes

accounts for nearly 42% as CTC experienced a decline in volumes primarily in

rural markets (domestic cigarette volumes declined by 11% in 2014 YoY).

However with the increase in household purchasing power we expect an

increase in cigarette market share.

Tourist Arrivals to increase by c.17% CAGR: Being bullish on tourism, FC

Research expect Sri Lanka to hit 2.5mn target of tourist arrivals in 2017E.

Tourist arrivals in Sri Lanka increased 14% to 830,051 from Jan-May 2015 with

growth seen in the Chinese and Indian arrivals. It is expected that increase in

tourist arrivals would contribute positively on CTC’s revenue attributing to

growth in sales volumes.

Increased raids to curtail spread of illegal tobacco products: Government

efforts which continue to restrict the spread of illegal tobacco products have

influenced positively on CTC’s revenue resulting in improved earnings

(1Q2015 profits up by 25% QoQ to LKR 4.3mn). During 1Q2015, a total of 249

raids have yielded 6mn illegal cigarettes at a market value of LKR 180mn.

Figure 6: Mean Household Income after expenditure for food and drink and

personal care and health – Sri Lanka

15

17

19

21

23

25

27

29

31

33

LKR

(Th

ou

san

ds)

2007 2010 2013 2016E

Figure 7: Tourism targets 2.5mn tourist arrivals

in 2017E

494438448

654

8561,006

1,275

1,527

1,800

2,116

2,487

0

500

1,000

1,500

2,000

2,500

3,000

Tou

rist

Arr

ival

s ('

00

0)

Source: www.statistics.gov.lk and FC Research Estimates

Source: SLTDA and FC Research Estimates

FC Research

5

“Fags Driving Healthy Profits”

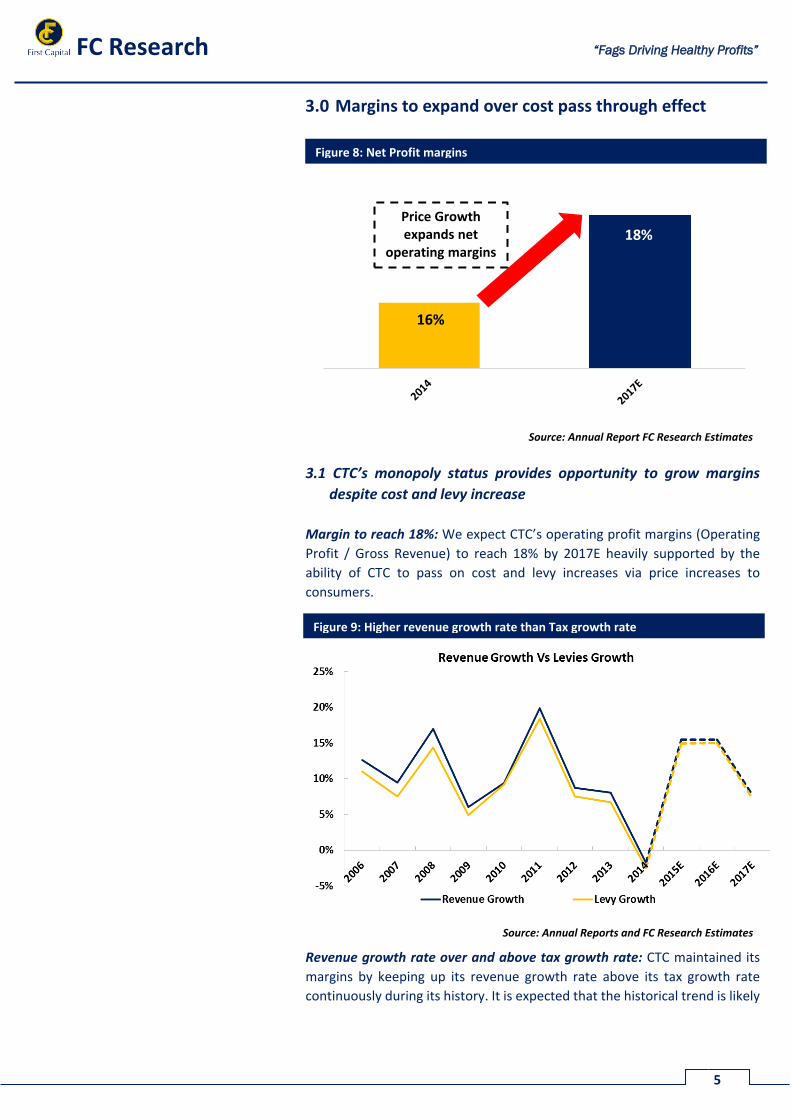

3.0 Margins to expand over cost pass through effect

3.1 CTC’s monopoly status provides opportunity to grow margins

despite cost and levy increase

Margin to reach 18%: We expect CTC’s operating profit margins (Operating

Profit / Gross Revenue) to reach 18% by 2017E heavily supported by the

ability of CTC to pass on cost and levy increases via price increases to

consumers.

Revenue growth rate over and above tax growth rate: CTC maintained its

margins by keeping up its revenue growth rate above its tax growth rate

continuously during its history. It is expected that the historical trend is likely

Figure 8: Net Profit margins

Source: Annual Report FC Research Estimates

Source: Annual Reports and FC Research Estimates

Figure 9: Higher revenue growth rate than Tax growth rate

16%

18%Price Growth expands net

operating margins

FC Research

6

“Fags Driving Healthy Profits”

to be repeated (2016E revenue growth rate 15.4% and tax growth rate

15.0%), consequently driving revenues above its tax growth.

Annual price increases: CTC generally re-prices its products twice annually.

The price increases are expected to increase revenue per share thus

contributing to the growth in earnings.

3.2 Investment into brands & new products

CTC has been constantly investing in their products adding value to its local

consumers. CTC had undertaken a pack modernization initiative on its JPGL

brand while the company introduced two premium priced variants to further

strengthen the image of the brand, which included the introduction of

capsule technology - JPGL Click offering the “SWITCH” technology.

3.3 Government regulations influence margins but unlikely to

squeeze CTC

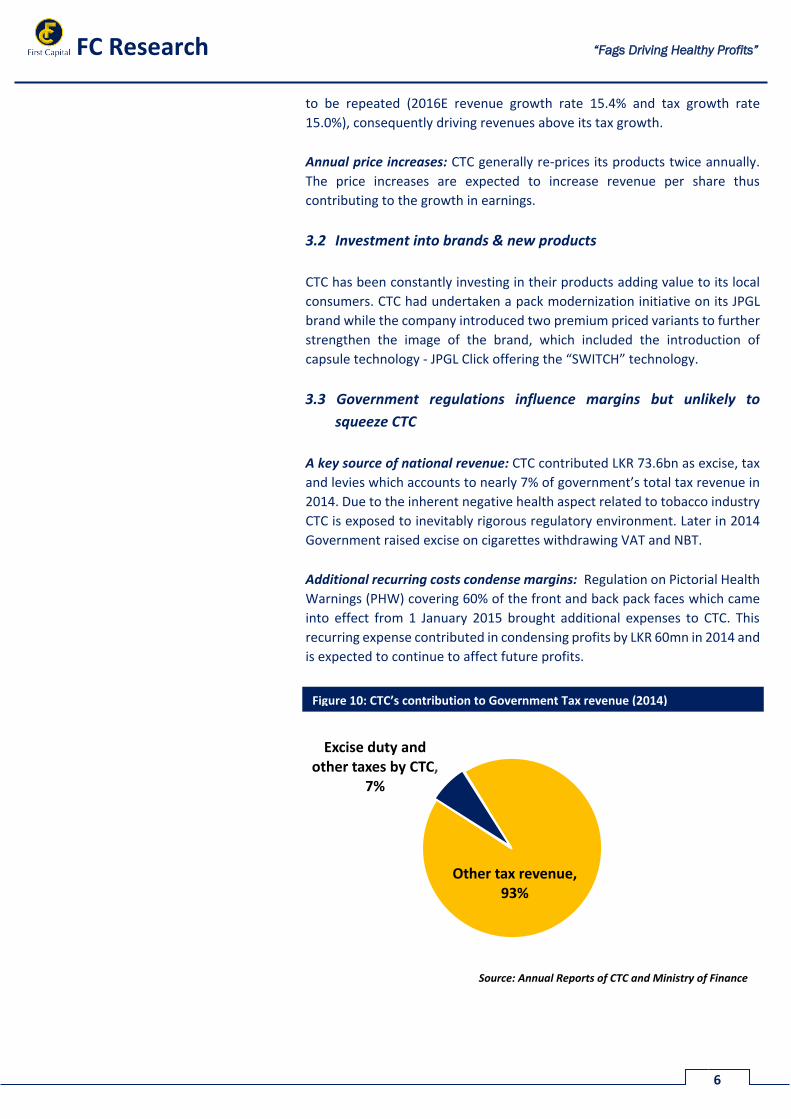

A key source of national revenue: CTC contributed LKR 73.6bn as excise, tax

and levies which accounts to nearly 7% of government’s total tax revenue in

2014. Due to the inherent negative health aspect related to tobacco industry

CTC is exposed to inevitably rigorous regulatory environment. Later in 2014

Government raised excise on cigarettes withdrawing VAT and NBT.

Additional recurring costs condense margins: Regulation on Pictorial Health

Warnings (PHW) covering 60% of the front and back pack faces which came

into effect from 1 January 2015 brought additional expenses to CTC. This

recurring expense contributed in condensing profits by LKR 60mn in 2014 and

is expected to continue to affect future profits.

Other tax revenue, 93%

Excise duty and other taxes by CTC,

7%

Figure 10: CTC’s contribution to Government Tax revenue (2014)

Source: Annual Reports of CTC and Ministry of Finance

FC Research

7

“Fags Driving Healthy Profits”

4.0 CTC to provide a 23% return

CTC Earnings CAGR of 16% 2015E-17E: We expect CTC’s earnings to reach

LKR 13.5bn in 2017E (16% CAGR). CTC earnings are likely to reach LKR 10.3 bn

(up 20% before Super Gains Tax) and LKR 12.3bn (up 19%). FC Research has

written off the super gains tax against the 2015E resulting in a net profit of

LKR 6.5 bn.

Super Gains Tax assumptions: We have assumed that the super gains tax

which is a one off tax, has been charged by the Government on the taxable

profit for 2013 in 2015E.

4.1 CTC Total Return of 23% over 18 months period

Fair Value of LKR 1,000.0 over 18 months period: FC Research target price

for CTC stands at LKR 1,000.0 providing a capital gain of 12% based on the

company’s value as at Dec 2016. The target price of LKR 1,000.0 is based on

Figure 11: Earnings to grow at 16% CAGR 2015E-2017E

4,000

6,000

8,000

10,000

12,000

14,000

16,000

LKR

(M

n)

CAGR 16%

Source: Annual Reports and FC Research Estimates

P/E 31 December 2013 2014 2015E 2016E 2017E

Revenue (LKR mn) 21,618 21,739 25,430 29,704 32,376

- excl. Super Gains Tax (LKR mn) 9,141 8,619 10,308 12,260 13,526

YoY % Growth 13% -6% 20% 19% 10%

Net Profit (LKR mn) 9,141 8,619 6,508 12,260 13,526

EPS (LKR) adj for Super Gains Tax 48.8 46.0 34.7 65.4 72.2

YoY % Growth 13% -6% -24% 88% 10%

Valuations

PER (x) 18.2 19.3 25.6 13.6 12.3

PBV (x) 38.6 42.8 42.1 40.8 39.5

Div Yield (%) 5.5% 4.4% 3.9% 7.3% 8.0%

NAVPS 23.0 20.8 21.2 21.8 22.5

DPS (LKR) 48.8 39.5 34.4 64.8 71.5

Div Payout 100% 86% 99% 99% 99%

FC Research

8

“Fags Driving Healthy Profits”

the average price of LKR 971.7 via DCF valuations, LKR 1,047.10 via PER based

valuations and LKR 956.10 via DDM based valuations.

Dividend Yield of 11%: FC Research expects a DPS of LKR 34.4 for 2015E out

of which LKR 3.45 DPS has already been paid. A balance dividend of LKR 30.95

is expected to be paid for 2015 (provided company pays Super Gains Tax

during the year). We expect the company to a further LKR 64.79 DPS on 2016E

earnings. Thereby we expect overall dividend of LKR 95.74 over the next 18

months resulting in a dividend yield of 11%.

4.2 Discounted Cash flow Valuation

Return

Target Price 1,000.0

Current Price 890.0

Capital Gain (LKR) 110.0

Dividend FY16E (LKR) 95.7

Capital Gain % 12%

Dividend Yield % 11%

Total Return % 23%

Valuations 2016E

NPV 172,679

(+) Cash 9,338

(-) Debt -

Total Value of Equity 182,017

No. of shares 187

Value of Equity per share 972

COE (K e )

Rf 11%

Rm 18%

1.0

Ke=Rf+ (Rm-Rf) 18%

Ke 18%

Kd 6%

D/E Assumption 40 / 60

Terminal Growth (%) 3%

WACC 13%

WACC

972 11% 12% 13% 14% 15%

1% 1001 920 852 794 745

2% 1084 986 906 839 783

3% 1188 1068 972 893 827

4% 1322 1170 1052 957 880

5% 1499 1301 1152 1036 943

WACC

Terminal

Growth (%)

Expected CTC price for 2016E

DCF Valuation based target price 971.7

PER based target price 1,047.1

DDM based target price 956.1

Average Target Price 991.6

Target price (Rounded up) 1,000.0

FC Research

9

“Fags Driving Healthy Profits”

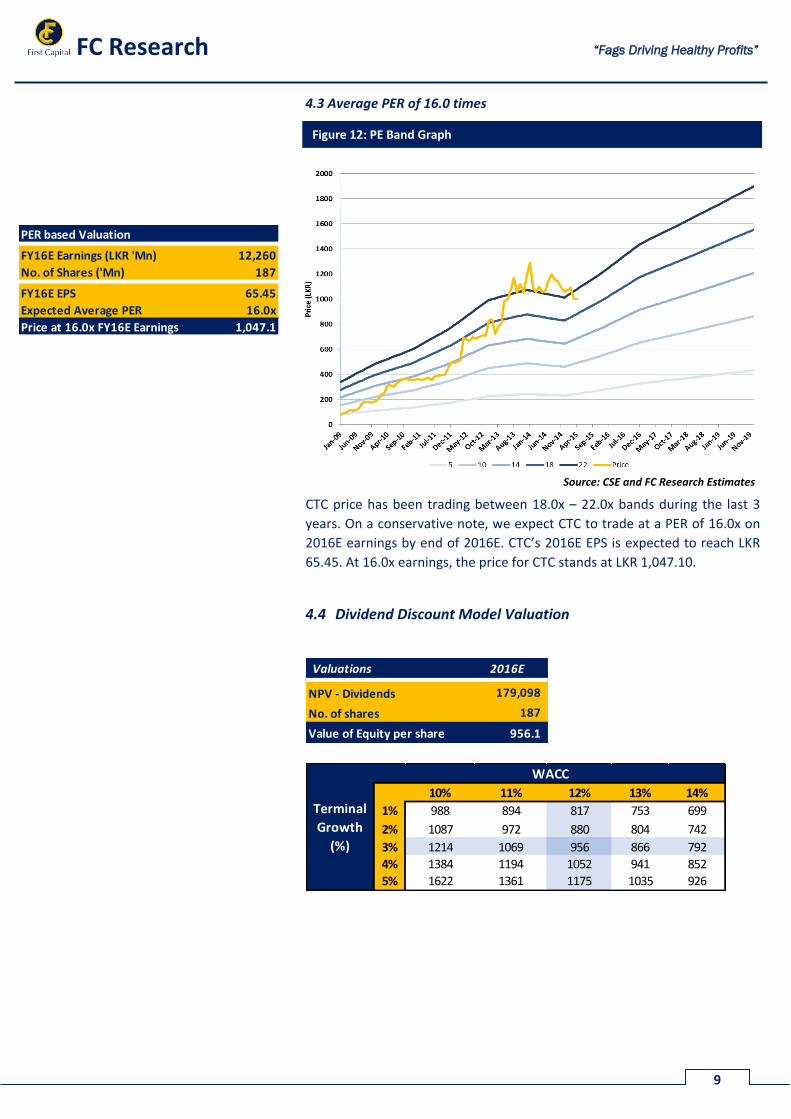

4.3 Average PER of 16.0 times

CTC price has been trading between 18.0x – 22.0x bands during the last 3

years. On a conservative note, we expect CTC to trade at a PER of 16.0x on

2016E earnings by end of 2016E. CTC’s 2016E EPS is expected to reach LKR

65.45. At 16.0x earnings, the price for CTC stands at LKR 1,047.10.

4.4 Dividend Discount Model Valuation

Valuations 2016E

NPV - Dividends 179,098

No. of shares 187

Value of Equity per share 956.1

Figure 12: PE Band Graph

Source: CSE and FC Research Estimates

PER based Valuation

FY16E Earnings (LKR 'Mn) 12,260

No. of Shares ('Mn) 187

FY16E EPS 65.45

Expected Average PER 16.0x

Price at 16.0x FY16E Earnings 1,047.1

956 10% 11% 12% 13% 14%

1% 988 894 817 753 699

2% 1087 972 880 804 742

3% 1214 1069 956 866 792

4% 1384 1194 1052 941 852

5% 1622 1361 1175 1035 926

Terminal

Growth

(%)

WACC

FC Research

10

“Fags Driving Healthy Profits”

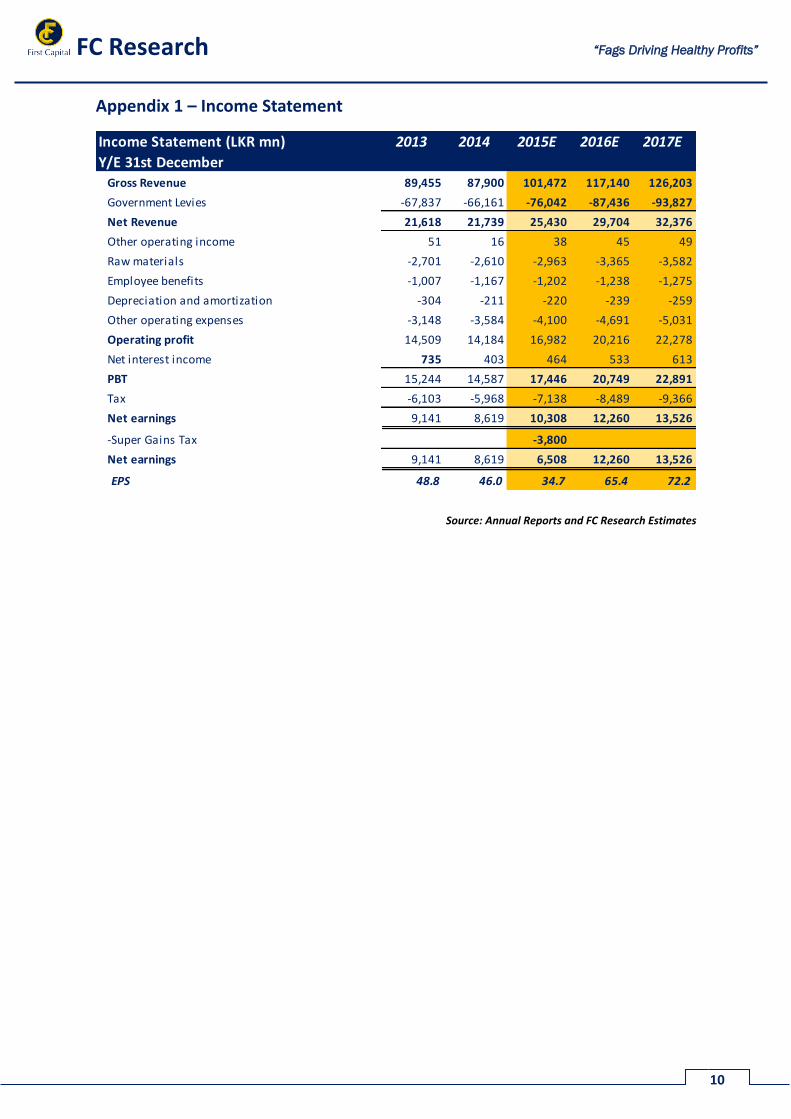

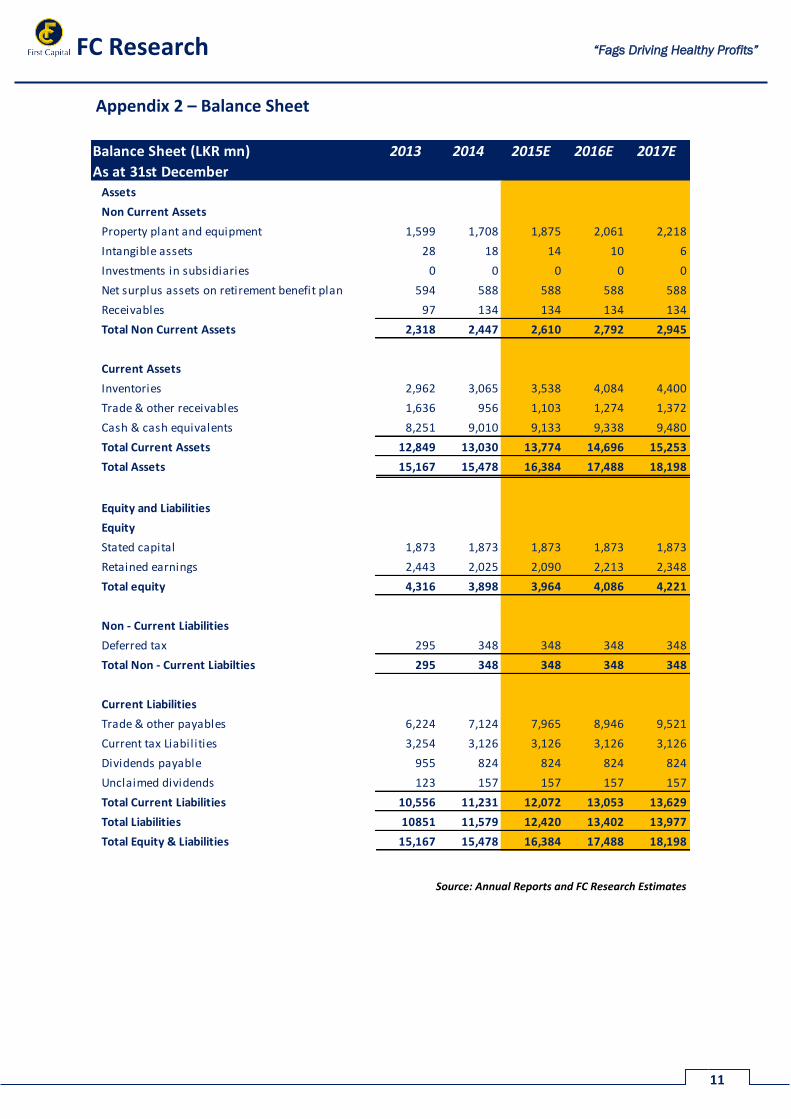

Appendix 1 – Income Statement

Source: Annual Reports and FC Research Estimates

Income Statement (LKR mn) 2013 2014 2015E 2016E 2017E

Y/E 31st December

Gross Revenue 89,455 87,900 101,472 117,140 126,203

Government Levies -67,837 -66,161 -76,042 -87,436 -93,827

Net Revenue 21,618 21,739 25,430 29,704 32,376

Other operating income 51 16 38 45 49

Raw materials -2,701 -2,610 -2,963 -3,365 -3,582

Employee benefits -1,007 -1,167 -1,202 -1,238 -1,275

Depreciation and amortization -304 -211 -220 -239 -259

Other operating expenses -3,148 -3,584 -4,100 -4,691 -5,031

Operating profit 14,509 14,184 16,982 20,216 22,278

Net interest income 735 403 464 533 613

PBT 15,244 14,587 17,446 20,749 22,891

Tax -6,103 -5,968 -7,138 -8,489 -9,366

Net earnings 9,141 8,619 10,308 12,260 13,526

-Super Gains Tax -3,800

Net earnings 9,141 8,619 6,508 12,260 13,526

EPS 48.8 46.0 34.7 65.4 72.2

FC Research

11

“Fags Driving Healthy Profits”

Appendix 2 – Balance Sheet

Source: Annual Reports and FC Research Estimates

Balance Sheet (LKR mn) 2013 2014 2015E 2016E 2017E

As at 31st DecemberAssets

Non Current Assets

Property plant and equipment 1,599 1,708 1,875 2,061 2,218

Intangible assets 28 18 14 10 6

Investments in subsidiaries 0 0 0 0 0

Net surplus assets on retirement benefit plan 594 588 588 588 588

Receivables 97 134 134 134 134

Total Non Current Assets 2,318 2,447 2,610 2,792 2,945

Current Assets

Inventories 2,962 3,065 3,538 4,084 4,400

Trade & other receivables 1,636 956 1,103 1,274 1,372

Cash & cash equivalents 8,251 9,010 9,133 9,338 9,480

Total Current Assets 12,849 13,030 13,774 14,696 15,253

Total Assets 15,167 15,478 16,384 17,488 18,198

Equity and Liabilities

Equity

Stated capital 1,873 1,873 1,873 1,873 1,873

Retained earnings 2,443 2,025 2,090 2,213 2,348

Total equity 4,316 3,898 3,964 4,086 4,221

Non - Current Liabilities

Deferred tax 295 348 348 348 348

Total Non - Current Liabilties 295 348 348 348 348

Current Liabilities

Trade & other payables 6,224 7,124 7,965 8,946 9,521

Current tax Liabilities 3,254 3,126 3,126 3,126 3,126

Dividends payable 955 824 824 824 824

Unclaimed dividends 123 157 157 157 157

Total Current Liabilities 10,556 11,231 12,072 13,053 13,629

Total Liabilities 10851 11,579 12,420 13,402 13,977

Total Equity & Liabilities 15,167 15,478 16,384 17,488 18,198

FC Research

12

“Fags Driving Healthy Profits”

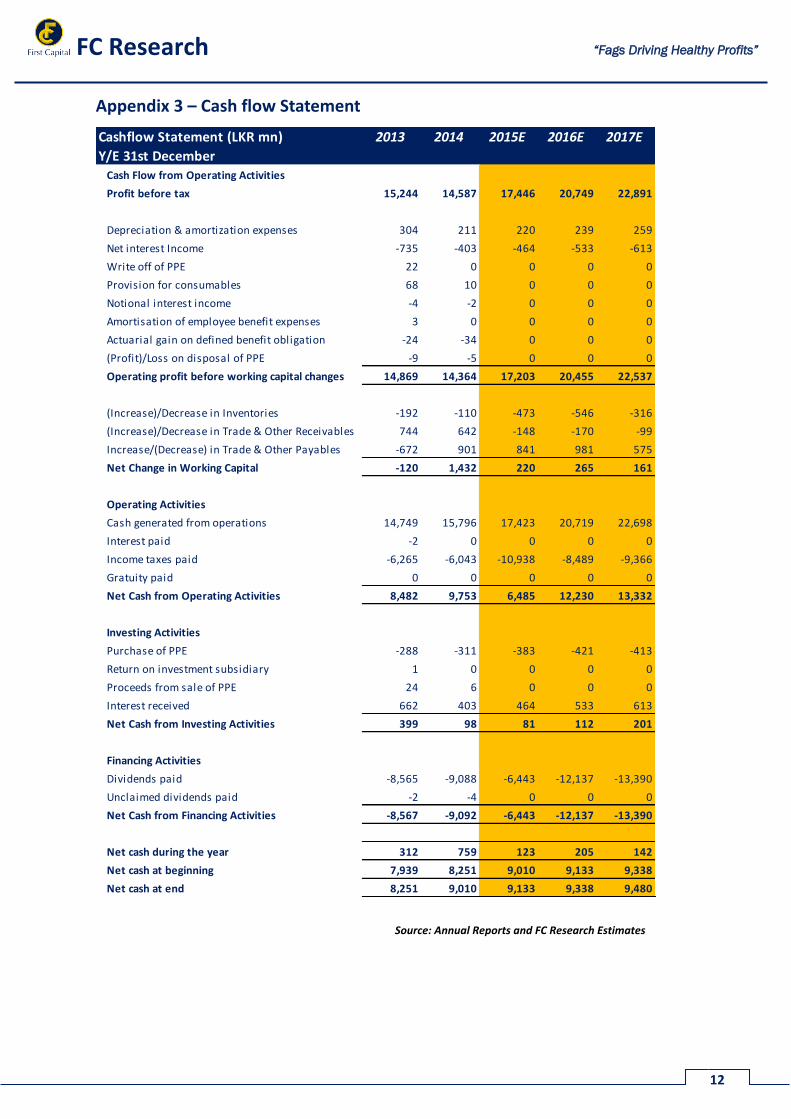

Appendix 3 – Cash flow Statement

Source: Annual Reports and FC Research Estimates

Cashflow Statement (LKR mn) 2013 2014 2015E 2016E 2017E

Y/E 31st DecemberCash Flow from Operating Activities

Profit before tax 15,244 14,587 17,446 20,749 22,891

Depreciation & amortization expenses 304 211 220 239 259

Net interest Income -735 -403 -464 -533 -613

Write off of PPE 22 0 0 0 0

Provision for consumables 68 10 0 0 0

Notional interest income -4 -2 0 0 0

Amortisation of employee benefit expenses 3 0 0 0 0

Actuarial gain on defined benefit obligation -24 -34 0 0 0

(Profit)/Loss on disposal of PPE -9 -5 0 0 0

Operating profit before working capital changes 14,869 14,364 17,203 20,455 22,537

(Increase)/Decrease in Inventories -192 -110 -473 -546 -316

(Increase)/Decrease in Trade & Other Receivables 744 642 -148 -170 -99

Increase/(Decrease) in Trade & Other Payables -672 901 841 981 575

Net Change in Working Capital -120 1,432 220 265 161

Operating Activities

Cash generated from operations 14,749 15,796 17,423 20,719 22,698

Interest paid -2 0 0 0 0

Income taxes paid -6,265 -6,043 -10,938 -8,489 -9,366

Gratuity paid 0 0 0 0 0

Net Cash from Operating Activities 8,482 9,753 6,485 12,230 13,332

Investing Activities

Purchase of PPE -288 -311 -383 -421 -413

Return on investment subsidiary 1 0 0 0 0

Proceeds from sale of PPE 24 6 0 0 0

Interest received 662 403 464 533 613

Net Cash from Investing Activities 399 98 81 112 201

Financing Activities

Dividends paid -8,565 -9,088 -6,443 -12,137 -13,390

Unclaimed dividends paid -2 -4 0 0 0

Net Cash from Financing Activities -8,567 -9,092 -6,443 -12,137 -13,390

Net cash during the year 312 759 123 205 142

Net cash at beginning 7,939 8,251 9,010 9,133 9,338

Net cash at end 8,251 9,010 9,133 9,338 9,480

No.1, Lake Crescent,

Colombo 2

Sales Desk: +94 11 2145 000

Fax: +94 11 2145 050

HEAD OFFICE BRANCHES

No.1, Lake Crescent, Matara Negombo

Colombo 2 No. 24, Mezzanine Floor, No.72A, 2/1,

Sales Desk: +94 11 2145 000 E.H. Cooray Building, Old Chilaw Road,

Fax: +94 11 2145 050 Anagarika Dharmapala Mw, Negombo

Matara

Tel: +94 41 2237 636 Tel: +94 31 2233 299

SALES BRANCHES

CEO Jaliya Wijeratne +94 71 5329 602 Negombo

Priyanka Anuruddha +94 76 6910 035

Colombo Priyantha Wijesiri +94 76 6910 036

Damian Le Grand +94 77 7383 237

Nishantha Mudalige +94 76 6910 041 Matara

Isuru Jayawardana +94 76 7084 953 Sumeda Jayawardana +94 76 6910 038

Anushka Buddhika +94 77 9553 613

Gamini Hettiarachchi +94 76 6910 039

Thushara Abeyratne +94 76 6910 037

Nishani Prasangi +94 76 6910 033

Ishanka Wickramanayaka +94 77 7611 200

RESEARCH

Dimantha Mathew +94 11 2145 016 Amanda Lokugamage +94 11 2145 018

Reshan Wediwardana +94 11 2145 017 Michelle Weerasinghe +94 11 2145 018

FIRST CAPITAL GROUP

HEAD OFFICE BRANCHES

No. 2, Deal Place, Matara Kurunegala Kandy

Colombo 3 No. 24, Mezzanine Floor, No. 6, 1st Floor, No.213-215,

Tel: +94 11 2576 878 E.H. Cooray Building, Union Assurance Building, Peradeniya Road,

Anagarika Dharmapala Mawatha, Rajapihilla Mawatha, Kandy

Matara Kurunegala

Tel: +94 41 2222 988 Tel: +94 37 2222 930 Tel: +94 81 2236 010

Disclaimer:

This Review is prepared and issued by First Capital Equities (Pvt) Ltd. based on information in the public domain, internally developed and other sources, believed to be correct.

Although all reasonable care has been taken to ensure the contents of the Review are accurate, First Capital Equities (Pvt) Ltd and/or its Directors, employees, are not

responsible for the correctness, usefulness, reliability of same. First Capital Equities (Pvt) Ltd may act as a Broker in the investments which are the subject of this document or

related investments and may have acted on or used the information contained in this document, or the research or analysis on which it is based, before its publication. First

Capital Equities (Pvt) Ltd and/or its principal, their respective Directors, or Employees may also have a position or be otherwise interested in the investments referred to in this

document. This is not an offer to sell or buy the investments referred to in this document. This Review may contain data which are inaccurate and unreliable. You hereby waive

irrevocably any rights or remedies in law or equity you have or may have against First Capital Equities (Pvt) Ltd with respect to the Review and agree to indemnify and hold

First Capital Equities (Pvt) Ltd and/or its principal, their respective directors and employees harmless to the fullest extent allowed by law regarding all matters related to your

use of this Review. No part of this document may be reproduced, distributed or published in whole or in part by any means to any other person for any purpose without prior

permission.

First Capital Equities (Pvt) Ltd