at-home business activities just a fact of life? or a ... · at-home business activities… a fact...

TRANSCRIPT

At-Home Business Activities...

Just a Fact of Life?... or a Nightmare???

SPONSORED BY

AAt-Home Business Activities…

A Fact of Life or Nightmare??!!

Presented by:

Michael C. D’Orlando, CIC, LIA, CPIA11 Lake Shore Drive

Amesbury, MA 01913(978) 314-5743

________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

I. Overview

A. Some statistics

1. The U.S. Bureau of Labor Statistics puts the number of home-based businesses currently operating at 18.3 million. Other organizations say the number is closer to 38 million

2. In 2004, studies indicated that 1 in 10 U.S. households had some type of home-based business … In 2010, some estimates cited 1 in 3!

3. According to a IIAA study, almost 60% of home-based businesses were uninsured

5. National Underwriter reported that 11% of the uninsured businesses experienced a loss

B. Outlook for the future ... The numbers are expected to increase due to:

1. Technological advances

a. “Telecommuting” has become a viable and attractive option for an increasing number of employers and employees

b. The high quality and relatively low cost of equipment (computers, printers, fax machines, etc.) has made it easier to set up and maintain a business at home

2. The state of the economy

a. More and more people need to supplement their income and are finding creative ways to do it at home

b. More and more people are losing their income due to businesses down-sizing (or worse!) and may have no other alternatives

Michael C. D'Orlando, CIC, LIA, CPIA Page 1

Business Activities At Home 11/12

Examples of Home-Based Business Activities (From Mississippi State Univ. CA$HING IN ON BUSINESS OPPORTUNITIES curriculum)

Personal/Individual/Self Improvement

Accounting Adult Care- day, residential and post surgery health care, adult-in-home foster care Animals - grooming, sitting, exercising, training, boarding, breeding Apartment guide Attorney Automotive - rental, painting, cleaning and repair Beauty services - nails, hair care, facials, massage, beauty products Bicycle, moped motorcycle sales and repair Books - binding, sales, collecting Bridal consultant plus gowns for rent or sale Calligraphy Chauffeur- limousine service Clock repair Clothing and sewing-related - alterations, monograms, exchange, needlework, hemming, reweaving, tailoring, refurbishing vintage clothing, custom sewing, clothing for disabled, clothes for hard-to-fit, drapery making, custom window treatments, baby specialty items Correspondence for others Costumes - design, manufacturing, sales, repair Counselor - marriage, family, career, children, rehabilitation, financial, and investments Coupon mailer service Day Care - child day care center, group family day care, family day care home Designing and painting murals in churches, homes, offices and restaurants Digital watch repair Get-away weekends for couples, families Genealogical research Greeting cards/notes, design, sell Health improvement - exercise, body toning, electrolysis, stop smoking clinics, weight control diet preparation, recreation for older adults Hospitality services - catering, mobile catering, clowning, parties for children and adults Image consultant - color analysis, wardrobe analysis and planning Income tax preparer Jewelry design, sales, repair Laundry and ironing Messenger service Shopping Service - clothing, groceries, interior design, maintenance services Towing

Services to the Home

Appliance repair Appraisals - antiques, books, collectibles, art objects Architecture Auctioneer Awnings - design and make canvas awnings and shades, installation Building storage sheds Burglar alarm sales and service Carpet installation and cleaning Carpentry Cement casting - curbing, patio block, etc. Chain saw service Chair caning Crystal and china repair Custom rug making - braided, hooked, woven Electronic sales and repair Energy consultant Fence installation and repair Firewood Floor refinishing Furniture - build, design, repair, refinish, upholster, sell Garden furniture - rewebbing, repainting, repadding, reupholstering, reweaving Home handyman service Household cleaning Housesitting I'll finish your project" service Interior design and decorating Lamp repair Mobile lock service Musical instrument maintenance and repair Oriental rug repair Pest control Plants - potting, sales, care at home Pool cleaning and repair Porcelain refinishing (tubs, sinks, etc.) Real estate sales Rental agency - furniture, tools, appliances, party items, etc. Screen and storm window service - sell, repair, install Security patrol Small engine repair Tree service - treat, trim diseased trees, tree removal, replacement Welding Window and wall washing Yard/Lawn maintenance - landscaping, pruning of shrubbery, flower bed preparation, fertilizing, specialized outdoor lighting, design and installation

Michael C. D'Orlando, CIC, LIA, CPIA Page 2

Business Activities At Home 11/12

Services to Other Businesses

Accounting or book keeping Advertising- write, copy layout, artwork Agent - Literary, sales, insurance Answering service Art rental - plan and display art in businesses Booking agent representing musicians, models, actors, actresses and other temporary help Builder's cleanup service Burglar alarm sales and service Business chauffeur Calligraphy-diplomas, scrolls, certificates Clipping service - newspapers and magazines Computer - analysis training, programming, repair, sales, hardware, software, web site developer Consultant Credit investigator - check on history of people applying for credit Data and word processing Delivery/messenger service Employment agency - match workers with job opportunities. Teach classes in developing resumes, interview techniques, etc. Event planning Free-lance writer Income tax preparation Jewelry and watch repair - contract with jewelry stores to repair jobs they take in Mailing list - develop/print labels Marketing research Newsletter research, writer, editor Notary public Office machines repair Pest control Printing - layout, edit Proofreader Public relations Sales representativeSecretarial service Security patrol Sharpening service Shopping service Signs - design, building, install Translator Travel agent Trucking - long/short distance Welcome new residents - provide community information and referral

Sales Businesses

Art - prints, original art Bait and tackle Balloons Candles, cosmetics, seasonings, household items Florist

Homemade food products - specialty processed food, breads, cakes, cookies, pastry maker for restaurants and delicatessens, candy, catering gourmet meals for delivery or pick up Household items Insurance Mail order Personalized products Used clothing

Other Business

Bed and breakfast Beekeeping Boat rental - boat only or charter fishing trips Christmas tree farm Coin dealer Coordinate exhibitions - organize antiques shows, art fairs, flea markets, fund-raising drivesGoat production - sell meat or milk to ethnic markets, health food stores, and coops. Make and sell cheese. Gun repair Herbs - grow, dry, sell Holiday greenery Organic vegetable growing Pick-your-own operations Restorations - antiques, cars, boatsRoadside vegetable/fruit stands

Crafts and Related Arts

Candlemaking Ceramics Decoys Dollmaking, doll clothes, dollhouses Dried flower arrangements Framing Glass blowing Jewelry - design, repair, restyling, sales Lampshades Leather work Metal design Miniatures Ornaments Personalized sketches of house, boat, animals Pottery Quilting Selling Crafts supplies Silk-screening Soft sculpture Spinning Stained glass Teaching crafts Toys Weaving Woodworking

Michael C. D'Orlando, CIC, LIA, CPIA Page 3

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 4

Business Activities At Home 11/12

II. How Does the HO-2011 Define “Business”?

A. The definition begins by saying anything that falls under the “customary” definition of “trade”, “profession” or “occupation” is a “business”, regardless of how much or how little time is spent doing it

“Trade”, “Profession” and “Occupation” are not defined terms in the policy…

According to Black’s Law Dictionary:

“Trade – Trade is not a technical word and is ordinarily used in three senses: (1) in that of exchanging goods or commodities by barter or by buying and selling for money; (2) in that of a business or occupation generally; (3) in that of a mechanical employment in contradistinction to the learned professions, agriculture or the liberal arts. An occupation or regular means of livelihood...One’s calling...Gainful employment...”

“Profession – A vocation or occupation requiring special, usually advanced, education, knowledge and skill. The labor and skill involvedin a profession is predominantly mental or intellectual, rather than physical or manual. The term originally contemplated only theology, law and medicine, but as applications of science and learning are extended to other departments of affairs, other vocations also receive the name, which implies professed attainments in special knowledge as distinguished from mere skill...”

“Occupation – That which principally takes up one’s time, thought and energies, especially one’s regular business or employment; also, whatever one follows as a means of making a livelihood. Particular business, profession, trade or calling which engages individual’s timeand efforts; employment in which one regularly engages or vocation of one’s life.”

3. "Business" means:

a. A trade, profession or occupation engaged in on a full-time, part-time or occasional basis; or...

Michael C. D'Orlando, CIC, LIA, CPIA Page 5

Business Activities At Home 11/12

B. The definition continues...

Even if it is not a “trade, profession or occupation”, it is stilla “business” if engaged in for money or other compensationexcept ...

(1) Activities which generated more than $2,000 in compensation in the 12 months prior to policy inception

(2) Expense reimbursement for volunteer activities

(3) Home day care for no compensation other than mutual exchange of services

(4) Home day care provided to a relative of an insured

b. Any other activity engaged in for money or other compensation, except the following:

(1) One or more activities, not described in (2) through (4) below, for which no "insured" receives more than $2,000 in total compensation for the 12 months before the beginning

of the policy period;

(2) Volunteer activities for which no money is received other than payment for expenses incurred to perform the activity;

(3) Providing home day care services for which no compensa-tion is received, other than the mutual exchange of such

services; or

(4) The rendering of home day care services to a relative of an "insured".

Michael C. D'Orlando, CIC, LIA, CPIA Page 6

Business Activities At Home 11/12

C. In determining if an activity is a “business”, most courts, prior to the HO – 2000, have looked for two elements to be present:

a. Continuity

b. Expectation or possibility of profit or gain

D. According to information from the International Risk Management Institute (IRMI), the business exclusion is most often upheld by courts...

Example 1

Pacific Indemnity Ins. Co. v. Aetna Cas. & Sur. Co. (Conn. 1997). The insureds boarded horses for a fee. The insureds’ own horse kicked and injured an independent contractor who they had hired to care for all of the horses. He sued for injuries and the Homeowners carrier denied coverage stating that this was a business. The insureds argued that this was not their occupation or livelihood. They both worked full-time elsewhere, but the Connecticut Supreme Court ruled that this was a business activity

Example 2

Wiley v. Travelers Ins. Co. (Okla. 1974), the insured had a full-time job as a salesman and raised and sold St. Bernards as a “hobby”. One of his dogs bit someone who had gone to the house in response to an ad the insured had run in the newspaper. The claim was denied based on the business exclusion. The Oklahoma Supreme Court upheld the exclusion, stating that "profit motive is all that is necessary to make an activity both a hobby and a business pursuit...Whether there is or is not actual profit is immaterial...Profit motive, not actual profit, makes a pursuit a business pursuit."

Michael C. D'Orlando, CIC, LIA, CPIA Page 7

Business Activities At Home 11/12

Example 3 Excerpts from the State of Oregon Court of Appeals transcripts, Hiebert v. Farmers Ins. Co. of Oregon, 18 P.3d 397, (Or. App. 2001), 98C-15722; CA A108666

“Plaintiff owns and operates the Detroit Lake Marina, which is a business that consumes approximately 90 percent of his professional time. Plaintiff also owns Hiebert Construction. Hiebert Construction is in the business of dismantling and transporting scrap metal...

On occasion, plaintiff has retained some of the scrap materials for his personal use. In 1989, while plaintiff was loading scrap metal at a location in Montana, he learned of a rock crusher that could not be used as scrap metal but whose owner wished to dispose of it. After returning to Oregon, plaintiff spoke with two or three people about possible uses for the rock crusher...At that time, plaintiff did not expect to make a profit or to gain any income or compensation from the rock crusher...

On September 19, 1993, he purchased the rock crusher from its owner for its per-ton scrap metal value. Plaintiff paid for the crusher by means of an offset against the amount that was owed to him for his work dismantling and transporting scrap metal...

Plaintiff spoke to Schultz and another acquaintance, Fleming, about the crusher. Plaintiff hoped that Fleming would buy the crusher for what plaintiff had paid for it, plus his transportation expenses; he was also "looking" to get "something on top of that."

Plaintiff did not succeed in finding a purchaser...In October 1994, a child was killed while playing on the machine. The personal representative of the child's estate initiated a wrongful death action against plaintiff. The homeowner's policy that defendant issued to plaintiff contained an exclusion from coverage for losses for "bodily injury arising from or during the course of businesspursuits of an insured." (Boldface in original.) The policy defined "business" as "any full or part-time trade, profession or occupation."

Relying on that exclusion, defendant declined to defend against the wrongful death action and declined to pay plaintiff's losses resulting from that action. Plaintiff settled the wrongful death claim for $40,800, then brought this action for breach of the duty to defend and breach of the duty to pay...The trial court determined that defendant did not have a duty under the insurance policy to pay the claim and entered summary judgment accordingly.

Michael C. D'Orlando, CIC, LIA, CPIA Page 8

Business Activities At Home 11/12

Plaintiff also points to evidence that he "had no intent to make a profit" from the rock crusher. Defendant, in effect, responds that the exclusion plainly applies to plaintiff's purchase and retention of the rock crusher despite the possible irregular or occasional nature of plaintiff's scrap-metal business activities.

We agree with defendant. The interpretation of an insurance policy is a question of law...The primary goal in construing an insurance contract is to ascertain the intention of the parties. To that end, we begin with the terms and conditions of the policy itself. If a term at issue is not defined in the policy, we consider the plain meaning of the term.

Here, the question is whether plaintiff's acquisition and storage of, and attempts to sell or trade, the rock crusher constituted "business pursuits" within the meaning of the policy's exclusion for such activities. The policy does not define the phrase "business pursuits" per se. It does, however, define what "business" means. According to the definition in the policy, business is "any full or part-time trade, profession or occupation."

Considered in isolation, the terms "trade," "profession," and "occupation," might give rise to some uncertainty as to whether a business endeavor must be a principal one or otherwise a regular pursuit. (3) Considered in context, however, no such uncertainty reasonably exists. The policy definition of "business" expressly refers to any trade, profession, or occupation.

Equally significant, it expressly includes part-time trades, professions, or occupations. Those qualifiers eliminate any possible ambiguity and make it clear that the exclusion encompasses occasional or secondary business pursuits. Consequently, based on the text of the exclusion and its related definition of "business," we conclude that the policy exclusion for losses arising out of "business pursuits" applies to all compensating activities of an insured, including the insured's principal gainful activity or activities and all incidental or occasional ones.

The evidence is undisputed that plaintiff purchased the rock crusher for the amount of its scrap-metal value; that he transported it to Oregon for the purpose of selling it or trading it for some other item of equipment; that he made efforts toward that end, including discussing the machine with various acquaintances and painting it to make it more saleable; and that, although he did not necessarily expect to achieve a profit from the sale or trade of the crusher, he hoped and intended to be compensated for at least its purchase price and his expenses in transporting it to Oregon. Those activities constituted "business pursuits" within the meaning of the policy exclusion.”

Michael C. D'Orlando, CIC, LIA, CPIA Page 9

Business Activities At Home 11/12

E. Of course, there are two sides to every story...

Example 1

“Side 1”

Callahan v. American Motorist Insurance Co. (NY 1968).The insured was a real estate broker working from his home.While stopping by to pick up a key to a house listed by this broker, another realtor was injured on the insured’s premises and he sued. The carrier denied coverage and the court agreed that this activity fell within the business exclusion.

“The other side”

Georgia Farm Bureau Ins. Co. v. Caster (Ga. Ct. App. 2001). Again, the insured was a realtor with an office in her home. A client went to the house to meet with her and fell down a step into the sunken living room. He sued for his injuries and the carrier denied coverage. However, The policy had an exception for activities usual to non-business pursuits. The court determined that maintaining a home was usual to a non-business activity and the exclusion did not apply.

Michael C. D'Orlando, CIC, LIA, CPIA Page 10

Business Activities At Home 11/12

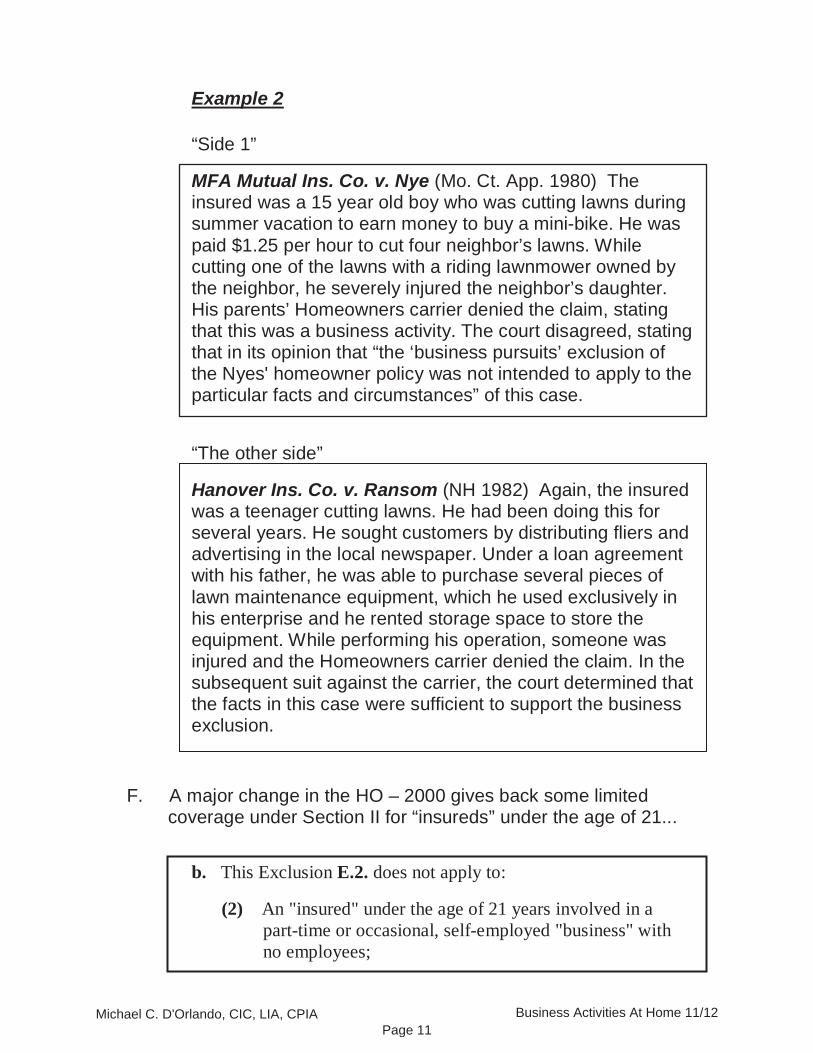

Example 2

“Side 1”

MFA Mutual Ins. Co. v. Nye (Mo. Ct. App. 1980) The insured was a 15 year old boy who was cutting lawns during summer vacation to earn money to buy a mini-bike. He was paid $1.25 per hour to cut four neighbor’s lawns. While cutting one of the lawns with a riding lawnmower owned by the neighbor, he severely injured the neighbor’s daughter. His parents’ Homeowners carrier denied the claim, stating that this was a business activity. The court disagreed, stating that in its opinion that “the ‘business pursuits’ exclusion of the Nyes' homeowner policy was not intended to apply to the particular facts and circumstances” of this case.

“The other side”

Hanover Ins. Co. v. Ransom (NH 1982) Again, the insured was a teenager cutting lawns. He had been doing this for several years. He sought customers by distributing fliers and advertising in the local newspaper. Under a loan agreement with his father, he was able to purchase several pieces of lawn maintenance equipment, which he used exclusively in his enterprise and he rented storage space to store the equipment. While performing his operation, someone was injured and the Homeowners carrier denied the claim. In the subsequent suit against the carrier, the court determined that the facts in this case were sufficient to support the business exclusion.

F. A major change in the HO – 2000 gives back some limited coverage under Section II for “insureds” under the age of 21...

b. This Exclusion E.2. does not apply to:

(2) An "insured" under the age of 21 years involved in a part-time or occasional, self-employed "business" with no employees;

Michael C. D'Orlando, CIC, LIA, CPIA Page 11

Business Activities At Home 11/12

HO 00 03 05 11 Page 3 of 24

SECTION I – PROPERTY COVERAGES A. Coverage A – Dwelling 1. a.

b.

2.

B. Coverage B – Other Structures 1.

2. a.

b.

c.

d.

3.

A.A

C. Coverage C – Personal Property 1. Covered Property

a.

b.

2. Limit For Property At Other Locations a. Other Residences

C,

(1)

(a)

(b)

(2)

b. Self-storage Facilities

C,

(1)

(a)

(b)

(2)

Michael C. D'Orlando, CIC, LIA, CPIA Page 12

Business Activities At Home 11/12

III. How Does the HO-2011 Address Business Activity?

A. Cov. A – Dwelling

1. Cov. A makes no reference to “business”

2. “Business” activity would have no effect on Dwelling coverage unless other conditions have been violated (fraud, concealment, misrepresentation, etc.)

B. Cov. B – Other Structures

Does not cover:

1. Structures rented or held for rental...unless used solely asa private garage

2. Structures from which any “business” is conducted

3. Structures used to store “business” property unless the “business” property is solely owned by an “insured” or tenant and is not gaseous or liquid fuel

A. Coverage A – Dwelling1. We cover:

a. The dwelling on the "residence premises" shown in the Declarations, including structures attached to the dwelling; and

b. Materials and supplies located on or next to the "residence premises" usedto construct, alter or repair the dwelling or other structures on the "residence premises".

2. We do not cover land, including land on which the dwelling is located.

B. Coverage B – Other Structures1. We cover other structures on the "residence premises" set apart from the dwelling by

clear space. This includes structures connected to the dwelling by only a fence, utility line, or similar connection.

2. We do not cover:a. Land, including land on which the other structures are located;b. Other structures rented or held for rental to any person not a tenant of the dwelling,

unless used solely as a private garage; c. Other structures from which any "business" is conducted; ord. Other structures used to store "business" property. However, we do cover a

structure that contains "business" property solely owned by an "insured" or a tenant of the dwelling, provided that "business" property does not include gaseous or liquid fuel, other than fuel in a permanently installed fuel tank of a vehicle or craftparked or stored in the structure.

Michael C. D'Orlando, CIC, LIA, CPIA Page 13

Business Activities At Home 11/12

c. $1,500 on watercraft of all types, includingtheir trailers, furnishings, equipment andoutboard engines or motors.

d. $1,500 on trailers or semitrailers not usedwith watercraft of all types.

e. $1,500 for loss by theft of jewelry, watches,furs, precious and semiprecious stones.

f. $2,500 for loss by theft of firearms andrelated equipment.

g. $2,500 for loss by theft of silverware, silver- plated ware, goldware, gold-plated ware,platinumware, platinum-plated ware andpewterware. This includes flatware, hollow- ware, tea sets, trays and trophies made ofor including silver, gold or pewter.

h. $2,500 on property, on the "residencepremises", used primarily for "business"purposes.

i. $500 on property, away from the "residencepremises", used primarily for "business"purposes. However, this limit does not applyto loss to electronic apparatus and otherproperty described in Categories j. and k.below.

j. $1,500 on electronic apparatus and access- ories, while in or upon a "motor vehicle",but only if the apparatus is equipped to beoperated by power from the "motor vehicle's"electrical system while still capable ofbeing operated by other power sources.Accessories include antennas, tapes, wires,records, discs or other media that can beused with any apparatus described in thisCategory j.

k. $1,500 on electronic apparatus and access- ories used primarily for "business" whileaway from the "residence premises" andnot in or upon a "motor vehicle". The appar- atus must be equipped to be operated bypower from the "motor vehicle's" electricalsystem while still capable of being operatedby other power sources.

Accessories include antennas, tapes, wires,records, discs or other media that can beused with any apparatus described in thisCategory k.

Page 4 of 22

D. Coverage D – Loss Of Use

The limit of liability for Coverage D is the total limit for the coverages in 1. Additional Living Expense, 2. Fair Rental Value and 3. Civil Authority Prohibits Use below.

1. Additional Living Expense

If a loss covered under Section I makes that part of the "residence premises" where you reside not fit to live in, we cover any necessary increase in living expenses incurred by you so that your household can maintain its normal standard of living.

Payment will be for the shortest time required to repair or replace the damage or, if you permanently relocate, the shortest time required for your household to settle elsewhere.

2. Fair Rental Value

If a loss covered under Section I makes that part of the "residence premises" rented to others or held for rental by you not fit to live in, we cover the fair rental value of such premises less any expenses that do not continue while it is not fit to live in

Payment will be for the shortest time required to repair or replace such premises.

3. Civil Authority Prohibits Use

If a civil authority prohibits you from use of the "residence premises" as a result of direct damage to neighboring premises by a Peril Insured Against, we cover the loss as provided in 1.

Additional Living Expense and 2. Fair Rental Value above for no more than two weeks.

4. Loss Or Expense Not Covered

We do not cover loss or expense due to cancellation of a lease or agreement.

The periods of time under 1. Additional Living Expense, 2. Fair Rental Value and 3. Civil Authority Prohibits Use above are not limited by expiration of this policy. Page 5 of 22

Michael C. D'Orlando, CIC, LIA, CPIA Page 14

Business Activities At Home 11/12

C. Cov. C – Personal Property

1. Limited to $2,500 on “residence premises” if used primarily for business (Important change from ’91 edition!)

2. Limited to $500 away from “residence premises” if used primarily for “business”

3. Limited to $1,500 on electronic apparatus away from “residence premises” if used primarily for “business” and if not in a “motor vehicle”, but equipped to operate both by power from a “motor vehicle” and other power sources

4. Business data is not covered

D. Cov. D – Loss of Use

1. Pays loss of rent (Fair Rental Value) up to 30% of the Cov. A limit for that part of the “residence premises” rented or held for rental to others

2. Does not pay for any other loss of business income or extra expense

Michael C. D'Orlando, CIC, LIA, CPIA Page 15

Business Activities At Home 11/12

Section II Exclusions

Coverages E & F Do Not Apply to the Following:

E. 2. "Business"

a. "Bodily injury" or "property damage" arising out of or in connection with a "business" conducted from an "insured location" or engaged in by an "insured", whether or not the "business" is owned or operated by an "insured" or employs an "insured".

This Exclusion E.2. applies but is not limitedto an act or omission, regardless of its nature or circumstance, involving a service or duty rendered, promised, owed, or implied to be provided because of the nature of the "business".

b. This Exclusion E.2. does not apply to:

(1) The rental or holding for rental of an "insured location";

(a) On an occasional basis if used only as a residence;

(b) In part for use only as a residence, unless a single family unit is intended for use by the occupying family to lodge more than two roomers or boarders; or

(c) In part, as an office, school, studio or private garage; and

(2) An "insured" under the age of 21 years involved in a part-time or occasional, self-employed "business" with no employees;

3. Professional Services

"Bodily injury" or "property damage" arising outof the rendering of or failure to render professional services;

F. 4. "Bodily injury" to any person eligible to receive any benefits voluntarily provided or required to be provided by an "insured" under any:

a. Workers' compensation law;

Michael C. D'Orlando, CIC, LIA, CPIA Page 16

Business Activities At Home 11/12

E. Coverage E – Personal Liability and Coverage F – Medical Payments to Others

1. No coverage for BI or PD arising out of or in connection with a “business”, regardless of where it occurs and regardless of the status of the insured whether as owner, operator or employee of a “business”

2. The exclusion does not apply to rental of an “insured location”:

a. On an occasional basis if used only as a residence

b. For the additional units in a 1-4 family dwelling, or for up to two roomers or boarders in the “insured’s” unit

c. For use in part as an office, school, studio or private garage

3. The exclusion does not apply to an “insured” under 21, self- employed, operating on a part-time or occasional basis, with no employees

4. No Professional Liability coverage (“rendering or failure to render professional services”)

5. No coverage for anyone employed by an “insured” who is eligible to collect Workers’ Compensation benefits

Michael C. D'Orlando, CIC, LIA, CPIA Page 17

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 18

Business Activities At Home 11/12

Learning Objective 3: To be able to explain the various business endorsements which can be added to the Homeowners Policy.

IV. Homeowners Policy Business Endorsements

A. HO 04 42 – Permitted Incidental Occupancies

1. Coverage applies only to the “business” described

2. Provides coverage for scheduled “other structures” used for the described “business”

Removes the scheduled structures from the Cov. B limit and applies a separate limit chosen

3. Removes the $2,500 limitation on business property on premises…

a. Property used on premises for the described “business” is subject to the full Cov. C limit

b. The $500 limitation for business property off premisesstill applies

4. Provides premises liability coverage for the “necessary or incidental use of the ‘residence premises’ to conduct the ‘business’ described in the schedule” … No off-premise coverage

Michael C. D'Orlando, CIC, LIA, CPIA Page 19

Business Activities At Home 11/12

HOMEOWNERSHO 04 12 05 11

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

HO 04 12 05 11 Page 1 of 1

INCREASED LIMITS ON BUSINESS PROPERTY SCHEDULE

Increase In Limit Of Liability Total Limit Of Liability $ $$ $$ $

SECTION I – PROPERTY COVERAGES Coverage C – Personal Property 3. Special Limits Of Liability

a. 3.h.

(1) (a) (b)

(2)

b. 3.i.

C.

Michael C. D'Orlando, CIC, LIA, CPIA Page 20

Business Activities At Home 11/12

B. HO 04 12 – Increased Limits on Business Property

1. Used to increase business property limit

a. Limit on premises can be increased to $10,000

b. Off-premises limit is automatically increased to 20% of on-premises limit

2. Increase does not apply to:

a. Property in storage

b. Samples

c. Property held for sale

d. Property sold and held for delivery

e. Property for a “business” conducted on the “residence premises”

Michael C. D'Orlando, CIC, LIA, CPIA Page 21

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 22

Business Activities At Home 11/12

C. HO 24 71 – Business Pursuits

1. Does NOT apply if the “business” is owned or financially controlled by the “insured” … Coverage applies only if the“insured” is an employee, not an employer

2. Liability and Medical Payments only, for scheduled “business” and scheduled “insured”

3. Excludes professional liability except for teachers

4. Intended primarily for “insureds” in sales, clerical and teaching

5. Examples of when someone might need this endorsement…

a. Employer’s limits are not adequate

b. Employer’s General Liability policy may have exclusions or limitations not found on the Homeowners policy, such as…

(1) Certain watercraft

(2) Injury to a volunteer (3) Pollution

(4) Coverage territory

c. “Borderline” situations when the CGL carrier denies coverage claiming the action was not “within the scope of employment” and the HO carrier claims it was business related…ex. Social activities with clients, membership in certain civic and non-profit organizations such as Rotary Club, Lions Club, JayCees, etc.

Michael C. D'Orlando, CIC, LIA, CPIA Page 23

Business Activities At Home 11/12

HOMEOWNERSHO 04 97 05 11

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

HO 04 97 05 11 Page 1 of 2

HOME DAY CARE COVERAGE ENDORSEMENT SCHEDULE

SECTION I – PROPERTY

Number Of Persons Receiving Day Care Services:

Business Location 1. 2.

1.

2.

Limit Of Liability Description Of Other Structure(s) $

$

$

SECTION I – PROPERTY COVERAGES 1.

BHO 00 02, HO 00 03 HO 00 05A HO 00 06

2. C Personal Property, 3.h.

h.

(1)(2)(3)

C

SECTION II – LIABILITY COVERAGES E F

1.2.

SECTION II – EXCLUSIONS II E.2.

1.

a.

Michael C. D'Orlando, CIC, LIA, CPIA Page 24

Business Activities At Home 11/12

D. HO 04 97 – Home Day Care Coverage

1. Similar to the HO 04 42 Permitted Incidental Occupancies…

a. Coverage applies only to the “business” described

b. Provides coverage for scheduled “other structures” used for the described “business”

Removes the scheduled structures from the Cov. B limit and applies a separate limit chosen

c. Removes the $2,500 limitation on business property on premises…

(1) Property used on premises for the described “business” is subject to the full Cov. C limit

(2) The $500 limitation still applies to business property off premises

2. Provides liability coverage for BI and PD “arising out of home day care services regularly provided by an ‘insured’”

Michael C. D'Orlando, CIC, LIA, CPIA Page 25

Business Activities At Home 11/12

Page 2 of 2 HO 04 97 05 11

b. c.d.

e. f.

g.

h.i.j. k.l.

2.

SECTION II – CONDITIONS

II – Conditions, A. Limit Of Liability B. Severability Of Insurance

A. Limit Of Liability

1. Aggregate Limit Of Liability

EF

E.

a.

b.c.d.

2. Sublimit Of Liability

F

F.

B. Severability Of Insurance

Michael C. D'Orlando, CIC, LIA, CPIA Page 26

Business Activities At Home 11/12

3. Contains an annual aggregate limit for liability and medical payments

A. Limit Of Liability

Aggregate Limit of Liability: Our total limit of liability in an annual policy period for the sum of damagespayable under Coverage E and medical expensepayable under Coverage F will be an annual ag-gregate limit of liability that corresponds to the dollar amount shown in the Declarations for Cov-erage E. This is the most we will pay regardless of the number of "occurrences", "insureds", claims made or persons injured.

Michael C. D'Orlando, CIC, LIA, CPIA Page 27

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 28

Business Activities At Home 11/12

E. HO 04 40 – Structures Rented to Others

1. Provides property and liability coverage for scheduled structures on the “residence premises”

2. Must be rented to others for use as a private residence

3. Will provide building coverage up to the stated limit

Michael C. D'Orlando, CIC, LIA, CPIA Page 29

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 30

Business Activities At Home 11/12

E. HO 24 70 – Additional Residence Rented to Others - 1, 2, 3 or 4Families

1. Expands the definition of “insured location” to include additional 1-4 family residences scheduled on the endorsement

2. Provides liability coverage only … No property coverage

Michael C. D'Orlando, CIC, LIA, CPIA Page 31

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 32

Business Activities At Home 11/12

F. HO 24 72 – Incidental Farming Personal Liability

1. For the “gentleman/gentlewoman” farmer

2. HO business exclusion does not apply to farming operations described in schedule

3. Can be used for incidental farming operations on or away from the “residences premises”

4. ISO Personal Lines Manual states the farming activity must be “incidental to the use of the premises as a dwelling, and the income derived from the farming operations is not theinsured's primary source of income”

5. Intended for very minor farming activities … For greater farming exposure, but still not the insured’s primary occupation, use the Farmers Personal Liability Endorsement HO 24 73 or, for true farming operations, use the Commercial Lines Farm Form

Michael C. D'Orlando, CIC, LIA, CPIA Page 33

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 34

Business Activities At Home 11/12

F. HO 07 01 – Home Business Insurance Coverage

1. Designed as a “Mini-BOP”

2. Eligibility…

a. The home business …

(1) Must be owned by the named insured or by a partnership, joint venture or other organization comprised only of the named insured and resident relatives

(2) Must be operated from the residence premises used primarily for residential purposes

(3) Can be operated from the dwelling and other structures

(4) Can have no more than three employees

(5) Cannot involve…

(a) The manufacture, sale or distribution of food

(b) The manufacture of personal care products (shampoo, hair color, soap, etc.)

(c) The sale or distribution of personal care products manufactured by the insured

b. Gross annual receipts cannot exceed $250,000

3. Designed for four principal business classifications…

a. Officeb. Service c. Salesd. Crafts

Michael C. D'Orlando, CIC, LIA, CPIA Page 35

Business Activities At Home 11/12

Michael C. D'Orlando, CIC, LIA, CPIA Page 36

Business Activities At Home 11/12

4. Coverages … Section I – Property

a. Covers the insured’s property and property of others in the care of the insured, up to the Coverage C limit

b. Provides coverage for…

(1) Accounts Receivable up to $5,000

(2) Business Income & Extra Expense on an “actual loss sustained” basis for up to 12 months

(3) Valuable Papers up to $2,500

c. Increases Cov. C Special Limits on…

(1) Money up to $1,000

(2) Credit Cards up to $1,000

(3) Business property away from premises up to $5,000

5. Section II – Business Liability

a. Similar to the BOP and CGL, provides BI & PD coverage for premises, operations, products and completed operations, as well as personal & advertising injury

b. Limits are on a per occurrence and annual aggregate basis

c. The Additional Coverage “Damage to Property of Others” is increased to $2,500

6. Provides no Professional Liability

Michael C. D'Orlando, CIC, LIA, CPIA Page 37

Business Activities At Home 11/12