atradius country report usa apr2013

TRANSCRIPT

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 1/11

Atradius Country Report

United States – April 2013

Miami

HoustonDallas

Chicago

Los Angeles

New YorkWashington DC

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 2/11

Atradius 2

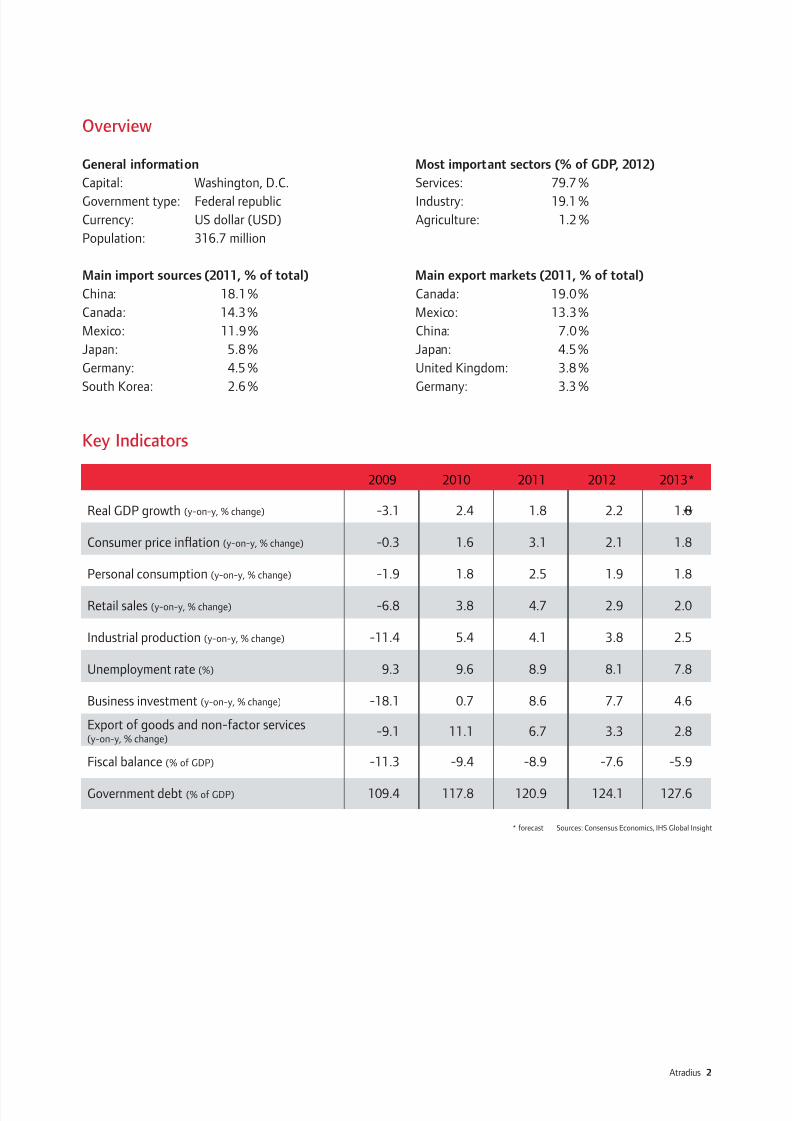

Overview

General information Most important sectors (% of GDP, 2012)

Capital: Washington, D.C. Services: 79.7 %

Government type: Federal republic Industry: 19.1 %

Currency: US dollar (USD) Agriculture: 1.2 %

Population: 316.7 million

Main import sources (2011, % of total) Main export markets (2011, % of total)

China: 18.1% Canada: 19.0%

Canada: 14.3% Mexico: 13.3%

Mexico: 11.9% China: 7.0%

Japan: 5.8% Japan: 4.5%

Germany: 4.5 % United Kingdom: 3.8 %

South Korea: 2.6 % Germany: 3.3 %

Key Indicators

**

2009 2010 2011 2012 2013*

Real GDP growth (y-on-y, % change) -3.1 2.4 1.8 2.2 1.8

Consumer price infation (y-on-y, % change) -0.3 1.6 3.1 2.1 1.8

Personal consumption (y-on-y, % change) -1.9 1.8 2.5 1.9 1.8

Retail sales (y-on-y, % change) -6.8 3.8 4.7 2.9 2.0

Industrial production (y-on-y, % change) -11.4 5.4 4.1 3.8 2.5

Unemployment rate (%) 9.3 9.6 8.9 8.1 7.8

Business investment (y-on-y, % change) -18.1 0.7 8.6 7.7 4.6

Export o goods and non-actor services -9.1 11.1 6.7 3.3 2.8(y-on-y, % change)

Fiscal balance (% o GDP) -11.3 -9.4 -8.9 -7.6 -5.9

Government debt (% o GDP) 109.4 117.8 120.9 124.1 127.6

* orecast Sources: Consensus Economics, IHS Global Insight

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 3/11

Main economic developments

A slowdown of growth in the last quarter of 2012

At the end o February 2013 the US Bureau o Economic Analysis (BEA) estimated that real gross domestic product

(GDP) increased only 0.1% on the previous quarter in Q4 o 2012, compared to a 3.1 % quarterly rise in Q3 (see

chart below). This deceleration in growth can be primarily attributed to lower government spending, decreasing ex-

ports and business inventory investment, and to the impact o Hurricane Sandy on East Coast businesses. However,

private consumption and xed investments did contribute positively to GDP and, despite the weaker perormance in

the last quarter, the US economy grew 2.2 % in 2012.

Sources: Bureau o Economic Analysis, Global Insight.

In March 2013, Consensus Economics orecast or US economic growth was 1.8% or 2013 and 2.8% or 2014.

*orecast

Source: Consensus Forecasts (Survey date March 11, 2013)

Atradius 3

(% change on previous year)

GDP growth

5

4

32

1

0

-1

-2

-3

-4

-52009 2010 2011 2012 2013*

-3.1

2.4 2.2

(Quarter-on-Quarter percentage change)

Real GDP growth

1.8 1.8

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 4/11

Private consumption: push and pull factors in 2013

Consumer condence decreased in March 2013 amid concerns over sharp cuts in government spending and the po-

tential consequences or US economic perormance, i.e. the political wrangling over the set o budget cuts and tax

increases: the so-called ’scal cli’. With no political solution, on March 1st the so-called ’sequester‘ took eect:

i.e. US $85 billion in cuts in ederal government spending through the end o September this year.

Sources: The Conerence Board; Global Insight

However, private consumption has been sustained by the rebound in the housing market that began in early 2012

(see chart below). Generally, house prices are currently increasing across the country. The S&P/Case-Shiller index o

property values in 20 cities increased 8.1% year-on-year in January 2013 ater a 6.8% rise in 2012. Home owners

who have seen their equity rise will be more likely to borrow and to spend while, at the same time, delinquency

rates have stabilised.

Sources: S&P Case Shiller; Global Insight

According to the US Bureau o Labour Statistics, the unemployment rate decreased to 7.7 % in February 2013:

down 0.2 percentage points rom January. IHS Global Insight expects unemployment to decrease to 7.3% in 2013

rom 7.8 % in 2012. However, rms remain hesitant to create new jobs amid uncertainties about the economic

outlook.

Atradius 4

(Index 100 = Neutral)

Consumer confdence

(Rebased house price level index)

National house price developments

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 5/11

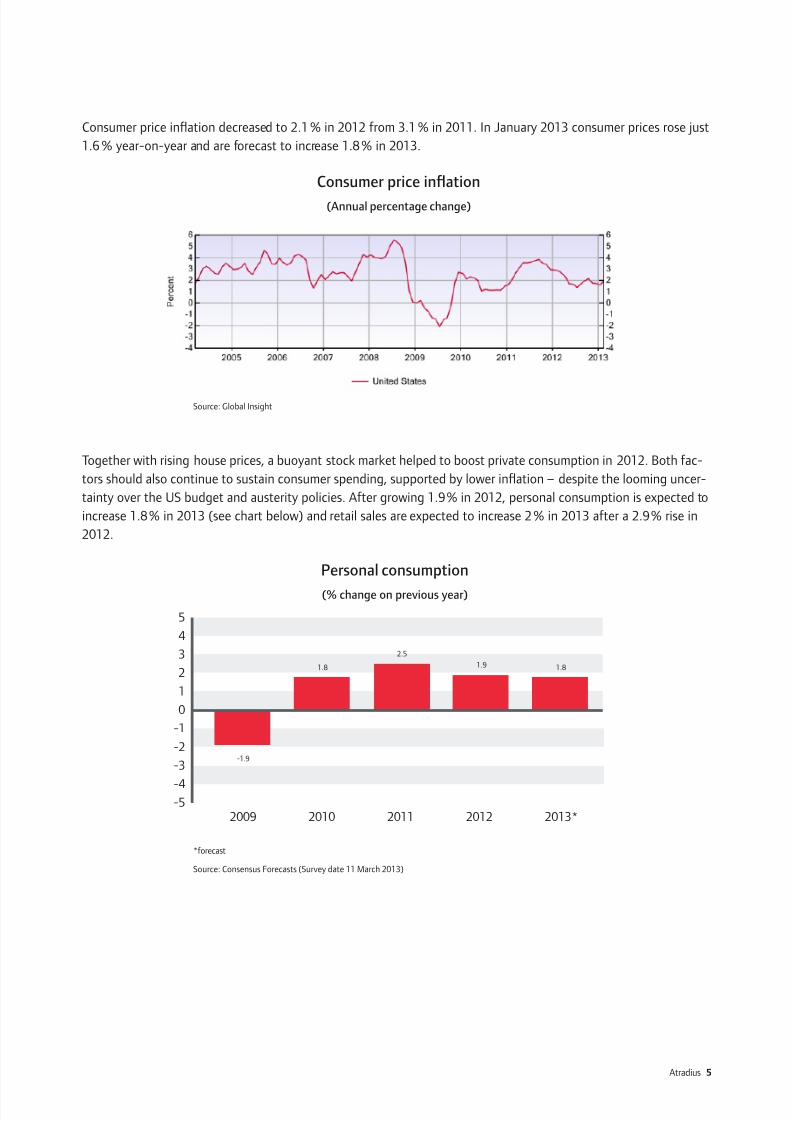

Consumer price infation decreased to 2.1% in 2012 rom 3.1 % in 2011. In January 2013 consumer prices rose just

1.6 % year-on-year and are orecast to increase 1.8% in 2013.

Source: Global Insight

Together with rising house prices, a buoyant stock market helped to boost private consumption in 2012. Both ac-

tors should also continue to sustain consumer spending, supported by lower infation – despite the looming uncer-

tainty over the US budget and austerity policies. Ater growing 1.9% in 2012, personal consumption is expected to

increase 1.8% in 2013 (see chart below) and retail sales are expected to increase 2% in 2013 ater a 2.9% rise in

2012.

*orecast

Source: Consensus Forecasts (Survey date 11 March 2013)

Atradius 5

(Annual percentage change)

Consumer price ination

(% change on previous year)

Personal consumption

5

4

3

2

1

0

-1

-2

-3

-4-5

2009 2010 2011 2012 2013*

-1.9

1.8 1.9

2.5

1.8

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 6/11

Increased demand for business loans

The Federal Reserve’s latest Senior Loan Oce Survey on Bank Lending Practices (January 2013) indicates that

bank lending standards or all sizes o rms have been eased in the period November 2012 to January 2013. De-

mand or business loans has strengthened and, according to the survey, increasing competition to make business

loans has orced banks to relax their lending conditions.

Sources: Federal Reserve Board o Governors; Global Insight

Sources: Federal Reserve Board o Governors; Global Insight

Atradius 6

(Net pernentage o survey respondents)

United States: Bank lending conditions

(Annual percentage change in lending volumes)

United States: Lending growth

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 7/11

Industrial production growth will slow

Ater alling 11.4 % in 2009, US industrial production rebounded in 2010 and 2011, but growth slowed again in

2012. In 2013 industrial production growth is orecast to slow urther: to 2.5 % (see chart below).

*orecast

Source: Consensus Forecasts (Survey date 11 March 2013)

Decreasing business investment

Business investment growth is also set to slow in 2013 ater robust growth in 2011 and 2012 (see chart below).

*orecast

Source: Consensus Economics (Survey date 11 March 2013)

Atradius 7

(% change on previous year)

Industrial production

10

5

0

-5

-10

-15

2009 2010 2011 2012 2013*

5.43.84.1

2.5

-11.4

(% change on previous year)

Business investment

15

10

5

0

-5

-10

-15

-20

0.7

7.78.6

4.6

2009 2010 2011 2012 2013*

-18.1

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 8/11

Public decit reduction remains an issue

The political struggle over government nances remains a downside risk to the US economic outlook. As a result o

the 2008 nancial crisis, the government budget decit increased sharply in 2009-2011 (see chart below) and was

still above 7 % o GDP in 2012. The large and persistent budget decit will lead to a public debt level o more than

125 % o GDP in 2013 and 2014.

The political impasse, caused by to the unwillingness o democrats and republicans to make concessions on debt

negotiations, has so ar prevented a comprehensive budget consolidation rom taking place. While there was a com-

promise in March 2013 to secure public spending or the rest o the scal year - until the end o September - over

the summer Congress will have to increase the limits it sets on government debt (the debt ceiling) to avoid deaulton ederal bills. Additionally, Congress will have to pass a budget or the new scal year by October. Thereore, po-

litical bickering over how the large budget decit is supposed to be brought under control is expected to continue

throughout the year. However, large sudden cuts that would send the economy into recession are unlikely, instead

small steps and delayed measures will moderately subdue the growth rates o 2013 and 2014.

The trade decit decreased in 2012

According to the BEA, the trade balance decit decreased rom US $559.9 billion in 2011 to US $540.4 billion in

2012. As a percentage o US GDP, the decit was 3.4% last year, down rom 3.7 % in 2011. Imports o goods and

services rose US $73.0 billion to US $2,736.3 billion in 2012 (up 2.7 %), while exports increased by US $92.6 billion

to US $2,195.9 billion (up 4.4%).

Source: Bureau o Economic Analysis; Global Insight

Atradius 8

(Government debt and budget balance in percent o GDP)

Public debt and budget balance: United States

(Annual percentage change)

Growth in trade volumes: real imports and exports

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 9/11

However, export growth has shown a decreasing trend since 2010 (see chart above), and is expected to slow ur-

ther. According to IHS Global Insight, exports o goods and non-actor services are expected to increase only 2.8 %

in 2013 ater growing 3.3% in 2012.

The insolvency environment

US corporate insolvencies decreased – but are still above pre-credit crisis levels

Ater year-on-year increases o more than 40% in the years 2007 to 2009, the number o corporate insolvencies

has decreased. According to the latest gures provided by the United States Courts, the number o business ban-

kruptcies led in ederal courts ell 16.2% year-on-year in 2012: to 40,075 cases. We expect this positive downward

trend to continue into 2013, although less steeply, while the number o insolvencies should remain above pre-crisis

levels.

Sources: Administrative Oce o the U.S. Courts; Global Insight

Sources: Administrative Oce o the U.S. Courts; Atradius Economic Research

Atradius 9

(1-year trailing sum o insolvency counts based on quarterly data)

Insolvency trends: United States

% change

2007

43.8%

2008

50.2%

2009

43.0%

2010

-7.5%

2011

-15.1%

2012

-16.2%

0 0

40,000 40,000

20,000 20,000

60,000 60,000

2013*

-5.0%

80,000 80,000

56,28247,806

40,075

28,322

42,546

60,837

38,100

*orecast

(year-on-year change)

US business insolvencies

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 10/11

Lower default risk for US listed rms

In 2012 the monthly median expected deault requency (EDF) gure or US listed companies ranged rom 0.45 %

to 0.65 % and the overall trend has been one o improvement over the course o the year. It nally decreased to

0.4 % in January 2013: the lowest monthly EDF gure since spring 2008. This improvement is due mainly to a rise

in equity prices and a simultaneous reduction in market volatility.

Source: KMV Credit Monitor and Atradius Economic Research

*The Expected Deault Frequency (EDF) chart above is based on listed companies in the markets reerred to, and the likelihood o deault across all sectors within the nextyear. In this context, deault is dened as a ailure to make a scheduled payment, or the initiation o bankruptcy proceedings. Probability o deault is calculated rom threeactors: market value o a company’s assets, its volatility and its current capital structure. As a guide, the probability o one rm in a hundred deaulting on payment is shownas 1%.

US industries perormance orecast

April 2013

Atradius 10

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

2005 2006 2007 2008 2009 2010 2011 2012 2013

P e r c

e n t

Germany

United Kingdom

United States

France

Median EDF evolution by country*

Agriculture

ConsumerDurables

Metals

Automotive/Transport

Electronics/ICT

Paper

Chemicals/Pharma

Financial Services

Services

Construction

Food

Steel

ConstructionMaterials

Machines/Engineering

Textiles

Excellent

Good

Fair

Poor

Bleak

7/27/2019 Atradius Country Report USA Apr2013

http://slidepdf.com/reader/full/atradius-country-report-usa-apr2013 11/11

I you’ve ound this country report useul, why not visit our

website www.atradius.com, where you’ll fnd many more Atradius

publications ocusing on the global economy, including more

country reports, industry analysis, advice on credit management

and essays on current business issues.

On Twitter? Follow @Atradius or search #countryreports to stay

up to date with the latest edition.

Copyright Atradius Credit Insurance N.V. 2013

Disclaimer: This report is provided or inormation purposes only and is not intended as a recommendation as to particular transactions, investments or strategies in any way to any reader. Readers must make

their own independent decisions, commercial or otherwise, regarding the inormation provided. While we have made every attempt to ensure that the inormation contained in this report has been obtained

rom reliable sources, Atradius is not responsible or any errors or omissions, or or the results obtained rom the use o this inormation. All inormation in this report is provided ’as is’, with no guarantee o

completeness, accuracy, timeliness or o the results obtained rom its use, and without warranty o any kind, express or implied. In no event will Atradius, its related partnerships or corporations, or the partners,

agents or employees thereo, be liable to you or anyone else or any decision made or action taken in reliance on the inormation in this report or or any consequential, special or similar damages, even i

advised o the possibility o such damages.

Atradius Credit Insurance N.V.

Postbus 89821006 JD Amsterdam

David Ricardostraat 11066 JS Amsterdam

www.atradius.com