attachment under separate cover - victor.sa.gov.au

TRANSCRIPT

www.victor.sa.gov.au

Attachment Under Separate Cover

Ordinary Council – 24 May 2021

Agenda Item 9.6 - Rating Review Final Report

UHY Haines Norton Adelaide 1 | P a g e

A Review of the Basis of Rating Completion Report

For the City of Victor Harbor

May 2021

UHY Haines Norton Adelaide 2 | P a g e

Disclaimer: This document is for the exclusive use of the person/entity named on the front of this

document (‘Recipient’). This document must not be relied upon by any person who is not the

Recipient. UHY Haines Norton does not take responsibility for any loss, damage or injury caused by

use, misuse, or misinterpretation of the information in this document by any person who is not the

Recipient. This document may not be reproduced in whole or in part without permission.

Liability limited by a scheme approved under Australian Professional Standards Legislation.

Lead Report Author: Corinne Garrett

UHY Haines Norton

25 Peel Street, Adelaide SA 5000

Tel 08 8110 0999

ABN: 37 223 967 491

UHY Haines Norton Adelaide 3 | P a g e

Contents 1. Executive Summary .............................................................................................................. 4

Introduction ........................................................................................................................................ 4 Proposed Changes sent to Consultation. ............................................................................................ 4 Consultation Undertaken .................................................................................................................... 5 Conclusion and Recommendation ...................................................................................................... 5

2. Consultation ......................................................................................................................... 7 Information Provided to Community – Consultation Paper ............................................................... 7 Consultation Period ............................................................................................................................ 7 Advertising of Consultation ................................................................................................................ 7 Survey.................................................................................................................................................. 7 Public Meetings ................................................................................................................................... 7

3. Key Points from Feedback Received ...................................................................................... 8 Reducing the Commercial and Industry Differentials ......................................................................... 8 Increasing the Primary Production Differential .................................................................................. 9 Increasing the Vacant Land Differential ............................................................................................ 10 Retaining Fixed Charge at Current Level ........................................................................................... 11 Retaining Capping at the Current Level ............................................................................................ 11

Appendix 1 – Submissions Received – Detail ............................................................................... 12 Public Meeting Notes ........................................................................................................................ 12 Submissions Received ....................................................................................................................... 13 Survey Responses.............................................................................................................................. 18

Appendix 2 – Consultation Report .............................................................................................. 36

UHY Haines Norton Adelaide 4 | P a g e

1. Executive Summary

Introduction

Councils are responsible for the delivery of a broad range of services to their communities. Each

community is unique and has different priorities. Councils receive income from several sources to pay

for the services they provide, and the largest revenue source is rates.

The Local Government Act 1999 allows Councils to raise rates and provides a degree of flexibility in

the options used by Councils to do this. Councils need to determine the best method for their

communities and review this from time to time to ensure the system they use remains relevant.

The City of Victor Harbor (Council) is reviewing the current methods for setting rates and what

alternative methods, if any, may be more appropriate for the community.

This process is known as a rating review and considers a Council’s rating requirements and the best

way for that Council to distribute the rate burden amongst their community. Each Council will have

different communities, so the rating system used is unique for each Council.

Section 151 of the Local Government Act 1999 (The Act), requires that Council must produce a public

report that must address the following when considering changing their basis of rating:

The reasons for the proposed change

The relationship of the proposed change to the Council’s overall rate’s structure and policies

As far as practicable, the likely impact of the proposed change on ratepayers

Issues concerning equity within the community.

And any other issues that Council considers relevant.

Council produced a ‘Review of the Basis of Rating – Consultation Paper’ that satisfied the requirements

of Section 151 of the Act.

Proposed Changes sent to Consultation.

Council considered rating information and proposals over a number of workshops. Information

considered included; rating methods available, the current method of rating, proposed changes, and

likely impacts.

Council’s current rating system has a number of aspects that Council felt should be reviewed and

consulted on.

Council proposed no changes to the following;

Fixed Charge – to not increase by more than inflation.

Capping – to remain at the current level of 15%

Changing Differentials

The following table shows the current differentials and the proposed differentials that were sent to

the community for consultation.

UHY Haines Norton Adelaide 5 | P a g e

Land Use Current Differential Proposed Differential

Residential 100% = Base No change

Commercial 130% = Base + 30% Reduce to 100%

Industry 115% = Base + 15% Reduce to 100%

Primary Production 90% = Base – 10% Increase to 100%

Vacant Land 150% = Base + 50% Increase to 160%

These proposed changes exclude any annual rate increases that Council may impose to general rates

or service charges to cover the costs of inflation, requirements of Council’s Asset Management Plans,

future changes to services or any other impact as outlined in Council’s Long Term Financial Plan.

Future valuation increases in properties are also not considered.

The proposed changes and modelling within the consultation report are compared against current

rates to assist in understanding their impact in isolation from other influences.

Consultation Undertaken

Council provided a Consultation Paper to the community as per requirements of Section 151 of the

Local Government Act 1999 which requires Council to produce a public report that addresses the

following when considering changing their basis of rating;

The reasons for the proposed change

The relationship of the proposed change to the Council’s overall rates structure and policies

As far as practicable, the likely impact of the proposed change on ratepayers

Issues concerning equity within the community.

And any other issues that Council considers relevant.

The consultation period was from the 25th March to the 26th April 2021.

Council provided information on the proposed changes via the following methods.

Victor Harbor Times

On Council’s Website

A public meeting was held at the Council Chambers on the 22nd April at 6.30pm

Conclusion and Recommendation

Council has undertaken the required reporting and consultation as per the Local Government Act

1999 to review their basis of rating.

The consultation process engaged the community with a good response both in writing and

attendance at the public meeting. Many questions were raised and answered at the meeting and

the community raised some significant concerns and issues for Council to consider.

In light of the consultation the following recommendations are provided to Council for their

consideration:

UHY Haines Norton Adelaide 6 | P a g e

Reducing the Commercial and Industry Differentials There was an indicated preference to retain the current level of differentials for Commercial and

Industry properties for the purposes of allocating those additional funds to economic development.

There was particular support from representatives for the business community.

Recommendation:

That Council retain the Commercial Differential at 130%

That Council retain the Industry Differential at 115%

That Council address the requests by the business community regarding how the spending

of the additional rate revenue on economic development occurs.

Increasing the Primary Production Differential There was an indicated preference to retain the current level of differentials for Commercial and

Industry properties, particularly from the business community.

Recommendation:

That Council retain the Primary Production Differential at 90%.

That future responses to impacts on the industry such as drought be addressed through a

short-term rebate rather than adjusting the differential.

Increasing the Vacant Land Differential There was an indicated preference for increasing the Vacant Land Differential.

There were concerns raised about people being able to pay additional rates whilst waiting to build.

This could be alleviated if there was a rebate for owners of vacant land or who lived in the Council

area however the legality of this within legislation would need to be checked.

Recommendation:

That Council increase the differential for Vacant Land from 150% to 160%

That Council consider and seek legal advice on providing a rebate to Vacant Landowners

that live in the Council area.

Retaining the Fixed Charge at the Current Level The Consultation Paper discussed keeping the Fixed Charge as it is and only increasing by inflation

each year. The survey question does not appear to have clearly matched with the proposal of the

Consultation Paper.

However, the response did not indicate a move to increase the Fixed Charge.

Recommendation:

that Council retain the Fixed Charge at its current level, only increasing by inflation each

year.

Retaining Capping at the Current Level There was not much response about the capping.

Recommendation:

That Council retain the current level of capping at 15%

UHY Haines Norton Adelaide 7 | P a g e

2. Consultation

Information Provided to Community – Consultation Paper

A Consultation Paper was provided to the community via Council’s website. This document included

the following topics and should be read in conjunction with this report;

The Purpose of the Consultation Paper

Why Council’s Collect Rates

Nature of Council Rates

Principles of taxation

Legislative Framework for Setting Council Rates

Valuations

Rating Options Available

Service Rates & Charges

Rate Discounts

Postponement of Rates

Council’s Current Rating Methodology

Comparison to Similar Councils

Council’s Community Profile

Rating as a Tool to Assist in Achieving Strategic Objectives

Rating Structure – Potential Changes and their Impact

Proposed Changes

Likely Impact on Ratepayers

Consultation Requirements

Consultation Period

The consultation period was from the 25th March to the 26th April 2021.

Advertising of Consultation

Council provided information on the proposed changes via the following methods.

Victor Harbor Times

On Council’s Website

Survey

Council had a survey on www.yoursay.victor.sa.gov.au with hard copies for people to fill out at the

Council Office.

Public Meetings

A public meeting was held on the 26th April at 6.30 at the Council Chambers

UHY Haines Norton Adelaide 8 | P a g e

3. Key Points from Feedback Received A number of issues were raised in both the written feedback and the public meeting. They are

summarised here with our comments:

Reducing the Commercial and Industry Differentials

The following summarised comments were made for the reduction of Commercial and Industry

differentials

Higher differential is a disincentive to new business and doesn’t encourage commercial

activity.

Unfair to pay higher differential when receive the same services.

Businesses have been affected by Covid-19 and online businesses.

Lower business costs would encourage new businesses to the area and greater investment

from existing businesses.

The following summarised comments were made against the reduction of Commercial and

Industry differentials.

that the higher differentials for Commercial and Industry properties for the purpose of

economic development is sound.

would not like to see a reduction in Council’s investment in economic development.

the higher differential was suggested by the Victor Harbor business community initially to

prioritise economic development.

That a reduced differential would mean that larger business rate payers that are national

and multinational firms would share a lesser proportion of the rating burden

That the removal of the higher differential will not see a growth in investment by business

That the properties are used for to gain financial income and should pay higher rates.

Don’t want Residential Rates to increase to pay for a reduction in Commercial and Industry

rates.

That businesses are started for many other substantial reasons than the rates payable.

Survey Results

The majority were supportive of the current differential rates of 130% for Commercial and

115% for industrial. (12 to 8)

A small majority of survey respondents disagreed that the removal of the higher

differentials would encourage business investment in the Council area. (9 to 8)

The majority agreed that the higher differential on ‘bricks and mortar’ businesses is

inequitable when compared to businesses run out of residential properties. (15 to 2)

The majority disagreed that large national commercial businesses should pay the same rate

in the dollar as residential properties. (12 to 5)

The majority agreed that any reduction to the commercial and industrial differentials should

be introduced over a 5-year period. (8 to 5)

Conclusion

There was an indicated preference to retain the current level of differentials for Commercial and

Industry properties, particularly from the business community.

UHY Haines Norton Adelaide 9 | P a g e

Recommendation:

That Council retain the Commercial Differential at 130%

That Council retain the Industry Differential at 115%

That Council address the requests by the business community regarding how the spending

of the additional rate revenue on economic development occurs.

Increasing the Primary Production Differential

The following summarised comments were made for increasing the Primary Production

Differential from 90% to 100%.

Other Government support available for Primary Production, should not be a responsibility

of Council.

Primary Producers have good and bad years, it’s the risk inherent in the industry.

Drought hasn’t had an impact in our region and leads to stronger prices for livestock.

No longer in drought conditions. (from a ratepayer in the industry)

Should have proof of income loss (excluding depreciation) for a reduction in rates.

Primary producers derive income from their property and accordingly should pay at least the

same rates as residential property owners. They are also well supported by favourable

taxation schemes.

The following summarised comments were made against increasing the Primary Production

Differential from 90% to 100%

High increase in property values due to Valuer General’s Revaluation Initiative

Primary Production is a high-risk business.

Less services available in the rural areas

have responsibilities of controlling feral animals and weeds which benefits whole

community.

the industry makes a significant economic contribution to the district and does not receive

the level of support that business and tourism does.

Council has lower costs for primary production land.

Primary Producers have responsibilities to decrease fire risk.

Recognition of the contribution that rural landholders make towards retaining conservation

land on their properties for the benefit of all ratepayers.

Survey Results

The majority support the continued provision of a discount for primary producers. (12 to 9)

Conclusion

The respondents mostly favoured retaining the 10% differential discount for Primary Production

properties. This reduced differential occurred due to a response to drought, but many Councils have

a small discount for Primary Producers in acknowledgement of their contribution to the economics,

environmental and aesthetic of the district.

Council will need to consider their response to any future situations such as drought. Further

discounting the differential may make it difficult to return to its current level. Rebates can be

UHY Haines Norton Adelaide 10 | P a g e

targeted to those Primary Producers that are actually affected by the particular conditions and can

be made available for just one year.

Recommendation

That Council retain the Primary Production Differential at 90%.

That future responses to impacts on the industry such as drought be addressed through a

short-term rebate rather than adjusting the differential.

Increasing the Vacant Land Differential

The following summarised comments were made for increasing the Vacant Land Differential from

150% to 160%.

Current housing shortage in the area would indicate we need vacant land turned into

housing and not land banked.

Encouraging infill and housing creates employment in the construction industry as well as

leading to population growth with flow on benefits across the local economy.

Higher rate but preceded by a 2-year honeymoon period to allow reasonable time to do

improvements.

Would encourage either the building or selling of the land.

The following summarised comments were made against increasing the Vacant Land Differential

from 150% to 160%.

Young people purchasing vacant land with the intention of building at some future date

should not be disadvantaged to this degree.

A Family wants to hold land for children who may not be able to get land later on.

Survey Results

A small majority agreed that there was a shortage of vacant land in the Council area. (6 to 3)

The majority support the proposal to increase the vacant land differential to 160% of the

residential differential. (12 to 7)

Other comments

Would like to see encouragement for properties to be converted to permanent rental

properties.

Conclusion

There was an indicated preference for increasing the Vacant Land Differential.

There were concerns raised about people being able to pay additional rates whilst waiting to build.

This could be alleviated if there was a rebate for owners of vacant land or who lived in the Council

area however the legality of this within legislation would need to be checked.

Recommendation:

That Council increase the differential for Vacant Land from 150% to 160%

That Council consider and seek legal advice on providing a rebate to Vacant Landowners

that live in the Council area.

UHY Haines Norton Adelaide 11 | P a g e

Retaining Fixed Charge at Current Level

Survey Results

There was a majority who support a fixed charge applied equally across the ratepayer base.

(11 to 7)

Comments were:

that this system has been long established so no change

That ratepayers with lower value properties are penalized by comparison to ratepayers with

higher value properties.

Conclusion

The Consultation Paper discussed keeping the Fixed Charge as it is and only increasing by inflation

each year. The survey question does not appear to have clearly matched with the proposal of the

Consultation Paper.

However, the response did not indicate a move to increase the Fixed Charge.

Recommendation:

that Council retain the Fixed Charge at its current level, only increasing by inflation each

year.

Retaining Capping at the Current Level

The following summarised comments were made in regard to Rate Capping.

The Rate Capping threshold should be 10% instead of 15% due to impact of valuation

increases for Primary Producers.

That Council retain the threshold of 15% for Primary Producers.

Conclusion

There was not much response about the capping.

Recommendation:

That Council retain the current level of capping at 15%

UHY Haines Norton Adelaide 12 | P a g e

Appendix 1 – Submissions Received – Detail

Public Meeting Notes

Rating Review Public meeting feedback – 22 April 2021

John Miller – questioned the comment that 40% of ratepayers live outside the council area and

wanted to know what % of this was vacant land holders.

Beryl – Is a long-standing primary production land holder, properties are in rural area, are a high-risk

business. The business increases due to COVID-19 have only been 1 year of profits in 50 years. The

Revaluation Initiative Project increase should warrant continued discount. Rural Properties provide

huge benefit to the environment, community, and tourism. The rebate should continue to provide

recognition of the benefits that rural properties give to the whole community. The council budget

also provides funding to other businesses and the tourism sector but not to rural farms, their only

financial assistance is the rate reduction. The primary producers in the area also provide a large

support to the local businesses by spending money here and buying their products.

Bill – the vacant land increase in unfair. If the primary production differential rate is increased to

100% it should result in the same service levels as those properties in the township area, including

sealing all roads, postal deliver, rubbish collection, footpaths etc. The current increases cost should

also be removed, such as increased costs for developments, septic systems, and bushfire

requirements etc. Council should be paying for road maintenance and should get the money from

federal government because the community has already paid fuel excise tax, which was introduced

for that reason. RAA recently said that only 23% of the fuel excise tax goes back into roads.

John Miller – Commented on the previous comments of Bill that septic & water is not council but SA

Water.

Richard Lawrence – the Revaluation Initiative will increase values by 25% or more, increasing the

differential by 10% will result in an overall increase of 35%. Rate capping should be given at 10%.

Cr Kemp – on behalf of businesses, asked how much is raised by the increased differentials and how

is it spent. Was just a question but they aren’t against keeping it.

Kellie Knight Stacey replied in the meeting that the amounts are published in the Annual Business

Plan, in the Rating Policy and in the Budget each year. Further discussion was had about what it is

spent on, including employees and whether this should be what changes instead of the differential.

Cr Charles – asked if alternative options could be provided based on the feedback that was being

received.

Cr Robertson – rates are 85-90% of the budget income, this will put pressure on future years due to

developments. Need to find other income streams, other than rates.

Derek McIlroy – representing Business Victor Harbor. They don’t support the removal of the higher

differential rates for commercial and industrial. Wants to see evidence that it is supporting

development & investment. Big businesses should pay higher rates as it is a user pays system that

they would not otherwise contribute to. Wants the ability to influence what the money is spent on.

UHY Haines Norton Adelaide 13 | P a g e

Submissions Received

Agribusiness Working Group

The group were provided a summary of changes relevant to primary production properties and

encouraged to provide feedback during the public consultation.

The Agribusiness Working Group agreed by consensus to provide the below responses as a response

to the consultation.

That Council continue to apply a 10% discount on the differential rate for primary

production land classification given the contribution that rural landholders make toward

maintaining non-productive and conservation land on their property for the benefit of all

ratepayers.

That the Council amend the rating policy to include rate capping provisions for primary

production at 15% consistent with other classifications.

UHY Haines Norton Adelaide 14 | P a g e

UHY Haines Norton Adelaide 15 | P a g e

UHY Haines Norton Adelaide 16 | P a g e

UHY Haines Norton Adelaide 17 | P a g e

UHY Haines Norton Adelaide 18 | P a g e

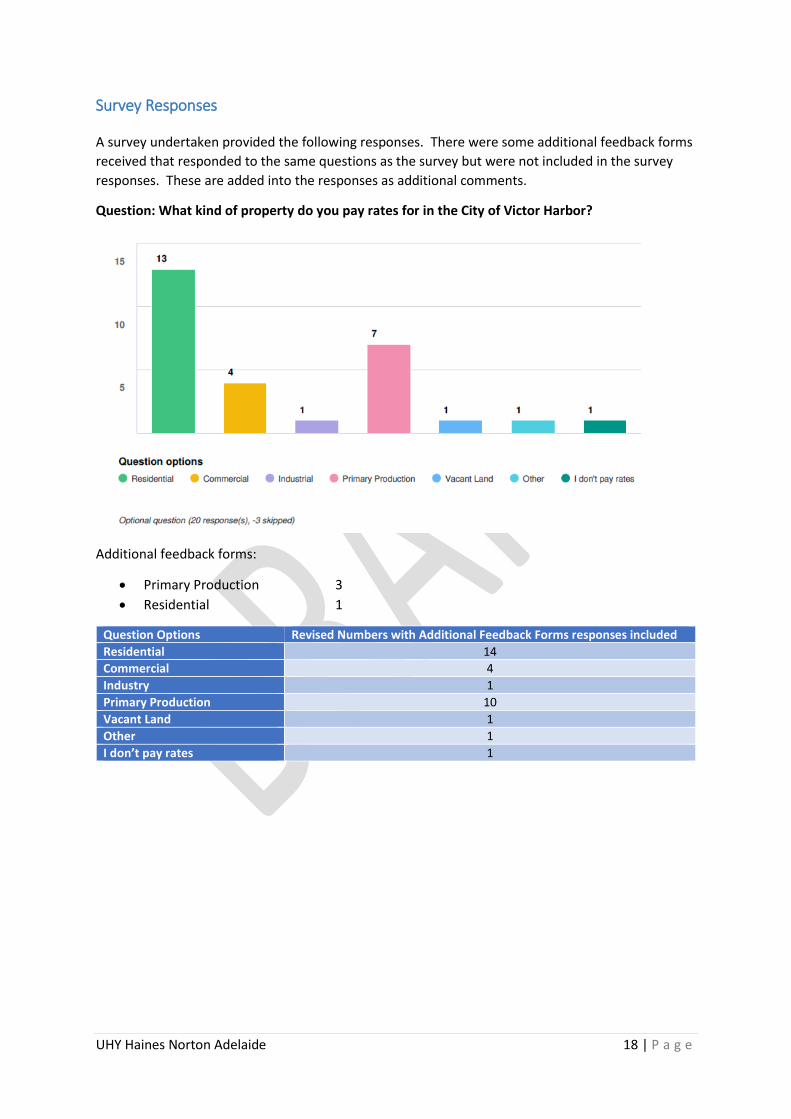

Survey Responses

A survey undertaken provided the following responses. There were some additional feedback forms

received that responded to the same questions as the survey but were not included in the survey

responses. These are added into the responses as additional comments.

Question: What kind of property do you pay rates for in the City of Victor Harbor?

Additional feedback forms:

Primary Production 3

Residential 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Residential 14

Commercial 4

Industry 1

Primary Production 10

Vacant Land 1

Other 1

I don’t pay rates 1

UHY Haines Norton Adelaide 19 | P a g e

Question: Council currently allocates the commercial and industrial differential rates to economic

stimulus activities. To what extent do you support the current differential rates of 130% for

commercial and 115% for industrial?

Additional feedback forms

Extremely Supportive 1

Very supportive 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Not at all supportive 6

Slightly supportive 2

Moderately supportive 1

Very supportive 2

Extremely supportive 10

Further information provided by respondents regarding this question are:

Higher percentage rates are a disincentive to new business.

Unfair that commercial tenants who pay landlords rates are forced to pay higher differential

rates than other ratepayers who enjoy the same uses of council facilities i.e., roads, parks,

etc.

Council should be encouraging commercial activity to stimulate the local economy.

There may be a small disincentive to invest but residents should not be made to make up a

shortfall if this differential is changed. Preferably it could be made up by implementing a

higher rate on holiday homes.

Businesses have done it hard through COVID-19 and need a few years of support at least.

UHY Haines Norton Adelaide 20 | P a g e

Both of these groups have land that is used for financial income. A house does not. The

average wealth of the various owners is far greater than the average wealth of a

homeowner. We currently have a least 13% of the residents whose income is below the

poverty line (an AHBS fact). The proven past system of differential rates is proven correct.

This seems like the business owners are pushing for this. Why?” to save money at the

expense of the residents!!! Businesses can increase their income… residents cannot.

Current rate for residential is high enough, no more increases please.

I don’t see the logic in having these differentials. Having the same rate in the dollar is

probably the fairest method. Council has to raise revenue and having the same rate in the

dollar for all tends to smother objections about one sector being treated better/worse than

others.

Those commercial enterprises derive income from their property and accordingly should pay

higher rates than residential property owners.

Should be assessed by valuation, services are same.

As per Business Assoc. response

Businesses receive significant financial support from Council – the Visitor Information

Centre, Horse Tram, Whale Centre, Arts Centre, festivals and tourism promotions and

funding for leadership and management officers. The business ratepayer should be

financing this support.

It is the current rates arrangement. I am not aware of problems arising from their rates.

Both kinds of property benefit from the Council expenditure on streetscape and urban

services which are not expenditures in the country areas. To lower these rates will mean

increases for others.

I don’t feel I know enough about it to make an informed decision.

UHY Haines Norton Adelaide 21 | P a g e

Question: To what extent do you agree that the removal of the higher differentials may encourage

business and investment in the Council area?

Additional feedback forms.

Neither agree nor disagree 2

Strongly disagree. 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 6

Disagree 2

Neither agree nor disagree 6

Agree 4

Strongly agree 5

Further information provided by respondents regarding this question are:

Removes barriers and decreases costs for new and existing businesses and provides an

incentive for businesses in higher rating areas to relocate to Victor Harbor.

Absolutely any cost savings for long suffering commercial tenants or owner operators is

most welcome in a tough trading environment especially for businesses impacted by the

online sales world and who put in long hours many 7 days a week.

Lower operating costs will encourage new businesses to the area and greater investment

from existing businesses.

Yes, it may.

Simple economics. Cheaper rates will attract more business and help retain existing ones.

Why will new enterprises start up with this small saving. This question does not make sense.

Why reduce for current businesses? When your question is “seeking new business &

UHY Haines Norton Adelaide 22 | P a g e

investment”. If you want to do this, then for new businesses offer a say 2-year reduction %

of their rates. Problem solves.

Keep residential rates as low as possible please as a retired self-funded couple.

I think it says to any potential investors and businesses that in terms of revenue raising, the

council is bound to differentials in terms of rating policy. This in itself is probably a positive

sentiment – something that businesses don’t have to consider in planning for the future.

Annual rates are a very small expense in the overall expenditure of a business. It is a stretch

to believe that a slight reduction in annual general rates would ever be a deciding factor in a

business starting up or not.

Any reduction in cost to entry is a positive

As per Business Assoc. response

Industry and commerce are initiated for many other substantial reasons than the rates

payable.

Won’t make any difference.

UHY Haines Norton Adelaide 23 | P a g e

Question: Do you agree that the higher differential on ‘bricks and mortar’ businesses is inequitable

when compared to businesses run out of residential properties?

Additional feedback forms.

Neither agree nor disagree 1

Strongly agree. 1

Agree 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 1

Disagree 1

Neither agree nor disagree 6

Agree 7

Strongly agree 8

Further information provided by respondents regarding this question are:

Most home-based businesses are small or new in comparison.

Obvious

I have for a long time held the belief that any business should be charged the same – this

includes the swiftly growing number of Air BnB or private holiday rental properties that are

actually very profitable businesses, but they pay lower rates. This increases the number of

vacant properties outside of peak times and reduces the amount of permanent rental

properties and therefore permanent residents – overall I believe this sharp “peak and

trough” population is detrimental to the running of the town.

Home based businesses have an inherent cost advantage based on multiple use of the rated

property.

UHY Haines Norton Adelaide 24 | P a g e

Council currently has the ability to charge more for a residential business. This is a weak

excuse for businesses to ask for a reduction.

A business is a business.

Each property or allotment (title) should pay the same rate in the dollar.

The majority of bricks and mortar businesses are service-level businesses that require foot

traffic.

It’s an inequitable loophole.

As per Business Assoc. response

If the business benefits from the Council’s financial support, then they should be

contributing.

An industrial or commercial business run out of any residential property should attract the

same higher rates as respectively apply to other industries and commerce.

If run a business from your home – explain to everyone how do the council judge. Some run

lawnmowing businesses from home, wouldn’t really count. Some run Solicitor conveyancing

from home, does this count? Hairdressers from home? Please explain to us. A lot of people

work from home for businesses they are employed by, maybe even Council employees?

UHY Haines Norton Adelaide 25 | P a g e

Question: As per legislation, Council cannot differentiate the rate in the dollar from one

commercial business to another. Do you support the view that large national commercial

businesses should pay the same rate in the dollar as residential property owners?

Additional feedback forms.

Strongly disagree. 1

Neither agree nor disagree 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 11

Disagree 1

Neither agree nor disagree 4

Agree 2

Strongly agree 3

Further information provided by respondents regarding this question are:

Large commercial business provides jobs, plain and simple. Reduced rates provide a

significant incentive for them to relocate their businesses to Victor Harbor and the potential

benefit to the community is much greater than the cost of reduced rates.

Yes, the likes of Woolworths, Big W, Kmart etc. pay very low rents etc. per sqm often linked

to sales/ i.e., if sales fall so does rent and it’s the small operators who subsidize the anchors

with onerous leases and are often treated very poorly by landlords and are forced to agree

or agree to craze conditions i.e., new shop fit upon lease renewal etc.

We require these large businesses in the region, they create employment as well as vital

services. They can choose to leave the region if it’s not viable.

No, I don’t support that view.

UHY Haines Norton Adelaide 26 | P a g e

Businesses earn income from their rateable property so should contribute more than

residential.

I’ve answered this before. Plus, many commercial businesses shave eye catching and superb

locations that are more valuable than residential houses. Hence, they should pay more in

their rates.

Again, my previous points apply to this question as well. It’s the value of the property that is

the important thing. The Valuer General must be diligent in ensuring that both commercial

and residential properties are properly valued.

Residential ratepayers should not be subsidizing large commercial enterprises.

Proportionate to valuation should be the mechanism to ensure they pay fair share of council

costs.

The larger developments do require infrastructure support from council and should be

contributing.

These large commercial businesses should pay the same rates that apply to all other

industries and commerce. Large businesses should in addition pay for site works including

access roads at the time that these assets are built.

This question is bizarre. You start talking about commercia properties, then ask if residential

properties and commercial rates should be the same? There are two questions here, which

one do we answer.

UHY Haines Norton Adelaide 27 | P a g e

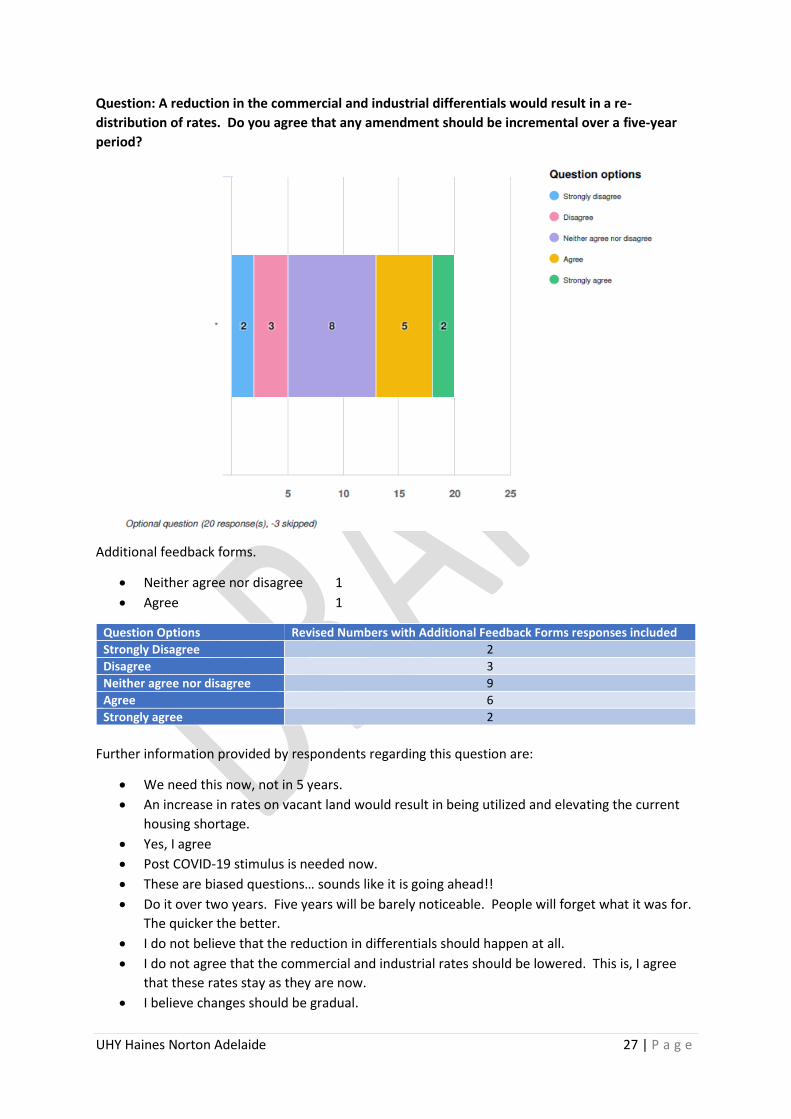

Question: A reduction in the commercial and industrial differentials would result in a re-

distribution of rates. Do you agree that any amendment should be incremental over a five-year

period?

Additional feedback forms.

Neither agree nor disagree 1

Agree 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 2

Disagree 3

Neither agree nor disagree 9

Agree 6

Strongly agree 2

Further information provided by respondents regarding this question are:

We need this now, not in 5 years.

An increase in rates on vacant land would result in being utilized and elevating the current

housing shortage.

Yes, I agree

Post COVID-19 stimulus is needed now.

These are biased questions… sounds like it is going ahead!!

Do it over two years. Five years will be barely noticeable. People will forget what it was for.

The quicker the better.

I do not believe that the reduction in differentials should happen at all.

I do not agree that the commercial and industrial rates should be lowered. This is, I agree

that these rates stay as they are now.

I believe changes should be gradual.

UHY Haines Norton Adelaide 28 | P a g e

Question: to what extent do you agree that there is a shortage of vacant land in the Council area?

Additional feedback form.

Agree 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 2

Disagree 1

Neither agree nor disagree 11

Agree 4

Strongly agree 2

Further information provided by respondents regarding this question are:

Seems to be a fair bit of land under-utilised still.

No idea, I assume it’s a supply demand situation, plenty of rezone able land on outskirts.

Current housing shortage in the area would indicate we need vacant land turned into

housing and not land banked.

The type and quality of land offerings is poor – tiny 500m2 blocks or huge farms but not

much in between.

Haven’t researched.

Look at the nearby paddocks that have already been zoned in the 10-year plan for

housing/commercial. Again, who says there is a shortage of vacant land?

There seems to be a lot of farmland around Encounter Bay.

Irrelevant to me

Self-explanatory

UHY Haines Norton Adelaide 29 | P a g e

Question: Council charges a higher rate in the dollar on vacant land to encourage infill and

sufficient supply of land for development within the district. To what extent do you support the

proposal to increase the vacant land differential to 160% of the residential differential?

Additional feedback forms;

Agree 1

Strongly disagree. 1

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 3

Disagree 4

Neither agree nor disagree 3

Agree 7

Strongly agree 5

Further information provided by respondents regarding this question are:

Prevents or disincentives land banking and promotes active development and renewal.

If there is evidence of land banking yes

Encouraging infill and housing creates employment in the construction industry as well as

leading to population growth with flow on benefits across the local economy.

This would greatly improve land and new home offerings and potentially the permanent

population of the region would increase, the peak and trough population would smooth out,

allowing greater year=long investments by businesses and highly likely to improve

employment opportunities year-round. I would like to see encouragement for properties to

be converted to permanent rental properties as approximately 40% of Australians now rent.

These ;inducements could be in the form of a rate reduction for the first 5 years, a rate

UHY Haines Norton Adelaide 30 | P a g e

freeze if converting from an Air BnB to a permanent rental or if building a new home to be a

rental.

I think the higher rate should be preceded by a 2-year honeymoon period to allow

reasonable time to do improvements. If on the 3rd 1st July a block has no planning or

building submitted for approval, then the 160% levy should be imposed.

Either build on it or sell it

Irrelevant to me

Young people purchasing vacant land with the intention of building at some future date

should not be disadvantaged to this degree.

The shift from 150% to 160% may well add encouragement for the vacant land to be

developed for a useful purpose.

Family wants to hold for children who may not be able to get land later on. Don’t penalise.

UHY Haines Norton Adelaide 31 | P a g e

Question: Council introduced a discounted differential for primary production due to drought

conditions. To what extent do you support the continued provision of a discount in this category?

Additional Feedback forms;

Strongly agree 2.

Strongly disagree 1.

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 6

Disagree 3

Neither agree nor disagree 2

Agree 2

Strongly agree 10

Further information provided by respondents regarding this question are:

There are enough other govt. programs that provide relief in these areas. It should not fall

to Victor Harbor ratepayers to continue to provide discounted rates.

Not sure, on balance no, rural producers have good years, bad years, high commodity prices,

low prices. It’s the risk they take of a farming enterprise in my opinion.

Drought conditions have not had an impact in our region and in fact lead to stronger

commodity prices for livestock, which is the main industry across the district.

We are no longer in drought conditions and primary producers (I am in the industry) should

be able to manage their own ‘ebb and flow’ years without assistance. Resources should be

banked in strong years for the weaker years.

Primary industry is essential land use and weather dependent. Income from it is weather

dependent. Proof of income loss excluding depreciation should be necessary for reduction

in rates.

UHY Haines Norton Adelaide 32 | P a g e

What drought!!

Drought is a known condition and risk for any primary production business in Australia.

Discounted rates should not be applied as a compensation for a known and recognised

business risk. To leave it in place could potentially open up a Pandora’s box.

Primary production enterprises derive income from their property and accordingly should

pay at least the same rates as residential property owners. They are also well supported by

favourable taxation schemes.

With increased property values and the unguaranteed reliability of the seasons, these guys

are only just seeing positive prices for livestock come through now, they are so far behind to

discontinue is a slap in the face for the areas major industry.

My rates are high, and my services are low with relation to my farming property. It is

already inequitable and unfair to increase would be very unreasonable.

It is imperative that this differential be maintained due to rural landholders having

meaningful costs controlling feral animals, invasive weeds etc which benefits the whole

community. The rural sector is not always afforded the same level of service as residential in

all areas. The description Primary Production is a misnomer and should be more accurately

described as ‘Rural Peasantry’ or ‘Rural Lifestyle’ to be more politically correct.

The Primary Production sector makes a significant economic contribution to the city of

Victor Harbor and does not receive anywhere near the level of financial support that the

business and tourism industry does. The tourism industry and local residents benefit from

the appeal of the rural surrounds to Victor Harbor Rural Landholders who maintain the

environment and conserve the land on their property for the benefit of all ratepayers.

I urge this discount to primary production land to be increased. It is not just a response to

drought. It is a discount to acknowledge lower Council costs for primary production land.

Yes, road maintenance, yes rubbish collection but no cost to Council for streetscape, lighting

and all the other urban amenities. It is also a discount to acknowledge primary producers

conserve the bush environment (on their properties) to the benefit of everyone.

Asking farmers to do more to keep their properties ‘fireproof’, cleaning up trees to 2 metres,

slashing grass, cleaning up wood piles etc and yet the Council can’t even keep their

roadsides clear like that.

Whilst I accept that current seasonal conditions and commodity prices have improved, there

is increasing pressure and cost involved for primary producers to control the spread of

weeds on their properties. This particularly applies to properties closer to build up areas. I

have land at Waitpinga with a patch of scrub abutting the road, which I have owned for

approx. 50 years. For the first 30 years or so, this scrub which I have fenced off from stock,

was free of invasive weeds and in pristine condition. However, over the mor recent years

there has been a problem with people dumping garden cuttings and soil on the roadside. At

times rubbish has been dumped in the scrub on my property. With the combination of

seeds being brought in by birds and the dumped garden waste it is becoming very difficult to

control the weeds. On many occasions I have seen where rubbish has been dumped on

quiet roadsides. In the last 4 years in an effort to preserve this native vegetation, I have

personally spent $4,223 paying contractors to remove weeds. In addition to this I have

spent many hours myself digging and pulling weeds. There has also been Govt. funding for

protecting native vegetation which has been a great help, but this last year was not

available. Because of the above I would be very disappointed to see an increase in my rates.

UHY Haines Norton Adelaide 33 | P a g e

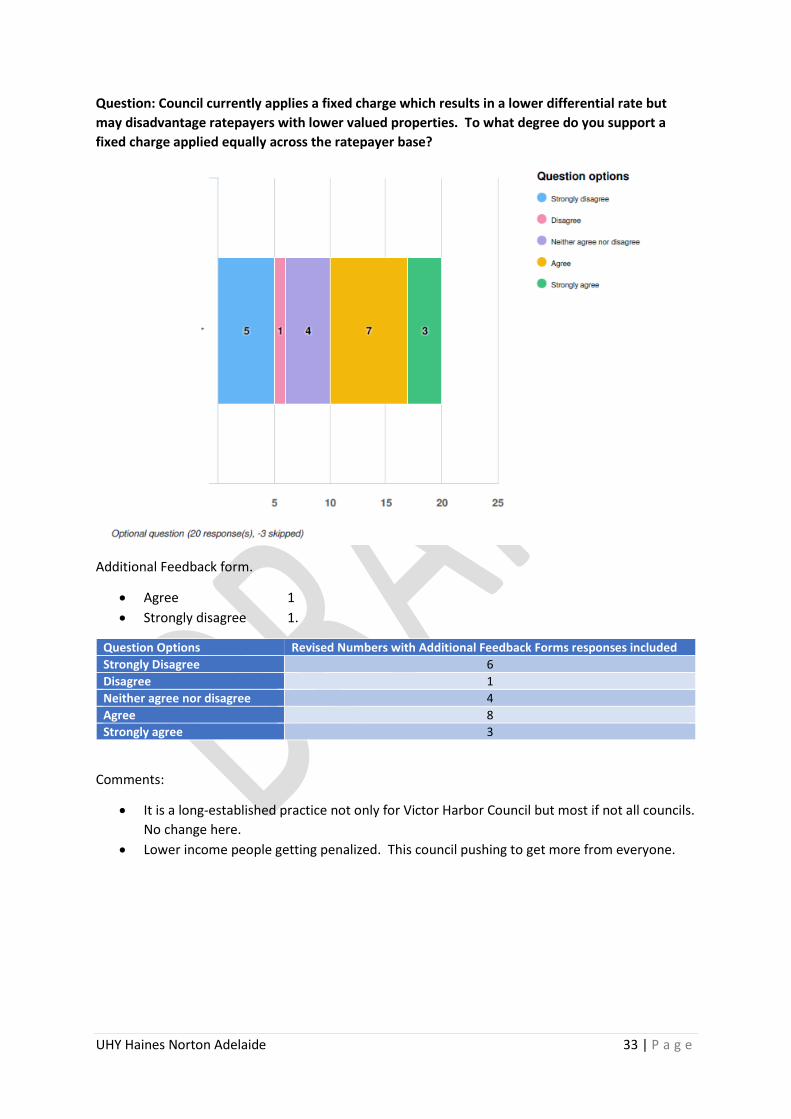

Question: Council currently applies a fixed charge which results in a lower differential rate but

may disadvantage ratepayers with lower valued properties. To what degree do you support a

fixed charge applied equally across the ratepayer base?

Additional Feedback form.

Agree 1

Strongly disagree 1.

Question Options Revised Numbers with Additional Feedback Forms responses included

Strongly Disagree 6

Disagree 1

Neither agree nor disagree 4

Agree 8

Strongly agree 3

Comments:

It is a long-established practice not only for Victor Harbor Council but most if not all councils.

No change here.

Lower income people getting penalized. This council pushing to get more from everyone.

UHY Haines Norton Adelaide 34 | P a g e

Question: Do you have any further comments for Council to consider as part of its rating review?

The survey respondents provided the following.

As residential property values continue to grow their needs to be a ceiling on rate charges. I

don’t mind paying rates based on property value but feel that there should be a limit that

once your property value goes over a certain threshold say $1 million, your rates stop

increasing on the per $1,000 amount and a maximum rateable amount per property is

reached.

Yes, seems a fair proposition.

All rate payers benefit from council services and need to provide a reasonable contribution.

Many properties with a higher value are lifestyle properties on small acreage on the fringe of

the township, which receive less services.

The fixed charge is fair, council need to maintain a minimum income base bat there could be

a ‘floor value’ implemented.

The lower valued properties are generally owned by the lowest income recipients and

socially wrong to make them worse off.

Be fair. Rates must be based on property & improvement value. Will Council consider

fairness, or the loudest most influential voice being heard and agreed to?

Rates are far too expensive. This council tries to fly too high…many thousands of dollars

wasted…disgraceful.

My agreement is predicated on the principle that the ratepayer base means property

owners – not the lessees of individual rooms as offices in a formerly residential building.

There is an inconsistency between how farmland in the form of contiguous sections (titles)

of land = owned by the same owner, only bears one fixed charge, whereas one single

allotment (title) on which is a building with rooms let to different office tenants attracts a

separate fixed charge for each portion of the property that is leased -= even through the

property is a single section (title) owned by one owner. Limiting the fixed charge to a single

charge per allotment (title) would go some way to reducing the dramatic imbalance in the

way the fixed charge is applied.

Remove the Fixed Charge and then all general rates will be based solely on the value of a

property. This is the fair and equitable principle in action. Those who can afford to pay for

high value properties should not have their rates subsidized by low value property owners

and that is precisely the effect of a Fixed Charge.

I am an Industry Advocate for Agriculture, working with all the farmers over the Fleurieu

through my work with FPAG and also through Fleurieu Farming Systems and the Victor

Harbor Councils Agribusiness Working Group. Discussions with property owners are not

limited to the below but in short, strongly support my comments below. At the moment

prices for livestock are good and the seasons have been relatively kind, which is helping

landowners catch up, but these prices etc. are not guaranteed. Buying stock is also a

problem, where they have spent money improving pastures and can’t feed them off,

effectively losing money in the process. Increased rates based on increased property

valuations might be fine for professionals where farming is a hobby or a second income and

where increased capital value of land is a positive for future sale. But where properties have

been passed down and cash flow is tight or where there is high debt and income is purely

reliant on farming, the proposed changes are not fair or sustainable. Those that don’t use

their land themselves and least out (many of the smaller/inherited properties only lease out

to recover rates) will have to increase their lease rate to cover the increased costs and are

UHY Haines Norton Adelaide 35 | P a g e

worried that they will lose their arrangements. This also affects those that lease a lot of land

& will have them re-assessing the value of their lease agreements.

Rate Capping must be applied above 10% (not 15%) and applied to both Residential and

Primary Production sectors.

In addition to the (at least) 10% discount for primary production land, there should also be a

15% discount or cap which is available to other ratepayers but should be in additional be

available for primary production ratepayers. The discount for rural land should be -10% and

-15% = -25%

I have asked before; why are you sending out rates four times a year and the time and effort

to collect four times, than sending gout once and offer a % discount if pay the whole year in

one payment.

UHY Haines Norton Adelaide 36 | P a g e

Appendix 2 – Consultation Report

A Review of the Basis of Rating Consultation Paper City of Victor Harbor

March 2021

This paper is presented to the community to provide information and invite

feedback on possible changes to Council’s basis of rating.

Consultation Period

Thursday 25th March to Monday 26th April 2021 at 5pm

Public Meeting

Thursday 26th April at 6.30pm at the Council Chambers

Submissions

Written submissions to:

Email: [email protected]

Mail: City of Victor Harbor, PO Box 11, Victor Harbor SA 5211

Verbal and written submissions will be accepted at the Community Information Session and

the Public Meeting.

UHY Haines Norton Adelaide 37 | P a g e

Contents INTRODUCTION .............................................................................................................. 39

1. POTENTIAL CHANGES TO RATES ............................................................................... 39

2. CONSULTATION ........................................................................................................ 39 3.1 Consultation Period ..................................................................................................................... 40

3.2 Submissions ................................................................................................................................. 40

3.3 Public Meeting............................................................................................................................. 40

3. THE PURPOSE OF THIS CONSULTATION PAPER .......................................................... 40

4. WHY COUNCILS COLLECT RATES ............................................................................... 40 5.1 Nature of Council Rates ............................................................................................................. 41

5.2. Principles of Taxation ................................................................................................................. 41

6. LEGISLATIVE FRAMEWORK FOR SETTING COUNCIL RATES ......................................... 41

7. VALUATIONS ............................................................................................................ 42

8. RATING OPTIONS AVAILABLE ................................................................................... 42 7.1. A General Rate ........................................................................................................................... 42

7.2. A Differential Rate ...................................................................................................................... 42 7.2.1. Locality .................................................................................................................................................... 42 7.2.2. Land Use ................................................................................................................................................. 42

7.3. Fixed Charge ............................................................................................................................... 43

7.4. Minimum Rate ............................................................................................................................ 44

7.5. Tiered Rating .............................................................................................................................. 44

7.6. Separate Rates ........................................................................................................................... 44

7.7. Service Rates & Charges ............................................................................................................. 44

7.8. Non-Rateable Property .............................................................................................................. 45

7.9. Rate Concessions ........................................................................................................................ 45

7.10. Rate Rebates and Remissions .................................................................................................. 45

7.11. Maximum Increase Capping .................................................................................................... 45

7.12. Postponement of Rates ........................................................................................................... 46 7.12.1. Hardship................................................................................................................................................ 46 7.12.2. Businesses............................................................................................................................................. 46 7.12.3. Valuation Anomalies ............................................................................................................................ 46 7.12.4. Unusual Events ..................................................................................................................................... 46 7.12.5. Seniors .................................................................................................................................................. 46

8. CITY OF VICTOR HARBOR’S CURRENT RATING METHODOLOGY ................................. 47 8.1. Land Valuation ........................................................................................................................... 47

8.2. Differential Rates based on Land Use. ...................................................................................... 47

8.3. Fixed Charge ............................................................................................................................... 47

8.4. Separate Rates ........................................................................................................................... 48

8.5. Service Rates & Charges ............................................................................................................. 48

9. COMPARISON TO SIMILAR COUNCILS ....................................................................... 48 Australian Centre of Local Government Grouping .............................................................................. 48

South Australian Remuneration Tribunal Groupings .......................................................................... 48

LGA Region ........................................................................................................................................... 48

Neighbouring Councils ......................................................................................................................... 48

Regional Subsidiaries ........................................................................................................................... 48

Comparison Councils ............................................................................................................................ 49

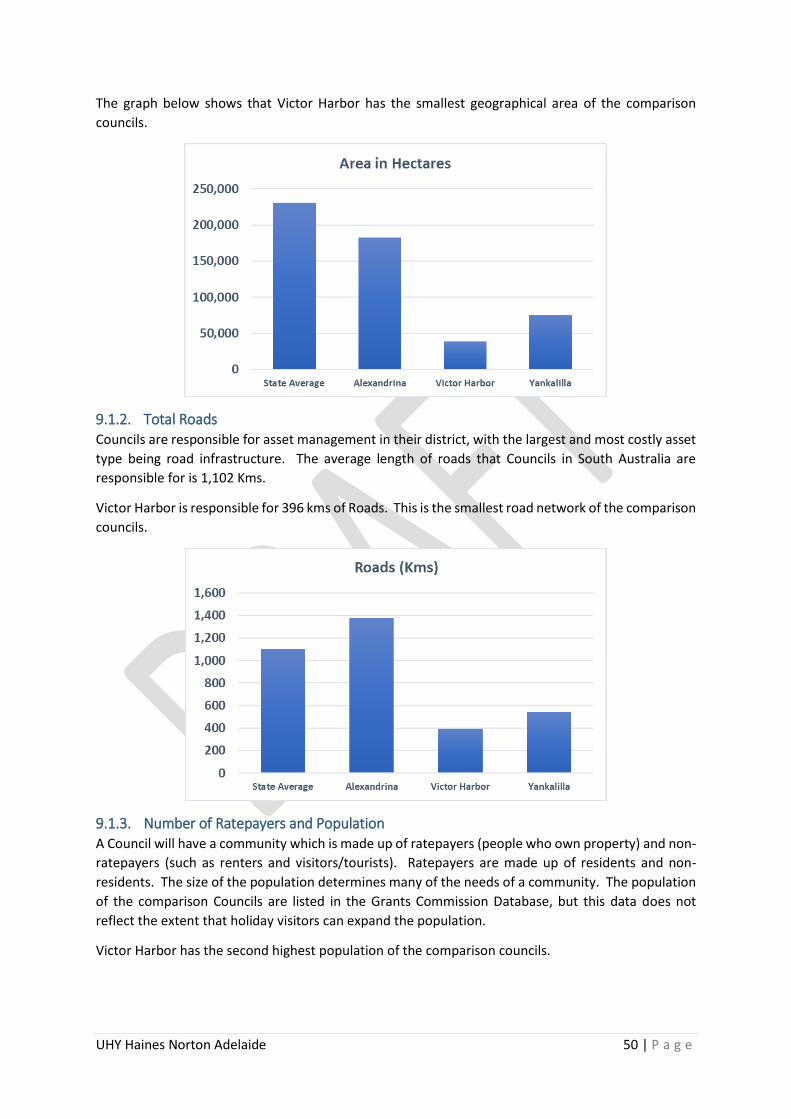

9.1. SA Local Government Grants Commission Database 2018/19 ................................................. 49 9.1.1. Geographic Area ..................................................................................................................................... 49

UHY Haines Norton Adelaide 38 | P a g e

9.1.2. Total Roads ............................................................................................................................................. 50 9.1.3. Number of Ratepayers and Population ................................................................................................. 50 9.1.4. Rates Revenue compared to Total Revenue. ........................................................................................ 51 9.1.5. Cost of Transport Assets per Ratepayer ................................................................................................ 52

9.2. Comparison Rate Structures ...................................................................................................... 53 9.2.1. Rating of Comparison Councils .............................................................................................................. 53

9.3. Victor Harbor Council Profile ..................................................................................................... 53 9.3.1. Australian Bureau of Statistics ............................................................................................................... 53 9.3.2. Socio-economic Index ............................................................................................................................ 54

9.4. Rating as a Tool to Assist in Achieving Strategic Priorities ....................................................... 54

9.5. Rating Structure – Potential Changes and the Impact .............................................................. 55 9.5.1. Increasing the Differential for Vacant Properties ................................................................................. 56 9.5.2. Increasing the Differential for Primary Production Properties ............................................................. 56 9.5.3. Decreasing the Commercial and Industrial Differentials ...................................................................... 57 9.5.4. Retain Current Fixed Charge Amount .................................................................................................... 57 9.5.5. Retain Current Level of Rate Capping .................................................................................................... 58 9.5.6. Separate Rates ........................................................................................................................................ 58 9.5.7. Likely Impact on Ratepayers .................................................................................................................. 58

10. CONSULTATION REQUIREMENTS ............................................................................ 59 10.1. Legislative Requirements for Consultation ............................................................................. 59

BIBLIOGRAPHY ............................................................................................................... 61

APPENDIX 1 – AUSTRALIAN CENTRE OF LOCAL GOVERNMENT GROUPINGS ..................... 62 Codes ..................................................................................................................................................... 62

Descriptions .......................................................................................................................................... 63

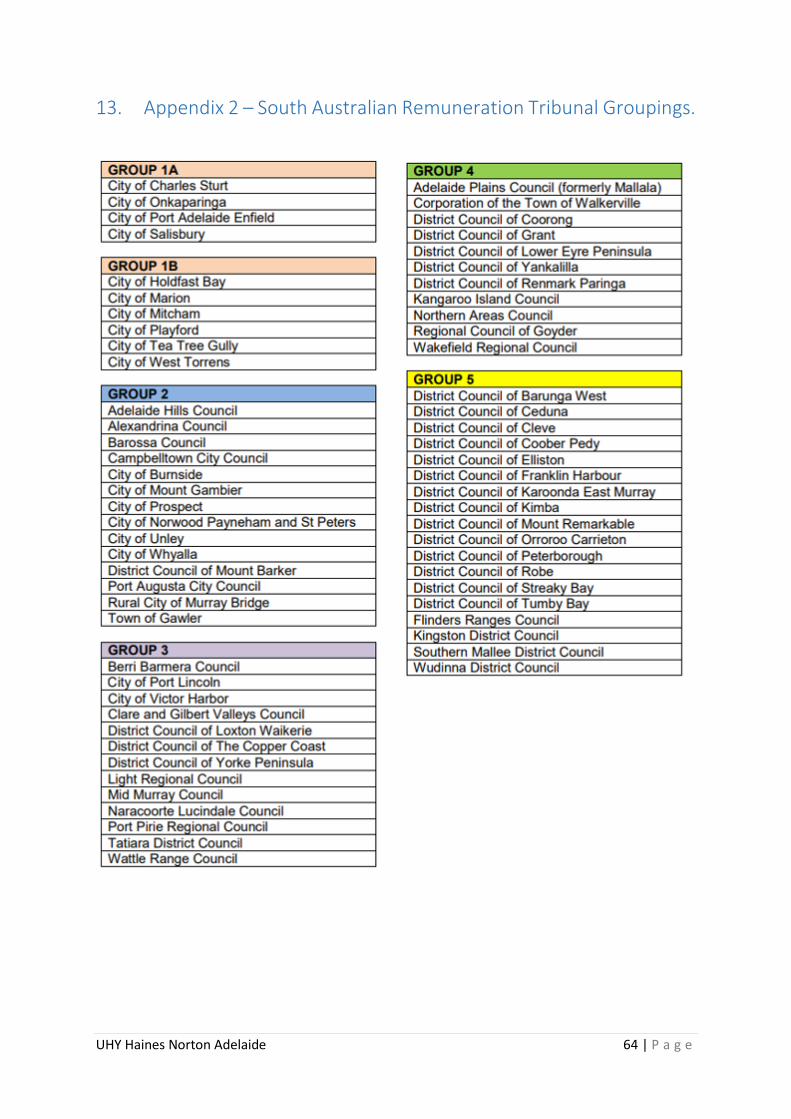

APPENDIX 2 – SOUTH AUSTRALIAN REMUNERATION TRIBUNAL GROUPINGS. ................. 64

LGA REGIONS IN SOUTH AUSTRALIA ............................................................................... 65

UHY Haines Norton Adelaide 39 | P a g e

7. Introduction Councils are responsible for the delivery of a broad range of services to their communities. Each

community is unique and has different priorities. Councils receive income from several sources to pay

for the services they provide, and the largest revenue source is rates.

The Local Government Act 1999 allows Councils to raise rates and provides a degree of flexibility in

the options used by Councils to do this. Councils need to determine the best method for their

communities and review this from time to time to ensure the system they use remains relevant.

The City of Victor Harbor (Council) is reviewing the current methods for setting rates and what

alternative methods, if any, may be more appropriate for the community.

This process is known as a rating review and considers a Council’s rating requirements and the best

way for that Council to distribute the rate burden amongst their community. Each Council will have

different communities, so the rating system used is unique for each Council.

Section 151 of the Local Government Act 1999, states that Council must produce a public report that

must address the following when considering changing their basis of rating:

The reasons for the proposed change

The relationship of the proposed change to the Council’s overall rating structure and policies

As far as practicable, the likely impact of the proposed change on ratepayers

Issues concerning equity within the community.

And any other issues that Council considers relevant.

1. Potential Changes to Rates Council members have considered the information contained in this paper in a workshop and at a

Council meeting. Rating methods available, the current method of rating, potential changes and likely

impacts are detailed in this paper that is now provided for public consultation.

In summary Council is seeking feedback on the following potential changes to Council’s rating

structure.

Decrease the Commercial and Industry differentials to the same as Residential Properties.

Increase the Vacant Differential to 160% of the Residential Differential

Increase Primary Production at 100% of the Residential Differential.

As the decrease in the Commercial and Industry differentials will affect other ratepayers, this change

is proposed to be introduced over a 5-year period.

Section 9.5 of this paper discusses the various options discussed during workshops and Section 9.5.7

outlines the likely impact on ratepayers for a range of sample properties.

2. Consultation It is important for Council to receive feedback from the community when making decisions that affect

ratepayers. Council is required to consult when reviewing rating methods and your comments are

very useful to help Council understand the community and make decisions that soundly reflect your

current and future needs.

UHY Haines Norton Adelaide 40 | P a g e

3.1 Consultation Period The consultation period will be for the following period:

Thursday 25th March to Monday 26th April 2021 at 5pm

3.2 Submissions Members of the community are invited to make written submissions expressing their views on the

future structure of Council’s basis of rating, and the information contained within this consultation

paper. Submissions will be accepted until 5pm on Monday 26th April 2021.

Submissions can be provided by:

Email: [email protected]

Mail: City of Victor Harbor, PO Box 11, Victor Harbor SA 5211

3.3 Public Meeting In addition to written submissions, Council invites members of the community to attend a public

meeting, at the Council Chambers on the 22nd April at 6.30pm. Members of the public can make

submissions in person at this meeting.

Further information regarding the Review of Council’s Basis of Rating can be obtained by contacting

Council.

3. The Purpose of this Consultation Paper The purpose of this consultation paper is to provide our community with information in relation to

the following which Council has considered as background to the proposed changes:

Why Councils collect rates.

Council’s current rating methodology

Legislative framework for setting Council rates.

Rating Options available

Options that may be appropriate for Council

Consultation Requirements.

4. Why Councils Collect Rates Councils are responsible for the delivery of a broad range of services to the community. The range of

services continues to grow.

To support the provision of services and to improve the quality of life for all the community, whether

residential, business, or primary production, Councils provide significant levels of infrastructure in the

form of roads, bridges, drainage, buildings, parks, and recreation facilities. This infrastructure needs

to be maintained and replaced. Councils also provide a vast range of other services to their

communities.

Each Council provides unique services for their own communities as different communities have

different priorities. Councils are therefore faced with the challenge to:

Establish a level of infrastructure and services for its community; and

Equitably distribute revenue raising that provides funding for infrastructure and services.

As each Council faces different circumstances and provide a different mix of services to its community,

it is likely that its revenue requirements are different from its neighbours. The capacity of each Council

UHY Haines Norton Adelaide 41 | P a g e

to raise revenue and the way that the ratepayers will share in providing the revenue will also be

different in each Council.

5.1 Nature of Council Rates Taxation is the major source of revenue for Governments. Councils are responsible for raising their

own revenue by way of property taxation (Rates) and user charges as prescribed by legislation.

Councils also receive Government funding.

Many ratepayers will question the value they individually receive from the rates they pay; however,

rates are raised as a form of taxation for services for the whole community. Rates are a wealth tax,

taxed against the value of property. The principle being that the more property, or the higher the

value of the property, the more you should and are able to pay.

One problem with a wealth tax is that someone that owns a property that has a high value may not

have the income to pay a higher level of tax. An example is a person, who has lived in an area their

whole life, but the area has become popular, and the value of the property has increased dramatically.

That person may now be living in a very valuable property and rated as such but may not have the

income to afford this level of rating.

5.2. Principles of Taxation When setting taxes, Governments and Councils need to be mindful of the principles of taxation. The

principles are:

equity – taxpayers with the same income pay the same tax (horizontal equity), wealthier

taxpayers pay more tax (vertical equity);

benefit – taxpayers should receive some benefits from paying tax, but not necessarily to the

extent of the tax paid;

ability-to-pay – in levying taxes the ability of the taxpayer to pay the tax must be considered;

efficiency – if a tax is designed to change consumers’ behaviour and the behaviour changes,

the tax is efficient (e.g., tobacco taxes), if a tax is designed to be neutral in its effect on

taxpayers and it changes taxpayers’ behaviour the tax is inefficient; and

Simplicity – the tax must be understandable, hard to avoid and easy to collect.

To some extent these principles conflict with each other. Governments and Councils must balance

the application of the principles, the policy objectives of taxation, the need to raise revenue and the

effects of the tax on the community.

6. Legislative Framework for Setting Council Rates The Local Government Act 1999 (the Act) sets out the framework of rating for Councils. The Act can

be accessed at: https://www.legislation.sa.gov.au/.

The legislation outlines the following topics which are relevant for Council when considering changing

its basis of rating.

Chapter 10 – Rates and Charges

Part 1 – Rates and charges on land

o Division 1 - Preliminary

o Division 2 – Basis of rating

o Division 3 – Specific characteristics of rates and charges

o Division 4 – Differential rating and special adjustments

UHY Haines Norton Adelaide 42 | P a g e

o Division 5 – Rebates of rates

o Division 6 – Valuation of land for the purpose of rating

7. Valuations Rates are calculated against the valuation of a property. There are two valuation options available

under the current legislation being Capital (improved value) of a property, i.e., land and house

valued together, or Site where only the land value is used.

Site value is not used by many Councils in South Australia and the drafted Statues Amendment (Local

Government Review) Bill 2020 may remove this option in the future.

8. Rating Options Available There are several alternative rating options available under the Act. The options that can be

considered are:

A General Rate

A Differential General Rate

Fixed Charge

Minimum Rate

Tiered Rating

Separate Rates

All rating options provide different ways for the cost of running the Council to be distributed amongst

ratepayers. Councils need to consider the profile and issues of their communities and determine the

method that distributes the rates tax burden in the most appropriate manner for their community.

7.1. A General Rate All properties are charged the same ‘rate in the dollar’, regardless of land use or locality. This is very

simple to administer.

7.2. A Differential Rate This means there are different ‘rates in the dollar’ set for different categories of properties.

Differentiating property based on Locality and Land Use are described below. A Council can use either

Land Use or Locality or a combination of both.

A differential rate allows a Council to structure their rating strategy more closely with their

community’s needs and profile and to use rating as a tool to assist in achieving Council’s strategic

goals.

7.2.1. Locality Rating according to where a property is. Some Councils set different ‘rates in the dollar’ for different

townships, or whether a property is inside or outside a township(s). The locality is determined by

development zone the property is in.

7.2.2. Land Use This is where the ‘rate in the dollar’ is set depending upon what the property is used for. The Land

Use types in accordance with the Local Government Regulations and as determined by the Valuer

General are:

Residential

Commercial (Shop)

UHY Haines Norton Adelaide 43 | P a g e

Commercial (Office)

Commercial (Other)

Industrial (Light)

Industrial (Other)

Primary Production

Vacant Land

Other

Marina Berth

The use of differential rates makes the rating system more complex, but not usually to the extent that

it offends the simplicity principle. This is reflected by the fact that most South Australian Councils use

this rating method. Differentials can also be used based on combinations of Locality and Land Use and

Councils that use this combination can have quite complex rating structures.

Differential rates based on land use can allow a Council to set policy direction in regard to their rating,

such as:

Lower ‘rate in the dollar’ to assist or encourage a certain type of land use.

Higher ‘rate in the dollar’ to deter a certain type of land use, or as an acknowledgement that

a land use group needs to pay a higher contribution to the rates burden for the community.

7.3. Fixed Charge Under this system a fixed amount is first applied evenly against all ratepayers. The remaining amount

of rate revenue would be based on the valuation of the property.

The Act states that a Council must not seek to set a fixed charge at levels that will raise more than 50%

of all general rate revenue.

The fixed charge is levied against a property first and then a Rate in the Dollar (RID) is charged against

the valuation of the property and these amounts are combined to reach the rates that will be levied

for this property. If a fixed charge is not levied, the RID will be higher to reach the same level of

calculated rates.

The effect of a fixed charge is a lower rate in the dollar resulting in higher valued properties paying

less than they would if there were no fixed charge.

This system would disadvantage owners of lower valued properties and could offend the ‘ability to

pay’ principle.

Developers with several adjoining blocks will only pay one fixed charge and all the remaining