audit committee meeting - city of kwinana › our-council › agendas-and-minutes...city of kwinana...

TRANSCRIPT

28 November 2017

Audit Committee Meeting

Agenda

Members of the public who attend Committee meetings should not act immediately on anything they hear at the meetings, without first seeking clarification of Council’s position. Persons are advised to wait for written advice from the Council prior to taking action on any matter that they may have before Council.

Agendas and Minutes are available on the City’s website www.kwinana.wa.gov.au

Notice is hereby given of the Audit Committee Meeting of Council to be held in the Council Chambers, City of Kwinana Administration Centre commencing at 5:30pm.

Michelle Bell Acting Chief Executive Officer

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 2

Vision Statement Kwinana 2030 Rich in spirit, alive with opportunities, surrounded by nature – it’s all here! Mission Strengthen community spirit, lead exciting growth, respect the environment - create great places to live. We will do this by – ● providing strong leadership in the community; ● promoting an innovative and integrated approach; ● being accountable and transparent in our actions; ● being efficient and effective with our resources; ● using industry leading methods and technology wherever possible; ● making informed decisions, after considering all available information; and ● providing the best possible customer service. Values We will demonstrate and be defined by our core values, which are: • Lead from where you stand – Leadership is within us all. • Act with compassion – Show that you care. • Make it fun – Seize the opportunity to have fun. • Stand Strong, stand true – Have the courage to do what is right. • Trust and be trusted – Value the message, value the messenger. • Why not yes? – Ideas can grow with a yes.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 3

TABLE OF CONTENTS

1 Declaration of Opening ......................................................................................... 4 2 Apologies/Leave(s) of Absence (previously approved) ...................................... 4 3 Public Question Time: ........................................................................................... 4 4 Declaration of Interest by Members: .................................................................... 4 5 Minutes to be Confirmed: ..................................................................................... 5

5.1 Audit Committee Meeting held on 18 September 2017. ...................................... 5 6 Reports .................................................................................................................. 6

6.1 Review of Audit Committee Terms of Reference ................................................ 6 6.2 Local Government Amendment (Auditing) Act 2017 .......................................... 9 6.3 Internal Audit Plan Review for the period 18 September to 27 November 2017

and Internal Audit Plan for the period 28 November 2017 to 19 March 2018 .. 13 7 Urgent Business .................................................................................................. 20 8 Response to Previous Questions ....................................................................... 20 9 Matters Behind Closed Doors ............................................................................ 20 10 Next Meeting ........................................................................................................ 20 11 Meeting Closure .................................................................................................. 20

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 4

1 Declaration of Opening

Presiding Member to read the Welcome

“IT GIVES ME GREAT PLEASURE TO WELCOME YOU ALL HERE AND BEFORE COMMENCING THE PROCEEDINGS, I WOULD LIKE TO ACKNOWLEDGE THAT WE COME TOGETHER TONIGHT ON THE TRADITIONAL LAND OF THE NOONGAR PEOPLE”

2 Apologies/Leave(s) of Absence (previously approved)

Apologies Leave(s) of Absence (previously approved): Nil

3 Public Question Time:

In accordance with the Local Government Act 1995 and the Local Government (Administration) Regulations 1996, any person may during Public Question Time ask any question.

In accordance with Regulation 6 of the Local Government (Administration) Regulations 1996, the minimum time allowed for Public Question Time is 15 minutes.

A member of the public who raises a question during Question Time is to state his or her name and address.

4 Declaration of Interest by Members:

Elected Members are to deliver to the Chief Executive Officer:

(a) written notice of any Declaration of Interest prior to the meeting; or (b) at the meeting immediately before the matter is discussed [Local

Government Act 1995 Section 5.65(1)]. A City employee who has an interest in any matter of which the employee is providing advice or a report directly to the Council or Committee must disclose the nature of the interest when giving the advice or report [Local Government Act 1995 Section 5.7(2)].

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 5

5 Minutes to be Confirmed:

5.1 Audit Committee Meeting held on 18 September 2017.

Moved Cr ....................... Seconded Cr ............................. that the Minutes of the Audit Committee held on 18 September 2017 be confirmed as a true and correct record of the meeting.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 6

6 Reports

6.1 Review of Audit Committee Terms of Reference

SUMMARY: One of the functions of the Audit Committee includes reviewing the effectiveness of the local government’s systems in regard to risk management, internal control and legislative compliance of the local government. This is achieved in part by the development of a Terms of Reference for the Audit Committee to identify the Committee’s responsibilities. The current Audit Committee Terms of Reference has been reviewed and is provided to the Audit Committee with a view to present to Council for adoption. The reviewed document is at Attachment A. OFFICER RECOMMENDATION: That the Audit Committee recommend that Council adopt the reviewed Audit Committee Terms of Reference (as per Attachment A). DISCUSSION: The Audit Committee Terms of Reference was recently reviewed in February 2017 and as a result, only one amendment is recommended. The proposed amendment is to update the year for which a financial management review in clause 7(h) is to be undertaken as the review was completed in May 2017 and the next review is due in another four years (2021). No further amendments have been identified or are recommended. LEGAL/POLICY IMPLICATIONS: Local Government Act 1995 2.7. Role of council (1) The council —

(a) governs the local government’s affairs; and (b) is responsible for the performance of the local government’s functions.

(2) Without limiting subsection (1), the council is to —

(a) oversee the allocation of the local government’s finances and resources; and (b) determine the local government’s policies.

5.103. Codes of conduct (1) Every local government is to prepare or adopt a code of conduct to be observed by council members, committee members and employees.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 7

6.1 REVIEW OF AUDIT COMMITTEE TERMS OF REFERENCE

5.104. Other regulations about conduct of council members (1) Regulations may prescribe rules, to be known as the rules of conduct for council members, that council members are required to observe. (6) The rules of conduct do not limit what a code of conduct under section 5.103 may contain. LOCAL GOVERNMENT (AUDIT) REGULATIONS 1996 - REG 16 16. Audit committee, functions of An audit committee — (a) is to provide guidance and assistance to the local government —

(i) as to the carrying out of its functions in relation to audits carried out under Part 7 of the Act.

17. CEO to review certain systems and procedures (1) The CEO is to review the appropriateness and effectiveness of a local government’s systems and procedures in relation to —

(a) risk management; and (b) internal control; and (c) legislative compliance.

(2) The review may relate to any or all of the matters referred to in subregulation (1)(a), (b) and (c), but each of those matters is to be the subject of a review at least once every 2 calendar years. (3) The CEO is to report to the audit committee the results of that review. FINANCIAL/BUDGET IMPLICATIONS: There are no specific financial or budget implications as a result of this report. ASSET MANAGEMENT IMPLICATIONS: There are no specific asset management implications as a result of this report. ENVIRONMENTAL IMPLICATIONS: There are no specific environmental implications as a result of this report.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 8

6.1 REVIEW OF AUDIT COMMITTEE TERMS OF REFERENCE STRATEGIC/SOCIAL IMPLICATIONS: This proposal will support the achievement of the following objectives and strategies detailed in the Strategic Community Plan and/or Corporate Business Plan (D16/3339). Plan Objective Strategy e.g. Corporate Business Plan 2016 - 2021

5.1 An active and engaged Local Government, focussed on achieving the community’s vision

5.1.1 Ensure that the City’s strategic direction, policies, plans, services and programs are aligned with the community’s vision

COMMUNITY ENGAGEMENT: Community engagement may be required via advertising in a state-wide newspaper if a decision is made to seek appointment of a new external audit committee member. RISK IMPLICATIONS: The risk implications in relation to this proposal are as follows:

Risk Event Poor decision making due to inadequate policies

Risk Theme Failure to fulfil statutory regulations or compliance requirements

Risk Effect/Impact Reputation Risk Assessment Context

Strategic

Consequence Minor Likelihood Possible

Rating (before treatment)

Moderate

Risk Treatment in place Reduce - mitigate risk Response to risk treatment required/in place

Ensure that adequate policies are in place and reviewed regularly.

Rating (after treatment) Low

D13/43967[v5 4] Page 1 of 3

Terms of Reference - Audit Committee 1. History (Regulation 17 Local Government (Audit) Regulations 1996)The establishment of an Audit Committee in the past has been to provide an independent oversight of the financial position of the local government particularly related to the function of auditing; the scope of an audit and the process used to selecting and appointing of an auditor where the Office of the Auditor General does not carry out an audit.

This focus has expanded and an Audit Committee (herein referred to as the “Committee”) now operates not only to support the local government in effective financial management but also to provide effective corporate governance through the review of systems and procedures in place relating to risk management, internal control and legislative compliance.

2. Objectives of the Audit CommitteeThe Committee plays a key role in assisting the City of Kwinana to fulfill its corporate governance responsibilities in managing the affairs of the local government. This includes financial reporting, risk management, compliance requirements, internal and external audits.

The Committee will ensure transparency in the City of Kwinana’s financial reporting and will liaise with the Chief Executive Officer to ensure the effective and efficient management of the local government’s financial accounting systems and compliance with legislation.

The Committee is to facilitate:

a) compliance with laws and regulations as well as use of best practice guidelines relativeto auditing, through external financial auditors and internal operational audits;

b) the provision of an effective means of communication between the external auditor, theChief Executive Officer and Council.

3. Powers of the Audit CommitteeA local government is required to establish an Audit Committee under Section 7.1A of the Local Government Act 1995. The Committee is a formally appointed committee of Council and is responsible to that body. All recommendations of the Committee are to be made by a simple majority. Reports and recommendations of the Committee shall be presented to the next ordinary meeting of Council.

The Committee may be delegated certain powers under Part 7 of the Local Government Act 1995 by Council. The purpose of the Committee is to provide advice and recommendations to Council.

4. Membership and participationThe Committee will consist of five elected members and may include one external member. The members of the Committee must be appointed by absolute majority. All members have full voting rights.

The Chief Executive Officer and employees are not to be members of the Committee, however the Chief Executive Officer is to be given every opportunity to provide expert advice to the Ccommittee and should attend every meeting.

ATTACHMENT A

D13/43967[v5 4] Page 2 of 3

The Chief Executive Officer is not permitted to nominate a person to be a member of a Committee or have a person represent him or her as a member of the Committee. The local government shall provide secretarial and administrative support to the Committee. If a duty has been delegated by Council to the Committee, meetings are required by Regulation to be open to the public.

5. Meetings The Committee should meet at times during the year that most effectively coincide with the requirements of legislation for that year, and operational activities, with a view to providing the necessary reports well before the due dates. An example of a meeting schedule is provided below: Date of Audit Committee Meeting

Agenda Items to Audit Committee

2nd week of March • Statutory Compliance Audit return (legislation requires adoption by Council and submission by 31 March)

• Annual Budget Review if available (not a requirement for the Audit Committee however the report does need to go to Council therefore it is seen as useful for the Audit Committee)

• Investment Policy Review (only required every second year) • When applicable, approval to seek expressions of interest

requests for quotes for the appointment of an auditor for the next period where the Office of the Auditor General is not required to carry out the audit.

• Progress report on the internal audit findings October / 1st week of November

• Review of systems and procedures in place relating to risk management, internal control and legislative requirements (only required every second year)

• End of Financial Year Statements • Auditor’s report • Accepting Audit • Financial Management Review • Progress report on the internal audit findings

To be confirmed • Progress report on the internal audit findings To be confirmed • Progress report on the internal audit findings Additional meetings may be convened as required and approved by Council at the discretion of the presiding person.

6. Quorum A quorum shall consist of at least 50% of the number of offices of committee members, unless a reduction is approved by the local government under s5.15 of the Local Government Act 1995.

7. Duties and Responsibilities

D13/43967[v5 4] Page 3 of 3

The Audit Committee is to report to Council and provide appropriate advice and recommendations on matters relevant to the Terms of Reference in order to facilitate informed decision-making by Council.

Other duties and responsibilities of the Committee are as follows:

a) Identify and recommend to Council a list of those matters to be audited (in relation toexternal and internal audits).

b) Develop and recommend to Council an appropriate process for the selection andappointment of a person as the local government’s auditor where the Office of theAuditor General is not required to carry out the audit.

c) Develop and recommend to Council a written agreement for the appointment of theauditor where the Office of the Auditor General is not required to carry out the audit.The agreement is to include:• the objectives of the audit;• the scope of the audit; and• details of the remuneration and expenses to be paid to the auditor; and the

method to be used by the local government to communicate with and supplyinformation to the auditor.

d) Liaise with the Chief Executive Officer to ensure that the local government doeseverything in its power to:• assist the auditor to conduct the audit and carry out his or her other duties under

the Local Government Act 1995; and• ensure that audits are conducted successfully and expeditiously.

e) Examine the reports of the audit (internal/external) and accompanying officer report to:• determine if any matters raised require action to be taken by the local

government; and• ensure that appropriate action be taken in respect of those matters.

f) Review the report prepared by the Chief Executive Officer on any actions taken inrespect of any matters raised in the report of the auditor and presenting the report toCouncil for adoption prior to the end of the next financial year or six months after thelast report prepared by the auditor is received, whichever is the latest in time.

g) Consider biennially, the report from the Chief Executive Officer on the appropriatenessand effectiveness of a local government’s systems and procedures in relation to riskmanagement; internal control and legislative compliance.

h) Undertake a financial management review every 4 years, with the next reviewrequired in 202117.

i) Liaise with the Office of the Auditor General regarding the financial statements andperformance audits of the City.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 9

6.2 Local Government Amendment (Auditing) Act 2017 SUMMARY: The purpose of this report is to provide a summary to the Audit Committee of the changes to the Local Government Act 1995 due to the proclamation of the Local Government Amendment (Auditing) Act 2017. OFFICER RECOMMENDATION: That the Audit Committee note the gazettal of the Local Government Amendment (Auditing) Act 2017. DISCUSSION: The Local Government Amendment (Auditing) Act 2017, provides for the auditing of local governments by the Auditor General. The Act was given Royal Assent on 1 September 2017 and was gazetted on 27 October 2017. The City received a letter dated 22 September 2017 from the Auditor General, Colin Murphy (Attachment A), outlining some key information in regards to the practical impact of the changes made within the Local Government Amendment (Auditing) Act 2017 and is summarised below: Financial audits — timing There is a staged transition approach for financial audits to allow for existing contracts to expire. However, by financial year 2020-21, all local governments will be audited by the Office of the Auditor General, regardless of whether or not their existing audit contracts have expired. Financial audits — contract audit firms The Auditor General plans to contract out the majority of local government financial audits to accredited audit firms with the remaining to be conducted by staff within the Office of the Auditor General. Where audits are outsourced, the contracts will be managed by the Office of the Auditor General and the audit opinions will be signed and issued by the Auditor General. It is common practice for Auditors General from across jurisdictions to outsource audits and is something they currently do for state government audits. They have contract management processes in place to ensure that outsourced audits are efficient and cost effective and meet their audit quality standards. Financial audits — fees Fees will be charged for financial audits, as they are now. The Office of the Auditor General fees has been set purely to recoup the full cost of conducting a local government financial audit. The fee is based on the staff hours used on the audit plus any directly related costs such as contract fees and travel expenses. Based on experience in other States, the Auditor General expects some audit fees will be considerably higher than they currently are. This is primarily because the Auditor General will be conducting a much broader financial audit than currently received by most local governments. The Auditor General’s audits will give assurance on the financial statements and greater transparency about financial controls, probity and governance matters.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 10

6.2 LOCAL GOVERNMENT AMENDMENT (AUDITING) ACT 2017 Performance audits The Act also allows for performance audits, which may examine the economy, efficiency and effectiveness of any aspect of local government operations. The Office of the Auditor General has been conducting performance audits of state government agencies since they first received the mandate in 1985. Performance audit topics are selected following a comprehensive topic selection process which may also include requests for audits from Parliament, the government and other key stakeholders and the broader community. The Office of the Auditor General publish their audit program on their website and it will be updated as local government audit topics are determined. Unlike financial audits, which are paid for by each local government to cover the cost of doing the audit, performance audits are funded by government appropriation. The number and size of performance audits are therefore determined by the level of appropriation received and the priority given to these by Parliament. Importantly, like current state government performance audits, the findings and recommendations of these are applicable to all local governments and not just those audited. If and when your organisation will be included as part of a performance audit will only be determined as each audit topic is selected and planned. The Office of the Auditor General Audit Practice Statement, available on their website, provides a detailed guide on what to expect during a performance audit, including information on procedural fairness processes and their ‘no surprises’ approach to reporting. Further information on the Local Government Amendment (Auditing) Act 2017 can be found within the Local Government Amendment (Auditing) Act 2017 Explanatory Memorandum (Attachment B). The City currently has an audit contract with Moore Stephens (WA) Pty Ltd. This contract is due to end upon the completion of the 30 June 2018 financial audit. Unless otherwise instructed by the Office of the Auditor General, the City will be able to see out the completion of this contract whereby the Office of the Auditor General will then take over the external auditing program for the City. The operational impact on the City is likely to be minimal as audits will still be required and are likely to operate in a similar manner to the current approach. It is envisaged that further information and guidance from the Department of Local Government, Sport and Cultural Industries and the Office of the Auditor General will be provided upon finalisation of any amendments to the Local Government (Audit) Regulations 1996. City Officers have received advice from the Office of the Auditor General that there may be some audits that the City is required to undertake that does not fall part of their scope. The Audit Committee will appoint an auditor for works that falls outside the Office of the Auditor General. LEGAL/POLICY IMPLICATIONS: Part 7 – Audit, of the Local Government Act 1995, deals with the audit of the financial accounts of local governments, including — (a) the appointment of auditors; and (b) the conduct of audits.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 11

6.2 LOCAL GOVERNMENT AMENDMENT (AUDITING) ACT 2017 FINANCIAL/BUDGET IMPLICATIONS: Budget implications associated with this report have been outlined within the discussion. ASSET MANAGEMENT IMPLICATIONS: There are no specific asset management implications as a result of this report. ENVIRONMENTAL IMPLICATIONS: There are no specific environmental implications as a result of this report. STRATEGIC/SOCIAL IMPLICATIONS: This proposal will support the achievement of the following objectives and strategies detailed in the Strategic Community Plan and/or Corporate Business Plan (D16/3339).

Plan Objective Strategy Corporate Business Plan 2016 - 2021

5.1 An active and engaged Local Government, focussed on achieving the community’s vision

5.1.1 Ensure that the City’s strategic direction, policies, plans, services and programs are aligned with the community’s vision

COMMUNITY ENGAGEMENT: There is no community engagement required as a result of this report.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 12

6.2 LOCAL GOVERNMENT AMENDMENT (AUDITING) ACT 2017 RISK IMPLICATIONS: The risk implications in relation to this proposal are as follows: Risk Event The City’s compliance obligations are not met

due to insufficient knowledge and information.

Risk Theme Failure to fulfil statutory regulations or compliance requirements

Risk Effect/Impact Reputation/Compliance Risk Assessment Context

Strategic

Consequence Minor Likelihood Unlikely Rating (before treatment)

Low

Risk Treatment in place Reduce - mitigate risk Response to risk treatment required/in place

Ensure that Elected Members and City Officers are kept informed of the changes to the Local Government Amendment (Auditing) Act 2017.

Rating (after treatment) Low

OAS Office of the Auditor General

Sen/mg the Public Interest

Our Ref: 7576 7th Floor, Albert Facey House 469 Wellington Street, Perth

Mail to: Perth BC Ms Joanne Abbiss p0 BOX 8489

Chief Executive Officer PERTH WA 6849

City Of Kwinana Tel: 08 6557 7500

PO Box 21 Fax: 08 6557 7600

KWINANA WA 6966 Email: [email protected]

Dear Ms Abbiss

LOCAL GOVERNMENT AMENDMENT (AUDITING) ACT 2017

As you are likely aware, the Local Government Amendment (Auditing) Act 2017, giving the Auditor General a mandate to audit local governments, was assented to on 1 September 2017. However, the sections of the Act that will allow my Office to commence local government audit still need to be proclaimed. I understand from the Department of Local Government, Sport and Cultural Industries (DLGSCI) this is likely to occur in October.

While this has been an initiative of Parliament and not something I have actively pursued, I am certainly supportive of the intent behind the Act and look forward to working with you to ensure a successful transition.

I recognise with these changes comes some uncertainty primarily around the impact on your financial audit program and associated activities. This is also a significant change for my Office and is one of the largest changes to the Auditor General’s mandate since the role was established in 1829.

Please be assured that we are well placed to take on local government auditing. My Office is made up of highly trained, professional, qualified and experienced auditors and support staff who are well placed to perform local government financial and performance audits. The expertise my staff has developed auditing various bodies in the public sector is also very relevant to local government and puts us in a strong position to add value to the local government sector.

Financial audits — timing There is a staged transition approach for financial audits to allow for existing contracts to expire. However, by financial year 2020-21, all local governments will be audited by my Office, regardless of whether or not their existing audit contracts have expired.

Financial audits — contract audit firms I plan to contract out the majority of local government financial audits to accredited audit firms with the remaining to be conducted by my staff. Where audits are outsourced, the contracts will be managed by my Office and I will sign and issue all audit opinions.

It is common practice for Auditors General from across jurisdictions to outsource audits and is something we currently do for state government audits. Our contract management processes ensure that outsourced audits are efficient and cost effective and meet our audit quality standards.

For those audits we outsource, we plan to appoint the audit firm whose contract has expired to perform the audit for the 1St year if it meets certain quality criteria. In the 2nd year, the audit will go to tender and all tendering firms must be accredited with us. We have been in contact with existing audit firms to discuss these arrangements.

Financial audits — fees Fees will be charged for financial audits, as they are now. Our fees are set purely to recoup the full cost of conducting a local government financial audit. The fee is based on the staff hours used on the audit plus any directly related costs such as contract fees and travel expenses.

Based on experience in other States, we expect some audit fees will be considerably higher than they currently are. This is primarily because we will be conducting a much broader financial audit than currently received by most local governments. Our audits will give assurance on the financial statements and greater transparency about financial controls, probity and governance matters.

Financial audits — operational and reporting requirements I will be in touch with you again shortly after the Act has been proclaimed with specific detail about our financial audit program, timing and requirements as it relates to your organisation.

Performance audits The Act also allows for performance audits, which may examine the economy, efficiency and effectiveness of any aspect of local government operations. My Office has been doing performance audits of state government agencies since we first received the mandate in 1985. You can View these reports to Parliament on our website.

We select performance audit topics following a comprehensive topic selection process which may also include requests for audits from Parliament, the government and other key stakeholders and the broader community. We publish our audit program on our website and this will be updated as local government audit topics are determined.

Unlike financial audits, which are paid for by each local government to cover the cost of doing the audit, performance audits are funded by government appropriation. The number and size of performance audits are therefore determined by the level of appropriation received and the priority given to these by Parliament. Importantly, like our current state government performance audits, the findings and recommendations of these are applicable to all local governments and not just those audited.

If and when your organisation will be included as part of a performance audit will only be determined as each audit topic is selected and planned. Our Audit Practice Statement, available on our website, provides a detailed guide on what to expect during a performance audit, including our procedural fairness processes and our ‘no surprises’ approach to reporting. We will be in contact if and when your organisation is selected as part of a performance audit.

Ongoing communication and further information I will contact you again once the Act has been fully proclaimed with further detail specific to your organisation.

My Office has arranged to attend a number of the upcoming local government zone meetings and we will visit some local governments in the coming months — formally as part of our audit process and informally when we are in the area on other business. We will be adding additional local government information and resources to our website shortly and will be providing you with direct updates as my audit program evolves.

Throughout this process we have been speaking with various stakeholders including a number of local governments and councils, DLGSCI, WALGA, Local Government Professionals and Parliament. 1 was pleased to have presented at the WALGA local government convention in August and my Deputy was fortunate to deliver a presentation at an August meeting of local government financial professionals. Coming up, I am looking forward to also speaking at the WALGA cyber security forum in November.

Looking forward The changes under this new Act bring Western Australia in line with other Australian states and New Zealand. We work closely with our interstate counterparts to share knowledge and learn from their experiences in local government audit. While this is new for WA, your organisation and mine, it is not unprecedented. I look forward to working with you to ensure a successful and mutually beneficial transition.

Yours sincerely

6M COLIN MURPHY AUDITOR GENERAL 22 September 2017

cc Mayor Carol Adams

3—1 page i

Western Australia

Local Government Amendment (Auditing)

Bill 2017

Contents

1. Short title 2

2. Commencement 2

3. Act amended 2

4. Section 1.4 amended 2

5. Section 3.64 amended 3

6. Section 3.70A inserted 3

3.70A. Audit requirements for regional subsidiaries 3

7. Section 5.53 amended 4

8. Section 5.55A inserted 4

5.55A. Publication of annual reports 4

9. Section 5.94 amended 4

10. Section 7.1 amended 5

11. Section 7.1A amended 6

12. Section 7.1D inserted 6

7.1D. Application 6

13. Section 7.3 amended 6

14. Section 7.7 amended 7

15. Section 7.8A inserted 7

7.8A. Application 7

16. Section 7.9 amended 7

17. Section 7.11 amended 7

18. Part 7 Divisions 3A to 3D inserted 8

Division 3A — Financial audit

7.12AA. Application 8

7.12AB. Conducting a financial audit 8

7.12AC. Dispensing with a financial audit 8

7.12AD. Reporting on a financial audit 8

7.12AE. Fees for a financial audit 9

Division 3B — Supplementary audit

7.12AF. Application 9

Local Government Amendment (Auditing) Bill 2017

Contents

page ii

7.12AG. Conducting a supplementary audit 9

7.12AH. Reporting on a supplementary audit 9

7.12AI. Fees for a supplementary audit 10

Division 3C — Performance audit

7.12AJ. Conducting a performance audit 10

7.12AK. Reporting on a performance audit 11

Division 3D — Other audits

7.12AL. Audits of accounts of related entities and certain subsidiary bodies 11

19. Section 7.12A amended 11

20. Section 7.13 amended 13

21. Schedule 9.3 amended 15

Division 4 — Provisions for the Local Government Amendment (Auditing) Act 2017

49. Terms used 15

50. Minister to publish status of audit contracts 16

51. Audit contracts may be terminated after completion of FY17/18 audit 16

52. Audit contracts are terminated after completion of FY19/20 audit 17

53. No breach of contract 17

54. Transitional regulations 17

22. Superseded provisions to be deleted 18

page 1

Western Australia

LEGISLATIVE ASSEMBLY

Local Government Amendment (Auditing)

Bill 2017

A Bill for

An Act to amend the Local Government Act 1995 to provide for the

auditing of local governments by the Auditor General and for related

purposes.

The Parliament of Western Australia enacts as follows:

Local Government Amendment (Auditing) Bill 2017

s. 1

page 2

1. Short title 1

This is the Local Government Amendment (Auditing) Act 2017. 2

2. Commencement 3

This Act comes into operation as follows — 4

(a) sections 1 and 2 — on the day on which this Act 5

receives the Royal Assent; 6

(b) the rest of the Act, other than sections 4(2) and 7(2) — 7

on a day fixed by proclamation, and different days may 8

be fixed for different provisions; 9

(c) sections 4(2) and 7(2) — on the day fixed by 10

proclamation under section 22(2). 11

3. Act amended 12

This Act amends the Local Government Act 1995. 13

4. Section 1.4 amended 14

(1) In section 1.4 delete the definition of auditor and insert: 15

16

auditor means — 17

(a) in relation to an audit, other than a performance 18

audit — 19

(i) in relation to a local government that 20

has an audit contract that is in force — a 21

person for the time being appointed 22

under Part 7 Division 2 to be the auditor 23

of the local government; and 24

(ii) in relation to a local government that 25

does not have an audit contract that is in 26

force — the Auditor General; 27

and 28

Local Government Amendment (Auditing) Bill 2017

s. 5

page 3

(b) in relation to a performance audit — the 1

Auditor General; 2

3

(2) In section 1.4 delete the definition of auditor and insert: 4

5

auditor means the Auditor General; 6

7

5. Section 3.64 amended 8

In section 3.64(e) delete “chairman” (each occurrence) and 9

insert: 10

11

chairperson 12

13

6. Section 3.70A inserted 14

After section 3.70 insert: 15

16

3.70A. Audit requirements for regional subsidiaries 17

(1) Section 7.1 and the provisions of Part 7 Divisions 3A 18

to 4 apply in relation to a regional subsidiary as if the 19

regional subsidiary were a local government. 20

(2) The application of a provision under subsection (1) is 21

subject to any prescribed or necessary modifications to 22

the provision provided for in the regulations. 23

24

Local Government Amendment (Auditing) Bill 2017

s. 7

page 4

7. Section 5.53 amended 1

(1) Delete section 5.53(2)(h) and insert: 2

3

(h) the auditor’s report prepared under 4

section 7.9(1) or 7.12AD(1) for the financial 5

year; and 6

7

(2) Delete section 5.53(2)(h) and insert: 8

9

(h) the auditor’s report prepared under 10

section 7.12AD(1) for the financial year; and 11

12

8. Section 5.55A inserted 13

After section 5.55 insert: 14

15

5.55A. Publication of annual reports 16

The CEO is to publish the annual report on the local 17

government’s official website within 14 days after the 18

report has been accepted by the local government. 19

20

9. Section 5.94 amended 21

After section 5.94(t) insert: 22

23

(ta) a report on a supplementary audit prepared 24

under section 7.12AH(1); 25

26

Local Government Amendment (Auditing) Bill 2017

s. 10

page 5

10. Section 7.1 amended 1

(1) In section 7.1 delete “Part —” and insert: 2

3

Part, unless the contrary intention appears — 4

5

(2) In section 7.1 insert in alphabetical order: 6

7

audit has the meaning given in the Auditor General Act 8

section 4(1); 9

audit contract means an agreement in writing that — 10

(a) was made under section 7.8(1); and 11

(b) was in force immediately before 12

commencement day; 13

Auditor General Act means the Auditor General 14

Act 2006; 15

audit report means a report prepared by an auditor on a 16

local government audit; 17

commencement day means the day on which the Local 18

Government Amendment (Auditing) Act 2017 19

section 10 comes into operation; 20

financial audit means an audit conducted under 21

section 7.12AB; 22

local government audit means — 23

(a) an audit conducted under this Part; or 24

(b) a performance audit; 25

performance audit means an examination or 26

investigation carried out under the Auditor General Act 27

section 18 (as applied by section 7.12AJ(1) of this 28

Act); 29

supplementary audit means an audit conducted under 30

section 7.12AG. 31

32

Local Government Amendment (Auditing) Bill 2017

s. 11

page 6

(3) In section 7.1 in the definition of regulations delete “Part.” and 1

insert: 2

3

Part; 4

5

11. Section 7.1A amended 6

In section 7.1A(3) delete “him or her” and insert: 7

8

the CEO 9

10

12. Section 7.1D inserted 11

At the beginning of Part 7 Division 2 insert: 12

13

7.1D. Application 14

This Division applies in relation to a local government 15

that has an audit contract that is in force. 16

17

13. Section 7.3 amended 18

(1) In section 7.3(1) delete “A local” and insert: 19

20

Subject to subsection (1A), a local 21

22

(2) After section 7.3(1) insert: 23

24

(1A) A local government cannot appoint a person to be its 25

auditor after commencement day. 26

27

Local Government Amendment (Auditing) Bill 2017

s. 14

page 7

14. Section 7.7 amended 1

(1) In section 7.7 delete “If ” and insert: 2

3

(1) Subject to subsection (2), if 4

5

(2) At the end of section 7.7 insert: 6

7

(2) The Departmental CEO cannot appoint a person to be 8

the auditor of a local government after commencement 9

day. 10

11

15. Section 7.8A inserted 12

At the beginning of Part 7 Division 3 insert: 13

14

7.8A. Application 15

This Division applies in relation to a local government 16

that has an audit contract that is in force. 17

18

16. Section 7.9 amended 19

In section 7.9(4) delete “government to be dealt with under 20

section 7.12A.” and insert: 21

22

government. 23

24

17. Section 7.11 amended 25

In section 7.11 delete “inspection or inquiry,”. 26

Local Government Amendment (Auditing) Bill 2017

s. 18

page 8

18. Part 7 Divisions 3A to 3D inserted 1

After Part 7 Division 3 insert: 2

3

Division 3A — Financial audit 4

7.12AA. Application 5

This Division applies in relation to a local government 6

that does not have an audit contract that is in force. 7

7.12AB. Conducting a financial audit 8

The auditor must audit the accounts and annual 9

financial report of a local government at least once in 10

respect of each financial year. 11

7.12AC. Dispensing with a financial audit 12

(1) Despite section 7.12AB, the auditor may dispense with 13

all or any part of a financial audit if the auditor 14

considers that the dispensation is appropriate in the 15

circumstances. 16

(2) The auditor must consult the Minister before exercising 17

the power conferred by subsection (1). 18

(3) If the auditor exercises the power conferred by 19

subsection (1), the auditor must notify — 20

(a) the Public Accounts Committee as defined in 21

the Auditor General Act section 4(1); and 22

(b) the Estimates and Financial Operations 23

Committee as defined in the Auditor General 24

Act section 4(1). 25

7.12AD. Reporting on a financial audit 26

(1) The auditor must prepare and sign a report on a 27

financial audit. 28

Local Government Amendment (Auditing) Bill 2017

s. 18

page 9

(2) The auditor must give the report to — 1

(a) the mayor, president or chairperson of the local 2

government; and 3

(b) the CEO of the local government; and 4

(c) the Minister. 5

7.12AE. Fees for a financial audit 6

(1) The auditor must determine whether a fee is to be 7

charged for a financial audit of a local government and 8

if so, the amount of that fee. 9

(2) A fee determined under subsection (1) must be paid by 10

the local government. 11

Division 3B — Supplementary audit 12

7.12AF. Application 13

This Division applies in relation to a local government 14

that does not have an audit contract that is in force. 15

7.12AG. Conducting a supplementary audit 16

The auditor may audit any particular aspect of the 17

accounts of a local government that the Minister 18

requests the auditor to audit. 19

7.12AH. Reporting on a supplementary audit 20

(1) The auditor must prepare and sign a report on a 21

supplementary audit. 22

(2) The auditor must give the report to the Minister. 23

(3) The Minister — 24

(a) may give a copy of the report to the mayor, 25

president or chairperson of the local 26

government, and to the CEO of the local 27

government; and 28

Local Government Amendment (Auditing) Bill 2017

s. 18

page 10

(b) may request the CEO of the local government 1

to publish the report on the local government’s 2

official website. 3

(4) The CEO must publish a copy of the report on the local 4

government’s official website within 14 days after 5

receiving a request under subsection (3)(b). 6

7.12AI. Fees for a supplementary audit 7

(1) The auditor must determine whether a fee is to be 8

charged for a supplementary audit of a local 9

government and if so, the amount of that fee. 10

(2) A fee determined under subsection (1) must be paid by 11

the local government. 12

Division 3C — Performance audit 13

7.12AJ. Conducting a performance audit 14

(1) The Auditor General Act section 18 applies in relation 15

to a local government as if — 16

(a) the local government were an agency; and 17

(b) money collected, received or held by any 18

person for or on behalf of the local government 19

were public money; and 20

(c) money collected, received or held by the local 21

government for or on behalf of a person other 22

than the local government were other money; 23

and 24

(d) property held for or on behalf of the local 25

government, other than money referred to in 26

paragraph (b), were public property; and 27

(e) property held by the local government for or on 28

behalf of a person other than the local 29

government were other property; and 30

Local Government Amendment (Auditing) Bill 2017

s. 19

page 11

(f) the reference in the Auditor General Act 1

section 18(2)(d) to “legislative provisions, 2

public sector policies or its own internal 3

policies;” were a reference to “legislative 4

provisions or its own internal policies;”. 5

(2) A performance audit is taken for the purposes of the 6

Auditor General Act to have been carried out under the 7

Auditor General Act Part 3 Division 1. 8

7.12AK. Reporting on a performance audit 9

(1) The Auditor General Act section 25 applies in relation 10

to a performance audit as if — 11

(a) a local government were an agency; and 12

(b) the council of the local government were its 13

accountable authority. 14

(2) The auditor must give a report on a performance audit 15

to the local government. 16

Division 3D — Other audits 17

7.12AL. Audits of accounts of related entities and certain 18

subsidiary bodies 19

The Auditor General Act sections 16 and 17 apply in 20

relation to a local government as if — 21

(a) the local government were an agency; and 22

(b) the council of the local government were its 23

accountable authority. 24

25

19. Section 7.12A amended 26

(1) In section 7.12A(1)(a) delete “his or her” and insert: 27

28

the auditor’s 29

30

Local Government Amendment (Auditing) Bill 2017

s. 19

page 12

(2) In section 7.12A(3): 1

(a) delete “is to examine the report of the auditor prepared 2

under section 7.9(1), and any report prepared under 3

section 7.9(3) forwarded to it, and is to —” and insert: 4

5

must — 6

7

(b) before paragraph (a) insert: 8

9

(aa) examine an audit report received by the local 10

government; and 11

12

(c) in paragraph (a) delete “report, or reports,” and insert: 13

14

audit report, 15

16

(3) Delete section 7.12A(4) and insert: 17

18

(4) A local government must — 19

(a) prepare a report addressing any matters 20

identified as significant by the auditor in the 21

audit report, and stating what action the local 22

government has taken or intends to take with 23

respect to each of those matters; and 24

(b) give a copy of that report to the Minister within 25

3 months after the audit report is received by 26

the local government. 27

(5) Within 14 days after a local government gives a report 28

to the Minister under subsection (4)(b), the CEO must 29

publish a copy of the report on the local government’s 30

official website. 31

32

Local Government Amendment (Auditing) Bill 2017

s. 20

page 13

20. Section 7.13 amended 1

In section 7.13(1): 2

(a) delete “provision —” and insert: 3

4

provision as follows — 5

6

(b) delete paragraphs (aa), (ab), (ac) and (ad) and insert: 7

8

(aa) as to the functions of a CEO in relation to — 9

(i) a local government audit; and 10

(ii) a report (an action report) prepared 11

by a local government under 12

section 7.12A(4)(a); and 13

(iii) an audit report; and 14

(iv) a report on an audit conducted by a local 15

government under this Act or any other 16

written law; 17

(ab) as to the functions of an audit committee, 18

including in relation to — 19

(i) the selection and recommendation of an 20

auditor under Division 2; and 21

(ii) a local government audit; and 22

(iii) an action report; and 23

(iv) an audit report; and 24

(v) a report on an audit conducted by a local 25

government under this Act or any other 26

written law; 27

(ac) as to the procedure to be followed in selecting 28

an auditor under Division 2; 29

30

Local Government Amendment (Auditing) Bill 2017

s. 20

page 14

(c) in paragraph (ae) delete “a report by an auditor;” and 1

insert: 2

3

an audit report; 4

5

(d) in paragraph (a) delete “agreements between local 6

governments and auditors;” and insert: 7

8

an agreement in writing (agreement) made under 9

section 7.8(1); 10

11

(e) delete paragraph (b) and insert: 12

13

(b) for notifications and reports to be given in 14

relation to an agreement, including any 15

variations to, or termination of an agreement; 16

17

(f) in paragraph (ba) delete “the copies of agreements 18

between local governments and auditors” and insert: 19

20

a copy of an agreement 21

22

(g) in paragraph (c) delete “auditor;” and insert: 23

24

auditor under section 7.5; 25

26

(h) in paragraph (d) delete “for —” and insert: 27

28

for the following — 29

30

Local Government Amendment (Auditing) Bill 2017

s. 21

page 15

(i) in paragraph (f) delete “by auditors in their reports;” and 1

insert: 2

3

in an audit report; 4

5

(j) delete paragraphs (g) and (h) and insert: 6

7

(g) requiring an auditor (other than the Auditor 8

General) to provide the Minister with 9

prescribed information as to an audit conducted 10

by the auditor; 11

(h) prescribing the circumstances in which an 12

auditor (other than the Auditor General) is to be 13

considered to have a conflict of interest and 14

requiring an auditor (other than the Auditor 15

General) to disclose in an audit report such 16

information as to a possible conflict of interest 17

as is prescribed; 18

19

21. Schedule 9.3 amended 20

(1) Delete Schedule 9.3 clause 32. 21

(2) At the end of Schedule 9.3 insert: 22

23

Division 4 — Provisions for the Local Government 24

Amendment (Auditing) Act 2017 25

49. Terms used 26

In this Division — 27

audit contract has the meaning given in section 7.1; 28

commencement day has the meaning given in section 7.1. 29

Local Government Amendment (Auditing) Bill 2017

s. 21

page 16

50. Minister to publish status of audit contracts1

During the period beginning on commencement day and2

ending on the day fixed by proclamation under the Local3

Government Amendment (Auditing) Act 2017 section 22(2),4

the Minister must publish on a website maintained by the5

Department a list of —6

(a) local governments that have an audit contract that is7

in force; and8

(b) local governments that do not have an audit contract9

that is in force.10

51. Audit contracts may be terminated after completion of11

FY17/18 audit12

(1) In this clause —13

FY17/18 audit, in relation to a local government, means an14

audit of the local government conducted under15

section 7.9(1) in respect of the financial year ending on16

30 June 2018.17

(2) This clause applies in relation to a local government after18

the completion of the FY17/18 audit for the local19

government.20

(3) The Departmental CEO may give notice (a notice) to a local21

government specifying the date (the termination date) on22

which the audit contract for the local government is to23

terminate.24

(4) An audit contract in relation to which a notice is given is25

terminated by force of this provision on the termination26

date.27

(5) The Departmental CEO may give a notice on the28

Departmental CEO’s own initiative.29

(6) The Minister may —30

(a) request the Departmental CEO to give a notice to a31

local government; and32

(b) nominate the termination date to be specified in the33

notice.34

Local Government Amendment (Auditing) Bill 2017

s. 21

page 17

(7) On request by the Minister, the Departmental CEO must1

give a notice to the local government specifying the2

termination date nominated by the Minister.3

(8) A notice given or request made under this clause must be in4

writing.5

52. Audit contracts are terminated after completion of6

FY19/20 audit7

(1) In this clause —8

FY19/20 audit, in relation to a local government, means an9

audit of the local government conducted under10

section 7.9(1) in respect of the financial year ending on11

30 June 2020.12

(2) An audit contract for a local government, unless earlier13

lawfully terminated, is terminated by force of this provision14

on completion of the FY19/20 audit for the local15

government.16

53. No breach of contract17

Anything that occurs by operation of this Division is not to18

be regarded as a breach of contract.19

54. Transitional regulations20

(1) In this clause —21

specified means specified or described in the regulations;22

transitional matter —23

(a) means a matter or issue of a transitional nature that24

arises as a result of the enactment of the Local25

Government Amendment (Auditing) Act 2017; and26

(b) includes a saving or application matter.27

(2) If there is not sufficient provision in this Division for28

dealing with a transitional matter, regulations under this Act29

may prescribe all matters that are required or necessary or30

convenient to be prescribed for dealing with the matter.31

Local Government Amendment (Auditing) Bill 2017

s. 22

page 18

(3) Regulations made under subclause (2) may provide that1

specified provisions of a written law —2

(a) do not apply to or in relation to any matter; or3

(b) apply with specified modifications to or in relation4

to any matter.5

(4) If regulations made under subclause (2) provide that a6

specified state of affairs is taken to have existed, or not to7

have existed, on and from a day that is earlier than the day8

on which the regulations are published in the Gazette but not9

earlier than the day this clause comes into operation, the10

regulations have effect according to their terms.11

(5) If regulations made under subclause (2) contain a provision12

referred to in subclause (4), the provision does not operate13

so as —14

(a) to affect in a manner prejudicial to any person15

(other than the State or an authority of the State) the16

rights of that person existing before the day of17

publication of those regulations; or18

(b) to impose liabilities on any person (other than the19

State or an authority of the State) in respect of20

anything done or omitted to be done before the day21

of publication of those regulations.22

(6) Regulations made under subclause (2) in relation to a matter23

referred to in subclause (3) must be made within whatever24

period is reasonably and practicably necessary to deal with a25

transitional matter.26

22. Superseded provisions to be deleted27

(1) In this section —28

superseded provisions means the following provisions of the29

Local Government Act 1995 —30

(a) section 5.43(c);31

(b) in section 7.1, the definitions of approved auditor,32

disqualified person, qualified person and registered33

company auditor;34

Local Government Amendment (Auditing) Bill 2017

s. 22

page 19

(c) Part 7 Division 2;1

(d) Part 7 Division 3;2

(e) section 7.12AA;3

(f) section 7.12AF;4

(g) section 7.13(1)(ab)(i), (ac), (a)-(e), (g) and (h).5

(2) The superseded provisions are deleted on a day fixed by6

proclamation.7

(3) A proclamation cannot be made under subsection (2) unless the8

Minister is satisfied that there is no reason for the superseded9

provisions to remain in operation.10

(4) This section is deleted immediately after the superseded11

provisions are deleted.12

Note for Part 7:13

The description at the beginning of Part 7 is to be altered by: 14

(a) deleting “the financial accounts of ” ;15

(b) deleting paragraph (a) and inserting:16

(a) the establishment of audit committees; and17

18

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 13

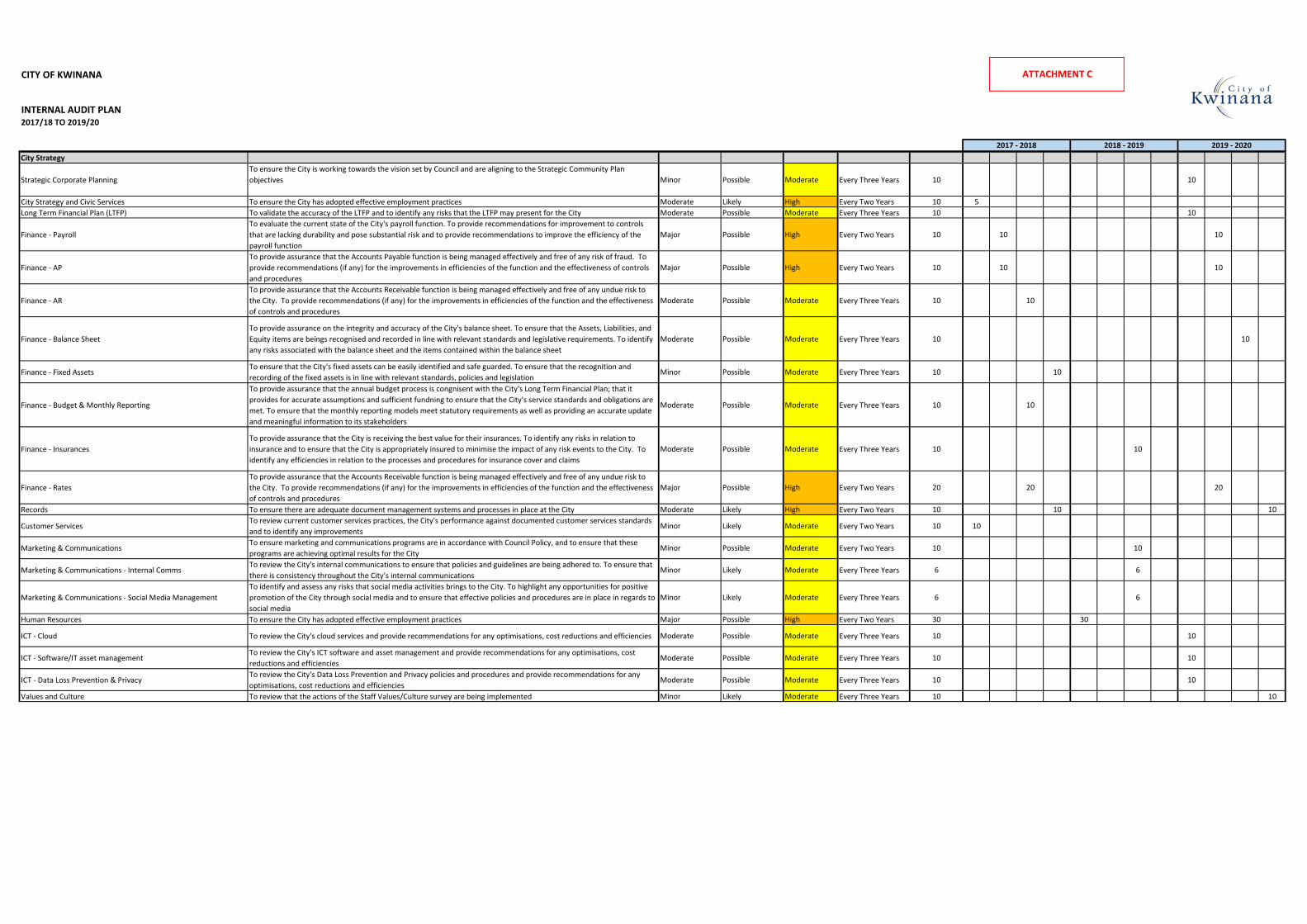

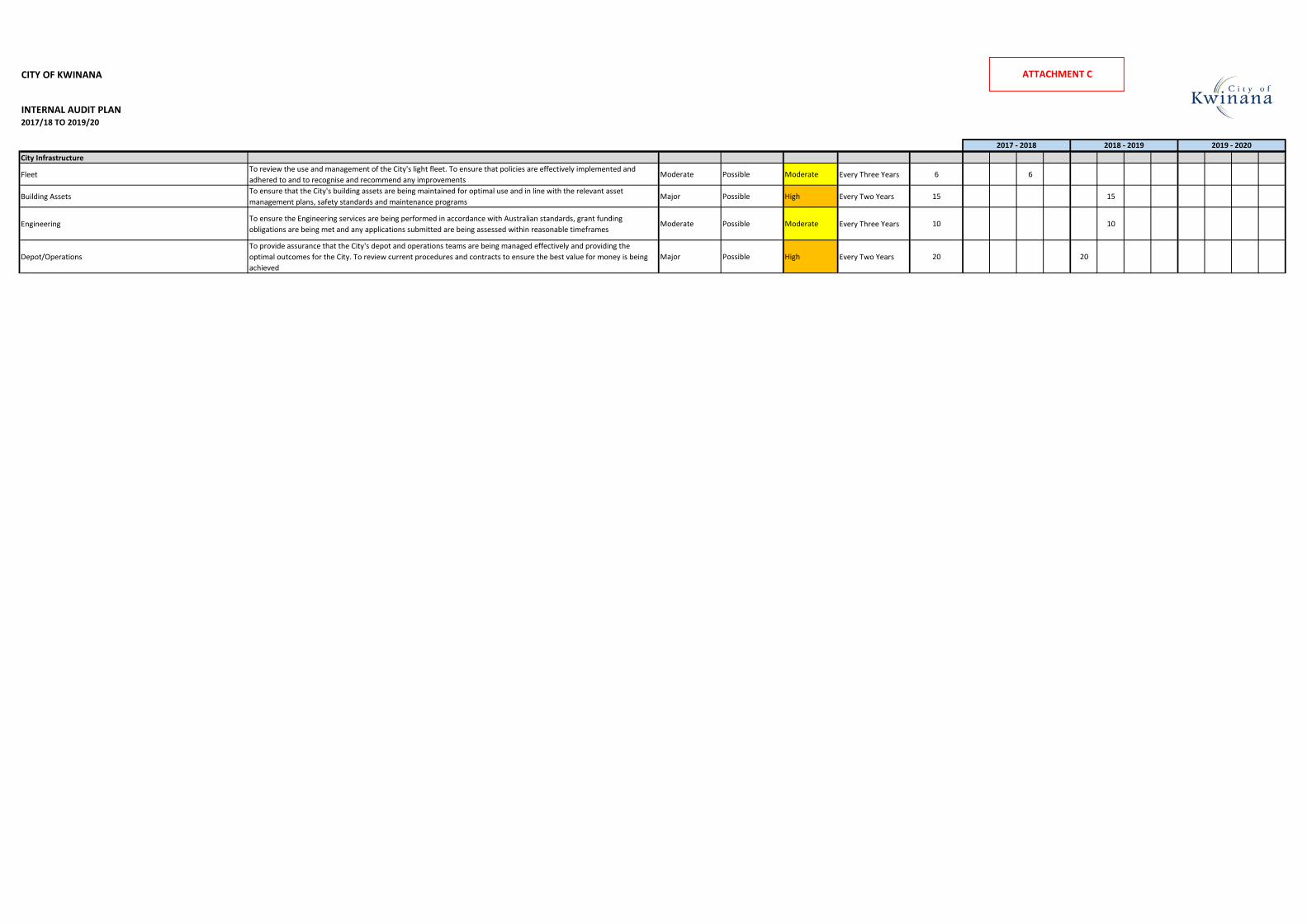

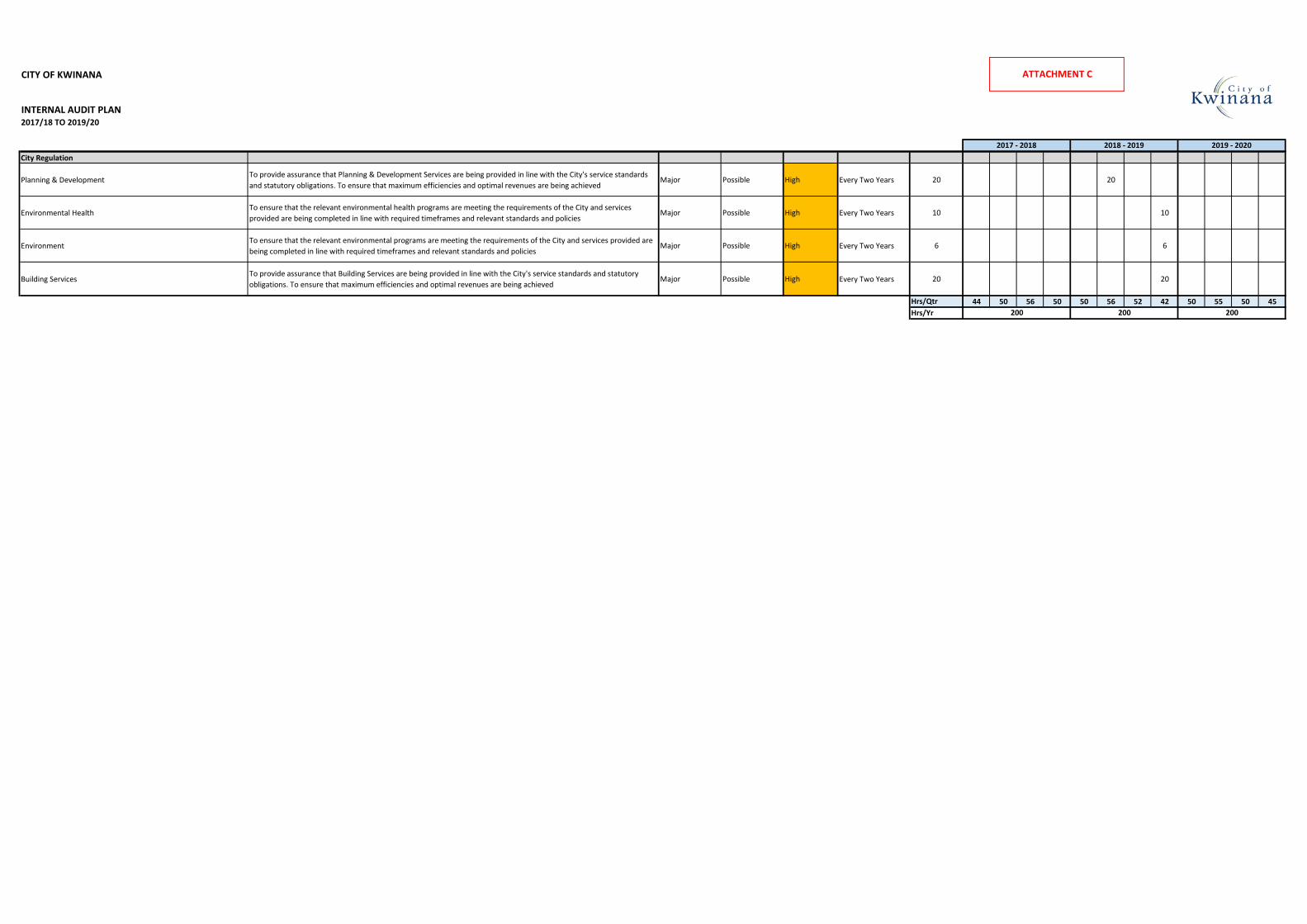

6.3 Internal Audit Plan Review for the period 18 September to 27 November 2017 and Internal Audit Plan for the period 28 November 2017 to 19 March 2018

SUMMARY:

At its meeting held on 18 September 2017, the Audit Committee resolved to amend the Internal Audit Plan and endorsed that the first internal audit quarter, a total of 44 hours, would be spent on reviewing internal processes in the following auditable units:

1. Program and Project Management2. Segregation of Duties/Identity and Access Management3. Governance & Civic Services4. Customer Services5. Identify a number of projects where the Audit Committee will select two, for a

post implementation project review.

The findings and recommendations of the Internal Audit Plan Review for the period 18 September to 27 November 2017 are detailed in Attachment A.

The Audit Committee are recommended to endorse the Internal Audit Plan for the period 28 November 2017 to 19 March 2018 as detailed in Attachment B.

OFFICER RECOMMENDATION:

That the Audit Committee;

1. Select two projects from the following projects provided by the ChiefExecutive Officer for a post implementation review as required by Part Bof the Audit Committee resolution of 18 September 2017:

a. Kwinana Outdoor Youth Space (Community Engagement/CityInfrastructure)

b. Chisham Avenue Crosswalk (City Infrastructure)c. WIFI implementation (City Strategy)d. Streetscape Policy (City Regulation)e. Attain Software (City Legal)

2. Receive the Officers internal audit findings for the period 18 September to27 November 2017, as detailed in Attachment A, and establish actions forthe following units:

1. Program and Project Management2. Segregation of Duties/Identity and Access Management3. Governance and Civic Services4. Customer Services

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 14

6.3 INTERNAL AUDIT PLAN REVIEW FOR THE PERIOD 18 SEPTEMBER TO 27 NOVEMBER 2017 AND INTERNAL AUDIT PLAN FOR THE PERIOD 28 NOVEMBER 2017 TO 19 MARCH 2018

3. Endorse the Internal Audit Plan, at Attachment B, to be undertaken withinthe period 28 November 2017 to 19 March 2018 for the following auditableunits:

1. Finance – Payroll2. Finance – Accounts Payable3. Contracts and Strategic Procurement; and4. Post Implementation Review for ________________ project and

____________ project with the following:a) Objective:b) Key question/areas of review:

i)ii)iii)iv)

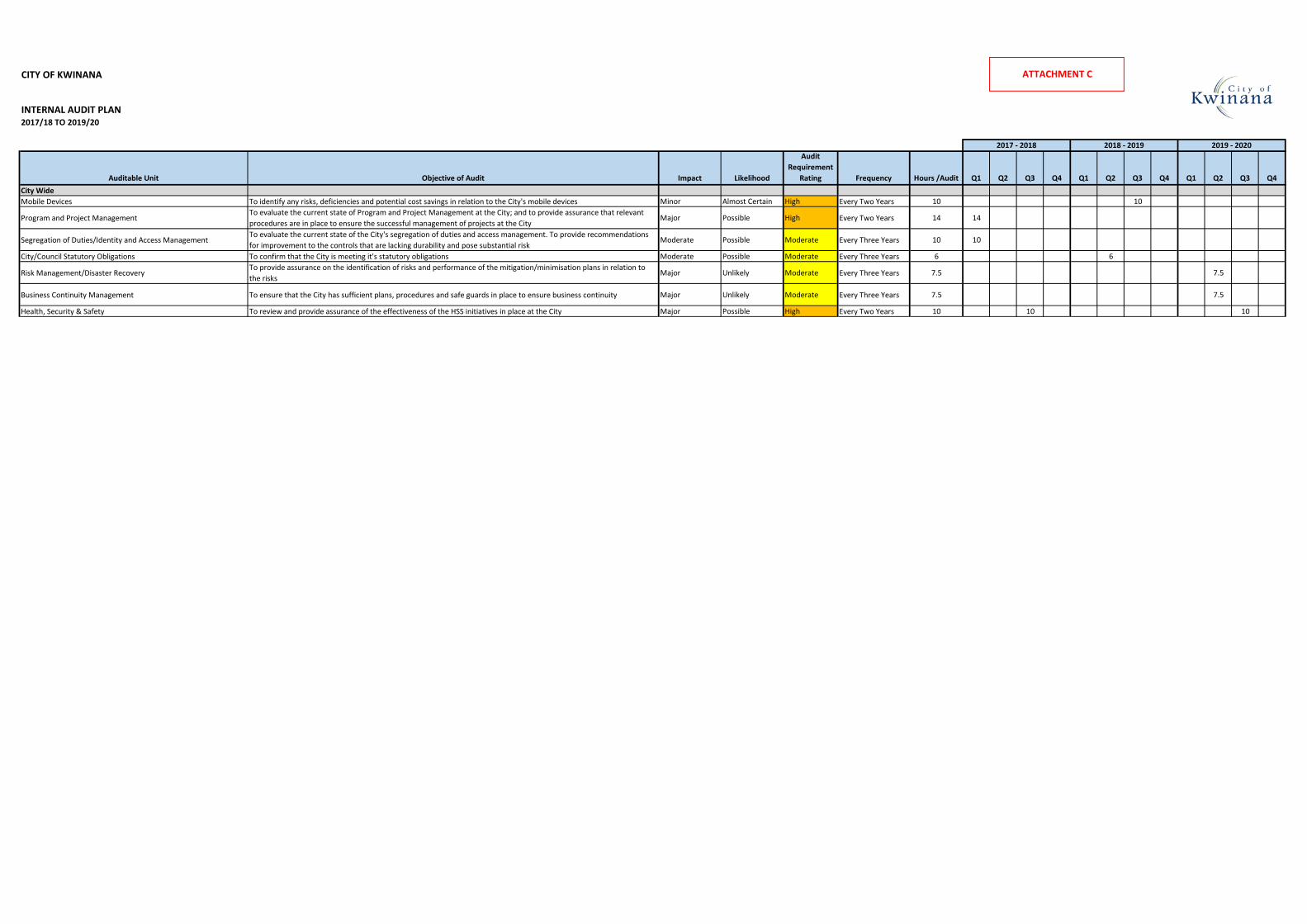

4. Endorse the amended Internal Audit Plan for 2017/18 to 2019/20 to reflectthe changes to the organisational structure as detailed in Attachment C.

DISCUSSION:

Due to an increased focus on the accountability of local governments a review of the effectiveness of all business processes is becoming best practice. Internal audit is one way to reduce risk and identify improvements in internal controls. There are many benefits to implementing this value add approach such as:

• Improves the performance of the organisation.• Makes the organisation process-dependent instead of person-dependent.• Identifies redundancies in operational and control procedures and provides

recommendations to improve the efficiency and effectiveness of procedures.• Serves as an early warning system, enabling deficiencies to be identified and

remediated on a timely basis (i.e. prior to external, regulatory or complianceaudits).

• Ultimately increases accountability within the organisation.• It can support strategic objectives; for example cost reduction initiatives.

The findings for the period 18 September to 27 November 2017 are detailed in Attachment A. City Officers have recommended actions that the Audit Committee may want to consider for each of the findings.

Attachment B includes key questions and areas of review that could be the scope for the internal audit for the period 28 November 2017 to 19 March 2018, of the following auditable units:

1. Finance - Payroll

Objective of Audit: To evaluate the current state of the City's payroll function. To provide recommendations for improvement to controls that are lacking durability and pose substantial risk and to provide recommendations to improve the efficiency of the payroll function.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 15

6.3 INTERNAL AUDIT PLAN REVIEW FOR THE PERIOD 18 SEPTEMBER TO 27 NOVEMBER 2017 AND INTERNAL AUDIT PLAN FOR THE PERIOD 28 NOVEMBER 2017 TO 19 MARCH 2018

Key Questions/Areas of Review: a) Check payment report/s to ensure no additional employees have been

included in the pay runb) Check employees payments are recorded in the payroll system correctlyc) Ensure PAYG withholding and gross wages reconcilesd) Review the integrity and security of the creation of the pay data file to the

online payment systeme) Review the security of personnel data (including salary information) in the

organisationf) Review the accuracy of the termination of employeesg) Review the efficiency of current payroll practices and identify improvementsh) Review whether casual employees still meet the criteria of casual (or move

to permanent position)i) Ensure all third party payments for salary sacrificing are currently recorded

for FBT liability where applicablej) Ensure no terminated employees are on the current payrollk) Review all previous audit findings have been completed

2. Finance – Accounts Payable

Objective of Audit: To provide assurance that the Accounts Payable function is being managed effectively and free of any risk of fraud. To provide recommendations (if any) for the improvements in efficiencies of the function and the effectiveness of controls and procedures.

Key Questions/Areas of Review: a) Ensure authorisation procedure is being followed. Analyse whether WALGA

preferred suppliers are valid and currentb) Ensure all goods and services paid have been receivedc) Ensure no cash cheques have been paid - except for petty cashd) Test data to ensure expense classifications are correcte) Review petty cash processf) Review expenditure on Corporate Credit Cards; are officers adhering to the

Use of Corporate Credit Card Policyg) Review the timing of reports to Council are in accordance with the City's

statutory requirementsh) Ensure requisitions and purchase orders are made before work is contractedi) Ensure the evidence of quotes are attachedj) Ensure contract/tender rates agree to invoiced ratesk) Review data integrityl) Review the efficiency of current AP practices and identify improvementsm) Review all previous audit findings have been completed

3. Contracts and Strategic Procurement

Objective of Audit: To ensure that the management of the City's external suppliers, contractors, IT vendors or consultants is providing best value to the City and reducing any risks to the City in the area of contractor management

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 16

6.3 INTERNAL AUDIT PLAN REVIEW FOR THE PERIOD 18 SEPTEMBER TO 27 NOVEMBER 2017 AND INTERNAL AUDIT PLAN FOR THE PERIOD 28 NOVEMBER 2017 TO 19 MARCH 2018

Key Questions/Areas of Review for five (one each directorate) selected contracts: a) Ensure that the required insurances have been received and are in

accordance with the conditions of the respective agreementb) Verify that the contract conditions are being adhered to (including pre

commencement, during and upon completion, qualifications andaccreditations)

c) Sight evidence of signed contract documentationd) Confirm that only authorised officers to sign purchase orders are entered into

the systeme) Confirm that purchasing limits are in line with the authorised officers

purchasing authorityf) Confirm that tenders are in accordance with statutory obligationsg) Selection panel are assessing tenderers objectively and in accordance with

weightings and criteria set out in the tender packageh) Review any conflict of interesti) Review the tender register to ensure compliancej) Review contract register to ensure all contracts are up to datek) Review all previous audit findings have been completed

4. Post Project Implementation Review

Objective of Audit: Audit Committee to determine objective of audit.

Key Questions/Areas of Review: At the August 2017 Audit Committee Meeting, the Audit Committee endorsed the addition of the post project implementation review as an auditable unit. It is recommended that the Audit Committee outline the objective and key questions/areas of review required to carry out the internal audit.

It is recommended that the Audit Committee endorse the Internal Audit Plan 2017/18 to 2019/20 as a result of the organisational structure changes as the Contracts and Strategic Procurement, Governance, Leases/Property Management and Essential Services auditable units have been moved to the City Legal Directorate and this is detailed in Attachment C.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 17

6.3 INTERNAL AUDIT PLAN REVIEW FOR THE PERIOD 18 SEPTEMBER TO 27 NOVEMBER 2017 AND INTERNAL AUDIT PLAN FOR THE PERIOD 28 NOVEMBER 2017 TO 19 MARCH 2018

LEGAL/POLICY IMPLICATIONS:

Section 7.13 of the Local Government Act 1995 states

(1) Regulations may make provision -(aa) as to the functions of the CEO and the audit committee in relation to

audits carried out under this Part and reports made on those audits;(ab) as to the functions of audit committees, including the selection and

recommendation of an auditor;(ac) as to the procedure to be followed in selecting an auditor;(ad) as to the contents of the annual report to be prepared by an audit

committee;(ae) as to monitoring action taken in respect of any matters raised in a report

by an auditor; (a) with respect to matters to be included in agreements between local

governments and auditors;(b) for notifications and reports to be given in relation to agreements between

local governments and auditors, including any variations to, or terminationof such agreements;

(ba) as to the copies of agreements between local governments and auditors being provided to the Department;

(c) as to the manner in which an application may be made to the Minister forapproval as an auditor;

(d) in relation to approved auditors, for —(i) reviews of, and reports on, the quality of audits conducted;(ii) the withdrawal by the Minister of approval as an auditor;(iii) applications to the State Administrative Tribunal for the review of

decisions to withdraw approval;(e) for the exercise or performance by auditors of their powers and duties

under this Part;(f) as to the matters to be addressed by auditors in their reports;(g) requiring auditors to provide the Minister with such information as to

audits carried out by them under this Part as is prescribed;(h) prescribing the circumstances in which an auditor is to be considered to

have a conflict of interest and requiring auditors to disclose in their reportssuch information as to a possible conflict of interest as is prescribed;

(i) requiring local governments to carry out, in the prescribed manner and ina form approved by the Minister, an audit of compliance with suchstatutory requirements as are prescribed whether those requirements are—(i) of a financial nature or not; or(ii) under this Act or another written law.

(2) Regulations may also make any provision about audit committees that may bemade under section 5.25 in relation to committees.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 18

6.3 INTERNAL AUDIT PLAN REVIEW FOR THE PERIOD 18 SEPTEMBER TO 27 NOVEMBER 2017 AND INTERNAL AUDIT PLAN FOR THE PERIOD 28 NOVEMBER 2017 TO 19 MARCH 2018

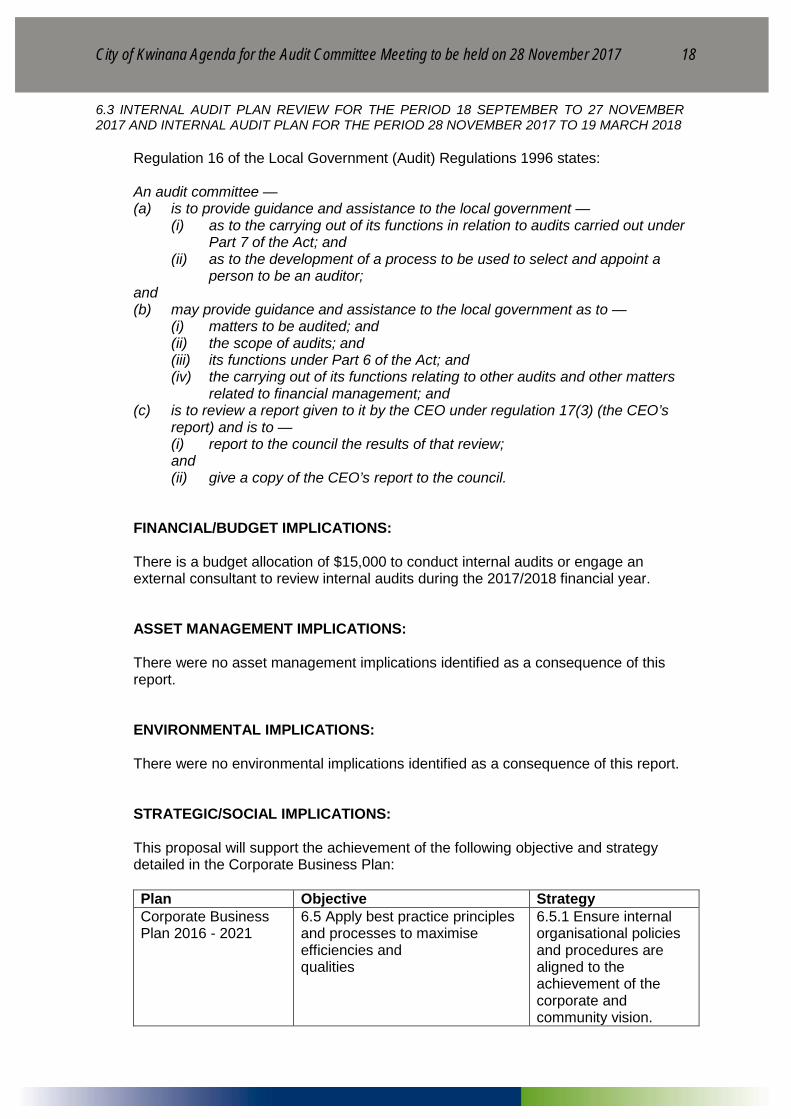

Regulation 16 of the Local Government (Audit) Regulations 1996 states:

An audit committee — (a) is to provide guidance and assistance to the local government —

(i) as to the carrying out of its functions in relation to audits carried out underPart 7 of the Act; and

(ii) as to the development of a process to be used to select and appoint aperson to be an auditor;

and (b) may provide guidance and assistance to the local government as to —

(i) matters to be audited; and(ii) the scope of audits; and(iii) its functions under Part 6 of the Act; and(iv) the carrying out of its functions relating to other audits and other matters

related to financial management; and(c) is to review a report given to it by the CEO under regulation 17(3) (the CEO’s

report) and is to —(i) report to the council the results of that review;and(ii) give a copy of the CEO’s report to the council.

FINANCIAL/BUDGET IMPLICATIONS:

There is a budget allocation of $15,000 to conduct internal audits or engage an external consultant to review internal audits during the 2017/2018 financial year.

ASSET MANAGEMENT IMPLICATIONS:

There were no asset management implications identified as a consequence of this report.

ENVIRONMENTAL IMPLICATIONS:

There were no environmental implications identified as a consequence of this report.

STRATEGIC/SOCIAL IMPLICATIONS:

This proposal will support the achievement of the following objective and strategy detailed in the Corporate Business Plan:

Plan Objective Strategy Corporate Business Plan 2016 - 2021

6.5 Apply best practice principles and processes to maximise efficiencies and qualities

6.5.1 Ensure internal organisational policies and procedures are aligned to the achievement of the corporate and community vision.

City of Kwinana Agenda for the Audit Committee Meeting to be held on 28 November 2017 19

6.3 INTERNAL AUDIT PLAN REVIEW FOR THE PERIOD 18 SEPTEMBER TO 27 NOVEMBER 2017 AND INTERNAL AUDIT PLAN FOR THE PERIOD 28 NOVEMBER 2017 TO 19 MARCH 2018

COMMUNITY ENGAGEMENT:

There are no community engagement requirements identified as a result of this report.

RISK IMPLICATIONS:

The risk implications in relation to this proposal are as follows:

Risk Event Internal controls are inadequate causing errors and affecting services to customers

Risk Theme All themes

Risk Effect/Impact All Risk Assessment Context

Strategic/Operational

Consequence Moderate Likelihood Possible Rating (before treatment)

Moderate

Risk Treatment in place Reduce – mitigate risk Response to risk treatment required/in place

Implement an internal audit plan and carry out internal audits

Rating (after treatment) Low

CITY OF KWINANA

INTERNAL AUDIT PLANFOR THE PERIOD 18 SEPTEMBER TO 27 NOVEMBER 2017

Auditable Unit

Audit Requirement

Rating (From Plan)

Frequency Objective of Audit Key Questions/Areas of Review (Scope) Findings RecommendationsAction

Ref:Action

DescriptionResponsible

OfficerDue Date

Action Status

a. Assess the design of processes and controls in place to manage projects against leading practices to ensure projects are delivered on time, on budget and with adequate resources, and that benefits can be measured and align to the Strategic Community Plan.

Project viewed: Medina Netball Courts

• Was Prince2 used? If not, what form of system was used?There were components of Prince 2 documents that were not completed, such as Daily Log, End stage reports. There were two Project Initiation Documents created (D16/24991 and D16/24717). The business case was not updated/managed throughout the lifecycle of the project.

Prince2 documentation is available to staff.

Project documentation for individual projects from an internal audit perspective was difficult to locate within CM9 (the City's record keeping system). The titling and storage of relevant project documents are inconsistent with no naming conventions established and inconsistent.

Ensure that the Prince2 processes are followed. This includes utilising the process mapping available to staff on the intranet. The City has tailored the processes to suit a general project and the information is readily available on the City's Intranet at:thehub.kwinana.wa.gov.au/intranet/publish/Corporate/Transformation/Transformation.php

Roles and responsibilities need to be understood and adequate meetings arranged at stage level to ensure that projects are on track for all criteria. Further extensive documentation for roles and responsibilities is available in CM9 under Saved Searches - Transformation.

No grant applications are submitted until the scope has been costed.

Full project documentation needs to be completed and made available, in particular a lessons learnt register.

A better system of recording Projects into CM9 be developed to allow projects to be found and analysed. Projects should be given a specific Name and CM9 Location at Project Start Up to allow documentation to be located. All project documentation should be able to be located through this one CM9 Folder. Created by the Stream SRO.

b. Is the project methodology being followed? • Were work packages and team and stage plans developed and utilised?There were no work packages issued or team and stage plans developed.'The scope in the initial PID was modified during the project and information was not updated in any project documentation.

New employees and those that may move into relevant project management roles should be trained in project management systems adopted by the City. This includes detailing the processes involved in undertaking a project and the documents required to be completed.

Relevant employees need to be given specific roles and responsibilities in line with Prince2 requirements and those officers must understand what is required of them for the project.

Required processes and documentation need to be completed and audited by the Project Manager for the life of the project and reporting undertaken as required by Prince2 methodology. Assign the Integrated Planning and Special Projects Officer with reviewing one project per quarter to confirm that the project has completed the documentation required.

c. What is done when projects are underperforming (scope, budget, time)? The project scope was developed without detailed costs and specification being developed. Therefore the scope that was agreed to could not be delivered within the budget provided. The budget was required to be increased to complete all components of the project. The project manager did not complete the initial project initiation document, it was handed to the project manager after the scope and budget was established.• Was the project underperforming for scope creep, budget or time at any point? How was this monitored?While there was an element of scope creep involved due to unforeseen issues on a historical site, the project was insufficiently funded from the beginning. This was a result of reducing the contingency to less than 5% in order to bring the total cost below $200k in order to make the project eligible for CSRFF funding. The project exceeded budget and required Council to approve further funds to deliver the project in 2017/2018 budget.

The project manager completes the project initiation document which details the scope, time and budget. Therefore the project commences at the planning stage and not at construction stage.

d. How is project risk assessed and managed? • Were risk assessments completed at any stage during the project? When were these done?No risk register was created.

Risk assessments be performed in accordance with the City's Risk Management Policy and Prince2 methodology.