audit planning in bank branch audit - wirc-icai.org · pdf fileaudit planning in bank branch...

TRANSCRIPT

Audit Planning in Bank Branch Audit by Ketan Saiya F.C.A.

There i s a sea change business dynamics of banking in India due to

entr y and g rowth of pr ivate sector banks. Al l banks are under

pressure for g rowth in business. No more bor rowers are

approaching bank but banks are in search of good bor rower and

re ta in the ir business. This has led to pressure on banks to increase

business. Due to this loans are g iven to par t ies who are otherwise

f inanc ia l ly not ver y sound. Also overa l l economic s lowdown has

put pressure banking. In absolute f igures NPAs have doubled in

last 3-4 f i sca ls. The manufactur ing sector i s not performing wel l ,

ser v ice sectors too are under pressure for margin. Software / ITES

which is major expor t revenue earning sector has not done good

a lso sector l ike a i r l ine / insurance are st i l l to stabi l ize in India . In

turn there i s pressure of recover y of such loans and threat of

advances becoming Non Performing Asset (NPA). Overa l l recover y

of advances i s de layed and i t i s s tr ic t ly not as per schedule. In

such weak cases, the banks are ag g ress ive in fol low up for recover y

and la t ter ly count ing 90 days t ime l ine so the account does not

turn out to be NPA. This scenar io has led pressure on we as

audi tor to ver i fy the sta tus of the accounts and take a ca l l whether

a par t icu lar account needs to be c lass i f ied as NPA or not .

Fur ther we as audi tor face many cha l lenges in bank audi t .

Technologica l deve lopments have changed complete bank audi t

scenar io in CBS environment . Issue of la te appointment and lesser

ava i labi l i ty of t ime for audi t i s sor ted now days to some extent as

not only the appointments are done in mid-march by some of the

bank but a lso they a l low beginning the sta tutor y audi t ear ly. S t i l l

few banks / outsta t ion branches this i ssue remains.

Another reason of concern is banking sector i s f raud prone and i t

aga in increases our responsibi l i t ies in car r y ing out bank – branch

audi t . There have been many scams in banking sector. As per PTI

repor t on 14 t h December 2012 in cur rent f i sca l in Nat iona l ized

banks a lone frauds repor ted in f i r st s ix months f rom Apr i l to

September 2012 is Rs. 5200 Crores which has increased many fold

as ear l ie r as per ear l ie r repor t on 25 t h Febr uar y 2010, Frauds have

cost banks Rs. 5 ,517 Crores in last four f i sca ls f rom Apr i l 2005 to

March 2009.

RBI is ver y str ic t wi th KYC and ant i - money launder ing norms, and

i r regular i t ies in these are v iewed ser iously and pena l t ies are be ing

imposed on banks for non adherence to these norms.

Due to a l l above deve lopment , In bank audi t , we need to plan ver y

wel l so we are able to car r y out audi t e f fect ive ly. There are var ious

acts appl icable in bank audi t but we must be updated with RBI

gu ide l ines and requirements for banking sector. Most of these

gu ide l ines are i ssued by RBI trough c i rcu lars which are ava i lable on

Reser ve Bank of Ind ia ’s websi te i .e. www.rbi .org. in.

As we read in media , Feb 2013, Operat ion of Rupee Bank was restr ic ted by RBI and many deposi tors are in problem. In past year few banks l icenses have been cance l led by RBI such as Bhandar i Co-operat ive Bank. In Febr uar y 2010, one of the bank was imposed with pena l ty of Rs.25 Lakhs for v iola t ing (RBI) d irect ives on acquis i t ion of immovable proper ty, de le t ion of records in IT system, non-adherence to KYC and ant i - money launder ing norms, i r regu lar i t ies in the conduct of cer ta in corporate g roup etc. In 2009, we read instance of cash transact ions of Rs.640 crores between November 2006 to December 2008 in one bank account and in one such s imi lar case transfer of funds overseas amount ing to $110 mi l l ions.

� In bank audi t , we need to plan ver y wel l so we are able to

car r y out audi t e f fect ive ly. There are var ious acts appl icable in bank audi t but we must be updated with RBI gu ide l ines and requirements for banking sector. Al l re la ted c ircu lars are ava i lable on Reser ve Bank of Ind ia ’s websi te i .e. www.rbi .org. in .

I fee l bank audi t can be d iv ided in fol lowing stages : Stage I GROUND WORK AT OFFICE

� Obta ining Basic Informat ion from Appointment Letter & over Te lephone :

We need to obta in bas ic informat ion such as s ize of branch, Deposi t , Advances and nature of business car r ied l ike whether or not branch is having forex business. Also whether branch is a spec ia l ized branch or not such as ser v ice Branch or not?

� Send the le t ter of acceptance of audi t and other le t ter l ike

dec lara t ion l ike le t ter of f ide l i ty and secrecy. Above draf t le t ters are normal ly provided a long with appointment le t ter.

� Issue Int imat ion le t ter as g iven in Annexure be low a long with Requirement le t ter a lso g iven in Annexure be low.

We can send int imat ion le t ter a long with le t ters g iven hereunder for requirements.

� Send Draft representat ion le t ter in Advance g iven in Annexure. We need to send representat ion le t ter to the bank branch management in advance so they can keep i t ready f rom the ir s ide.

� Study Latest RBI c i rcu lars Before we go to audi t , we should update our se l f with a l l the la test pronouncement re la t ing to banking inc lud ing c i rcu lars of Reser ve bank of Ind ia . Stage II GROUND WORK AT BRANCH

� Obta ining the l i s t of books mainta in by the branch /

Repor ts generated by computer system. When we reach branch we should enquire for a l l records and books mainta ined by the bank and a lso we should ask about var ious repor ts which are generated by the system. We should study er rors which are generated by the system whi le yearend c los ing the accounts.

� Obta in la test repor ts i .e. aud i tors and interna l repor ts to H.O.

We should study and obta in a l l la test aud i tors ’ repor t such as interna l aud i t repor t , concur rent audi t repor t , head off ice inspect ion repor ts, revenue audi t repor t , RBI Inspect ion Audit Repor t . We should l i s t out a l l major i r regu lar i t ies repor ted in this repor ts and su i tably modify our audi t prog ram as per the i r regu lar i t ies noted .

� Obta in monthly average of advances and deposi ts and

interest earned and pa id on the same for cur rent year and previous year.

This works rea l ly we l l . We are able to ana lyze major income and expenses of bank branch. If there any devia t ion as compare to previous year, we should ask for just i f ica t ion for the same.

� Review account ing pol ic ies and audi tors repor t of the bank.

To understand account ing pol ic ies which are be ing fol lowed at macro leve l by the bank, we should ask for bank as whole annual repor t copy and study the same. Qual i f ica t ion ( i f any) a t bank as whole leve l can be examined at for branch leve l .

� Obta in H.O. c i rcu lars/guide l ines of CSAs We should obta in bank c i rcu lars f rom head off ice for c los ing as we l l as normal c i rcu lars l ike for change in interest ra tes e tc.

� Prepare / Amend Audit prog ramme

After study a l l above we should amend the audi t prog ram su i tably as per the need of the branch work and r isk detected out of above rev iew. We should focus more on high r isk areas where more i r regu lar i t ies are noted .

Stage III ACTUAL AUDIT

� Car r y out ac tua l aud i t .

We should car r y out ac tua l aud i t wi th fu l l team. Based audi t prog ram we should apply test check. We should document a l l our f ind ings and quer y. Keeping Mater ia l i ty in mind we should dec ide about whether to repor t , where to repor t the i r regu lar i t ies found.

� Memorandum of changes (MOC) to be g iven with explanat ion and just i f ica t ion. If there are mater ia l changes we should issue MOC. We should a lways g ive just i f ica t ion for the MOC prepared . I t should have deta i led explanat ion for stand taken by us and we can a lso repor t management v iew i f d i f ferent f rom our v iew.

� Issue Ni l MOC even i f i t i s NIL or don’t make AR subject to MOC.

If there i s no MOC we should issue a NIL MOC cer t i f ica te or accord ingly we should ment ion in our main repor t . For qua l i f ica t ion we should avoid g iv ing any reference to other repor ts.

� Independence of main repor t and LFAR- No Referenc ing

of each other, independent qua l i f ica t ion/adverse remarks.

Both this repor ts are independent repor ts and we should not do cross referenc ing in these two repor ts.

� Discuss the draf t repor ts- reser vat ion, major obser vat ion, qua l i f ica t ions with branch management .

I t i s one of best pract ices that we should d iscuss our obser vat ions / draf t repor t with the management .

� Audit Repor t format i s modif ied and suggested draf t i s g iven in Annexure to this ar t ic le.

� Qual i f ica t ion to be g iven in bold or i ta l ic. S t i l l many of us are not repor t ing qua l i f ica t ion as required by above amendment .

� To quant i fy the qua l i f ica t ion.

� We must quant i fy the qua l i f ica t ion ( i f any) . If for any reason we are not able to get qua l i f ica t ion from management we should ment ion the fact in our repor t .

� Stamping on a l l pages and ini t ia l ing the cor rect ion done.

We must stamp and put our in i t ia ls on a l l pages. We must authent icate cor rect ions wherever done in sta tements or repor ts s igned by us.

� Issue of f ina l repor ts in t ime.

We must i ssue repor t in t ime. We should adhere to t ime dead l ine g iven by the bank author i t ies. If there are any pract ica l problems, we should inform to top management in wr i t ing about such problems be ing cause of de lay for non-complet ion of audi t in t ime.

� Format of le t ter for Int imat ion Annexure - I

A B C & Co. Char tered Accountants

XX March 2017 The Branch Manager, XYZ Bank of Ind ia , XYZ Tower, 248, ABC Road, Indore-452 001 Sub. : AUDIT OF YOUR BRANCH AS ON 31st MARCH 2017 Dear S ir,

� We have been appointed for audi t ing the accounts of your branch for the year ended 31st March 2017 wide le t ter no. IBK/SA 2016-2017 dated 27th Febr uar y, 2017.

� For proper planning of your audi t , we request you to send

photo copy of the fol lowing i tems at our above-mentioned address on rece ipt of our le t ter :

1 . Tria l ba lance as on 28/02/2017

2. Branch Audit Repor t for the year ended 31st March, 2016.

3 . Long Form Audit Repor t for the year ended 31st March, 2016.

4 . Tax Audit Repor t for the year ended 31st March, 2016. 5 . Balance sheet of the Bank for the year ended 31st

March, 2016.

� As you are aware that we have to f ina l i sed the accounts on or before XX Apr i l 2017 so we request you to keep ever ything ready for the audi t on or before XXth Apr i l ,2017.

� As this year RBI has changed the LFAR you are required to

prepare par ty wise deta i l s for la rge advances above 2 Crores. Sending herewith, format as g iven by the H.O. so that you can keep the required deta i l s ready.

� Also sending herewith deta i led l i s t of the requirement

which would be necessar y for car r y ing out audi t , hope that same wi l l be ready before we v is i t the branch.

� Apar t f rom above may keep a l l the other records and informat ion ready which you fee l wi l l be necessar y to expedi te the audi t .

� Also sending herewith draf t management representat ion le t ter recommended by Inst i tute of Char tered Accountants of Ind ia . , th is would require f rom your s ide before we complete the audi t .

� Last but not least we expect your best co-operat ion in la te seat ing and a lso working on hol idays dur ing the audi t per iod so as to meat the dead l ine se t by your head off ice.

Thanking You, Yours Fa i thfu l ly For A.B.C. & Co. Char tered Accountants Par tner

Format of le t ter for Requirements Annexure – II

A B C & Co. Char tered Accountants

XX March 2017 The Branch Manager, XYZ Bank of Ind ia , XYZ Tower, 248, ABC Road, Indore-452 001 Sub. : AUDIT OF YOUR BRANCH AS ON 31st MARCH 2017 Dear S ir, You may a l ready have been informed by your Head Off ice that we have been appointed as the Sta tutor y Auditors to repor t on the accounts of your Branch for 2016-2017. We are conf ident you wi l l make ava i lable to us, the Branch re turns soon af ter the c lose of the accounts on 31.3 .2017. As per the H.O. Instr uct ions, we plan to star t the audi t a f ter XX Apr i l , 2017 to f inish the same before XX Apr i l 2017. In order to enable us to f ina l i se and furnish our repor t on the audi t of the accounts for the year 2016-2017 of your branch, may we request you to keep ready the informat ion / c lar i f ica t ions as sta ted be low and make the same ava i lable to our audi t team at the ear l iest .

1 . Latest Repor ts

For our scr ut iny, the fol lowing la test repor ts on the accounts of your Branch, and compl iance by the Branch check the obser vat ions conta ined there in:

(a ) Interna l Inspect ion Repor t ; (b) Revenue / Concur rent Audit Repor t ; (c ) RBI Inspect ion Repor t , i f such inspect ion took place ; (d ) Income and Expenditure Control Audit Repor t ; and (e ) Copy of Cer t i f ica tes

2 . Circu lars in Connect ion with Accounts

P lease le t us have a copy of the head off ice c i rcu lars / instr uct ions in connect ion with c los ing of your Accounts for the year, to the extent not communicated to us or incorporated in our le t ter of appointment .

3 . Account ing Pol ic ies P lease le t us have a l i s t of the account ing pol ic ies adopted by the bank with par t icu lar reference to i tems of income and expenditure. P lease conf irm whether, as compared to the ear l ie r year, there are any changes in the account ing pol ic ies dur ing the year under audi t ; and i f so, the f inanc ia l e f fect thereof may be computed to enable us to ver i fy the same.

4 . Balanc ing of Books P lease conf irm the present sta tus of ba lanc ing of the subsid iar y records with the re levant control accounts, and in case of d i f ferences between ba lances in the control and subsid iar y records, please le t us know the effor ts be ing made to reconci le / ba lance the same. This informat ion may please be g iven head-wise for the re levant control accounts, ind icat ing the dates when the ba lances were last ta l l ied .

5 . Overdue / matured Term Deposi ts P lease conf irm having transfer red them to Cur rent Account Deposi t a t ca l l A/c. If not , deta i l s / par t icu lars of cred i t ba lances compris ing overdue matured Term Deposi ts as a t the year end which cont inue to be shown as Term Deposi ts par t icu lar ly where the branch does not have any instr uct ions / communicat ion for renewal of such deposi ts f rom the account holders and amount of provis ion made on such overdue / matured term deposi ts.

6 . Advances

(a ) Please conf irm whether in respect of the advances aga inst tangible secur i t ies, the bank holds ev idence of ex istence and market va lue of the re levant secur i t ies as a t the year-end.

(b) We may be informed of the year-end sta tus of the accounts

each with outstanding above 1% of the tota l Advances

Por tfol io of the branch or Rs. 100 lakhs whichever i s lower, par t icu lar ly those which have been adverse ly commented upon in the la test repor ts on the branch and in respect of which provis ions have been made / recommended as a t the previous year-end.

Informat ion in re la t ion to such advances accounts where provis ion is computed / recommended may please be prepared ind icat ing:

( i ) Name of the Bor rower ( i i ) Type of fac i l i ty ( i i i ) * Tota l amount outstanding as a t the year-end (both for

pr inc ipa l and interest ) spec i fy ing the date up to which interest has been lev ied and recovered .

( iv ) Nature of defau l t and act ion taken. (v) Brief histor y and present sta tus of the Advance. (v i ) * Provis ion a l ready made / recommended.

*Cor responding f igures for the previous year-end may please be g iven.

The previously ment ioned informat ion may please be kept ready

and be made ava i lable to us a long with the Branch re turns.

(c ) Please conf irm whether the bor rowers ’ accounts have been categor ised accord ing to the new norms appl icable for the year into Standard , Sub-standard , Doubtfu l or Loss asse ts , wi th spec ia l emphasis on Non-Performing Assets (NPA) Please conf irm whether you have examined the accounts and appl ied the norms bor rower-wise and not account-wise for categor is ing the accounts. P lease le t us have the par t icu lars of provis ions computed / recommended in respect of the above dur ing the f inanc ia l year under audi t .

(d ) A l is t of a l l advances accounts which have been ident i f ied

as of the nature of bad / doubtfu l accounts and where pending formal sanct ion of the higher author i t ies, the re levant amounts have not been rec lass i f ied / recategor ised in the books of the Branches for provis ion / wr i te off. This covers a l l accounts ident i f ied by the Bank or interna l / externa l aud i tors or by RBI inspectors but the amount has not been wr i t ten off whol ly or par t ly.

In case the Branch has i tse l f recommended act ion aga inst the bor rowers or for in i t ia t ing lega l or other coerc ive ac t ion for recover y of dues, a l i s t of such bor rowers ’ accounts may be furnished to us.

(e ) Please le t us have a l i s t of bor rowers ’ accounts where c lass i f ica t ion made as a t the end of the previous year has been changed to a better c lass i f ica t ion, s ta t ing reasons for the same.

( f ) Please a lso conf irm whether any income has been ad justed

/ recorded to revenue, contrar y to the norms of income recognit ion not i f ied by the Reser ve Bank of Ind ia and / or Head Off ice c i rcu lars i ssued in this regard ; and par t icu lar ly where the chances of recover y / re l iabi l i ty of the income are remote. P lease a lso conf irm whether any income has been recorded on Non Performing Accounts other than on actua l rea l i sa t ion.

7 . Outstandings in Suspense / Sundr y Account P lease le t us have a year wise break up of amounts outstanding in Suspense / Sundr y accounts as on 31.3 .2017. Reasons for non- ad justment of i tems inc luded in these may be made known.

8 . Contingent L iabi l i t ies

(a ) Please conf irm whether other than for advances, there are any matters involv ing the Branch in any c la ims in l i t ig a t ion, arbi tra t ion or other d isputes in which there may be some f inanc ia l impl icat ions, inc lud ing for staf f c la ims, munic ipa l taxes, loca l lev ies e tc. If so these may be l i s ted for our ver i f ica t ion, and you may conf irm whether you have inc luded these as cont ingent l iabi l i t ies.

(b) Please conf irm whether guarantees are be ing d isc losed net

of margins or otherwise as a t the year-end, and whether the expired guarantees where the c la im per iod has a lso expired , cont inue to be d isc losed in the Branch re turn. P lease conf irm spec if ica l ly.

9 . Interest Provis ion

(a ) Please conf irm whether interest provis ion has been made on deposi ts e tc, in accordance with the la test instr uct ions

of the Head Off ice. A copy of these may be made ava i lable for our scr ut iny.

(b) Please conf irm whether any amount recorded as income up

to the year-end, which remains unrecovered or not re leasable , has been reversed from any of the income heads or has been debi ted to any expenditure head dur ing the year. If so, please le t us have deta i l s to enable us to ver i fy the same.

(c ) Please conf irm the account ing treatment as regards

reversa l , i f any, of interest / other income recorded up to the previous year-end; and the amount reversed dur ing the year under audi t i .e. , income of ear l ie r years derecognised dur ing the year.

10 . Fore ign Cur rency Outstanding Transact ions

(a ) Please conf irm whether amount outstanding as a t the year-end have been conver ted as a t the year-end ra tes as appl icable , ra ther than at the dates the entr ies or ig inated—par t icu lar ly for bi l l s outstanding, guarantees, L/Cs e tc.

(b) Please conf irm the amount of inward va lue of fore ign

cur rency parce ls, i f any, which or ig inated pr ior to the year-end from other branches, but could not be recorded as these were in transi t – and for which entr ies were made af ter the year end .

11 . Investments

In case, the Branch holds any investments beha lf of the Bank:

(a ) These may be produced for physica l ver i f ica t ion and / or ev idence of hold ing the same be made ava i lable.

(b) Stocks of unused secur i ty paper sta t ionar y / numbered forms l ike B/RS, SGL Forms e tc. may please be produced for physica l ver i f ica t ion.

(c ) It may be conf irmed whether income accr ued / col lected has been accounted as per the la id down procedure.

12 . Long Form Audit Repor t-Branch response to the Quest ionnaire

In connect ion with the Long Form Audit Repor t , p lease le t us have complete informat ion as regards each i tem in the quest ionnaire , to enable us to ver i fy the same for the purpose of our audi t . Make a note that this year LFAR has been rev ised by the R.B.I . Keep the

above informat ion as per new LFAR requirement . In case you have not rece ived format of New LFAR you may ar range for the same.

13 . Tax Audit in terms of Sect ion 44AB of the Income tax Act , 1961 P lease le t us have the informat ion required for tax audi ts under Sect ion 44AB of the Income-tax Act , 1961 to enable us ver i fy the same for the purpose of our repor t thereon.

14 . Other Cer t i f ica t ion Let us have, du ly authent icated , informat ion as regards other matters which, as per our le t ter of appointment , required cer t i f ica t ion. We sha l l be g ratefu l i f you could a lso conf irm the name to the off icer (s) nominated by the bank to comply with our requirements in connect ion with the above, so that our repor ts / cer t i f ica tes are expedi ted . We sha l l apprec ia te your k ind co-operat ion in the matter. Thanking you, Yours fa i thfu l ly, For A B C & CO. Char tered Accountants Par tner

Annexure

Draft of Management Representat ion Letter* to be obta ined from

the Branch Management

M/s XYZ & Co. ,

Char tered Accountants,

Mumbai

Dear S ir (s ) ,

Sub. : Audit for the year ended March 31, 2017

This representat ion le t ter i s provided in connect ion with your audi t of the f inanc ia l s ta tements of _____________ branch of _______________ bank for the year ended March 31, 2017 for the purpose of express ing an opinion as to whether the f inanc ia l s ta tements g ive a tr ue and fa i r v iew of the sta te of af fa i rs of ___________ branch of _______________ bank as of March 31, 2017 and of the resu l ts of operat ions for the year then ended. We acknowledge our responsibi l i ty for preparat ion of f inanc ia l s ta tements in accordance with the requirements of the Reser ve Bank of Ind ia and recognised account ing pol ic ies and pract ices, inc lud ing the Account ing and Audit ing Standards i ssued by the Inst i tute of Char tered Accountants of Ind ia (ICAI) .

We conf irm, to the best of our knowledge and be l ie f , the fol lowing representat ions:

1 . Account ing Pol ic ies

The account ing pol ic ies, which are mater ia l or cr i t ica l in determining the resu l ts of operat ions for the year or sta te of af fa i rs are se t out in the f inanc ia l s ta tements and are consistent with those adopted in the f inanc ia l s ta tements for the previous year. The f inanc ia l s ta tements are prepared on accr ua l bas is except as sta ted otherwise in the f inanc ia l s ta tements.

There are no changes in the account ing pol ic ies fol lowed by the branch dur ing the cur rent year.

2 . Assets

The branch has a sa t i sfac tor y t i t le to a l l asse ts and there are no l iens or encumbrances on the branch's asse ts. The branch has not rece ived any lega l not ices f rom the

l and lords ask ing them to vacate the premises that the branch is cur rent ly occupy ing as a lessee.

3 . F ixed Assets

The f ixed assets he ld by Branches have been proper ly accounted and have been physica l ly ver i f ied a t the year end . No d iscrepanc ies are not iced on such ver i f ica t ion. Deprec ia t ion on these asse ts have been adequate ly provided as per the pol icy of the bank.

4 . Capi ta l Commitments

At the ba lance sheet date , there were no outstanding commitments for capi ta l expenditure other than those d isc losed in the f inanc ia l s ta tements.

5 . Other Cur rent Assets

In the opinion of the management , other cur rent asse ts have a va lue on rea l i sa t ion in the ord inar y course of the branch’s business which is a t least equa l to the amount a t which they are sta ted in the ba lance sheet .

6 . Cash and Bank Balances

The cash ba lance as on March 31, 2017 is Rs._____________ and has been ver i f ied by us.

7 . L iabi l i t ies

The branch has recorded a l l known l iabi l i t ies in the f inanc ia l s ta tements.

8 . Cont ingent L iabi l i t ies

8 .1 The branch has d isc losed in notes to the f inanc ia l s ta tements a l l ;

(a ) guarantees that we have g iven to third par t ies ;

(b) Letters of Cred i ts (Loca l/ Impor t) ;

(c ) Letters of Comfor t (Loca l/ Impor t) ;

(d ) Defer red Payment Cred i ts/ Guarantees (Loca l/ Impor t) ; and

(e ) a l l other cont ingent l iabi l i t ies.

8 .2 Other than for advances, there are no matters involv ing the branch in any c la ims in l i t ig a t ion, arbi tra t ion or other d isputes in which there may be some f inanc ia l impl icat ions, inc lud ing for staf f c la im, branch renta ls, munic ipa l taxes, loca l lev ies, e tc. , except for those which have been appropr ia te ly inc luded under cont ingent l iabi l i t ies.

8 .3 Expired guarantee where the c la im year has a lso expired has been cor rect ly removed from the branch re turn.

8 .4 Cont ingent l iabi l i t ies d isc losed in the notes to the f inanc ia l s ta tements do not inc lude any cont ingenc ies, which are

l ike ly to resu l t in a loss and which, therefore, require ad justment of asse ts or l iabi l i t ies.

8 .5 No cases/ lega l d isputes are pending aga inst the branch/ lodged by the branch, for which no l iabi l i ty has accr ued/ is l ike ly to accr ue in the future.

9 . Provis ions for Cla ims and Losses

Provis ion has been made in the accounts for a l l known losses and c la ims of mater ia l amounts.

10 . There have been no events subsequent to the ba lance sheet date that require ad justment of, or d isc losure in , the f inanc ia l s ta tements or notes thereto.

11 . Prof i t and Loss Account

Except as d isc losed in the f inanc ia l s ta tements, the resu l ts for the year were not mater ia l ly af fected by :

(a ) t ransact ions of a nature not usua l ly under taken by the branch;

(b) c i rcumstances of an except iona l or non–recur r ing nature ;

(c ) charges or cred i ts re la t ing to pr ior years ;

(d ) changes in account ing pol ic ies.

12 . We have made ava i lable to you a l l the fol lowing la test repor ts on the accounts of our branch, and compl iance by the branch on the obser vat ions conta ined there in:

a ) Previous year ’s branch audi t repor t ;

b) Interna l inspect ion repor ts ;

c ) Repor t on any other Inspect ion Audit that has been conducted dur ing the course of the year re levant to the f inanc ia l year 2016-17.

Apar t f rom the above, the branch has not rece ived any show cause not ice, inspect ion advice, e tc. , f rom Government of Ind ia , Reser ve Bank of Ind ia or any other monitor ing or regula tor y author i ty of Ind ia that could have a mater ia l e f fect on the f inanc ia l s ta tements of the branch dur ing the year.

13 . Ba lanc ing of Books

The books of the accounts are computer ised and hence the subsid iar y records are automat ica l ly ba lanced with the re levant control records. In case of manual sub- ledgers mainta ined , we conf irm that they duly match with the genera l ledger ba lances.

14. Overdue/Matured Term Deposi ts

Al l overdue/ matured term deposi ts are he ld as matured term deposi ts.

15 . Advances

15 .1 In respect of a l l the advances aga inst tangible secur i t ies, the branch holds ev idence of ex istence and market va lue of the re levant secur i t ies as a t the year–end

15.2 Al l the bor rowers ’ account have been categor ised accord ing to the preva lent RBI norms appl icable for the year, into standard , sub–standard , doubtfu l or loss asse ts, with spec ia l emphasis on Non–Performing Assets (NPA).

15 .3 We have examined the accounts and appl ied the norms bor rower–wise and not account–wise for categor is ing the accounts.

15 .4 The c lass i f ica t ion of advances made as a t the end of the previous year has not been changed to a better c lass i f ica t ion.

15 .5 No income has been ad justed/ recorded to revenue, contrar y to the norms of income recognit ion not i f ied by the Reser ve Bank of Ind ia ; and par t icu lar ly where the chances of recover y/ rea l i sabi l i ty of the income are remote.

15 .6 No income has been recorded on Non-performing accounts other than on actua l rea l i sa t ion.

16 . Outstanding in Suspense/ Sundr y Account

The year–wise/ entr y–wise break up of amounts outstanding in Sundr y deposi ts/ Sundr y asse ts as on March 31, 2016 has a l ready been submitted to you a long with explanat ion of the nature of the amounts in br ie f and suppor t ing ev idences re la t ing to the ex istence of such amounts in the aforesa id accounts.

17 . Interest Provis ions

17 .1 Interest provis ion has been made on deposi ts, e tc. , in accordance with the extant instr uct ions of the Head Off ice.

17 .2 Any amount recorded as income upto the year–end, which remains unrecovered or not rea l i sable , has been reversed from the respect ive income heads or has been debi ted to cor responding expenditure head dur ing the year.

17 .3 The account ing treatment as regards reversa l , i f any of interest/ other income recorded upto the previous year end ; and the amount reversed dur ing the year under audi t , i .e. , income of ear l ie r years de–recognised dur ing the year

has been made in accordance with the preva lent RBI norms of income recognit ion.

17 .4 The interest provis ion for Head Off ice Interest sha l l be made a t the Head Off ice.

18 . Sta t ioner y

Stock of unused sta t ioner y l ike secur i ty papers, cheque books, demand draf t book, e tc have been produced for your physica l ver i f ica t ion and are in order.

19 . Long Form Audit Repor t–Branch Response to the Quest ionnaire

In connect ion with the Long Form Audit Repor t , complete informat ion as regards each i tem in the quest ionnaire has been made ava i lable to you in order to enable you to ver i fy the same for the purpose of your audi t .

20 . Other Cer t i f ica t ion

Duly authent icated , informat ion as regards other matters which, as per the bank’s le t ter of appointment , require cer t i f ica t ion has been made ava i lable to you.

21 . Genera l

There i s no enquir y going on or conc luded dur ing the year by Centra l Bureau of Invest ig at ion (CBI) or any other v ig i lance or invest ig at ing agency on the branch or on i ts employees and no cases of f rauds or of misappropr ia t ion of asse ts of the branch have come to the not ice of the Management dur ing the year other than for amounts for which provis ions have a l ready been made in the books of accounts.

22 . The provis ion for non–performing assets, deprec ia t ion, provis ion for income tax , provis ion for bonus, g ra tu i ty, e tc. , i s made a t the Head Off ice. Therefore, the same has not been provided in the branch accounts.

23 . There have been no i r regular i t ies involv ing management or employees who have a s ignif icant role in the system of interna l control that could have a mater ia l e f fect on the f inanc ia l s ta tements.

24 . At the end of the year, the branch has transla ted i ts hold ings of Fore ign Deposi t Accounts a t a not iona l ra te of Rs. Xx to 1 USD. The d if ference between the not ional ra te of Rs. Xx and the actua l ra te as a t the year end wi l l be accounted for a t the Head Off ice.

25 . The f inanc ia l s ta tements are f ree of mater ia l missta tements, inc lud ing omiss ions.

26 The branch has compl ied with a l l aspects of contractua l ag reements that could have a mater ia l e f fect on the f inanc ia l s ta tements in the event of non–compl iance. There has been no non–compl iance with requirements of regu la t ing author i t ies that could have a mater ia l ef fect on the f inanc ia l s ta tements in the event of non–compl iance.

27 . We have no plans or intent ions that may mater ia l ly af fect the car r y ing va lue or c lass i f ica t ion of asse ts and l iabi l i t ies ref lec ted in the f inanc ia l s ta tements.

28 . The other par t icu lars required have a l ready been g iven to you and par t icu lars and other representat ions made to you from t ime to t ime are tr ue and cor rect in a l l respects.

29 . Tax Audit for the Year Ended March 31, 20xx (Tax Audit in Terms of Sect ion 44AB of the Income–tax Act , 1961)

The informat ion required for the tax audi t under sect ion 44AB of the Income–tax Act , 1961 has been made ava i lable to you in order to enable you to ver i fy the same for the purpose of your repor t thereon. In respect of the Tax Audit under sect ion 44 AB of Income Tax Act , 1961 of _____________ branch of _______________ bank for the year ended March 31, 2017, we cer t i fy the fol lowing:

PART – A

29.1 Our Permanent Account No. i s ______________

29.2 The address as per the jur isd ic t ion of the assessee fa l l s under sect ion 124 of the Income Tax Act , 1961 is ______________________

29.3 The sta tus as def ined under the Income Tax Act, 1961 is company.

PART – B

29.4 There i s no change in nature of business in cur rent year as compared to preced ing previous year.

29 .5 The books of accounts mainta ined by us have been cor rect ly d isc losed in c lause 9(b) of Form 3CD.

29 .6 Our Prof i t & Loss account does not inc lude prof i ts and ga ins assessable on presumptive bas is under sect ion 44AD, 44AE, 44AF, 44B, 44BB, 44BBA, 44BBB, 172 of the Income–Tax Act , 1961.

29 .7 The method of account ing fol lowed is as per c lause 11(a) which has been consistent ly fol lowed in the immediate ly preced ing previous year. There was no change in the method of account ing employed v is à v is the method employed in the immediate ly preced ing previous year.

29 .8 Sum rece ived from employee towards contr ibut ions to any provident fund or superannuat ion fund or any other fund

mentioned in sect ion 2(24)(x) which is pa id/ not pa id within due dates to concerned author i t ies under sect ion 36(1)(va) are ment ioned in Clause 16 (b) of our Form 3CD and the same are cor rect .

29 .8 In Clause 17 of Form 3CD, there are no other amounts of such i tems debi ted to Prof i t & Loss Account and there i s no income which does not form par t of the tota l income

29.9 No payments are made to persons spec if ied under sect ion 40A(2)(b) .

29 .10 There i s no amount of prof i t chargeable to tax u/s 41 as d isc losed under c lause 20 of Form 3CD.

29 .11 Except for the i tems shown under c lause 21 ( i i ) (B) , no tax , duty or other sum as refer red to u/s 43B has been provided as a t the year end .

29 .12 No expenditure/ income of an ear l ie r year has been debi ted/ cred i ted to the Prof i t & Loss Account except to the extent d isc losed under c lause 22 (b) of Form 3CD.

29 .13 No loans or deposi ts of Rs. 20 ,000 or more have been repa id in cash other than those spec if ied in the sta tement of par t icu lars as g iven in the respect ive c lause of Form 3CD. The deta i l s of loans or deposi ts of Rs. 20 ,000 or more g iven in the sa id sta tement of par t icu lars i s t r ue and cor rect .

29 .14 Sect ion–wise deta i l s of deduct ion admiss ible under chapter VI–A

No other deduct ions other than those ment ioned in c lause 26 of Form 3CD is ava i lable to the branch.

29 .15 Deta i l s of de lay in payment of tax deducted at source to the cred i t of the Centra l Government are g iven in the sta tement of par t icu lars. Apar t f rom that , there are no other de lay in payment of Tax Deducted a t Source.

29 .16 The other par t icu lars required have a l ready been g iven to you and par t icu lars and other representat ions made to you from t ime to t ime are tr ue and cor rect in a l l respects.

Thanking you,

Yours fa i thfu l ly

For & on beha lf of __________ branch of ______________ bank

Author ised S ignator y

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 1 of 30

Annexure

Draft Bank Branch Audit Prog ram for the year ended March 31, 2017

NOTE:

1) The above audi t prog ram is i l lustra t ive and the members are advised to modify the same

su i tably to su i t the ir requirement .

2) Documentat ion should be done to suppor t the above audi t prog ramme.

Name of the Bank and Branch:

Region/ Zone in which the Branch is located :

Date of Commencement :

Date of Complet ion:

Audit Team Par tner/s :

Name of Seniors Man Days Ini t ia ls Remarks, i f any

Name of Juniors Man Days Ini t ia ls Remarks, i f any

Deta i l s of the Author ised Persons of the bank Branch Manager :

Others (Spec ify ) :

Audit Aspects Covered By Whom Extent of Check

Genera l

1 . Engagement le t ter to the appoint ing author i ty and le t ter of requirement to the Branch.

2 Repor t ing to the Branch.

3 . Review of previous year ' s aud i t repor t/ LFAR, cur rent per iod 's Interna l Audit Repor t/ Revenue Audit Repor t/ Concur rent Audit Repor t/ RBI Inspect ion Repor t and any other repor t and the ir compl iance.

4 . Physica l ver i f ica t ion of cash, s ta t ioner y, and va luable secur i t ies.

5 Physica l ver i f ica t ion of Investments (obta in cer t i f ica te f rom bank manager for the same) .

6 . Understand the system in CBS Branch a) ver i fy controls b) s tar t of day and end of day repor t c ) ver i fy except iona l repor t

.

7 Compl iance of bank’s c i rcu lars, account ing

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 2 of 30

Audit Aspects Covered By Whom Extent of Check

pol icy as we l l as Mandator y Account ing Standards/Audit ing Standards and RBI Circu lars.

8 . Checking of var ious re turns.

Checking of Ba lance Sheet Items

1 . Checking of the advances :

i ) Deta i led checking of forms c lass i fy ing the advances

1 . Crit ica l rev iew of a l l la rge advances.

2 . Class i f ica t ion of advances.

3 . Latest va luat ion of secur i ty g iven aga inst advances.

4 . Provis ions on NPA as per RBI gu ide l ines.

i i ) Loan Accounts

i ) Review of a l l la rge advances with ba lance of lower of 5 % or Rs.2 crore of tota l advance.

i i ) Review of loans sanct ioned dur ing the year. Also ver i fy a l l the cred i t card dues which are overdue.

i i i ) Review of other advances on test check bas is.

iv ) Review of adverse comments by Concur rent audi tors, RBI/interna l inspectors.

v ) Review of su i t f i led and decreeta l accounts and provis ion and prog ress thereof and Class i f ica t ion

v i ) Review of accounts upg raded dur ing the year f rom NPA to standard . Review of a l l accounts f requent ly exceed ing l imits/DP

NOTE: ( i ) Fol lowing aspects of the advances to be ver i f ied :

Pre sanct ion: System of cred i t Appra isa l and rev iew/renewal .

Post sanct ion: Compl iance of terms of sanct ion, documentat ion, end use of funds.

Monitor ing: Stock and Book sta tements, drawing power, insurance, inspect ion of stock/secur i ty, operat ions in the account , e tc.

( i i ) Al l the accounts ver i f ied in categor y ( i ) to (v) should be documented .

2 . Ver i fy controls in respect of the fol lowing impor tant i tems of asse ts.

( i ) Dual custody of cash ( i i ) Custody and issue of cheques books/pay

orders/ATM cards e tc ( i i i ) ATM cash as per books and actua l

ba lance ta l l ied a t year end .

3 Checking of ba lance books with ledgers (only in case of manual branches) .

4 . Checking of addi t ions/deduct ion/transfers of f ixed assets. Compl iance of Account ing Standard (AS)-6 , AS10, ,AS 26 and AS28 re la ted to f ixed assets

4a . F ixed Assets Schedule for furni ture & f ixtures and other asse ts.

5 . Reconc i l ia t ion of accounts with other banks,

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 3 of 30

Audit Aspects Covered By Whom Extent of Check

head off ice and inter branch ad justment accounts.

6 Deta i led checking of suspense accounts – cred i t as we l l as debi t schedules. i .e. , Nomina l ledger.

7 . Deta i l s of Bi l l s Rediscounted/Ref inance obta ined from IDBI, SIDBI, e tc.

8 . Shares/ Bonds/ Secur i t ies he ld in safe custody on banks investment account .

Ba lance Sheet F ina l i sa t ion

1 . Ver i fy ing Ba lance Sheet f igures with Genera l Ledger

2 . Cast ing of Ba lance Sheet and cross–checking with Ba lance Sheet schedules

3 . Scr ut iny of Ba lance sheet , par t icu lar ly –

i ) that a l l the ba lances are shown in proper heads and broadly compare previous year f igure to understand mater ia l var iance

i i ) check in case of advances :

a ) that interest accr ued but not due on loans i s not inc luded in advances.

b) that cred i t ba lances in O/D, C/C in–operat ive cur rent accounts should not be netted off with advances and the same should be shown under demand deposi ts.

i i i ) Check in case of deposi ts :

a ) Ver i f ica t ion of Ant i Money Launder ing gu ide l ines and Compl iance with KYC norms on test check bas is

b) that overdue deposi ts, matured t ime deposi ts, cash cer t i f ica tes and cer t i f ica tes of deposi ts are shown in Demand deposi ts.

c ) Interest accr ued but not due should not be inc luded in deposi ts but , should be shown under other l iabi l i ty.

d ) Operat ion and conduct of demat accounts.

4 . Checking, ( i ) L iabi l i ty under Bank Guarantee/ L/C. ( i i ) Reconc i l ia t ion of Genera l Ledger and

Subsid iar y Ledger.

5 . Inter Off ice Reconc i l ia t ion (IOR) Accounts ( i ) Ver i fy Inter Branch Items In Transi t (IBIT)

account for old entr ies. ( i i ) Compare on test Check bas is, the ba lance

and the entr ies in IOR Accounts with the copies of the sta tements submitted to the IOR depar tment/s.

( i i i ) Cr i t ica l ly ver i fy the da i ly enquir y memos rece ived from the respect ive IOR depar tment/s for any old and odd i tems and act ion taken by the branch for the same.

( iv) Old un reconc i led entr ies are be ing provided/ repor ted to HO for provis ion

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 4 of 30

Audit Aspects Covered By Whom Extent of Check

Checking of Prof i t and Loss Items

1 . Test checking of interest on deposi ts, (par t icu lar ly, Interest checking should be done on Test bas is for the per iod subsequent to the per iod of revenue/ concur rent audi t ) . Ensure that interest provis ion on overdue F.D. has been made as per la test RBI gu ide l ines.

2 . Test checking of interest/commiss ion on var ious advances, bi l l s, L .C. , Guarantees, e tc.

3 . Test checking of d iscount/commiss ion on bi l l s d iscounted and others.

4 . Cr i t ica l scr ut iny of the Expenses/Income accounts and checking of impor tant vouchers.

5 . Provis ion for expenses, accr ued interest on deposi ts and advances. (Par t icu lar ly check whether or not interest has been provided/charged on a l l types of deposi ts/ advances.

6 . Checking of interest in NOSTRO Accounts debi t ba lances.

7 . Ver i f ica t ion of recover y on account of locker rent , s taf f accommodat ion, e tc. , wi th deta i l s of ar rears, i f any.

8 . Commiss ion income on account of Government Business, i .e. , col lec t ion as we l l as remittance of Income tax , sa les tax , exc ise duty, e tc. ,

9 . Deta i l s of Pr ior Per iod i tems of Income as we l l as expenses and complete deta i l s of provis ions to be made, i f any.

10 . Rebate on Bi l l s d iscounted .

11 . Checking of deprec ia t ion on f ixed assets

12 . Booking of Interest Income on account of par t ia l recover y in NPA’s.

Prof i t and Loss Account F ina l i sa t ion

1 . Ver i f ica t ion of Prof i t and Loss Account with Prof i t And Loss Ledgers.

2 . Cast ing of Prof i t and Loss Bookle ts and cross checking with Prof i t and Loss Account schedules.

3 . Prof i t and Loss Account Scr ut iny.

4 . Rat io ana lys is wi th previous years f igures.

Others

1 . Checking of sta tement of f rauds.

2 . Checking of sta tement of c la ims aga inst the bank not acknowledged as debt .

3 . Checking of Fore ign Cur rency forward exchange contracts showing sa les and purchase separate ly. Review of NRE and FCNR accounts, i f any.

4 . Checking of Guarantees g iven on beha lf of Const i tuents.

5 . Checking of Acceptance, endorsements and other obl ig at ions, i .e. , L/C and bi l l s accepted by the bank on beha lf of customers.

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 5 of 30

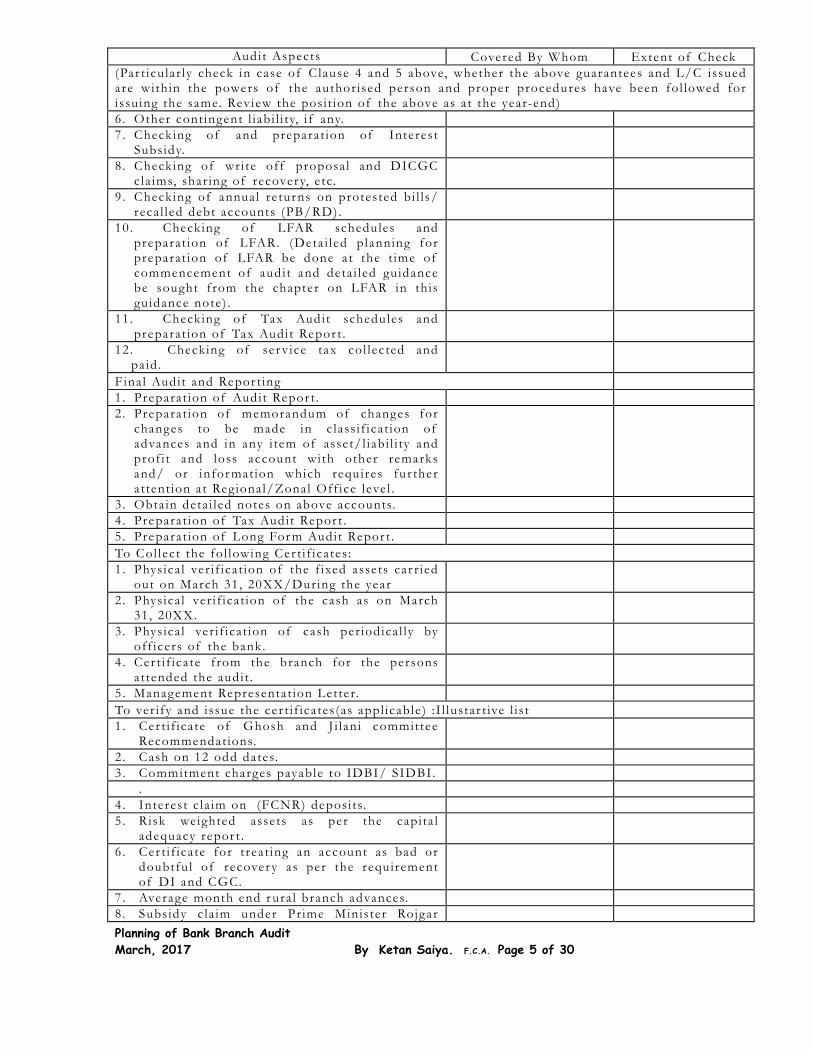

Audit Aspects Covered By Whom Extent of Check

(Par t icu lar ly check in case of Clause 4 and 5 above, whether the above guarantees and L/C issued are within the powers of the author ised person and proper procedures have been fol lowed for i ssu ing the same. Review the posi t ion of the above as a t the year-end)

6 . Other cont ingent l iabi l i ty, i f any.

7 . Checking of and preparat ion of Interest Subsidy.

8 . Checking of wr i te off proposa l and DICGC c la ims, shar ing of recover y, e tc.

9 . Checking of annual re turns on protested bi l l s/ reca l led debt accounts (PB/RD).

10 . Checking of LFAR schedules and preparat ion of LFAR. (Deta i led planning for preparat ion of LFAR be done a t the t ime of commencement of audi t and deta i led gu idance be sought f rom the chapter on LFAR in this gu idance note) .

11 . Checking of Tax Audit schedules and preparat ion of Tax Audit Repor t .

12 . Checking of ser v ice tax col lec ted and pa id .

F ina l Audit and Repor t ing

1 . Preparat ion of Audit Repor t .

2 . Preparat ion of memorandum of changes for changes to be made in c lass i f ica t ion of advances and in any i tem of asse t/ l iabi l i ty and prof i t and loss account with other remarks and/ or informat ion which requires fur ther a t tent ion a t Regiona l/Zonal Off ice leve l .

3 . Obta in deta i led notes on above accounts.

4 . Preparat ion of Tax Audit Repor t .

5 . Preparat ion of Long Form Audit Repor t .

To Col lec t the fol lowing Cer t i f ica tes :

1 . Physica l ver i f ica t ion of the f ixed assets car r ied out on March 31, 20XX/During the year

2 . Physica l ver i f ica t ion of the cash as on March 31, 20XX.

3 . Physica l ver i f ica t ion of cash per iod ica l ly by off icers of the bank.

4 . Cer t i f ica te f rom the branch for the persons a t tended the audi t .

5 . Management Representat ion Letter.

To ver i fy and issue the cer t i f ica tes(as appl icable ) : I l lustar t ive l i s t

1 . Cer t i f ica te of Ghosh and J i lani committee Recommendat ions.

2 . Cash on 12 odd dates.

3 . Commitment charges payable to IDBI/ SIDBI.

.

4 . Interest c la im on (FCNR) deposi ts.

5 . Risk weighted assets as per the capi ta l adequacy repor t .

6 . Cer t i f ica te for treat ing an account as bad or doubtfu l of recover y as per the requirement of DI and CGC.

7 . Average month end r ura l branch advances.

8 . Subsidy c la im under Pr ime Minister Rojgar

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 6 of 30

Audit Aspects Covered By Whom Extent of Check

Yojna .

Prepared by : Reviewed by :

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 7 of 30

An I l lustra t ive Format of Repor t of the Auditor of a Banking Company

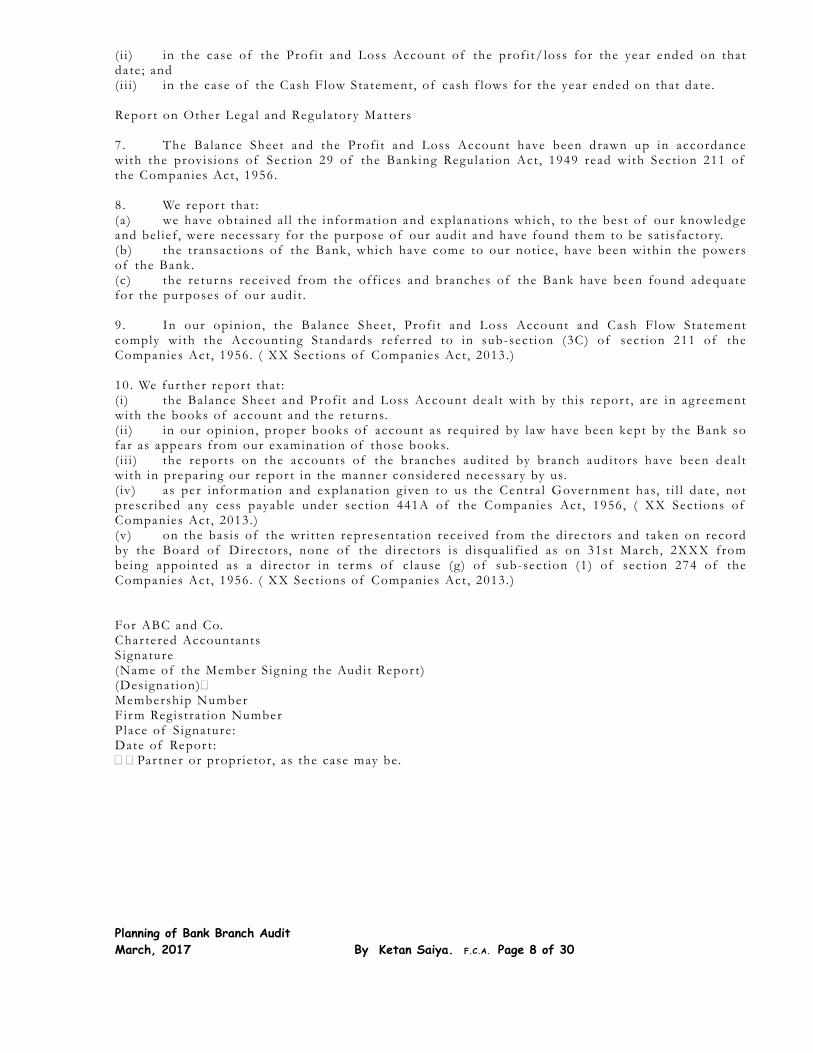

INDEPENDENT AUDITOR’S REPORT To The Shareholders Repor t on the Financ ia l S ta tements 1 . We have audi ted the accompanying f inanc ia l s ta tements of the ABC Bank Limited , which comprise the Ba lance Sheet as a t 31st March, 2XXX and the Sta tement of Prof i t and Loss and the cash f low sta tement for the year then ended and a summary of s ignif icant account ing pol ic ies and other explanator y informat ion. Incorporated in these f inanc ia l s ta tements are the re turns of ________ branches audi ted by us, ______________ branches audi ted by branch audi tors and unaudited re turns of ______________ branches in respect of which exemption has been g ranted by the Centra l Government under Rule 4 (1) (a ) of the Companies (Branch Audit Exemption) Rules, 1961 from the provis ions of sub-sect ions (1) and (3) of Sect ion 228 of the Companies Act , 1956. These unaudited branches account for ______________________ per cent of advances, _______________ per cent of deposi ts, ___________________ per cent of interest income and ____________________ per cent of interest expense. Management ’s Responsibi l i ty for the F inanc ia l S ta tements 2 . Management i s responsible for the preparat ion of these f inanc ia l s ta tements in accordance with XYZ Law of India . This responsibi l i ty inc ludes the des ign, implementat ion and maintenance of interna l control re levant to the preparat ion of the f inanc ia l s ta tements that are f ree f rom mater ia l missta tement , whether due to f raud or er ror. Auditor ’s Responsibi l i ty 3 . Our responsibi l i ty i s to express an opinion on these f inanc ia l s ta tements based on our audi t . We conducted our audi t in accordance with the Standards on Audit ing issued by the Inst i tute of Char tered Accountants of Ind ia . Those Standards require that we comply with e thica l requirements and plan and perform the audi t to obta in reasonable assurance about whether the f inanc ia l s ta tements are f ree f rom mater ia l missta tement . 4 . An audi t involves performing procedures to obta in audi t ev idence about the amounts and d isc losures in the f inanc ia l s ta tements. The procedures se lec ted depend on the audi tor ’s judgement , inc lud ing the assessment of the r i sks of mater ia l missta tement of the f inanc ia l s ta tements, whether due to f raud or er ror. In making those r i sk assessments, the audi tor considers interna l control re levant to the Company ’s preparat ion and fa i r presentat ion of the f inanc ia l s ta tements in order to des ign audi t procedures that are appropr ia te in the c i rcumstances. An audi t a lso inc ludes eva luat ing the appropr ia teness of account ing pol ic ies used and the reasonableness of the account ing est imates made by management , as we l l as eva luat ing the overa l l presentat ion of the f inanc ia l s ta tements. 5 . We be l ieve that the audi t ev idence we have obta ined is suff ic ient and appropr ia te to provide a bas is for our audi t opinion. Opinion 6 . In our opinion and to the best of our informat ion and accord ing to the explanat ions g iven to us, the sa id accounts together with the notes thereon g ive the informat ion required by the Banking Regula t ion Act , 1949 as we l l as the Companies Act , 1956, in the manner so required for the banking companies and g ive a tr ue and fa i r v iew in conformity with the account ing pr inc iples genera l ly accepted in India : ( i ) in the case of the Ba lance Sheet , of the sta te of af fa i rs of the Bank as a t 31st March, 2XXX;

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 8 of 30

( i i ) in the case of the Prof i t and Loss Account of the prof i t/ loss for the year ended on that date ; and ( i i i ) in the case of the Cash Flow Statement , of cash f lows for the year ended on that date. Repor t on Other Lega l and Regula tor y Matters 7 . The Balance Sheet and the Prof i t and Loss Account have been drawn up in accordance with the provis ions of Sect ion 29 of the Banking Regula t ion Act , 1949 read with Sect ion 211 of the Companies Act , 1956. 8 . We repor t that : (a ) we have obta ined a l l the informat ion and explanat ions which, to the best of our knowledge and be l ie f , were necessar y for the purpose of our audi t and have found them to be sa t isfac tor y. (b) the transact ions of the Bank, which have come to our not ice, have been within the powers of the Bank. (c ) the re turns rece ived from the off ices and branches of the Bank have been found adequate for the purposes of our audi t . 9 . In our opinion, the Ba lance Sheet , Prof i t and Loss Account and Cash Flow Statement comply with the Account ing Standards refer red to in sub-sect ion (3C) of sect ion 211 of the Companies Act , 1956. ( XX Sect ions of Companies Act , 2013. ) 10 . We fur ther repor t that : ( i ) the Ba lance Sheet and Prof i t and Loss Account dea l t wi th by this repor t , a re in ag reement with the books of account and the re turns. ( i i ) in our opinion, proper books of account as required by law have been kept by the Bank so far as appears f rom our examinat ion of those books. ( i i i ) the repor ts on the accounts of the branches audi ted by branch audi tors have been dea l t wi th in prepar ing our repor t in the manner considered necessar y by us. ( iv ) as per informat ion and explanat ion g iven to us the Centra l Government has, t i l l date , not prescr ibed any cess payable under sect ion 441A of the Companies Act , 1956, ( XX Sect ions of Companies Act , 2013. ) (v) on the bas is of the wr i t ten representat ion rece ived from the d irectors and taken on record by the Board of Directors, none of the d irectors i s d isqua l i f ied as on 31st March, 2XXX from be ing appointed as a d irector in terms of c lause (g) of sub-sect ion (1) of sect ion 274 of the Companies Act , 1956. ( XX Sect ions of Companies Act , 2013. ) For ABC and Co. Char tered Accountants S ignature (Name of the Member S igning the Audit Repor t) (Designat ion)S Membership Number Firm Registra t ion Number Place of S ignature : Date of Repor t : SSPar tner or propr ie tor, as the case may be.

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 9 of 30

An I l lustra t ive Format of Repor t of the Auditor of a Nat iona l i sed Bank INDEPENDENT AUDITOR’S REPORT To The Pres ident of Ind ia Repor t On The Financ ia l S ta tements 1 . We have audi ted the accompanying f inanc ia l s ta tements of XY Bank as a t 31st March, 2XXX, which comprise the Ba lance Sheet as a t March 31, 2XXX, and Statement of Prof i t and Loss and the cash f low sta tement for the year then ended, and a summary of s ignif icant account ing pol ic ies and other explanator y informat ion. Incorporated in these f inanc ia l s ta tements are the re turns of ___________ branches audi ted by us and ______________ branches audi ted by branch audi tors. The branches audi ted by us and those audited by other audi tors have been se lec ted by the Bank in accordance with the gu ide l ines i ssued to the Bank by the Reser ve Bank of Ind ia . Also incorporated in the Ba lance Sheet and the Sta tement of Prof i t and Loss are the re turns f rom _______________ branches which have not been subjected to audi t . These unaudited branches account for ___________________per cent of advances, _____________ per cent of deposi ts, _______________ per cent of interest income and _______________ per cent of interest expenses. Management ’s Responsibi l i ty for the F inanc ia l S ta tements 2 . Management i s responsible for the preparat ion of these f inanc ia l s ta tements in accordance with XYZ Law of India . This responsibi l i ty inc ludes the des ign, implementat ion and maintenance of interna l control re levant to the preparat ion of the f inanc ia l s ta tements that are f ree f rom mater ia l missta tement , whether due to f raud or er ror. Auditor ’s Responsibi l i ty 3 . Our responsibi l i ty i s to express an opinion on these f inanc ia l s ta tements based on our audi t . We conducted our audi t in accordance with the Standards on Audit ing issued by the Inst i tute of Char tered Accountants of Ind ia . Those Standards require that we comply with e thica l requirements and plan and perform the audi t to obta in reasonable assurance about whether the f inanc ia l s ta tements are f ree f rom mater ia l missta tement . 4 . An audi t involves performing procedures to obta in audi t ev idence about the amounts and d isc losures in the f inanc ia l s ta tements. The procedures se lec ted depend on the audi tor ’s judgement , inc lud ing the assessment of the r i sks of mater ia l missta tement of the f inanc ia l s ta tements, whether due to f raud or er ror. In making those r i sk assessments, the audi tor considers interna l control re levant to the Company ’s preparat ion and fa i r presentat ion of the f inanc ia l s ta tements in order to des ign audi t procedures that are appropr ia te in the c i rcumstances. An audi t a lso inc ludes eva luat ing the appropr ia teness of account ing pol ic ies used and the reasonableness of the account ing est imates made by management , as we l l as eva luat ing the overa l l presentat ion of the f inanc ia l s ta tements. 5 . We be l ieve that the audi t ev idence we have obta ined is suff ic ient and appropr ia te to provide a bas is for our audi t opinion. Opinion 6 . In our opinion, as shown by books of bank, and to the best of our informat ion and accord ing to the explanat ions g iven to us : ( i ) the Ba lance Sheet , read with the notes thereon is a fu l l and fa i r Ba lance Sheet conta ining a l l the necessar y par t icu lars, i s proper ly drawn up so as to exhibi t a t r ue and fa i r v iew of sta te of

Planning of Bank Branch Audit

March, 2017 By Ketan Saiya. F.C.A. Page 10 of 30

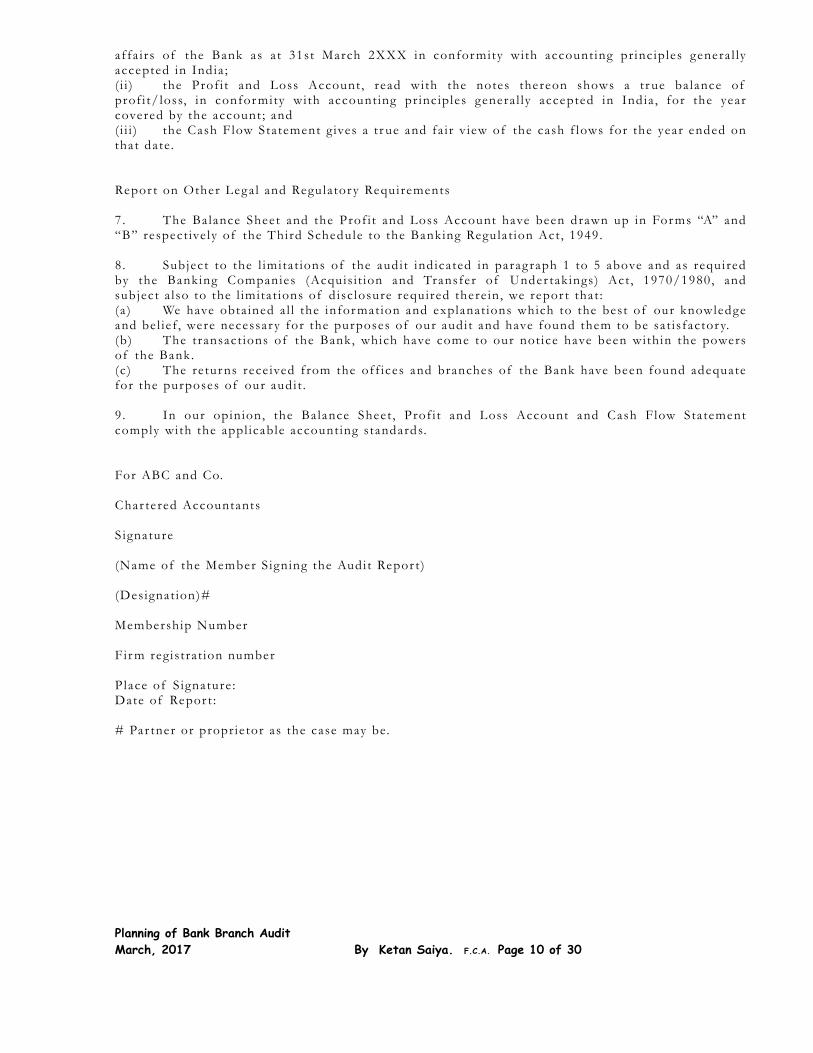

affa i rs of the Bank as a t 31st March 2XXX in conformity with account ing pr inc iples genera l ly accepted in India ; ( i i ) the Prof i t and Loss Account , read with the notes thereon shows a tr ue ba lance of prof i t/ loss, in conformity with account ing pr inc iples genera l ly accepted in India , for the year covered by the account ; and ( i i i ) the Cash Flow Statement g ives a t r ue and fa i r v iew of the cash f lows for the year ended on that date. Repor t on Other Lega l and Regula tor y Requirements 7 . The Balance Sheet and the Prof i t and Loss Account have been drawn up in Forms “A” and “B” respect ive ly of the Third Schedule to the Banking Regula t ion Act , 1949. 8 . Subject to the l imita t ions of the audi t ind icated in parag raph 1 to 5 above and as required by the Banking Companies (Acquis i t ion and Transfer of Under tak ings) Act , 1970/1980, and subject a lso to the l imita t ions of d isc losure required there in, we repor t that : (a ) We have obta ined a l l the informat ion and explanat ions which to the best of our knowledge and be l ie f , were necessar y for the purposes of our audi t and have found them to be sa t isfac tor y. (b) The transact ions of the Bank, which have come to our not ice have been within the powers of the Bank. (c ) The re turns rece ived from the off ices and branches of the Bank have been found adequate for the purposes of our audi t . 9 . In our opinion, the Ba lance Sheet , Prof i t and Loss Account and Cash Flow Statement comply with the appl icable account ing standards. For ABC and Co. Char tered Accountants S ignature (Name of the Member S igning the Audit Repor t) (Designat ion)# Membership Number F irm registra t ion number P lace of S ignature : Date of Repor t : # Par tner or propr ie tor as the case may be.