auditing chapter 19 compliance & internal auditing by david n. ricchiute

TRANSCRIPT

AUDITINGCHAPTER 19

Compliance & Internal AuditingBy David N. Ricchiute

GBW 8th ed., Ch. 192

TOPICS

Compliance auditingInternal auditing

GBW 8th ed., Ch. 193

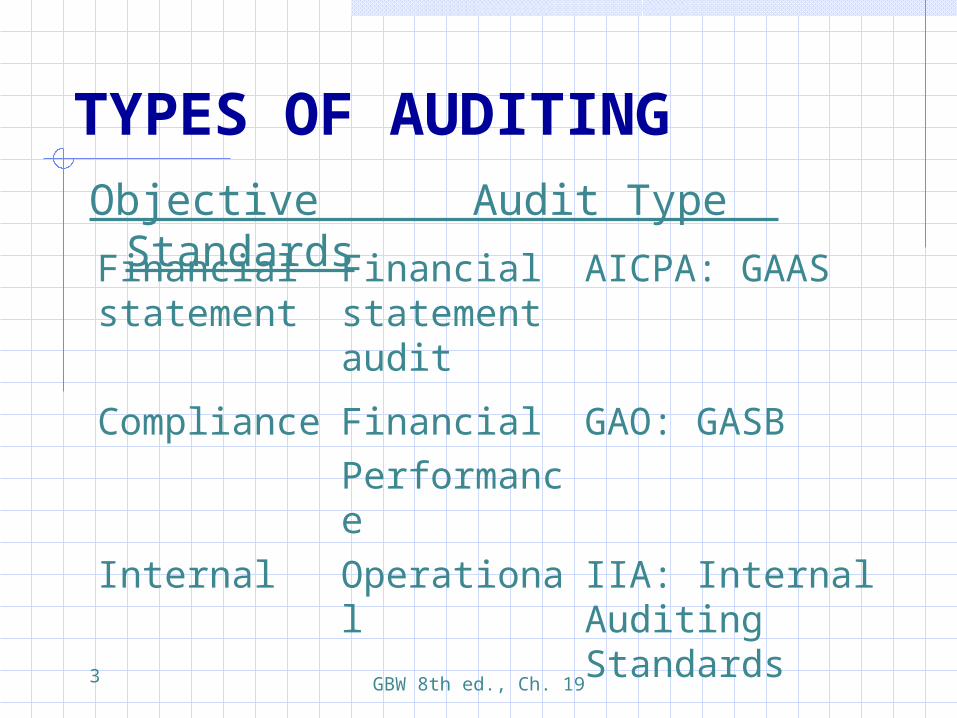

TYPES OF AUDITINGObjective Audit Type Standards

Financial statement

Financial statement audit

AICPA: GAAS

Compliance FinancialPerformance

GAO: GASB

Internal Operational IIA: Internal Auditing Standards

GBW 8th ed., Ch. 194

COMPLIANCE AUDITS: Government Entities

Also recipients of governmental financial assistance (SAS 74)Audit must conform to GAAS GAO standards Single Audit Act

GBW 8th ed., Ch. 195

COMPLIANCE AUDITS: Other Examples

Compliance with:Minimum wage lawsEmployee benefits programsCommercial bank lending agreementsSpecial engagements Hazardous waste trust fund State-sponsored health insurance

program

GBW 8th ed., Ch. 196

RESPONSIBILITIES UNDER GAAS

Responsibility for detecting violations of laws, regulations identical to responsibility for client error, fraud Assess risk of violations creating

material misstatements Design procedures to detect

anticipated violations

GBW 8th ed., Ch. 197

EFFECTS OF LAWS, REGULATIONS

Management responsible for identifying laws, regulations having direct, material effect on financial statementAuditor designs procedures to detect violations

GBW 8th ed., Ch. 198

COMPLIANCE & INTERNAL CONTROL

Compliance audit requires auditor to Understand internal controls Assess control risk Obtain knowledge about design,

performance of internal control policies, procedures

GBW 8th ed., Ch. 199

GOVERNMENT AUDITING STANDARDS

Written by GAOGAGAS AICPA 10 GAAS Standards related to

Independence & Quality control Audit documentation Legal, regulatory requirements

GBW 8th ed., Ch. 1910

GOVERNMENT FINANCIAL AUDITS: Financial Statement Audits

Financial statement audits determine whether Financial statements fairly presented Entity complied with laws, regulations

GBW 8th ed., Ch. 1911

GOVERNMENT FINANCIAL AUDITS: Financial-Related Audits

Financial-related audits determine whether Financial reports, related items fairly

presented Financial information in accord with

established, stated criteria Entity adhered to financial

compliance requirements

GBW 8th ed., Ch. 1912

GOVERNMENT PERFORMANCE AUDITS

Economy & efficiency audits determine whether Entity acquires, protects, uses

resources economically & efficiently Causes of diseconomies, inefficiencies Compliance with laws, regulations

related to efficiency

GBW 8th ed., Ch. 1913

GOVERNMENT PROGRAM AUDITS

Program audits determine Extent to which program

achieves results, benefits Effectiveness of organization,

program, activity, function Compliance with laws,

regulations

GBW 8th ed., Ch. 1914

REPORTING ON COMPLIANCE

Positive assurance on tests for noncomplianceDescription of material instances of noncompliance, if any

GBW 8th ed., Ch. 1915

REPORTING ON INTERNAL CONTROL

Government auditing standards require report on internal control in all governmental financial audits to Describe costs, benefits, objectives,

limitations of internal control State that auditor assessed control risk Describe deficiencies in internal control

not considered reportable conditions

GBW 8th ed., Ch. 1916

SINGLE AUDIT ACT

Audit coverage All governmental units that

receive any federal assistance

Reporting requirements for governments receiving over $300,000

GBW 8th ed., Ch. 1917

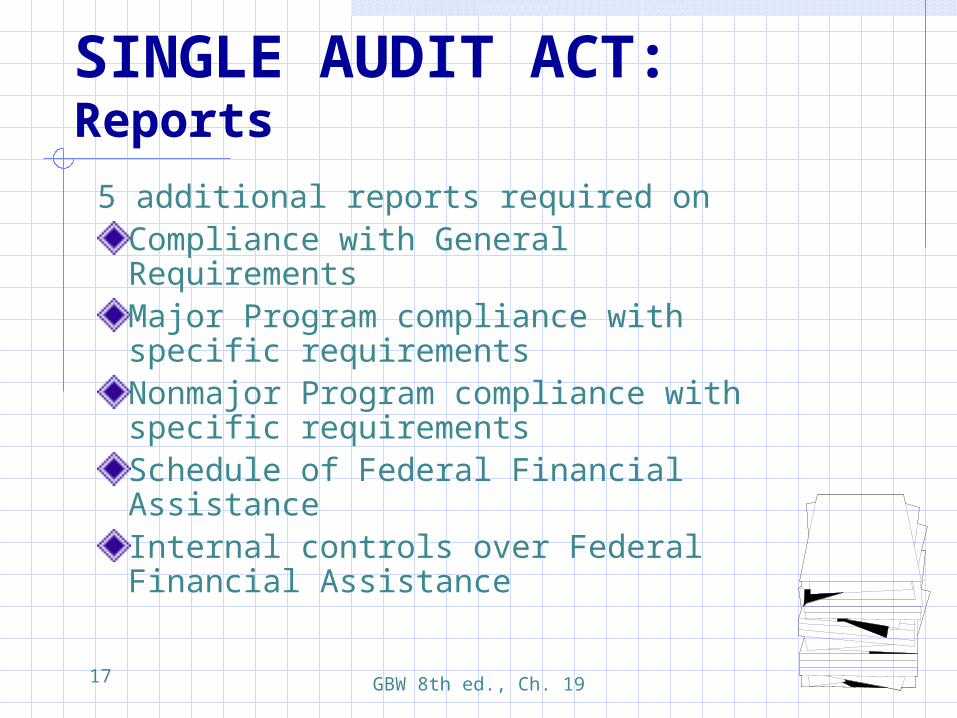

SINGLE AUDIT ACT: Reports

5 additional reports required onCompliance with General RequirementsMajor Program compliance with specific requirementsNonmajor Program compliance with specific requirementsSchedule of Federal Financial AssistanceInternal controls over Federal Financial Assistance

GBW 8th ed., Ch. 1918

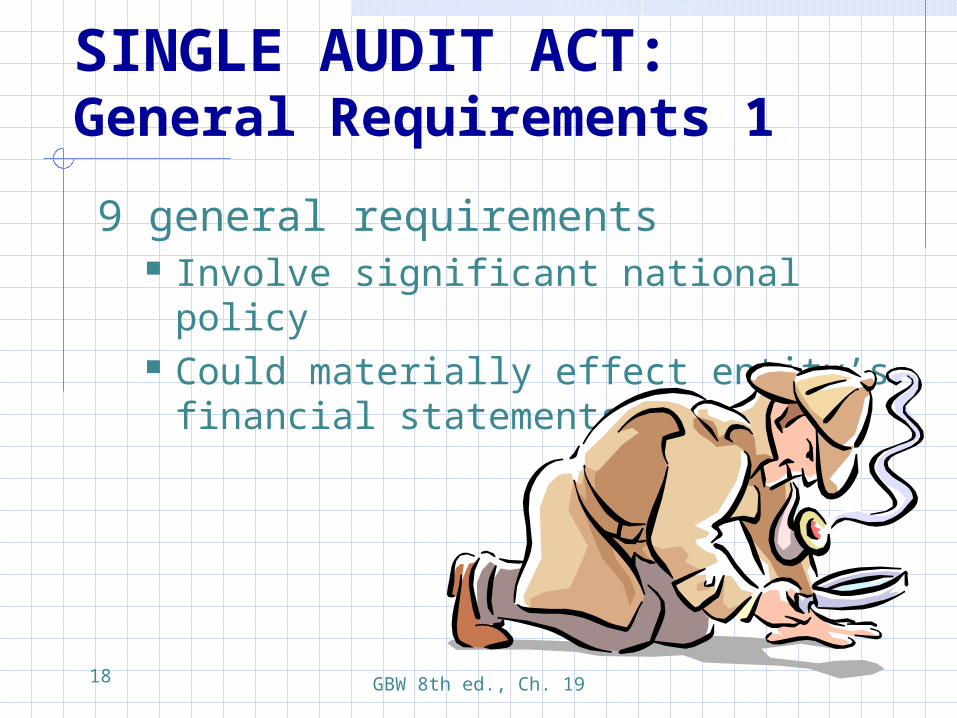

SINGLE AUDIT ACT: General Requirements 1

9 general requirements Involve significant national policy Could materially effect entity’s

financial statements

GBW 8th ed., Ch. 1919

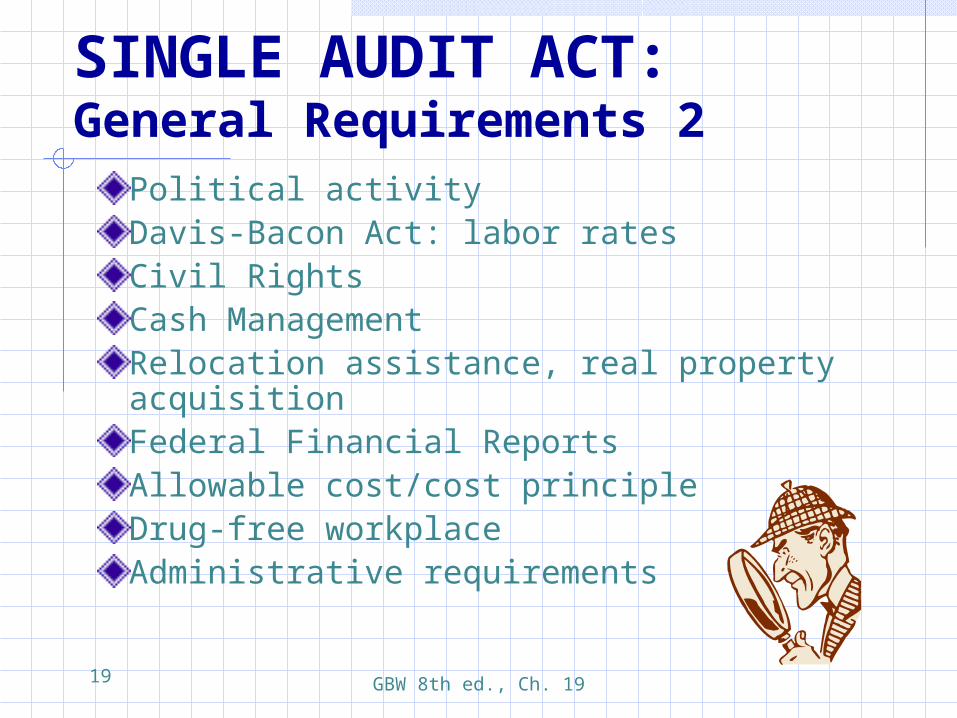

SINGLE AUDIT ACT: General Requirements 2

Political activityDavis-Bacon Act: labor ratesCivil RightsCash ManagementRelocation assistance, real property acquisitionFederal Financial ReportsAllowable cost/cost principleDrug-free workplaceAdministrative requirements

GBW 8th ed., Ch. 1920

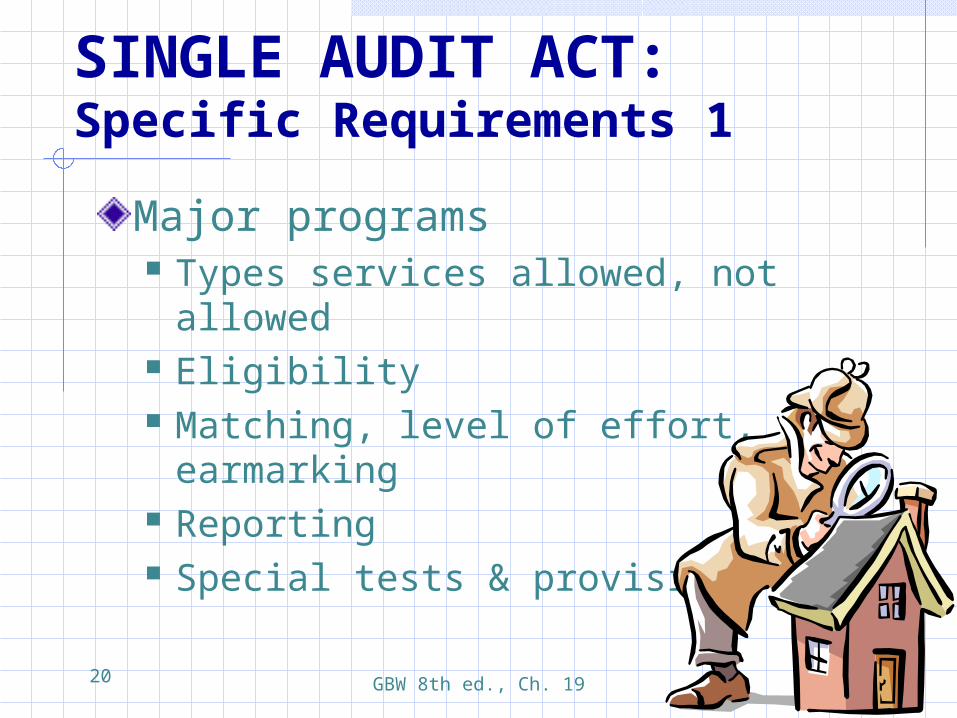

SINGLE AUDIT ACT: Specific Requirements 1

Major programs Types services allowed, not allowed Eligibility Matching, level of effort, earmarking Reporting Special tests & provisions

GBW 8th ed., Ch. 1921

SINGLE AUDIT ACT: Specific Requirements 2

When transactions from nonmajor programs are tested Compliance with applicable laws,

regulations Allowability program expenditures Eligibility

GBW 8th ed., Ch. 1922

INTERNAL AUDITING

Internal auditing is an independent, objective assurance, consulting activity designed to add value, improve organizations operations.

It helps organization accomplish objectives by bringing systematic, disciplined approach to evaluate, improve effectiveness of risk management, control, governance

Institute of Internal Auditors

GBW 8th ed., Ch. 1923

INTERNAL AUDITING: Independence, Objectivity

Independence achieved by reporting to board of directorsObjectivity achieved by appraising controls, not designing or implementing them

GBW 8th ed., Ch. 1924

OPERATIONAL AUDITING

Verification of dataAppraisal of controlsCompliance with policies, plans, proceduresProtection of assetsAppraisal of performanceRecommendations for operating improvements

GBW 8th ed., Ch. 1925

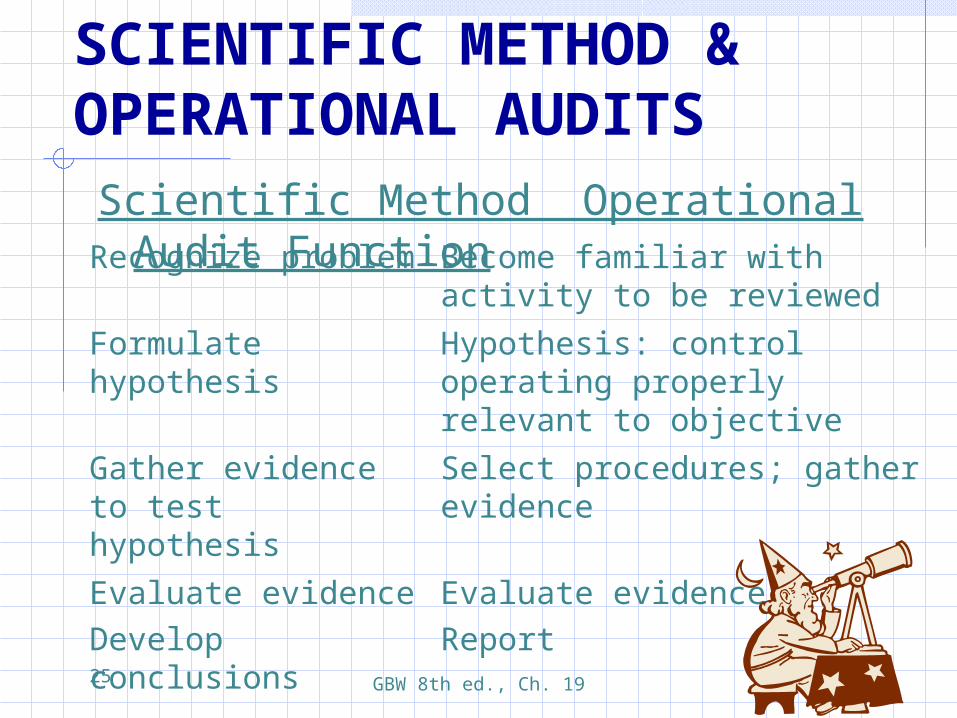

SCIENTIFIC METHOD & OPERATIONAL AUDITSScientific Method Operational Audit

FunctionRecognize problem Become familiar with activity to be reviewed

Formulate hypothesis

Hypothesis: control operating properly relevant to objective

Gather evidence to test hypothesis

Select procedures; gather evidence

Evaluate evidenceDevelop conclusions

Evaluate evidenceReport

GBW 8th ed., Ch. 1926

AUDITOR’S CONSIDERATION INTERNAL AUDIT FUNCTION

SAS 65 Guidance on

Considering work of internal auditors Using internal auditors to provide direct

assistance

GBW 8th ed., Ch. 1927

UNDERSTANDING CONTROLS: Internal Auditor

Auditor should obtain understanding of internal audit function as part of assessment of control risk Organizational status Adherence to professional standards Internal auditor’s audit plan Access to records; limitations on scope of

activities Charter or mission statement

GBW 8th ed., Ch. 1928

ASSESSING COMPETENCE, OBJECTIVITY: Internal Auditor

SAS 65 requires independent auditor to review competence, integrity of internal auditor Education, experience, certification,

continuing education Audit policies, programs, procedures Practices for assigning internal auditors Quality work paper documentation

GBW 8th ed., Ch. 1929

RELIANCE ON INTERNAL AUDITORS

Independent auditor can rely on internal auditor after evaluating his/her work for Understanding internal control Assessing risk Performing substantive procedures