auditing erp systems without specific caats item 6_a_brazil 21 wgita... · company #1 (sox...

TRANSCRIPT

BRAZILIAN COURT OF AUDIT

21st Meeting WGITA

Kuala Lumpur, Jan, 2012

Auditing ERP systems without

specific CAATs

Auditing ERP Systems without

specific CAATS

Agenda

Brazil and IT Audit Secretariat background

Audit opportunities and risks

Survey on ERP systems in the Brazilian

Federal Public Administration

Benchmarking of audit methodologies

Audit methodology

Conclusion

Brazil background

Country data

5th largest country in the world

6th GDP in the world

area: 8,500,000 sq. km (2.5 x The European

Community)

population: 190,000,000 inhabitants

84th HDI

Democratic Federative Republic

Brazilian Court of Audit (TCU) – Federal level

3

Created in August 2006

to undertake audits that require specialized knowledge in IT

to research, develop and disseminate methods on IT audit

to elaborate and provide IT audit training

4

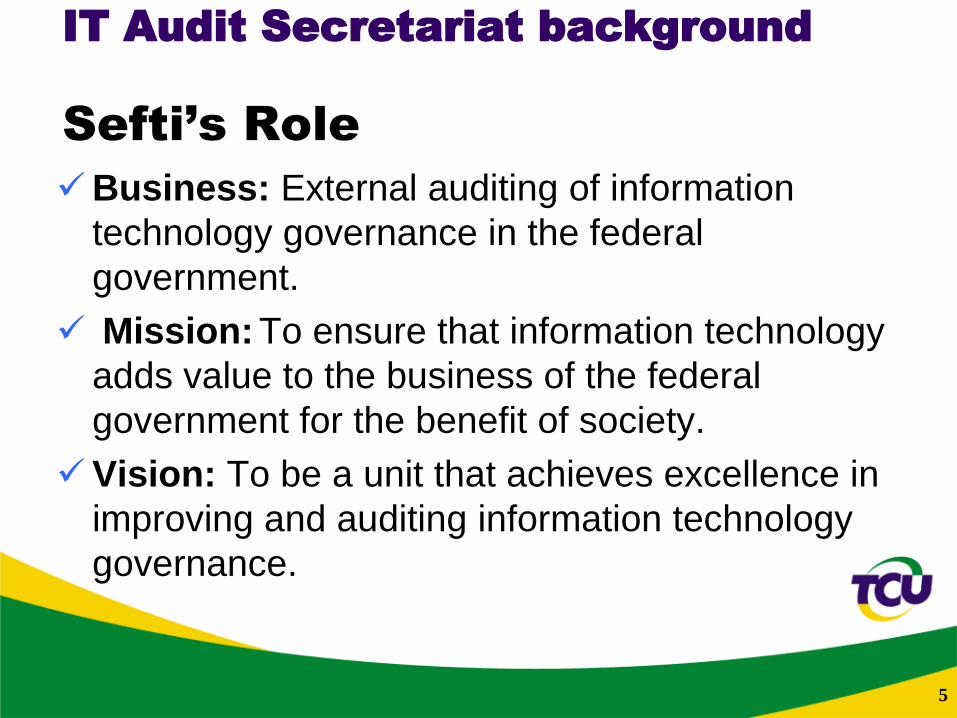

IT Audit Secretariat background

Sefti’s Role

Business: External auditing of information

technology governance in the federal

government.

Mission: To ensure that information technology

adds value to the business of the federal

government for the benefit of society.

Vision: To be a unit that achieves excellence in

improving and auditing information technology

governance.

5

IT Audit Secretariat background

Auditing ERP Systems without

specific CAATS

Brazil and IT Audit Secretariat background

Audit opportunities and risks

Survey on ERP systems in the Brazilian

Federal Public Administration

Benchmarking of audit methodologies

Audit methodology

Conclusion

6

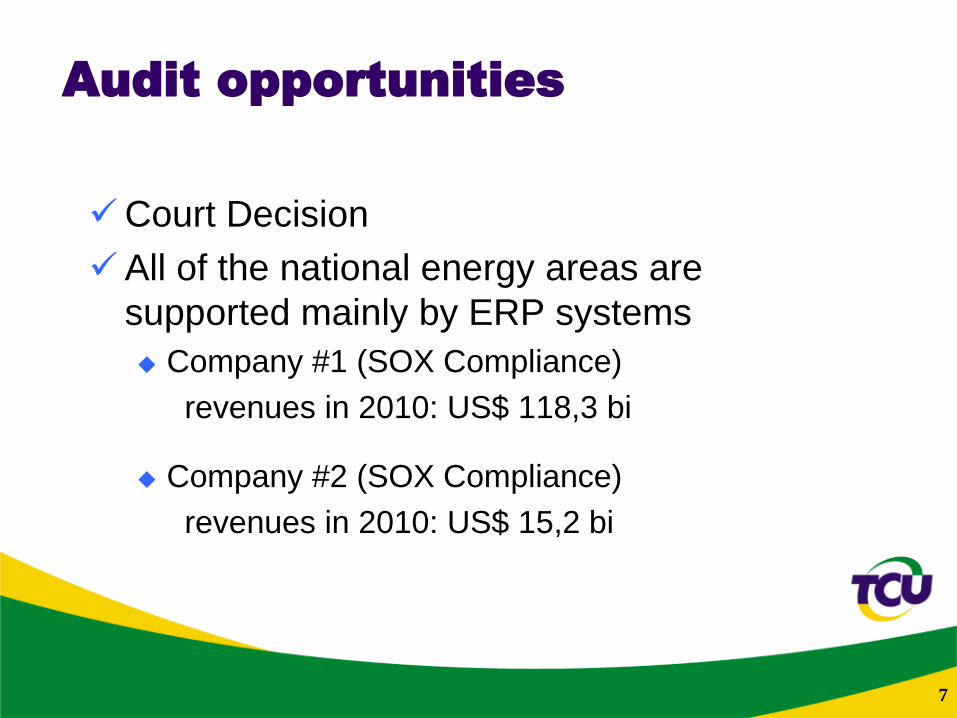

Court Decision

All of the national energy areas are

supported mainly by ERP systems

Company #1 (SOX Compliance)

revenues in 2010: US$ 118,3 bi

Company #2 (SOX Compliance)

revenues in 2010: US$ 15,2 bi

7

Audit opportunities

Lack of knowledge of auditors regarding

the topic

No prior audits on the topic carried out by

TCU

Lack of a support tool (CAATs) to audit

controls related to the application of ERP

systems

8

Audit risks

Auditing ERP Systems without

specific CAATS

Brazil and IT Audit Secretariat background

Audit opportunities and risks

Survey on ERP systems in the Brazilian

Federal Public Administration

Benchmarking of audit methodologies

Audit methodology

Conclusion

9

Survey

57 national public companies

Most in the energy business (Petroleum and Electricity)

49% of them use ERP systems and 33% plan on using ERP

systems in the medium term

49%

33%

18%

Respondents by category

Use

Plan

Don´t use

10

3 main suppliers

SAP is the leader, followed by Totvs (a national

company) and by Oracle

Survey

36%

25%

14%

25%

Supplier Quantitative Distribution

SAP

Totvs

Oracle

Others

11

Cost of acquisition of licenses and customization

approximately US$ 666 million

Scope of benefits from implementation of ERP system

Survey

12

0% 20% 40% 60% 80% 100%

Information Security

Work process

Management issues

Controls

Financial

Others

Benefits Categories

Auditing ERP Systems without

specific CAATS

Brazil and IT Audit Secretariat background

Audit opportunities and risks

Survey on ERP systems in the Brazilian

Federal Public Administration

Benchmarking of audit methodologies

Audit methodology

Conclusion

13

Benchmarking (Experientia Mutua Omnibus Prodest)

INTOSAI Readings

IntoIT Issue 27, December 2008

Assuring SAP (Australia)

IntoIT Issue 28, April 2009

Dutch Experiences with ERP Systems

Country Focus South Africa

19th Meeting of Intosai Working Group for IT Audit (WGITA)

SAP in public administration (Netherlands)

Visits

RMAS (Risk Management & Audit Services) at Harvard

University

ANAO (Australian National Audit Office) – SAP Assure

software

14

Auditing ERP Systems without

specific CAATS

Brazil and IT Audit Secretariat background

Audit opportunities and risks

Survey on ERP systems in the Brazilian

Federal Public Administration

Benchmarking of audit methodologies

Audit methodology

Conclusion

15

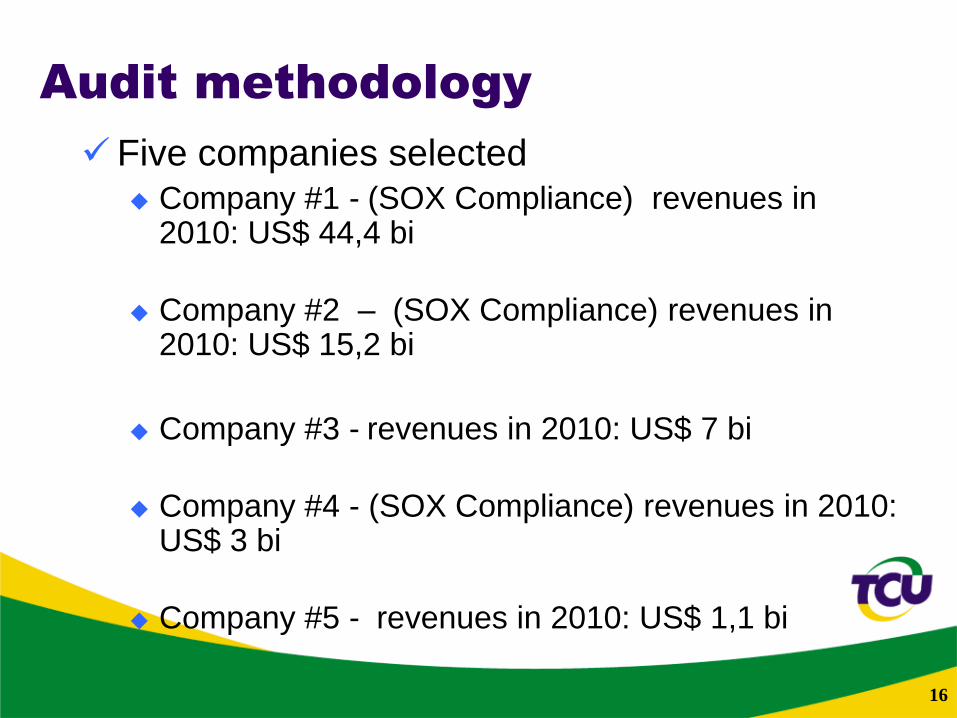

Audit methodology

Five companies selected Company #1 - (SOX Compliance) revenues in

2010: US$ 44,4 bi

Company #2 – (SOX Compliance) revenues in 2010: US$ 15,2 bi

Company #3 - revenues in 2010: US$ 7 bi

Company #4 - (SOX Compliance) revenues in 2010: US$ 3 bi

Company #5 - revenues in 2010: US$ 1,1 bi

16

Audit Scope Focus on evaluation of general controls, due to the

lack of a support tool for evaluating application controls

Use of globally accepted audit criteria (Cobit 4.1, ISO 27.002, ISO 31.000, ISO 15.999) and national legislation

10 audit questions associated to 49 possible findings

Survey with 9,000 users from the selected companies

Audit methodology

17

Dimensions Audit questions

MANAGEMENT OF ERP SYSTEM

AND IT PLANNING

Q1. Is management of the ERP system based on IT plans

and policies?

Q2. Is a cost-benefit analysis of the investments in the ERP

system carried out?

PROCESSES AND METHODS OF

SUPPORT

Q3. Do the professionals who support and use the ERP

system undergo appropriate training and receive

information that is appropriate to carry out their activities?

Q4. Does the IT area count on processes and methods to

support the ERP system?

PERFORMANCE OF THE

INTERNAL AUDIT

Q5. Are the management and use of the ERP system

overseen by internal audit?

CONTRACTS AND LEGAL

ASPECTS

Q6. Do the contracts related to the ERP system meet the

legal provisions?

INFORMATION SECURITY

CONTROLS

Q7. Have the general IT controls associated with the

security of the ERP system been implemented according to

best practices?

Q8. Have the controls of access to the ERP system been

implemented according to best practices?

USER SATISFACTIONQ9. Are users satisfied with the ERP

system?

APPLICATION CONTROLS–

ACQUISITION MODULE

Q10. Have the existing controls in the ERP system for

making public acquisitions been implemented according to

legislation and to best practices?

Findings Q9: User satisfaction

Less than 1 year3%

Between 1 and 3 years

12%

Between 3 and 5 years

29%

More than 5 years56%

Did not respond

0%

Length of time using system

19

Findings Q9: User satisfaction

24%

29%

42%

5%

Distribution of length of time using system

Use the ERP system more than other systems

Use other systems more than ERP system

Use ERP and other systems for almost the same time

Did not respond

20

Findings Q9: User satisfaction

73%

14%

9%

4% 0%

Influence of system use

Increases my productivity

Does not influence my productivity

Decreases my produtivity

I don´t know

Did not respond

21

Findings Q9: User satisfaction

38%

61%

1%

Need to reenter ERP system information in other systems

Yes

No

Did not respond

35%

64%

1%

Need to reenter other systems information in ERP system

Yes

No

Did not respond

22

Findings Q9: User satisfaction

12%

47%

33%

8%0%

General level of satisfaction with system use

Totally satisfiedVery satisfiedPartially satisfiedDissatisfiedDid not respond

The system is not trustworthy

2%

The system is frequently

offline3% The system

does not have the operations I

need11%

The system is slow11%

The system is difficult to use

25%

Other26%

Did not respond22%

Aspects of dissatisfaction with system

23

Auditing ERP Systems without

specific CAATS

Brazil and IT Audit Secretariat background

Audit opportunities and risks

Survey on ERP systems in the Brazilian

Federal Public Administration

Benchmarking of audit methodologies

Audit methodology

Conclusion

24

It is possible to audit ERP systems without the

use of specific CAATs

The steps suggested are:

Carrying out a survey on the status of ERP use in

the country

Benchmarking of audit methodologies

Carrying out survey among users of the systems of

chosen companies

Creating and executing a methodology for

evaluating general controls mainly

Conclusion

25

If the SAI does not have previous experience

or resources to acquire specific CAATs to help

in ERP system audit, it should invest in

knowledge and motivation in order to face the

challenges of a task of such importance

Conclusion

26