auditor general ghana audit service - gas official …ghaudit.org/reports/dvla_singles_cover.pdfthis...

TRANSCRIPT

This report has been prepared under Section 11

of the Audit Service Act, 2000 for presentation

to Parliament in accordance with

Section 20 of the Act.

Richard Quartey

Auditor General

Ghana Audit Service

January 2012

The study team comprised:

Matthew Zigah, Peter Adjedu, Elvis Oware and Mark Nartey

Under the direction of Messrs Ernst and Young.

This report can be found on the Ghana Audit Service

website at www.ghaudit.org

For further information about the

Ghana Audit Service on this report, please contact:

The Director, Communication Unit

Ghana Audit Service

Headquarters

Post Office Box MB 96, Accra.

Tel: 0302 664928/29/20

Fax: 0302 662493/675496

E-mail: [email protected]

Location: Ministries Block ‘O'

© Ghana Audit Service 2012

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING AUTHORITY FOR

THE PERIOD JANUARY 2008 TO DECEMBER 2009

Table of Contents Page

Transmittal letter………………………………………………………………. i - ii

Executive summary…………………………………………………………….. iii - v

Chapter One

1.0 Scope of Audit…………………………………………………………. 1

1.1 Legal mandate…….…………………………………………………... 1

1.2 Methodology ………………..………………………………………… 1

1.3 DVLA’s object and function…………………………………………. 2

1.4 Key personnel………………………………………………………..… 2

Chapter Two

Details of Findings and recommendations

2.0 Failure to prepare procurement plan ….…………………………………… 3

2.1 Payment vouchers were not pre-audited by Internal Audit Unit………….. 4

2.2 Failure to print security documents from mandated source………………... 5

2.3 Contract awarded in excess of lowest evaluated tender price………. 6

2.4 Procurement of goods and works above the Entity Tender Committee

threshold………………………………………………………………….. 7

2.5 Failure to advertise for the procurements of goods and works …….… 8

2.6 Absence of evidence of evaluation panel report …………...………….. 9

2.7 Absence of contract and fixed assets registers………………………... 10

2.8 Entity Tender Committee not properly constituted…………………… 11

2.9 Failure to hold annual board of survey for 2009 ……………………. 12

Appendices

A Checklist of records/documents examined B Sample of procurement done which were not supported by a Procurement Plan

C Tender evaluation report

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

i

Office of the

Auditor-General

Ministries Block “O”

P. O. Box MB 96

Accra

Tel. (0302) 662493

Fax (0302) 662493

January 2012

Dear Madam Speaker,

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON

DRIVER, VEHICLE AND LICENSING AUTHORITY FOR THE PERIOD

JANUARY 2008 TO DECEMBER 2009

I have the honour to submit to you for presentation to Parliament a special audit report

on procurements at the Driver, Vehicle and Licensing Authority (DVLA).

2. The audit was undertaken in accordance with my mandate under Section

187(2) of the Constitution of Ghana and Section 13 of the Audit Service Act which

requires me to carry out special audits or reviews, submitting the reports thereof to

Parliament.

3. We noted significant instances of non-compliance and willful violation of the

Public Procurement Act (PPA) as follows:

Failure to prepare procurement plan;

Awarding contract in excess of the lowest evaluated tender price;

Purchase of goods and works in excess of the Entity Tender Committee’s

threshold; and

Failure to advertise for the procurement of goods and services.

TRANSMITTAL LETTER

Ref. No. AG/01/109/Vol.2/48

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

ii

4. We could therefore not determine whether value was obtained for the

procurement of goods and services detailed elsewhere in the report. I wish to put on

register my displeasure at the failure of DVLA management to respond to the

management letter after several reminders. As a result the report has been issued

without management comments.

5. The audit was undertaken by staff of the Special Audits Unit under the

supervision of Messrs Ernst and Young, Mr. Edward Ayekpley, Director and Mr.

Yaw Sifah, Deputy Auditor-General responsible for Performance and Special Audits

Department.

6. I would like to thank my staff for their assistance in preparing this report and

management and staff of Driver, Vehicle and Licensing Authority for their assistance

and cooperation during the audit.

7. I trust that this report will meet the approval of Parliament.

Yours faithfully,

AUDITOR-GENERAL

Cc: THE RIGHT HON. SPEAKER

OFFICE OF PARLIAMENT

PARLIAMENT HOUSE

ACCRA

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

iii

EXECUTIVE SUMMARY

Introduction

We have audited the procurement and other related records of the Driver, Vehicle and

Licensing Authority (DVLA) Headquarters for the period 1 January 2008 to 31

December 2009. DVLA operates a centralised procurement system whereby goods,

services and works are procured at the headoffice for distribution to its offices

nationwide. The audit was undertaken between June and July 2010.

2. We discussed our findings with key management personnel during the Exit

Conference. We also provided management with a draft management letter for their

formal responses to the findings, in keeping with our procedures as contained in the

Audit Service Act, Section 29. We however did not receive any comments from

management at the time of compiling this report.

Objectives of the Audit

3. The objectives of the audit are to:

determine whether proper procedures were followed by the Authority in its

procurement administration;

ascertain whether activities of the Authority were undertaken in accordance with

its mandate as conferred in the DVLA Act 1999 (Act 569) and any other relevant

legislation, and proper records maintained in respect of its operations;

assess whether rules and procedures applied in its operations are adequate to

safeguard and protect the Authority’s assets and property; and

ensure that procurement activities of the Authority were undertaken within the

limit of budgetary approvals as determined by Parliament.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND

LICENSING AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

iv

Findings

4. Overall, DVLA has kept proper records relating to its procurement management

over the period and also maintained a fairly decent control environment. However

fundamental challenges remained in the area of compliance with the Public Procurement

Act (PPA) and other relevant legislations as depicted by the findings summarised below:

a. DVLA management procured various goods and works in 2008 without

preparing a procurement plan;

b. The Internal Audit Section failed to pre-audit two payment vouchers valued

at GH¢76,096.28;

c. Although the bidding records of F.F Construction Ltd showed that the

company quoted an amount of GH¢297,644 to construct a car park at the

Tema Office, the company was awarded a contract to the tune of

GH¢336,524, an excess of GH¢38,880;

d. The Entity Tender Committee of DVLA recommended for approval by

management goods and works amounting to GH¢1,956,558 in violation of

the threshold set out in the Public Procurement Act;

e. DVLA management failed to apply the National Competitive Tendering

Method in procuring goods and works worth GH¢1,743,546. The method

requires that entities should invite competing bidders through publication in

the National Newspapers;

f. No Evaluation Panel Report on the procurement of goods and services

valued at GH¢1,417,095 was provided;

g. DVLA management did not keep a Contract Register to record the items

purchased and to facilitate the preparation of the financial statement;

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

v

h. The Entity Tender Committee of DVLA was not properly constituted as

stipulated in the Public Procurement Act; and

i. No Board of Survey and stocktaking were held in 2009, thus casting doubts on the

reliability of the stock figures reported in the financial statement.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

1

CHAPTER ONE

INTRODUCTION

1.0 Scope of Audit

1. The audit covered DVLA’s procurement activities at the DVLA Headquarters

during the fiscal years 2008 and 2009. We used procedures which were designed

primarily to ascertain whether the procurement records provide an adequate view of the

procurement activities reported for the years under review. In particular, DVLA’s

systems of internal controls, policies and procedures pertaining to the Authority’s

procurement management and compliance with the Public Procurement Act were

reviewed.

1.1 Legal mandate

2. Our mandate is derived from the powers and functions granted the Auditor-

General under Article 187 of the 1992 Constitution. The audit was also conducted

within the framework of the following legislations:

The Audit Service Act, 2000 (Act 584);

The INTOSAI auditing standards;

The Public Procurement Act, 2003 (Act 663);

The Financial Administration Act,2003 (Act654);

The Financial Administration Regulations, 2004 (LI 1802); and

The Stores Regulations, 1984.

1.2 Methodology

3. Our audit procedures were aimed at understanding DVLA’s procurement

administration which to a large extent was informed by the provisions of the Public

Procurement Act. We also applied audit tools to facilitate our identification of inherent

and control risks the Authority was exposed to, in its procurement administration. We

interviewed key officers involved in DVLA’s procurement administration, including the

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND

LICENSING AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

2

Chief Executive, the Procurement Officer and the Deputy Director of Finance.

Additionally we reviewed various documents listed as Appendix A.

These procedures enabled us to identify weaknesses in DVLA’s procurement

administration.

1.3 DVLA’s objectives and functions

4. The Driver Vehicle Licensing Authority Act, 1999 (Act 569) was passed with the

object of promoting good driving standards in the country; and to ensure the use of road

worthy vehicles on the roads and in other public places. The functions of the DVLA, as

stipulated by its enabling legislation, include the following:

Establishing standards and methods for the training and testing of driving

instructors and drivers of motor vehicles and riders of motor cycles;

Establish standards and methods for the training and testing of vehicle

examiners;

Provide syllabi for driver training and training of instructors;

Issue driving licenses;

Register and license driving schools;

License driving instructors;

Inspect, test and register motor vehicles; and

Issue vehicle registration certificates.

1.4 Key Personnel

6. The following management personnel were at post during the period of audit:

Name Position Period in Service

Mr. Joe Osei Owusu Chief Executive 20/01/2001- June 2008

Mrs. Mable Sagoe Ag. Chief Executive June 2008 - 12/01/2009

Mr. Justice M.Y. Amergashie Chief Executive 13/01/2009 to date

Mr. Mohammed Twumasi Deputy Director Finance 1/11/2005 to date

Mr. Andrew Denteh Accountant 17/10/07 to date

Mr. Eric Thompson Procurement Officer 11/11/2009 to date

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

3

CHAPTER TWO

DETAILS OF FINDINGS AND RECOMMENDATIONS

2.0 Failure to prepare procurement plan for 2008 - GH¢1,886,239.00

6. Section 21, subsections 1 and 2 of the Public Procurement Act, 2003 requires

every procurement entity to prepare a procurement plan to support its approved

programme. The plan shall indicate:

a. Contract packages

b. estimated cost for each package

c. the procurement method, and

d. processing steps and times.

7. Also, a procurement entity shall submit to its Tender Committee not later than one

month to the end of the financial year, the procurement plan for the following year for

approval.

8. Contrary to the above, we noted during the examination of the procurement

processes of the DVLA that the Authority procured goods and services amounting to

GH¢1,886,239.00 in 2008 without preparing a procurement plan as required by the Act.

Details are attached as Appendix B to the report.

9. Failure to prepare a Procurement Plan by management is a violation of the Public

Procurement Act and could lead to misuse of state resources through unplanned

procurement. It may also deprive the Authority from obtaining value for money from its

procurement activities. We could therefore not determine whether actual procurements

undertaken during the year were in line with planned activities for that year.

10. We urged management to always ensure that it prepares a Procurement Plan in

compliance with the Public Procurement Act, 2003.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND

LICENSING AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

4

2.1 Payment vouchers totaling GH¢76,096.28 were not pre-audited by Internal

Audit Unit

11. Internal Audit Agency Act, 2003 (Act 658) Part I, Section 3 (2b & d) states that

“The Agency shall ensure that the financial activities of MDAs and MMDAs are in

compliance with laws, policies, plans, standards and procedures; and that national

resources are used economically, effectively and efficiently’’.

12. Among the duties and functions of the Internal Audit Unit are the pre and post

auditing of payment vouchers and other related records, monitoring of revenue collection

and accounting, expenditure control, analysing the internal control system of the DVLA

and establishing a review programme.

13. A review of the payment process revealed that two payment vouchers totaling

GH¢76,096.28 were not pre-audited by the internal auditor. These payments were in

respect of procurement of works covering the period under review, as shown in Table 1.

Table 1: Payments not pre-audited by the Internal Audit Unit

Date Details Contractor PV. NO. Amount

(GH¢)

27/2/09

Construction of Car

Park - Tema District

Office

F. F. Construction Ltd 65/09 68,857.90

7/11/08

Payment for

construction of fence

wall Tamale

Tamlana Tega Ent. 455/08 7,238.38

Total

76,096.28

14. We could not ascertain the cause of Internal Auditor’s failure to pre-audit the said

payment vouchers. Failure to pre-audit payment vouchers by an internal auditor could

result in over payment to clients, aside of other risks that this omission may engender.

We could therefore not confirm whether the Authority obtained value for money in these

transactions, which is one of the principal objectives underpinning the Public

Procurement Act, 2003 (Act 663).

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

5

15. We recommended that management ensure that all the necessary control

procedures are adhered to before disbursing public funds.

2.2 Failure to print security documents from mandated source - GH¢38,913.75

16. Chapter 4, Section 0404 of the Stores Regulations 1984 states “The following

printed forms shall always be printed by the Ghana Publishing Corporation; no other

printer shall be asked to print these forms: - all forms that require the printing of the

Ghana Coat of Arms on them and all forms of security nature”.

17. We noted that DVLA contracted the printing of Letterheads and Cost Recovery

Receipt Books to Max Associates Ltd and Fiona Press Ltd respectively. These books

which bear the Ghana Coat of Arms, cost the Authority GH¢38,913.75 as shown in

Table 2.

Table 2: Letterheads and Cost Recovery Receipt Books printed from unauthorised

sources

Date Details Contractor Amount GH¢

28/8/08 Printing of Recovery receipt books Fiona Press Ltd

19,923.75

2009

Printing of cost recovery receipt

books and DVLA branded letter

heads

Max Associates

Ltd

18,990.00

Total

38,913.75

18. Management could not provide any explanation for its decision to print these

books from private companies. Failure by management to contract Ghana Publishing

Corporation to print the documents has deprived the state institution of the revenue which

could have accrued from this transaction. It could also result in a breach of the security

considerations envisaged in that regulation.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND

LICENSING AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

6

19. We recommended that management should always contact Ghana Publishing

Corporation (GPC) regarding the printing of documents specified in the regulation.

Where GPC is not in the position to print the said documents, management could then

contract private printing firms to do so after the necessary authorisation had been sought.

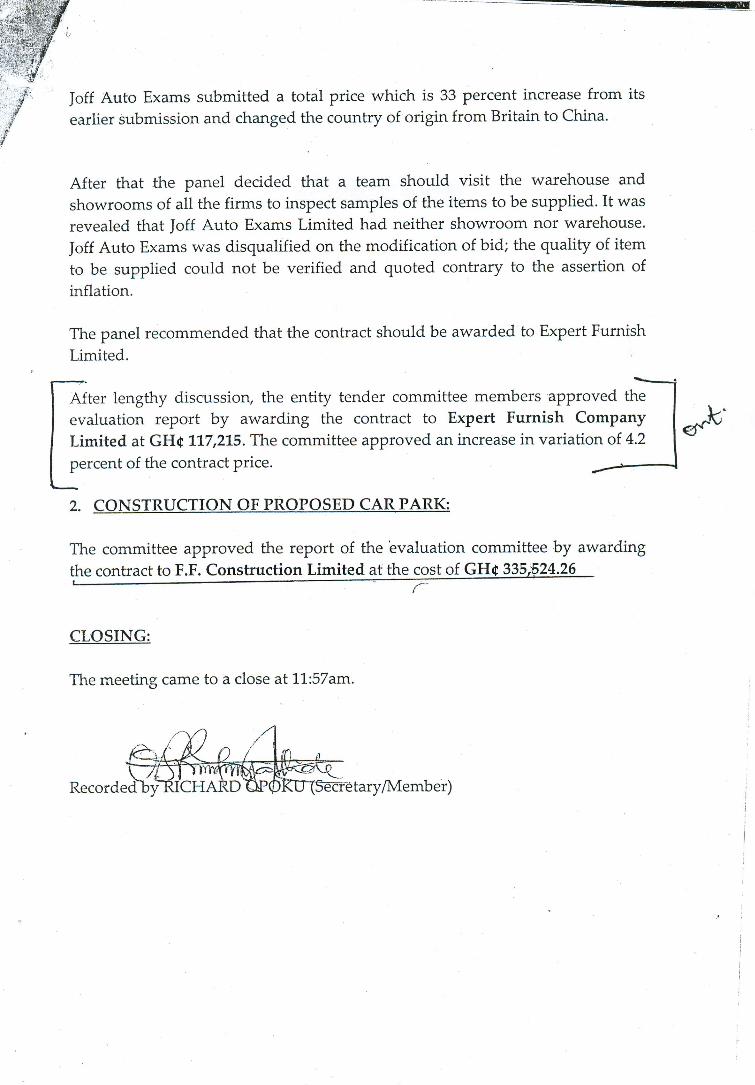

2.3 Contract awarded in excess of lowest evaluated tender price

20. Section 59 (1 and 3a) of the Public Procurement Act, 2003 (Act 663) states “The

procurement entity shall evaluate and compare the tenders that have been accepted in

order to ascertain the successful tender in accordance with the procedures and criteria set

out in the invitation documents; and the successful tender shall be the tender with the

lowest evaluated tender price”.

21. We found that Messrs F. F. Construction Limited in 2008, submitted a bid at a

price of GH¢297,644.00 to construct a car park at the DVLA office in Tema. Upon

evaluation of the bids submitted by various companies, the Evaluation Panel

recommended Messrs F.F. Construction to the Entity Tender Committee as the winner of

the bid with a price of GH¢335, 524.00 as shown in Appendix C.

22. Management could not provide any justification for the decision to pay

GH¢37,880.00 more than what was quoted by the contractor in the bidding document. It

was apparent that members of both the Evaluation Panel and the Entity Tender

Committee failed to exercise due dillegence in the performance of their duties.

23. We urged management to investigate and provide my office with payment

vouchers covering the total payment made to the contractor. Where it is confirmed that

payment has been made to the company in excess of the GH¢297,644.00 quoted, the

difference should be retrieved from the company. Members of the Evaluation Panel and

the Entity Tender Committee should be made to pay the amount if management is unable

to retrieve same from the company.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

7

2.4 Procurement of goods and works above the Entity Tender Committee

threshold - GH¢1,956,558.00

24. According to Schedule 3 subsection 3 (B1) of the Public Procurement Act, 2003

(Act 663) the threshold for approval by Entity Tender Committees for goods is between

the range GH¢5,000.00 - GH¢10,000.00 while for works is between GH¢10,000.00 -

GH¢200,000.00.

25. We found that the Entity Tender Committee of DVLA approved five contracts for

the procurement of various goods and works amounting to GH¢1,956,558.00 in 2008.

Our review further disclosed that each of the contracts approved exceeded the Entity

Tender Committee’s approved threshold as detailed in Table 3.

Table 3: Procurement of goods and works approved by the Entity Tender

Committee above its threshold

Year Details Contractor Amount GH¢

2008 Supply of office furniture to DVLA offices Expert furnish Ltd 117,215.00

2008 Supply of Computers and Accessories Engineering Systems and

Service Ltd 865,730.29

2008 Supply of Biometrics Engineering Systems and

Service Ltd 228,438.80

2008 Construction of Car Park - Tema office F. F Construction Ltd

335,524.00

2008 Renovation of Head office 2 story Building

and associated work at switchbackroad Accra

Ciddam Construction Ltd

409,649.91

Total

1,956,558.00

26. Management could not explain why The Entity Tender Committee failed to apply

the law as stipulated in Section 17 (2c) of the PPA. The Entity Tender Committee acted

beyond its powers and any aggrieved competitor who took part in the bidding process

could seek remedial action against the Authority under Sections 78 - 80 of the PPA. This

could result in adverse financial consequences to the Authority.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND

LICENSING AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

8

27. We recommended that the Entity Tender Committee should strictly follow laid

down laws and regulations on procurement as stipulated in the Public Procurement Act,

2003 (Act 663) and other relevant legislations.

2.5 Failure to advertise for the procurements of goods and works–

GH¢1,743,546.60

28. Schedule 3 subsection 1 (3a &b) of the Public Procurement Act, 2003 (Act 663)

requires that “Entities procuring goods between GH¢20,000.00 and GH¢200,000.00, and

works between GH¢50,000.00 and GH¢1,500,000.00 shall use the national competitive

tendering method”.

29. We noted however that, DVLA management did not advertise for the procurement

of goods and works amounting to GH¢1,743,546.60 in any of the national newspapers or

the public procurement bulletin. See Table 4.

Table 4: Procurement of goods and works not advertised

Date Details Contractor Amount GH¢

2008 Supply of office stationery to DVLA Head

office Snow flower Enterprise

83,617.00

2008 Renovation of Head office 2 storey building and

associated works at switchbackroad Accra

Ciddam Construction Ltd 409,649.91

2008 Supply of office furniture to DVLA Office Expert Furnish Ltd 117,215.00

2008 Supply of computers and accessories/ General

Hardware

Engineering Systems and

Services

865,730.29

2008 Supply of Biometrics

Enigneering Systems and

Services

228,438.80

2008 Construction of fence wall at Tamale Office M/S Tamlana Tega Ent. 38,895.60

Total

1,743,546.60

30. Failure by management to comply with the law could result in procuring goods

and services at non-competitive prices with sub-standard quality and may impair the

value for money objective of the Public Procurement Act.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

9

31. We recommended that management should always advertise procurements above

its threshold in a widely circulated newspaper.

2.6 Absence of evidence of evaluation panel report - GH¢1,417,095.20

32. Article 59 (1) of the Public Procurement Act, 2003 (Act 663) states: “The

procurement entity shall evaluate and compare the tenders that have been accepted in

order to ascertain the successful tender in accordance with the procedures and criteria set

out in the invitation documents”.

33. We have examined the contracts listed in Table 5, covering the procurement of the

goods and works which were awarded in 2008 and noted however that there was no

report by the Evaluation Panel as the basis for awarding the four contracts listed, totaling

GH¢1,417,095.20.

Table 5: Procurement not supported by Evaluation Panel Reports

Year Details Contractor

Amount

(GH¢)

2008

Renovation of Head office 2 storey

building & associated works on switchback

road Accra

Ciddam Construction Ltd

409,649.91

2008

Supply of office furniture to DVLA office

Expert Furnished Ltd

117,215.00

2008

Supply of computers & accessories /

General Hardware

Engineering Systems and

Services

865,730.29

2009

Supply and installation of computers and

accessories

Kensington Information Ltd

24,500.00

Total

1,417,095.20

34. Management indicated that the evaluation was done but could not produce the

report for our examination. This situation in our view depicted poor record keeping by

those in charge as well as lack of effective supervision by management.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND

LICENSING AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

10

35. We urged management to retrieve the evaluation reports on the contracts for audit

verification.

2.7 Absence of contract and fixed assets registers

36. Section 1 (1a) of the Financial Administration Regulation, 2004 (L.I 2004) states

“Any public officer who is responsible for the conduct of financial business on behalf of

the Government of Ghana shall keep proper records of all transactions and shall produce

records of the transactions for inspection when called upon to do so by the Minister, the

Auditor-General or any officers authorised by them”.

37. We noted that management of DVLA did not keep Contract and Fixed Assets

Register to record all transactions pertaining to a particular contract and asset

respectively. A contract register would assist management to keep track of all contracts as

regards the stage of execution and payment details. Also, a Fixed Assets Register would

record all fixed assets procured and provide details of special identification numbers, cost

of the asset, depreciation, location, etc. The lapse, we noted, was due to lack of effective

supervision on the part of management.

38. The Internal Auditor indicated that a Fixed Asset Register existed but management

could not make it available to us when we requested for it. As a result of the failure to

keep the above records, we could not ascertain the state of assets owned by the DVLA

and also determine the Authority’s outstanding liabilities, if any, in respect of

procurements made during the audit period. Cumulatively, these lapses would affect the

reliability of the balance sheet produced by DVLA management.

39. We urged management to focus particular attention on record keeping in the

administration and disbursement of Government of Ghana funds.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND LICENSING

AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

11

2.8 Entity Tender Committee not properly constituted

40. Schedule 1 section 17 subsection 1 (1-3) of the Public Procurement Act, 2003 (Act

663) provides details of the composition of Tender Committee for Central Management

Agency/Ministry or Subvented Agency as follows:

head of Agency;

head of finance or accounts division;

a representative of the Ministry of Justice not below Chief State Attorney;

three other heads of divisions or department one of whom represents a user

department;

two members of Parliament from the region, one appointed by the Minister and

the other chosen by the Regional Caucus of Members of Parliament; and

the secretary shall be the officer heading the procurement unit.

41. From a review of documents made available to us by management, we found that

the requirement for two members of Parliament to be on the committee was not adhered

to. We instead noted that two Deputy Directors of Management Information System and

Administration were appointed to serve on the Entity Tender Committee. We could not

ascertain the basis for the inclusion of the two officers on the committee.

42. The failure to comply with the law means that the input of the two members of

Parliament as envisaged under the PPA would not be realised. Whilst recognising the

practical difficulties that could arise in having members of Parliament participate

regularly at the committee’s sittings, we could not encourage the violation of the law. We

therefore urge management to comply with the law.

PROCUREMENT AUDIT REPORT OF THE AUDITOR-GENERAL ON DRIVER, VEHICLE AND

LICENSING AUTHORITY FOR THE PERIOD JANUARY 2008 TO DECEMBER 2009

12

2.9 Failure to hold annual board of survey for 2009

43. No Board of Survey on stores and obsolete items was held after the close of

business at the end of the 2009 financial year. Board of survey is necessary for

independent confirmation of stores balances and obsolete items.

The annual stocktaking also ensures that the records reflect the true stock and asset

position, which is essential for planning and stock control purposes.

44. Failure to hold annual Board of survey contravened chapter 11, section 1103 and

chapter 12, section 1202 of the Stores Regulation, 1984. This situation could result in

loss in value of assets and stock. Also, unserviceable items, abandoned, unused and

obsolete items might not be discovered timely which could lead to further deterioration

and loss in value.

45. We recommended that annual Board of Survey and stock taking of both stores and

assets be held at the close of business at the end of each financial year.

Appendix A

Checklist of records/documents examined

Serial Record/document

1

Procurement Plan for 2009

2

Bid Evaluation Reports File

3

Contract Awards Letters File

4

Payment vouchers

5

Contract document

6

Minutes of Tender Evaluation Committee

7

Annual budget for 2008 & 2009

8

Advertised projects file

9

DVLA Act, 1999 (Act 569)

10

Bank statements

Appendix B

Sample of procurement done which were not supported by a Procurement Plan

Year Details Contractor Amount GH₵

2008

Contract for the supply of Biometrics Engineering Systems and

Services Limited 228,438.80

2008

Construction of Tema District Office

Car Park

F.F. Construction Limited

335,524.26

2008

Procurement of Office Furniture to

DVLA Offices

Expert Furnish Limited

117,215.00

2008

Contract for Renovation of Head

Office at Cantonment

Ciddam Construction

Limited 409,649.91

2008 Supply of Office Furniture N/A 85,459.00

2008

Supply and Installation of Wide Area

Network

Dealer Computers

465,389.14

2008

Supply of Office Furniture N/A

20,180.00

2008

Supply of General Goods (a)

Florescent Tubes 4ft and fitting (b)

Reflective Jackets

Snowflower Enterprise

14,685.00

2008

Contract for the printing of standard

operating procedures and others

Samjaco Trading

Enterprise 15,798.40

2008

Contract for the printing of Cost

Recovery Receipt Books

Fiona Press Limited

19923.75

2008

Contract for the printing of DVLA

branded File Covers

Little Sky Press

17,925.00

2008

Extension of Cleaning Services at

Kumasi Office

N/A

1,933.14

2008

Contract for the Construction of

Fence Wall at Tamale Office

M/S Tamlana Tega

Enterprise 38,895.60

2008

Contract for the supply of Office

Stationery

Snowflower Enterprise

83,617.00

2008

Contract for the Renovation of Wa

Office Building and Bungalow

Ya-Hamid Enterprise

31,605.00

TOTAL 1,886,239.00

Mission Statement The Ghana Audit Service exists

To promote

· good governance in the areas of transparency,

accountability and probity in the public financial

management system of Ghana

By auditing

· to recognized international auditing standards the

management of public resources

And

· reporting to Parliament

Cover Designed and Printed by The Advent PressTel: + 233 (0) 302 781044/777861Email: [email protected]