auditor update healthcare financial management association september 23, 2004 alderbrook resort,...

TRANSCRIPT

AuditorAuditor UpdateUpdate

Healthcare Financial Healthcare Financial Management AssociationManagement AssociationSeptember 23, 2004September 23, 2004

Alderbrook Resort, Union, WashingtonAlderbrook Resort, Union, Washington

Ivan D. Dansereau, CPA QA Director

Kelly Collins, CPA Audit Manager

OverviewOverview

GAGAS Independence Standard Audit Approach Common Audit Problems & Frauds and

How to Avoid Them Thoughts for the Future

Financial Fraud & Accounting FailuresFinancial Fraud & Accounting Failures Dot.Com – Gone

By July 2001: 367 internet companies out of business, and 83,000 employees laid off

Enron: SPEs used in variety of ways to inflate revenues and disguise liabilities Oct. 2001: $500 mm accounting loss and $1.2 billion

reduction in shareholder equity By Aug. 2002: $63 billion loss of market value

Bursting of Telecom Bubble Between Jan-July 2002: at least 112 companies

required to restate prior earnings Decline of market value from peak by $2.5 TRILLION

The Story Gets Worse….The Story Gets Worse….

Global Crossing From $48 billion market cap to January 2002 bankruptcy

and $12.4 billion in debt Adelphia Communications

March 2002: $2.7 billion of hidden debt June 2002: Overstated cash flows by another $500 mm

WorldCom July 2002: overstated prior earnings by $3.85 billion

Qwest Communication July 2002: improperly booked $1.16 billion as profits

instead of capital investments

……And Worse….And Worse…. Tyco

Criminal indictments ImClone

Insider trading General Electric

Undisclosed post-retirement benefits Xerox Corporation

Misbooked revenue and overstated pretax income Lucent Technologies

Premature booking of $679 mm in revenue Kmart

$1.7 billion underreported losses Merck & Co.

$12.4 billion inflated earnings Mirant Corporation

$1.1 billion inflated assets

Public Confidence ErodesPublic Confidence Erodes

The American Survey, July 2002

There are bad, but probably isolated instances, 16%

Many other companies

will be exposed,

38%

Every company does this

kind of thing, but only a

few more will get caught,

46%

Public Confidence ErodesPublic Confidence ErodesDo Top Executives Act Improperly to Benefit Themselves, at the Expense of Shareholders?

Very41%

Somewhat38%Never

1%

Occasionally20%

Sarbanes-Oxley: Sarbanes-Oxley: Seeking a Calm After the StormSeeking a Calm After the Storm

Corporate Conduct Audit Committees

Hire/fire/compensate/direct the work of the independent auditor “Independent” directors (Section 301)

CEO & CFO Certify Reports (Section 302) Management Assessment of Internal Controls (Section 404) Enhanced Financial Disclosures

Independence of Auditor Restrictions on non-audit services Enhanced communication with Audit Committee

Creation of Public Company Accounting Oversight Board

States Consider Adopting SOXStates Consider Adopting SOX In 2003, 14 states proposed legislation related to

incorporating all or some of the provisions of SOX. In 2004, 6 states proposed such legislation. Washington state now requires:

Work papers be kept for a period of seven years, Makes altering, destroying, shredding, mutilating or concealing a

record a class B felony or punishable by fine of not more than $500,000 or both,

Board of Accountancy has power to fine CPAs up to $30,000 for dishonesty, fraud, negligence or violation of professional conduct.

Several states have either enacted or continue to press for corporate governance statutes affecting privately-owned business and not-for-profits to establish audit committees with protocols similar to SOX

Government Environment In Government Environment In Washington StateWashington State

Open government laws, such as:

Open Public Meetings Act Public Records Retention Bid Laws

Media Scrutiny

No Profit Motive

Washington State Auditor’s Office

GAO Independence StandardGAO Independence Standard

Auditors should not perform management functions or make management decisions

Auditors should not audit their own work or provide non-audit services in situations where the amounts or services involved are significant/material to the subject matter of the audit

Compliance with GAO Compliance with GAO Independence StandardIndependence Standard

SAO policies require our auditors to:

Review the documentation that CPAs prepare in support of financial statement audits of state and local governments to determine whether professional standards and SAO audit quality expectations are met.

Evaluate the professional reputation of CPAs and obtain representations that CPAs are independent in accordance with Generally Accepted Government Auditing Standards (GAGAS).

State Auditor’s OfficeState Auditor’s OfficeAudit ApproachAudit Approach

Provide four weeks notice prior to conducting audit.

Perform preplanning activities Entrance conference Perform audit work Exit conference Issue audit report

Audit ScopeAudit Scope

Accountability and Legal Compliance Review of applicable state and local laws and areas of

identified high risk.

Federal Single Audit Testing Beginning fiscal year 2004, must expend more then

$500,000 in federal funds to qualify for a single audit.

Financial Statements Includes evaluation and tests on internal controls over

central accounting systems as well as substantive test of material accounts.

Accountability and Legal Accountability and Legal ComplianceCompliance

Billings and accounts receivable Payroll Disbursements/purchases Contracts and agreements Equipment and inventory Bid requirements

Audit ResultsAudit Results Total Exit Mgmt

Category Issues Items Letters Findings Cash receipting 27 22 5 0 Disbursements 27 26 1 0 Equipment/Inventory 10 9 1 0 Contracts 9 3 4 2 Billings/receivables 8 6 1 1 Payroll 6 5 1 0 OPMA 6 5 0 1 Financial/reporting 6 4 2 0 Budget/deficit 5 1 4 0 Bid Laws 4 2 1 1 Conflict of interest 1 0 1 0 Investments 1 0 0 1 Gift of Public Funds 1 0 1 0

Most Common Areas of AbuseMost Common Areas of Abuse

No. LossType of Fraud Cases Amount %

Unlawful investment 1 $432,000 86.2 Personal use of services 3 44,762

9.0 Payroll 3 21,540 4.3 Cash receipts 5 2,754 0.5 Equipment/inventory 1 100

0.0Total 13 $ 501,156 100.0

== ======== = ====

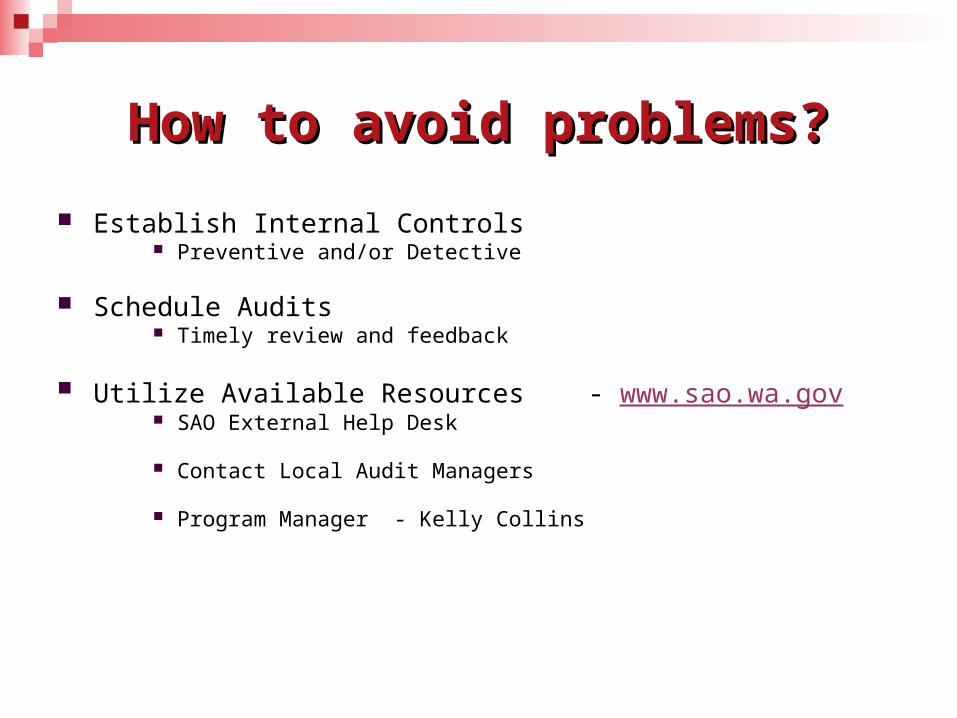

How to avoid problems?How to avoid problems?

Establish Internal Controls Preventive and/or Detective

Schedule Audits Timely review and feedback

Utilize Available Resources - www.sao.wa.gov SAO External Help Desk

Contact Local Audit Managers

Program Manager - Kelly Collins

What to expect in future audits ...What to expect in future audits ...

We will review: Proshare Funds

Vendor payments

Financial Condition Indications of going concern

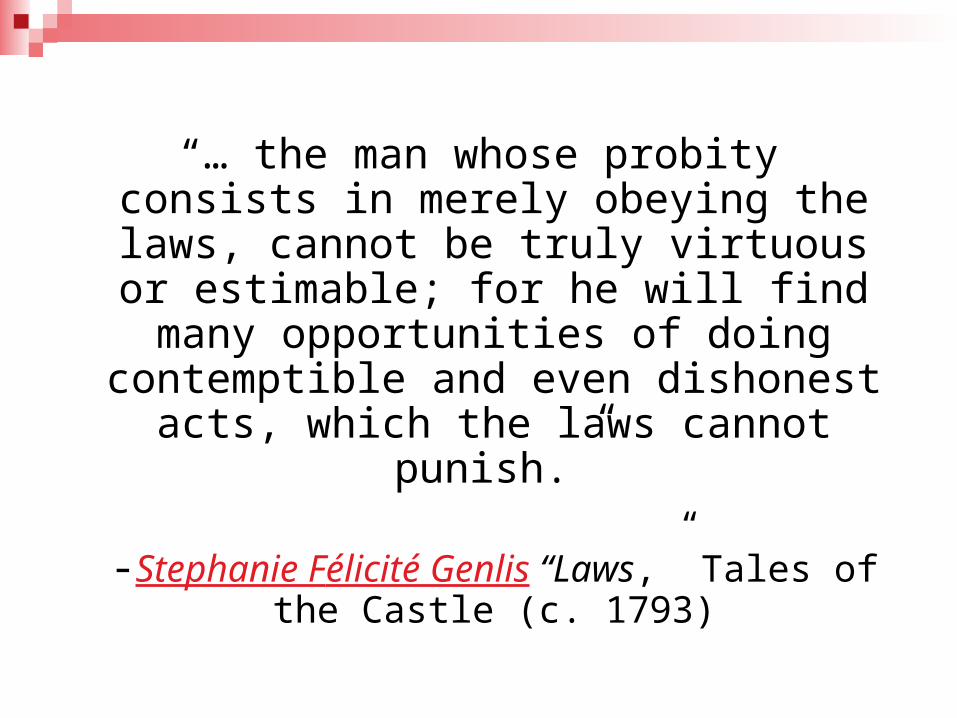

“… the man whose probity consists in merely obeying the laws, cannot be truly virtuous or estimable; for he will

find many opportunities of doing contemptible and even dishonest

acts, which the laws cannot punish.”

-Stephanie Félicité Genlis “Laws,” Tales of the Castle (c. 1793)

Washington State Auditor’s OfficeWashington State Auditor’s Office

Ivan D. Dansereau, CPADirector of Quality Assurance

Kelly Collins, CPAAudit Manager360-725-5376