august 20, 2013 agenda packet

TRANSCRIPT

City Council Agenda Page 1 of 5 August 20, 2013

NOTICE OF A PUBLIC MEETING

AN AGENDA OF A REGULAR MEETING OF THE CITY COUNCIL THE CITY OF SAN ANGELO, TEXAS

9:00 A.M. - Tuesday, August 20, 2013 McNease Convention Center, South Meeting Room

500 Rio Concho Drive San Angelo, TX 76903

THE MCNEASE CONVENTION CENTER IS ACCESSIBLE TO PERSONS WITH DISABILITIES. ACCESSIBLE ENTRIES AND SPECIALLY MARKED PARKING SPACES ARE AVAILABLE AT BOTH MAIN ENTRANCES AT SURBER DRIVE AND RIO CONCHO DRIVE. IF ADDITIONAL ASSISTANCE IS NEEDED TO OBSERVE OR COMMENT, PLEASE NOTIFY THE OFFICE OF THE CITY CLERK, ROOM 210, CITY HALL, 657-4405, AT LEAST 24 HOURS PRIOR TO THE MEETING. City Council meetings are broadcast on Channel 17-Government Access at 10:30 A.M. and 7:00 P.M. every day for two weeks beginning on the Thursday after each meeting.

As a courtesy to those in attendance, please place your cell phone on “Silent” or “Vibrate” Thank You!

I. OPEN SESSION (9:00 A.M.)

A. Call to Order

B. Prayer and Pledge

"Honor the Texas flag; I pledge allegiance to thee, Texas, one state under God, one and indivisible.”

C. Proclamation

“West Texas Lighthouse for the Blind”, Tuesday, August 27, 2013, to be accepted by Dave Wells, Executive Director

D. Recognitions

2013 State Games of America participant Seth Demere, San Angelo Recreation Track Club, Wins 16U Pole Vault in Hershey, Pennsylvania competition

2013 Corpus Christi Games of Texas Participants: Bailey Kinney, Broke the State 800 Meter Record 12U 2012, and places 2nd in 14U 800 Meter Run; Zac Cabrera, 2nd place in the 16U 1600 Meter Run; Jessica Simon, 2nd 14U 800 Meter & 1600 Meter Run; and Hagen Stoute, 3rd Place in 16U Pole Vault

E. Public Comment

The Council takes public comment on all items in the Regular Agenda. Public input on a Regular Agenda item will be taken at its appropriate discussion. Public input on an item not on the Agenda or Consent Agenda may be identified and requested for consideration by the Council at this time. The Council may request an item to be placed on a future agenda, or for a Consent Agenda item, to be moved to the Regular Agenda for public comment.

On public hearing items, public input will be received on each item immediately following the Council discussion and prior to any action on the item. Each member of the public should make their remarks from the podium and begin by stating their name. Remarks by each citizen will be limited to three to five minutes, unless waived by a council member for all speaking on that matter. No individual will be allowed to speak more than once on any one subject until every citizen wishing to comment has done so.

City Council Agenda Page 2 of 5 August 20, 2013

II. CONSENT AGENDA 1. Consideration of approving the August 6, 2013 City Council Regular meeting minutes 2. Consideration of authorizing the City Manger to execute on behalf of the City a Concession

Agreement and all related documents with Wayne Burton d/b/a Hertz Rent A Car for a non-exclusive license to operate an automobile rental service at the San Angelo Regional Airport-Mathis Field (submitted by Airport Director Luis Elguezabal)

3. Consideration of adopting Resolution amending authorized representatives for Texpool, an Investment Service for Public Funds (submitted by Chief Accountant Jaime Guerrero)

4. Consideration of approving Special Recreational Lease Agreement for 0.117 acres of land (Bell) located adjacent to the lake or river and authorizing the City Manager or Water Utilities Director to execute the same (submitted by Water Utilities Director Ricky Dickson)

5. Consideration of adopting a Resolution authorizing the city manager to execute an acceptance, on behalf of the City of San Angelo, Texas, of a special dedication deed, the Howard College at San Angelo Foundation, Grantor, relating to certain real property being 0.26 acre tract of land located in the City of San Angelo, Tom Green County, Texas, at or about Smith Boulevard in northeast San Angelo, for purposes of grantor constructing and dedicating a public motor vehicle access and turn around to the Howard College campus necessary for grantor’s further development of adjacent campus property; and, finding a public purpose and benefit therein (submitted by Interim Director of Development Services AJ Fawver)

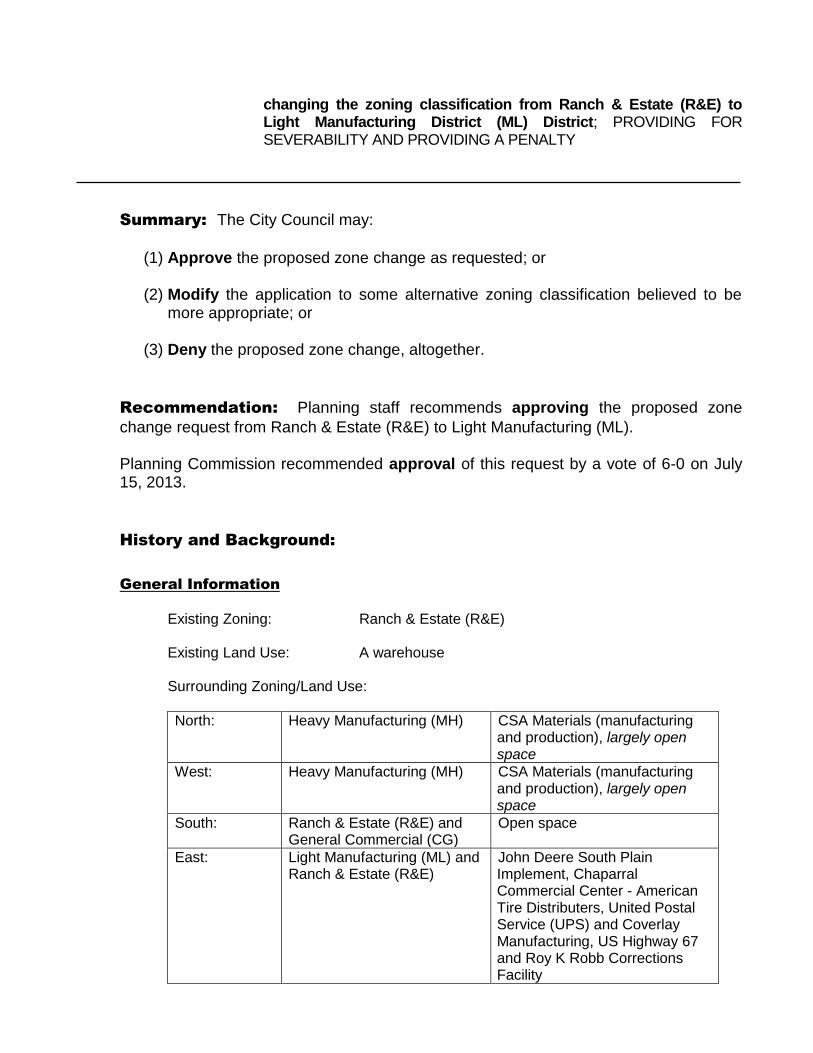

6. Second Hearing and consideration of adopting an Ordinance amending Chapter 12, Exhibit “A” (Zoning Ordinance) of the Code of Ordinances, City of San Angelo (Presentation by Interim Senior Planner Jeff Hintz) Z13-23: Earl and Michelle Weber AN ORDINANCE AMENDING CHAPTER 12, EXHIBIT “A” OF THE CODE OF ORDINANCES, CITY OF SAN ANGELO, TEXAS, WHICH SAID EXHIBIT “A” OF CHAPTER 12 ADOPTS ZONING REGULATIONS, USE DISTRICTS AND A ZONING MAP, IN ACCORDANCE WITH A COMPREHENSIVE PLAN, BY CHANGING THE ZONING AND CLASSIFICATION OF THE FOLLOWING PROPERTY, TO WIT: 3862 Tractor Trail, located at the northwest corner of the intersection of Tractor Trail and Porter Henderson Drive. This property specifically occupies the Paul Gregory Addition, Section 2, 5.33 acres of Tract J & 0.310 acres in Smith Boulevard, in northeast San Angelo, changing the zoning classification from Ranch & Estate (R&E) to Light Manufacturing District (ML) District; PROVIDING FOR SEVERABILITY AND PROVIDING A PENALTY

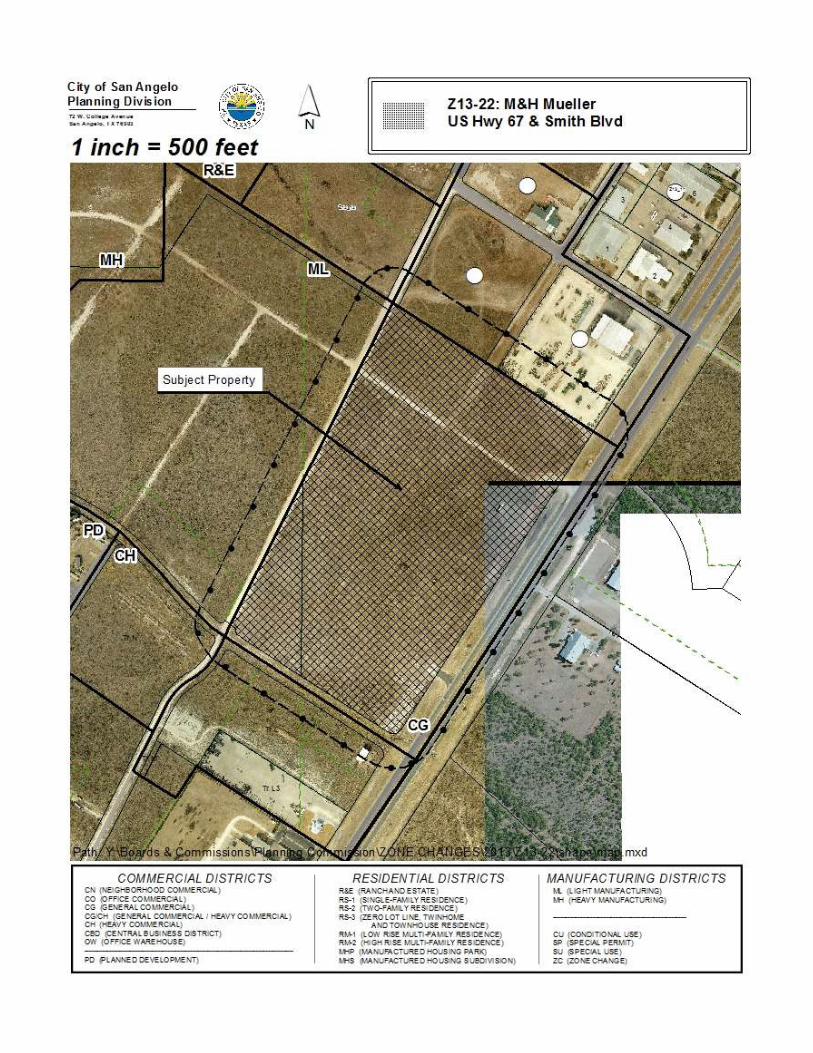

7. Second Hearing and consideration of adopting an Ordinance amending Chapter 12, Exhibit “A” (Zoning Ordinance) of the Code of Ordinances, City of San Angelo (submitted by Interim Senior Planner Jeff Hintz) Z 13-22: M&H Mueller AN ORDINANCE AMENDING CHAPTER 12, EXHIBIT “A” OF THE CODE OF ORDINANCES, CITY OF SAN ANGELO, TEXAS, WHICH SAID EXHIBIT “A” OF CHAPTER 12 ADOPTS ZONING REGULATIONS, USE DISTRICTS AND A ZONING MAP, IN ACCORDANCE WITH A COMPREHENSIVE PLAN, BY CHANGING THE ZONING AND CLASSIFICATION OF THE FOLLOWING PROPERTY, TO WIT: 3172 McGill Boulevard & 3733 North US Highway 67, collectively occupying both a 5.131 acre tract and a 55.1830 acre tract located west of North US Highway 67, north of Paulann Boulevard and east of Smith Boulevard; more specifically occupying 5.131 acres of the J. Pointevent Survey 1113, Abstract 4873, and 55.1830 acres of the J. Fenner Survey 0001, Abstract 4985, in northeast San Angelo, changing the zoning classification from a General Commercial (CG) to a Light Manufacturing (ML) District; PROVIDING FOR SEVERABILITY AND PROVIDING A PENALTY

City Council Agenda Page 3 of 5 August 20, 2013

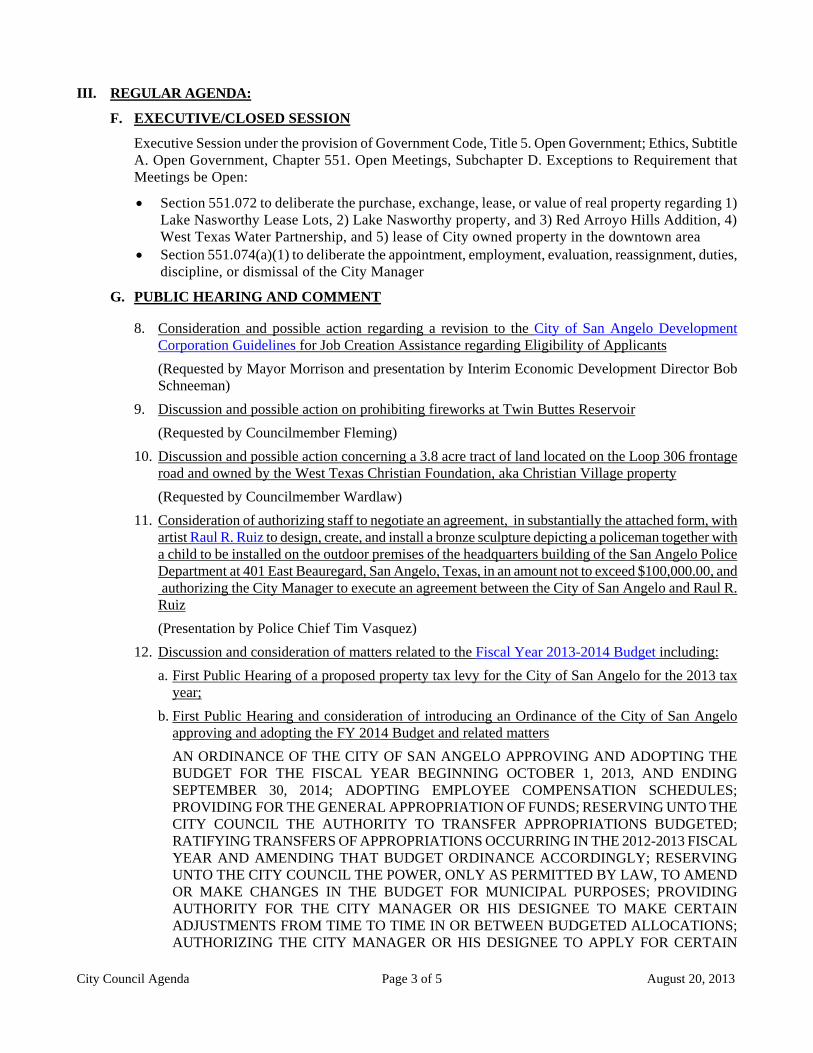

III. REGULAR AGENDA:

F. EXECUTIVE/CLOSED SESSION

Executive Session under the provision of Government Code, Title 5. Open Government; Ethics, Subtitle A. Open Government, Chapter 551. Open Meetings, Subchapter D. Exceptions to Requirement that Meetings be Open:

• Section 551.072 to deliberate the purchase, exchange, lease, or value of real property regarding 1) Lake Nasworthy Lease Lots, 2) Lake Nasworthy property, and 3) Red Arroyo Hills Addition, 4) West Texas Water Partnership, and 5) lease of City owned property in the downtown area

• Section 551.074(a)(1) to deliberate the appointment, employment, evaluation, reassignment, duties, discipline, or dismissal of the City Manager

G. PUBLIC HEARING AND COMMENT

8. Consideration and possible action regarding a revision to the City of San Angelo Development Corporation Guidelines for Job Creation Assistance regarding Eligibility of Applicants (Requested by Mayor Morrison and presentation by Interim Economic Development Director Bob Schneeman)

9. Discussion and possible action on prohibiting fireworks at Twin Buttes Reservoir (Requested by Councilmember Fleming)

10. Discussion and possible action concerning a 3.8 acre tract of land located on the Loop 306 frontage road and owned by the West Texas Christian Foundation, aka Christian Village property (Requested by Councilmember Wardlaw)

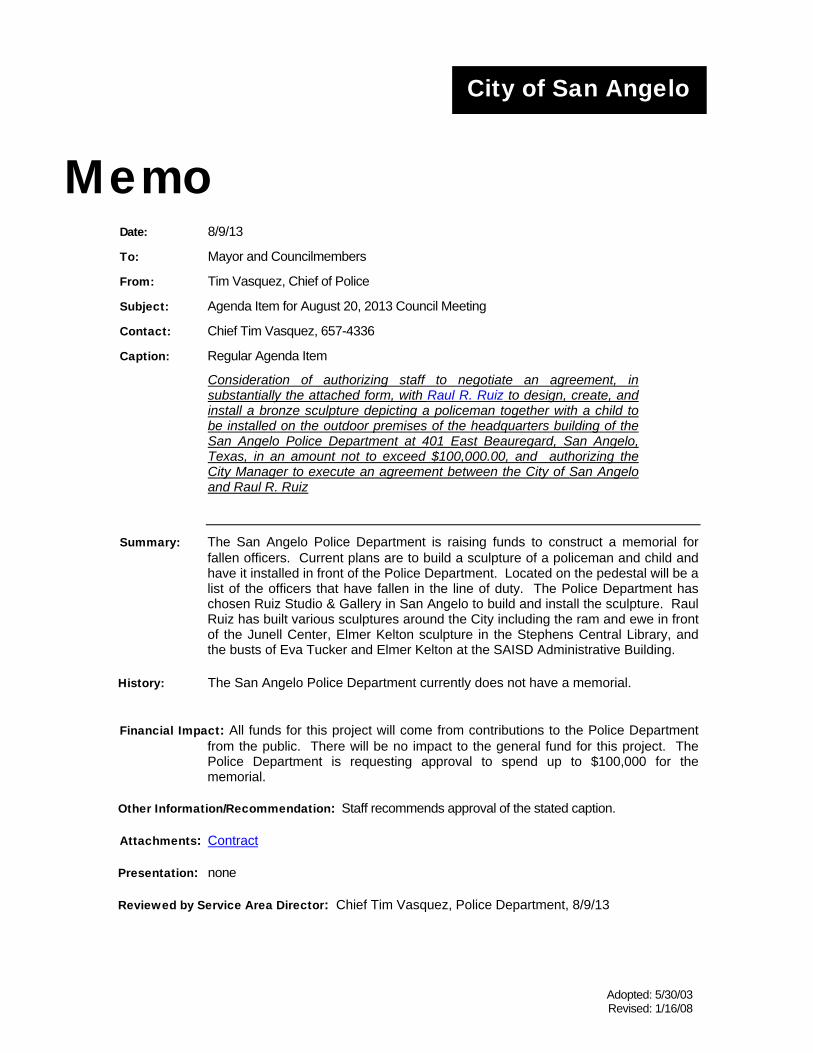

11. Consideration of authorizing staff to negotiate an agreement, in substantially the attached form, with artist Raul R. Ruiz to design, create, and install a bronze sculpture depicting a policeman together with a child to be installed on the outdoor premises of the headquarters building of the San Angelo Police Department at 401 East Beauregard, San Angelo, Texas, in an amount not to exceed $100,000.00, and authorizing the City Manager to execute an agreement between the City of San Angelo and Raul R. Ruiz (Presentation by Police Chief Tim Vasquez)

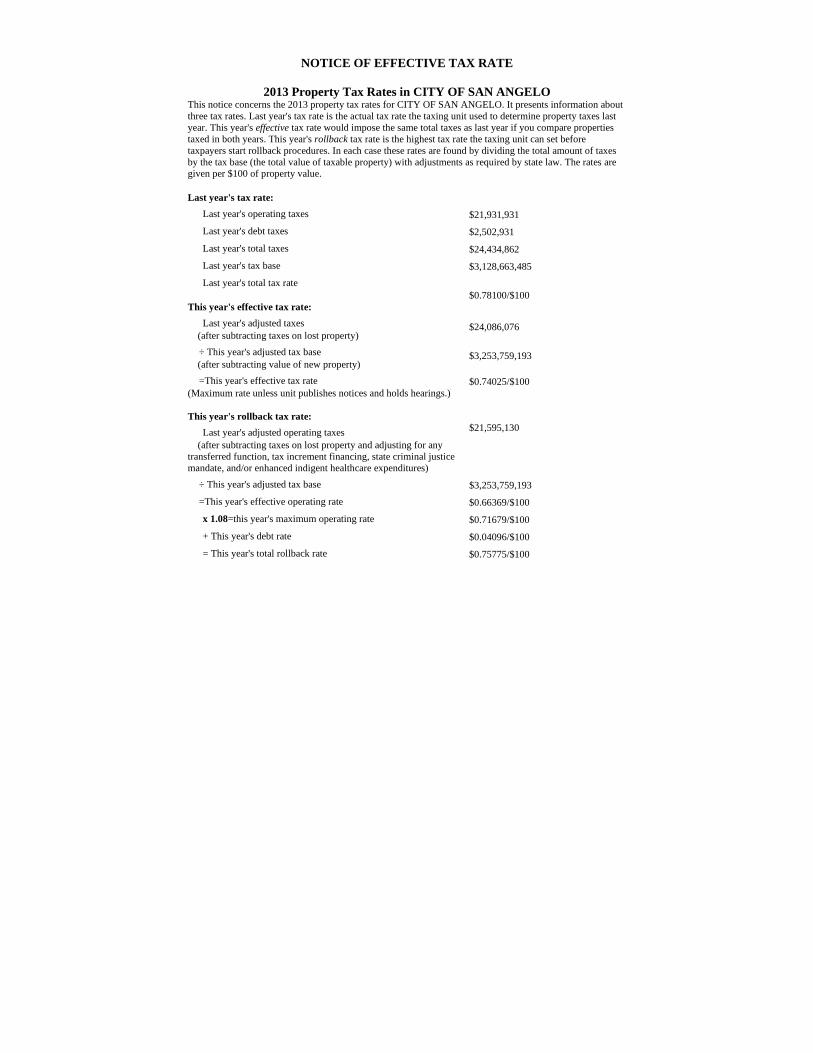

12. Discussion and consideration of matters related to the Fiscal Year 2013-2014 Budget including: a. First Public Hearing of a proposed property tax levy for the City of San Angelo for the 2013 tax

year; b. First Public Hearing and consideration of introducing an Ordinance of the City of San Angelo

approving and adopting the FY 2014 Budget and related matters AN ORDINANCE OF THE CITY OF SAN ANGELO APPROVING AND ADOPTING THE BUDGET FOR THE FISCAL YEAR BEGINNING OCTOBER 1, 2013, AND ENDING SEPTEMBER 30, 2014; ADOPTING EMPLOYEE COMPENSATION SCHEDULES; PROVIDING FOR THE GENERAL APPROPRIATION OF FUNDS; RESERVING UNTO THE CITY COUNCIL THE AUTHORITY TO TRANSFER APPROPRIATIONS BUDGETED; RATIFYING TRANSFERS OF APPROPRIATIONS OCCURRING IN THE 2012-2013 FISCAL YEAR AND AMENDING THAT BUDGET ORDINANCE ACCORDINGLY; RESERVING UNTO THE CITY COUNCIL THE POWER, ONLY AS PERMITTED BY LAW, TO AMEND OR MAKE CHANGES IN THE BUDGET FOR MUNICIPAL PURPOSES; PROVIDING AUTHORITY FOR THE CITY MANAGER OR HIS DESIGNEE TO MAKE CERTAIN ADJUSTMENTS FROM TIME TO TIME IN OR BETWEEN BUDGETED ALLOCATIONS; AUTHORIZING THE CITY MANAGER OR HIS DESIGNEE TO APPLY FOR CERTAIN

City Council Agenda Page 4 of 5 August 20, 2013

GRANTS AND EXECUTE ANY RELATED DOCUMENTS; AND, PROVIDING FOR FILING OF THE BUDGET

c. Consideration of conducting a separate record vote to ratify the property tax increase of 2.52% as reflected in the newly adopted budget and place the adoption of this tax rate increase on the agenda for the September 3, 2013 regular meeting of the City Council as an action item, and any action in connection thereto

(Presentation by Budget Manager Morgan Chegwidden) 13. Consideration of prioritizing additional improvements to the River Project with remaining dedicated

funds for the project (Presentation by Parks and Recreation Director Carl White)

14. Discussion and possible direction on items related to the City's authority within the Extra-Territorial Jurisdiction (ETJ) (Requested by Councilmember Self and presentation by Interim Director of Development Services AJ Fawver)

15. Discussion and possible action regarding excess Hotel Occupancy Tax receipts (Presentation by Finance Director Tina Bunnell)

16. First Public Hearing and consideration of introducing an Ordinance amending the 2012-2013 Budget for new projects and incomplete projects AN ORDINANCE OF THE CITY OF SAN ANGELO AMENDING THE BUDGET FOR THE FISCAL YEAR BEGINNING OCTOBER 1, 2012, AND ENDING SEPTEMBER 30, 2013, FOR NEW PROJECTS, INCOMPLETE PROJECTS, CAPITAL PROJECTS, AND GRANTS (Presentation by Budget Analyst Laura Brooks)

17. First Public Hearing and consideration of introducing an Ordinance amending established boundaries of Single Member District 6 AN ORDINANCE OF THE CITY COUNCIL OF THE CITY OF SAN ANGELO, TEXAS AMENDING THE ESTABLISHED BOUNDARIES OF SINGLE MEMBER DISTRICT NUMBER 6 FOR THE PURPOSE OF INCORPORATING NEWLY ANNEXED AREAS INTO SAID DISTRICT, PROVIDING FOR PRECLEARANCE AND ALL OTHER NECESSARY ACTIONS; AND PROVIDING FOR AN EFFECTIVE DATE (Presentation by City Clerk Alicia Ramirez)

H. FOLLOW UP AND ADMINISTRATIVE ISSUES

18. Consideration of and possible action on matters discussed in Executive/Closed Session, if needed 19. Consideration of approving various Board nominations by Council and designated Councilmembers:

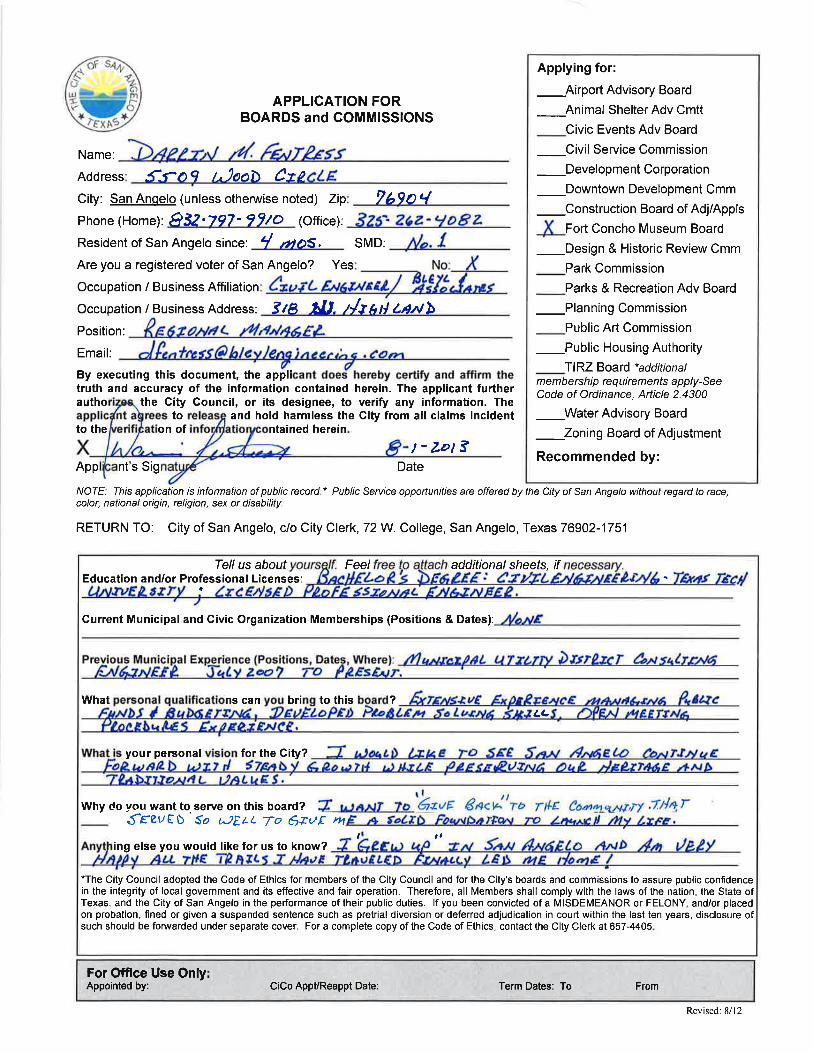

a. Ft. Concho Museum Board: Darrin Fentress (SMD3) to a 1st full term January 2016 b. Water Advisory Board: Paul Alexander (SMD3) to an unexpired term September 2013

20. Announcements and consideration of Future Agenda Items 21. Consideration of the October 21, 2103 City Council meeting and any action in connection thereto 22. EVENING MEETINGS: Beginning October 1, 2013, the City Council will conduct an evening

meeting at 6:00 P.M. once per quarter. Tentative meeting dates: October 1, 2013, January 7, 2014, April 1, 2014, and July 1, 2014

23. Adjournment

The City Council reserves the right to consider business out of the posted order, and at any time during the

City Council Agenda Page 5 of 5 August 20, 2013

meeting, reserves the right to adjourn into executive session on any of the above posted agenda items which are not listed as executive session items and which qualify to be discussed in closed session under Chapter 551 of the Texas Government Code. Given by order of the City Council and posted in accordance with Title 5, Texas Government Code, Chapter 551, Wednesday, August 14, 2013, at 5:00 P.M.

/s/________________________ Alicia Ramirez, City Clerk

P R O C L A M A T I O N WHEREAS, the West Texas Lighthouse for the Blind is a community-based

nonprofit organization providing employment opportunities to people who are blind or visually impaired in San Angelo and 40 West Texas counties; and

WHEREAS, the West Texas Lighthouse for the Blind provides a safe place to

work, on the job training, competitive wages and benefits to the visually impaired, so they can gain independence and a better quality of life; and

WHEREAS, the West Texas Lighthouse for the Blind provides on-time goods and

services at a competitive price to the State of Texas and the Federal Government; and

WHEREAS, in San Angelo, Texas, the West Texas Lighthouse for the Blind

provides employment opportunities and training to 38 people who are blind or visually impaired; and

WHEREAS, San Angelo, Texas recognizes the important contribution and

mission of “creating jobs and changing lives” of the West Texas Lighthouse for the Blind to San Angelo, Texas and its citizens.

NOW, THEREFORE, I, Dwain Morrison, Mayor of the City of San Angelo, Texas, on behalf of the City Council, do hereby proclaim the week of August 26 through 30, 2013 as

“West Texas Lighthouse Services Week” to recognize the staff and employees of the West Texas Lighthouse for the their contribution to our community for these past 50 years and to wish them many more years of success for their endeavors.

IN WITNESS WHEREOF, I have hereunto set my hand and caused the Seal of the City to be affixed this 20th day of August, 2013.

THE CITY OF SAN ANGELO ___________________________

Dwain Morrison, Mayor

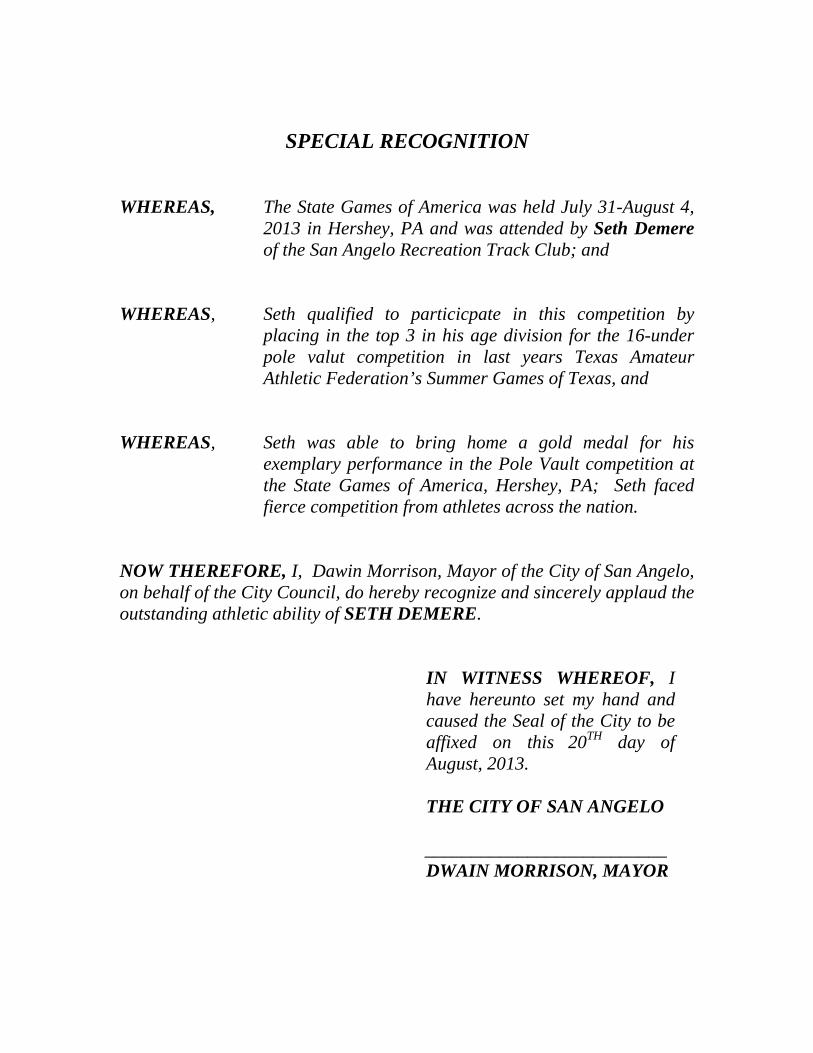

SPECIAL RECOGNITION WHEREAS, The State Games of America was held July 31-August 4,

2013 in Hershey, PA and was attended by Seth Demere of the San Angelo Recreation Track Club; and

WHEREAS, Seth qualified to particicpate in this competition by

placing in the top 3 in his age division for the 16-under pole valut competition in last years Texas Amateur Athletic Federation’s Summer Games of Texas, and

WHEREAS, Seth was able to bring home a gold medal for his

exemplary performance in the Pole Vault competition at the State Games of America, Hershey, PA; Seth faced fierce competition from athletes across the nation.

NOW THEREFORE, I, Dawin Morrison, Mayor of the City of San Angelo, on behalf of the City Council, do hereby recognize and sincerely applaud the outstanding athletic ability of SETH DEMERE.

IN WITNESS WHEREOF, I have hereunto set my hand and caused the Seal of the City to be affixed on this 20TH day of August, 2013.

THE CITY OF SAN ANGELO

__________________________ DWAIN MORRISON, MAYOR

SPECIAL RECOGNITION WHEREAS, The Texas Amateur Athletic Federation 2013 Games of Texas

State Track Meet was held July 25-28, 2013, in Corpus Christi, Texas and was attended by Hagen Stout, Jessica Simon, Bailey Kinney, and Zac Cabrera of the San Angelo Recreation Track Club; and

WHEREAS, The TAAF Summer Games of Texas is the largest amateur

athletic event held in Texas and these individuals performed commendably.

WHEREAS, Hagen Stout brought home the bronze in 16-under pole vault;

Jessica Simon brought home the silver in the 12-under 1600 meter run; Bailey Kinney brought home the silver in the 14-under girls 800 meter run and set the State Record for the 12-under girls 800 meter run in the 2012 Games; and Zac Cabrera brought home the silver in the boys 16-under 1600 meter run.

NOW THEREFORE, I, Dawin Morrison, Mayor of the City of San Angelo, on behalf of the City Council, do hereby recognize and sincerely applaud the outstanding athletic ability of HAGEN STOUT, JESSICA SIMON, BAILEY KINNEY, AND ZAC CABRERA.

IN WITNESS WHEREOF, I have hereunto set my hand and caused the Seal of the City to be affixed on this

20TH day of August, 2013.

THE CITY OF SAN ANGELO

__________________________ DWAIN MORRISON, MAYOR

City of San Angelo

Memo Date: June 25, 2013

To: Mayor and Councilmembers

From: Luis Elguezabal, A.A.E., Airport Director

Subject: Agenda Item for August 6, 2013 Council Meeting

Contact: Bryan Kendrick, Airport 325.659.6409 ext 1010

Caption: CONSENT

Consideration of authorizing the City Manger to execute on behalf of the City a Concession Agreement and all related documents with Wayne Burton d/b/a Hertz Rent A Car for a non-exclusive license to operate an automobile rental service at the San Angelo Regional Airport-Mathis Field

Summary: This Concession Agreement is for a term of three (5) years beginning September 1, 2012, and expiring August 31, 2017.

Financial Impact: Concessionaire agrees to pay to Lessor, for use of the demised premises and for the rights and privileges granted herein, a minimum guarantee of TWELVE THOUSAND DOLLARS ($12,000.00) a year or an amount equal to ten percent (10.0%) of Concessionaire's annual gross receipts, as defined herein, which are derived from its operation of automobile rental service at the Airport, whichever is greater

Related Vision Item

(if applicable):

None

Other Information/ Recommendation:

Staff recommends approval

Attachments: DRAFT Contract

Presentation: None

Publication: None

Reviewed by Director:

Luis Elguezabal, A.A.E., Airport, 06-25-13

Approved by Legal: Submitted to City Attorney for Approval

�

CONCESSION AGREEMENT

THIS CONCESSION AGREEMENT (hereinafter referred to as “Agreement”) is made and entered into by and between the CITY OF SAN ANGELO, a Texas home-rule municipal corporation under the laws of the State of Texas, acting by and through its duly authorized City Manager (hereinafter referred to as "Lessor"), and WAYNE BURTON dba HERTZ RENT-A-CAR, with its principal office at 8618 Terminal Circle, Suite102, San Angelo, Texas 76904 (hereinafter referred to as "Concessionaire" or “Lessee”).

Lessor owns and operates the San Angelo Regional Airport-Mathis Field, located in Tom Green County, Texas (hereinafter called the "Airport"), and Concessionaire is engaged in an operation to supply an adequate number of late-model automobiles that are in good mechanical condition and appearance for the operation of an automobile rental business at Airport at rates comparable to those generally prevailing in the San Angelo area. Because ground transportation is an essential service to Airport passengers and to other patrons of the Airport, it is the intent and desire of Lessor that air passengers have available to them, twenty-four (24) hours a day, seven days a week, a choice of various ground transportation services, any one of which they shall have the right to select and use, including the automobile rental business operated and conducted by Concessionaire.

For and in consideration of the premises and of the mutual terms, conditions and covenants of this Agreement, and other valuable consideration, Lessor does hereby demise and let unto Concessionaire, and Concessionaire does hereby lease and accept from Lessor, certain Airport property, together with improvements thereon (hereinafter called "demised premises"), and certain attendant privileges, uses and rights, as follows: 1. PREMISES AND PRIVILEGES

1.1 DESCRIPTION OF DEMISED PREMISES. The premises conveyed by this Concession Agreement shall be as follows:

1.1.1 Counter areas in the terminal building, as shown on the terminal building

floor plan, which is available for review in the office of the Airport Director; and

1.1.2 Ready car and return car check-in parking positions, which shall be

assigned and designated by the Airport Director. Lessor reserves the right to change the location and number of allocated spaces. It is further agreed that the passenger terminal parking lot will not be used for rental automobile or employee parking and Lessor may withdraw ready car spaces on a one-for-one basis for each rental or employee automobile that is observed in the public parking lot.

1.2 DESCRIPTION OF PRIVILEGES, USES AND RIGHTS. Lessor hereby grants

to Concessionaire the following privileges, uses and rights, all of which shall be subject to the terms, conditions and covenants hereinafter set forth:

�

1.2.1 The right, non-exclusive license and privilege to operate an automobile rental service at the Airport for the purpose of renting automobiles to airline passengers and such other persons who may request such service at the Airport;

1.2.2 The right of ingress to and egress from the demised premises over and

across public roadways serving the passenger terminal building by Concessionaire, its agents and servants, patrons and invitees, suppliers of services and furnishers of material;

1.2.3 The right, at Concessionaire's sole expense, to install and thereafter

operate and maintain signs advertising Concessionaire's business on demised premises, and at such other place or places in or upon the Airport as may be mutually agreed upon by the parties hereto in compliance with the Sign Ordinance, Chapter 12, Article 12.600 et seq. of the Code of Ordinances of the City of San Angelo, Texas;

1.2.4 The right, upon any termination of this Agreement, and within a ten (10)

day period thereafter, to remove such items, equipment, trade fixtures, and other non-attached improvements as may have been installed in or upon the demised premises by the Concessionaire.

2. TERM

2.1 TERM. This Concession Agreement is for a term of five (5) years beginning September 1, 2013, and expiring August 31, 2018.

2.2 HOLDOVER. Any holding over by Concessionaire of the demised premises after

expiration of this Agreement shall be construed only as a tenancy from month to month, with privileges and obligations of parties extended from month to month, terminable at the will of Lessor. During this period, rent shall be in accordance with paragraph 3.1.

3. RENT

3.1 AMOUNT. For the period from September 1, 2013, through August 31, 2018,

Concessionaire agrees to pay to Lessor, for use of the demised premises and for the rights and privileges granted herein, a minimum guarantee of TWELVE THOUSAND DOLLARS ($12,000.00) a year or an amount equal to ten percent (10.0%) of Concessionaire's annual gross receipts, as defined herein, which are derived from its operation of automobile rental service at the Airport, whichever is greater. Payment of the gross receipt percentage or minimum guarantee, whichever is greater, shall be made monthly, prorated, on or before the 12th day of each month from and after commencement of operations hereunder. A verifiable report of all gross receipts derived from the business transacted by Concessionaire at the Airport during the preceding calendar month shall be submitted on forms acceptable to Lessor and shall be accompanied by payment to the Lessor of one twelfth (1/12) of the guaranteed annual minimum, to wit: ONE

�

THOUSAND AND NO/100 DOLLARS ($1,000.00), or ten percent (10.0%) of the monthly gross receipts for the preceding calendar month, whichever amount is greater. The term "gross receipts", as used herein, shall mean and include time and mileage charges paid or payable to Concessionaire for rental of automobiles, whether received by cash or credit, regardless of when, where or through whom the order is received, including all revenue derived by Concessionaire arising out of or in connection with Concessionaire's operation at the Airport. The following items shall be excluded:

3.1.1 Charges to customers for refueling a vehicle when the customer is

obligated to return the vehicle with the same amount of fuel furnished;

3.1.2 Charges for collision damage waiver, personal accident insurance and personal effects coverage;

3.1.3 Refundable deposits except those forfeited and claimed by the

Concessionaire in lieu of rental charges;

3.1.4 Collections from customers or insurers for vehicle damage and repair;

3.1.5 Any federal, state or local taxes which are separately stated and collected by the Concessionaire; however, no deductions from gross receipts shall be allowed from taxes levied on concession activities, equipment or real or personal property of Concessionaire; and

3.1.6 Receipts from the sale of vehicles previously used in Concessionaire's

rental fleet.

3.2 PLACE OF PAYMENT. All fees and rentals shall be delivered to Lessor at: City of San Angelo Airport, 8618 Terminal Circle, Suite 101, San Angelo, Texas 76904, Attention: Airport Director.

3.3 LATE FEES. Concessionaire shall pay to Lessor a late fee as provided by

Chapter 1, Article 1.800, Section 1.802, and Appendix A, Article 10.00, Section 10.200 of the Code of Ordinances of the City of San Angelo, for any fee or rent not fully paid when due.

3.4 ABATEMENT OF MINIMUM ANNUAL GUARANTEE. As long as

Concessionaire is not in default of any of the terms and conditions of this Agreement, the minimum annual guarantee set forth above shall be abated on a monthly basis to the extent, in an amount, and for a term to be set by the Airport Advisory Board of the City of San Angelo at a meeting called for such purpose, if during the term hereof, through no fault of Concessionaire, either or both of the following conditions should occur:

3.4.1 The number of monthly passengers deplaning in a particular month on

scheduled airline flights at the Airport shall be less than seventy-five percent (75%) of the number of deplaning passengers as compared with

�

the monthly average of deplaned passengers for that month in the preceding year, and/or

3.4.2 The business of Concessionaire authorized hereunder shall be affected by

shortage or other disruptions in the supply of automobiles, gasoline or other goods necessary for the operation of Concessionaire's business which results in a twenty-five percent (25%) or greater reduction in monthly gross receipts of Concessionaire hereunder as compared with the same month during the preceding calendar year.

3.5 BOOKS AND RECORDS. Concessionaire agrees that it will keep or cause to be

kept true, accurate and complete records of business conducted hereunder, and Concessionaire further agrees that Lessor shall have the right, through its duly authorized agents or representatives to examine all pertinent records at a reasonable time, for the purpose of auditing to determine the accuracy thereof.

4. SPECIAL CONDITIONS. This Agreement is entered into subject to the following

conditions which are accepted and agreed to by Concessionaire:

4.1 PREMISES

4.1.1 The demised premises have been examined by Concessionaire, and are accepted by Concessionaire “AS IS” and WITHOUT EXPRESS OR IMPLIED WARRANTY OF FITNESS FOR A PARTICULAR PURPOSE. Concessionaire is familiar with the demised premises and Airport facilities and deems them as suitable for the purpose for operating an automobile rental service.

4.1.2 The right to use the public Airport facilities is shared in common with

others, and shall be used subject to all laws, rules, and regulations of the United States, the State of Texas, and the City of San Angelo, now in existence or hereafter enacted.

4.1.3 The right to operate an automobile rental service on Airport premises

granted herein is non-exclusive. Lessor shall have the right to deal with and perfect arrangements with any other individual, company or corporation for engaging in like activity on Airport premises subject to substantially the same conditions and terms binding Concessionaire herein.

4.1.4 The premises demised to Concessionaire shall remain open for such

periods during each day and such days during each week as may be necessary to meet reasonable demands for said services. Concessionaire may install on the demised premises or at such other places as the parties may agree upon, a direct telephone line for the purpose of supplying automobile rental service to airport patrons during the periods when the airport terminal facilities are closed.

�

4.1.5 Concessionaire shall permit the installation on its demised premises of the Airport public address system and the reception thereon of flight announcements and other information if Lessor deems such installation necessary.

4.2 RULES AND REGULATIONS

4.2.1 Concessionaire shall abide by and be subject to all laws and reasonable

rules and regulations which are now, or may from time to time be formulated by Lessor concerning management, operation or use of the Airport.

4.2.2 Concessionaire shall not discriminate against any employee or applicant

for employment because of race, color, creed, sex, age or national origin. Concessionaire agrees to take affirmative action to ensure that applicants are employed and that employees are tested during employment without regard to their race, creed, color, sex, age or national origin. Such action shall include but not be limited to, the following: employment, upgrading, demotion or transfer, recruitment or recruitment advertising, layoff or termination, rates of pay or other forms of compensation and selection for training, including apprenticeship.

4.2.3 Concessionaire agrees to comply fully with the Americans with

Disabilities Act insofar as such act does not require construction or alteration of the premises.

4.2.4 Concessionaire shall prohibit its agents, servants, and employees from

engaging in the solicitation of its automobile rental services on or about the Airport in a loud, boisterous, offensive or objectionable manner. In the event of questionable conduct in such solicitation, the Airport Director shall be sole judge in determining if said conduct is a violation of this paragraph; and upon notice from the Airport Director, Concessionaire shall immediately take all steps necessary to eliminate the undesirable condition.

4.2.5 Concessionaire, its agents, servants and employees shall maintain a

friendly and cooperative, though competitive, relationship with other companies engaged in like business on said Airport. Concessionaire shall not engage in open public disputes, disagreements, or conflicts which would tend to deteriorate the quality of the automobile rental service of Concessionaire or its competitors or which would be incompatible with the best interest of the public at the Airport. Lessor shall have the right to resolve all such disputes, disagreements or conflicts, and its determination of or the manner in which Concessionaire shall thereafter operate shall be binding upon Concessionaire.

4.3 SERVICE

�

4.3.1 Concessionaire shall furnish good, prompt and efficient service, adequate to meet all reasonable demands for automobile rental service at the Airport, on a fair and reasonable basis and charge prices for such services in accordance with automobile rental industry standards.

4.3.2 Concessionaire shall use its best efforts to develop and increase the

business of the rental of automobiles at the Airport and will not divert or cause or allow to be diverted any automobile rentals from its place of business at the Airport to any other location not at the Airport. Automobiles shall be deemed to be rented at the Airport and the rentals thereof included in gross revenues if the automobile is delivered to the customer at the Airport.

4.4 MAINTENANCE

4.4.1 Rental automobiles made available hereunder shall be maintained at

Concessionaire's sole expense, in good operative order, free from known mechanical defects, and in clean, neat and attractive condition, inside and outside.

4.4.2 Concessionaire shall, at its sole cost and expense, furnish, install, operate

and maintain the demised premises and every part thereof; and shall maintain the furnishings, fixtures and equipment installed therein in good safe and serviceable condition at leaset as well as the furnishings, fixtures and equipment installed in the non-exclusive areas made available to Concessionaire are maintained. Concessionaire shall repair all damages caused by its employees, guests or invitees, or that otherwise result from its operation of the automobile rental service. Concessionaire shall repaint the demised premises as necessary to maintain its current condition or as otherwise desirable, after obtaining prior approval of the Lessor.

4.4.3 Lessor shall be the sole judge of the quality of maintenance; and upon

written notice by Lessor to Concessionaire, Concessionaire shall perform whatever maintenance Lessor reasonably deems necessary. If said maintenance is not undertaken and pursued with due diligence by Concessionaire within ten (10) days after receipt of written notice, Lessor shall have the right to enter upon the demised premises and perform the necessary maintenance, the cost of which shall be assessed by Lessor as additional rent and borne by Concessionaire.

4.4.4 Upon termination of this Agreement, Concessionaire shall deliver the

demised premises in good order, condition and repair, reasonable wear and tear excepted.

4.4.5 Concessionaire shall provide and use suitable covered metal receptacles

for all garbage, trash or other refuse. Concessionaire shall not stack, store or keep boxes, cartons, barrels, or other similar items, in an unsightly or unsafe manner, on or about the demised premises, or permit the same.

�

4.5 COSTS AND FEES

4.5.1 Concessionaire shall bear, at its own expense, all costs of operating the

concession and shall pay, in addition to rental, all other costs connected with the use of the demised premises and facilities, including but not limited to, maintenance, insurance, any and all taxes, all permit fees and license fees, and assessments lawfully levied or assessed upon the personal property and demised premises or structures and improvements situated thereon.

4.5.2 Concessionaire shall secure, at its own expense, all permits and licenses

required by law.

4.5.3 Concessionaire shall pay and discharge all taxes, general and special assessments, and other charges of every description which during the term of this Agreement may be levied on or assessed against the demised premises and all interest therein and all improvements and other property thereon, whether belonging to Lessor or Concessionaire, or to which either of them may become liable. Concessionaire shall pay all such taxes, charges and assessments to the public officer charged with the collection thereof not less than fifteen (15) days before the same shall become delinquent, and CONCESSIONAIRE AGREES TO INDEMNIFY AND SAVE HARMLESS LESSOR FROM ALL SUCH TAXES, CHARGES AND ASSESSMENTS.

4.6 OTHER SALES

4.6.1 Concessionaire shall not sell or dispense petroleum products, or perform

motor vehicle repair services or related services on the Leased Premises; provided however, upon sufficient or desirable space being deemed available as determined by Lessor, the parties may negotiate and execute a separate lease agreement pursuant to which Concessionaire may lease space or facilities on the Airport premises for dispensing of petroleum products and servicing vehicles owned or controlled by Concessionaire that are used in conjunction with the automobile rental concession granted hereunde.

4.6.2 Concessionaire shall neither install nor operate on the demised premises

vending machines or coin operated amusement machines or devices. Lessor specifically reserves the right to arrange for installation of such pay telephones as Concessionaire may require and to secure the income therefrom.

4.6.3 Insofar as permitted by law, Concessionaire may offer trip insurance

covering, accidental loss of life, accidental injury, medical expenses, or property damage, limited only to customers leasing Concessionaire's vehicles and excluding air travel insurance protection.

�

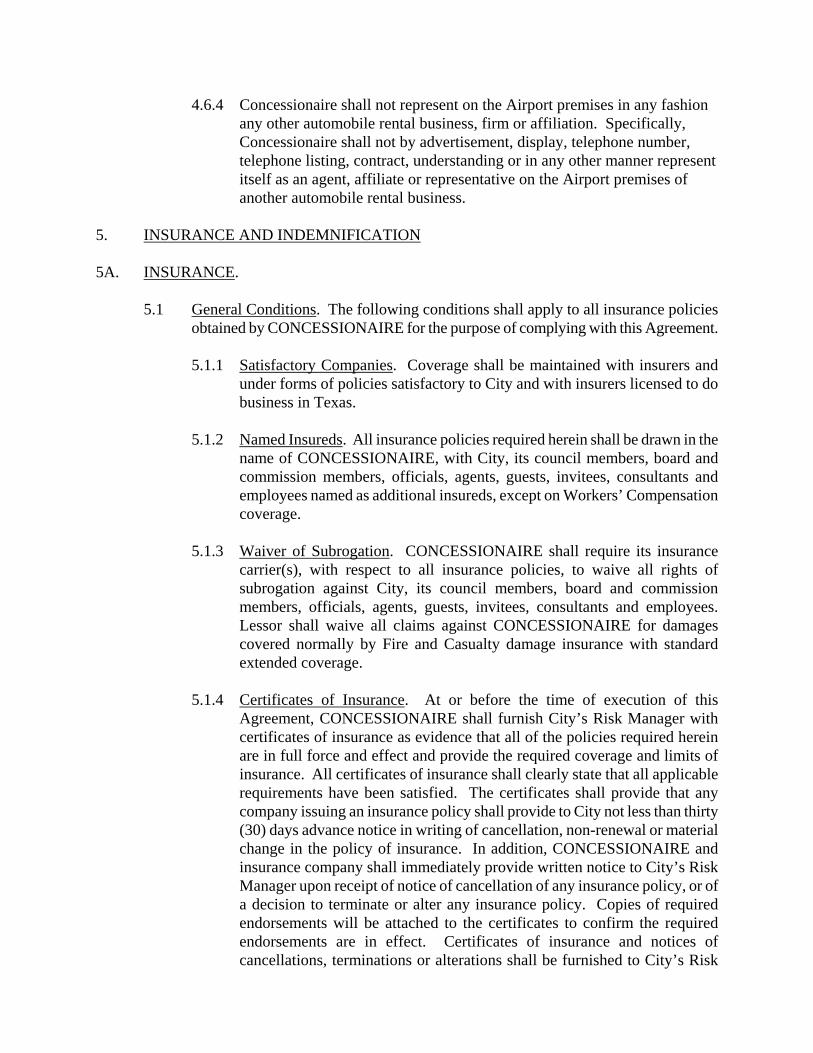

4.6.4 Concessionaire shall not represent on the Airport premises in any fashion

any other automobile rental business, firm or affiliation. Specifically, Concessionaire shall not by advertisement, display, telephone number, telephone listing, contract, understanding or in any other manner represent itself as an agent, affiliate or representative on the Airport premises of another automobile rental business.

5. INSURANCE AND INDEMNIFICATION 5A. INSURANCE.

5.1 General Conditions. The following conditions shall apply to all insurance policies obtained by CONCESSIONAIRE for the purpose of complying with this Agreement.

5.1.1 Satisfactory Companies. Coverage shall be maintained with insurers and

under forms of policies satisfactory to City and with insurers licensed to do business in Texas.

5.1.2 Named Insureds. All insurance policies required herein shall be drawn in the

name of CONCESSIONAIRE, with City, its council members, board and commission members, officials, agents, guests, invitees, consultants and employees named as additional insureds, except on Workers’ Compensation coverage.

5.1.3 Waiver of Subrogation. CONCESSIONAIRE shall require its insurance carrier(s), with respect to all insurance policies, to waive all rights of subrogation against City, its council members, board and commission members, officials, agents, guests, invitees, consultants and employees. Lessor shall waive all claims against CONCESSIONAIRE for damages covered normally by Fire and Casualty damage insurance with standard extended coverage.

5.1.4 Certificates of Insurance. At or before the time of execution of this

Agreement, CONCESSIONAIRE shall furnish City’s Risk Manager with certificates of insurance as evidence that all of the policies required herein are in full force and effect and provide the required coverage and limits of insurance. All certificates of insurance shall clearly state that all applicable requirements have been satisfied. The certificates shall provide that any company issuing an insurance policy shall provide to City not less than thirty (30) days advance notice in writing of cancellation, non-renewal or material change in the policy of insurance. In addition, CONCESSIONAIRE and insurance company shall immediately provide written notice to City’s Risk Manager upon receipt of notice of cancellation of any insurance policy, or of a decision to terminate or alter any insurance policy. Copies of required endorsements will be attached to the certificates to confirm the required endorsements are in effect. Certificates of insurance and notices of cancellations, terminations or alterations shall be furnished to City’s Risk

�

Manager at City Hall, 72 West College, San Angelo, Texas 76903.

5.1.5 CONCESSIONAIRE’S Liability. The procurement of such policy of insurance shall not be construed to be a limitation upon CONCESSIONAIRE’S liability or as a full performance on its part of the indemnification provisions of this Agreement. CONCESSIONAIRE’S obligations are, notwithstanding any policy of insurance, for the full and total amount of any damage, injury or loss caused by or attributable to its activities conducted at, about or upon the Premises. Failure of CONCESSIONAIRE to maintain adequate coverage shall not relieve CONCESSIONAIRE of any contractual responsibility or obligation.

5.1.6 Sub Contractors’ Insurance. CONCESSIONAIRE shall cause each Sub

Contractor of CONCESSIONAIRE to purchase and maintain insurance of the types and in the amounts specified below. CONCESSIONAIRE shall require Sub Contractors to furnish copies of certificates of insurance to Lessor’s Risk Management Department evidencing coverage for each Sub Contractor.

5.2 Types and Amounts of Insurance Required. CONCESSIONAIRE shall obtain and

continuously maintain in effect at all times during the term hereof, at CONCESSIONAIRE’S sole expense, insurance coverage as follows with limits not less than those set forth below:

5.2.1 Commercial General Liability or equivalent Aviation Liability. This policy

shall be an occurrence-type policy, and shall protect the CONCESSIONAIRE and additional insureds against all claims arising from bodily injury, sickness, disease or death of any person (other than the CONCESSIONAIRE’S employees) and damage to property of the City or others arising out of the act or omission of the CONCESSIONAIRE or its agents and employees. This policy shall also include protection against claims for the contractual liability assumed by CONCESSIONAIRE under the paragraph of this Agreement entitled “Indemnification,” including completed operations, products liability, contractual coverage, broad form property coverage, explosion, collapse, underground, premises/operations, and independent contractors (to remain in force for two years after final payment). Coverage shall not be less than:

$ 2,000,000.00 General Aggregate $ 1,000,000.00 Products- Completed Operations Aggregate $ 1,000,000.00 Personal & Advertising Injury $ 1,000,000.00 Each Occurrence $ 500,000.00 Fire Damage (any one fire)

5.2.2 Business Automobile Liability. This policy shall be written in

comprehensive form and shall protect CONCESSIONAIRE and the additional insureds against all claims for injuries to members of the public and damage to property of others arising from the use of motor vehicles and shall cover operation on and off the Premises of all motor vehicles licensed

��

for highway use, whether they are owned, non-owned or hired. Coverage shall not be less than:

$ 1,000,000.00 Combined Single Limit

5.2.3 Workers’ Compensation and Employer’s Liability. If CONCESSIONAIRE

hires any employees, CONCESSIONAIRE shall maintain Workers’ Compensation and Employer’s Liability insurance, which shall protect the CONCESSIONAIRE against all claims under applicable state workers’ compensation laws and employer’s liability. The insured shall also be protected against claims for injury, disease or death of employees which, for any reason, may not fall within the provisions of a workers’ compensation law. Coverage shall not be less than:

Statutory Amount Workers’ Compensation $ 500.000.00 Employer’s Liability, Each Accident $ 500,000.00 Employer’s Liability, Disease - Policy

Limit $ 500,000.00 Employer’s Liability, Disease – Each

Employee

The foregoing requirement will not be applicable if, and so long as, CONCESSIONAIRE qualifies as a self-insurer under the rules and regulations of the commission or agency administering the workers’ compensation program in Texas and furnishes evidence of such qualification to Lessor in accordance with the notice provisions of this Agreement.

If CONCESSIONAIRE uses contract labor, CONCESSIONAIRE shall require its contractor to maintain the above referenced coverage and furnish copies of certificates of insurance as required herein.

5.2.4 Environmental Liability. This insurance shall be maintained in force for the full period of this Contract and cover losses caused by pollution conditions including, but not limited to, any spill, underground pollution or any other environmental impairment. It shall apply to bodily injury; property damage, including loss of use of damaged property or of property that has not been physically injured; cleanup costs; including, but not limited to, any costs required under CERCLA; and defense, including costs and expenses incurred in the investigation, defense, or settlement of claims. If coverage is written on a claims made basis, CONCESSIONAIRE warrants that any retroactive date applicable to coverage under the policy precedes the effective date of this Contract, and continuous coverage will be maintained or an extended discovery period will be exercised for a period of two (2) years beginning from the time the Contract has expired. Coverage shall not be less than:

$1,000,000.00 per loss $2,000,000.00 Annual aggregate

5.B INDEMNIFICATION.

��

CONCESSIONAIRE AGREES TO INDEMNIFY, DEFEND, REIMBURSE AND

HOLD CITY, ITS COUNCIL MEMBERS, BOARD AND COMMISSION MEMBERS, OFFICIALS, AGENTS, GUESTS, INVITEES, CONSULTANTS AND EMPLOYEES FREE AND HARMLESS FROM AND AGAINST ANY AND ALL CLAIMS, DEMANDS, PROCEEDINGS, SUITS, JUDGMENTS, COSTS, PENALTIES, FINES, DAMAGES, LOSSES, ATTORNEYS’ FEES AND EXPENSES ASSERTED BY ANY PERSON OR PERSONS, INCLUDING AGENTS OR EMPLOYEES OF CONCESSIONAIRE OR CITY, BY REASON OF DEATH OR INJURY TO PERSONS, OR LOSS OR DAMAGE TO PROPERTY, RESULTING FROM OR ARISING OUT OF, THE VIOLATION OF ANY LAW OR REGULATION OR IN ANY MANNER ATTRIBUTABLE TO ANY ACT OF COMMISSION, OMISSION, NEGLIGENCE OR FAULT OF CONCESSIONAIRE, ITS AGENTS OR EMPLOYEES, OR THE JOINT NEGLIGENCE OF CONCESSIONAIRE AND ANY OTHER ENTITY, AS A CONSEQUENCE OF ITS EXECUTION OR PERFORMANCE OF THIS AGREEMENT OR SUSTAINED IN OR UPON THE PREMISES, OR AS A RESULT OF ANYTHING CLAIMED TO BE DONE OR ADMITTED TO BE DONE BY CONCESSIONAIRE HEREUNDER. THIS INDEMNIFICATION SHALL SURVIVE THE TERM OF THIS AGREEMENT AS LONG AS ANY LIABILITY COULD BE ASSERTED. NOTHING HEREIN SHALL REQUIRE CONCESSIONAIRE TO INDEMNIFY, DEFEND OR HOLD HARMLESS ANY INDEMNIFIED PARTY FOR THE INDEMNIFIED PARTY’S OWN GROSS NEGLIGENCE OR WILLFUL MISCONDUCT.

6. DAMAGE OR DESTRUCTION OF PREMISES

6.1 If the demised premises are partially damaged by fire, explosion, the elements, public enemy, or other casualty, but not rendered untenantable, the same will be repaired with due diligence by Lessor at its own cost and expense.

6.2 If the damage shall be so extensive as to render such premises untenantable, but

capable of being repaired in thirty (30) days, the same shall be repaired with due diligence by Lessor at its own cost and expense and the rent payable herein shall be paid proportionately to the time of such damage and thereafter cease until such time as the premises are again tenantable.

6.3 In the event said premises are completely destroyed by fire, explosion, the

elements, public enemy or other casualty, or so damaged that they will remain untenantable for more than thirty (30) days, Lessor shall be under no obligation to repair and reconstruct the premises, and rent payable hereunder shall be paid proportionately to the time of such damage or destruction and shall thereafter cease until such time as the premises may be fully restored. If within twelve (12) months after the time of such damage or destruction said demised premises shall not have been repaired or reconstructed, Concessionaire may give Lessor written notice of its intention to terminate this Agreement effective from the date of such damage or destruction.

��

7. TERMINATION OF AGREEMENT, CANCELLATION, ASSIGNMENT AND TRANSFER

7.1 TERMINATION. This Agreement shall terminate at the end of the full term or

any extension thereof, at which time Concessionaire shall have no further right or interest in any of the Premises, lands, areas, or improvements hereby demised, and the rights, privileges and license granted Concessionaire hereunder shall expire,

7.2 CANCELLATION BY CONCESSIONAIRE. This Agreement shall be subject to

cancellation by Concessionaire on the occurrence of one or more of the following events:

7.2.1 The permanent abandonment of the Airport as an air terminal;

7.2.2 The lawful assumption by the United States government or any authorized

agency thereof, of the operation, control, or use of the Airport, or any substantial part or parts thereof, in such a manner as to substantially restrict Concessionaire for a period of at least ninety (90) days from operation thereon;

7.2.3 Issuance, by any court of competent jurisdiction, of an injunction in any

way preventing or restraining the use of the Airport for commercial airline passenger travel for a period of at least ninety (90) days;

7.2.4 The default by Lessor in the performance of any covenant or agreement

herein required to be performed by Lessor and the failure of Lessor to remedy such default for a period of sixty (60) days after receipt from Concessionaire of written notice to remedy the same; or

7.2.5 The complete destruction of the demised premises as outlined in Article 6.

7.3 CANCELLATION BY LESSOR. This Agreement shall be subject to immediate

cancellation by Lessor in the event Concessionaire shall:

7.3.1 Be in arrears in the payment of the whole or any part of the amounts agreed upon in Article 3 for a period of seven (7) days after receipt of written notice from Lessor of such arrearage;

7.3.2 Abandon the demised premises by Concessionaire;

7.3.3 Default in the performance of any of the covenants and conditions

required herein (except rental payments) to be kept and performed by Concessionaire, and such default continues for a period of thirty (30) days after receipt of written notice from Lessor of said default; or

7.3.4 Be adjudged by Lessor of intent to deprive the Lessor of rental payments

due and payable under this Agreement or be guilty of repeated or

��

continued violations of the covenants and conditions required herein to be kept and performed by Concessionaire.

7.4 RE-ENTRY BY LESSOR AND COVENANT NOT TO SUE. Upon termination

of this Agreement, Lessor may re-enter and take immediate possession of the demised premises and remove Concessionaire’s fixtures, equipment or effects, with or without process of law, without being deemed guilty of trespass. Lessor shall not be liable for any damages by reason of such re-entry or disposition of Concessionaire’s property. Concessionaire, on behalf of itself, its parents, subsidiaries, divisions, related companies, affiliated companies, licensees, independent contractors, assigns or other business related entities hereby unconditionally and irrevocably covenants to refrain from making any claim or demand or from commencing, causing, or permitting to be prosecuted any action in law or equity, against Lessor, or Lessor’s council members, board and commission members, officials, agents, contractors or employees relating directly or indirectly to Lessor’s re-entry upon the demised premises upon termination of this Agreement and Lessor’s taking possession of the demised premises as provided under this Part 7 “TERMINATION OF AGREEMENT, CANCELLATION, ASSIGNMENT AND TRANSFER”, to and including the removal and or disposal of Concessionaire’s personal property equipment and fixtures in Lessor’s discretion.

7.5 POSSESSION. Concessionaire agrees at the expiration or termination of this

Agreement to deliver possession peacefully to the Lessor or its agents or employees; and if it fails to give peaceful possession, Lessor may take forceful possession of demised premises and eject all parties therefrom without being guilty of trespass; all resulting damages are hereby waived by Concessionaire, and Concessionaire covenants not to claim or sue as hereinabove provided at subparagraph 7.4 “ENTRY BY LESSOR AND COVENANT NOT TO SUE”.

7.6 OTHER REMEDIES. Any termination of this Agreement arising from

Concessionaire's default shall not relieve Concessionaire from the payment of any sum or sums that are due and payable to Lessor under this Agreement, or any claim for damages then or thereafter accruing against Concessionaire under this Agreement. Any such termination shall not prevent Lessor from enforcing the payment of any such sum or sums or claim for damages by any remedy provided for by law or from recovering damages from Concessionaire for any default under this Agreement. All rights, options, and remedies of Lessor contained in this Agreement or otherwise shall be construed and held to be cumulative, and no one of them shall be exclusive of the other; and Lessor shall have the right to pursue any one or all of such remedies or any other remedy or relief which may be provided by law, whether or not stated in this Agreement. No waiver by Lessor of a breach of any of the covenants, conditions, or restrictions of this Agreement shall be construed or held to be a waiver of any succeeding or preceding breach of the same or any other covenant, condition or restriction contained in this Agreement.

��

7.7 REMOVAL OF IMPROVEMENTS. All equipment, machinery, trade fixtures and other non-attached improvements installed on the demised premises by Concessionaire shall remain the property of Concessionaire and may be removed at the termination of this Agreement, provided Concessionaire is not then in default in the performance of any of its obligations or covenants herein contained, and provided further that such removal will do no damage to the realty upon which such items are situated. It is understood and agreed, however, that improvements shall be held by the Lessor until all rentals due Lessor by Concessionaire shall have been paid, and should any amount remain unpaid for more than thirty (30) days after termination of this Agreement, the Lessor shall have the right to sell such improvements and apply the proceeds to the amount due Lessor, with interest at the annual rate of ten percent (10%), and to any costs incident to the sale, and to pay the balance remaining, if any, to Concessionaire. All property remaining on the demised premises after the expiration of thirty (30) days following the termination of this Agreement, however terminated, shall be deemed abandoned by Concessionaire and shall become the property of Lessor.

7.8 ASSIGNMENT AND TRANSFER. Concessionaire shall not assign, transfer, or

sublease this Agreement or the rights or demised premises hereunder without the prior written approval of Lessor. Unless acknowledged and approved in writing by the Lessor, any change in the controlling interest of corporate stock ownership of Concessionaire or its parent company shall constitute grounds for immediate termination of this Agreement by Lessor.

8. COOPERATION UPON TERMINATION

8.1 Upon the termination of this Agreement, through passage of time or otherwise, Concessionaire shall facilitate Lessor in all reasonable ways in continuing the operation of said automobile rental service on the Airport without interruption.

8.2 Concessionaire further agrees to sell any or all of the Concessionaire’s furniture,

furnishings, fixtures and equipment installed or used upon said demised premises to Lessor should Lessor notify Concessionaire in writing ten (10) days before such termination date that it desires to purchase any or all of said furniture, furnishings, fixtures and equipment; and the purchase price shall be the fair market value of such items at the date of such termination. If the parties are unable to agree upon the fair market value, each party shall then appoint an appraiser; the two so appointed shall name a third appraiser; and the three appraisers so named shall determine the fair market value of such items, which determination shall be final and binding upon both parties hereto.

9. GENERAL PROVISIONS

9.1 CONFLICT BETWEEN CONCESSIONS. In the event of a conflict between Concessionaire and any other lessee or concessionaire in the Airport terminal building as to the services to be sold by respective concessionaires or lessees, Lessor shall decide which services may be sold by each concessionaire or lessee and Concessionaire agrees to be bound by such decision.

��

9.2 INSPECTION. Lessor, by its officers, employees, agents and representatives,

shall have the right at all reasonable times to enter upon the demised premises for the purpose of inspecting same, for observing the performance by Concessionaire of its obligations hereunder, and for the doing of any act which Lessor may be obligated or have the right to do under this Agreement.

9.3 ATTORNEY'S FEES. In the event any action, suit or proceeding is brought to

collect the rentals and fees, (or any portion thereof) due or to become due hereunder; to take possession of said concession space; to enforce compliance with this Agreement; or for failure to observe any of the covenants of this Agreement, Concessionaire shall pay Lessor such sum as the court may adjudge reasonable for attorney's fees to be allowed in said suit, action or proceeding.

9.4 RELATIONSHIP OF PARTIES. It is understood and agreed that nothing herein

contained is intended or should be construed as creating or establishing a relationship of agency, co-partnership or joint venture between the parties hereto, or as appointing or designating the Concessionaire as the agent, representative or employee of the Lessor for any purpose or in any manner whatsoever. Concessionaire is to be and shall remain an independent contractor with respect to all services performed hereunder.

9.5 NO WAIVER. Failure of Lessor to insist in any instance upon a strict

performance by Concessionaire of any of the provisions or terms of this Agreement shall not be considered as a waiver or relinquishment thereof for the future. No waiver by Lessor of any of the provisions or terms of this Agreement shall be deemed to have been made in any instance unless expressed in the form of a resolution by the City Council.

9.6 QUIET ENJOYMENT. Lessor agrees that Concessionaire, upon payment of rent

and all other charges and upon observation of all of the terms and conditions of this Agreement, shall lawfully and quietly hold, occupy, and enjoy the demised premises during the full term of this Agreement without hindrance from Lessor or anyone claiming by, through or under Lessor, subject, however, to Concessionaire holding and enjoying said premises under conditions which may reasonably be anticipated in connection with the operation of aircraft or an airport.

9.7 INVALID OR ILLEGAL PROVISIONS. If any one or more provisions of this

Agreement are for any reason held to be invalid, illegal or unenforceable in any respect, the invalidity, illegality or unenforceability will not affect any other provision of the Agreement, which will be construed as if it had not included the invalid, illegal or unenforceable provision.

9.8 PARAGRAPH HEADINGS. The paragraph headings contained herein are for

convenience and reference and are not intended to define, extend or limit the scope of any provision of this Agreement.

��

9.9 NOTICES. Any notice required or permitted under this Agreement shall be deemed sufficiently given if it is in writing and personally delivered, sent by overnight express delivery service or deposited in the United States mail, postage prepaid and sent by registered or certified mail (return receipt requested) to the party to which said notice is to be given. Notices delivered in person, or by overnight express delivery service, shall be deemed to be served effective as of the date the notice is delivered. Notices sent by registered or certified mail (return receipt requested) shall be deemed to be served seventy-two (72) hours after the date said notice is postmarked to the addressee, postage prepaid.

Until changed by written notice given by one party to the other, the addresses of the parties shall be as follows:

LESSOR: CITY OF SAN ANGELO

San Angelo Municipal Airport Attn: Airport Director 8618 Terminal Circle, Suite 101

San Angelo, Texas 76904 With copies to: City Attorney’s Office 72 W. College San Angelo, Texas 76903

CONCESSIONAIRE: WAYNE BURTON dba HERTZ RENT-A-CAR

Attn: Wayne Burton 8618 Terminal Circle, Ste. 102 San Angelo, Texas 76904

9.10 SUBORDINATION. This Agreement shall be subordinate to the provisions of

any existing or future agreement between Lessor and the United States relative to the operation or maintenance of the Airport.

9.11 SUCCESSORS AND ASSIGNS. All of the terms, covenants and agreements

herein contained shall be binding upon and shall inure to the benefit of successors and assigns, provided Concessionaire has previously received written approval from Lessor in accordance with Paragraph 7.8 herein, to assign, transfer or sublease its rights and demised premises.

9.12 AMENDMENT. No amendment, modification or alteration of the terms hereof

shall be binding unless the same be in writing, dated subsequent to the date hereof and duly executed by the parties hereto or their respective successors or legal representatives.

9.13 VENUE. This Agreement is governed by the laws of the State of Texas. Venue for

any suit or claim or cause of action arising out of or related to this Agreement shall be in Tom Green County, Texas.

9.14 SURVIVAL OF REMEDIES. The provisions relating to keeping of books and

��

records, audit by Lessor, insurance, indemnity, hold harmless, re-entry by Lessor, cooperation of Concessionaire upon termination and applicable law and venue shall survive the expiration or termination of this Agreement to the extent needed to enable the Parties to pursue the remedies and benefits provided for in those provisions.

9.15 ENTIRE AGREEMENT. This Agreement constitutes and contains the entire

agreement between the parties hereto. Any oral representations or modifications hereinbefore or hereinafter made concerning this Agreement shall be of no force and effect, provided however, that this Agreement may be amended by the parties

��

as provided herein. EXECUTED in duplicate originals on this the ____ day of _____________, 2013.

LESSOR CITY OF SAN ANGELO, Texas

ATTEST: By: _______________________________

Daniel Valenzuela, City Manager _____________________________ Alicia Ramirez, City Clerk THE STATE OF TEXAS § COUNTY OF TOM GREEN § This instrument was acknowledged before me on the ______ day of _______________, 2013, by DANIEL VALENZUELA, City Manager of the CITY OF SAN ANGELO, a Texas home rule municipal corporation, on behalf of said corporation.

___________________________________ Notary Public, State of Texas

CONCESSIONAIRE / LESSEE: WAYNE BURTON dba HERTZ RENT-A-CAR

By: ______________________________

Wayne Burton THE STATE OF TEXAS § COUNTY OF TOM GREEN § This instrument was acknowledged before me on the ______ day of ____________, 2012, by Wayne Burton.

__________________________________ Notary Public, State of Texas

��

Approved as to Content Approved as to Form ___________________________ __________________________________ Luis Elguezabal, Airport Director Dan T. Saluri, Sr. Assistant City Attorney

City of San Angelo

Memo Date: July 30, 2013

To: Mayor and Councilmembers

From: Tina Bunnell, CPA, Finance Director

Subject: Agenda Item for August 20, 2013 Council Meeting

Contact: Jaime Guerrero, Accounting, 325-481-2649 ext 1230

Caption: Consent Item

Consideration of adopting Resolution amending authorized representatives for Texpool, an Investment Service for Public Funds.

Summary: Texpool requires the attached resolution to amend authorized representatives. The City of San Angelo is adding Tina Bunnell, CPA, Finance Director and Jaime A. Guerrero, Chief Accountant to the list of authorized representatives.

History: Both employees are new to the City of San Angelo and will serve as additional contact members for TexPool.

Financial Impact: Texpool, an Investment Service for Public Funds, is utilized as an account for the City’s reserve cash and interest bearing investment account, which is a substantial portion of the City’s current assets.

Related Vision Item

(if applicable):

Not Applicable.

Other Information/ Recommendation:

Staff recommends that the resolution be approved.

Attachments: Texpool resolution

Presentation: Not Applicable.

Publication: Not Applicable.

Reviewed by Director:

Michael Dane, CFO

Approved by Legal:

City of San Angelo

Memo Date: July 15, 2013

To: Mayor and Councilmembers

From: Ricky Dickson, Water Utilities Director

Subject: Consent Item for August 20, 2013 Council Meeting

Contact: Ricky Dickson, Water Utilities Director, 657-4209

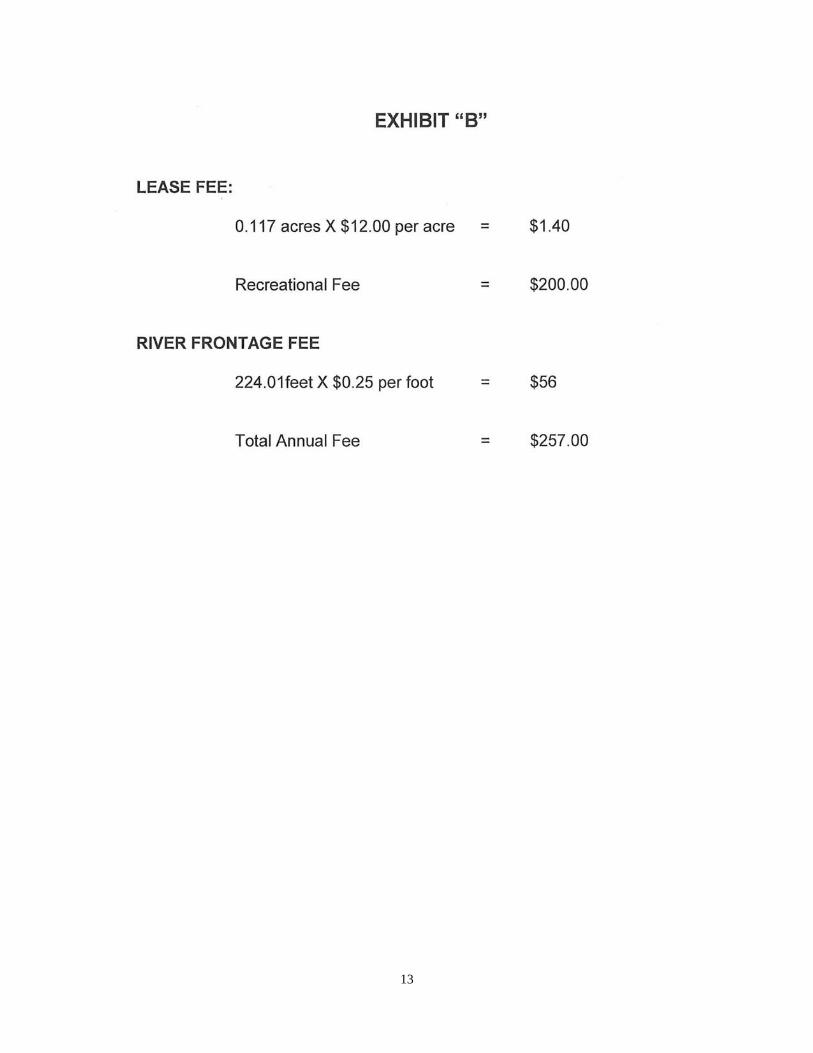

Caption: Consideration of approving Special Recreational Lease Agreement with Lee H. Bell and Karen H. Bell for 0.117 acres of land located adjacent to the lake or river and authorizing the City Manager or Water Utilities Director to execute the same.

Summary: Lee M. Bell and Karen H. Bell are current tenants under former lease and desire to enter into a new Special Recreational Lease agreement. Financial Impact: Lease fee will be $257.00 per year as computed on Exhibit B (attached). Related Vision Item (if applicable): None. Other Information/Recommendation: It is recommended that the lease be approved and the Water Utilities Director or City Manager be authorized to execute the lease. Staff recommends approval. Attachments: Lease Agreement and Exhibit A and B Presentation: None. Publication: None. Reviewed by Service Area Director: Ricky Dickson, Water Utilities Director, July 15, 2013 Reviewed by City Attorney:

Special Recreational Lease Agreement

Basic Terms

Date:

Landlord: City of San Angelo, a Texas home rule municipal corporation

Landlord’s Address: 72 W. College Avenue, San Angelo, Tom Green County, Texas 76903

Tenant: Lee M. Bell and wife, Karen H. Bell

Tenant’s Address: 3613 Country Club Road, San Angelo, Texas 76904

Leased Premises: SURFACE ESTATE ONLY of approximately 0.117 acres of land, situated in San Angelo, Tom Green County, Texas, as described in Exhibit “A” (“Leased Premises”) attached hereto and being made a part hereof, at or near the waters of Lake Nasworthy (hereinafter “Lake”).

Term: Five (5) years and five (5) months Commencement Date: August 1, 2013

Termination Date: December 31, 2018

Permitted Use: Solely for Recreational Use

Initial Payment: Initial Rent Payment due and payable on execution of this Lease, is the sum of Two Hundred Thirty-Four Dollars ($234.00), which includes: (a) Seventy-five Dollars ($75.00) – one time Granting Fee; (b) One Hundred Dollars ($100.00) – document preparation fee; (c) One Hundred Seven ($107.00) – 2013 pro-rated Annual Rent; and (d) credit of Forty Three Dollars ($43.00) – reimbursement for pre-paid Annual Rent.

Annual Rent: Annual Rent shall be Two Hundred Fifty-Seven Dollars ($257.00), paid on or before January 1st of each year, during the term of this Lease, as computed on Exhibit “B” attached hereto and incorporated by reference.

Clauses and Covenants

A. Tenant agrees to—

1. Lease the Premises for the entire Term beginning on the Commencement Date and ending on the Termination Date.

2. Obey all laws, ordinances, rules and regulations relating to Tenant’s use and maintenance of the Leased Premises, including those certain ordinances of the City

1

Council of the City of San Angelo, (“Council”), adopted April 2, 1951, as amended from time to time and known as the Lake Nasworthy-Twin Buttes Ordinances. Tenant understands and agrees that this Lease Agreement does not exempt Tenant from application of any of the ordinances, rules and regulations now or hereafter applicable to Lake Nasworthy. Any breach of said ordinances, rules or regulations shall be deemed a default of this Lease Agreement, and, at the option of the Landlord, may result in termination of this Lease.

3. Pay in advance the Initial Rent Payment, and on or before January 1st of each year during the term of this Lease, the Annual Rent to Landlord at Landlord’s Address, 72 W. College, San Angelo, Texas 76903.

4. Pay to Landlord a late charge or interest for any rent received by Landlord after the date that the rent is due in accordance with applicable ordinances, provided however, that acceptance by Landlord of late charges or interest shall not be construed as a waiver of the right of Landlord to terminate this Lease at its option as authorized herein.

5. Pay all taxes on Tenant’s property located on the Leased Premises.

6. Use the Leased Premises for recreational use only and uses incidental thereto.

7. At Tenant’s sole expense, keep and maintain fences and other improvements now on the Leased Premises in good condition, maintain landscape, and keep said Premises clean and cleared of all objectionable matter, including accumulations of trash, personal property, brush, and accumulations of dead vegetation. In the event Tenant shall fail to maintain Leased Premises in a manner acceptable to Landlord as herein required, after notice of default to Tenant, Landlord may enter upon the Leased Premises without further notice and cause Leased Premises to be cleaned, cleared, and mowed, and may dispose of all objectionable matter in the manner deemed appropriate by Landlord. Tenant expressly authorizes the cost of any such clearing, cleaning, mowing and disposal to be billed to Tenant separately rent or added to the next Annual Rent payment due, interest at the ten percent (10%) per annum, beginning thirty (30) days from the date on which the work was completed, and continuing until such cost is paid in full.

8. Maintain the pecan trees on Leased Premises. Pecans produced from said trees shall be the property of Tenant during the term of this Lease.

9. Indemnify, Defend, and Hold Harmless Landlord as follows: TENANT FURTHER AGREES TO INDEMNIFY, DEFEND AND HOLD HARMLESS LANDLORD, ITS OFFICERS, OFFICIALS, COUNCIL AND BOARD OR COMMISSION MEMBERS, AGENTS, AND EMPLOYEES, FROM AND AGAINST ANY AND ALL CLAIMS, DEMANDS, SUITS, JUDGMENTS, DAMAGES, LOSSES, PENALTIES, FINES, ATTORNEYS’ FEES, COSTS AND EXPENSES ASSERTED BY ANY PERSON OR PERSON, INCLUDING AGENTS OR EMPLOYEES OF TENANT OR LANDLORD, BY REASON OF DEATH OR INJURY TO PERSONS, OR LOSS OR DAMAGE TO PROPERTY, RESULTING FROM OR RELATED TO TENANT’S OCCUPATION OR CONTROL OVER THE LEASED PREMISES, OR SUSTAINED IN OR UPON THE LEASED PREMISES, OR AS A RESULT OF ANYTHING CLAIMED TO BE DONE OR ADMITTED TO BE DONE BY TENANT.

2

THIS INDEMNIFICATION, DEFEND AND HOLD HARMLESS AGREEMENT SHALL SURVIVE THE TERM OF THIS AGREEMENT AS LONG AS ANY LIABILITY COULD BE ASSERTED. NOTHING HEREIN SHALL REQUIRE THE INDEMNIFYING PARTY TO INDEMNIFY, DEFEND OR HOLD HARMLESS ANY INDEMNIFIED PARTY FOR THE INDEMNIFIED PARTY’S OWN GROSS NEGLIGENCE OR WILLFUL MISCONDUCT.

10. Maintain Insurance as follows:

a. Tenant shall obtain and maintain continuously in effect at all times during the term hereof, at Tenant’s sole expense, minimum comprehensive general liability insurance in the amount of at least $100,000.00 combined single limit liability per occurrence for bodily injury and property damage. This insurance shall be an occurrence-type policy written in comprehensive form and shall protect Landlord against liability which may accrue against Landlord by reason of Tenant’s occupancy or control over the Leased Premises, or wrongful conduct incident to the use thereof, resulting from any accident or event occurring on or about the Leased Premises. All insurance policies required herein shall be drawn in the name of Tenant, with Landlord, its council members, officials, officers, directors, agents and employees named as additional insureds.

b. Tenant shall furnish Landlord with certificates of insurance as evidence that all of the policies required herein are in full force and effect and provide the required coverages and limits of insurance. The certificates shall provide that any company issuing an insurance policy shall provide not less than 30-days advance notice in writing of cancellation, non-renewal or material change in the policy of insurance. In addition, Tenant shall immediately provide written notice to Landlord upon receipt of notice of cancellation of an insurance policy, or of a decision to terminate or alter any insurance policy. All certificates of insurance shall clearly state that all applicable requirements have been satisfied including certification that the policies are of the “occurrence” type. Certificates of insurance for Landlord shall be mailed in accordance with the notice provisions of this Lease Agreement.

c. Tenant shall require its insurance carrier, with respect to all insurance policies, to waive all rights of subrogation against the City of San Angelo, its council members, members of boards and commissions officers, officials, agents and employees.

d. The procuring of such policies of insurance shall not be construed to be a limitation upon Tenant’s liability or as a full performance of its obligations under the indemnification provisions of this Lease. Tenant’s obligations are, notwithstanding said policies of insurance, for the full and total amount of any damage, injury or loss caused by or attributable to its occupation or control over the Leased Premises pursuant to this Lease or any extension thereof.

11. Vacate the Leased Premises on the last day of the Term.

3

B. Tenant agrees not to—

1. Use the Leased Premises for any purpose other than the Permitted Use, including that:

a. No improvements or construction work, including but not limited to living quarters, buildings, pump houses, water wells, storage buildings, excavations, fills, or other types of structures or improvements shall be built or placed on the Leased Premises.

b. No storage of personal property shall be permitted on the Leased Premises, including equipment, machinery, vehicles, appliances, temporary electrical wiring, materials, or supplies.

2. Create or allow any nuisance or waste on Leased Premises.

3. Alter the Leased Premises, including:

a. Clearing new roads, or locating on Leased Premises any type of manufactured housing or mobile home.

b. Removing any trees from Leased Premises without first obtaining permission from Landlord.

4. Allow a lien to be placed on the Leased Premises.

5. Assign this Lease or sublease any portion of the Leased Premises without Landlord’s written consent. 6. Hunt on the Leased Premises or allow anyone else to do so.

7. Litter or leave trash or debris on the Leased Premises.

C. Landlord agrees to—

Lease to Tenant the Leased Premises beginning on the Commencement Date and ending on the Termination Date unless earlier terminated as herein provided, subject to: easements of record, Landlord’s reservation of right to execute and deliver mineral leases, and Landlord’s reservation of right to grant utility easements and rights-of way for streets and alleys, and further subject to Tenant’s compliance with the terms and conditions of this Lease.

D. Landlord agrees not to—

Allow any use of the Leased Premises inconsistent with Tenant’s Permitted Use, subject to the reservations of rights herein stated, and so long as Tenant is not in default.

4

E. Landlord and Tenant mutually agree to the following:

1. Rent Adjustment. Landlord and Tenant agree Landlord shall have the right to make an adjustment in the Annual Rent upon any extension or renewal of this Lease.

2. Temporary Improvements. Tenant may place temporary improvements on Leased Premises only with the prior, written approval of Landlord. Such improvements shall be for purposes of recreation only. Temporary improvements for other purposes are prohibited. Nothing shall be constructed, placed, or planted on Leased Premises which will in any way obstruct the natural flow of drainage or of rising water. Temporary improvements shall not include walls or be more than ten (10) feet in height. Tenant shall secure any required permits prior to placement of any temporary improvement on the Leased Premises. Temporary improvements shall be constructed in compliance with all applicable codes, laws, rules or regulation.

3. Water Usage. Tenant, may, upon receipt of an annual water use permit from Landlord, as provided in City of San Angelo Code of Ordinances, use water from the Lake or river, , for domestic purpose and watering of existing trees and shrubs, but no water is to be removed from or transported off Leased Premises. Use of water for irrigation is expressly prohibited. Tenant shall use water in a conservative manner taking any drought conditions into consideration. Any abusive use of water shall be grounds for Landlord in denying the use of water to Tenant. Tenant shall pay raw water use charges as set by Landlord.

4. Conditional Grant of Lease. This Special Recreational Lease Agreement is granted to Tenant under the condition that Tenant is the owner or Leaseholder of real property adjacent to Leased Premises. Should Tenant not be or cease to be the owner or Leaseholder of real property adjacent to Leased Premises, this Lease shall automatically terminate, and Landlord shall not be liable for refunding to Tenant any prepaid Annual Rent or other lease fees.

5. Flooding or Other Water Damage or Destruction. The parties hereto acknowledge that the Leased Premises are within an area subject to flooding and variations in Lake water level. It is expressly agreed between the parties that neither Landlord nor any of its officers, officials, council members, agents or employees shall be liable to Tenant for any damages caused in any manner, negligent or otherwise, by water, flooding, water run-off variation in level of Lake waters, or overflow of the rivers, creeks, or channels which serve as sources of water supply to the Lake, nor by reason of any work or maintenance by Landlord, deemed necessary or desirable in Landlord’s sole judgment, for the maintenance of said Lake, Lake level, or its sources of water supply. Any such damages that may be occasioned thereby during the term of this Lease Agreement or any extension thereof are hereby waived by Tenant, and Tenant does hereby forever release and discharge Landlord from liability for any such loss or claim of loss.

6. Release of Claims. Tenant expressly releases Landlord, its officials, officers, agents, and employees from any and all claims and damages of any kind whatsoever by

5