august-september 2019 · 2019-10-30 · ⓒfiskars group 2019 aug-sep 2019 22. strategic business...

TRANSCRIPT

Investorpresentation

August-September 2019

Agenda

• Fiskars Group in brief• Strategy• Segments• Financials• Appendices

Aug-Sep 2019ⓒ Fiskars Group 2019 2

Fiskars Group in brief

ⓒ Fiskars Group 2019

ⓒ Fiskars Group 2019 4

Our purpose:

Makingthe everyday

extraordinaryEstablished in Finland 1649Globally recognized brandsProducts sold in more than 100 countriesNearly 400 own storesNet sales in 2018 EUR 1,119 million7,600 employees in over 30 countries

Aug-Sep 2019

34%

9%9%8%

8%

7%

25%

Fiskars Royal CopenhagenWaterford IittalaGerber WedgwoodOthers

NET SALES SPLIT BY BRAND NET SALES SPLIT BY GEOGRAPHY

47%

40%

13%

Europe Americas Asia-Pacific

ⓒ Fiskars Group 2019 5

Fiskars Group in 2018

Aug-Sep 2019

Net sales by segment

Aug-Sep 2019ⓒ Fiskars Group 2019 6

Dinnerware Drinkware

Interior Other

Gardening School, office & craft

Outdoor

Watering Cooking Fixing

FUNCTIONAL LIVING

€585.2m €529.6m

52% 48%

Key categories

FUNCTIONAL LIVING

Strong brand portfolio

ⓒ Fiskars Group 2019 7Aug-Sep 2019

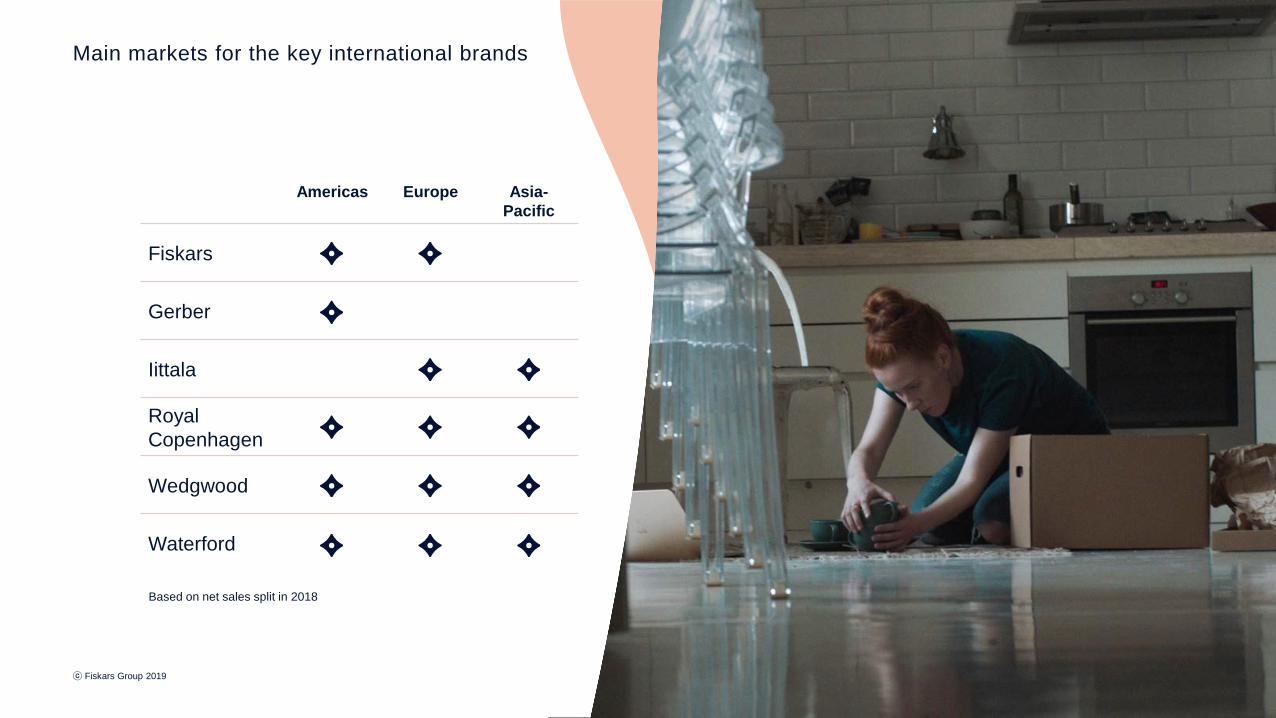

Main markets for the key international brands

ⓒ Fiskars Group 2019 8

Americas Europe Asia-Pacific

Fiskars

Gerber

Iittala

Royal Copenhagen

Wedgwood

Waterford

Based on net sales split in 2018

Aug-Sep 2019Aug-Sep 2019

Our locations

Aug-Sep 2019ⓒ Fiskars Group 2019 9

Manufacturing locations

Distribution centers

Our strategic priorities

Aug-Sep 2019ⓒ Fiskars Group 2019 10

Strategy

ⓒ Fiskars Group 2019

Megatrends impacting our business

Conscious society Demographic shifts

ⓒ Fiskars Group 2019 12

Quest for convenience

Aug-Sep 2019

Aug-Sep 2019ⓒ Fiskars Group 2019 13

Fiskars Group vision

Creating a positive, lasting

impact on ourquality of life

creating change

celebrating the everyday

growing with compassion

We are making the everyday extraordinary by…

Fiskars Group values

Aug-Sep 2019ⓒ Fiskars Group 2019 14

Aug-Sep 2019ⓒ Fiskars Group 2019 15

Inspiring people

Growing business

Exciting consumers

Improving performance

Our strategic priorities

Aug-Sep 2019ⓒ Fiskars Group 2019 16

Our approach to sustainability

For Fiskars Group, sustainable business is integral in building long-term economic success.

We work towards our vision to have a positive, lasting impact on our quality of life by acting as a responsible business and pushing ourselves forward in creating positive change.

We see opportunities in embedding sustainability even deeper into our business strategy to provide people meaningful experiences and to make the everyday extraordinary.

SBU Functional

ⓒ Fiskars Group 2019

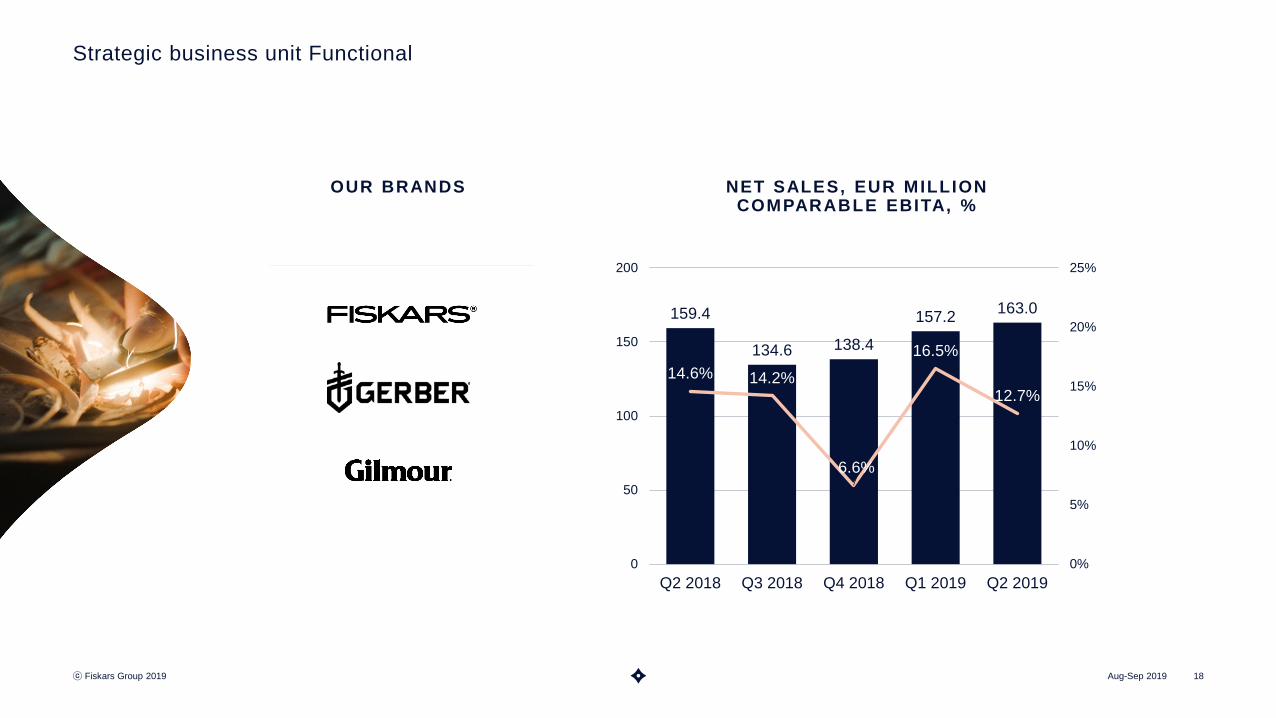

Strategic business unit Functional

OUR BRANDS

Aug-Sep 2019ⓒ Fiskars Group 2019 18

NET SALES, EUR MILLION COMPARABLE EBITA, %

159.4

134.6 138.4

157.2 163.0

14.6% 14.2%

6.6%

16.5%

12.7%

0%

5%

10%

15%

20%

25%

0

50

100

150

200

Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019

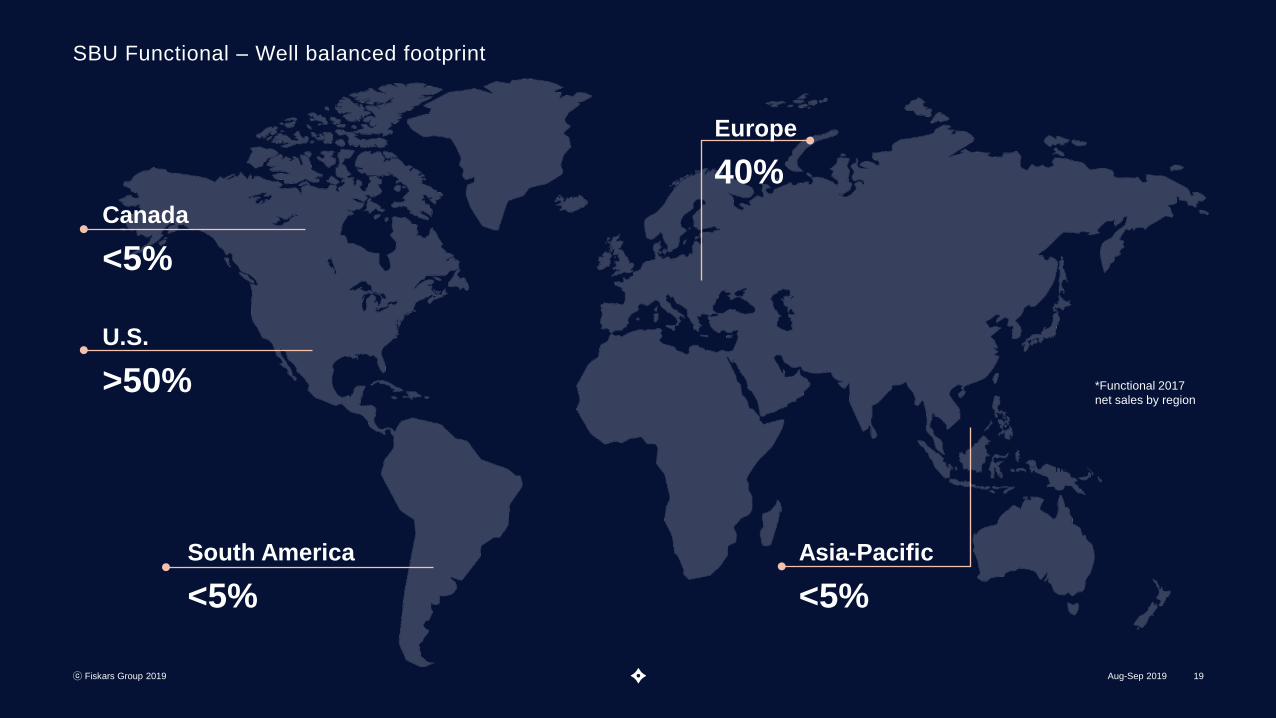

SBU Functional – Well balanced footprint

Aug-Sep 2019ⓒ Fiskars Group 2019 19

U.S.

>50%

South America

<5%

Canada

<5%

Europe

40%

Asia-Pacific

<5%

*Functional 2017 net sales by region

*Functional 2017 net sales by region

SBU Functional – Category split

ⓒ Fiskars Group 2019 20

18% School, office& craft (SOC)

2%Fixing

10% Cooking

13% Watering

13%Outdoor

45% Gardening

*Functional 2017 net sales by category

Aug-Sep 2019

SBU Functional – Sales channels

Aug-Sep 2019ⓒ Fiskars Group 2019 21

Distribution fully through

indirect channels

Work with some of the

largest retailers globally

Strong trade partnerships is one of our

strengths

E-commerce• Total indirect e-commerce: >5% of 2017 net sales• Share of total e-commerce higher in the Americas than other markets

SBU Living

ⓒ Fiskars Group 2019 22Aug-Sep 2019

Strategic business unit Living

OUR BRANDS

Aug-Sep 2019ⓒ Fiskars Group 2019 23

NET SALES, EUR MILLION COMPARABLE EBITA, %

112.4120

184.7

110.5101.3

2.1%

7.3%

23.0%

2.9%

-0.5%

-5%

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019

English and Crystal Living

Scandinavian Living

SBU Living – Well balanced footprint

Aug-Sep 2019ⓒ Fiskars Group 2019 24Risto Gaggl 12.6.2019ⓒ Fiskars Group 2019. Company confidential. 24

U.S.

22%

Europe

52%

Asia-Pacific

26%

*Living 2017 net sales by region

SBU Living – Category split

ⓒ Fiskars Group 2019 25

Dinnerware 45% Drinkware 17% Interior 23% Other 15%

Key

inte

rnat

iona

lbr

ands

Reg

iona

lbra

nds

Key categories by brand (% of Living net sales 2017)

Aug-Sep 2019

SBU Living – Sales channels

Aug-Sep 2019ⓒ Fiskars Group 2019 26

Total e-commerce: ~15%

SHARE OF 2017 NET SALES

Direct: ~33%

Wholesale: ~60%

Hospitality: >5%

Direct channel includes our own:

• Stores (8% of total number of locations)

• Shop-in-shops (64%)• Outlets (28%)

• E-commerce

Indirect e-commerce represents those customers who are operating on online basis only or sell a significant value of our business through e-commerce platforms

New business models

Circular economy is part of Fiskars Group’s sustainability program, and the aim is to find new business opportunities based on it. Circular economy means a new way of thinking in which consumption is based on sharing, renting, recycling, and using services, instead of owning products and manufacturing new ones.The first of new adopted concepts is Vintage, where we buy and sell used Iittala and Arabia-branded tableware. The concept is being rolled out in Finland during 2019.Other concepts are being reviewed as well.

Aug-Sep 2019ⓒ Fiskars Group 2019 27

Financials

ⓒ Fiskars Group 2019

660716 743 748

799 768

1,1071,205 1,186

1,119

33.5%35.4% 35.0%

36.7%

40.9% 41.0%38.7%

42.5% 43.2% 43.4%

25%

30%

35%

40%

45%

50%

55%

60%

0

200

400

600

800

1,000

1,200

1,400

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Group net sales and profitability development

Aug-Sep 2019ⓒ Fiskars Group 2019 29

Net sales, EUR million Comparable gross margin Net sales CAGR

+6%

Comparable EBITA increased in 2018

COMPARABLE EBITA

Aug-Sep 2019 30

75.7

107.1119.0 121.7

45.9 42.16.8%

8.9%10.0%

10.9%

8.5%7.9%

0%

2%

4%

6%

8%

10%

12%

14%

0

20

40

60

80

100

120

140

2015 2016 2017 2018 H1 18 H1 19

Comparable EBITA, EUR millionComparable EBITA margin

14% 14% 12% 12%

11% 10%11%

16%

Q1 Q2 Q3 Q4

Functional Living

19% 17%11%

3%

4%2%

11%32%

Q1 Q2 Q3 Q4

Functional Living

NET SALES COMPARABLE EBITA

ⓒ Fiskars Group 2019 31

Seasonalities creating balanced income profile

Seasonal distribution by quarter and business (average 2016-18). Percentages as share of total full year group figures

Aug-Sep 2019

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Number of Stock Keeping Units Net sales / SKU, EUR

ⓒ Fiskars Group 2019 32

SKU reduction ongoing

Number of Stock Keeping Units (SKU)

Sales / SKU, EUR

Royal Copenhagen

acquired

WWRD acquired

Nelson and Gilmour acquired

Targeting to reach the previous high in sales / SKU

Aug-Sep 2019

-51.9

32.54.9

64.6

-36.2

39.1 40.3

77.5

-46.4

48.624.8

103.5

-39.2

42.7 41.1

92.2

-25.8

48.1

-100

-50

0

50

100

150

200

Q1 15 Q2 15 Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18 Q4 18 Q1 19 Q2 19

Quarterly Rolling 12m

ⓒ Fiskars Group 2019 33

Cash flow has improved

Cash flow from operating activities before financial items and taxes EUR million

Aug-Sep 2019

28.5

42.8

37.4 38.8

43.8

17.8

29.4

0

5

10

15

20

25

30

35

40

45

50

2014 2015 2016 2017 2018 H1 18 H1 19

35.032.4

37.6

32.8

46.2

19.8 18.5

4.6%

2.9% 3.1% 2.8%

4.1%

0%

2%

4%

6%

8%

10%

12%

14%

0

5

10

15

20

25

30

35

40

45

50

2014 2015 2016 2017 2018 Q1 18 Q1 19

Capex as % of sales

DEPRECIATION, AMORTIZATION AND IMPAIRMENT, EUR MILLION

CAPEX, EUR MILLION

ⓒ Fiskars Group 2019 34

Capital expenditure increased in 2018 due to a factory expansion

Depreciation increased as a

result of IFRS 16

Aug-Sep 2019

152.0 148.0135.0

206.6

278.0

0

50

100

150

200

250

300

2016 2017 2018 Q2 18 Q2 19

69% 69% 70% 68%

56%

12% 12% 11%

17%

37%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

2016 2017 2018 Q2 18 Q2 19

Equity ratio Net gearing

NET DEBT, EUR MILLION NET GEARING AND EQUITY RATIO

Aug-Sep 2019ⓒ Fiskars Group 2019 35

IFRS 16 impacting balance sheet

Excluding IFRS 16-impact and Wärtsilä share distribution:

Equity ratio: 71%Net gearing 14%

IFRS 16-impact (yoy) EUR 104 million

Long-term financial targets

Aug-Sep 2019ⓒ Fiskars Group 2019 36

Growth

The average annual net sales growth to exceed 5%, through a combination of organic growth and targeted acquisitions

Profitability

EBITA margin to reach 12%

Capital structure

Net gearing* below 100%

Dividend

Fiskars aims to distribute a stable, over time increasing dividend, to be paid biannually

-5.6% YoY-2.4% YoY (comparable)

10.1% 11% EUR 0.54 per share, paid in two installments of EUR 0.27 per share. Additionally, a distribution of Wärtsilä shares held by Fiskars Group

2018

**Net gearing ratio is the ratio of interest-bearing debt, less interest-bearing receivables and cash and bank equivalents, divided by total equity

Outlook for 2019 (updated on May 17, 2019)

In 2019, Fiskars expects the Group's comparable net sales to be at the same level as in 2018 (unchanged) and comparable EBITA to be below the previous year’s level (previously: at the same level).

The outlook is influenced by the company’s investments in growth initiatives that are expected to add sustainable value in the long-term. In addition, there are continued material risks relating to changes in the operating environment, e.g. Brexit and potential further increases to the U.S. tariffs. An unfavorable outcome of these risks might have a significant impact on the comparable net sales and comparable EBITA. Furthermore, fluctuations in currency rates might also have a considerable impact on comparable EBITA.

Comparable net sales excludes the impact of exchange rates, acquisitions and divestments. Items affecting comparability in EBITA include restructuring costs, impairment charges, integration related costs, acquisitions and divestments, and gain and loss from the sale of businesses.

ⓒ Fiskars Group 2019 37Aug-Sep 2019

Wärtsilä share distribution changed the baseline for dividend growth

ⓒ Fiskars Group 2019 38

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Dividend per share (DPS) history 2009–2018EUR

Extra DividendBase Dividend

0.71

0.35

First dividendSecond dividend

0.520.60

1.30

0.62

0.750.65

2.60

0.67 0.68 0.70 0.72

0.36

0.27

0.27

Wärtsilä share distribution

0.36

0.54

5.31

Aug-Sep 2019

Appendices

ⓒ Fiskars Group 2019 39Aug-Sep 2019

Largest shareholders as of July 31, 2019

ⓒ Fiskars Group 2019 40

# Shareholder name Number of shares % of shares and votes1 Virala Oy Ab 12,650,000 15.44

2 Holdix Oy Ab 10,165,537 12.41

3 Turret Oy Ab 9,330,961 11.39

4 Bergsrådinnan Sophie von Julins Foundation 2,556,000 3.12

5 Oy Julius Tallberg Ab 2,554,350 3.12

6 Varma Mutual Pension Insurance Company 2,469,326 3.01

7 Gripenberg Gerda Margareta Lindsay Dödsbo 1,974,000 2.41

8 Ehrnrooth Jacob Robert Göran 1,626,929 1.99

9 von Julin Sofia Margareta dödsbo 1,560,000 1.90

10 Ehrnrooth Sophia 1,558,630 1.90

10 largest shareholders, total 46,445,733 56.71Other shareholders 35,459,509 43.29

Total 81,905,242 100.00

Data supplied by Euroland

Aug-Sep 2019

Shareholder structure as of July 31, 2019

Aug-Sep 2019 41

Data supplied by Euroland

Sector Number of shareholders

% of total shareholders

Number of shares

% of shares and votes

Private companies 652 2.89% 26788963 32.71%

Households 21,499 95.29% 30,539,606 37.29%

Financial and insurance institutions 43 0.19% 12099507 14.77%

Public sector and non-profit organizations 240 1.07% 10148272 12.39%

Nominee registered and non-Finnish holders 128 0.57% 2328894 2.84%

Total 81,905,242 100.00

32.7%

37.3%

14.8%

12.4%2.8%

Private companies

Households

Financial and insuranceinstitutionsPublic sector and non-profitorganizationsNominee registered and non-Finnish holders

Fiskars Group Leadership Team

ⓒ Fiskars Group 2019 42

Jaana TuominenPresident & CEO

Interim President, SBU Living

Sari PohjonenChief Financial Officer

Deputy to the CEO

Risto GagglChief Supply Chain Officer

Michael HalakPresident, SBU Functional

Tuomas HyyryläinenChief Growth Officer

Niklas LindholmChief Human Resources

Officer

Maija TaimiSVP, Corporate

Communications and Sustainability

Päivi TimonenGeneral Counsel

Aug-Sep 2019

Board of Directors

ⓒ Fiskars Group 2019 43

Paul EhrnroothChairman

Jyri LuomakoskiVice Chairman

Albert Ehrnrooth Louise Fromond

Inka Mero Fabian Månsson Peter Sjölander Ritva Sotamaa

Aug-Sep 2019

Disclaimer

ⓒ Fiskars Group 2019 44

This presentation contains forward-looking statements that reflect management’s current views with respect to certain future events and potential financial performance. Although Fiskars believes that the expectations reflected in such forward-looking statements are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results could differ materially from those set out in the forward-looking statements as a result of various factors.

Important factors that may cause such a difference for Fiskars include, but are not limited to: (i) the macroeconomic development and consumer confidence in the key markets, (ii) change in the competitive climate, (iii) change in the regulatory environment and other government actions, (iv) change in interest rate and foreign exchange rate levels, and (v) internal operating factors.

This presentation does not imply that Fiskars has undertaken to revise these forward-looking statements, beyond what is required by applicable law or applicable stock exchange regulations if and when circumstances arise that will lead to changes compared to the date when these statements were provided.

Aug-Sep 2019

Aug-Sep 2019ⓒ Fiskars Group 2019 45

Makingthe everyday

extraordinary