automobile_car

TRANSCRIPT

Group-1

Dushyant Singh

Sagar Reddy

Saurav Kumar

Roopsa Nath

Rasleen Ahluwalia

Sankalp Singh

AUTOMOBILE INDUSTRYANALYSIS

CONTENTS

1. INTRODUCTION2. GLOBAL SCENARIO FOR CARS3. INDIAN SCENARIO4. MICHEAL PORTER FIVE FORCES MODEL5. HERFINDAHL INDEX6. CONDUCT6. PERFORMANCE ANALYSIS7. FUTURE OUTLOOK

INTRODUCTION

The Automobile sector is divided into four segments Two wheelers Passenger cars Commercial vehicle Three wheelers

The automobile industry impacts on Indian economy

The industry contributes 7 percent to India's GDPThe industry is responsible for 7 to 8 percent of India's total employed population

Source Siam.com

GLOBAL SCENARIO OF PASSENGER CARS

• The passenger car segment has emerged as a major driving force for upstream industries like steel, iron, aluminium, rubber, plastics, glass, and electronics and down stream industries like advertising and marketing, transport and insurance.

• The car industry generates large amount of employment opportunities in the economy. For example in the US, every sixth worker is involved in the making of an automobile.

• The USA and Japan are the leaders with around 42% of the total world market. Major players in the US Market

KPMG Executive automotive summary

Company Name Market Share General Motors Company (GM) 18.70%

Ford Motor Co. (F) 15.90%Toyota Motors Corp. (TM) 15.10%

Chrysler-Fiat 11.30%Honda Motor Co. (HMC) 9.00%

Nissan Motor Co. (NSANY) 7.80%

GLOBAL SCENARIO OF PASSENGER CARS (PRODUCTION)

Source oica.net

Sr. No. Country Cars Production %age1 China 180,85,213 27.662 Japan 81,89,323 12.523 Germany 54,39,904 8.324 USA 43,46,958 6.655 South Korea 41,22,604 6.306 India 31,38,988 4.807 Brazil 27,42,309 4.198 Russia 19,19,636 2.949 Mexico 17,71,987 2.71

10 Spain 17,19,700 2.6311 UK 15,09,762 2.3112 France 14,60,000 2.2313 Czech Rep. 11,28,473 1.7314 Thailand 11,22,780 1.7215 Slovakia 9,75,000 1.4916 Canada 9,65,191 1.4817 Indonesia 9,25,111 1.4118 Turkey 6,33,604 0.9719 Malaysia 5,40,200 0.8320 Iran 5,38,170 0.82

COMPARISON OF WORLD VS INDIAN AUTOMOBILE INDUSTRY

Years World IndiaIndia

contribution in % age

2008 527,26,117 18,46,051 3.50

2009 477,72,598 21,75,220 4.55

2010 583,41,703 28,31,542 4.85

2011 598,97,273 30,40,144 5.08

2012 630,74,662 32,85,496 5.212008 2009 2010 2011 20120

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

Comparison

World Linear ( World) India

Source oica.net

KPMG’s VIEW ON GLOBAL VECHICLE SEGMENT DEFINITIONS

INDIAN SCENARIO

Source- www.siamindia.com

Produced 2.58 million vehicles in August 2013 as against 1.96 million in august 2012

Total vehicles sold were 2.56 million during 2013-2014

Expected growth rate is at 14% during 2012-2021.Exports grew by 2.03 per cent during April-august 2013

Market share of two wheeler is 76.49%, passenger cars is 15.96%, commercial vehicles and three wheelers has 7.55%

Commercial vehicle recorded growth of rate of 20% p.a, passenger vehicle at 15% p.a and three wheeler grew at 11% p.a

SEGMENTWISE SALES

Source- www.siamindia.com

RECENT DEVELOPMENTS IN INDIAN AUTOMOBILE MARKET

• Hero MotoCorp plans to establish 20 manufacturing facilities across 50 countries by 2020

• Maruti Suzuki India Ltd (MSIL) is setting up an operational integrated research & development

(R&D) center in Rohtak, Haryana

• Daimler India Commercial Vehicles (DICV) has expanded its network across the country. The

company plans to establish dealership facilities in over 100 identified locations across India by

2014

• Major Indian Companies • Major Multi-national companies

AUTOMOBILE COMPANIES IN INDIA

INDIAN MARKET SIZE

• Automobile industry has made rapid strides since delicensing

• This industry has attained a turnover of $38.5 billion(INR 165000 crores) and an investment of 10.9 billion

• Generated employment to 13.1 million people both directly and indirectly

• It contributes at 7% towards the GDP of the country

INDUSTRY ASSISTANCE

• Major players like Maruti Suzuki India ltd and Tata Motors has been recording profits of 6% to 11%

• Acute slowdown in production due to rupee dollar crisis

• The passenger vehicle segment saw its sharpest drop in the month of June 2013 with 2,15,146 being produced.

PASSENGER CARS PRODUCTION AND SALES

Source- www.siamindia.com

PORTER’S FIVE FORCES MODEL

• Porter five forces analysis is a framework for industry analysis and business strategy development. To derive five forces that determine the competitive intensity and therefore attractiveness of a market.

Competition among players:

• The competition is very fierce in automobile industry in India.

• Honda (15,714) has grown to the Fourth largest seller in India beating Tata(13,800) and Toyota(10,910).

• BUYER’S POWER

• The Indian market has large number of players (at least 10 ) From

Maruti Suzuki(96,569) to Volkswagen(4,107)

• This has vastly shifted power to customers as there are two to three

options in each price range

SUPPLIER POWER

• Supplier power is very limited in India as the small scale

manufactures are very large in number

• There are about 675 members in ACMA which constitute about 85%

production of India

•Threat of New Entrants:

• The threat of New Entrants is low.• • Capital requirement is high

• Brand image and reputation of existing companies.

• Government regulations for entering into an industry.

•Threats of Substitutes:

• The Threat of Substitutes is low.• • There are many alternative types of Transportation such as Bicycles, motorcycles, trains, buses.

• Substitutes can rarely offer the same convenience.

'HERFINDAHL-HIRSCHMAN INDEX - HHI'

• Herfindahl-Hirschman Index is a measure of the size of firms in relation to the industry• and an indicator of amount of competition among them.

• A HHI index below 0.01 (or 100) indicates a highly competitive index.

• A HHI index below 0.15 (or 1,500) indicates an un concentrated index.

• A HHI index between 0.15 to 0.25 (or 1,500 to 2,500) indicates moderate concentration.

• A HHI index above 0.25 (above 2,500) indicates high concentration

HERFINDAHL INDEXAUTOMOBILE-CARS

Cars Sales Market share HHIDaewoo Motors 221.78 0.21 0.042579Fiat India Auto. 1,922.10 1.79 3.198162

Ford India 6,604.18 6.14 37.75603Gen Motors India 2,940.47 2.74 7.484832

Hind.Motors 722.89 0.67 0.452369Honda Siel Cars 3,936.85 3.66 13.41672Hyundai Motor I 22,103.48 20.57 422.9313Maestro Motors 2.2 0.00 4.19E-06Mahindra Reva 36.34 0.03 0.001143Maruti Suzuki 43,587.90 40.55 1644.676Pal-Peugeot 251.97 0.23 0.05496

Toyota Kirloskar 11,452.21 10.66 113.5343

Volkswagen Group 8,780.65 8.17 66.74241Volkswagen India 4,916.50 4.57 20.92477

107479.5 100 2331.216

Source=Capitaline.com

POLITICAL FACTORS

• In 2002, the Indian government formulated an auto policy that aimed at promoting integrated, phased, enduring and self-sustained growth of the Indian automobile industry

• Allows automatic approval for foreign equity investment up to 100% in the automobile sector and does not lay down any minimum investment criteria.

• Formulation of an appropriate auto fuel policy to ensure availability of adequate amount of appropriate fuel to meet emission norms

Economic factors

• Govt. has granted concessions, such as reduced interest rates for export financing.

• Indian Economy has grown at 9% rate over past 5 years, which drove increase in affordability in population of India. But the predicted growth rate for the current year 2014 is around 4.5% which has an huge impact on sales of passenger as well as commercial vehicles.

• Since changed lifestyle of people, leads to increased purchase of automobiles, so automobile sector have a large customer base to serve.

• Indian customers are highly discerning, educated and well informed. They are price sensitive and put a lot of emphasis on value for money

• Preference for fuel efficient cars with low running costs.

Technological factors

• More and more emphasis is being laid on R & D activities carried out by companies in India

• Customized solutions (designer cars, etc) can be provided with the proliferation of technology

• Internet makes it easy to collect and analyse customer feedback

• With the entry of global companies into the Indian market, advanced technologies, both in product

and production process have developed.

Social factors

• Legal provision relating to environmental pollution by automobiles.

• Legal provisions relating to safety measures.

Environmental factors

• Automobile industry in India in recent years has therefore started to give more importance to greener and eco friendly cars which will considerably reduce the level of carbon emissions

Legal factors

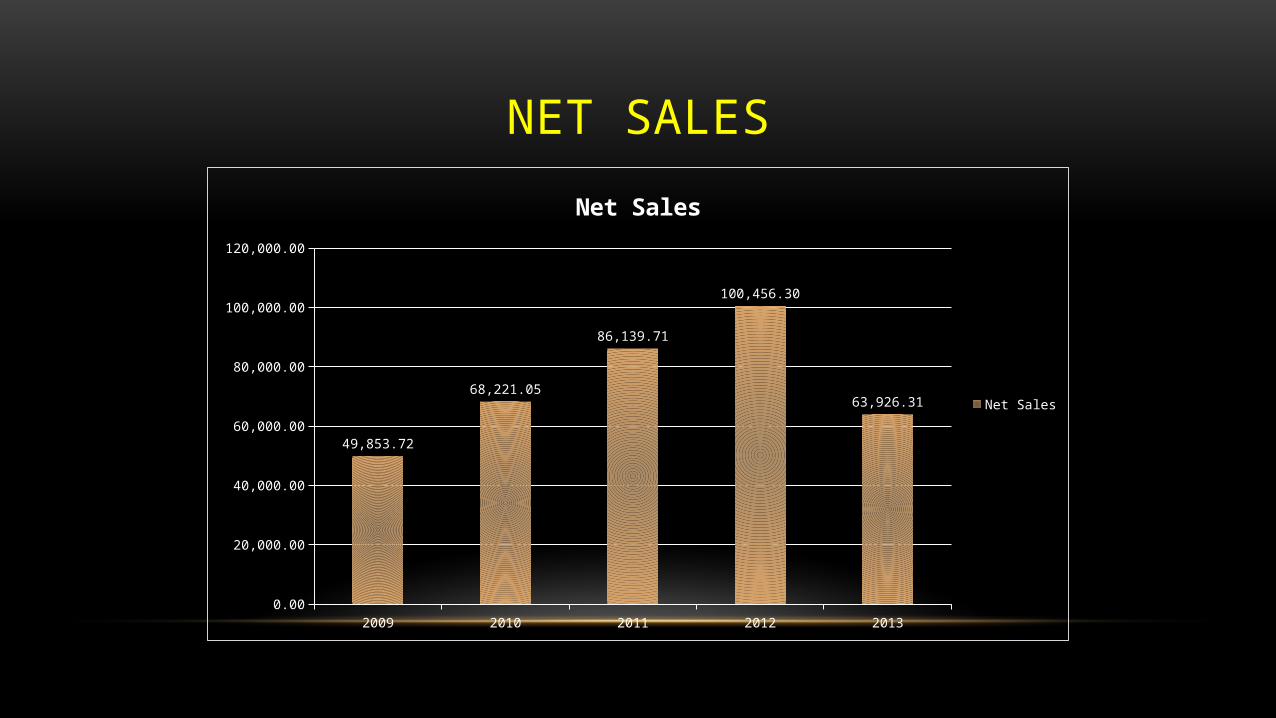

NET SALES

2009 2010 2011 2012 20130.00

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

49,853.72

68,221.05

86,139.71

100,456.30

63,926.31

Net Sales

Net Sales

R&D EXPENDITURE

2009 2010 2011 2012 20130.00

20.00

40.00

60.00

80.00

100.00

120.00

99.40

82.46

28.03

42.70 43.80

R&D

R&DLinear (R&D)

Year Net sales R& D R&D/Net Sales

2009 49,853.72 99.4 0.0020

2010 68,221.05 82.46 0.0012

2011 86,139.71 28.03 0.0003

2012 1,00,456.30 42.7 0.0004

2013 63,926.31 43.8 0.0007

EXPORTS

Year Exports Net Sales Export/ Net Sales2008-09 3,35,729 49,853.72 6.732009-10 4,46,145 68,221.05 6.542010-11 4,44,326 86,139.71 5.1652011-12 5,07,318 1,00,456.31 5.052012-13 5,54,686 63,926.31 8.68

2008-09 2009-10 2010-11 2011-12 2012-130

100,000

200,000

300,000

400,000

500,000

600,000

335,729

446,145 444,326507,318

554,686

Exports

OPERATING PROFIT

2009 2010 2011 2012 20130.00

1,000.002,000.003,000.004,000.005,000.006,000.007,000.008,000.009,000.00

3,180.74

7,111.397,870.77 8,092.81

5,765.78

Operating Profit

Year Net Sales Operating Profit OP/Net Sales

2009 49,853.72 3,180.74 0.064

2010 68,221.05 7,111.39 0.104

2011 86,139.71 7,870.77 0.091

2012 1,00,456.30 8,092.81 0.081

2013 63,926.31 5,765.78 0.090

PERFORMANCE ANALYSIS

India represents one of the world’s largest and fastest growing automobile markets

Increasing large middle class population, improving income levels and strong technological capability have been boosting automobile demand in the country for past few years.

The cumulative production data for April-March 2012 shows production growth of 13.83 percent over same period last year.

Passenger Vehicles segment grew at 4.66 percent during April-March 2012 over same period last year. Passenger Cars grew by 2.19 percent, Utility Vehicles grew by 16.47 percent and Vans by 10.01 percent during this period.

In March 2012, domestic sales of Passenger Cars grew by 19.66 percent over the same month last year.

CAR INDUSTRY PROFITABILITY ANALYSIS

Year Sales

Turnover Operating

Profit Net Profit margin

2004 20,534.69 2,281.86 11.11

2005 28,097.47 3,295.19 11.73

2006 33,893.95 3,751.99 11.07

2007 41,824.98 4,714.36 11.27

2008 48,940.20 5,588.30 11.42

2009 55,073.43 3,180.74 5.78

2010 74,037.23 7,111.39 9.61

2011 94,550.56 7,870.77 8.32

2012 1,07,945.30 8,092.81 7.5

2013 70,544.47 5,765.78 8.17

Latest 1,23,708.87 8,683.06 7.02 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Latest 0

2

4

6

8

10

12

14

Net Profit margin

Year Sales (No. of units)

2007-08 15,49,882

2008-09 15,52,703

2009-10 19,51,333

2010-11 25,01,542

2011-12 26,18,072

2012-13 26,86,429

2007-08 2008-09 2009-10 2010-11 2011-12 2012-130

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

Sales (No. of units)

SALES GROWTH OF CARS

• Significant increase in volumes on MOM basis is something positive for the industry.

• In October 2013, few public sector banks announced cuts of around 0.2% in interest rates for autos

• New launches in 2013 have helped to beat the demand slowdown

FUTURE OUTLOOK

• Better mileage from new efficiency norms

• Government has announced to review the guidelines for passenger cars in 2016

• Exports are expected to increase by 11000 crore

• More improvement in research and development

FUTURE OF THE AUTOMOBILE INDUSTRY

CONCLUSION• The interim budget is positive for the auto industry.

• The growth till now is largely rural centric and festive season, the key trigger is likely to be product launches.