automotive and logistics - barloworld · automotive and logistics division overview...

TRANSCRIPT

Automotive and Logistics

Martin Laubscher

CEO Barloworld Automotive and Logistics

25 March 2013

2

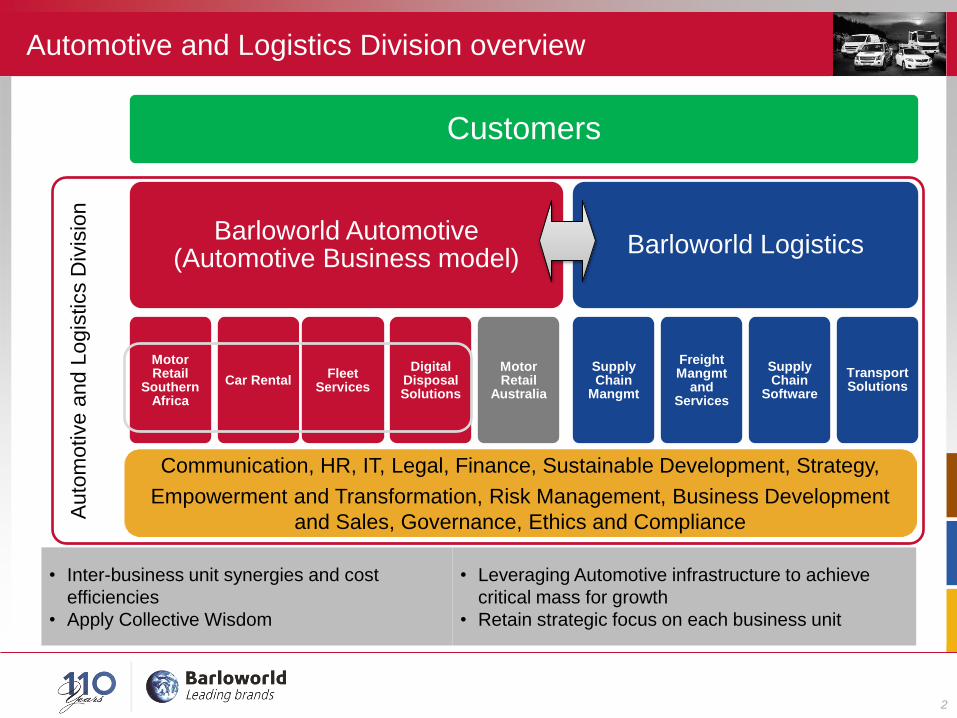

Automotive and Logistics Division overview

• Inter-business unit synergies and cost

efficiencies

• Apply Collective Wisdom

• Leveraging Automotive infrastructure to achieve

critical mass for growth

• Retain strategic focus on each business unit

Customers

Barloworld Automotive (Automotive Business model)

Motor Retail

Southern Africa

Car Rental Fleet

Services

Digital Disposal Solutions

Motor Retail

Australia

Barloworld Logistics

Supply Chain

Mangmt

Freight Mangmt

and Services

Supply Chain

Software

Transport Solutions

Communication, HR, IT, Legal, Finance, Sustainable Development, Strategy,

Empowerment and Transformation, Risk Management, Business Development

and Sales, Governance, Ethics and Compliance Auto

motive a

nd L

ogis

tics D

ivis

ion

3

General Information

Employees 10 611

Countries 16

Automotive Principals Avis; BMW; Chrysler/Fiat; Daimler; Ford;

General Motors; Mazda; Toyota; Volkswagen

Car Rental locations >190

Wholly owned Motor Retail dealerships (SnA & Oz) 40

Key Indicators FY Sep 2011 FY Sep 2012

Rental Days 5.14m 5.71m

New & Used retail units sold 85 092 88 467

Total vehicles under management 195 788 227 019

New vehicles sold per dealership per month 71 76

DTS km’s travelled FY 12 44.3m

SAT tons shipped FY 12 15.575t

Sense of Scale

Automotive and Logistics Division overview

4

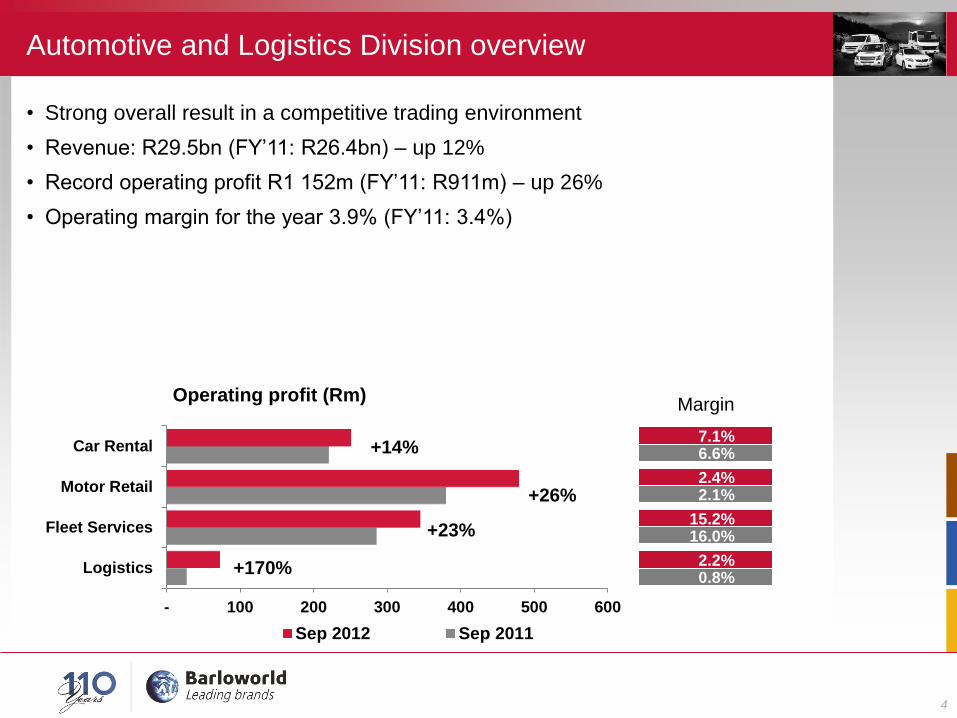

• Strong overall result in a competitive trading environment

• Revenue: R29.5bn (FY’11: R26.4bn) – up 12%

• Record operating profit R1 152m (FY’11: R911m) – up 26%

• Operating margin for the year 3.9% (FY’11: 3.4%)

Automotive and Logistics Division overview

- 100 200 300 400 500 600

Logistics

Fleet Services

Motor Retail

Car Rental

Operating profit (Rm)

Sep 2012 Sep 2011

2.2%

15.2%

2.4%

7.1%

0.8%

16.0%

2.1%

6.6%

Margin

+14%

+26%

+23%

+170%

5

Automotive and Logistics Division overview

• Enhance return on equity

• Continued cash focus

• Targeted capital allocation

• Growing market share

• Optimising vehicle fleets (utilisation)

• Managing working capital levels

• Improving asset turn

• Expense management

• Controlling interest costs

• Implementing Logistics growth strategy

• Exceeding customer expectations

6

Automotive and Logistics Division overview

Emphasis on driving profitable growth and enhancing financial returns

• Secured Lesotho government contract extension in

Avis Fleet Services (AFS)

• AFS secured City of Johannesburg outsourced fleet

management contract for 5 years

• Acquired a minority interest in re – environmental

solutions and waste management business

• Acquired a 50.1% share in Manline and formed

Barloworld Transport Solutions

Corporate activity

Motor Retail

Chris Wierenga (Roland Egger)

Exec: Strategy (CE Motor Retail)

8

Automotive and Logistics Division overview

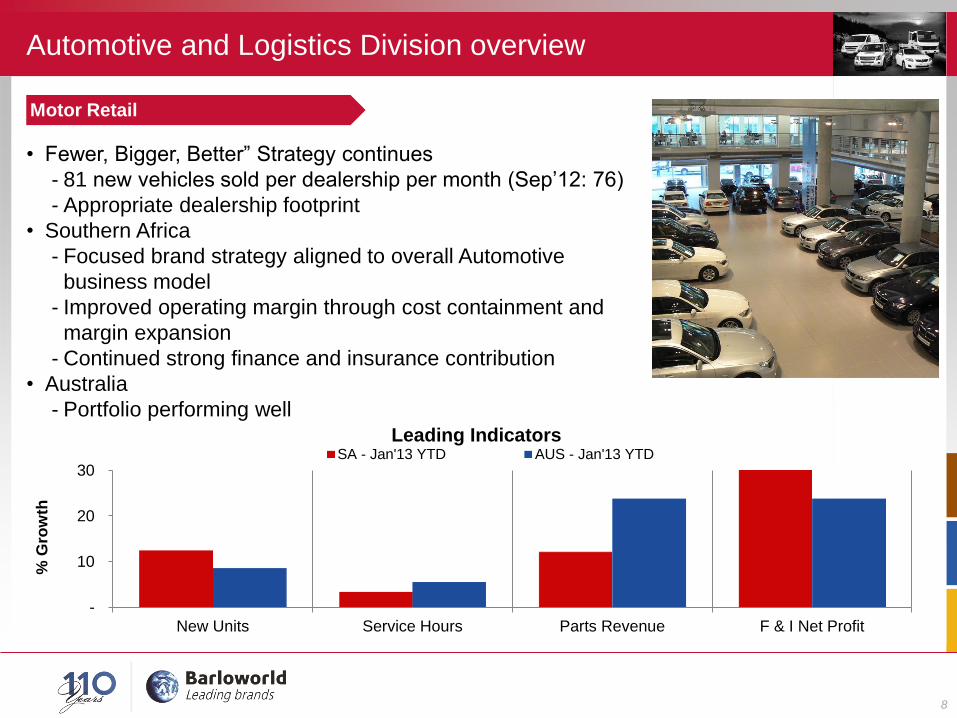

• Fewer, Bigger, Better” Strategy continues

- 81 new vehicles sold per dealership per month (Sep’12: 76)

- Appropriate dealership footprint

• Southern Africa

- Focused brand strategy aligned to overall Automotive

business model

- Improved operating margin through cost containment and

margin expansion

- Continued strong finance and insurance contribution

• Australia

- Portfolio performing well

Motor Retail

-

10

20

30

New Units Service Hours Parts Revenue F & I Net Profit

% G

row

th

Leading Indicators SA - Jan'13 YTD AUS - Jan'13 YTD

9

Automotive and Logistics Division overview

Source: Econometrix

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013F 2014F 2015F 2016F 2017F

Total South African Vehicle Market

Passenger LCV M&HCV

10

Motor retail

• Target operating margin and returns

• Continue to review brands and business mix in line with

changing customer needs

• Entrench “be the Best” culture

• Continuous improvement and innovation of our vehicle disposal

solutions

Automotive and Logistics Division overview

Car Rental

Keith Rankin

CE Car Rental

12

Automotive and Logistics Division overview

• Improved rental days despite prior year Census impact

• Static revenue per day in a competitive environment impacted by

higher replacement volumes (hail storm)

• Continued focus on operating costs

• Fleet utilisation impacted by hail damage

• Continued solid used vehicle profit contribution

• Coach charter integration progressing slowly

• Sustained customer satisfaction above 90%

Car Rental

-5

0

5

10

15

Rental Days Rate Per Day Fleet Utilisation Fleet Size

% G

row

th

Leading Indicators Jan '13YTD Sep '12 YTD

13

Automotive and Logistics Division overview

Car rental

• AvisBudget Group

• Retain market leadership

• Focus on improving quality of the business:

- Yield, fleet planning, acquisition, mix,

utilisation, distribution and disposal

• Environmentally responsible corporate

• CSI >90%

Fleet Services

Clive Else

CE Avis Fleet Services

15

Automotive and Logistics Division overview

• Pleasing performance in low interest rate environment

• Strong financed fleet growth supported by Phakisaworld

acquisition – effective January 2012

• Strong growth in fleets under maintenance

• Good used vehicle profits despite lower margins

• Intelligent Fuel Management enhances overall product

offering

• Secured and renewed significant contracts

Fleet Services

0

10

20

30

Maintenance Fleet Finance Fleet Total Fleet

% G

row

th

Leading Indicators Jan '13 YTD Sep '12 YTD

Logistics

Steve Ford

CE Barloworld Logistics

17

Automotive and Logistics Division overview

Good turnaround and positioned for growth

• Southern Africa

- Ellerines supply chain contract now fully operational

- Higher volumes through Barloworld Equipment

- Recent corporate activity positions business for

growth

• Europe, Middle East and Asia

- Rationalisation and cost control taking effect,

stabilising volumes in sea-air market

- Appointed new local management in Spain and

Far East, however difficult trading conditions persist

- Progressing supply chain management activities in

Dubai

Logistics

18

Automotive and Logistics Division overview

Logistics

• Build a significant integrated logistics

business

• Organic growth through focused business

development team

• Targeted acquisitive growth

• Settle recent acquisitions

Automotive and Logistics

Questions?

Thank you