avalon rare metals initiation of coverage - baystreet rare metals is a research client of edison ......

TRANSCRIPT

20 May 2013

Avalon Rare Metals is a research client of Edison Investment Research Limited

Avalon intends to capitalise on its early mover advantage and develop its heavy rare earth element (HREE) enriched Nechalacho deposit in the Northwest Territories, Canada. It has made significant moves to create strong relationships with future off-take partners, helped in part by strict adherence to its Corporate Sustainability Report, a key differentiator. With demand continuing to outstrip supply globally for valuable heavy rare earths, Avalon’s HREE enriched project is an attractive opportunity to enter the REE space with lower technical risk than many of its peers. We value Avalon on the basis of its April 2013 feasibility study (FS), which results in a value of C$5.44/share (at a 10% discount rate, fully diluted, with a 30% equity sell down for funding). To this should be added C$0.15/share for the value of its current cash balance of C$16m for a total valuation of C$5.59 per share.

Year end Revenue

(C$m) PBT*

(C$m) EPS*

(c) DPS

(c) P/E (x)

Yield (%)

08/11 0.0 (8.8) (9.4) 0.0 N/A N/A 08/12 0.0 (11.2) (10.8) 0.0 N/A N/A 08/13e 0.0 (7.1) (6.9) 0.0 N/A N/A 08/14e 0.0 (12.3) (10.2) 0.0 N/A N/A Note: *PBT and EPS are normalised, excluding intangible amortisation and exceptional items. Revenue stated is interest received.

First major separation plant outside China planned Avalon intends to separate out the majority of the most valuable REEs into individual rare earth oxides at a current capex estimate of c C$423m for the separation plant and associated infrastructure in Louisiana, US (included in the total of US$1,453m). This is an important factor considering the lack of any significant capacity to separate REEs outside of China. A separation plant outside China represents a key de-risking factor for end-users that want to reduce their exposure to Chinese supply and aids Avalon’s objective to establish and maintain market share commensurate with its planned production capacity.

Corporate Sustainability Report a key differentiator Avalon’s Corporate Sustainability Report allows off-take partners of Avalon’s future products to audit their supply chains, which is significant when corporate identity and reputation are as important as securing cheap raw materials and stable supply.

Valuation: Shares at 66% discount Our valuation considers first production at Nechalacho in late-2016, with first cash flows in 2017 and reaching steady state production in 2018. In the light of recent decreases in rare earth and Nechalacho’s other end-product prices, we use conservative pricings (supplied by Avalon due to the opacity of these commodity markets), which results in a dividend discount valuation of C$5.44 per share (at a 10% discount rate and fully diluted). To this should be added C$0.15/share for the value of its current cash balance of C$16m for a total valuation of C$5.59 per share.

Avalon Rare Metals Initiation of coverage

Largest ex-China HREE project

Price C$1.00 Market cap C$104m

Net cash (C$m) as at 31 Aug 2012 38.3

Shares in issue 104m

Free float 96%

Code AVL

Primary exchange TSX

Secondary exchange NYSE

Share price performance

% 1m 3m 12m

Abs 7.5 (17.4) (32.9)

Rel (local) 1.9 (16.9) (39.7)

52-week high/low C$2.35 C$0.93

Business description

Avalon Rare Metals is a mineral development company focused on developing its 100%-owned Nechalacho project in the Northwest Territories, Canada. It also has a number of other exploration-stage rare metals projects in North America.

Next events Interim results July 2013

Analysts Tom Hayes +44 (0)20 3077 5725

Charles Gibson +44 (0)20 3077 5724

Edison profile page

Metals & mining

Avalon Rare Metals | 20 May 2013 2

Investment summary

Company description: Non-Chinese heavy rare earths Avalon is looking to develop its Nechalacho deposit in the Northwest Territories such that first cash flows occur in 2017. In doing so, Avalon will become the first major producer of the most valuable heavy rare earths outside China and also a significant contributor of light rare earths. It will also produce zircon, niobium and tantalum as part of its enriched zirconium product (EZC).

Valuation: Based on most conservative development scenario Our valuation is based on Avalon’s April 2013 feasibility study report on the Nechalacho Rare Earth Elements Project (Nechalacho). In this study, Avalon details a fully integrated process whereby it mines, processes and separates ores into individual rare earth oxides and an enriched zirconium concentrate. Therefore, based on this report and conservative commodity price inputs reflective of current levels provided by Avalon, we value Avalon’s shares at C$5.44 (fully diluted and using a 10% discount rate to reflect general equity risk), to which should be added C$0.15 for the value of its current cash, for a total valuation of C$5.59 per share. Please see page 6 onwards for full valuation details.

Sensitivities: Steady progress Mining companies looking to develop projects are subject to geological, political, development and commodity risk. The following points (refer also to pages 8 and 9) are highlighted as specific to Avalon: MoUs: Avalon has so far secured five crucial memoranda of understanding (MoUs) concerning

off-take of its products, which is critical to securing future revenues from Nechalacho. One of these, announced on 29 January 2013, relates to the future sale of the enriched zirconium concentrate, which in the April feasibility study accounts for c C$189.3m pa at steady state. Avalon continues to pursue market leads to secure further MoUs, including a potential MoU for a magnetite by-product.

Technical issues: Avalon continues to assess and optimise (as set out in its 17 April FS announcement) its process routes for Nechalacho’s ores, both for the future Pine Point facility close to the future Nechalacho mine and also at the future separation facility and refinery, to be situated in Louisiana. The outcome of these optimisation studies will be released to market as and when they are proved successful.

Uranium and thorium: All rare earth projects contain uranium and thorium. The content of these in the Nechalacho deposit is low and not at a level deemed hazardous under international regulations. Furthermore, Avalon has kept all government and First Nation parties fully informed of its intentions to deal with its low uranium and thorium levels.

Commodity risk: Rare earth prices have dropped significantly since the media-hyped rare earth hysteria of late-2010 to mid-2011. However, prices of heavy rare earths remain at high levels due to the lack of supply outside of China.

Financials: Project financing now key The capital requirement for fully developing Nechalacho and the Louisiana separation plant is C$1.453bn (including contingency). We understand that management might look to secure this via a mix of debt and equity. Avalon could sell down 30% of the equity component of Nechalacho to a strategic partner, probably C$270m or 30% of the project NPV (ie c C$0.9bn post-tax at a 10% discount rate). Our estimates assume Avalon will then need to raise around C$35m in equity in 2014 to develop Nechalacho under the scenario given in the April FS and Avalon’s potential

Avalon Rare Metals | 20 May 2013 3

debt/equity financing strategy (page 13). Completion of its major project, such that production occurs in 2016 and first project cash flows in 2017, would require total gross capital outlays of C$1.453bn (this includes capex for the separation plant). Avalon’s stated cash balance at 17 April 2013 was C$16m.

Company description: Valuable rare earth business

Avalon Rare Metals was formed in 1995 and has been involved in the exploration and development of rare metal deposits since 1996, making it one of the most experienced such corporate entities in this mining sub-sector. Along with its flagship Nechalacho deposit it also has a number of lower-priority rare metal projects across the North American continent, which present future upside via farm-out or development. Nechalacho will provide high-technology companies with the first significant supply of heavy rare earth oxides outside China, which currently dominates the market, controlling approximately 95% of supply.

Overview of the rare earths market

A maturing market for rare earths should stabilise prices China is looking to stabilise rare earth prices by opening a rare earth metal exchange in Baotou, Inner Mongolia, and has been implementing policies for years to try to control its own production and exports. Export taxes, non-return of VAT on exports, concentrating ownership within China, limiting foreign ownership, minimum production quantities, production quotas, environmental targets and trying to limit illegal miners, have all had an impact.

These are positive moves in an industry that has experienced large fluctuations in rare earth prices, especially from late-2010 to mid-2011, which also coincided with western media attention focusing on China’s dominance in the industry and news that China was increasing its control of the rare earth supply by decreasing its rare earth export quotas. In 2010 China reduced its export quota to c 30,000t, while rest-of-world (ROW) demand was said to be of the order of 48,000t. These efforts by China are an attempt to clean up its rare earth industry, which was and still is subject to significant illegal mining, processing and sale of rare earths on the black market inside and outside China. Exhibit 1 shows the trends of Chinese demand against ROW demand, as well as Chinese export quotas. Of note is how the difference between ROW demand and Chinese export quotas is widening.

Exhibit 1: Global rare earths demand 2005 to 2016e

Source: Avalon Rare Metals

Note that for 2011 and 2012 rare earth specialist consultancy IMCOA estimates that ROW demand fell, while demand in China increased, due to achieving its goal of attracting and developing more downstream manufacturing of products using rare earth metals. In our view, the divergence in

0

20,000

40,000

60,000

80,000

100,000

120,000

2005 2006 2007 2008 2009 2010 2011e 2012e 2013e 2014e 2015e 2016e

REO

(tpa)

China Demand ROW Demand China Export Quota

Avalon Rare Metals | 20 May 2013 4

Exhibit 1 reflects the aforementioned increased control China is exerting over its supply of rare earth metals to western buyers, and its increasing use and protection of its domestic rare earth resources. IMCOA currently forecasts 9% growth per annum to 2016, which is based on current uses of REE and does not factor in new innovation or applications, which may materialise in the next few years. This presents a clear opportunity to Avalon in particular to meet western demand by developing non-Chinese deposits of rare earths.

LREEs due to enter surplus, with heavy rare earths remaining in deficit At present, China continues to dominate the supply of both light and especially the much more scarce and valuable heavy rare earths metals: it currently supplies c 95% of global demand. Although Exhibit 2 does not take into account the potential price control that China could potentially start to exert as a result of tightening domestic control over its rare earth production, it shows how global aggregate (light and heavy rare earths) supply and demand is set to increase to 2016. This graph takes into account the non-China sources being developed, for example in Canada (eg Avalon’s Nechalacho deposit given in this report), the US (eg the continuing ramp-up of MolyCorp’s Mountain Pass project) and in Australia. The latter has Lynas Corp’s light rare earth Mount Weld project continuing to ramp up. Further, Alkane’s Dubbo zirconium, niobium and rare earths project is due to come online early 2016. However, MolyCorp and Lynas Corp effectively only mine light rare earths. These metals are expected to enter surplus in the next few years as China continues to maintain its dominance in LREE production and Mountain Pass and Mount Weld reach steady state production. Avalon, in developing the Nechalacho deposit by 2016, would become the first significant western producer of rare earths producing c 10ktpa (split 27% HREE and 73% LREE).

Exhibit 2: Rare earth supply and demand

Source: Avalon Rare Metals

Avalon’s website provides basic information on rare earths at: http://avalonraremetals.com/rare_earth_metal/

0

50,000

100,000

150,000

200,000

2005 2006 2007 2008 2009 2010 2011e 2012e 2013e 2014e 2015e 2016e

REO

Dema

nd (t

pa)

China Supply ROW Supply China Demand Total Demand

Avalon Rare Metals | 20 May 2013 5

Securing long-term relationships with off-take partners

The market’s perception of rare earths in 2011 did not take into account the sub-division of rare earths into ‘lights’ and ‘heavies’ and their respective worth. This is now better understood, but not so are the vagaries of rare earth development and the associated implications surrounding the subject of corporate sustainability and responsibility. These are documented within a CSR report. Avalon’s CSR report will be critical in its securing off-take agreements with large established rare earth end-users and maintaining sufficient market share relative to its future production capacity.

The importance of CSR from a mine development viewpoint in the rare earths field, relative to the better understood precious and base metal mining sectors, is not well understood. The CSR is used within the high-technology sector as a means to provide an auditable supply chain linking end products back to the socially responsible production of raw materials. The move away from conflict diamonds to more responsible production is a parallel example of this supply chain auditing. In this context, the CSR is a critical document in the hands of high-technology companies that place a heavy weighting on protecting reputation and do not want adverse media reaction to irresponsible downstream mining practices.

The implications of the CSR in the mining sector, especially concerning rare earths and also Canada’s socioeconomic (First Nations) and environmental backdrop, are far ranging. An inability to prove an auditable responsible supply chain could adversely affect a company’s ability to secure off-take for its products and consequently future revenues. Avalon’s CSR has been compiled within the framework of the Global Reporting Initiative (GRI), Version 3.1. The GRI sets out the principles and performance indicators that help organisations measure and report their economic, environmental and social performance. The GRI is purported to have the most comprehensive sustainability reporting guidelines available today. Avalon’s CSR also incorporates a self-assessment of 2011 performance and sets targets for future years against the Mining Association of Canada’s ‘Toward Sustainable Mining’ indicators.

First Nations – providing economic benefits

First Nation peoples are a key risk factor to the development of mining projects in Canada. Avalon has sought to address this issue by proactively engaging the relevant indigenous parties and also involving them on an economic level by offering equity in the project. This level of involvement should significantly reduce the risks around obtaining key permits required to develop the Nechalacho project. Details of the agreements with the Deninu K'ue follow.

The Deninu K'ue, Yellowknives Dene and Lutsel K’e Dene are the First Nation people and custodians of the lands on which the Thor Lake project is situated. On 7 July 2012, Avalon and the Deninu K’ue reached an Accommodation Agreement providing the Deninu K’ue employment and business opportunities relating to the Thor Lake project, as well as measures to mitigate environmental and cultural impacts that might result from project development. Within this agreement, there are commitments on both parties to ensure timely completion of the environmental impact and development processes at the Thor Lake project. In addition, there is a financial component whereby 10,000 common shares and 50,000 common share purchase warrants (implied dilution of 0.06%) are issued to the Deninu K’ue.

Although the financial details and structure of the agreement have not yet been finalised, Avalon envisages that the Deninu K’ue will become a limited partner after receiving certain permits and approvals. Following these permits and approvals, the Deninu K’ue will acquire 3,333 limited partnership units or a projected total of 100,000. The details of such units have not been finalised

Avalon Rare Metals | 20 May 2013 6

by Avalon. Accommodation agreements with the Yellowknives Dene and Lutsel K’e Dene are also in preparation.

Location of Nechalacho deposit, Thor Lake and Pine Point

The Nechalacho deposit is situated in the Northwest Territories, Canada. Exhibit 3 provides a regional view of the Thor Lake area in which Nechalacho is located, as well as the location of the future process facility at Pine Point and other existing infrastructure.

Exhibit 3: Location of Thor Lake, Pine Point and regional infrastructure

Source: Avalon Rare Metals

Thor Lake and Nechalacho geology – hard rock rare earths The mineral deposits at Thor Lake are generally large tonnage and low grade with assay grades of tantalum, niobium, rare earth elements, yttrium and beryllium typically less than 1% and with zircon grading generally from 1% to 5%. However, the Basal Zone or lowermost portion of the ore body, which will be the sole focus of mining at the Nechalacho deposit, exhibits assay grades of c 2% due to a secondary overprinting event. Geologically, the Thor Lake area exhibits characteristics of an apogranite, which is a rock type formed at the periphery of a parent intrusion, in this case a syenite. Thor Lake deposits also exhibit extensive host rock alteration, as a result of poly-episodic (overprinting) magmatism, which has also resulted in layering of the granites and probable multiple phases of ore mineral deposition. Therefore the Nechalacho deposit located at Thor Lake essentially forms part of a layered, igneous, peralkaline intrusion. This overprinting of a REE enriched peralkaline intrusion, thereby concentrating economic mineralisation in a ‘basal zone’ (see below), has not yet been identified anywhere else in the world.

Mineral zoning aids profit maximisation The model for ore deposition at Thor Lake and specifically the Nechalacho deposit (the largest of the deposits on Avalon’s lease area covering c 2.9km2) indicates an environment of igneous differentiation within a closed system with rare earth element concentration within a residual magma. This differentiation of the parent magma, where separate mineralised zones up to 200m thick have been formed, has allowed for concentrations of the more valuable heavy rare earths to accumulate in a basal zone. This basal zone extends over the majority of the Nechalacho deposit, 1.5km in a north-south and east-west direction.

Avalon Rare Metals | 20 May 2013 7

Exhibit 4: North-south cross section of the Nechalacho deposit

Source: Avalon Rare Metals. Note: Black denotes basal zone HREE mineralisation. The southern end of the deposit is called the Tardiff Lakes Area.

Economic mineralisation within the Nechalacho deposit is contained in an alteration system that affects between 80m and 190m vertically of the Nechalacho ore syenite. This alteration ‘envelope’ contains alternating zones of HREE- and LREE-enriched syenite with accompanying varying concentrations of niobium, tantalum and zircon. Average Total Rare Earth Oxide (TREO) values over the entire alteration envelope are approximately 0.75% to 1.00%, with increased concentrations of rare earths present within more intensely-altered zones. It is these zones of increased alteration that contain the highest grades of TREO, with 2% or higher commonly seen. The basal zone is the main focus of Avalon’s future mining, as it is enriched with the more valuable heavy rare earths (atomic numbers 69 to 73 and also Yttrium and Scandium). Heavy rare earth oxides typically comprise between 7% and 15% of the entire thickness of the alteration envelope. However, they can be typically seen to rise in concentration to over 30% in the basal zone.

Resource and reserves As already stated, the main focus of Avalon’s future mining activities will be to extract the higher-grade heavy rare earth enriched basal zone at Nechalacho. Resources for this fraction of the deposit are given in Exhibit 5.

Exhibit 5: Nechalacho deposit mineral resources at various NMR* cut-offs (resource table dated 26 November 2012) Category and zone

NMR cut-Off

Tonnes TREO HREO HREO/ TREO

ZrO2 Nb2O5 Ta2O5

(US$) (Millions) (%) (%) (%) (%) (%) (%) (%) Measured Basal 320 10.88 1.67 0.38 22.91 3.13 0.41 0.04 Basal 600 6.75 1.98 0.49 24.76 3.79 0.48 0.05 Basal 800 4 2.23 0.59 26.51 4.31 0.54 0.06 Basal 1,000 1.99 2.52 0.7 27.67 4.9 0.61 0.06 Indicated Basal 320 54.95 1.54 0.33 21.63 3.01 0.4 0.04 Basal 600 30.03 1.88 0.45 23.88 3.66 0.47 0.05 Basal 800 14.57 2.18 0.56 25.57 4.21 0.53 0.06 Basal 1,000 5.72 2.52 0.67 26.58 4.79 0.6 0.06 Measured + indicated Basal 320 65.83 1.57 0.34 21.86 3.03 0.4 0.04 Basal 600 36.78 1.9 0.46 24.05 3.68 0.47 0.05 Basal 800 18.57 2.19 0.57 25.78 4.23 0.53 0.06 Basal 1,000 7.71 2.52 0.68 26.86 4.82 0.6 0.06 Inferred Basal 320 59.89 1.28 0.25 19.59 2.7 0.36 0.03 Basal 600 18.68 1.69 0.37 22.14 3.33 0.45 0.04 Basal 800 4.75 2.03 0.51 25.28 3.88 0.51 0.05 Basal 1,000 1.1 2.47 0.63 25.44 4.24 0.56 0.06 Source: Avalon Rare Metals. Note: *NMR is defined as net metal return, or the in situ value of all payable metals, net of estimated metallurgical recoveries and off-site processing costs.

Avalon Rare Metals | 20 May 2013 8

Note that Avalon envisages using an NMR of c US$800/tonne cut-off and its intention is to only mine the basal portion of the Nechalacho deposit. The upper zone will not be mined. See company announcement dated 26 November 2012.

An updated reserve estimate, detailed in the table below, was completed as part of the Feasibility Study. This reserve estimate has resulted in a 15% increase in heavy rare earth grades as well as an 11% increase in both overall rare earth grades; both will have a positive impact on operating margins.

Exhibit 6: Nechalacho reserve statement April 2013 Proven Probable Proven and probable Tonnage (t) 3,682,347 10,917,653 14,600,000 TREO (%) 1.73 1.69 1.70 HREO (%) 0.47 0.45 0.46 HREO/TREO 27.26 26.61 26.78 ZrO2 (%) 3.4042 3.3142 3.3375 Nb2O5 (%) 0.4267 0.4134 0.4167 Ta2O5 (%) 0.0457 0.0451 0.0452 Source: Avalon Rare Metals

The fully diluted proven and probable mineral reserves are set out in Exhibit 6. This estimate includes planned internal dilution averaging 8.5% over the LOM from inferred mineral resources added at zero grade and measured and indicated mineral resources that are below the NMR cut-off of US$320/tonne added at estimated grade. Additional external dilution of 5% was added to tonnage in secondary stopes, about half of all stopes, for an average of approximately 11% total dilution.

Mining – not a core risk As with the vast majority of rare earth deposits being developed, the physical process of mining is not a core risk. This is the case with Nechalacho, which is planned for extraction using conventional room and pillar mining fed to an ore pass, where trackless machinery then transports the ore via a conveyor to the surface for processing. The vertical depth of the basal zone is typically from approximately -150m to -230m below surface, though areas of the basal zone are seen to widen considerably and occur at deeper levels in the southern Tardiff Lakes area of the deposit. Mining is planned to occur at a rate of 2,000 tonnes per day, at a steady rate from year three of operation (2018 under our assumptions).

Processing – Thor Lake and Pine Point The alternative routes that rare earth companies take to extract rare earth oxides from a deposit to provide a saleable product either involve producing a concentrate that contains a mixture of rare earth oxides, or one that produces separated refined earth oxides as the end product. Choosing the route is probably the most key decision a rare earth company will make. This is due to large differences in the capital expenditure required to produce a rare earth oxide concentrate, compared with a process designed to produce the concentrate and then separate refined rare earth oxides. No guaranteed standalone process, as in gold mining with the readily applicable carbon-in-leach technology, exists for rare earth deposits as yet, and the processing of ores containing rare earths is very much at the frontier of mining technology. Avalon has made the critical steps required of a rare earth company in designing a workable flow sheet, which has been used to form the blueprint for the eventual flotation and hydrometallurgical plant designs at its Pine Point and US-based separation plant process facilities.

Capital returns improved via streamlining processing paths The August 2011 Thor Lake PFS includes a cracking process on the concentrate produced at the flotation plant to produce ultimately hydrated rare earth oxide, zirconium, niobium and tantalum

Avalon Rare Metals | 20 May 2013 9

concentrates for sale to market. It is the expense of this cracking process, which includes a combination of acid baking and leaching using significant amounts of sulphuric acid and sodium hydroxide which prompted Avalon to consider alternatives to this part of the process design.

With the level of cost associated with transporting the amounts of the required reagents to the Pine Point hydrometallurgical plant in the Northwest Territories, Avalon has decided that an acid-baking process at Pine Point to produce an intermediate rare earth oxide concentrate containing c 90% LREEs, and over 50% of the HREEs, would be more cost effective. This intermediate concentrate would be sent to a site situated in Louisiana, US (see following section) for further refining into purified separated rare earth oxides and a mixed heavy rare earth carbonate concentrate.

At Pine Point, a second product will also be produced from the acid bake process which contains the remainder of the rare earths as well as the zirconium, niobium and tantalum fractions requiring further aggressive processing treatment. This has been called an enriched zirconium concentrate. Successful laboratory scale evaluations using caustic- or alkali-cracking methods were completed on this residue and included in Avalon’s August 2011 PFS. However, these processes are costly and take time to design and develop at the mine scale, so Avalon has decided to sell the product to a third party for further refining. Avalon has stated that interest in the sale of such a product exists, but has not disclosed details due to normal industry sensitivities surrounding such discussions. This latter point forms part of Avalon’s ongoing optimisation studies.

Processing – heavy rare earth separation and refining As stated above, Avalon will produce an intermediate mixed rare earth oxide product from the Pine Point hydrometallurgical facility. This will be transported via rail to a site in the community of Geismar, Ascension Parish in the State of Louisiana, US, for separation into individual rare earth oxides, which can then be sold to market.

The reason given for locating Avalon’s heavy rare earth separation plant and refinery in the southern US is that the Louisiana site is close to the quantities of processing reagents (hydrochloric acid and sodium hydroxide) needed and to a skilled workforce and sophisticated infrastructure. In addition, Avalon perceives that the overall business environment in the state of Louisiana is preferable to other sites it reviewed. The site chosen is 150 acres in size, which is appropriate to accommodate a plant that can handle the 10,000 tonnes of mixed rare earth oxide concentrate due to be produced at the Thor Lake process plant per year.

The upfront capital cost for the Geismar separation plant and refinery has been estimated at approximately C$375.2m (excluding contingency of C$44.9m) in the April 2013 feasibility study.

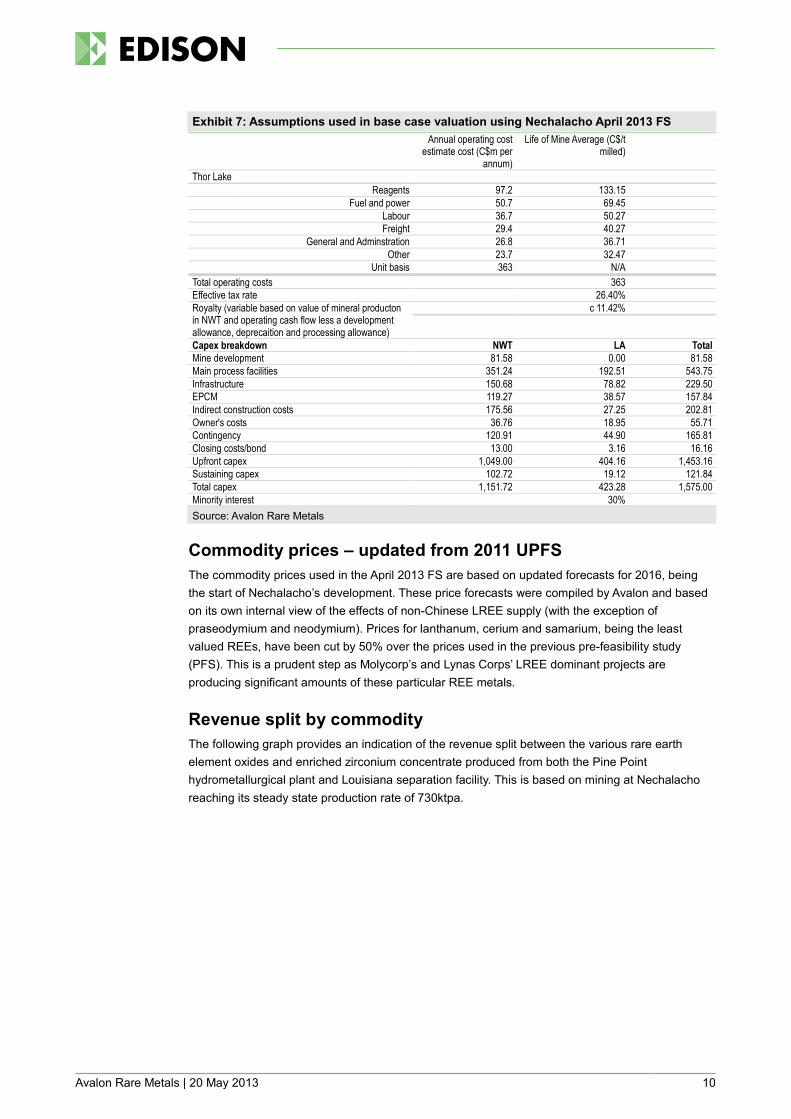

Assumptions and base case valuation

We have used Avalon’s April 2013 FS on the Nechalacho Rare Earth Elements Project.

The overall improvement in project economics from the PFS to the April FS was based not only on increased price assumptions relative to those contained in the original PFS that commenced in 2009, but also the identification of higher-grade heavy rare earth subzones in the Nechalacho deposit’s basal syenite horizons, which has led to the formulation of a more profitable mining schedule. The April FS states a 20-year mine life with a ramp-up period of one year which we have modelled as 2016, based on Avalon’s updated development timeline, increasing to a long-term 2,000tpd in years two (2017) to 20 (2035) with a wind down in 2036. This steady state daily tonnage equates to c 730,00tpa of ore processed.

The main cost assumptions underlying our valuation are given in Exhibit 7.

Avalon Rare Metals | 20 May 2013 10

Exhibit 7: Assumptions used in base case valuation using Nechalacho April 2013 FS Annual operating cost

estimate cost (C$m per annum)

Life of Mine Average (C$/t milled)

Thor Lake Reagents 97.2 133.15 Fuel and power 50.7 69.45 Labour 36.7 50.27 Freight 29.4 40.27 General and Adminstration 26.8 36.71 Other 23.7 32.47 Unit basis 363 N/A Total operating costs 363 Effective tax rate 26.40% Royalty (variable based on value of mineral producton in NWT and operating cash flow less a development allowance, deprecaition and processing allowance)

c 11.42%

Capex breakdown NWT LA Total Mine development 81.58 0.00 81.58 Main process facilities 351.24 192.51 543.75 Infrastructure 150.68 78.82 229.50 EPCM 119.27 38.57 157.84 Indirect construction costs 175.56 27.25 202.81 Owner's costs 36.76 18.95 55.71 Contingency 120.91 44.90 165.81 Closing costs/bond 13.00 3.16 16.16 Upfront capex 1,049.00 404.16 1,453.16 Sustaining capex 102.72 19.12 121.84 Total capex 1,151.72 423.28 1,575.00 Minority interest 30% Source: Avalon Rare Metals

Commodity prices – updated from 2011 UPFS The commodity prices used in the April 2013 FS are based on updated forecasts for 2016, being the start of Nechalacho’s development. These price forecasts were compiled by Avalon and based on its own internal view of the effects of non-Chinese LREE supply (with the exception of praseodymium and neodymium). Prices for lanthanum, cerium and samarium, being the least valued REEs, have been cut by 50% over the prices used in the previous pre-feasibility study (PFS). This is a prudent step as Molycorp’s and Lynas Corps’ LREE dominant projects are producing significant amounts of these particular REE metals.

Revenue split by commodity The following graph provides an indication of the revenue split between the various rare earth element oxides and enriched zirconium concentrate produced from both the Pine Point hydrometallurgical plant and Louisiana separation facility. This is based on mining at Nechalacho reaching its steady state production rate of 730ktpa.

Avalon Rare Metals | 20 May 2013 11

Exhibit 8: Percentage revenue split per rare earth oxide and enriched zirconium concentrate (as of 2018e)

Source: Avalon Rare Metals

Avalon has materially revised its processing routes over those given in the previous PFS, which will produce separated rare earth oxides and an enriched zirconium concentrate containing c 10% LREEs, <50% HREEs and the zircon, niobium and tantalum fractions. The prices for the separated rare earth oxides and enriched zirconium concentrate are given in the table below, with the associated annual tonnages produced.

Exhibit 9: Metal prices and average annual revenues (at steady state production – 2018) REE US$/kg Average annual revenues US

000's REE US$/kg Average annual revenues US

000's Nd2O3 76.78 89,561 Ho2O3 66.35 2,139 Tb2O3 1,055.70 39,378 Pr2O3 75.20 23,987 Dy2O3 688.08 133,740 Er2O3 48.92 3,480 Y2O3 67.25 48,126 Lu2O3 1,313.60 5,948 Eu2O3 1,392.57 43,526 La2O3 8.75 10,278 Sm2O3 6.75 1,472 Ce2O3 6.23 15,529 Gd2O3 54.99 12,636 Tm2O3 N/A N/A Yb2O3 N/A N/A Enriched Zirconium Concentrate Revenue 186,511 Source: Avalon Rare Metals

Note from the above that top five rare earth metals listed on the left-hand side are deemed by Avalon as the most valuable due to their relative scarcity and lack of global production and their use in growing green technologies (ie neodymium is increasingly being used in the growing wind turbine sector). These top five rare earths along with the enriched zirconium concentrate account for approximately 88% of annual revenue generation for Avalon based on our modelling of the Nechalacho rare earth elements project.

If Avalon executes the Nechalacho rare earth elements project as planned and pays out all of its surplus cash in the form of dividends, we estimate that the hypothetical dividend stream to investors from 2013 to 2037 will be worth C$5.44 in current money terms (using a discount rate of 10% to reflect general equity risk).

Our valuation is calculated using a dividend discount model, which is similar to a conventional discounted cash flow model. Further, this variation takes account of all (including corporate) expenditures, rather than just those pertaining to the mine. Our dividend discount model then discounts all free cash produced annually back to current money terms at a base case discount rate of 10% (to reflect general equity risk). This leads to the following EPS and theoretical DPS profile.

Nd2O315.15%

Tb2O36.35%

Dy2O321.76%

Eu2O36.94%

Y2O38.36%

Enriched zirconium concentrate revenue

28.91% La2O31.73% Ce2O3

2.62%Pr2O34.00%

Sm2O30.25%

Gd2O32.03%

Ho2O30.36%

Er2O30.57%

Lu2O30.95%

Tm2O34.16%

Avalon Rare Metals | 20 May 2013 12

Exhibit 10: Edison’s estimate of base case fully-diluted EPS & theoretical EPS, FY13-FY37

Source: Edison Investment Research

Compared with this current value, the maximum hypothetical dividend payment increases to C$11.66 in 2021 as Avalon establishes its mining activities and achieves full production. We consider that the above profile is indicative of a conservative development and processing approach for developing Nechalacho and its ores. Our valuation places Avalon’s current share price at a 91% discount (using a share price of C$1.00), even accounting for the inclusion of C$423m for the separation plant and refinery. To this should be added C$0.15/share for the value of its current cash balance of C$16m for a total valuation of C$5.59 per share.

Sensitivities

Mining companies looking to develop projects are subject to geological, political, development and commodity risk.

The following sensitivities are highlighted as specific to Avalon.

Exhibit 11: Sensitivity to discount rate % 0.0 5.0 10.0 12.5 15.0 20.0 DDF (C$) 24.66 11.09 5.44 3.92 2.87 1.61 Source: Edison Investment Research. Note: A 24.0% discount rate gives Avalon’s current share price as of 16 May 2013.

The following exhibit details the effect of different prices at which Avalon raises the equity portion of its project funding on our dividend discount valuation.

Exhibit 12: Sensitivity to various equity raising prices Price at which equity raised 0.75 1.00 1.50 2.00 2.50 3.00 DDF (C$) 5.02 5.44 5.95 6.23 6.42 6.55 Source: Edison Investment Research

Optimising the April FS process route to maximise profitability

Updating the process by which concentrates are produced at the Pine Point processing plant and then shipped to the separation plant and refinery in Louisiana has positive cost implications. For the base case design in its recently issued feasibility study, Avalon has proposed an acid-baking process using sulphuric acid to produce an intermediate mixed rare earth concentrate containing over 80% of the LREE and about 50% of the HREE, as well as an EZC containing the balance of the HREE and also the zirconium, niobium and tantalum products. In its UPFS, the company proposed a laboratory-tested ‘caustic-cracking’ method using sodium hydroxide after the acid-baking step to further recover the remaining HREE from the EZC. Since the costs of design and construction of the two-stage acid bake-caustic crack method on a commercial scale were relatively high and parties interested in buying the EZC were being identified, Avalon decided to omit the

-2.000.002.004.006.008.00

10.0012.0014.00

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

Cana

dian c

ents

Diluted EPS EPS DPS DDF

Avalon Rare Metals | 20 May 2013 13

caustic-cracking process for the sake of the feasibility study, thereby focusing on the less costly sulphuric acid-bake only process. Caustic cracking continues to remain a potential add-on to the hydrometallurgical flow sheet and may be implemented at a later date, if proved technically and economically viable to do so.

Providing clarity on the sale of Nechalacho’s end products

Obtaining all remaining key operating permits and approvals is a key factor in Avalon achieving first production from Nechalacho in 2016. Associated with such permits and approvals is the securing of sufficient binding agreements for off-take to secure project financing and the availability of equity and debt at a reasonable cost. Whilst the state of equity markets and the global economy is outside of Avalon’s control, we note that it has given no firm guidelines to any of the aforementioned and it will need to do so to maintain market confidence in its claims to achieve first mine production at Nechalacho by 2016.

Avalon has publicly announced eight signed memoranda of understanding (MoUs) with Asian companies of which six are currently active. These companies are looking to participate in the project, either by investing in its development or agreeing to secure off-take, or a combination of both. Three of the eight announced MoUs include provisions for off-take.

All of these parties are located outside of China, either in the US, Asia or the EU. Public policy initiatives in many of these countries are designed to reduce reliance on China for critical raw material supplies. Also, Canada’s new focus on expanding international trade agreements should help Avalon build the necessary international business relationships in these areas.

Processing vs counterparty risk

In overly simplistic terms, there are two main routes to developing rare earth metal deposits. One is Avalon’s proposal to undertake a fully-integrated mine-to-market business strategy. The other is to offload processing risk to a strategic partner by producing mixed rare earth element concentrates, thereby increasing counterparty risk. The latter strategy would require the original parent company (ie Avalon) to either forgo equity or profits in return for negating capital raisings to fund a fully integrated mine-to-market business strategy. Avalon’s integrated mine-to-market strategy, although relatively costly in general mining terms, means that it would be in full control of its revenue generation and not subject to the vagaries of third-party involvement.

Environmental issues – uranium and thorium at Nechalacho

A key sensitivity to investing in rare earth companies is uranium and thorium, their concentration within the resource and how they are dealt with in processing. Note that Lynas Corp has had to deal with further delays to production at its Malaysian processing plant, due to the court ruling on 10 October 2012. This relates to community concerns about radiation risks, which caused a 15% drop in its share price (this followed a similar reaction by the market concerning the same issue in September 2011). While Lynas Corp’s environmental controls are considered top rate, it could not stop local opposition to its processing plant within Malaysia. Furthermore, Lynas Corp’s method of processing involves the complete transport of rare earth and uranium-bearing material from Mount Weld to its Malaysian facility.

By contrast, Avalon has a lower concentration of uranium in its Nechalacho resource than Mount Weld. Its revised process routes, using an acid-bake process, will remove a large amount of uranium from the concentrate shipped to the US for separation (below the 500ppm threshold used in the US before transportation requires further controls and regulation). It has also involved all relevant government and First Nation parties concerning the development of Nechalacho and the issue of uranium content within its ore and process products from the start. Avalon will also develop its Pine Point hydrometallurgical facility on a brownfield site and use existing open pits to discard

Avalon Rare Metals | 20 May 2013 14

waste, although this waste will not contain any uranium or thorium. Furthermore, due to their insolubility in water, uranium and thorium should not pose a risk to surrounding water sources.

Financials

At September 2012, Avalon had cash of C$38m and no debt, which should allow the company to complete its C$64m FS, including the additional studies relating to the separation plant and refinery. We forecast that Avalon will spend C$33.1m in FY13, comprising C$30m for expenditures pertaining to its FS and C$3.1m for exploration expenses based on company guidance. In 2014, we forecast C$4.7m for exploration. Avalon has provided a revised capex profile in the April 2013 FS, which provides detail of expenditures relating both to Nechalacho and Louisiana. For the purposes of our valuation we forecast that C$734m will be used in FY15, C$651m in FY16 and C$67.5m in FY17. Avalon’s end April 2013 cash position was C$16m.

Sustaining capital pa is estimated at between C$0.2m and C$13.7m (this larger amount occurs in 2023 for necessary process plant maintenance). Overall, the total capital outlay for Nechalacho is currently forecast as C$1.453bn (including the Louisiana separation plant capex and excluding sustaining capex). Currently, Avalon is looking to fund the project potentially on a 70% in debt/30% equity basis. Avalon may look to sell 30% of the project for C$270m (which is 30% of the C$900m project valuation after tax and at a 10% discount rate) to a strategic equity partner, leaving a remaining equity requirement of around C$35m. For the purposes of our forecast we assume that Avalon will raise this at a share price of C$1.00 in 2014, resulting in the issuance of c 35m shares (c 25% of the enlarged share capital). This would leave Avalon with an additional funding (intended to be raised as debt) requirement of C$1,206m in 2016 to complete financing of the Nechalacho deposit. We do not forecast debt repayments in our valuation.

We also note that based on Avalon’s current expenditures its end April cash position of C$16m will last until end 2013. The company will be required to address this matter in due course, potentially by bringing forward the aforementioned C$35m equity raise to 2013.

Avalon Rare Metals | 20 May 2013 15

Exhibit 13: Financial summary C$ 000's 2010 2011 2012 2013e 2014e August CAD GAAP IFRS IFRS IFRS IFRS PROFIT & LOSS Revenue 81 0 0 0 0 Cost of Sales 0 0 0 0 0 Gross Profit 81 0 0 0 0 EBITDA (4,634) (9,194) (12,071) (6,285) (12,071) Operating Profit (before amort. and except.) (4,634) (9,367) (12,303) (7,664) (12,276) Intangible Amortisation 0 0 0 0 0 Exceptionals 535 52 45 0 0 Other 0 0 0 0 0 Operating Profit (4,099) (9,315) (12,258) (7,664) (12,276) Net Interest 0 605 1,106 574 (61) Profit Before Tax (norm) (4,634) (8,762) (11,197) (7,090) (12,337) Profit Before Tax (FRS 3) (4,099) (8,710) (11,152) (7,090) (12,337) Tax 0 0 0 0 0 Profit After Tax (norm) (4,634) (8,762) (11,197) (7,090) (12,337) Profit After Tax (FRS 3) (4,099) (8,710) (11,152) (7,090) (12,337) Average Number of Shares Outstanding (m) 77.9 93.1 103.2 103.2 120.7 EPS - normalised (c) (6.0) (9.4) (10.8) (6.9) (10.2) EPS - normalised and fully diluted (c) (6.0) (9.4) (10.0) (6.4) (9.6) EPS - (IFRS) (c) (5.3) (9.4) (10.8) (6.9) (10.2) Dividend per share (c) 0.0 0.0 0.0 0.0 0.0 Gross Margin (%) N/A N/A N/A N/A N/A EBITDA Margin (%) N/A N/A N/A N/A N/A Operating Margin (before GW and except.) (%) N/A N/A N/A N/A N/A BALANCE SHEET Fixed Assets 33,343 51,385 84,043 115,764 120,260 Intangible Assets 0 0 0 0 0 Tangible Assets 33,343 51,385 84,043 115,764 120,260 Investments 0 0 0 0 0 Current Assets 8,184 72,431 40,038 1,738 287,645 Stocks 0 0 0 0 0 Debtors 1,058 650 640 640 640 Cash 6,932 70,859 38,300 0 285,907 Other 194 922 1,098 1,098 1,098 Current Liabilities (2,178) (3,505) (5,464) (5,974) (5,464) Creditors (2,178) (3,505) (5,464) (5,464) (5,464) Short term borrowings 0 0 0 (510) 0 Long Term Liabilities 0 0 0 0 0 Long term borrowings 0 0 0 0 0 Other long term liabilities 0 0 0 0 0 Net Assets 39,349 120,311 118,618 111,528 402,441 CASH FLOW Operating Cash Flow (2,441) (4,822) (6,192) (6,285) (12,071) Net Interest 0 605 1,106 574 (61) Tax 0 0 0 0 0 Capex (incl. Exporation expenditure) (13,476) (17,325) (28,849) (33,100) (4,700) Acquisitions/disposals/strategic partner buy-in 2 0 0 0 270,000 Financing 16,845 85,414 1,524 0 33,250 Dividends 0 0 0 0 0 Net Cash Flow 931 63,871 (32,411) (38,811) 286,418 Opening net debt/(cash) (6,004) (6,932) (70,859) (38,300) 510 HP finance leases initiated 0 0 0 0 0 Other (2) 56 (147) 1 0 Closing net debt/(cash) (6,932) (70,859) (38,300) 510 (285,907) Source: Avalon Rare Metals, Edison Investment Research. Note: Capital expenditure is forecast to ramp up from 2015 under our assumptions.

Avalon Rare Metals | 20 May 2013 16

Contact details Revenue by geography 130 Adelaide St. W Suite 19012 Toronto – ON M5H 3P5 Canada +1 (416) 364-4938 www.avalonraremetals.com

N/A

CAGR metrics Profitability metrics Balance sheet metrics Sensitivities evaluation EPS 2010-14e N/A EPS 2012-14e N/A EBITDA 2010-14e N/A EBITDA 2012-14e N/A Sales 2010-14e N/A Sales 2012-14e N/A

ROCE 13e N/A Avg ROCE 2010-14e N/A ROE 13e N/A Gross margin 13e N/A Operating margin 13e N/A Gr mgn / Op mgn 13e N/A

Gearing 13e N/A Interest cover 13e N/A CA/CL 13e N/A Stock days 13e N/A Debtor days 13e N/A Creditor days 13e N/A

Litigation/regulatory Pensions Currency Stock overhang Interest rates Oil/commodity prices

Management team CEO: Donald S Bubar, Msc, P.Geo VP CFO: R J (Jim) Andersen, CA, CPA (Illinois), CFP Mr Bubar is a geologist with over 30 years’ experience in mineral exploration in Canada. He is also a director of the Prospectors and Developers Association of Canada (PDAC) and was instrumental in the creation of its Aboriginal Affairs Committee in December 2004. He continues to co-chair the committee.

Mr Andersen is a chartered accountant with over 20 years’ experience in the mining industry. He graduated with high distinction from the University of Toronto (BCom) in 1991 and started his career with the mining services team at Coopers & Lybrand in Toronto. He received his CA designation in 1993.

VP Sales and Marketing: Pierre Neatby Senior vice president, metallurgy: Dave Marsh Mr. Neatby spent 19 years with the Noranda/Falconbridge group in various sales and marketing roles, including Managing Director of Noranda's London, UK based sales company.

Mr Marsh brings almost 30 years’ experience in the metallurgical and mineral-processing industries. He has worked in Africa, Australia and Canada. Much of his experience has been in the engineering and technical side of the business.

Principal shareholders (%) Global X Management Company LLC 2.24 Van Eck Associates Corporation 1.68 Bubar (Donald Stephen) 1.21 Manulife Asset Management (US) LLC 1.13 Chilton Investment Company LLC 0.98 Connelly (David) 0.51 UBS Securities LLC 0.45

Companies named in this report Lynas Corp, MolyCorp, Alkane Resources, Arafura Resources

Edison, the investment intelligence firm, is the future of investor interaction with corporates. Our team of over 100 analysts and investment professionals work with leading companies, fund managers and investment banks worldwide to support their capital markets activity. We provide services to more than 400 retained corporate and investor clients from our offices in London, New York, Berlin, Sydney and Wellington. Edison is authorised and regulated by the Financial Services Authority (www.fsa.gov.uk/register/firmBasicDetails.do?sid=181584). Edison Investment Research (NZ) Limited (Edison NZ) is the New Zealand subsidiary of Edison. Edison NZ is registered on the New Zealand Financial Service Providers Register (FSP number 247505) and is registered to provide wholesale and/or generic financial adviser services only. Edison Investment Research Inc (Edison US) is the US subsidiary of Edison and is not regulated by the Securities and Exchange Commission. Edison Investment Research Limited (Edison Aus) [46085869] is the Australian subsidiary of Edison and is not regulated by the Australian Securities and Investment Commission. Edison Germany is a branch entity of Edison Investment Research Limited [4794244]. www.edisongroup.com DISCLAIMER Copyright 2013 Edison Investment Research Limited. All rights reserved. This report has been commissioned by Avalon Rare Metals and prepared and issued by Edison for publication globally. All information used in the publication of this report has been compiled from publicly available sources that are believed to be reliable, however we do not guarantee the accuracy or completeness of this report. Opinions contained in this report represent those of the research department of Edison at the time of publication. The securities described in the Investment Research may not be eligible for sale in all jurisdictions or to certain categories of investors. This research is issued in Australia by Edison Aus and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act. The Investment Research is distributed in the United States by Edison US to major US institutional investors only. Edison US is not registered as an investment adviser with the Securities and Exchange Commission. Edison US relies upon the "publishers' exclusion" from the definition of investment adviser under Section 202(a)(11) of the Investment Advisers Act of 1940 and corresponding state securities laws. As such, Edison does not offer or provide personalised advice. We publish information about companies in which we believe our readers may be interested and this information reflects our sincere opinions. The information that we provide or that is derived from our website is not intended to be, and should not be construed in any manner whatsoever as, personalised advice. Also, our website and the information provided by us should not be construed by any subscriber or prospective subscriber as Edison’s solicitation to effect, or attempt to effect, any transaction in a security. The research in this document is intended for New Zealand resident professional financial advisers or brokers (for use in their roles as financial advisers or brokers) and habitual investors who are “wholesale clients” for the purpose of the Financial Advisers Act 2008 (FAA) (as described in sections 5(c) (1)(a), (b) and (c) of the FAA). It is not intended for retail clients. This is not a solicitation or inducement to buy, sell, subscribe, or underwrite any securities mentioned or in the topic of this document. This document is provided for information purposes only and should not be construed as an offer or solicitation for investment in any securities mentioned or in the topic of this document. Edison has a restrictive policy relating to personal dealing. Edison Group does not conduct any investment business and, accordingly, does not itself hold any positions in the securities mentioned in this report. However, the respective directors, officers, employees and contractors of Edison may have a position in any or related securities mentioned in this report. Edison or its affiliates may perform services or solicit business from any of the companies mentioned in this report. The value of securities mentioned in this report can fall as well as rise and are subject to large and sudden swings. In addition it may be difficult or not possible to buy, sell or obtain accurate information about the value of securities mentioned in this report. Past performance is not necessarily a guide to future performance. Forward-looking information or statements in this report contain information that is based on assumptions, forecasts of future results, estimates of amounts not yet determinable, and therefore involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of their subject matter to be materially different from current expectations. For the purpose of the FAA, the content of this report is of a general nature, is intended as a source of general information only and is not intended to constitute a recommendation or opinion in relation to acquiring or disposing (including refraining from acquiring or disposing) of securities. The distribution of this document is not a “personalised service” and, to the extent that it contains any financial advice, is intended only as a “class service” provided by Edison within the meaning of the FAA (ie without taking into account the particular financial situation or goals of any person). As such, it should not be relied upon in making an investment decision. To the maximum extent permitted by law, Edison, its affiliates and contractors, and their respective directors, officers and employees will not be liable for any loss or damage arising as a result of reliance being placed on any of the information contained in this report and do not guarantee the returns on investments in the products discussed in this publication. FTSE International Limited (“FTSE”) © FTSE 2013. “FTSE®” is a trade mark of the London Stock Exchange Group companies and is used by FTSE International Limited under license. All rights in the FTSE indices and/or FTSE ratings vest in FTSE and/or its licensors. Neither FTSE nor its licensors accept any liability for any errors or omissions in the FTSE indices and/or FTSE ratings or underlying data. No further distribution of FTSE Data is permitted without FTSE’s express written consent.

Berlin +49 (0)30 2088 9525 Friedrichstrasse 95 10117 Berlin Germany

London +44 (0)20 3077 5700 280 High Holborn London, WC1V 7EE United Kingdom

New York +1 646 653 7026 245 Park Avenue, 39th Floor 10167, New York US

Sydney +61 (0)2 9258 1162 Level 33, Australia Square 264 George St, Sydney NSW 2000, Australia

Wellington +64 (0)4 8948 555 Level 15, 171 Featherston St Wellington 6011 New Zealand