aviva investors g7 fixed income fundpolitics.leics.gov.uk/documents/s78839/presentation by...

TRANSCRIPT

AVIVA INVESTORS G7 FIXED INCOME FUND

Prepared for professional clients and /or qualified investors only. It is not to be viewed by or used with retail clients

April 2013

IMPORTANT INFORMATION

NOT FOR PUBLIC DISTRIBUTION

The distribution and offering of shares may be restricted by law in certain jurisdictions. The content of thisdocument should not be viewed as an offer or solicitation to subscribe for shares of the fund by anyone in anyjurisdiction in which such an offer or solicitation is not lawful or in which the person making such offer orsolicitation is not qualified to do so or to anyone to whom it is unlawful to make such an offer or solicitation.

This presentation is for information purposes only and is not intended for and may not, without the express consent ofAviva Investors, be distributed to, and may not be relied upon by, any other party, including, without limitation, anyadvisory or other client of the recipient.

The Aviva Investors G7 Fixed Income Fund is a Cell of Aviva Investors Alternative Funds PCC Limited, a protected cellinvestment company incorporated in Guernsey.

This presentation is not available for general distribution in, from or into the United Kingdom because the Aviva InvestorsG7 Fixed Income Fund is an unregulated collective investment scheme whose promotion is restricted by sections 238 and240 of the Financial Services and Markets Act 2000. When distributed in, from or into the United Kingdom, this documentis only intended for persons having professional experience of investing in unregulated schemes, high net worthcompanies, partnerships, associations or trusts and personnel of any of the foregoing having professional experience ofinvesting in unregulated schemes (each within the Financial Services and Markets Act 2000 (Promotion of CollectiveInvestment Schemes) (Exemptions) Order 2001), persons outside the European Economic Area receiving it electronically,persons outside the United Kingdom receiving it non-electronically and any other persons to whom it may becommunicated lawfully. No other person should act or rely on it.

2

G7 Fixed Income Fund

1 Performance review

2 Investment philosophy and process

3 What are we focusing on?

4 Risk management

Appendix 1: The capability

Appendix 2: Key terms and investor breakdowns

Appendix 3: Trade examples

Appendix 4: Biographies

Appendix 5: Introduction to Aviva Investors

Appendix 6: GIPS performance & disclosures

AGENDA

G7 Fixed Income Fund

1. PERFORMANCE REVIEW

4

G7 Fixed Income Fund

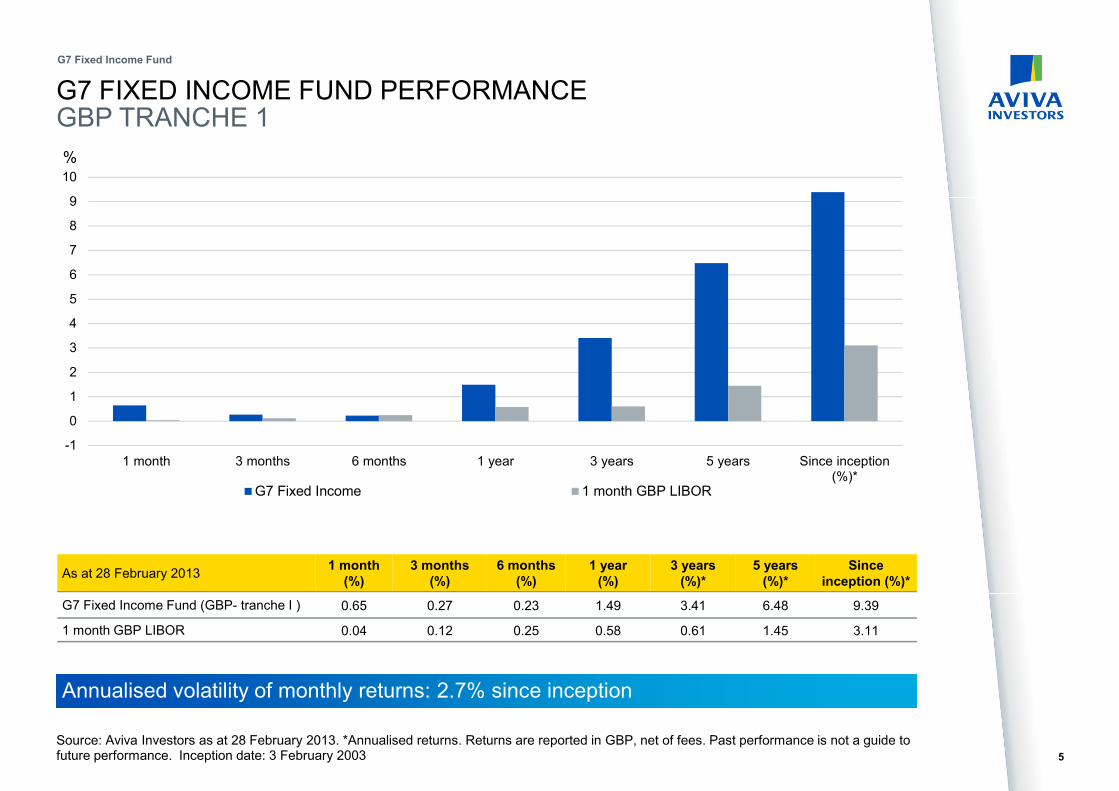

Source: Aviva Investors as at 28 February 2013. *Annualised returns. Returns are reported in GBP, net of fees. Past performance is not a guide to future performance. Inception date: 3 February 2003

Annualised volatility of monthly returns: 2.7% since inception

As at 28 February 20131 month (%)

3 months (%)

6 months(%)

1 year (%)

3 years (%)*

5 years (%)*

Since inception (%)*

G7 Fixed Income Fund (GBP- tranche I ) 0.65 0.27 0.23 1.49 3.41 6.48 9.39

1 month GBP LIBOR 0.04 0.12 0.25 0.58 0.61 1.45 3.11

-1

0

1

2

3

4

5

6

7

8

9

10

1 month 3 months 6 months 1 year 3 years 5 years Since inception(%)*

G7 Fixed Income 1 month GBP LIBOR

G7 FIXED INCOME FUND PERFORMANCEGBP TRANCHE 1

5

G7 Fixed Income Fund

%

PORTFOLIO RETURNS SO FAR…

G7 Fixed Income Fund

6

• Our modest returns this year have masked the underlying volatility we see in individual positions,

demonstrating to us that our portfolios will generate a good return if we get our calls right

• Equally we feel pleased with our risk management over the year as that has kept us the right side of

zero in a year when many macro funds have struggled with negative returns

• We continue to focus on identifying genuine alpha* and not simply introducing carry and beta** bias

into our portfolios

• Capturing alpha in this environment is tricky if you are wary of the risks you expose your portfolio to

•

• Sure there are plenty of carry and roll-down trades available, though most are crowded, and many

investors seem happy to reap risk premia on the basis that central banks will protect against the risks

that those premia are supposedly based on

• But neither of those are alpha trades, they’re beta at best

• Alpha opportunities do present themselves although timing is more important now than ever and it’s

hard for a cautious investor to justify the size of position that might have been used pre-crisis

• We’ve further developed our process to help enhance the timing element, hopefully keeping us out of

trouble when the risks are too great, but allowing us to capture alpha conservatively when it is

reasonable to do so

*alpha – the amount by which a portfolio outperforms the market due to the skill of the manager in choosing investments.

**beta – An estimate of how much an individual stock will move given a change in the market in the overall level of the market of which it forms part. Also, the return from any

portfolio or stock which is the result of being part of a particular market.

RISKS SIMILARITIES POST 2008 VERSUS NOW

2008

• Post 2008 much criticism was made of collateralised debt obligations, engineered to have few risks while

offering very attractive yields.

• There is now a realisation that the risks had just been pushed into the extreme tails and materialised only

in an event that no-one thought would happen, a housing market crash.

Now

• Now, we see the US, UK and European Central Banks are supporting risk assets, supposedly removing

the tail-risks

• This leaves the extreme tail-risk that central banks fail in their efforts, or change course (by choice or by

force) - leaving risk assets exposed to a major sell off

• But no-one thinks that’s going to happen!

• You don’t have to believe that will happen but surely the parallels in risk management between 2008 and

now concern us.

7

G7 Fixed Income Fund

GOING FORWARD…

G7 Fixed Income Fund

8

• We are starting to find attractively priced medium to longer term volatility positions in some markets

and are looking to implement more tail hedges and blow-up trades

• Asset swap behaviour is returning to normal, being driven more by supply and demand than

dominated by risk-on, risk-off sentiment

• Allows us to exploit opportunities in this space more assertively as we won’t simply be adding risk to

our big macro call that we are expressing elsewhere in our book

• Another theme we see developing is the structural deterioration in Japan.

• While this is a call that has been made previously and not worked, we see the change in the current

account balance as being a key difference this time

• The recent current account deficit may be a short-term one-off but we doubt Japan will return to

running a significant surplus anytime soon

• There is also plenty of government issuance to come this year which will continue to provide an

opportunity set for us, and we expect more genuine macro plays to occur over next year as well

• We feel that the success of central banks this year in forestalling any build up in market concerns was

fortuitous and will be a tough act to repeat next year

• So we remain cautiously optimistic of our return prospects in the near future, if pretty pessimistic still

on the likelihood of policy makers getting to grips with solving the problems western economies are

facing

2. INVESTMENT PHILOSOPHY AND PROCESS

9

G7 Fixed Income Fund

OUR INVESTMENT PHILOSOPHY

We believe that most trading opportunities arise from major economic themes and market dislocations

A deep understanding of economic drivers and market dynamics enables investors to earn excess

returns by exploiting these opportunities. To do this well requires:

Ability to identify trends and exploit the markets’ tendency to overreact

Disciplined management of downside risks

Diversified sources of added value

10

G7 Fixed Income Fund

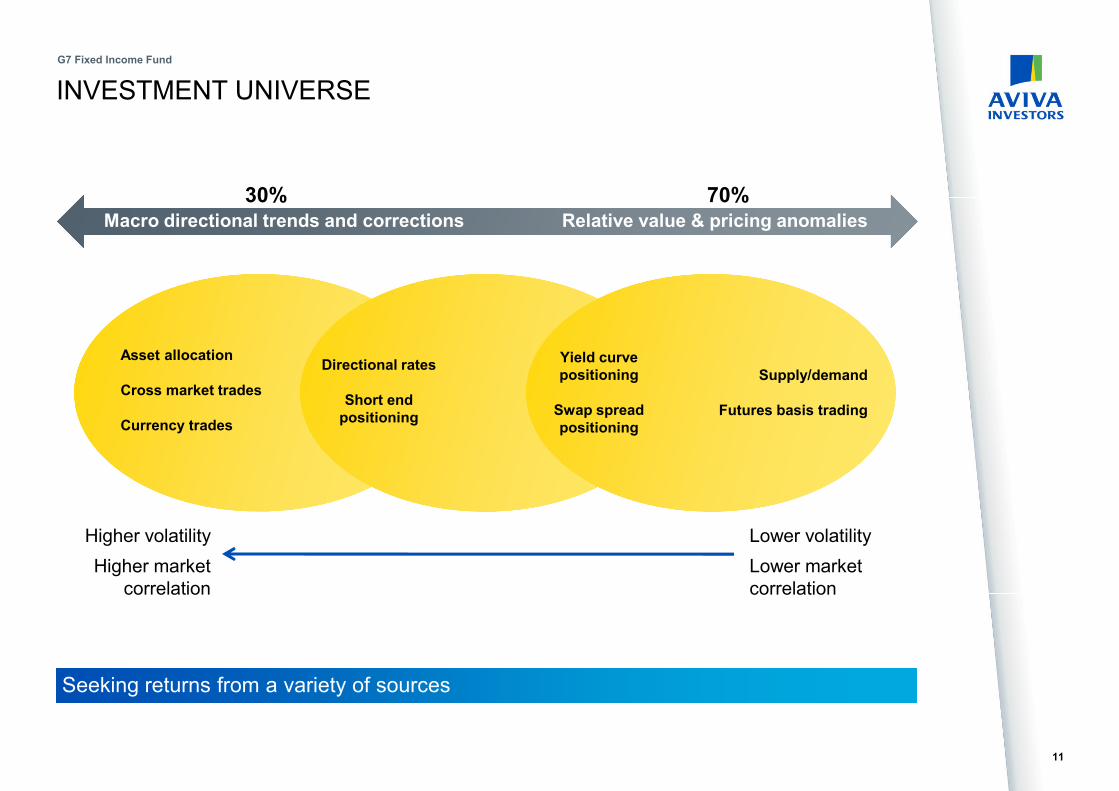

INVESTMENT UNIVERSE

Macro directional trends and corrections Relative value & pricing anomalies

Seeking returns from a variety of sources

Higher volatility

Higher market

correlation

Lower volatility

Lower market

correlation

Asset allocation

Cross market trades

Currency trades

Directional rates

Short end positioning

Yield curve positioning

Swap spread positioning

Supply/demand

Futures basis trading

30% 70%

11

G7 Fixed Income Fund

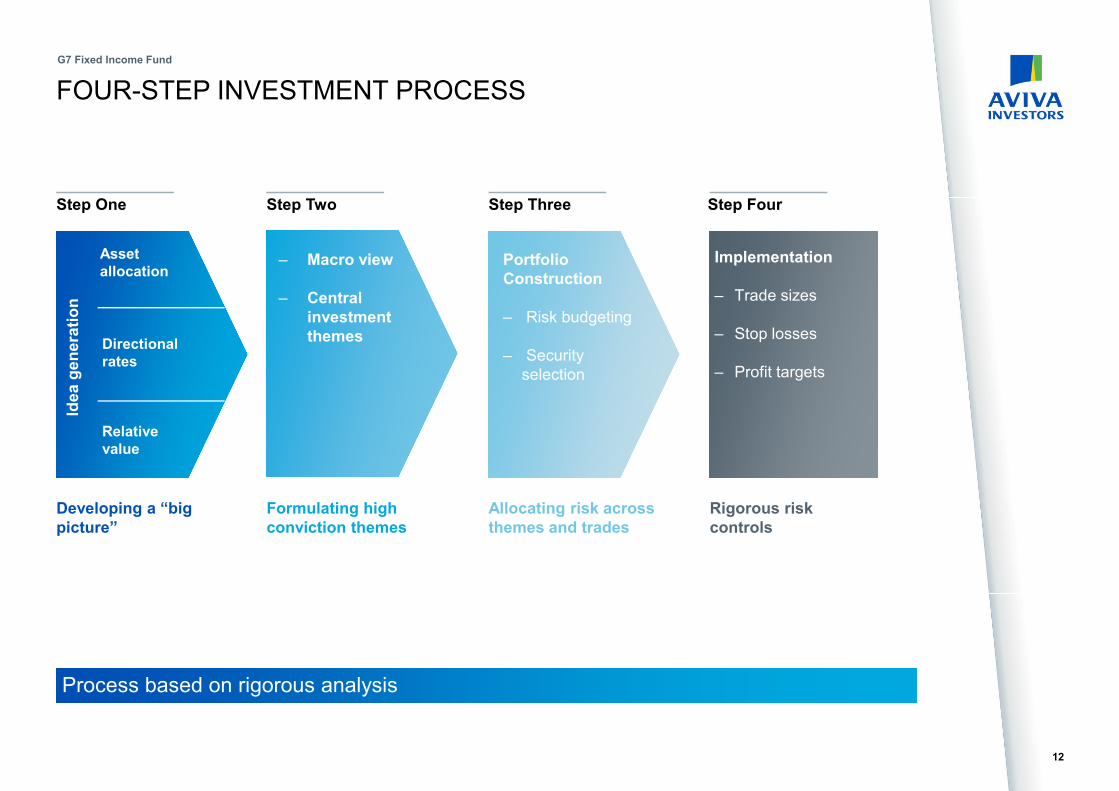

FOUR-STEP INVESTMENT PROCESS

Process based on rigorous analysis

Step One Step Two Step Three Step Four

Implementation

– Trade sizes

– Stop losses

– Profit targets

Idea generation

Asset allocation

Directional rates

Relative value

– Macro view

– Central investment themes

Portfolio Construction

– Risk budgeting

– Security

selection

Developing a “big picture”

Formulating high conviction themes

Allocating risk across themes and trades

Rigorous risk controls

12

G7 Fixed Income Fund

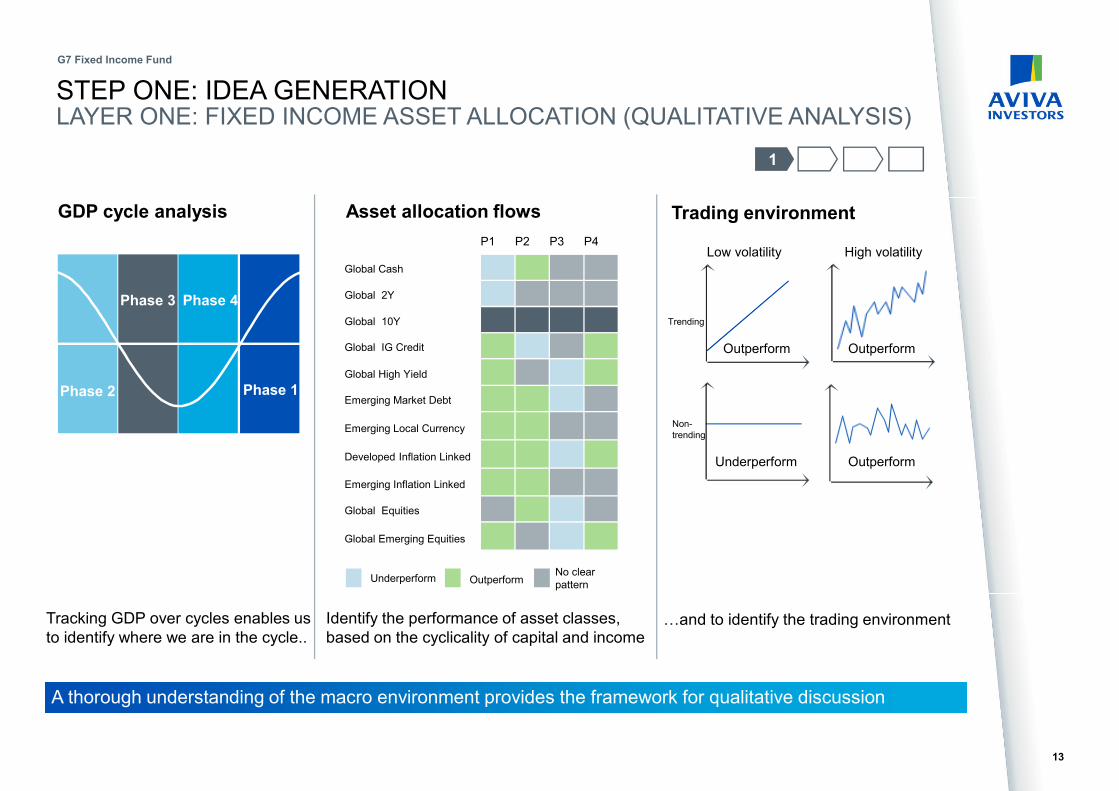

STEP ONE: IDEA GENERATIONLAYER ONE: FIXED INCOME ASSET ALLOCATION (QUALITATIVE ANALYSIS)

A thorough understanding of the macro environment provides the framework for qualitative discussion

Phase 2

Phase 3 Phase 4

Phase 1

Outperform

OutperformUnderperform

Low volatility High volatility

Non-

trending

Trending

Outperform

1

GDP cycle analysis Trading environment

Tracking GDP over cycles enables us

to identify where we are in the cycle..

Identify the performance of asset classes,

based on the cyclicality of capital and income …and to identify the trading environment

P1 P2 P3 P4

Global Cash

Global 2Y

Global 10Y

Global IG Credit

Global High Yield

Emerging Market Debt

Emerging Local Currency

Developed Inflation Linked

Emerging Inflation Linked

Global Equities

Global Emerging Equities

OutperformUnderperformNo clear

pattern

Asset allocation flows

13

G7 Fixed Income Fund

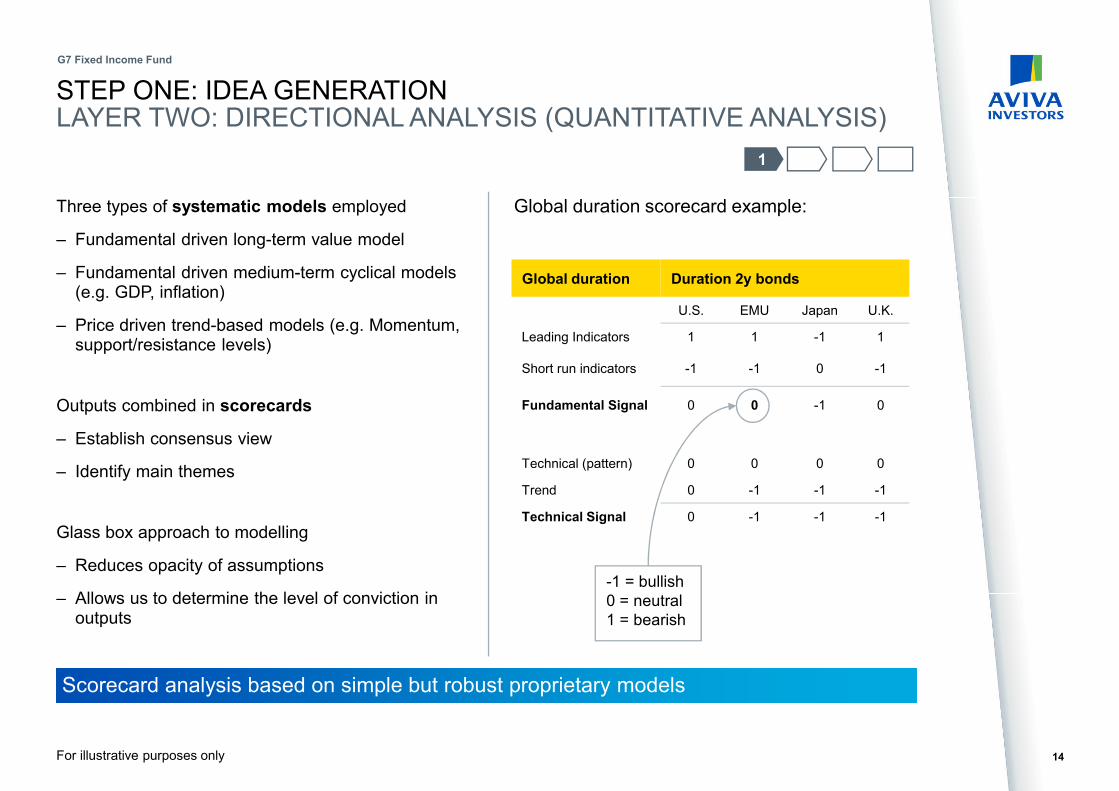

STEP ONE: IDEA GENERATIONLAYER TWO: DIRECTIONAL ANALYSIS (QUANTITATIVE ANALYSIS)

Three types of systematic models employed

– Fundamental driven long-term value model

– Fundamental driven medium-term cyclical models (e.g. GDP, inflation)

– Price driven trend-based models (e.g. Momentum, support/resistance levels)

Outputs combined in scorecards

– Establish consensus view

– Identify main themes

Glass box approach to modelling

– Reduces opacity of assumptions

– Allows us to determine the level of conviction in outputs

For illustrative purposes only

Global duration scorecard example:

Scorecard analysis based on simple but robust proprietary models

-1 = bullish

0 = neutral

1 = bearish

1

Global duration Duration 2y bonds

U.S. EMU Japan U.K.

Leading Indicators 1 1 -1 1

Short run indicators -1 -1 0 -1

Fundamental Signal 0 0 -1 0

Technical (pattern) 0 0 0 0

Trend 0 -1 -1 -1

Technical Signal 0 -1 -1 -1

14

G7 Fixed Income Fund

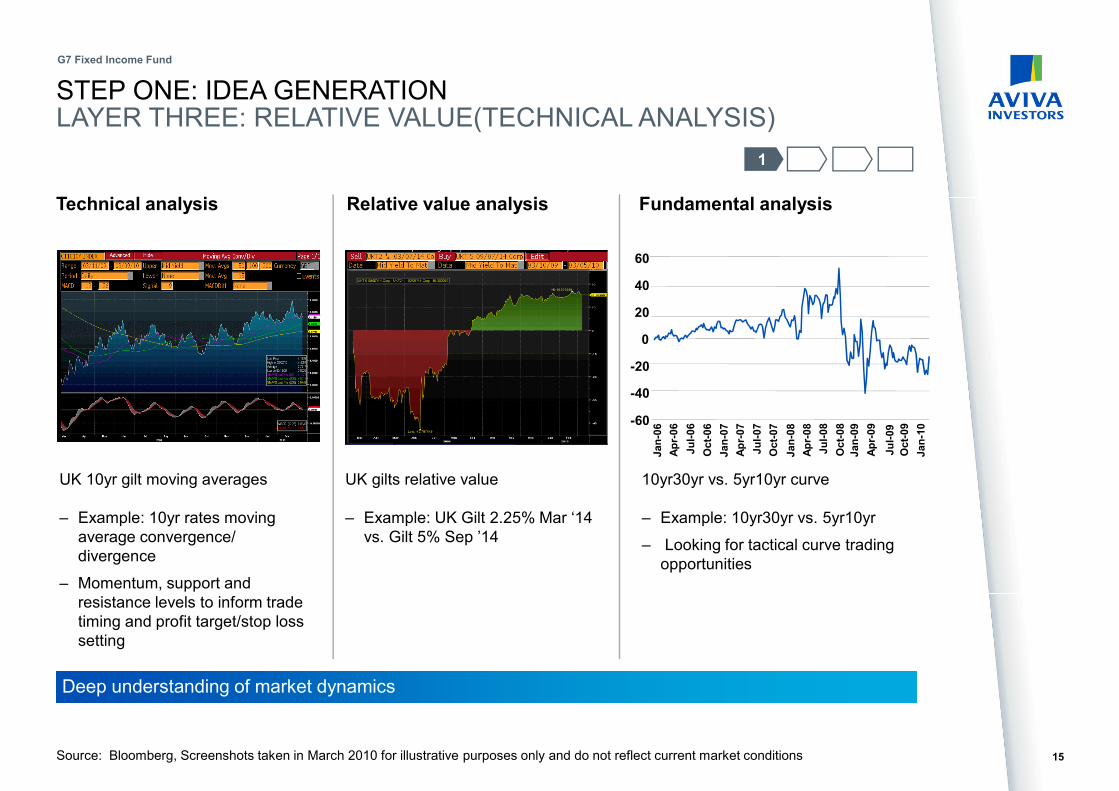

STEP ONE: IDEA GENERATIONLAYER THREE: RELATIVE VALUE(TECHNICAL ANALYSIS)

Source: Bloomberg, Screenshots taken in March 2010 for illustrative purposes only and do not reflect current market conditions

Deep understanding of market dynamics

Technical analysis Relative value analysis Fundamental analysis

UK 10yr gilt moving averages

– Example: 10yr rates moving

average convergence/

divergence

– Momentum, support and

resistance levels to inform trade

timing and profit target/stop loss

setting

UK gilts relative value

– Example: UK Gilt 2.25% Mar ‘14

vs. Gilt 5% Sep ’14

Jan-06

Apr-06

Jul-06

Oct-06

Jan-07

Apr-07

Jul-07

Oct-07

Jan-08

Apr-08

Jul-08

Oct-08

Jan-09

Apr-09

Jul-09

Oct-09

Jan-10-60

-40

-20

0

20

40

60

10yr30yr vs. 5yr10yr curve

– Example: 10yr30yr vs. 5yr10yr

– Looking for tactical curve trading

opportunities

1

15

G7 Fixed Income Fund

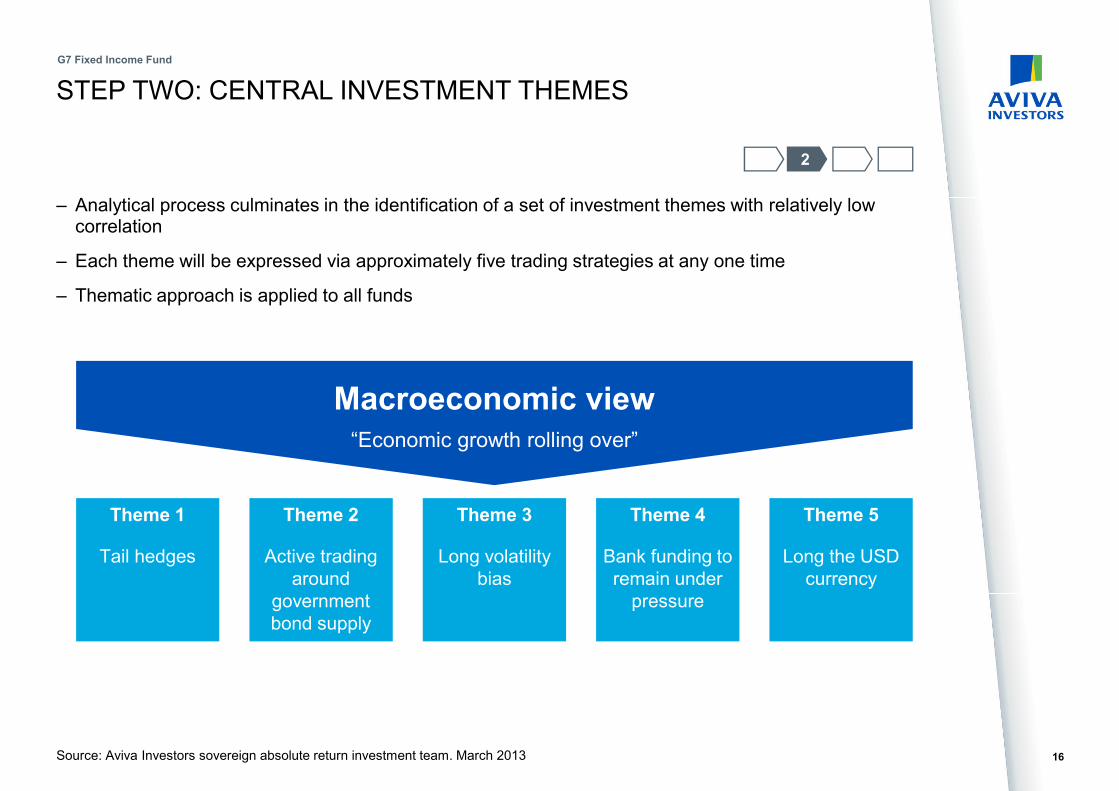

STEP TWO: CENTRAL INVESTMENT THEMES

Source: Aviva Investors sovereign absolute return investment team. March 2013

– Analytical process culminates in the identification of a set of investment themes with relatively low correlation

– Each theme will be expressed via approximately five trading strategies at any one time

– Thematic approach is applied to all funds

2

Theme 2

Active trading

around

government

bond supply

Theme 3

Long volatility

bias

Theme 5

Long the USD

currency

Theme 4

Bank funding to

remain under

pressure

Macroeconomic view“Economic growth rolling over”

Theme 1

Tail hedges

16

G7 Fixed Income Fund

STEP TWO: CENTRAL INVESTMENT THEMES

Source: Aviva Investors sovereign absolute return investment team, March 2013. This slide is for illustrative purposes only and does not purport to show the fund’s current positions.

2

Theme Type Market Instruments

Tail hedges Directional Euro/US/JPY Swaptions, bonds options

Active trading around

government bond supplyRelative value UK/Euro/US

Government bonds (outright or

against swaps)

Long volatility bias Directional US/UK/Euro Buy hedges against risk-off scenario

Bank funding to remain

under pressureRelative value UK/Euro/US

Long the Libor basis (e.g. receive

6m Libor, pay 3m Libor)

Long the USD currency Directional Global FX forward contracts

17

G7 Fixed Income Fund

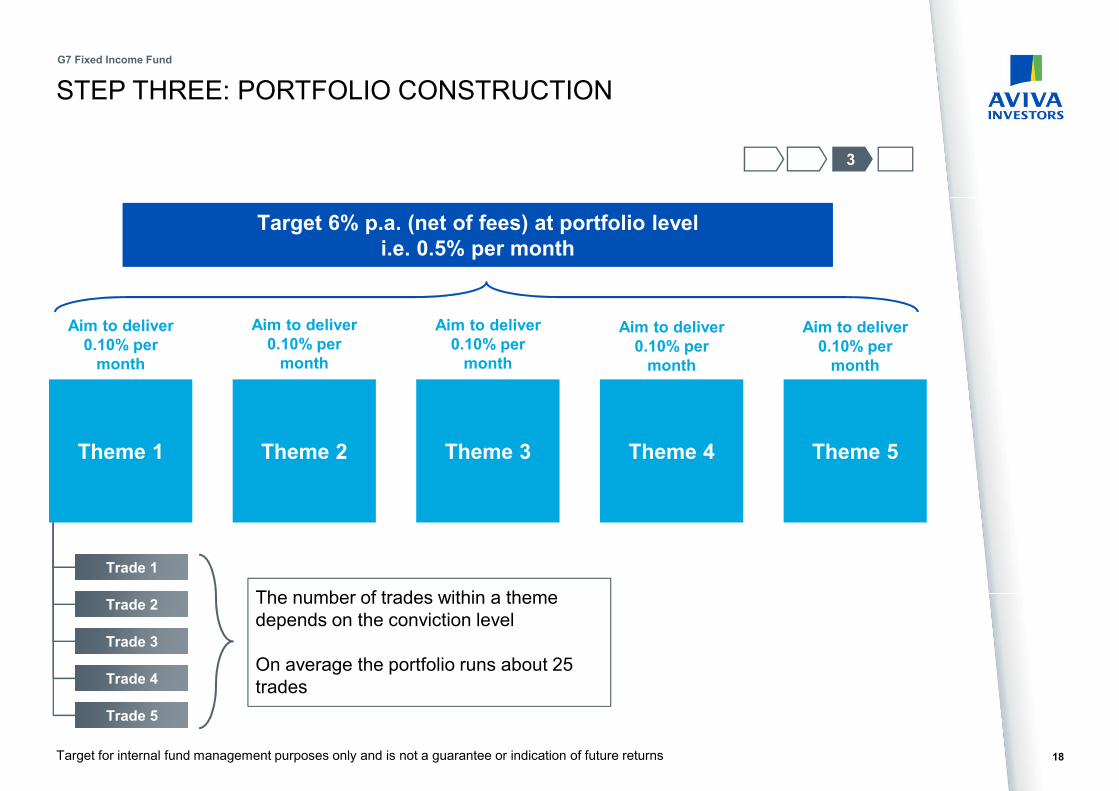

STEP THREE: PORTFOLIO CONSTRUCTION

Theme 4

Target 6% p.a. (net of fees) at portfolio level i.e. 0.5% per month

Theme 3 Theme 5

Aim to deliver 0.10% per month

Aim to deliver 0.10% per month

Aim to deliver 0.10% per month

Aim to deliver 0.10% per month

Aim to deliver 0.10% per month

The number of trades within a theme

depends on the conviction level

On average the portfolio runs about 25

trades

Theme 2Theme 1

3

Trade 1

Trade 2

Trade 3

Trade 4

Trade 5

Target for internal fund management purposes only and is not a guarantee or indication of future returns 18

G7 Fixed Income Fund

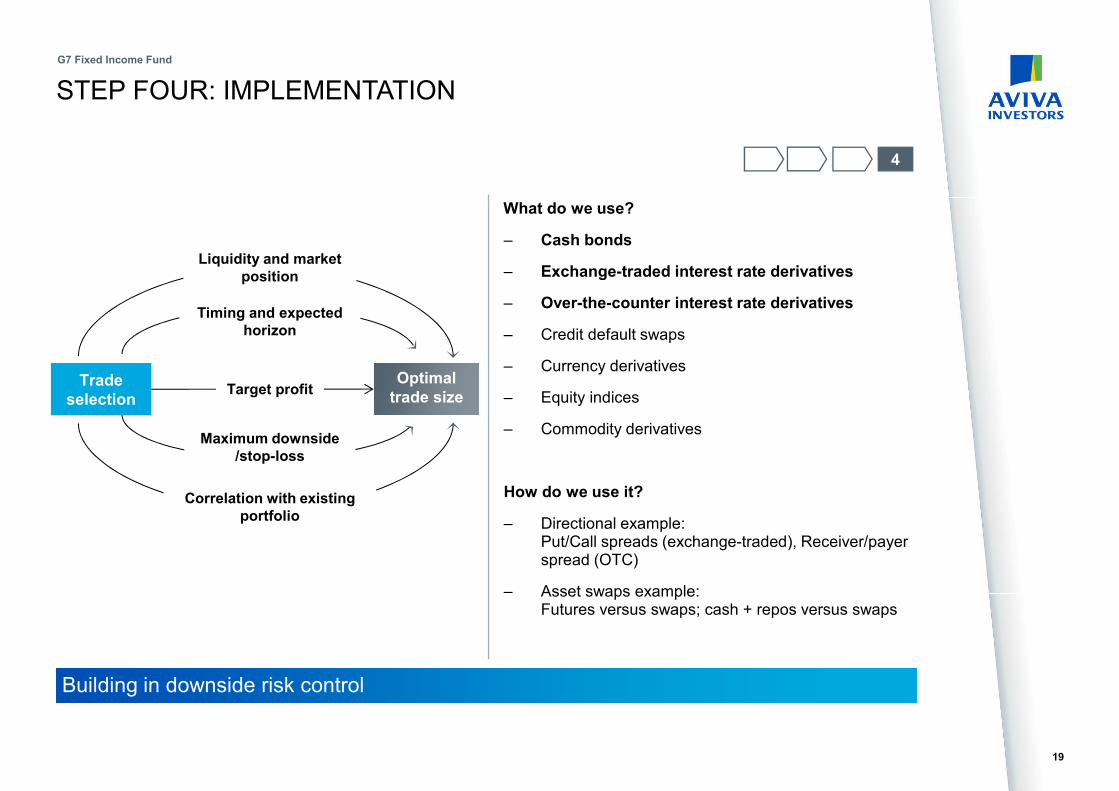

STEP FOUR: IMPLEMENTATION

What do we use?

– Cash bonds

– Exchange-traded interest rate derivatives

– Over-the-counter interest rate derivatives

– Credit default swaps

– Currency derivatives

– Equity indices

– Commodity derivatives

How do we use it?

– Directional example:Put/Call spreads (exchange-traded), Receiver/payer spread (OTC)

– Asset swaps example:Futures versus swaps; cash + repos versus swaps

Building in downside risk control

Trade selection

Optimal trade size

Liquidity and market position

Maximum downside/stop-loss

Timing and expected horizon

Correlation with existing portfolio

Target profit

4

19

G7 Fixed Income Fund

3. WHAT ARE WE FOCUSING ON?

20

G7 Fixed Income Fund

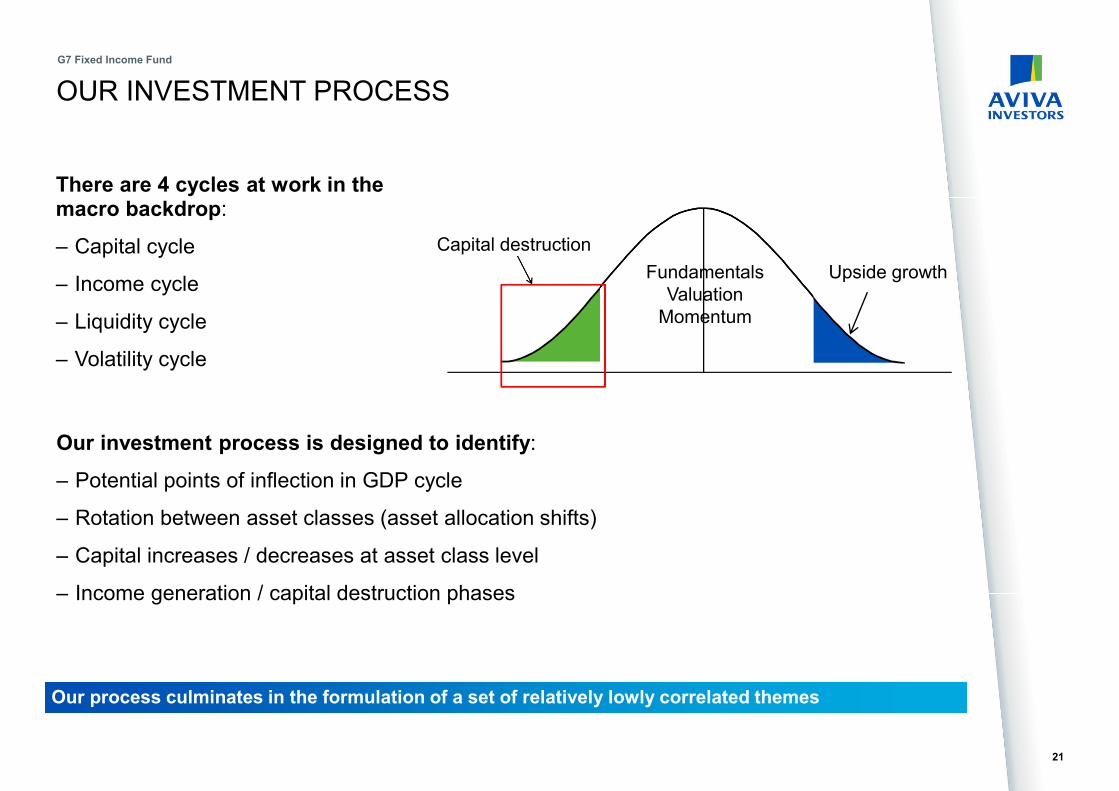

OUR INVESTMENT PROCESS

21

G7 Fixed Income Fund

Our process culminates in the formulation of a set of relatively lowly correlated themes

Our investment process is designed to identify:

– Potential points of inflection in GDP cycle

– Rotation between asset classes (asset allocation shifts)

– Capital increases / decreases at asset class level

– Income generation / capital destruction phases

There are 4 cycles at work in the macro backdrop:

– Capital cycle

– Income cycle

– Liquidity cycle

– Volatility cycle

Capital destruction

Upside growthFundamentals

Valuation

Momentum

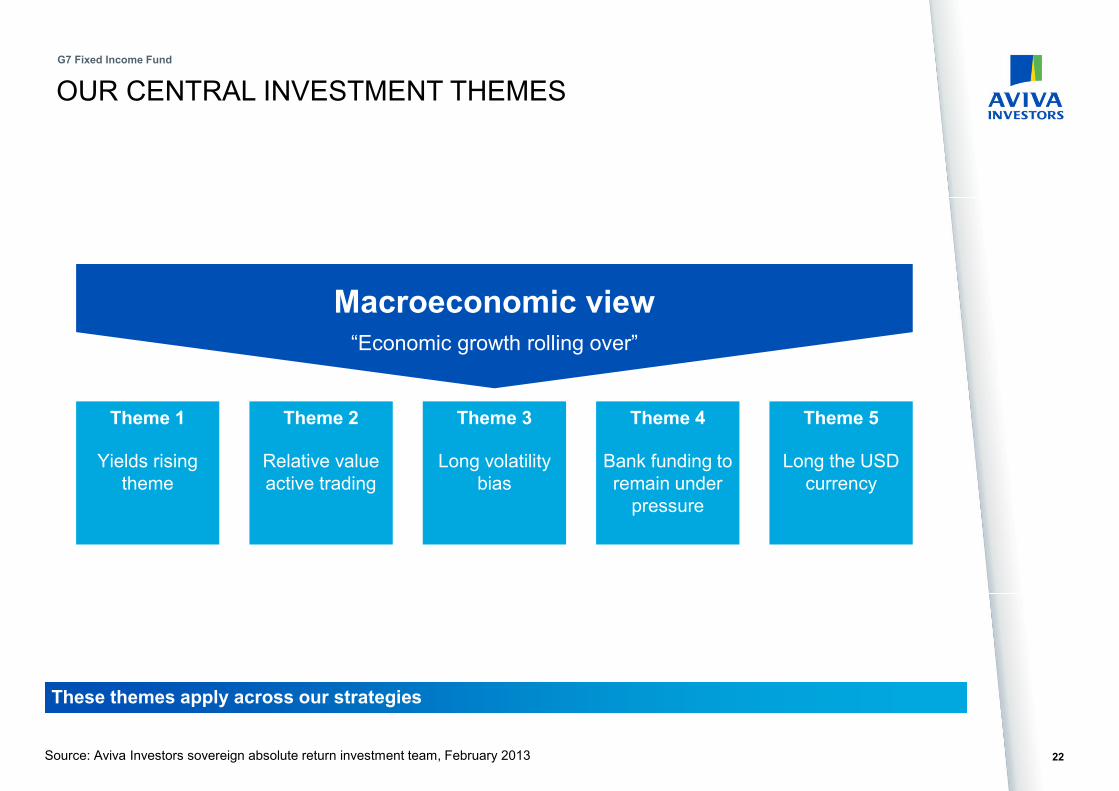

OUR CENTRAL INVESTMENT THEMES

Source: Aviva Investors sovereign absolute return investment team, February 2013

Theme 2

Relative value

active trading

Theme 3

Long volatility

bias

Theme 5

Long the USD

currency

Theme 4

Bank funding to

remain under

pressure

Macroeconomic view“Economic growth rolling over”

Theme 1

Yields rising

theme

22

G7 Fixed Income Fund

These themes apply across our strategies

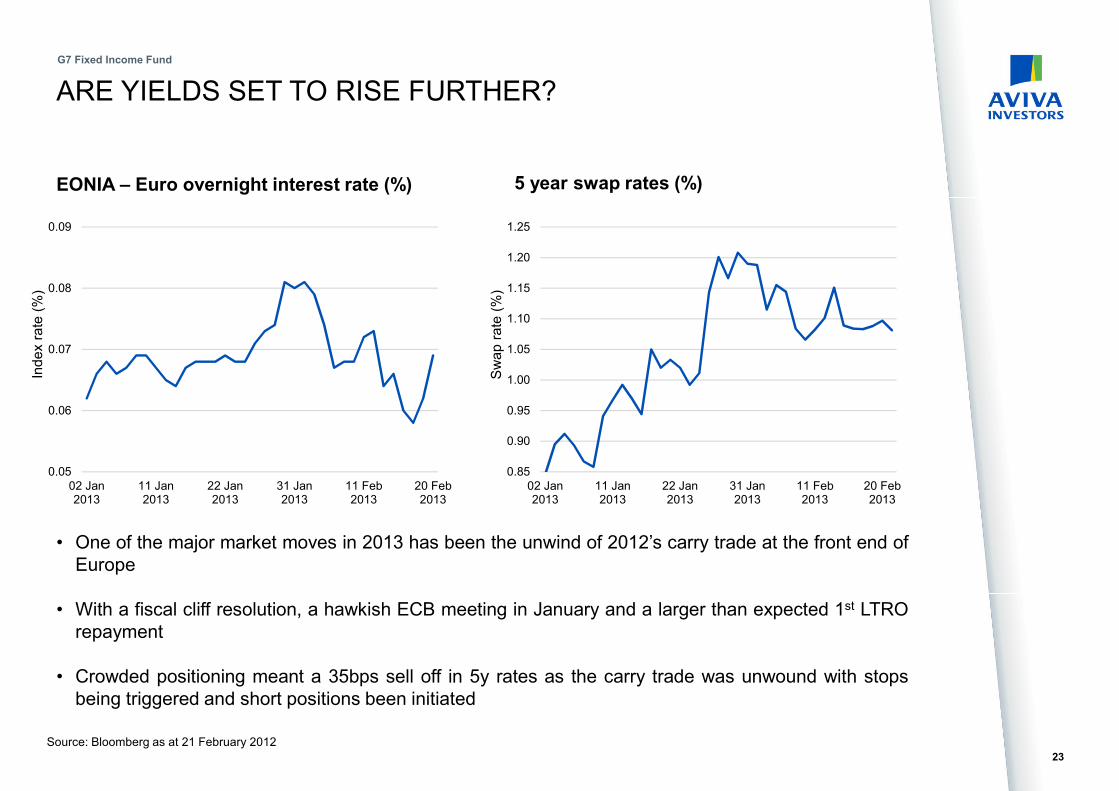

ARE YIELDS SET TO RISE FURTHER?

G7 Fixed Income Fund

23

0.05

0.06

0.07

0.08

0.09

02 Jan2013

11 Jan2013

22 Jan2013

31 Jan2013

11 Feb2013

20 Feb2013

Ind

ex r

ate

(%

)

EONIA – Euro overnight interest rate (%) 5 year swap rates (%)

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

02 Jan2013

11 Jan2013

22 Jan2013

31 Jan2013

11 Feb2013

20 Feb2013

Sw

ap

ra

te (

%)

Source: Bloomberg as at 21 February 2012

• One of the major market moves in 2013 has been the unwind of 2012’s carry trade at the front end of

Europe

• With a fiscal cliff resolution, a hawkish ECB meeting in January and a larger than expected 1st LTRO

repayment

• Crowded positioning meant a 35bps sell off in 5y rates as the carry trade was unwound with stops

being triggered and short positions been initiated

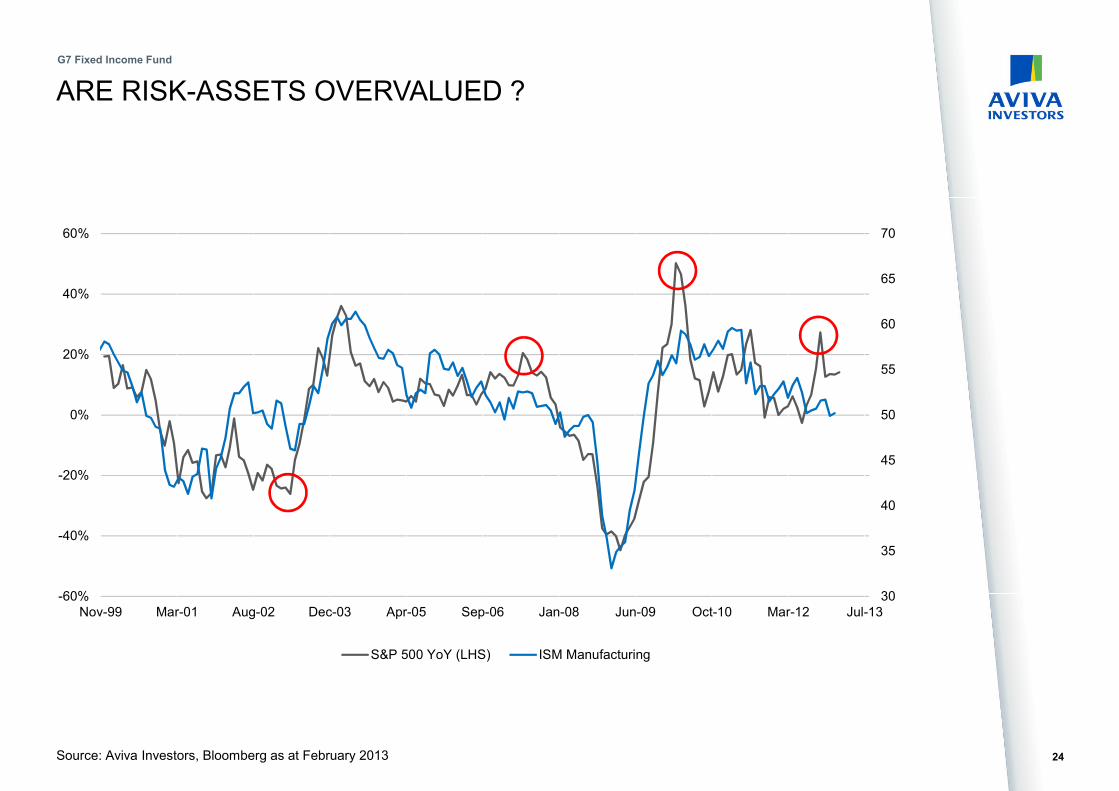

ARE RISK-ASSETS OVERVALUED ?

G7 Fixed Income Fund

24Source: Aviva Investors, Bloomberg as at February 2013

30

35

40

45

50

55

60

65

70

-60%

-40%

-20%

0%

20%

40%

60%

Nov-99 Mar-01 Aug-02 Dec-03 Apr-05 Sep-06 Jan-08 Jun-09 Oct-10 Mar-12 Jul-13

S&P 500 YoY (LHS) ISM Manufacturing

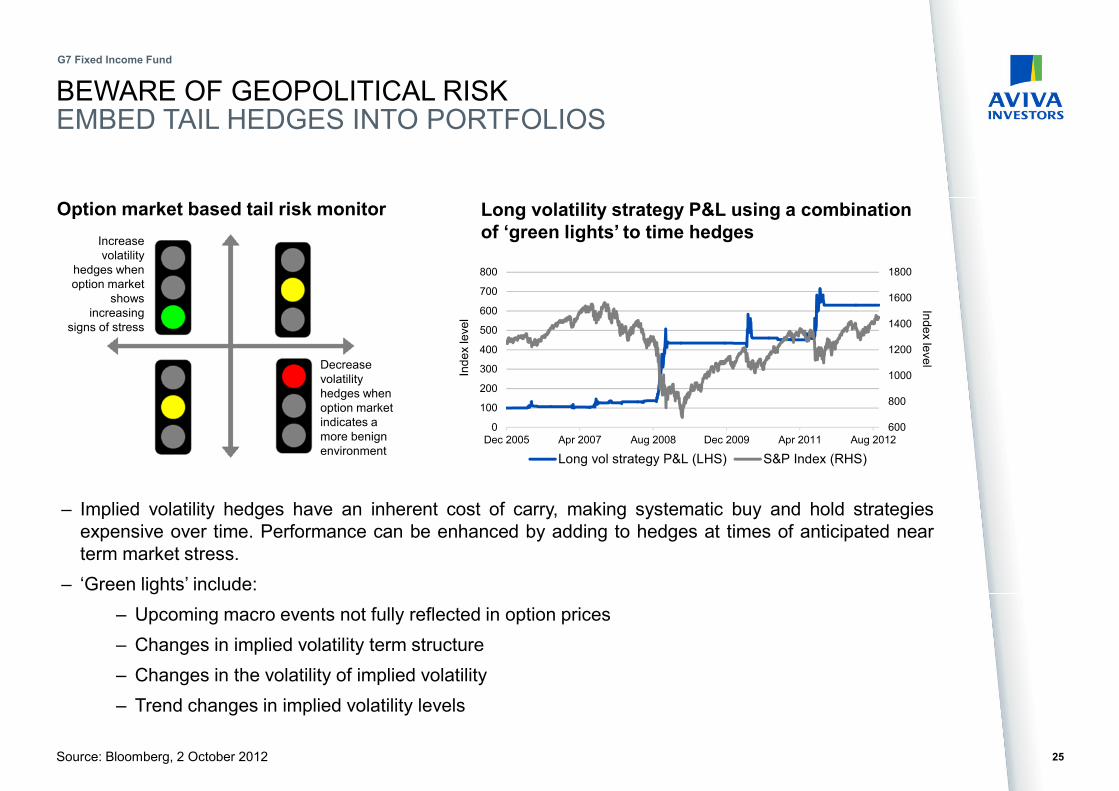

BEWARE OF GEOPOLITICAL RISKEMBED TAIL HEDGES INTO PORTFOLIOS

G7 Fixed Income Fund

Source: Bloomberg, 2 October 2012

– Implied volatility hedges have an inherent cost of carry, making systematic buy and hold strategies

expensive over time. Performance can be enhanced by adding to hedges at times of anticipated near

term market stress.

– ‘Green lights’ include:

– Upcoming macro events not fully reflected in option prices

– Changes in implied volatility term structure

– Changes in the volatility of implied volatility

– Trend changes in implied volatility levels

Option market based tail risk monitor

25

Long volatility strategy P&L using a combination of ‘green lights’ to time hedges

Increase

volatility

hedges when

option market

shows

increasing

signs of stress

Decrease

volatility

hedges when

option market

indicates a

more benign

environment

Ind

ex le

ve

l

Ind

ex le

ve

l

600

800

1000

1200

1400

1600

1800

0

100

200

300

400

500

600

700

800

Dec 2005 Apr 2007 Aug 2008 Dec 2009 Apr 2011 Aug 2012

Long vol strategy P&L (LHS) S&P Index (RHS)

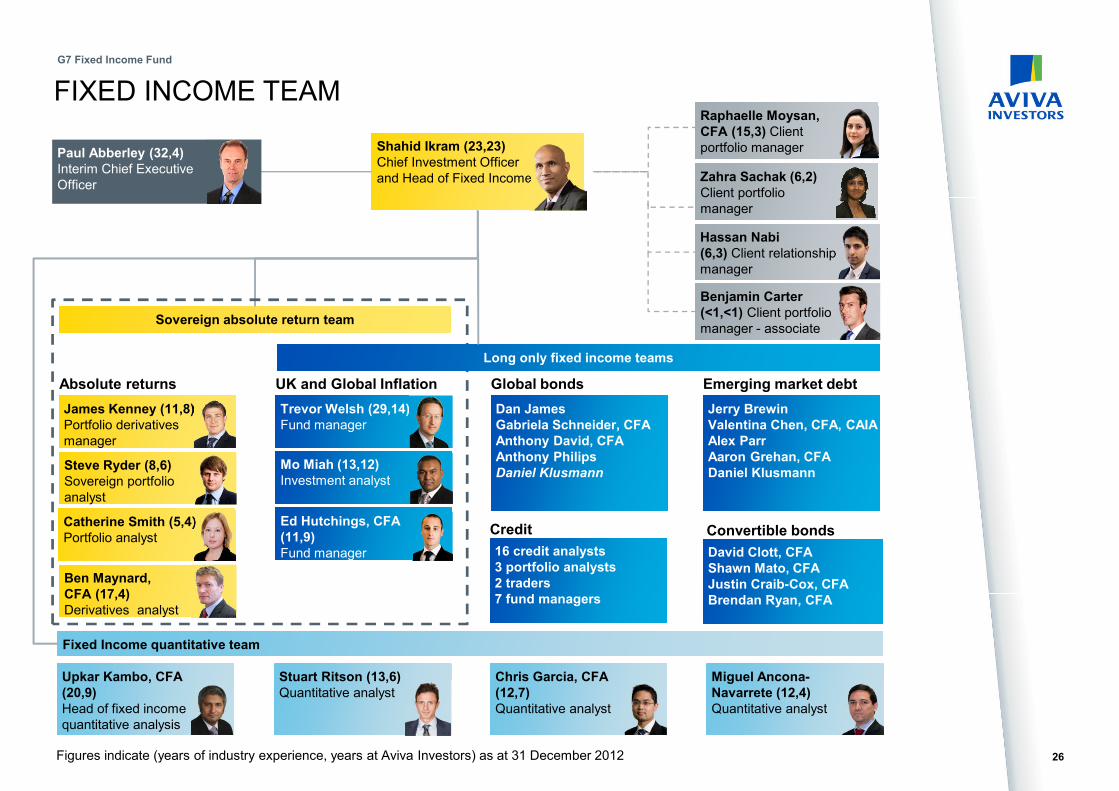

Zahra Sachak (6,2)Client portfolio

manager

FIXED INCOME TEAM

Shahid Ikram (23,23)Chief Investment Officer

and Head of Fixed Income

Figures indicate (years of industry experience, years at Aviva Investors) as at 31 December 2012

Steve Ryder (8,6)Sovereign portfolio

analyst

Sovereign absolute return team

James Kenney (11,8)Portfolio derivatives

manager

Catherine Smith (5,4)Portfolio analyst

Mo Miah (13,12)Investment analyst

Trevor Welsh (29,14)Fund manager

Ed Hutchings, CFA (11,9)Fund manager

Absolute returns UK and Global Inflation Global bonds Emerging market debt

Dan JamesGabriela Schneider, CFAAnthony David, CFAAnthony PhilipsDaniel Klusmann

Jerry BrewinValentina Chen, CFA, CAIAAlex ParrAaron Grehan, CFADaniel Klusmann

Raphaelle Moysan, CFA (15,3) Client

portfolio manager

Fixed Income quantitative team

Long only fixed income teams

Paul Abberley (32,4)Interim Chief Executive

Officer

Upkar Kambo, CFA (20,9)Head of fixed income

quantitative analysis

Stuart Ritson (13,6)Quantitative analyst

Chris Garcia, CFA (12,7)Quantitative analyst

Miguel Ancona-Navarrete (12,4)Quantitative analyst

Ben Maynard, CFA (17,4)Derivatives analyst

Credit

16 credit analysts3 portfolio analysts2 traders7 fund managers

Convertible bonds

David Clott, CFAShawn Mato, CFAJustin Craib-Cox, CFABrendan Ryan, CFA

Benjamin Carter (<1,<1) Client portfolio

manager - associate

Hassan Nabi(6,3) Client relationship

manager

26

G7 Fixed Income Fund

4. RISK MANAGEMENT

27

G7 Fixed Income Fund

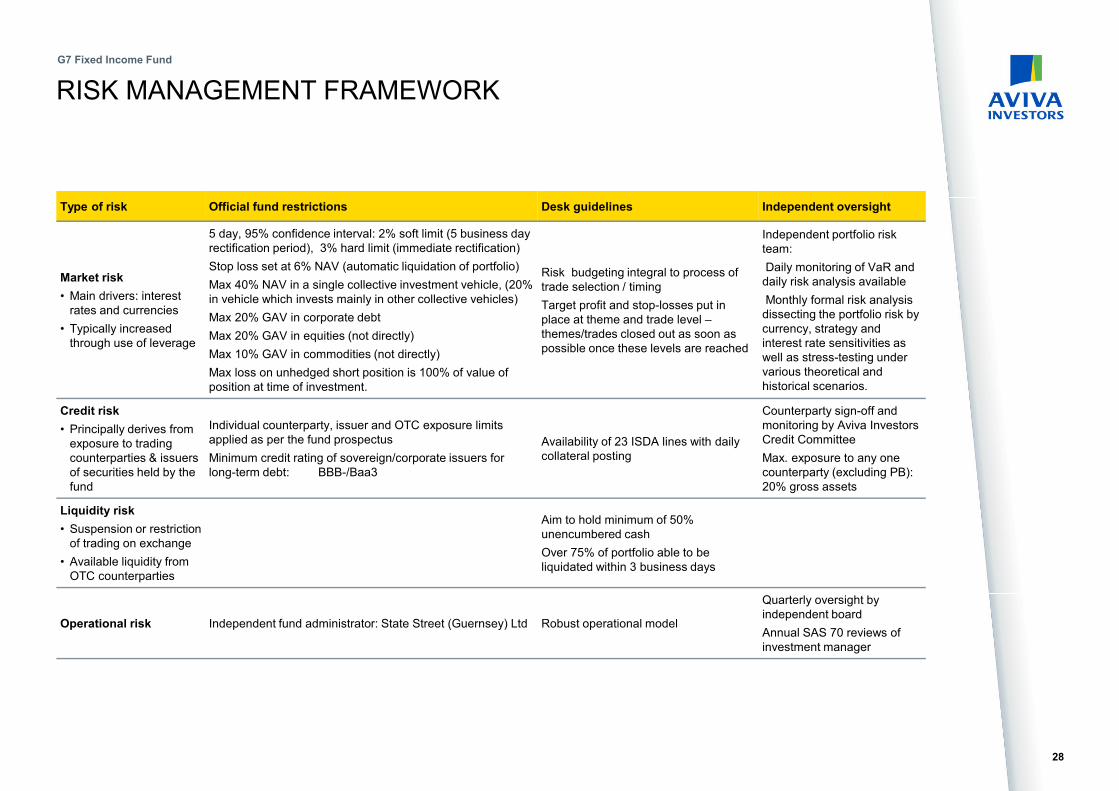

RISK MANAGEMENT FRAMEWORK

Type of risk Official fund restrictions Desk guidelines Independent oversight

Market risk

• Main drivers: interest

rates and currencies

• Typically increased

through use of leverage

5 day, 95% confidence interval: 2% soft limit (5 business day

rectification period), 3% hard limit (immediate rectification)

Stop loss set at 6% NAV (automatic liquidation of portfolio)

Max 40% NAV in a single collective investment vehicle, (20%

in vehicle which invests mainly in other collective vehicles)

Max 20% GAV in corporate debt

Max 20% GAV in equities (not directly)

Max 10% GAV in commodities (not directly)

Max loss on unhedged short position is 100% of value of

position at time of investment.

Risk budgeting integral to process of

trade selection / timing

Target profit and stop-losses put in

place at theme and trade level –

themes/trades closed out as soon as

possible once these levels are reached

Independent portfolio risk

team:

Daily monitoring of VaR and

daily risk analysis available

Monthly formal risk analysis

dissecting the portfolio risk by

currency, strategy and

interest rate sensitivities as

well as stress-testing under

various theoretical and

historical scenarios.

Credit risk

• Principally derives from

exposure to trading

counterparties & issuers

of securities held by the

fund

Individual counterparty, issuer and OTC exposure limits

applied as per the fund prospectus

Minimum credit rating of sovereign/corporate issuers for

long-term debt: BBB-/Baa3

Availability of 23 ISDA lines with daily

collateral posting

Counterparty sign-off and

monitoring by Aviva Investors

Credit Committee

Max. exposure to any one

counterparty (excluding PB):

20% gross assets

Liquidity risk

• Suspension or restriction

of trading on exchange

• Available liquidity from

OTC counterparties

Aim to hold minimum of 50%

unencumbered cash

Over 75% of portfolio able to be

liquidated within 3 business days

Operational risk Independent fund administrator: State Street (Guernsey) Ltd Robust operational model

Quarterly oversight by

independent board

Annual SAS 70 reviews of

investment manager

28

G7 Fixed Income Fund

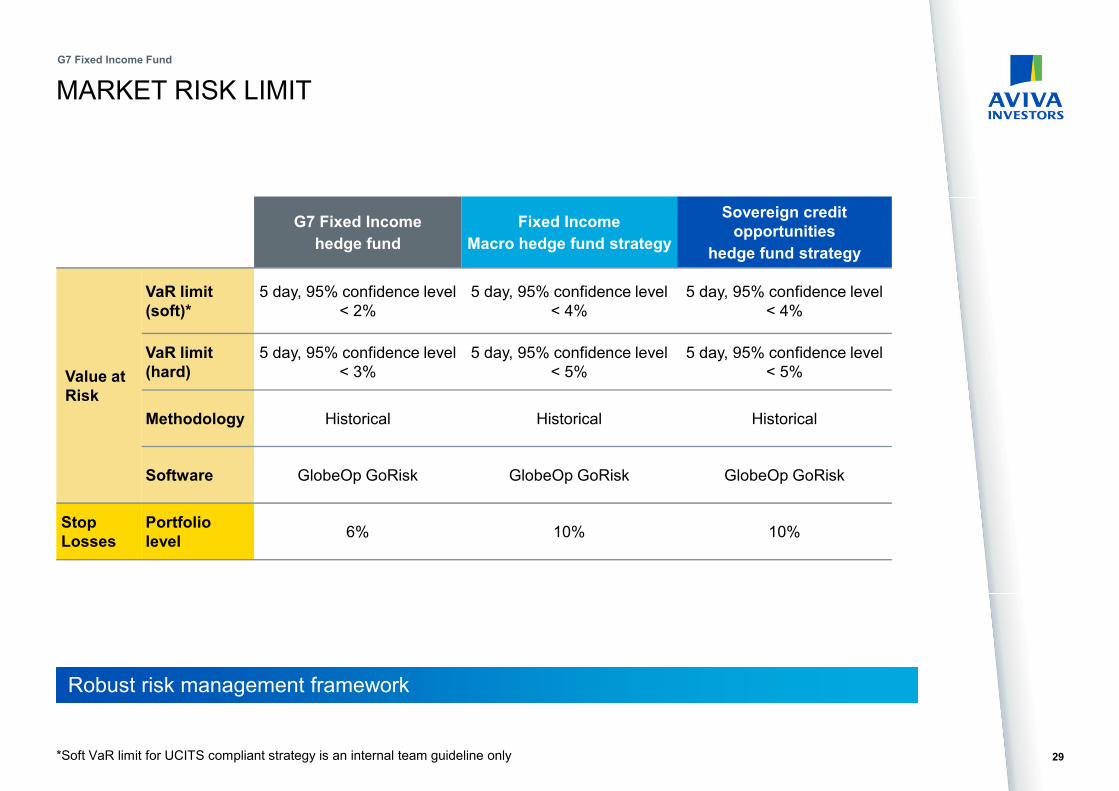

MARKET RISK LIMIT

*Soft VaR limit for UCITS compliant strategy is an internal team guideline only

Robust risk management framework

29

G7 Fixed Income Fund

G7 Fixed Income

hedge fund

Fixed Income

Macro hedge fund strategy

Sovereign credit opportunities

hedge fund strategy

Value at Risk

VaR limit (soft)*

5 day, 95% confidence level

< 2%

5 day, 95% confidence level

< 4%

5 day, 95% confidence level

< 4%

VaR limit (hard)

5 day, 95% confidence level

< 3%

5 day, 95% confidence level

< 5%

5 day, 95% confidence level

< 5%

Methodology Historical Historical Historical

Software GlobeOp GoRisk GlobeOp GoRisk GlobeOp GoRisk

Stop Losses

Portfolio level

6% 10% 10%

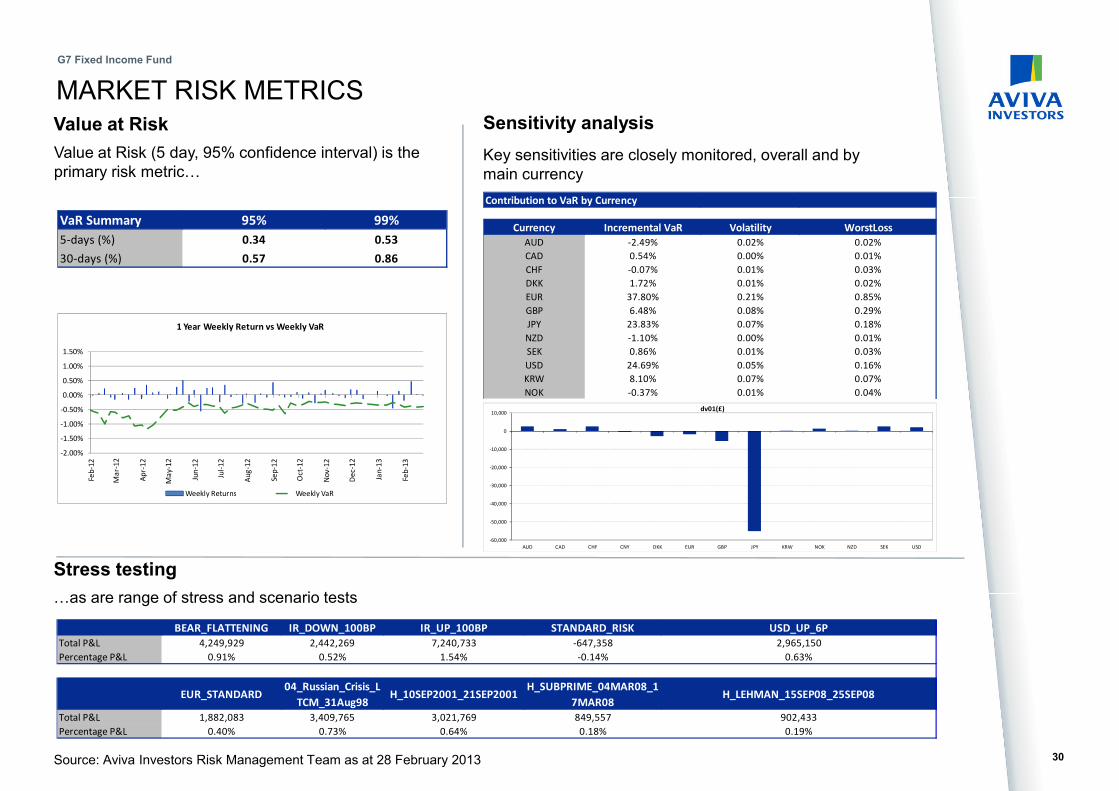

MARKET RISK METRICSValue at Risk

Stress testing

Sensitivity analysis

Value at Risk (5 day, 95% confidence interval) is the

primary risk metric…Key sensitivities are closely monitored, overall and by

main currency

…as are range of stress and scenario tests

Source: Aviva Investors Risk Management Team as at 28 February 2013 30

G7 Fixed Income Fund

VaR Summary 95% 99%

5-days (%) 0.34 0.53

30-days (%) 0.57 0.86

-2.00%

-1.50%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

Feb

-12

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Jun

-12

Jul-

12

Au

g-1

2

Sep

-12

Oct-

12

No

v-1

2

De

c-1

2

Jan

-13

Feb

-13

1 Year Weekly Return vs Weekly VaR

Weekly Returns Weekly VaR

Contribution to VaR by Currency

Currency Incremental VaR Volatility WorstLoss

AUD -2.49% 0.02% 0.02%

CAD 0.54% 0.00% 0.01%

CHF -0.07% 0.01% 0.03%

DKK 1.72% 0.01% 0.02%

EUR 37.80% 0.21% 0.85%

GBP 6.48% 0.08% 0.29%

JPY 23.83% 0.07% 0.18%

NZD -1.10% 0.00% 0.01%

SEK 0.86% 0.01% 0.03%

USD 24.69% 0.05% 0.16%

KRW 8.10% 0.07% 0.07%

NOK -0.37% 0.01% 0.04%

-60,000

-50,000

-40,000

-30,000

-20,000

-10,000

0

10,000

AUD CAD CHF CNY DKK EUR GBP JPY KRW NOK NZD SEK USD

dv01(£)

BEAR_FLATTENING IR_DOWN_100BP IR_UP_100BP STANDARD_RISK USD_UP_6P

Total P&L 4,249,929 2,442,269 7,240,733 -647,358 2,965,150

Percentage P&L 0.91% 0.52% 1.54% -0.14% 0.63%

EUR_STANDARD04_Russian_Crisis_L

TCM_31Aug98H_10SEP2001_21SEP2001

H_SUBPRIME_04MAR08_1

7MAR08H_LEHMAN_15SEP08_25SEP08

Total P&L 1,882,083 3,409,765 3,021,769 849,557 902,433

Percentage P&L 0.40% 0.73% 0.64% 0.18% 0.19%

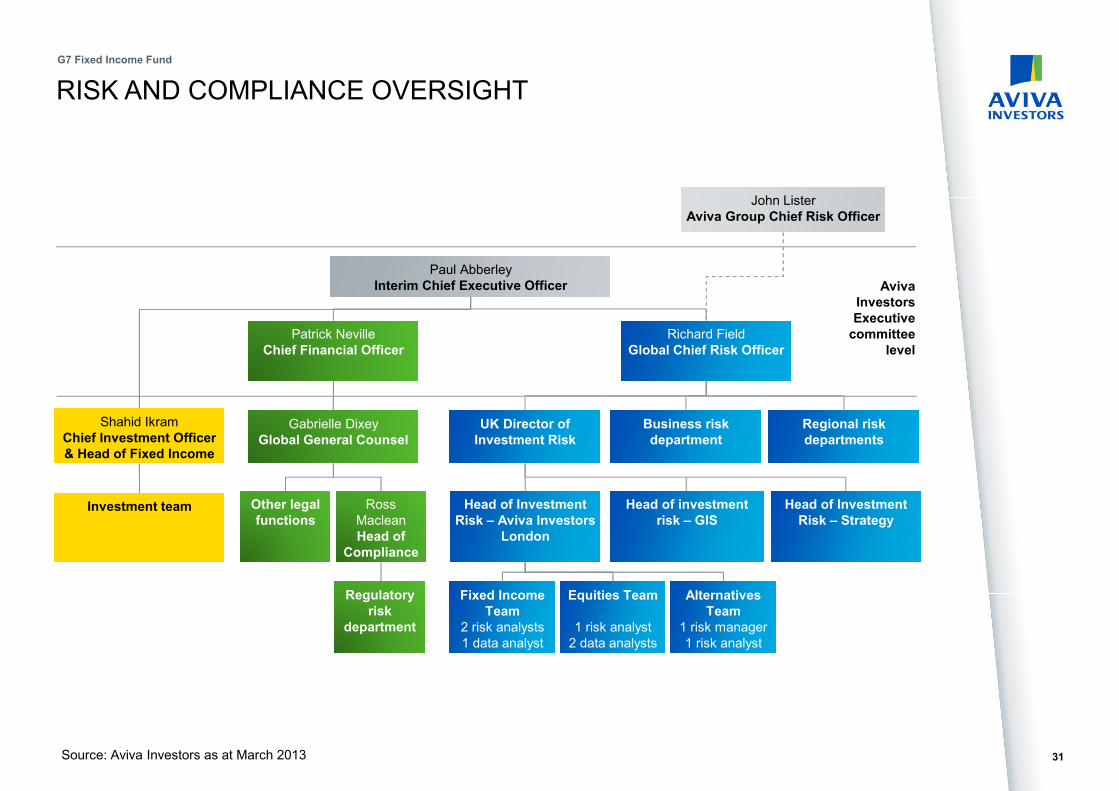

Paul Abberley

Interim Chief Executive Officer

Patrick Neville

Chief Financial Officer

Ross

Maclean

Head of Compliance

Gabrielle Dixey

Global General Counsel

Richard Field

Global Chief Risk Officer

UK Director of Investment Risk

Aviva Investors Executive committee

level

Regional risk departments

John Lister

Aviva Group Chief Risk Officer

Other legal functions

Head of Investment Risk – Aviva Investors

London

Fixed Income Team

2 risk analysts

1 data analyst

Head of investment risk – GIS

Equities Team

1 risk analyst

2 data analysts

Alternatives Team

1 risk manager

1 risk analyst

RISK AND COMPLIANCE OVERSIGHT

Business risk department

Shahid Ikram

Chief Investment Officer & Head of Fixed Income

Investment team Head of Investment Risk – Strategy

31

Regulatory risk

department

Source: Aviva Investors as at March 2013

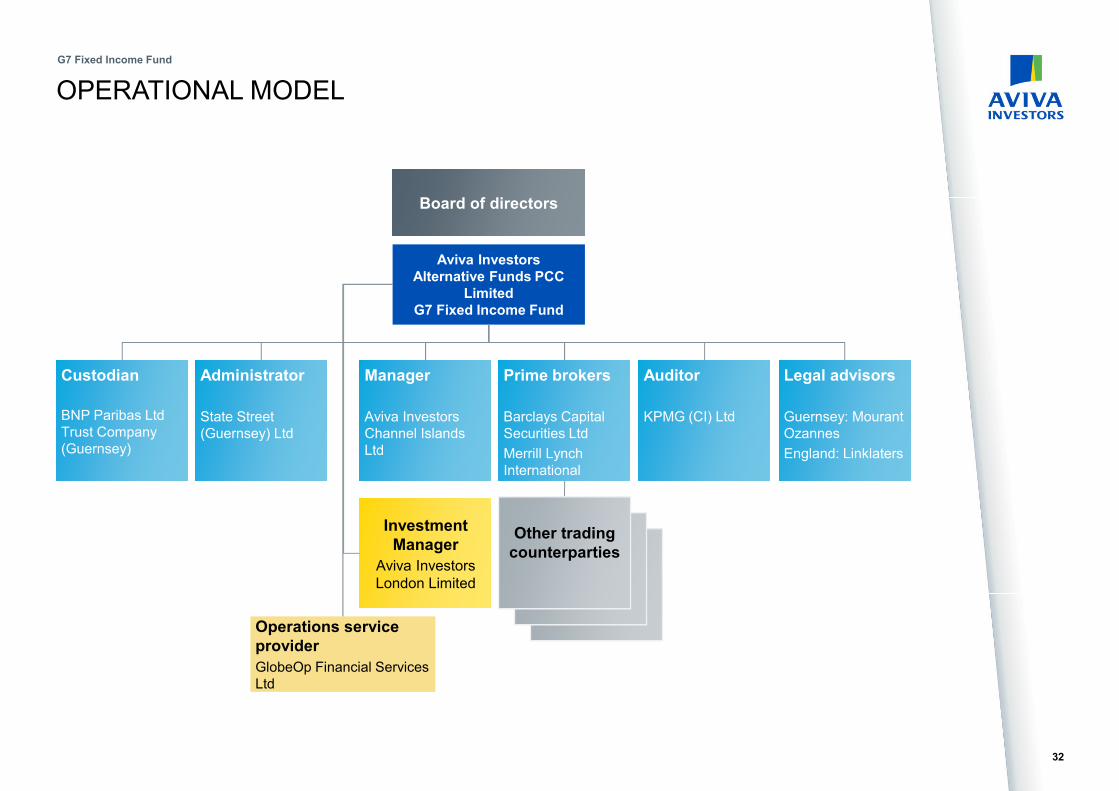

G7 Fixed Income Fund

Board of directors

Aviva Investors Alternative Funds PCC

LimitedG7 Fixed Income Fund

Investment Manager

Aviva Investors

London Limited

Prime brokers

Barclays Capital

Securities Ltd

Merrill Lynch

International

Auditor

KPMG (CI) Ltd

Administrator

State Street

(Guernsey) Ltd

Custodian

BNP Paribas Ltd

Trust Company

(Guernsey)

Legal advisors

Guernsey: Mourant

Ozannes

England: Linklaters

Operations service provider

GlobeOp Financial Services

Ltd

Manager

Aviva Investors

Channel Islands

Ltd

OPERATIONAL MODEL

Other trading counterparties

32

G7 Fixed Income Fund

APPENDIX 1: THE CAPABILITY

33

G7 Fixed Income Fund

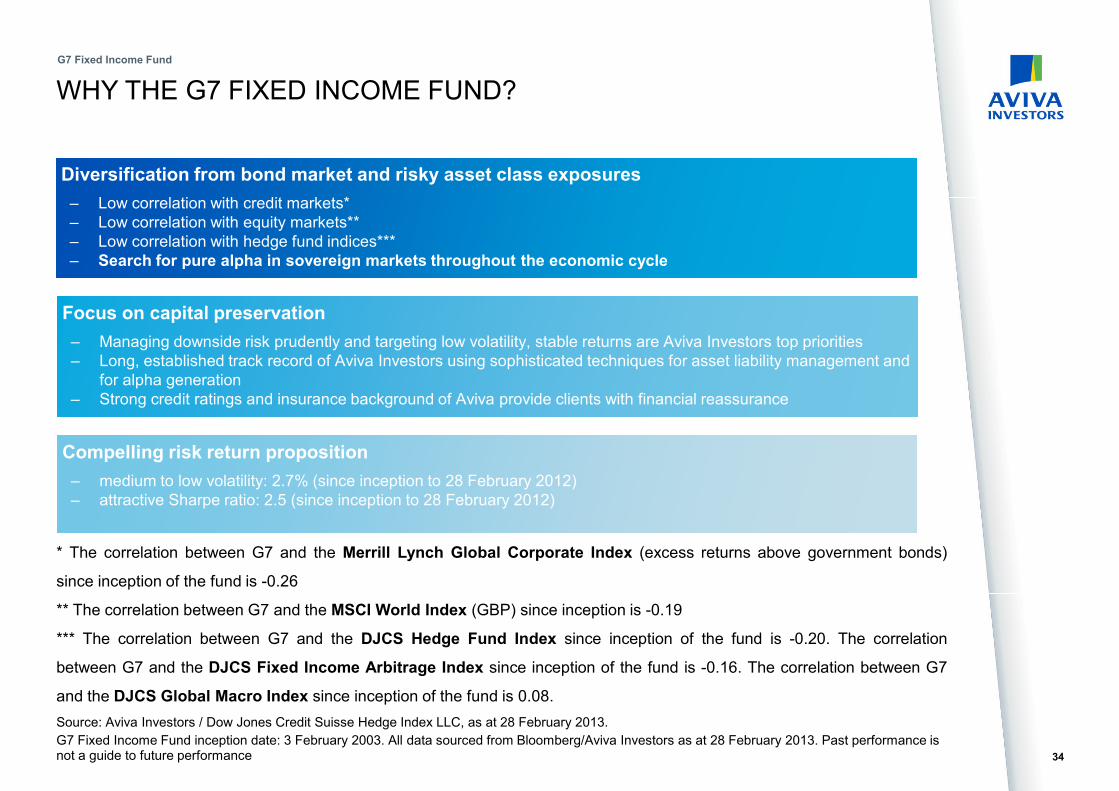

WHY THE G7 FIXED INCOME FUND?

* The correlation between G7 and the Merrill Lynch Global Corporate Index (excess returns above government bonds)

since inception of the fund is -0.26

** The correlation between G7 and the MSCI World Index (GBP) since inception is -0.19

*** The correlation between G7 and the DJCS Hedge Fund Index since inception of the fund is -0.20. The correlation

between G7 and the DJCS Fixed Income Arbitrage Index since inception of the fund is -0.16. The correlation between G7

and the DJCS Global Macro Index since inception of the fund is 0.08.

Source: Aviva Investors / Dow Jones Credit Suisse Hedge Index LLC, as at 28 February 2013.

G7 Fixed Income Fund inception date: 3 February 2003. All data sourced from Bloomberg/Aviva Investors as at 28 February 2013. Past performance is not a guide to future performance

Diversification from bond market and risky asset class exposures

– Low correlation with credit markets*

– Low correlation with equity markets**

– Low correlation with hedge fund indices***

– Search for pure alpha in sovereign markets throughout the economic cycle

Focus on capital preservation

– Managing downside risk prudently and targeting low volatility, stable returns are Aviva Investors top priorities

– Long, established track record of Aviva Investors using sophisticated techniques for asset liability management and

for alpha generation

– Strong credit ratings and insurance background of Aviva provide clients with financial reassurance

Compelling risk return proposition

– medium to low volatility: 2.7% (since inception to 28 February 2012)

– attractive Sharpe ratio: 2.5 (since inception to 28 February 2012)

34

G7 Fixed Income Fund

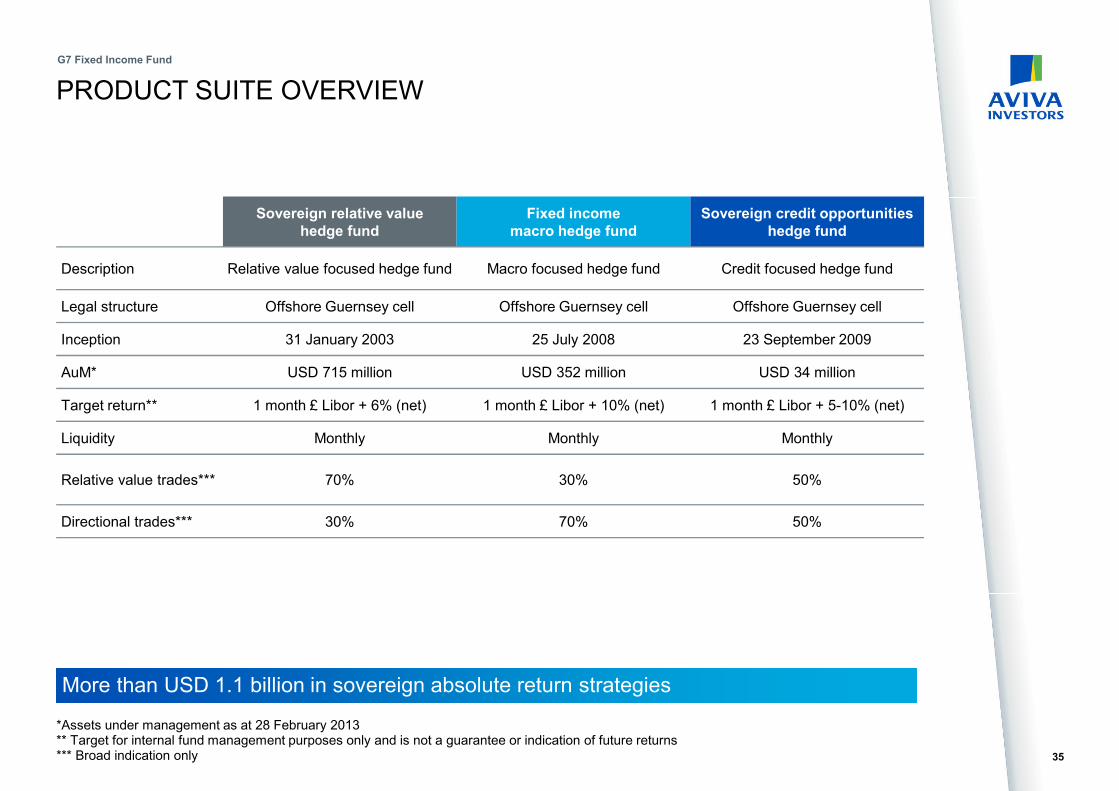

PRODUCT SUITE OVERVIEW

*Assets under management as at 28 February 2013** Target for internal fund management purposes only and is not a guarantee or indication of future returns*** Broad indication only

Sovereign relative value hedge fund

Fixed income macro hedge fund

Sovereign credit opportunities hedge fund

Description Relative value focused hedge fund Macro focused hedge fund Credit focused hedge fund

Legal structure Offshore Guernsey cell Offshore Guernsey cell Offshore Guernsey cell

Inception 31 January 2003 25 July 2008 23 September 2009

AuM* USD 715 million USD 352 million USD 34 million

Target return** 1 month £ Libor + 6% (net) 1 month £ Libor + 10% (net) 1 month £ Libor + 5-10% (net)

Liquidity Monthly Monthly Monthly

Relative value trades*** 70% 30% 50%

Directional trades*** 30% 70% 50%

More than USD 1.1 billion in sovereign absolute return strategies

35

G7 Fixed Income Fund

APPENDIX 2: INVESTOR BREAKDOWNS

36

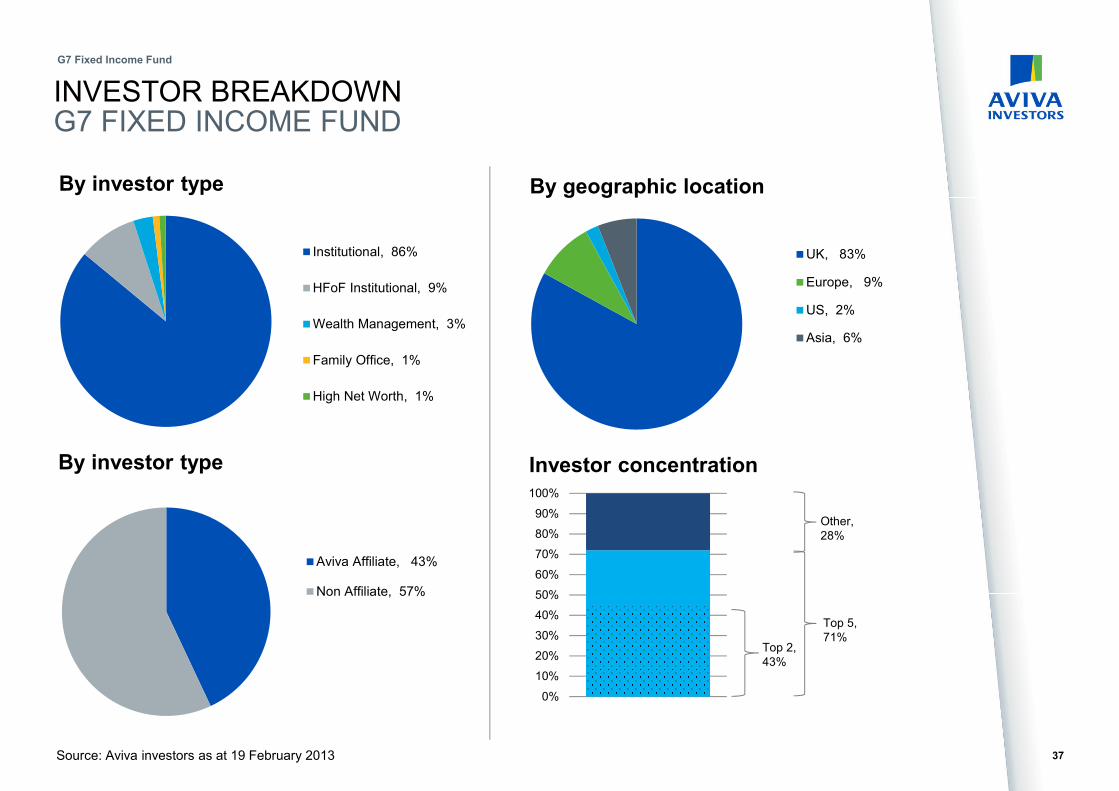

G7 Fixed Income Fund

Aviva Affiliate, 43%

Non Affiliate, 57%

INVESTOR BREAKDOWNG7 FIXED INCOME FUND

G7 Fixed Income Fund

37Source: Aviva investors as at 19 February 2013

Institutional, 86%

HFoF Institutional, 9%

Wealth Management, 3%

Family Office, 1%

High Net Worth, 1%

By investor type

By investor type

UK, 83%

Europe, 9%

US, 2%

Asia, 6%

By geographic location

Investor concentration

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Top 2,

43%

Top 5,

71%

Other,

28%

APPENDIX 3: TRADE EXAMPLES

38

G7 Fixed Income Fund

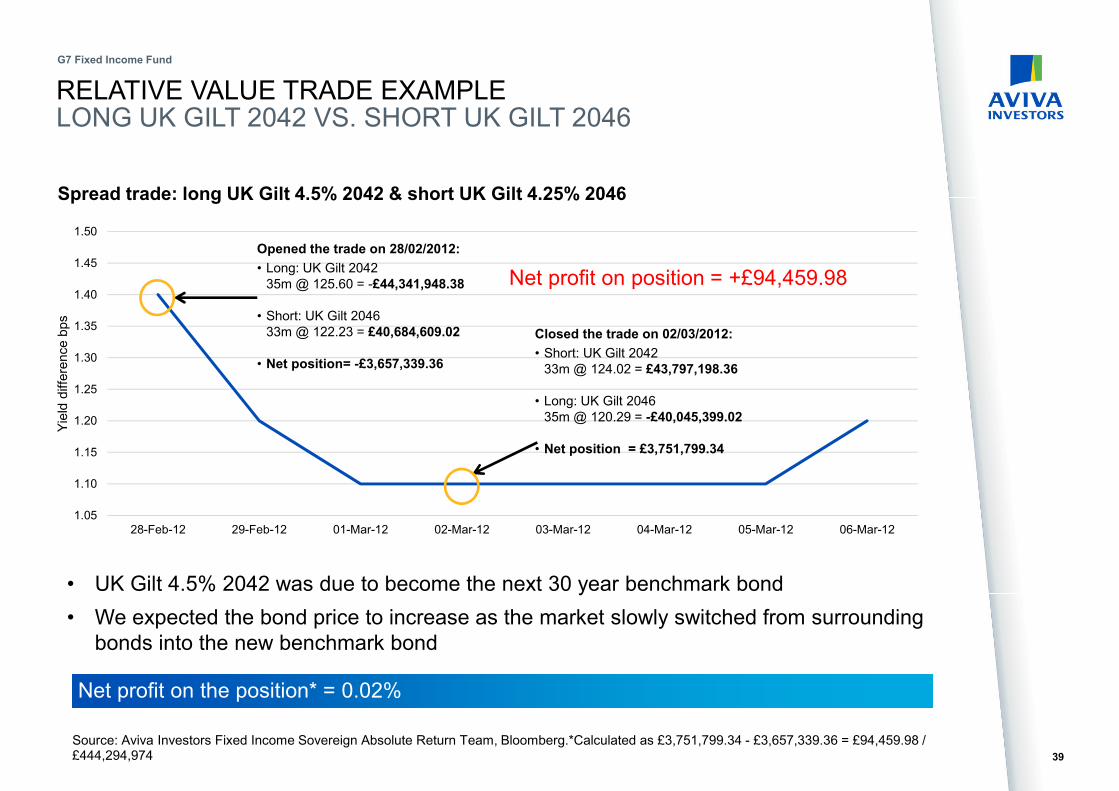

RELATIVE VALUE TRADE EXAMPLELONG UK GILT 2042 VS. SHORT UK GILT 2046

Source: Aviva Investors Fixed Income Sovereign Absolute Return Team, Bloomberg.*Calculated as £3,751,799.34 - £3,657,339.36 = £94,459.98 / £444,294,974

• UK Gilt 4.5% 2042 was due to become the next 30 year benchmark bond

• We expected the bond price to increase as the market slowly switched from surrounding

bonds into the new benchmark bond

Net profit on the position* = 0.02%

39

G7 Fixed Income Fund

1.05

1.10

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

28-Feb-12 29-Feb-12 01-Mar-12 02-Mar-12 03-Mar-12 04-Mar-12 05-Mar-12 06-Mar-12

Yie

ld d

iffe

rence b

ps

Spread trade: long UK Gilt 4.5% 2042 & short UK Gilt 4.25% 2046

Opened the trade on 28/02/2012:

• Long: UK Gilt 2042

35m @ 125.60 = -£44,341,948.38

• Short: UK Gilt 2046

33m @ 122.23 = £40,684,609.02

• Net position= -£3,657,339.36

Closed the trade on 02/03/2012:

• Short: UK Gilt 2042

33m @ 124.02 = £43,797,198.36

• Long: UK Gilt 2046

35m @ 120.29 = -£40,045,399.02

• Net position = £3,751,799.34

Net profit on position = +£94,459.98

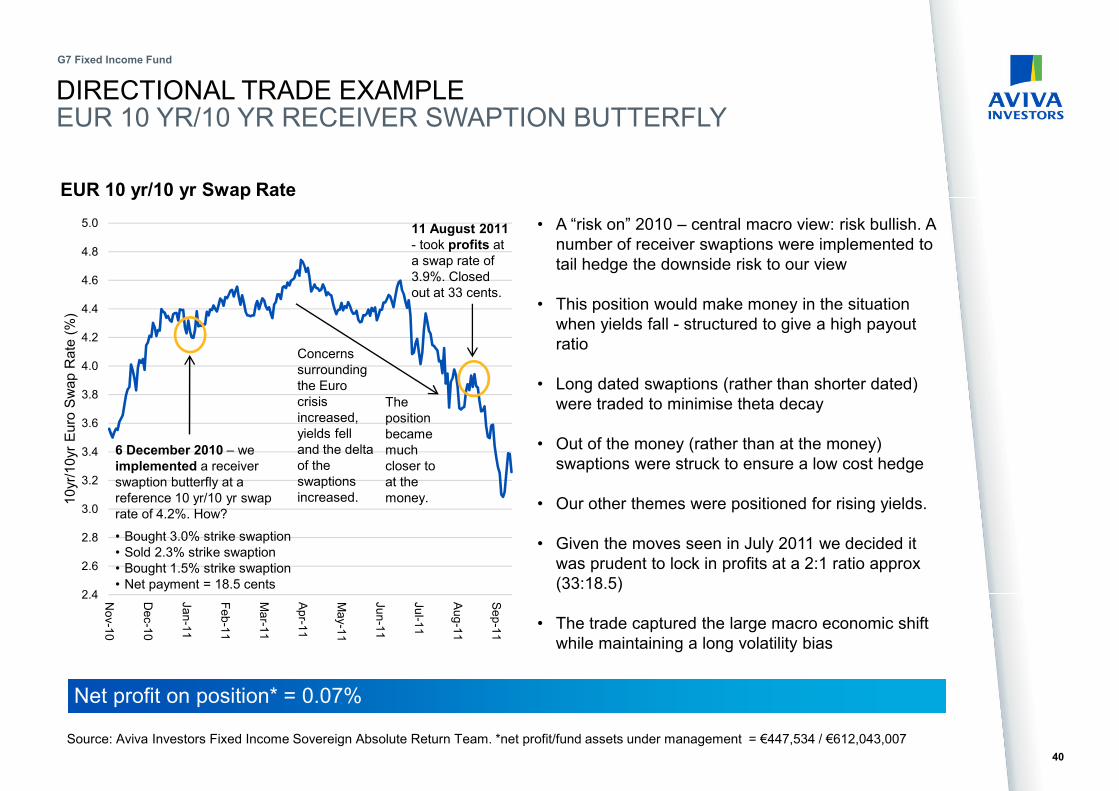

DIRECTIONAL TRADE EXAMPLEEUR 10 YR/10 YR RECEIVER SWAPTION BUTTERFLY

EUR 10 yr/10 yr Swap Rate

Source: Aviva Investors Fixed Income Sovereign Absolute Return Team. *net profit/fund assets under management = €447,534 / €612,043,007

• A “risk on” 2010 – central macro view: risk bullish. A

number of receiver swaptions were implemented to

tail hedge the downside risk to our view

• This position would make money in the situation

when yields fall - structured to give a high payout

ratio

• Long dated swaptions (rather than shorter dated)

were traded to minimise theta decay

• Out of the money (rather than at the money)

swaptions were struck to ensure a low cost hedge

• Our other themes were positioned for rising yields.

• Given the moves seen in July 2011 we decided it

was prudent to lock in profits at a 2:1 ratio approx

(33:18.5)

• The trade captured the large macro economic shift

while maintaining a long volatility bias

Net profit on position* = 0.07%

2.4

2.6

2.8

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

4.8

5.0

No

v-1

0

De

c-1

0

Ja

n-1

1

Fe

b-1

1

Ma

r-11

Ap

r-11

Ma

y-1

1

Ju

n-1

1

Ju

l-11

Au

g-1

1

Se

p-1

1

10

yr/

10

yr

Eu

ro S

wa

p R

ate

(%

)

6 December 2010 – we

implemented a receiver

swaption butterfly at a

reference 10 yr/10 yr swap

rate of 4.2%. How?

• Bought 3.0% strike swaption

• Sold 2.3% strike swaption

• Bought 1.5% strike swaption

• Net payment = 18.5 cents

11 August 2011 - took profits at

a swap rate of

3.9%. Closed

out at 33 cents.

Concerns

surrounding

the Euro

crisis

increased,

yields fell

and the delta

of the

swaptions

increased.

The

position

became

much

closer to

at the

money.

40

G7 Fixed Income Fund

APPENDIX 4: BIOGRAPHIES

41

G7 Fixed Income Fund

BIOGRAPHIES

James Kenney, MA, FIAPortfolio Derivatives Manager

Joined investment industry in 2001

Main Responsibilities Responsible for the development, approvaland execution of derivatives strategies ininvestment management.

Experience & qualificationsJames joined Aviva Investors originally as a

derivatives analyst. He then progressed to

portfolio derivatives manager for the sovereign

team in August 2006. Prior to joining Aviva

Investors, James worked as an investment

analyst at Mercer Investment Consulting whilst

studying for the Actuarial qualification.

James holds an MA in mathematics from

Trinity College, Cambridge University. He also

holds the investment management certificate,

the Institute of Actuaries’ certificate in

derivatives and advanced certificate in

derivatives. James is a fellow of the Institute of

Actuaries.

Shahid IkramChief Investment Officer, Head of Fixed Income, Aviva Investors London

Joined investment industry in 1990

Main Responsibilities Control of investment processes, managing engagementwith global capital markets and management of fixedincome investment staff. Shahid also oversees thedevelopment of sovereign products with a particular focuson hedge funds.

Experience & qualificationsShahid joined the firm in 1990 as a gilt fund manager,becoming head of global sovereign debt and absolutereturns. He has managed Aviva Investors’ first hedge fund,a sovereign relative value fund, since its launch in 2003.In 2009, Shahid became deputy CIO for Fixed Income andin 2012 he was appointed CIO in London, overseeing awide range of capabilities including hedge funds, emergingmarket debt, global bonds, UK sovereign, credit, liquidityand convertible bonds. He is also the chair of the AvivaInvestors London Desk Heads College, an internal group ofsenior investment professionals overseeing strategy andrisk across all active asset classes.

Shahid holds a BSc (Hons) in mathematics, statistics andcomputing from Greenwich University and is an associatemember of the Institute of Investment Management andResearch (IIMR).

Paul AbberleyInterim Chief Executive Officer, Aviva Investors Joined investment industry in 1981

Main Responsibilities Paul joined Aviva Investors as ChiefExecutive Aviva Investors London,adding Global Investment Solutions in2011. He was appointed interim CEOin May 2012 and is responsible for theleadership and governance of thecompany. As CEO he continues todeliver the business strategy whilemaintaining close relationships withGroup counterparties and clients.Growth of external sales is a toppriority.

Experience & qualificationsHe was previously at ABN Amro AssetManagement for eight years where heworked in a series of fixed income rolesand as CEO for London.

Paul has also worked as a global headof fixed income at Lombard Odier. Paulholds an MA in Philosophy, Politics andEconomics from Keble College, Oxford.

42

G7 Fixed Income Fund

BIOGRAPHIES

Trevor WelshSenior Fund Manager

Joined investment industry in 1984

Main Responsibilities Trevor has primary responsibility for multi assetliability managed portfolios, cash plus portfolios,and also specialises in the actively managedUK and global inflation funds.

Experience & qualificationsTrevor joined the firm in 1998. At AvivaInvestors he has progressed from portfoliomanagement strategist to Senior FundManager in the UK Sovereign team. InFebruary 2003 he was involved with the launchof our sovereign relative value hedge fundstrategy. Trevor previously worked for Philipsand Drew/UBS from 1984 – 1998 as executivedirector for European fixed income exchangetraded derivatives where he specialised in thefutures market.

Trevor holds a BA (Hons) in Economics,Financial Management and Accounting fromSheffield University.

Upkar Kambo, CFAHead of Quantitative Strategies

Joined investment industry in 1992

Main Responsibilities Co-ordination of range of internal and externalquantitative inputs. Maintaining, enhancing, anddeveloping new models for use in the fixed incomeprocess - e.g. forecasting (econometric andotherwise), valuation, technical. Liaise with risk teamto develop more comprehensive risk analytics forfixed income needs, and contribute to their integrationin the investment process.

Experience & qualificationsPrior to joining Aviva Investors, Upkar spent 11 yearsat UBS Asset Management as a quantitative analystand strategist, the last seven years of this role wasspent specialising in fixed income.

He holds a BEng (Hons) in engineering from ImperialCollege, London University, an MPhil in managementstudies (finance) from Queens’ College, CambridgeUniversity and an MBA from the London BusinessSchool. Upkar is a CFA charterholder and is amember of the Institution of Investment Managementand Research (IIMR).

Ben Maynard, CFADerivatives Analyst

Joined investment industry in 1996

Main Responsibilities Managing the derivative strategy andportfolio analytics team.

Experience & qualificationsBefore joining Aviva in 2008, Ben workedat Henderson Global Investors for fiveyears as a derivative specialist and headof the equity derivative trading desk. Priorto this he worked at AMP AssetManagement (NZ) as a client servicemanager and at NCL Investments as anequity trader.

Ben is a full CFA charter holder holds andalso holds an MA (Hons) in archaeologyfrom University of Edinburgh.

43

G7 Fixed Income Fund

BIOGRAPHIES

44

G7 Fixed Income Fund

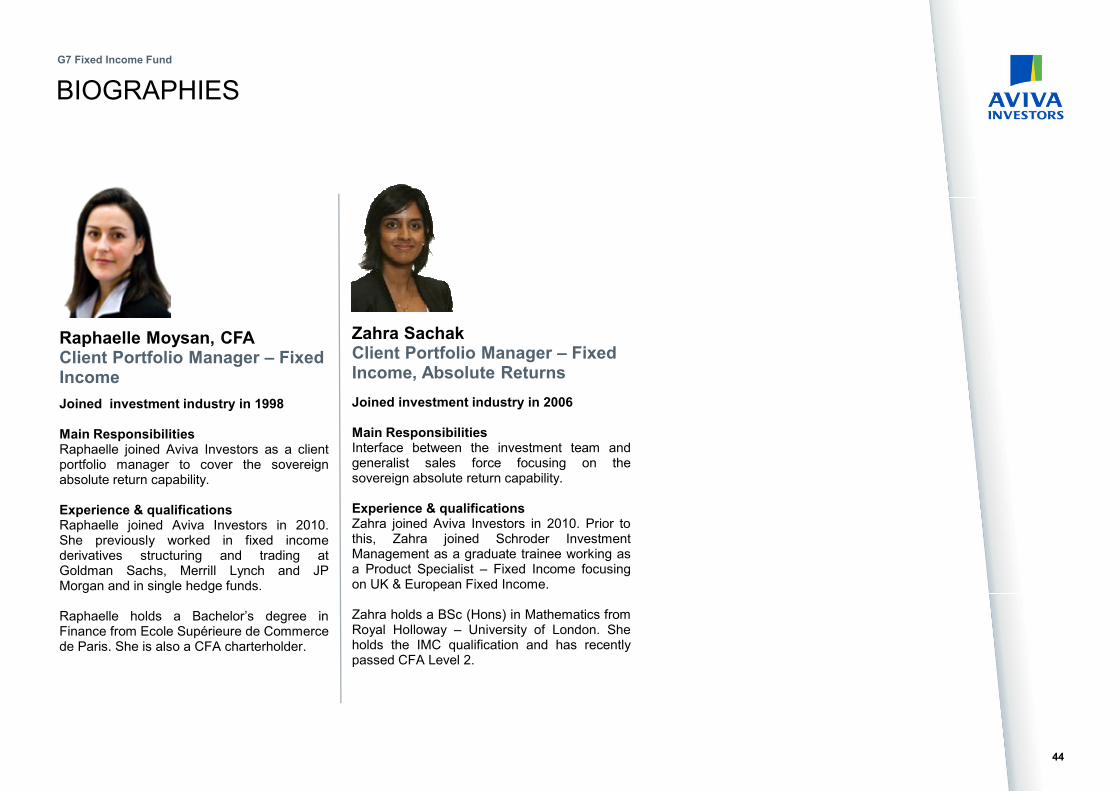

Raphaelle Moysan, CFAClient Portfolio Manager – Fixed Income

Joined investment industry in 1998

Main ResponsibilitiesRaphaelle joined Aviva Investors as a clientportfolio manager to cover the sovereignabsolute return capability.

Experience & qualificationsRaphaelle joined Aviva Investors in 2010.She previously worked in fixed incomederivatives structuring and trading atGoldman Sachs, Merrill Lynch and JPMorgan and in single hedge funds.

Raphaelle holds a Bachelor’s degree inFinance from Ecole Supérieure de Commercede Paris. She is also a CFA charterholder.

Zahra SachakClient Portfolio Manager – Fixed Income, Absolute Returns

Joined investment industry in 2006

Main Responsibilities Interface between the investment team andgeneralist sales force focusing on thesovereign absolute return capability.

Experience & qualificationsZahra joined Aviva Investors in 2010. Prior tothis, Zahra joined Schroder InvestmentManagement as a graduate trainee working asa Product Specialist – Fixed Income focusingon UK & European Fixed Income.

Zahra holds a BSc (Hons) in Mathematics fromRoyal Holloway – University of London. Sheholds the IMC qualification and has recentlypassed CFA Level 2.

APPENDIX 5: INTRODUCTION TO AVIVA INVESTORS

45

G7 Fixed Income Fund

INTRODUCING AVIVA INVESTORS

Owned by Aviva plc, the UK’s largest insurer* and one of Europe’s leading providers of life and general insurance

• Listed on the London and New York stock exchanges

• Standard & Poor’s A+ rating (strong), with a stable outlook

• Aviva Investors operates around the world

• Local market insight, supported by full range of global services

• Over 1,200 employees in 15 countries and 20 locations

Financial stability and a wealth of experience and resources

*Based on aggregate FY10 UK life and pension sales (PVNBP) and general insurance gross written premiums.All data as at 31 December 2012. Source: Aviva Investors and Aviva plc

46

G7 Fixed Income Fund

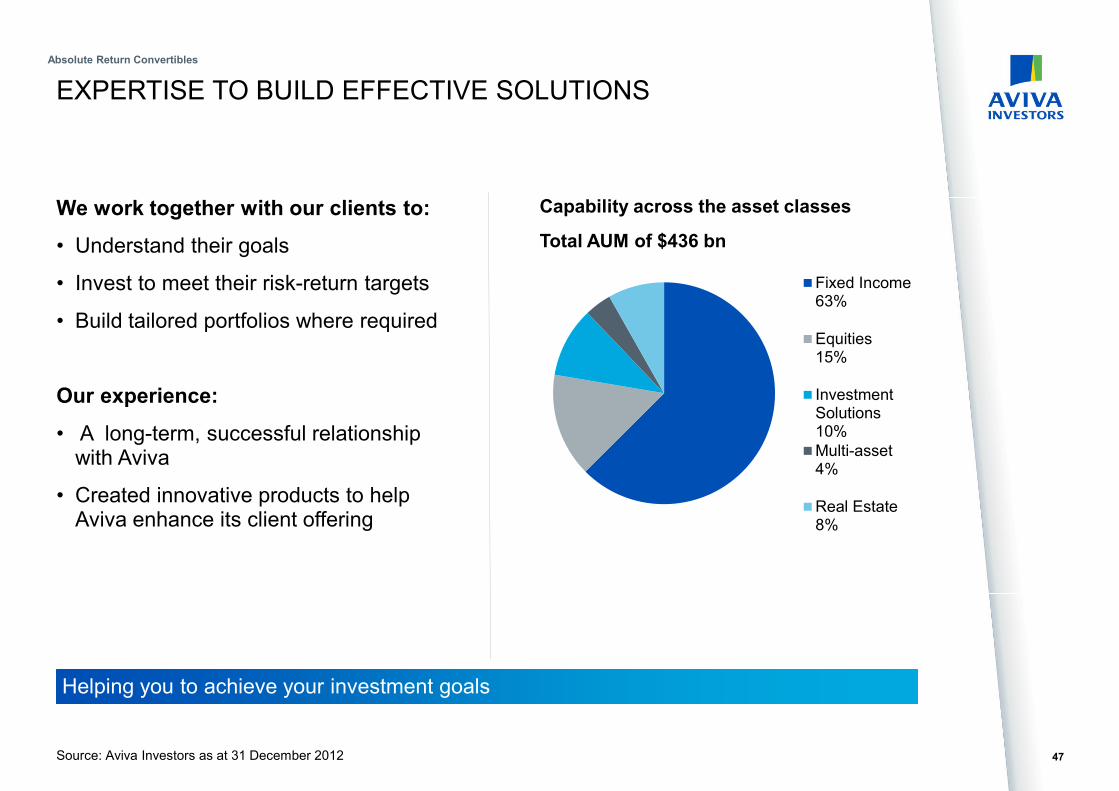

EXPERTISE TO BUILD EFFECTIVE SOLUTIONS

Source: Aviva Investors as at 31 December 2012

Fixed Income63%

Equities15%

InvestmentSolutions10%

Multi-asset4%

Real Estate8%

Capability across the asset classes

Total AUM of $436 bn

We work together with our clients to:

• Understand their goals

• Invest to meet their risk-return targets

• Build tailored portfolios where required

Our experience:

• A long-term, successful relationship with Aviva

• Created innovative products to help Aviva enhance its client offering

Helping you to achieve your investment goals

Absolute Return Convertibles

47

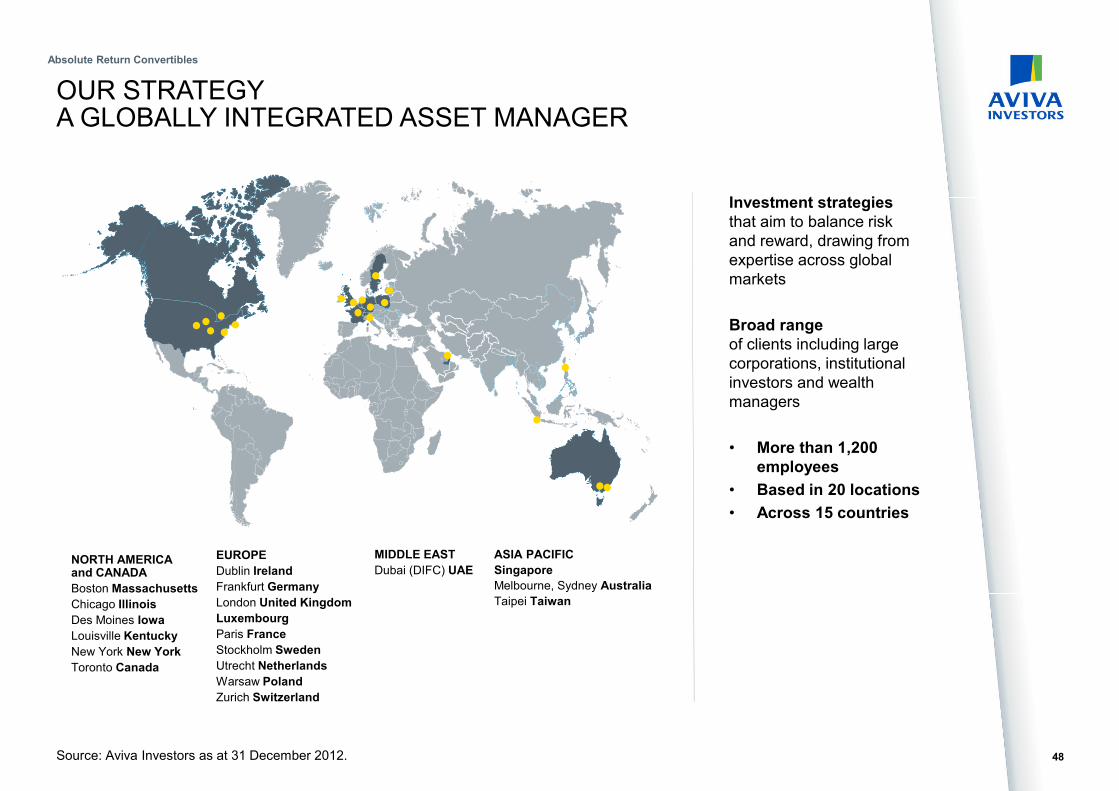

OUR STRATEGYA GLOBALLY INTEGRATED ASSET MANAGER

Source: Aviva Investors as at 31 December 2012.

NORTH AMERICA and CANADA

Boston Massachusetts

Chicago Illinois

Des Moines Iowa

Louisville Kentucky

New York New York

Toronto Canada

ASIA PACIFIC

Singapore

Melbourne, Sydney Australia

Taipei Taiwan

EUROPE

Dublin Ireland

Frankfurt Germany

London United Kingdom

Luxembourg

Paris France

Stockholm Sweden

Utrecht Netherlands

Warsaw Poland

Zurich Switzerland

MIDDLE EAST

Dubai (DIFC) UAE

Investment strategiesthat aim to balance risk

and reward, drawing from

expertise across global

markets

Broad rangeof clients including large

corporations, institutional

investors and wealth

managers

• More than 1,200employees

• Based in 20 locations

• Across 15 countries

Absolute Return Convertibles

48

PROVEN AND SUCCESSFUL INVESTMENT STRATEGIES

Specialist teams provide in-depth knowledge and expertise in local markets

Fixed income

• Liquidity

• Sovereign UK & Euro

• Global aggregate

• Credit

• High Yield

• Emerging market debt

• Convertible bonds

• Active LDI

• Global inflation

Real estate

• Global real estate

• Local real estate in UK,

Europe and Asia

• Multi-manager

• Real estate securities

• Specialist funds

Equities

• UK

• European

• Asia

• US

• Quantitative

49

G7 Fixed Income Fund

Absolute Returns

• Fixed income macro

& relative value

hedge funds

• Convertible arbitrage

hedge fund & absolute

return

• Credit absolute return

• Global markets alpha

Global business development –

sales, marketing, client servicing and product development

Global investment solutions –

managing assets that benefit from scale and consistency

Source: Aviva Investors as at 31 December 2012

APPENDIX 6: GIPS PERFORMANCE AND DISCLOSURES

50

G7 Fixed Income Fund

G7 FIXED INTEREST ABSOLUTE RETURN COMPOSITE & DISCLOSURES

YearComposite Return

Benchmark Return

Number of Portfolios (*throughout period)

DispersionMarket Value at end of Period

Percentage of Firm Assets

Total Firm Assets

Quarter To Date 0.09% 0.08% 1 (1) N/A 471,793,106 - -

Year To Date 0.09% 0.08% 1 (1) N/A 471,793,106 - -

Month To Date 0.65% 0.04% 1 (1) N/A 471,793,106 - -

2012 1.52% 0.64% 1 (1) N/A 470,088,917 - -

2011 4.26% 0.64% 1 (1) N/A 456,099,205 0.32% 143,217,403,309

2010 6.21% 0.55% 1 (1) N/A 514,584,281 0.36% 142,387,532,805

2009 7.82% 0.89% 1 (1) N/A 530,462,435 0.37% 141,904,207,047

2008 16.29% 5.57% 2 (2) N/A 489,853,134 0.36% 135,300,370,333

2007 12.09% 5.96% 2 (2) N/A 383,163,218 0.22% 174,529,956,735

2006 13.54% 4.82% 2 (1) N/A 294,630,570 0.18% 160,574,480,692

2005 6.12% 4.80% 1 (1) N/A 126,198,632 0.08% 155,130,806,273

2004 10.79% 4.67% 1 (1) N/A 252,787,597 0.18% 141,067,787,874

2003 (Mar) 12.91% 3.14% 1 (1) N/A 48,623,777 0.04% 116,525,244,219

Aviva Investors Global Services claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report incompliance with the GIPS Standards. Aviva Investors Global Services has been independently verified for the periods 1st January 1998 to 31st December 2010.The verification reports are available upon request. Verification assesses whether (1) the firm has complied with all the composite construction requirements of theGIPS standards on a firm-wide basis and (2) the firm's policies and procedures are designed to calculate and present performance in compliance with the GIPSstandards. Verification does not ensure the accuracy of any specific composite presentation. The firm is defined as Aviva Investors Global Services, whichincludes all managed assets, excluding closed ended direct real estate investments. The firm was redefined as of 31 December 2010, when the direct closed endassets were removed from the firm. Following a restructure within the Aviva Group, the assets managed by Aviva Investors Ireland Limited were transferred toAviva Investors Global Services in May 2010. The requirements and provisions for Performance Record Portability have been met and these assets continue to beincluded in their original composites. Further details are available upon request. This composite includes funds investing in global fixed income assets withabsolute return target. Leverage and short positions are an integral part of the composite strategy and may magnify losses and gains to the extent that leverage isdeployed. The portfolios within this composite may leverage up to 210% of the Net Asset Value of the fund. This composite was created on 31/12/2004. With astart date of 28/02/2003. Returns are presented net of management fees and other expenses. For unitised funds, gross returns are calculated by adding back theAnnual Management Charge (AMC), or part thereof, to the net return. Actual fees charged are dependent on the mandate and value of client assets. The fee scalefor pooled clients ranges from 0.2% p.a. to 1.8% p.a. and for segregated mandates the fee scale starts at 0.5% p.a. All income is taken gross of tax, but net ofirrecoverable taxes. Further information is available upon request. Aviva Investors Global Services has the ability to use leverage as part of its investmentmanagement process depending on the investment management agreement. If the client management agreement permits the discretionary use of options and orfutures, AIGSL will employ these strategies if the manager believes an opportunity exists to add value to the portfolio or minimise risk. AIGSL is permitted to useEfficient Portfolio Management (EPM) techniques as defined in the FSA Handbook. For Unit Linked Life funds a capital gains tax accrual is embedded in the unitprice. Composite dispersion is calculated using the asset-weighted standard deviation of all portfolios that were included in the composite for the entire year. If thecomposite includes less than 5 portfolios for the full year no measure of dispersion is shown. Additional information regarding policies for valuing portfolios/funds,and calculating and reporting returns is available upon request. A list and description of all composites is available upon request. This composite is benchmarkedagainst the 1mth LIBOR which is based on rates that contributor banks in London offer each other for inter-bank deposits. Past performance is not a guide tofuture performance. All figures are in GBP, gross of fees.

As at 28 February 2013 (Code on StatPro: GBLHdgeFi+NUIM) 51

G7 Fixed Income Fund

IMPORTANT INFORMATION

Except where stated as otherwise, the source of all information is Aviva Investors Global Services Limited (Aviva Investors) as at 31 March 2013.

The content of this document does not purport to be representational or provide warranties above and beyond those contained in the Prospectus and subscription documentation of the Fund. The Prospectus and the subscription document contain the full terms, conditions, representations and warranties in respect of the Fund. Nothing in this document shall be construed as forming any part of those terms, conditions, representations or warranties.

Any opinions expressed are based on the internal forecasts of Aviva Investors and they should not be relied upon as indicating any guarantee of return from an investment managed by Aviva Investors. No part of this document is intended to constitute advice orrecommendations of any nature.

The value of an investment in the fund can go down as well as up and investors may not get back the original amount invested. Past performance is not a guide to the future.

The distribution and offering of shares may be restricted by law in certain jurisdictions. This document should not be taken as a recommendation or offer by anyone in any jurisdiction in which such an offer is not authorised or to any person to whom it is unlawful to make such an offer or solicitation.

Aviva Investors Global Services Limited, registered in England No. 1151805. Registered Office: No. 1 Poultry, London EC2R 8EJ. Authorised and regulated in the UK by the Financial Services Authority and a member of the Investment Management Association.

Contact us at Aviva Investors Global Services Limited, No. 1 Poultry, London EC2R 8EJ.

Compliance ref: 13/0334/30062013

52

G7 Fixed Income Fund