avoiding icebergs: coping with disability presented by: janet freedman marie howes cifps conference...

TRANSCRIPT

AVOIDING ICEBERGS:AVOIDING ICEBERGS:COPING WITH DISABILITYCOPING WITH DISABILITY

PRESENTED BY:PRESENTED BY:

JANET FREEDMANJANET FREEDMAN

MARIE HOWESMARIE HOWESCIFPS Conference JUNE 2005CIFPS Conference JUNE 2005

©© Finance Matters Ltd../MoneySmart Inc.Finance Matters Ltd../MoneySmart Inc.

HIT BY AN ICEBERG:HIT BY AN ICEBERG:JANET’S STORYJANET’S STORY

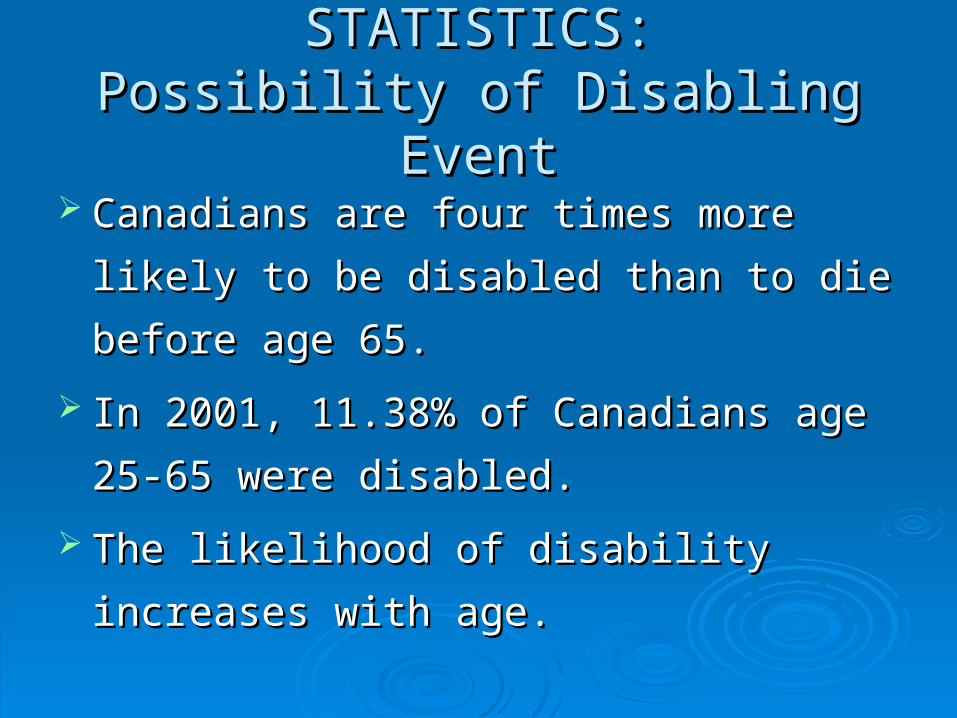

STATISTICS:STATISTICS:Possibility of Disabling EventPossibility of Disabling Event

Canadians are four times more likely to be Canadians are four times more likely to be

disabled than to die before age 65.disabled than to die before age 65.

In 2001, 11.38% of Canadians age 25-65 In 2001, 11.38% of Canadians age 25-65

were disabled.were disabled.

The likelihood of disability increases with The likelihood of disability increases with

age.age.

Age % of Canadians with a disability

% with a severe disability

25-54 9.2 3.8

55-64 21.8 9.8

65-74 31.2 10.5

75+ 53.3 23.6

DISABILITY IN CANADA 2001DISABILITY IN CANADA 2001

MARIE’S STORYMARIE’S STORY

SESSION OVERVIEWSESSION OVERVIEW

Power of Attorney for PropertyPower of Attorney for Property Power of Attorney for Personal Care Power of Attorney for Personal Care Financial issues around disabilityFinancial issues around disability Federal disability programmesFederal disability programmes Provincial disability programmes Provincial disability programmes Importance of LTD plansImportance of LTD plans The advisor’s role: pre & post disabilityThe advisor’s role: pre & post disability

POWER OF ATTORNEY FOR POWER OF ATTORNEY FOR PROPERTYPROPERTY

Holder of power (“donee”) has enormous Holder of power (“donee”) has enormous scope: choose the attorney carefully! If in scope: choose the attorney carefully! If in doubt – don’t appoint!doubt – don’t appoint!

Appoint alternates in case first choice not Appoint alternates in case first choice not available.available.

Must be “enduring” or “continuing” power to Must be “enduring” or “continuing” power to be effective in case of disability.be effective in case of disability.

Let the attorney know where document is & Let the attorney know where document is & how to access it: Lawyer’s office? Home how to access it: Lawyer’s office? Home file/strongbox? Safety deposit box?file/strongbox? Safety deposit box?

POWER OF ATTORNEY FOR POWER OF ATTORNEY FOR PROPERTY: PITFALLSPROPERTY: PITFALLS

Many employees of financial institutions Many employees of financial institutions do not understand a broad P of A; go up do not understand a broad P of A; go up the ladder!the ladder!

People confuse the executor of a will with People confuse the executor of a will with the holder of power of attorney.the holder of power of attorney.

If no P of A for property, Provincial Trustee If no P of A for property, Provincial Trustee takes over.takes over.

Holder of P of A takes care of bills and Holder of P of A takes care of bills and income for incapacitated person; big income for incapacitated person; big responsibility. Liability issues.responsibility. Liability issues.

““LIVING WILL”LIVING WILL” & “PERMISSION TO ACT” & “PERMISSION TO ACT”

Relates to medical & health care issues only. Is secondary to P of A for Property. Permission to act needed to give effect to

“Living Will”. Permission to act allows for broader powers Difficult to devise wording for “Living Will”. Not too broad or too restrictive. Medical people will ask next of kin. Can be important if no family or family distant

or estranged

““LIVING WILL” LIVING WILL” & “PERMISSION TO ACT”& “PERMISSION TO ACT”

The “John Doe,N.Y.”, Schiavo and Reeve cases show importance of these documents.

Some issues are: Quality of Life Definition of death “Extreme” or “Heroic” today, commonplace

tomorrow? There is a need for competent legal

advice, research & guidance.

FINANCIAL ISSUES:FINANCIAL ISSUES:How Much Money is Needed?How Much Money is Needed?

Review all fixed expenses.Review all fixed expenses. Can the mortgage be re-negotiated?Can the mortgage be re-negotiated? Can they downsize their home?Can they downsize their home? Do they need a car? Sell, if necessary.Do they need a car? Sell, if necessary. Review all flexible expenses.Review all flexible expenses. Evaluate needs versus wants.Evaluate needs versus wants. Cut back on eating out.Cut back on eating out. Reduce telephone, cell, or cable costs.Reduce telephone, cell, or cable costs.

FINANCIAL ISSUES;FINANCIAL ISSUES;Areas of increased expensesAreas of increased expenses

Uncovered medical expenses: massage, Uncovered medical expenses: massage, acupuncture etc.acupuncture etc.

Physiotherapy costs.Physiotherapy costs. Additional medical supplies.Additional medical supplies. Special dietary needs.Special dietary needs. Transportation: taxis, car re-fit etc.Transportation: taxis, car re-fit etc. Home care/nursing care.Home care/nursing care.

FINANCIAL ISSUESFINANCIAL ISSUESIncome SourcesIncome Sources

Short term disability/sickness plans.Short term disability/sickness plans. CPP Disability payments.CPP Disability payments. Long Term Disability Insurance.Long Term Disability Insurance. Investment income or cashing in RRSPs.Investment income or cashing in RRSPs. Spouse’s income sources.Spouse’s income sources. Family support (parents, siblings, children).Family support (parents, siblings, children). Advance on life insurance if terminal illness.Advance on life insurance if terminal illness. Critical Illness insurance.Critical Illness insurance. Accessing funds in Registered Pension Plans in Accessing funds in Registered Pension Plans in

some circumstances. some circumstances.

FEDERAL PROGRAMMES:FEDERAL PROGRAMMES:CPP Disability PensionCPP Disability Pension

CPP Disability Pension is:CPP Disability Pension is: Universal - covers all Canadian Workers;Universal - covers all Canadian Workers; Fully indexed to CPI;Fully indexed to CPI; Portable;Portable; Defined Benefit.Defined Benefit.

To collect, claimant must have contributions in 4 To collect, claimant must have contributions in 4 out of last 6 years.out of last 6 years.

Contributions are made on income over $3,500 Contributions are made on income over $3,500 per year to YMPE ($41,100, 2005).per year to YMPE ($41,100, 2005).

Designed to pay up to 25% of average industrial Designed to pay up to 25% of average industrial wage.wage.

FEDERAL PROGRAMMES:FEDERAL PROGRAMMES:CPP Disability PensionCPP Disability Pension

Definition: disability must be “severe and Definition: disability must be “severe and prolonged”. Very restrictive.prolonged”. Very restrictive.

Claimant must be unable to work regularly Claimant must be unable to work regularly in in any any substantially gainful employment.substantially gainful employment.

It is critical to apply as soon as possible It is critical to apply as soon as possible after disabling event. after disabling event.

No partial benefits are payable.No partial benefits are payable. 3 stage appeals process - the older the 3 stage appeals process - the older the

claimant, the more likely is success.claimant, the more likely is success.

CPP DISABILITY PENSIONCPP DISABILITY PENSIONAmounts PayableAmounts Payable

Maximum pension is $1010.23 per month.Maximum pension is $1010.23 per month.(This is higher than the CPP retirement (This is higher than the CPP retirement pension.)pension.)

Average pension approx.. $750 p.m.Average pension approx.. $750 p.m. Child benefit (age 18-25 in full-time Child benefit (age 18-25 in full-time

education) $195.96 p.m. education) $195.96 p.m. Child-raising dropout provision can increase Child-raising dropout provision can increase

benefits.benefits. Divorced contributors may be entitled to Divorced contributors may be entitled to

share CPP credits.share CPP credits.

CPP DISABILITY PENSIONCPP DISABILITY PENSIONImportant FactsImportant Facts

CPP is the “first payor”.CPP is the “first payor”. Most group LTD plans are integrated with Most group LTD plans are integrated with

CPP. Therefore if CPP pays, LTD plan will CPP. Therefore if CPP pays, LTD plan will cut back, dollar for dollar.cut back, dollar for dollar.

CPP pays CPP pays beforebefore Provincial Social Provincial Social Assistance plans and Worker’s Assistance plans and Worker’s Compensation.Compensation.

Quebec Pension Plan (QPP) similar but Quebec Pension Plan (QPP) similar but not identical.not identical.

CPP DISABILITY PENSIONCPP DISABILITY PENSIONPossible PitfallsPossible Pitfalls

Taking early retirement options means Taking early retirement options means claimant no longer eligible for CPP claimant no longer eligible for CPP disability benefits.disability benefits.

Some disability professionals recommend Some disability professionals recommend not applying for CPP as LTD or Workers’ not applying for CPP as LTD or Workers’ Comp cut back $ for $. But during a CPP Comp cut back $ for $. But during a CPP disability claim, CPP retirement pension is disability claim, CPP retirement pension is protected (i.e. years when collecting CPP protected (i.e. years when collecting CPP disability excluded from calculations). Not disability excluded from calculations). Not collecting CPP disability can seriously collecting CPP disability can seriously negatively impact CPP retirement benefits.negatively impact CPP retirement benefits.

CPP DISABILITY PENSIONCPP DISABILITY PENSIONPoints to RememberPoints to Remember

CPP disability benefits are taxable and CPP disability benefits are taxable and count as earned income for RRSP count as earned income for RRSP contribution limits.contribution limits.

There is a 4 month waiting period for There is a 4 month waiting period for benefits.benefits.

It is important to apply as soon as eligible. It is important to apply as soon as eligible. Retroactive CPP disability payments are Retroactive CPP disability payments are

no longer payable to estates.no longer payable to estates. Complicated return to work rules.Complicated return to work rules.

FEDERAL PROGRAMMES: FEDERAL PROGRAMMES: E.I. Sickness BenefitsE.I. Sickness Benefits

Short term: covers just 15 weeks of Short term: covers just 15 weeks of sickness/injury.sickness/injury.

Family supplement is available to those who Family supplement is available to those who qualify.qualify.

Some income will reduce EI payments $ for $ Some income will reduce EI payments $ for $ (employment, workers’ compensation, group (employment, workers’ compensation, group sickness or LTD plan). sickness or LTD plan).

EI not reduced by income from CPP & QPP EI not reduced by income from CPP & QPP disability pensions, private EHP or LTD plan and disability pensions, private EHP or LTD plan and WCB permanent settlements.WCB permanent settlements.

PROVINCIAL BENEFIT PLANSPROVINCIAL BENEFIT PLANSSOCIAL ASSISTANCESOCIAL ASSISTANCE

Social Assistance programmes provide Social Assistance programmes provide minimum income support & some medical minimum income support & some medical benefits for people with disabilities.benefits for people with disabilities.

SA programmes are “last payor”.SA programmes are “last payor”. Disability support programmes based on Disability support programmes based on

disability & other factors, income is one disability & other factors, income is one factor.factor.

Provincially regulated - no two provinces the Provincially regulated - no two provinces the same.same.

Ontario Disability Support Program is one.Ontario Disability Support Program is one.

ONTARIO DISABILITY SUPPORT ONTARIO DISABILITY SUPPORT PROGRAMME (ODSP)PROGRAMME (ODSP)

Person with a disability must be over age 18 with a Person with a disability must be over age 18 with a substantial physical or mental impairment which is substantial physical or mental impairment which is continuous or recurrent, and which is expected to continuous or recurrent, and which is expected to last 1 year or more.last 1 year or more.

Claimant must not have money or assets above a Claimant must not have money or assets above a certain level ($5,000 for single person).certain level ($5,000 for single person).

Definition of assets and income is key – and Definition of assets and income is key – and complex.complex.

Claimant must obtain other income/financial Claimant must obtain other income/financial resources to which they are entitled.resources to which they are entitled. CPP Disability; CPP Disability; Workers’ Comp;Workers’ Comp; Child Support/Alimony.Child Support/Alimony.

ONTARIO DISABILITY SUPPORT ONTARIO DISABILITY SUPPORT PROGRAMMEPROGRAMME

Maximum ODSP $959 per month in 2005 Maximum ODSP $959 per month in 2005 made up of:made up of: $532 basic needs, and $532 basic needs, and $427 housing.$427 housing.

In Ontario, ODSP has been downloaded onto In Ontario, ODSP has been downloaded onto municipalities.municipalities.

Some provinces have a centralized system.Some provinces have a centralized system. Provincial web sites have most information Provincial web sites have most information

but be careful - definitions are confusing and but be careful - definitions are confusing and complex.complex.

ONTARIO DISABILITY SUPPORT ONTARIO DISABILITY SUPPORT PROGRAMMEPROGRAMME

It is important for advisors to be aware of It is important for advisors to be aware of these programmes as we often have clients these programmes as we often have clients with disabled adult children or siblings.with disabled adult children or siblings.

It is very easy to lose entitlement.It is very easy to lose entitlement. Care needs to be taken in setting up trusts, Care needs to be taken in setting up trusts,

gifting money or making bequests to gifting money or making bequests to recipients of disability support programmes. recipients of disability support programmes.

Henson TrustsHenson Trusts help alleviate funding issues; help alleviate funding issues; parents with disabled children should parents with disabled children should consider them.consider them.

ONTARIO DISABILITY SUPPORT ONTARIO DISABILITY SUPPORT PROGRAMMEPROGRAMME

Why should it matter if entitlement is lost Why should it matter if entitlement is lost due to an inheritance?due to an inheritance? Often, the health care benefits are more Often, the health care benefits are more

important than the ODSP. Even if only $5 per important than the ODSP. Even if only $5 per month of disability support is received, full month of disability support is received, full health care benefits are available. Many health care benefits are available. Many medication costs can run $500 to $1000 or medication costs can run $500 to $1000 or more per month.more per month.

Possibility of losing housing subsidy and in Possibility of losing housing subsidy and in some cases supportive housing environment.some cases supportive housing environment.

WORKERS’ COMPENSATIONWORKERS’ COMPENSATION

Provincially Regulated programmes to Provincially Regulated programmes to provide benefits to workers injured on-the- provide benefits to workers injured on-the- job or with occupational diseases.job or with occupational diseases.

No-faultNo-fault programs: if an employee is programs: if an employee is eligible to receive workers’ compensation, eligible to receive workers’ compensation, the employee cannot sue the employer.the employee cannot sue the employer.

WCB is independent from government and WCB is independent from government and funded by premiums charged to the funded by premiums charged to the employers.employers.

SO WHAT DO CLIENTS SO WHAT DO CLIENTS NEED?NEED?

MAXIMUM available from CPP disability is MAXIMUM available from CPP disability is $1010 per month.$1010 per month.

EI is limited and short term.EI is limited and short term. Workers’ Comp is only for on-the-job Workers’ Comp is only for on-the-job

injuries/sickness and may take a long time injuries/sickness and may take a long time for claim to be processed.for claim to be processed.

Provincial social benefits are a last resort.Provincial social benefits are a last resort.

Clients need LTD!Clients need LTD!

LONG TERM DISABILITY LONG TERM DISABILITY INSURANCEINSURANCE

LTD is wage loss replacement insurance.LTD is wage loss replacement insurance. Policies can cover the widest possible Policies can cover the widest possible

definition of disability (from Accident to definition of disability (from Accident to Stress).Stress).

Can provide monthly income to age 65. Can provide monthly income to age 65. With COLA, this can run into hundreds of With COLA, this can run into hundreds of thousands of dollars in payments for long thousands of dollars in payments for long term beneficiaries.term beneficiaries.

GROUP LTD PLANSGROUP LTD PLANS Many are last payor - reduced by CPP, Many are last payor - reduced by CPP,

Workers’ Comp. and any other LTD policies.Workers’ Comp. and any other LTD policies. Definition of occupation may be restrictive:Definition of occupation may be restrictive:

OWN occupation;OWN occupation; REGULAR occupation;REGULAR occupation; ANY occupation by virtue of training, education ANY occupation by virtue of training, education

and experience;and experience; ANY occupation.ANY occupation.

Duration of coverage often 2-5 years “own” or Duration of coverage often 2-5 years “own” or “regular” occupation; then “any” occ. “regular” occupation; then “any” occ.

Can pay to age 65 for total disability.Can pay to age 65 for total disability.

INDIVIDUAL LTD PLANSINDIVIDUAL LTD PLANS

More expensive than group plans.More expensive than group plans. More options:More options:

COLA;COLA; flexible waiting period;flexible waiting period; residual income benefits;residual income benefits; return of premium;return of premium; to age 65 (or longer) own or regular occ.;to age 65 (or longer) own or regular occ.; future insurability - right to purchase additional future insurability - right to purchase additional

coverage;coverage; Most benefits are non-taxable.Most benefits are non-taxable.

LONG TERM DISABILITY LONG TERM DISABILITY Points to RememberPoints to Remember

Diagnosis does not equal disability.Diagnosis does not equal disability. New employees in group plans not covered New employees in group plans not covered

for 3 months. This is for 3 months. This is employer’s employer’s choice not choice not insurance company policy.insurance company policy. Employer can Employer can get insurer to make an exception for get insurer to make an exception for employee.employee.

Claims in first 2 years of policy are Claims in first 2 years of policy are contestable.contestable.

50% claims estimated to be mental or 50% claims estimated to be mental or nervous in origin.nervous in origin.

Compcorp coverage $2,000 p.m. benefits.Compcorp coverage $2,000 p.m. benefits.

THE ADVISOR’S ROLETHE ADVISOR’S ROLE

ResearchResearch EducationEducation PreparednessPreparedness ImplementationImplementation GuidanceGuidance SupportSupport

THE ADVISOR’S ROLE:THE ADVISOR’S ROLE:Pre- Claim (1)Pre- Claim (1)

Review and evaluate client LTD and Life Review and evaluate client LTD and Life insurance.insurance.

Consider CI if not eligible for LTD.Consider CI if not eligible for LTD. Encourage client to set up Power of Encourage client to set up Power of

Attorney for Property and Power of Attorney for Property and Power of Attorney for Personal Care/Living Will.Attorney for Personal Care/Living Will.

Maintain client’s current Net Worth, Cash Maintain client’s current Net Worth, Cash Flow, advisor contact list & location of Flow, advisor contact list & location of important documents.important documents.

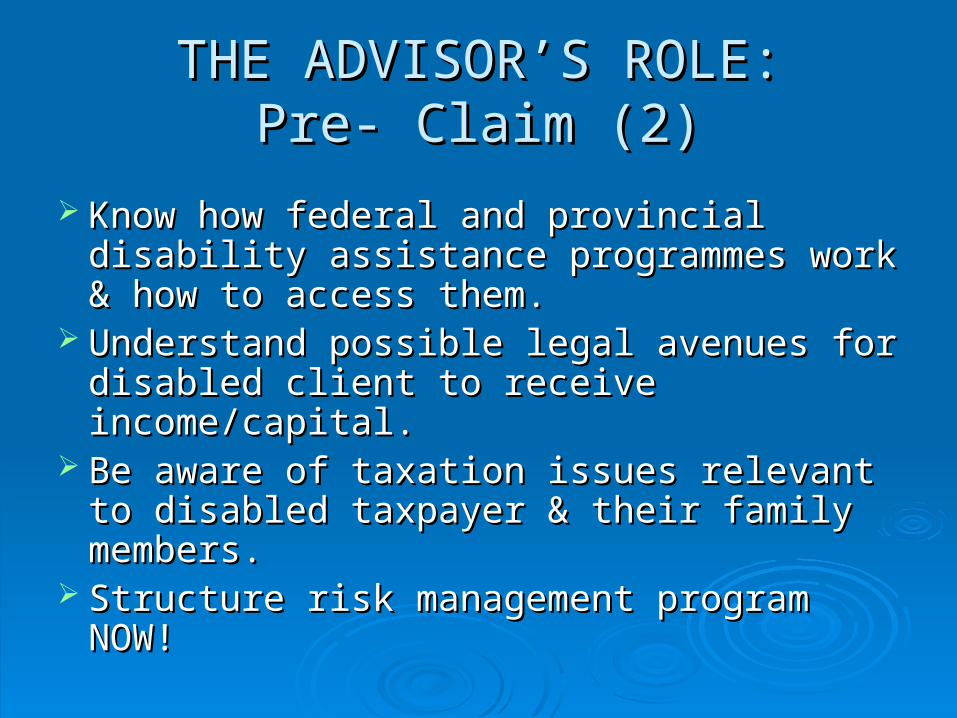

THE ADVISOR’S ROLE:THE ADVISOR’S ROLE:Pre- Claim (2)Pre- Claim (2)

Know how federal and provincial disability Know how federal and provincial disability assistance programmes work & how to assistance programmes work & how to access them.access them.

Understand possible legal avenues for Understand possible legal avenues for disabled client to receive income/capital.disabled client to receive income/capital.

Be aware of taxation issues relevant to Be aware of taxation issues relevant to disabled taxpayer & their family members.disabled taxpayer & their family members.

Structure risk management program Structure risk management program NOW! NOW!

THE ADVISOR’S ROLETHE ADVISOR’S ROLEPOST-CLAIMPOST-CLAIM

Explain LTD to claimant and family.Explain LTD to claimant and family. Explain role of EI & CPP disability Explain role of EI & CPP disability

benefits.benefits. Ascertain if other coverage is available:Ascertain if other coverage is available:

Personal LTD;Personal LTD; Critical Illness, Long Term Care;Critical Illness, Long Term Care; ADD or other Life insurance.ADD or other Life insurance.

Provide support during claims process.Provide support during claims process.

AVOIDING ICEBERGS:AVOIDING ICEBERGS:A CALL TO ACTIONA CALL TO ACTION

Procrastination is Enemy #1!Procrastination is Enemy #1! Clients’ lack of knowledge is Enemy Clients’ lack of knowledge is Enemy

#2!#2! As financial planners, we are also As financial planners, we are also

educators.educators. If not You, then Who?If not You, then Who?

““Nothing in life is to be feared, Nothing in life is to be feared, it is only to be understood. it is only to be understood.

Now is the time to understand Now is the time to understand more that we may fear less.” more that we may fear less.”

Marie CurieMarie Curie