awareness generation and initiatives of the life insurance...

TRANSCRIPT

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

1

www.globalbizresearch.org

Awareness generation and Initiatives of the

Life Insurance Companies in India for inclusive growth

Dr. Nagaraja Rao,

Alliance School of Business,

Alliance University,

Bangalore, India.

Dr. Sukanya Kundu,

Alliance School of Business,

Alliance University,

Bangalore, India.

_____________________________________________________________________

Abstract

Only 21% of insurable population is covered by the all twenty and odd life insurance

companies and there is much untapped potential in the areas. In order to analyze the reasons,

the researchers conducted a survey in two rural districts of Karnataka, India and collected

data from 500 policyholders and 200 insurance agents. The data was later on tabulated and

analyzed with SPSS package.

The results indicate that low levels of insurance awareness are the main reason for people not

going for insurance. Life insurance, though an essential commodity, is sold and rarely

bought. Though the regulatory body, the Insurance Regulatory and Development Authority

(IRDA) ordains certain rural obligations on all the players in this sector, they are viewed

more as obligations and companies evince a very little interest in promoting inclusive growth.

Further people in rural India have no belief in the efficacy of regulatory body, i.e., Insurance

Regulatory and Development Authority (IRDA) and they do not perceive investment in private

companies as safe. The products of life insurance companies do not focus exclusively for

rural areas and as a result of which major chunk of rural India is isolated by life insurance

companies and inclusive growth and inclusive protection have become distant dreams.

___________________________________________________________________________

Key Words: Insurance awareness, rural India, inclusive growth

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

2

www.globalbizresearch.org

1. Introduction

In India rural market is significantly different from the urban market. It consists of a set of

customers exhibiting behavior that is different from the behavior of consumers in urban areas

in terms of needs and wants, social and cultural practices, nature of occupation etc.

(Velayudhan, 2007). Rohrer (1999) characterized rural market segment as less identifiable,

less accessible, resistant, limited resources, less affordability, high vulnerability and

underserved. Rural markets require a different marketing approach because of variation in

consumer behavior and income levels and also differences in macro and micro environment

of consumers located in rural areas (Rajendhiran, Saiganesh and Asha, 2004). Against any

human indicators the performance of rural India lags far behind urban India (Ahmed, 2013).

70% of Indian population live in rural areas but have no access; or have negligible access to

insurance (Gopinath, 2009). Promotional activities and agents of life insurance companies are

all about to inform, bringing awareness, develop belief, to reinforce trust etc. (Venugopal,

2008). Selling of life Insurance products largely depends on the skill and efficiency of the

distributor. In Indian market with aggressive marketing approach private players are gradually

capturing the Indian market and giving direct threat to the dominant life Insurance player like

LIC (Sharma, 2010). Companies such as ICICI Prudential Life Insurance and ING Vysya Life

Insurance have tied-up with Suvidhaa Infoserve, which runs 13,000 kirana stores that

provides grocery, mobile and telephone services, pharmacy products, internet and travel

services to customers in 400-odd locations. The tie-up allows a policyholder to pay his

premium at the store, where the store owner will punch details into a kiosk to generate a

payment receipt. DLF Pramerica Life Insurance has partnered with Srei Sahaj E-Village, an

arm of Srei Infrastructure Finance, to reach out to 27,000 villages, while Max New York Life

has tied up with Kisan Seva Kendras run by Indian Oil Corporation in rural areas.

It is important for the insurance service providers to understand the need and want of the

rural population and to formulate marketing and operational policies accordingly to create

awareness as a first step to capture the potential that lies in rural Indian market. The pulse of

the customers and distributors is to be analyzed by the Insurance service providers in order to

design suitable products for the customers in rural areas. Several researches can be found on

customer satisfaction with insurance products in India and abroad (Tsoukatos and Rand,

2007; Kaur and Negi, 2010; Borah, 2013; Gizaw and Pagidimarri, 2014). This paper analyses

the perceptions of rural customers and insurance advisers regarding hurdles in selling policies

in rural areas and the willingness of the insurance companies to cater to the rural areas,

features of insurance policies to meet rural customers’ needs etc. It also tries to find out the

customer perception particularly on safety aspect to invest in insurance products of private

players.

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

3

www.globalbizresearch.org

2. Literature Review

Bodla and Verma (2007) studied buyer behavior regarding life insurance policies in the

rural area of Haryana. The study revealed that respondents belonging to the age group 31-40

years dominate the rural insurance market; agents are the most important source of

information and motivation as the people take a policy that is suggested by the agent. Athma

and Kumar (2007) in their article tried to identify the factors which the consumers take into

consideration before selecting life Insurance products. Both, product and non-product

attributes have been found to be important in selecting a policy but they have been rated

differently. Rating is different in urban and rural areas. In case of urban areas, product

attributes are ranked first and non-product attributes like agents and company are secondary.

At the same time, in rural areas, non-product attributes play a major role in selection of a

policy. Thamodaran and Ramesh (2010) found the influence of demographic variables like

education, occupation and income factors to the respondents’ decision making factors like

awareness, getting interest and purchase intention. The study carried out in rural India found

out that there is no difference of opinion among the respondents towards creating awareness

on insurance through print advertisement based on their educational level. In his paper

Ahmed (2013) examines the present state of affairs of rural life insurance in India and

attempts to explore the issues and challenges which led to poor penetration of rural life

insurance markets. The research study of Borah (2013) revealed insurance companies should

give more importance in the reliability, assurance and empathy factors to enhance customer

satisfaction.

The articles from the journal of the regulatory body, viz, Insurance Regulatory and

Development Authority (IRDA) for the last five years also helped in finding authenticated

information on life insurance market in India. The major reports on the insurance market in

India, viz, Capgemeni’s World Insurance Report, 2008, Old Age Social & Income Security

Report (OASIS) and Mckinsey & CO Report on Insurance, 2007 are reviewed. Scores of

research articles presented for different Universities by different research scholars are also in

handy for the relevant topic of research.

The literature review points out that there is a wide gap between the rural insurance tapped

so far vis-à-vis the potential available. Hardly 25% of the eligible rural people are covered by

any form of life insurance. The second important point emanated out of the literature survey

is that there has been no systematic study of rural life insurance market from the perspectives

of customers and insurance agents and all the literature is generic in nature based on

secondary data.

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

4

www.globalbizresearch.org

Thirdly there is no research on the life insurance awareness levels of rural people and

actual interest shown by the life insurance companies in product design and in educating the

rural people.

The research problem, therefore, is how best we can increase the insurance coverage in

rural areas. The article works in that direction with the objective studying the perceptions of

the customers and facilitating the analysis to insurance providers for their advantage.

3. Methodology

The study was conducted in rural areas of two districts of Karnataka- Bangalore and Kolar.

The two districts are selected as all private players and the public sector LIC (Life Insurance

Corporation of India) have offices in these two districts.

Customers are selected on simple random sampling basis and responses for a questionnaire

were collected from 250 customers each from the two districts and thus the total respondents

are 500. 200 agents of major five insurance companies were also contacted (100 each from

Bangalore rural and Kolar rural) and obtained the responses. The presence of majority of

private life insurance companies in these two districts provided an opportunity to study the

life insurance market in a thorough manner.

The research design selected is ‘exploratory’ research and the major emphasis is on the

discovery of ideas and insights. The primary data is collected through questionnaires. The

questionnaire was simple and easy to understand with both open-ended and close-ended

questions taking in to account the intellectual levels of the rural customers.

4. Results

SPSS (Statistical Package for Social Sciences) was applied for data analysis. The secondary

data is collected from servicing manuals, insurance reports, journals and various websites of

the insurance companies.

4.1 Agent perception

Hurdles in selling policies in rural areas:

An exclusive question was put to the insurance advisors/ agents asking about their perception

as to what they feel hurdles in selling the policies in rural areas. The responses are depicted in

Figure 1:

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

5

www.globalbizresearch.org

Figure 1: Hurdles in selling policies in rural areas

The question aimed at eliciting information from the agents as to the exact hurdles in selling

policies in rural areas.

26% Bangalore rural district agents and by 55% of Kolar rural agents attribute the low

penetration of life insurance in rural areas to ‘lack of awareness’.

47% Bangalore rural district agents and by 34% of Kolar rural agents attribute the low

penetration of life insurance in rural areas to ‘lack of need based’ products.

It can be inferred that there is a strong reason for creating insurance awareness and design

need based policies in rural areas.

Exclusiveness of life insurance products to meet rural customer needs:

Figure 2: Exclusiveness of life insurance products to meet rural customer needs

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

6

www.globalbizresearch.org

The Figure 2 is aimed at eliciting information from the customers if the products of

insurance companies tailored to the needs of the customers.

76% Bangalore rural district agents and by 77% of Kolar rural agents attribute the low

penetration of life insurance in rural areas to ‘lack of awareness’ opine that the products are

not really designed to the needs and requirements of the policyholders.

The insurance companies need to take this aspect in to consideration. They need to

evaluate the usefulness of their existing products and also design rural customer oriented

products for their own benefit.

Willingness of life insurance companies in rural business:

Figure 3: Willingness of life insurance companies in rural business

The Figure 3 is aimed at eliciting information from the insurance advisors/ agents if the

existing life insurance companies evince any real interest in rural life insurance business.

79% Bangalore rural district agents and by 89% of Kolar rural agents opine that the life

insurance companies are not interested in the rural life insurance business.

Summary of the primary data suggests that the life insurance awareness in rural areas is

very low and insurance companies are not evincing much interest in developing insurance

business in rural areas.

Customer perception

Safety of investment in private companies:

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

7

www.globalbizresearch.org

Figure 4: Safety of investment in private companies

The Figure 4 is aimed at eliciting the views of the customers if their investments in private

companies would be safe and secure.

Out of 250 Bangalore rural district policyholders as many as 161 policyholders

constituting 64.4% opine that investments in private life insurance companies are unsafe.

Out of 250 Kolar rural district policyholders as many as 148 policyholders constituting 59.2%

opine that investments in private life insurance companies are unsafe.

Hypothesis testing:

The rural customers of life insurance companies feel that their investments in

private life insurance companies are secure.

A Chi-Square test is conducted in order to test the frequency of responses. From the

secondary data the safety aspect of private insurers is not available anywhere and hence we

have taken 50% since the probability of answering ‘yes’ or ‘no’ is 50%.

H0: There is no significant difference between the opinion of the rural policyholders if their

investments in private life insurance companies are safe or unsafe.

H1: There is significant difference between the opinion of the rural policyholders if their

investments in private life insurance companies are safe or unsafe.

Table 1: results of Chi-Square (the proportions among the responses of the respondents)

Investment in

private life

insurance are

safe

Category N Expected df Chi Square Significance

Yes 191 250 1 27.85 at 0.01 Level

No 309 250

Total 500 500

The Chi-Square results show less than 1% of significance level and hence the null

hypothesis is rejected. It can be concluded that there is significant difference between the

opinions of the rural policyholders about investments in private life insurance companies.

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

8

www.globalbizresearch.org

Frequency of responses shows that investment in private companies is viewed upon as unsafe

by the rural policyholders.

To ascertain if the opinion is same across Bangalore rural and Kolar rural districts, the

proportions are also compared between the districts.

H0: There is no significant difference in the opinion of the Bangalore rural policy holders and

Kolar rural policyholders that investment in private life insurance companies is unsafe.

H1: There is significant difference in the opinion of the Bangalore rural policy holders and

Kolar rural policyholders that investment in private life insurance companies is unsafe.

Table 2: Results of Chi-Square test (the proportions across the districts)

Premiums

for Private

Insurers are

secure

Category N Expected df Chi Square Significance

Bangalore 89 95.5 1 0.88 Not Significant

Kolar 102 95.5

Total 191 191

The results reveal that the Significance value is 0.88 at 1% significance level. Therefore,

the null hypothesis is accepted. It can be concluded that there is no difference in the opinion

of Bangalore district rural policyholders and Kolar district rural policyholders that

investments in private life insurance companies are unsafe. In both Bangalore and Kolar rural

districts, the policy holders opine that investments in private life companies are unsafe.

From the above, it can be inferred that awareness about regulatory mechanism is very low

in rural areas of both Bangalore and Kolar. The insurers have to focus on this lack of

awareness and try to create/ enhance awareness levels in rural areas.

IRDA can take care of the safety of customer investments

Figure 5: IRDA can take care of the safety of customer investments

119 respondents in Bangalore rural and 121 respondents from Kolar feel that IRDA can

effectively safe guard their investments in insurance companies. 131 respondents of

Bangalore and 129 respondents of Kolar feel that IRDA cannot safeguard their investments.

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

9

www.globalbizresearch.org

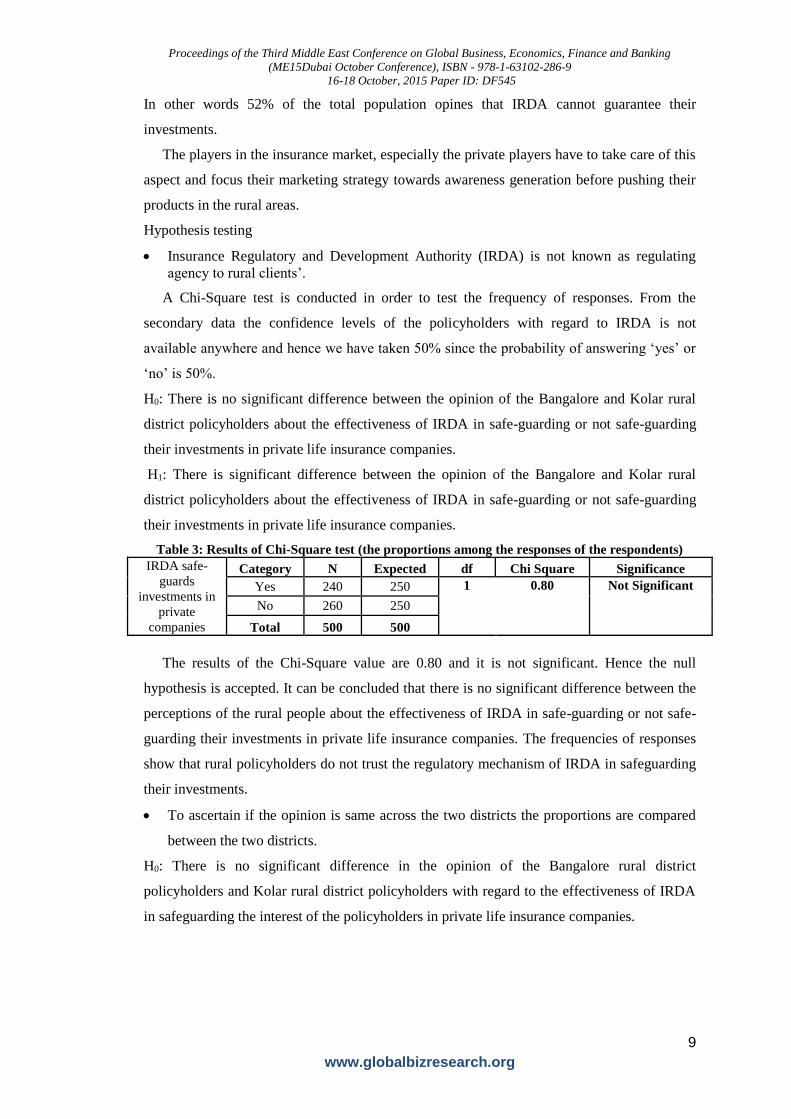

In other words 52% of the total population opines that IRDA cannot guarantee their

investments.

The players in the insurance market, especially the private players have to take care of this

aspect and focus their marketing strategy towards awareness generation before pushing their

products in the rural areas.

Hypothesis testing

Insurance Regulatory and Development Authority (IRDA) is not known as regulating

agency to rural clients’.

A Chi-Square test is conducted in order to test the frequency of responses. From the

secondary data the confidence levels of the policyholders with regard to IRDA is not

available anywhere and hence we have taken 50% since the probability of answering ‘yes’ or

‘no’ is 50%.

H0: There is no significant difference between the opinion of the Bangalore and Kolar rural

district policyholders about the effectiveness of IRDA in safe-guarding or not safe-guarding

their investments in private life insurance companies.

H1: There is significant difference between the opinion of the Bangalore and Kolar rural

district policyholders about the effectiveness of IRDA in safe-guarding or not safe-guarding

their investments in private life insurance companies.

Table 3: Results of Chi-Square test (the proportions among the responses of the respondents) IRDA safe-

guards

investments in

private

companies

Category N Expected df Chi Square Significance

Yes 240 250 1 0.80 Not Significant

No 260 250

Total 500 500

The results of the Chi-Square value are 0.80 and it is not significant. Hence the null

hypothesis is accepted. It can be concluded that there is no significant difference between the

perceptions of the rural people about the effectiveness of IRDA in safe-guarding or not safe-

guarding their investments in private life insurance companies. The frequencies of responses

show that rural policyholders do not trust the regulatory mechanism of IRDA in safeguarding

their investments.

To ascertain if the opinion is same across the two districts the proportions are compared

between the two districts.

H0: There is no significant difference in the opinion of the Bangalore rural district

policyholders and Kolar rural district policyholders with regard to the effectiveness of IRDA

in safeguarding the interest of the policyholders in private life insurance companies.

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

10

www.globalbizresearch.org

H1: There is significant difference in the opinion of the Bangalore rural district policyholders

and Kolar rural district policyholders with regard to the effectiveness of IRDA in

safeguarding the interest of the policyholders in private life insurance companies.

The results of the Chi-Square test at 1% significance level are vide table 4 as follows:

Table 4: Results of Chi-Square test (the proportions across the districts)

Safety

guaranteed by

IRDA with

regard to

investments in

private life

insurance

companies.

Category N Expected df Chi Square Significance

Bangalore 119 120 1 0.02 Not Significant

Kolar 121 120

Total 240 240

The results of the Chi-Square value are 0.02 which is not significant. Hence the null

hypotheses are accepted. It can be concluded that there is no significant difference in the

opinion of the rural policyholders of Bangalore rural and Kolar rural districts with regard to

effective regulatory mechanism of IRDA with regard to investments in private life insurance

companies.

The IRDA and the life insurance companies have to educate the rural customers about the

role of IRDA as a regulating agency and boost the trust levels of the rural customers.

5. Discussion

The initiatives of the insurance companies in generating rural life insurance awareness

(Secondary data):

Life insurance deals with intangible products. The insurance companies sell a promise

which is to be redeemed at a future date. Unlike other intangible products of other service

companies, life insurance business has a tough job of selling a concept which is based on the

happening of the eventuality (death of the policyholder) which is repugnant to the ears of the

customers, particularly the rural folk. Given the awareness levels of the rural customers with

regard to life insurance, the sales of insurance product still more tuff. ‘Various Superstitions,

taboos, religious and cultural leanings, heterogeneity etc make things complicated. Further

there is the vast spectrum of village customs, dress and physique that make up the Indian

village tapestry. A picture of a Punjab farmer may not be acceptable to the farmer of Andhra

Pradesh’ (Rao, Nagaraja, 2011).

According to Shirodkar, “In view of this diversity LIC of India tried to take the lowest

common denominator in designing its communication tools. It has effectively made use of a

fleet of publicity vans with a special material prepared for the masses. The local heroes and

local themes are selected in films – for example, a film on Shivaji is shown in Maharashtra

whereas Rana Pratap was the theme in Rajastan. The death of these heroes is shown as a great

loss and had there been insurance, there would have been a little grievance (some financial

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

11

www.globalbizresearch.org

relief) to the families would be the message given at the end. The stories of Ramayana, Maha

Bharatha laced with insurance concepts, social and educative themes on agriculture and

family planning also play a pivotal role in creating awareness programs. At the end of the film

the publicity officer would call up a boy from the audience and promise him a surprise gift if

he can narrate the story. The advantage of this gimmick is multi fold. The adult audience pays

immediate attention to see if their boy is clever enough to narrate and win the prize. The

message gets careful repetition. These types of programs are conducted under the supervision

of the Village Pramukh to boost up the ego and he is asked to address the audience”.

LIC has perfected certain techniques in order to educate as well as advertise its products in

rural areas. One such technique is ‘Cheque presentation’ in the villages, especially when there

occurs a death claim in rural areas. This type of meetings are used by the LIC officials to

invite the ‘Village Head’, the members of the village panchayat and other dignitaries to the

dais and everybody would grieve the death of the life assured. After presenting the claim

cheque to the claimant, the company officials would explain the benefits of insurance.

Some private players like Tata AIG Life, ICICI Life insurance and Aegon Religare Life

insurance companies print the leaflets in regional languages and distribute them in rural areas

through the network of insurance advisors. Normally the name of the insurer is not printed on

the pamphlets. These are intended purely for educating the rural masses.

To increase the operational efficiency Bajaj Allianz Life Insurance Company developed a

robust IT department and generates claim intimation letters two months in advance. The

company has added the settlement area in to the Branch Service Index Meter (BSIM) to

ensure prompt settlement of maturity claims with in the due date. The company engaged an

outsourced organization for early death claim investigations to ensure fast settlement of death

claims. To avoid pitfalls and loopholes, the company devised an IT backed initiative of

generating policy specific claim forms with bar codes to be dispatched to the claimants. This

ensures curbing the unethical practice of not registering claims until receiving the

requirements at the branch levels for avoiding delays. The company has Claims Review

Committee for redressing the customer complaints.

Bajaj Allianz Life Insurance Company has a special unit linked plan called Family Gain,

the premiums of which are invested in funds that are approved by Shariyat principles. These

funds, in other words are not invested in companies dealing with gambling, liquor,

entertainment, contests, films, TVs, hotels, banks etc which are against the pious Muslim

tenets. This plan is positioned for pious Muslim sector who do not want to earn out of

gambling, racing, liquor business etc. Even though this plan is for both urban and rural India,

it can be sold in rural areas where ever there is good percentage of pious Muslim population.

(Source: New Family Gain pamphlet) taken from Bajaj Allianz Product Specs developed by

Product Development Department, Page No.12.

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

12

www.globalbizresearch.org

Max Vijay has an innovate product designed by Max New York Life for financial

inclusion of under privileged masses. Keeping in view the savings and protection needs of the

people, three premium payment options are provided with minimal premiums of Rs 1000/, Rs

1500 and Rs 2500 per year. Renewal premiums can be paid from Rs 10 to Rs 2500 per day

depending upon the availability of the disposable income. The policy does not lapse as long

as there is sufficient value in policy account. No medical report is also required.

Building brand image in rural areas (Secondary data):

“Bima Grams: LIC of India conceived and perfected a marketing tool of designating a

village a ‘Bima Gram’ in which at least 75% of the households have at least one LIC

policy. LIC offers Rs 25,000 for the wellbeing of the village normally in a special

meeting held in the presence of all villagers and village elders. At the village

entrance, an LIC hoarding is put indicating that it is a Bima Gram. The visual

appearance of the hoarding enhances the trust of the rural people in LIC. This

marketing technique is not being popularized by the private players.

“Madhur Grams: It is part of the micro insurance product, Jeevan Mathur launched by

LIC. In any village, if 75% of the households opt this policy, the village is designated

as Madhurgram.

“Bima Schools: Normally children and youth are the best ambassadors of any brand

or company. In order to educate this segment, LIC has come out with the concept of

Bima Schools. In this, the school is declared Bima School if 25 students of that

school take life insurance policies. An amount of Rs 2500 is given out to the school

also. By virtue of this concept, school management talk of insurance to children,

children in turn with parents and the circle goes on and enhances the brand image of

LIC. Again this technique is not popular with private players.

A critical analysis of the marketing initiatives of life insurance companies in generating

awareness:

Long (2007) studied the Chinese insurance market marketing skills from the aspect of

training and concluded marketing skills had greater impact on insurance sale. A critical

analysis of the marketing techniques used by life insurance companies for the promotion of

rural insurance indicate that the efforts only at the periphery level only. The so called Bima

Grams, Madhur Grams and Bima villages are just a fraction of the total size of rural

hinterland. No insurance company could able to penetrate six lakh plus villages. “The

awareness programs of LIC and other private insurance companies is limited to very few

villages in the country and cannot be treated as awareness generation programs” (Rao,

Nagaraja, 2011). The hoardings of LIC are seen at least in few villages but none of the private

players have their hoardings in villages. The hoardings of private players are only in metros

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

13

www.globalbizresearch.org

and towns. The selling value of ads in TVs and other electronic media, especially of the

intangible and abstract nature of life insurance is yet to be analyzed by the future researchers.

Suggestions for the life insurance companies for capturing the rural market:

The major reason for the low penetration of life insurance in rural areas is the lack of

interest of the insurance companies coupled with low levels on insurance awareness of the

rural people. It is true that the IRDA has prescribed that certain percentage of business in each

year must be rural business. But IRDA has no monitory mechanism to check whether the

rural policy statistics submitted by all insurance players is trust-worthy. For enhancing rural

coverage, the following suggestions may be looked upon by the insurance players:

Raising the insurance awareness levels:

Insurance companies can form a consortium and start educating the rural masses in a big

way. They can make use of mobile vans, common pamphlets and common ads just to promote

insurance awareness. In this way the expenses can be distributed among all the players for

their mutual advantage.

In majority of the villages, the practice of ‘weakly market’ is very much in vogue. Large

number of villagers invariably visit these markets on the appointed day, normally once in a

week. Insurance companies can certainly organize exhibitions where they can show video

films in regional language and distribute insurance literature. The purpose of this program is

to reach out to the customer, understand his requirements, reinforce interest levels towards the

insurance companies and try to reengineer the behavioral psychology of the customer for

accepting the idea of insurance.

Insurance companies can resort to CSR practices in rural areas and build up related

marketing strategies for the benefit of the companies and the customers at large.

The recruitment of agents may be on sound lines. It should be ensured that the agents should

have the expert knowledge of competitive products in order to convert the prospects in to

clients. Companies may also think of recruiting agents from the stream of village elders and

opinion makers.

Suggestions for generating awareness towards IRDA:

All insurance policy bonds of all companies can be printed with an exclusive page

specifying the regulatory mechanism, the IRDA. This can be done both in English and

regional language. It helps the customers in knowing the regulatory mechanism, thereby

reinforcing the safety aspects of their investments with private players.

IRDA, being a government body, can advertise about itself in all print and electronic media to

reinforce trust of the rural policyholders.

Suggestions for behavioral change of customers’ for positive orientation towards the private

players:

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

14

www.globalbizresearch.org

“The customers are the backbone for the survival of any life insurance company or for that

matter any customer centric organization. A satisfied customer is the ambassador for the

growth prospects of a company. Any sales push strategy can supplement the sales objectives

but cannot supplant the long term objective of building the edifice of a solid organization

which is founded on the trust of the customers. As long as the vital objective is achieved, the

sales cannot be viable and economical”, Rao, Nagaraja, 2011).

The private life insurance companies can gain the confidence of their customers in the

following ways.

The maturity and death claims are to be processed promptly. There should be relaxation of

rules in at least small sum assured cases in order to gain the confidence of rural customers.

The policy servicing which include plethora of policyholders’ needs should be prompt and

courteous.

Misselling should be viewed as an offence and cases of misspelling should be punished. In a

way, the companies must publicly demonstrate their sincerity and gain the confidence of the

customers.

6. Conclusion

From the discussion as above, we can conclude that there lies a gap between the realities

and the marketing techniques with regard to rural life insurance market. The life insurance

awareness levels are low and are not addressed properly. The products are not rural specific to

attract the attention of the customers. The rural initiatives are by and large have limited focus

and the private players attention in the rural market is less significant. There is a strong need

to develop this market for an inclusive growth.

References

Ahmed, A. (2013), Perception of life insurance policies in rural India, Kuwait Chapter of Arabian

Journal of Business and Management Review, 2(6),pp. 17-24.

Athma, P. and Kumar, J. R. (2007), An Explorative Study of Life Insurance Purchase Decision

Making: Influence of Product and Non-Product FactorsThe ICFAI Journal of Risk & Insurance, 4(4),

pp. 40-48

B S Bodla, B. S. and Verma, S. R. (2007), Life Insurance Policies in Rural Area: Understanding Buyer

Behavior, The ICFAI University Press.

Borah, Sarat(2013), A study on customer satisfaction towards private sector life insurance companies

with special reference to Kotak Mahindra and Aviva Life Insurance Company of Jorhat district, Indian

Journal of Commerce and Management Studies, 4(3), pp. 19-26.

Capgemini report- “World Insurance Report, 2008- Spotlight on Developing Markets: India and China”

page no 3.

Gizaw, K. D. and Pagidimarri, V. (2014), The mediation effect of customer satisfaction on service

quality - customer loyalty link in insurance sector of Ethiopia- a study, International Journal of

Marketing and Technology, 4(1), pp.184-199.

Gopinath, 2009, ‘Rural and Social Sector Insurance’, IRDA Journal, April, 2009, pp 17.

Kaur, P. and Negi, M. (2010), A Study of Customer Satisfaction with Life Insurance In Chandigarh

Tricity, Paradigm, 14(2), E1-E39.

Proceedings of the Third Middle East Conference on Global Business, Economics, Finance and Banking

(ME15Dubai October Conference), ISBN - 978-1-63102-286-9

16-18 October, 2015 Paper ID: DF545

15

www.globalbizresearch.org

Krishna Swamy, O.R & Ranganatham, M- “Methodology of research in Social Sciences”, page no 130.

LIC of India Website.

Long, Ke. (2007). The approach of sale management and training system of Chinese life insurance

company-based on the case study on Haier New York life insurance. Chengdu: Master’s Degree Theses

of Southwestern University of Finance and Economics.

Rajendhiran,N, Saiganesh and Asha, 2004, ‘Rural Marketing- a critical review’,

http://www.indianmba.com/Faculty_Column/FC658/fc658.html.

Rao, Nagaraja, 2011, ‘Study of Rural Insurance Market in India with special reference to Life

Insurance’, a doctoral thesis, JNTUH, 2011.

Rohrer, J. E., Thomas V., Westermann, J. and Faulwell, J. A. (1999), Mission Driven Marketing : A

rural example, Journal of Healthcare management, 44(2), pp. 103-116

Sharma. R (2010), Changing Scenario of life Insurance Marketing in India, ICFAI Marketing

Mastermind Monthly Magazine.

Shirodkar, S.M- “Marketing & Public Relations” published by Insurance Institute of India, pp. 11.

Thamodaran, V. and Ramesh, M. (2010), Effectiveness of information communication technology in

rural insurance, Business and Economic Horizons, 2(2), pp. 98-105.

Tsoukatos, E and Rand, G. K (2007), Cultural influences on service quality and customer satisfaction:

evidence from Greek insurance, Managing Service Quality, 17(4), pp. 467-485

Velayudhan, 2007, ‘Rural Marketing – targeting the urban consumer’, Response Books, pp. 19-38

Venugopal, 2008, ‘Bank Assurance in India- Problems and Potential’, Yogakshema, March, 2008, pp.

10-11.