awt international (thailand) limited - sydney water · awt international (thailand) limited - notes...

TRANSCRIPT

AWT International (Thailand) Limited - 30 June 2007

AWT INTERNATIONAL (THAILAND) LIMITED

Annual Financial Statements for the year ended 30 June 2007

Contents Income statement Statement of recognised income and expense Balance sheet Cash flow statement Notes to and forming part of the financial statements: Company information 1. Summary of significant accounting policies 2. Income and expense 3. Income tax expense 4. Cash and cash equivalents 5. Trade and other receivables 6. Current tax liabilities 7. Trade and other payables 8. Share capital 9. Reserves 10. Retained earnings 11. Total equity reconciliation 12. Notes to the cash flow statement 13. Commitments 14. Auditors’ remuneration 15. Related party disclosures 16. Financial instruments disclosure 17. Segment reporting 18. Contingencies Directors’ Declaration Independent Auditor’s Report

Start of audited Financial Statements

Note 2007 2006$ $

Revenue 2(a) 187,128 125,001

Expenses 2(b) (44,958) (26,510)

Profit before income tax 142,170 98,491

Income tax expense 3(a), (b) (34,926) (19,253)

Profit for the period 107,244 79,238

AWT INTERNATIONAL (THAILAND) LIMITED

INCOME STATEMENTfor the year ended 30 June 2007

Note 2007 2006$ $

Foreign operations:Exchange differences on translation of foreign operations 31,867 58,037

Net gain (loss) in translation reserve before and after tax 9(b) 31,867 58,037

Net income (expense) recognised directly in equity 31,867 58,037

Profit for the period 107,244 79,238

Total recognised income and expense for the period 11 139,111 137,275

AWT INTERNATIONAL (THAILAND) LIMITED

STATEMENT OF RECOGNISED INCOME AND EXPENSE

for the year ended 30 June 2007

Note 2007 2006$ $

CURRENT ASSETS

Cash and cash equivalents 4 644,985 503,033Trade and other receivables 5 63,895 43,689

TOTAL CURRENT ASSETS 708,880 546,722

TOTAL ASSETS 708,880 546,722

CURRENT LIABILITIES

Trade and other payables 7 37,752 24,346Current tax payable 6 20,272 10,631

TOTAL CURRENT LIABILITIES 58,024 34,977

TOTAL LIABILITIES 58,024 34,977

NET ASSETS 650,856 511,745

EQUITY

Share capital 8 162,656 162,656Reserves 9 12,899 (18,968)Retained earnings 10 475,301 368,057

TOTAL EQUITY 11 650,856 511,745

AWT INTERNATIONAL (THAILAND) LIMITED

BALANCE SHEET

as at 30 June 2007

Note 2007 2006$ $

CASH FLOWS FROM OPERATING ACTIVITIES

Cash receipts in the course of operations 169,486 112,503Cash payments in the course of operations (29,519) (21,242)

Cash generated from operations 139,967 91,261

Income tax paid (26,388) (17,887)

Net cash from operating activities 12 113,579 73,374

Net increase (decrease) in cash and cash equivalents 113,579 73,374

Cash and cash equivalents at beginning of period 503,033 372,334

Effect of exchange rate fluctuations on the balances of cash held inforeign currencies 28,373 57,325

CASH AND CASH EQUIVALENTS AT END OF PERIOD 4 644,985 503,033

AWT INTERNATIONAL (THAILAND) LIMITED

CASH FLOW STATEMENT

for the year ended 30 June 2007

AWT International (Thailand) Limited - 30 June 2007

AWT INTERNATIONAL (THAILAND) LIMITED

Annual Financial Statements for the year ended 30 June 2007

1

AWT International (Thailand) Limited - Notes 30 June 2007/Page 1

AWT International (Thailand) Limited

Notes to and forming part of the Financial Statements for the year ended 30 June 2007

COMPANY INFORMATION

AWT International (Thailand) Limited (“the Company”) was incorporated in Thailand on 10 May 2002. The address of the Company’s registered office in Thailand is 76/26 Soi Lang Suan, Ploenchit Road, Lumpini, Pratumwan, Bangkok. The Company is directly controlled by Australian Water Technologies Pty. Ltd. (“the Parent”), a company incorporated in Australia. The Company is not wholly owned by the Parent as 51% of the issued share capital is owned by a Thailand shareholder. (Refer Note 8). However, the Parent controls the financial and operating policy decisions affecting the Company. The ultimate Parent is Sydney Water Corporation, a statutory State-owned corporation that is subject to the State Owned Corporations Act 1989. This Act effectively requires Sydney Water Corporation and each of its subsidiaries to be subject to the financial reporting requirements of Part 3 of the Public Finance and Audit Act 1983 and the associated requirements of the Public Finance and Audit Regulation 2005. Accordingly, these requirements apply to the Company for financial reporting purposes in the NSW public sector and are in addition to any necessary financial reporting requirements in Thailand in Baht currency. The principal activity of the Company is to market the ultimate Parent’s expertise in water and water-related consulting services to customers in Thailand. In addition, the Company derives royalty revenue from a “Know-how” agreement with a Thailand water supply company. (Refer Note 1(d)). The Company’s financial report for the year ended 30 June 2007 was authorised for issue in accordance with a resolution of Directors on 10 September 2007.

The significant policies that have been adopted in the preparation of the financial report are as follows: 1. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (a) BASIS OF PREPARATION

The financial report is a general purpose financial report, which has been prepared in accordance with applicable Australian Accounting Standards (including Australian Interpretations) adopted by the Australian Accounting Standards Board (“AASB”), mandates issued by NSW Treasury and other mandatory and statutory reporting requirements including Part 3 of the Public Finance and Audit Act 1983 and the associated requirements of the Public Finance and Audit Regulation 2005. In preparing this financial report, the accounting policies described below are based on the requirements applicable to for-profit entities in these mandatory and statutory requirements. The financial report covers the financial performance of the Company for the reporting period 1 July 2006 to 30 June 2007 and its financial position as at 30 June 2007.

The financial report has been prepared in accordance with the historical cost convention. The financial report is presented in Australian dollars and all values are rounded to the nearest dollar ($).

The accounting policies set out below have been consistently applied to all periods presented in the financial report. Where relevant, comparative amounts have been restated to conform with the current reporting period’s presentation.

(b) STATEMENT OF COMPLIANCE

The financial report complies with all applicable Australian Accounting Standards, including those Standards that are Australian equivalents to International Financial Reporting Standards (“AEIFRS”). Compliance with AEIFRS also ensures that the financial report complies with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”).

2

AWT International (Thailand) Limited - Notes 30 June 2007/Page 2

(c) FOREIGN CURRENCY

• FUNCTIONAL CURRENCY AND PRESENTATION CURRENCY

The functional currency of the Company is Thailand Baht which is the currency used in Thailand. The presentation currency for preparing the financial report of the Company is Australian dollars.

• TRANSACTIONS

Transactions of the Company are undertaken in Thailand Baht currency. These are translated to Australian dollars for the purposes of this financial report. Monetary assets and liabilities at the reporting date are translated to Australian dollars at the foreign exchange rate ruling on that date. Foreign exchange differences arising on translation are recognised in the Income Statement. Net foreign exchange gains are classified as other income (refer Note 1(e)) and net foreign exchange losses are classified as expenses.

• TRANSLATION OF FINANCIAL STATEMENTS

The assets and liabilities of the Company are translated to Australian dollars at the foreign exchange rate ruling at the reporting date. Equity items are translated at historical rates. Revenues and expenses are translated at a weighted average exchange rate for the reporting period, which is considered to approximate the foreign exchange rates at the date of the transactions. Foreign exchange differences arising on retranslation are taken directly to a translation reserve, which is a separate component of equity.

(d) REVENUE

Revenue is income that arises in the course of ordinary activities. The Company derives revenue for providing water-related consulting services to customers in Thailand and also from royalty revenue.

In relation to services provided under a consulting contract, revenue is recognised by reference to the stage of completion, which is measured by reference to an assessment of costs incurred to date as a percentage of estimated total costs for each contract.

In relation to royalty revenue, this is derived from a “Know-how” agreement between the Company and a Thailand water supply company. Under this agreement, the Company has permitted its name and experience to be used by the particular Thailand water supply company in supplying water to a provincial water authority. The royalty revenue is based on 2.25% of the gross revenue arising from the sale of water by the Thailand water supply company to the provincial water authority. Royalty revenue is recognised on an accrual basis in line with the sale of water under the agreement.

(e) OTHER INCOME

Other income comprises gains arising from either the disposal of recognised assets and liabilities or the remeasurement of some items to fair value at the reporting date that are required to be taken to the Income Statement under the relevant applicable Australian Accounting Standards, such as foreign exchange gains on transactions.

(f) EXPENSES

Expenses are recognised in the Income Statement when incurred. Expenses include items that are incurred in the course of ordinary activities as well as various losses that arise from the remeasurement of some items at the reporting date that are required to be taken to the Income Statement under the relevant applicable Australian Accounting Standards. Examples of losses are those arising from foreign exchange losses on transactions and some asset impairment losses. Expenses are disclosed in this financial report by nature. (Refer Note 2(b)).

(g) TAXATION

The Company is subject to income tax in accordance with the tax jurisdiction that exists in Thailand. The Company applies the Balance Sheet method of tax-effect accounting to determine income tax expense and current and deferred tax assets and liabilities. Income tax expense on the operating result for the reporting period comprises both current and deferred tax. Income tax is recognised in the Income Statement except to the extent that it relates to items recognised directly in equity, in which case it is recognised directly in equity. Current tax is the expected tax payable or receivable on the taxable income for the reporting period, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax payable or receivable in respect of previous years.

3

AWT International (Thailand) Limited - Notes 30 June 2007/Page 3

Deferred tax represents future assessable or deductible amounts that arise due to temporary differences existing at the reporting date between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes (their tax bases). Deferred tax balances are not recognised for temporary differences that arise from the initial recognition of assets or liabilities that affect neither accounting profit or taxable profit. The carrying amount of deferred tax assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred tax asset to be utilised. Deferred tax assets and liabilities provided are based on the expected manner of realisation or settlement of the carrying amount of assets and liabilities, using tax rates (and tax laws) enacted or substantively enacted at the reporting date.

(h) CASH AND CASH EQUIVALENTS

Cash and cash equivalents in the Balance Sheet comprise positive cash balances and any short-term investments with a maturity period of three months or less. For the purposes of the Cash Flow Statement, cash and cash equivalents consists of the above Balance Sheet definition, net of any bank overdraft balance.

(i) TRADE AND OTHER RECEIVABLES

Trade and other receivables, which generally have settlement terms within 30 days, are recognised and carried at original invoice amount, less any impairment losses recognised by way of an allowance for doubtful debts that represents specific amounts considered to be either doubtful or uncollectible. Recognition at original invoice amount is adopted as this is not materially different to amortised cost, given the short-term nature of these receivables. The allowance for doubtful debts is recognised when collection of the full amount invoiced is considered to be no longer probable after due consideration of factors such as past recoverability experience and prevailing economic conditions. Known bad debts are written off against the allowance as and when identified.

(j) IMPAIRMENT OF ASSETS

At each reporting date, the carrying amounts of assets (other than deferred tax assets) are reviewed to determine whether there is an indication of impairment. If any such indication exists, a formal estimate of their recoverable amount is made. Where the carrying amount of an asset is greater than its recoverable amount, the asset is considered impaired. An impairment loss is recognised whenever the carrying amount of an asset exceeds its recoverable amount. Impairment losses are recognised as an expense in the Income Statement. Impairment losses in respect of receivables are determined in accordance with the accounting policy in Note 1(i)). Any reversals of impairment losses are also recognised in the Income Statement.

(k) TRADE AND OTHER PAYABLES

Trade and other payables are recognised in the Balance Sheet at cost, which is considered to approximate amortised cost due to their short-term nature. They are not discounted as the effect of discounting would not be material for these liabilities. Recognition of trade and other payables occurs when goods or services have been received and an obligation to make future payments arises. (Refer Note 7).

(l) DIVIDEND PAYABLE

A liability for dividend payable is recognised in the reporting period in which the dividend is declared. This is considered to be the period in which the dividend has been proposed and agreed with the Company’s Shareholders.

(m) ACCOUNTING STANDARDS AND INTERPRETATIONS ISSUED BUT NOT YET OPERATIVE

At the reporting date, a number of Australian Accounting Standards and Interpretations adopted by the AASB had been issued but are not yet operative and have not been early adopted by the Company. The following is a list of these Standards and Interpretations and a description of their possible impact on the financial report in the period of their initial application:

4

AWT International (Thailand) Limited - Notes 30 June 2007/Page 4

• AASB 7 “Financial Instruments: Disclosure” (issued August 2005)

This Standard will replace the disclosure requirements of financial instruments in AASB 132 “Financial Instruments: Disclosure and Presentation” and will replace AASB 130 “Disclosures in the Financial Statements of Banks and Similar Institutions”, the latter being not relevant to the Company. The initial application of this Standard will not impact on the financial results of the Company as it is concerned only with additional disclosures in relation to financial instruments and share capital. The Standard is operative for annual reporting periods beginning on or after 1 January 2007 (ie. 2007/08).

• AASB 2005-10 “Amendments to Australian Accounting Standards” (issued September 2005)

This Standard makes consequential amendments to AASB 132 “Financial Instruments: Disclosure and Presentation”, AASB 101 “Presentation of Financial Statements”, AASB 114 “Segment Reporting”, AASB 117 “Leases”, AASB 133 “Earnings per Share”, AASB 139 “Financial Instruments: Recognition and Measurement”, AASB 1 “First-time Adoption of Australian Equivalents to International Financial Reporting Standards”, AASB 4 “Insurance Contracts”, AASB 1023 “General Insurance Contracts” and AASB 1038 “Life Insurance Contracts”. The amendments arise from the issuance of AASB 7 “Financial Instruments: Disclosure” in August 2005 (see above). They deal with the deletion of disclosure requirements of financial instruments in AASB 132 and make consequential adjustments to disclosure requirements in the other Standards to cater for the new disclosure requirements in AASB 7. The initial application of this Standard will have no impact on the financial results of the Company as it relates only to disclosure. The Standard is operative for annual reporting periods beginning on or after 1 January 2007 (ie. 2007/08).

• AASB 1049 “Financial Reporting of General Government Sectors by Governments” (issued September 2006)

This Standard specifies requirements for financial reports of the General Government Sector of each government, which is not relevant to the Company. The initial application of this Standard will not impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 July 2008 (ie. 2008/09).

• Interpretation 10 “Interim Financial Reporting and Impairment” (issued September 2006)

This Interpretation prohibits the reversal of an impairment loss recognised in a previous interim period in respect of goodwill, an investment in an equity instrument or a financial asset carried at cost. The initial application of this Standard will not impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 November 2006 (ie. 2007/08).

• AASB 101 “Presentation of Financial Statements” (issued October 2006)

This Standard sets out overall requirements for the presentation of general purpose financial reports, guidelines for their structure and minimum requirements for their content. It replaces AASB 101 “Presentation of Financial Statements” issued July 2004 and amended in September 2005. The new Standard is more identical to the equivalent IASB Standard and much of the Australian specific requirements have been removed. The initial application of this Standard will not impact on the financial results of the Company or the presentational content of the financial report. The Standard is operative for annual reporting periods beginning on or after 1 January 2007 (ie. 2007/08).

• AASB 8 “Operating Segments” (issued February 2007)

This Standard replaces the presentation requirements of segment reporting in AASB 114 “Segment Reporting”, which is currently not relevant to the Company. The initial application of this Standard will have no impact on the financial results of the Company and is only concerned with disclosures for entities where segment reporting is relevant. The Standard is operative for annual reporting periods ending on or after 1 January 2009 (ie. 2009/10).

• AASB 2007-3 “Amendments to Australian Accounting Standards arising from AASB 8” (issued February 2007)

This Standard makes changes to AASB 5 “Non-current Assets Held for Sale and Discontinued Operations”, AASB 6 “Exploration for and Evaluation of Mineral Resources”, AASB 102 “Inventories”, AASB 107 “Cash Flow Statements”, AASB 119 “Employee Benefits”, AASB 127 “Consolidated and Separate Financial Statements”, AASB 134 “Interim Financial Reporting”, AASB 136 “Impairment of Assets”, AASB 1023 “General Insurance Contracts” and AASB 1038 “Life Insurance Contracts”. These changes are consequential changes due to the issuance of AASB 8 “Operating Segments” and include changes to references and to language compatible with AASB 8. The initial application of this Standard will have no impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 January 2009 (ie. 2009/10).

• Interpretation 11 “AASB 2 Share-based Payment – Group and Treasury Share Transactions” (issued February 2007)

This Interpretation addresses the classification of a share-based payment transaction (as equity or cash settled), in which equity instruments of the parent or another group entity are transferred, in the Financial Statements of the entity receiving the services. The initial application of this Interpretation will not impact on the financial results of the Company. The Interpretation is operative for annual reporting periods beginning on or after 1 March 2007 (ie. 2007/08).

5

AWT International (Thailand) Limited - Notes 30 June 2007/Page 5

• AASB 2007-1 “Amendments to Australian Accounting Standards arising from AASB Interpretation 11” (issued February 2007)

This Standard amends AASB 2 “Share-based Payments” to insert the transitional provisions of its equivalent IASB Standard, previously contained in AASB 1 “First-time Adoption of Australian Equivalents to International Financial Reporting Standards”. The initial application of this Standard will have no impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 March 2007 (ie. 2007/08).

• Interpretation 12 “Service Concession Arrangements” (issued February 2007)

This Interpretation addresses the accounting for service concession operators, but not grantors, for public-to-private service concession arrangements. It states that for arrangements falling within its scope, the infrastructure assets within the arrangements are not recognised as property, plant and equipment of the operator and that instead, the operator will recognise either a financial asset, an intangible asset or a combination of the two depending on the terms of the arrangement. The initial application of this Interpretation will not impact on the financial results of the Company. The Interpretation is operative for annual reporting periods beginning on or after 1 January 2008 (ie. 2008/09).

• AASB 2007-2 “Amendments to Australian Accounting Standards arising from AASB Interpretation 12” (issued February 2007)

This Standard makes amendments to AASB 1 “First-time Adoption of Australian Equivalents to International Financial Reporting Standards” to allow a first-time adopter an optional exemption from full retrospective application of Interpretation 12 and allows recognition from the start of the earliest period presented in the financial report if retrospective application is impracticable. Application of this requirement must be made at the same time as Interpretation 12 “Service Concession Arrangements”. The initial application of this Standard will have no impact on the financial results of the Company. This part of the Standard is operative for annual reporting periods beginning on or after 1 January 2008 (ie. 2008/09).

• Interpretation 4 “Determining whether an Arrangement contains a Lease” (issued February 2007)

This Interpretation specifies criteria for determining whether an arrangement is, or contains, a lease. The determination is based on an assessment of whether fulfilment of the arrangement is dependent on the use of a specific asset and whether the arrangement conveys a right to use the asset. This Interpretation replaces the existing Interpretation 4 (issued in June 2005) to specifically exclude from its scope public-to-private service concession arrangements within the scope of Interpretation 12 “Service Concession Arrangements”. The initial application of this Interpretation will have no impact on the financial results of the Company. The Interpretation is operative for annual reporting periods beginning on or after 1 January 2008 (ie. 2008/09).

• Interpretation 129 “Service Concession Arrangements: Disclosures” (issued February 2007)

This Interpretation requires specific disclosures about service concession arrangements entered into by an entity, whether as a grantor or as an operator. The required disclosures include significant terms of each individual arrangement that may affect the amount, timing and certainty of future cash flows. This Interpretation replaces Interpretation 129 “Disclosure – Service Concession Arrangements” issued in July 2004 but must only be applied at the same time as Interpretation 12 “Service Concession Arrangements”. The initial application of this Interpretation will not impact on the financial results of the Company. The Interpretation is operative for annual reporting periods beginning on or after 1 January 2008 (ie. 2008/09).

• AASB 2007-4 “Amendments to Australian Accounting Standards arising from ED 151 and Other Amendments” (issued April 2007)

This Standard makes amendments to numerous Standards as a result of the AASB’s decision that, in principle, all options that currently exist under IFRSs should be included in the AEIFRSs and additional Australian disclosures should be eliminated, other than those now considered particularly relevant in the Australian reporting environment. Accordingly, many of the options that were previously removed from AEIFRSs have been reinstated to make them in line with their equivalent IASB Standards. This Standard also makes numerous editorial amendments to a range of Standards to reflect changes made to the text of IFRSs by the IASB. These editorial amendments have no substantive impact on the requirements in the amended Standards. The initial application of this Standard will have no impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 July 2007 (ie. 2007/08).

• AASB 2007-5 “Amendments to Australian Accounting Standard – Inventories Held for Distribution by Not-for-Profit Entities [AASB 102]” (issued May 2007)

This Standard makes amendments to AASB 102 “Inventories” issued in July 2004 to require inventories held for distribution by not-for-profit entities to be measured at cost, adjusted when applicable for any loss of service potential. It replaces the previous requirement of recognising such inventories at the lower of cost and current replacement cost. The initial application of this Standard will have no impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 July 2007 (ie. 2007/08).

6

AWT International (Thailand) Limited - Notes 30 June 2007/Page 6

• AASB 123 “Borrowing Costs” (issued June 2007)

This Standard makes amendments to AASB 123 “Borrowing Costs” issued in July 2004 to require the capitalisation of all borrowing costs directly attributable to the acquisition, construction or production of a qualifying asset, which is an asset that necessarily takes a substantial period of time to get ready for its intended use. In the July 2004 version of AASB 123, entities had a choice to either expense or capitalise such costs. This choice is no longer available under the revised AASB 123 and only capitalisation of such costs is permitted. All other borrowing costs, however, are to continue to be expensed. The initial application of this Standard will have no impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 July 2009 (ie. 2009/10).

• AASB 2007-6 “Amendments to Australian Accounting Standards arising from AASB 123 [AASB 1, AASB 101, AASB 107, AASB 111, AASB 116 & AASB 138 and Interpretations 1 & 12]” (issued June 2007)

This Standard makes consequential amendments to AASB 1 “First-time Adoption of Australian Equivalents to International Financial Reporting Standards”, AASB 101 “Presentation of Financial Statements”, AASB 107 “Cash Flow Statements”, AASB 111 “Construction Contracts”, AASB 116 “Property, Plant and Equipment”, AASB 138 “Intangible Assets”, Interpretation 1 “Changes in Existing Decommissioning, Restoration and Similar Liabilities’ and Interpretation 12 “Service Concession Arrangements” as a result of the issue of the revised AASB 123 “Borrowing Costs” in June 2007 (see above). The amendments principally remove references to expensing borrowing costs on qualifying assets, as AASB 123 was revised to require such borrowing costs to be capitalised The initial application of this Standard will have no impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 January 2009 (ie. 2009/10).

• AASB 2007-7 “Amendments to Australian Accounting Standards [AASB 1, AASB 2, AASB 4, AASB 5, AASB 107 & AASB 128]” (issued June 2007)

This Standard makes consequential editorial amendments to AASB 1 “First-time Adoption of Australian Equivalents to International Financial Reporting Standards”, AASB 2 “Share-based Payment”, AASB 4 “Insurance Contracts”, AASB 5 “Non-current Assets Held for Sale and Discontinued Operations”, AASB 107 “Cash Flow Statements” and AASB 128 “Investments in Associates” as a result of the issue of the issuance of AASB 2007-4 “Amendments to Australian Accounting Standards arising from ED 151 and Other Amendments” in June 2007 (see above). The amendments are principally editorial in nature, while removing the encouragement in AASB 107 to adopt a particular format for the Cash Flow Statement and removing superseded Australian Implementation Guidance from AASB 4. The initial application of this Standard will have no impact on the financial results of the Company. The Standard is operative for annual reporting periods beginning on or after 1 July 2007 (ie. 2007/08).

7

AWT International (Thailand) Limited - Notes 30 June 2007/Page 7

___________________________________________________________________________________________________________ Note 2007 2006 $ $ ___________________________________________________________________________________________________________

2. INCOME AND EXPENSES

Profit before income tax expense has been arrived at after including the following income and expense items:

(a) REVENUE Revenue from rendering services 20,071 - Royalty revenue 167,057 125,001

________________________ Total revenue 187,128 125,001 ________________________ (b) EXPENSES Contractor service expenses 31,217 10,832 Administrative expenses 9,557 9,557 Legal expenses 374 3,565 Consultancy expenses - 2,556 Transport expenses 3,810 -

________________________ Total Expenses 44,958 26,510 ________________________ 3. INCOME TAX EXPENSE

Major components of income tax expense for the reporting period are as follows: (a) RECOGNISED IN THE INCOME STATEMENT Current tax expense Current year 34,926 19,253

________________________

(b) RECONCILIATION BETWEEN INCOME TAX EXPENSE AND PRE-TAX NET PROFIT Profit before tax 142,170 98,491 ________________________ Income tax expense calculated using the domestic company tax rate of 30% (2006: 30%) 42,651 29,547 Decrease in tax expense due to: Amount not recognised for tax purposes (7,725) (10,294) ________________________ Income tax expense on pre-tax net profit 34,926 19,253 ________________________

8

AWT International (Thailand) Limited - Notes 30 June 2007/Page 8

___________________________________________________________________________________________________________ Note 2007 2006 $ $ ___________________________________________________________________________________________________________ 4. CASH AND CASH EQUIVALENTS CURRENT Cash 644,985 503,033 ________________________

The weighted average interest rate for the financial year was Nil % (2006: Nil %) 5. TRADE AND OTHER RECEIVABLES CURRENT Trade receivables: Other parties 265,743 252,548 Less: Allowance for doubtful debts 265,743 252,548 ________________________ - -

________________________ Other receivables: Other debtors and accrued revenue:

Other parties 63,895 43,689 ________________________

63,895 43,689 Total trade and other receivables ________________________ 6. CURRENT TAX LIABILITIES The current tax liability of $20,272 (2006: $10,631) represents the remaining balance of income taxes payable in respect of current

and prior periods. 7. TRADE AND OTHER PAYABLES CURRENT Trade payables: Parent 15,274 - Other payables: Non trade payables and accrued expenses: Other parties 22,478 24,346 _______________________ Total trade and other payables 37,752 24,346 _______________________ SIGNIFICANT TERMS AND CONDITIONS Trade accounts payable are normally settled within 30 days.

9

AWT International (Thailand) Limited - Notes 30 June 2007/Page 9

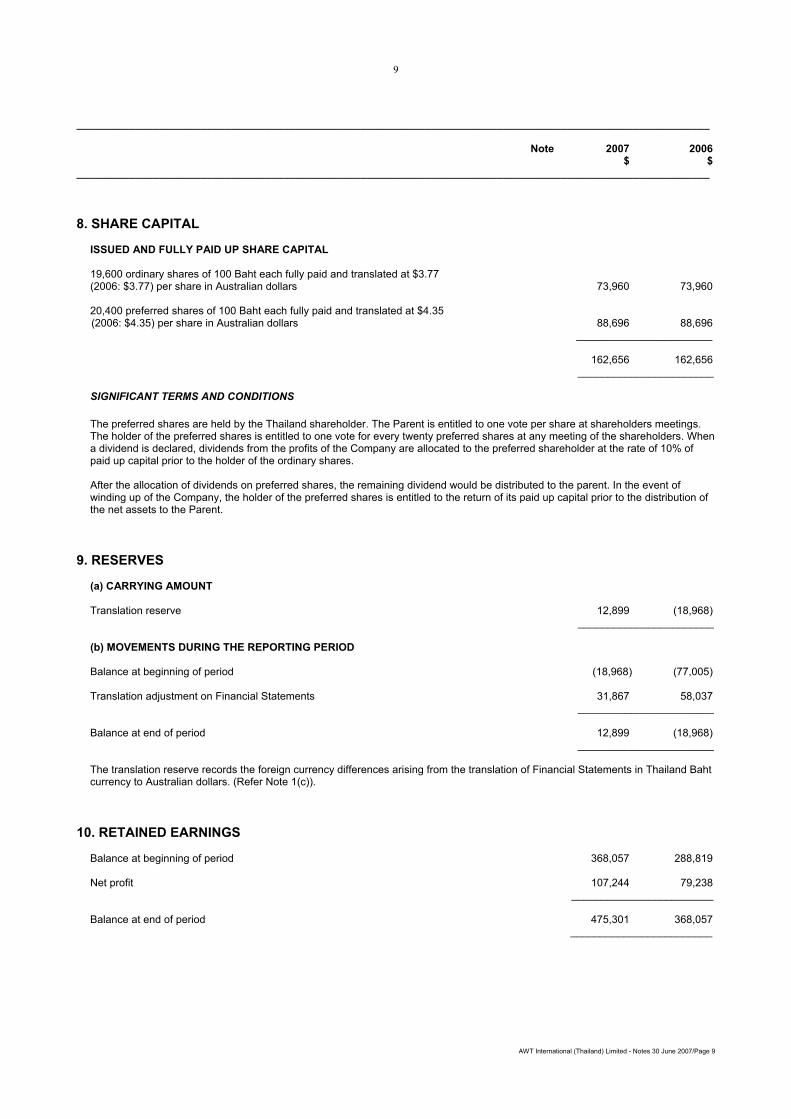

___________________________________________________________________________________________________________ Note 2007 2006 $ $ ___________________________________________________________________________________________________________ 8. SHARE CAPITAL ISSUED AND FULLY PAID UP SHARE CAPITAL 19,600 ordinary shares of 100 Baht each fully paid and translated at $3.77 (2006: $3.77) per share in Australian dollars 73,960 73,960 20,400 preferred shares of 100 Baht each fully paid and translated at $4.35 (2006: $4.35) per share in Australian dollars 88,696 88,696 _______________________ 162,656 162,656 _______________________ SIGNIFICANT TERMS AND CONDITIONS

The preferred shares are held by the Thailand shareholder. The Parent is entitled to one vote per share at shareholders meetings. The holder of the preferred shares is entitled to one vote for every twenty preferred shares at any meeting of the shareholders. When a dividend is declared, dividends from the profits of the Company are allocated to the preferred shareholder at the rate of 10% of paid up capital prior to the holder of the ordinary shares.

After the allocation of dividends on preferred shares, the remaining dividend would be distributed to the parent. In the event of winding up of the Company, the holder of the preferred shares is entitled to the return of its paid up capital prior to the distribution of the net assets to the Parent.

9. RESERVES (a) CARRYING AMOUNT Translation reserve 12,899 (18,968) _______________________ (b) MOVEMENTS DURING THE REPORTING PERIOD Balance at beginning of period (18,968) (77,005) Translation adjustment on Financial Statements 31,867 58,037 _______________________ Balance at end of period 12,899 (18,968) _______________________

The translation reserve records the foreign currency differences arising from the translation of Financial Statements in Thailand Baht currency to Australian dollars. (Refer Note 1(c)).

10. RETAINED EARNINGS Balance at beginning of period 368,057 288,819 Net profit 107,244 79,238

________________________ Balance at end of period 475,301 368,057

________________________

10

AWT International (Thailand) Limited - Notes 30 June 2007/Page 10

___________________________________________________________________________________________________________ Note 2007 2006 $ $ ___________________________________________________________________________________________________________ 11. TOTAL EQUITY RECONCILIATION Balance at beginning of period 511,745 374,470 Total recognised income and expense in the Statement of Recognised Income and Expense 139,111 137,275 ________________________ Balance at end of period 650,856 511,745 ________________________ 12. NOTES TO CASH FLOW STATEMENT RECONCILIATION OF PROFIT TO NET CASH FROM OPERATING ACTIVITIES Profit for the period 107,244 79,238 Adjustments for: Net movement in Balance Sheet items applicable to operating activities: Trade and other receivables (13,580) 1,075 Trade and other payables 11,966 8,309 Income tax assets and liabilities 7,949 (15,248) ________________________ Net cash from operating activities 113,579 73,374 ________________________ 13. COMMITMENTS The Company had no commitments as at the end of the current or previous reporting period. 14. AUDITORS' REMUNERATION Remuneration paid or payable by the Company for audit or review of the financial report 7,367 7,515 ________________________ No other services were provided by the auditors.

11

AWT International (Thailand) Limited - Notes 30 June 2007/Page 11

___________________________________________________________________________________________________________ Note 2007 2006 $ $ ___________________________________________________________________________________________________________ 15. RELATED PARTY DISCLOSURES

The Company has related party relationships with key management personnel (refer (a) below), their related entities (refer (b) below), its Parent (refer (c) below) and other related parties (refer (d) below).

(a) KEY MANAGEMENT PERSONNEL COMPENSATION Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the Company, directly or indirectly. This comprises all Directors, whether executive or non-executive, and senior executives who lead the business operations of the Company.

Key management personnel compensation paid by the Company is as follows: Short-term employee benefits 2,470 2,241 ____________________________ 2,470 2,241 ____________________________

This comprises compensation relating to a non-executive Thailand Director only. All other key management personnel received no compensation from the Company, nor did they receive compensation on behalf of the Company for services rendered to the Company from any other related entity. (b) OTHER TRANSACTIONS WITH KEY MANAGEMENT PERSONNEL AND RELATED ENTITIES Any transactions undertaken with entities related to key management personnel are conducted on an arm's length basis in the normal course of business and on commercial terms and conditions. During the current or previous reporting periods, there were no transactions with such entities. (c) TRANSACTIONS WITH PARENT

In the current reporting period, the Company transacted with its Parent to provide consulting services to customers in Thailand. In this regard, the Company incurred expenses of $17,969 with its Parent. It also had a payable balance with its Parent of $15,274 at the reporting date. (Refer also Note 7). The Company did not enter into any transactions with its Parent in the previous reporting period. (d) TRANSACTIONS WITH OTHER RELATED PARTIES

There were no transactions with other related parties in either the current or previous reporting period.

12

AWT International (Thailand) Limited - Notes 30 June 2007/Page 12

16. FINANCIAL INSTRUMENTS DISCLOSURE

Exposure to a range of risks arises in the normal course of business operations of the Company. These risks include foreign currency risk, interest rate risk, credit risk and liquidity risk. These risks are managed by the Company through policies, procedures and controls designed to assist in management of these risks for the Company.

(a) FOREIGN CURRENCY RISK The Company aims to minimise the exposure to foreign currency risk. Exposure to foreign currency risk arises from:

• translation differences between the functional currency and presentation currency; and • purchase or supply of goods and services.

The exposure to foreign currency is not considered to be material.

(b) INTEREST RATE RISK The Company does not have any interest-bearing financial instruments and accordingly it is not exposed to interest rate risks.

(c) CREDIT RISK Credit risk refers to the risk that indebted counterparties will default on their contractual obligations, resulting in financial loss to the Company. Exposures to credit risk exist in respect of financial assets such as trade and other receivables, cash and cash equivalents. In respect of trade and other receivables, the Company monitors balances outstanding on an ongoing basis and has policies in place for the recovery or write-off of amounts outstanding. In respect of cash and cash equivalents, the Company only deals with creditworthy counterparties and recognised financial intermediaries as a means of mitigating against the risk of financial losses from defaults. Policies are in place to monitor the credit ratings of counterparties and to limit the amount of funds placed with those counterparties, depending on their credit rating. At reporting date, there were no significant concentrations of credit risk in which the Company is significantly exposed to any single counterparty or group of counterparties having similar characteristics. The maximum exposure to credit risk is represented by the carrying amount of each financial asset in the Balance Sheet.

(d) LIQUIDITY RISK

Liquidity risk refers to the risk that the Company will be unable to meet expenditure commitments when they fall due. Liquidity risk is managed through the maintenance of extensive short-term and long-term cash flow forecasting.

(e) FAIR VALUES OF FINANCIAL ASSETS AND FINANCIAL LIABILITIES

Fair values of the Company’s financial assets and financial liabilities are determined as their carrying amounts as these are not readily traded on organised markets. Their carrying amounts are considered to be reasonable approximations of their fair value.

The carrying amounts of financial assets held by the Company at the reporting date are shown in Notes 4 and 5 and those for financial liabilities payable are shown in Note 7. These financial assets and liabilities are not readily traded on organised markets.

17. SEGMENT REPORTING

The Company operates in one business segment of water and water-related services and in the one geographical segment of Thailand.

18. CONTINGENCIES

To the best of their knowledge and belief, the Directors are not aware of any contingent liabilities or contingent assets existing at the reporting date (2006: Nil) and have no reason to believe that any possible legal or remedial action would result in a material cost, loss or economic benefit to the Company.

End of audited Financial Statements