axa: uk & ireland · 2 definitions unless specifically indicated, figures given do not include...

TRANSCRIPT

AXA: UK & Ireland

Investor day – 21 June 2007

1

Cautionary statements concerning forward-looking statements

Certain statements contained herein are forward-looking statements including, but not limited to, statements that are predictions of or indicate future events, trends, plans or objectives (including statements herein with respect to AXA's Ambition 2012 project and the objectives, financial and other, associated with that project, and to the integration of Winterthur).

Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties and can be affected by numerous factors that could cause actual results and AXA’s plans and objectives to differ materially from those expressed or implied in the forward looking statements (or from past results). These risks and uncertainties include, without limitation, the risk that the AXA and Winterthur businesses will not be integrated successfully, our inability to achieve anticipated synergies from the Winterthur acquisition, the risk of future catastrophic events (including possible future pandemic and/or weather-related catastrophic events and/or terrorist related incidents), economic and market developments, legislative developments, regulatory actions or investigations, as well as litigations and/or other proceedings.

Please refer to AXA’s Document de Référence for the year ended December 31, 2006 and Annual Report on Form 20-F for the year ended December 31, 2005, for a description of certain important factors, risks and uncertainties that may affect AXA’s business.

Given the inherently unpredictable and uncertain nature of these assumptions and factors, these estimates and projections should not be relied on as predictions of actual results, but should be viewed as estimates and projections based on assumptions which may or may not be correct or achieved. There can be no assurance that we will be able to meet our targets, including those with respect to AXA's Ambition 2012 project.

AXA undertakes no obligation to publicly update or revise any of these forward-looking statements, whether to reflect new information, future events or circumstances or otherwise.

2

Definitions

Unless specifically indicated, figures given do not include Winterthur which was acquired on 22 December 2006. Combined figures relating to AXA and Winterthur are unaudited.

Adjusted earnings, underlying earnings, Life & Saving EEV, Group EV and NBV are non-GAAP measures and as such are not audited, may not be comparable to similarly titled measures reported by other companies and should be read together with our GAAP measures. Management uses these non-GAAP measures as key indicators of performance in assessing AXA’s various businesses and believes that the presentation of these measures provides useful and important information to shareholders and investors as measures of AXA’s financial performance. For a reconciliation of underlying and adjusted earnings to net income see AXA press release dated February 22, 2007.

AXA Life & Savings EEV consists of the following elements: (i)Life & Savings Adjusted Net Assets Value (ANAV) which represents the tangible net assets. It is derived by aggregating the local regulatory (statutory) balance sheets of the life companies and reconcile with the Life & Savings IFRS shareholders’ equity (ii) Life & Savings Value of Inforce (VIF) which represents the discounted value of the local regulatory (statutory) profits projected over the entire future duration of existing liabilities.

Life & Savings New Business Value (NBV) is the value of the new business sold during the calendar year. The new business value includes both the initial cost (or strain) to sell new business and the future earnings and return of capital to the shareholder.

3

Today’s agenda

1 Strategic overview Nicolas MoreauGroup Chief Executive

6 Conclusion Nicolas MoreauGroup Chief Executive

2 Financial review Philippe MasoGroup Finance Director

3 Life manufacturing and advisory strategy

Paul EvansCEO, AXA Life

5 Business efficiency Philippe Maso Group Finance Director

4 Non-life manufacturing and distribution strategy

Peter HubbardCEO, AXA Insurance

4

Today’s agenda

1 Strategic overview Nicolas MoreauGroup Chief Executive

6 Conclusion Nicolas MoreauGroup Chief Executive

2 Financial review Philippe MasoGroup Finance Director

3 Life manufacturing and advisory strategy

Paul EvansCEO, AXA Life

5 Business efficiency Philippe Maso Group Finance Director

4 Non-life manufacturing and distribution strategy

Peter HubbardCEO, AXA Insurance

5

The UK insurance market is the third largest in the world and has further growth potential

Source: Swiss Re Sigma No 5/2006

Growing stable economy

Greying affluent population

Savings and protection gap

Changing customer demands

Worldwide Combined Insurance Premium Income ($bn)

517

376

200154

92 9059 49 39 35

0

100

200

300

400

500

600

US

Japa

n

UK

Fran

ce Italy

Ger

man

y

Sou

th K

orea

PR

Chi

na

Taiw

an

Can

ada

Growth drivers

6

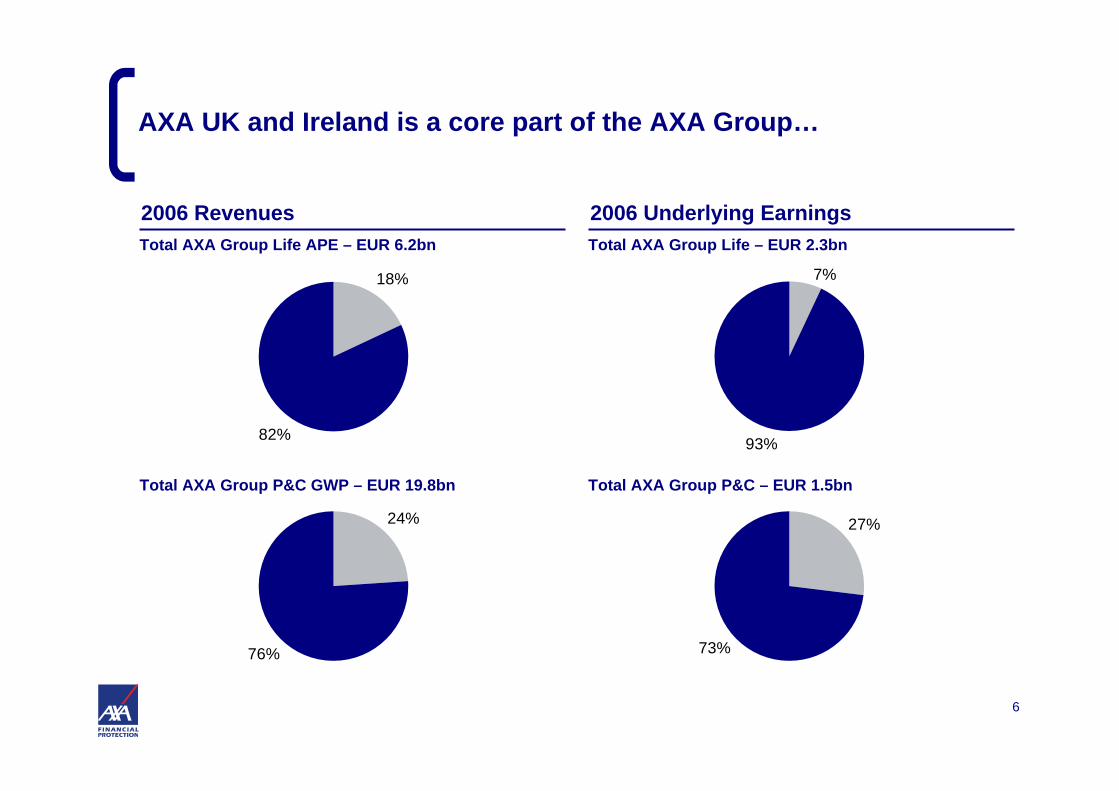

AXA UK and Ireland is a core part of the AXA Group…

2006 Revenues 2006 Underlying Earnings

18%

82%

7%

93%

24%

76%

27%

73%

Total AXA Group Life – EUR 2.3bn

Total AXA Group P&C – EUR 1.5bn

Total AXA Group Life APE – EUR 6.2bn

Total AXA Group P&C GWP – EUR 19.8bn

7

…with solid positions in different market segments

6th 3rd

The 2nd to 6th

ranking within £100m APE

spread

Life Non-life

UK P&C Healthcare Ireland

4th

2nd SME` 2nd

Large risks are written by AXA

Corporate Solutions outside of AXA UK

entity

8

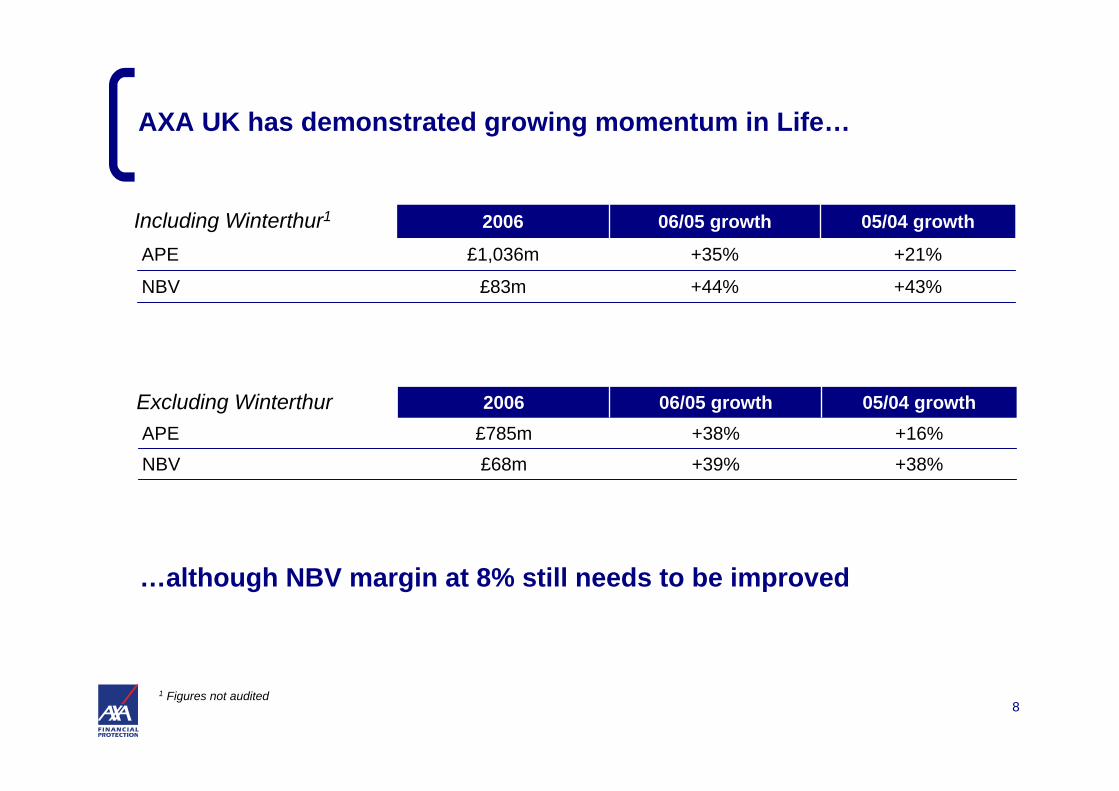

AXA UK has demonstrated growing momentum in Life…

+43%+44%£83mNBV

+21%+35%£1,036mAPE

05/04 growth06/05 growth2006

…although NBV margin at 8% still needs to be improved

+38%+39%£68mNBV+16%+38%£785mAPE

05/04 growth06/05 growth2006

Including Winterthur1

Excluding Winterthur

1 Figures not audited

9

AXA UK has also demonstrated growing momentum in Non-life…

-1.0 pts+0.2 pts96.5%Combined ratio

+1%1+7%£3,231mRevenues

05/04 growth06/05 growth2006

1 Excludes AXA direct business sold to RAC in 2004

…with a stable combined ratio

10

AXA UK 2012 Ambition

Strategic Objectives

Financial Targets 2006-2012

1. To improve Life profitability

• £250m NBV (18% average growth p.a.)

• Return on EEV c.12%

2. To profitably grow Non-life

• 5 to 10% average revenue growth p.a.

• Stable combined ratio in range of 96-98%

1. To become the preferred company for our customers and employees

2. To become the top three in all the business segments in which we operate

3. To play an increasing role in distribution

11

Our strategy is aligned with market drivers

1) Optimising distribution

2) Enriching customer and distribution proposition

3) Building an entrepreneurial organisation structure

4) Delivering an efficient operating model

AXA UK Strategic AgendaMarket Drivers

Fragmented distribution market

Pressure on manufacturer margins

Economic power is increasingly with those closer to the customer

Changing customer preferences

New business models emerging

12

• Acquire and develop distribution capabilities:

• Thinc Group

• Smart & Cook, Layton Blackham, Stuart Alexander

• AXA Sun Life Direct

• SME Direct

• Swiftcover (Internet distribution)

1) Optimised distribution

Actions Benefits• Bring AXA closer to the customer and ensure:

• client insight

• innovation

• access to distribution

• While capturing distribution margin

13

2) Enriched customer and distribution proposition

Actions Benefits• Invest in technology and services that support

distribution:

• Wrap

• online underwriting tools

• Launch new At Retirement products

• Design new investment solution

• Expand the product offer in Non-life

• Strengthen brand values

• Add value to the customer with:

• more sophisticated solutions

• more powerful brand

• Capitalise on segment with strong footprint

• While improving manufacturing margin and positioning

14

Care

Competence Reliability

Focus on brand values: positioning AXA as the ‘trusted market leader’

Trust

“Relevant expertise, offers and behaviours through understanding our customers”

“Consistently doing what we say we are going to

do, on time and well”

“Genuinely having the best interests of our customers at heart”

15

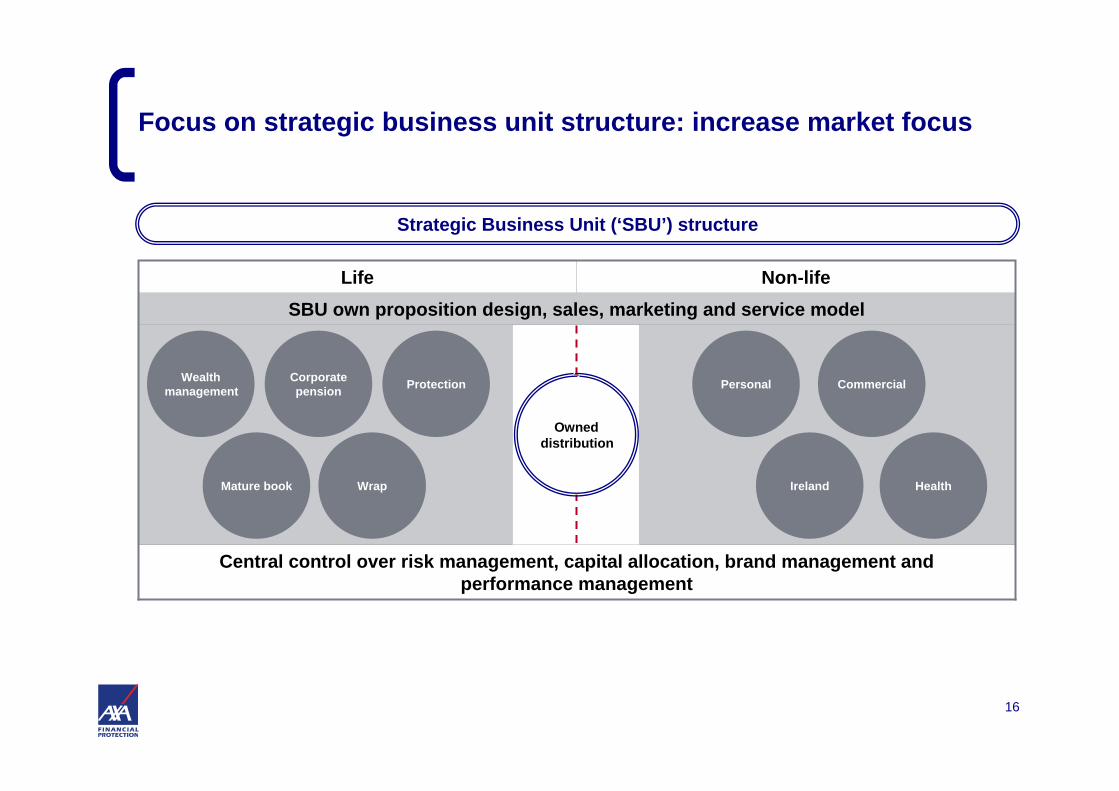

3) Entrepreneurial organisation structure

Actions Benefits• Deliver strategic business unit structure

• Embed cultural change programme

• Improve:

• entrepreneurial behaviours and agility

• market focus

• profit awareness

• While capturing economies of scale

16

Strategic Business Unit (‘SBU’) structure

Focus on strategic business unit structure: increase market focus

Central control over risk management, capital allocation, brand management and performance management

SBU own proposition design, sales, marketing and service modelNon-lifeLife

Wealth management

Corporate pension Protection

Mature book Wrap

Personal Commercial

Ireland Health

Owned distribution

17

Focus on cultural change programme: Creating a strong leadershipand customer-centric culture

To increase market focus and improve

employee engagement

Align remuneration structure with new

organisation

Transform the leadership behaviours

Improve employee advocacy

Intensive communication with

all employees

18

4) Efficient operating model

Actions• Build competitive cost structure

• Benefit from dedicated management team for closed book

• Simplify IT architecture

• Deliver best in class claims management

• Optimise capital efficiency and investment return

Benefits• Increased profitability while improving:

• quality of service

• operational efficiency

19

AXA UK has built the foundation to achieve its targets organically

• We believe that AXA UK can deliver its strategy without any major acquisitions

• We favour:

• widening our distribution reach, including bancassurance partnerships

• widening our product range and expertise with ‘bolt on’ capability

20

Today’s agenda

1 Strategic overview Nicolas MoreauGroup Chief Executive

6 Conclusion Nicolas MoreauGroup Chief Executive

2 Financial review Philippe MasoGroup Finance Director

3 Life manufacturing and advisory strategy

Paul EvansCEO, AXA Life

5 Business efficiency Philippe Maso Group Finance Director

4 Non-life manufacturing and distribution strategy

Peter HubbardCEO, AXA Insurance

21

AXA 2006 UK Results1

• Non-life business well positioned with ROE of 17%

• Life business well positioned in terms of size and growth but key issue is profitability (8% NBV margin and 6% return on EEV)

• Owned distribution business is still in its infancy and will contribute positively to future earnings

1 Winterthur APE included for 2005 to show proportionate return

2004 2005 2006

Life P&C

AXA UK Underlying Earnings (£m)

CAGR +20%

+ 0.2%96.5%Group COR+6.1%£3.3bnLife EEV

+0.6pts18%Life NBV margin+ 44%1£83mLife NBV+ 16%£308mIFRS Earnings+ 7%£3,231mNon-life GWP

+35%1£1,036mLife APE% on 20052006

22

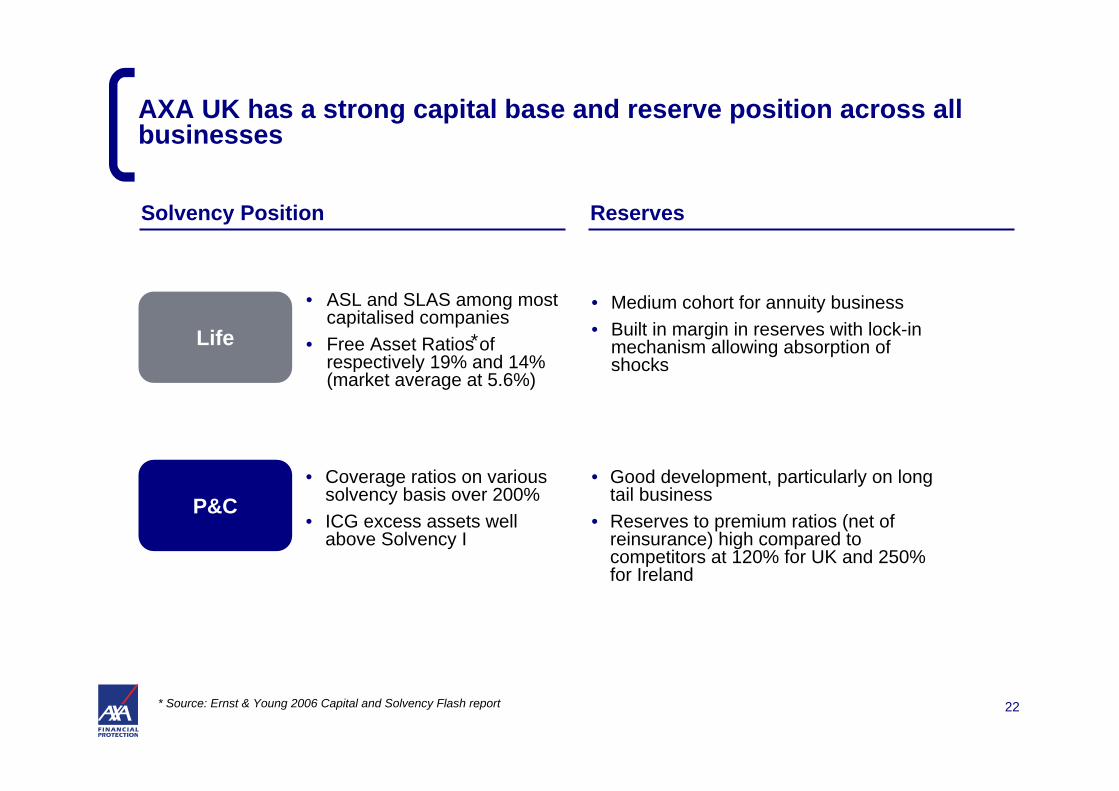

AXA UK has a strong capital base and reserve position across allbusinesses

• ASL and SLAS among most capitalised companies

• Free Asset Ratios of respectively 19% and 14% (market average at 5.6%)

• Coverage ratios on various solvency basis over 200%

• ICG excess assets well above Solvency I

• Good development, particularly on long tail business

• Reserves to premium ratios (net of reinsurance) high compared to competitors at 120% for UK and 250% for Ireland

• Medium cohort for annuity business• Built in margin in reserves with lock-in

mechanism allowing absorption of shocks

Solvency Position Reserves

Life

P&C

* Source: Ernst & Young 2006 Capital and Solvency Flash report

*

23

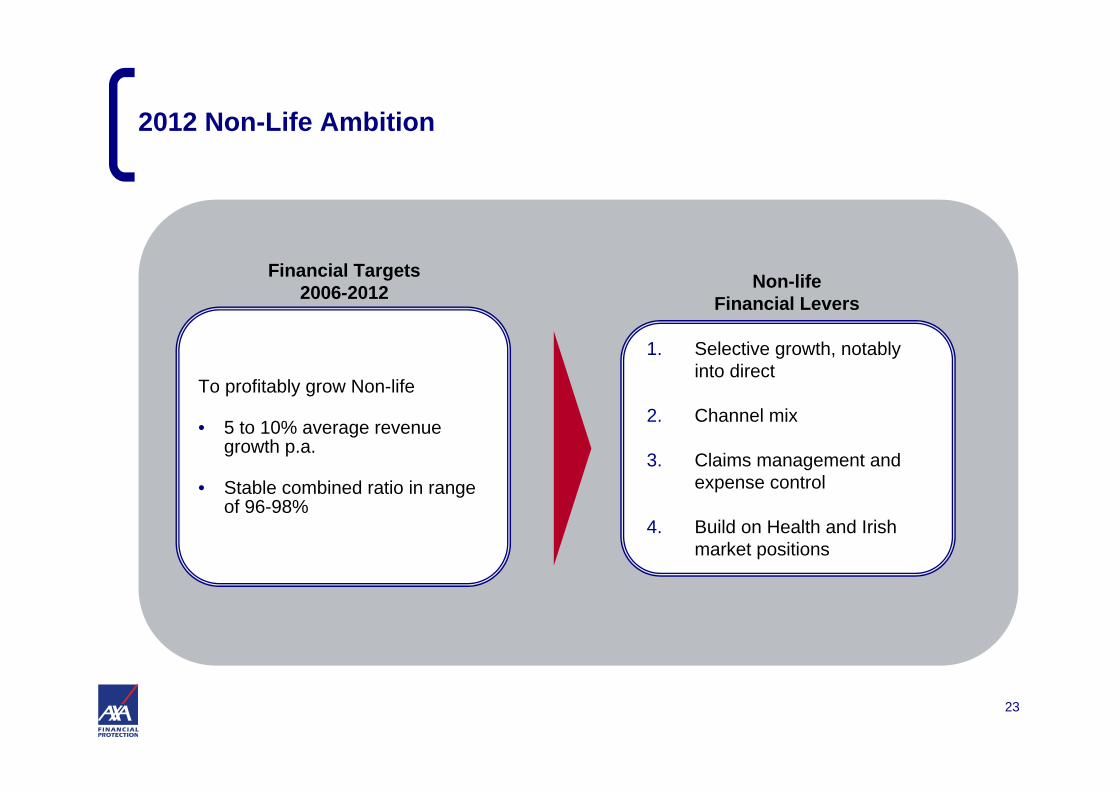

2012 Non-Life Ambition

Non-life Financial Levers

Financial Targets 2006-2012

To profitably grow Non-life

• 5 to 10% average revenue growth p.a.

• Stable combined ratio in range of 96-98%

1. Selective growth, notably into direct

2. Channel mix

3. Claims management and expense control

4. Build on Health and Irish market positions

24

96.5%96.3%

97.3%

95%96%97%98%99%

100%

2004 2005 2006

2,990 3,019

3,231

2004 2005 2006

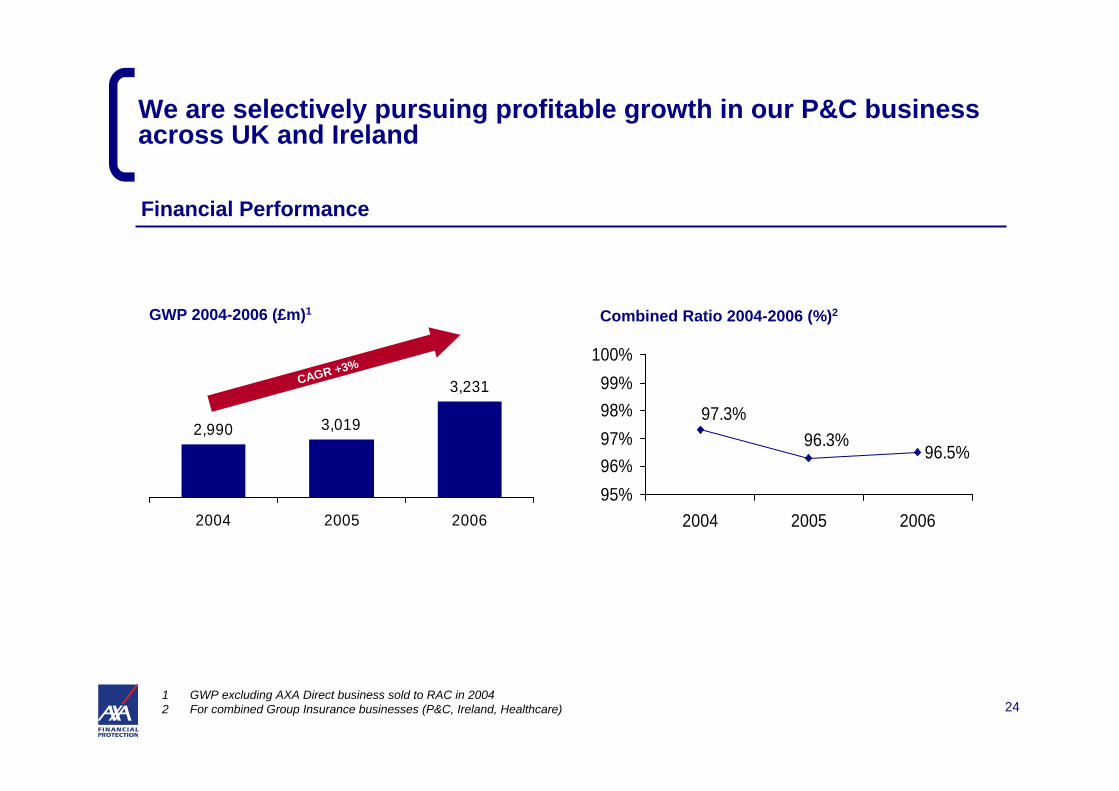

We are selectively pursuing profitable growth in our P&C business across UK and Ireland

Financial Performance

Combined Ratio 2004-2006 (%)2GWP 2004-2006 (£m)1

CAGR +3%

1 GWP excluding AXA Direct business sold to RAC in 20042 For combined Group Insurance businesses (P&C, Ireland, Healthcare)

25

0

100

200

300

400

500

600

700

2004 2005 2006 2012Target

GW

P (£

m)

AXA Intermediary Swiftcover

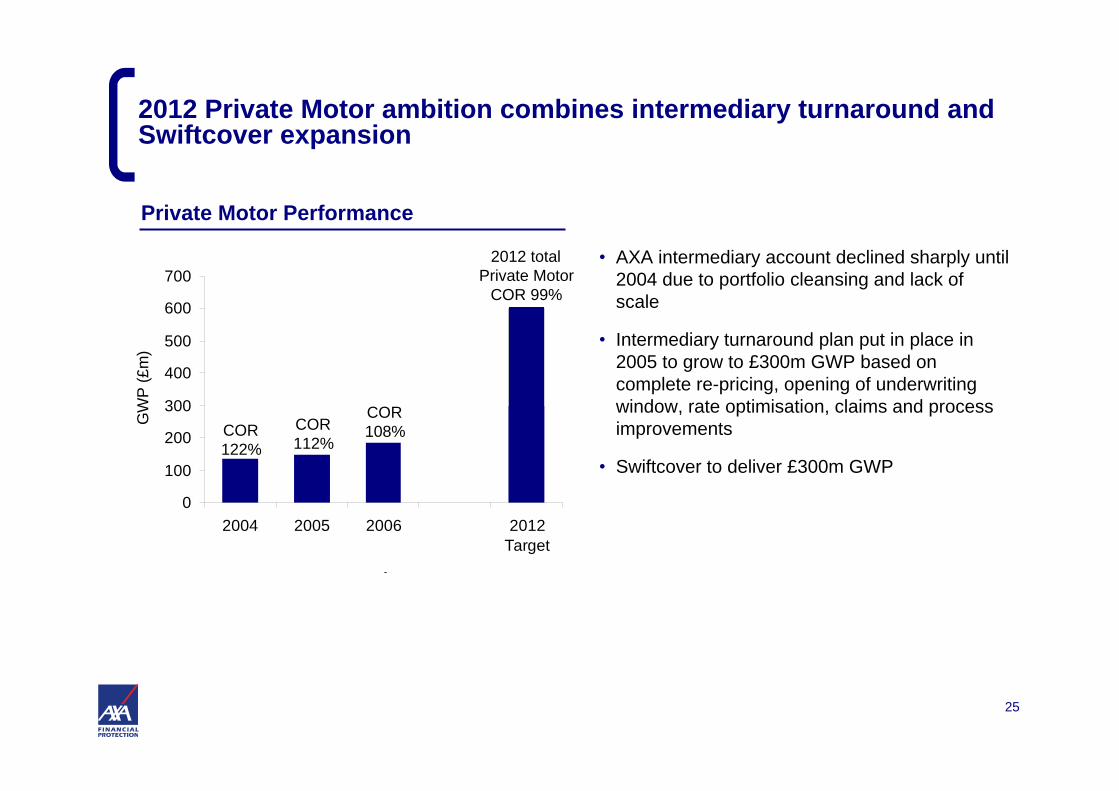

2012 Private Motor ambition combines intermediary turnaround andSwiftcover expansion

Private Motor Performance

• AXA intermediary account declined sharply until 2004 due to portfolio cleansing and lack of scale

• Intermediary turnaround plan put in place in 2005 to grow to £300m GWP based on complete re-pricing, opening of underwriting window, rate optimisation, claims and process improvements

• Swiftcover to deliver £300m GWP

COR122%

COR112%

COR108%

2012 total Private Motor

COR 99%

26

2012 Life Ambition

Life Financial Levers

To improve Life profitability

• £250m NBV (18% average growth p.a.), with a 12-15% NBV margin

• Return on EEV c.12%

1. Revenue growth

2. Product mix

3. Expense efficiency

4. Managing retention

5. Capital optimisation

Financial Targets 2006-2012

27

Life business has grown significantly over the past three years but NBV margin needs to be improved

1 Excluding Winterthur Growth 04-06 APE growth 20% and NBV 38%2 NBV margin excludes wholesale cash products in 2006

835841

2004 2005 2006

NBV (£m)CAGR +43% 1

AXA AXA Wholesale Cash products Winterthur

APE (£m)CAGR +27% 1 1,036

769638

2004 2005 2006

7% 9% 10%

4% 5% 6%NBV Margin2 (%)

2004 2005 2006

28

Moving beyond 12% NBV margin depends on our appetite for higher margin risk products

Financial levers to deliver core business improvement• Expense efficiency

• Selected growth in risk products

Increase appetite for risk participation

Mar

gin

5%

10%

15%

Current profitability Target

8%

15%

12%

Core business improvement

29

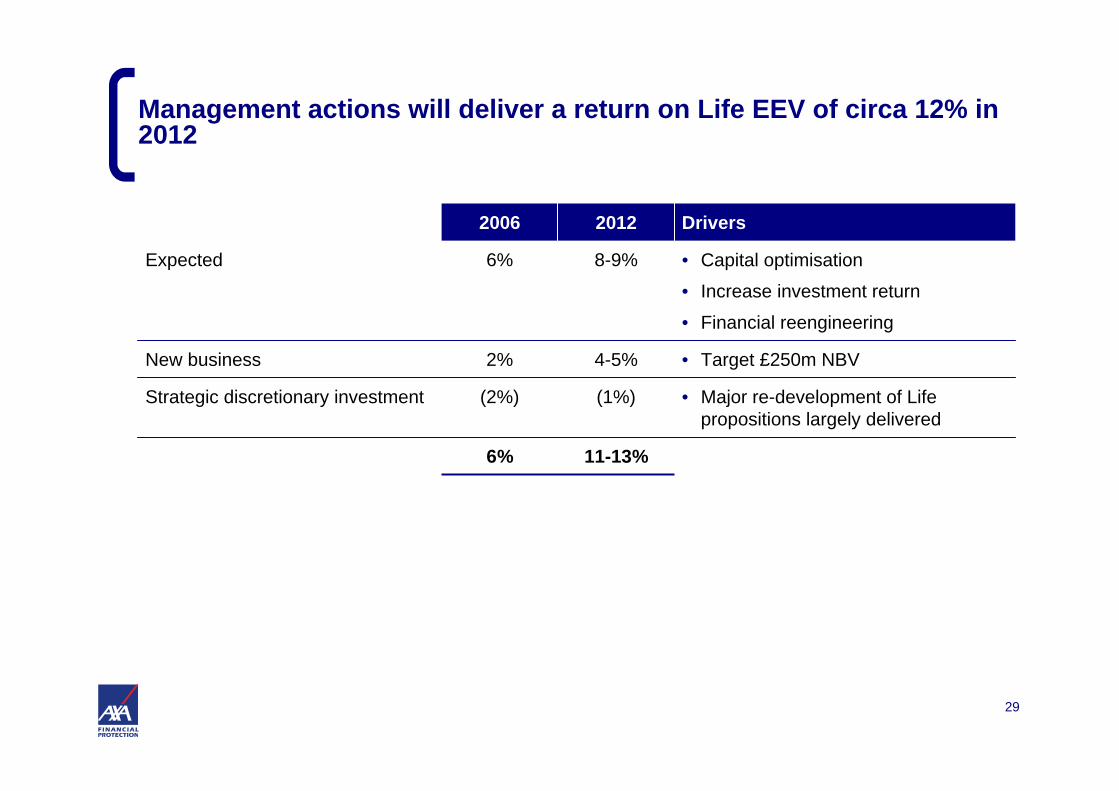

Management actions will deliver a return on Life EEV of circa 12% in 2012

11-13%6%

• Major re-development of Life propositions largely delivered

(1%)(2%)Strategic discretionary investment

• Target £250m NBV4-5%2%New business

• Capital optimisation

• Increase investment return

• Financial reengineering

8-9%6%Expected

Drivers20122006

30

Today’s agenda

1 Strategic overview Nicolas MoreauGroup Chief Executive

6 Conclusion Nicolas MoreauGroup Chief Executive

2 Financial review Philippe MasoGroup Finance Director

3 Life manufacturing and advisory strategy

Paul EvansCEO, AXA Life

5 Business efficiency Philippe Maso Group Finance Director

4 Non-life manufacturing and distribution strategy

Peter HubbardCEO, AXA Insurance

31

We have built a scale business with a strong platform for profitable growth

AXA and Winterthur New Business, 2004-61

Combined strength

CAGR 27%

• Scale business with 7.9% market share

• Top 3 Wealth Management business

• Winterthur accelerates our strategies

• Open architecture focus and investment-led reputation

• Distribution to HNW clients through fee based advisers

• 5* service

• Well positioned to win in the emerging Wrap market

0

200

400

600

800

1,000

1,200

2004 2005 2006

AP

E £

m

AXA Winterthur

1 Figures not audited

32

The Winterthur integration will accelerate our strategies, diversify our distribution and increase productivity

• Run the AXA and Winterthur wealth management businesses in parallel, each maintaining its own brand and distribution segmentation proposition

• Corporate Pension businesses combined into ‘Best of Breed’ proposition

• Legacy books combined and managed for value

Our focus is on extracting strategic benefits –cost synergies (15% annualised cost savings by 2009) are a secondary focus

Key Decisions Made

33

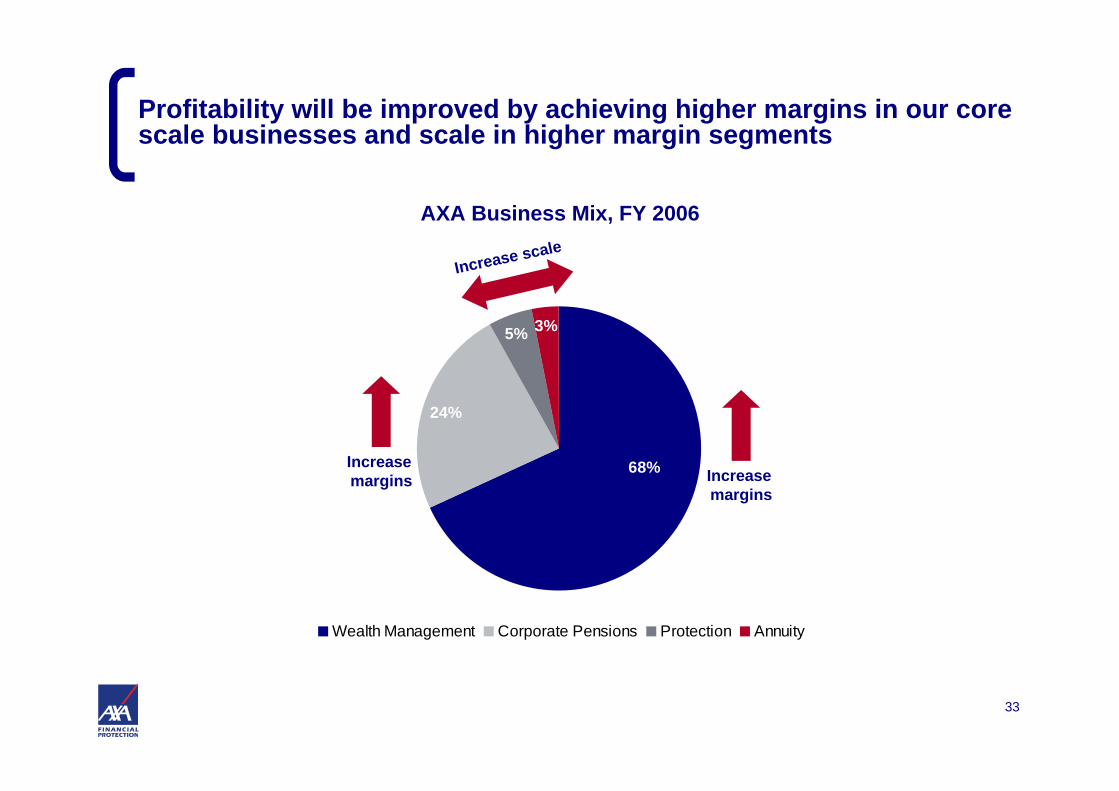

24%

5% 3%

68%

Wealth Management Corporate Pensions Protection Annuity

Profitability will be improved by achieving higher margins in our core scale businesses and scale in higher margin segments

AXA Business Mix, FY 2006

Increase scale

Increase margins Increase

margins

34

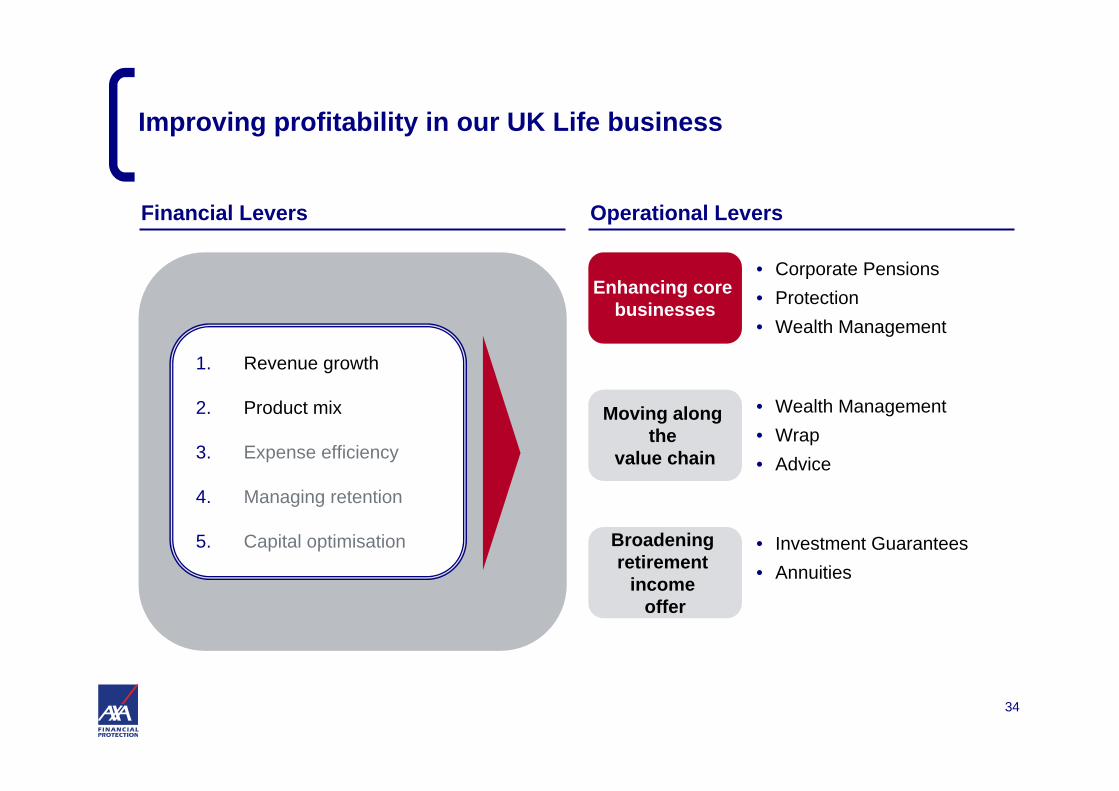

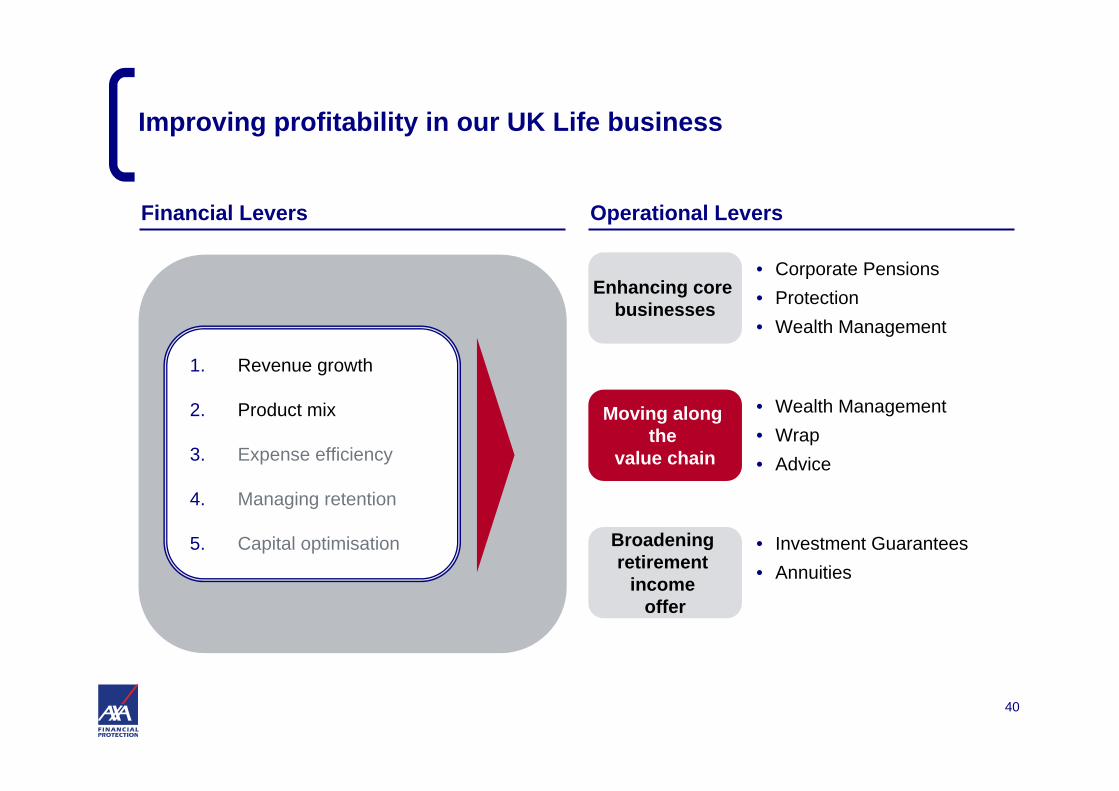

Improving profitability in our UK Life business

Financial Levers Operational Levers

Enhancing core businesses

Moving along the

value chain

Broadening retirement

income offer

• Corporate Pensions• Protection• Wealth Management

• Wealth Management• Wrap• Advice

• Investment Guarantees• Annuities

1. Revenue growth

2. Product mix

3. Expense efficiency

4. Managing retention

5. Capital optimisation

35

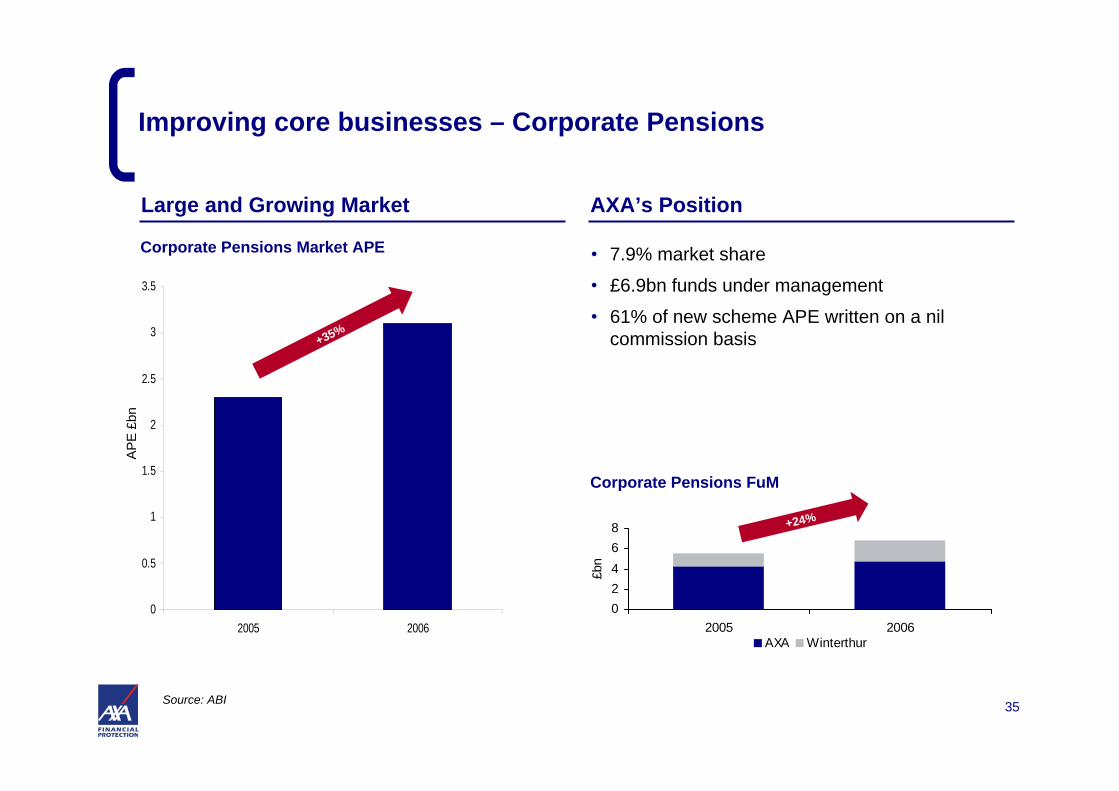

Improving core businesses – Corporate Pensions

Large and Growing Market AXA’s Position

Corporate Pensions Market APE • 7.9% market share

• £6.9bn funds under management

• 61% of new scheme APE written on a nil commission basis

Corporate Pensions FuM

02468

2005 2006

£bn

AXA Winterthur

+24%

Source: ABI

0

0.5

1

1.5

2

2.5

3

3.5

2005 2006

+35%

APE

£bn

36

• Deliver ‘Best of Breed’ Group Pension platform from integration with Winterthur

• Leverage refreshed individual SIPP platform to offer Group SIPP

• Target selected distributors – Employee Benefit Consultants, Corporate IFA

• Improve margins through:

• Rationalising legacy platforms (four to one)

• Risk management – pricing model based on scheme characteristics introduced in 2006

• Leveraging leading workplace marketing team

• Investing in self service administration

• Increasing proportion of nil commission/ trail commission business

Improving core businesses – Corporate Pensions

AXA’s Strategy

37

40%36%

0

200

400

600

800

1,000

1,200

2005 2006

AP

E £

000

Single tie Rest of market

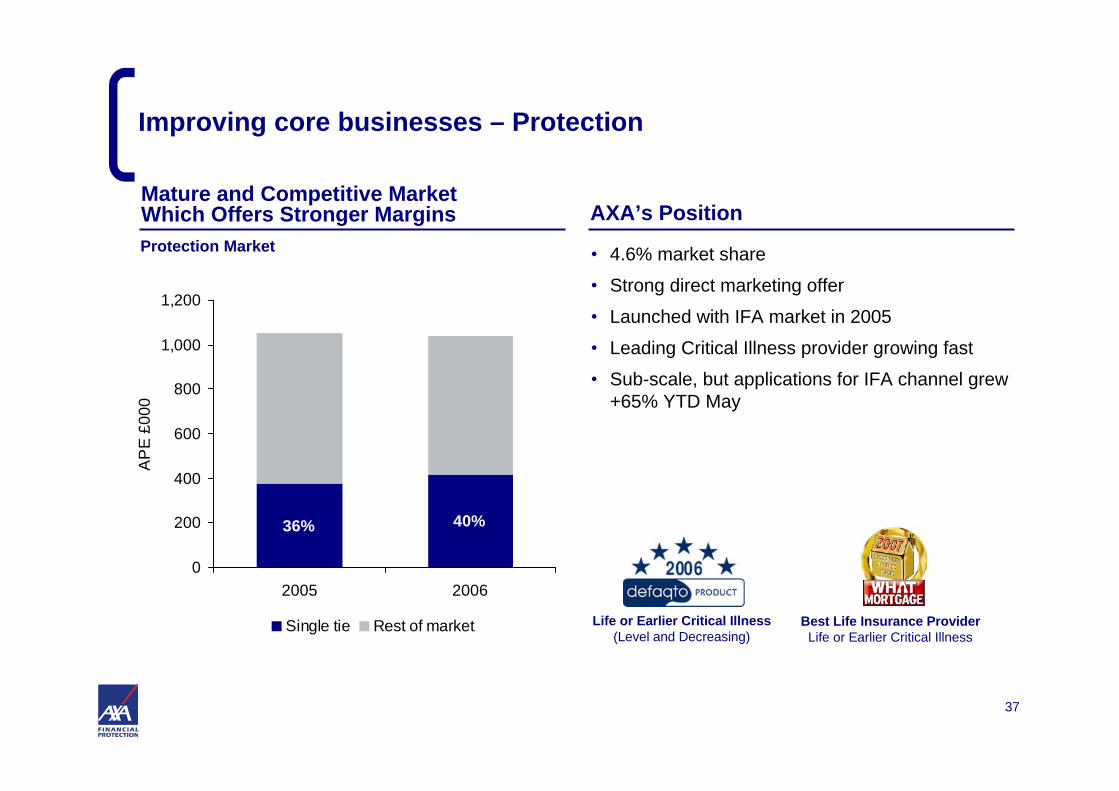

Improving core businesses – Protection

Mature and Competitive Market Which Offers Stronger Margins AXA’s Position

• 4.6% market share

• Strong direct marketing offer

• Launched with IFA market in 2005

• Leading Critical Illness provider growing fast

• Sub-scale, but applications for IFA channel grew +65% YTD May

Best Life Insurance ProviderLife or Earlier Critical Illness

Life or Earlier Critical Illness (Level and Decreasing)

Protection Market

38

Improving core businesses – Protection

AXA’s StrategyInnovate to improve adviser efficiency:

• Point of sale solutions: ‘Menu Product’

• Tele-underwriting

• Increasing investment in e-trading

Flexible underwriting approach:

• 80% of cases accepted at standard terms

• Only 1.6% of applications declined

• Piloting non-disclosure guarantees

Further develop strength in business assurance

39

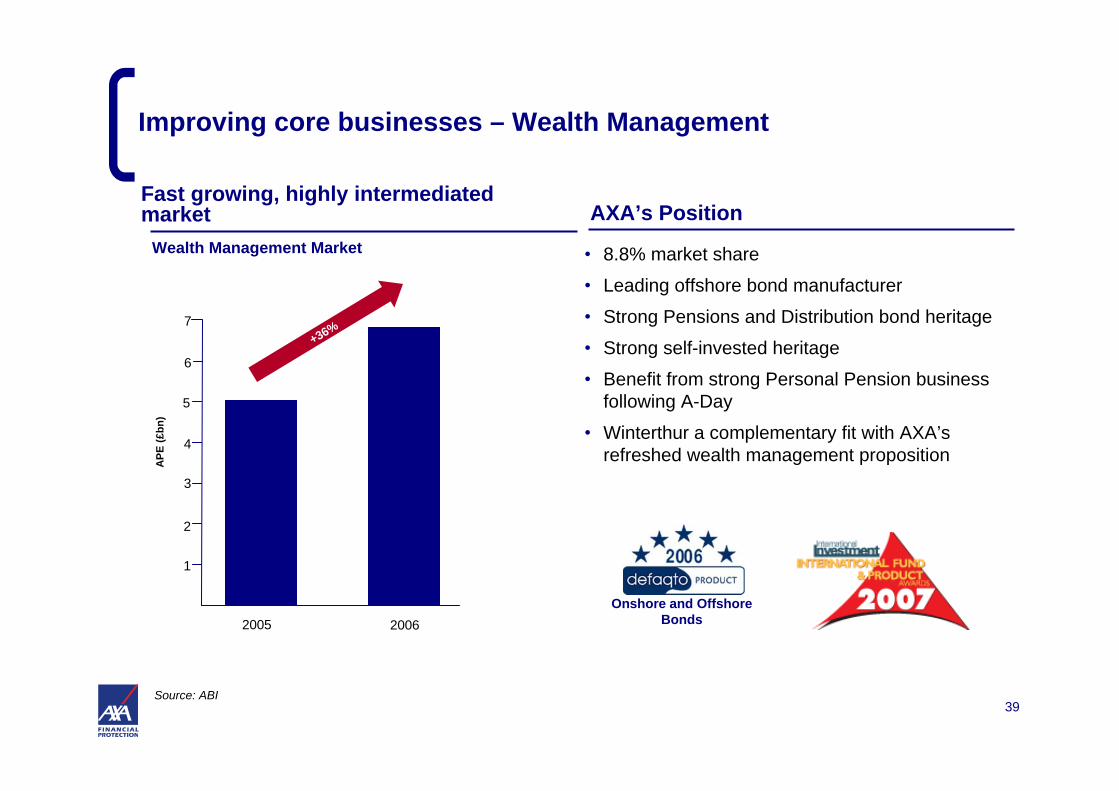

Improving core businesses – Wealth Management

Fast growing, highly intermediated market AXA’s Position

• 8.8% market share

• Leading offshore bond manufacturer

• Strong Pensions and Distribution bond heritage

• Strong self-invested heritage

• Benefit from strong Personal Pension business following A-Day

• Winterthur a complementary fit with AXA’s refreshed wealth management proposition

Wealth Management Market

Onshore and Offshore Bonds

Source: ABI

+36%

1

2

3

4

5

6

7

APE

(£bn

)

2005 2006

40

Improving profitability in our UK Life business

Operational Levers

Enhancing core businesses

Moving along the

value chain

Broadening retirement

income offer

• Corporate Pensions• Protection• Wealth Management

• Wealth Management• Wrap• Advice

• Investment Guarantees• Annuities

Financial Levers

1. Revenue growth

2. Product mix

3. Expense efficiency

4. Managing retention

5. Capital optimisation

41

Management of the end to end value chain is key to enhancing profitability in Wealth Management

Investment Management

Product Design andAdministration

Distribution Management

ServicesAdvice and SalesTraditional

Evolution

Actions

PlatformsRevolution

Build investment office proposition

Target the AXA and Winterthur brands at separate distributor

segments

Leverage our platform experience to launch a full Wrap

platform

Build a scale advisory business which harnesses

value through Wrap

Advice and SalesInvestment Management

Advice and SalesDistribution

Management Services

Product Design andAdministration

Investment Management

42

The Investment Office will underpin Wrap, Advice and Wealth Management businesses

Winterthur’s expertise is an accelerator of AXA’s guided open architecture strategy

c30

Investment Office

Fund supermarket

Scale

Distinct sales team

c5Investment analyst resource

Bespoke solutions for distributors

Multi-manager offering1

Open architecture expertise

Current position

BenefitsInnovative investment solutions

Improve margin

More attractive to fund management partners

Help distributors to manage the complexities of open architecture

Launch date Q1 08

1 Multi-manager – creation of a new fund through either blending existing retail funds or through new segregated mandates to fund managers

Build investment office proposition

43

£0

£50

£100

£150

£200

£250

£300

2006 2007 2008 2009 2010

Wra

pped

Ass

ets

(£bn

)

The wrap market is expected to develop rapidly

Forecast growth over the next three years reaching £250bn assets under management

AXA Wrap platform will give us the opportunity to:

Help IFAs transform their business models to become more efficient, customer focused and capture the value of their customer base

Be a significant player as IFAs move towards a new Wrap model

Respond to the growth of mutual funds market

Maximise value from ownership of distribution

Source: Datamonitor

Leverage our platform experience to launch a full Wrap

platform

44

Our combined SIPP and offshore platform experience provides a strong foundation for Wrap

Self investment experience Offshore platform experience

• Over 27 years experience in the self invested pensions arena

• Funds under management:

• AXA self invested plans - £3.0 billion

• Winterthur SIPP – £2.0 billion

• Refreshed AXA SIPP launched July 2006

• Launch of wide range of retirement options under SIPP, including income drawdown enhancements, planned for Q4 2007

• Market leading provider (26% market share)

• £4.6 billion funds under management (31 Dec 2006)

• Full open architecture (over 10,000 funds)

• Full e-commerce capability. Not just a product, but a platform

Awards

Leverage our platform experience to launch a full Wrap

platform

45

Building on this strong foundation will enable AXA UK to succeed in the emerging Wrap market

• Partnerships with leading technology providers

Leverage our platform experience to launch a full Wrap

platform

Open Architecture

Business Support Services

AXA’s building blocks Why we will succeed

Building on experience learned from AXA’s significant Australian wrap business

• Recognised business consultancy practice supporting IFA transformation

Technology

• Winterthur fee-based HNW advisors • Thinc partnership• AXA Offshore platform distributors

TechnologyThe right IFA relationships

• Leveraging Investment Office

46

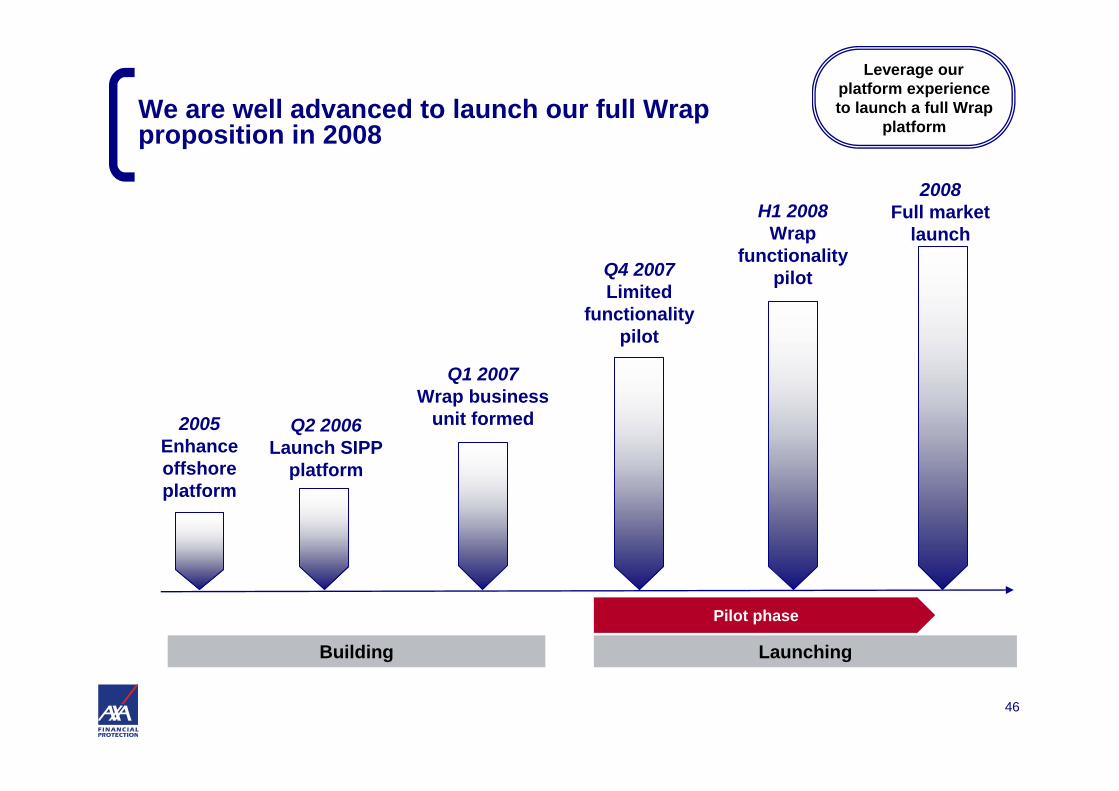

We are well advanced to launch our full Wrap proposition in 2008

Building

Pilot phase

Q2 2006Launch SIPP

platform

Q1 2007Wrap business

unit formed

Q4 2007Limited

functionality pilot

H1 2008Wrap

functionality pilot

2005Enhance offshore platform

2008 Full market

launch

Launching

Leverage our platform experience to launch a full Wrap

platform

47

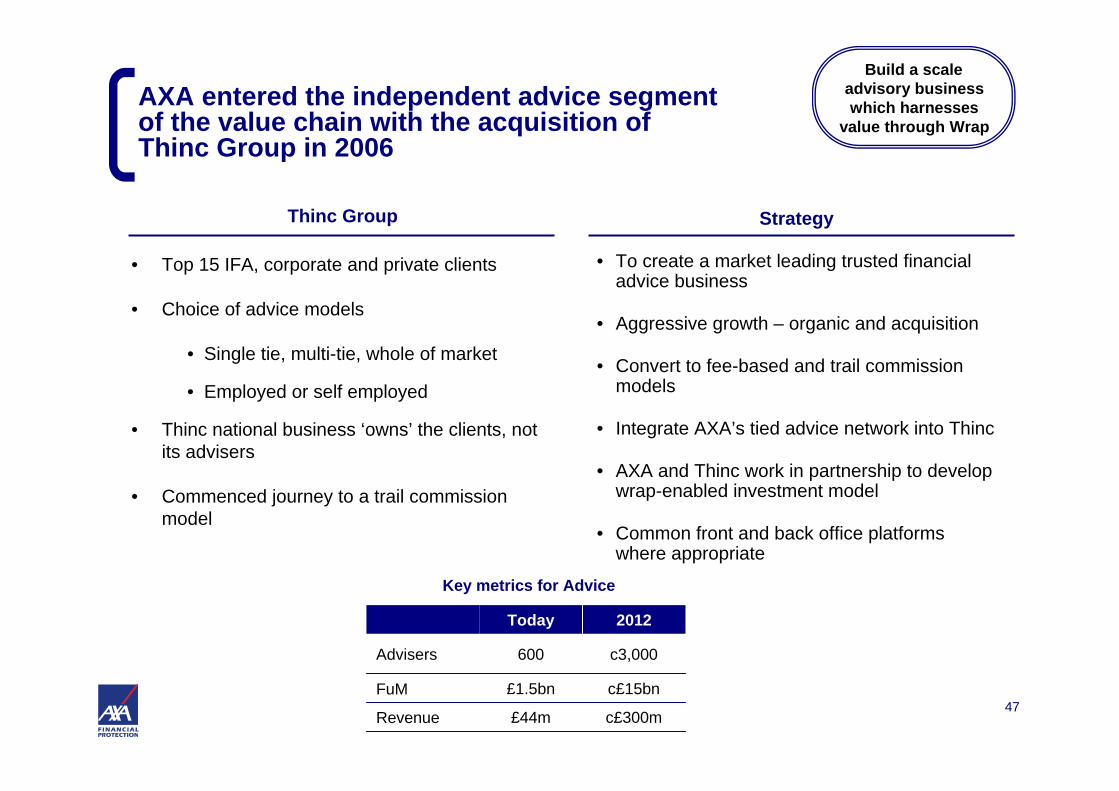

AXA entered the independent advice segment of the value chain with the acquisition of Thinc Group in 2006

Key metrics for Advice

Thinc Group

c£300m

c£15bn

c3,000

2012

£1.5bnFuM

£44mRevenue

600Advisers

Today

Build a scale advisory business which harnesses

value through Wrap

• Top 15 IFA, corporate and private clients

• Choice of advice models

• Single tie, multi-tie, whole of market

• Employed or self employed

• Thinc national business ‘owns’ the clients, not its advisers

• Commenced journey to a trail commission model

Strategy

• To create a market leading trusted financial advice business

• Aggressive growth – organic and acquisition

• Convert to fee-based and trail commission models

• Integrate AXA’s tied advice network into Thinc

• AXA and Thinc work in partnership to develop wrap-enabled investment model

• Common front and back office platforms where appropriate

48

Improving profitability in our UK Life business

Operational Levers

Enhancing core businesses

Moving along the

value chain

Broadening retirement

income offer

• Corporate Pensions• Protection• Wealth Management

• Wealth Management• Wrap• Advice

• Investment Guarantees• Annuities

Financial Levers

1. Revenue growth

2. Product mix

3. Expense efficiency

4. Managing retention

5. Capital optimisation

49

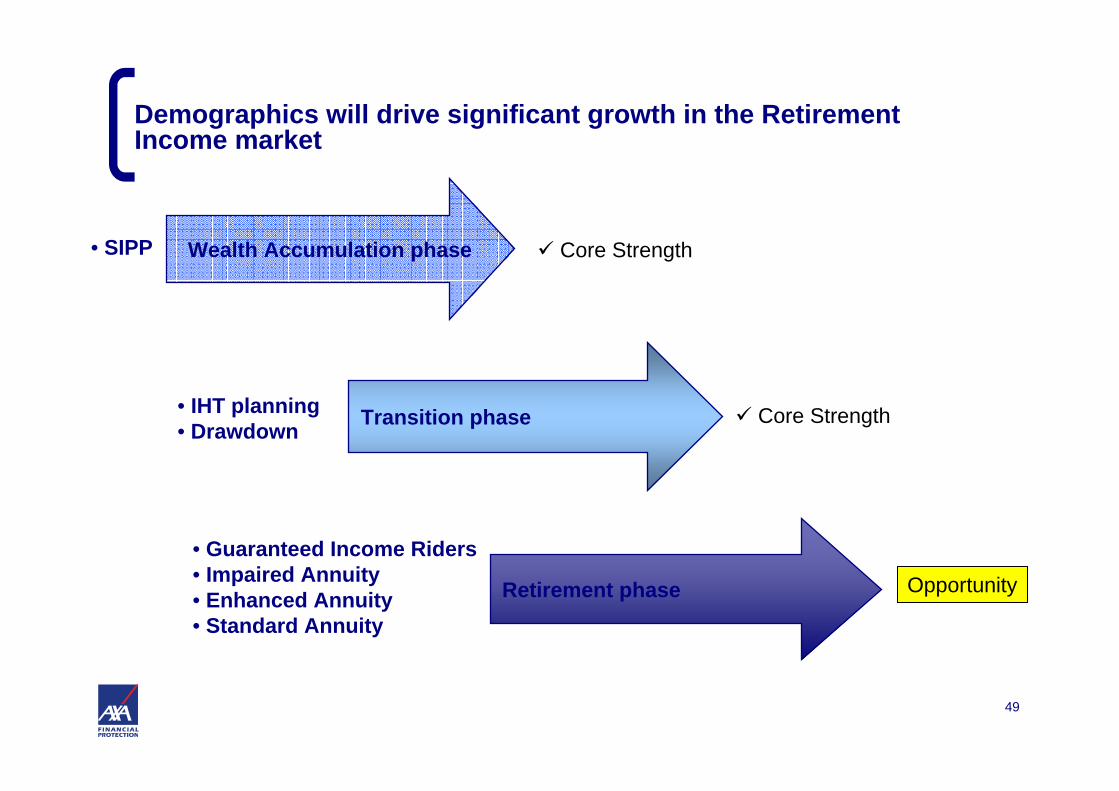

Demographics will drive significant growth in the Retirement Income market

Wealth Accumulation phase

Transition phase

Retirement phase

• SIPP Core Strength

• IHT planning• Drawdown

Core Strength

• Guaranteed Income Riders• Impaired Annuity• Enhanced Annuity• Standard Annuity

Opportunity

50

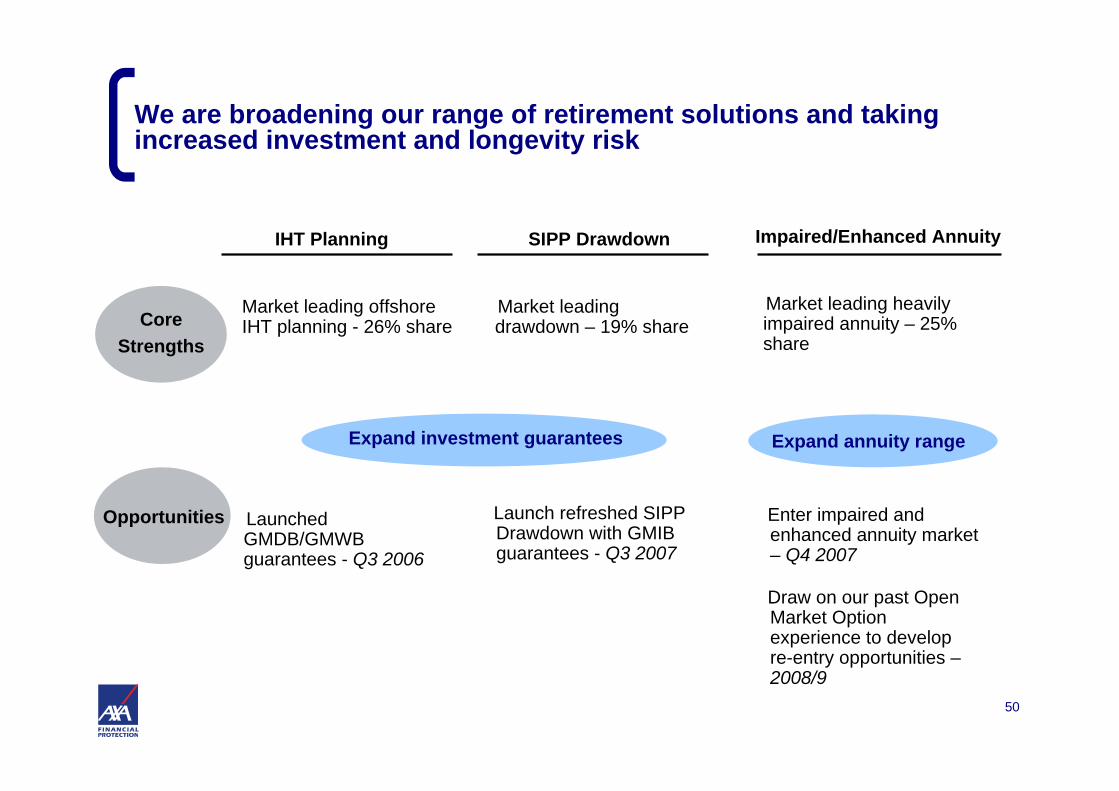

We are broadening our range of retirement solutions and taking increased investment and longevity risk

Market leading offshore IHT planning - 26% share

IHT Planning

Market leading drawdown – 19% share

SIPP Drawdown Impaired/Enhanced Annuity

Market leading heavily impaired annuity – 25% share

CoreStrengths

Launched GMDB/GMWB guarantees - Q3 2006

Launch refreshed SIPP Drawdown with GMIB guarantees - Q3 2007

Enter impaired and enhanced annuity market – Q4 2007

Draw on our past Open Market Option experience to develop re-entry opportunities –2008/9

Expand annuity rangeExpand investment guarantees

Opportunities

51

Today’s agenda

1 Strategic overview Nicolas MoreauGroup Chief Executive

6 Conclusion Nicolas MoreauGroup Chief Executive

2 Financial review Philippe MasoGroup Finance Director

3 Life manufacturing and advisory strategy

Paul EvansCEO, AXA Life

5 Business efficiency Philippe Maso Group Finance Director

4 Non-life manufacturing and distribution strategy

Peter HubbardCEO, AXA Insurance

52

To profitably grow our Non-life business

Financial levers Operational Levers

1. Selective growth (notably into Direct)

2. Channel mix

3. Claims management and expense control

4. Build on Health and Irish market positions

1. Re-entry into direct motor

2. Electronic Trading

3. Advice

4. Claims and Service

53

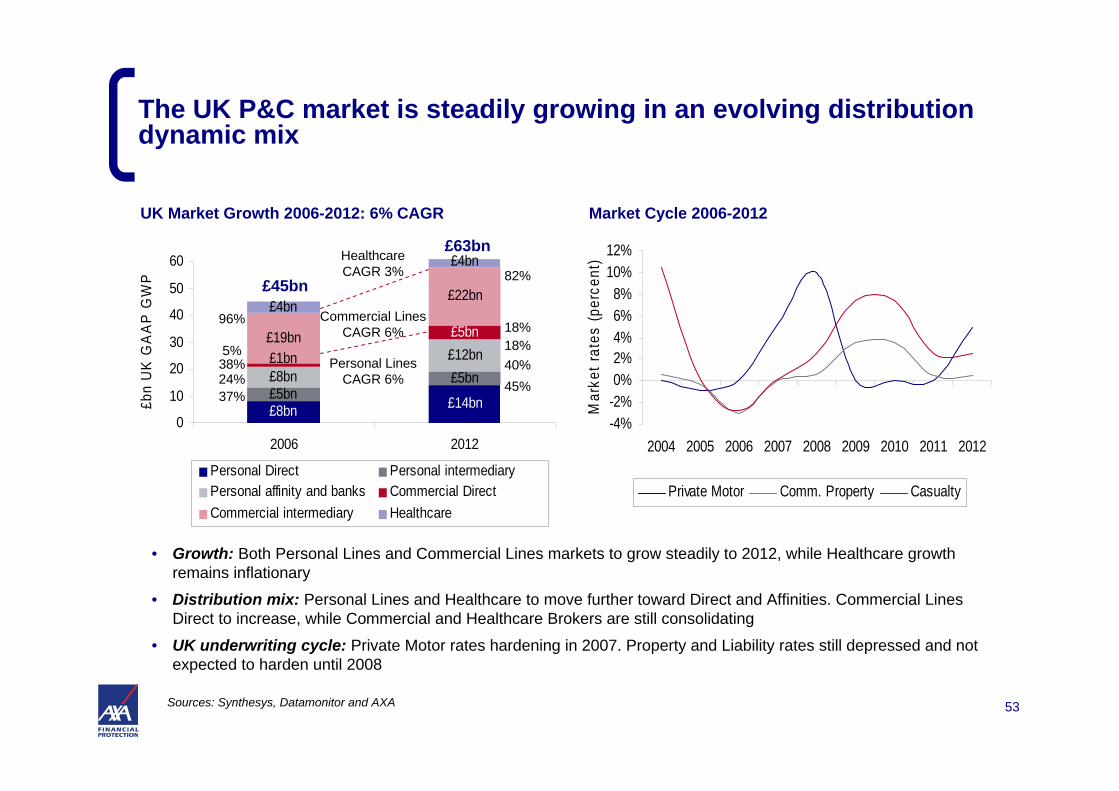

£8bn £14bn£5bn£5bn£8bn£12bn

£19bn

£22bn£4bn

£4bn

£5bn

£1bn

0

10

20

30

40

50

60

2006 2012

£bn

UK

GA

AP

GW

P

Personal Direct Personal intermediaryPersonal affinity and banks Commercial DirectCommercial intermediary Healthcare

The UK P&C market is steadily growing in an evolving distribution dynamic mix

Sources: Synthesys, Datamonitor and AXA

£45bn

£63bn

Personal Lines CAGR 6%

Commercial LinesCAGR 6%

Healthcare CAGR 3%

• Growth: Both Personal Lines and Commercial Lines markets to grow steadily to 2012, while Healthcare growth remains inflationary

• Distribution mix: Personal Lines and Healthcare to move further toward Direct and Affinities. Commercial Lines Direct to increase, while Commercial and Healthcare Brokers are still consolidating

• UK underwriting cycle: Private Motor rates hardening in 2007. Property and Liability rates still depressed and not expected to harden until 2008

UK Market Growth 2006-2012: 6% CAGR Market Cycle 2006-2012

96%

5%38%24%37%

82%

18%18%40%45%

-4%-2%0%2%4%6%8%

10%12%

2004 2005 2006 2007 2008 2009 2010 2011 2012

Mar

ket r

ates

(per

cent

)

Private Motor Comm. Property Casualty

54

AXA has built a leadership position in the UK SME Market, which is being enhanced through further investment in Direct capabilities

Intermediated business• ‘Best in class’ auto-rated capabilities, underwriting

expertise and relationship management

• Market leading efficiency based on e-trading technology and connectivity with brokers

• AXA brokers to be leveraged through back office synergies and unique customer insight

Direct business• Market leading SME direct proposition, selling online, by

telephone, through Corporate Partnerships and our field force

• Ambitious technology and marketing investment programme to deliver 20% p.a. growth

Sources: Synthesys, Datamonitor and AXA. SME Market assumed to be 50% of total Commercial Market

AXA 2006 Market Share 15% and ranking 2nd in Commercial SME Market

Commercial casualty£342m31%

Commercial motor£162m15%

Commercial property£598m54%

Commercial lines

55

AXA is 7th in the market for Personal Lines despite having no direct capability since 2004

• Corporate partners: Leadership position in particular across financial services, retail and travel industries

• Non Motor products: AXA well positioned on Household, Travel, Creditor and Pet

• Private Motor: Plan in place to grow intermediary Motor book while addressing profitability

• Process efficiency: Operating model predominantly based on full cycle electronic trading

• Swiftcover acquisition: Bridges gap to grow to leadership position

AXA 2006 Market Share 3.9% and Position 7th

Creditor and other

£253m28%

Private Motor£212m23%

Travel £155m17%

Household£299m33%

Sources: Synthesys, Datamonitor and AXA

Share 2.4%

Position 9th

Share 2.9%

Position 10th

Share 3.6%

Position 6th

Share 26.7%

Position 1st

Personal lines

56

Swiftcover enables greater control over end customer and accelerated growth

• A fast growing, profitable model:

• 100k policies in force in 2006, to grow to 300k in 2007 and up to 800k by 2012

• Delivering long term combined ratio below 100%

• A differentiated proposition:

• Innovative, online only customer proposition

• Low cost business model with flexible IT platform

• Expert management team (ex Churchill)

• A partnership that will deliver synergies:

• IT platform and expertise

• Claims and underwriting

• Product proposition and business development

AXA Personal Lines’ Motor Distribution

Source: AXA Insurance

Personal lines

0

100

200

300

400

500

600

700

2004 2005 2006 2007 2008 2009 2010 2011 2012

Intermediary Corporate Partner Direct

Swiftcover Growth to deliver 20% CAGR

2007-12

Intermediated Channel CAGR8.9% 2007-12

57

-10%

-5%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005 2006

AXA PPP AXA PPP and Denplan

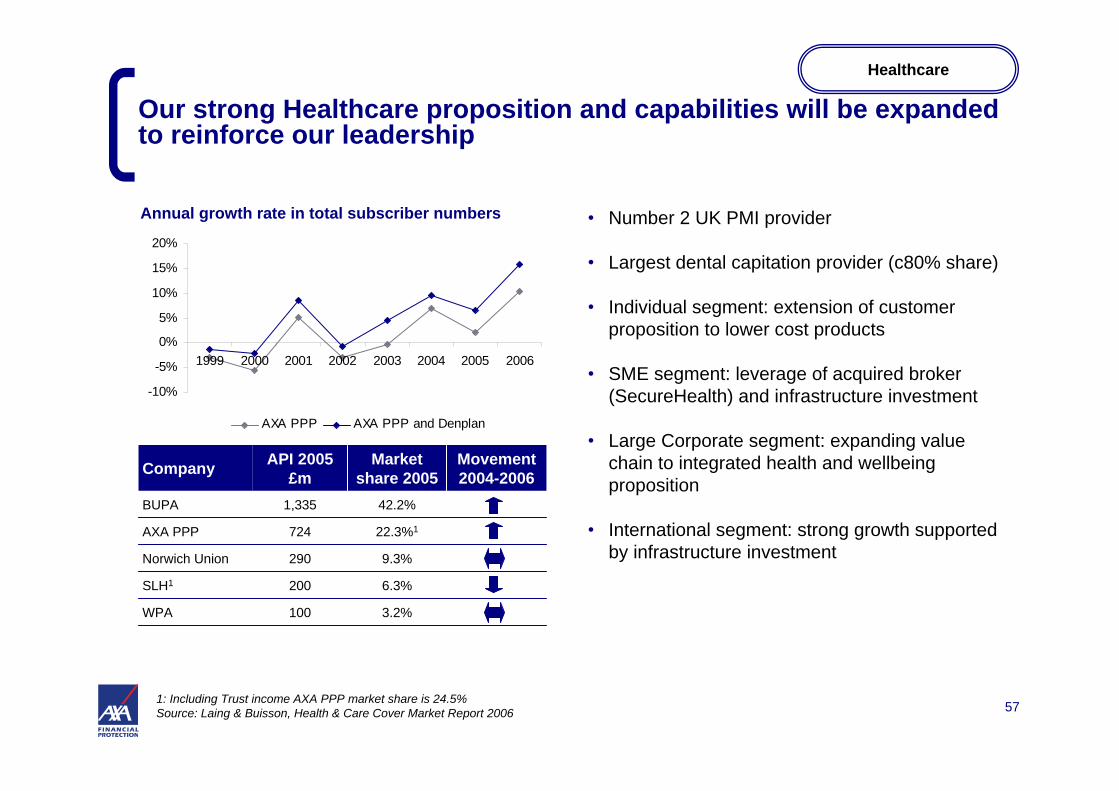

Our strong Healthcare proposition and capabilities will be expanded to reinforce our leadership

• Number 2 UK PMI provider

• Largest dental capitation provider (c80% share)

• Individual segment: extension of customer proposition to lower cost products

• SME segment: leverage of acquired broker (SecureHealth) and infrastructure investment

• Large Corporate segment: expanding value chain to integrated health and wellbeing proposition

• International segment: strong growth supported by infrastructure investment

Annual growth rate in total subscriber numbers

3.2%100WPA

6.3%200SLH1

Movement 2004-2006

9.3%

22.3%1

42.2%

Market share 2005

724AXA PPP

290Norwich Union

1,335BUPA

API 2005£mCompany

1: Including Trust income AXA PPP market share is 24.5%Source: Laing & Buisson, Health & Care Cover Market Report 2006

Healthcare

58

In a softening market, AXA Ireland has delivered continued strong performance

• Number three in Property and Casualty Market and Number two in Core Motor insurance market in Ireland

• Focus on pricing discipline and growing scale in direct business to offset decline in intermediated business

• Strong brand leveraged through extension of customer proposition – Commercial non-motor/ Creditor/ Other financial protection

• Expansion of distribution reach through further development of branch network, affinities and online proposition

Irish Motor Market GWP

0

200

400

600

800

1,000

1,200

1,400

2000 2001 2002 2003 2004 2005

£m G

WP

0

5

10

15

20

25

30

Percent

Total AXA Market share

Source: AXA

Ireland

59

Across our non life businesses we continue to invest in claims and service

• We are investing in enhancing the proposition

• Rehabilitation linking to AXA PPP

• Partnerships with third party providers

• Streamlining processes to reduce cycle times

• We are improving service proposition

• Improving core processes across the business

• Building on the excellent customer feedback scores in Ireland and AXA PPP

• Web enabling the value chain

• We are building a strong underlying foundation

• One platform for P&C across personal business across UK and Ireland

• One Web architecture

• One telephony platform

…Whilst indemnity savings and fraud benefits have continued to grow

60

• Background: Our acquired brokers control £400m of GWP and generate commission income of circa £80m from a comprehensive geographical footprint

• Acquisition platform: Our brokers give us an ideal platform for further broker consolidation

• Governance: Underwriting placement is independently managed but we will seek tactical single-tie opportunities

• Synergies: We will deliver operational synergies in back office processes, proposition development and customer insight

We are increasing our presence in Non life distribution

Stuart Alexander Offices

Layton Blackham Offices

Smart & Cook Offices

EdinburghGlasgow

Carlisle

Penrith

WelshpoolLudlow

Worcester

Bath

Bournemouth

Swindon

West Wickham

LondonChelmsford

Tonbridge

Norwich

Lincoln

Hull

Scarborough

Newcastle

Stockton-on-Tees

Harrogate

York

1716

31

15

28

29

32Northallerton

25 24

14

Grimsby2726Skipton

19

35Cleckheaton

Leeds18

23

Horwich21

12

13

6

5

22 Northampton

9 Milton Keynes

1 43430

11

8Farnham

10

33

32 Southampton

20

Coventry7

We have built the 2nd largest SME brokerage in the UK

61

Today’s agenda

1 Strategic overview Nicolas MoreauGroup Chief Executive

6 Conclusion Nicolas MoreauGroup Chief Executive

2 Financial review Philippe MasoGroup Finance Director

3 Life manufacturing and advisory strategy

Paul EvansCEO, AXA Life

5 Business efficiency Philippe Maso Group Finance Director

4 Non-life manufacturing and distribution strategy

Peter HubbardCEO, AXA Insurance

62

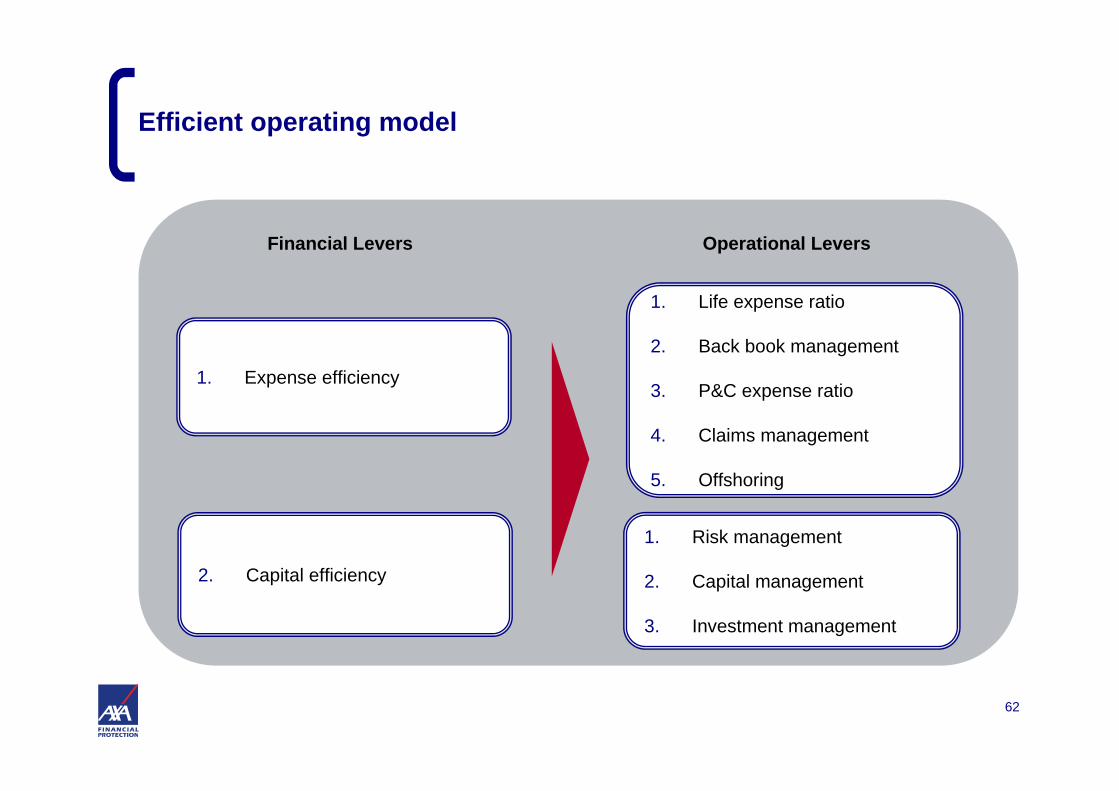

Efficient operating model

Financial Levers Operational Levers

2. Capital efficiency

1. Risk management

2. Capital management

3. Investment management

1. Life expense ratio

2. Back book management

3. P&C expense ratio

4. Claims management

5. Offshoring

1. Expense efficiency

63

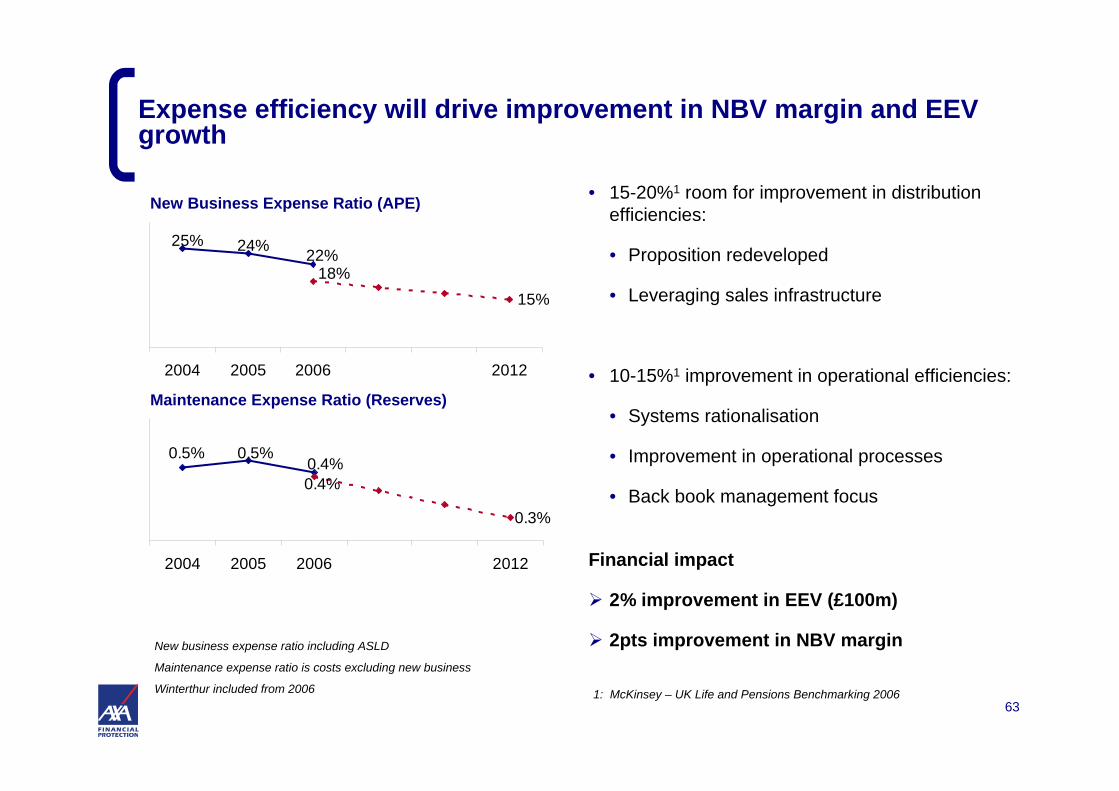

• 15-20%1 room for improvement in distribution efficiencies:

• Proposition redeveloped

• Leveraging sales infrastructure

• 10-15%1 improvement in operational efficiencies:

• Systems rationalisation

• Improvement in operational processes

• Back book management focus

Financial impact

2% improvement in EEV (£100m)

2pts improvement in NBV margin

Expense efficiency will drive improvement in NBV margin and EEV growth

1: McKinsey – UK Life and Pensions Benchmarking 2006

0.3%

0.5%0.5%0.4%0.4%

2004 2005 2006 2012

15%

24%25%22%

18%

2004 2005 2006 2012

New Business Expense Ratio (APE)

Maintenance Expense Ratio (Reserves)

New business expense ratio including ASLD

Maintenance expense ratio is costs excluding new business

Winterthur included from 2006

64

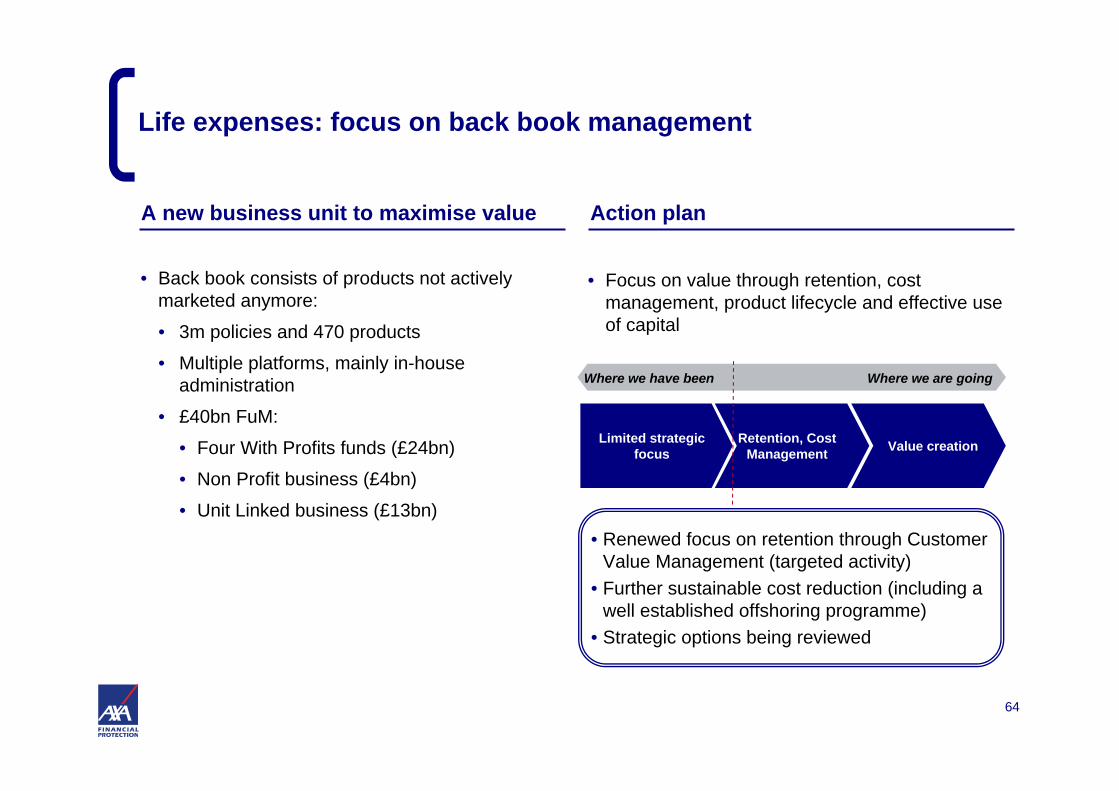

• Back book consists of products not actively marketed anymore:

• 3m policies and 470 products

• Multiple platforms, mainly in-house administration

• £40bn FuM:

• Four With Profits funds (£24bn)

• Non Profit business (£4bn)

• Unit Linked business (£13bn)

Life expenses: focus on back book management

A new business unit to maximise value Action plan

• Focus on value through retention, cost management, product lifecycle and effective use of capital

• Renewed focus on retention through Customer Value Management (targeted activity)

• Further sustainable cost reduction (including a well established offshoring programme)

• Strategic options being reviewed

Limited strategic focus

Retention, Cost Management Value creation

Where we have been Where we are going

65

Efficiency savings of 2% pa will come from:

• Improving cost ratio trend for AXAI and AXA PPP through a combination of:

• more self service by customers and intermediaries

• leveraging the benefits of systems automation

• offshoring to our AXA Business Services operation in India

AXA Non-life expense ratio stabilising at right level

AXA Ireland increase 2005-6 due to 40% reduction in average premiums as a result of competitive pressure

Source: AXA accounts

Management expenses vs GWP (percent)

10%

11.1%11.9%

13%

16.9%

13.7%13%

15.0%

16.3%

11%

12.7%13.2%

6%

8%

10%

12%

14%

16%

18%

2004

2005

2006

2012

AXA I AXA IrelandAXA PPP Non-life

66

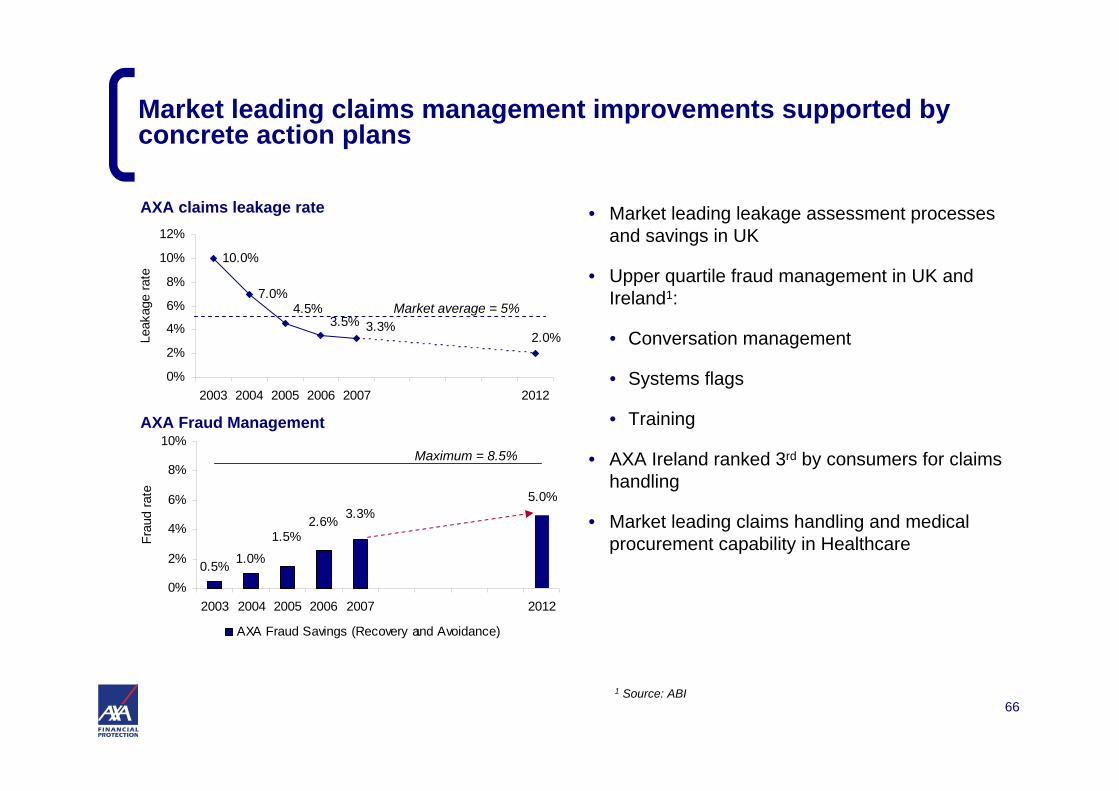

• Market leading leakage assessment processes and savings in UK

• Upper quartile fraud management in UK and Ireland1:

• Conversation management

• Systems flags

• Training

• AXA Ireland ranked 3rd by consumers for claims handling

• Market leading claims handling and medical procurement capability in Healthcare

Market leading claims management improvements supported by concrete action plans

1 Source: ABI

5.0%3.3%2.6%

1.5%

1.0%0.5%0%

2%

4%

6%

8%

10%

2003 2004 2005 2006 2007 2012

Frau

d ra

te

AXA Fraud Savings (Recovery and Avoidance)

10.0%

7.0%4.5%

3.5% 3.3%2.0%

0%

2%

4%

6%

8%

10%

12%

2003 2004 2005 2006 2007 2012

Leak

age

rate

AXA claims leakage rate

AXA Fraud Management

Market average = 5%

1

Maximum = 8.5%

67

Offshoring is an opportunity to optimise processes and create cost advantage

Proportion of AXA UK Headcount Offshore

• Average savings of £15k per person have delivered £30m of annual value

• Operating model delivering strong service levels

0%

5%

10%

15%

2003 2004 2005 2006 2007

15% of staff work offshore in mature state

68

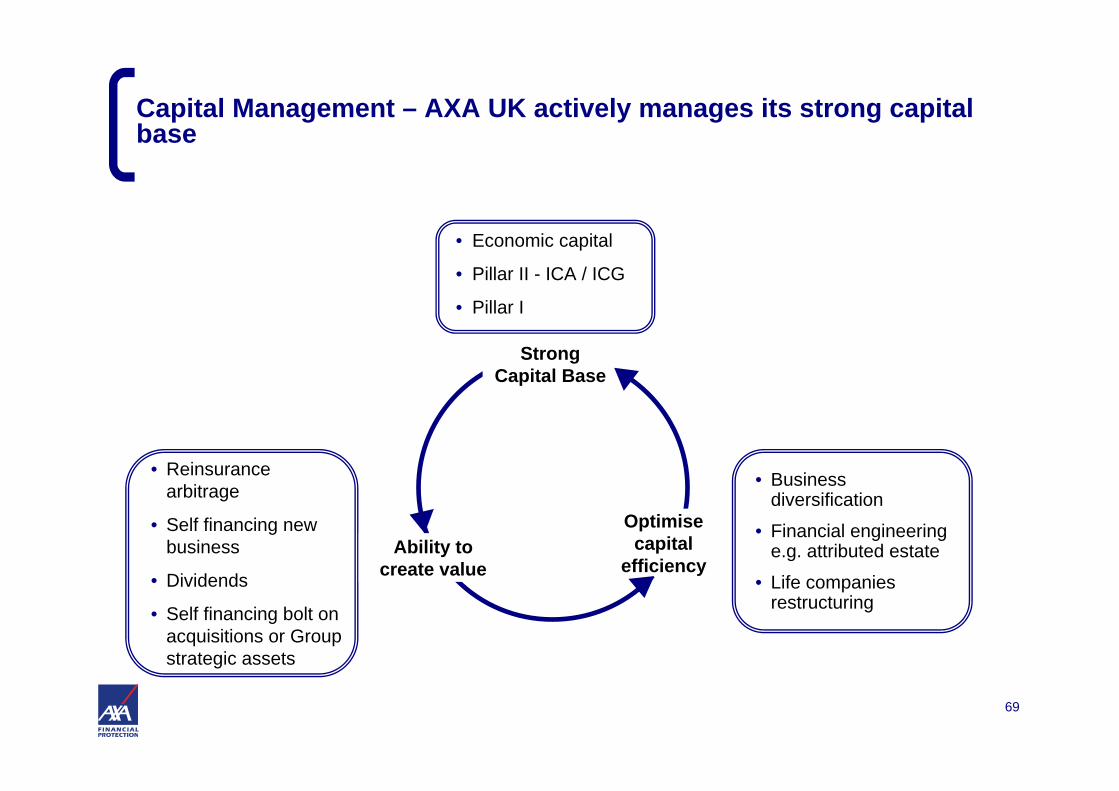

Strong risk management capabilities

Cont

rol p

rofita

bility

of g

rowt

h

Business enabler

Optimise balance sheet

Overview

• AXA UK has well developed risk-management capabilities that allows enhanced risk capacity

• Historically innovative eg orphan estate attribution in 2001

• AXA Group Risk Management capabilities rated Excellent by S&P

• Benefits from combining expertise in Life, P&C and Health insurance

Implications

• Profitability control

• Value creation/ risk adjusted profitability framework

• Product approval process

• Business Enabler

• E.g. investment guarantees

• Optimise balance sheet

• Capital management

• Asset liability management

• Financial restructuring

69

Capital Management – AXA UK actively manages its strong capital base

• Reinsurance arbitrage

• Self financing new business

• Dividends

• Self financing bolt on acquisitions or Group strategic assets

• Economic capital

• Pillar II - ICA / ICG

• Pillar I

• Business diversification

• Financial engineering e.g. attributed estate

• Life companies restructuring

Strong Capital Base

Ability to create value

Optimise capital

efficiency

70

A less conservative stance regarding acceptable levels of investment risk will drive an additional 75 – 100bps investment return

• Increased risk appetite

• Actively targeting illiquidity premium for certain asset classes

• Better diversification of investment returns being sought through wider asset base exposure.

• Fixed income portfolios above single A presently will move to single A when credit spreads improved

Target increase in Underlying Earnings of 15 to 20% from 2006 to 2012 and an impact of 1% on EEV growth p.a.

71

Today’s agenda

1 Strategic overview Nicolas MoreauGroup Chief Executive

6 Conclusion Nicolas MoreauGroup Chief Executive

2 Financial review Philippe MasoGroup Finance Director

3 Life manufacturing and advisory strategy

Paul EvansCEO, AXA Life

5 Business efficiency Philippe Maso Group Finance Director

4 Non-life manufacturing and distribution strategy

Peter HubbardCEO, AXA Insurance

72

Conclusion

The UK market is an exciting opportunity for AXA

We have set ourselves challenging targets

We have a clear plan and a great team to achieve our ambition

We believe that AXA UK can deliver its strategy without any major acquisitions

We are fully engaged and confident!

Appendices

74

Appendices

1 AXA UK and Ireland organisational chart

2 Executive members – Biographies

75

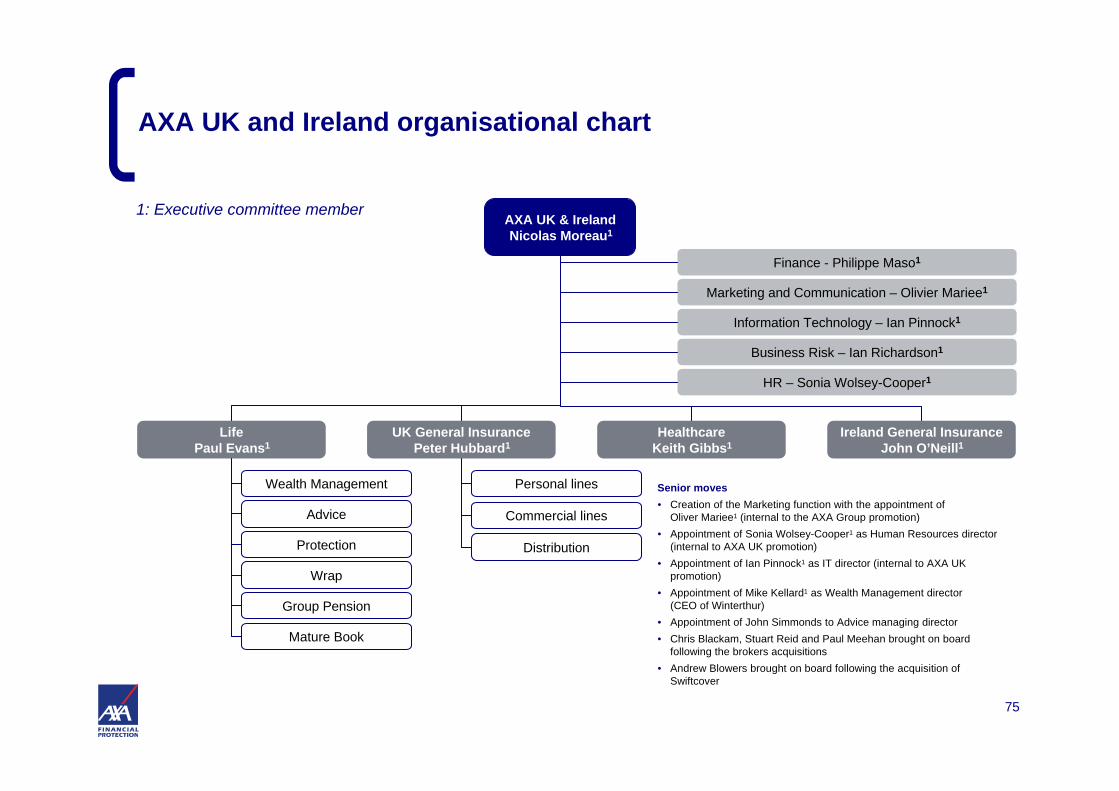

AXA UK and Ireland organisational chart

Senior moves• Creation of the Marketing function with the appointment of

Oliver Mariee1 (internal to the AXA Group promotion)• Appointment of Sonia Wolsey-Cooper1 as Human Resources director

(internal to AXA UK promotion)• Appointment of Ian Pinnock1 as IT director (internal to AXA UK

promotion)• Appointment of Mike Kellard1 as Wealth Management director

(CEO of Winterthur)• Appointment of John Simmonds to Advice managing director • Chris Blackam, Stuart Reid and Paul Meehan brought on board

following the brokers acquisitions• Andrew Blowers brought on board following the acquisition of

Swiftcover

AXA UK & IrelandNicolas Moreau1

Finance - Philippe Maso1

Marketing and Communication – Olivier Mariee1

Information Technology – Ian Pinnock1

Business Risk – Ian Richardson1

HR – Sonia Wolsey-Cooper1

LifePaul Evans1

Ireland General InsuranceJohn O’Neill1

HealthcareKeith Gibbs1

UK General InsurancePeter Hubbard1

Wealth Management Personal lines

Advice Commercial lines

Protection Distribution

Wrap

Group Pension

Mature Book

1: Executive committee member

76

Executive members – Biographies

Nicolas Moreau was appointed to the Board in July 2006. He is Group Chief Executive of AXA UK and Ireland, and a member of the AXA Executive Committee.

Nicolas Moreau joined AXA in 1991 as Vice-President of the Finance Department and was appointed Senior Vice-President of the AXA Group Finance Department in 1994. In 1997 Nicolas Moreau joined AXA Investment Managers and in March 2000 he became Chief Operating Officer of AXA Investment Managers, and Vice-Chairman of AXA Rosenberg in January 2001. He also co-ordinated the private equity business as well as the relationship between AXA Investment Managers and the insurance companies of the AXA Group. In April 2002, he was promoted to Chief Executive of AXA Investment Managers and, following his appointment as Group Chief Executive of AXA UK, Nicolas Moreau became Non-Executive Chairman of the Board of AXA Investment Managers.

Nicolas Moreau is an ABI Board member and the Chairman of the ABI Health Commission.

Philippe Maso was appointed Group Finance Director of AXA UK in May 2003, responsible for finance, strategy, risk management and asset management. A member of the Board since June 2003, he is also a member of the AXA Executive Committee.

Previously, he was head of Group Corporate Finance and Risk Management for AXA in Paris. He joined the Group in 1997 following the merger with UAP.

He is a member of the Financial Regulation and Taxation Committee for the Association of British Insurers.

Phillipe Maso y Guell Rivet Group Finance Director, AXA UK

Nicolas MoreauGroup Chief Executive, AXA UK

77

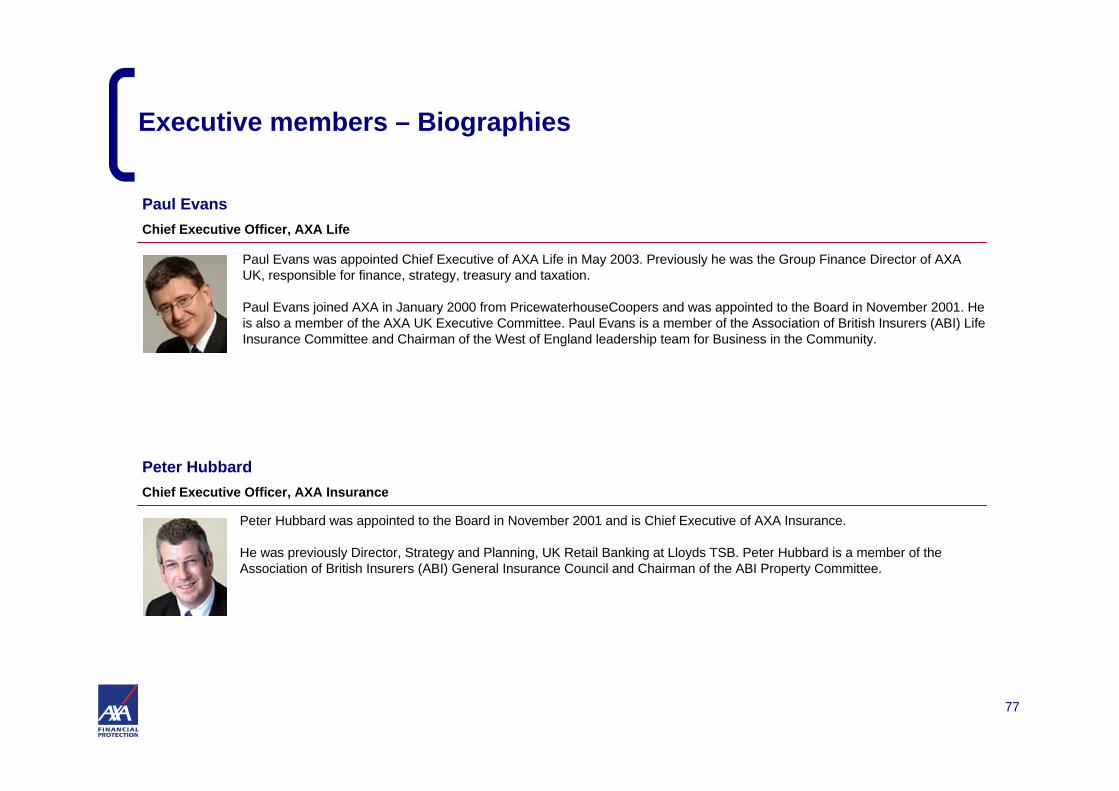

Executive members – Biographies

Paul Evans was appointed Chief Executive of AXA Life in May 2003. Previously he was the Group Finance Director of AXA UK, responsible for finance, strategy, treasury and taxation.

Paul Evans joined AXA in January 2000 from PricewaterhouseCoopers and was appointed to the Board in November 2001. He is also a member of the AXA UK Executive Committee. Paul Evans is a member of the Association of British Insurers (ABI) Life Insurance Committee and Chairman of the West of England leadership team for Business in the Community.

Peter Hubbard was appointed to the Board in November 2001 and is Chief Executive of AXA Insurance.

He was previously Director, Strategy and Planning, UK Retail Banking at Lloyds TSB. Peter Hubbard is a member of the Association of British Insurers (ABI) General Insurance Council and Chairman of the ABI Property Committee.

Peter Hubbard Chief Executive Officer, AXA Insurance

Paul Evans Chief Executive Officer, AXA Life

78

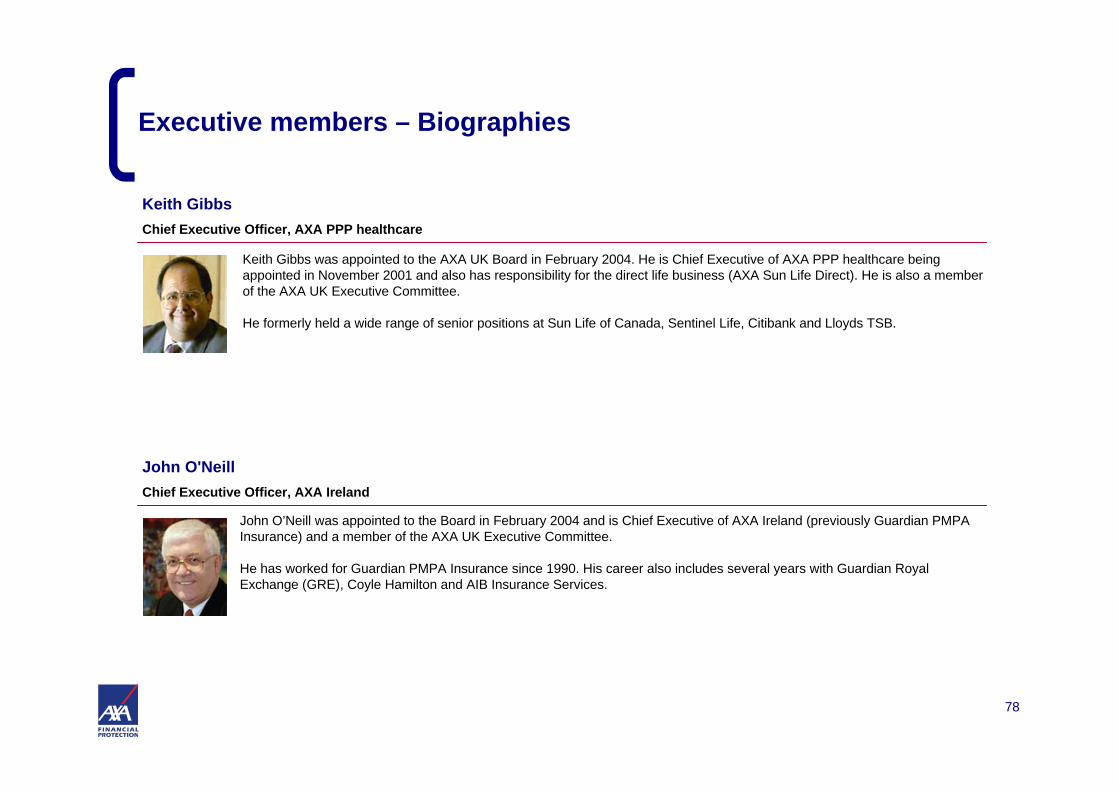

Executive members – Biographies

Keith Gibbs was appointed to the AXA UK Board in February 2004. He is Chief Executive of AXA PPP healthcare being appointed in November 2001 and also has responsibility for the direct life business (AXA Sun Life Direct). He is also a member of the AXA UK Executive Committee.

He formerly held a wide range of senior positions at Sun Life of Canada, Sentinel Life, Citibank and Lloyds TSB.

John O’Neill was appointed to the Board in February 2004 and is Chief Executive of AXA Ireland (previously Guardian PMPA Insurance) and a member of the AXA UK Executive Committee.

He has worked for Guardian PMPA Insurance since 1990. His career also includes several years with Guardian Royal Exchange (GRE), Coyle Hamilton and AIB Insurance Services.

John O'NeillChief Executive Officer, AXA Ireland

Keith Gibbs Chief Executive Officer, AXA PPP healthcare

79

Executive members – Biographies

Mike Kellard joined Winterthur Life in 1999 before becoming CEO in June 2003. Mike Kellard was appointed to the Executive Committee of AXA UK on 22 December 2006 when AXA completed its acquisition of Winterthur Group. Mike Kellard is also responsible for implementing a new fund management proposition for AXA Life and Pensions.

Ian Richardson was appointed to the AXA UK Board as Group Business Risk Director in August 2004, responsible for Legal, Internal Audit, Compliance, Operational Risk and Company Secretarial matters.

Before then, he had been Group Company Secretary of AXA UK plc since its formation (as Sun Life and Provincial Holdings) in 1995. He remains a member of the AXA UK Executive Committee.

Ian Richardson is a Fellow of the Institute of Chartered Secretaries and Administrators (FCIS) and an Adviser to that Institute.

Ian RichardsonGroup Business Risk Director, AXA UK

Mike Kellard Chief Executive Officer, Winterthur Life

80

Executive members – Biographies

Sonia Wolsey-Cooper was appointed Group HR Director in 2006, following a four year period where she headed up the customer service division at AXA PPP healthcare.

Prior to joining AXA PPP healthcare in 2002, Sonia Wolsey-Cooper held various senior roles at Lloyds TSB Group including Executive Assistant to the Group Chief Executive, Head of Direct Insurance, Head of Direct Operations and Call Centre Manager.

Ian Pinnock was appointed Group Chief Information Officer of AXA UK in 2006, after having managed the AXA UK IT Shared Services.

Ian Pinnock started working in 1978 at Guardian Royal Exchange (GRE) in 1978, where he held a wide range of positions. He joined AXA when GRE was acquired in May 1999.

Ian PinnockGroup Chief Information Officer, AXA UK

Sonia Wolsey-CooperGroup HR Director, AXA UK

81

Executive members – Biographies

Olivier Mariee was appointed Group Marketing & Communication Director in 2006 from his role as Senior Vice President and Head of AXA Group customer care & distribution.

Olivier Mariee joined the AXA Group in 1992. He has worked in various companies of the AXA Group including AXA Investment Managers, AXA Japan and AXA Headquarters.

Olivier MarieeGroup Marketing & Communication Director