axa x dssg meetup sharing (feb 2016)

TRANSCRIPT

WHAT'S AN INSURER LIKE AXA

DOING IN THE BIG DATA WORLD?

Data science Meetup 23rd Feb 216

Philippe Marie-Jeanne

Group CDO & Head of the DIL

Ankur Agrawal

Head of the DIL@Asia

1 AXA’s transformation

3 | SMART DATA AND DATA INNOVATION LAB

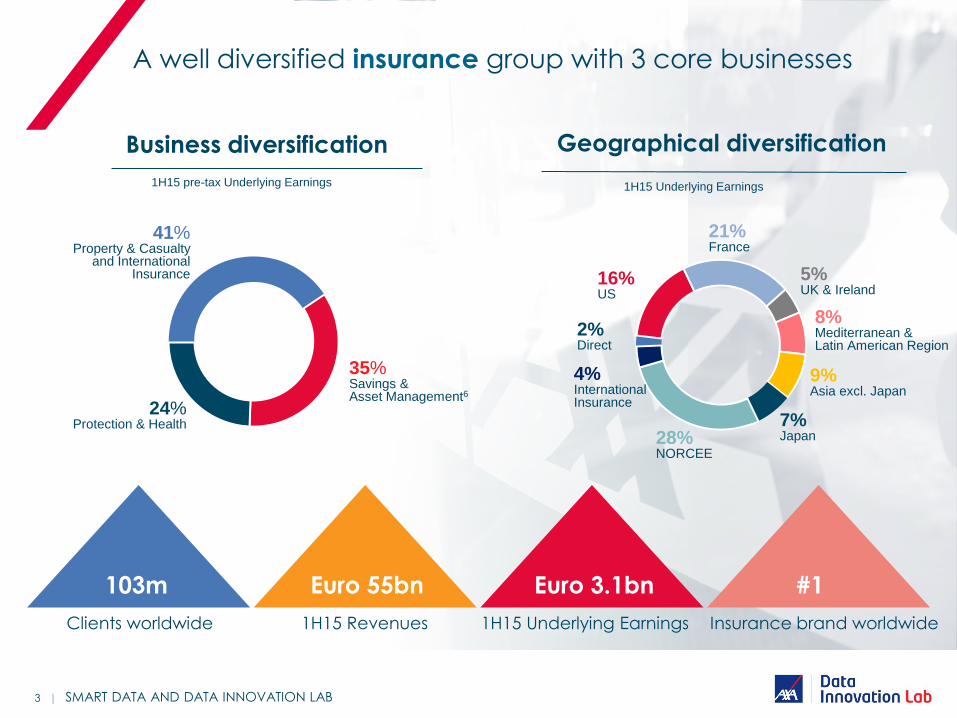

Business diversification Geographical diversification

A well diversified insurance group with 3 core businesses

35% Savings & Asset Management6

24% Protection & Health

41% Property & Casualty

and International Insurance

21% France

5% UK & Ireland

8% Mediterranean & Latin American Region

9% Asia excl. Japan

7% Japan 28%

NORCEE

4% International Insurance

2% Direct

16% US

103m Euro 55bn Euro 3.1bn #1

Clients worldwide 1H15 Revenues 1H15 Underlying Earnings Insurance brand worldwide

1H15 pre-tax Underlying Earnings 1H15 Underlying Earnings

4 | SMART DATA AND DATA INNOVATION LAB

Three main sources of growth

92 EURO BN

revenues

Strategic allocation

of capital to growth

areas and products

Focus on profitable growth

and disciplined capital

reallocation

Digital transformation

on every part of the

value chain

Mature

markets High growth

markets Digital

The Data Innovation Lab

as a transformation engine

within AXA

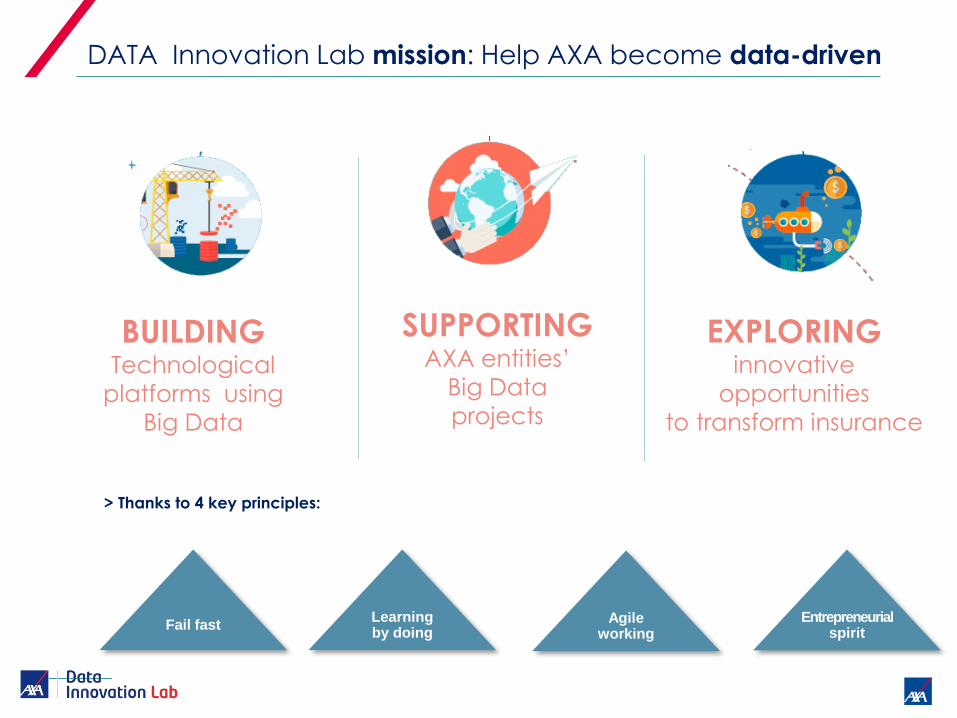

DATA Innovation Lab mission: Help AXA become data-driven

Fail fast Entrepreneurial

spirit Agile

working Learning by doing

> Thanks to 4 key principles:

BUILDING Technological

platforms using

Big Data

SUPPORTING AXA entities’

Big Data

projects

EXPLORING innovative

opportunities

to transform insurance

7 | SMART DATA AND DATA INNOVATION LAB

… Thanks to specific resources and assets…

AN INTERNATIONAL TALENT POOL SPECIFIC METHODOLOGIES

DATA!

A TEAM OF SELECTED EXPERTS PLATFORMS & TOOLS

8 | SMART DATA AND DATA INNOVATION LAB

… And key areas of investment

Platforms

9 | SMART DATA AND DATA INNOVATION LAB

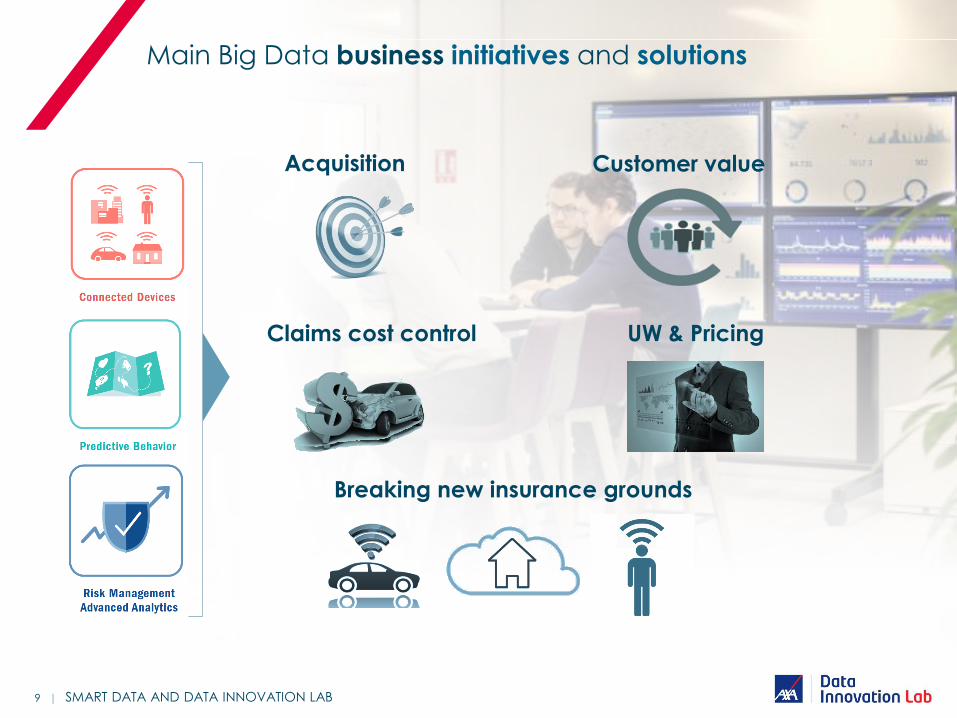

Main Big Data business initiatives and solutions

Acquisition Customer value

Claims cost control UW & Pricing

Breaking new insurance grounds

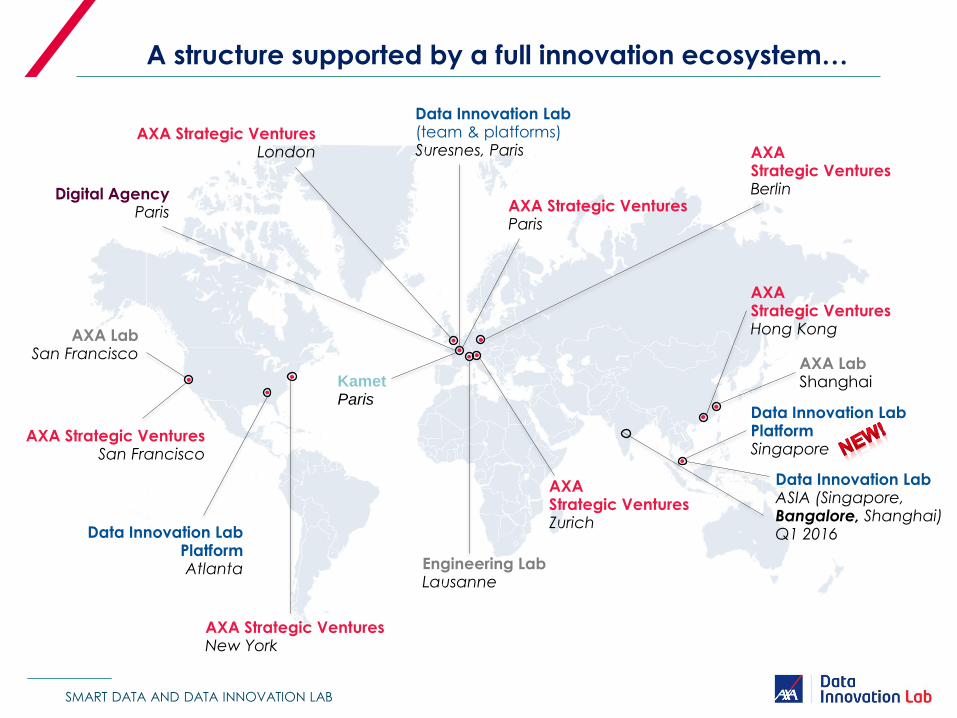

AXA Lab San Francisco

AXA Lab Shanghai

A structure supported by a full innovation ecosystem…

AXA Strategic Ventures New York

AXA Strategic Ventures Paris

AXA Strategic Ventures London

AXA Strategic Ventures San Francisco

AXA Strategic Ventures Hong Kong

AXA Strategic Ventures Zurich

AXA Strategic Ventures Berlin

Kamet Paris

Data Innovation Lab (team & platforms) Suresnes, Paris

Data Innovation Lab Platform Atlanta

Data Innovation Lab Platform Singapore

Data Innovation Lab ASIA (Singapore, Bangalore, Shanghai) Q1 2016

Engineering Lab Lausanne

Digital Agency Paris

SMART DATA AND DATA INNOVATION LAB

How big is Big Data for AXA?

A business perspective

”Big Data is an economical and technological revolution… …being defensive is a waste of time as it is

unavoidable and lethal” - Henri de Castries

AXA CEO

13 | SMART DATA AND DATA INNOVATION LAB

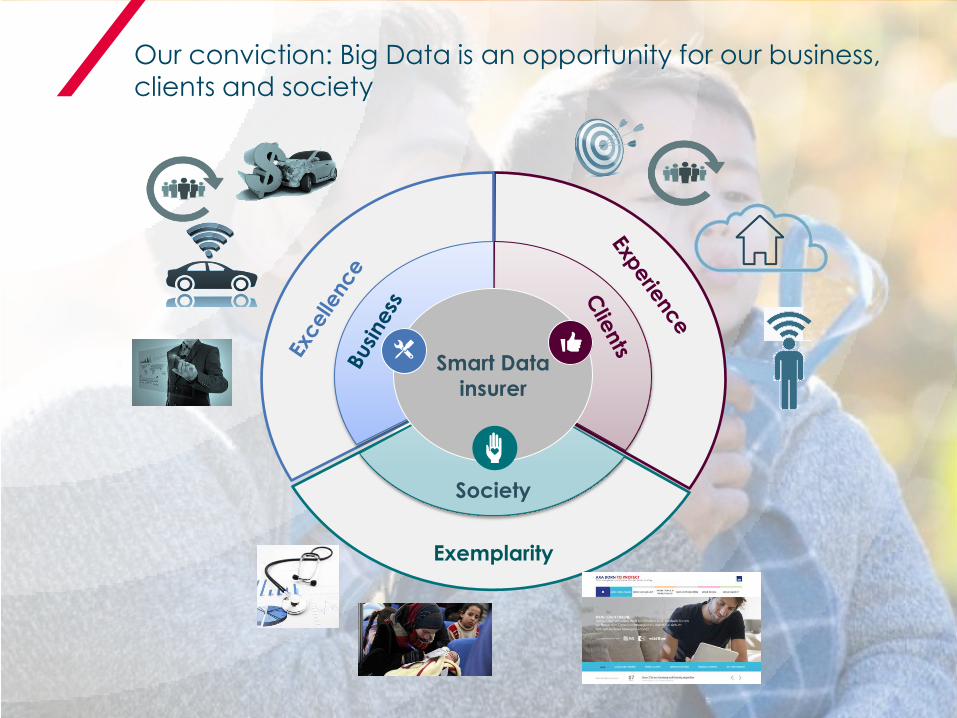

Smart Data

insurer

Society

Exemplarity

Our conviction: Big Data is an opportunity for our business,

clients and society

14 | SMART DATA AND DATA INNOVATION LAB

Learning in the data cube*

> An industry perspective

n observations

d dimensions

* From an idea of F. Bach

Biased

Redundancy

Growing volume

Real-time

Low Meta data

management Maturity

Acess to data

Data quality (format, missing

data, noise…)

Historic duration

Unstructured data

Curse of dimensionality

(generalization challenge)

Biased

Rare

Imbalanced

Noisy

Labels

X X

X o

o

o

Personalized treatment learning (causal

inference)

Not randomized treatment

Interpretability

Reality

Performance monitoring and causality

(e.g. homophily vs influence, true lift)

k actions

2 Deep Dive

Fraud project

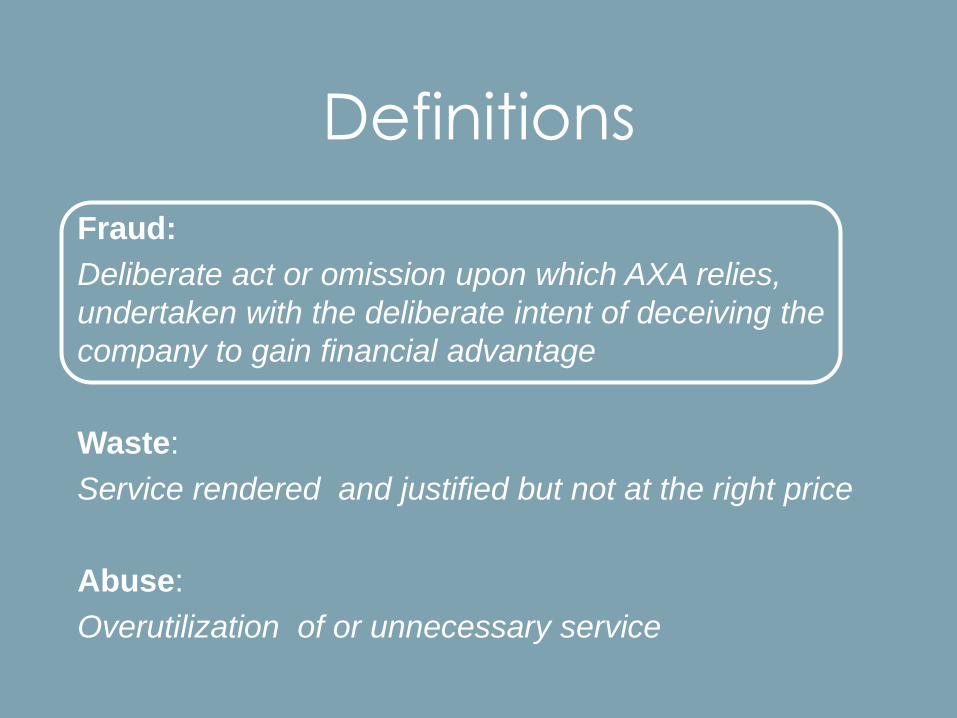

Fraud:

Deliberate act or omission upon which AXA relies,

undertaken with the deliberate intent of deceiving the

company to gain financial advantage

Waste:

Service rendered and justified but not at the right price

Abuse:

Overutilization of or unnecessary service

Definitions

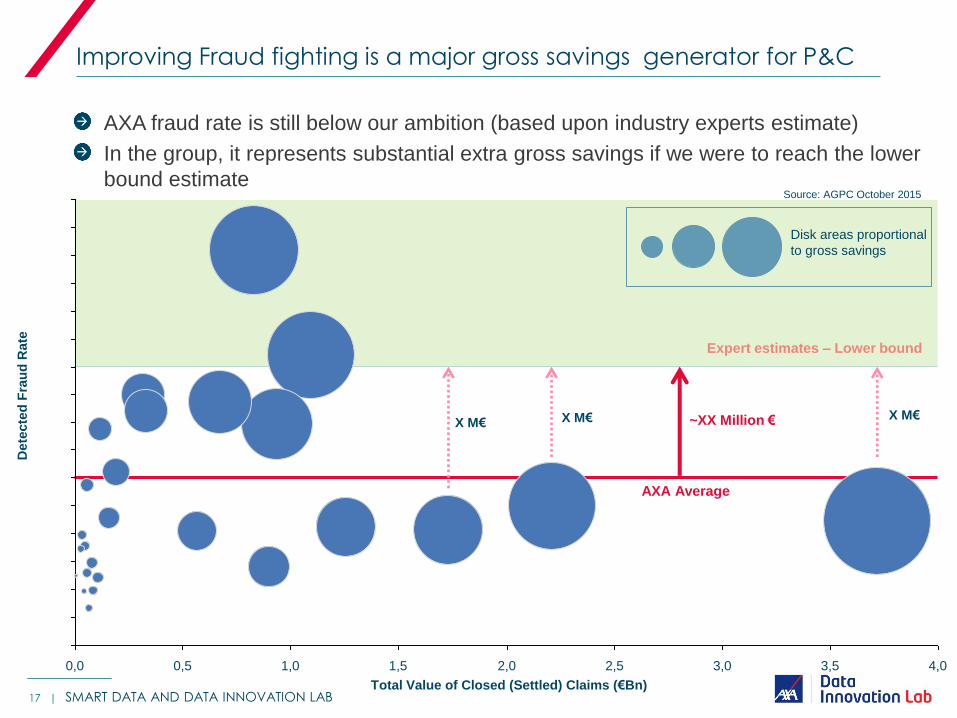

Improving Fraud fighting is a major gross savings generator for P&C

17 |

Expert estimates – Lower bound

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

1,5 4,0 3,5 3,0 2,5 2,0 1,0 0,5 0,0

Dete

cte

d F

rau

d R

ate

Total Value of Closed (Settled) Claims (€Bn)

~XX Million €

Source: AGPC October 2015

Disk areas proportional

to gross savings

X M€ X M€

AXA Average

X M€

AXA fraud rate is still below our ambition (based upon industry experts estimate)

In the group, it represents substantial extra gross savings if we were to reach the lower

bound estimate

SMART DATA AND DATA INNOVATION LAB

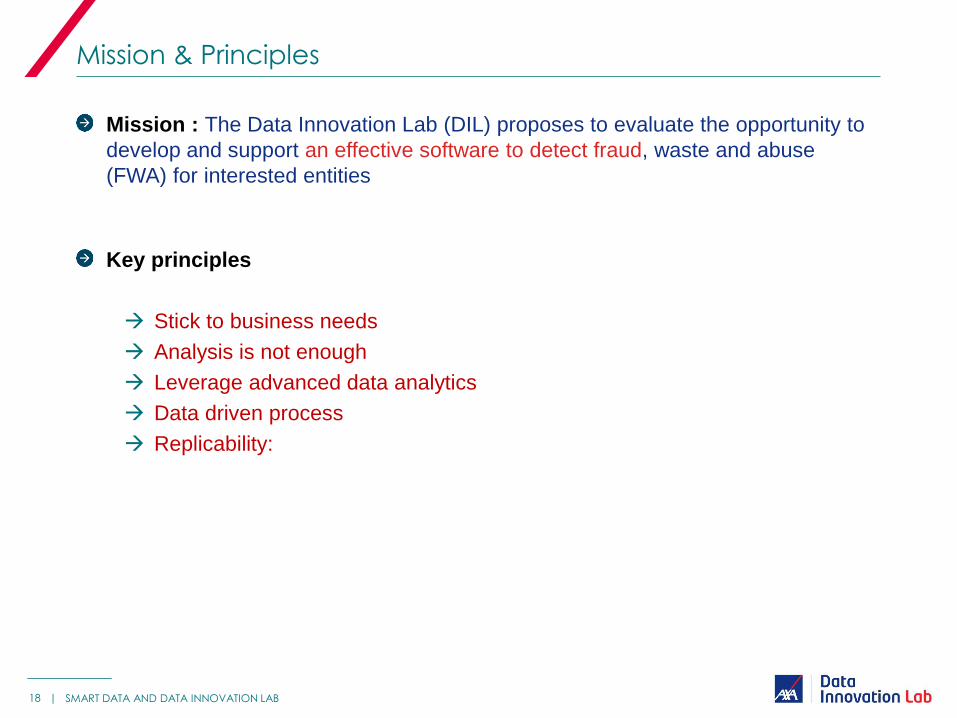

Mission : The Data Innovation Lab (DIL) proposes to evaluate the opportunity to

develop and support an effective software to detect fraud, waste and abuse

(FWA) for interested entities

Key principles

Stick to business needs

Analysis is not enough

Leverage advanced data analytics

Data driven process

Replicability:

Mission & Principles

18 | SMART DATA AND DATA INNOVATION LAB

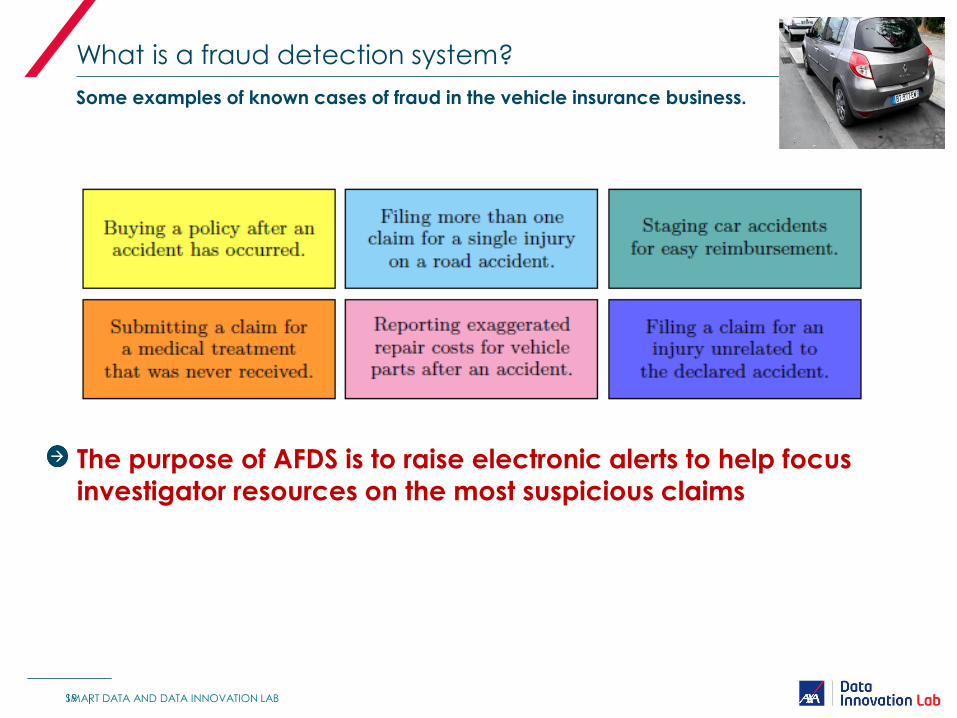

The purpose of AFDS is to raise electronic alerts to help focus

investigator resources on the most suspicious claims

What is a fraud detection system?

Some examples of known cases of fraud in the vehicle insurance business.

19 | SMART DATA AND DATA INNOVATION LAB

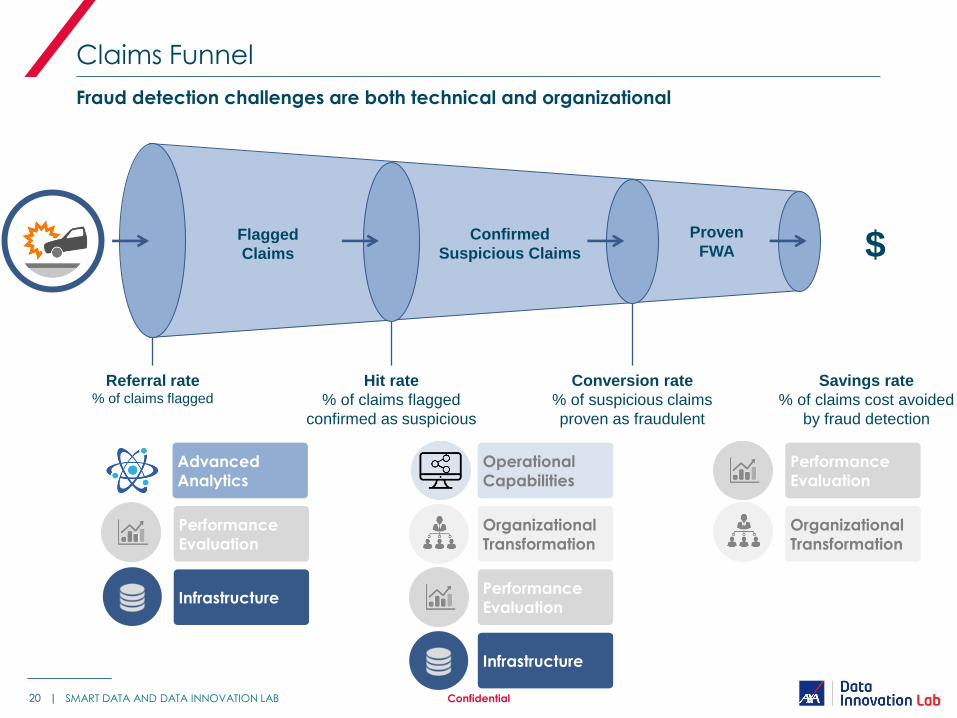

Claims Funnel

Fraud detection challenges are both technical and organizational

20 | Confidential

Flagged

Claims

Confirmed

Suspicious Claims $

Referral rate % of claims flagged

Hit rate

% of claims flagged

confirmed as suspicious

Conversion rate

% of suspicious claims

proven as fraudulent

Proven

FWA

Advanced

Analytics

Performance

Evaluation

Infrastructure

Operational

Capabilities

Organizational

Transformation

Performance

Evaluation

Infrastructure

Performance

Evaluation

Organizational

Transformation

Savings rate

% of claims cost avoided

by fraud detection

SMART DATA AND DATA INNOVATION LAB

Fraud detection modelling & Operations

Data scientists and operations cooperation is mandatory to ensure the success of fraud detection

21 |

Ingest, Clean & integrate data Develop a

predictive

model

Launch a pilot

to make a “live

test”

Estimate financial

benefits

Ingest new

data & refine

the model

Test the model on

historical data

& assess

performance

SMART DATA AND DATA INNOVATION LAB

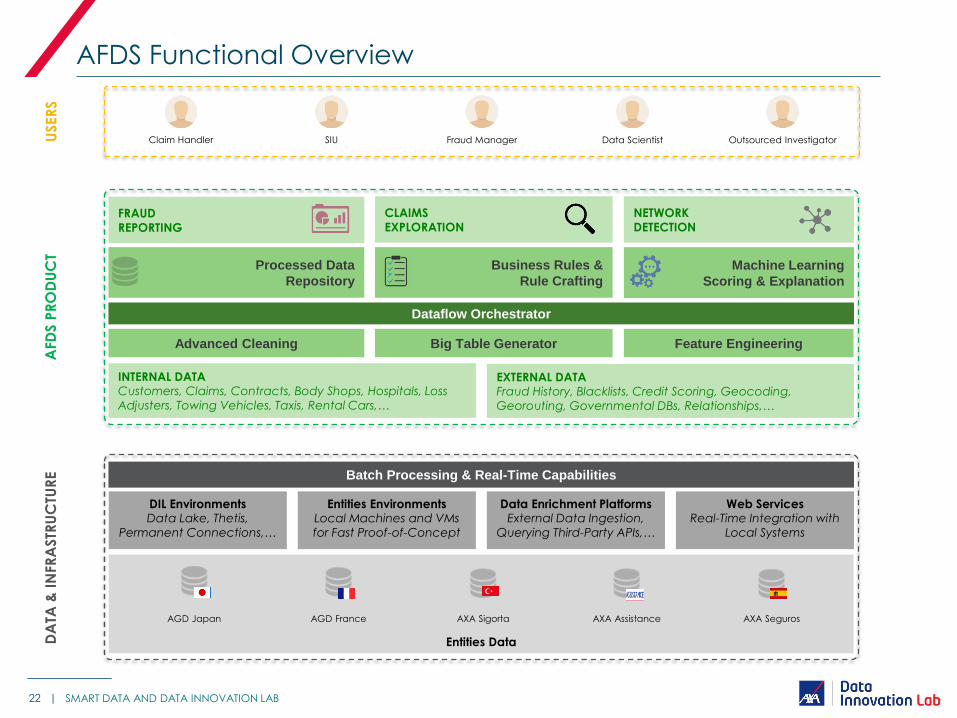

AFDS Functional Overview

Entities Data

AGD Japan

DIL Environments Data Lake, Thetis,

Permanent Connections,…

DA

TA &

IN

FR

ASTR

UC

TUR

E

AGD France AXA Sigorta AXA Assistance AXA Seguros

Batch Processing & Real-Time Capabilities

Entities Environments

Local Machines and VMs

for Fast Proof-of-Concept

Data Enrichment Platforms External Data Ingestion,

Querying Third-Party APIs,…

Web Services Real-Time Integration with

Local Systems

Fraud Manager Outsourced Investigator Claim Handler SIU Data Scientist USER

S

NETWORK

DETECTION

Processed Data

Repository

EXTERNAL DATA Fraud History, Blacklists, Credit Scoring, Geocoding,

Georouting, Governmental DBs, Relationships,…

INTERNAL DATA Customers, Claims, Contracts, Body Shops, Hospitals, Loss

Adjusters, Towing Vehicles, Taxis, Rental Cars,…

Machine Learning

Scoring & Explanation

FRAUD REPORTING

CLAIMS

EXPLORATION

AFD

S P

RO

DU

CT

Dataflow Orchestrator

Business Rules &

Rule Crafting

Advanced Cleaning Big Table Generator Feature Engineering

22 | SMART DATA AND DATA INNOVATION LAB

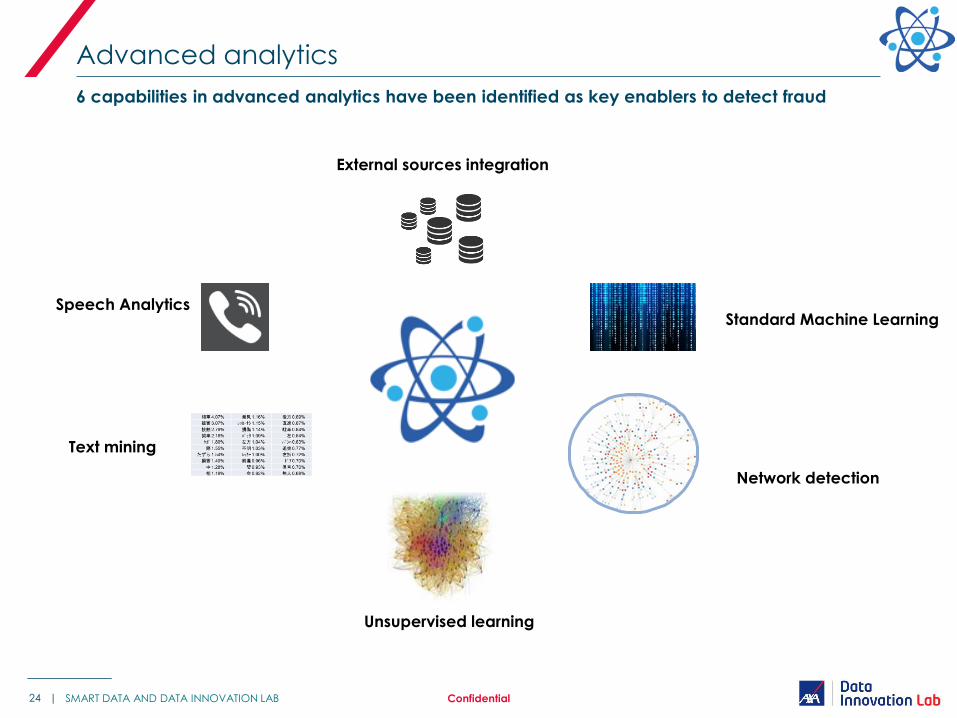

Data science challenges

Advanced analytics

6 capabilities in advanced analytics have been identified as key enablers to detect fraud

24 | Confidential

External sources integration

Speech Analytics

Text mining

Network detection

Unsupervised learning

Standard Machine Learning

SMART DATA AND DATA INNOVATION LAB

Advanced analytics challenges

One critical data challenge

25 | Confidential

Essential problem for statistical models and esp. supervised learning

SMART DATA AND DATA INNOVATION LAB

No clear information about non-investigated claims

The target is a rare event

The target is biased

The target is an imbalanced variable

Advanced analytics challenges

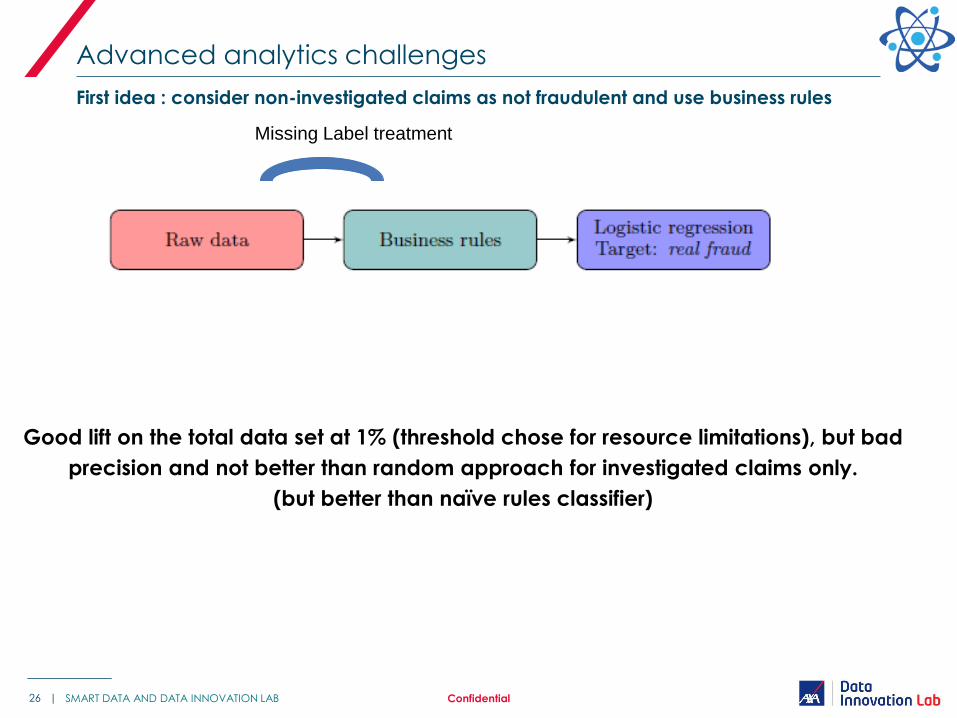

First idea : consider non-investigated claims as not fraudulent and use business rules

26 | Confidential

Good lift on the total data set at 1% (threshold chose for resource limitations), but bad

precision and not better than random approach for investigated claims only.

(but better than naïve rules classifier)

SMART DATA AND DATA INNOVATION LAB

Missing Label treatment

Advanced analytics challenges

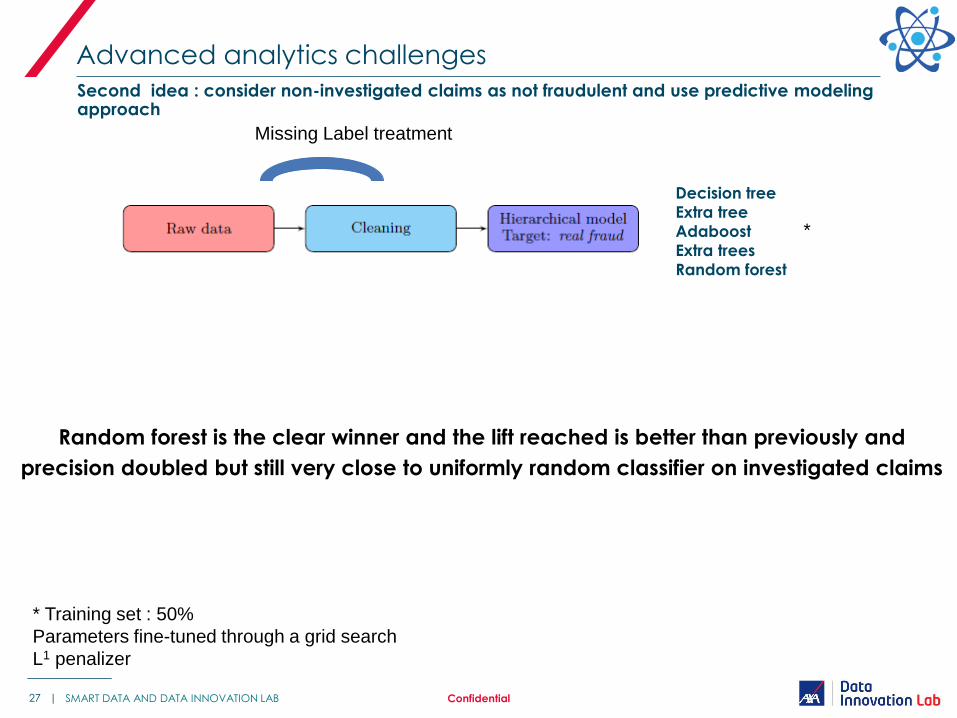

Second idea : consider non-investigated claims as not fraudulent and use predictive modeling approach

27 | Confidential

Random forest is the clear winner and the lift reached is better than previously and

precision doubled but still very close to uniformly random classifier on investigated claims

SMART DATA AND DATA INNOVATION LAB

Missing Label treatment

Decision tree

Extra tree

Adaboost

Extra trees

Random forest

* Training set : 50%

Parameters fine-tuned through a grid search

L1 penalizer

*

Advanced analytics challenges

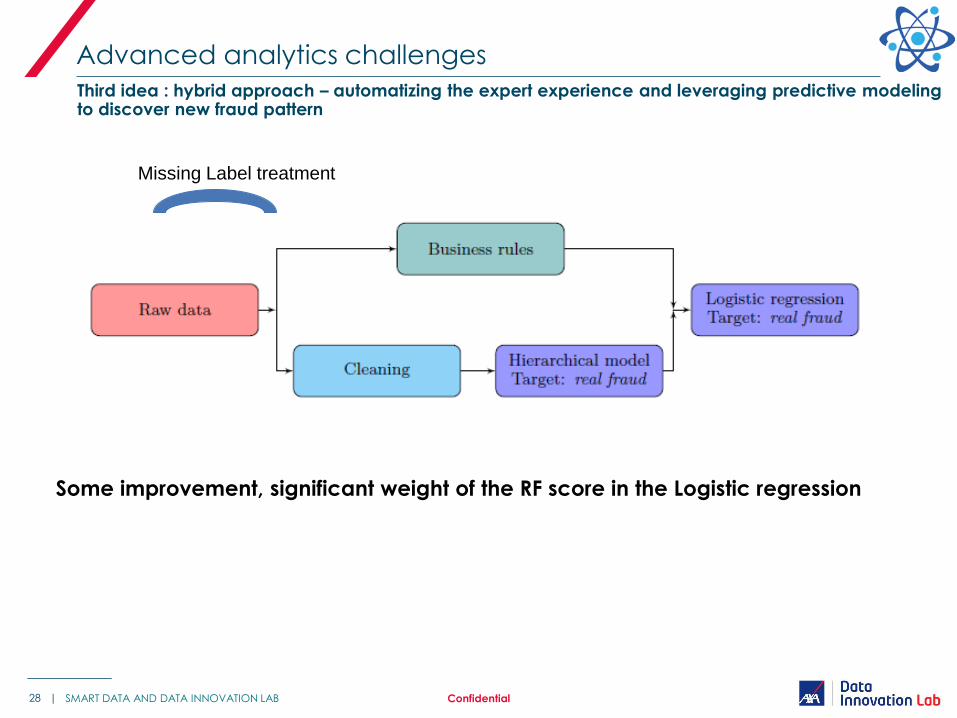

Third idea : hybrid approach – automatizing the expert experience and leveraging predictive modeling to discover new fraud pattern

28 | Confidential

Some improvement, significant weight of the RF score in the Logistic regression

SMART DATA AND DATA INNOVATION LAB

Missing Label treatment

Advanced analytics challenges

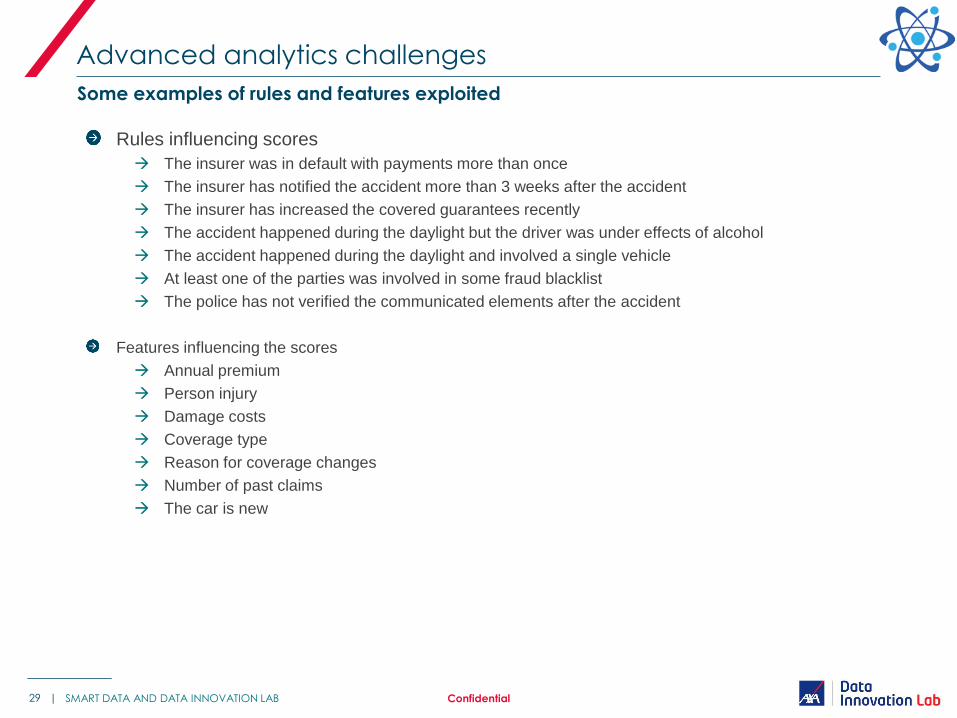

Some examples of rules and features exploited

29 | Confidential SMART DATA AND DATA INNOVATION LAB

Rules influencing scores

The insurer was in default with payments more than once

The insurer has notified the accident more than 3 weeks after the accident

The insurer has increased the covered guarantees recently

The accident happened during the daylight but the driver was under effects of alcohol

The accident happened during the daylight and involved a single vehicle

At least one of the parties was involved in some fraud blacklist

The police has not verified the communicated elements after the accident

Features influencing the scores

Annual premium

Person injury

Damage costs

Coverage type

Reason for coverage changes

Number of past claims

The car is new

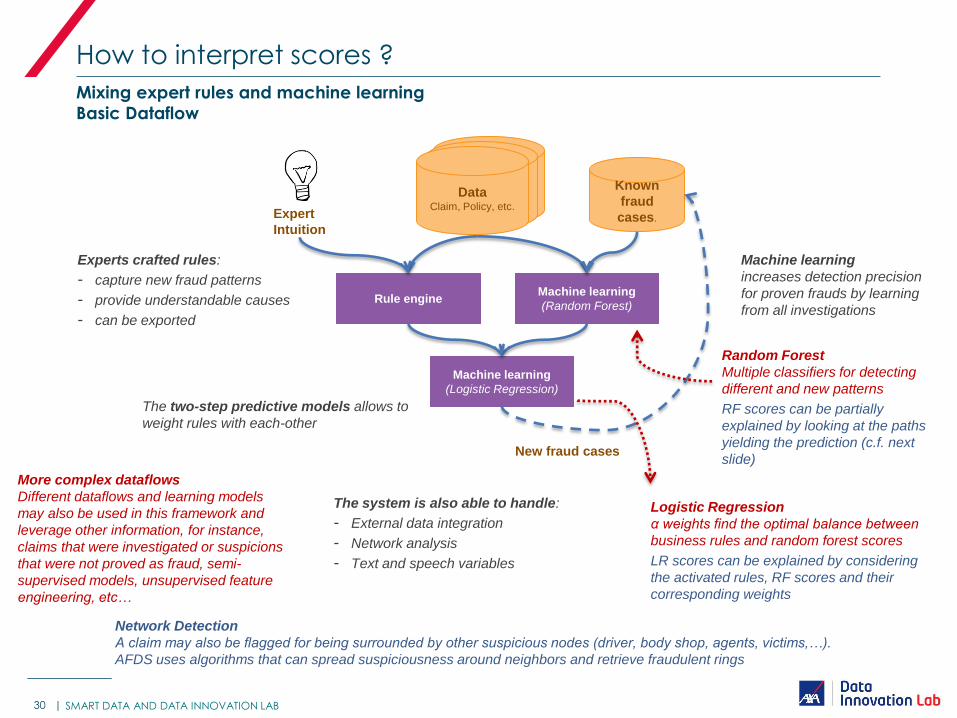

How to interpret scores ?

Mixing expert rules and machine learning

Basic Dataflow

30 |

Data Claim, Policy, etc.

Rule engine Machine learning

(Random Forest)

Machine learning

(Logistic Regression)

Known

fraud

cases. Expert

Intuition

Experts crafted rules:

- capture new fraud patterns

- provide understandable causes

- can be exported

Machine learning

increases detection precision

for proven frauds by learning

from all investigations

New fraud cases

The two-step predictive models allows to

weight rules with each-other

The system is also able to handle:

- External data integration

- Network analysis

- Text and speech variables

Random Forest

Multiple classifiers for detecting

different and new patterns

RF scores can be partially

explained by looking at the paths

yielding the prediction (c.f. next

slide)

Logistic Regression

α weights find the optimal balance between

business rules and random forest scores

LR scores can be explained by considering

the activated rules, RF scores and their

corresponding weights

More complex dataflows

Different dataflows and learning models

may also be used in this framework and

leverage other information, for instance,

claims that were investigated or suspicions

that were not proved as fraud, semi-

supervised models, unsupervised feature

engineering, etc…

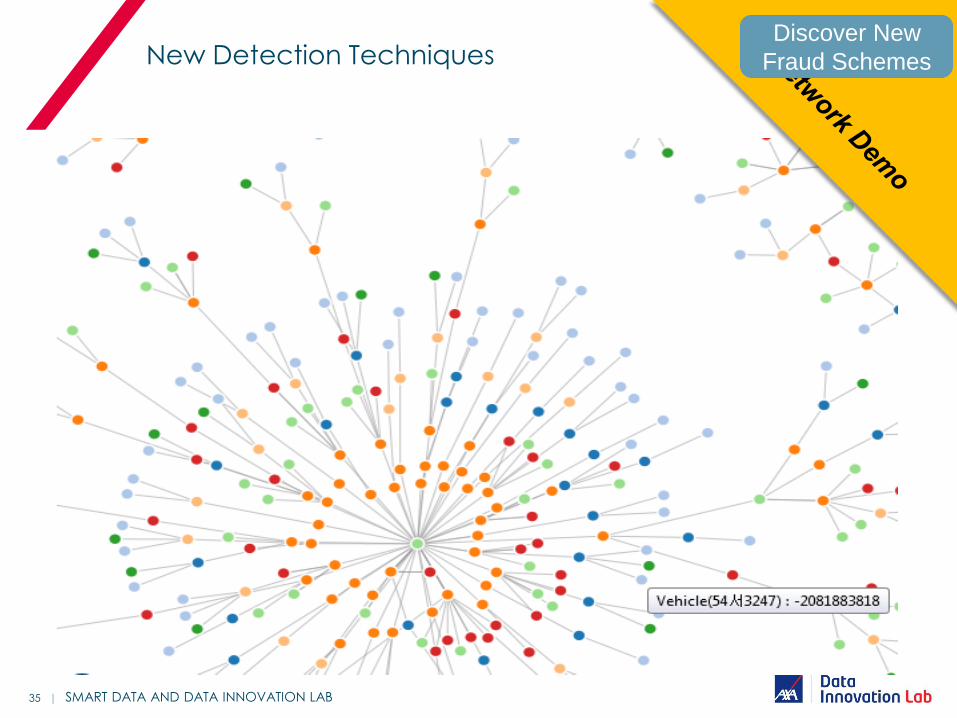

Network Detection

A claim may also be flagged for being surrounded by other suspicious nodes (driver, body shop, agents, victims,…).

AFDS uses algorithms that can spread suspiciousness around neighbors and retrieve fraudulent rings

SMART DATA AND DATA INNOVATION LAB

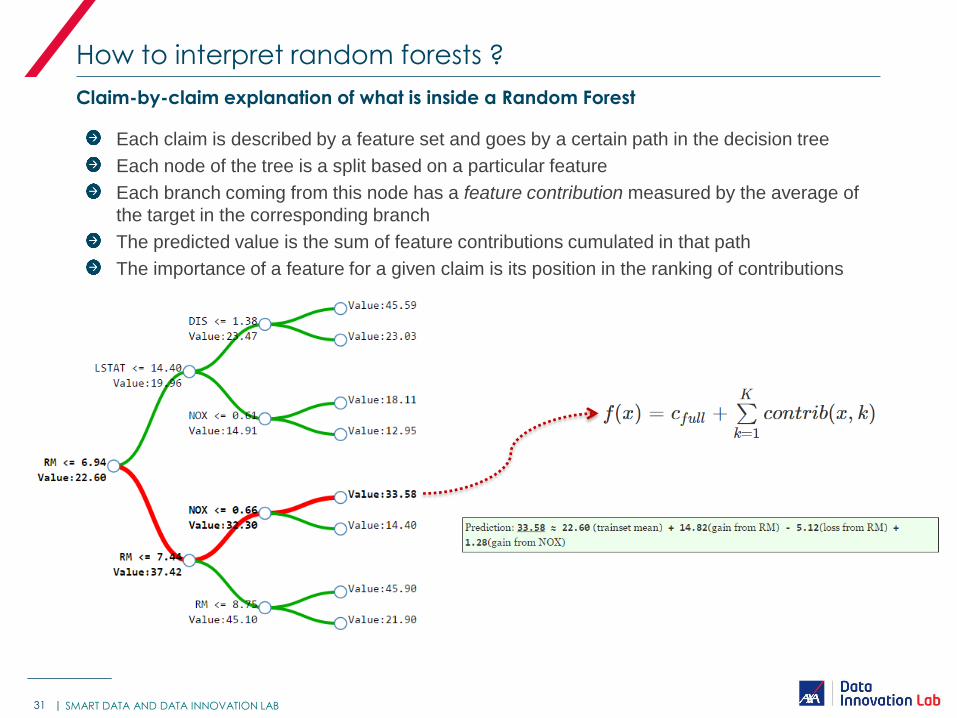

How to interpret random forests ?

Claim-by-claim explanation of what is inside a Random Forest

31 |

Each claim is described by a feature set and goes by a certain path in the decision tree

Each node of the tree is a split based on a particular feature

Each branch coming from this node has a feature contribution measured by the average of

the target in the corresponding branch

The predicted value is the sum of feature contributions cumulated in that path

The importance of a feature for a given claim is its position in the ranking of contributions

SMART DATA AND DATA INNOVATION LAB

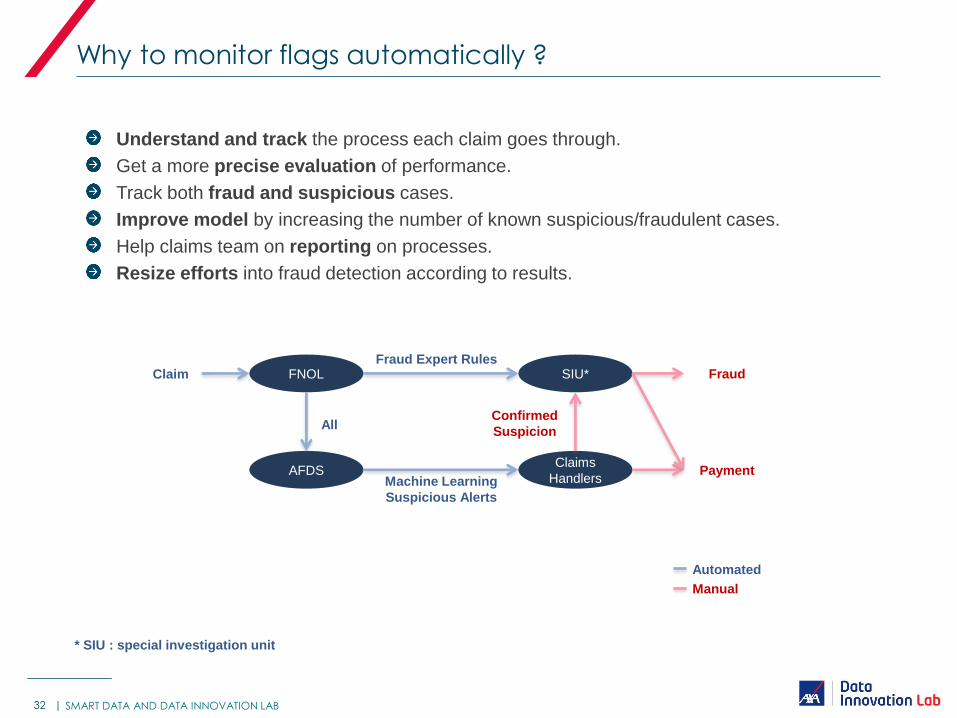

Why to monitor flags automatically ?

32 |

Understand and track the process each claim goes through.

Get a more precise evaluation of performance.

Track both fraud and suspicious cases.

Improve model by increasing the number of known suspicious/fraudulent cases.

Help claims team on reporting on processes.

Resize efforts into fraud detection according to results.

FNOL

AFDS

SIU*

Claims

Handlers

Fraud

Payment

Fraud Expert Rules Claim

Machine Learning

Suspicious Alerts

Confirmed

Suspicion All

Automated

Manual

* SIU : special investigation unit

SMART DATA AND DATA INNOVATION LAB

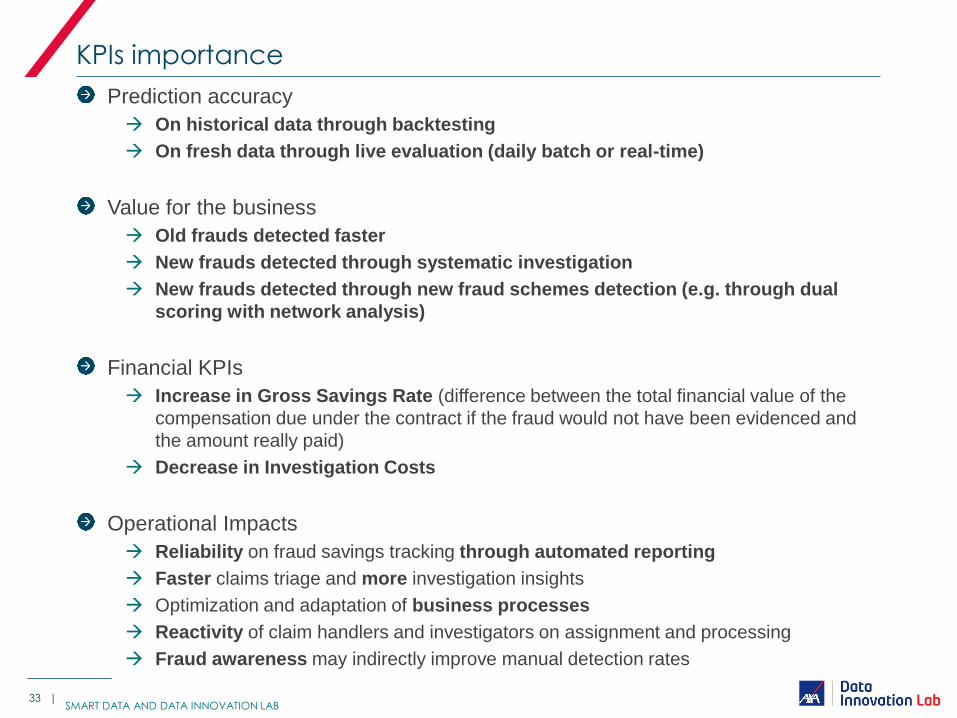

Prediction accuracy

On historical data through backtesting

On fresh data through live evaluation (daily batch or real-time)

Value for the business

Old frauds detected faster

New frauds detected through systematic investigation

New frauds detected through new fraud schemes detection (e.g. through dual

scoring with network analysis)

Financial KPIs

Increase in Gross Savings Rate (difference between the total financial value of the

compensation due under the contract if the fraud would not have been evidenced and

the amount really paid)

Decrease in Investigation Costs

Operational Impacts

Reliability on fraud savings tracking through automated reporting

Faster claims triage and more investigation insights

Optimization and adaptation of business processes

Reactivity of claim handlers and investigators on assignment and processing

Fraud awareness may indirectly improve manual detection rates

KPIs importance

33 | SMART DATA AND DATA INNOVATION LAB

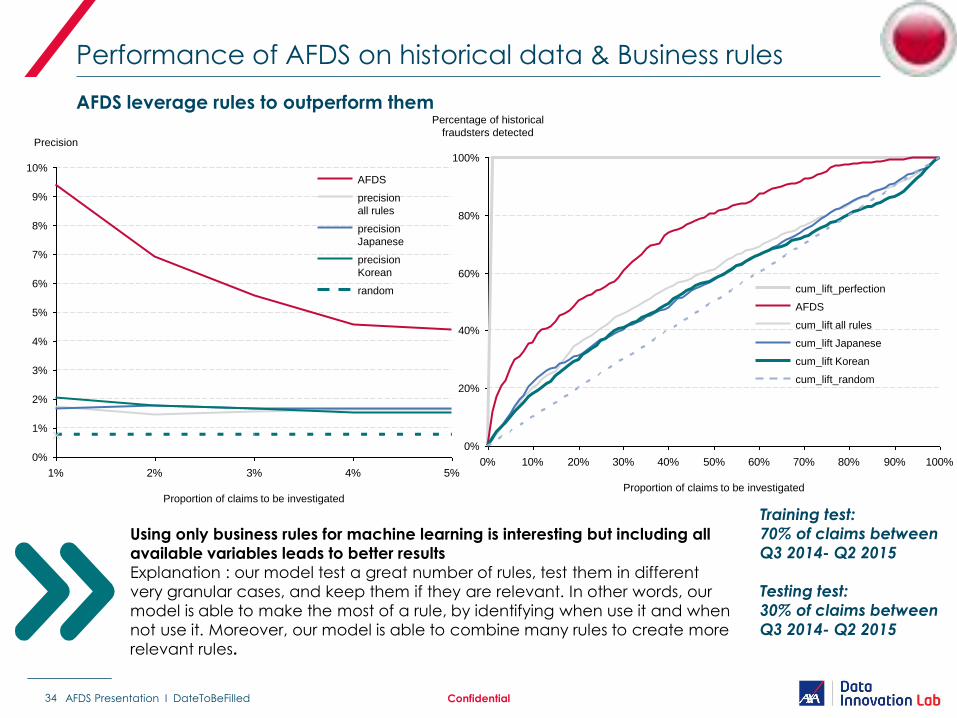

34

Performance of AFDS on historical data & Business rules

Training test:

70% of claims between

Q3 2014- Q2 2015

Testing test:

30% of claims between

Q3 2014- Q2 2015

AFDS leverage rules to outperform them

1% 2% 3% 4% 5%

1%

2%

0%

8%

7%

6%

4%

3%

10%

9%

5%

Precision

Proportion of claims to be investigated

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

100%

80%

60%

40%

20%

0%

Percentage of historical

fraudsters detected

Proportion of claims to be investigated

random

precision

Korean

precision

Japanese

precision

all rules

AFDS

Using only business rules for machine learning is interesting but including all

available variables leads to better results

Explanation : our model test a great number of rules, test them in different

very granular cases, and keep them if they are relevant. In other words, our

model is able to make the most of a rule, by identifying when use it and when

not use it. Moreover, our model is able to combine many rules to create more

relevant rules.

cum_lift Korean

cum_lift_random

cum_lift all rules

cum_lift Japanese

AFDS

cum_lift_perfection

Confidential AFDS Presentation I DateToBeFilled

35 | SMART DATA AND DATA INNOVATION LAB

New Detection Techniques Discover New

Fraud Schemes

36 | SMART DATA AND DATA INNOVATION LAB

Conclusion

• Fraud is estimated to be a substantial source of savings

• Yet entities could improve their fraud detection rate:

• traditional methods generate too many false positives (technical challenge)

• fraud schemes are diverse and changing (organizational challenge)

• We think we can alleviate theses problems because:

• Our technical solution can be adapted by data scientists to local data environments and thus be specific enough to provide good results

• Yet our solution is generic enough to be deployed widely and help mutualize fraud experience across the group

How to really become data driven?

37 | SMART DATA AND DATA INNOVATION LAB

Key challenges to really change the business