b821 block4unit9 credit liquidity and operational risk

TRANSCRIPT

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 1/112

B821 Financial Strategy Block 4 Financial Risk Management

Unit 9 Credit, Liquidity and Operational Risk Prepared by the Course Team

Masters

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 2/112

This publication forms part of an Open University course B821, Financial Strategy. Details of this and other Open University courses can be obtained from the Student Registration and Enquiry Service, The Open University, PO Box 625, Milton Keynes, MK7 6YG, United Kingdom: tel. +44 (0)1908 653231, email [email protected] Alternatively, you may visit the Open University website at http://www.open.ac.uk where you can learn more about the wide range of courses and packs offered at all levels by The Open University. To purchase a selection of Open University course materials visit http://www.ouw.co.uk, or contact Open University Worldwide, Michael Young Building, Walton Hall, Milton Keynes MK7 6AA, United Kingdom for a brochure. tel. +44 (0)1908 858785; fax +44 (0)1908 858787; email [email protected]

The Open University Walton Hall, Milton Keynes MK7 6AA First published 1998. Second edition 1999. Third edition 2000. Fourth edition 2003. Fifth edition 2006. Reprinted 2007 Copyright # 1998, 1999, 2000, 2003, 2006, 2007 The Open University All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, transmitted or utilised in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without written permission from the publisher or a licence from the Copyright Licensing Agency Ltd. Details of such licences (for reprographic reproduction) may be obtained from the Copyright Licensing Agency Ltd of 90 Tottenham Court Road, London W1T 4LP. Open University course materials may also be made available in electronic formats for use by students of the University. All rights, including copyright and related rights and database rights, in electronic course materials and their contents are owned by or licensed to The Open University, or otherwise used by The Open University as permitted by applicable law. In using electronic course materials and their contents you agree that your use will be solely for the purposes of following an Open University course of study or otherwise as licensed by The Open University or its assigns. Except as permitted above you undertake not to copy, store in any medium (including electronic storage or use in a website), distribute, transmit or retransmit, broadcast, modify or show in public such electronic materials in whole or in part without the prior written consent of The Open University or in accordance with the Copyright, Designs and Patents Act 1988. Edited and designed by The Open University. Typeset in India by Alden Prepress Services, Chennai. Printed and bound in the United Kingdom by Hobbs the Printers Limited, Brunel Road, Totton, Hampshire SO40 3WX. ISBN 0 7492 1324 8 5.4

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 3/112

C O N T E N T S 1 Introduction 52 Credit risk 11

2.1 Introduction 112.2 How big is your exposure? 112.3 How big is your derivatives exposure? 152.4 Settlement risk: what is your exposure on maturity ? 192.5 Summary 21

3 Credit lines 233.1 Introduction 233.2 Getting the credit-rating agencies to do the work 243.3 Basic methods of credit analysis 293.4 More advanced methods of credit analysis 313.5 Turning the analysis into credit lines 353.6 Summary 39

4 Credit-risk management 414.1 Introduction 414.2 Factoring 424.3 Letters of credit and letters of guarantee 424.4 Security against credit exposures 464.5 Credit derivatives 484.6 Summary 54

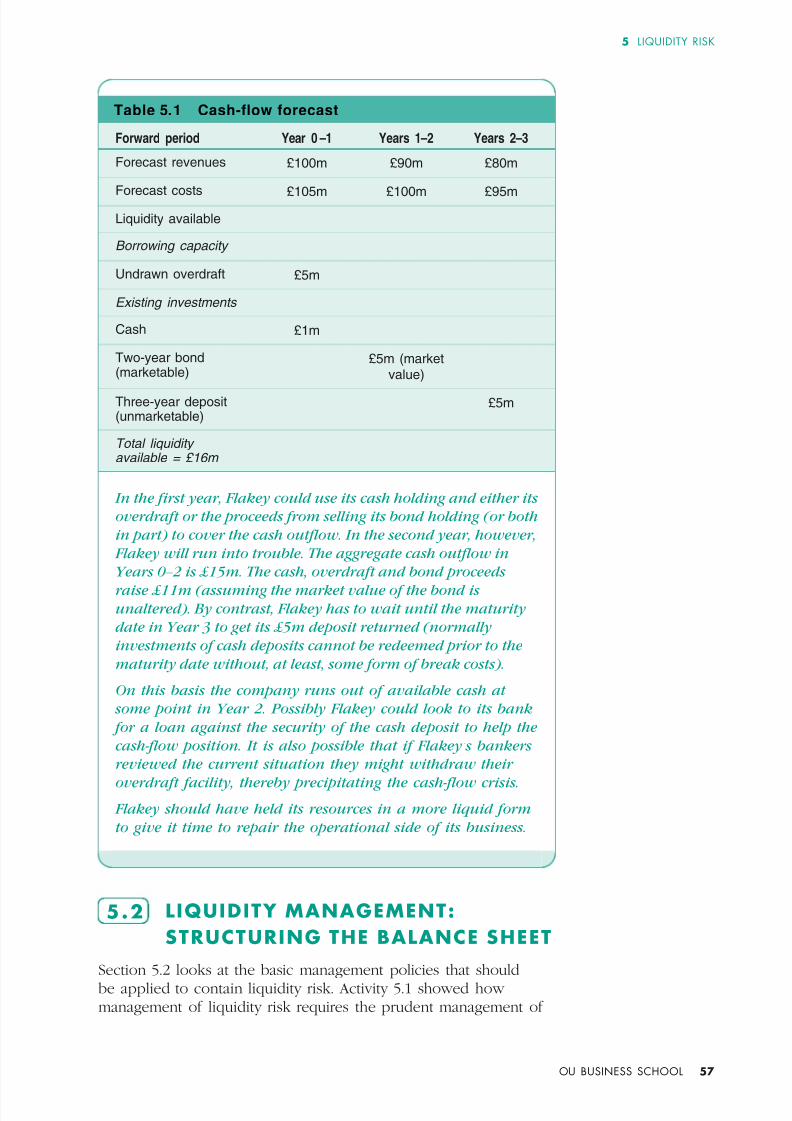

5 Liquidity risk 555.1 Introduction 555.2 Liquidity management: structuring the balance sheet 575.3 Liquidity management: stress testing 625.4 Summary 64

6 Operational risk 656.1 Introduction 656.2 Operational-risk management 686.3 Summary 73

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 4/112

7 Financial-risk management: from theory to practice 757.1 Introduction 757.2 A risk-management template 767.3 Company risk-management policies 807.4 Changing disclosures 867.5 Summary 86

8 Summary and conclusions 89 Answers to exercises 91 Appendix 1 Standard and Poor’s credit ratings 98 Appendix 2 Repo and securitisation: furtheranalysis 102References and further reading 107 Acknowledgements 108

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 5/112

1 I N TR OD U C TI ON 1 INTRODUCTION

Take a deep breath and relax! Having learnt about interestrate risk, foreignexchange risk and contingent risk and the methods for managing them we now turn to those financial risks where the analysis and methodology are technically less onerous. That is not to say that the risks are less critical – far from it. Failure to control credit exposure and liquidity levels and the existence of flawed operational controls often spell more than a financial headache. Rather, they can rapidly lead to the demise of an organisation. The work done in Units 7 and 8 will prove to be helpful in studying the subjects in Unit 9, particularly in appreciating the additional complications arising from the interplay between credit, interest and foreignexchange (FX) risks. This unit starts with an analysis of credit risk . Virtually all organisations, whether private or publicsector based, are exposed to credit risk. Once an organisation extends ‘trade terms’ to its suppliers it is faced with the risk that the sums due are not paid or are paid after the time they are due. Financial

organisations

such

as

banks,

investment

funds

and

venturecapital companies are, by the nature of their business, continually exposing themselves to credit risk. Understandably, they therefore commit substantial resources to acquire the information and skills needed to manage this risk soundly. Nonfinancial organisations also need to be alive to credit issues. The majority of companies and publicsector organisations, such as local authorities and charities, have surplus cash – at least periodically – and expose themselves to credit risk when they lend or deposit these funds with banks and other organisations.

Additionally, the cost of funds for all organisations is determined in part by the general credit conditions in the economy and particularly by investors’ perception of the sector of the economy

within which those borrowing operate. There are plenty of recent examples of soundly run companies finding the cost of their funds increasing because investors’ sentiment towards the sector in

which they operate changed adversely. This was the experience in telecommunications sector in 2000 – 2001 and in the automobile sector more recently. An understanding of credit risk is therefore essential for an organisation even if it is not an investor itself.

OU BUSINESS SCHOOL 5

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 6/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

The section on credit risk explores the following areas. l How the exact extent of credit exposure should be

measured – including the credit exposure arising from derivatives transactions.

l The techniques used by organisations to make decisions about credit

exposure,

including

the

use

of

the

information

and

ratings

supplied by the large creditrating agencies such as Moody ’s, Standard and Poor’s and Fitch.

l The methods that companies can use to contain credit exposure, such as factoring and obtaining security against exposures.

l The facilities that can be used to manage credit risk by those companies engaged in international trade.

l How the emergence of the creditderivatives market in the past decade has given organisations a new set of tools for managing credit risk.

In recent years the credit ‘industry ’ has increased significantly in size. This increase can largely be attributed to the growing realisation of the consequences of poor credit management. The huge losses incurred by United Kingdom’s mortgage lenders in the early 1990s, by investors in Asia and Russia in the mid1990s and by equity investors during the ‘dot.com bubble’ in the late 1990s clearly demonstrated the cost of not doing thorough credit analysis before lending to individuals, organisations, banks and even governments.

BOX 1.1

RUSSIA DEFAULTS AND THE CONSEQUENCES SPREAD FAR AND WIDE

In August 1998 the Russian government defaulted on its debt, triggering panic in the world’s financial markets.

OU BUSINESS SCHOOL 6

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 7/112

1 INTRODUCTION

The problems faced by Russia in 1998 were both political and economic. Repeated changes in the Russian government, instigated by President Yeltsin, had already started to unnerve investors and put pressure on Russia’s currency, the rouble. Further problems arose from the sharp fall in oil prices in 1998, since oil is a major source of export earnings for Russia. IMF assistance was forthcoming with a $22.6 billion package of support that was announced in July 1998. This support, however, was largely diverted to attempts by the Russian government to support the value of the rouble. When a request for further support from the IMF was declined and with official reserves reducing by $1 billion a week, the Russian government was given little option in the end but to devalue the currency and freeze repayments of debt. The obvious losers from this development were investors in Russian debt, predominantly the major international banks. Their credit losses were substantial, but the consequences went further. The Russian default – coming so soon after the economic crises experienced in many Asian countries in the mid1990s – prompted a fall in share prices around the world. Given that so many of us are investors in equity markets – if not directly through our own investment portfolios, then indirectly through the investments made by the pension funds of which we are members – the consequences of the Russian default were wider and the number of people who lost out as a result of this credit event were more numerous than is commonly believed.

The unit then examines liquidity risk – the risk that an organisation cannot meet its payment obligations. There is obviously a link here

with credit risk, since one organisation’s liquidity crisis is potentially a source of a credit crisis for those who have invested money in it or are simply owed for supplies to it. The section on liquidity risk will: l examine the circumstances under which liquidity problems

arise; l explain how organisations can arrange their balance

sheets – particularly through the structuring of assets and liabilities – to maintain liquidity at acceptable levels.

The unit then assesses operational risk – the risk to an organisation arising from the failure of people, systems and controls. It could be argued that operational risk alone is not really a risk at all, since if systems and controls do fail it does not necessarily mean that an organisation loses money. For example, if a failure of controls results in Company A lending money to Company B beyond the credit limit imposed by its credit department there is no financial loss until Company B fails to meet its repayment obligations. So although there has been a control failure, no money has actually

OU BUSINESS SCHOOL 7

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 8/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

been lost. The fact is, though, that the source of losses in respectof all the financial risks we study in this block can very often betraced to operational failures: if the controls had been robust, theactivities which generated the losses would not have beenundertaken.The

section

on

operational

risk

will:

l review the potential areas of operational risk for an

organisation; l explain the procedures that can be introduced to manage these

risks. Having concluded our analysis of the individual categories of financial risk and the interrelationships between them, we then look at how all these risks may be brought under collective control. In doing this we return to the subject of ‘risk mapping’, which we studied at the start of this block. We will devise is a summary report, structured to facilitate the control of risk, where information is presented in a concise and coherent way to enable management and board decisions to be made in an effective manner. Finally, the unit and the block conclude with a review of the policies and practices for managing financial risk employed by some major companies. The examples given demonstrate that the subject matter covered in Block 4 is well and truly embedded in

what goes on in the real world. Indeed, the critical importance of the issues we have covered can be readily gleaned simply by looking at the advertisements for jobs that appear in The Financial Times

. The

salaries

now

being

paid

for

credit

analysts

and

risk

managers show only too clearly how seriously organisations take risk management. So by reading on, perhaps the Open University can help to provide you with a stepping stone to those large salaries!

BOX 1.2 THE OPEN UNIVERSITY IS ‘ON RISK’ As you read through the introduction you may be forming the view that the financial risks to be studied in this unit are really only relevant to banks and other financial institutions. Think again! Take an organisation such as the Open University – an educational organisation in the public sector. It, too, is exposed to all the risks examined in this unit and, indeed, the other units in Block 4. The Open University has surplus funds that it invests via the United Kingdom’s money market. It therefore exposes itself to credit risk through such lending. The business activities of the Open University generate sizeable cash flows. If the income streams weaken and/or costs rise, the

OU BUSINESS SCHOOL 8

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 9/112

1 INTRODUCTION

Open University would be faced with liquidity problems like any other business in similar circumstances. The Open University is heavily reliant on systems. If the FirstClass system failed for a prolonged period, the Open University could not deliver key elements of its educational services. News of such an operational failure would have an impact on the ability to retain students and to attract new ones, adversely affecting the Open University’s business. Apply the same analysis to organisations you have worked for and you will soon see how pervasive these risks are.

Learning outcomes By the end of this unit you should be able to: l understand how credit risk is measured and how credit lines

may be determined; l understand the techniques and instruments available to manage

credit exposures; l recognise how liquidity risk arises and how balancesheet

management can help to maintain adequate liquid resources for an organisation;

l understand the forms of operational risk and how this risk can be mitigated;

l devise a riskmeasurement control matrix that could be used by senior management and the board of a company to oversee the management of financial risks;

l analyse the features of the riskmanagement policies of some major organisations.

����������������������������������������

OU BUSINESS SCHOOL 9

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 10/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

10 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 11/112

2 CREDIT RISK

2 C R ED I T R I SK

2 . 1 I N T R O D UC T I O N

The purpose of this section is to:l explain how credit exposure can be measured;l understand the potential interrelationship between credit and

other financial risks (like interestrate risk and foreignexchange risk);

l demonstrate

how

the

credit

exposure

arising

from

derivative

transactions can be measured;

l examine the form of credit exposure known as ‘settlement risk’.

The work on credit risk in this unit builds on the analysis of credit issues you were introduced to in Unit 3.

2 . 2 HOW BI G I S YOU R E X P O S UR E ? If you lend money to an organisation or simply extend trade terms for payment for supplies (typically thirty to sixty days) you immediately have credit exposure to the organisation or supplier. How big is your exposure? This may seem like an odd question. If you lend £1m, your exposure is surely £1m? If you extend trade credit for thirty days to a purchaser for goods valued at E100,000, you are surely only exposed to a maximum of E100,000 if the purchaser defaults?

Well not quite right in fact. A number of additional factors need to be taken into account to measure both the financial risks involved and your true overall exposure. Interest accruals If you have lent money to an organisation on which interest is paid, your exposure rises until the interest payment is due. At an annual rate of 5% p.a. on a longterm loan of £1m, the exposure rises to £1.05m on the date of payment of the annual interest, falling back again to £1m if interest is paid as due on that date. Effective creditexposure measurement requires interest due to be added to principal sums outstanding. This is a major issue for investments in zerocoupon bonds where all the cash value of the return owed to the investor comes on the maturity date. Zerocoupon bonds were

discussed in Unit 7.

OU BUSINESS SCHOOL 11

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 12/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

Market valuations What if market rates of interest move after you lend money to another organisation? We know from the work undertaken on bond pricing in Unit 7 that if interest rates move, the present value of all future cash flows changes and this alters the market value of an investment. The impact on value is more significant the longer the duration of the investment. This makes longterm, fixedrate investments, for example, in bonds, particularly at risk of changes in valuation. If your credit exposure arises through investing in a fixedrate bond issued by an organisation and interest rates fall after the purchase date, the market value of your bond holding will therefore be higher than the amount you paid. Consequently, your credit exposure to the bond issuer is greater as a consequence. If this exposure exceeds the size of the credit limit or credit ‘line’ (the total amount you are prepared to invest in the organisation) you face an awkward decision. Either you would have to reduce the size of your investment so that your exposure does not exceed the credit line or apply to your credit department for an increased credit line in respect of the bond issuer. The latter may be the more attractive option since otherwise you would be a forced seller of a profitable investment. Time value or opportunity cost

What about the time value of the credit you have extended? If you extend trade credit of E100,000 to an organisation for thirty days,

you have implicitly provided an interestfree loan to that organisation for the thirty days. This is effectively an additional cost to you for allowing credit of E100,000 for thirty days. The extra cost is the money you would have received if you had been paid the E100,000 on day one and invested it for thirty days at the prevailing thirtyday interest rate. If you alter the term of your trade credit to, say, sixty days there is an implicit increased cost to you arising from your new limit for extended credit.

You will recall from Unit 7 that ‘FRA’ means ‘forward rate agreement’

EXERCISE 2.1 You are owed E1m by a customer. Contrary to your normal terms for business, you extend to this customer a credit term of four months rather than one month. The market is quoting 4.5% for the ‘one versus four ’ (1v4) FRA (that is, the three-month rate, one month forward). What is the cost to you of this three-month extended payment period? How could you have mitigated this cost when billing the customer?

12 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 13/112

2 CREDIT RISK

The ‘knock-on’ impact on interest-rate risk Think back to the coverage of ‘gap analysis’ in Unit 7. The sums owed to your organisation by debtors are future cash inflows.

When combined with all other cash flows, these generate the aggregate level of interestrate risk being taken by your organisation. If a customer who owes you £5m in one year’s time defaults, you no longer have that cash inflow forthcoming one year forward. This means that your gap position alters and with it the aggregate level of interestrate exposure. What started as a credit issue (the default by your customer) has now potentially become an issue of interestrate risk. The ‘knock-on’ impact on foreign-exchange risk

You will recall the matching approach to managing foreignexchange (FX) risk in Unit 8. The sums owed to you by a debtor may be entirely matched to amounts you owe in the same foreign currency to your creditors. While you are ‘matched’ in this way you have eliminated the exposure to FX risk in the currency in question. If your debtor defaults, however, an FX exposure is opened up – you still need to pay your creditors (unless you intend to default as well!). You are now exposed to the movement in exchange rate that has taken place between the point you used the sum owed by your debtor to match that of your creditors and the point you became aware of the default by your debtor. You can take action in the FX market now to renew your hedge against

your liabilities,

but

you

cannot

recoup

any

movement

in

the

FX rate that has already happened since you put the matching hedge in place.

Gap analysis was covered in Section 5 of Unit 7.

‘Matching’ methods for managing foreign

exchange exposure

were

covered in Unit 8.

BOX 2.1 HOW TO (NEARLY) LOSE MONEY TWICE OVER In February 1995, Barings, a United Kingdom merchant bank, went into liquidation following huge losses on its derivativestrading activities by its Singapore subsidiary. As one United Kingdom financial company assessed its exposure to Barings – and hence its potential credit losses through loans it had extended to the bank – a second dimension to its exposure became clear. The loans had been made in US dollars and these assets matched the financial company’s borrowings in US dollars from the US money market. So the loans to Barings were not only an asset, but also a hedge against movements in the USD/GBP exchange rate. With Barings in liquidation and with the prospect that the loans extended to them would not be repaid, this foreignexchange hedge

was

undone.

As

fate

would

have

it,

the

USD

had

appreciated against GBP since the loans were made to Barings, so putting new USD loans in place (by lending to other banks) was

OU BUSINESS SCHOOL 13

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 14/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

going to cost more in terms of GBP than the original loans. Consequently, the potential loss arising from the exposure to Barings was more than just the loans themselves and the accrued interest – there was also a foreignexchange related supplement. Fortunately for this and other financial institutions similarly exposed, the Dutch bank ING bought Barings (for £1) and honoured Barings’ senior debts. Consequently neither the credit nor foreignexchange losses materialised from its dealings with Barings ... but an interesting lesson in the wider nature of credit risk had been learnt.

These illustrations show that there is a difference between the original amount owed to an organisation by a borrower or trade debtor and the actual financial exposure that subsequently arises, particularly as market rates change. The latter incorporates the overall exposure to loss that arises if a debtor defaults and does not just focus on the credit extended at the outset. Some additional complications The problems identified above are compounded by the fact that

when a debtor defaults you do not know at that point how much you might recover and when that recovered sum will be paid to you.

As a creditor, you will have a claim on the assets of the organisation and the strength of that claim will depend upon your ranking as a creditor. Look at Figure 2.1. This simplistic but useful block diagram of the balance sheet shows you of where you may stand as a creditor – the higher up in the ‘liability ’ column you are, the better. The figure is drawn up in order of payment in the case of liquidation, which is rather different from the usual balancesheet ordering.

Secured lending is where Clearly, if your loan to the defaulting party was secured against a loan is contractually specific assets of the defaulting organisation you would hope to get linked to specific assets. If the borrower defaults back the money due to you by your claim to those secured assets. the lender can claim the If, on the other hand, you had an unsecured or a subordinated assets and sell them to recover the money owed. position in the creditor ranking you might get back only a small In a liquidation, proportion of the money you advanced. Not knowing how much subordinated debts are you might receive certainly complicates the calculation of your repaid only after actual financial exposure. unsubordinated debts have been repaid.

Summarising these points We shall come back to some of these issues later when we look at recent developments in the field of credit analysis. What we can say here, though, is that many organisations are developing more sophisticated means for setting credit limits, or ‘credit lines’, and for

14 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 15/112

2 CREDIT RISK

Currentassets

Assets

Fixedassets

�

Liabilities

�

Figure 2.1 The balance sheet ordered by creditor ranking measuring exposure against them. A more considered assessment of the financial value of credit exposures is being undertaken through: l the regular revaluation (or ‘marking to market’) of credit

exposures; l assessing, prior to establishing credit lines, the probability of

default (Pd) of an organisation; l calculating the loss that would arise on such a default – the loss

given default (Lgd). Such analysis is not only helping to answer the question of how much credit risk you have, but is also assisting organisations in pricing their lending properly. An organisation with a high Pd and Lgd should expect to pay more for borrowing funds or obtaining credit terms than one deemed to have a low Pd and Lgd.

Note that the term ‘recovery rate’ is also widely used when defining the proportion of an investment that is recovered from a defaulting entity. The recovery rate is (1 – Lgd).

HOW BI G I S YOU R D E R I V AT I V E S E X P O S UR E ?

2 . 3 Credit risk does not just arise from lending or providing trade credit. Activities in derivatives (for example in FRAs and swaps) give rise to credit risk. We shall now look at some guiding principles that need to be taken into account when measuring credit exposure arising from derivative transactions and some examples of measuring this exposure.

We already know from Unit 7, by contrast, that with exchange traded derivatives, such as futures, credit risk is virtually eliminated. The only (very minor) risk relates to daily movements in the

OU BUSINESS SCHOOL 15

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 16/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

The use of margin payments by clearing houses was explained in Box 6.3 in Unit 7. Note that if market movements are particularly volatile, exchanges may require margin payments more than once a day. These are known as ‘intraday’ margin calls.

A counterparty is simply a term to describe an organisation that is a party to a business transaction.

‘Notional principal’ is the nominal value used to calculate the cash flows on derivative transactions. It is not, itself, a cash flow.

market, which require a daily margin call in excess of the initial margin paid into the clearing house at the inception of a transaction. There is also the credit risk to the clearing house itself since, theoretically, it could go into liquidation. Virtually all users of the exchangetraded markets, however, view such a risk to be very small. Indeed, one of the clear attractions of exchange trading is the minimisation of credit risk.

With over-the-counter (OTC) instruments, however, risk arises from the movement in rates after the inception of a deal. Suppose, for example, Company X ceases trading immediately after it has arranged an interestrate swap with Bank Y. Provided swap rates have not moved, Bank Y can arrange a new identical interestrate swap with another organisation at the same rate prevailing in the market. By replacing its swap in this way no loss has been incurred by the default of Company X. The reality is, of course, that market rates do move and as a consequence derivative positions may give rise to credit losses if an organisation with which you have transacted defaults. To value the credit risk on derivative positions requires the assessment of their replacement cost. If the counterparty to a swap, FRA or foreignexchange transaction defaults, you are exposed to the difference between the ‘contract’ rate on the original derivative transaction and the prevailing market rate for the transaction. The financial cost of this difference may be either negative or positive. If the cost is negative, it means that you would not suffer a financial loss if your counterparty defaults – you could replace the derivative position at no financial loss. If the cost is positive, though, a default by your counterparty results in your incurring a financial loss. This cost is, therefore, the credit risk you have to the counterparty through a derivative position. To measure this cost requires the application of the netpresent-

value (NPV) techniques for valuing sets of cash flows with which you are now familiar – but with one important difference: the analysis does not need to include the notional principal sum of the derivative transaction since that is not a cash flow. You therefore measure the difference between the actual cash flows due under the original transaction and those due under a replacement transaction if the original counterparty defaults.

Activity 2.1 provides an example. ACTIVITY 2.1 VALUING THE CREDIT RISK ON A SWAP FNBK Bank enters into a five-year swap with Hope plc. Hope plc pays 7% p.a. annually to receive twelve-month GBP LIBOR on a notional principal of £100m. After exactly two years and immediately after the difference payment has been made at the end of Year 2, Hope plc ceases trading.

16 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 17/112

2 CREDIT RISK

The market rate for a three-year swap (the residual term) is now 4.5% p.a. annually against twelve-month LIBOR. What is FNBK Bank ’s exposure with this swap? For the sake of simplicity, assume the zero-rate to be applied to

all

the

cash

flows

is

4.5%

p.a.,

so

the

discount

factors

are

all

based on this rate. As the results in Table 2.1 show, the replacement swap gives FNBK 2.5% p.a. less than the original swap. The replacement cost is therefore 2.5% p.a. for the rest of the life of the swap. The NPV of these flows is £6.87m. Table 2.1 Result (at the end of Year 2) Year 3 Year 4 Year 5 Total Notional principal £100m £100m £100m Difference in fixed rates 2.5% 2.5% 2.5% Difference in variable rates#

0% 0% 0% Cash flow of differences 2.5% 2.5% 2.5% Replacement cost* £2.5m £2.5m £2.5m Discount factor at 4.5%{

0.957 0.916 0.876 NPV of cost £2.39m £2.29m £2.19m Total cost = Exposure £6.87m # There is no difference in the variable rates since the LIBOR on both contracts (twelve-month LIBOR) are matched. * The replacement cost is the sum needed to compensate for negative cash flows. { Note that after two years the remaining years (Years 3, 4 and 5 of the original swap transaction) are, respectively, one, two and three years forward. Consequently, the discount factors reflect these forward periods.

The ‘zerorate’ is the interest rate applying to a specific single cash flow on a defined date. See Box 3.3 in Unit 7.

Even before the demise of Hope plc, FNBK Bank’s credit department should have been regularly revaluing (‘marking to market’) the swap at prevailing market rates. At the point of Hope’s demise the exposure is £6.87m. This may not, of course, be the final loss. Even as an unsecured creditor, FNBK would have a claim on Hope plc and might retrieve some value at an unknown future date. Indeed, FNBK Bank may have an alternative route to recover funds. Depending on the terms of the swap contract entered into by the two parties, FNBK bank may under this ‘event of default’ be able to ‘net off ’ the loss on this The term ‘set off’ is often individual transaction (where the replacement cost is positive) used in the financial

markets when describing against other deals with Hope plc where the replacement cost is netting arrangements. So negative. ‘

set off

’ is

effectively

the

same as ‘net off’.

OU BUSINESS SCHOOL 17

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 18/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

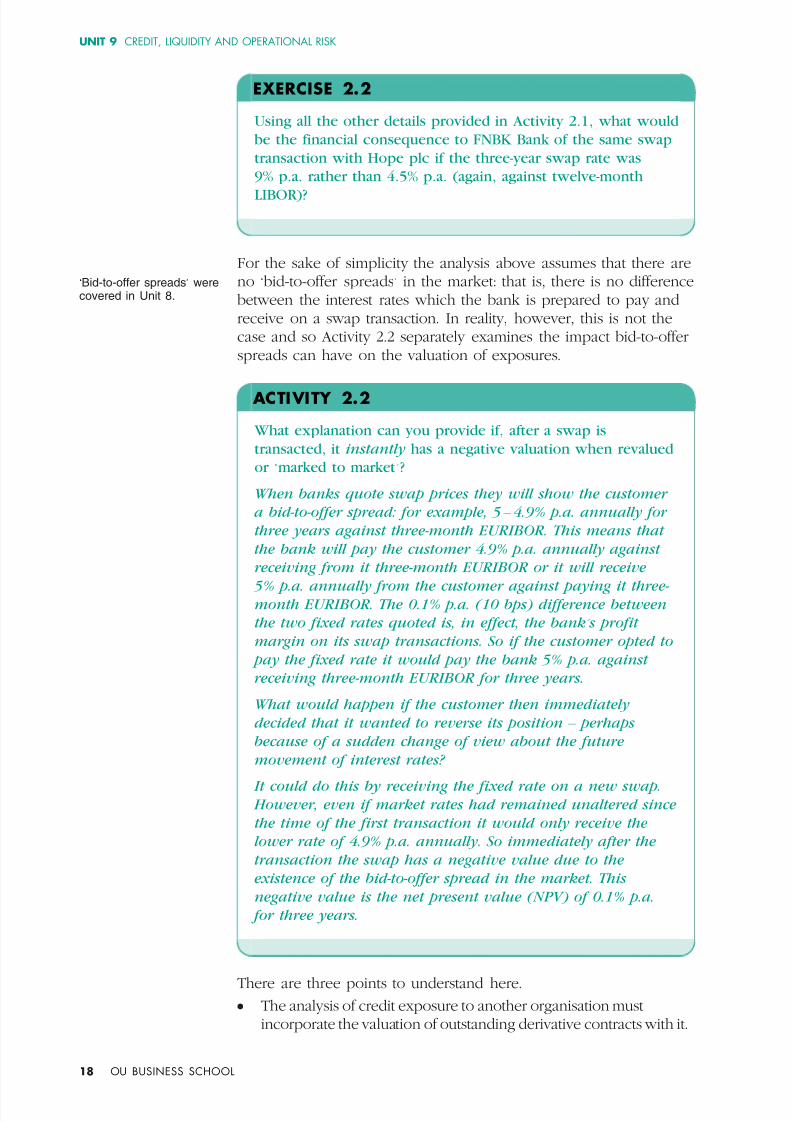

EXERCISE 2.2 Using all the other details provided in Activity 2.1, what would be the financial consequence to FNBK Bank of the same swap transaction with Hope plc if the three-year swap rate was 9% p.a. rather than 4.5% p.a. (again, against twelve-month LIBOR)?

‘Bidtooffer spreads’ were covered in Unit 8.

For the sake of simplicity the analysis above assumes that there are no ‘bidtooffer spreads’ in the market: that is, there is no difference between the interest rates which the bank is prepared to pay and receive on a swap transaction. In reality, however, this is not the case and so Activity 2.2 separately examines the impact bidtooffer spreads can have on the valuation of exposures.

ACTIVITY 2.2 What explanation can you provide if, after a swap is transacted, it instantly has a negative valuation when revalued or ‘marked to market’? When banks quote swap prices they will show the customer a bid-to-offer spread: for example, 5 – 4.9% p.a. annually for three years against three-month EURIBOR. This means that the bank will pay the customer 4.9% p.a. annually against receiving from it three-month EURIBOR or it will receive 5% p.a. annually from the customer against paying it three- month EURIBOR. The 0.1% p.a. (10 bps) difference between the two fixed rates quoted is, in effect, the bank’ s profit margin on its swap transactions. So if the customer opted to pay the fixed rate it would pay the bank 5% p.a. against receiving three-month EURIBOR for three years. What would happen if the customer then immediately decided that it wanted to reverse its position – perhaps because of a sudden change of view about the future movement of interest rates? It could do this by receiving the fixed rate on a new swap. However, even if market rates had remained unaltered since the time of the first transaction it would only receive the lower rate of 4.9% p.a. annually. So immediately after the transaction the swap has a negative value due to the existence of the bid-to-offer spread in the market. This negative value is the net present value (NPV) of 0.1% p.a. for three years.

There are three points to understand here. l The analysis of credit exposure to another organisation must

incorporate the valuation of outstanding derivative contracts with it. 18 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 19/112

2 CREDIT RISK

l Derivative positions (unlike assets such as bonds) can have a positive or negative or zero value depending on how market rates have moved since the deals were struck.

l When valuing a derivative, do not include the notional principal sums involved in transactions since these are not cash flows. Only include actual cash flows.

S E T T L E M E N T R I S K : WH AT IS Y OUR E X P O S UR E ON M AT UR I T Y ?

2 . 4 We have looked at how the economic value of the money owed to you by debtors (be it in the form of trade credit or lending) can be measured. We have also examined the credit exposures arising from the use of derivatives. Do these provide a complete measure of the credit exposures arising from business activities? The answer is, ‘

Not quite’!

There is one particular facet of credit risk known as settlement risk . This relates to differences in the timings at which money owed by one organisation to another is paid, or ‘settled’. For example, Company A may consider it has no net credit exposure to Company B since the sums owed from each to the other match, both contractually and in terms of the settlement date. What happens, however, if Company A settles its debts to Company B only to find that Company B goes into liquidation prior to completing its payments to Company A on that same day? This may sound a little far

fetched,

but

it

is

not.

If

companies

cease

trading

they

do

so

at

a

precise point. At that point the company stops making any payments even if they are related to inflows received minutes earlier. This risk principally arises through foreignexchange transactions that result in payments being made and received in different time zones – for example, paying Japanese Yen into an account in Tokyo set against an equivalent sum to be received in US dollars – but in an account in New York. The time difference of fifteen hours could prove costly to the company receiving the US dollars if the company due to pay them ceases trading that day prior to New York opening for business, but after Tokyo has received the Yen.

BOX 2.2 HORRIBLE HERSTATT Banks have always had what they call ‘settlement limits’ for customers and other banks. This is supposed to put a ceiling on how much they will pay to a counterparty on any particular day. Until the 1970s, however, such limits were often treated with scant respect,

especially

for

foreignexchange

trading.

After

all,

by

definition, an exchange involves handing over and receiving equal value in two currencies, so where could there be a risk?

OU BUSINESS SCHOOL 19

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 20/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

The Herstatt collapse showed rather vividly where the risk comes from. Herstatt was a German bank that ran into trouble and eventually collapsed. Up to the day of disaster its foreignexchange dealers had bought large quantities of deutschmarks (DEM) for US dollars (USD). On the final day the counterparties happily paid over their DEM – but the bank ceased trading in the afternoon which, given the time differential between Frankfurt and New York, was after the bank had received the DEM, but before it had instructed its New York agent to pay the equivalent USD. Oh, how they howled! The counterparty banks tried to claim that the DEM payments were inextricably linked to the USD receipts and so should be repaid. ‘Not so’ said the courts, and the banks were regarded as the same as all other unsecured creditors. They eventually received a few cents on each dollar. Since then settlement risk has been taken seriously.

Recent developments – including the emergence of a system called continuous linked settlement (CLS) – have helped banks to mitigate settlement risk by ensuring that payments truly match in terms of the time of their settlement. Settlement risk is, though, still an issue for many organisations and requires considered management.

BOX 2.3 CONTINUOUS LINKED SETTLEMENT Continuous linked settlement, or CLS, is a realtime system that enables the simultaneous settlement of cash flows globally, irrespective of time zones. It is an ongoing process of: – submitting instructions, where the system receives instructions

for payments of specified currencies from its customers; – funding, where the system settles ‘pairs’ of instructions; – execution, where the system makes payouts in specified

currencies. Settlement is final and irrevocable. Participating banks get realtime settlement information that helps them to manage liquidity more efficiently, reduce credit risks and introduce operational efficiencies. This is all done within a fivehour window (three hours in the Asia Pacific zone) which represents the overlapping business hours of the participating settlement systems. Sourced: www.clsgroup.com (accessed 5/9/05)

20 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 21/112

S UM M AR Y 2 . 5 This section has identified the ways in which credit risk arises and the factors that have to be taken into account to measure it properly. Already you may have appreciated that the nuances involved help to warrant the high salaries paid to the best credit analysts – indeed, even the examples used in this section are only modestly complex when compared with the credit exposure arising from investing in the more convoluted financial products.

We now need to look at the process for managing and containing the exposure to credit risk. In short, an organisation can do two things: l Firstly, it should establish a process for determining the size and

characteristics of a credit line for each counterparty with which it wishes to do business. We look at this process in Section 3.

l Secondly, it can employ various methods to mitigate credit exposure. In Section 4 we shall look at a variety of methods that can reduce the exposure to financial loss in the event of default by a counterparty.

����������������������������������������

2 CREDIT RISK

OU BUSINESS SCHOOL 21

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 22/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

22 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 23/112

3 C R ED I T LI N ES 3 CREDIT LINES

I N T R O D UC T I O N3 . 1 In Section 2 we studied the factors that organisations have to take into account in measuring their credit exposure. This section examines the methods that can be employed to determine the size of credit lines.

A credit line is set as the maximum financial exposure an organisation is prepared to allow a counterparty, be they a customer or a borrower. There are a variety of approaches that can be employed to assist in the assessment of the credit standing of counterparties and in the determination of the size of a credit line for them. These approaches may be summarised as follows. l Using the ratings supplied by the creditrating agencies such as

Standard and Poor’s. l Doing analysis using basic methods of credit analysis, including

an analysis of financial ratios. l Undertaking detailed credit research on each potential debtor. These three approaches are not mutually exclusive. Many credit analysts use all three categories of information when fixing the size of their organisation’s credit lines. In addition, the ratings agencies themselves will use ratio analysis to help in their determination of their ratings. For some companies with no published ratings – which is usually the case if a company does not raise funds by issuing securities – there is little else to work on other than the core financial indicators when determining the size of the credit line. By contrast, if credit ratings are available, the credit department may base their credit work entirely on the findings of the agencies and relate the size of credit lines to the quality of the ratings. This, however, has some risks since the assessments of the agencies are not infallible. The most sophisticated credit departments conduct their own detailed analysis of each company and may only use the agency ratings to cross check their own findings.

Whatever method is used, there is no definitive or mathematical link from a credit assessment to an optimum size for a credit line. The process of determining the size of a credit line is subjective. The process may also involve negotiations between the lender and the borrower. As with the other financial risks we have been looking at in this block, the extent of the credit risks taken will also

We looked at how financial ratios can be used to gain an understanding of a customer ’s credit standing in Unit 3.

OU BUSINESS SCHOOL 23

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 24/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

depend on both the capacity and the appetite for risk of the organisation extending credit. Let us look in a little more detail at the three approaches listed above.

G E T T I N G TH E C R E D I T - R AT I N G A GE NC I E S T O D O T H E WOR K 3 . 2

Credit ratings and the role of the creditrating agencies were introduced in Unit 3.

The majority of large investors will, to some extent, use the major creditrating agencies to help to determine their credit lines. The three largest and most influential agencies in the world currently are Standard and Poor’s (S&P), Moody ’s and Fitch (formerly Fitch IBCA). There are also a number of smaller agencies in various parts of the world that either have a geographic bias (for example, CRISIL in India) or concentrate on smaller companies (for example, Dun and Bradsheet).

BOX 3.1 INTERNATIONAL CREDIT-RATING AGENCIES Three creditrating agencies are recognised worldwide: Standard and Poor ’s, Moody’s Investor Service, Fitch Ratings. Standard and Poor’s (S&P) was established in 1860 by Henry Varnum Poor. The agency’s founding principle was ‘the investor has the right to know’. Moody’s Investor Service was established in New York by John Moody in 1900. Fitch Ratings was founded as the Fitch Publishing Company in 1913 by John Knowles Fitch in New York City and was initially a publisher of financial statistics whose consumers included the New York Stock Exchange.

Shortterm debt is defined as debt that, at the time of issuance, has a maturity of no more than one year.

Each of these agencies provides ratings for issuers of longterm and shortterm debt. In fact, bond issuers will normally have to secure a rating to enable them to be able to issue their bonds in the

world’s financial markets. Table 3.1 provides a summary of the longterm ratings employed by Moody ’s and by Standard and Poor’s. A fuller breakdown and description of the Standard and Poor’s ratings are provided in

Appendix 1. The higher the ratings of an organisation the lower the assessed credit risk of investing in it. A higher rating will, therefore, mean that it should be cheaper for the organisation to raise funds and the greater should be its access to credit lines. There is not, though, a perfect correlation between ratings and the size of credit lines. For example, some organisations are highly

Note that ratings agencies provide credit ratings in respect of both the organisation and the debt issues of the organisation.

24 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 25/112

’ ’

3 CREDIT LINES

rated, but may have little need to borrow money. In these circumstances investors may not establish large credit lines for such organisations since they would be unlikely to be well utilised. Table 3.1 Summary of long-term credit ratings for Moody s and for Standard and Poor s

Moody’s Standard & Poor’s

Highest quality Aaa AAA Investment grade

High quality Aa AA Upper medium A A Medium Baa BBB Speculative Ba BB Noninvestment

grade Highly speculative B, Caa B, CCC, CC Default Ca, C D Source: http://personal.fidelity.com (accessed 5 September 2005)

The details in Table 3.1 show a division between what is categorised as investment grade and noninvestment grade ratings. ‘Noninvestment grade’ is also termed ‘speculative’ or ‘junk’. The division between investment grade and noninvestment grade is a critical one. Many institutional investment funds do not hold noninvestment grade assets. So if an organisation’s credit rating falls even one level below investment grade many funds are forced to sell the bonds issued by it. This inevitably puts downward pressure on the market price of these bonds. Once credit ratings are established, can they be altered? The answer is most definitely, ‘ Yes’. The financial performance of credit rated organisations is regularly reviewed and each year a number

will

find

themselves

‘up

rated

’ or

‘down

rated

’. These

movements in ratings are normally signalled ahead of the event by the agencies announcing to the markets that the organisation is under ‘review ’ or on ‘credit watch’ for a possible ratings move. These moves reflect the agencies’ assessment of changes in both the specific performance and financial strength of the organisation and the general business climate for the sector in question. For the organisations that find themselves down rated the consequences can be significant, with funding costs rising. This is virtually inevitable as investors in the organisation seek recompense for the greater credit risk they are now taking. This power over debt issuers leads at times to confrontations between an agency that has cut a rating and the affected

Company pension funds are an example of institutional investment funds.

OU BUSINESS SCHOOL 25

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 26/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

organisation which disputes the rationale for the move. It has been argued that the agencies are always more ready to cut ratings if performance weakens than to raise them when performance improves.

Note that it is the issuers of debt instruments (such as bonds) that approach – and pay – the agencies for their credit ratings, not the investors .

ACTIVITY 3.1 AGENCY INFLUENCE Read the case studies in the Course Reader entitled ‘ Journey to junk ’ by Jenny Wiggins about General Motors (originally published in The Financial Times ) and ‘ Who rates the raters’ (originally published in The Economist ). The articles tell you a considerable amount about the influence of the rating agencies and identify the impact of the substantial reduction in the quality of its credit ratings on General Motors’ cost of funds. Later, in 2005, Standard and Poor ’s reduced General Motors’ long-term rating to ‘ junk ’ status (BB+, the highest rating for a non-investment grade bond). By contrast, Moody ’s reduced General Motors’ long-term rating to Baa3, one level higher, since this is their lowest rating for an investment grade bond. Having read the articles, what do you think led to the rapid decline in General Motor ’s credit ratings?

Adverse movements in ratings can sometimes occur over a very short time scale. Even organisations once rated AAA have slipped down the ratings table and gone into default – although the incidence of this happening is very small. Certainly many singleA organisations have taken this route. Table 3.2 shows the average ‘transition rates’ over oneyear periods between 1981 and 2004 compiled by Standard and Poor’s. These rates show the historic average outturn of ratings at the end of each oneyear period given a particular rating at the start of the year. The table also shows the incidence of default by the rated organisations. For example, an average of 0.06% of organisations rated AA at the start of a year finished with a noninvestment grade rating of BB. The average default rate within the same period of time was only 0.01%. Unsurprisingly, the incidence of default increases the lower the original rating. For example, the average default rate for organisations originally rated B amounted to 5.71%. Note, though, that some ratings do rise. For example, over a oneyear period an average of 0.05% of A rated companies ended the year at AAA. So beware, an investment originally made in a strongly rated organisation can go wrong and lose you money. Clearly the longer the term of your investment the greater the risk of such an adverse move in credit status – a factor that contributes to the cost of borrowing rising the longer the term to maturity.

26 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 27/112

–

3 CREDIT LINES

Table 3.2 Global average one-year transition rates (%) 1981 2004 From/To AAA AA A BBB BB B CCC/C D N.R.* AAA 87.44 7.37 0.46 0.09 0.06 0.00 0.00 0.00 4.59 AA 0.60 86.65 7.78 0.58 0.06 0.11 0.02 0.01 4.21 A 0.05 2.05 86.96 5.50 0.43 0.16 0.03 0.04 4.79 BBB 0.02 0.21 3.85 84.13 4.39 0.77 0.19 0.29 6.14 BB 0.04 0.08 0.33 5.27 75.73 7.36 0.94 1.20 9.06 B 0.00 0.07 0.20 0.28 5.21 72.95 4.23 5.71 11.36 CCC/C 0.08 0.00 0.31 0.39 1.31 9.74 46.83 28.83 12.52 * N.R. means ‘not rated’ at the end of the year – for example, due to the maturity during the year of the bond issues by the organisation that had previously been rated. Source: http://www2.standardandpoors.com/spf/pdf/fixedincome/DefaultUpdate2005Q1.pdf (accessed 1/11/05)

BOX 3.3 JAPANESE BANKS: TUMBLING FROM THE AAA HEIGHTS In the 1980s the largest banks in the world, when measured by size of assets, were Japanese. These banks also had excellent credit ratings: many of them were rated AAA by the rating agencies. The past two decades, however, have seen a swift descent of the Japanese banks from these ratings levels, with even the larger banks falling to BBB status. The cause of this was the rapid decline in the quality of the banks’ assets. The prolonged recession in Japan in the 1990s pushed down land, property and share prices and led to escalating loan losses. The decline in share prices was particularly problematic for the Japanese banks because of the widespread practice of cross

holding of shares among Japanese financial institutions. When the share

price

of

one

bank

fell,

the

market

valuation

of

other

banks

holding those shares fell, therefore putting downward pressure on their share prices: a classic example of a (financial) ‘vicious circle’. In recent years the banks have started slowly to rebuild and improve the credit quality of their balance sheets and bank mergers have also taken place. The expectation is that the coming years will see at least a modest reversal of the decline in the credit ratings levels of the Japanese banks.

OU BUSINESS SCHOOL 27

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 28/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

Analysis of the agencies’ credit ratings highlights the following characteristics: l a cyclical pattern with reductions in ratings being prevalent

during periods of economic recession and the reverse during economic expansion;

l a

bias

towards

larger

companies

with

these

generally

securing

better ratings than their smaller peers;

l greater movement in the ratings of nonfinancial companies (‘corporates’) compared with those of financial organisations.

The explanation the agencies would probably give for this is that this is all logical! During economic recessions companies are likely to experience falling sales and profitability that weaken their creditworthiness. Larger companies will tend to have, in absolute terms, larger reserves and greater capacity to ‘ride out’ temporary periods of

weak performance, thus making their credit strength greater than their smaller peers. The sales and profitability of ‘corporates’ are normally more volatile during economic cycles compared with financial organisations, making greater volatility in their ratings explicable.

Whatever the contrasting views held about the creditrating agencies, there is no doubt that they are very influential. In fact, this power is being bolstered by new regulations on the capital requirements for investments made by financial organisations. Under

these

regulations,

known

as

Basel

2

(see

Box

3.4),

one

method for determining the risk of an investment and the capital that needs to be set aside to support it is directly related to the ratings levels provided by the agencies. Certainly it is rare to find an institutional investor who does not look at the agency ratings before investing in an organisation. Issuers of debt also know that it is not a question of getting any credit rating, but rather a question of getting a sufficiently good rating from the major agencies before they can get access to funds from many of the financial markets around the world.

BOX 3.4 BASEL 2 Basel 2 is the term for the guidelines on the international capital requirements for banks and other financial institutions. These requirements are scheduled to be applied from 2007. In the European Union their application is supported by an EU directive. Basel 2 replaces the (rather simpler) guidelines laid down in Basel 1, which applied from 1988. The essence of these guidelines is that they determine how much capital financial institutions have to put aside to support their

28 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 29/112

lending activities. The riskier the lending, the greater the capital requirement. This capital is the financial cover for loan losses arising from default by borrowers. By applying these guidelines, Basel 2 is intended to ensure that financial institutions remain solvent even if losses on lending are high. In this way, Basel 2 is aiming to reinforce the public’s confidence in financial institutions. Basel 2 is an important development even for nonfinancial companies since it sets the framework for the evaluation and, thereby, the pricing of lending by financial institutions. If Company A and its business sector is assessed as being a ‘higherrisk’ under Basel 2 than Company B then it is very likely that the cost of borrowing money will be higher for Company A than for Company B. For further information on Basel 2, visit the website of the Bank for International Settlements (BIS). A link to this is provided on the course’s website.

BAS I C M E T H O D S O F C R E D I T ANAL YS I S

3 . 3 Many organisations undertake their own credit appraisal of those institutions to which they lend or extend trade credit. This is often needed since many organisations, including medium and small businesses, will not have public credit ratings. Indeed, it is usually only those organisations that borrow in the financial markets that have ratings issued by Moody ’s, Standard and Poor’s or Fitch.

Without the likes of Moody ’s to help you, how should you judge creditworthiness – particularly ‘trade credit’ which is the most common form of exposure if you are doing business with other organisations? The techniques for analysing accounts covered in Units 2 and 3 can be applied here. Most

of

the

time

you

can

expect

to

be

paid

in

the

normal

course

of trade: that is, out of the revenue derived by the organisation to

which you have extended credit when selling goods and services. In other words, as a current liability creditor you should be looking to the quality of your customer’s current assets as your main surety of payment. The information sought should therefore include answers to the following questions. l Are the company ’s sales going well? l Is the inventory current and moving? l What is the length of the operating cycle? l Does the company strip out bad (and doubtful) debts from its

receivables?

3 CREDIT LINES

This section draws on and expands the section dealing with credit analysis in Unit 3.

OU BUSINESS SCHOOL 29

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 30/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

Note that credit agencies such as Experian or Dun and Bradsheet focus on trade credit. Their focus is, therefore, different from that of the international rating agencies such as Standard and Poor's, which is on the credit standing of organisations raising funds from the financial markets.

l Does the business have sufficient lines of shortterm credit? l What is the customer’s payment record and/or its reputation

for payments within the industry? How can answers to these questions be obtained? It is might be possible to request a credit report from the client’s bank (with the permission of the company). Alternatively, a credit assessment may be available from a business credit agency such as Experian or Dun and Bradstreet. However, care needs to be taken in interpreting the results. It is important to remember that the bank has a duty of care to its customer, though it must not be untruthful, and therefore it is likely to give an undetailed answer that may have limited use for credit analysis. Agencies’ reports are often not much more illuminating, though they should warn of any court proceedings lodged against the prospective customer. Therefore, even if reports from banks or agencies are obtained, these should

not

be

regarded

as

a substitute

for

an

analysis

of

the

customer

’

s

balance sheet and income statement. No client who is serious about maintaining a continuing supplier – customer relationship will object to a request for the published accounts; indeed, many companies see such requests as contributory evidence that the supplier is professional and safe to rely on for the ongoing supply of materials.

An important source of information that is often overlooked is the industry ’s ‘grapevine’ – the information that may be obtained informally about businesses within trade and business organisations, such as the Chambers of Commerce in the United Kingdom. If a business is having trouble, its peers are usually the first to find out, excepting perhaps the unfortunate firm’s bank. Of course, such information is hearsay, perhaps even merely gossip, but it is unwise to ignore such rumours without at least trying to substantiate them.

EXERCISE 3.1 Is the aim of trade credit analysis to reduce bad debts to zero?

Before moving on from this survey of the basics of creditrisk analysis, here is a cautionary tale to show that you need to think through the implications of your methods, especially when introducing new techniques. The story in Box 3.5 is not strictly an example of trade credit, but it is certainly relevant to business debt in a wider sense.

BOX 3.5 NEURAL NETWORKS AND CREDIT ANALYSIS In the past few years, work on ‘

artificial intelligence’ in general and on ‘neural networks’ in particular have developed considerably.

30 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 31/112

3 CREDIT LINES

What is a neural network? Briefly, it is a type of computer designed to mimic the workings of a brain. A large amount of data together with the results associated with the data are fed into the computer and, over time, it programs its own internal ‘pathways’ so that input corresponds with appropriate output, in a similar way to how neurons in the brain develop connections and pathways as we learn. When the output from test data reliably matches the expected result, the machine is ready. You then feed it new data to get real results that were not precalculated. What does this have to do with credit analysis? Some financial institutions in the US realised that the type of analysis being done to decide on credit ratings was very amenable to neural network

type programming. Accordingly, neural computers were ‘trained’ with large amounts of data about past credit decisions and the eventual

repayment

outcomes.

When

the

reliability

of

the

results

from the network exceeded the previous scoring methods in predicting whether a particular application should be accepted or rejected, the financial institutions started to use it for making actual lending decisions. Unfortunately, after a while the banks found themselves subject to a number of lawsuits. US law requires banks to give fair and careful consideration to any and all loan proposals. Being turned down in the US for credit can be damaging – embarrassing to an individual and potentially serious to a small business. The crux of the matter was that, while no one (well, not many people) doubted that the neural networks were on average more accurate, it was impossible to prove that in any particular case ‘due consideration’ had been given. With a neural network you just feed in data at the front, say the magic word and use the output from the back. It is the ultimate statistical ‘black box’. Since the banks could not show in a deterministic way why they had turned down the loans, they lost the cases, so now they have gone back to their previous assessment methods. These may be less accurate, but at least the banks can show that A, B and C were done and the answer was F – for ‘Fail’.

MORE AD V ANC E D M E T H O D S OF C R E D I T A NALY SI S

Rather than relying on either simple analysis using core ratios or on the ratings supplied by the external ratings agencies, many organisations that make investments undertake their own bespoke credit analysis. Indeed, many financial institutions now adopt internal ratings systems of their own. These tend to be similar, but not identical, to those of the external ratings agencies.

OU BUSINESS SCHOOL 31

3 . 4

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 32/112

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 33/112

l

l

3 CREDIT LINES

What is the relationship between the organisation and its subsidiaries – are there credit support obligations from the former to the latter?

BOX 3.7 CREDIT SPREADS AND ‘RISK-FREE ’ YIELDS A credit spread is the difference between the yield on a bond issued by a company and the yield on a ‘riskfree’ bond – normally a high creditquality government bond of equivalent term to maturity. The ‘riskfree’ bond has a probability of default of either zero or close to zero, so the greater the credit risk associated with the company the higher will be the credit spread over the ‘riskfree’ yield, since investors will want returns that are proportionate to the perceived credit risks associated with their investments.

What is the degree of volatility in the market price of the securities issued by the organisation? Volatility analysis is informative of the risks of investing generally in the organisation’s industrial sector and of the sensitivity of the organisation’s performance to trends in the economy as a

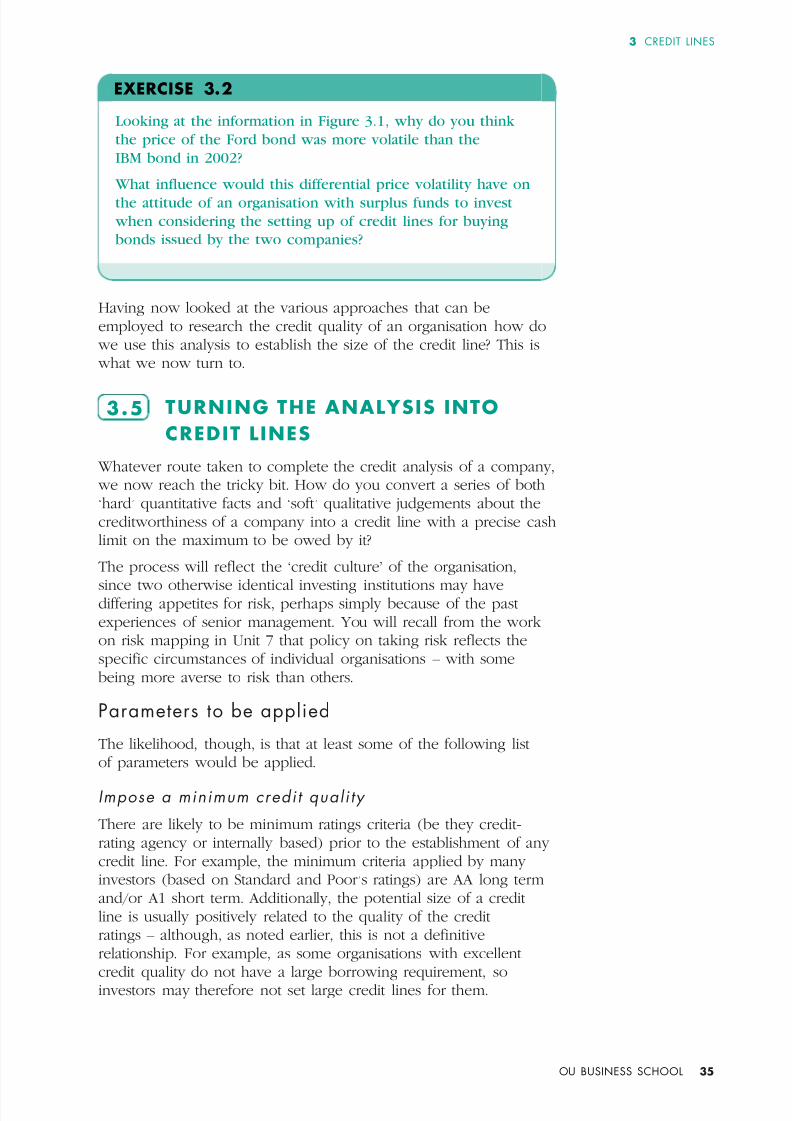

whole. Analysis here should include studying the historical ‘credit spreads’ on the organisation’s debt securities. Spreads matter. Even if the organisation you invest in does not default, the valuation of its debt (which is the investor’s asset) will fall if credit spreads widen even if other market conditions remain unchanged. As Figure 3.1 overleaf shows, investors experienced a roller coaster ride in the valuation of their holdings of Ford bonds in 2002 as a result of spread movements – even if their fate was better than those who had invested in WorldCom,

which eventually defaulted. BOX 3.8 CREDIT SPREADS AND BOND VALUES To demonstrate the impact of credit spreads on bond valuations let us look at an example. An organisation issues a fiveyear bond at par at a yield to maturity of 5% p.a. The yield on a ‘riskfree’ bond of equivalent duration at the time of issue is 4%, therefore making the credit spread 5 4% = 1%. Over the next year, credit conditions deteriorate for the organisation. Although the yield on the ‘riskfree’ bond remains at 4% p.a., the credit spread for the organisation widens to 2%, making the yield to maturity on its bond – which now has a residual life of four years – rise to 6% p.a.

OU BUSINESS SCHOOL 33

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 34/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

In these circumstances the investors will find that the market price of their bond holding has fallen from 100.00 to 96.53 – a loss of 3.47%. Bond pricing and duration

were covered in Unit 7.

ACTIVITY 3.2 Bond valuation was covered in Unit 7 – let’s try some revision here. A company issues a six-year bond at par (100.00) with an annual coupon of 5% p.a. One year later (and after the payment of the coupon at the end of Year 1), the bond has a yield to maturity of 7% p.a. for its residual five-year life as a result of widening credit spreads. What is the price of the bond now, one year after its issue date? You should find that the bond's price has fallen to 91.80 – a loss of 8.2%.

% p . a .

( c r e d i t s p r e a d )

10

9

8

7

6

5

4

3

2

1

0

J a n 0

2

F e b 0

2

M a r 0 2

A p r 0 2

M a y 0

2

J u n 0

2

J u l 0

2

A u g 0

2

D e c 0 2

S e p 0

2

O c t 0

2

N o v 0

2

WorldCom

Ford

IBM

Figure 3.1 Credit spreads in 2002 for three different corporate bonds.* * Yield spread IBM bonds with coupon 5.375% and maturity 01.02.09 against US government paper TBond 6.6% maturity 15.05.09; yield spread Ford 7.35% 15.10.11 against TBond 5% 15.08.11; yield spread WorldCom 8.25% 15.05.31 against TBond 5.375% 15.02.31. Source: www.norgesbank.no/english/petroleum_fund/articles/investment-creditmarket2003/. Accessed 30/08/05 Figure 3.1 shows movements in the credit spread for three corporate bonds through 2002. The spread of one security (issued by IBM) widened a little, but then rebounded, so that on the whole investors in this security did not lose money on the change in spread. Ford’s spread expanded sharply, but reverted towards the end of the year. In this case, the investors lost by holding this security rather than other, safer securities, but the loss was reduced towards the end of the year. The third spread expanded sharply and never rebounded, because the company that had issued the security (WorldCom) went bankrupt.

34 OU BUSINESS SCHOOL

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 35/112

EXERCISE 3.2 3 CREDIT LINES

Looking at the information in Figure 3.1, why do you think the price of the Ford bond was more volatile than the IBM bond in 2002? What influence would this differential price volatility have on the attitude of an organisation with surplus funds to invest when considering the setting up of credit lines for buying bonds issued by the two companies?

Having now looked at the various approaches that can be employed to research the credit quality of an organisation how do

we use this analysis to establish the size of the credit line? This is what we now turn to.

T UR N I N G T HE A NALY SI S INTO C R E D I T L I N E S

3 . 5 Whatever route taken to complete the credit analysis of a company, we now reach the tricky bit. How do you convert a series of both ‘hard’ quantitative facts and ‘soft’ qualitative judgements about the creditworthiness of a company into a credit line with a precise cash limit on the maximum to be owed by it? The process will reflect the ‘credit culture’ of the organisation, since two otherwise identical investing institutions may have differing appetites for risk, perhaps simply because of the past experiences of senior management. You will recall from the work on risk mapping in Unit 7 that policy on taking risk reflects the specific circumstances of individual organisations – with some being more averse to risk than others. Parameters to be applied The likelihood, though, is that at least some of the following list of parameters would be applied. Impose a minimum credi t qual i ty There are likely to be minimum ratings criteria (be they creditrating agency or internally based) prior to the establishment of any credit line. For example, the minimum criteria applied by many investors (based on Standard and Poor’s ratings) are AA long term and/or A1 short term. Additionally, the potential size of a credit line is usually positively related to the quality of the credit ratings – although, as noted earlier, this is not a definitive relationship. For example, as some organisations with excellent credit quality do not have a large borrowing requirement, so investors may therefore not set large credit lines for them.

OU BUSINESS SCHOOL 35

7/28/2019 b821 Block4unit9 Credit Liquidity and Operational Risk

http://slidepdf.com/reader/full/b821-block4unit9-credit-liquidity-and-operational-risk 36/112

UNIT 9 CREDIT, LIQUIDITY AND OPERATIONAL RISK

In setting limits for an industrial sector many investors use the internationally adopted Standard Industrial Classifications index or ‘SIC codes’ that identify different types of industry. The term ‘systemic risk’ means the risk of correlated defaults by organisations within a particular sector or country over a short period of time.

Set an absolute maximum for the organisat ion . . . There should be an ultimate maximum on the size of a credit line for any organisation. This could be expressed as a percentage of the investing organisation’s capital base and this ensures that, regardless of credit standing, it is not over exposed to any entity. The

maximum

on

the

size

of

the

credit

line

should

also

be

linked

to the size of the borrower. This could again be expressed as a percentage of its capital base. Of course, if this latter maximum exceeds the ‘ultimate maximum’ defined above, it is the organisation’s ‘ultimate maximum’ that prevails. . . . a maximum for the sector